Embed Size (px)

Citation preview

Efficiency and Productivity Growth: Modelling in the Financial Services Industry, First Edition. Edited by Fotios Pasiouras.

© 2013 John Wiley & Sons, Ltd. Published 2013 by John Wiley & Sons, Ltd.

6

The impact of merger and acquisition on efficiency and market power

Franco Fiordelisi1 and Francesco Saverio Stentella Lopes2

1Department of Business Studies, University of Rome III, Italy and

Bangor Business School, Bangor University, UK2Department of Business Studies, University of Rome III, Italy and

Finance Department, Tilburg University, The Netherlands

6.1 Introduction

Merger and acquisition (M&A) deals are the two most visible expressions of the functioning

of the corporate control market. While M&A refer to two different deals, these are usually

analyzed together since both achieve the same goal (i.e., the ownership of an entire company

changes hands in a single transaction). Specifically, in a merger deal, two companies agree to

combine into a single corporate entity (rather than remain separately owned) by issuing stock

of the controlling firm to replace most of the other company’s stock. In an acquisition deal, a

company purchases a company through another company.1

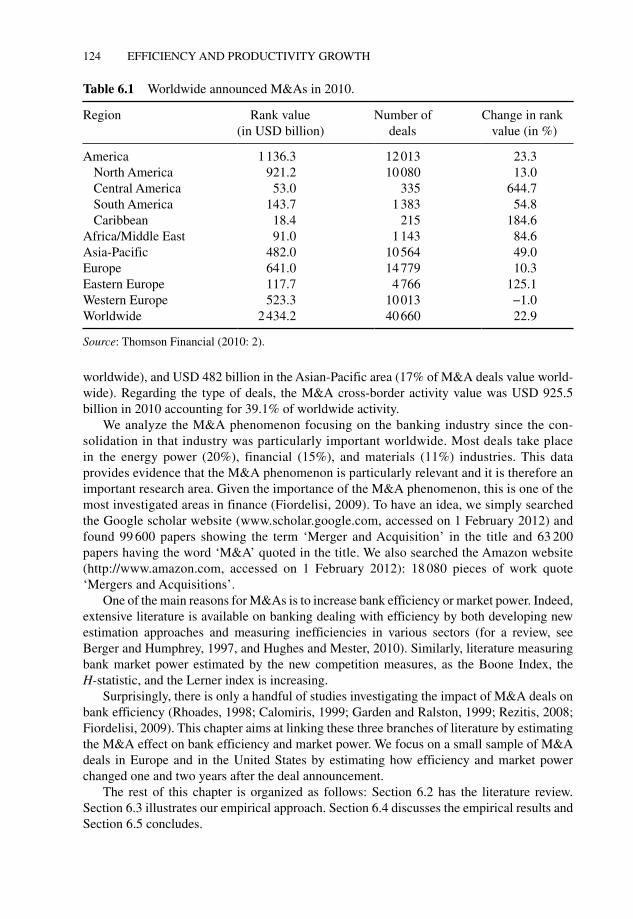

The volume of M&A transactions boosted until the end of 2007, then strongly dropped

until the second quarter of 2009 (caused by concerns in the credit markets), and thereafter

increased until the end of 2010. According to the Thomson Financial (2010), the worldwide

volume of announced M&A in 2010 was USD 2.4 trillion, that is, 22.9% increase from

the comparable 2009 levels. The M&A phenomenon concerns all countries worldwide

(Table 6.1): in 2010, M&A deals in North America was USD 821 billion (i.e., 34% of M&A

deals value worldwide), USD 523 billion in Western Europe (i.e., 21% of M&A deals value

1 For further details, see Fiordelisi (2009).

124 EFFICIENCY AND PRODUCTIVITY GROWTH

worldwide), and USD 482 billion in the Asian-Pacific area (17% of M&A deals value world-

wide). Regarding the type of deals, the M&A cross-border activity value was USD 925.5

billion in 2010 accounting for 39.1% of worldwide activity.

