Embed Size (px)

Citation preview

1

Employee Stock Ownership Plans

Alterna(ves for Liquidity and Capital While Maintaining Independence

W. William Gust, J.D., LLM President, Corporate Capital Resources, LLC

Michael A. Coffey Managing Vice President, Corporate Capital Resources, LLC

Andrew K. Gibbs, CFA, CPA/ABV Senior Vice President, Mercer Capital

March 8, 2012

2

Introduction

» Is there such a thing as board-‐controlled, “friendly” capitaliza(on?

» Is there another market for your stock, besides inside or outside investors or the public markets?

» Is there a way to purchase bank stock with tax-‐deduc(ble dollars?

» Could a closely held community bank ever become 100% tax-‐exempt on all earnings; i.e., have a fully tax-‐exempt income statement?

3

Introduction

» Can a tax-‐deduc(ble private stock market purchase stock with less dilu(on to exis(ng shareholders than that from investment capital?

» Can Tier 1 capital be created with tax-‐deduc(ble earnings and acceptable dilu(on?

» Can sellers of bank shares ever reinvest sales proceeds without taxa(on?

» Can a Bank make acquisi(ons with tax-‐deduc(ble dollars?

» And if this can be done, who benefits and how?

4

Introduction

1. An ESOP is not THE answer but may be a component of a larger strategy

2. A well-‐designed ESOP should be integrated with a broad spectrum of business goals besides just capitaliza(on and employee benefits – e.g., coordina(on with major shareholder estate plans, governance, techniques to reduce the number of shareholders, etc.

5

Overview of Today’s Presentation

» ESOP Basics

» ESOP Pros and Cons

» ESOP Structures

» Valua(on Issues

» Q & A

6

ESOP Basics

» ESOPs are a qualified re(rement plan under IRC Sec(on 401(a) mandated to invest primarily in employer securi(es (bank holding company shares)

» ESOPs must own the highest and best class of employer securi(es with respect to vo(ng, dividend and liquida(on rights § Coincides with regulators’ desire to see common equity ownership

» Employees are not the stock owners § The legal owners of the stock are the Trustees

7

ESOP Basics

» ESOP shares are voted in most instances by the Trustees

§ Vote pass-‐through for closely-‐held bank ESOP par(cipants in limited cases

§ Public company ESOP vote pass-‐through to par(cipants in all cases subject to shareholder vote

» ESOP can borrow money to buy stock with deduc(ble P+I payments

» Level of ESOP stock ownership is subject to Bank Change of Control Act; Reg W may also come into play

8

ESOP Bene>its

» Stock and/or cash contribu(ons are tax-‐deduc(ble to the sponsoring company

» ESOP contribu(ons may be used, when approved by the Plan Trustees, to purchase shares from the company and its shareholders

» For C Corpora(ons § “Reasonable” dividends paid are deduc(ble by the sponsor when used

to buy stock or service ESOP stock acquisi(on debt

» For S Corpora(ons § Earnings on shares held by an ESOP are untaxed

9

ESOP Bene>its

» Enhances ability to build and/or maintain capital

§ Capital is mission cri(cal for banks

» ESOP can be used as part of a broader capital management strategy

§ Conven(onal sources of capital

» Acer-‐tax earnings § ESOP creates poten(al tax savings

» ESOP bank’s Tier 1 capital can be augmented using pre-‐tax dollars

» Allows for either a faster build-‐up or a higher level of capital

» Outside investors § ESOP provides certain advantages rela(ve to raising external capital

