Embed Size (px)

Citation preview

Edelweiss Research is also available on www.edelresearch.com, Bloomberg EDEL <GO>, Thomson First Call, Reuters and Factset.

Edelweiss Securities Limited

Larsen & Toubro’s (L&T) Q1FY17 net income missed Street’s and our estimates primarily as transition to Ind-AS required much higher-than-expected provisioning. Business outlook indicates a slow and steady improvement with orders rising 14% YoY and international revenue, once again, surprising us on the upside. We perceive a few challenges: (a) weak revenue prospects for realty business in interim; (b) domestic execution up mere ~5% YoY; and (c) NWC/sales at 23.5%. We trim FY17/18E EPS ~20% each building in the Ind-AS impact. We maintain ‘BUY’ with revised TP of INR 1650 (INR1750 earlier) valuing L&T core E&C at 25x, in line with S&P BSE Cap goods index. Interim results appear good on what probably may be a new goal post We agree with management that L&T’s Q1FY17 net income at INR 219 bn, up 9% YoY,

is impressive, given the sluggish capital formation growth in the economy. Order wins

at INR 250 bn(ex-services), up 14%, are in line with the annual run-rate set by

management. 50 bps margin expansion helped EBITDA rise 15% YoY.

Our challenge is the timelines for full disclosures on transition to Ind-AS Post adoption of Ind-AS, Q1FY17 net income was impacted by INR1.65bn (same as last

year) due to Expected Credit Loss (ECL) on receivables beyond 3 months. Also, the first

balance sheet under Ind-AS may not be immediately available. Based on management

commentary that provisions do not have quarterly volatility and other IND AS charges,

we revise down FY17/18E EPS to INR46/INR62.

Guidance maintained; bid pipeline healthy at INR4.2tn Management maintained 12-15% sales & 15% order intake guidance led by healthy bid

pipeline of INR4.25tn (INR3.1tn from India) and strong execution in export businesses.

NWC/sales remained at Q4 level despite a good intake, indicating that a sustained

inflection in revenue is still a few quarters away.

Outlook and valuations: A good medium-term play; maintain ‘BUY’ Post realignment of EPS in Ind-AS, we realign our TP to INR 1,650. We continue using

SOTP. We assign P/E to 25x, in line with S&P-BSE cap good index for core E&C business

(v/s 19x standalone estimate). With EPS CAGR (FY16-18E) estimate of 30%+ in core E&C

, valuations appear reasonable v/s position in cycle. We maintain ‘BUY/SO’.

RESULT UPDATE

LARSEN & TOUBRO Transition to Ind-AS could be a long-term positive

EDELWEISS 4D RATINGS

Absolute Rating BUY

Rating Relative to Sector Outperform

Risk Rating Relative to Sector Medium

Sector Relative to Market Overweight

MARKET DATA (R: LART.BO, B: LT IN)

CMP : INR 1559

Target Price : INR 1650

52-week range (INR) : 1,844 / 1,016

Share in issue (mn) : 932.0

M cap (INR bn/USD mn) : 1,453/ 21,688

Avg. Daily Vol.BSE/NSE(‘000) : 2,290.8

SHARE HOLDING PATTERN (%)

Current Q3FY16 Q2FY16

Promoters *

- - -

MF's, FI's & BK’s 38.7 38.3 38.4

FII's 16.6 16.2 16.4

Others 44.7 45.5 45.2

* Promoters pledged shares (% of share in issue)

: NIL

PRICE PERFORMANCE (%)

Stock Nifty EW

Construction Index

1 month 7.0 6.6 6.9

3 months 25.2 10.4 17.8

12 months (10.3) 3.9 (12.0)

Manish Saxena +91 22 6620 3105

[email protected] Amit Mahawar +91 22 4040 7451

Swarnim Maheshwari +91 22 4040 7418

India Equity Research| Engineering and Capital Goods

July 29, 2016

Financials (Consolidated) (INR bn)

Year to March Q1FY17 Q1FY16 % change Q4FY16 % change FY16 FY17E FY18E

Net rev. 218.7 200.5 9.1 331.6 (34.0) 1,026 1,142 1,321

EBITDA 19.1 16.4 16.1 48.6 (60.8) 123 114 138

Adjusted profit 6.1 4.2 45.5 24.1 (74.7) 47 42 58

Diluted EPS (INR) 6.6 4.5 45.5 25.9 (74.7) 50.9 45.5 61.9

Diluted P/E (x) 30.6 34.2 25.1

EV/EBITDA (x) 19.3 21.7 18.3

ROAE (%) 10.7 8.8 11.0

Engineering and Capital Goods

2 Edelweiss Securities Limited

Con-call highlights:

FY17 guidance (consol) maintained: Revenue: 12-15% growth, Order intake: 15%

growth , Margins: 50bps improvement (ex-services business).

Ordering pipeline: Total ordering pipeline for next 9 months stands at INR4.25tn. 25%

of order prospects are from international projects and balance from the domestic

market.

Large jobs drive strong order intake: Telangana barrage (water segment) order

received in Q1FY17 apart from Saudi Aramco are some of the large projects awarded in

Q1FY17 which drove 15% growth in order intake.

IND-AS : P&L impacted by INR1.65bn mainly due to Expected Credit loss (ECL) in

Q1FY17 apart from provisioning for performance link reward. A large part of ECL

expense of INR10bn has been adjusted against opening reserves of March 15 B/S.

