Embed Size (px)

Citation preview

Strictly Private and Confidential

Edelweiss Financial Services Limited

Annual Investor Presentation – May 2014

Focused on Long Term Value Creation

Quality Businesses

Corporate Overview

Driving Non Linear Growth

2

Contents

Focused on Long Term Value Creation

Quality Businesses

Corporate Overview

Driving Non Linear Growth

3

Contents

Another Year of Non-Linear Growth

(INR cr) FY12 FY13 FY14

PAT 128 178 220

PAT Ex-Insurance 141 226 272

Balance Sheet Size* 12,986 14,224 16,043

*EOP numbers

23%

YoY Growth

20%

13%

4

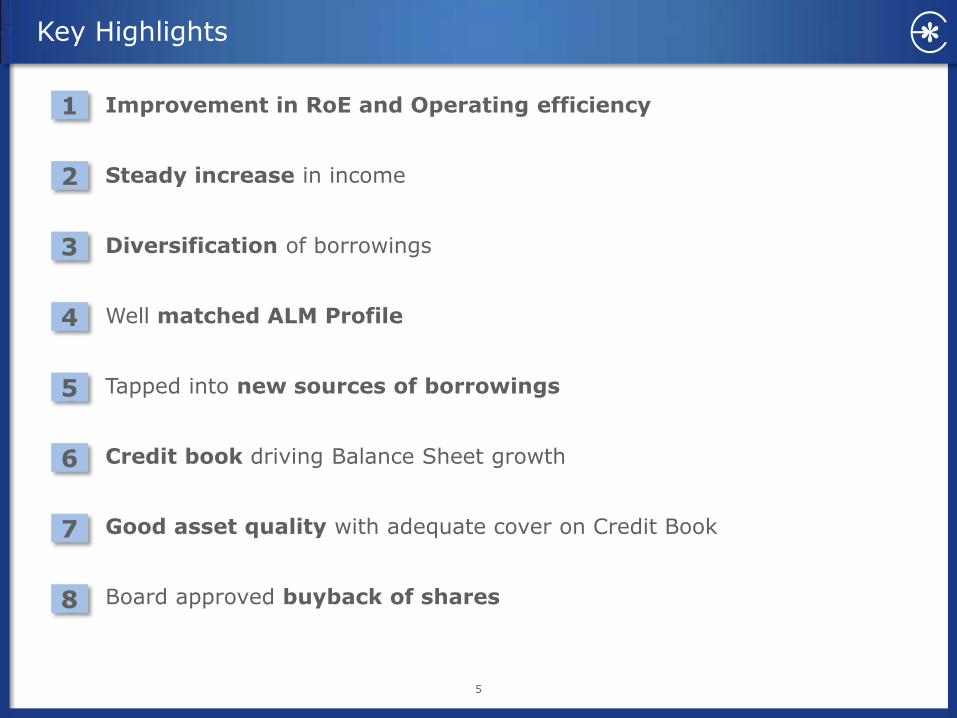

Key Highlights

5

Improvement in RoE and Operating efficiency

Steady increase in income

Diversification of borrowings

Well matched ALM Profile

Tapped into new sources of borrowings

Credit book driving Balance Sheet growth

Good asset quality with adequate cover on Credit Book

Board approved buyback of shares

1

2

3

4

5

6

7

8

Improvement in RoE and Operating Efficiency

72%

67%

64%

FY12 FY13 FY14

Reducing Cost to Income Ratio

(Ex-Insurance )

7.0%

11.3% 12.3%

FY12 FY13 FY14

Improved Tangible RoE (Ex-Insurance )

1

6 Cost to Income Ratio = Opex/(Revenue – Interest Cost)

Steady Increase in Net Fund Based Income

7

(INR cr)

FY12 FY13 FY14

Net Fund Based Income 509 699 883

As % of Total Assets 3.9% 4.9% 5.5%

2

Notes: Net Fund Based Income = Fund Based Revenue – Financing Costs

Stronger Balance Sheet: Diversified Sources of Borrowings

8

Debt Market

Bank

ASB

Retail

Others

FY11 FY14

Number of lenders have increased manifold

50%

26%

14%

5%

34%

15%

13%

3%

Total Borrowings

INR 7,858 cr INR 12,948 cr

35%

5%

3

9

% o

f A

ssets

an

d L

iab

ilit

ies

Positive ALM ALCO manages and monitors ALM, Interest Rate Risk and Liquidity

13%

38%

48%

62%

79%

100%

13%

36%

46%

59%

76%

100%

ASB 0-3 Mnth 3-6 Mnth 6-12 Mnth 1-3 years 3+ years

Assets Liabilities

March’14 - INR 16,043 cr

Notes: ASB – Asset Specific Borrowing

Stronger Balance Sheet: Well Matched ALM Profile 4

Stronger Balance Sheet: Successfully Tapped Into New Sources of Borrowings & Improved Long Term Rating

10

• Added Tier II capital of INR 77 Cr in form of preference shares to boost networth

Preference Shares

• Issued INR 500 cr of Retail Bonds to strengthen Balance Sheet and reduce dependence on short term borrowing

