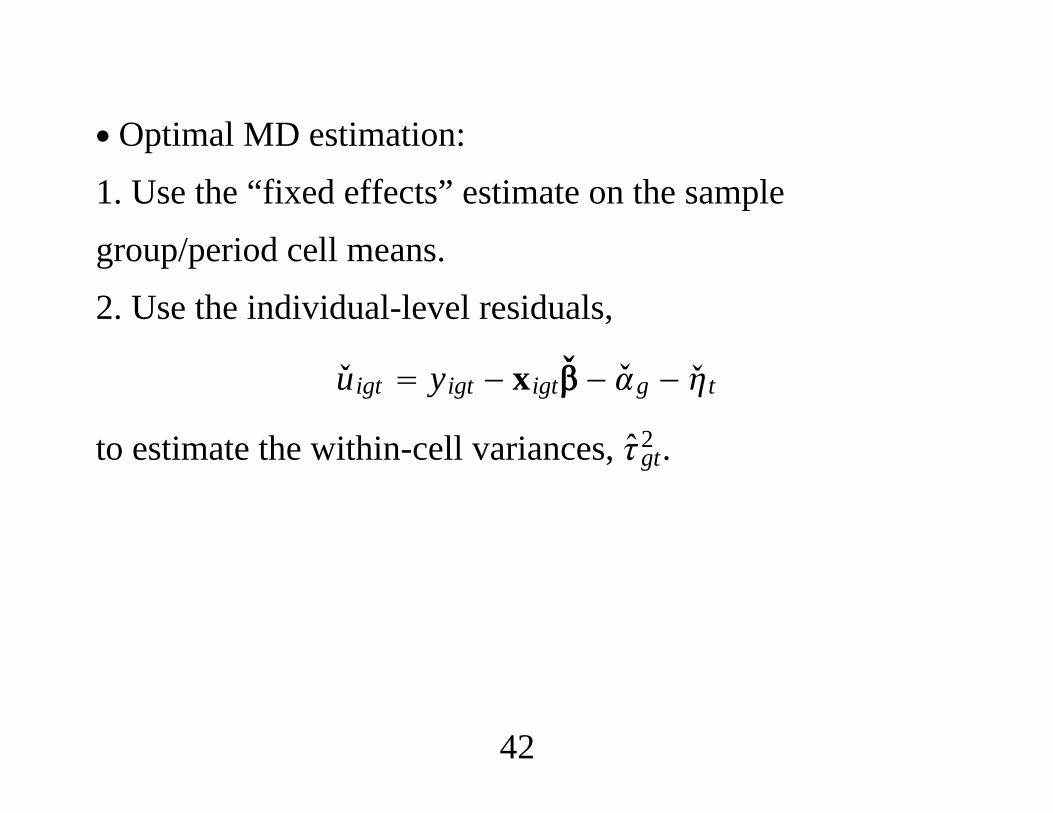

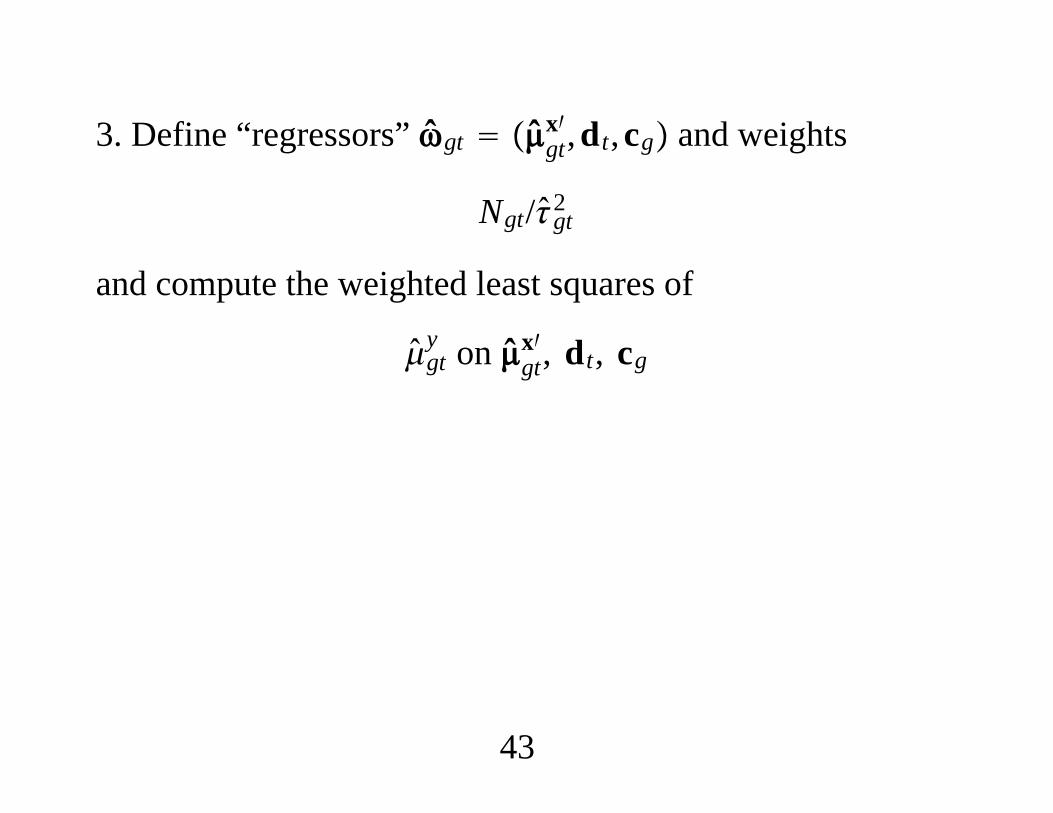

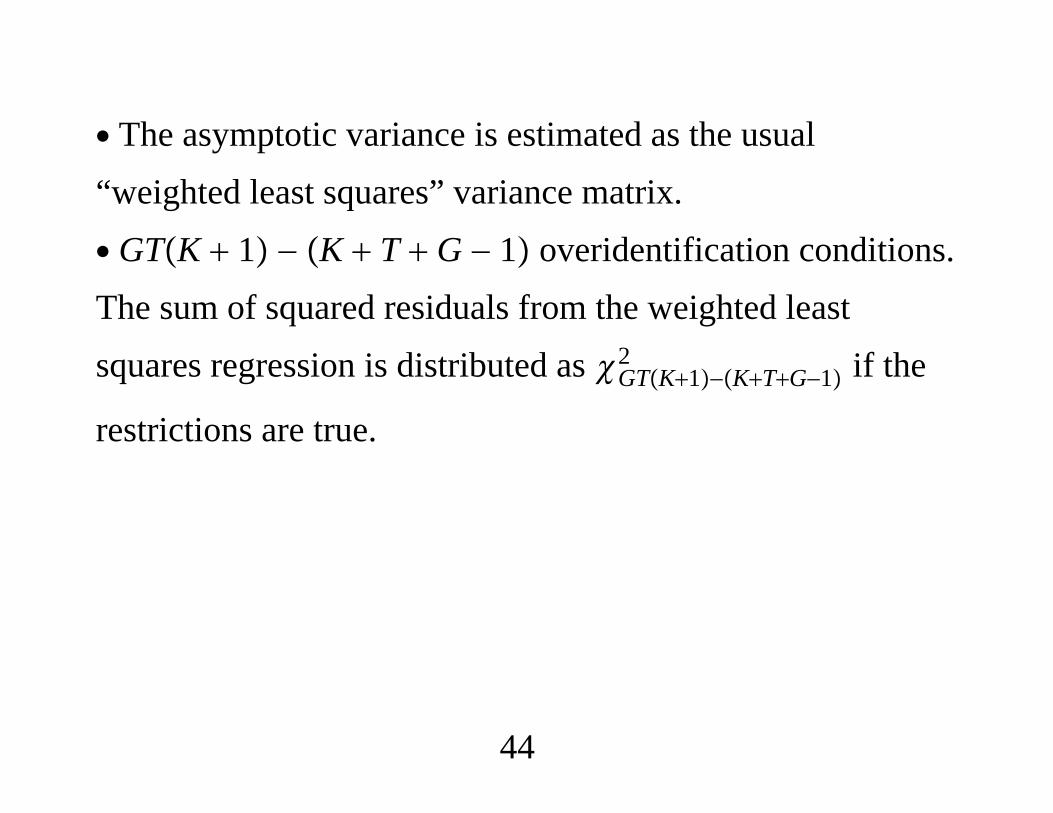

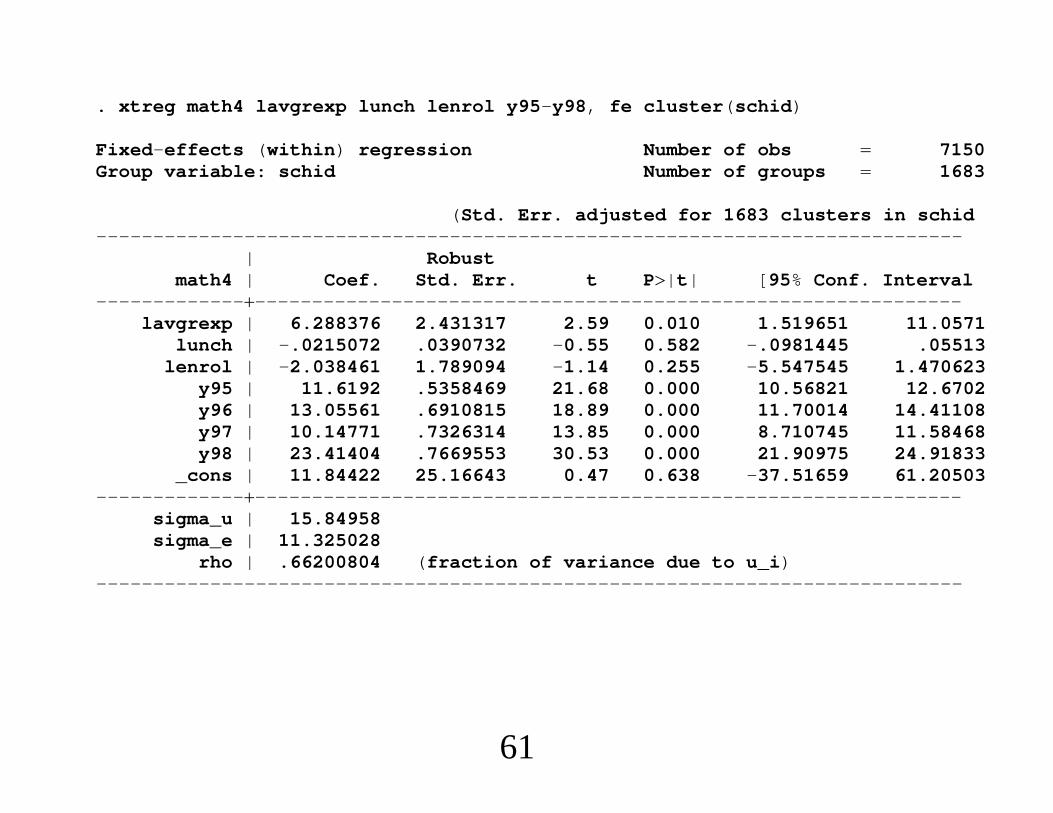

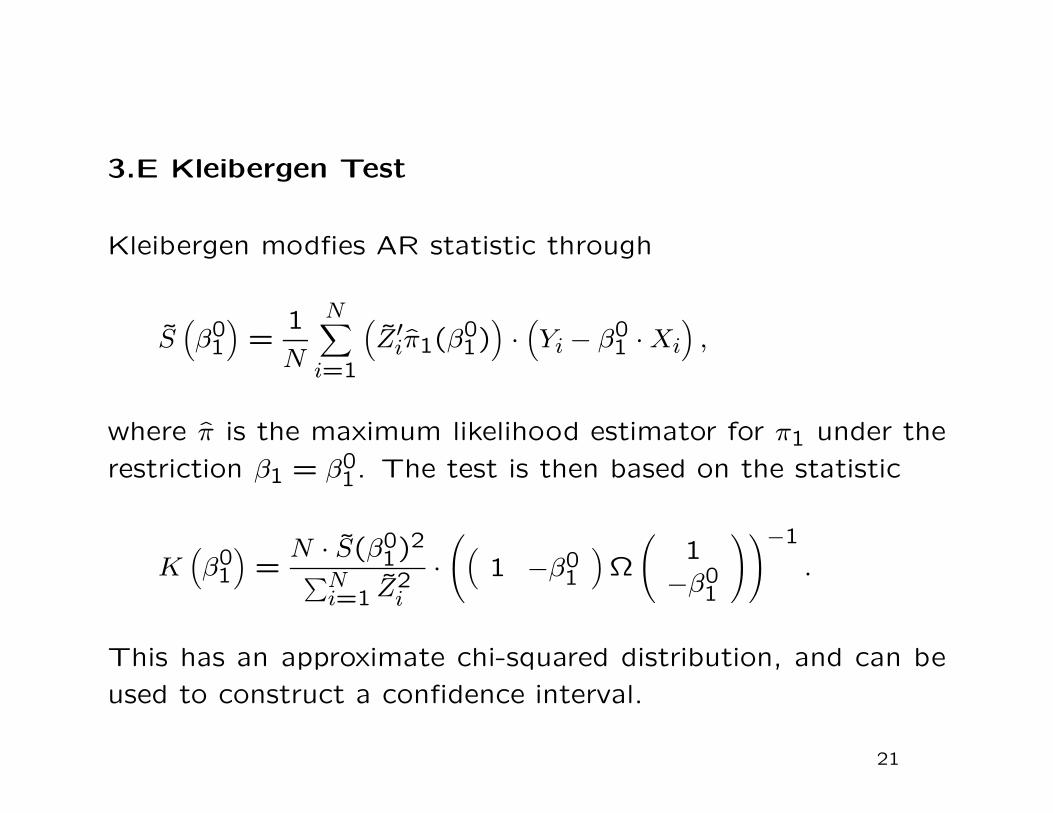

Embed Size (px)

Citation preview

"Econometrics of Cross Section and Panel Data"

Lecture 1

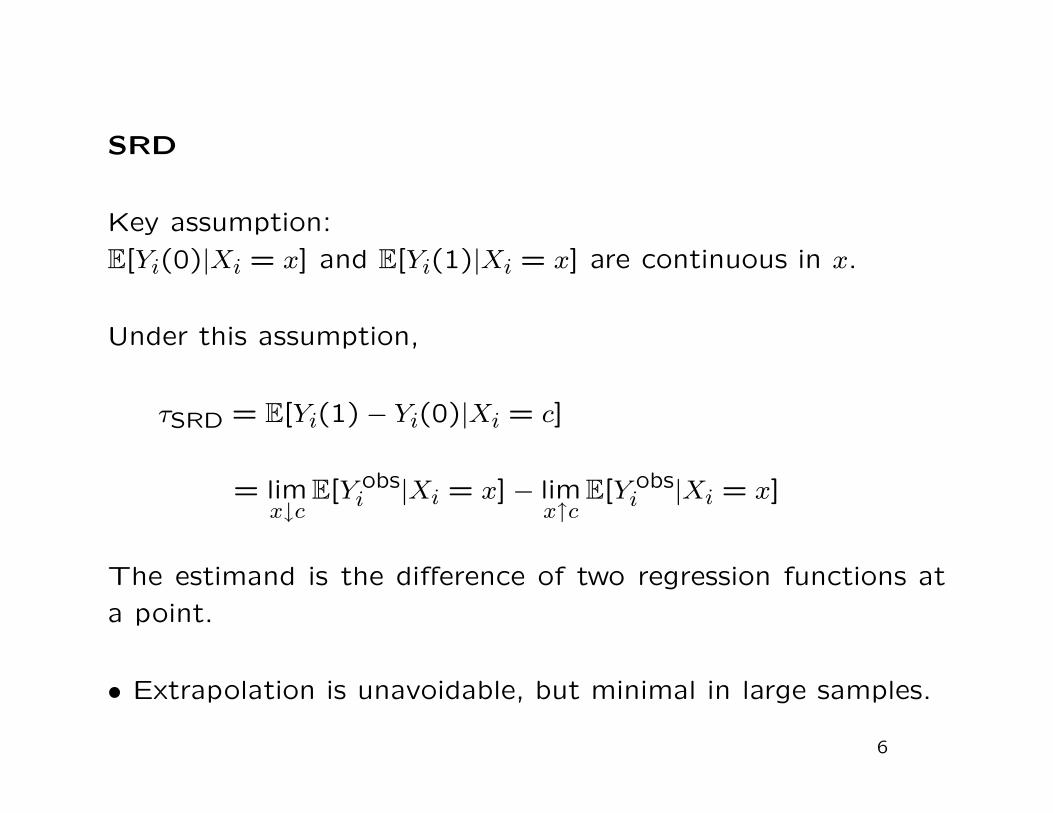

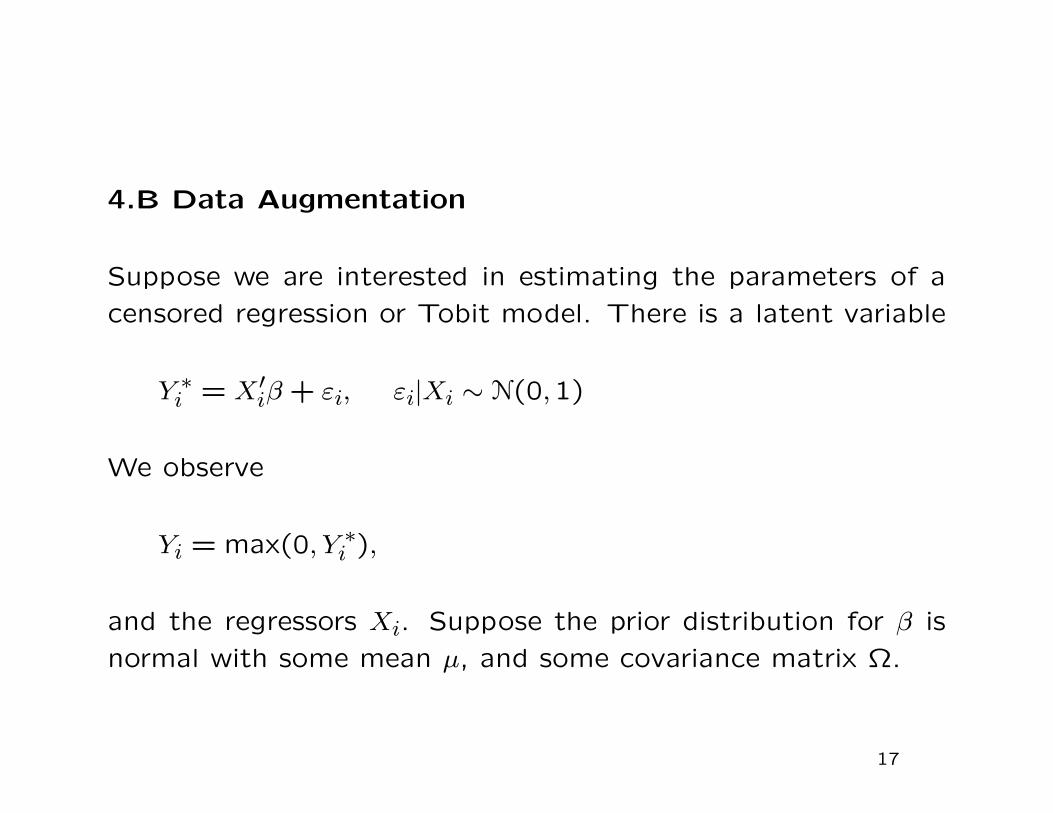

Methods for Estimating Treatment Effects

Under Unconfoundedness, Part I

Guido Imbens

Cemmap Lectures, UCL, June 2014

1.A Introduction

Two applications where unconfoundedness/selection-on-observables

/exogeneity of treatment may be reasonable. How do we go

about analyzing these data?

• Summary Statistics

• Design: ensuring overlap

• Estimates of average treatment effects

• Assessing plausibility of unconfoundedness (should really be

done before estimation of average treatment effects)

2

1.B outline

1. introduction/notation

2. description of applications and summary statistics

3. unconfoundedness

4. concerns with linear regression methods

5. design: assessing and ensuring overlap

6. estimation of average treatment effects

7. assessing unconfoundedness

3

1.C Notation

Treatment indicator: Wi

Potential Outcomes Yi(0), Yi(1)

Covariates Xi

Observed outcome: Y obsi = Wi · Yi(1) + (1 − Wi) · Yi(0).

Nc =∑

(1 − Wi) number of controls, Nt =∑

i Wi number of

treated units.

Yobsc and Y

obst are average outcomes for controls and treated.

4

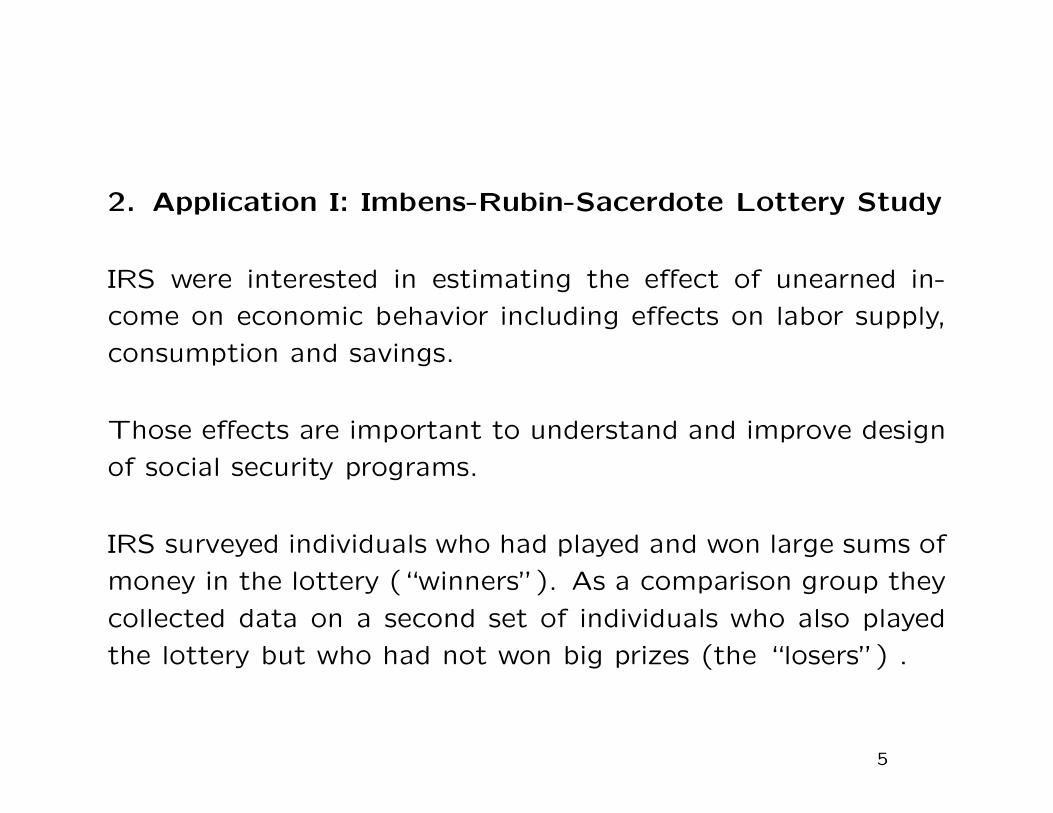

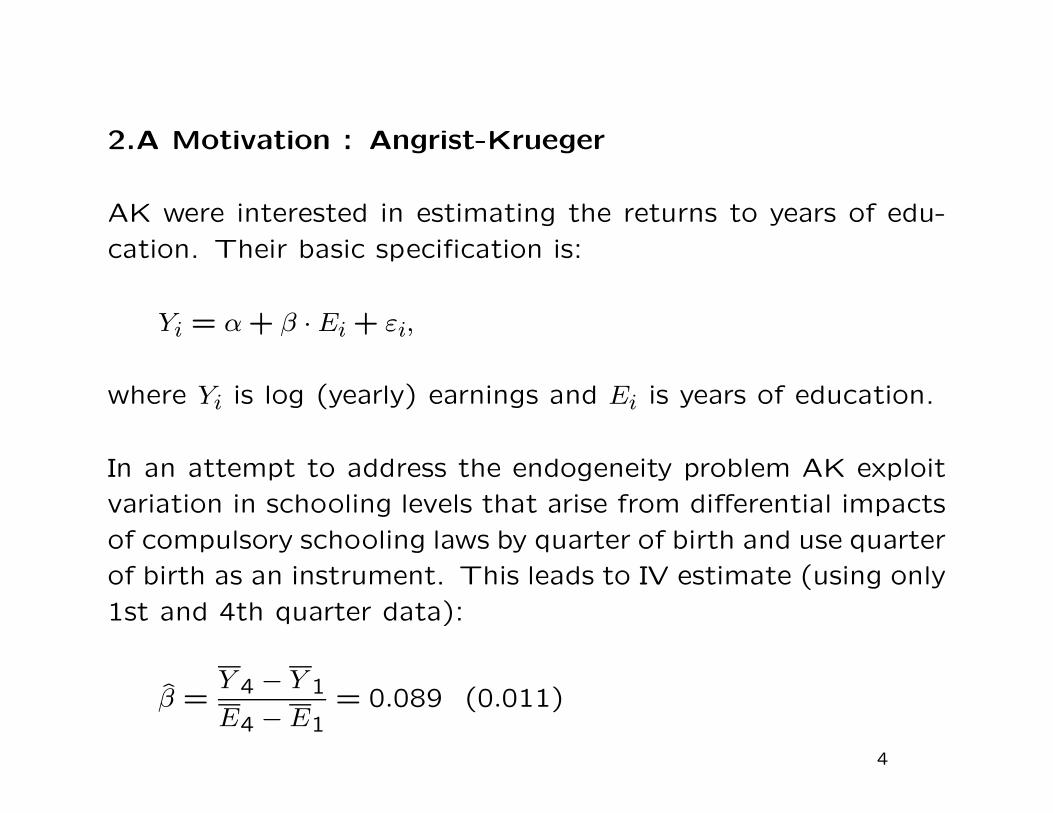

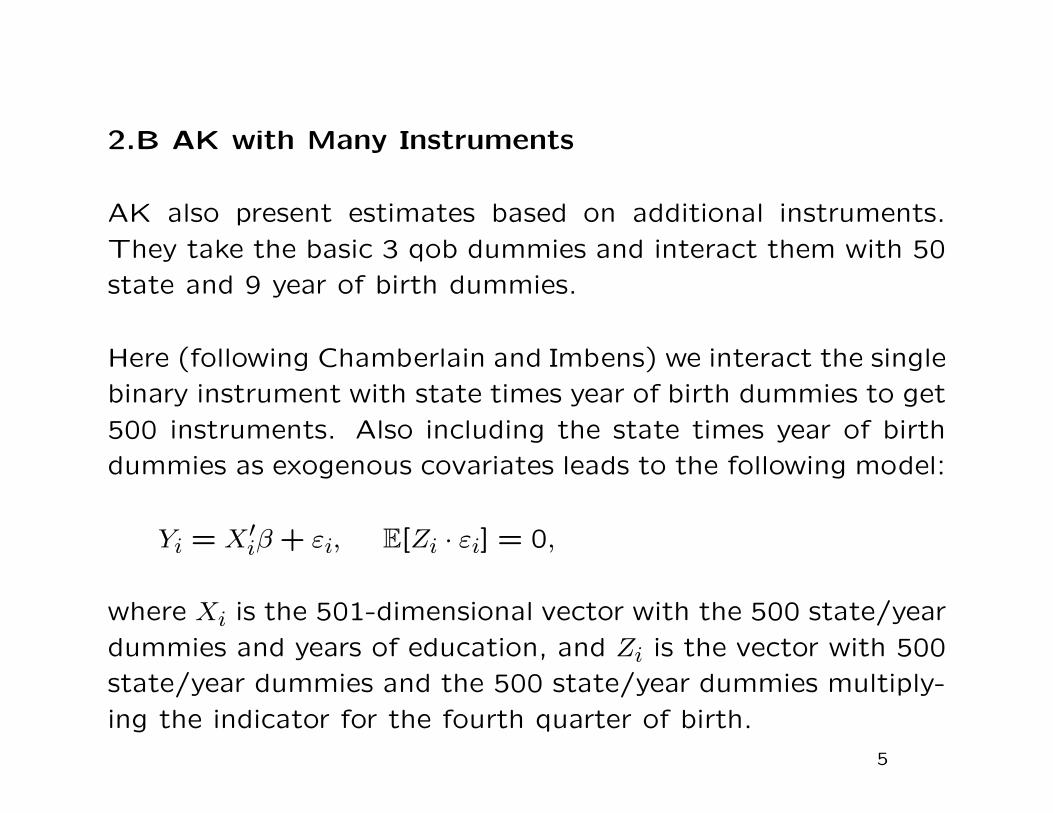

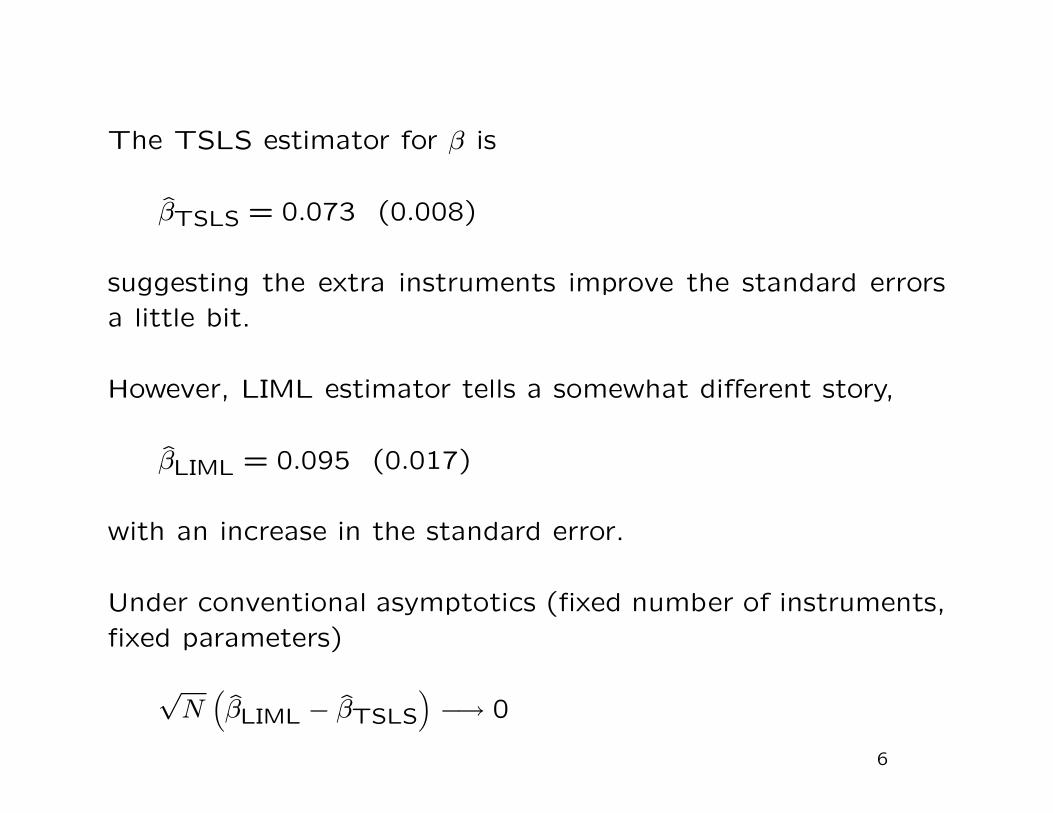

2. Application I: Imbens-Rubin-Sacerdote Lottery Study

IRS were interested in estimating the effect of unearned in-

come on economic behavior including effects on labor supply,

consumption and savings.

Those effects are important to understand and improve design

of social security programs.

IRS surveyed individuals who had played and won large sums of

money in the lottery (“winners”). As a comparison group they

collected data on a second set of individuals who also played

the lottery but who had not won big prizes (the “losers”) .

5

Nt = 259 winners and Nc = 237 losers in the sample of N = 496

lottery players.

We know the year individuals played the lottery, the number of

tickets they typically bought, age, sex, education, and their so-

cial security earnings for the six years preceeding their winning.

(what else should we have asked for?)

We present averages and standard deviations for the full sam-

ple, t-statistics for the null hypothesis of equal means in the

two groups, and the normalized differences in the means.

6

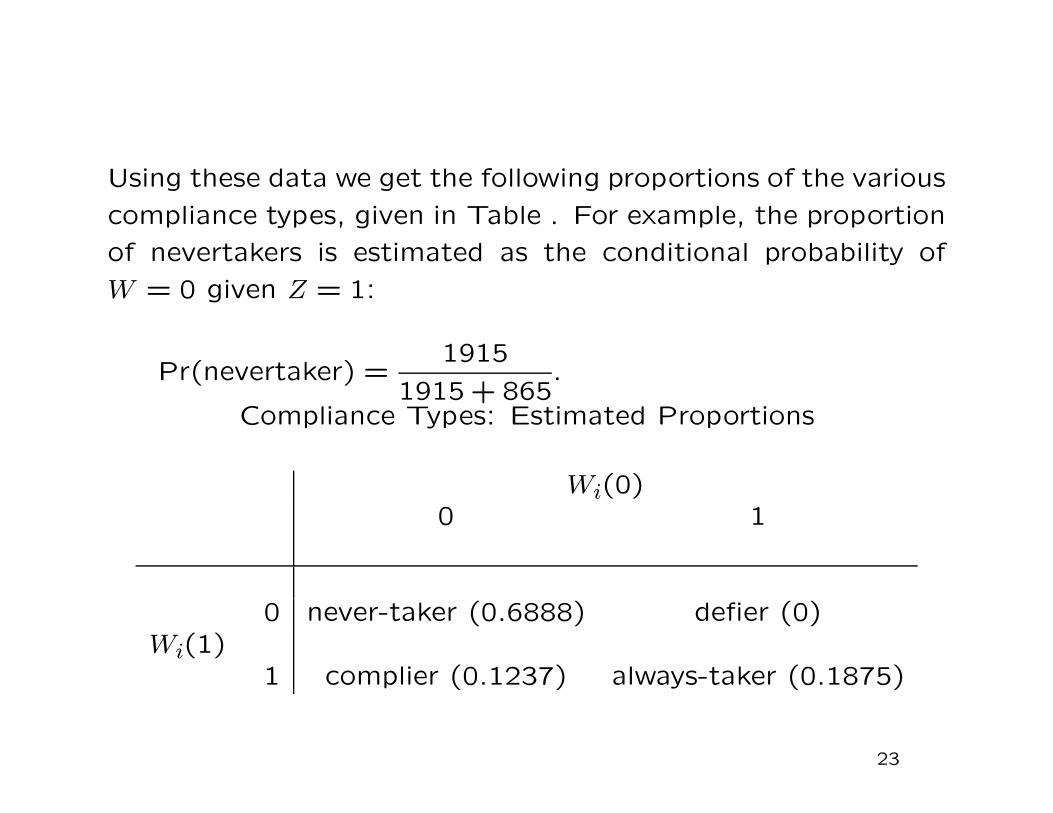

Normalized Difference in Covariates

Xc =1

Nc

∑

i:Wi=0

Xi S2c =

1

Nc − 1

∑

i:Wi=0

(

Xi − Xc

)2

Xt =1

Nt

∑

i:Wi=1

Xi S2t =

1

Nt − 1

∑

i:Wi=1

(

Xi − Xt

)2

Normalized difference:

nd =Xt − Xc

√

(S2c + S2

t )/2

More relevant for assessing balance than the t-statistic

t =Xt − Xc

√

S2c /Nc + S2

t /Nt

7

Summary Statistics Lottery Sample

Variable All Losers WinnersN=496 Nt=259 Nc=237 Norm.

mean (s.d.) mean mean [t-stat] Dif.

Year Won 6.23 1.18 6.38 6.06 -3.0 -0.27# Tickets 3.33 2.86 2.19 4.57 9.9 0.90Age 50.2 13.7 53.2 47.0 -5.2 -0.47Male 0.63 0.48 0.67 0.58 -2.1 -0.19Education 13.73 2.20 14.43 12.97 -7.8 -0.70Working Then 0.78 0.41 0.77 0.80 0.9 0.08Earn Y -6 13.8 13.4 15.6 12.0 -3.1 -0.27...Earn Y -1 16.3 15.7 18.0 14.5 -2.5 -0.23Pos Earn Y-6 0.69 0.46 0.69 0.70 0.3 0.03...Pos Earn Y-1 0.71 0.45 0.69 0.74 1.2 0.10

8

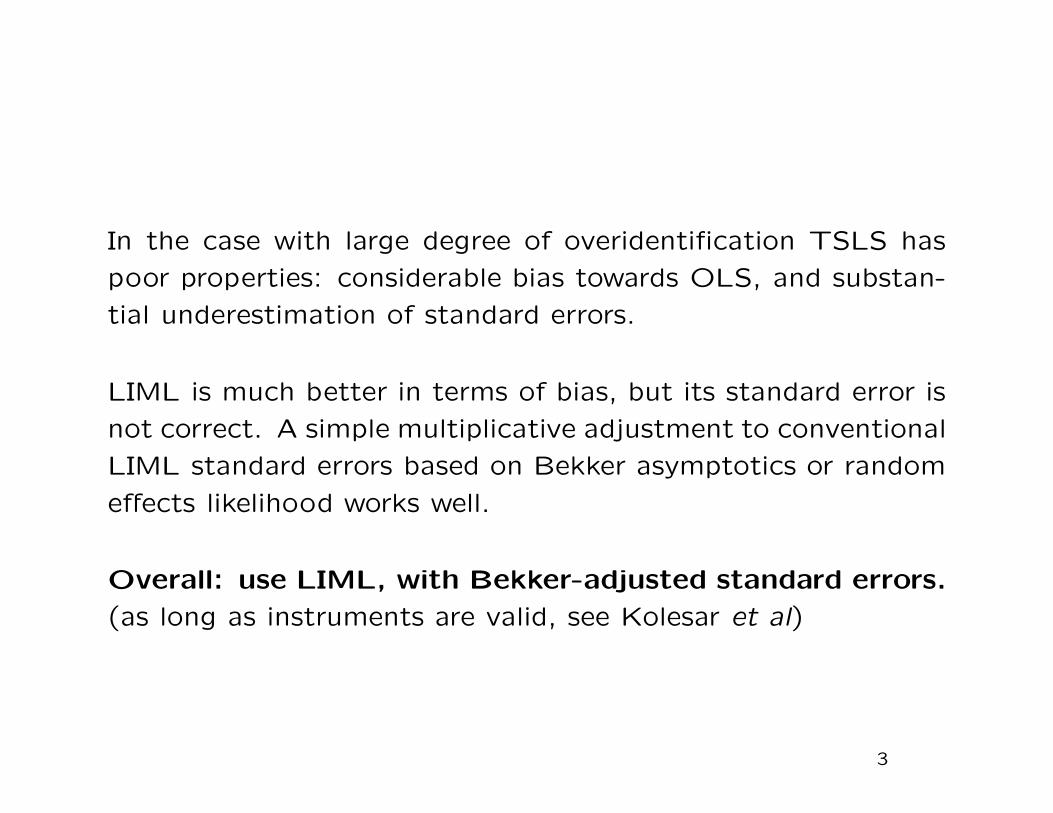

There are substantial differences between the two groups, in-

cluding in pre-winning earnings and the number of lottery tick-

ets bought. This suggests that simple regression methods will

not necessarily be adequate for removing the biases associated

with the differences in covariates.

Where do these differences come from?

• People buying more tickets are more likely to win.

• Nonresponse may differ by prize and individual characteris-

tics (including labor income)

Is unconfoundedness plausible?

9

Application II: Lalonde Study

Lalonde (1986) analyzed data from a randomized experiment

designed to evaluate the effect of a labor market program, the

National Supported Work (NSW) program.

Women with poor labor market histories.

Randomized evaluation shows average effect on earnings

≈ $2,000. (Substantial for participants).

Lalonde: could we have estimated this without random-

ized experiment?

10

Lalonde Evaluation of the Effectiveness of Observational

Methods to Recover Causal Effects:

Put aside experimental control group.

Constructs comparison sample from public use data set: Cur-

rent Population Survey (CPS), and Panel Study of Income

Dynamics (PSID).

Estimate average effect using CPS (or PSID) and trainees, as

observational study.

Is estimated effect close to experimental estimate?

Lalonde concludes that nonexperimental evaluations are

not credible. Influential conclusion in policy circles.

11

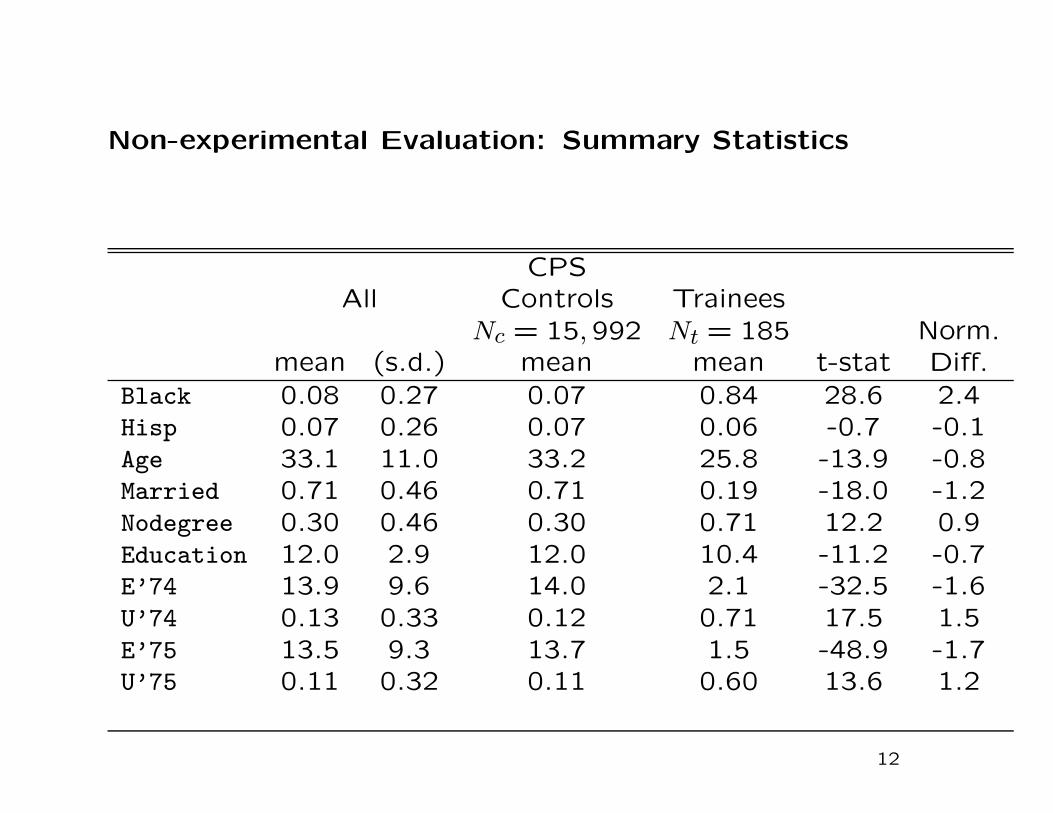

Non-experimental Evaluation: Summary Statistics

CPSAll Controls Trainees

Nc = 15,992 Nt = 185 Norm.mean (s.d.) mean mean t-stat Diff.

