Embed Size (px)

DESCRIPTION

Economic Market Potential for Electric Utility Use of Distributed Generation. For The Edison Electric Institute June 20, 2001 By Joe Iannucci (925) 447-0604 [email protected]. Introduction Methodology Overview Assumptions: Utility and DG DG Economic Market Potential - PowerPoint PPT Presentation

Citation preview

Distributed Utility Associates

Economic Market Potential for Electric Utility Use

of Distributed Generation

For

The Edison Electric Institute

June 20, 2001

By

Joe Iannucci(925) 447-0604 [email protected]

EEI_DG_2001_Results

2 Distributed Utility Associates04/19/23

Agenda

• Introduction

• Methodology Overview

• Assumptions: Utility and DG

• DG Economic Market Potential

• Observations and Conclusions

• R&D Needs and Opportunities

EEI_DG_2001_Results

3 Distributed Utility Associates04/19/23

Utility Economics lower cost of servicebetter asset utilization improved operationSubstation and feeder locations

G, T, D,FUEL

g,fuel,

customer services

DUVal

EEI_DG_2001_Results

4 Distributed Utility Associates04/19/23

Utility Avoided Cost “Value Mountain” Illustration

Peak Load @ Feeder, 2002, Base Case Fuel Prices

0

5

10

15

20

25

30

61 71 81 91 101 111 121 131

Avoided Cost ($/kW-yr)

Fre

qu

ency

of

Occ

urr

ence

(of

a g

iven

co

st)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eco

no

mic M

arket P

oten

tial (% o

f MW

)

Avoided Cost Frequency

Portion of MW (Market)DR Cost -> Economic Market Potential

Economic Economic Market Market

PotentialPotentialDR CostDR Cost

EEI_DG_2001_Results

5 Distributed Utility Associates04/19/23

Peak Load and Load Growth,Load “In-play”

• TECHNICAL Potential = Load Growth

• NERC Load GROWTH Projections

• Increase “Direct” Load Growth to account for Load Diversity multiply by 1.6, approximate ratio of end-of-line transformer capacity (kVA* power factor)

central load (kW)

• 2002: 21,822 MW 2010: 22,205 MW

EEI_DG_2001_Results

6 Distributed Utility Associates04/19/23

DG Hours of Operation

• Peak Load: 200 Hours/year

• Base Load: 5,256 hours/year– load factor .6

EEI_DG_2001_Results

7 Distributed Utility Associates04/19/23

DG Fuel Price Assumptions

• Base Case– relatively flat gas and coal prices

• High Fuel Cost Case– gas price based on futures price, Feb 2001– assume coal prices “track” gas prices

• Natural Gas Volume-based Prices@ Substation: Wholesale On-site: Retail

• Transportation Charges per EIA/NEMS, added to Commodity Prices

EEI_DG_2001_Results

8 Distributed Utility Associates04/19/23

Fuel Cost Case Location 2002 2010Base Case Industrial/Substation 3.515 3.613

Commercial/Feeder 5.691 5.749

High Price Industrial/Substation 6.565 7.096Commercial/Feeder 8.919 9.306

DG Natural Gas Prices Assumed

• DG Natural Gas Prices Assumed

• Forward Averaged

• Diesel Fuel: EIA Retail Price Forecast

EEI_DG_2001_Results

9 Distributed Utility Associates04/19/23

Peak Load Electricity Cost Assumptions

• “blend” of common peaking resources’ + capacity cost + O&M + fuel cost

Fuel Cost CaseBase High

Low 38.1 40.0Mean 44.3 48.1

Max 53.4 60.8

Peak Electricity Cost, 2002, Summary ($/kW-yr)

Fuel Cost CaseBase High

Low 38.4 40.0Mean 44.4 48.8

Max 53.7 62.0

Peak Electricity Cost, 2010, Summary ($/kW-yr)

EEI_DG_2001_Results

10 Distributed Utility Associates04/19/23

Baseload Electric Energy Cost Assumptions

• Base Case and High Case Fuel Cost Cases

• “Blend” of combined cycle gas and coal.