• Issue was subscribed 2X within 2 days

Retail Bond Issue

• Securitized INR 150 Cr of Mortgage and SME lending portfolio

Securitization

• Long Term rating notched up to AA Rating

Improvement

• NHB re-finance sanctioned NHB

Re-Finance

5

11

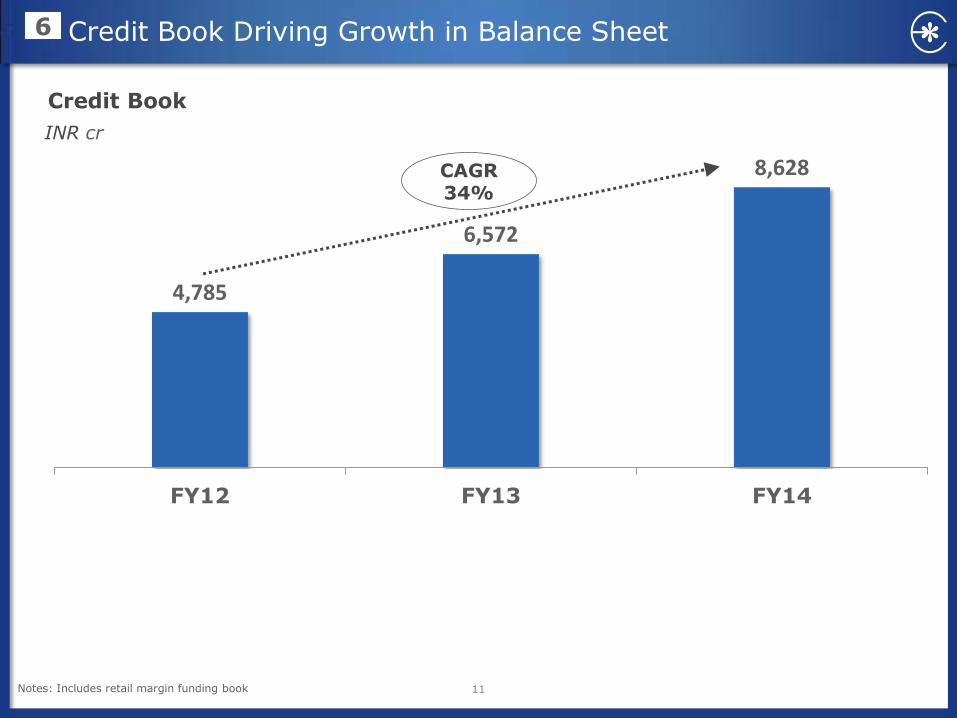

Credit Book Driving Growth in Balance Sheet

4,785

6,572

8,628

FY12 FY13 FY14

CAGR 34%

INR cr

6

Credit Book

Notes: Includes retail margin funding book

Good asset quality and cover on Credit book 7

12

(INR cr) FY12 FY13 FY14

Asset Quality

Total Loans1 4,785 6,572 8,628

Gross GNPLs 23 28 82

Net NPLs 7 7 21

Gross GNPLs 0.47% 0.43% 0.95%

Net NPLs 0.14% 0.11% 0.25%

Total Provision Held2 26 37 82

Total Provision Cover2 116% 131% 100%

Collateral Cover

Collateral Cover in Corporate Loans 2.6x 2.4x 2.6x

LTV% in Retail Finance ~55% ~56% ~55%

Notes: Numbers are Management Estimates 1 Includes retail margin funding book 2 Total Provision includes General Loan Loss Provision on Standard Assets

13

Board has approved buyback of shares which commenced on 5th May 2014

Price not exceeding INR 45/share

Current Market Price (NSE) ~INR 37.3 / share as on 16th May 2014

Continued Investor Distribution through Dividends and Buyback

60% 60%

65%

70%

FY11 FY12 FY13 FY14

Dividend payout %

Consistent dividend payout history

Approved buyback of INR 135 Cr

8

Focused on Long Term Value Creation

Quality Businesses

Corporate Overview

Driving Non Linear Growth

14

Contents

To be a respected Financial Services firm with a portfolio of high quality growth businesses

Our Strategy is:

15

Diversification led to a De-risked Model…

16

Life

Insurance

Small Ticket

Housing

loans

1996 - 2000

Corporate

Loans & Asset

Mgmt.