Black 0.08 0.27 0.07 0.84 28.6 2.4Hisp 0.07 0.26 0.07 0.06 -0.7 -0.1Age 33.1 11.0 33.2 25.8 -13.9 -0.8Married 0.71 0.46 0.71 0.19 -18.0 -1.2Nodegree 0.30 0.46 0.30 0.71 12.2 0.9Education 12.0 2.9 12.0 10.4 -11.2 -0.7E’74 13.9 9.6 14.0 2.1 -32.5 -1.6U’74 0.13 0.33 0.12 0.71 17.5 1.5E’75 13.5 9.3 13.7 1.5 -48.9 -1.7U’75 0.11 0.32 0.11 0.60 13.6 1.2

12

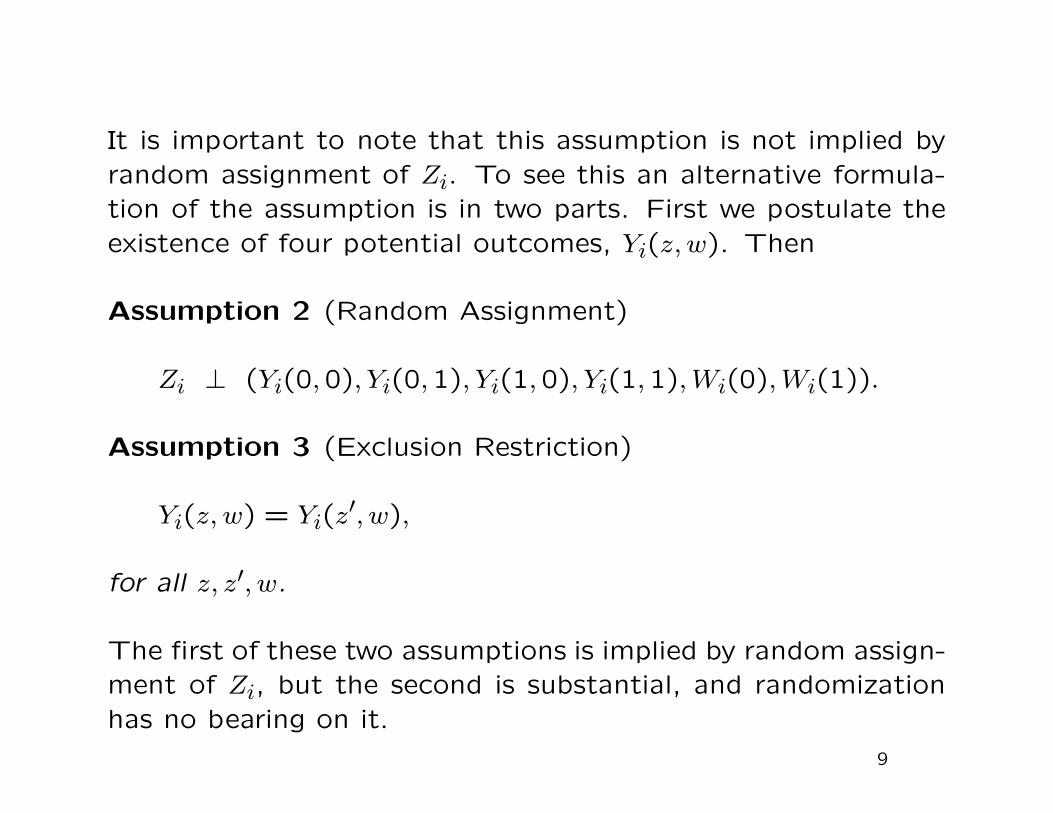

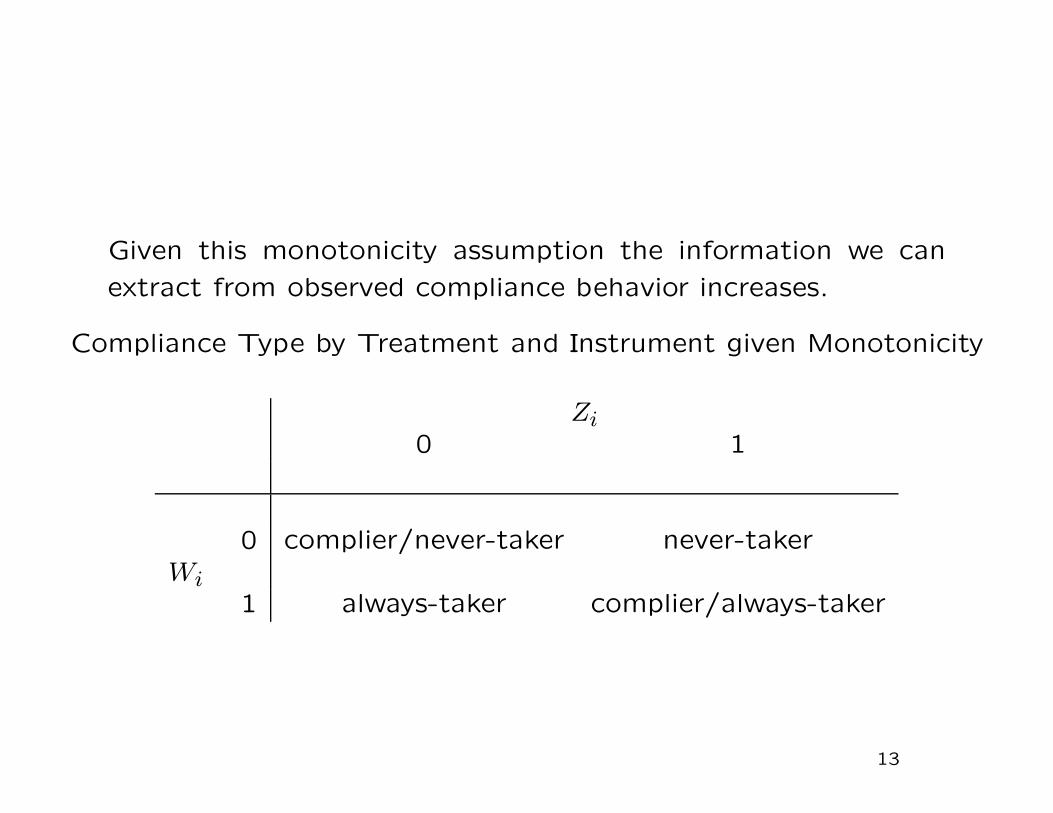

3. Assumptions

I. Unconfoundedness

Yi(0), Yi(1) ⊥ Wi

∣

∣

∣

∣

Xi.

This form due to Rosenbaum and Rubin (1983). Sometimes

referred to as “selection on observables”, or “exogeneity” but

those terms are not well defined.

Suppose

Yi(0) = α + β′Xi + εi, and Yi(1) = Yi(0) + τ,

then

Yi = α + τ · Wi + β′Xi + εi,

and unconfoundedness ⇐⇒ εi ⊥ Wi|Xi (exogeneity)

13

Motivation for Unconfoundedness

I. Descriptive statistics. After simple difference in mean out-comes by treatment status, compare average outcomes ad-justed for covariates.

II. Unconfoundedness follows from some economic models: Sup-pose individuals choose treatment w to max expected utility,equal to outcome minus cost ci, Yi(w) − ci · w, given a set ofcovariates X:

Wi = argmaxw E[Yi(w)|Xi]− ci · w.

Suppose that costs vary between individuals, indep. of poten-tial outcomes. Then (i) choices will vary between individualswith the same covariates, (ii) conditional on the covariates Xthe choice is independent of the potential outcomes.

III. Alternative: bounds (e.g., Manski, 1990)

IV Unconfoundedness is not testable

14

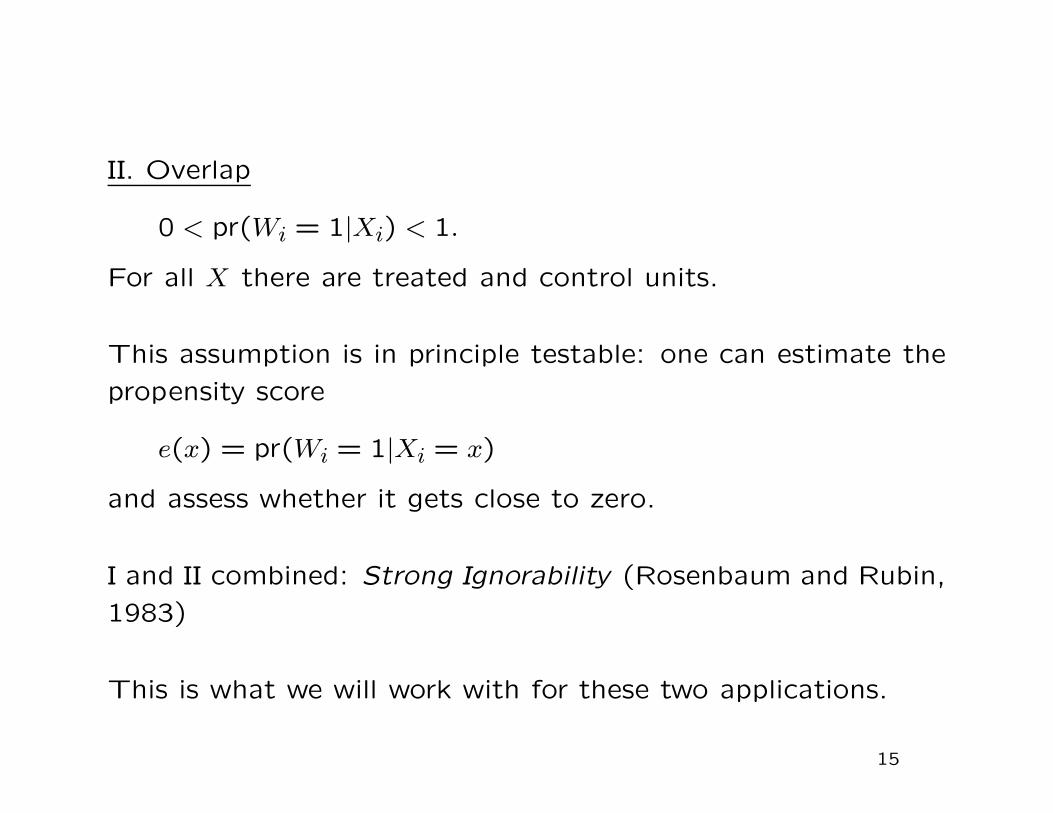

II. Overlap

0 < pr(Wi = 1|Xi) < 1.

For all X there are treated and control units.

This assumption is in principle testable: one can estimate the

propensity score

e(x) = pr(Wi = 1|Xi = x)

and assess whether it gets close to zero.

I and II combined: Strong Ignorability (Rosenbaum and Rubin,

1983)

This is what we will work with for these two applications.

15

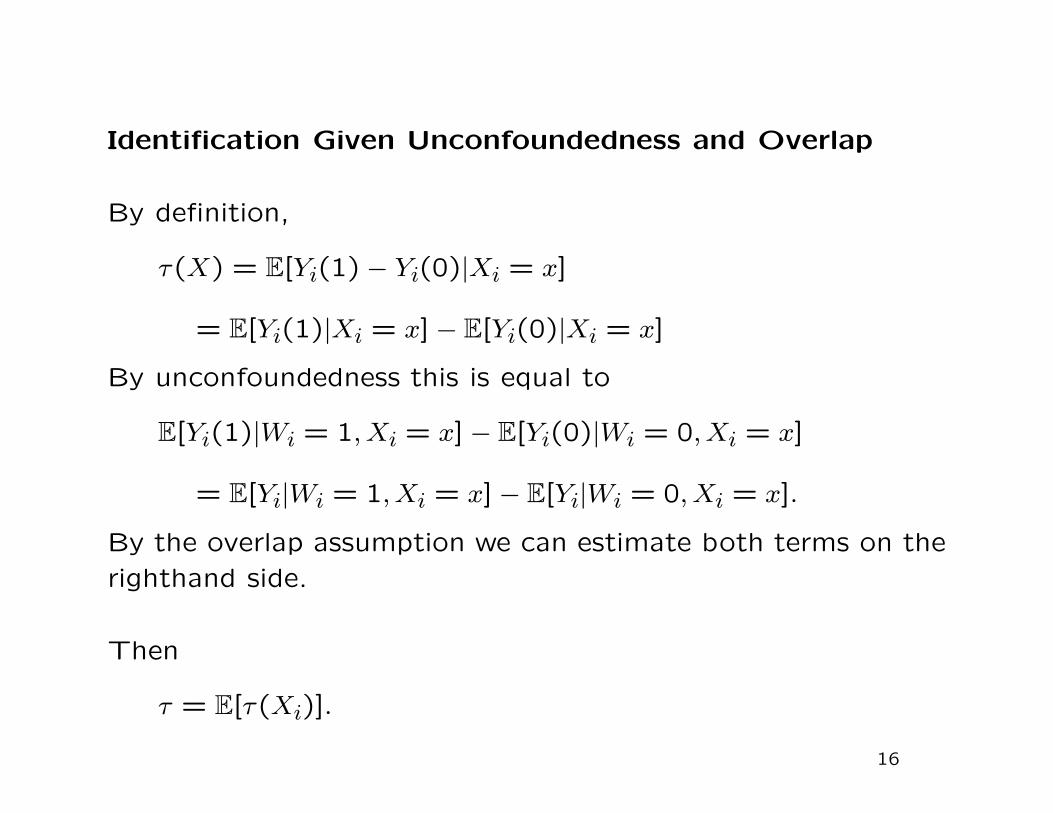

Identification Given Unconfoundedness and Overlap

By definition,

τ(X) = E[Yi(1) − Yi(0)|Xi = x]

= E[Yi(1)|Xi = x] − E[Yi(0)|Xi = x]

By unconfoundedness this is equal to

E[Yi(1)|Wi = 1, Xi = x] − E[Yi(0)|Wi = 0,Xi = x]

= E[Yi|Wi = 1,Xi = x] − E[Yi|Wi = 0, Xi = x].

By the overlap assumption we can estimate both terms on the

righthand side.

Then

τ = E[τ(Xi)].

16

4. Concern with regression estimators in cases with lim-

ited overlap in covariate distributions (distinct from plausi-

bility of unconfoundedness assumption)

Regression estimators are the most widely used methods for

estimating treatment effects

Sometimes simple linear regression:

Y obsi = β0 + τ · Wi + β1 · Xi + ε

Sometimes allowing for interactions:

Y obsi = β0 + τ · Wi + β1 · Xi + β2 · (Xi − X) · Wi + ε

What is the problem with these methods?

17

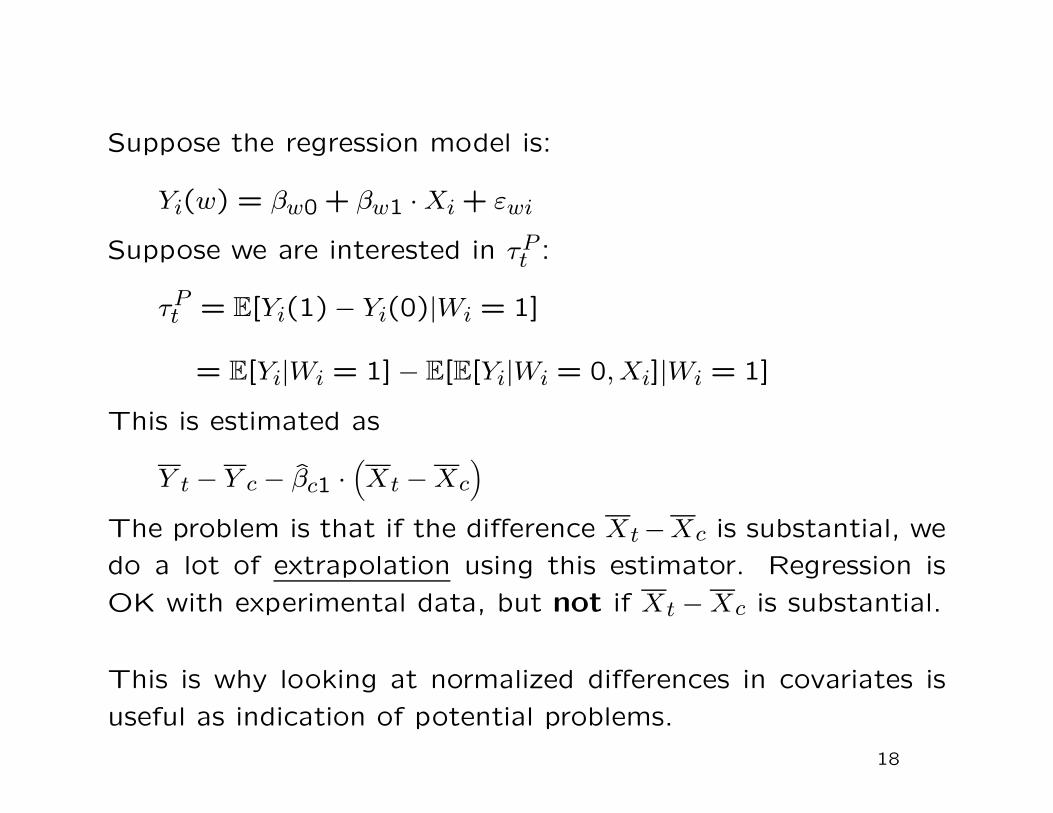

Suppose the regression model is:

Yi(w) = βw0 + βw1 · Xi + εwi

Suppose we are interested in τPt :

τPt = E[Yi(1)− Yi(0)|Wi = 1]

= E[Yi|Wi = 1] − E[E[Yi|Wi = 0, Xi]|Wi = 1]

This is estimated as

Y t − Y c − βc1 ·(

Xt − Xc

)

The problem is that if the difference Xt−Xc is substantial, we

do a lot of extrapolation using this estimator. Regression is

OK with experimental data, but not if Xt − Xc is substantial.

This is why looking at normalized differences in covariates is

useful as indication of potential problems.

18

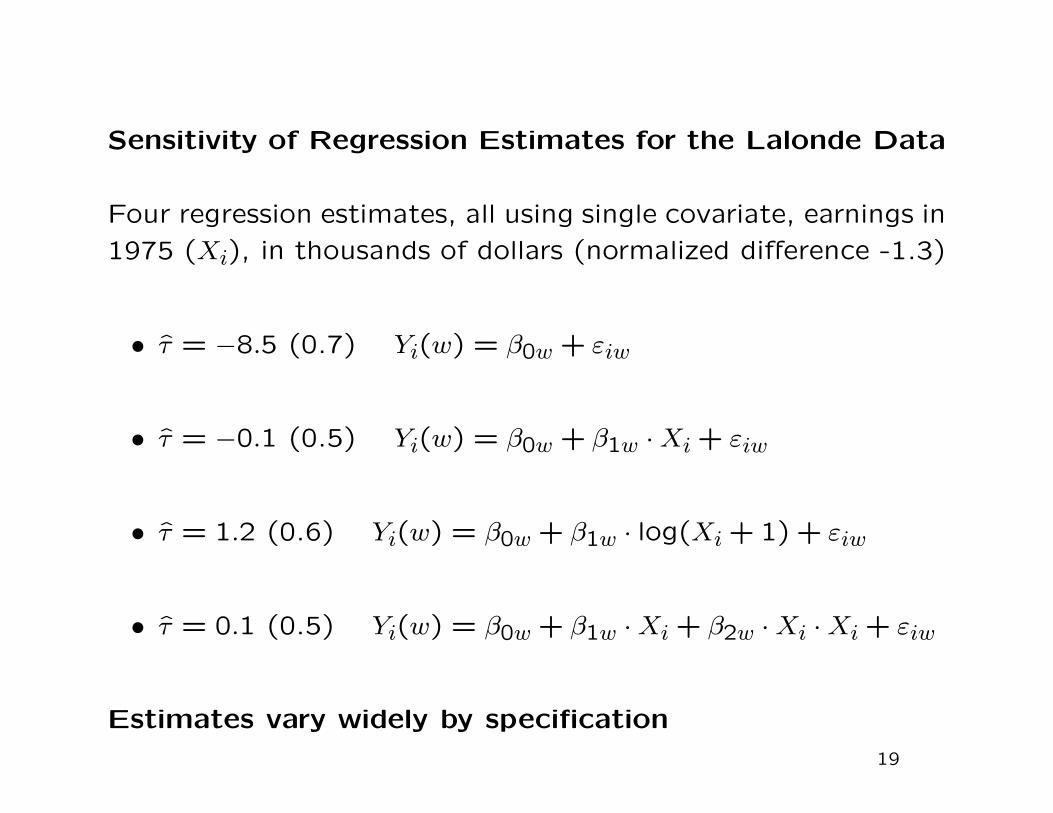

Sensitivity of Regression Estimates for the Lalonde Data

Four regression estimates, all using single covariate, earnings in

1975 (Xi), in thousands of dollars (normalized difference -1.3)

• τ = −8.5 (0.7) Yi(w) = β0w + εiw

• τ = −0.1 (0.5) Yi(w) = β0w + β1w · Xi + εiw

• τ = 1.2 (0.6) Yi(w) = β0w + β1w · log(Xi + 1) + εiw

• τ = 0.1 (0.5) Yi(w) = β0w + β1w · Xi + β2w · Xi · Xi + εiw

Estimates vary widely by specification

19

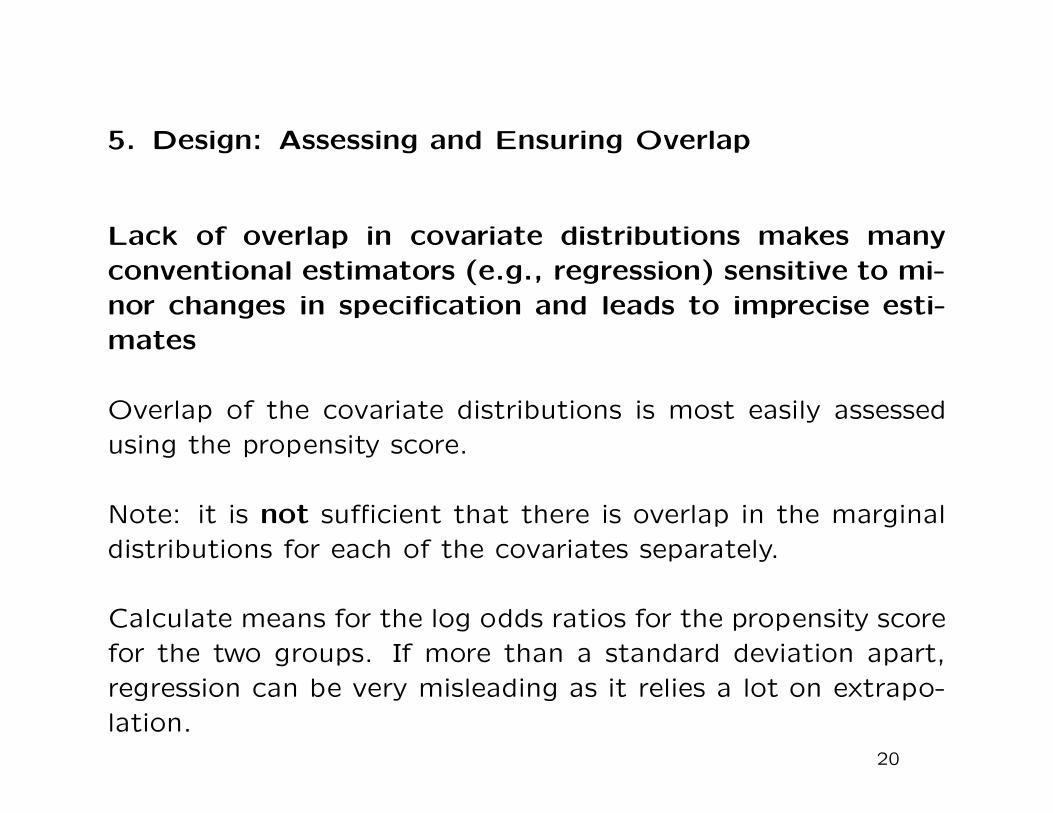

5. Design: Assessing and Ensuring Overlap

Lack of overlap in covariate distributions makes many

conventional estimators (e.g., regression) sensitive to mi-

nor changes in specification and leads to imprecise esti-

mates

Overlap of the covariate distributions is most easily assessed

using the propensity score.

Note: it is not sufficient that there is overlap in the marginal

distributions for each of the covariates separately.

Calculate means for the log odds ratios for the propensity score

for the two groups. If more than a standard deviation apart,

regression can be very misleading as it relies a lot on extrapo-

lation.

20

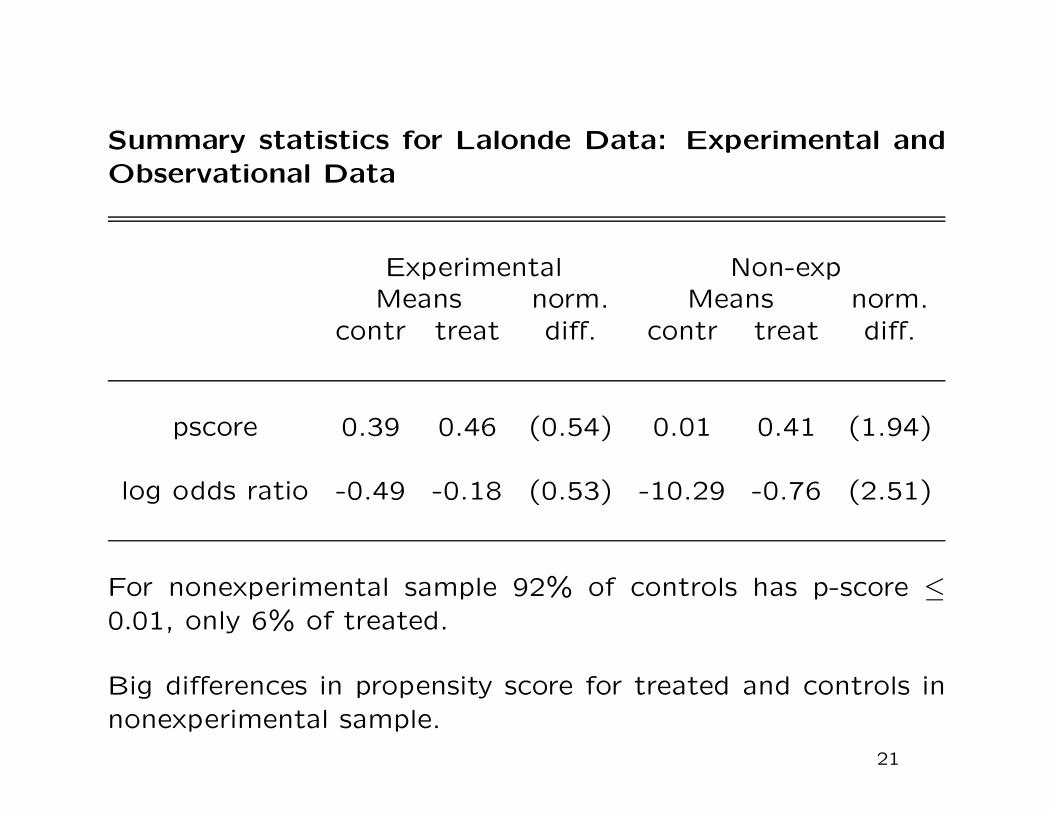

Summary statistics for Lalonde Data: Experimental and

Observational Data

Experimental Non-expMeans norm. Means norm.

contr treat diff. contr treat diff.

pscore 0.39 0.46 (0.54) 0.01 0.41 (1.94)

log odds ratio -0.49 -0.18 (0.53) -10.29 -0.76 (2.51)

For nonexperimental sample 92% of controls has p-score ≤

0.01, only 6% of treated.

Big differences in propensity score for treated and controls in

nonexperimental sample.

21

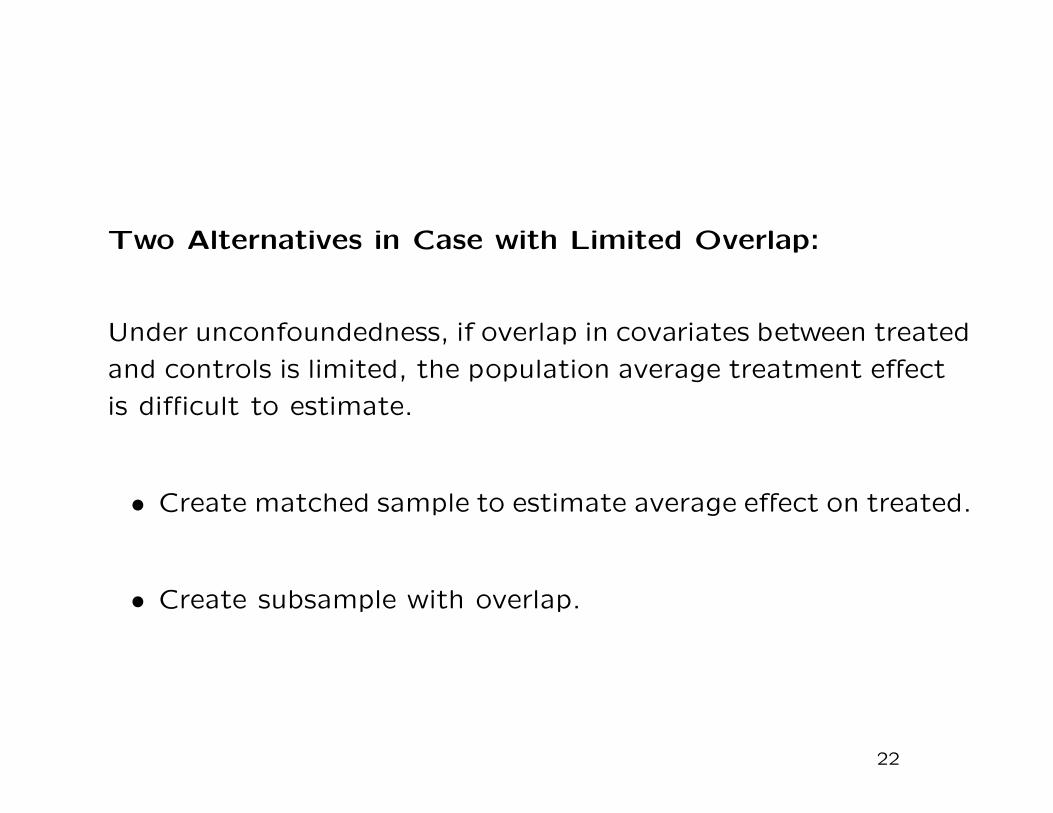

Two Alternatives in Case with Limited Overlap:

Under unconfoundedness, if overlap in covariates between treated

and controls is limited, the population average treatment effect

is difficult to estimate.

• Create matched sample to estimate average effect on treated.

• Create subsample with overlap.

22

5.A Alternative I for Creating Balanced Sample: MatchedSample

Focus on average effect for treated. (e.g., Lalonde data):

E[Yi(1)− Yi(0)|Wi = 1]

Note: the focus is not on estimation of treatment effects yet.We first create a sample with more balance.

match on propensity score (better here than matching onall covariates) and order treated observations by decreasingpropensity score

First match the treated observation with the highest value ofthe propensity score to the closest control. Go down the listof treated units till all are matched to a unique control (noreplacement) Now analyse the sample ignoring the matchingstep. (do regression, do matching, do propensity score analy-sis)

23

Matching to Improve Balance

We first estimate the propensity score, using the 185 trainees

and 15,992 CPS controls.

Then we order the 185 trainees by the estimated propensity

score, the largest first.

Then, going down the list of trainees, we match each to the

nearest CPS control, in terms of the estimated propensity

score, without replacement.

Now we have a new data set with 185 treated and 185 matched

CPS controls.

Balance is much improved.

24

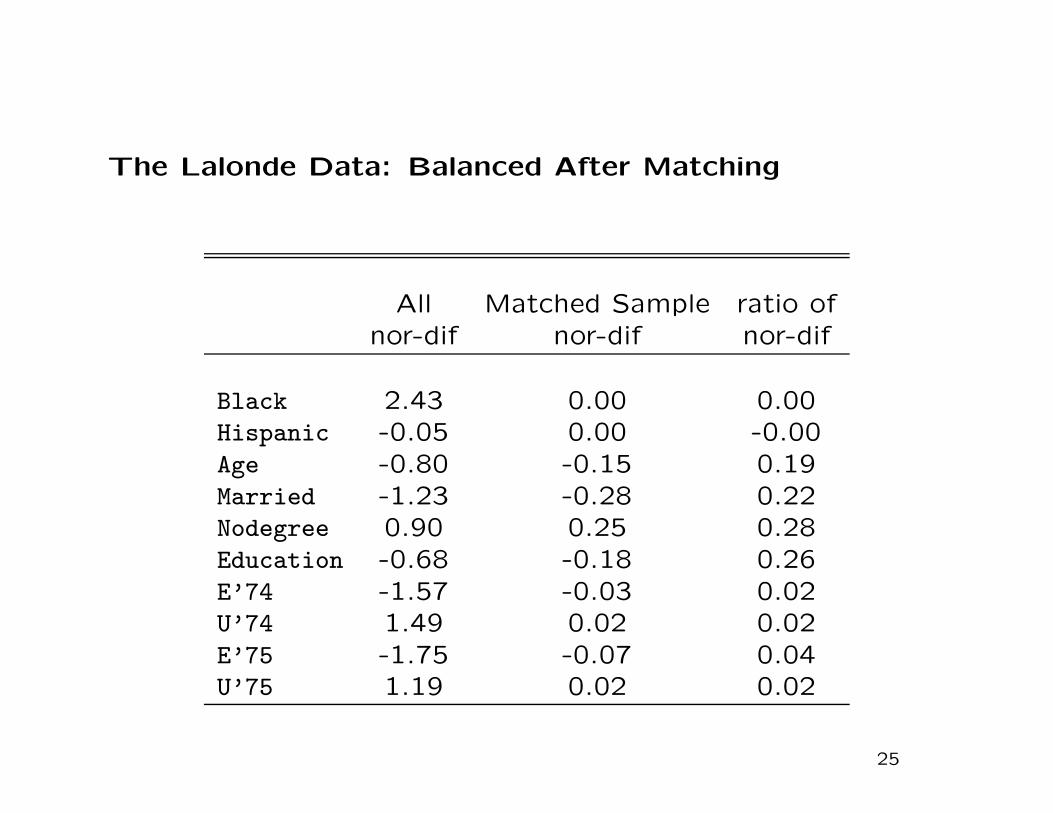

The Lalonde Data: Balanced After Matching

All Matched Sample ratio ofnor-dif nor-dif nor-dif

Black 2.43 0.00 0.00Hispanic -0.05 0.00 -0.00Age -0.80 -0.15 0.19Married -1.23 -0.28 0.22Nodegree 0.90 0.25 0.28Education -0.68 -0.18 0.26E’74 -1.57 -0.03 0.02U’74 1.49 0.02 0.02E’75 -1.75 -0.07 0.04U’75 1.19 0.02 0.02

25

• Matching leads to greatly improved balance.

• matching on propensity score generally works better here

than matching on individual covariates.

26

Aside: How did we estimate the propensity score?

• often researchers simply include all covariates linearly and no

second order terms.

• More attractive to select some of the covariates to be in-

cluded, and select some second order terms.

27

Specification Search

Given K covariates, we first choose a subset of the K covariates

for linear inclusion in the propensity score, and in a second

step we selection subset of all second order terms involving the

covariates that are selected in the first step.

Limitation: we only include linear, quadratic and interaction

terms, no third order terms (rarely substantitively important).

Sequential selection of covariates based on likelihood ratio test

and repeated estimation of logistic regression model. (see IR

book for details)

Other algorithms possible, e.g., lasso.

28

5.B Design Option II: Trimming the Sample

Traditional Estimand

τP = E[Yi(1)− Yi(0)] = E[τ(Xi)] (Population Average Treat-

ment Effect)

Problem:

τP can be difficult to estimate when there are values x ∈ X

such that e(x) close to zero or one.

• estimates are imprecise (high variance)

• estimates are sensitive to small changes in specification

29

Previous Solutions:

I Dehejia & Wahba (1999): Drop control units i with e(Xi) <

minj:Wj=1 e(Xj). Generalization (Lechner): discard all con-

trol units with e(Xi) smaller than kth smallest propensity score

among treated.

II Heckman, Ichimura, Todd (1998): Estimate f0(x) = f(X|W =

0), f1(x) = f(X|W = 1). Drop unit i if f0(Xi) ≤ q0 or

f1(Xi) ≤ q1, where q0 and q1 are quantiles of the distribution

of f0(X) and f1(X) respectively.

Both are ad hoc, and potentially sensitive to choice of threshold

(k for DW, q0 and q1 in HIT).

30

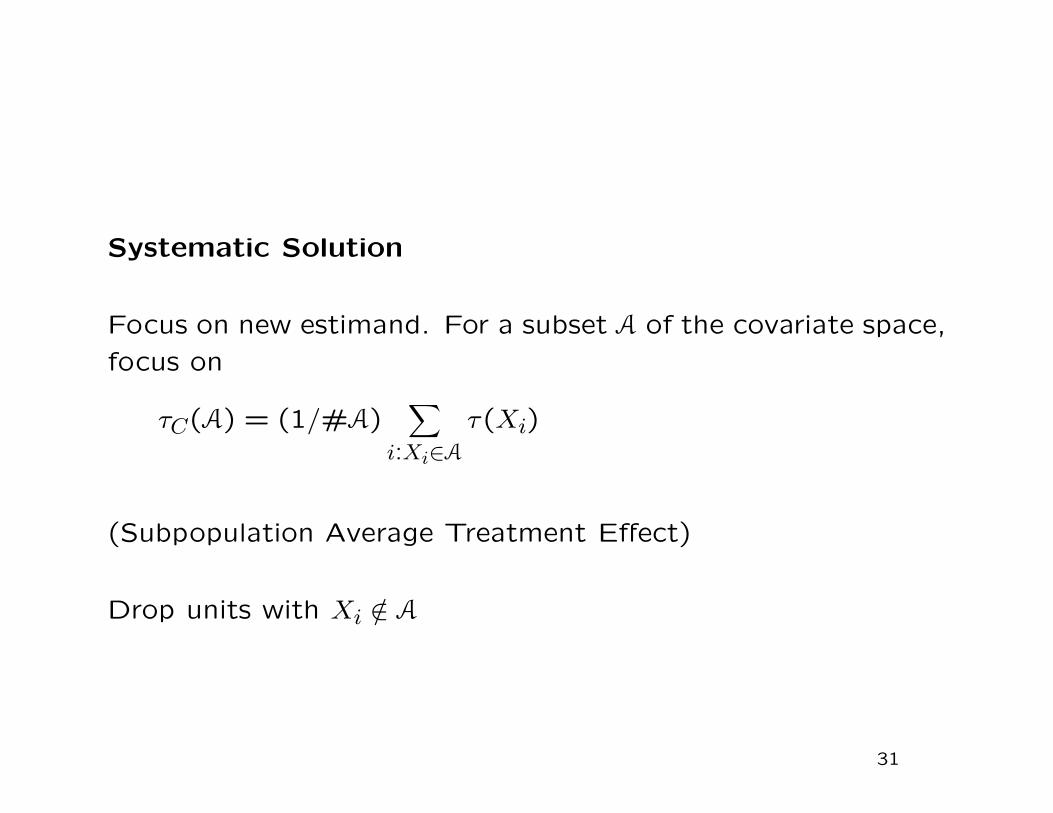

Systematic Solution

Focus on new estimand. For a subset A of the covariate space,

focus on

τC(A) = (1/#A)∑

i:Xi∈A

τ(Xi)

(Subpopulation Average Treatment Effect)

Drop units with Xi /∈ A

31

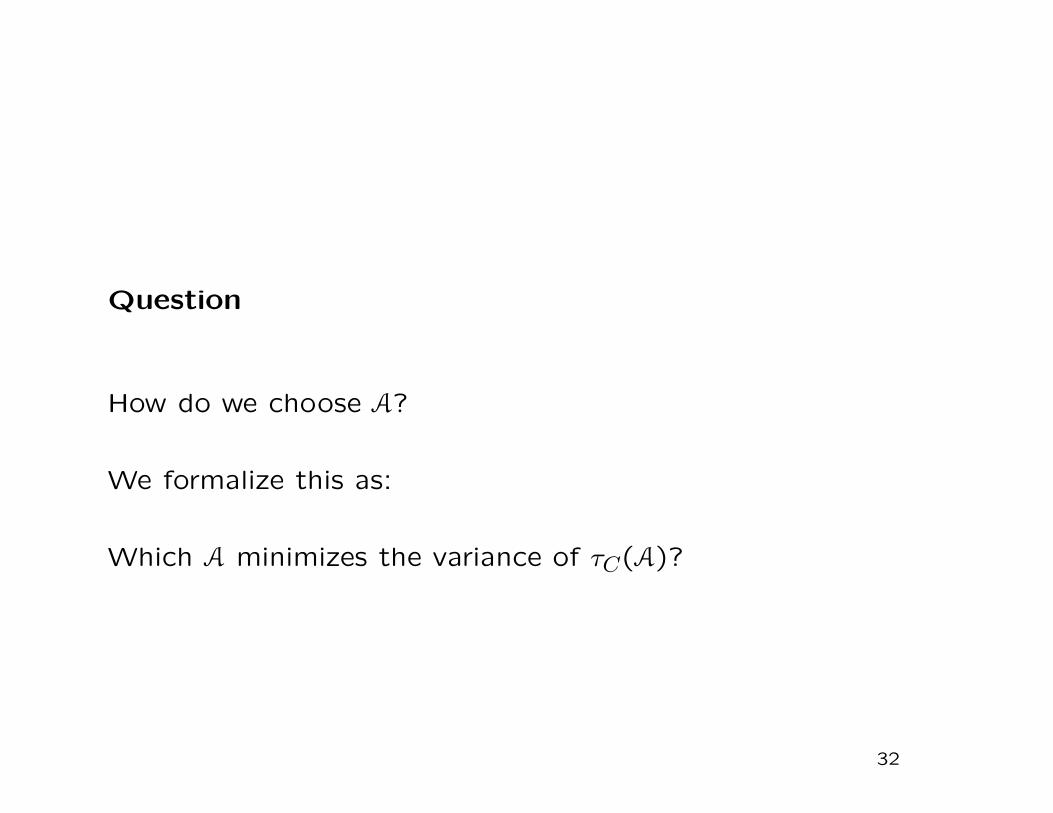

Question

How do we choose A?