• Annual Cost $/kW-yrBase Case Scenario High Fuel Price Scenario

2002 2010 2002 2010CostElement CC Coal CC Coal CC Coal CC Coal

Capital 65.5 171.6 58.5 168.1 65.5 171.6 58.5 168.1

O&M 10.5 23.6 10.5 23.6 10.5 23.6 10.5 23.6

Fuel 153.9 43.3 139.1 36.1 287.4 80.8 273.1 71.0

Total 229.9 238.5 208.1 227.9 363.4 276.1 342.1 262.7

Mean 234.2 218.0 319.8 302.4

lowmean

high

EEI_DG_2001_Results

11 Distributed Utility Associates04/19/23

Utility T&D Capacity Cost Assumptions

• FERC Form 1 T&D Budgets

• Load Growth per NERC Forecasts

• Statistical Spread Derived Assuming Mean Values of:

$/kW-year

Transmission $12.1

Distribution $41.9

EEI_DG_2001_Results

12 Distributed Utility Associates04/19/23

Other Utility Assumptions• Value-of service & “Reliability Benefits”

– applies at feeder locations • assume cause for 99% of outages beyond substation

• outage losses “avoided”

– outage rate .029% * 8760 = 2.5 hours per year– Value of service (unserved energy) $3/kWh– TOTAL: 2.5 hours * $3/kWh = $7.50/kW-year

• T&D Losses – affects fuel use and grid capacity needs

average: 4% on-peak: 7%

~ 8% of total!

EEI_DG_2001_Results

13 Distributed Utility Associates04/19/23

Peaking Distributed Generators’ Cost and Performance

2002

Distributed Installed CostHeatRate

VariableO&M

Generator Type $/kW $/kW-yr* Btu/kWh $/kWh

Microturbine 400 60.00 12,000 .01

ATS 525 78.75 8,985 .006

Combustion Turbine 400 60.00 10,500 .01

Dual Fuel Engine 450 67.50 8,600 .02

Otto/Spark Engine 425 63.75 9,700 .025

Diesel Engine 410 61.50 7,800 .025

* Utility fixed charge rate of 0.15 is assumed.

2010

Distributed Installed CostHeatRate

VariableO&M

Generator Type $/kW $/kW-yr* Btu/kWh $/kWh

Microturbine 400 60.00 12,000 .01

ATS 525 78.75 8,985 .006

Combustion Turbine 400 60.00 10,500 .01

Dual Fuel Engine 450 67.50 8,600 .02

Otto/Spark Engine 425 63.75 9,700 .025

Diesel Engine 410 61.50 7,800 .025

* Utility fixed charge rate of 0.15 is assumed.

