Embed Size (px)

Citation preview

January 23, 2003

THE SOURCE OF INDEPENDENT EQUITY RESEARCH™

Analyst: Bruce Reid

Independent Equity Research Corp. 130 Adelaide St. W, Suite 2215, Toronto Ont., Canada M5H 3P5, www.eresearch.ca

Fortune Minerals Limited

Recent Price C$0.00Symbol FT:TSXShares O/S 19.575 million52 Wk. Range $0.99-$0.30Fiscal Year End Dec 31

EPS CFPS2000 n.a. n.a.2001 n.a. n.a.2002e n.a. n.a.2003e n.a. n.a.

eResearch

Data Source: www.wallstreetcity.com

Recommendation

Speculative Buy

Target Price

C$1.60

Risk

High

Ave. Monthly Trading Vol.

139,958

Quick Facts

We are continuing to recommend FortuneMinerals' shares as a speculative buy forinvestors seeking leverage to a naturalresource company with exposure to a widerange of deposits and commodities.

The Company has recently finished itsscoping study on the 80% owned gold,cobalt, bismuth NICO Project in theNorthWest Territories. The new study isbased on an underground miningdevelopment scenario with supplementalmill feed from smaller pits. Resultsindicated an attractive pretax 16.5% internalrate of return (I R.R). and $20.7 million netpresent value (NPV) at a 7% discount rateusing US$315 per ounce of gold US$7 perlb. cobalt and US$3.25 per lb. bismuth.Under this mining scenario gold is thegreatest contributor to the bottom line. AtUS$355 per ounce gold, and US$8 per lb.cobalt the IRR and NPV increases to31.7% and C$60.9 million respectively.Additional drilling is planned for this winterto expand the high-grade parts of the depositfor a feasibility study.

The Company continues to work on itsrecent acquisition of Mount Klappan.This is a world class anthracite coalproject which has had extensive workcompleted on it with a variety offeasibility studies. The studies indicatedthe project has robust economics as aresult of the numerous premium productsthat could be produced. As a testamentof the value of this type of Coal asset,the past three months has seen severalmining and financial heavyweights bidand counter-bid for control of FordingCoal, Canada’s largest metallurgical coalproducer.

The Company's 30% interest in the highcalcium limestone deposits nearWalkerton, Ontario is close to having allpermits in place. The company isconfident that this project will providecash flow by 2003 upon receipt of theextraction license.

STRENGTHS

• Excellent portfolio ofdevelopment projects withgood stream of newsexpected over the next 12months

• Cash flow from theiraggregates divisionexpected in 2003

• Officers and directors arehighly experiencedprofessionals

RISKS

• Inherent risk in themining industry

CONCLUSION

• Excellent portfolio ofpotential properties

Fortune Minerals is a Canadian based mining company with exploration and development interestsin a variety of coal and specialty base metal and precious metal prospects and projects.

QUICKVIEW QUARTERLY UPDATE

0

100

200

300

400

500

600

Thou

sand

s

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

eResearch Fortune Minerals Limited

2 January 23, 2003

THE COMPANY

Fortune Minerals is a diversified natural resources exploration and developmentcompany listed on the TSX exchange. The Company has interests in a variety ofmineral deposits and exploration projects all located in Canada. The officers anddirectors are highly experienced professionals and entrepreneurs who have a varietyof skills and backgrounds that provide Fortune shareholders with the managementand governance to be a successful junior resource company. The officers and directorsown 42% of the issued stock. Fortune has $1.4 million in working capital sufficientto fund the activities of the Company in the near term.

Fortune recently acquired a 100% interest in the Mount Klappan anthracite coal projectnear Stewart, British Columbia from the Canadian subsidiary of ConocoPhilips Inc.This is an extremely large development project that had in excess of $60 millionexpended on it for exploration and development. Feasibility studies, environmentalassessments and test mining were previously completed on this project.