We formalize this as:

Which A minimizes the variance of τC(A)?

32

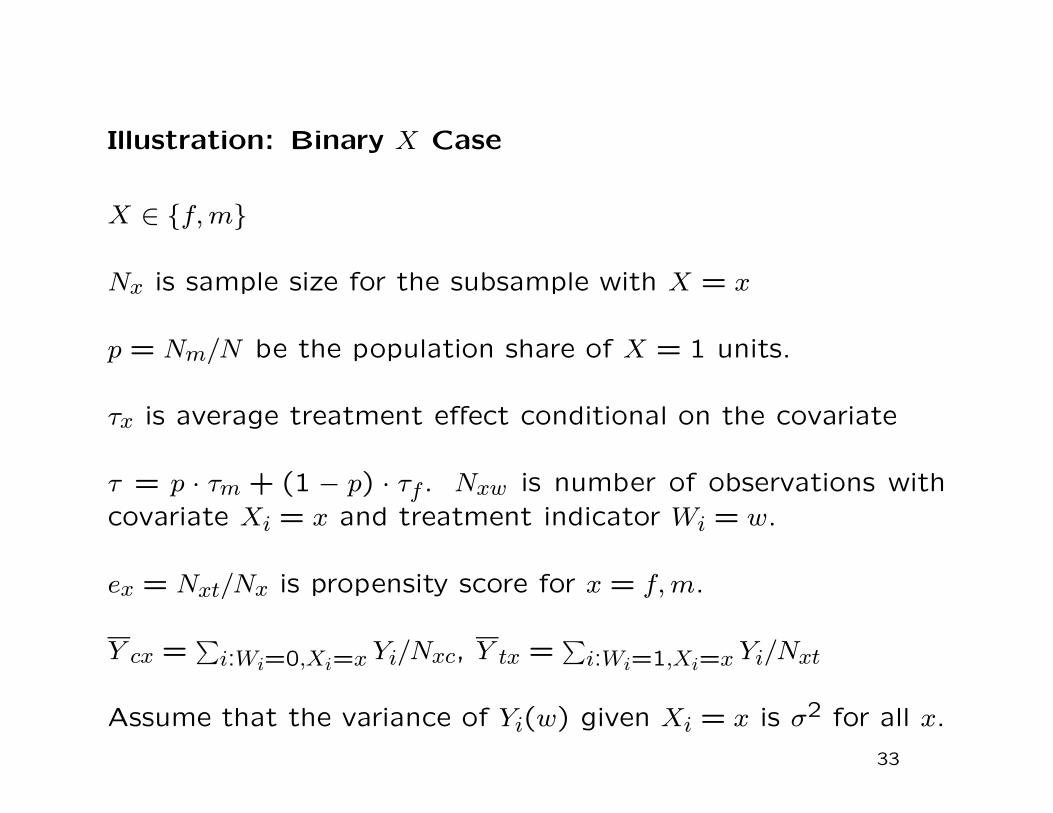

Illustration: Binary X Case

X ∈ f, m

Nx is sample size for the subsample with X = x

p = Nm/N be the population share of X = 1 units.

τx is average treatment effect conditional on the covariate

τ = p · τm + (1 − p) · τf . Nxw is number of observations with

covariate Xi = x and treatment indicator Wi = w.

ex = Nxt/Nx is propensity score for x = f, m.

Y cx =∑

i:Wi=0,Xi=x Yi/Nxc, Y tx =∑

i:Wi=1,Xi=x Yi/Nxt

Assume that the variance of Yi(w) given Xi = x is σ2 for all x.

33

τx = Y tx − Y cx

with variances

V (τf) =σ2

N · (1 − p)·

1

ef · (1 − ef),

V (τm) =σ2

N · p·

1

em · (1 − em),

The estimator for the population average treatment effect is

τ = p · τm + (1 − p) · τf .

with variance

V (τ) =σ2

N· E

[

1

eX · (1 − eX)

]

.

34

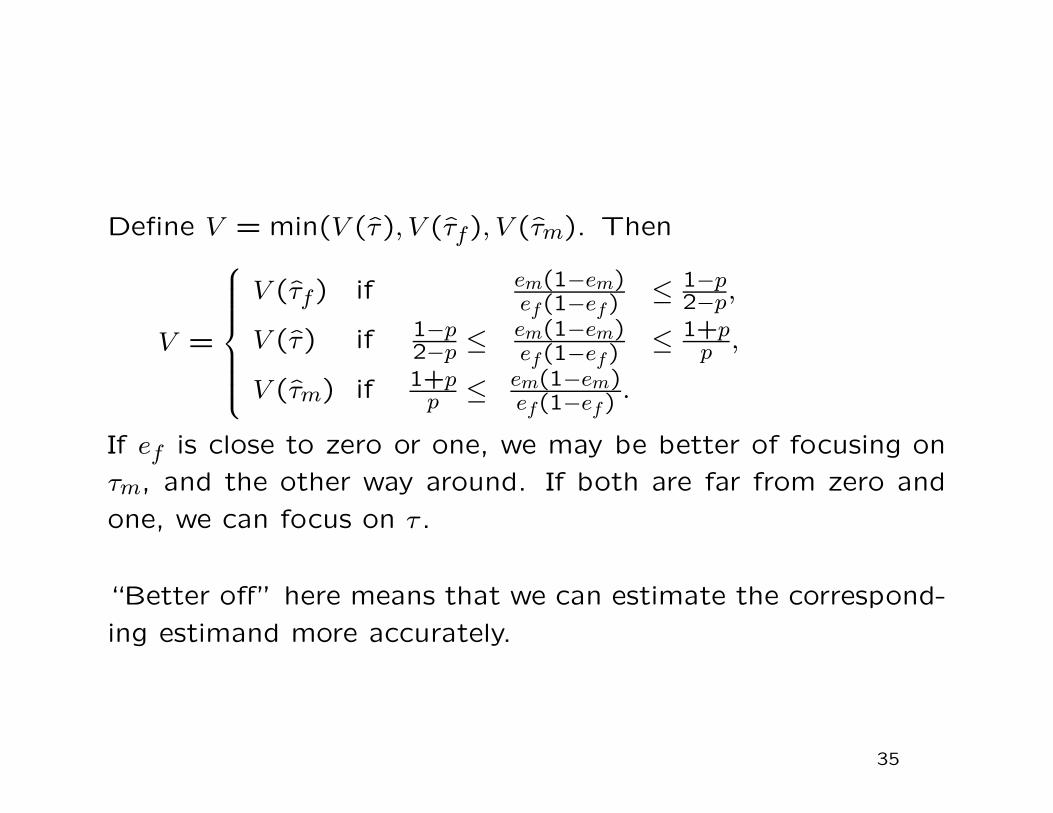

Define V = min(V (τ), V (τf), V (τm). Then

V =

V (τf) if em(1−em)ef(1−ef)

≤ 1−p2−p,

V (τ) if 1−p2−p ≤ em(1−em)

ef(1−ef)≤ 1+p

p ,

V (τm) if 1+pp ≤ em(1−em)

ef(1−ef).

If ef is close to zero or one, we may be better of focusing on

τm, and the other way around. If both are far from zero and

one, we can focus on τ .

“Better off” here means that we can estimate the correspond-

ing estimand more accurately.

35

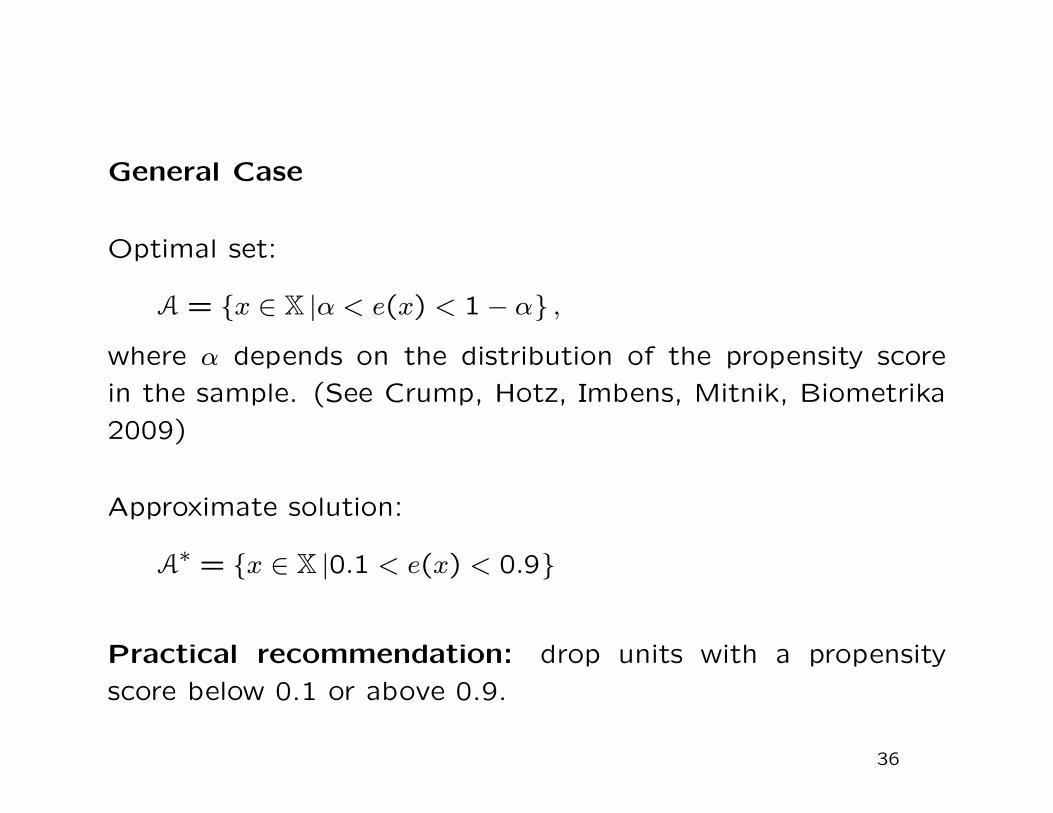

General Case

Optimal set:

A = x ∈ X |α < e(x) < 1 − α ,

where α depends on the distribution of the propensity score

in the sample. (See Crump, Hotz, Imbens, Mitnik, Biometrika

2009)

Approximate solution:

A∗ = x ∈ X |0.1 < e(x) < 0.9

Practical recommendation: drop units with a propensity

score below 0.1 or above 0.9.

36

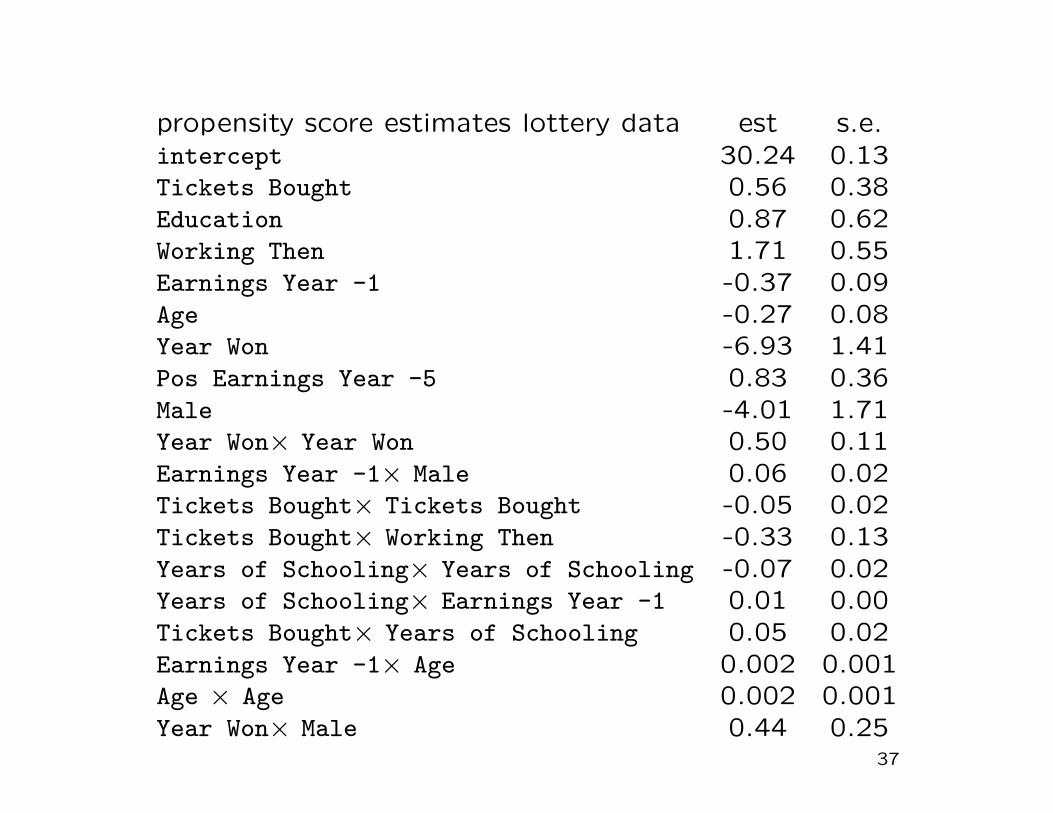

propensity score estimates lottery data est s.e.intercept 30.24 0.13Tickets Bought 0.56 0.38Education 0.87 0.62Working Then 1.71 0.55Earnings Year -1 -0.37 0.09Age -0.27 0.08Year Won -6.93 1.41Pos Earnings Year -5 0.83 0.36Male -4.01 1.71Year Won× Year Won 0.50 0.11Earnings Year -1× Male 0.06 0.02Tickets Bought× Tickets Bought -0.05 0.02Tickets Bought× Working Then -0.33 0.13Years of Schooling× Years of Schooling -0.07 0.02Years of Schooling× Earnings Year -1 0.01 0.00Tickets Bought× Years of Schooling 0.05 0.02Earnings Year -1× Age 0.002 0.001Age × Age 0.002 0.001Year Won× Male 0.44 0.25

37

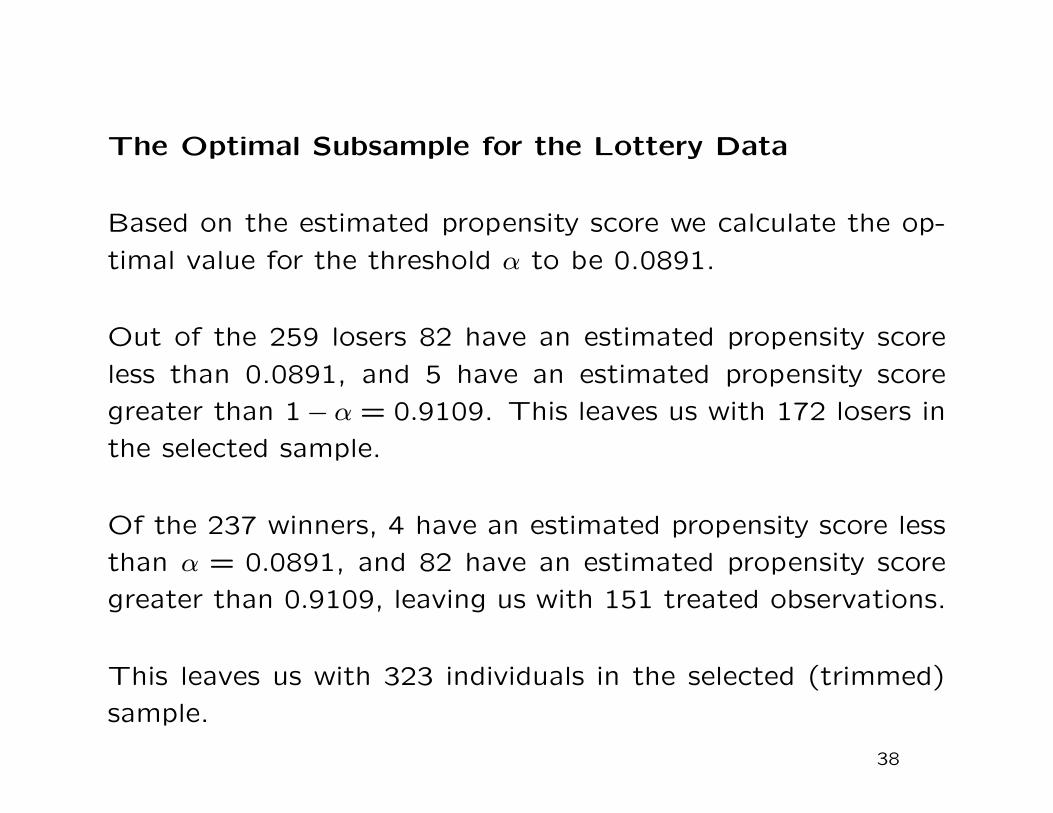

The Optimal Subsample for the Lottery Data

Based on the estimated propensity score we calculate the op-

timal value for the threshold α to be 0.0891.

Out of the 259 losers 82 have an estimated propensity score

less than 0.0891, and 5 have an estimated propensity score

greater than 1− α = 0.9109. This leaves us with 172 losers in

the selected sample.

Of the 237 winners, 4 have an estimated propensity score less

than α = 0.0891, and 82 have an estimated propensity score

greater than 0.9109, leaving us with 151 treated observations.

This leaves us with 323 individuals in the selected (trimmed)

sample.

38

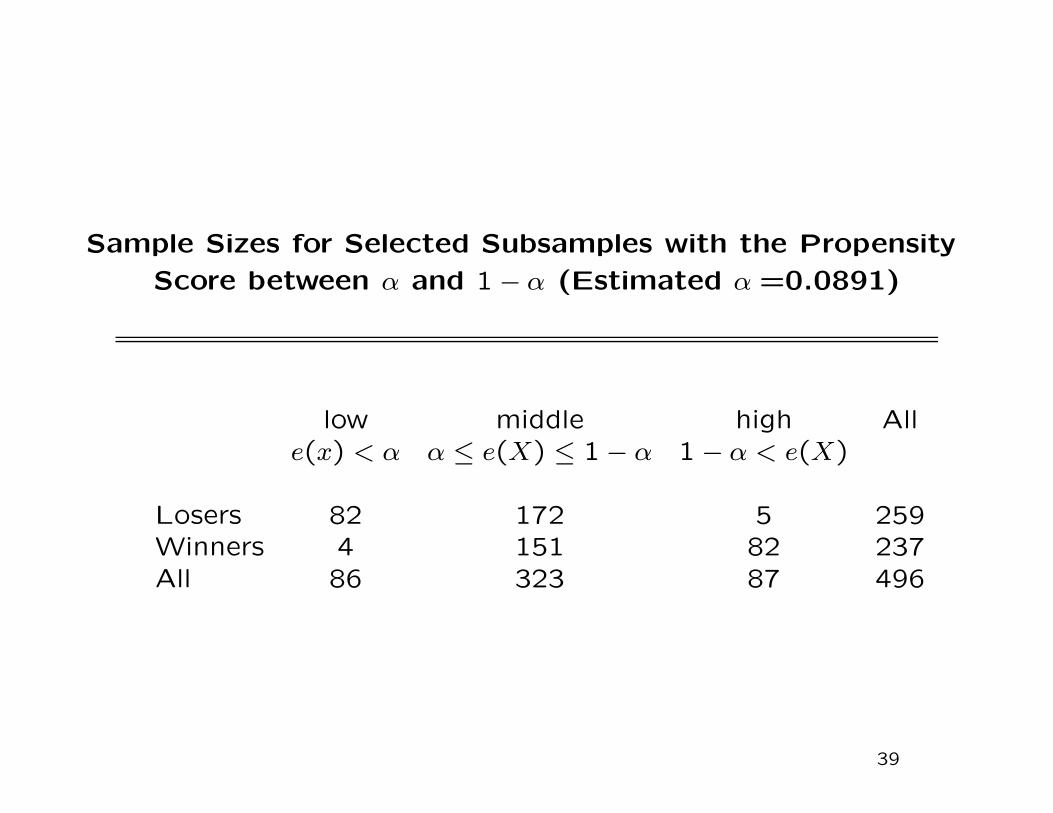

Sample Sizes for Selected Subsamples with the Propensity

Score between α and 1 − α (Estimated α =0.0891)

low middle high Alle(x) < α α ≤ e(X) ≤ 1 − α 1 − α < e(X)

Losers 82 172 5 259Winners 4 151 82 237All 86 323 87 496

39

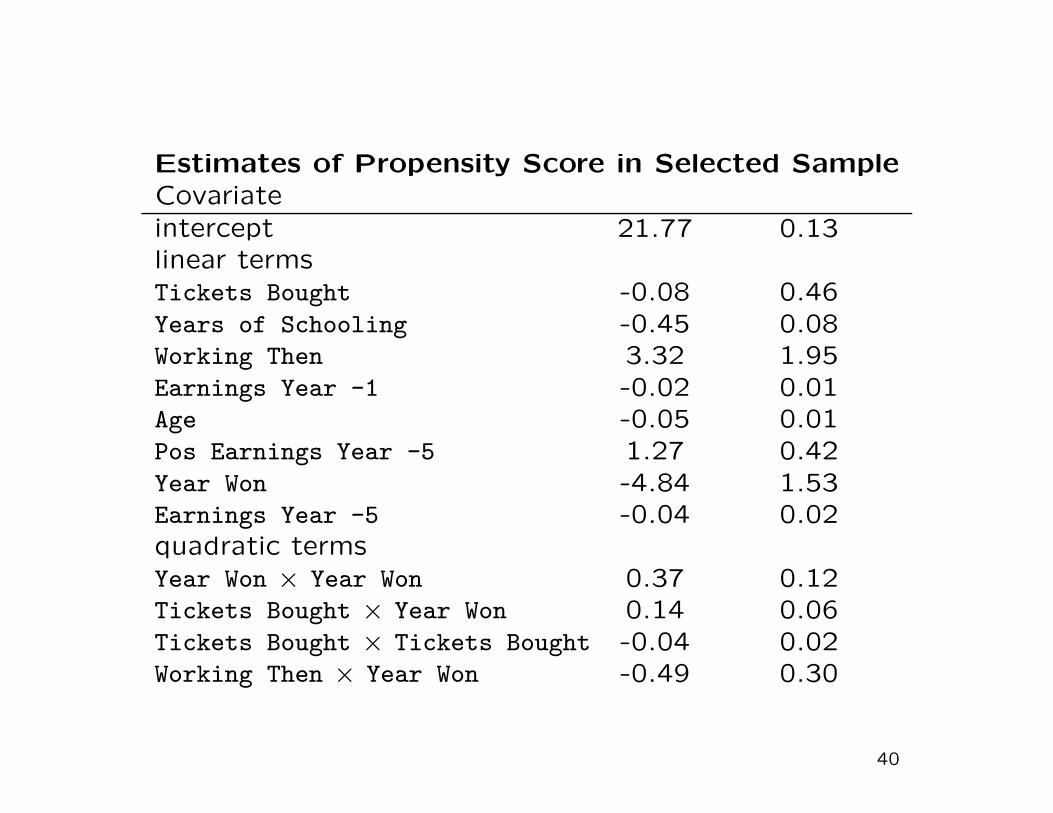

Estimates of Propensity Score in Selected SampleCovariate

intercept 21.77 0.13linear termsTickets Bought -0.08 0.46Years of Schooling -0.45 0.08Working Then 3.32 1.95Earnings Year -1 -0.02 0.01Age -0.05 0.01Pos Earnings Year -5 1.27 0.42Year Won -4.84 1.53Earnings Year -5 -0.04 0.02quadratic termsYear Won × Year Won 0.37 0.12Tickets Bought × Year Won 0.14 0.06Tickets Bought × Tickets Bought -0.04 0.02Working Then × Year Won -0.49 0.30

40

"Econometrics of Cross Section and Panel Data"

Lecture 2

Methods for Estimating Treatment Effects

Under Unconfoundedness, Part II

Guido Imbens

Cemmap Lectures, UCL, June 2014

6. Estimation of Average Treatment Effects

Focus on two specific methods:

• matching combined with regression within matched pairs.

• subclassification on the propensity score combined with re-

gression within the subclasses.

2

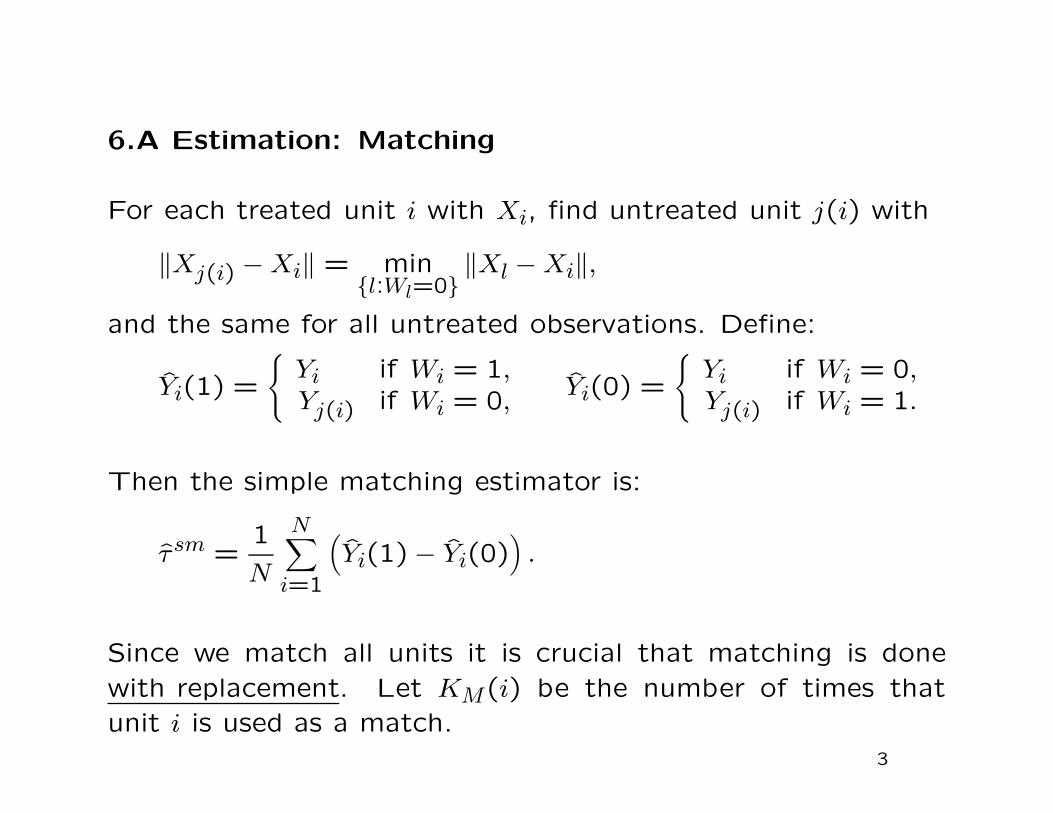

6.A Estimation: Matching

For each treated unit i with Xi, find untreated unit j(i) with

‖Xj(i) − Xi‖ = minl:Wl=0

‖Xl − Xi‖,

and the same for all untreated observations. Define:

Yi(1) =

Yi if Wi = 1,Yj(i) if Wi = 0,

Yi(0) =

Yi if Wi = 0,Yj(i) if Wi = 1.

Then the simple matching estimator is:

τsm =1

N

N∑

i=1

(Yi(1)− Yi(0)

).

Since we match all units it is crucial that matching is done

with replacement. Let KM(i) be the number of times that

unit i is used as a match.

3

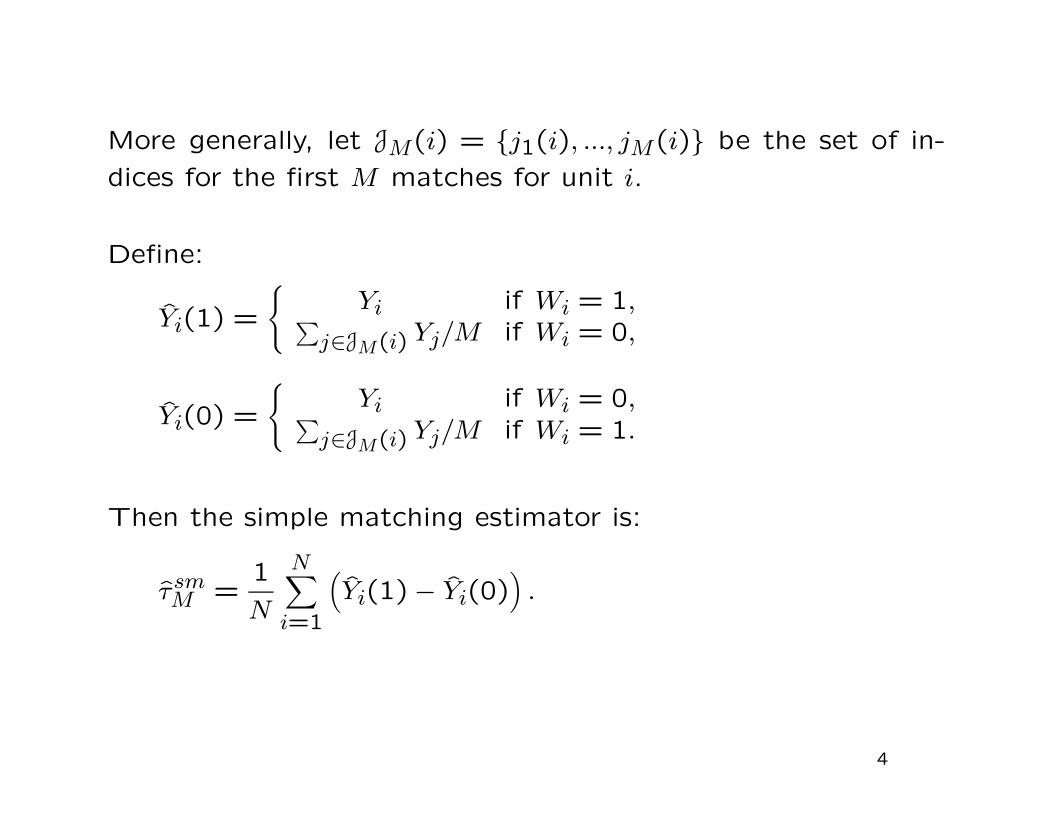

More generally, let JM(i) = j1(i), ..., jM(i) be the set of in-

dices for the first M matches for unit i.

Define:

Yi(1) =

Yi if Wi = 1,∑

j∈JM(i) Yj/M if Wi = 0,

Yi(0) =

Yi if Wi = 0,∑

j∈JM(i) Yj/M if Wi = 1.

Then the simple matching estimator is:

τsmM =

1

N

N∑

i=1

(Yi(1)− Yi(0)

).

4

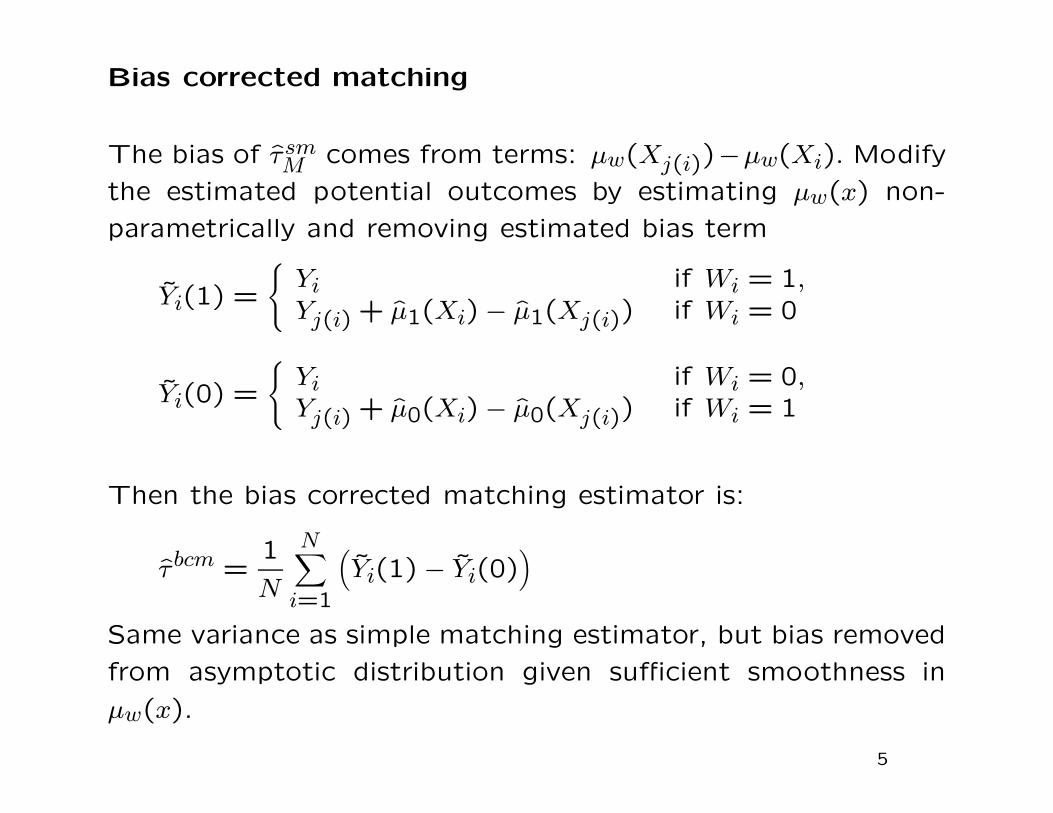

Bias corrected matching

The bias of τsmM comes from terms: µw(Xj(i))−µw(Xi). Modify

the estimated potential outcomes by estimating µw(x) non-

parametrically and removing estimated bias term

Yi(1) =

Yi if Wi = 1,Yj(i) + µ1(Xi) − µ1(Xj(i)) if Wi = 0

Yi(0) =

Yi if Wi = 0,Yj(i) + µ0(Xi) − µ0(Xj(i)) if Wi = 1

Then the bias corrected matching estimator is:

τ bcm =1

N

N∑

i=1

(Yi(1) − Yi(0)

)

Same variance as simple matching estimator, but bias removed

from asymptotic distribution given sufficient smoothness in

µw(x).

5

Variance of Matching Estimators

The variance of τsmM conditional on W and X, normalized by

the sample size N , is

1

N

N∑

i=1

(

1 +KM(i)

M

)2

· σ2Wi

(Xi).

6

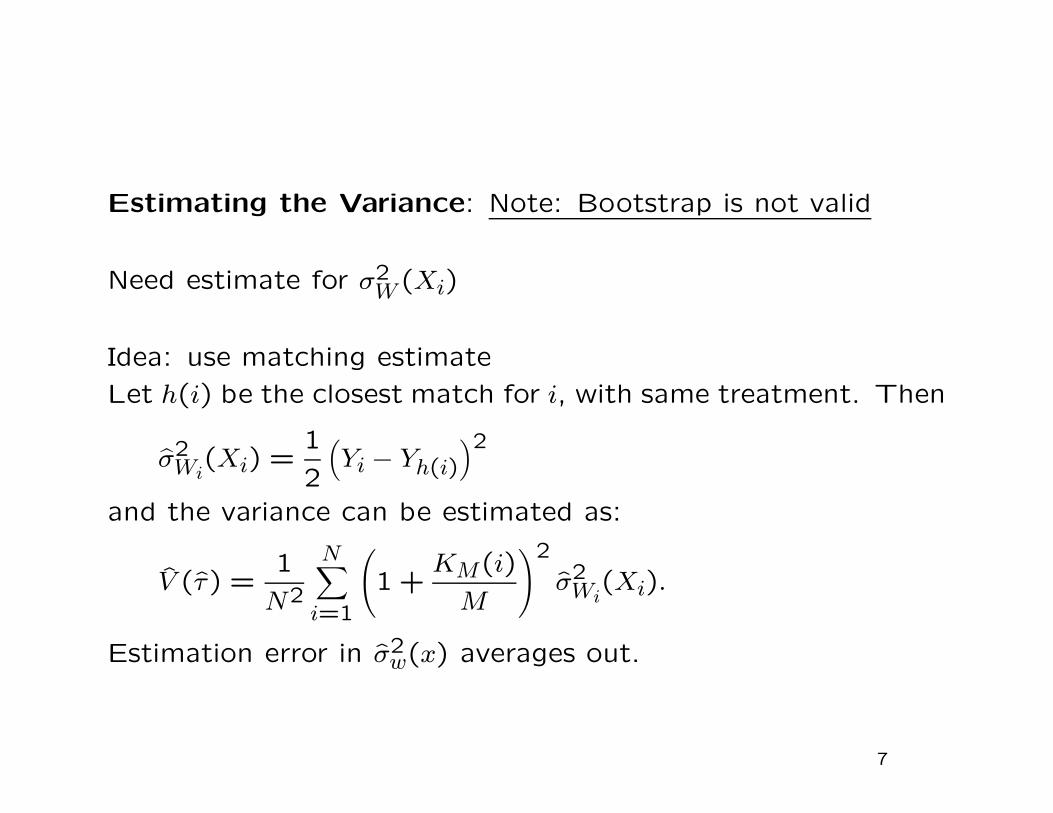

Estimating the Variance: Note: Bootstrap is not valid

Need estimate for σ2W (Xi)

Idea: use matching estimate

Let h(i) be the closest match for i, with same treatment. Then

σ2Wi

(Xi) =1

2

(Yi − Yh(i)

)2

and the variance can be estimated as:

V (τ) =1

N2

N∑

i=1

(

1 +KM(i)

M

)2

σ2Wi

(Xi).

Estimation error in σ2w(x) averages out.

7

Experimental and Non-experimental Estimates for the Lalonde Data

M = 1 M = 4 M = 16 M = 2490est (s.e.) est (s.e.) est (s.e.) est (s.e.)

Panel A: Experimental Datasimple 1.22 (0.84) 1.99 (0.74) 1.75 (0.74) 1.80 (0.67)bias-adj 1.16 (0.84) 1.84 (0.74) 1.54 (0.75) 1.72 (0.68)Linear Regression Estimatesdiff 1.79 (0.67)linear 1.72 (0.65)quadr 2.27 (0.73)

Panel B: Non-experimental Datasimple 2.07 (1.13) 1.62 (0.91) 0.47 (0.85) -15.20 (0.61)bias-adj 2.42 (1.13) 2.51 (0.90) 2.48 (0.83) 0.84 (0.63)Linear Regression Estimatesdiff -15.20 (0.66)linear 0.84 (0.86)quadr 3.26 (0.98)

8

Matching: Comments

• With experimental data all estimators give more or less the

same results.

• With nonexperimental data, the regression estimates per-

form terribly. Matching estimates perform much better.

• With no regression adjustment within matched pairs, match-

ing works ok with very few matches.

• Regression adjustment within matched pairs performs well

even with 4 or 16 matches.