EEI_DG_2001_Results

14 Distributed Utility Associates04/19/23

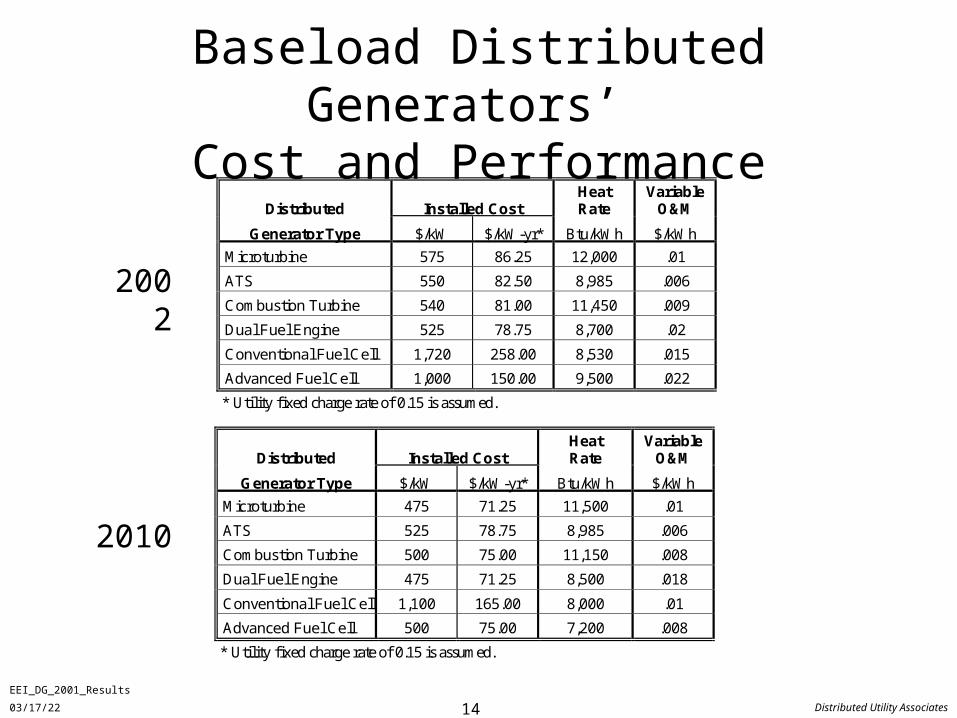

Baseload Distributed Generators’ Cost and Performance

2010

2002

Distributed Installed CostHeatRate

VariableO&M

Generator Type $/kW $/kW-yr* Btu/kWh $/kWh

Microturbine 575 86.25 12,000 .01

ATS 550 82.50 8,985 .006

Combustion Turbine 540 81.00 11,450 .009

Dual Fuel Engine 525 78.75 8,700 .02

Conventional Fuel Cell 1,720 258.00 8,530 .015

Advanced Fuel Cell 1,000 150.00 9,500 .022

* Utility fixed charge rate of 0.15 is assumed.

Distributed Installed CostHeatRate

VariableO&M

Generator Type $/kW $/kW-yr* Btu/kWh $/kWh

Microturbine 475 71.25 11,500 .01

ATS 525 78.75 8,985 .006

Combustion Turbine 500 75.00 11,150 .008

Dual Fuel Engine 475 71.25 8,500 .018

Conventional Fuel Cell 1,100 165.00 8,000 .01

Advanced Fuel Cell 500 75.00 7,200 .008

* Utility fixed charge rate of 0.15 is assumed.

EEI_DG_2001_Results

15 Distributed Utility Associates04/19/23

Economic Market Potential Estimates, Peak 2002

Base Case Fuel Prices

High Fuel Prices

Peaking DG Economic Market Potential, Base Case Fuel Price, 2002

16,000

17,000

18,000

19,000

20,000

21,000

22,000

Mic

rotu

rbin

e

ATS

Con

vent

iona

l CT

Dua

l Fue

led

Otto

/Spa

rk

Die

sel

MW

Peaking DG Economic Market Potential, High Fuel Price, 2002

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Mic

rotu

rbin

e

ATS

Con

vent

iona

l CT

Dua

l Fue

led

Otto

/Spa

rk

Die

sel

MW

EEI_DG_2001_Results

16 Distributed Utility Associates04/19/23

Economic Market Potential Estimates, Peak 2010

High Fuel Cost

Base Case Fuel CostPeaking DG Economic Market Potential,

Base Case Fuel Price, 2010

0

5,000

10,000

15,000

20,000

25,000

Mic

rotu

rbin

e

ATS

Con

vent

iona

l CT

Dua

l Fue

led

Otto

/Spa

rk

Die

sel

MW

Peaking DG Economic Market Potential, High Fuel Price, 2010

0

5,000

10,000

15,000

20,000

25,000

Mic

rotu

rbin

e

ATS

Con

vent

iona

l CT

Dua

l Fue

led

Otto

/Spa

rk

Die

sel

MW

EEI_DG_2001_Results

17 Distributed Utility Associates04/19/23

Value Mountain 2002 Peaker, Feeder Location

Peak Load @ Feeder, 2002, Base Case Fuel Prices

0

5

10

15

20

25

30

61 71 81 91 101 111 121 131

Avoided Cost ($/kW-yr)

Fre

qu

ency

of

Occ

urr

ence

(o

f a

giv

en c

ost

)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eco

no

mic M

arket P

oten

tial (% o

f MW

)

Avoided Cost Frequency

Portion of MW (Market)

EEI_DG_2001_Results

18 Distributed Utility Associates04/19/23

Observations and Conclusions Peaker DGs

• very competitive with respect to total annual cost to serve new load as capacity resources

EEI_DG_2001_Results

19 Distributed Utility Associates04/19/23

Value Mountain 2002 Baseload, Feeder Location

Baseload @ Feeder, Base, 2002, Base Case Fuel Prices

0

5

10

15

20

25

30

261 271 281 291 301 311 321 331

Avoided Cost ($/kW-yr)

Fre

qu

ency

of

Occ

urr

ence

(o

f a

giv

en c

ost

)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eco

no

mic M

arket P

oten

tial (% o

f MW

)

Avoided Cost Frequency

Portion of MW (Market)

EEI_DG_2001_Results

20 Distributed Utility Associates04/19/23

Results, Baseload• Markets are essentially zero with two

important exceptions.