Power segment: Power segment sales up 60% YoY led by Bangladesh, Chhabra etc.,

large project execution.

Hydrocarbon segment: Large order inflow in Q1 adds significantly to FY18E revenue

growth visibility. L&T has completely exited old jobs in HC segment and is now expects

improving margin profile for this segment.

HC, Hydrocarbon & MMH will see rationalization in manpower. The company continues

to add manpower in infra division which has sustained reasonable growth, especially in

international jobs.

Development projects (IND AS): Nabha Power, Kattupali port & Hyderabad metro

included. However, in PAT profits/losses from road projects are also included. In capital

employed, Equity-Accumulated losses of IDPL have been also recorded. Loss of road

revenues from the development project segment was compensated by Hyderabad

Metro revenue (Under IND-AS, whatever execution is done by outside party gets

recognised as revenue).

Real estate business: Revenues are expected to be a bit weak in near term till the time

the company gets permission for IInd phase of Powai, Parel projects. Bengaluru project

is expected to contribute in sometime. Realty revenues were INR4bn during Q1FY17.

Other business: Margins have declined due to inventory write down (INR1bn) in the

shipbuilding business and lower revenues in the realty business. There have been cost

overruns in certain ship contracts which are under arbitration.

Working capital: Working capital under IND-AS is at similar levels to those of March 16

which was 23.5% as % of sales. No real improvement seen as such.

Other key highlights:

SGA has risen sharply due to NPAs in fin services and on doubtful debts & expected

credit loss.

Salary cost for technology services has been included in staff cost versus other

expenses earlier.

Excise duty was NR1.5bn during Q1FY16.

Kuwait, Saudi still continue to award many projects . But ordering from Oman & UAE

has reduced. The company is not facing any working capital related challenges in Saudi

Arabia unlike Korean engineering majors.

Larsen & Toubro

3 Edelweiss Securities Limited

Table 2: Key segmental performance

Table 2: Edelweiss bottoms-up order intake assumptions

Source: Company, Industry,Edelweiss research

Segments

Q1FY17 Q1FY16 % change

Revenues

Infra 90,700 83,100 9.1

Power 17,200 10,800 59.3

Heavy Engineering 6,500 6,200 4.8

Electrical Automation 9,300 9,600 (3.1)

Hydrocarbons 21,300 21,200 0.5

IT & services 23,500 20,500 14.6

Financial Services 20,907 17,817 17.3

Development projects 11,500 9,900 16.2

Others 16,200 19,400 (16.5)

Total 217,107 198,517 9.4

EBITDA margins

Infra 9.2 8.9

Power 5.8 1.2

Heavy Engineering 14.9 8.9

Electrical Automation 7.8 5.8

Hydrocarbons 2.0 2.3

IT & services 21.9 18.4

Financial Services 13.3 11.7

Development projects 9.8 5.9

Others (2.5) 11.9

Total 9.3 9.0

Consolidated

(INR bn) FY14 FY15 FY16 FY17E FY18E

Process (MMH) 29 62 41 49 58

Power 28 155 27 97 155

BoP/Gas/EPC etc 28 75 27 28 52

BTG 0 80 0 69 103

Hydrocarbons 97 108 95 150 174

India 32 40 45 50 54

Exports 65 68 50 100 120

Infrastructure 762 854 849 804 863

T&D- Middle East 61 64 51 50 55

T&D- India 67 126 133 143 140

Factories & Buildings (Residential) 109 134 90 60 65

Factories & Buildings (Commercial/IT

park/ Industrials)

154 171 154 175 184

Transportation/Urban Infra (India) 107 120 150 120 130

Transportation/Urban Infra (Middle 104 120 75 56 68

Roads (Including ME) 70 55 110 100 108

Water 91 64 86 99 114

Developmental Projects - - - - -

Defence & shipbuilding 30 45 25 110 140

Others 92 120 113 90 90

TOTAL 1,037 1,345 1,149 1,299 1,481

% change 16.0 29.7 (14.5) 13.0 14.1

Engineering and Capital Goods

4 Edelweiss Securities Limited

Table 3: SOTP valuation

Source: Company, Edelweiss research

Valuation

methodologyMultiple

L&T's

stake (%)

Value

(INR mn)

Per share

(INR)Remark

L&T Core Engineering

business

PE 25 100 1,221,643 1,314 In l ine with S&P BSE Cap Goods Index

adjusted for June Quarter earnings

L&T MHI (BTG JVs) DCF - 51 62,960 35 DCF basis

L&T Infotech & technology

services

PER 85% 122,340 132 Assuming value in l ine with Current market

Cap adjusted for minority stake

L&T Finance Holdings 67% 98,352 106 Assuming value in l ine with Current market

Cap adjusted for minority stake

L&T Develoment Projects P/BV 1.2 80% 62,000 67 Equity Invested til l FY16

Hyderabad Metro DCF 100 (6,375) (3) Remains to be seen if Telangana state

would like to take a controlling stake in the

project

Total 1,567,295 1,650

Financial snapshot: Consol (INR mn)

Year to March Q1FY17 Q1FY16 % change Q4FY16 % change FY16 FY17E FY18E

Total revenues (net) 218,738 200,482 9.1 331,570 (34.0) 1,026,317 1,142,351 1,321,144