Housing Finance

Investment

Banking

Institutional

Equities

& Treasury

HNI Broking

SME

Finance

Precious Metals &

Debt Capital

Markets

Retail Capital

Markets

2005 - 2008 2008 - 2014

Retail Businesses

Wholesale Businesses

…Resulting in a More Stable Revenue Pool

17

Credit 15%

Financial Markets &

Asset Management

44%

Treasury 34%

Commodities 7%

FY08

Credit 44%

Financial Markets &

Asset Management

21%

Treasury 15%

Commodities 14%

Insurance 6%

FY14

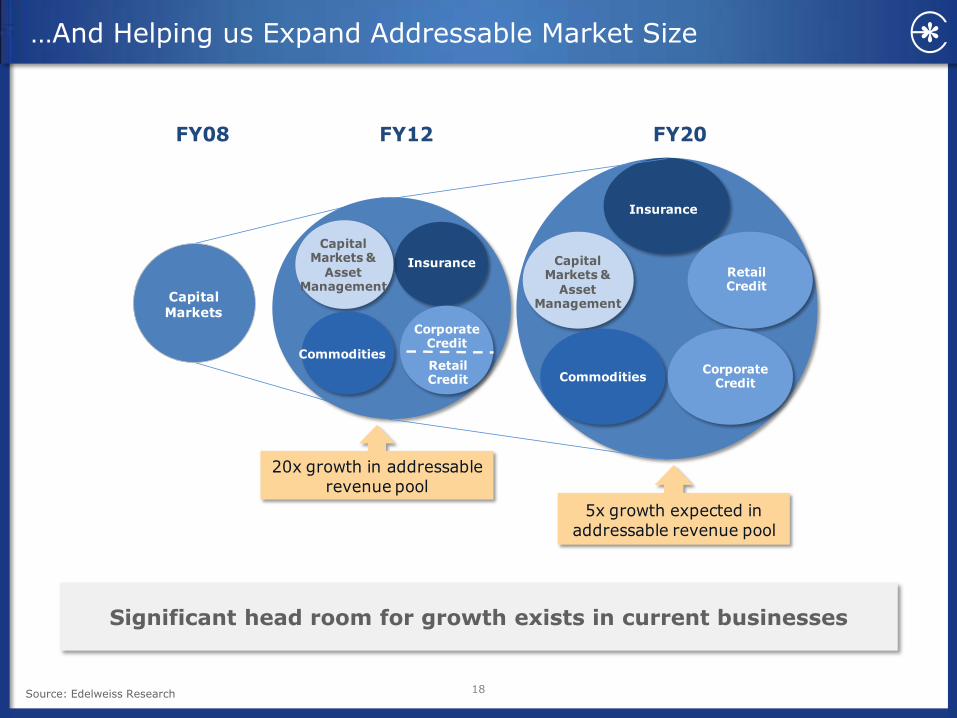

…And Helping us Expand Addressable Market Size

18 Source: Edelweiss Research

CapitalMarkets

FY08 FY12 FY20

Commodities

Capital Markets &

Asset Management

Insurance

CorporateCredit

RetailCredit

Capital Markets &

Asset Management

Insurance

Retail Credit

Corporate Credit

Commodities

20x growth in addressable revenue pool

5x growth expected in addressable revenue pool

Significant head room for growth exists in current businesses

19

Our Value Proposition is: Long Term Value Creation

Profitability

Scalability

Sustainability

Management Quality

Governance Long term Value Creation

Our long term value drivers

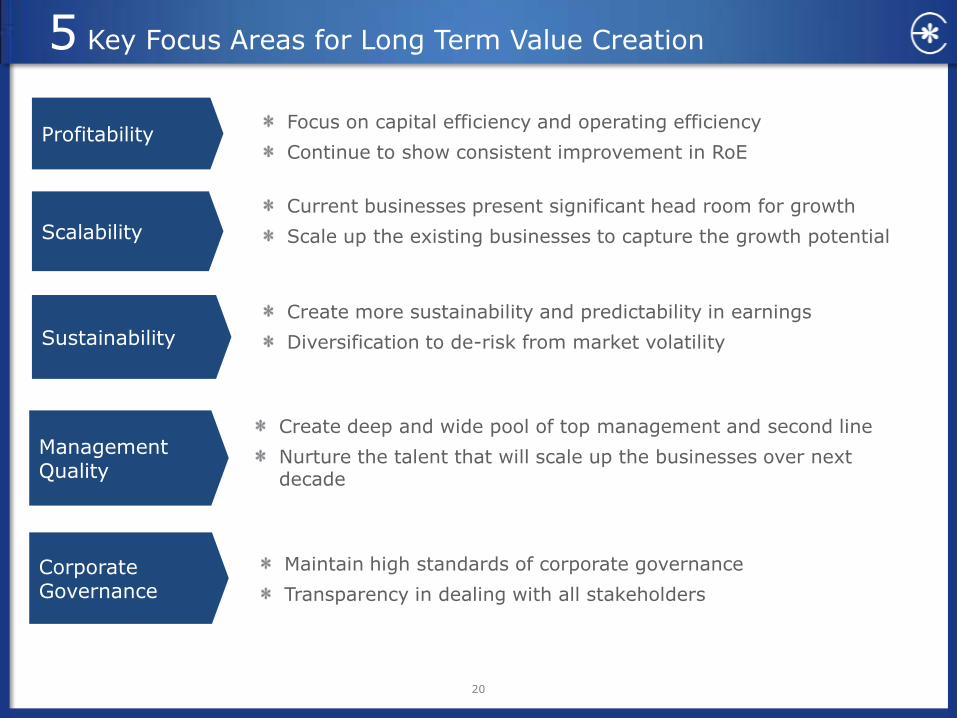

5 Key Focus Areas for Long Term Value Creation

20

Focus on capital efficiency and operating efficiency

Continue to show consistent improvement in RoE Profitability

Create more sustainability and predictability in earnings

Diversification to de-risk from market volatility Sustainability

Current businesses present significant head room for growth

Scale up the existing businesses to capture the growth potential Scalability

Create deep and wide pool of top management and second line

Nurture the talent that will scale up the businesses over next decade

Management Quality

Maintain high standards of corporate governance

Transparency in dealing with all stakeholders

Corporate Governance

Focused on Long Term Value Creation

Quality Businesses

Corporate Overview

Driving Non Linear Growth

21

Contents

22

Edelweiss Operating Structure – 5 Business Groups

Balance Sheet Management

Unit

• Liquidity management

• Capital preservation with optimum returns

Financial Markets

• Corporate Finance Advisory

• Broking & Wealth Management

Strong franchise

across product spectrum

Commodities

• Agri Commodities

• Precious Metals

• Agri Services

• Credit & Distribution

Bringing efficiency to commodities

Asset Management Credit

Corporate Collateral Based

Lending & Advisory

Retail Housing Finance

SME Finance Rural Finance

Customer centric credit

solutions

Life Insurance

• JV with Tokio Marine

• Proprietary need based selling approach

New age player with no legacy

issues

• Asset Reconstruction

• Mutual Funds

• Offshore Funds

• Alternative Asset Management

Differentiated offerings and top quartile performance

Business Groups – FY14 Financial Snapshot

23

(INR cr) Revenue Profit Before

Tax

Tangible Networth1

Total Capital

Employed1

Pre-tax RoE

Pre-tax RoA

Credit 1,112 291 1,200 7,905 24% 3.7%

Financial Markets 464 30 211 1,362 14% 2.2%

Asset Management 60 15 243 719 6% 2.1%

Commodities 412 86 362 1,344 24% 6.4%

Balance Sheet Management Unit 344 41 253 2,981 16% 1.4%

Corporate & Unallocated2 -42 189 1,095 N/A N/A

Total - Ex Insurance 2,392 420 2,458 15,406 17% 2.7%