• ATS all at sub (low cost gas), base case fuel price

only

2002: ~29% 2010: <3%

• Advanced Fuel Cell all at sub (low cost gas), 2010 only

2010 base case fuel prices: 68.3%

2010 high fuel prices: 4.1%

EEI_DG_2001_Results

21 Distributed Utility Associates04/19/23

Baseload DGs: Observations• Difficult for even superior DGs to compete

with grid as utility-owned energy resource, especially with regard to– production cost / wholesale price of electricity– capacity cost for new central generation

• Conversely: Viability Very Sensitive to Fuel Price and Efficiency

• “Low cost,” efficient fuel cells can compete for “small” portion of load growth

EEI_DG_2001_Results

22 Distributed Utility Associates04/19/23

Baseload DGs: Conclusions

• May need one or more of the following– more run hours– DGs with even lower cost than expected– DGs with even higher efficiency than expected– CHP benefits– Aggregated/Bulk Purchases of Gas

• to reduce fuel cost for feeder/customer locations

EEI_DG_2001_Results

23 Distributed Utility Associates04/19/23

Caveats and Considerations

• “Economic Market Potential”– based purely on direct cost-effectiveness for

meeting load growth– based on utility annual (avoided) cost ($/kW-year)

– without regard to institutional challenges

• Estimates made assuming that technologies are commercially viable and readily available.

EEI_DG_2001_Results

24 Distributed Utility Associates04/19/23

Caveats and Considerations

• Baseload and Peaking duty cycles evaluated in isolation.

• Each DG evaluated individually– without regard to substitutes

(i.e., other types of distributed generation, storage, or geographically targeted DSM)

• Assumed fuel access and availability.

EEI_DG_2001_Results

25 Distributed Utility Associates04/19/23

Implementation Issuesor, if it’s so good why isn’t it happening?

EXCEPTION:increasing use of DGs for “supply” benefits…

…limited regard to “local” benefits (T&D)…

...for now?

EEI_DG_2001_Results

26 Distributed Utility Associates04/19/23

Implementation Issuesor, if it’s so good why isn’t it happening?

• Complexity – versus planning of “conventional” option:

Fuel + G + T + D

• Not Standard Engineering Practice

• Insufficient Evaluation Tools– engineering – financial

• Insufficient Data

EEI_DG_2001_Results

27 Distributed Utility Associates04/19/23

Implementation Issuesor, if it’s so good why isn’t it happening?

• Financials– utility-owned DGs -- financing and rules?– lease or rent DGs -- strains modest utility

expense budgets (especially distribution)– benefits sharing arrangements/partnerships?

• Intra-utility Discontinuities– overlapping / divergent missions– uncertain incentives

• Emissions Issues

EEI_DG_2001_Results

28 Distributed Utility Associates04/19/23

R&D Needs and Opportunities• Utility Markets Topics

– Plant Capital Cost Sensitivities– Regional Analysis– Activate Customer-owned Backup Generators

as Utility Resource– Intermediate Load DG Operation, i.e.,

• Peak/capacity DG’s seem great

• difficult for baseload/energy DG’s to compete

– Air Emissions Implications

EEI_DG_2001_Results

29 Distributed Utility Associates04/19/23

R&D Needs and Opportunities• Customer Perspective Market Potential

– Bill Reduction

• Customer Perspective, segments– commercial – institutional– industrial – IT operations

• DR Options– CHP

–Targeted Demand Management

– Storage

EEI_DG_2001_Results

30 Distributed Utility Associates04/19/23

Backups

EEI_DG_2001_Results

31 Distributed Utility Associates04/19/23

Customer Economics

lower energy billbetter service--quality, reliability

Comparing Central to DU Solutions

Bill and Benefits Comparison

Purchasingpower

cost and benefits ofDG options

DUVal-C

EEI_DG_2001_Results

32 Distributed Utility Associates04/19/23

Institutional Customer Bill Analysis Results Summary

2002

DG Type B/CEconomic

Run-Hours B/CEconomic

Run-Hours B/CEconomic

Run-Hours

Microturbine 1.294 3,465 .615 881 .594 599Microturbine

CHP1.472 7,778 .856 7,828 .79 5,234

Diesel .985 1,914 .708 881 .653 599ATS-cogen 1.311 7,778 .898 7,828 .725 2,782Gas Spark 1.196 3,465 .684 881 .654 599