» Ability to maintain control

» Possibly less dilu(on using ESOP

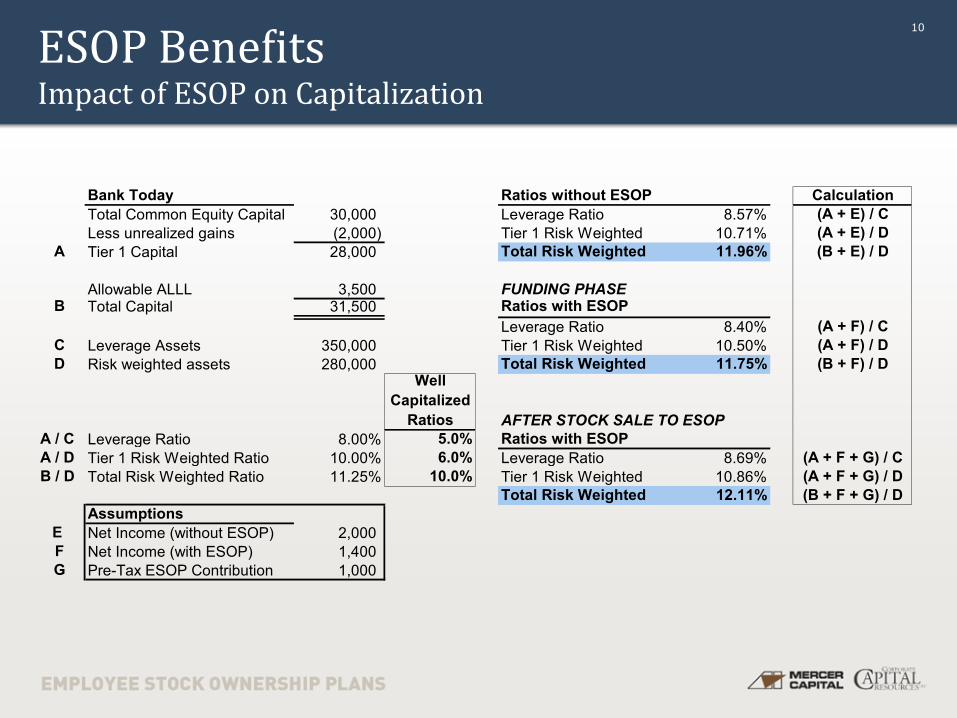

10 ESOP Bene>its Impact of ESOP on Capitalization

Bank Today Ratios without ESOP CalculationTotal Common Equity Capital 30,000 Leverage Ratio 8.57% (A + E) / CLess unrealized gains (2,000) Tier 1 Risk Weighted 10.71% (A + E) / D

A Tier 1 Capital 28,000 Total Risk Weighted 11.96% (B + E) / D

Allowable ALLL 3,500 FUNDING PHASEB Total Capital 31,500 Ratios with ESOP

Leverage Ratio 8.40% (A + F) / CC Leverage Assets 350,000 Tier 1 Risk Weighted 10.50% (A + F) / DD Risk weighted assets 280,000 Total Risk Weighted 11.75% (B + F) / D

Well Capitalized

Ratios AFTER STOCK SALE TO ESOPA / C Leverage Ratio 8.00% 5.0% Ratios with ESOP A / D Tier 1 Risk Weighted Ratio 10.00% 6.0% Leverage Ratio 8.69% (A + F + G) / CB / D Total Risk Weighted Ratio 11.25% 10.0% Tier 1 Risk Weighted 10.86% (A + F + G) / D

Total Risk Weighted 12.11% (B + F + G) / DAssumptions

E Net Income (without ESOP) 2,000F Net Income (with ESOP) 1,400G Pre-Tax ESOP Contribution 1,000

11

ESOP Bene>its

» Create an internal stock market

§ ESOP provides an addi(onal source of liquidity for investors

§ Transac(on ac(vity promotes confidence in stock pricing

» Provides an employee benefit

§ Benefit is (ed to long-‐term stock performance

» Alloca(ons of benefits in par(cipant popula(ons can be skewed using formulas which reward loyal, long-‐term employees and s(ll meet the requirements of non-‐discrimina(on

§ Smaller banks have seen highly compensated execu(ves receive 25% to 45% of all alloca(ons in the ESOP

12

Bene>its for TARP/SBLF Banks

» Banks using TARP/SBLF capital face the following challenges

§ Paying escala(ng acer-‐tax dividends over (me

§ Ul(mately redeeming the TARP/SBLF securi(es with acer-‐tax dollars

§ Poten(ally obtaining external capital to redeem TARP/SBLF preferred stock

» A minority-‐interest ESOP is not governed by TARP compensa(on regula(ons

» An ESOP can provide a poten(al source to repay TARP/SBLF obliga(ons through a combina(on of the following

§ Tax-‐deduc(ble contribu(ons used or accumulated to purchase stock

§ Tax-‐deduc(ble dividends paid on ESOP stock

13

120803 TODAY’S CPE CODE

14

ESOP Negatives

» Repurchase obliga(on § Stock in the ESOP must ul(mately be repurchased by the sponsoring corpora(on or the

plan § Represents a long-‐term, emerging obliga(on § While obliga(on is typically not booked on the balance sheet and does not impair

capital, it is a real obliga(on and will require funding § Can be managed using prudent funding and key execu(ve plans