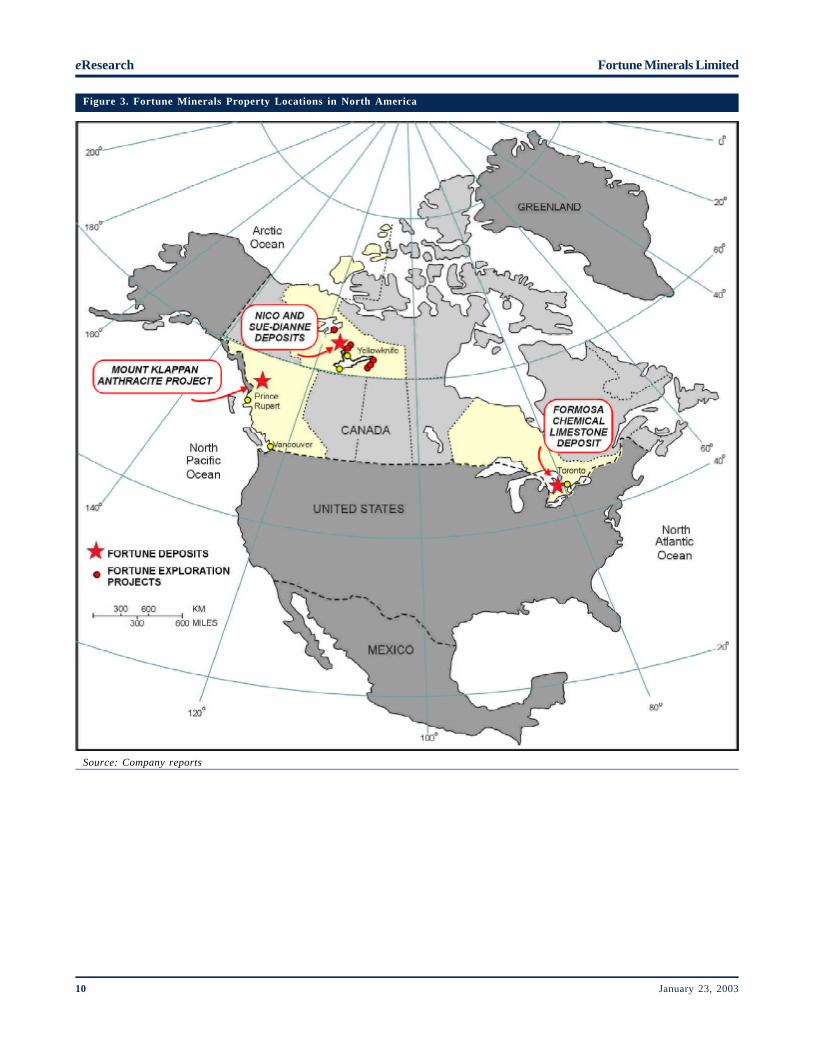

Other projects include an 80% interest in the NICO gold-cobalt-bismuth deposit nearYellowknife, Northwest Territories. NICO is a large, near surface deposit locatedclose to existing infrastructure and provides an opportunity to participate in gold playwith specialty metal credits. The Company's 100% owned Sue-Dianne copper-silverdeposit is located just north of the NICO and is also a near surface deposit.

Fortune is active in the industrial minerals business through its 30% operating interestin the Formosa Environmental Aggregates Ltd. The Company is forecasting cashflow from the Greenock Quarry next year as most permits for this high calciumchemical grade limestone operations are almost in place.

THE PROJECTS

Nico Gold Project

NICO is a large near-surface deposit of gold, cobalt, and bismuth located 160 kmnorthwest of Yellowknife, Northwest Territories. The NICO mineralization has similarcharacteristics to the prolific Olympic dam deposit in southern Australia. The depositis near existing infrastructure only 6 km from a government maintained winter roadand 20 km from four hydro-electric dams. The government of the NWT also plansto re-align the winter road to an all-land route with bridged water crossings capableof sustaining heavy truck traffic. This would facilitate haulage of concentrates fromthe property to the Con Mine in Yellowknife where there is a plant capable of processingthe cobalt and gold concentrates. Bismuth concentrates could be trucked to TeckCominco's smelter in Trail, B.C.