Direct cost 136,532 127,095 7.4 244,355 (44.1) 749,463 778,612 910,205

Staff cost 34,200 31,494 8.6 22,421 52.5 92,048 124,850 144,477

Other operating expenses 28,955 25,482 13.6 16,203 78.7 61,378 124,741 128,170

Total expenditure 199,687 184,072 8.5 282,979 (29.4) 902,890 1,028,203 1,182,852

EBITDA 19,051 16,411 16.1 48,592 (60.8) 123,427 114,148 138,292

Depreciation 4,648 4,658 (0.2) 8,203 (43.3) 27,560 29,297 30,479

EBIT 14,403 11,752 22.6 40,389 (64.3) 95,867 84,852 107,813

Interest 3,375 3,893 (13.3) 7,737 (56.4) 30,412 15,685 16,663

Other income 3,024 2,833 6.8 2,182 38.6 11,830 10,426 10,974

Add: Exceptional items 0 0 485 3,581 0 0

PBT 14,052 10,692 31.4 35,319 (60.2) 80,866 79,593 102,124

Tax 5,488 4,282 28.2 9,537 (42.5) 25,487 26,266 33,701

Less: Minority Interest 732 258 1,230 4,450 3,466 4,448

Add: Share in profits of assoc. (1,736) (1,963) (15) (25) (7,500) (6,375)

Reported Profit 6,097 4,189 45.5 24,537 (75.2) 50,905 42,361 57,601

Adjusted net profit 6,097 4,189 45.5 24,051 (74.7) 47,324 42,361 57,601

Equity capital (FV: INR 2) 1,245 1,245 1,245 1,245 1,246 1,247

# of shares (mn) 930 930 930 930 930 930

Adjusted EPS (INR) 6.6 4.5 45.5 25.9 (74.7) 50.9 45.5 61.9

As % of net revenues 0.0 0.0 0.0 2.0 3.0 4.0

Direct cost 62.4 63.4 73.7 73.0 68.2 68.9

Employee cost 15.6 15.7 6.8 9.0 10.9 10.9

Other operating expenses 13.2 12.7 4.9 6.0 10.9 9.7

EBITDA 8.7 8.2 14.7 12.0 10.0 10.5

Adjsuted net profit 2.8 2.1 7.3 4.6 3.7 4.4

Tax rate 39.1 40.1 27.0 31.5 33.0 33.0

Larsen & Toubro

5 Edelweiss Securities Limited

Company Description

Larsen & Toubro (L&T), headquartered in Mumbai, is a technology-driven engineering and

construction organization, and one of the largest companies in India's private sector. It has

additional interests in manufacturing, services, and information technology. A strong

customer-focused approach and the constant quest for top-class quality has enabled the

company attain and sustain leadership in its major lines of businesses over seven decades.

L&T has an international presence, with a global spread of offices. A thrust on international

business over the past few years has seen overseas earnings growing to 18% of total

revenues. With factories and offices located around the country, further supplemented by a

wide marketing and distribution network, L&T's image and equity extend to virtually every

district of India. Investment Theme

Diversified business dominance imparts unique flexibility: L&T has a dominant position and

market share in most operating verticals, be it oil & gas, process projects, roads, bridges, or

industrial structures. This imparts flexibility to cherry-pick projects across a wide range of

projects and thus helps optimize overall business profitability.

New segments: Potent growth Catalysts: L&T will have to garner INR100-150bn new orders

annually over FY17-18E to cover lost ground owing to tepid Middle East market and weak

F&B segment. We believe, the much needed succor will come from defense, transportation

and power T&D sectors in the domestic market, which are anticipated to gain palpable

momentum in light of the government’s ‘Make in India’ focus.

Strong OB and domestic execution pick up to drive earnings from FY18 (+20% core earnings).

Diversified presence across key verticals has helped L&T sustain healthy order book traction

over past three years of investment slowdown. Though this elongates its execution cycle, it

also imparts good revenue visibility over the next few years. L&T could see a substantial

scale up in execution as these factors reverse going ahead.

Key Risks

Perceived risk of a slowdown in Middle East capex due to sharp drop in global oil prices

can severely impact L&T’s order intake and revenue accruals.

Further delay in recovery of the domestic investment cycle.

Continued deterioration in working capital requirement.

6 Edelweiss Securities Limited

Engineering and Capital Goods

Financial Statements (Consolidated)

Key assumptions

Year to March FY15 FY16E FY17E FY18E

Macros

GDP(Y-o-Y %) 7.2 7.4 7.9 8.3

Inflation (Avg) 5.9 4.8 5.0 5.2

Repo rate (exit rate) 7.5 6.8 6.0 6.0

USD/INR (Avg) 61.2 65.0 67.5 67.0

Key financial assumptions

Order inflow growth vertical wise (%)

A) Process 73.1 (33.6) 20.0 20.0

B) Oil & Gas 11.7 (11.9) 55.0 2.0

C) Power 463.0 (86.4) 400.0 45.0

D) Infra 12.1 (0.7) (8.0) 10.0

E) Others 40.0 (20.0) 55.0 13.0

Excise duty as a % of sales 0.9 1.0 0.9 1.3

Total no. of employees (SA) 46,392 47,784 51,129 54,708

Empl. cost per head (INR mn) 0.89 0.94 0.99 1.04

Depriciation as a % of FA 8.5 7.8 7.4 7.4

Net borrowings (INR mn) 8,408 13,086 6,000 4,500

Tax rate (%) 24.3 20.6 26.0 27.0

Capex (INR mn) 9,012 6,434 10,100 5,100

Customer adv. (as a % of OI) 7.3 8.6 10.0 10.0

Income statement (INR mn)