9

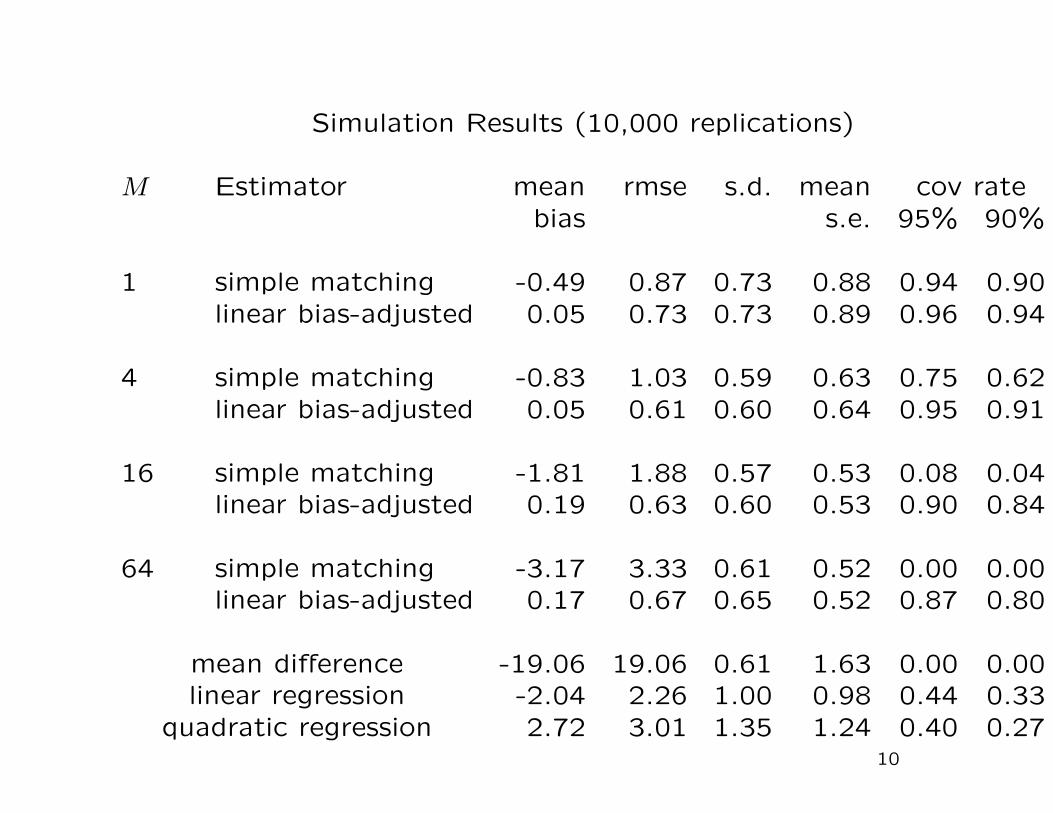

Simulation Results (10,000 replications)

M Estimator mean rmse s.d. mean cov ratebias s.e. 95% 90%

1 simple matching -0.49 0.87 0.73 0.88 0.94 0.90linear bias-adjusted 0.05 0.73 0.73 0.89 0.96 0.94

4 simple matching -0.83 1.03 0.59 0.63 0.75 0.62linear bias-adjusted 0.05 0.61 0.60 0.64 0.95 0.91

16 simple matching -1.81 1.88 0.57 0.53 0.08 0.04linear bias-adjusted 0.19 0.63 0.60 0.53 0.90 0.84

64 simple matching -3.17 3.33 0.61 0.52 0.00 0.00linear bias-adjusted 0.17 0.67 0.65 0.52 0.87 0.80

mean difference -19.06 19.06 0.61 1.63 0.00 0.00linear regression -2.04 2.26 1.00 0.98 0.44 0.33

quadratic regression 2.72 3.01 1.35 1.24 0.40 0.2710

Matching works fairly well

Bias addresses imbalance in covariates directly.

Regression within matched pairs is effective at removing

remaining bias and is recommended.

Implemented in stata, matlab.

11

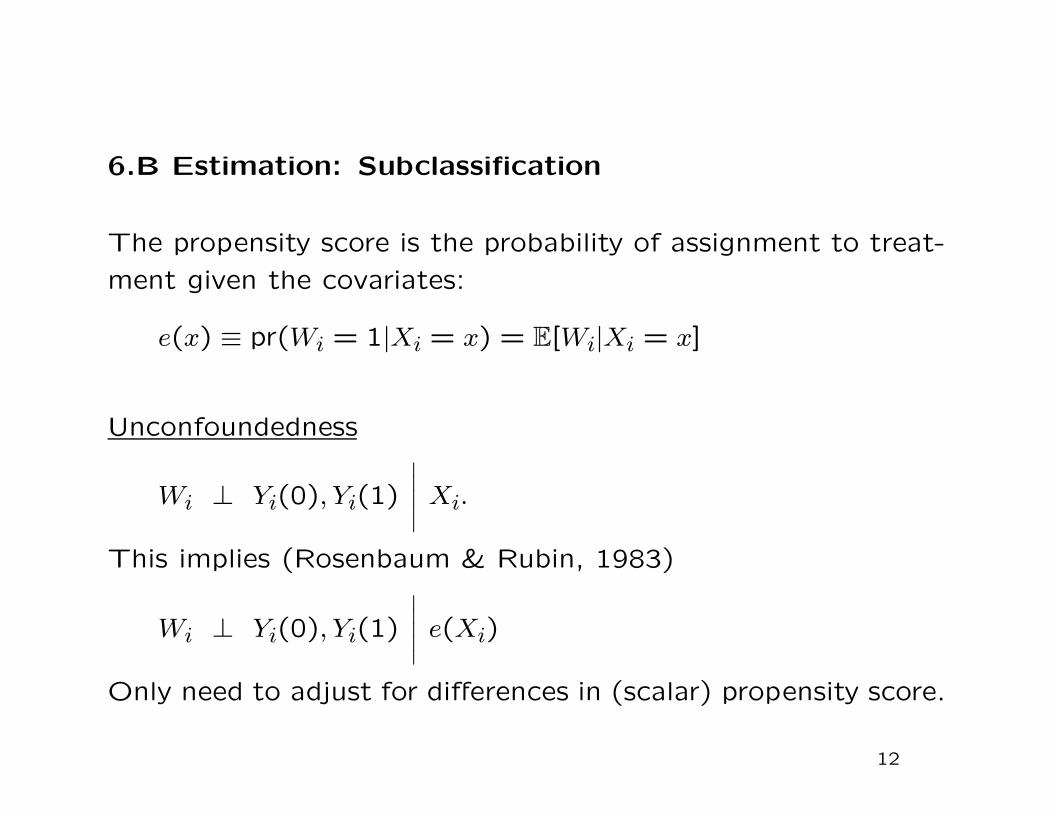

6.B Estimation: Subclassification

The propensity score is the probability of assignment to treat-

ment given the covariates:

e(x) ≡ pr(Wi = 1|Xi = x) = E[Wi|Xi = x]

Unconfoundedness

Wi ⊥ Yi(0), Yi(1)

∣∣∣∣∣ Xi.

This implies (Rosenbaum & Rubin, 1983)

Wi ⊥ Yi(0), Yi(1)

∣∣∣∣∣ e(Xi)

Only need to adjust for differences in (scalar) propensity score.

12

Implementation Using the Propensity Score

• Regression (compare to regression estimator with all covari-

ates)

Not recommended: not efficient (Hahn, 1998), functional

form is difficult to justify.

• Weighting on the Propensity Score

Exploit idea that

E

[Wi · Yi

e(Xi)

]

= E[Yi(1)] E

[(1 − Wi) · Yi

1 − e(Xi)

]

= E[Yi(0)]

Not recommended: sensitive to parametric form of propensity

score.

13

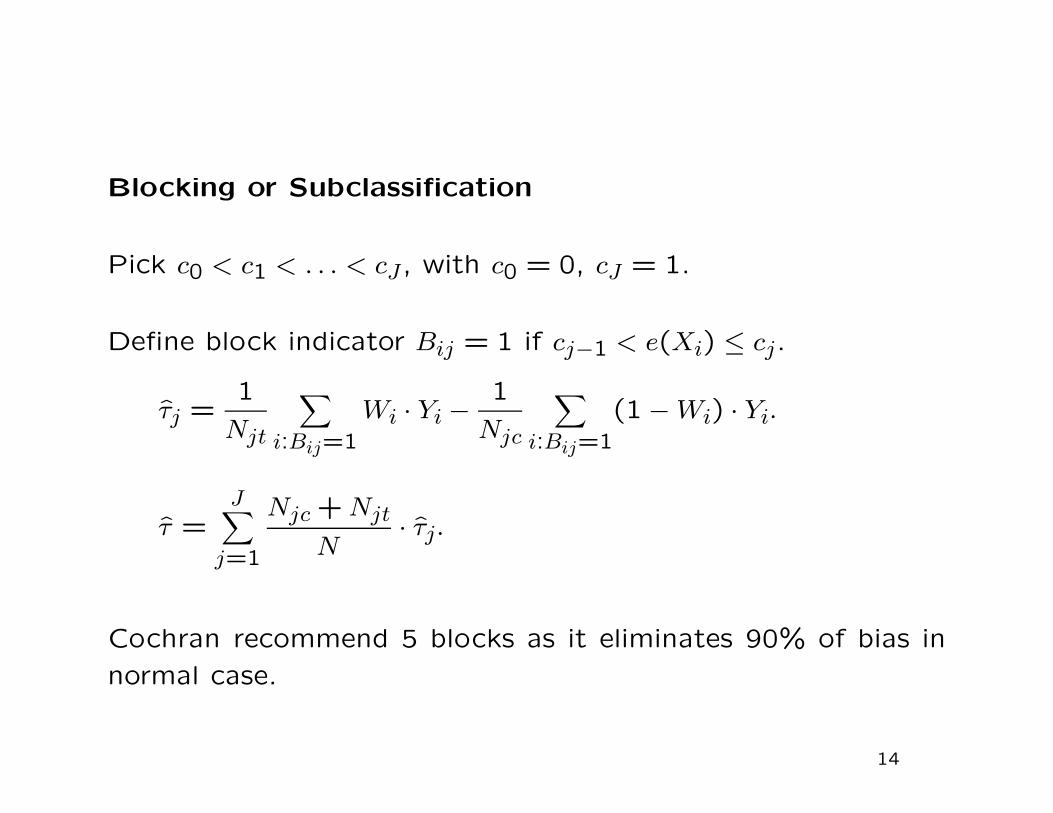

Blocking or Subclassification

Pick c0 < c1 < . . . < cJ , with c0 = 0, cJ = 1.

Define block indicator Bij = 1 if cj−1 < e(Xi) ≤ cj.

τj =1

Njt

∑

i:Bij=1

Wi · Yi −1

Njc

∑

i:Bij=1

(1 − Wi) · Yi.

τ =J∑

j=1

Njc + Njt

N· τj.

Cochran recommend 5 blocks as it eliminates 90% of bias in

normal case.

14

Lottery Data: Normalized Diffs in Covariates after SubclassificationFull Selected 2 Subclasses 5 Subclasses

Year Won -0.27 -0.06 0.03 -0.07Tickets Bought 0.90 0.51 -0.18 -0.07Age -0.47 -0.08 0.02 -0.04Male -0.19 -0.11 0.10 0.14Years of Schooling -0.70 -0.47 0.19 0.10Working Then 0.08 0.03 -0.03 -0.02Earnings Year -6 -0.27 -0.19 0.10 0.03...Earnings Year -1 -0.23 -0.19 0.02 -0.00Pos Earnings Year -6 0.03 -0.00 0.08 0.08...Pos Earnings Year -1 0.10 -0.01 0.04 0.07

15

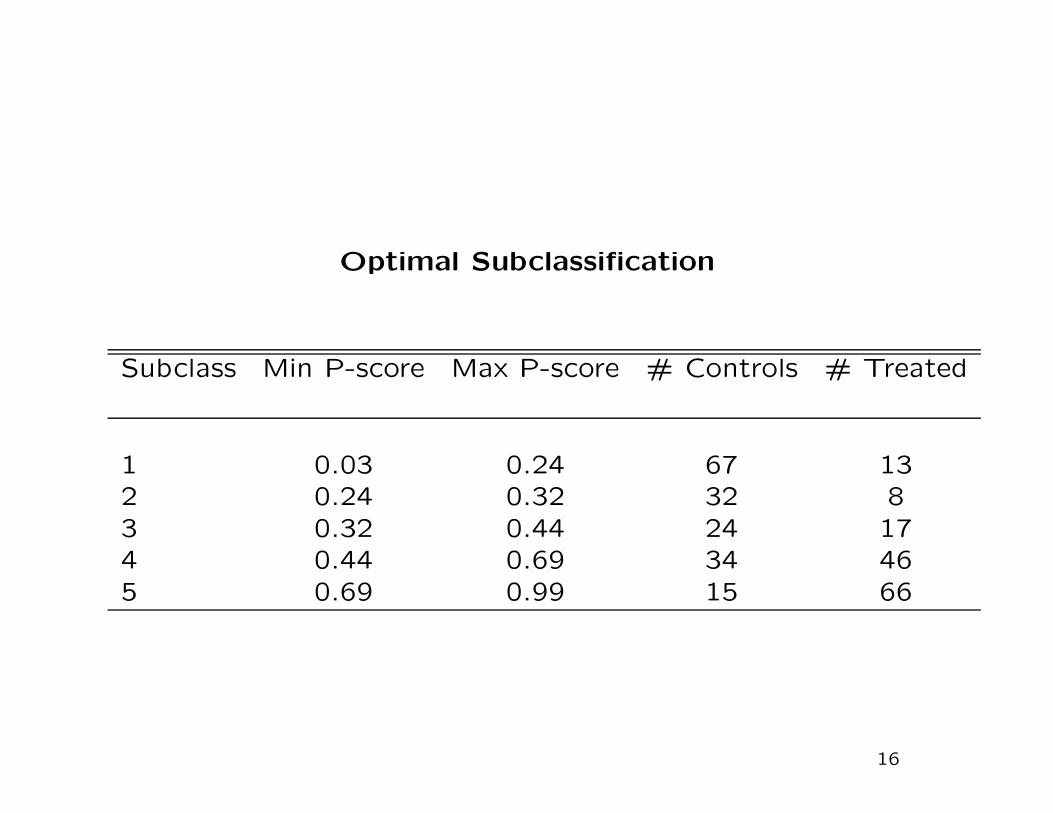

Optimal Subclassification

Subclass Min P-score Max P-score # Controls # Treated

1 0.03 0.24 67 132 0.24 0.32 32 83 0.32 0.44 24 174 0.44 0.69 34 465 0.69 0.99 15 66

16

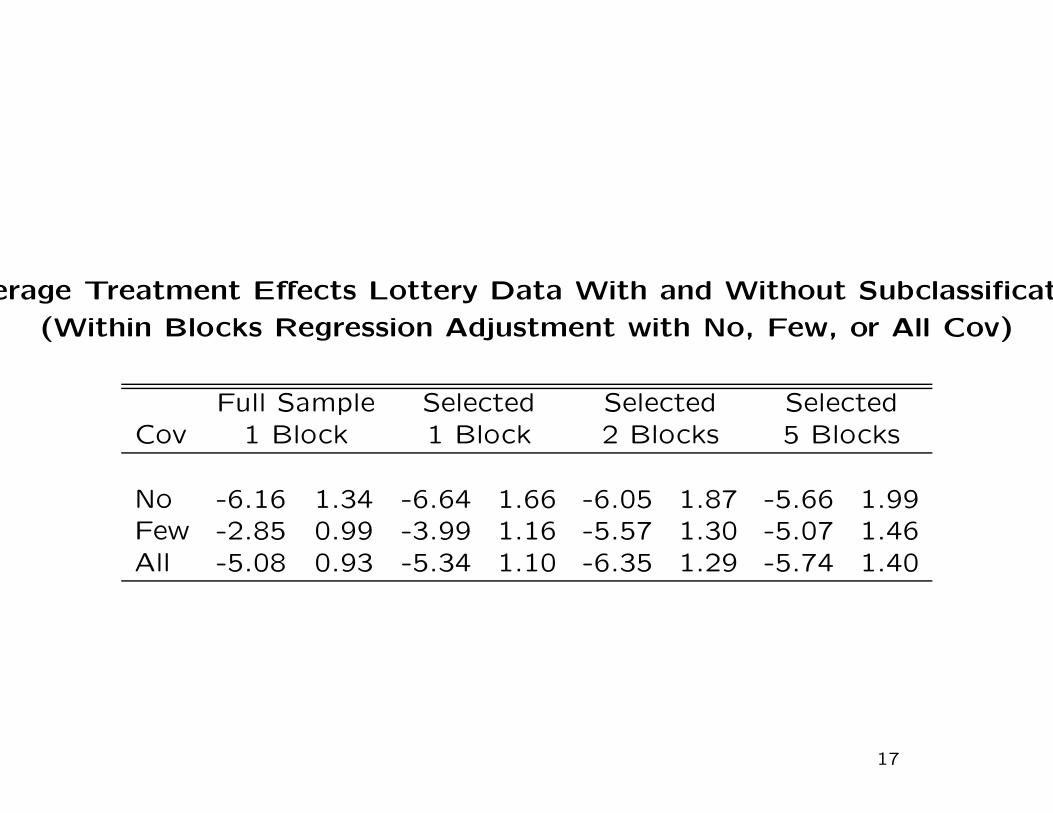

Average Treatment Effects Lottery Data With and Without Subclassification

(Within Blocks Regression Adjustment with No, Few, or All Cov)

Full Sample Selected Selected SelectedCov 1 Block 1 Block 2 Blocks 5 Blocks

No -6.16 1.34 -6.64 1.66 -6.05 1.87 -5.66 1.99Few -2.85 0.99 -3.99 1.16 -5.57 1.30 -5.07 1.46All -5.08 0.93 -5.34 1.10 -6.35 1.29 -5.74 1.40

17

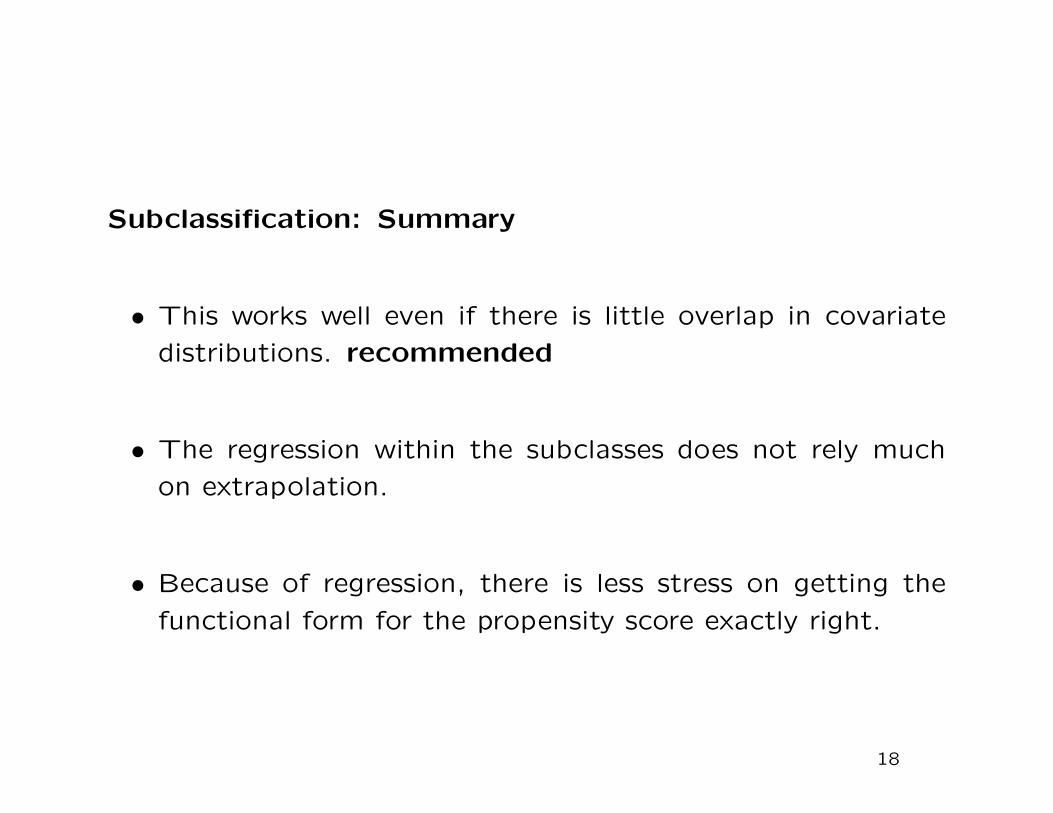

Subclassification: Summary

• This works well even if there is little overlap in covariate

distributions. recommended

• The regression within the subclasses does not rely much

on extrapolation.

• Because of regression, there is less stress on getting the

functional form for the propensity score exactly right.

18

7. Assessing Unconfoundedness

Main question:

• what can we say about the plausibility of unconfounded-

ness?

• Recall, unconfoundedness is not testable.

19

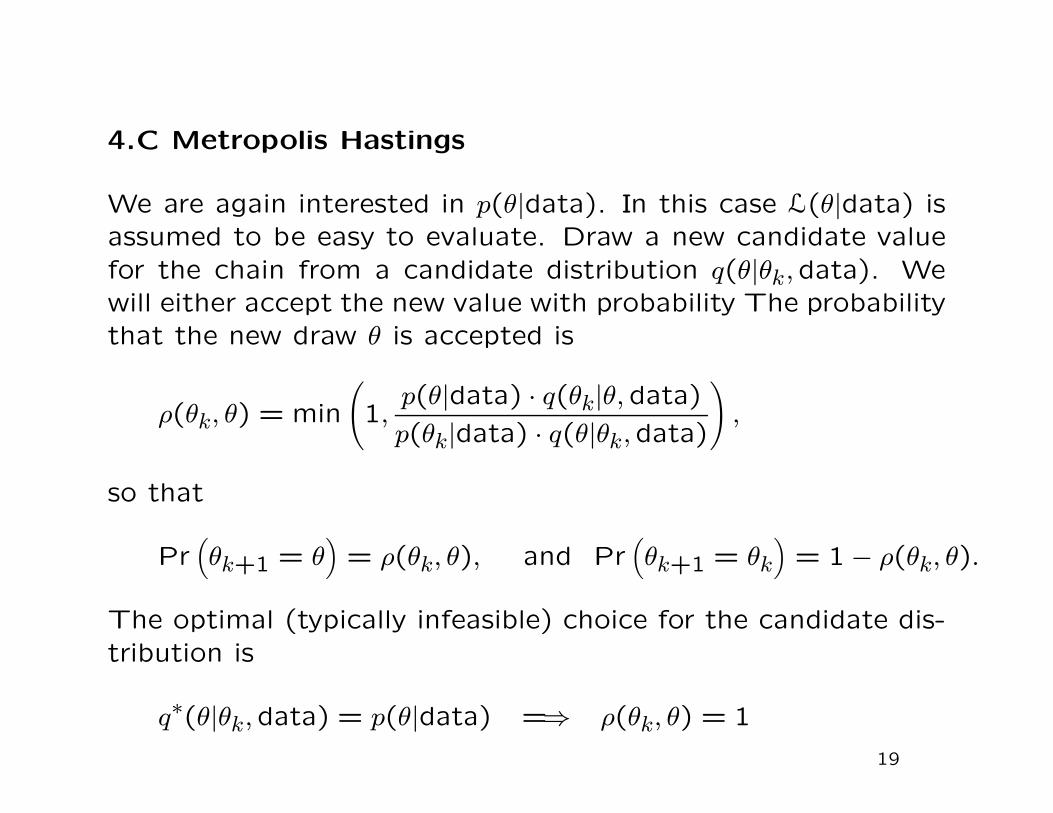

Assessing Unconfoundedness: Two Approaches

Both approaches estimate zero effects:

• Estimate effect of treatment on pseudo outcome

• Estimate effectof pseudo treatment on outcome

20

7. A Assessing Unconfoundedness by Estimating Effecton Pseudo Outcome

We consider the unconfoundedness assumption,

Yi(0), Yi(1) ⊥⊥ Wi

∣∣∣∣∣ Xi. (1)

We partition the vector of covariates Xi into two parts, a(scalar) pseudo outcome, denoted by Xp

i , and the remainder,denoted by Xr

i , so that Xi = (Xpi , Xr′

i )′.

Now we assess whether the following conditional independencerelation holds:

Xpi ⊥⊥ Wi

∣∣∣∣∣ Xri .

The two issues are (i) the interpretation of this and the relationto the unconfoundedness assumption that is of primary interest,and (ii) the implementation of the test.

21

The first issue concerns the link between the conditional inde-

pendence relation and unconfoundedness . This link is indirect,

as unconfoundedness cannot be tested directly.

First consider a related condition:

Yi(0), Yi(1) ⊥⊥ Wi

∣∣∣∣∣ Xri .

If this modified unconfoundedness condition were to hold, one

could use the adjustment methods using only the subset of

covariates Xri . In practice this is a stronger condition than the

original unconfoundedness condition.

The modified unconfoundedness condition is not testable. We

use the pseudo outcome Xpi as a proxy variable Yi(0), and test

Xpi ⊥⊥ Wi

∣∣∣∣∣ Xri .

22

A leading example is that where Xi contains multiple lagged

measures of the outcome. In the lottery example we have

observations on earnings for six, years prior to winning. Denote

these lagged outcomes by Yi,−1, . . . , Yi,−6, where Yi,−1 is the

most recent and Yi,−6 is the most distant pre-winning earnings

measure.

One could implement the above ideas using earnings for the

most recent pre-winning year Yi,−1 as the pseudo outcome

Xpi , so that the vector of remaining pretreatment variables Xr

i

would still include the five prior years of pre-winning earnings

Yi,−2, . . . , Yi,−6 (ignoring additional pre-treatment variables).

23

Now we turn to the second issue, the implementation. One

approach to testing the conditional independence assumption

is to estimate the average difference in Xpi by treatment status,

after adjusting for differences in Xri .

This is exactly the same problem as estimating the average

effect of the treatment, using Xpi as the pseudo outcome and

Xri as the vector of pretreatment variables. We can do this

using any of the methods discussed so far.

24

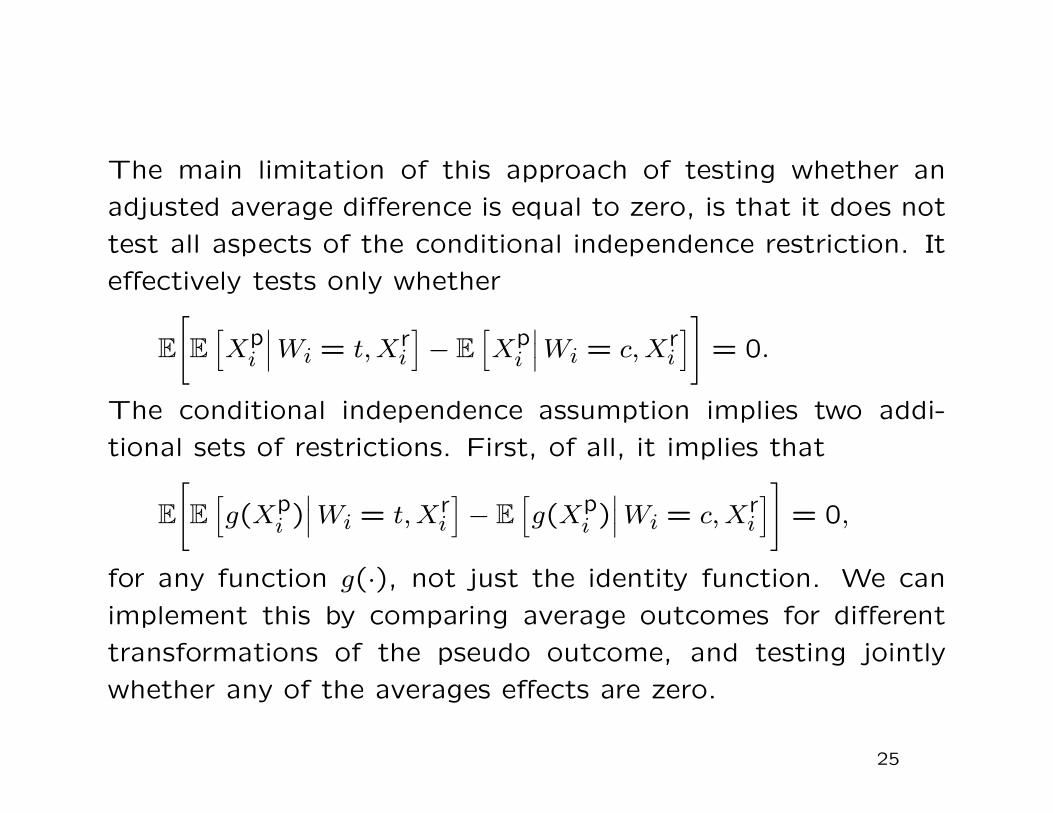

The main limitation of this approach of testing whether an

adjusted average difference is equal to zero, is that it does not

test all aspects of the conditional independence restriction. It

effectively tests only whether

E

[

E

[Xp

i

∣∣∣Wi = t,Xri

]− E

[Xp

i

∣∣∣Wi = c, Xri

]]

= 0.

The conditional independence assumption implies two addi-

tional sets of restrictions. First, of all, it implies that

E

[

E

[g(Xp

i )∣∣∣Wi = t,Xr

i

]− E

[g(Xp

i )∣∣∣Wi = c, Xr

i

]]

= 0,

for any function g(·), not just the identity function. We can

implement this by comparing average outcomes for different

transformations of the pseudo outcome, and testing jointly

whether any of the averages effects are zero.

25

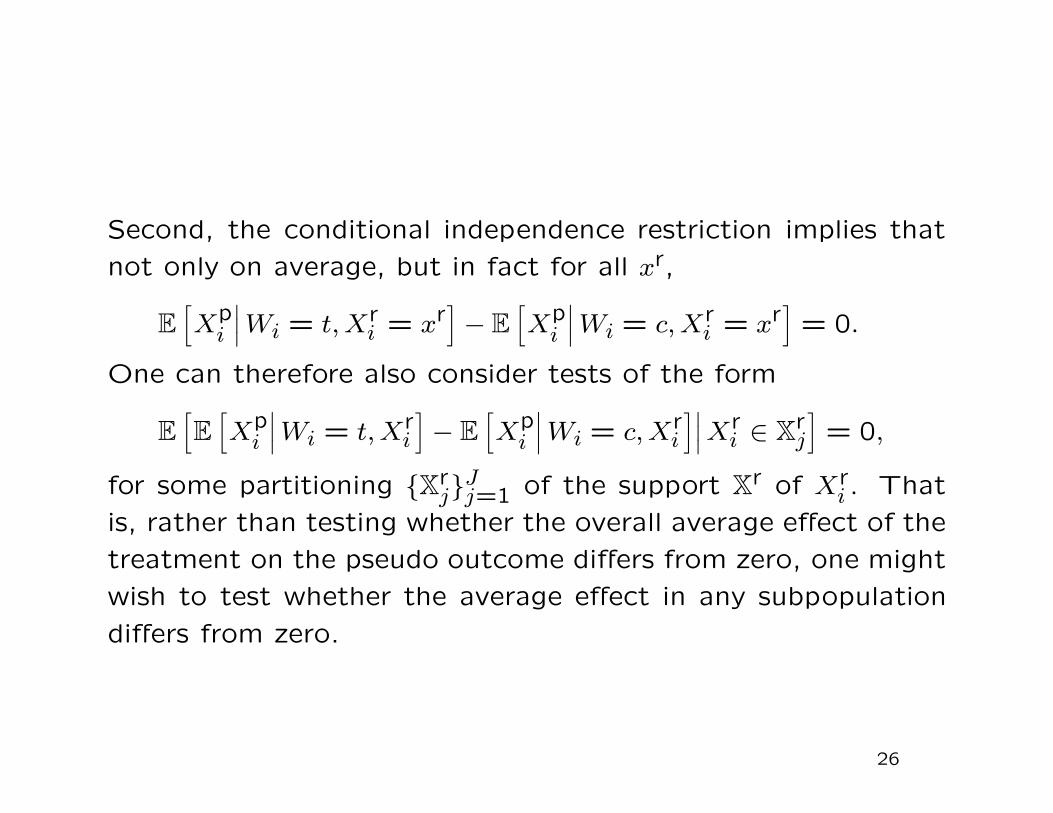

Second, the conditional independence restriction implies that

not only on average, but in fact for all xr,

E

[Xp

i

∣∣∣Wi = t, Xri = xr

]− E

[Xp

i

∣∣∣Wi = c, Xri = xr

]= 0.

One can therefore also consider tests of the form

E

[E

[Xp

i

∣∣∣Wi = t, Xri

]− E

[Xp

i

∣∣∣Wi = c, Xri

]∣∣∣Xri ∈ X

rj

]= 0,

for some partitioning Xrj

Jj=1 of the support X

r of Xri . That

is, rather than testing whether the overall average effect of the

treatment on the pseudo outcome differs from zero, one might

wish to test whether the average effect in any subpopulation

differs from zero.

26

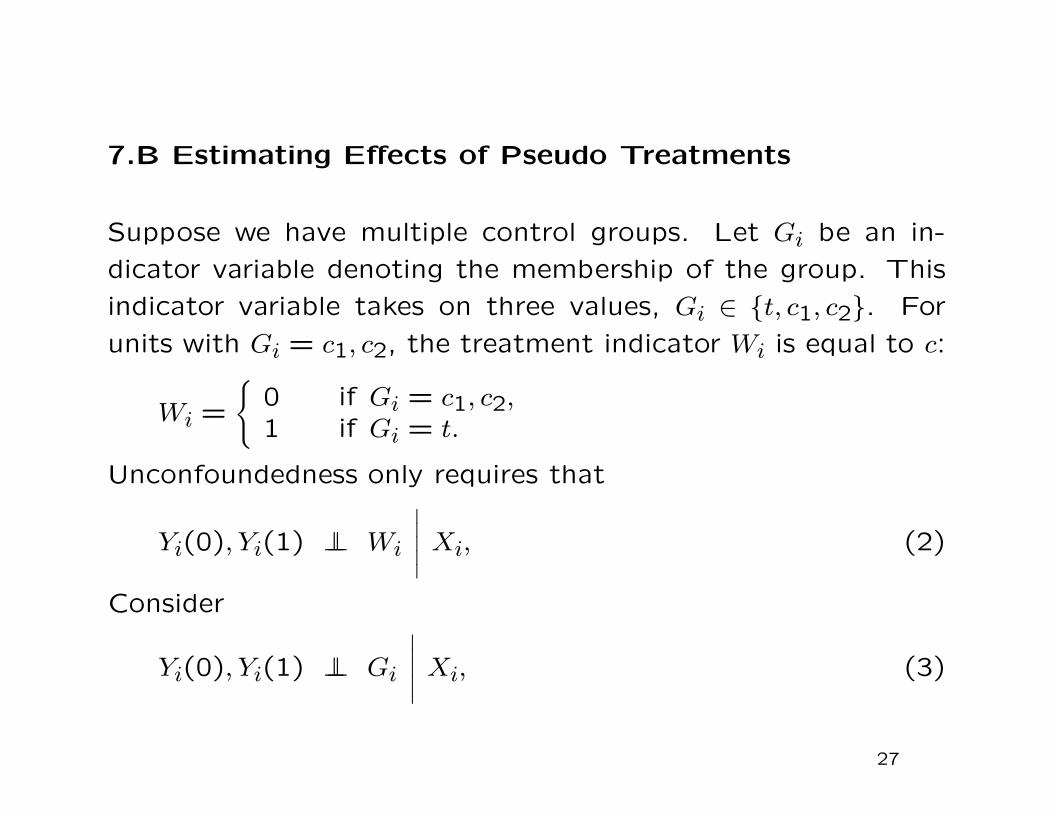

7.B Estimating Effects of Pseudo Treatments

Suppose we have multiple control groups. Let Gi be an in-

dicator variable denoting the membership of the group. This

indicator variable takes on three values, Gi ∈ t, c1, c2. For

units with Gi = c1, c2, the treatment indicator Wi is equal to c:

Wi =

0 if Gi = c1, c2,1 if Gi = t.

Unconfoundedness only requires that

Yi(0), Yi(1) ⊥⊥ Wi

∣∣∣∣∣ Xi, (2)

Consider

Yi(0), Yi(1) ⊥⊥ Gi

∣∣∣∣∣ Xi, (3)

27

This has the testable implication

Yi(0) ⊥⊥ Gi

∣∣∣∣∣ Xi, Gi ∈ c1, c2

which is equivalent to

Y obsi ⊥⊥ Gi

∣∣∣∣∣ Xi, Gi ∈ c1, c2,

because Gi ∈ c1, c2 implies that Y obsi = Yi(0).

28

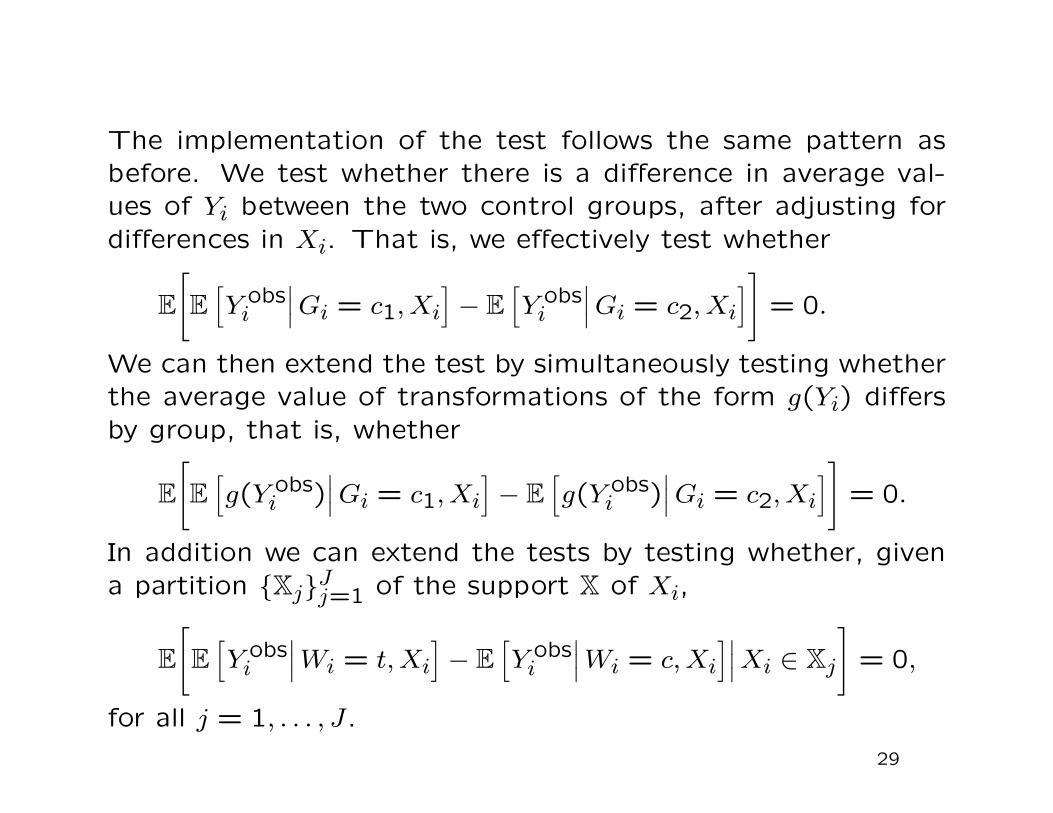

The implementation of the test follows the same pattern as

before. We test whether there is a difference in average val-

ues of Yi between the two control groups, after adjusting for

differences in Xi. That is, we effectively test whether

E

[

E

[Y obs

i

∣∣∣Gi = c1, Xi

]− E

[Y obs

i

∣∣∣Gi = c2, Xi

]]

= 0.

We can then extend the test by simultaneously testing whether

the average value of transformations of the form g(Yi) differs

by group, that is, whether

E

[

E

[g(Y obs

i )∣∣∣Gi = c1, Xi

]− E

[g(Y obs

i )∣∣∣Gi = c2, Xi

]]

= 0.

In addition we can extend the tests by testing whether, given

a partition XjJj=1 of the support X of Xi,

E

[

E

[Y obs

i

∣∣∣Wi = t, Xi

]− E

[Y obs

i

∣∣∣Wi = c, Xi

]∣∣∣Xi ∈ Xj

]

= 0,

for all j = 1, . . . , J.

29

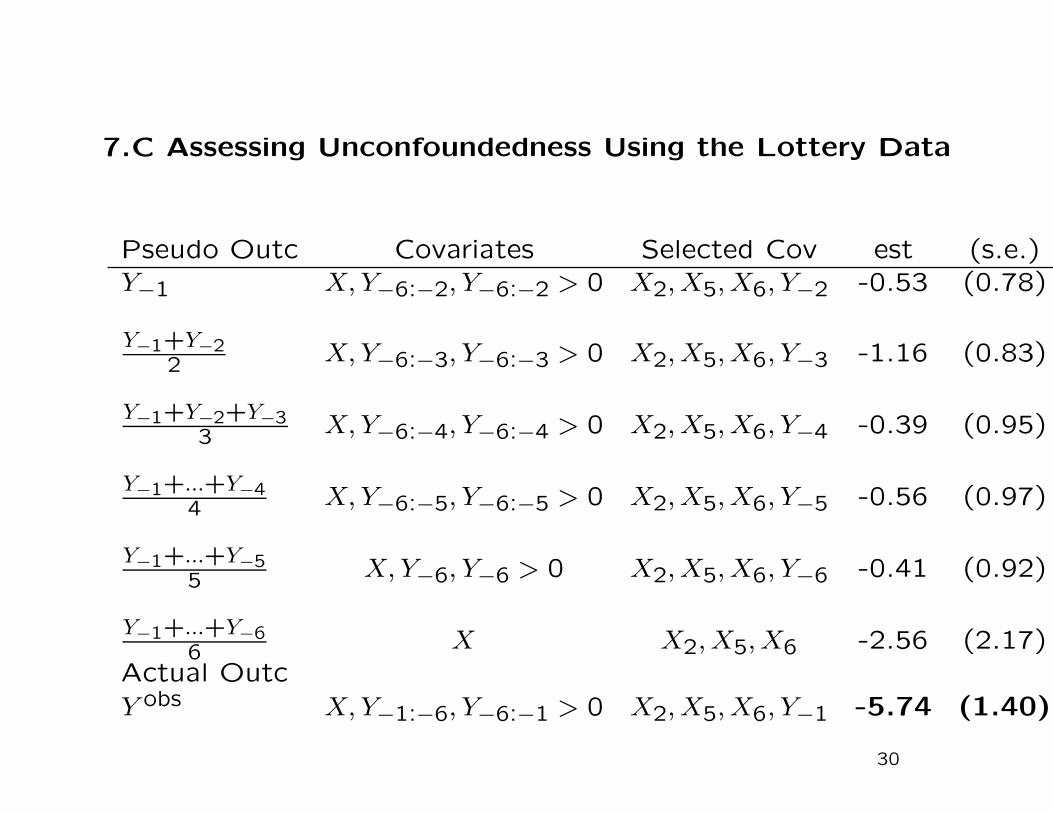

7.C Assessing Unconfoundedness Using the Lottery Data

Pseudo Outc Covariates Selected Cov est (s.e.)