Fortune owns an 80% interest in NICO, and together with its joint venture partner,have expended $8 million on exploration since discovering the deposit in 1995. Workhas included geology and geophysical surveys, 250 drill holes, metallurgical testing,mine planning, geotechnical engineering, and environmental baseline studies.

Excellent portfolio ofdevelopment projectswith good stream ofnews expected over thenext 12 months

NICO is a large near-surface gold depositwith cobalt-bismuthcredits northwest ofYellowknife in theNorthwest Territories

Gold with specialtymetal credits

eResearchFortune Minerals Limited

3January 23, 2003

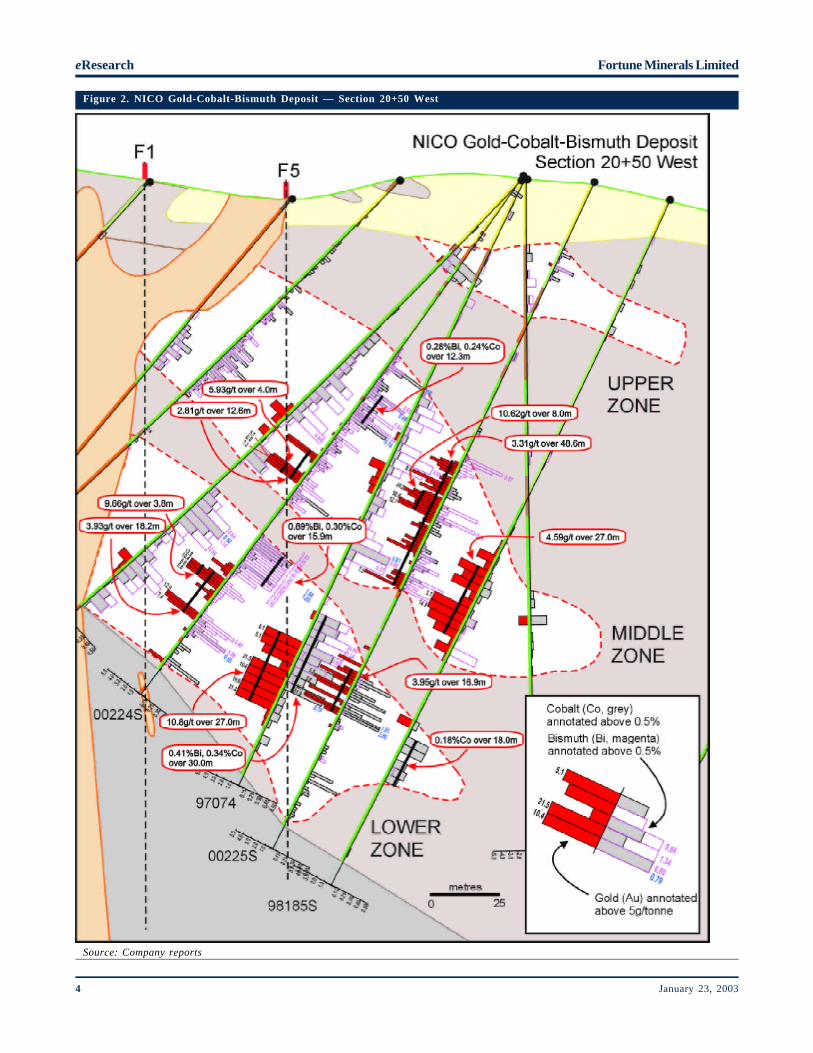

Current studies are focused on the higher grade, gold-rich core of the deposit. Higher-grade lenses are also present at or near the surface at the east and west ends of thedeposit. Grades encountered in these lenses are locally in excess of 10 g/tonne gold,with significant cobalt and bismuth values. Fortune's management has shown that acombination of bulk underground mining with smaller open pits is economic to mineat current prices. The study has identified about 5 million tonnes of underground oreand 3 million tonnes in smaller pits of higher-grade material. The initial assessment ofthe project on this basis indicates a more favourable rate of return even at currentmetal prices.