» Fiduciary Roles § Directors and ESOP trustee(s) are fiduciaries § Personally liable for opera(ng the plan for the exclusive benefit of the plan par(cipants § Care must be taken to document the fiduciary prudence and carry the appropriate

fiduciary liability insurance for both the BOD and Trustee(s)

» Complexi(es § Added requirement to understand stock flow management

15

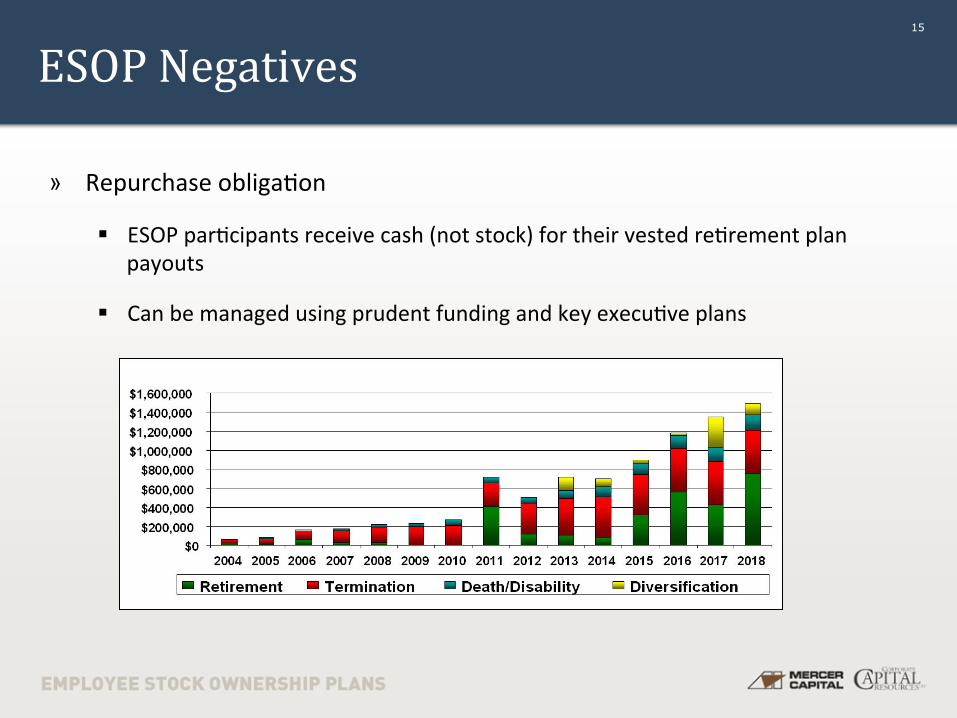

ESOP Negatives

» Repurchase obliga(on

§ ESOP par(cipants receive cash (not stock) for their vested re(rement plan payouts

§ Can be managed using prudent funding and key execu(ve plans

16 Structures Simple Annual Tax-‐Deductible Stock Contributions

C CorporaEon

The corporaEon receives a tax-‐

deducEon for the value of the newly

issued shares contributed to the

ESOP

Annual Tax-‐DeducEble ContribuEons; 25% of Pay Limit

Possible DeducEble Dividends Paid on ESOP Shares with Dividend

Paying Security

The contribuEons are discreEonary each year and deducEble, if within IRC 404 limits and paid by

the filing date of the corporate returns

ESOP Tax-‐Exempt Employee Trust ReErement Plan

ParEcipaEng Employee Stock Accounts Long-‐Term Emerging Non-‐GAAP ObligaEon

Simplified Example: The corpora(on has $5 M of pre-‐tax earnings. Its normal acer tax cash flow for capital accumula(on or dividend payments would be $3 M. With a payroll of $10 M and a 15% of pay contribu(on to the ESOP in new shares, the $1.5 M tax-‐deduc(ble stock contribu(on (a dilu(ve event) would increase the capital accumula(on to $3.6 million ($3 million + 40% of the ESOP contribu(on). The key ques(on is dilu(on: who benefits and how?