Insurance 164 -69 637 637 N/A N/A

Total 2,556 351 3,095 16,043 11% 2.2%

Notes: Numbers are Management Estimates 1 Does not include Goodwill and shares owned by employee trust 2 Investments in office building, Strategic Investments and Advance tax paid

24

CREDIT

Credit Opportunity in India

25

Source: Edelweiss Research, RBI

Bank and NBFC Credit INR’000 cr

Low penetration of Mortgage in India

Huge market for credit exists

Market has been growing at 15% p.a. even in tough market conditions

NBFCs have been growing faster than Banks in recent past

Quality risk management systems are a must before scaling up of books

Edelweiss has been investing in credit systems and gradually scaling up the books

1,885 2,318

2,729 3,196

3,878

4,531

5,164

211 279 318 381 496 620 744

2007 2008 2009 2010 2011 2012 2013

Banks NBFCs

8% 15%

32% 44% 45%

54%

76% 84%

Mort

gages a

s %

of G

DP

Collateralized Lending

Debt Capital Markets

Real Estate Finance

Construction Finance

26

Present across Retail, SME and Corporate Segments

Secured SME Finance

Unsecured SME Finance

Client Segments

Product Suite

Housing Finance

Loan against Property

Small Ticket Housing Loans

Rural Finance

Public Issue Finance

Corporate

SME

Retail

27

Strengths & Key Parameters

Key Parameters

Book Size (INR cr)

FY12 FY13 FY14

Corporate Loans

3,626 4,437 5,815

Retail Finance 776 1,627 2,089

Business Strengths

• Ability to understand client needs and structure products to suit their needs

• Strong client relations

Client Centric Solutions

• Three tier risk management approach – Business risk team supplemented by Global risk team & Global Risk Committee

• Robust underwriting and credit appraisal processes

Proactive Risk

Management

• NPAs in check even in tough market conditions

• Comfortable asset cover

Good Asset Quality

28

Commodities Opportunity in India

29

67 95

136

185

269 292

2008 2009 2010 2011 2012 2013

Bullion

Bullion Imports INR’000 cr

India is a large producer and importer/exporter of Agri Commodities

Commodities is an unorganized business with huge scope of bringing efficiencies

Farmers and Agri value chain can benefit greatly from entry of organized players

Agri imports and exports have been growing at more than 24% CAGR

INR’000 cr Agri Exports1 & Imports2 in India

64 68 68

89

149

184

20 26 46 43

61

83

2008 2009 2010 2011 2012 2013

Exports Imports

1. Agri Exports includes tea, coffee, rice, wheat, cotton, tobacco, fruits and vegetables, oil meals, agriculture and allied products & sugar 2. Agri imports includes edible oil, pulses, sugar, cashew nuts and cereals & cereal preparations Source: Edelweiss Research, RBI, FMC

30

Strengths

Wide spread network

• Network of intermediaries, presence in sourcing locations, mandi access, working with key warehousing service providers

• Diverse sourcing capabilities with a wide reach across domestic and international locations

Strong Risk Management

Practices

• Focus on operational risk management

• Price risk minimized through hedging

• Business risk team supported by Global Risk team overseen by Global Risk Committee

Robust Backend

• Significant investment in technology

• Robust back-office and mid-office to handle multiple types of contracts and commodities across geographies