We analyze the M&A phenomenon focusing on the banking industry since the con-

solidation in that industry was particularly important worldwide. Most deals take place

in the energy power (20%), financial (15%), and materials (11%) industries. This data

provides evidence that the M&A phenomenon is particularly relevant and it is therefore an

important research area. Given the importance of the M&A phenomenon, this is one of the

most investigated areas in finance (Fiordelisi, 2009). To have an idea, we simply searched

the Google scholar website (www.scholar.google.com, accessed on 1 February 2012) and

found 99 600 papers showing the term ‘Merger and Acquisition’ in the title and 63 200

papers having the word ‘M&A’ quoted in the title. We also searched the Amazon website

(http://www.amazon.com, accessed on 1 February 2012): 18 080 pieces of work quote

‘Mergers and Acquisitions’.

One of the main reasons for M&As is to increase bank efficiency or market power. Indeed,

extensive literature is available on banking dealing with efficiency by both developing new

estimation approaches and measuring inefficiencies in various sectors (for a review, see

Berger and Humphrey, 1997, and Hughes and Mester, 2010). Similarly, literature measuring

bank market power estimated by the new competition measures, as the Boone Index, the

H-statistic, and the Lerner index is increasing.

Surprisingly, there is only a handful of studies investigating the impact of M&A deals on

bank efficiency (Rhoades, 1998; Calomiris, 1999; Garden and Ralston, 1999; Rezitis, 2008;

Fiordelisi, 2009). This chapter aims at linking these three branches of literature by estimating

the M&A effect on bank efficiency and market power. We focus on a small sample of M&A

deals in Europe and in the United States by estimating how efficiency and market power

changed one and two years after the deal announcement.

The rest of this chapter is organized as follows: Section 6.2 has the literature review.

Section 6.3 illustrates our empirical approach. Section 6.4 discusses the empirical results and

Section 6.5 concludes.

Table 6.1 Worldwide announced M&As in 2010.

Region Rank value

(in USD billion)

Number of

deals

Change in rank

value (in %)

America 1136.3 12013 23.3

North America 921.2 10080 13.0

Central America 53.0 335 644.7

South America 143.7 1383 54.8

Caribbean 18.4 215 184.6

Africa/Middle East 91.0 1143 84.6

Asia-Pacific 482.0 10564 49.0

Europe 641.0 14779 10.3

Eastern Europe 117.7 4766 125.1

Western Europe 523.3 10013 −1.0

Worldwide 2434.2 40660 22.9

Source: Thomson Financial (2010: 2).

THE IMPACT OF MERGER AND ACQUISITION 125

6.2 Literature review

There is a large number of studies dealing with M&As in the financial service industry, but

there is little consensus as to the effects of this consolidation on industry performance

(DeYoung, Evanoff, and Molyneux, 2009). We review studies assessing the M&A impact on

the bank’s efficiency and operating performance beyond the short time period (i.e., these

papers usually run an event study).

The first papers dealing with this issue go back to the early 1980s (Frieder and Apilado,

1983; Rhoades, 1986; Rose, 1987a, b), while most recent studies are from Huizinga, Nelissen,

and Vander Vennet (2001), Cuesta and Orea (2002), Berger and Mester (2003), Wang (2003),

Carbo-Valverde and Humphrey (2004), Humphrey and Vale (2004), Koetter (2005), De

Guevara and Maudos (2007), Ashton and Pham’s (2007), Rezitis (2008), Altunbaş and

Marqués-Ibanez (2008), Hagendorff and Vallascas (2011), and Behr and Heid (2011).

Specifically, Huizinga, Nelissen, and Vander Vennet (2001) estimate substantial scale,

cost and profit efficiency gains by analyzing 52M&As in Europe between 1994 and 1998.

Cuesta and Orea (2002) show that merged and nonmerged banks have different technical

efficiency changes by examining 858 Spanish saving banks (132 of which were involved in

M&As) over the period 1985–1998. Berger and Mester (2003) estimate substantial profit

efficiency gains by assessing a sample of US banks over the period 1984–1997. According to

Carbo-Valverde and Humphrey (2004), M&As produced positive effects both for sharehold-

ers and customers for a sample of 20M&As in Spain between 1986 and 1998. Humphrey and

Vale (2004) estimated an average cost reduction of 2.81% after assessing 26M&As in

Norway. Koetter (2005) and Ashton and Pham (2007) observe that M&As improve bank cost

efficiency in Germany and the United Kingdom, respectively. Rezitis (2008) shows that the

M&A effects on technical efficiency and total factor productivity growth of Greek banks

(1993–2004) are negative. Altunmaş and Marqués-Ibanez (2008) show that it is costly to

integrate dissimilar financial institutions by assessing a sample of European M&As from

1992 to 2001. Hagendorff and Vallascas (2011) analyze 134 European bidding banks and

show that bank mergers are generally risk neutral; for relatively safe banks, mergers also

generate a significant increase in default risk. Behr and Heid (2011) run a new analysis of

German bank mergers (1995–2000) showing a neutral effect of mergers on profitability and

cost efficiency.