17

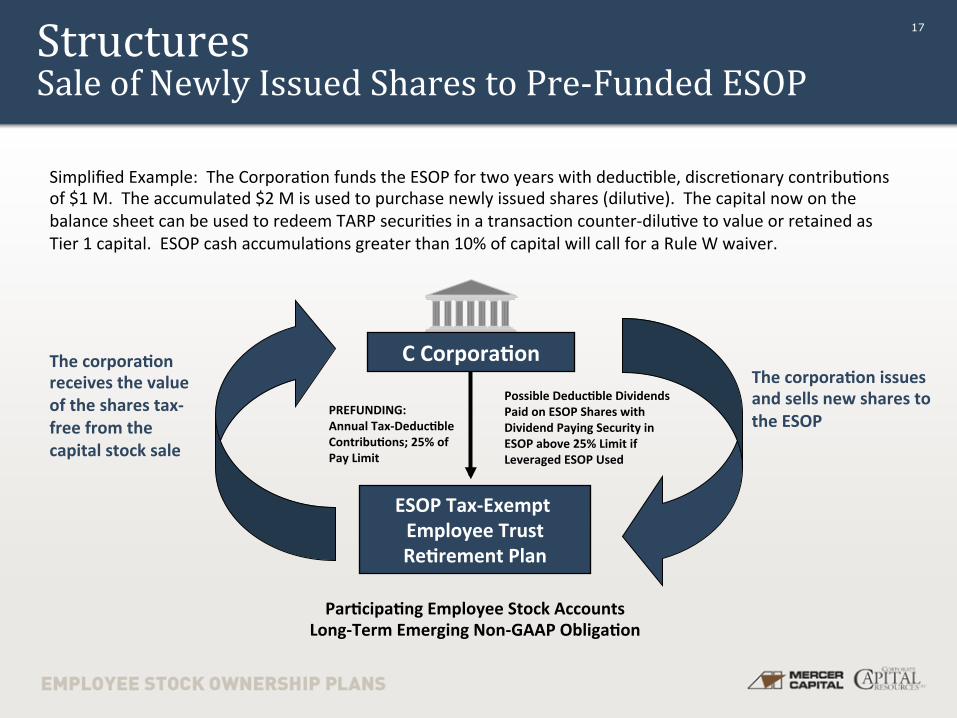

Simplified Example: The Corpora(on funds the ESOP for two years with deduc(ble, discre(onary contribu(ons of $1 M. The accumulated $2 M is used to purchase newly issued shares (dilu(ve). The capital now on the balance sheet can be used to redeem TARP securi(es in a transac(on counter-‐dilu(ve to value or retained as Tier 1 capital. ESOP cash accumula(ons greater than 10% of capital will call for a Rule W waiver.

Structures Sale of Newly Issued Shares to Pre-‐Funded ESOP

C CorporaEon

ESOP Tax-‐Exempt Employee Trust ReErement Plan

ParEcipaEng Employee Stock Accounts Long-‐Term Emerging Non-‐GAAP ObligaEon

Possible DeducEble Dividends Paid on ESOP Shares with Dividend Paying Security in ESOP above 25% Limit if Leveraged ESOP Used

The corporaEon issues and sells new shares to the ESOP

PREFUNDING: Annual Tax-‐DeducEble ContribuEons; 25% of Pay Limit

The corporaEon receives the value of the shares tax-‐free from the capital stock sale

18 Structures Tax-‐Free ESOP Cash Warehouse

» Since there may be a linle (me (perhaps two to three years) before any stock purchase, consider the following scenario:

1. Make contribu(ons to ESOP

» Contribu(on is discre(onary § Can be up to 25% of eligible compensa(on, net of other qualified plan contribu(ons

§ Can be contributed annually acer mee(ng core capital and other liquidity requirements

2. Let dollars compound tax-‐free net of trust anri(on (due to depar(ng par(cipants)

3. When funds and (ming permit, buy newly issued shares

» Poten(ally enhanced valua(on when shares are repurchased in the future

19 Structures Stock Purchase with Holding Company Financing

C CorporaEon This is the only type of ESOP loan which does not require an outside lender for the transacEon; however, the a]er-‐tax retained earnings must be accumulated first

The corporaEon repays the loan to itself with tax-‐deducEble dollars

Loan Principal and Interest Repaid to Company Loan to

ESOP Annual Tax-‐DeducEble Cash ContribuEons (Loan Principal and Interest)