31

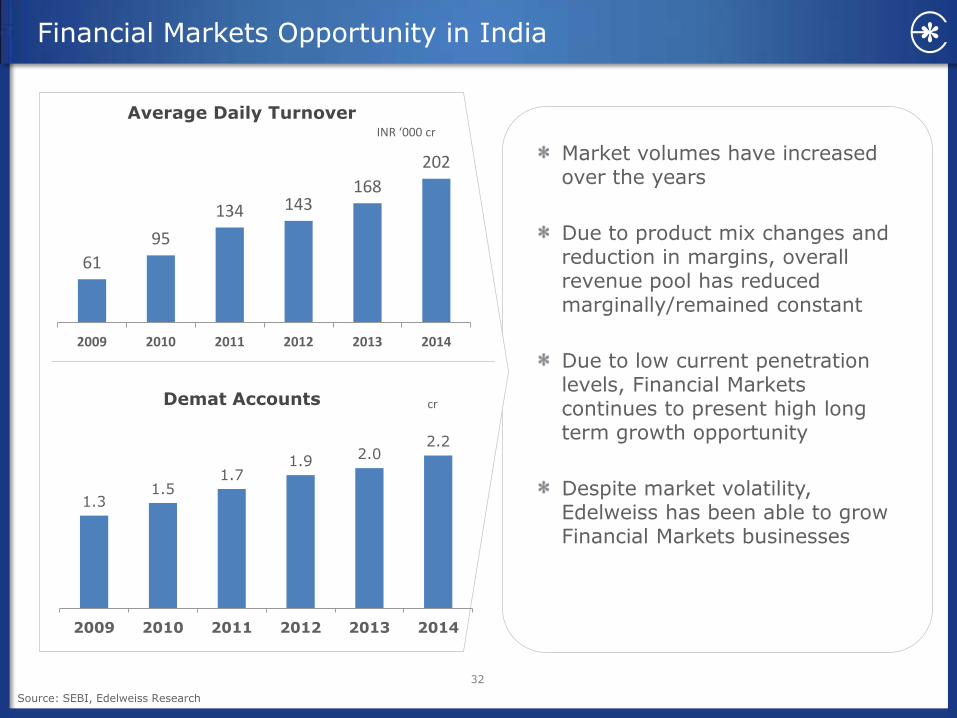

Financial Markets Opportunity in India

32

Market volumes have increased over the years

Due to product mix changes and reduction in margins, overall revenue pool has reduced marginally/remained constant

Due to low current penetration levels, Financial Markets continues to present high long term growth opportunity

Despite market volatility, Edelweiss has been able to grow Financial Markets businesses

Average Daily Turnover

61

95

134 143 168

202

2009 2010 2011 2012 2013 2014

INR ‘000 cr

Demat Accounts

1.3 1.5

1.7 1.9 2.0

2.2

2009 2010 2011 2012 2013 2014

cr

Source: SEBI, Edelweiss Research

Product Suite to Cater to All Client Segments

33

Institutional Equities

Corporate Finance Advisory

Prime Broking

Custody

Insurance Advisory

Wealth Management

HNI Broking

Financial Markets

Retail Broking

Financial Planning

Financial Product Distribution

Client Segments

Corporates Institutions

HNIs

Retail

34

Strengths & Key Parameters

Business Strengths

• Deep understanding of client needs

• Strong client relations built and maintained over the years

Client Centric Approach

• Known for differentiated product offerings across Broking & other platforms

• Pioneers in India in Algo Trading, Derivatives , Structured Products etc

Cutting Edge Products

• Best in class execution platforms with strong technology backend

• Established a cost efficient structure

Execution Efficiencies

Key Parameters

FY12 FY13 FY14

IB deals* 40 46 61

Retail Capital Market clients (lac)

3.8 4.1 4.3

Wealth AUAs (INR cr)

3,000 3,200 4,800

* Includes DCM deals

35

ASSET MANAGEMENT

Asset Management Opportunity in India

36

Recent sluggishness in Asset Management Business due to poor equity market returns and changes in operating environment

Overall long term potential continues to be very high due to

Low penetration of asset management in India

Expected increase in investment surplus of individuals

Edelweiss has focused on differentiating itself through its unique product offerings and top quartile fund performance