NICO also has significant exploration potential both within the deposit and in otherparts of the property. High-grade gold intersections of 10-30g/tonne gold wereidentified in lower parts of the deposit, which indicate potential for expansion atdepth. These deeper intersections would not have been accessed for several years inan open pit scenario but are very important in the underground mining plan.

Fortune is in discussions with major mining companies interested in joint venturedevelopment of the NICO deposit.

Recent Developments

The Company recently finished its scoping study based on an underground miningdevelopment scenario with supplemental mill feed from smaller pits. Results indicatean attractive pretax 16.5% internal rate of return (IRR) and a C$20.7 million netpresent value (NPV) at a 7% discount rate using US$315 per ounce gold, US$7 per lbcobalt and US$3.25 per lb. bismuth. The greatest contributor to the bottom lineunder this scenario is gold. At US$355 per ounce gold, and US$8 per lb. of cobalt,the IRR are and NPV increased to 31.7% and C$60.9 million respectively.

The new study assessed underground mining focused on the gold rich high-gradecore of the deposits and provide early access to ores that produce higher cash flows.Ores produced from the mine would be processed in a 2,500 t per day mill constructedat the site. The process flow sheet consists of a conventional crushing and grindingcircuit followed by a simple flotation to generate cobalt-gold and gold-bismuth sulfideconcentrates. The gold cobalt concentrates would be trucked Yellowknife forprocessing in the Con mine autoclave. The gold bismuth concentrate would be truckedto Trail British Columbia for processing at the Teck Cominco smelter.

Diluted indicated underground and open pit resources were calculated from the mineralresource inventory based on operating costs at the two metal price scenarios (Tables5 and 6). Underground resources were based on a C$51/tonne cost whereas open pitresources used an external cut-off of C$20/tonne and internal cut-off of C$17/tonne.

The Company iscurrently re-evaluatingthe economics of thisproject by focusing onaccessing the higher-grade core first. Theresults of this studyshow an attractive rateof return at currentgold and cobalt prices.

eResearch Fortune Minerals Limited

4 January 23, 2003

Figure 2. NICO Gold-Cobalt-Bismuth Deposit — Section 20+50 West

Source: Company reports

eResearchFortune Minerals Limited

5January 23, 2003

Table 5. Diluted Underground & Open Pit Indicated Resources

(US$315/oz Gold, $7/lb Cobalt & $3.25/lb Bismuth)

Tonnes Au Co Bi Dilution Strip NSR(g/t) (%) (%) (%) ($C/T)

Underground @C$51 Cut-off 4,479,165 3.55 0.16 0.25 15 - $76.92Open Pit @C$17/20 Cut-off 2,692,415 0.73 0.12 0.15 20 1.82 $31.88

Source: Company Reports-If a much higher cut-off rate is used to determine the resource inventory it clearlydemonstrates that there is a significant core of much higher grade material. (SeeTable 6).

Table 6. Diluted Underground Indicated Resource

(US$315/oz Gold, $7/lb Cobalt & $3.25/lb Bismuth)

Tonnes Au Co Bi Dilution Strip NSR(g/t) (%) (%) (%) ($C/T)

Underground @C$70 Cut-off 2,225,282 5.21 0.16 0.27 15 - $98.05

Fortune Minerals’ has reported that the underground mining scenario with smallerpits produces a positive economic return for the development of the NICO Deposit atthe current low metal price environment. Other attractive features include lowercapital costs, less pre-stripping, early access to the gold-rich high-grade parts of thedeposit for capital repayment, higher metal recoveries and less of an impact on themarkets for cobalt and bismuth from a lower production rate. There also remains agood potential to expand the high-grade parts of the deposit with additional drillingwhich the company plans to conduct this winter. Any improvement in metal prices inthe future would also improve the project economics.