Fuel Cell .619 3,465 .228 881 .206 599

2010

DG Type B/CEconomic

Run-Hours B/CEconomic

Run-Hours B/CEconomic

Run-Hours

Microturbine 1.434 3,465 .716 881 .699 599Microturbine

CHP1.575 7,778 .916 7,828 .856 5,234

Diesel 1.006 3,465 .712 881 .662 599ATS-cogen 1.378 7,778 .913 7,828 .758 2,782Gas Spark 1.249 3,465 .707 881 .665 599

Fuel Cell 1.063 3,465 .611 2,403 .403 599

Region 3

Region 1 Region 2 Region 3

Region 1 Region 2

EEI_DG_2001_Results

33 Distributed Utility Associates04/19/23

Diesel Gensets, Cost Versus B/C Ratio

Installed Cost versus Benefit Cost Ratio, for Diesel Gensets

.6

.7

.8

.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

50 100 150 200 250 300 350 400Installed Cost ($/kW)

B/C

Ra

tio

PG&E-599 Hours

SDG&E-1,913 Hours

EEI_DG_2001_Results

34 Distributed Utility Associates04/19/23

Customer Bill Reduction Potential (Economic Benefits)

Technology

Operation Hours Per

YearTotal B/C

Ratio

Incremental Savings ($/kW-yr)

Total Savings ($/kW-yr)

Incremental Savings

($Milion/yr)Total Savings ($Million/yr)

Microturbine 3,465 1.29 208.42 83.70 1,955 785

Microturbine w/CHP

7,778 1.47 343.17 168.56 3,219 1,581

Diesel 1,914 0.99 85.30 -3.63 800 -34ATS w/CHP 7,778 1.31 272.33 124.84 2,554 1,171

Gas Spark 3,465 1.20 163.38 60.35 1,532 566Fuel Cell 3,465 0.62 180.70 -227.05 1,695 -2,130

EEI_DG_2001_Results

35 Distributed Utility Associates04/19/23

Customer Bill Analysis with Resulting DG Air Emissions

Operation Portion of Total % Change, Relative to In-state, Average Central Generation Only

TechnologyHours Per

YearEnergy

From DGB/C

Ratio NOx SOx CO CO2 PM VOC

Microturbine 3,465 44.5% 1.29 +346% +13% +648% +210% -12% +44%Micro

turbine 7,778 100.0% 1.47 +398% +29% +970% -117% -74% -294%

Diesel 1,914 24.6% .99 +3,032% +5,819% +1,341% +173% +590% +2,433%

ATS w/CHP 7,778 100.0% 1.31 +376% +2% +1,017% -47% -75% -214%

Gas Spark 3,465 44.5% 1.2 +1,095% -23% +1,933% +165% +141% +4,405%

Fuel Cell 3,465 44.5% .62 -45% -45% -45% +134% -45% -45%

EEI_DG_2001_Results

36 Distributed Utility Associates04/19/23

Emissions Due to Cost-effective Utility Use of DG

2010 Load Growth (MW/yr): 1,144 Tons of Emissions (000 tons CO2)

Peaking DG OptionPortion of Growth NOx SOx CO CO2 VOCs PM

System Only 100% 15 2 238 24 2 13

Microturbine 75.3% 90 2 278 101 4 10

ATS 70.3% 89 2 280 83 3 9

Conventional CT 79.0% 104 3 170 100 4 10

Dual Fueled Engine 52.0% 602 7 1,897 63 61 25

Otto/Spark Engine 54.5% 169 2 607 71 95 1,890

Diesel Engine 74.8% 1,457 26 2,625 151 172 260

EEI_DG_2001_Results

37 Distributed Utility Associates04/19/23

DG Gas Price Details

Commodity ($/MMBtu)

Transportation ($/MMBtu)

Price($/MMBtu)

Industrial/Substation Base Case 2002 2.727 .787 3.5152010 2.821 .792 3.613

High Price 2002 5.741 .824 6.5652010 6.268 .828 7.096

Commercial/Feeder Base Case 2002 2.727 2.963 5.6912010 2.821 2.928 5.749

High Price 2002 5.741 3.178 8.9192010 6.268 3.038 9.306

* 2002 values = average of 2002 - 2020 prices

** 2010 values = average of 2010 - 2020 prices

*** Base Case values from AE2001, $1999

**** High Price Case based on Futures Prices, Walls Street Journal. Feb 28, 2001.

Price Escalation based on growth rate in EIA AE2000 for High Gas Case.