Mutual Funds AUM

419

615 597 588

701

825

2009 2010 2011 2012 2013 2014

INR ‘000 cr

Source: AMFI, Press searches; Karvy Wealth Report

India Individual Wealth

7,308 8,650

9,226

10,986

FY10 FY11 FY12 FY13

INR ‘000 Cr

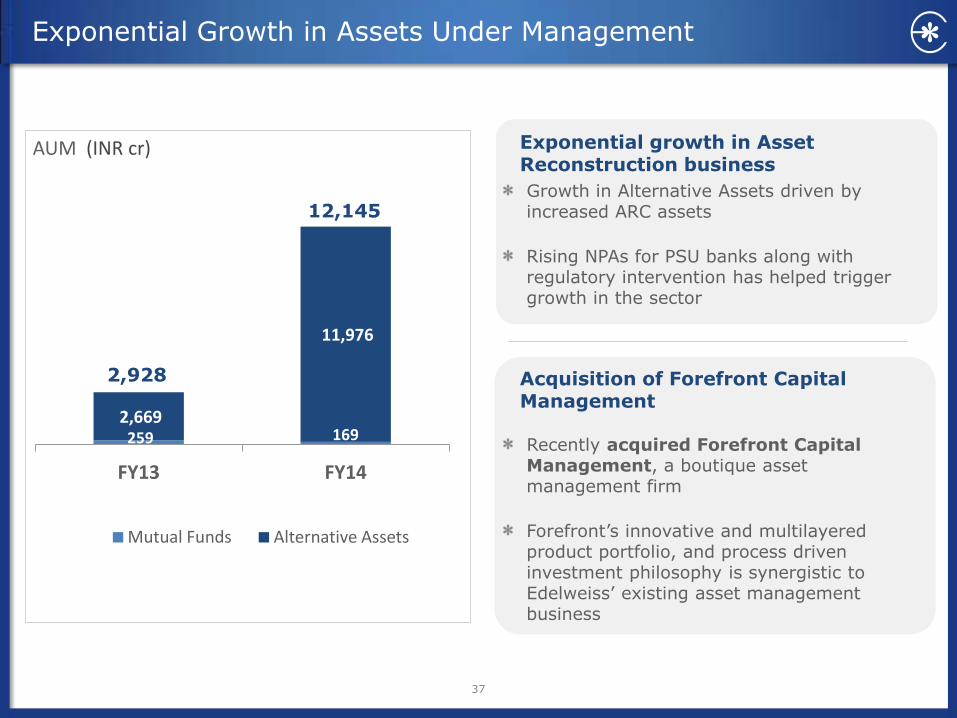

Exponential Growth in Assets Under Management

Growth in Alternative Assets driven by increased ARC assets

Rising NPAs for PSU banks along with regulatory intervention has helped trigger growth in the sector

Recently acquired Forefront Capital Management, a boutique asset management firm

Forefront’s innovative and multilayered product portfolio, and process driven investment philosophy is synergistic to Edelweiss’ existing asset management business

Exponential growth in Asset Reconstruction business

Acquisition of Forefront Capital Management

259 169 2,669

11,976

FY13 FY14

Mutual Funds Alternative Assets

AUM (INR cr)

2,928

12,145

37

38

Strengths

• Fund performance consistently ranked in top quartile

• Leading Asset Reconstruction Company in the country

Top Quartile Fund

Performance

• Known for differentiated product offerings across MF and Alternative Assets

• ARC to help unlock productive assets and assist Banks

Differentiated offerings

• Robust and lean execution platforms with strong technology backend

Cost-Efficient

39

LIFE INSURANCE

40

Life Insurance Opportunity in India

4

11 12 11 12

18

India Japan S Korea UK Hongkong Taiwan

Low Penetration*

-

400

800

1,200

1,600

FY02 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Rapid Premium Growth INR bn

18% CAGR

Life

Insu

ran

ce N

ew B

usi

nes

s p

rem

ium

Li

fe in

sura

nce

pre

miu

ms

as %

of

GD

P

* Insurance penetration is measured as ratio of premium (USD) to GDP (USD) Source: Edelweiss Research, Swiss Re, IRDA

Life Insurance in India is a sizable

opportunity space in financial services

~16% of household savings flow into life insurance, second only to banking

Life Insurance sector going through major shifts due to regulatory changes

Current shifts present unique discontinuities and opportunity for a new player to enter Life Insurance

Edelweiss tied up with one of the biggest Insurers worldwide – Tokio Marine to offer Life Insurance in India

41

Strengths & Key Parameters

Business Strengths

• “Need Based Sales” approach

• Comprehensive product portfolio – across 6 needs and product platforms

• Top decile performance for all ULIP schemes since inception

Customer Focused Approach

• Branch productivity of vintage1 branches ahead of private sector average

• Agent productivity close to that of leading private sector leaders

Productive Sales Force

• Core team in place both at Head office and at Regional sales offices

• One of the few new age2 non Bank led Insurance firms to have a Bancassurance tie-up

Built on a Strong

Foundation

Key Parameters

(INR cr) FY12 FY13 FY14

Total Income 53 101 169

Premium Income

11 55 111

Investment Income

42 46 58

Policies issued 6,600 23,000 33,000

Branches 29 45 58

PFAs 825 3,401 7,255

Employees 659 1,275 1,400

Individual Products

7 15 18

Notes: 1. At least 2 years old 2. Started after 2005

42

BALANCE SHEET MANAGEMENT UNIT

Balance Sheet Management Unit continues to be a function of:

Capital requirement of businesses

Opportunities in the markets

Liquidity management needs; Maintain a liquidity

cushion of ~ INR 500 crs

Treasury and BMU assets ~19% of effective Balance Sheet size

Focus on:

Balance sheet management

Liquidity management

Capital preservation with optimum returns

43

BMU Assets INR 2,982 cr

821

213 1,948

Bonds and others FDs Gsecs

Balance Sheet Management Unit

Focused on Long Term Value Creation

Quality Businesses

Corporate Overview

Driving Non Linear Growth

44

Contents

45

Growing Business Presence

India Global Presence

Strong ~497,000 clients/accounts base across businesses Over 262,000 Depository Participant Accounts 216 offices in 118 cities including six international offices Touch points include over 5,700 Authorised Persons and Sub-brokers across India