As far as we are aware, there are no studies that have empirically measured the impact of

M&As on the bank’s market power.

6.3 Empirical design

This section illustrates the empirical design by presenting our data (Section 6.3.1), variables

(Section 6.3.2), and the econometric approach (Section 6.3.3).

6.3.1 Data

Our sample included mergers selected according to the following criteria: (a) merger

announced between 1 January 1998 and 2006; (b) acquirers are banks; (c) target firms are

banks, insurance companies, or other financial companies; (d) both targets and acquirers

126 EFFICIENCY AND PRODUCTIVITY GROWTH

are located in Austria, France, Germany, Greece, Italy, and the United States; (e) both the

acquiring and the target banks have been publicly quoted on a stock exchange for an entire

year prior to the announcement date and at least 20 days after the announcement day;

(f) the value of the transaction is greater than or equal to €100 million; (g) the merger was

effectively completed, generating a change of control of the target bank (i.e., the acquiring

bank has complete corporate control, holding more than 50% of the target company’s equity).

Merger data was obtained from the Thompson One bankers’ database. In order to esti-

mate the cost, scale, and revenue efficiency, we focus on both listed and nonlisted banks with

financial information obtained from Bankscope database. Overall, our sample comprises

1720 observations from unconsolidated commercial banks’ balance sheets. One hundred and

seventeen of those banks were implicated in large mergers involving target(s?) from the

United States and five European countries.

Table 6.2 (Panel A) shows the dimensions of banks in our sample. Return on equity

(ROE) is quite dispersed in the sample when we group our observation on countries. However,

looking at the overall sample average by year (Table 6.2, Panel B), we can observe that the

banks’ dimensions, in terms of total asset and total loan, have increased year by year.

Table 6.2 Descriptive statistics.

Country Total asset

(billion)

Total loan

(billion)

Return on

equity (%)

Number

observation

Panel A: Descriptive statistics grouped by countryAustria 4 2 8.00 141

France 62 18 3.00 351

Germany 16.5 8 9.00 287

Greece 12 7 2.00 173

Italy 27 12 8.00 217

United States 10 6 7.00 551

Total 22 9 6.00 1720

Year Total asset

(billion)

Total loan

(billion)

Return on

equity (%)

Number

observation

Panel B: Full sample descriptive statistics grouped by year1998 10 5 8.00 145

1999 12 5 7.00 144

2000 16 7 8.00 177

2001 19 8 6.00 142

2002 18 8 4.00 137

2003 19 8 7.00 135

2004 22 9 6.00 150

2005 27 11 8.00 169

2006 32 12 9.00 156

2007 29 12 9.00 140

2008 37 13 0.00 151

2009 53 18 −8.00 74

Total 25 10 5.00 1720

THE IMPACT OF MERGER AND ACQUISITION 127

In particular, focusing on the increased dimension in terms of total asset, we can observe

decreases in the average dimension on two occasions only, the first time between 2001 and

2002 and the second between 2006 and 2007.

6.3.2 Variables

First, we estimate bank cost efficiency (CE) by the ratio of operating cost and operating income.