Y−1 X, Y−6:−2, Y−6:−2 > 0 X2, X5, X6, Y−2 -0.53 (0.78)

Y−1+Y−22 X, Y−6:−3, Y−6:−3 > 0 X2, X5, X6, Y−3 -1.16 (0.83)

Y−1+Y−2+Y−33 X, Y−6:−4, Y−6:−4 > 0 X2, X5, X6, Y−4 -0.39 (0.95)

Y−1+...+Y−44 X, Y−6:−5, Y−6:−5 > 0 X2, X5, X6, Y−5 -0.56 (0.97)

Y−1+...+Y−55 X, Y−6, Y−6 > 0 X2, X5, X6, Y−6 -0.41 (0.92)

Y−1+...+Y−66 X X2, X5, X6 -2.56 (2.17)

Actual Outc

Y obs X, Y−1:−6, Y−6:−1 > 0 X2, X5, X6, Y−1 -5.74 (1.40)

30

Estimates of Average Treatment Effect

on Transformations of Pseudo Outcome for Subpopulations

Pseudo Subpopulation est (s.e.)Outcome

1Y−1 = 0 Y−2 = 0 -0.07 (0.78)1Y−1 = 0 Y−2 > 0 0.02 (0.02)Y−1 Y−2 = 0 -0.31 (0.30)Y−1 Y−2 > 0 0.05 (0.06)

statistic p-valueCombined Statistic(chi-squared, dof 4) 2.20 0.135

31

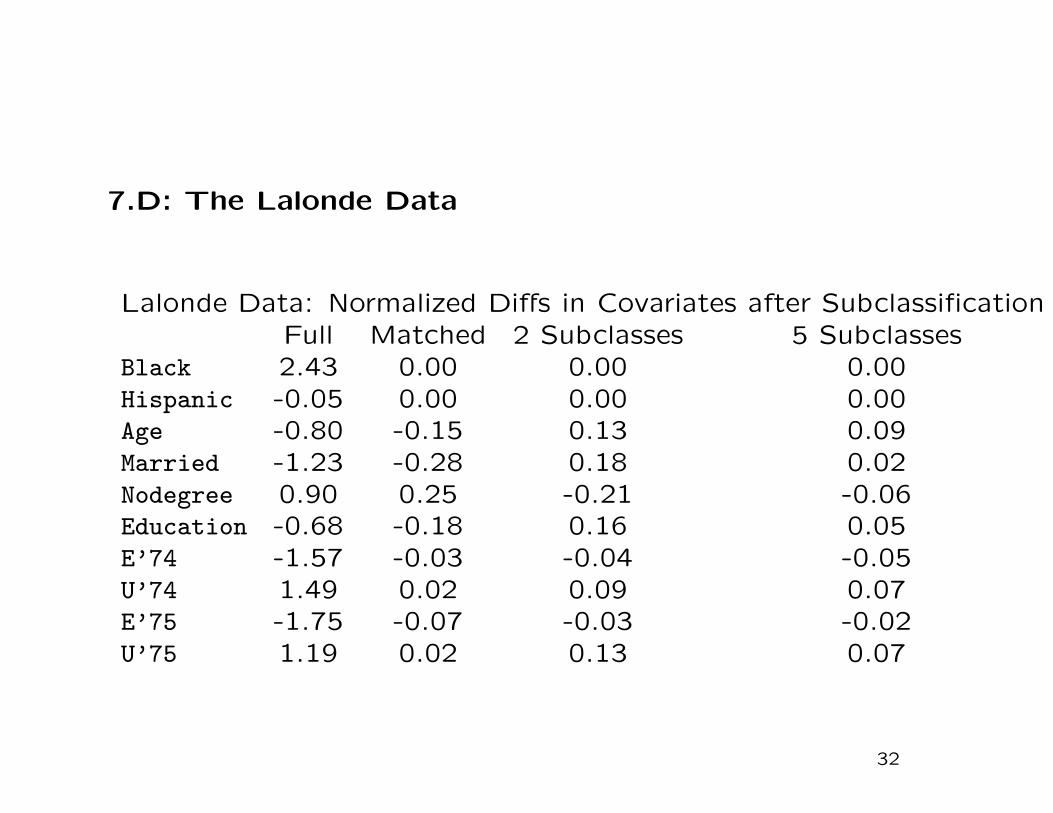

7.D: The Lalonde Data

Lalonde Data: Normalized Diffs in Covariates after SubclassificationFull Matched 2 Subclasses 5 Subclasses

Black 2.43 0.00 0.00 0.00Hispanic -0.05 0.00 0.00 0.00Age -0.80 -0.15 0.13 0.09Married -1.23 -0.28 0.18 0.02Nodegree 0.90 0.25 -0.21 -0.06Education -0.68 -0.18 0.16 0.05E’74 -1.57 -0.03 -0.04 -0.05U’74 1.49 0.02 0.09 0.07E’75 -1.75 -0.07 -0.03 -0.02U’75 1.19 0.02 0.13 0.07

32

Next let us look at the estimates for effect on 1978 earnings.

We use the matched sample and use subclassification to re-

move additional bias.

Full Sample Matched Matched MatchedCov 1 Block 1 Block 2 Blocks 4 Blocks

No -8.50 0.58 1.72 0.74 1.81 0.75 1.86 0.76Few 0.69 0.59 1.81 0.73 1.80 0.73 1.99 0.75All 1.07 0.55 1.97 0.66 1.90 0.67 2.06 0.66

33

Covariate still make some difference, but reasonably robust.

With all covariates included the estimate is close to experimen-

tal one, but would we have known that?

With only the trainee and CPS comparison data would we have

concluded that the evaluation was succesful?

34

Analyse trainee/CPS-control data with earnings ’75 as out-

come, and remaining eight covariates as pre-treatment vari-

ables.

We take the original full sample, create a matched sample base-

don the eight remaining covariates, and estimate the “effect”

of the training on 1975 earnings.

Also: test effect on earnings ’75, earnings ’75>0, separately

for those with positive and zero earnings in 1974. Leads to 4

estimated effects, and we test that all four are jointly zero.

35

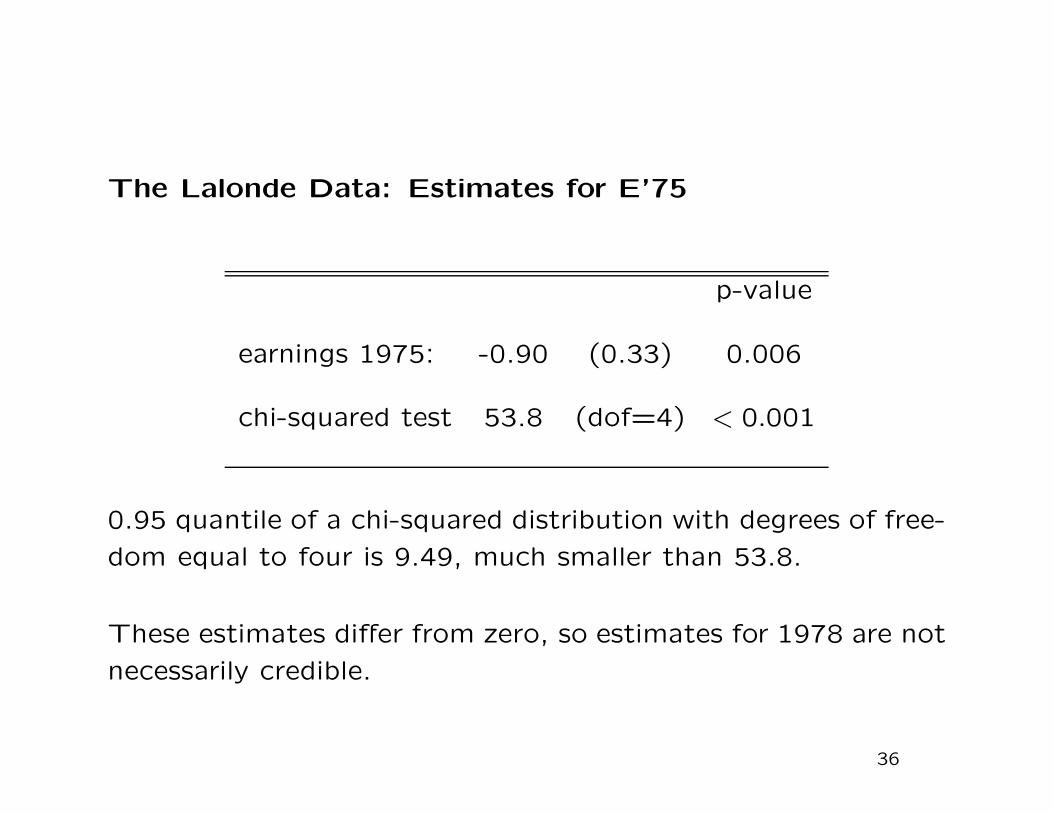

The Lalonde Data: Estimates for E’75

p-value

earnings 1975: -0.90 (0.33) 0.006

chi-squared test 53.8 (dof=4) < 0.001

0.95 quantile of a chi-squared distribution with degrees of free-

dom equal to four is 9.49, much smaller than 53.8.

These estimates differ from zero, so estimates for 1978 are not

necessarily credible.

36

In the Lalonde case, had we done this analysis first, we would

not necessarily have even estimated the effect for 1978 earn-

ings: the initial analysis suggests that the estimates would not

necessarily be credible.

37

7.E Assessing Unconfoundedness: Summary

Whenever possible, assess the plausibility of unconfoundedness.

Having good covariates available is important here.

Analysis may suggest that results are not credible. They dont

point in direction of alternative analysis, only suggest that pro-

ceeding under the assumption of unconfoundedness is not rea-

sonable.

38

• for the lottery data we obtain credible and precise estimates,

robust to small changes in the specification and with uncon-

foundedness plausible.

• for the lalonde data the results are more mixed. the estimates

are robust to changes in the specification, but the assessments

of unconfoundedness raises doubts.

39

Econometrics of Cross Section and Panel DataLecture 3: Linear Panel Data Models I

Jeff WooldridgeMichigan State University

cemmap/PEPA, June 2014

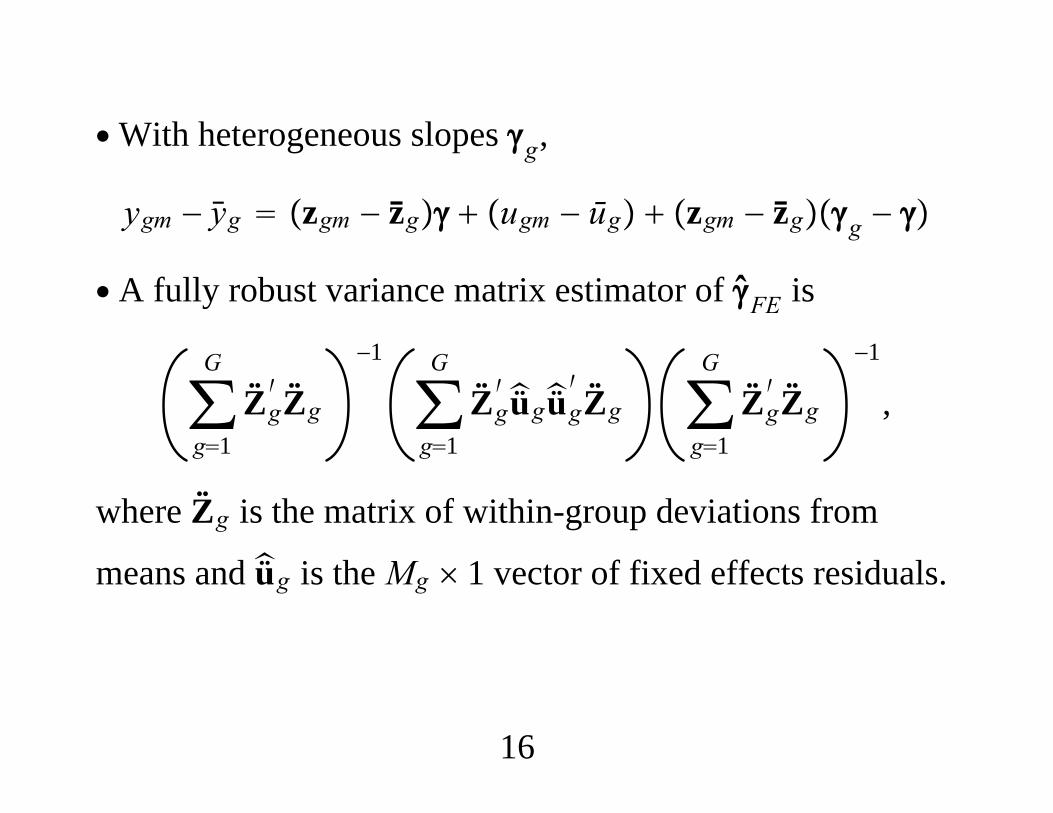

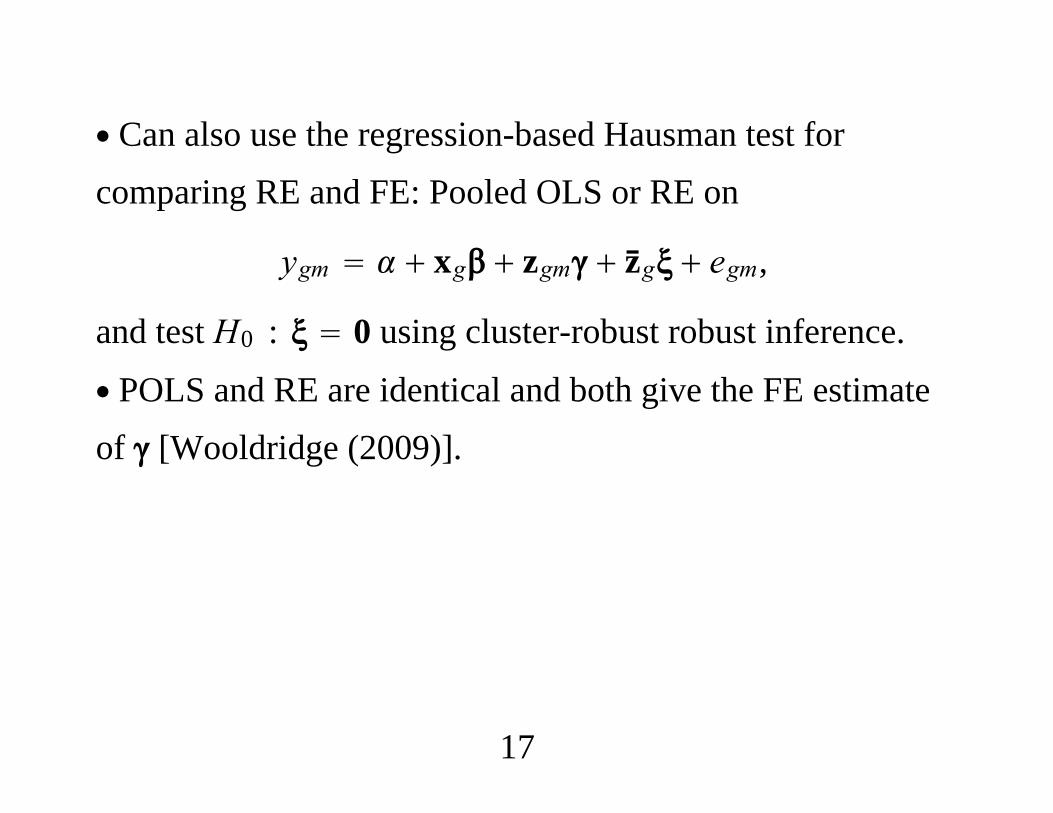

1. Introduction and Summary2. The Basic Model and Assumptions3. The Standard Estimators4. Comparing RE and FE5. Comparing FE and FD

1

1. Introduction and Summary∙Microeconometric setting: Access to a large cross sectionand short time series.∙ Random sampling in the cross section.∙ Important to think through the assumptions that implyconsistency for the different estimators. What is the sourceof bias?∙ Distinguish between “ideal” assumptions and thosesufficient for consistent estimation.

2

∙ Inference robust to general serial correlation andheteroskedasticity should be used.∙When using specification tests (Hausman test), make testsas robust as inference on the coefficients.

3

2. The Basic Model and Assumptions∙ For a random draw i from the population,

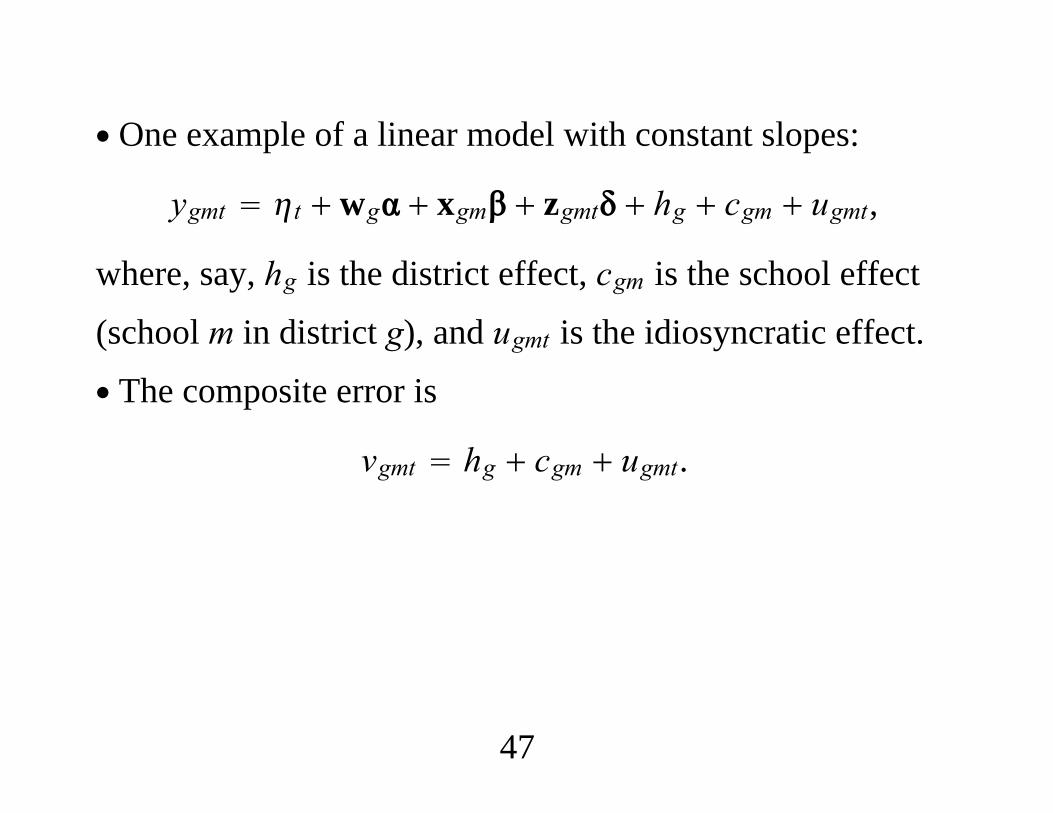

yit t xit ci uit, t 1, . . . ,T

∙ View the ci as random variables (that may be correlatedwith the xit).∙ The phrases “unobserved effects” or “individualheterogeneity” for ci are neutral and preferred.

4

yit t xit ci uit, t 1, . . . ,T

∙ The uit : t 1, . . . ,T are the idiosyncratic errors.∙ The composite error at time t is

vit ci uit

∙ Except by fluke vit : t 1, . . . ,T is serially correlated,and could be heteroskedastic.

5

yit t xit ci uit, t 1, . . . ,T

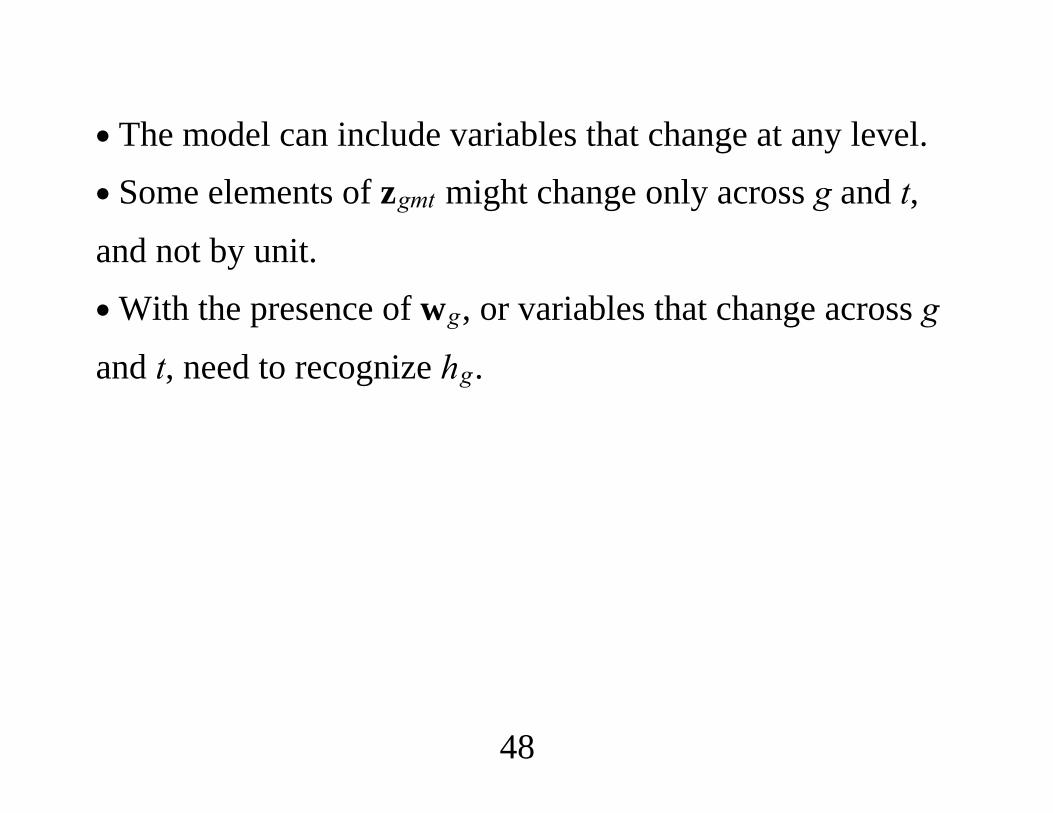

∙ xit is a 1 K row vector; it can contain variables thatchange across i only, or across i and t.∙With a short panel, the time period intercepts, t, are

usually treated as parameters that can be estimated.∙ Separate period intercepts are handled easily with timedummies.

6

∙ Often useful to write

yit gt zi wit ci uit

∙ gt is a vector of aggregate time effects (usually time

dummies)∙ zi is a set of time-constant observed variables∙ wit changes across i and t∙We cannot identify without fairly strong assumptions.

7

Assumptions about Covariates and IdiosyncraticErrors

yit xit ci uit

1. Contemporaneous Exogeneity:

Covxit,uit 0, t 1, . . . ,T

or a conditional mean version:

Eyit|xit,ci xit ci.

∙ Ideally, we could proceed with this assumption.

8

2. Strict Exogeneity:

Covxis,uit 0, s, t 1, . . . ,T.

∙ In other words, the covariates at any time s areuncorrelated with the idiosyncratic errors at any time t.∙ All of the standard estimation methods assume strictexogeneity.∙ Theoretically, this assumption should often fail.∙ Is the failure of strict exogeneity empirically important?

9

∙ Strict exogeneity implies correct distributed lag dynamicsin covariates.∙ Strict exogeneity rules out lagged dependent variables(because if s t 1, xis yit)∙ Strict exogeneity rules out other situations where shockstoday affect future decisions about the covariates.∙ In applications we need to ask: Why are the explanatoryvariables changing over time, and might those changes berelated to past shocks to yit?

10

∙ Example: If a worker changes his union status, is hereacting to past shocks to earnings?∙ Example: Do shocks to air fares feed back into futurechanges in route concentration?∙ Example: Might a principal assign students to classroomsbased on past shocks to academic performance?

11

3. Sequential Exogeneity:

Covxis,uit 0, s ≤ t

∙ This assumption can hold with lagged dependent variables,but it does require correct dynamic specification.∙ Key: Sequential exogeneity is silent on feedback. It allowsxi,t1 to be correlated with uit.

12

Assumptions about Covariates and UnobservedEffect

yit xit ci uit

1. “Random effects” means

Covxit,ci 0, t 1, . . . ,T.

2. “Fixed effects” means that no restrictions are placed onthe relationship between ci and xit.3. “Correlated random effects” (CRE): We model therelationship between ci and xit.

13

3. The Standard Estimators∙ Best to think of there being one model, the unobservedeffects model

yit xit ci uit, i 1, . . . ,T.

∙ There are several possible estimators of .

∙ “OLS Model”?

14

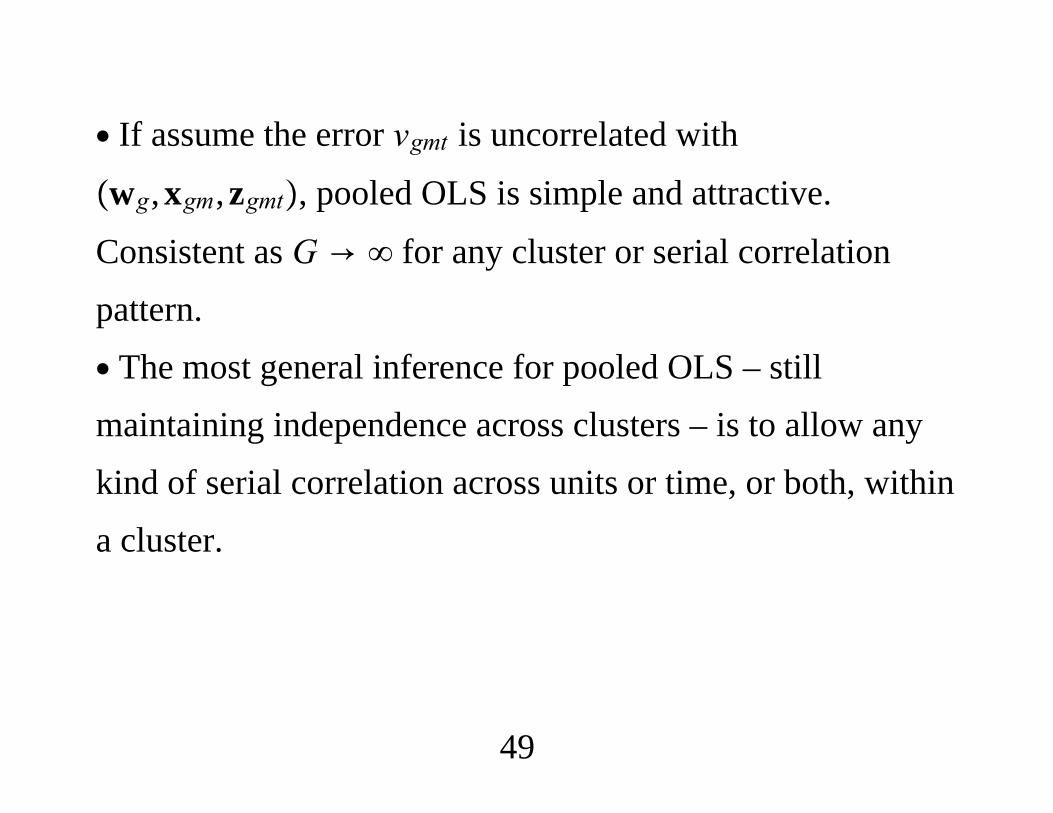

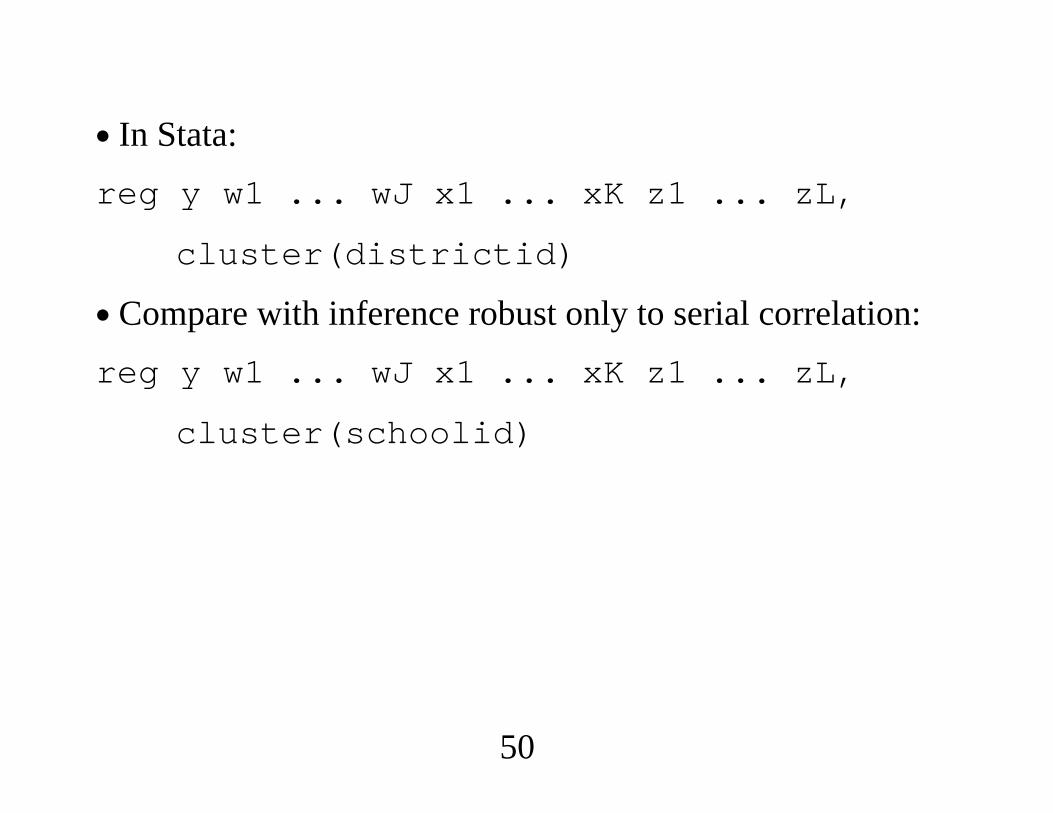

3.1. Pooled OLS∙ Pool the observations and apply OLS:

yit xit vitvit ci uit

∙ Consistency (fixed T, N → ) of POLS ensured by

Covxit,ci 0Covxit,uit 0, t 1, . . . ,T.

15

∙ Because of the large N, fixed T asymptotics, any kind ofserial dependence is allowed in xit and uit.∙ Inference should be made robust to arbitrary serialcorrelation and heteroskedasticity in vit ci uit.∙ No need to downweight correlations farther apart in time(as in Newey-West).

16

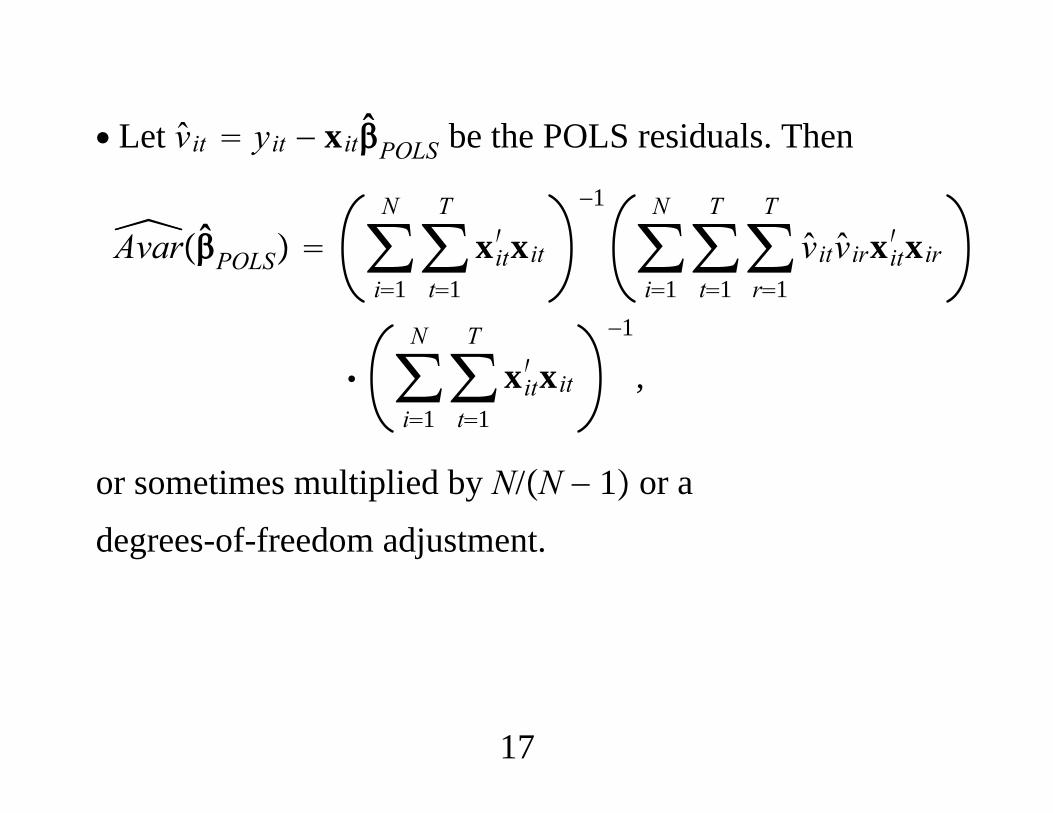

∙ Let vit yit − xitPOLS be the POLS residuals. Then

AvarPOLS ∑i1

N

∑t1

T

xit′ xit−1

∑i1

N

∑t1

T

∑r1

T

vitvirxit′ xir

∑i1

N

∑t1

T

xit′ xit−1

,

or sometimes multiplied by N/N − 1 or adegrees-of-freedom adjustment.

17

∙ Can include aggregate time effects, variables that changeonly across units, and variables that change across i and t.∙With good controls – say, industry dummies when we havefirm-level data or state dummies with county-level data – wemight find Covxit,ci 0 plausible.∙ (Quasi-)randomization of an intervention?∙ Dynamic OLS, which includes lagged yit, useful for“astructural” treatment effects estimation.

18

3.2. Random Effects Estimation∙ RE assumes

Covxit,ci 0Covxis,uit 0, s, t 1, . . . ,T.

∙ Letting xi xi1,xi2, . . . ,xiT, vit ci uit is uncorrelatedwith xi (not just xit).∙We can apply generalized least squares methods.

19

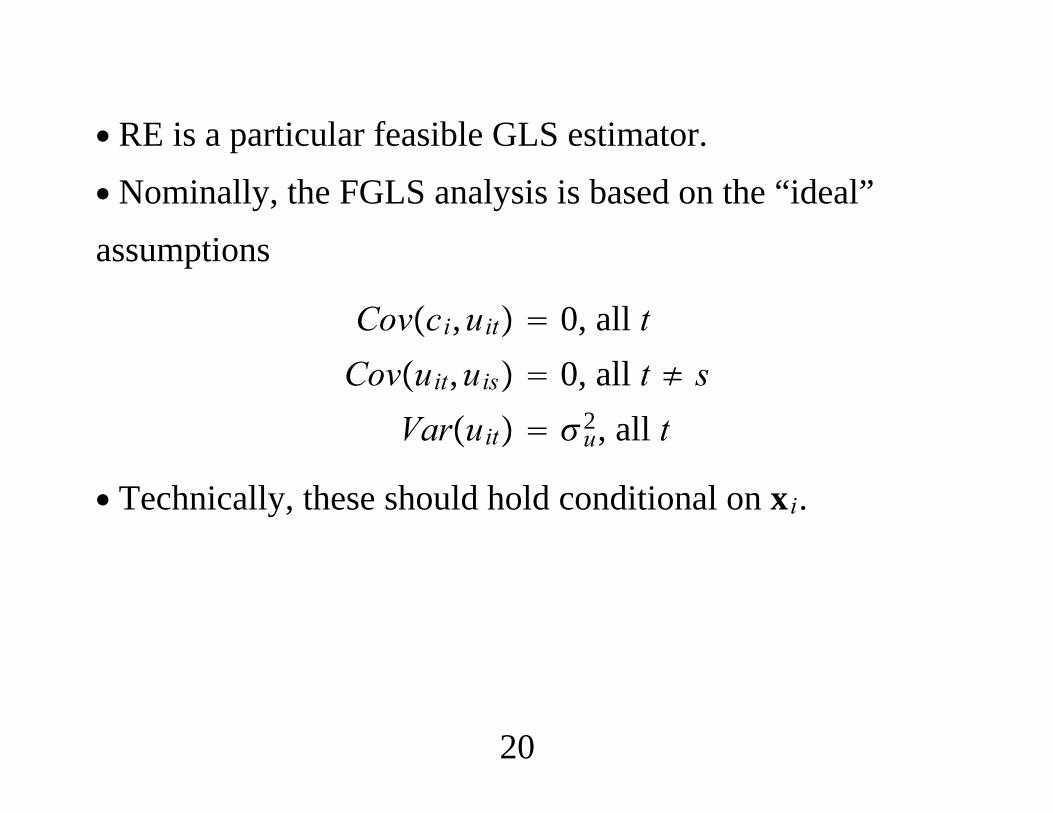

∙ RE is a particular feasible GLS estimator.∙ Nominally, the FGLS analysis is based on the “ideal”assumptions

Covci,uit 0, all tCovuit,uis 0, all t ≠ s

Varuit u2, all t

∙ Technically, these should hold conditional on xi.

20

Evivi′

c2 u2 c2 c2

c2 c2 u2

c2

c2 c2 c2 u2

∙ Depends on only two parameters, c2 Varci andu2 Varuit, rather than TT 1/2.

21

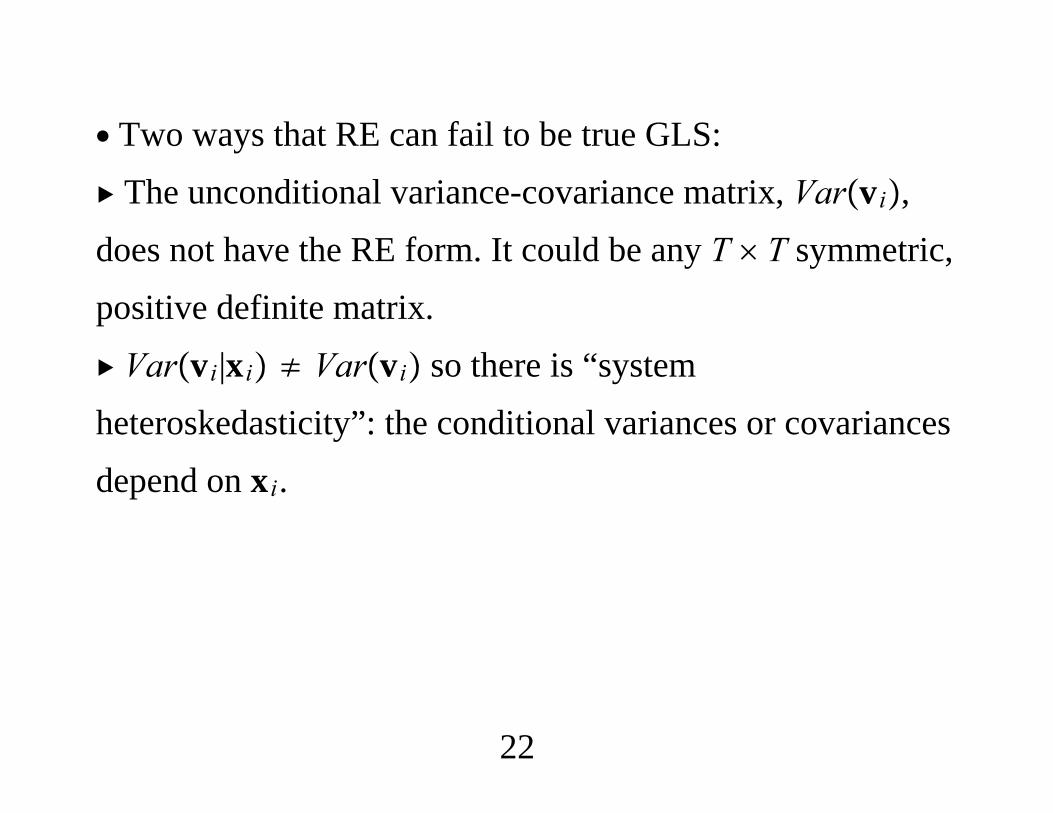

∙ Two ways that RE can fail to be true GLS: The unconditional variance-covariance matrix, Varvi,does not have the RE form. It could be any T T symmetric,positive definite matrix. Varvi|xi ≠ Varvi so there is “systemheteroskedasticity”: the conditional variances or covariancesdepend on xi.

22

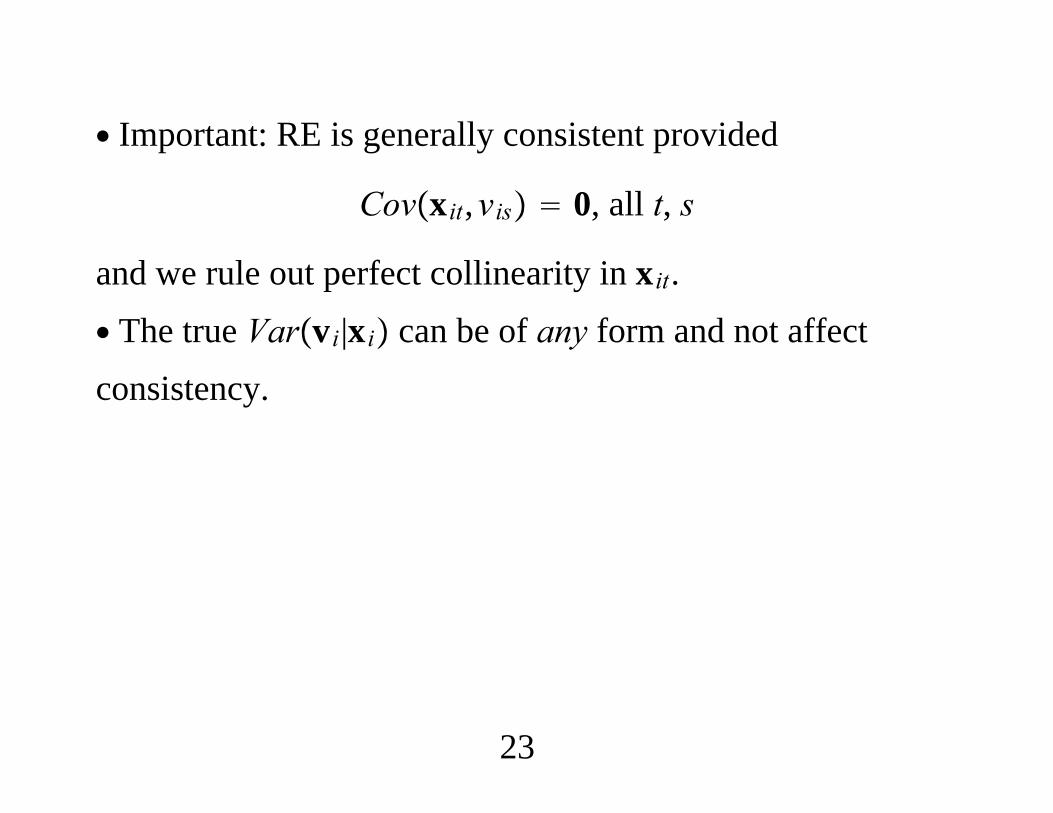

∙ Important: RE is generally consistent provided

Covxit,vis 0, all t, s

and we rule out perfect collinearity in xit.∙ The true Varvi|xi can be of any form and not affectconsistency.