Year to March FY15 FY16 FY17E FY18E

Income from operations 920,046 1,026,317 1,142,351 1,321,144

Direct costs 672,937 749,463 778,612 910,205

Employee costs 79,222 92,048 124,850 144,477

Other expenses 54,531 61,378 124,741 128,170

Total operating expenses 806,690 902,890 1,028,203 1,182,852

EBITDA 113,356 123,427 114,148 138,292

Depreciation & amortisation 26,225 27,560 29,297 30,479

EBIT 87,131 95,867 84,852 107,813

Interest expenses 28,507 30,412 15,685 16,663

Other income 10,072 11,830 10,426 10,974

Add: Exceptional items 3,477 3,581 - -

Profit before tax 72,172 80,866 79,593 102,124

Provision for tax 22,836 25,487 26,266 33,701

Less: Minority interests 1,710 4,450 3,466 4,448

Add: Share in profits of assoc. 21 (25) (7,500) (6,375)

Reported Profit 47,648 50,905 42,361 57,601

Less: Exceptional Items 3,477 3,581 - -

Adjusted profit 44,171 47,324 42,361 57,601

Basic sh. outstanding (mn) 930 930 930 930

Adjusted Basic EPS 47.5 50.9 45.6 62.0

No. of Dil. Sh. outstand. (mn) 930 930 930 930

Adjusted Diluted EPS 47.5 50.9 45.6 62.0

Adjusted Cash EPS 71.3 80.6 77.1 94.8

Dividend per share (DPS) 13.9 18.3 15.3 16.1

Dividend Payout Ratio (%) 31.6 40.1 42.1 32.5

2% -2% 10%

Common size metrics- as % of net revenues

Year to March FY15 FY16 FY17E FY18E

Direct cost 73.1 73.0 68.2 68.9

Employee expenses 8.6 9.0 10.9 10.9

S G &A expenses 5.9 6.0 10.9 9.7

Operating expenses 87.7 88.0 90.0 89.5

Depreciation & amortization 2.9 2.7 2.6 2.3

Interest expenditure 3.1 3.0 1.4 1.3

EBITDA margins 12.3 12.0 10.0 10.5

EBIT margins 9.5 9.3 7.4 8.2

Net Profit margins 5.0 5.0 4.0 4.7

Growth metrics (%)

Year to March FY15 FY16 FY17E FY18E

Revenues 8.1 11.6 11.3 15.7

EBITDA 5.6 8.9 (7.5) 21.2

PBT (3.6) 12.0 (1.6) 28.3

Adjusted Profit (2.9) 7.1 (10.5) 36.0

EPS (2.8) 7.1 (10.5) 36.0

7 Edelweiss Securities Limited

Larsen & Toubro

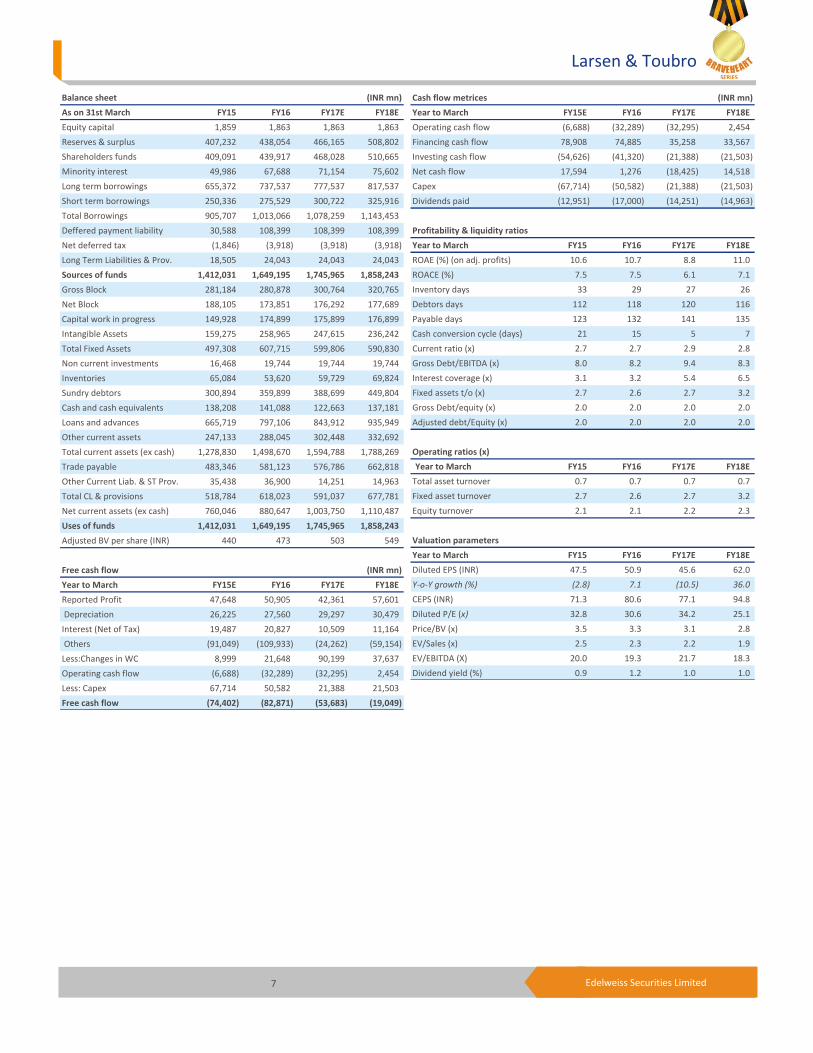

Balance sheet (INR mn)