Sue-Dianne Copper-Silver Deposit

Sue-Dianne a near-surface deposit is located 20 km north of NICO and 170 kmnorthwest of Yellowknife. Originally Fortune acquired a 50% earn-in from Norandaby spending $2 million in exploration. Later Fortune earned a 100% interest andconverted Noranda to a 1.5% NSR. The success of this project is dependent onhigher metal prices as well as having the NICO project in production to provide thenecessary critical mass. Metallurgical test results have indicated the ores from Sue-Dianne can be processed in the same plant as the cobalt concentrates from NICO.

The Company iscurrently undertaking aseries of studies aimedat re-evaluating theeconomics of thisproject using differentparameters and moremodern numbers

eResearch Fortune Minerals Limited

6 January 23, 2003

Table 7. Sue-Dianne Minerals Resources

Tonnage Class Copper Silver(Tonnes) % g/tonne 24,259,200 Measured & Indicated 0.56 2.2(@ 0.10% Cu cutoff)17,330,100 Measured & Indicated 0.72 2.7(@ 0.25% Cu cutoff)10,569,800 Measured & Indicated 0.95 3.3(@ 0.50% Cu cutoff)

Formosa Environmental Aggregates Ltd.

Fortune is active in the industrial minerals business through its 30% operating interestin Formosa Environmental Aggregates Ltd. Formosa owns 170 hectares in theMunicipality of Brockton in South Bruce County, Ontario. Formosa intends to developthe Greenock Quarry in order to mine a 15 million tonne deposit of 99% CaCO3.This is the purest known resource of high calcium chemical grade limestone in Ontarioand its uses include chemical, environmental, agriculture, manufacturing andconstruction material industries. Formosa has received its Official Plan and ZoningChange Amendments and is expecting to receive a Class A Extraction License fromthe Ministry of Natural Resources in short order, for up to 850,000 tonnes of productionper year. Formosa will then spend about C$500,000 to develop the quarry, initially ata smaller (~250,000 tonne/year) production rate. This project is forecast to generatecash flow of approximately C$400,000 per annum to Fortune with production startingin 2003.

Mount Klappan Anthracite Coal Project

The world Class Mount Klappan anthracite coal project was purchased earlier thisyear from Conoco Canada Resources Limited following their takeover of Gulf CanadaResources in 2001. The 100% interest was purchased for $3 million cash, theremaining $100,000 pro-rata portion of annual lease rental, replacement of a $200,000reclamation bond and a $1/tonne finished coal product royalty.

The total global resource of this project is over 2.8 billion tonnes in four deposits.This includes 236 million tonnes in the Measured and Indicated categories(Demonstrated Resources). A 1991 feasibility study on the proposed Lost-Fox mine,identified Proven and Probable Mining Reserves of 51.46 million tonnes. This wasconsidered sufficient for a mine life of over twenty years using open pit mining at aproduction rate of 1.7 million tonnes per annum.

Table 1. Mount Klappan Mineral Resources by Deposit and Category

(millions of tonnes)Area Measured Indicated Demonstrated Inferred SpeculativeLost-Fox 111.4 111.7 223.1 36.8 798.6Hobbit-Broach - 13.5 13.5 258.4 753.0Summit - - - 9.6 508.9Nass - - - - 201.5Total 111.4 125.2 236.6 304.8 2,262.0

eResearchFortune Minerals Limited

7January 23, 2003

Anthracite is a desiredproduct with highcarbon and energycontent as well as beinga relatively hardmaterial and cleanburning

Table 2. Mount Klappan Mining Reserves By Category

(millions of tonnes)Proven Probable Total

Lost-Fox 40.51 10.95 51.46

Mount Klappan is located close to tidewater in northwest British Columbia. The projectis currently accessible to the ice-free, deepwater port of Stewart from Highway 37 viaa gravel road constructed along the B.C. Rail right-of-way. Another option is to useB.C. Rail. The end of steel for the railway is currently only 70 km to the south and canbe accessed by upgrading the sub-grade for truck haulage to a load-out facility. Thiswould provide access to markets in North America by rail or to the Ridley Island coalterminal at Prince Rupert. This deep-water terminal was originally built to ship coal forthe closed Quintette coal mine and the soon-to-be-closed Bullmoose mine.