23

∙ RE is “quasi-” GLS when the RE variance structure doesnot hold.∙ RE still can be notably better than pooled OLS. (Keyinsight in Generalized Estimating Equations literature.)∙ Serial correlation in uit or heteroskedasticity in ci or uitmeans we should make inference fully robust.

24

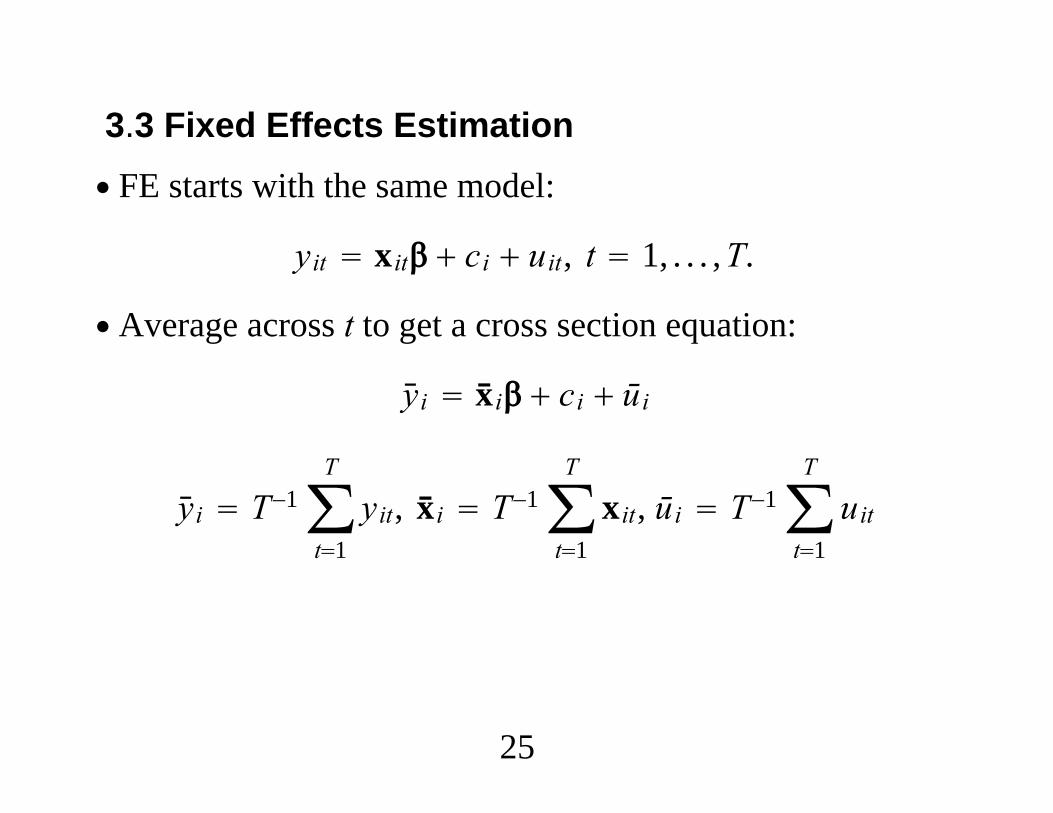

3.3 Fixed Effects Estimation∙ FE starts with the same model:

yit xit ci uit, t 1, . . . ,T.

∙ Average across t to get a cross section equation:

yi xi ci ūi

yi T−1∑t1

T

yit, xi T−1∑t1

T

xit, ūi T−1∑t1

T

uit

25

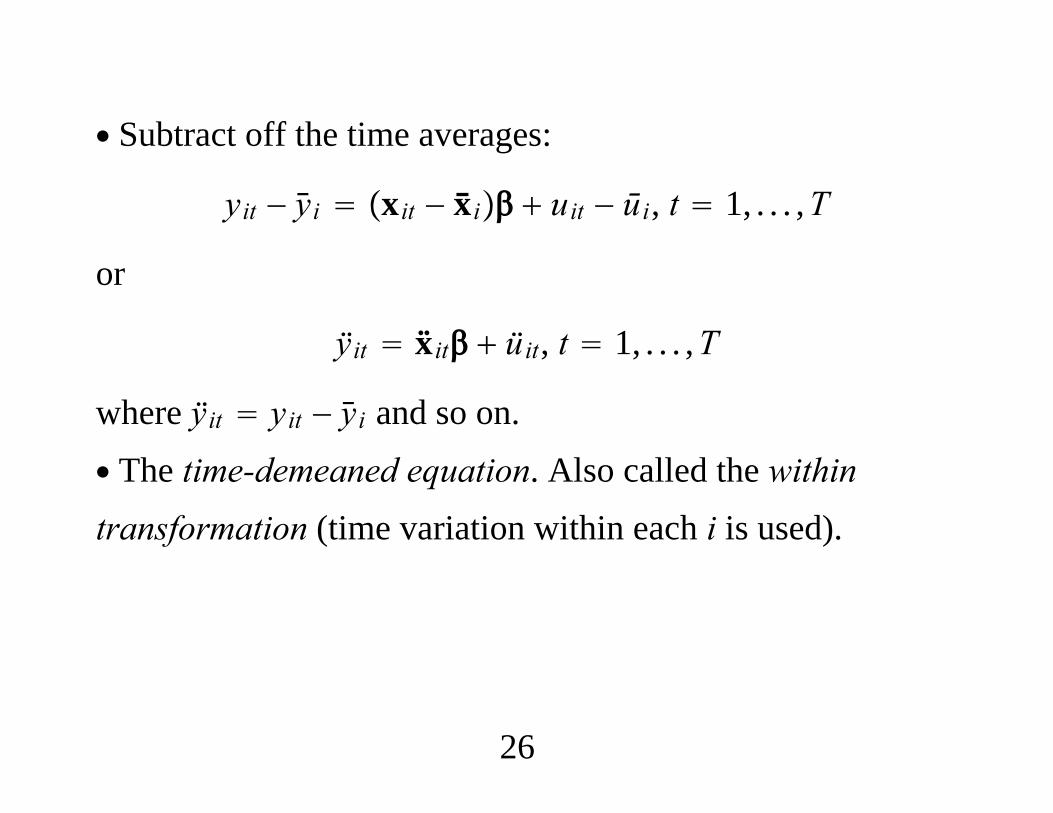

∙ Subtract off the time averages:

yit − yi xit − xi uit − ūi, t 1, . . . ,T

or

ÿit xit üit, t 1, . . . ,T

where ÿit yit − yi and so on.∙ The time-demeaned equation. Also called the withintransformation (time variation within each i is used).

26

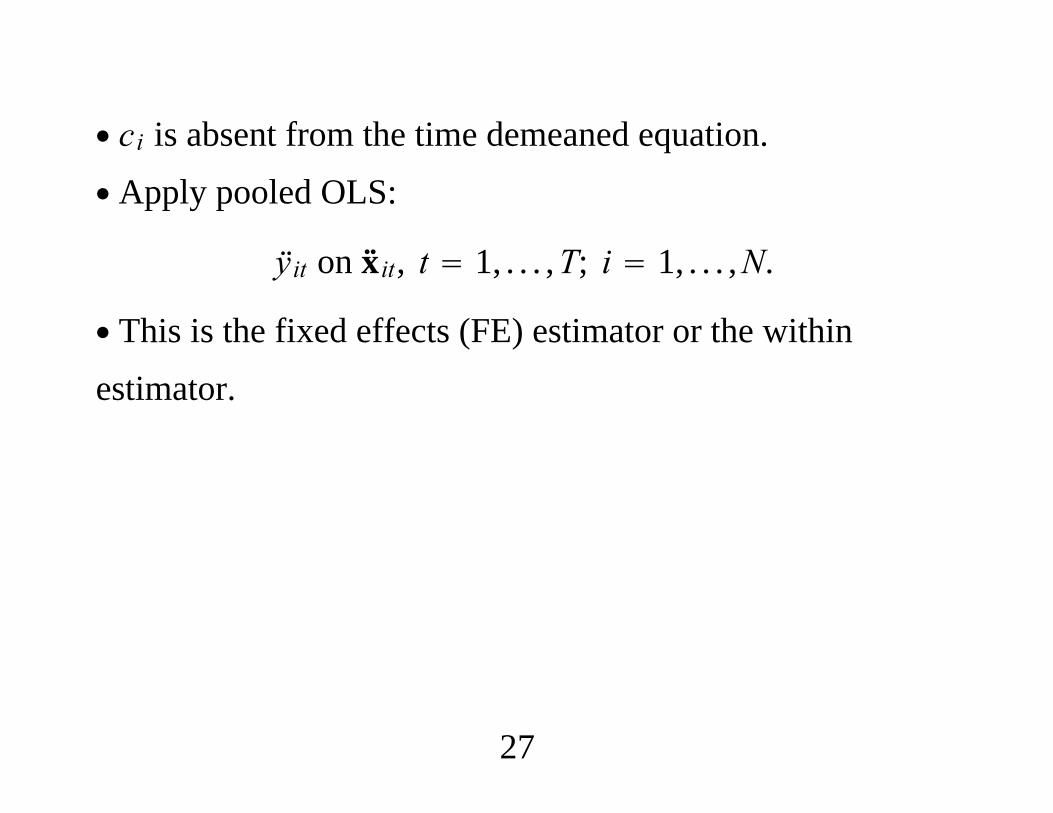

∙ ci is absent from the time demeaned equation.∙ Apply pooled OLS:

ÿit on xit, t 1, . . . ,T; i 1, . . . ,N.

∙ This is the fixed effects (FE) estimator or the withinestimator.

27

∙ Least restrictive exogeneity condition for consistency:

∑t1

T

Exit − xi′uit 0.

∙ Essentially, for t 1, . . . ,T,

Exit′ uit 0Exi′uit 0

∙ Relationship between ci and xit is unrestricted.

28

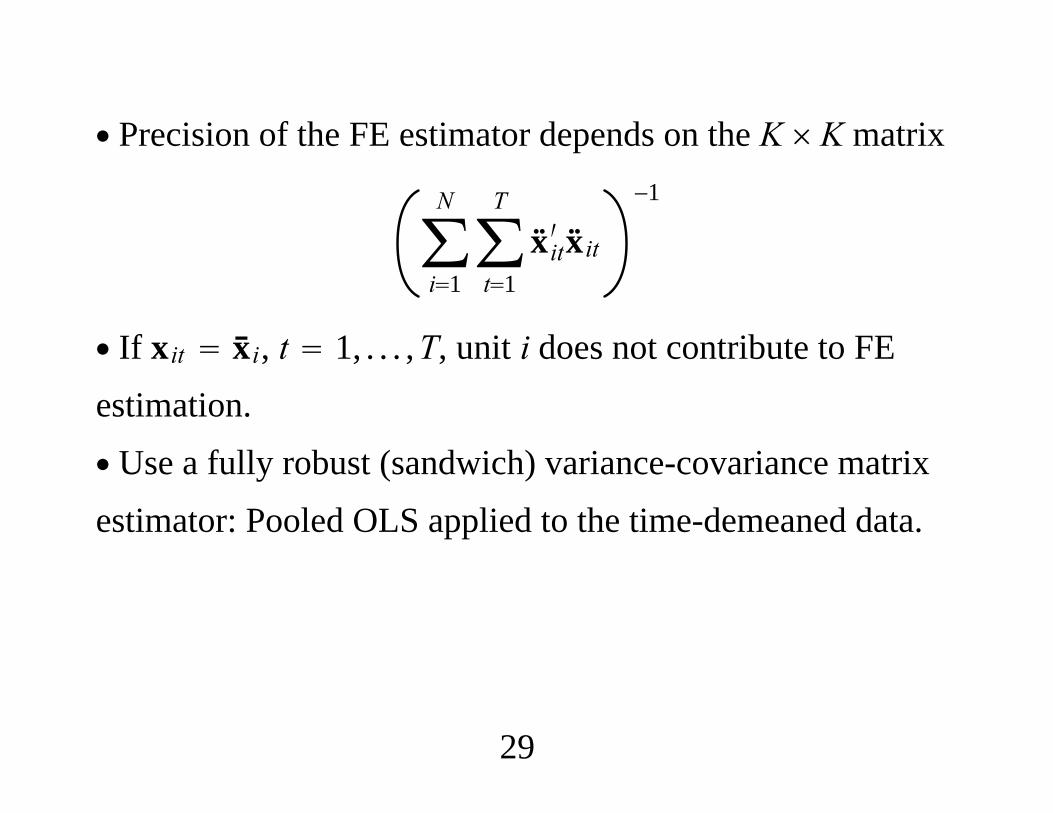

∙ Precision of the FE estimator depends on the K K matrix

∑i1

N

∑t1

T

xit′ xit−1

∙ If xit xi, t 1, . . . ,T, unit i does not contribute to FEestimation.∙ Use a fully robust (sandwich) variance-covariance matrixestimator: Pooled OLS applied to the time-demeaned data.

29

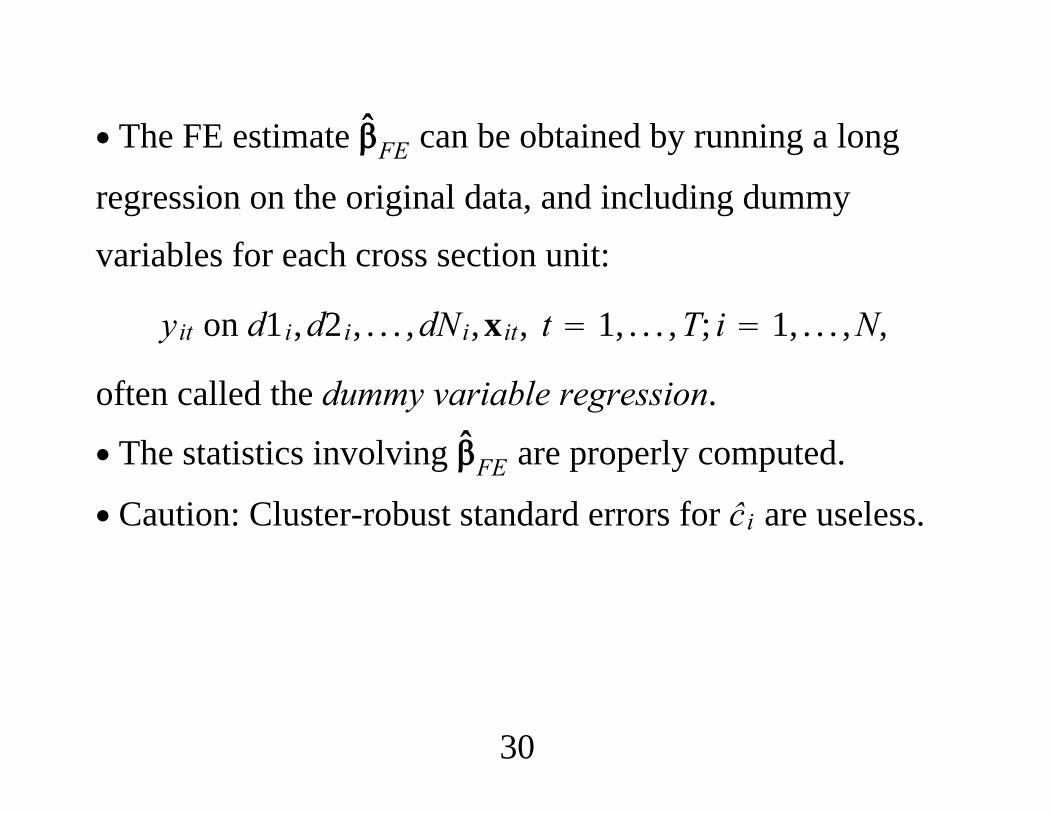

∙ The FE estimate FE can be obtained by running a long

regression on the original data, and including dummyvariables for each cross section unit:

yit on d1i,d2i, . . . ,dNi,xit, t 1, . . . ,T; i 1, . . . ,N,

often called the dummy variable regression.

∙ The statistics involving FE are properly computed.

∙ Caution: Cluster-robust standard errors for ĉi are useless.

30

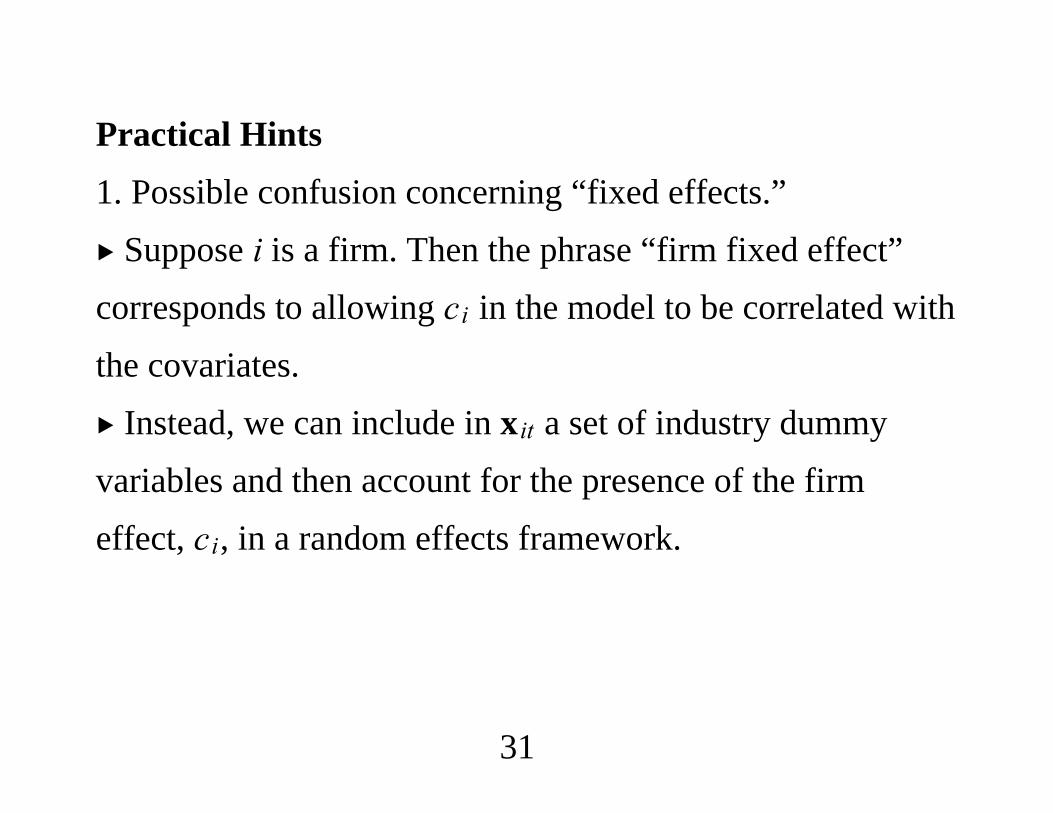

Practical Hints1. Possible confusion concerning “fixed effects.” Suppose i is a firm. Then the phrase “firm fixed effect”corresponds to allowing ci in the model to be correlated withthe covariates. Instead, we can include in xit a set of industry dummyvariables and then account for the presence of the firmeffect, ci, in a random effects framework.

31

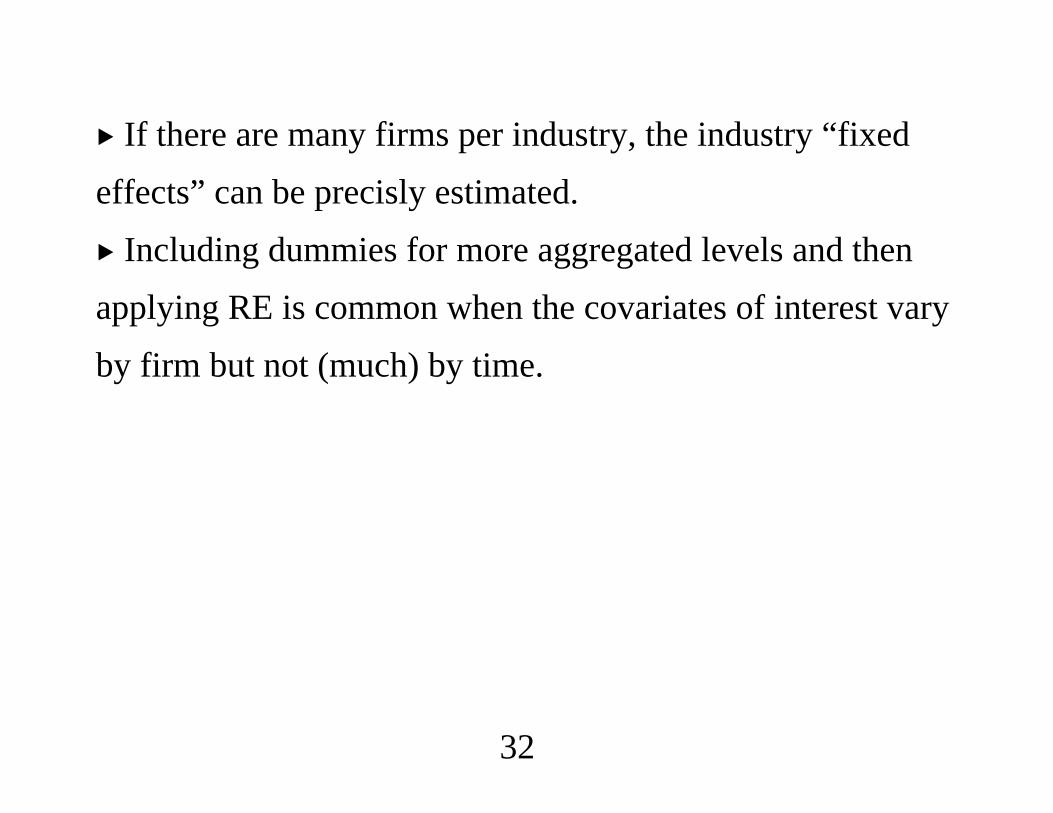

If there are many firms per industry, the industry “fixedeffects” can be precisly estimated. Including dummies for more aggregated levels and thenapplying RE is common when the covariates of interest varyby firm but not (much) by time.

32

2. For most applications, unless T is large, a full set oftime-period effects should be included.(i) Any aggregate time variables are automatically accountedfor.(ii) It guards against spuriously concluding that a policy didor did not have an effect.(iii) Using time dummies can reduce cross-sectionalcorrelation.

33

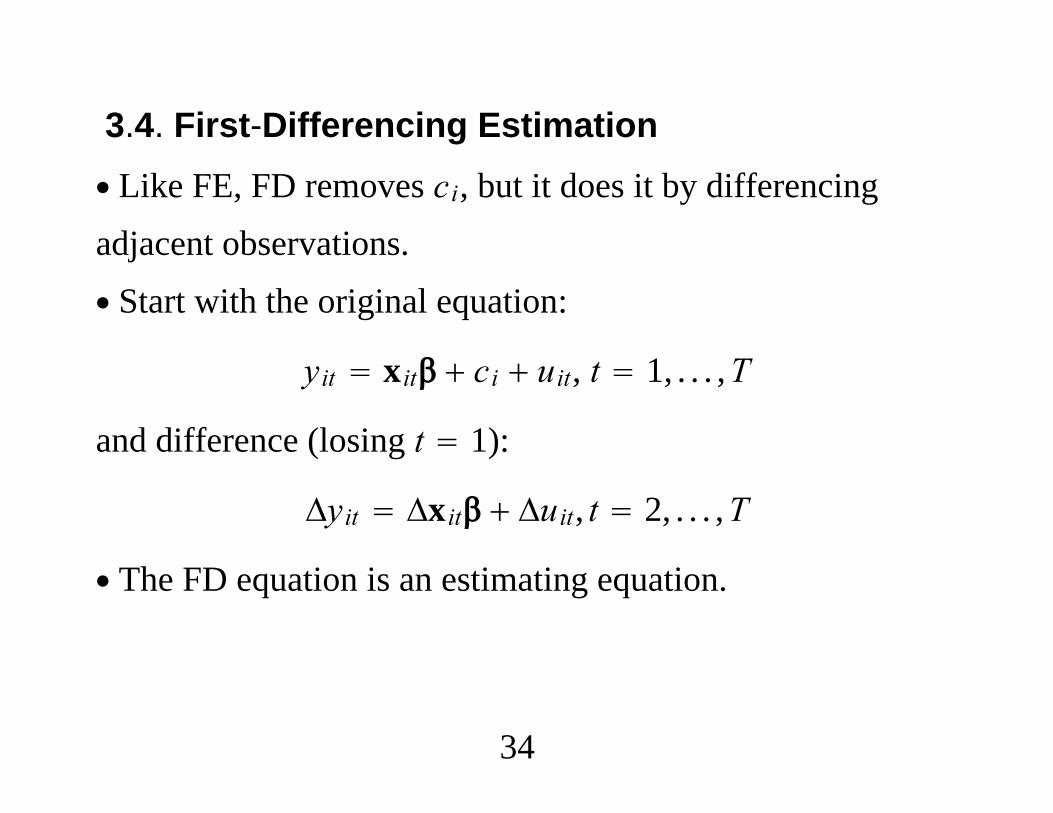

3.4. First-Differencing Estimation∙ Like FE, FD removes ci, but it does it by differencingadjacent observations.∙ Start with the original equation:

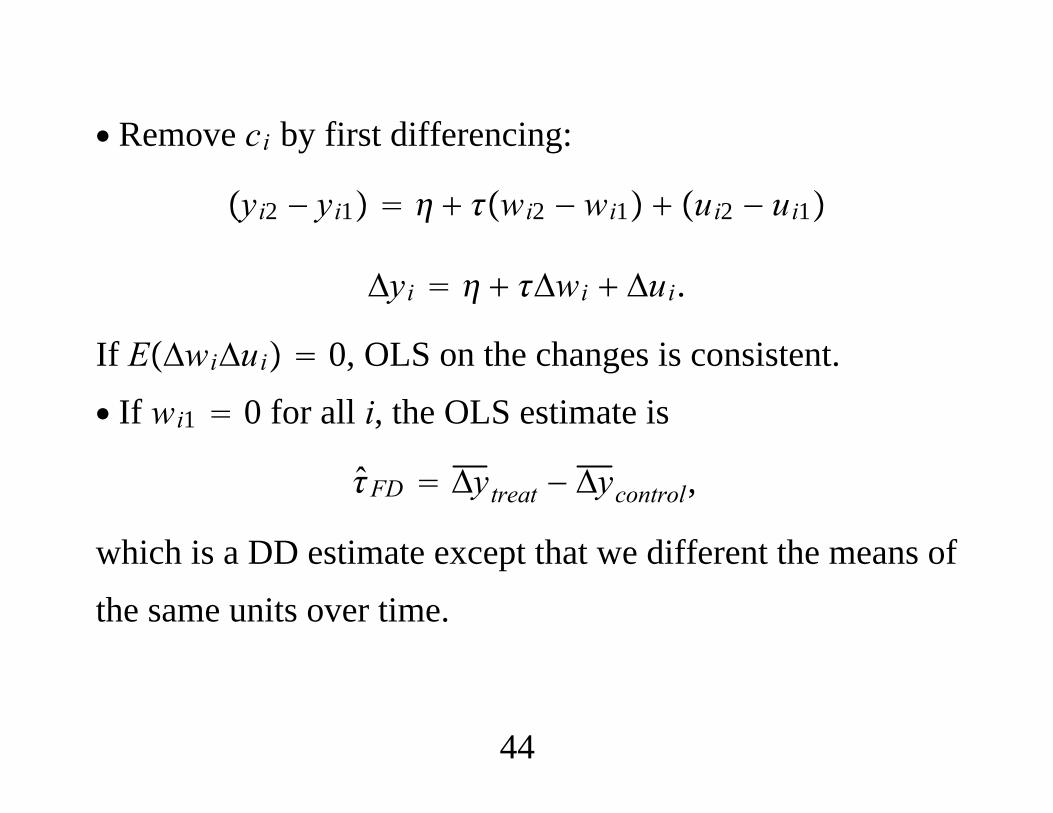

yit xit ci uit, t 1, . . . ,T

and difference (losing t 1):

Δyit Δxit Δuit, t 2, . . . ,T

∙ The FD equation is an estimating equation.

34

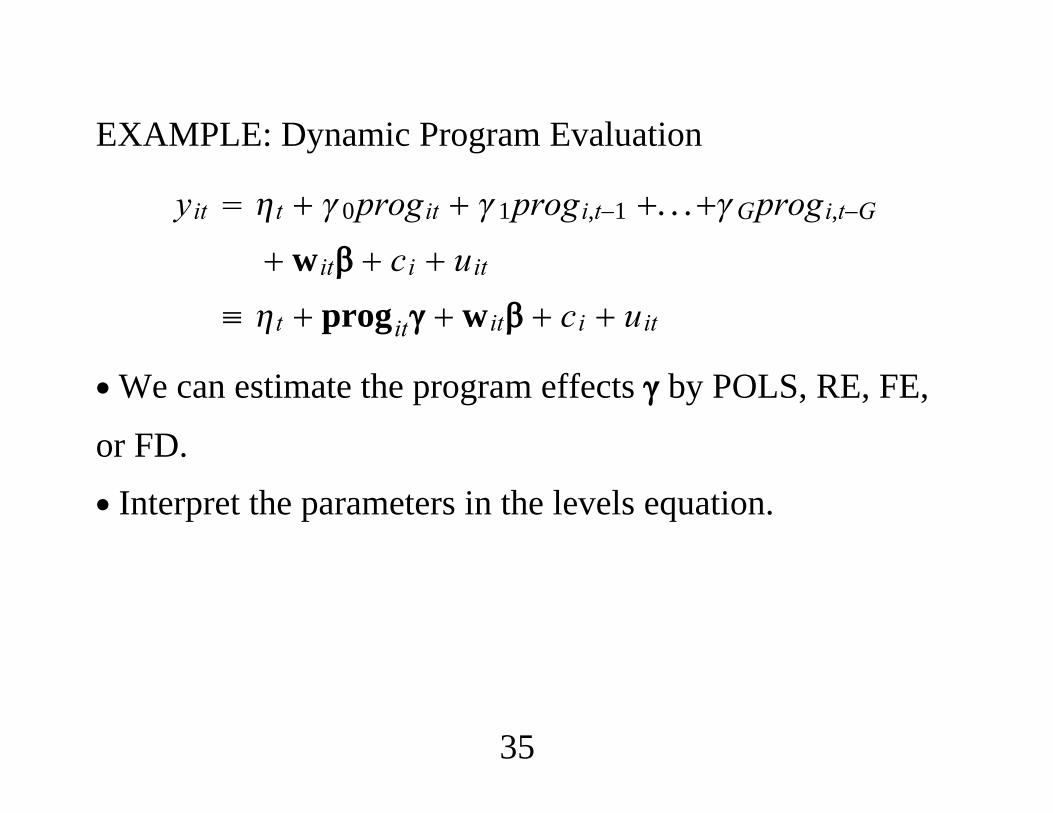

EXAMPLE: Dynamic Program Evaluation

yit t 0progit 1progi,t−1 . . .Gprogi,t−G wit ci uit

≡ t progit wit ci uit

∙We can estimate the program effects by POLS, RE, FE,

or FD.∙ Interpret the parameters in the levels equation.

35

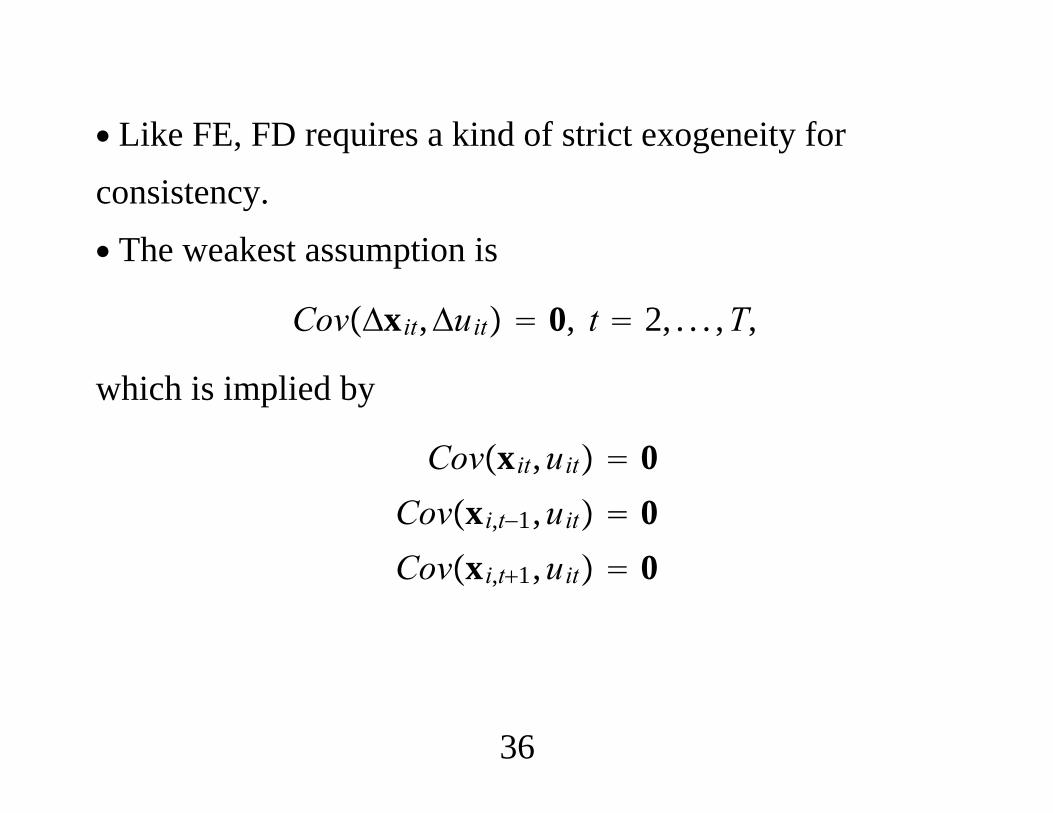

∙ Like FE, FD requires a kind of strict exogeneity forconsistency.∙ The weakest assumption is

CovΔxit,Δuit 0, t 2, . . . ,T,

which is implied by

Covxit,uit 0Covxi,t−1,uit 0Covxi,t1,uit 0

36

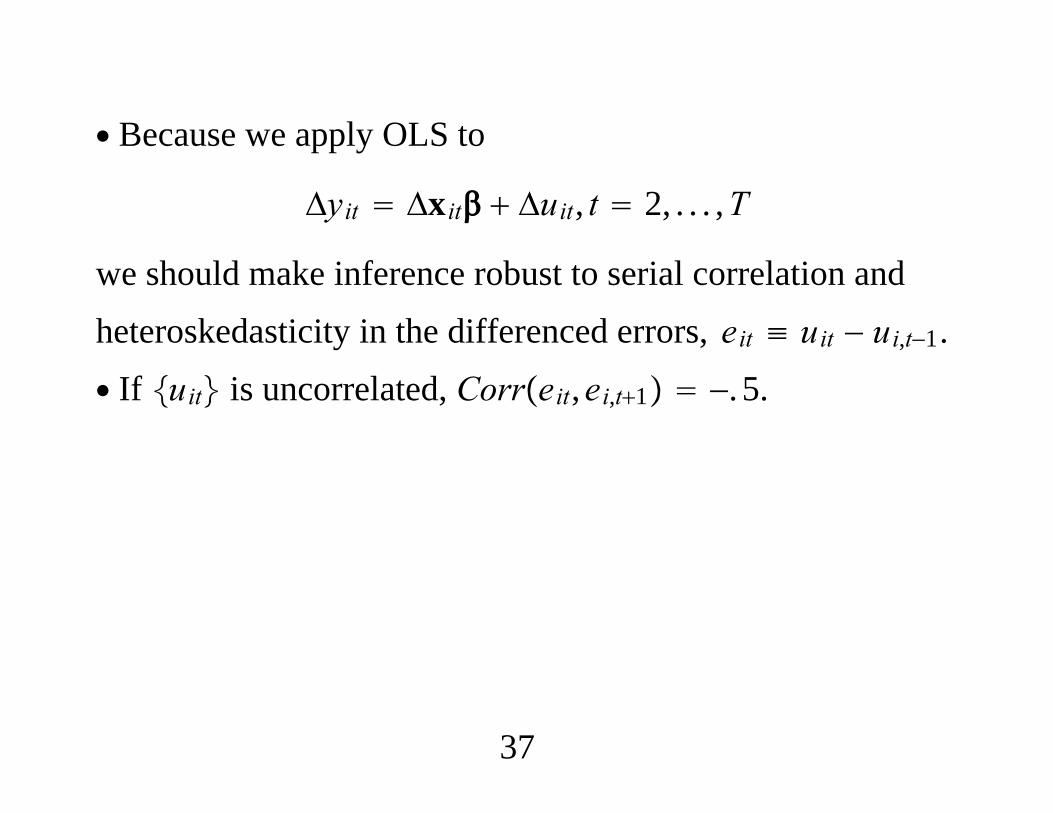

∙ Because we apply OLS to

Δyit Δxit Δuit, t 2, . . . ,T

we should make inference robust to serial correlation andheteroskedasticity in the differenced errors, eit ≡ uit − ui,t−1.∙ If uit is uncorrelated, Correit,ei,t1 −. 5.

37

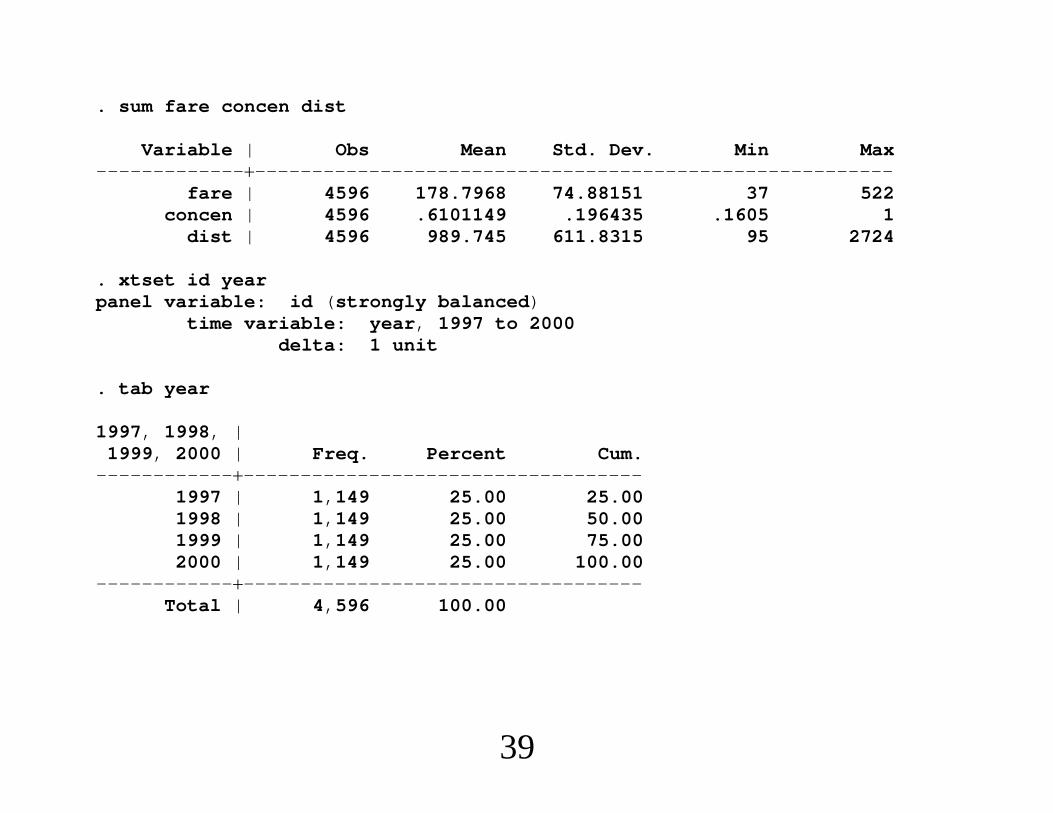

AIRFARE EXAMPLE:∙ For N 1,149 U.S. air routes and the years 1997 through2000, yit is logfareit and the key explanatory variable isconcenit, the concentration ratio for route i.. des fare concen dist

storage display valuevariable name type format label variable label----------------------------------------------------------------------------fare int %9.0g avg. one-way fare, $concen float %9.0g pass. share, larg. carrierdist int %9.0g distance, in miles

38

. sum fare concen dist

Variable | Obs Mean Std. Dev. Min Max---------------------------------------------------------------------

fare | 4596 178.7968 74.88151 37 522concen | 4596 .6101149 .196435 .1605 1

dist | 4596 989.745 611.8315 95 2724

. xtset id yearpanel variable: id (strongly balanced)

time variable: year, 1997 to 2000delta: 1 unit

. tab year

1997, 1998, |1999, 2000 | Freq. Percent Cum.