Second, we estimate bank market power using the Lerner index of Monopoly Power

(LER). In this case, we use one single output in the cost function (Shaffer, 1993; Berg and

Kim, 1994; Angelini and Cetorelli, 2003; Fernandez de Guevara, Maudos, and Perez, 2005;

Casu and Girardone, 2009). The Lerner index measures the extent to which market power

allows firms to fix a price above marginal cost (MC):

MCLERNER ,it it

it

p

p

−= (6.1)

where p is the price of output Q and is calculated as total revenue (interest plus noninterest

income) divided by total assets. Marginal costs are obtained by estimating the cost function

(TC). We use the stochastic frontier approach, originally proposed by Aigner, Lovell, and

Schmidt (1977), assuming half-normal distribution for the inefficiency and pooling the data

at the country level. The final specification is as follows:

0 1 1 2 2 1

332 2 2

3 1 4 1 2

1 1

3

5 1 1 1 1

1

3 3

2 1 1 1 2 1

11

ln TC ln ln

1ln ln ln ln

2

ln ln ln ln

ln ln ln ln ln ,

it

ij j ij i

j jj

j j j j itjj

Q Z T

Q Z P P T

Z Q Q P

Z P T Q T Z T P

β β β τ

β β β τ

β β

β θ θ ψ ε

= =

=

==

= + + +

⎡ ⎤+ + + +⎢ ⎥

⎣ ⎦

+

+ + + + +

∑∑

∑

∑ ∑

(6.2)

where TC is the sum of personnel expenses, other administrative expenses, other operating

expenses, and price of funds; a, b, d, g, r, t, q, y are coefficients to be estimated; and eit is a

two-component error term eit=u

it+v

it, where v

it is a two-sided error term.2

We posit that banks’ inputs are the price of labor calculated as personnel expenses over

total assets (P1); price of funds, measured as interest expenses over total deposits plus money

market funding and other funding (P2); and one additional input, the price of physical capital,

measured as other administrative expenses plus other operating expenses over total assets

(P3). On the other hand, and despite the multi-output nature of the investment banking busi-

ness, we define total assets (Q1) as one single output. By doing so, we assume that the flow

of services produced by an investment bank is proportional to its total assets. Finally, to

2 The vit are assumed to be independently and identically normal distributed with mean 0 and variance σ 2

v and

independent of uit, where the latter is a one-sided error term capturing the effects of inefficiency and assumed to be

half-normally distributed with mean 0 and variance σ 2

u . We apply the common restrictions of standard symmetry

and homogeneity in prices to the translog functional form.

128 EFFICIENCY AND PRODUCTIVITY GROWTH

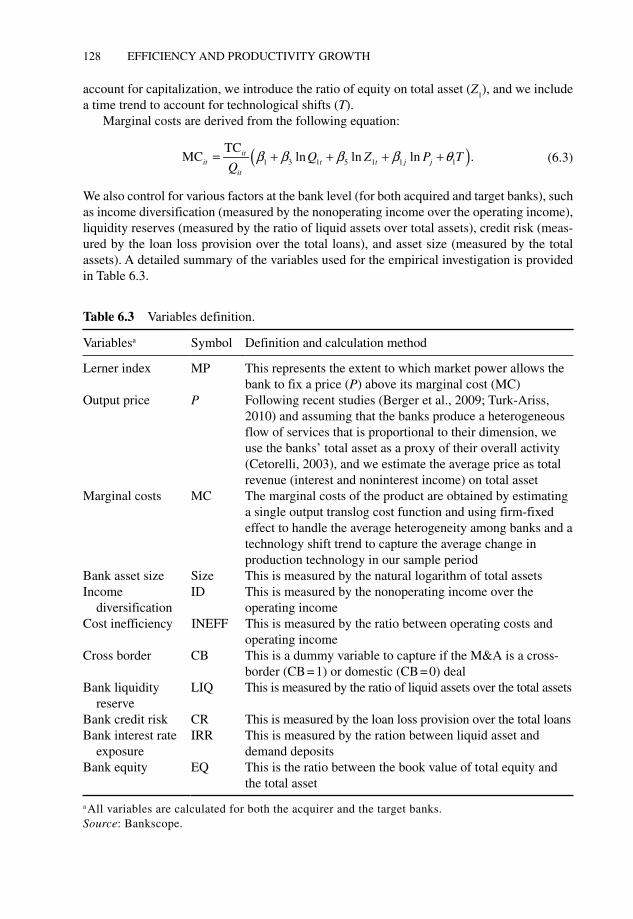

account for capitalization, we introduce the ratio of equity on total asset (Z1), and we include

a time trend to account for technological shifts (T).