As on 31st March FY15 FY16 FY17E FY18E

Equity capital 1,859 1,863 1,863 1,863

Reserves & surplus 407,232 438,054 466,165 508,802

Shareholders funds 409,091 439,917 468,028 510,665

Minority interest 49,986 67,688 71,154 75,602

Long term borrowings 655,372 737,537 777,537 817,537

Short term borrowings 250,336 275,529 300,722 325,916

Total Borrowings 905,707 1,013,066 1,078,259 1,143,453

Deffered payment liability 30,588 108,399 108,399 108,399

Net deferred tax (1,846) (3,918) (3,918) (3,918)

Long Term Liabilities & Prov. 18,505 24,043 24,043 24,043

Sources of funds 1,412,031 1,649,195 1,745,965 1,858,243

Gross Block 281,184 280,878 300,764 320,765

Net Block 188,105 173,851 176,292 177,689

Capital work in progress 149,928 174,899 175,899 176,899

Intangible Assets 159,275 258,965 247,615 236,242

Total Fixed Assets 497,308 607,715 599,806 590,830

Non current investments 16,468 19,744 19,744 19,744

Inventories 65,084 53,620 59,729 69,824

Sundry debtors 300,894 359,899 388,699 449,804

Cash and cash equivalents 138,208 141,088 122,663 137,181

Loans and advances 665,719 797,106 843,912 935,949

Other current assets 247,133 288,045 302,448 332,692

Total current assets (ex cash) 1,278,830 1,498,670 1,594,788 1,788,269

Trade payable 483,346 581,123 576,786 662,818

Other Current Liab. & ST Prov. 35,438 36,900 14,251 14,963

Total CL & provisions 518,784 618,023 591,037 677,781

Net current assets (ex cash) 760,046 880,647 1,003,750 1,110,487

Uses of funds 1,412,031 1,649,195 1,745,965 1,858,243

Adjusted BV per share (INR) 440 473 503 549

Contingent liabilities

Free cash flow (INR mn)

Year to March FY15E FY16 FY17E FY18E

Reported Profit 47,648 50,905 42,361 57,601

Depreciation 26,225 27,560 29,297 30,479

Interest (Net of Tax) 19,487 20,827 10,509 11,164

Others (91,049) (109,933) (24,262) (59,154)

Less:Changes in WC 8,999 21,648 90,199 37,637

Operating cash flow (6,688) (32,289) (32,295) 2,454

Less: Capex 67,714 50,582 21,388 21,503

Free cash flow (74,402) (82,871) (53,683) (19,049)

Cash flow metrices (INR mn)

Year to March FY15E FY16 FY17E FY18E

Operating cash flow (6,688) (32,289) (32,295) 2,454

Financing cash flow 78,908 74,885 35,258 33,567

Investing cash flow (54,626) (41,320) (21,388) (21,503)

Net cash flow 17,594 1,276 (18,425) 14,518

Capex (67,714) (50,582) (21,388) (21,503)

Dividends paid (12,951) (17,000) (14,251) (14,963)

Profitability & liquidity ratios

Year to March FY15 FY16 FY17E FY18E

ROAE (%) (on adj. profits) 10.6 10.7 8.8 11.0

ROACE (%) 7.5 7.5 6.1 7.1

Inventory days 33 29 27 26

Debtors days 112 118 120 116

Payable days 123 132 141 135

Cash conversion cycle (days) 21 15 5 7

Current ratio (x) 2.7 2.7 2.9 2.8

Gross Debt/EBITDA (x) 8.0 8.2 9.4 8.3

Interest coverage (x) 3.1 3.2 5.4 6.5

Fixed assets t/o (x) 2.7 2.6 2.7 3.2

Gross Debt/equity (x) 2.0 2.0 2.0 2.0

Adjusted debt/Equity (x) 2.0 2.0 2.0 2.0

Operating ratios (x)

Year to March FY15 FY16 FY17E FY18E

Total asset turnover 0.7 0.7 0.7 0.7

Fixed asset turnover 2.7 2.6 2.7 3.2

Equity turnover 2.1 2.1 2.2 2.3

Valuation parameters

Year to March FY15 FY16 FY17E FY18E

Diluted EPS (INR) 47.5 50.9 45.6 62.0

Y-o-Y growth (%) (2.8) 7.1 (10.5) 36.0

CEPS (INR) 71.3 80.6 77.1 94.8

Diluted P/E (x) 32.8 30.6 34.2 25.1

Price/BV (x) 3.5 3.3 3.1 2.8

EV/Sales (x) 2.5 2.3 2.2 1.9

EV/EBITDA (X) 20.0 19.3 21.7 18.3

Dividend yield (%) 0.9 1.2 1.0 1.0

8 Edelweiss Securities Limited

Engineering and Capital Goods

Insider Trades

Reporting Data Acquired / Seller B/S Qty Traded

No Data Available

*in last one year

Bulk Deals Data Acquired / Seller B/S Qty Traded Price

No Data Available

*in last one year

Holding – Top10 Perc. Holding Perc. Holding

Life insurance corp 15.71 L&t employ welfare f 12.31

Unit trust of india 8.15 Hdfc asset managemen 2.23

General insurance co 1.84 Prudential icici ass 1.54

Gic private limited 1.48 Icici prudential lif 1.34

Reliance capital tru 1.24 Blackrock 1.05

*in last one year

Additional Data

Directors Data AM Naik Group Executive Chairman MR. D. K. SEN Whole-time Director & Sr. Executive Vice President (Infra)