ESOP Tax-‐Exempt Employee Trust ReErement Plan

Seller Cash to Fund Stock Purchase

Stock

ParEcipaEng Employee Stock Accounts Create a Long Term ESOP Stock Repurchase ObligaEon

20 Structures S Corporation ESOP

S CorporaEon

Key ExecuEve Accounts

Employees’ Accounts

Key ExecuEve Deferred

CompensaEon

$

S Corp DistribuEons

Support of ESOP Stock Repurchase ObligaEons

DeducEble ESOP ContribuEons

DeducEble ESOP ContribuEons & Pro-‐Rata Share of any S CorporaEon DistribuEons

Note: Earnings distributed to ESOP are not taxed

Note: The IRS counts key execu(ve deferred compensa(on and restricted stock as types of ‘synthe(c equity’ for the Sub S IRC §409(p) an(-‐abuse tes(ng. This is not typically an issue for properly designed plans with over 20 to 30 par(cipants. For any small bank plan, the qualified (ESOP) plan and any non-‐qualified plans should be monitored in the future to comply with this interpreta(on of EGTRRA 2001 as well as IRC 409(A). Fiduciary implica(ons of key execu(ve rewards should be discussed with ERISA counsel.

ESOP Tax-‐Exempt Single Shareholder

21

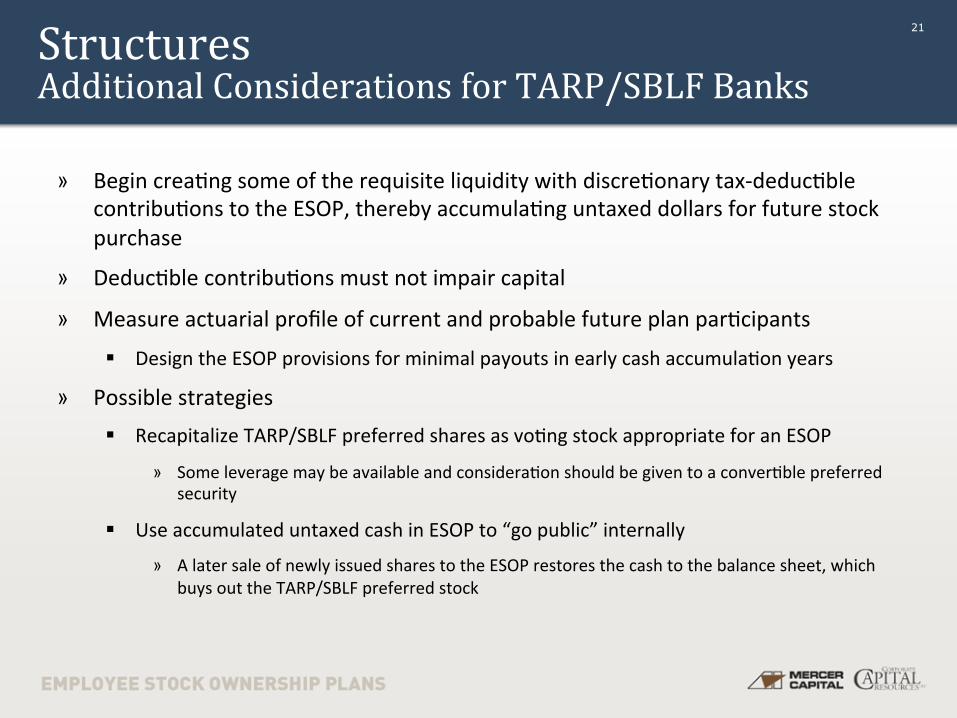

» Begin crea(ng some of the requisite liquidity with discre(onary tax-‐deduc(ble contribu(ons to the ESOP, thereby accumula(ng untaxed dollars for future stock purchase

» Deduc(ble contribu(ons must not impair capital

» Measure actuarial profile of current and probable future plan par(cipants

§ Design the ESOP provisions for minimal payouts in early cash accumula(on years

» Possible strategies § Recapitalize TARP/SBLF preferred shares as vo(ng stock appropriate for an ESOP

» Some leverage may be available and considera(on should be given to a conver(ble preferred security

§ Use accumulated untaxed cash in ESOP to “go public” internally

» A later sale of newly issued shares to the ESOP restores the cash to the balance sheet, which buys out the TARP/SBLF preferred stock