46

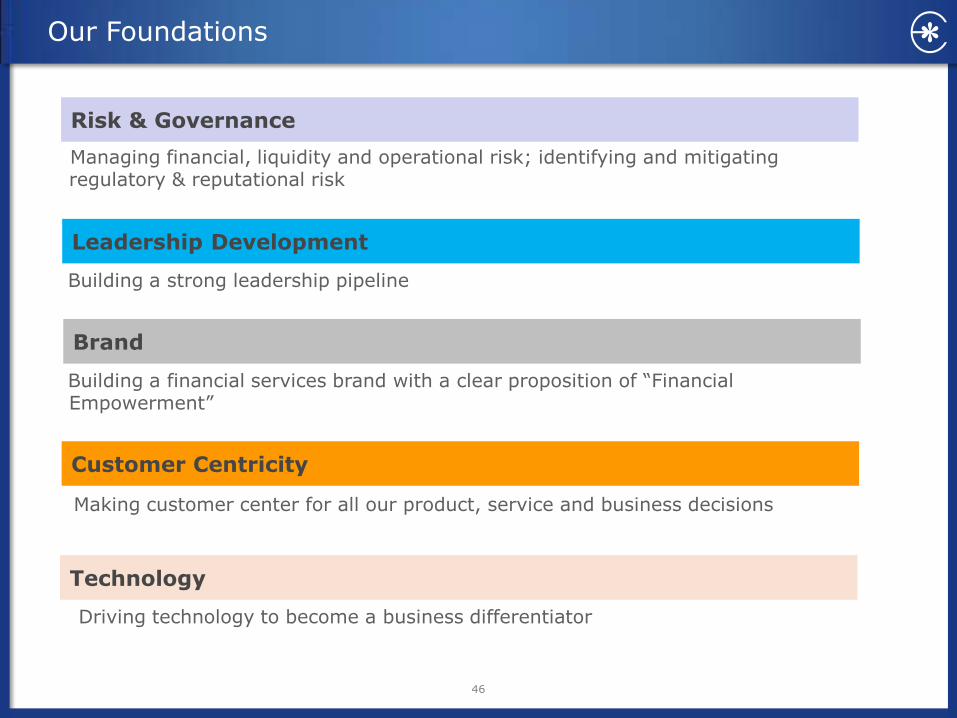

Managing financial, liquidity and operational risk; identifying and mitigating regulatory & reputational risk

Our Foundations

Risk & Governance

Building a strong leadership pipeline

Leadership Development

Building a financial services brand with a clear proposition of “Financial Empowerment”

Brand

Making customer center for all our product, service and business decisions

Customer Centricity

Driving technology to become a business differentiator

Technology

Risk Governance Framework

Business Risk The Primary Risk Team

Group Risk Second Line of Defense

Global Risk Committee Apex Risk Body

Global Risk Group

• Consolidated Risk Overview

• Adequate Risk Controls

• Policy Formation

• Risk directory

• Consists of senior management personnel including CEO and COO

• Risk Strategy

• Periodic risk review

47

• Defined risk metrics

• Day to Day Risk Monitoring

• Policy Enforcement

Oversight by Board Risk Committee

Investment Committees & Credit Committees to approve exposure levels

Awards: Best Managed & Best Corporate Governance Company

Capital Finance International, London, UK Corporate Governance Awards, 2013

48

Corporate Social Responsibility - EdelGive Foundation

49

Current portfolio of 18 non - profit organisations

Committed ` 226 mn till date

Over 8,000 hours of pro-bono support

Focus on Education, Livelihoods and Womens’ Rights

Impacted over 1,60,000 lives

Philanthropic initiative to drive sustainable social change

EdelGive has supported Indian athletes MC MaryKom, P V Sindhu and Pooja Ghatkar by funding through Olympic Gold Quest Movement

Over 3,500 Edelweiss employees touched via volunteering or

financial contribution

50

Name Percent

1 Carlyle 8.8%

2 Govt. of Singapore 8.1%

3 BIH SA 5.7%

4 Greater Pacific Capital 5.1%

5 SAIF Advisors 3.3%

6 Fidelity 2.1%

7 Amansa Investments 1.5%

8 GKFF Ventures (Argonaut)

1.5%

9 Sequoia Capital 1.0%

(#) Holding of known affiliates have been clubbed together for the purpose of this information

Foreign Institutions &

Companies 39%

Promoters, Employees &

Employee Trusts 49%

Non Institutions (Incl. Corporates and Individuals)

12%

Shareholding Pattern

Top Institutional Shareholders above 1%#

As on Mar 31, 2014

Stable Institutional Ownership

51

Independent Directors with Complementary Skills

INDEPENDENT / NON-EXECUTIVE DIRECTORS

Mr. Narendra Jhaveri Independent Director

Has occupied important positions in National Council of Applied Economic Research (NCAER), RBI & ICICI Ltd

Mr. P N Venkatachalam Independent Director Banking sector expert and Former Member of the Interim Pension Fund Regulatory Authority of India, Former MD, State Bank of India

Mr. Berjis Desai Independent Director

Reputed and respected legal practioner. Managing Partner J. Sagar & Associates

Mr. Sanjiv Misra Independent Director

Worked with Goldman Sachs, Citigroup. Is the President of Phoenix Advisers Pte. Ltd, a boutique advisory firm