S N Subrahmanyan Deputy Managing Director & President Shailendra Roy Whole Time Director & Senior Executive Vice President

MR. SUSHOBHAN SARKER Nominee Director - LIC MRS. SUNITA SHARMA Nominee Director - LIC

MR. M. V. SATISH Whole Time Director & Sr. EVP R Shankar Raman Whole-time Director & Chief Financial Officer

V K Magapu Whole Time Director AK Jain Nominee Director

M M Chitale Non Executive Director S N Talwar Non Executive Director

S Rajgopal Non Executive Director Subodh Bhargava Non Executive Director

Auditors - Sharp Tannan & Co.

*as per last annual report

9 Edelweiss Securities Limited

Company Absolute

reco

Relative

reco

Relative

risk

Company Absolute

reco

Relative

reco

Relative

Risk

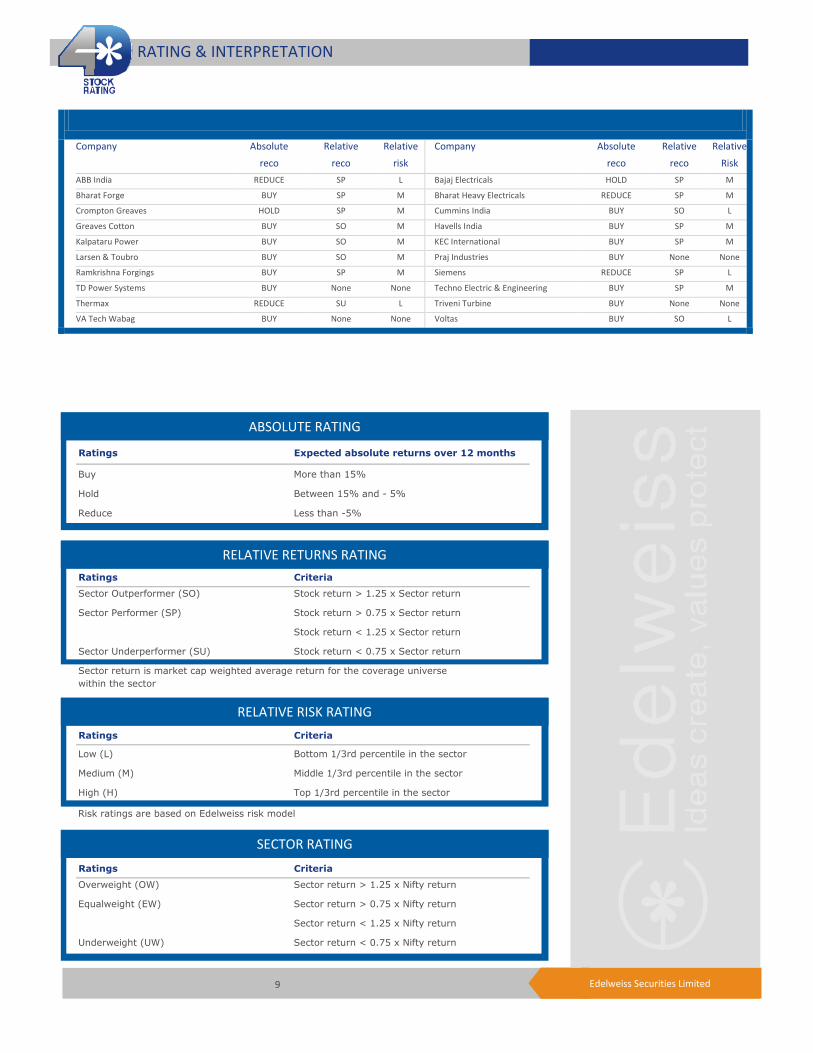

ABB India REDUCE SP L Bajaj Electricals HOLD SP M

Bharat Forge BUY SP M Bharat Heavy Electricals REDUCE SP M

Crompton Greaves HOLD SP M Cummins India BUY SO L

Greaves Cotton BUY SO M Havells India BUY SP M

Kalpataru Power BUY SO M KEC International BUY SP M

Larsen & Toubro BUY SO M Praj Industries BUY None None

Ramkrishna Forgings BUY SP M Siemens REDUCE SP L

TD Power Systems BUY None None Techno Electric & Engineering BUY SP M

Thermax REDUCE SU L Triveni Turbine BUY None None

VA Tech Wabag BUY None None Voltas BUY SO L

RATING & INTERPRETATION

ABSOLUTE RATING

Ratings Expected absolute returns over 12 months

Buy More than 15%

Hold Between 15% and - 5%

Reduce Less than -5%

RELATIVE RETURNS RATING

Ratings Criteria

Sector Outperformer (SO) Stock return > 1.25 x Sector return

Sector Performer (SP) Stock return > 0.75 x Sector return

Stock return < 1.25 x Sector return

Sector Underperformer (SU) Stock return < 0.75 x Sector return

Sector return is market cap weighted average return for the coverage universe

within the sector

RELATIVE RISK RATING

Ratings Criteria

Low (L) Bottom 1/3rd percentile in the sector

Medium (M) Middle 1/3rd percentile in the sector

High (H) Top 1/3rd percentile in the sector

Risk ratings are based on Edelweiss risk model

SECTOR RATING

Ratings Criteria

Overweight (OW) Sector return > 1.25 x Nifty return

Equalweight (EW) Sector return > 0.75 x Nifty return

Sector return < 1.25 x Nifty return

Underweight (UW) Sector return < 0.75 x Nifty return

10 Edelweiss Securities Limited

Engineering and Capital Goods

Edelweiss Securities Limited, Edelweiss House, off C.S.T. Road, Kalina, Mumbai – 400 098.