EEI_DG_2001_Results

38 Distributed Utility Associates04/19/23

Peaking Generation Cost Details Year 2002

Base Case Total Cost

Variable Cost Fixed Cost Total Total Cost

Capacity Type

HeatRate

(Btu/kWh)

FuelPrice

($/MMBtu)

FuelCost

(¢/kWh)O&M

(¢/kWh) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr)

Upgrade Emergency Generators 12,000 9.0 10.8 3.0 13.8 27.6 9.0 18.0 22.8 45.6Refurbish Old CT - gas 13,000 3.5 4.6 2.5 7.1 14.1 12.0 24.0 19.1 38.1

New Utility Peaker CT - gas 12,000 3.5 4.2 1.5 5.7 11.4 21.0 42.0 26.7 53.4Purchase Capacity - gas -- 3.5 0.0 -- -- 20.0 40.0 20.0 40.0

Annual Hours of operation = 200

Fixed Charge Rate = .1200

High Fuel Cost Case Total Cost

Variable Cost Fixed Cost Total Total Cost

Capacity Type

HeatRate

(Btu/kWh)

FuelPrice

($/MMBtu)

FuelCost

(¢/kWh)O&M

(¢/kWh) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr)

Upgrade Emergency Generators 12,000 9.0 10.8 3.0 13.8 27.6 9.0 18.0 22.8 45.6Refurbish Old CT - gas 13,000 6.6 8.5 2.5 11.0 22.1 12.0 24.0 23.0 46.1

New Utility Peaker CT - gas 12,000 6.6 7.9 1.5 9.4 18.8 21.0 42.0 30.4 60.8Purchase Capacity - gas -- 6.6 0.0 -- -- -- 20.0 40.0 20.0 40.0

Annual Hours of operation = 200

Fixed Charge Rate = .1200

EEI_DG_2001_Results

39 Distributed Utility Associates04/19/23

Peaking Generation Cost Details Year 2010

Base Fuel Cost Case Total Cost

Variable Cost Fixed Cost Total Total Cost

Capacity Type

HeatRate

(Btu/kWh)

FuelPrice

($/MMBtu)

FuelCost

(¢/kWh)O&M

(¢/kWh) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr)

Upgrade Emergency Generators 12,000 9.0 10.8 3.0 13.8 27.6 9.0 18.0 22.8 45.6Refurbish Old CT - gas 13,000 3.6 4.7 2.5 7.2 14.4 12.0 24.0 19.2 38.4

New Utility Peaker CT - gas 12,000 3.6 4.3 1.5 5.8 11.7 21.0 42.0 26.8 53.7Purchase Capacity -- 3.6 0.0 -- -- -- 20.0 40.0 20.0 40.0

Annual Hours of operation = 200

Fixed Charge Rate = .1200

High Fuel Cost Case Total Cost

Variable Cost Fixed Cost Total Total Cost

Capacity Type

HeatRate

(Btu/kWh)

FuelPrice

($/MMBtu)

FuelCost

(¢/kWh)O&M

(¢/kWh) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr) (¢/kWh) ($/kW-yr)

Upgrade Emergency Generators 12,000 9.0 10.8 3.0 13.8 27.6 9.0 18.0 22.8 45.6Refurbish Old CT - gas 13,000 7.1 9.2 2.5 11.7 23.5 12.0 24.0 23.7 47.5

New Utility Peaker CT - gas 12,000 7.1 8.5 1.5 10.0 20.0 21.0 42.0 31.0 62.0Purchase Capacity -- 7.1 0.0 -- -- -- 20.0 40.0 20.0 40.0

Annual Hours of operation = 200

Fixed Charge Rate = .1200

EEI_DG_2001_Results

40 Distributed Utility Associates04/19/23

T&D Cost Calculations Details

Item 1997 1998 1999 AverageIOU T All Years ($000) 63,800,198 66,932,701 68,542,040

Budget ($000) 1,875,926 2,118,026 2,311,942 2,101,965IOU D All Years ($000) 158,485,763 169,539,790 179,702,556