Marginal costs are derived from the following equation:

( )1 3 1 5 1 1 1

TCMC ln ln ln .it

it t t j jit

Q Z P TQ

β β β β θ= + + + + (6.3)

We also control for various factors at the bank level (for both acquired and target banks), such

as income diversification (measured by the nonoperating income over the operating income),

liquidity reserves (measured by the ratio of liquid assets over total assets), credit risk (meas-

ured by the loan loss provision over the total loans), and asset size (measured by the total

assets). A detailed summary of the variables used for the empirical investigation is provided

in Table 6.3.

Table 6.3 Variables definition.

Variablesa Symbol Definition and calculation method

Lerner index MP This represents the extent to which market power allows the

bank to fix a price (P) above its marginal cost (MC)

Output price P Following recent studies (Berger et al., 2009; Turk-Ariss,

2010) and assuming that the banks produce a heterogeneous

flow of services that is proportional to their dimension, we

use the banks’ total asset as a proxy of their overall activity

(Cetorelli, 2003), and we estimate the average price as total

revenue (interest and noninterest income) on total asset

Marginal costs MC The marginal costs of the product are obtained by estimating

a single output translog cost function and using firm-fixed

effect to handle the average heterogeneity among banks and a

technology shift trend to capture the average change in

production technology in our sample period

Bank asset size Size This is measured by the natural logarithm of total assets

Income

diversification

ID This is measured by the nonoperating income over the

operating income

Cost inefficiency INEFF This is measured by the ratio between operating costs and

operating income

Cross border CB This is a dummy variable to capture if the M&A is a cross-

border (CB=1) or domestic (CB=0) deal

Bank liquidity

reserve

LIQ This is measured by the ratio of liquid assets over the total assets

Bank credit risk CR This is measured by the loan loss provision over the total loans

Bank interest rate

exposure

IRR This is measured by the ration between liquid asset and

demand deposits

Bank equity EQ This is the ratio between the book value of total equity and

the total asset

a All variables are calculated for both the acquirer and the target banks.

Source: Bankscope.

THE IMPACT OF MERGER AND ACQUISITION 129

6.3.3 The econometric approach

We estimate the effect of M&A on bank market power by running the following linear mul-

tiple regression models:

( ) ( ) ( ) ( ) ( )α β γ ε −− − − − −Δ = + + + + + +∑ ∑0 1,; 1, , 1 , 1 ; 1 ; 1MP ID CI CB ,i j t tTj t t i t j t Tj t Tj tX Z (6.4)

( ) ( ) ( ) ( ) ( )α β γ ε −− − − − −Δ = + + + + + +∑ ∑0 1,; 2, , 2 , 2 ; 2 ; 2MP ID CI CB ,i j t tTj t t i t j t Tj t Tj tX Z (6.5)

( ) ( ) ( ) ( ) ( )α β γ ε −− − − − −Δ = + + + + + +∑ ∑0 1,; 1, , 1 , 1 ; 1 ; 1MP ID CI CB ,i j t tAj t t i t j t Aj t Aj tX Z (6.6)

( ) ( ) ( ) ( ) ( )α β γ ε −− − − − −Δ = + + + + + +∑ ∑0 1,; 2, , 2 , 2 ; 2 ; 2MP ID CI CB ,i j t tAj t t i t j t Aj t Aj tX Z (6.7)

where ΔMP(Aj;t − 1,t)

is the Lerner index change for the acquirer bank j between the time period

t and t − 1; ΔMP(Aj;t − 2,t)

is the Lerner index change for the acquirer bank j between the time

period t and t − 2; ΔMP(Tj;t − 1,t)

is the Lerner index change for the target bank j between the

time period t and t − 1; ΔMP(Tj;t − 2,t)

is the Lerner index change for the target bank j between

the time period t and t − 2; Xi (i =1, …, 5) is a set of features of the target bank (that is also

considered for the acquirer bank), Zi (i=1, …, 5) is a set of features of the acquirer bank (that

is also considered for the target bank); ID is the income diversification (measured by the

nonoperating income over the operating income); CI is the cost income ration (measured by

the ratio of operating income over operating costs); CB is a dummy variable to capture if the

M&A is a cross-border (CB=1) or domestic (CB=0) deal. Specifically, we include as bank

variables the following three items: liquidity reserves (measured by the ratio of liquid assets

over total assets), credit risk (measured by the loan loss provision over the total loans), and

asset size. A detailed summary of the variables used for the empirical investigation is

provided in Table 6.3.