Board: (91-22) 4009 4400, Email: [email protected]

Manoj Bahety

Deputy Head Research

Coverage group(s) of stocks by primary analyst(s): Engineering and Capital Goods

ABB India, Bharat Heavy Electricals, Bharat Forge, Bajaj Electricals, Crompton Greaves, Greaves Cotton, Havells India, KEC International, Cummins India, Kalpataru Power, Larsen & Toubro, Praj Industries, Ramkrishna Forgings, Siemens, TD Power Systems, Techno Electric & Engineering, Thermax, Triveni Turbine, VA Tech Wabag, Voltas

Distribution of Ratings / Market Cap

Edelweiss Research Coverage Universe

Rating Distribution* 158 59 12 229 * - stocks under review

Market Cap (INR) 156 62 11

Date Company Title Price (INR) Recos

Recent Research

25-Jul-16 Praj Industries

Slow start to the year; growth matrix intact; Result Update

85 Buy

25-Juj-16 Havells India

Beat on all counts; well equipped for next leg of growth; Result Update

376 Buy

22-Jul-16 Bharat Heavy Electricals

Breaking shackles of extreme pessimism; Company Update

141 Buy

> 50bn Between 10bn and 50 bn < 10bn

Buy Hold Reduce Total

Rating Interpretation

Buy appreciate more than 15% over a 12-month period

Hold appreciate up to 15% over a 12-month period

Reduce depreciate more than 5% over a 12-month period

Rating Expected to

-

149

297

446

594

743

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

De

c-1

4

(IN

R)

One year price chart

500

800

1,100

1,400

1,700

2,000

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

De

c-1

5

Jan

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

(IN

R)

Larsen & Toubro

11 Edelweiss Securities Limited

Larsen & Toubro

DISCLAIMER

Edelweiss Securities Limited (“ESL” or “Research Entity”) is regulated by the Securities and Exchange Board of India (“SEBI”) and is licensed to carry on the business of broking, depository services and related activities. The business of ESL and its Associates (list available on www.edelweissfin.com) are organized around five broad business groups – Credit including Housing and SME Finance, Commodities, Financial Markets, Asset Management and Life Insurance.

This Report has been prepared by Edelweiss Securities Limited in the capacity of a Research Analyst having SEBI Registration No.INH200000121 and distributed as per SEBI (Research Analysts) Regulations 2014. This report does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Securities as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 includes Financial Instruments and Currency Derivatives. The information contained herein is from publicly available data or other sources believed to be reliable. This report is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this report should make such investigation as it deems necessary to arrive at an independent evaluation of an investment in Securities referred to in this document (including the merits and risks involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors.

This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ESL and associates / group companies to any registration or licensing requirements within such jurisdiction. The distribution of this report in certain jurisdictions may be restricted by law, and persons in whose possession this report comes, should observe, any such restrictions. The information given in this report is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. ESL reserves the right to make modifications and alterations to this statement as may be required from time to time. ESL or any of its associates / group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. ESL is committed to providing independent and transparent recommendation to its clients. Neither ESL nor any of its associates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including loss of revenue or lost profits that may arise from or in connection with the use of the information. Our proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein. Past performance is not necessarily a guide to future performance .The disclosures of interest statements incorporated in this report are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The information provided in these reports remains, unless otherwise stated, the copyright of ESL. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of ESL and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.

ESL shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the ESL to present the data. In no event shall ESL be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented by the ESL through this report.

We offer our research services to clients as well as our prospects. Though this report is disseminated to all the customers simultaneously, not all customers may receive this report at the same time. We will not treat recipients as customers by virtue of their receiving this report.

ESL and its associates, officer, directors, and employees, research analyst (including relatives) worldwide may: (a) from time to time, have long or short positions in, and buy or sell the Securities, mentioned herein or (b) be engaged in any other transaction involving such Securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company/company(ies) discussed herein or act as advisor or lender/borrower to such company(ies) or have other potential/material conflict of interest with respect to any recommendation and related information and opinions at the time of publication of research report or at the time of public appearance. ESL may have proprietary long/short position in the above mentioned scrip(s) and therefore should be considered as interested. The views provided herein are general in nature and do not consider risk appetite or investment objective of any particular investor; readers are requested to take independent professional advice before investing. This should not be construed as invitation or solicitation to do business with ESL.

12 Edelweiss Securities Limited

Engineering and Capital Goods

ESL or its associates may have received compensation from the subject company in the past 12 months. ESL or its associates may have managed or co-managed public offering of securities for the subject company in the past 12 months. ESL or its associates may have received compensation for investment banking or merchant banking or brokerage services from the subject company in the past 12 months. ESL or its associates may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months. ESL or its associates have not received any compensation or other benefits from the Subject Company or third party in connection with the research report. Research analyst or his/her relative or ESL’s associates may have financial interest in the subject company. ESL and/or its Group Companies, their Directors, affiliates and/or employees may have interests/ positions, financial or otherwise in the Securities/Currencies and other investment products mentioned in this report. ESL, its associates, research analyst and his/her relative may have other potential/material conflict of interest with respect to any recommendation and related information and opinions at the time of publication of research report or at the time of public appearance.