Mr. K Chinniah Independent Director

Served as Global Head - Portfolio, Strategy & Risk Group with GIC Special Invst. (Pvt. Equity arm of the Govt. of Singapore Invst Corp ("GIC“)

Mr. Sunil Mitra Independent Director

Broad experience in economic policy making. Former Finance Secretary of Govt. of India

Mr. Navtej S. Nandra Independent Director President of E*TRADE Financial Corporation. Prior to this he served as Head of International for Morgan Stanley Investment Management

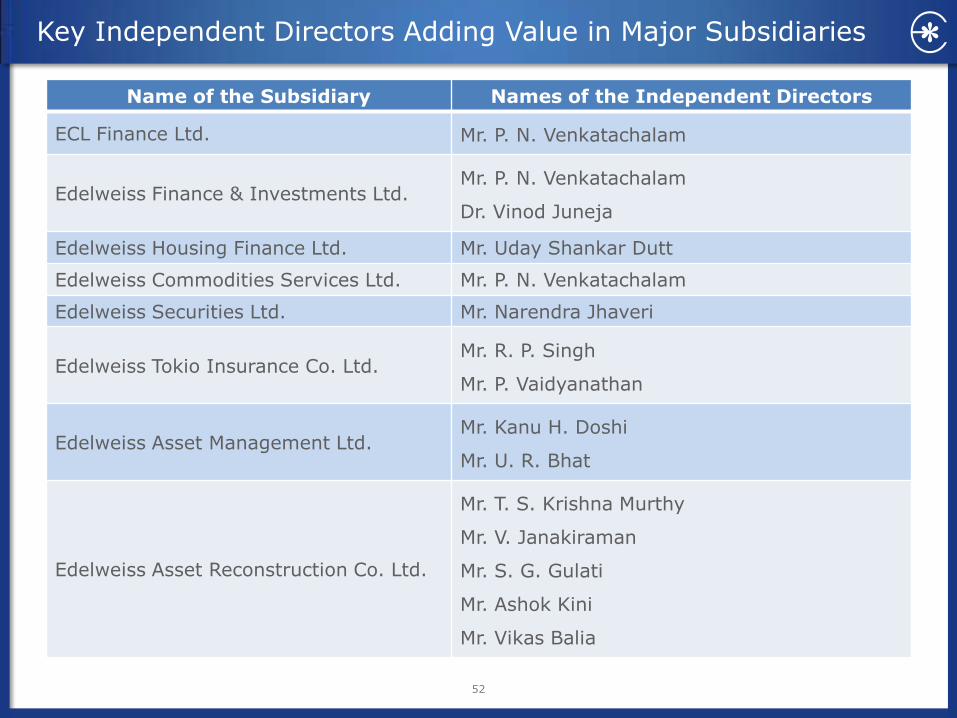

Key Independent Directors Adding Value in Major Subsidiaries

Name of the Subsidiary Names of the Independent Directors

ECL Finance Ltd. Mr. P. N. Venkatachalam

Edelweiss Finance & Investments Ltd. Mr. P. N. Venkatachalam

Dr. Vinod Juneja

Edelweiss Housing Finance Ltd. Mr. Uday Shankar Dutt

Edelweiss Commodities Services Ltd. Mr. P. N. Venkatachalam

Edelweiss Securities Ltd. Mr. Narendra Jhaveri

Edelweiss Tokio Insurance Co. Ltd. Mr. R. P. Singh

Mr. P. Vaidyanathan

Edelweiss Asset Management Ltd. Mr. Kanu H. Doshi

Mr. U. R. Bhat

Edelweiss Asset Reconstruction Co. Ltd.

Mr. T. S. Krishna Murthy

Mr. V. Janakiraman

Mr. S. G. Gulati

Mr. Ashok Kini

Mr. Vikas Balia

52

This presentation and the discussion may contain certain words or phrases that are forward - looking statements, based on current expectations of the management of Edelweiss Financial Services Ltd. or any of its subsidiaries and associate companies (“Edelweiss”). Actual results may vary significantly from the forward-looking statements contained in this presentations due to various risks and uncertainties. These risks and uncertainties include the effect of economic and political conditions in India and outside India, volatility in interest rates and in the securities market, new regulations and Government policies that may impact the businesses of Edelweiss as well as the ability to implement its strategy. The information contained herein is as of the date referenced and Edelweiss does not undertake any obligation to update these statements. Edelweiss has obtained all market data and other information from sources believed to be reliable or are its internal estimates, although its accuracy or completeness can not be guaranteed. The presentation relating to financial performance of various businesses of Edelweiss herein is based on Management estimates. This presentation is for information purposes only and does not constitute an offer or recommendation to buy or sell any securities of Edelweiss. This presentation also does not constitute an offer or recommendation to buy or sell any financial products offered by Edelweiss. Any action taken by you on the basis of the information contained herein is your responsibility alone and Edelweiss or its directors or employees will not be liable in any manner for the consequences of such action taken by you. Edelweiss and/or its directors and/or its employees may have interests or positions, financial or otherwise, in the securities mentioned in this presentation. For more information, please visit www.edelweissfin.com or drop us an e-mail on [email protected]

53

Safe Harbor