-----------------------------------------------1997 | 1,149 25.00 25.001998 | 1,149 25.00 50.001999 | 1,149 25.00 75.002000 | 1,149 25.00 100.00

-----------------------------------------------Total | 4,596 100.00

39

. reg lfare concen ldist ldistsq y98 y99 y00

Source | SS df MS Number of obs 4596------------------------------------------- F( 6, 4589) 523.

Model | 355.453858 6 59.2423096 Prob F 0.0000Residual | 519.640516 4589 .113236112 R-squared 0.4062

------------------------------------------- Adj R-squared 0.4054Total | 875.094374 4595 .190444913 Root MSE .33651

----------------------------------------------------------------------------lfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------concen | .3601203 .0300691 11.98 0.000 .3011705 .4190702

ldist | -.9016004 .128273 -7.03 0.000 -1.153077 -.6501235ldistsq | .1030196 .0097255 10.59 0.000 .0839529 .1220863

y98 | .0211244 .0140419 1.50 0.133 -.0064046 .0486533y99 | .0378496 .0140413 2.70 0.007 .010322 .0653772y00 | .09987 .0140432 7.11 0.000 .0723385 .1274015

_cons | 6.209258 .4206247 14.76 0.000 5.384631 7.033884----------------------------------------------------------------------------

. * The above standard errors assume no serial correlation.

40

. reg lfare concen ldist ldistsq y98 y99 y00, cluster(id)

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| Robustlfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------concen | .3601203 .058556 6.15 0.000 .2452315 .4750092

ldist | -.9016004 .2719464 -3.32 0.001 -1.435168 -.3680328ldistsq | .1030196 .0201602 5.11 0.000 .0634647 .1425745

y98 | .0211244 .0041474 5.09 0.000 .0129871 .0292617y99 | .0378496 .0051795 7.31 0.000 .0276872 .048012y00 | .09987 .0056469 17.69 0.000 .0887906 .1109493

_cons | 6.209258 .9117551 6.81 0.000 4.420364 7.998151----------------------------------------------------------------------------

. * Indirect evidence of plenty of serial correlation in the composite error

. * Other than introspection we have no way of knowing whether .360 is a

. * reliable estimate of the concentration effect.

41

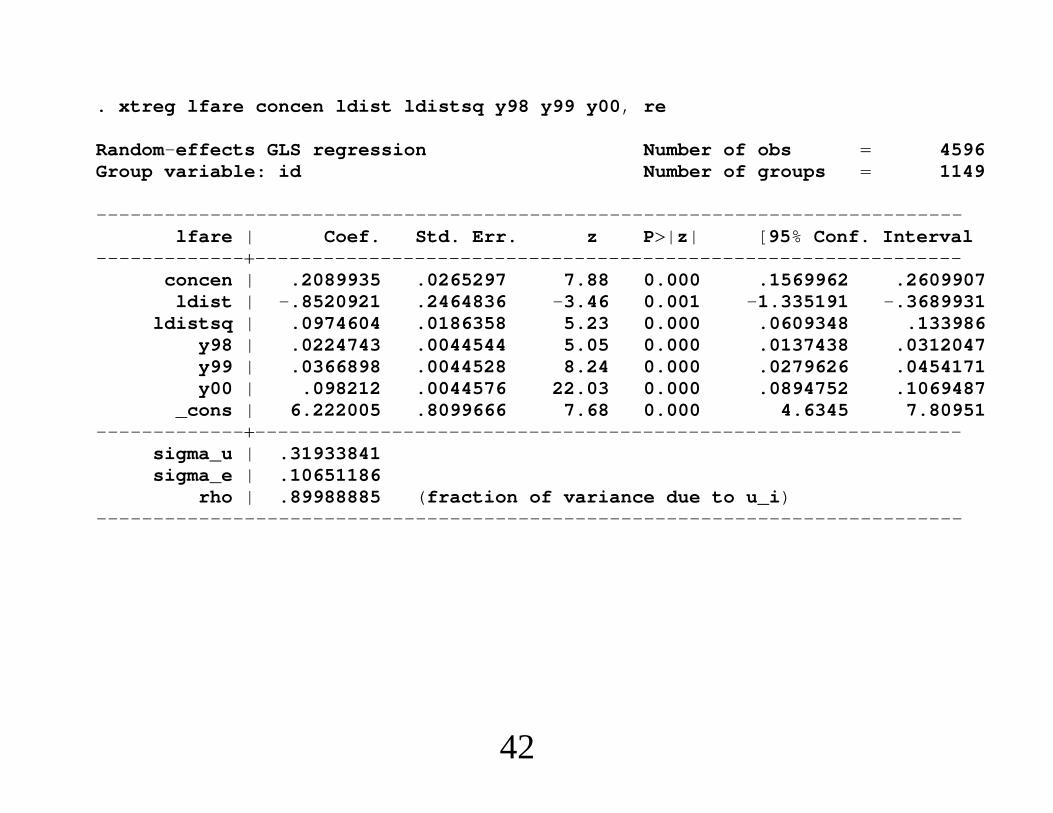

. xtreg lfare concen ldist ldistsq y98 y99 y00, re

Random-effects GLS regression Number of obs 4596Group variable: id Number of groups 1149

----------------------------------------------------------------------------lfare | Coef. Std. Err. z P|z| [95% Conf. Interval

---------------------------------------------------------------------------concen | .2089935 .0265297 7.88 0.000 .1569962 .2609907

ldist | -.8520921 .2464836 -3.46 0.001 -1.335191 -.3689931ldistsq | .0974604 .0186358 5.23 0.000 .0609348 .133986

y98 | .0224743 .0044544 5.05 0.000 .0137438 .0312047y99 | .0366898 .0044528 8.24 0.000 .0279626 .0454171y00 | .098212 .0044576 22.03 0.000 .0894752 .1069487

_cons | 6.222005 .8099666 7.68 0.000 4.6345 7.80951---------------------------------------------------------------------------

sigma_u | .31933841sigma_e | .10651186

rho | .89988885 (fraction of variance due to u_i)----------------------------------------------------------------------------

42

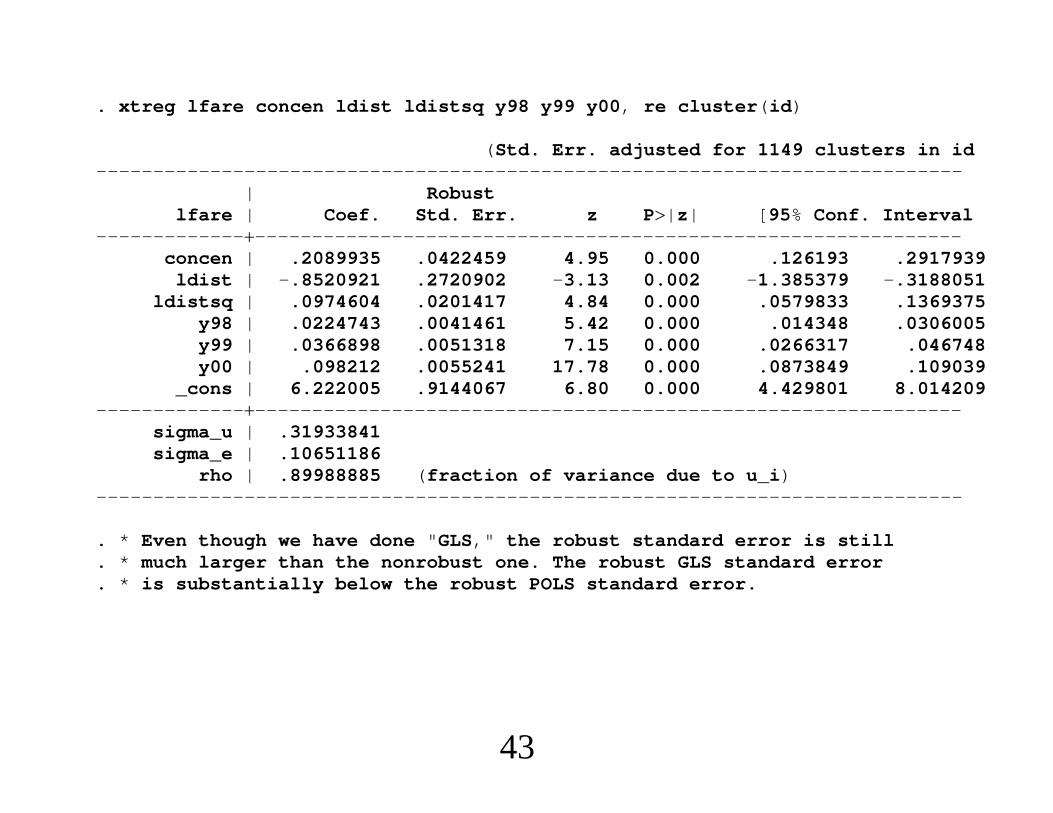

. xtreg lfare concen ldist ldistsq y98 y99 y00, re cluster(id)

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| Robustlfare | Coef. Std. Err. z P|z| [95% Conf. Interval

---------------------------------------------------------------------------concen | .2089935 .0422459 4.95 0.000 .126193 .2917939

ldist | -.8520921 .2720902 -3.13 0.002 -1.385379 -.3188051ldistsq | .0974604 .0201417 4.84 0.000 .0579833 .1369375

y98 | .0224743 .0041461 5.42 0.000 .014348 .0306005y99 | .0366898 .0051318 7.15 0.000 .0266317 .046748y00 | .098212 .0055241 17.78 0.000 .0873849 .109039

_cons | 6.222005 .9144067 6.80 0.000 4.429801 8.014209---------------------------------------------------------------------------

sigma_u | .31933841sigma_e | .10651186

rho | .89988885 (fraction of variance due to u_i)----------------------------------------------------------------------------

. * Even though we have done "GLS," the robust standard error is still

. * much larger than the nonrobust one. The robust GLS standard error

. * is substantially below the robust POLS standard error.

43

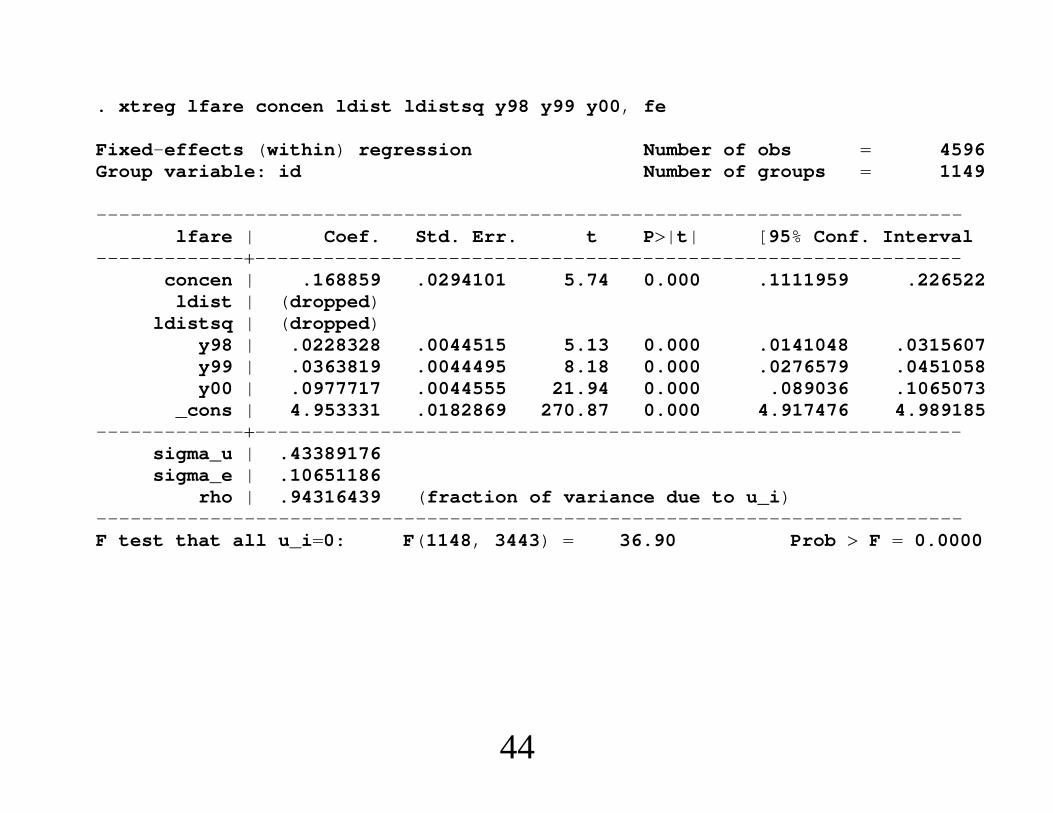

. xtreg lfare concen ldist ldistsq y98 y99 y00, fe

Fixed-effects (within) regression Number of obs 4596Group variable: id Number of groups 1149

----------------------------------------------------------------------------lfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------concen | .168859 .0294101 5.74 0.000 .1111959 .226522

ldist | (dropped)ldistsq | (dropped)

y98 | .0228328 .0044515 5.13 0.000 .0141048 .0315607y99 | .0363819 .0044495 8.18 0.000 .0276579 .0451058y00 | .0977717 .0044555 21.94 0.000 .089036 .1065073

_cons | 4.953331 .0182869 270.87 0.000 4.917476 4.989185---------------------------------------------------------------------------

sigma_u | .43389176sigma_e | .10651186

rho | .94316439 (fraction of variance due to u_i)----------------------------------------------------------------------------F test that all u_i0: F(1148, 3443) 36.90 Prob F 0.0000

44

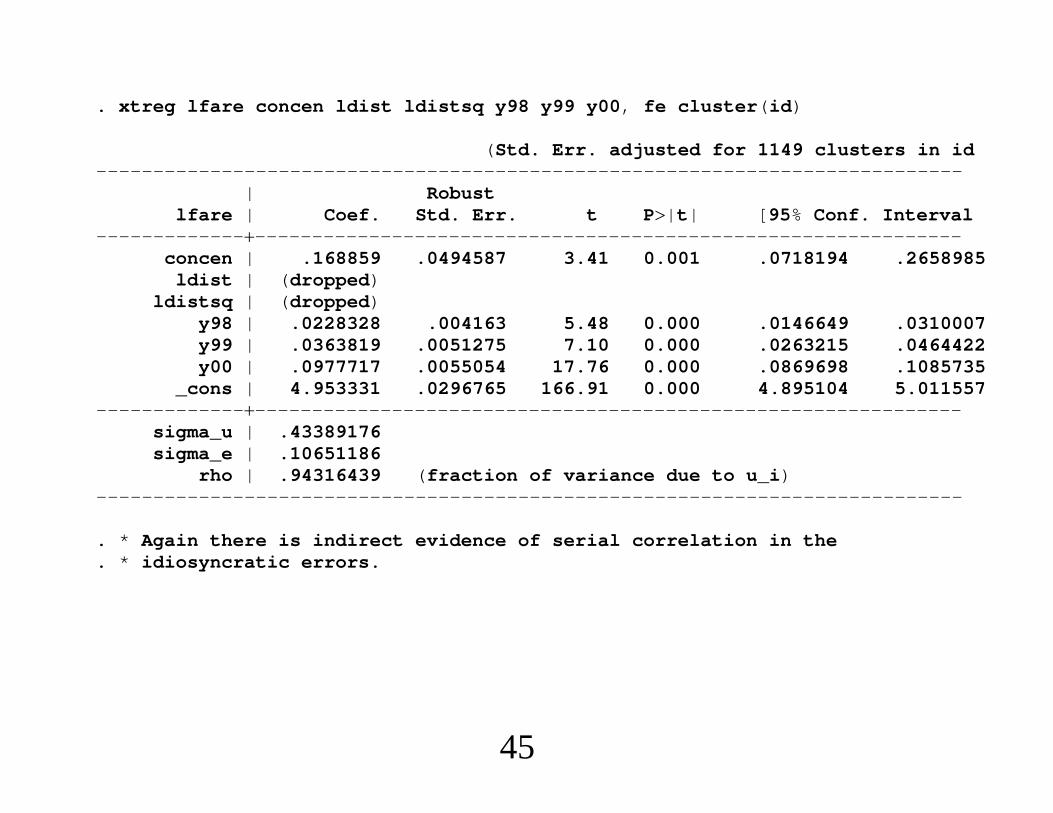

. xtreg lfare concen ldist ldistsq y98 y99 y00, fe cluster(id)

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| Robustlfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------concen | .168859 .0494587 3.41 0.001 .0718194 .2658985

ldist | (dropped)ldistsq | (dropped)

y98 | .0228328 .004163 5.48 0.000 .0146649 .0310007y99 | .0363819 .0051275 7.10 0.000 .0263215 .0464422y00 | .0977717 .0055054 17.76 0.000 .0869698 .1085735

_cons | 4.953331 .0296765 166.91 0.000 4.895104 5.011557---------------------------------------------------------------------------

sigma_u | .43389176sigma_e | .10651186

rho | .94316439 (fraction of variance due to u_i)----------------------------------------------------------------------------

. * Again there is indirect evidence of serial correlation in the

. * idiosyncratic errors.

45

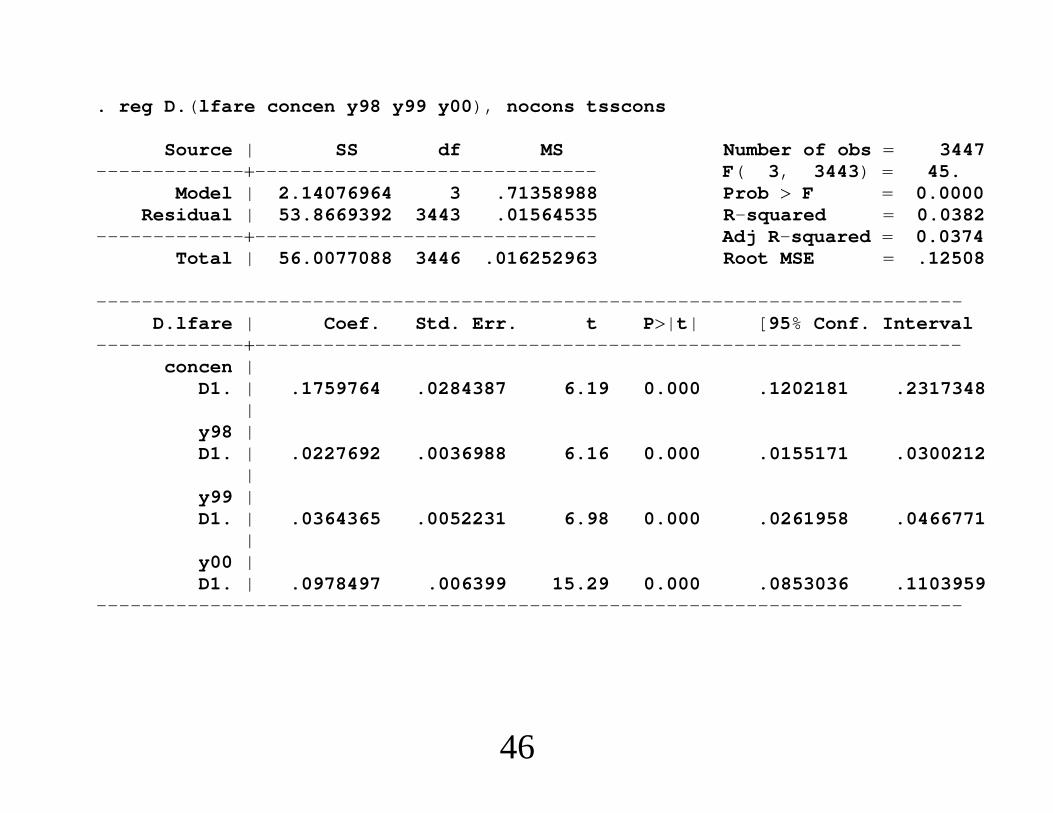

. reg D.(lfare concen y98 y99 y00), nocons tsscons

Source | SS df MS Number of obs 3447------------------------------------------- F( 3, 3443) 45.

Model | 2.14076964 3 .71358988 Prob F 0.0000Residual | 53.8669392 3443 .01564535 R-squared 0.0382

------------------------------------------- Adj R-squared 0.0374Total | 56.0077088 3446 .016252963 Root MSE .12508

----------------------------------------------------------------------------D.lfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------concen |

D1. | .1759764 .0284387 6.19 0.000 .1202181 .2317348|

y98 |D1. | .0227692 .0036988 6.16 0.000 .0155171 .0300212

|y99 |D1. | .0364365 .0052231 6.98 0.000 .0261958 .0466771

|y00 |D1. | .0978497 .006399 15.29 0.000 .0853036 .1103959

----------------------------------------------------------------------------

46

. reg D.(lfare concen y98 y99 y00), nocons tsscons cluster(id)

Linear regression Number of obs 3447F( 3, 1148) 26.Prob F 0.0000

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| RobustD.lfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------concen |

D1. | .1759764 .0430367 4.09 0.000 .0915371 .2604158|

y98 |D1. | .0227692 .0041573 5.48 0.000 .0146124 .030926

|y99 |D1. | .0364365 .005153 7.07 0.000 .026326 .0465469

|y00 |D1. | .0978497 .0055468 17.64 0.000 .0869666 .1087328

----------------------------------------------------------------------------

47

4. Comparing RE and FE∙ FE allows for correlation between ci and xit.∙ Time-constant variables drop out of FE estimation.Removes much of the covariate variation.∙ FE has more robustness to heterogeneous slopes.

48

yit ci xitbi uitEuit|xi,ci,bi 0, t 1, . . . ,T,

where bi is K 1.∙ Apply usual FE estimator. (Act as if bi constant.)∙ Define the average partial effects, Ebi?

49

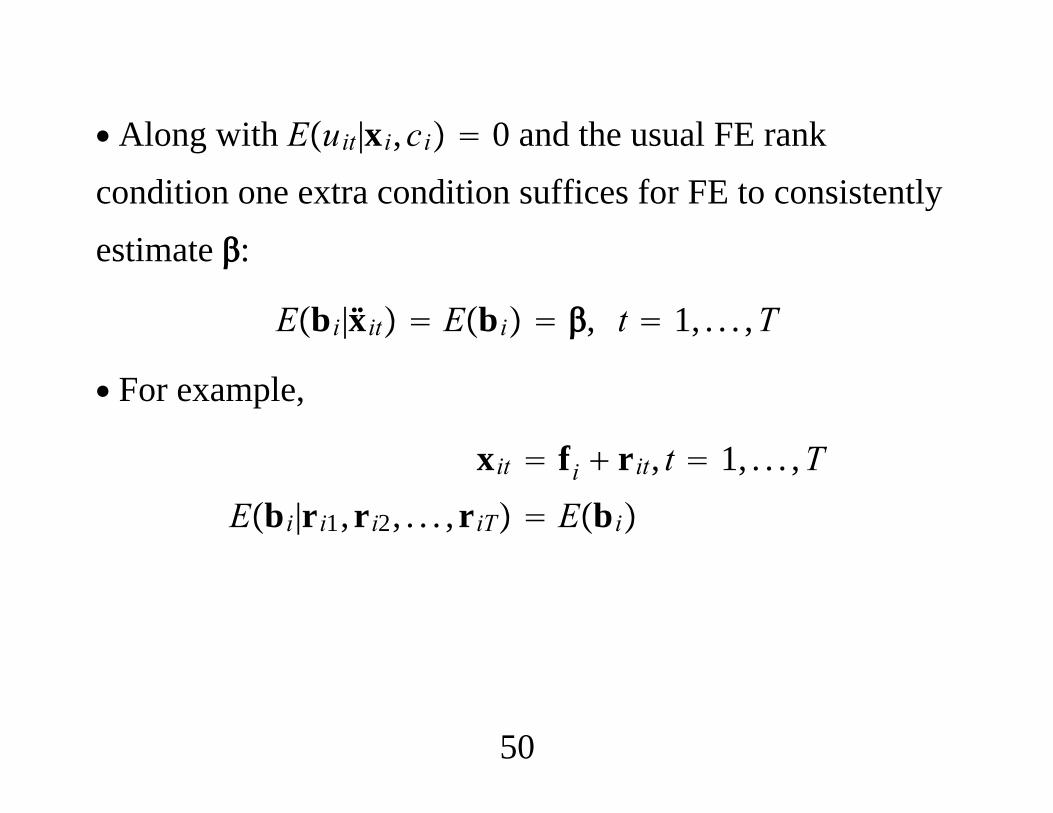

∙ Along with Euit|xi,ci 0 and the usual FE rankcondition one extra condition suffices for FE to consistentlyestimate :

Ebi|xit Ebi , t 1, . . . ,T

∙ For example,

xit fi rit, t 1, . . . ,TEbi|ri1,ri2, . . . ,riT Ebi

50

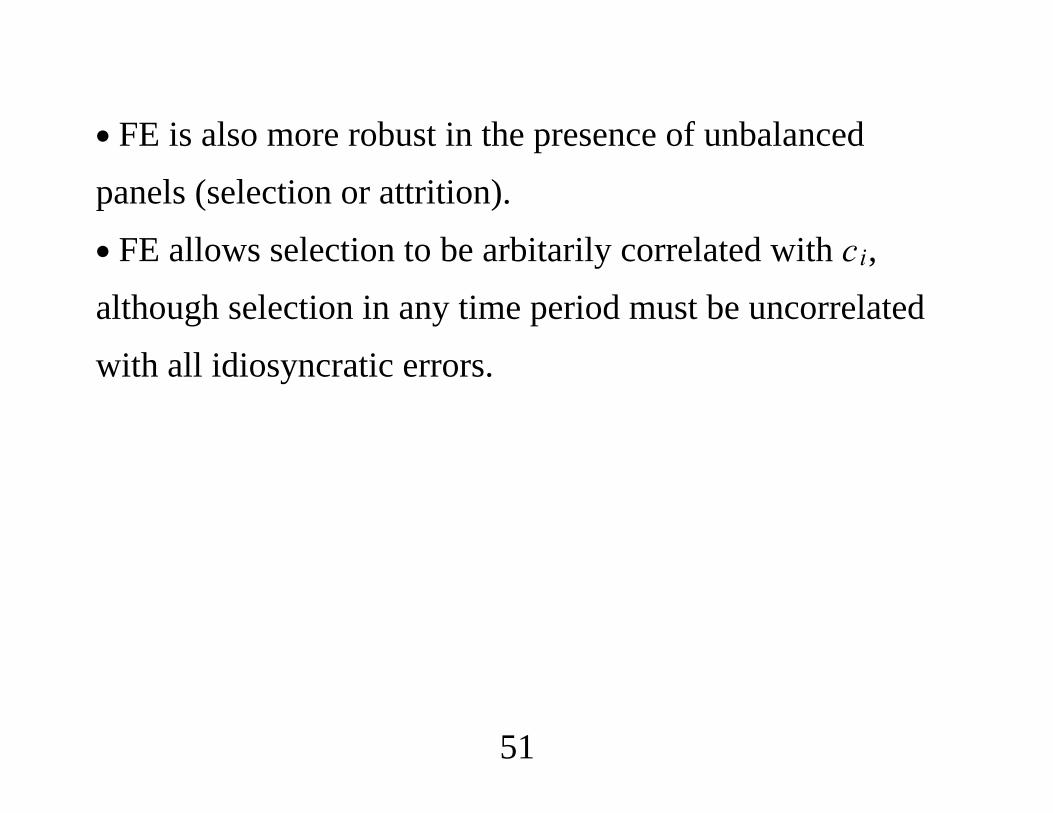

∙ FE is also more robust in the presence of unbalancedpanels (selection or attrition).∙ FE allows selection to be arbitarily correlated with ci,although selection in any time period must be uncorrelatedwith all idiosyncratic errors.

51

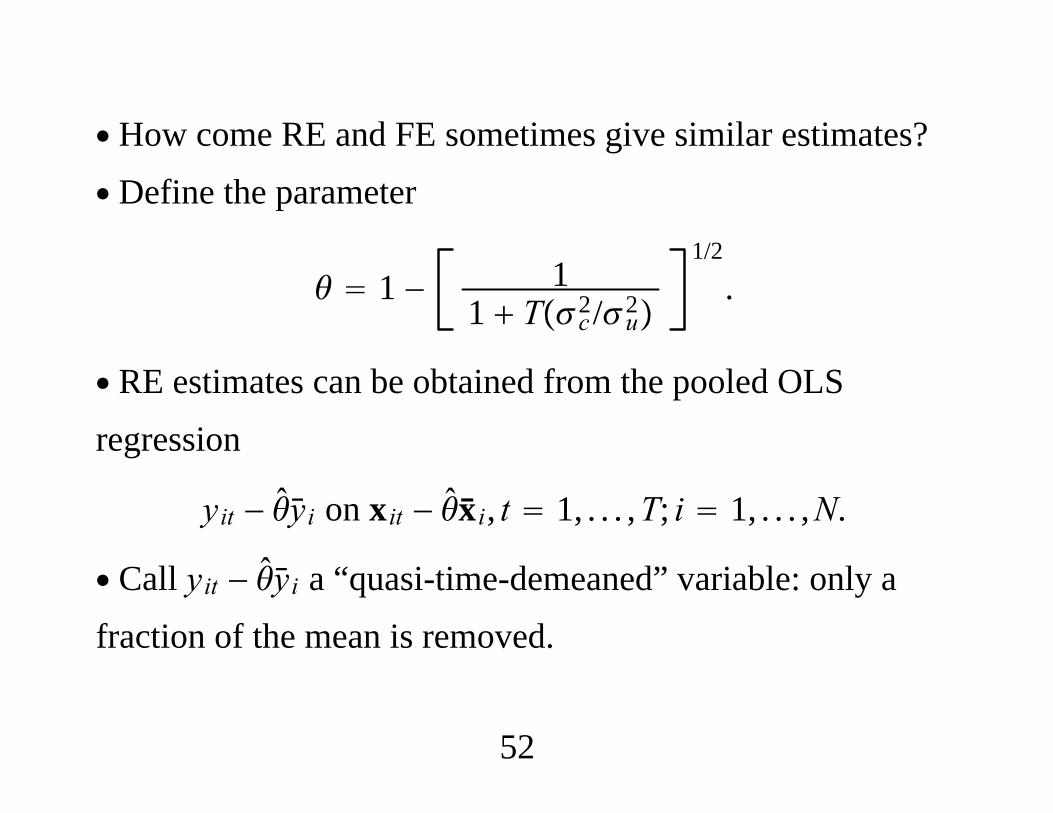

∙ How come RE and FE sometimes give similar estimates?∙ Define the parameter

1 − 11 Tc2/u2

1/2

.

∙ RE estimates can be obtained from the pooled OLSregression

yit − yi on xit − xi, t 1, . . . ,T; i 1, . . . ,N.

∙ Call yit − yi a “quasi-time-demeaned” variable: only afraction of the mean is removed.

52

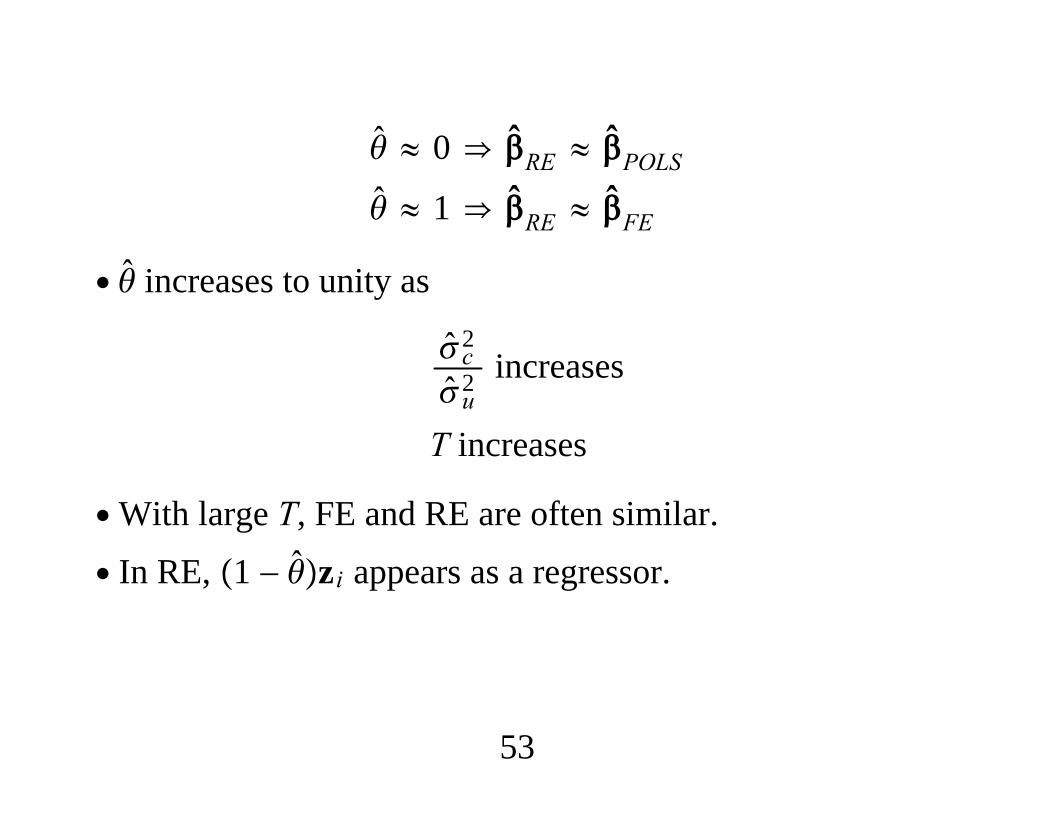

≈ 0 RE ≈ POLS ≈ 1 RE ≈ FE

∙ increases to unity as

c2

u2increases

T increases

∙With large T, FE and RE are often similar.

∙ In RE, 1 − zi appears as a regressor.

53

Testing the Key RE Assumption∙ Both RE and FE require strict exogeneity,Covxis,uit 0, all s and t.∙ RE adds the assumpiton Covxit,ci 0 for all t.∙We can test Covxit,ci 0 by comparing the RE and FEestimates, but care is needed.

54

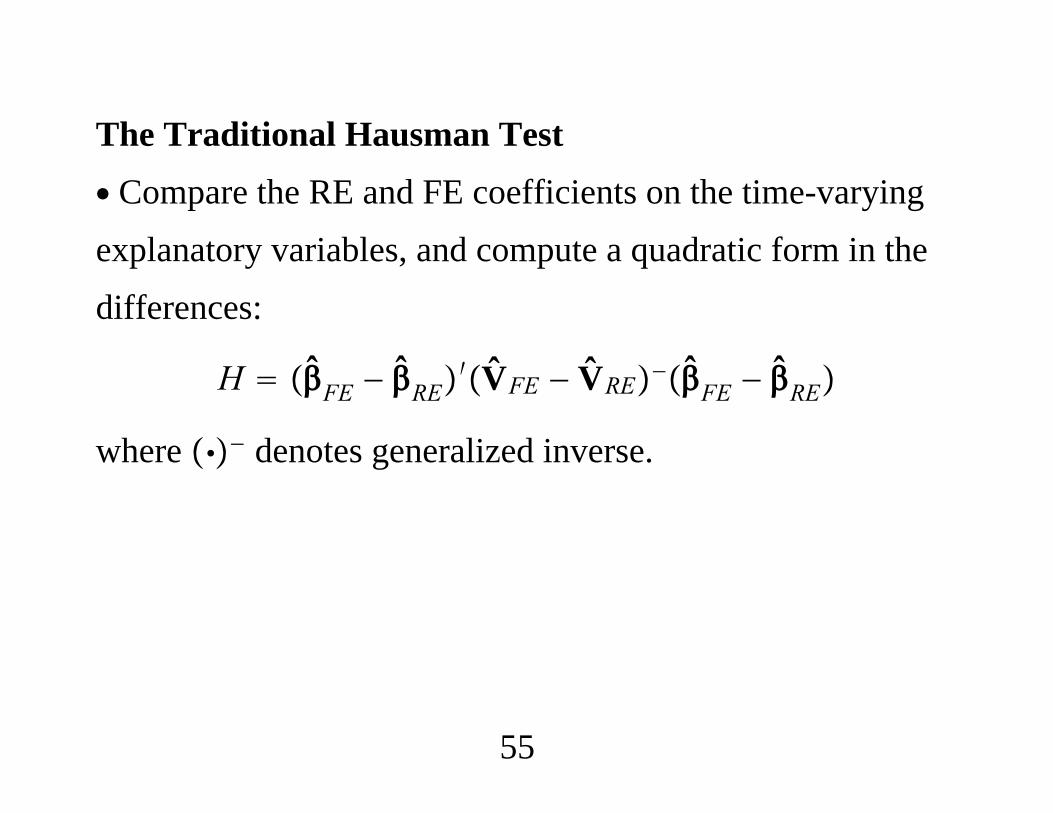

The Traditional Hausman Test∙ Compare the RE and FE coefficients on the time-varyingexplanatory variables, and compute a quadratic form in thedifferences:

H FE − RE′VFE − VRE−FE − RE

where − denotes generalized inverse.

55

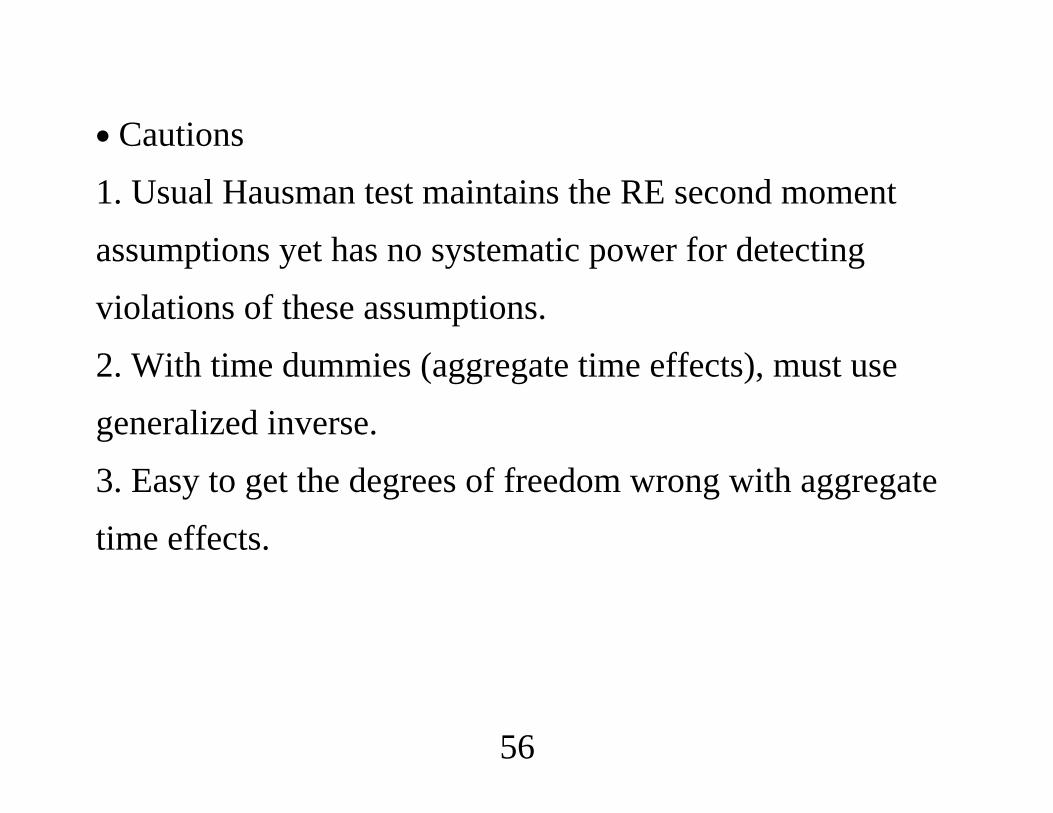

∙ Cautions1. Usual Hausman test maintains the RE second momentassumptions yet has no systematic power for detectingviolations of these assumptions.2. With time dummies (aggregate time effects), must usegeneralized inverse.3. Easy to get the degrees of freedom wrong with aggregatetime effects.

56

Variable Addition Test (VAT)∙Write the model as

yit gt zi wit ci uit.

∙ Cannot compare FE and RE estimates of .∙ Less obvious: Cannot compare FE and RE estimates of .

We can obtain FE and RE, but there is a degeneracy.∙We can only compare FE and RE.

57

∙ Correlated random effects (CRE) approach:

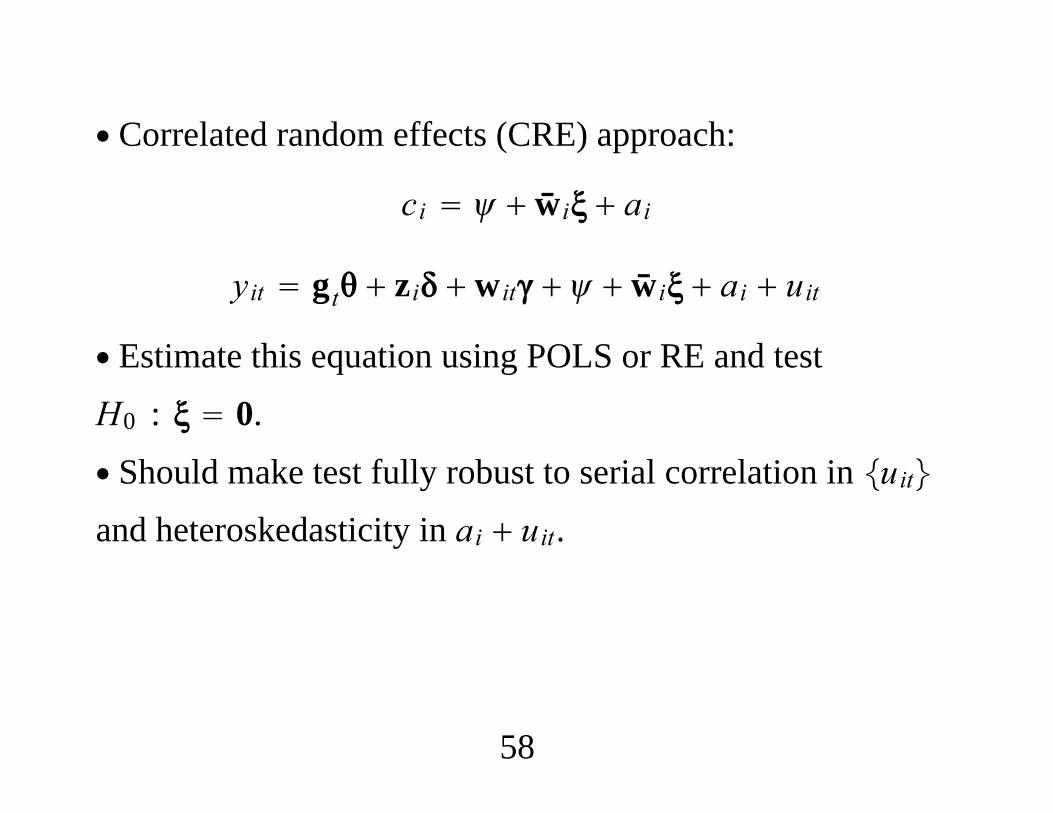

ci wi ai

yit gt zi wit wi ai uit

∙ Estimate this equation using POLS or RE and testH0 : 0.