The initial exploration licenses for this project were acquired by Gulf Canada in 1981.During the next 10 years extensive exploration was conducted on the property. Thisincluded geology, rotary and core drilling, trenching, the driving of two exploratory aditsplus engineering, marketing, environmental and feasibility studies. A 200,000 tonne bulksample was mined and 100,000 tonnes of finished anthracite products were produced ina pilot plant constructed at the site for shipment to select customers in North America,Asia and Europe. The project was mothballed after Gulf Canada was sold to Olympia &York Developments, which subsequently went into receivership following the collapse oftheir real estate empire. Mount Klappan became an orphan within Gulf during the 1990'sas management chose to focus on their core oil and gas business. It became available forpurchase after Conoco acquired Gulf Canada last year.

There are at least 33 coal horizons indentified on the Mount Klappan property, somewith thickness up to 11.3 meters. Mining is initially contemplated in the "I" Seam thathas an average true thickness of over 4 meters. The finished coal strip ratio is 8:1which is typical for Canadian mountain coal deposits. Washing and heavy mediaseparation produces high quality anthracite products with high carbon and energycontents and that are low in sulphur, moisture and volatiles as compared to othercoals. Production of various sized coal with low, medium and high ash contents arecontemplated. Anthracite coals are relatively uncommon representing less than 1%of all world coal reserves. The high carbon and energy content as well as beingrelatively hard material and clean burning makes anthracite a desired product. Thevalue-added anthracite products are used in carbon filtration water purification andspace heating and sell at prices of between US$100—250/tonne. Anthracite is alsoused as a reductant in metallurgical processing, pulverized coal injection for steelmaking, in cooking and heating briquettes, and as fuels used in the manufacture ofcement and generation of electricity. It should be noted that 37% of the world'selectricity is generated by coal-fired thermal power plants and most of the cementplants throughout the world are coal-fired.

The Lost-Fox deposit at Mount Klappan has undergone several feasibility studies toassess its economics. The most recent and comprehensive study was completed in1991 by Kilborn Engineering (plant and site design), Marston and Marston (mine planningand reserves) and Wright Engineers (economic analysis). The study assessed an openpit mine at an annual production rate of 1.7 million tonnes of finished anthracite coalproducts over a twenty-one year mine life. The study is now out of date but at thattime indicated an attractive rate of return for the development.

eResearch Fortune Minerals Limited

8 January 23, 2003

This Company providesshareholders withexposure to a widevariety of projects andcommodities

Fortune is currently preparing a computer block model of the Lost-Fox deposit foropen pit optimization and updating of the feasibility study with current information.The Company is also re-establishing contact with potential purchasers identified inearlier marketing studies by Gulf. Fortune is assessing a new development plan withlower capital costs for the mine than was originally contemplated by Gulf. Thesestudies are also looking at possibly incorporating used equipment from the closedQuintette mine and soon-to-be-closed Bullmoose mine. Fortune has budgeted $1million for all of this work over the next year.

OTHER PROJECTS

Fortune Minerals recently staked the 200 hectare Slave claims along the south shoreof the East Arm of Great Slave Lake in the Northwest Territories. Numerous coppershowings are identified in both trenches and drilling done by previous owners. Alsonarrow zones of high-grade anomalies of gold and silver have been identified.

Fortune has interests in a number of other projects in Mazenod Lake area and otherparts of the Northwest Territories. The JBG and OLYM-PIC-PAM claims hostnumerous iron oxide showings that warrant drill testing for sulphide deposits similarto the nearby NICO and Sue-Dianne deposits. GMD Resource Corp. continues tocarry out additional work on the Wheel-of-Fortune claims, 100 km north ofYellowknife, in which Fortune has a 2% gross royalty on diamond sales.