6.4 Results

Focusing on a sample of large M&A deals, we analyze the relationship between market

power changes (after one and two years) and various bank characteristics for both target and

bidder banks.

First, we analyze the M&A effects for the target bank. As shown in Panel A of Table 6.4,

we find that target banks’ market power variation between two consecutive years is negatively

related to their asset size (at the 1% confidence level), their liquidity reserves (at the 1%

confidence level), and their credit risk (at the 5% confidence level): this shows that target

banks achieve larger market power changes in one year if they are smaller, with lower credit

risk and smaller liquid assets. The negative link between bank asset size and market power

seems to support the existence of increasing returns to scale: as a bank increases its size by

merging with another bank, the latter increases its market power. The negative link between

bank credit risk and market power shows that the bank’s ability in screening and managing

loans is positively related to the bank’s market power. The negative link between liquidity

reserves and market power may appear surprising since one may expect that safer banks

will also have a larger market power. There are various reasons that explain this result:

130 EFFICIENCY AND PRODUCTIVITY GROWTH

first, liquidity reserves have a high opportunity cost, and this affects the bank’s market

power negatively; second, our empirical analysis is based on a period of banking stability

(1998–2006) – the recent financial crisis reminded bankers of the fact that liquidity manage-

ment is critical in banking, but this point was underestimated (and taken for granted) in

times of banking prosperity. Surprisingly, we find that the acquirer bank features do not

display a statistically significant (at the 10% confidence level or less) link with the target

banks’ market power changes.

When we extend our analysis over a two-year time period (Panel B of Table 6.4), we

find that only the target bank credit risk is statistically significantly related to the target

banks’ market power changes: this shows that the bank’s ability in screening and managing

loans is the only factor that is (statistically significant at 10% or less) related to its market

power changes.

Focusing on the acquirer bank, we find that the banks’ market power variation between

two consecutive years is negatively related to their asset size (at the 5% confidence level) and

cross-border deals (at the 5% confidence level). We also observe a positive link between

banks’ market power variation and income diversification (at the 10% confidence level). Our

findings suggest that acquirer banks achieve larger market power changes in one year if they

are smaller, involved in domestic deals, and more diversified. The negative link between the

bank asset size and market power seems to support the existence of increasing returns to

scale: as a bank increases its size by merging with another bank, this bank increases its market

power. The negative link between cross-border merger deals and market power is consistent

with the previous studies showing that these deals do not create value for acquirer banks.

Table 6.4 The merger effects on bank market power: the target.

Panel A (one year) y=ΔMP(Tj;t − 1,t)

Panel B (two years) y=ΔMP(Tj;t − 2,t)

Coefficient Standard error Coefficient Standard error

SizeT

−0.6297* 0.3291 −0.6422 0.3793

LIQT

−0.0260* 0.0148 −0.0247 0.0250

CRT

−2.7845** 1.2507 −4.0360** 1.9511

SizeA

−0.0010 0.0028 −0.0030 0.0045

LIQA

−0.0033 0.0356 0.0024 0.0528

CRA

−0.0211 0.0247 −0.0015 0.0361

CB 0.0074 0.0135 −0.0154 0.0179

IDT

−0.0132 0.0118 −0.0008 0.0308

INEFFT

−0.0340 0.0419 −0.0463 0.0834

INEFFT

0.0842 0.2849 −0.1107 0.4188

Intercept 0.0756 0.0604 0.1487 0.0944

Number of

observations 56 56

Adjusted R2 0.3256 0.3494

The subscript T denotes that the variable refers to the target bank; A denotes that the variable refers to

the acquirer bank.

*Statistically significant at the 1% level.

**Statistically significant at the 5% level.

THE IMPACT OF MERGER AND ACQUISITION 131

The positive link between income diversification and market power is not surprising since

more diversified banks achieve higher benefit than less diversified banks by merging with

other banks. Surprisingly, we find that target bank features do not display a statistically signifi-

cant (at the 10% confidence level or less) link with the acquirer banks’ market power changes.

When we extend our analysis over a two-year time period (Panel B of Table 6.5), we find

very consistent results with the ones discussed earlier. As such, we find that the estimated

relationships between market power changes are more time-persistent for acquirer banks than

for target banks.