Budget ($000) 9,358,122 9,423,258 10,385,483 9,722,287

Load (MW) 637,677 660,293 681,449 659,806

Load Growth (MW) 20,000 21,000 22,000 21,000T Estimated* Capacity Added 24,000 25,200 26,400 25,200T Incremental Cost*** $/kW 102.8 110.6 115.2 109.6

$/kW-yr 11.3 12.2 12.7 12.1D Estimated** Capacity Added 32,000 33,600 35,200 33,600

D Incremental Cost*** $/kW 384.8 369.0 388.2 380.7$/kW-yr 42.3 40.6 42.7 41.9

• Load Diversity Factors

T = 1.2 D = 1.6 • Fixed Charge Rates

T = .1100 D = .1100

EEI_DG_2001_Results

41 Distributed Utility Associates04/19/23

Economic Market Potential Estimates Details Year 2002

High Fuel Cost

2002 Mkt Size: 21,822 MWBaseload Peakload

Technology System @ Sub @ Feeder Technology System @ Sub @ FeederMicroturbine 99.7% 0.2% 0.1% Microturbine 16.6% 0.0% 83.4%

ATS 41.0% 58.7% 0.3% ATS 1.3% 0.0% 98.7%Conventional CT 99.3% 0.6% 0.1% Conventional CT 15.4% 0.0% 84.6%Dual Fuel Engine 99.3% 0.5% 0.2% Dual Fuel Engine 13.2% 0.0% 86.8%

Fuel Cell 100.0% 0.0% 0.0%Spark Engine (Natural Gas) 4.8% 0.0% 95.2%Advanced Fuel Cell 100.0% 0.0% 0.0% Diesel 4.9% 0.0% 95.1%

Base Case Fuel Cost

2002 Mkt Size: 21,822 MWBaseload Peakload

Technology System @ Sub @ Feeder Technology System @ Sub @ FeederMicroturbine 99.8% 0.0% 0.2% Microturbine 61.0% 0.0% 39.0%

ATS 99.5% 0.3% 0.2% ATS 16.4% 0.0% 83.6%Conventional CT 99.8% 0.0% 0.2% Conventional CT 58.5% 0.0% 41.5%Dual Fuel Engine 99.8% 0.0% 0.2% Dual Fuel Engine 51.1% 0.0% 48.9%

Fuel Cell 100.0% 0.0% 0.0%Spark Engine (Natural Gas) 33.6% 0.0% 66.4%Advanced Fuel Cell 100.0% 0.0% 0.0% Diesel 16.6% 0.0% 83.4%

EEI_DG_2001_Results

42 Distributed Utility Associates04/19/23

Economic Market Potential Estimates Details Year 2010

High Fuel Cost

Base Case Fuel Cost

2010 Mkt Size: 22,205 MWBaseload Peakload

Technology System @ Sub @ Feeder Technology System @ Sub @ FeederMicroturbine 99.9% 0.0% 0.1% Microturbine 23.2% 0.0% 76.8%

ATS 99.9% 0.0% 0.1% ATS 10.0% 0.0% 90.0%Conventional CT 99.9% 0.0% 0.1% Conventional CT 15.9% 0.0% 84.1%Dual Fuel Engine 99.9% 0.0% 0.1% Dual Fuel Engine 31.8% 0.0% 68.2%

Fuel Cell 100.0% 0.0% 0.0%Spark Engine (Natural Gas) 29.7% 0.0% 70.3%Advanced Fuel Cell 95.7% 4.1% 0.2% Diesel 13.6% 0.0% 86.4%

2010 Mkt Size: 22,205 MWBaseload Peakload

Technology System @ Sub @ Feeder Technology System @ Sub @ FeederMicroturbine 99.8% 0.0% 0.2% Microturbine 11.4% 0.0% 88.6%

ATS 97.3% 2.4% 0.3% ATS 4.4% 0.0% 95.6%Conventional CT 99.6% 0.2% 0.2% Conventional CT 7.6% 0.0% 92.4%Dual Fuel Engine 99.8% 0.2% 0.0% Dual Fuel Engine 27.1% 0.0% 72.9%

Fuel Cell 100.0% 0.0% 0.0% Spark Engine (Natura 23.0% 0.0% 77.0%Advanced Fuel Cell 31.4% 68.3% 0.3% Diesel 25.0% 0.0% 75.0%