CONCLUSION

We believe that Fortune Minerals is in an excellent position to add additional value toa series of extremely interesting development projects. The Company will be releasingnew feasibility forecasts for the Mount Klappan coal project over the next 12-15months after modernizing and updating the previous work from 10-12 years ago.This will provide investors with a fresh look to this coal project based on current andexpected parameters. As a sidebar, the current takeover attempt of Fording Inc. bySherritt Coal Partnership II clearly demonstrates to the investing public the real potentialof a project of this magnitude.

Management will have several new press releases this winter on the NICO Project asthe Company has undertaken to conduct further drilling to expand the deposit forfeasibility. These are expected to demonstrate the real value of this project. Furtherto increasing the potential value of this asset, management has initiated discussionswith several large mining companies who have shown an interest in the project.

Adding to expected near-term improvement in shareholder value will be the start-upof the Greenock limestone quarry in 2003. Fortune owns 30% of the Company andis the operator. It is forecasting approximately C$400,000 in annualized cash flownet to Fortune. This will provide Fortune with a long life annuity which will providemanagement with increased flexibility and the ability to focus on other initiatives thatcan add substantial value to shareholders.

We are recommending this company to investors seeking exposure to a wide varietyof interesting mineral development projects in Canada.

Fortune has budgeted$1 million for the re-evaluation studies onthis project over thenext 12 months

eResearchFortune Minerals Limited

9January 23, 2003

OFFICERS & DIRECTORS

William A. Breukelman, MBA, P.Eng, BA.Sc, Director, Mississauga, OntarioBill Breukelman has owned, founded and funded numerous businesses in the high techfield, with particular interests in information systems and imaging. Bill is a pioneer ofimaging, having co-owned and later chaired IMAX Corporation form 1970-1995. Today,Bill is the Chairman and Principal of Business Arts Inc., a high tech incubation andinvestment firm with funds and co-develops companies such as MDS SCIEX, amolecular imaging company, Arius3D, a surface imaging company, and GEDEX ageological imaging company.

The Honorable Carl. L. Clouter, Director, Gander, NewfoundlandCarl Clouter is a commercial pilot who owned a charter airline service in the NorthwestTerritories. Carl has been active in mineral exploration and prospecting carried out inconjunction with more that 30 years of flying though-out remote areas of Canada.Carl also served as a Sentencing Justice of the Peace and a member of the board forthe mineral development assistance program for the Government of the NorthwestTerritories. He is currently a commercial pilot in Gander.

George M. Doumet, M.Sc., MBA., Chairman, Vancouver, BCGeorge Doumet is a chemical and nuclear engineer who has founded and owns anumber of industrial companies in Canada and internationally. He is President ofCandou Industries Ltd., an investment holding company and a principal in otherbusinesses involved in the production and marketing of specialty building products,chemicals and industrial minerals.

Robin E. Goad, M.Sc., P.Geo., President, CEO & Director, Arva, OntarioRobin Goad is a geologist with more than 20 years of experience in the mining andexploration industries. Robin previously worked for major mining companies includingNoranda and Teck, and as a consultant for junior resource companies and governmentin Canada and internationally. He co-founded Fortune Minerals in 1988. Robin alsoserves as a director of Ursa Major Minerals Incorporated.

David A. Knight, BA., LL.B., Secretary & Director, Oakville, OntarioDavid Knight is a partner in Macleod Dixon LLP, Barristers & Solicitors, a Canadianand international law firm, with extensive experience in the resource sector. Davidspecializes in all areas of securities law, including public and private financings,takeovers, stock exchange listings, mergers and acquisitions and regulatorycompliance. He acts for a number of large and mid-tier investment dealers andresource companies. David is a member of the Law Society of Upper Canada and theCanadian Bar Association.