6.5 Conclusions

We analyzed the relationship between market power changes (after one and two years) and

various bank characteristics for both target and bidder banks by using a sample of large M&A

deals in Europe and the United States, prior to the financial crisis. Overall, our sample

comprises 1720 observations from unconsolidated commercial banks’ balance sheets. One

hundred and seventeen of those banks were implicated in large mergers involving targets

from the United States and five European countries.

Despite the economic literature dealing with M&As in banking being vast, there are no

studies that have empirically measured the impact of M&As on bank’s market power.

We show that target banks achieve larger market power changes in one year if these banks

are smaller, with lower credit risk and smaller liquid assets. These results suggest the exist-

ence of increasing returns to scale and that the bank’s ability in screening and managing loans

is positively related to the bank market power. When we extend our analysis over a two-year

period, the target bank credit risk is statistically significantly related to the target banks’ market

Table 6.5 The merger effects on bank market power: the acquirer.

Panel A y=ΔMP(Tj;t − 1,t)

Panel B y=ΔMP(Tj;t − 2,t)

Coefficient Standard error Coefficient Standard error

SizeT

−0.9529 2.1112 −0.5267 2.0001

LIQT

−0.1312 0.1062 −0.1391 0.1049

CRT

9.5915 11.3126 6.1812 10.4669

SizeA

−0.0391* 0.0179 −0.0201* 0.0104

LIQA

−0.2376 0.2201 −0.2717 0.2159

CRT

−0.0909 0.1358 −0.1331 0.1383

CB −0.1963** 0.0830 −0.1448* 0.0762

IDA

0.1867* 0.1070 0.1642* 0.0870

INEFFA

−0.0423 0.4206 0.0119 0.4310

INEFFA

1.8546 1.9692 2.3783 2.0114

Intercept 0.6220 0.4466 0.2844 0.3946

Number of observations 56 56

Adjusted R2 0.2659 0.2179

*Statistically significant at the 1% level.

**Statistically significant at the 5% level.

132 EFFICIENCY AND PRODUCTIVITY GROWTH

power changes. Focusing on the acquirer banks, we show that they achieve larger market

power changes in one year if these banks are smaller, involved in domestic deals, and more

diversified. Surprisingly, we find that the target bank features do not display a statistically

significant link with the acquirer banks’ market power changes and the reverse.

References

Aigner, D.J., Lovell, C.A.K., and Schmidt, P. (1977) Formulation and estimation of stochastic frontier

production function models. Journal of Econometrics, 6, 21–37.

Altunbaş, Y. and Marqués-Ibanez, D. (2008) Mergers and acquisitions and bank performance in Europe:

the role of strategic similarities. Journal of Economics and Business, 60, 204–222.

Angelini, P. and Cetorelli, N. (2003) The effects of regulatory reform on competition in the banking

industry. Journal of Money, Credit and Banking, 35, 663–684.

Ashton, J.K. and Pham, K. (2007) Efficiency and price effects of horizontal bank mergers. CCP

working paper no. 07-9. Available at SSRN: http://ssrn.com/abstract=997995 (accessed on 12

December 2012).

Behr, A. and Heid, F. (2011) The success of bank mergers revisited: an assessment based on a matching

strategy. Journal of Empirical Finance, 18, 117–135.

Berg, S.A. and Kim, M. (1994) Oligopolistic interdependence and the structure of production in bank-

ing: an empirical evaluation. Journal of Money, Credit and Banking, 26, 309–322.

Berger, A.N. and Humphrey, D.B. (1997) Efficiency of financial institutions: international survey and

directions for future research. European Journal of Operational Research, 98, 175–212.

Berger, A.N. and Mester, L.J. (2003) Explaining the dramatic changes in performance of US banks:

technological change, deregulation, and dynamic changes in competition. Journal of Financial Intermediation, 12, 57–95.

Berger, A.N., Klapper F.L. and Turk-Ariss, R. (2009) Bank competition and financial stability. Journal of Financial Services Research, 35, 99–118.

Calomiris, C.W. (1999) Gauging the efficiency of bank consolidation during a merger wave. Journal of Banking and Finance, 23, 615–621.

Carbo-Valverde, S. and Humphrey, D.B. (2004) Predicted and actual costs from individual bank mergers.