Structures Additional Considerations for TARP/SBLF Banks

22

» Future dividends paid on any preferred shares owned by the ESOP should be deduc(ble in the amount of 5% of value in years 3-‐5 and 9% of value acer 5 years

» Dividends paid on ESOP shares and used to finance the acquisi(on of the shares are tax-‐deduc(ble

» Could start the buydown process, which will con(nue each year un(l the preferred is fully redeemed in a series of transac(ons

» Other hybrid combina(ons of cash and stock may work bener

§ Final decision should be based on studies of taxes, capital requirements, employee benefits, and other variables feeding into the structure

Structures Additional Considerations for TARP/SBLF Banks

23

Parties Involved in Implementation

» Financial Advisor

» Trustee

» Administrator

» Plan Sponsor

» Administra(ve Comminee

» Anorney or Plan Designer

» Fund Manager

» Appraiser

24

120803 TODAY’S CPE CODE

25 Valuation Issues Role of Financial Advisor

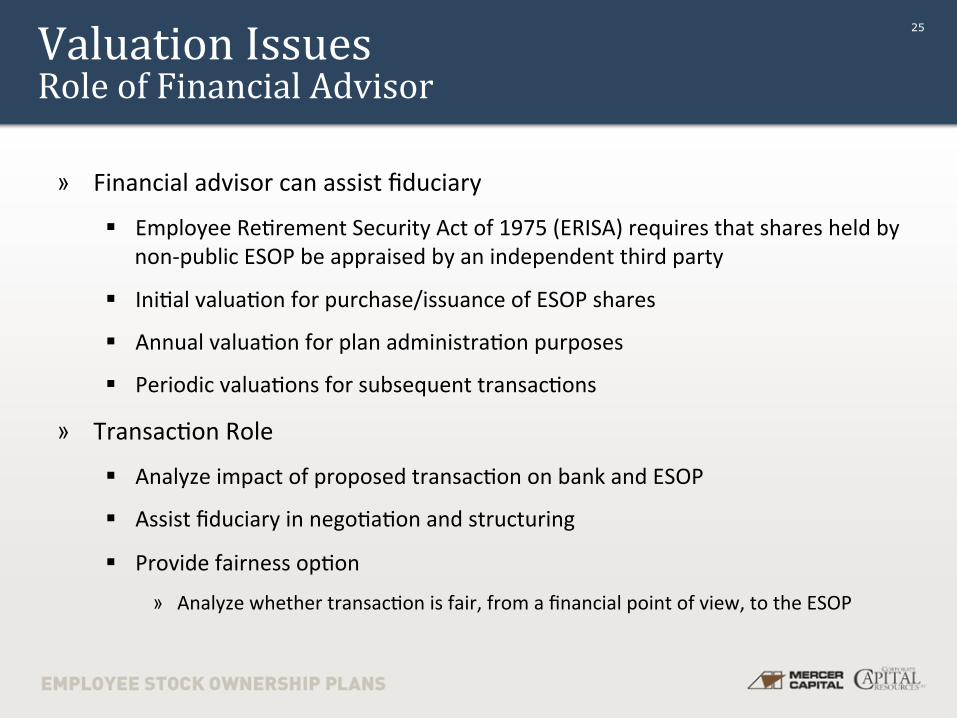

» Financial advisor can assist fiduciary

§ Employee Re(rement Security Act of 1975 (ERISA) requires that shares held by non-‐public ESOP be appraised by an independent third party

§ Ini(al valua(on for purchase/issuance of ESOP shares

§ Annual valua(on for plan administra(on purposes

§ Periodic valua(ons for subsequent transac(ons

» Transac(on Role

§ Analyze impact of proposed transac(on on bank and ESOP

§ Assist fiduciary in nego(a(on and structuring

§ Provide fairness op(on

» Analyze whether transac(on is fair, from a financial point of view, to the ESOP

26 Valuation Issues Regulatory Guidance

» Primary regulator of ESOPs is the Department of Labor (DOL)

§ Authority drawn from ERISA

» Secondarily, Internal Revenue Service has authority to review ac(vi(es of plan

» Depending upon trading volume, there are specific rules issued by the DOL & IRS to govern the valua(on process for ESOP shares

» ESOP and valua(on community have taken steps to informally create them

27 Valuation Issues Regulatory Guidance

» Adequate Considera(on

§ DOL has proposed that ESOPs must pay no more than “adequate considera(on” when buying ESOP shares and sell for no less than “adequate considera(on” when disposing of employer stock