Sidney Miszczuk, Director, Mississauga, OntarioSidney Miszczuk is the President and owner of Cooksville Steel Ltd., a major fabricatorand erector of structural steel he co-founded in 1952. Cooksville Steel has plants inMississauga and Kitchener, Ontario. Sidney has been associated with mineralexploration companies for 25 years, including serving as Chairman of Flag Resources(1985) Ltd. and a substantial investor in Golden Briar Mines Ltd., which trade on theTSX-Venture Exchange.

eResearch Fortune Minerals Limited

10 January 23, 2003

Figure 3. Fortune Minerals Property Locations in North America

Source: Company reports

eResearchFortune Minerals Limited

11January 23, 2003

NOTES

For further informationsand subscription contact:

Independent EquityResearch Corp.

130 Adelaide St. W,Suite 2215, Toronto Ont.,Canada M5H 3P5Toll-free: 1-866-854-0765

Our research is accessible on:www.eresearch.ca

Price

Single Report $29*Annual Subscription $99*(full service)Annual Subscription $50*(single company)

* plus applicable tax

Disclosure StatementeResearch accepts fees from the companies it researches (the “covered companies”) and from major financial

institutions. The sole purpose of this policy is to defray the cost of researching small and medium capitalization stockswhich otherwise receive little research coverage. In this manner, eResearch can minimize fees to its subscribers.

To ensure complete independence and editorial control over its research, eResearch follows certain business prac-tices and compliance procedures. Among other things, fees from covered companies are due and payable prior to thecommencement of research and, as a contractual right, eResearch retains complete editorial control over the research.

eResearch analysts are compensated on a per-company basis and not on the basis of his/her recommendations.Analysts are not allowed to solicit prospective covered companies for research coverage by eResearch and are notallowed to accept any fees or other consideration from the companies they cover for eResearch. Analysts are also notallowed to trade in the shares, warrants, convertible securities or options of companies they cover for eResearch.

In addition, eResearch, its officers and directors cannot trade in shares, warrants, convertible securities or optionsof any of the covered companies. eResearch accepts payment for research only in cash and will not accept paymentin shares, warrants, convertible securities or options of covered companies. eResearch will not conduct investmentbanking or other financial advisory, consulting or merchant banking services for the covered companies. eResearch isnot a brokerage firm and does not trade in securities of any kind.

eResearch’s sole business is in providing independent equity research to its institutional and retail subscribers.

No representations, express or implied are made by eResearch as to the accuracy, completeness or correctness ofits research. Opinions and estimates expressed in its research represent eResearch’s judgment as of the date of itsreports and are subject to change without notice and are provided in good faith and without legal responsibility. Itsresearch is not an offer to sell or a solicitation to buy any securities. The securities discussed may not be eligible forsale in all jurisdictions. Neither eResearch nor any person accepts any liability whatsoever for any direct or indirectloss resulting from any use of its research or the information it contains. This report may not be reproduced, distrib-uted or published without the express permission of eResearch.

eResearch Recommendation System

Buy: Expected total return within the next 12 months is at least 20%

Speculative Buy: Expected total return within the next 12 months is at least 40%. Risk is High (seebelow)

Hold: Expected total return within the next 12 months is between 20% and the T-Bill rate

Sell: Expected total return within the next 12 months is less than the T-Bill rate

eResearch Risk Rating System

A company may have some but not necessarily all of the following characteristics of a specific riskrating to qualify for that rating:

High Risk: Financial - Little or no revenue and earnings, limited financial history, weak bal-ance sheet, negative free cash flows, poor working capital solvency, no dividends.

Operational - Weak competitive market position, high cost structure, industry con-solidating, business model/technology unproven or out-of-date.

Medium Risk: Financial - Several years of revenue and positive earnings, balance sheet in linewith industry average, positive free cash flow, adequate working capital solvency,may or may not pay a dividend.

Operational - Competitive market position and cost structure, industry stable,business model/technology is well established and consistent with current stateof industry

Low Risk: Financial - Strong revenue growth and earnings over several years, stronger thanaverage balance sheet, strong positive free cash flows, above average working capi-tal solvency, company may pay (and stock may yield) substantial dividends or com-pany may actively buy back stock.

Operational - Dominant player in its market, below average cost structure, com-pany may be a consolidator, company may have a leading market/technology posi-tion.