Journal of Economics and Business, 56, 137–157.

Casu, B. and Girardone, C. (2009) Testing the relationship between competition and efficiency in banking:

a panel data analysis. Economics Letters, 105, 134–137.

Cetorelli, N. (2003) Life-cycle dynamics in industrial sectors: the role of banking market structure.

The Federal Reserve Bank of St. Louis Review, 85, 135–148.

Cuesta, R.A. and Orea, L. (2002) Time varying efficiency and stochastic distance functions: the effect

of mergers on Spanish savings banks. Journal of Banking and Finance, 26, 2231–2247.

De Guevara, J.F. and Maudos, J. (2007) Explanatory factors of market power in the banking system.

The Manchester School, 75, 275–296.

DeYoung, R., Evanoff, D., and Molyneux, P. (2009) Mergers and acquisitions of financial institutions:

a review of the post-2000 literature. Journal of Financial Service Research, 36, 87–110.

Fernandez de Guevara, J., Maudos, J., and Perez, F. (2005) Market power in European banking sector.

Journal of Financial Services Research, 27, 109–137.

Fiordelisi, F. (2009) M&A in Banking, Palgrave Macmillan, Studies in Banking and Financial

Institution, UK.

Frieder, L.A. and Apilado, V.P. (1983) Bank holding company expansion: a refocus on its financial

rationale. Journal of Financial Research, 6, 67–81.

THE IMPACT OF MERGER AND ACQUISITION 133

Garden, K.A. and Ralston, D.E. (1999) The x-efficiency and allocative efficiency effects of credit union

mergers. Journal of International Financial Markets, Institutions and Money, 9, 285–301.

Hagendorff, J. and Vallascas, F. (2011) CEO pay incentives and risk-taking: evidence from bank acqui-

sitions. Journal of Corporate Finance, 17 (4), 1078–1095.

Hughes, J.P. and Mester, L.J. (2010) Efficiency in banking: theory, practice, and evidence, in TheOxford Handbook of Banking (eds A.N. Berger, P. Molyneux, and J. Wilson), Oxford University

Press, Oxford.

Huizinga, H.P., Nelissen, J.H.M., and Vander Vennet, R. (2001) Efficiency effects of bank mergers and

acquisitions in Europe. Tinbergen Institute, discussion paper no. 2001-088/3.

Humphrey, D.B. and Vale, B. (2004) Scale economies, bank mergers, and electronic payments: a spline

function approach. Journal of Banking and Finance, 28, 1671–1696.

Koetter, M. (2005) Evaluating the German bank merger wave. Deutsche Bundesbank, discussion paper,

series 2: banking and financial studies no. 12.

Rezitis, A.N. (2008) Efficiency and productivity effects of bank mergers: evidence from the Greek

banking industry. Economic Modelling, 25, 236–254.

Rhoades, S.A. (1986) The Operating Performance of Acquired Firms in Banking Before and After Acquisition. Staff Studies 149. Washington: Board of Governors of the Federal Reserve System,

1986. A version with alternative statistical tests is, The Operating Performance of Acquired Firms in Banking (eds R. Wills, J.A. Caswell, and J.D. Culbertson), Issues after a Century of Federal.

Rhoades, S.A. (1998) The efficiency effect of bank mergers: an overview of case studies of nine mergers.

Journal of Banking and Finance, 22, 273–291.

Rose, P.S. (1987a) Improving regulatory policy for mergers: an assessment of bank merger motivations

and performance effects. Issues in Bank Regulation, 10 (3, Winter), 32–39.

Rose, P.S. (1987b) The impact of mergers in banking: evidence from a nationwide sample of federally

chartered banks. Journal of Economics and Business, 39, 289–312.

Shaffer, S. (1993) A test of competition in Canadian banking. Journal of Money, Credit and Banking,

25, 49–61.

Thomson Financial (2010) Mergers & Acquisitions Review, Fourth Quarter 2010. http://banker.

thomsonib.com (accessed on 20 December 2012).

Turk-Ariss, R. (2010) On the implications of market power in banking: evidence from developing countries.

Journal of Banking and Finance, 34, 765–775.

Wang, J.C. (2003) Merger-related cost savings in the production of bank services. Federal Reserve

Bank of Boston, working paper no. 03-8.