» IRS Revenue Ruling 59-‐60

» Fair Market Value

§ The price, expressed in terms of cash equivalents, at which property would change hands between a hypothe;cal willing and able buyer and a hypothe;cal willing and able seller, ac;ng at arms’ length in an open and unrestricted market, when neither is under compulsion to buy or sell and when both have reasonable knowledge of relevant facts

Source: ASA BV Standards (November 2009)

28 Valuation Issues Marketability Discount

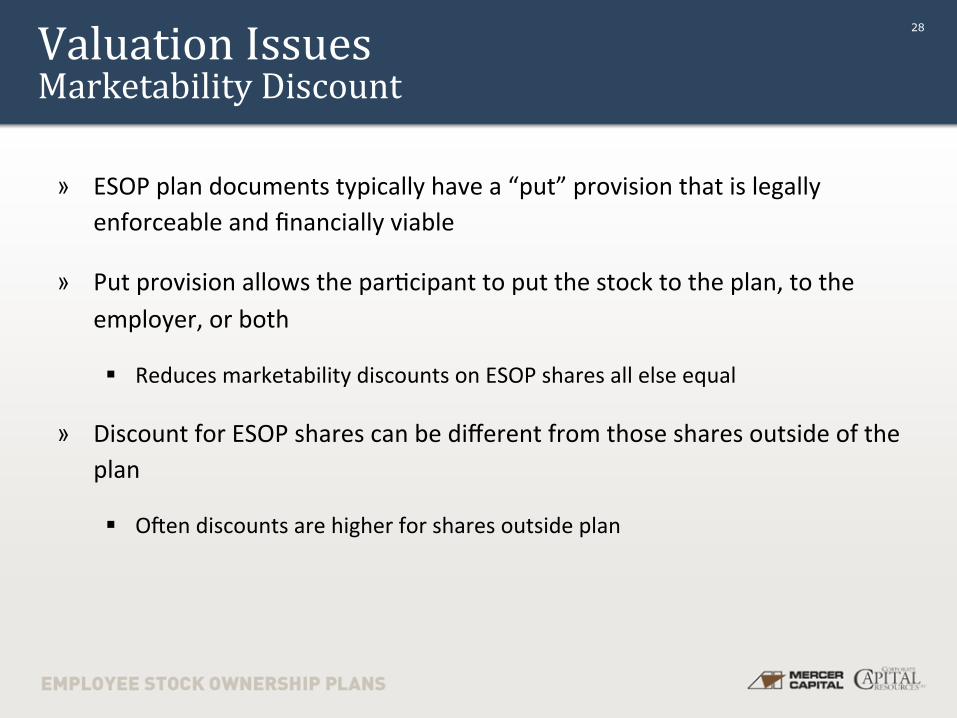

» ESOP plan documents typically have a “put” provision that is legally enforceable and financially viable

» Put provision allows the par(cipant to put the stock to the plan, to the employer, or both

§ Reduces marketability discounts on ESOP shares all else equal

» Discount for ESOP shares can be different from those shares outside of the plan

§ Ocen discounts are higher for shares outside plan

29 Valuation Issues Repurchase Obligation

» Valua(on treatment of the obliga(on to repurchase shares from par(cipants exi(ng the plan is subject to some debate

§ At one extreme, the ESOP repurchase obliga(on could be treated as an on balance sheet obliga(on

§ At the other extreme, no adjustment for the ESOP repurchase obliga(on may be made in the valua(on process

§ If adjustments are made, some argue for changing the marketability discount while others propose adjus(ng the future cash flow es(mates

§ Ul(mate adjustment, if any, depends on the circumstances of the plan (ownership interest in the sponsor, demographics of the par(cipants, available cash flow to the ESOP, etc.) and the financial performance of the sponsor

» Repurchase obliga(on can also be managed through effec(ve planning

30

Thank you for attending Andrew K. Gibbs, CFA, CPA/ABV

Senior Vice President MERCER CAPITAL

[email protected] » 901.685.2120

W. William Gust, J.D., LLM President

Corporate Capital Resources, LLC [email protected] » 540.345.4190

Michael A. Coffey

Managing Vice President Corporate Capital Resources, LLC

[email protected] » 540.345.4190