Participants in foreign exchange transactions may incur risks arising from several factors, including the following: ( i) exchange rates can be volatile and are subject to large fluctuations; ( ii) the value of currencies may be affected by numerous market factors, including world and national economic, political and regulatory events, events in equity and debt markets and changes in interest rates; and (iii) currencies may be subject to devaluation or government imposed exchange controls which could affect the value of the currency. Investors in securities such as ADRs and Currency Derivatives, whose values are affected by the currency of an underlying security, effectively assume currency risk.

Research analyst has served as an officer, director or employee of subject Company: No

ESL has financial interest in the subject companies: No

ESL’s Associates may have actual / beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report.

Research analyst or his/her relative has actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report: No

ESL has actual/beneficial ownership of 1% or more securities of the subject company at the end of the month immediately preceding the date of publication of research report: No

Subject company may have been client during twelve months preceding the date of distribution of the research report.

There were no instances of non-compliance by ESL on any matter related to the capital markets, resulting in significant and material disciplinary action during the last three years except that ESL had submitted an offer of settlement with Securities and Exchange commission, USA (SEC) and the same has been accepted by SEC without admitting or denying the findings in relation to their charges of non registration as a broker dealer.

A graph of daily closing prices of the securities is also available at www.nseindia.com

Analyst Certification:

The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

Additional Disclaimers

Disclaimer for U.S. Persons

This research report is a product of Edelweiss Securities Limited, which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Edelweiss Securities Limited only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

13 Edelweiss Securities Limited

Larsen & Toubro

Access the entire repository of Edelweiss Research on www.edelresearch.com

In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Edelweiss Securities Limited has entered into an agreement with a U.S. registered broker-dealer, Edelweiss Financial Services Inc. ("EFSI"). Transactions in securities discussed in this research report should be effected through Edelweiss Financial Services Inc. Disclaimer for U.K. Persons

The contents of this research report have not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 ("FSMA"). In the United Kingdom, this research report is being distributed only to and is directed only at (a) persons who have professional experience in matters relating to investments falling within Article 19(5) of the FSMA (Financial Promotion) Order 2005 (the “Order”); (b) persons falling within Article 49(2)(a) to (d) of the Order (including high net worth companies and unincorporated associations); and (c) any other persons to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”). This research report must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this research report relates is available only to relevant persons and will be engaged in only with relevant persons. Any person who is not a relevant person should not act or rely on this research report or any of its contents. This research report must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person. Disclaimer for Canadian Persons

This research report is a product of Edelweiss Securities Limited ("ESL"), which is the employer of the research analysts who have prepared the research report. The research analysts preparing the research report are resident outside the Canada and are not associated persons of any Canadian registered adviser and/or dealer and, therefore, the analysts are not subject to supervision by a Canadian registered adviser and/or dealer, and are not required to satisfy the regulatory licensing requirements of the Ontario Securities Commission, other Canadian provincial securities regulators, the Investment Industry Regulatory Organization of Canada and are not required to otherwise comply with Canadian rules or regulations regarding, among other things, the research analysts' business or relationship with a subject company or trading of securities by a research analyst. This report is intended for distribution by ESL only to "Permitted Clients" (as defined in National Instrument 31-103 ("NI 31-103")) who are resident in the Province of Ontario, Canada (an "Ontario Permitted Client"). If the recipient of this report is not an Ontario Permitted Client, as specified above, then the recipient should not act upon this report and should return the report to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any Canadian person. ESL is relying on an exemption from the adviser and/or dealer registration requirements under NI 31-103 available to certain international advisers and/or dealers. Please be advised that (i) ESL is not registered in the Province of Ontario to trade in securities nor is it registered in the Province of Ontario to provide advice with respect to securities; (ii) ESL's head office or principal place of business is located in India; (iii) all or substantially all of ESL's assets may be situated outside of Canada; (iv) there may be difficulty enforcing legal rights against ESL because of the above; and (v) the name and address of the ESL's agent for service of process in the Province of Ontario is: Bamac Services Inc., 181 Bay Street, Suite 2100, Toronto, Ontario M5J 2T3 Canada. Disclaimer for Singapore Persons

In Singapore, this report is being distributed by Edelweiss Investment Advisors Private Limited ("EIAPL") (Co. Reg. No. 201016306H) which is a holder of a capital markets services license and an exempt financial adviser in Singapore and (ii) solely to persons who qualify as "institutional investors" or "accredited investors" as defined in section 4A(1) of the Securities and Futures Act, Chapter 289 of Singapore ("the SFA"). Pursuant to regulations 33, 34, 35 and 36 of the Financial Advisers Regulations ("FAR"), sections 25, 27 and 36 of the Financial Advisers Act, Chapter 110 of Singapore shall not apply to EIAPL when providing any financial advisory services to an accredited investor (as defined in regulation 36 of the FAR. Persons in Singapore should contact EIAPL in respect of any matter arising from, or in connection with this publication/communication. This report is not suitable for private investors.

Copyright 2009 Edelweiss Research (Edelweiss Securities Ltd). All rights reserved