∙ Should make test fully robust to serial correlation in uitand heteroskedasticity in ai uit.

58

∙ Important Algebraic Result: The RE estimate of ,

when wi is included is the FE estimate.∙ POLS and RE of all coefficients with wi are identical.∙ Including wi effectively proxies for ci (even though ai isstill in error term).∙ Implication of Algebraic Result: Test is valid for anyrelationship between ci and wi1,wi2, . . . ,wiT.

59

∙ CRE unifies RE and FE.∙ In the equation

yit gt zi wit wi ai uit

under the full set of RE assumptions, RE is the true GLSestimator and RE properly imposes 0.

∙ So RE is asymptotically more efficient than FE (under fullRE assumptions).

60

∙ Guggenberger (2010, Journal of Econometrics) studies thepretesting problem with the traditional Hausman test.∙ The VAT version of the test shows it is the classic problemof pre-testing on a set of regressors, wi.∙ If ≠ 0 but the test has low power, we will omit wi when

we should include it. That is, we will incorrectly opt for RE.

61

∙ Apply to airfare model:. * First use the Hausman test that maintains all of the RE assumptions under. * the null:

. qui xtreg lfare concen ldist ldistsq y98 y99 y00, fe

. estimates store b_fe

. qui xtreg lfare concen ldist ldistsq y98 y99 y00, re

. estimates store b_re

62

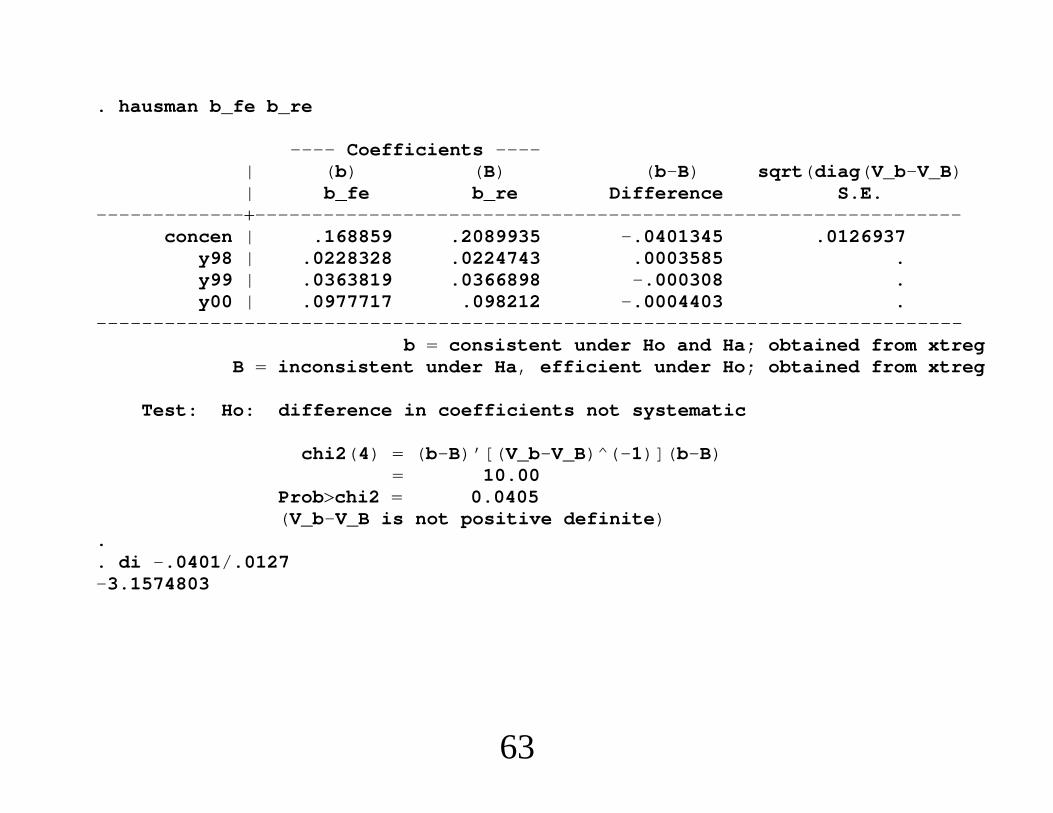

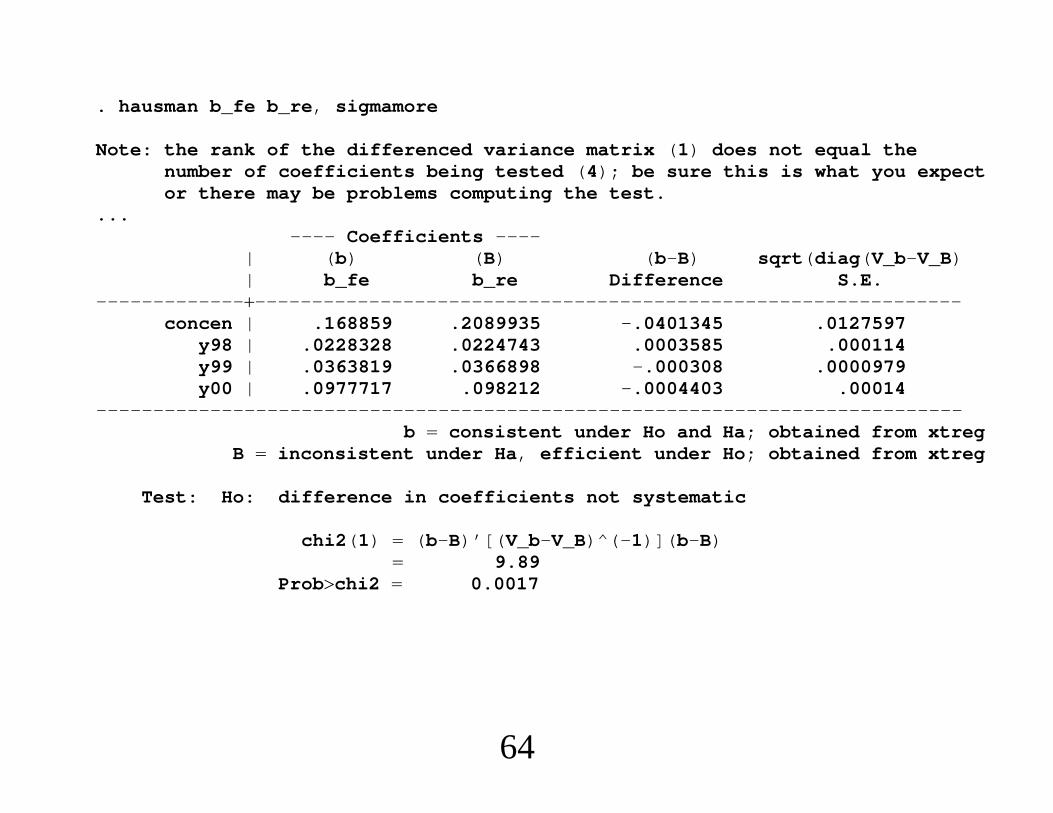

. hausman b_fe b_re

---- Coefficients ----| (b) (B) (b-B) sqrt(diag(V_b-V_B)| b_fe b_re Difference S.E.

---------------------------------------------------------------------------concen | .168859 .2089935 -.0401345 .0126937

y98 | .0228328 .0224743 .0003585 .y99 | .0363819 .0366898 -.000308 .y00 | .0977717 .098212 -.0004403 .

----------------------------------------------------------------------------b consistent under Ho and Ha; obtained from xtreg

B inconsistent under Ha, efficient under Ho; obtained from xtreg

Test: Ho: difference in coefficients not systematic

chi2(4) (b-B)’[(V_b-V_B)^(-1)](b-B) 10.00

Probchi2 0.0405(V_b-V_B is not positive definite)

.

. di -.0401/.0127-3.1574803

63

. hausman b_fe b_re, sigmamore

Note: the rank of the differenced variance matrix (1) does not equal thenumber of coefficients being tested (4); be sure this is what you expector there may be problems computing the test.

...---- Coefficients ----

| (b) (B) (b-B) sqrt(diag(V_b-V_B)| b_fe b_re Difference S.E.

---------------------------------------------------------------------------concen | .168859 .2089935 -.0401345 .0127597

y98 | .0228328 .0224743 .0003585 .000114y99 | .0363819 .0366898 -.000308 .0000979y00 | .0977717 .098212 -.0004403 .00014

----------------------------------------------------------------------------b consistent under Ho and Ha; obtained from xtreg

B inconsistent under Ha, efficient under Ho; obtained from xtreg

Test: Ho: difference in coefficients not systematic

chi2(1) (b-B)’[(V_b-V_B)^(-1)](b-B) 9.89

Probchi2 0.0017

64

. egen concenbar mean(concen), by(id)

. xtreg lfare concen concenbar ldist ldistsq y98 y99 y00, re cluster(id)

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| Robustlfare | Coef. Std. Err. z P|z| [95% Conf. Interval

---------------------------------------------------------------------------concen | .168859 .0494749 3.41 0.001 .07189 .2658279

concenbar | .2136346 .0816403 2.62 0.009 .0536227 .3736466ldist | -.9089297 .2721637 -3.34 0.001 -1.442361 -.3754987

ldistsq | .1038426 .0201911 5.14 0.000 .0642688 .1434164y98 | .0228328 .0041643 5.48 0.000 .0146708 .0309947y99 | .0363819 .0051292 7.09 0.000 .0263289 .0464349y00 | .0977717 .0055072 17.75 0.000 .0869777 .1085656

_cons | 6.207889 .9118109 6.81 0.000 4.420773 7.995006---------------------------------------------------------------------------

sigma_u | .31933841sigma_e | .10651186

rho | .89988885 (fraction of variance due to u_i)----------------------------------------------------------------------------

. * The robust t statistic is 2.62 --- still a rejection, but not as strong.

65

Coefficients on Time-Constant Variables∙What if in

yit gt zi wit ci uit

we assume

Covzi,ci 0

but want to allow

Covwit,ci ≠ 0?

66

∙ Simple estimator: Use 1,gt,zi, wit as instruments in a

pooled IV procedure. Special case of Hausman-Taylor.∙ The estimator of , is the usual FE estimator.

∙ Use cluster-robust inference.∙ Contrast with the CRE approach: POLS (RE) applied to

yit gt zi wit wi ai uit,

which partials out wi.∙ Identical to pooled IV with instruments 1,gt,zi, wit, wi.

67

5. Comparing FE and FD∙ FE and FD are different ways of estimating

yit xit ci uit, t 1, . . . ,T

∙ Estimates and inference are numerically identical whenT 2.∙ Often see differences as T increases.∙With T 2, FE and FD use different implications of strictexogeneity.

68

∙ If strict exogeneity holds, choice between FE and FDcomes down to the nature of the serial correlation in uit.

With little serial correlation, FE is preferred. With lots of serial correlation, FD is preferred.

∙ Try both with cluster-robust inference!∙ Feasible GLS with unrestricted correlations on the FDequation is easy.

69

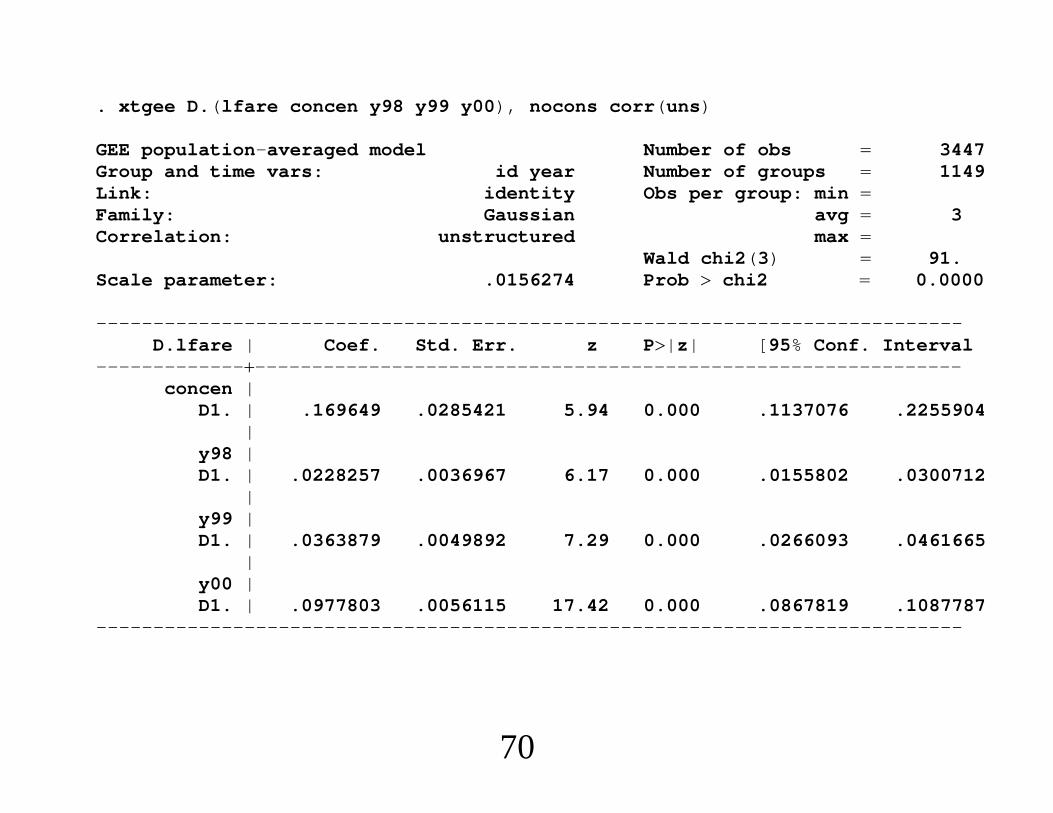

. xtgee D.(lfare concen y98 y99 y00), nocons corr(uns)

GEE population-averaged model Number of obs 3447Group and time vars: id year Number of groups 1149Link: identity Obs per group: min Family: Gaussian avg 3Correlation: unstructured max

Wald chi2(3) 91.Scale parameter: .0156274 Prob chi2 0.0000

----------------------------------------------------------------------------D.lfare | Coef. Std. Err. z P|z| [95% Conf. Interval

---------------------------------------------------------------------------concen |

D1. | .169649 .0285421 5.94 0.000 .1137076 .2255904|

y98 |D1. | .0228257 .0036967 6.17 0.000 .0155802 .0300712

|y99 |D1. | .0363879 .0049892 7.29 0.000 .0266093 .0461665

|y00 |D1. | .0977803 .0056115 17.42 0.000 .0867819 .1087787

----------------------------------------------------------------------------

70

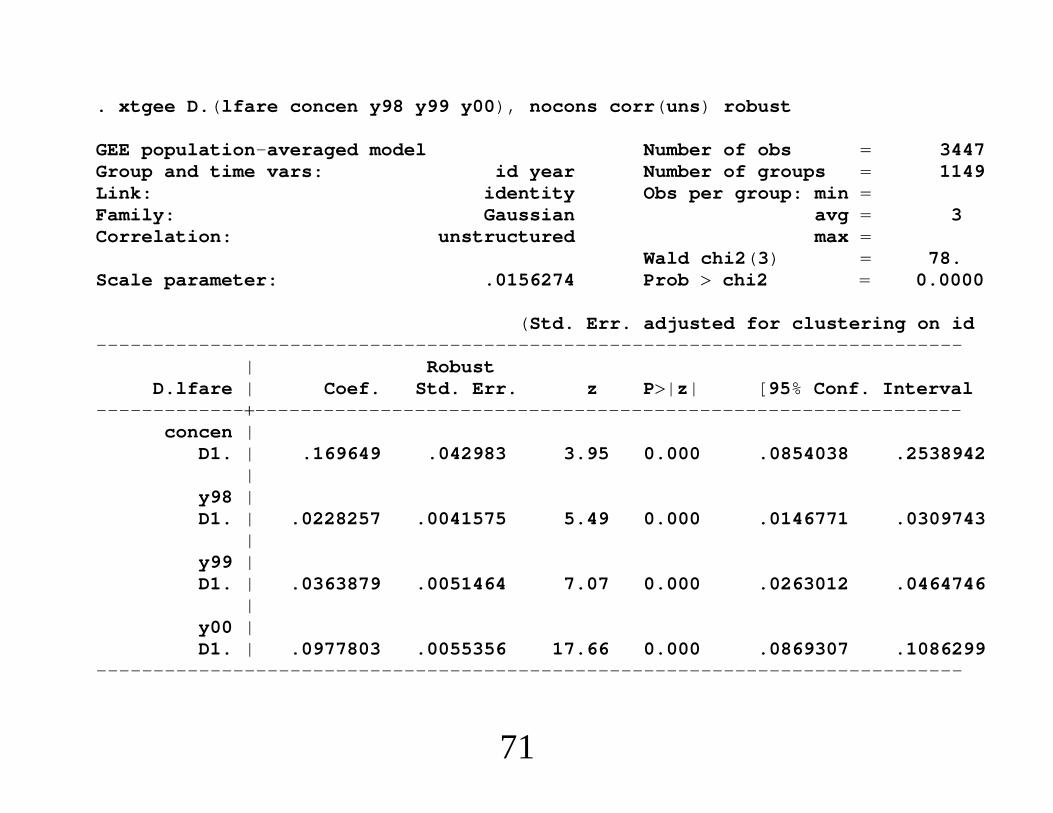

. xtgee D.(lfare concen y98 y99 y00), nocons corr(uns) robust

GEE population-averaged model Number of obs 3447Group and time vars: id year Number of groups 1149Link: identity Obs per group: min Family: Gaussian avg 3Correlation: unstructured max

Wald chi2(3) 78.Scale parameter: .0156274 Prob chi2 0.0000

(Std. Err. adjusted for clustering on id----------------------------------------------------------------------------

| RobustD.lfare | Coef. Std. Err. z P|z| [95% Conf. Interval

---------------------------------------------------------------------------concen |

D1. | .169649 .042983 3.95 0.000 .0854038 .2538942|

y98 |D1. | .0228257 .0041575 5.49 0.000 .0146771 .0309743

|y99 |D1. | .0363879 .0051464 7.07 0.000 .0263012 .0464746

|y00 |D1. | .0977803 .0055356 17.66 0.000 .0869307 .1086299

----------------------------------------------------------------------------

71

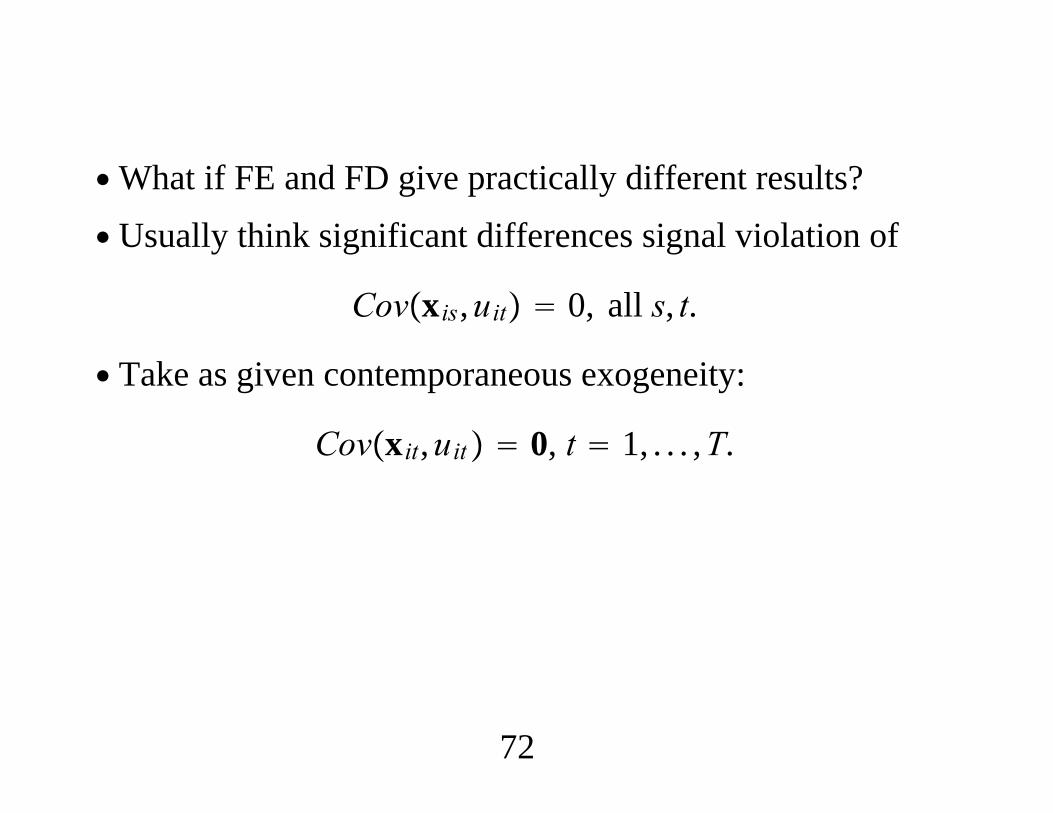

∙What if FE and FD give practically different results?∙ Usually think significant differences signal violation of

Covxis,uit 0, all s, t.

∙ Take as given contemporaneous exogeneity:

Covxit,uit 0, t 1, . . . ,T.

72

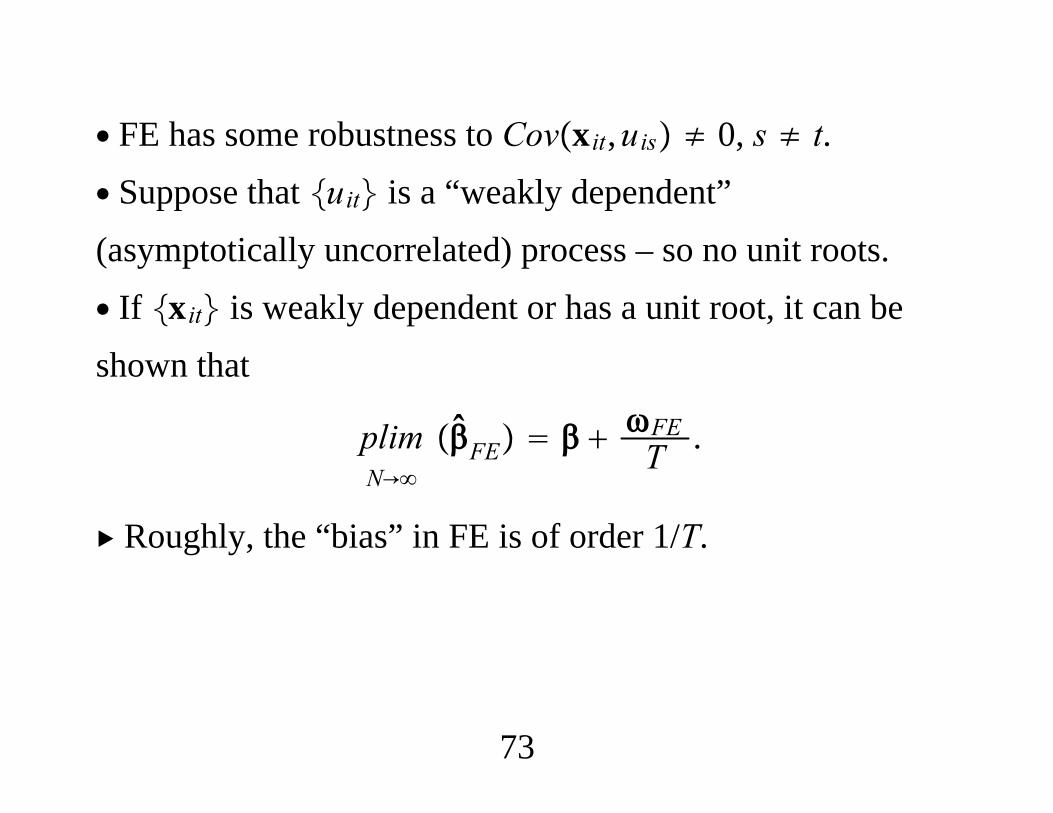

∙ FE has some robustness to Covxit,uis ≠ 0, s ≠ t.∙ Suppose that uit is a “weakly dependent”(asymptotically uncorrelated) process – so no unit roots.∙ If xit is weakly dependent or has a unit root, it can beshown that

N→plim FE FE

T .

Roughly, the “bias” in FE is of order 1/T.

73

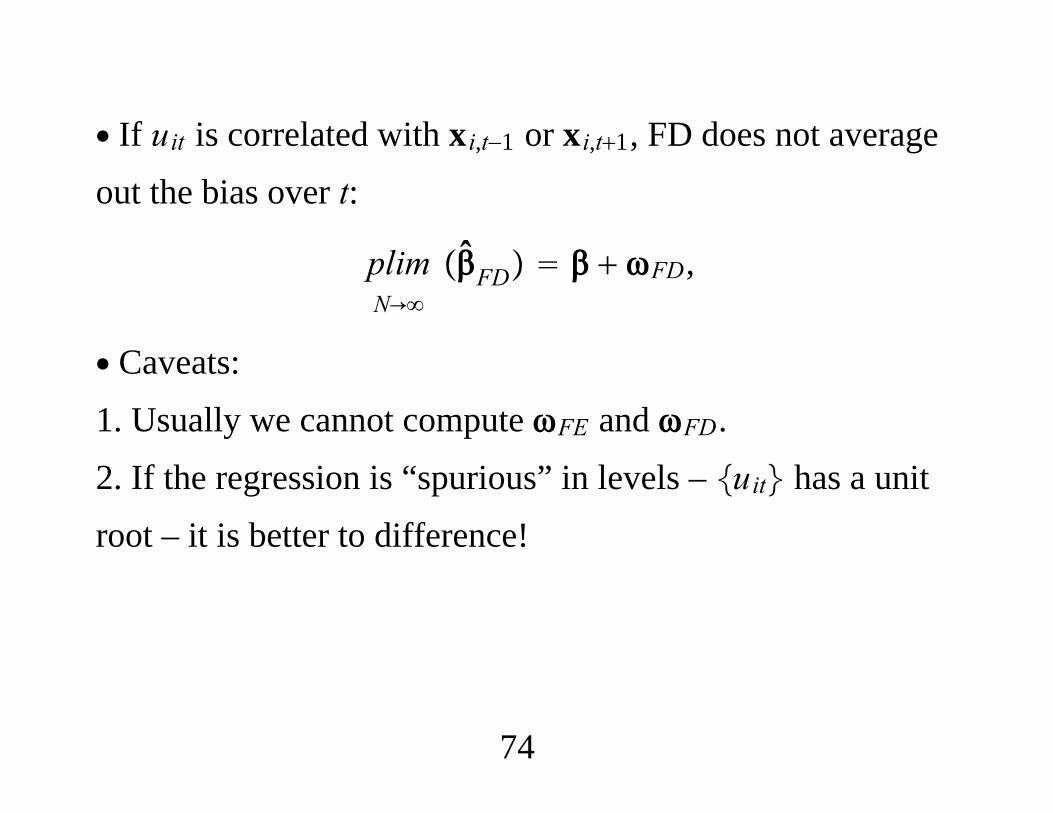

∙ If uit is correlated with xi,t−1 or xi,t1, FD does not averageout the bias over t:

N→plim FD FD,

∙ Caveats:1. Usually we cannot compute FE and FD.2. If the regression is “spurious” in levels – uit has a unitroot – it is better to difference!

74

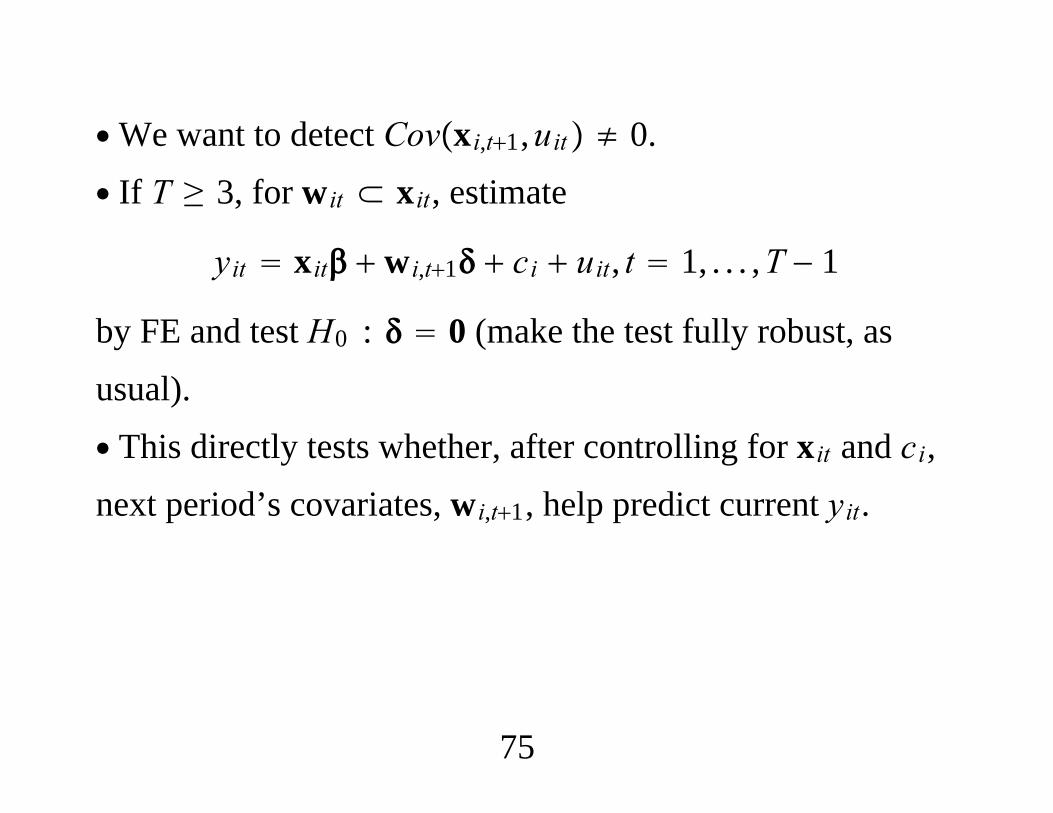

∙We want to detect Covxi,t1,uit ≠ 0.∙ If T ≥ 3, for wit ⊂ xit, estimate

yit xit wi,t1 ci uit, t 1, . . . ,T − 1

by FE and test H0 : 0 (make the test fully robust, asusual).∙ This directly tests whether, after controlling for xit and ci,next period’s covariates, wi,t1, help predict current yit.

75

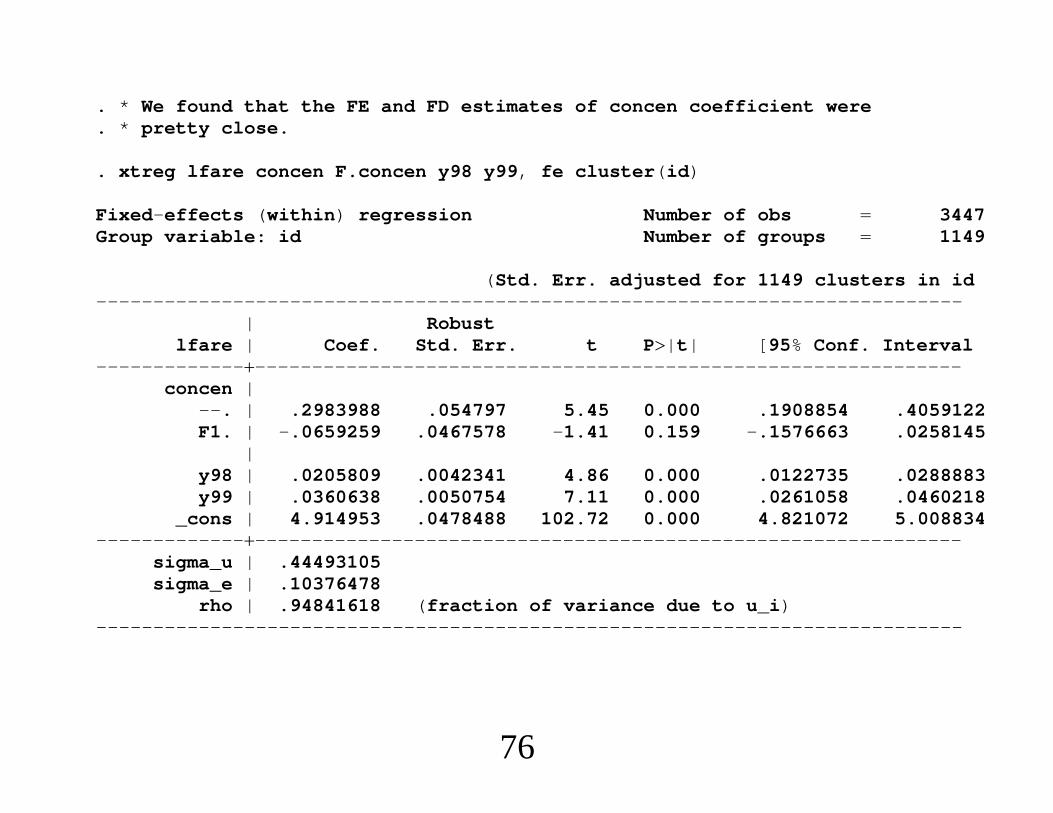

. * We found that the FE and FD estimates of concen coefficient were

. * pretty close.

. xtreg lfare concen F.concen y98 y99, fe cluster(id)

Fixed-effects (within) regression Number of obs 3447Group variable: id Number of groups 1149

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| Robustlfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------concen |

--. | .2983988 .054797 5.45 0.000 .1908854 .4059122F1. | -.0659259 .0467578 -1.41 0.159 -.1576663 .0258145

|y98 | .0205809 .0042341 4.86 0.000 .0122735 .0288883y99 | .0360638 .0050754 7.11 0.000 .0261058 .0460218

_cons | 4.914953 .0478488 102.72 0.000 4.821072 5.008834---------------------------------------------------------------------------

sigma_u | .44493105sigma_e | .10376478

rho | .94841618 (fraction of variance due to u_i)----------------------------------------------------------------------------

76

Econometrics of Cross Section and Panel DataLecture 4: Linear Panel Data Models II

Jeff WooldridgeMichigan State University

cemmap/PEPA, June 2014

1. Linear Models under Sequential Exogeneity2. Estimating Production Functions Using Proxy Variables3. Pseudo Panels from Pooled Cross Sections

1

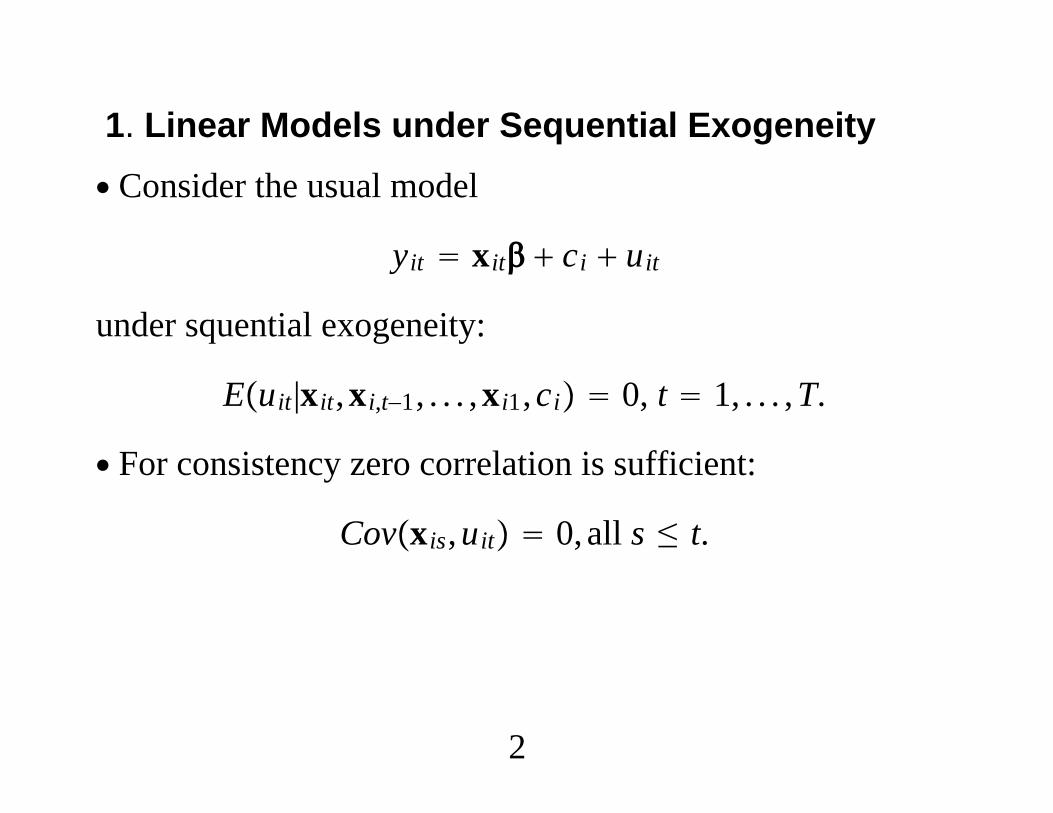

1. Linear Models under Sequential Exogeneity∙ Consider the usual model

yit xit ci uit

under squential exogeneity:

Euit|xit,xi,t−1, . . . ,xi1,ci 0, t 1, . . . ,T.

∙ For consistency zero correlation is sufficient:

Covxis,uit 0, all s ≤ t.

2

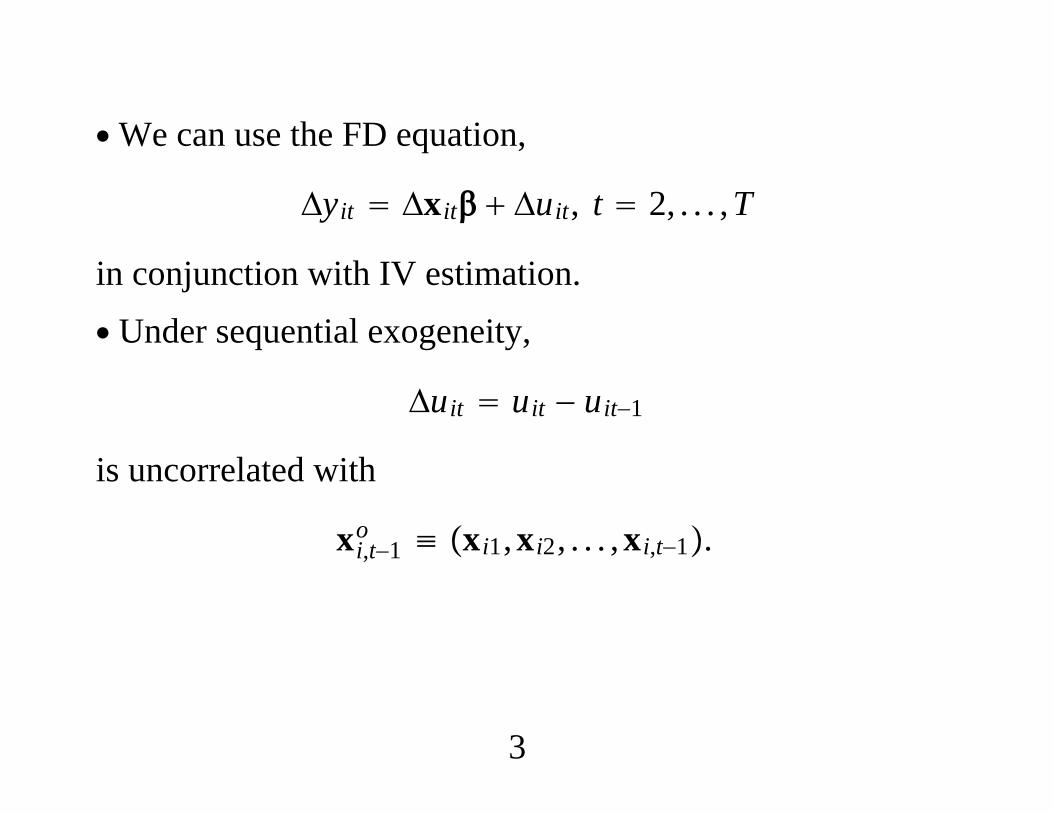

∙We can use the FD equation,

Δyit Δxit Δuit, t 2, . . . ,T

in conjunction with IV estimation.∙ Under sequential exogeneity,

Δuit uit − uit−1

is uncorrelated with

xi,t−1o ≡ xi1,xi2, . . . ,xi,t−1.

3

∙We have the moment conditions

Exi,t−1o′ Δuit 0, t 2, . . . ,T.

∙ Fairly routine to apply GMM estimation.∙ For each t, first run the reduced form regressions

Δxit on xi,t−1o , i 1, . . . ,N

to determine if there is a “weak instrument” problem.

4

∙ If Δxit is the 1 K vector of fitted values, can use these asIVs (not regressors!) in the equation

Δyit Δxit Δuit, t 2, . . . ,T

∙ Just pooled IV using serial correlation-roust inference.

5

∙ One case where xi,t−1o are irrelevant instruments for Δxit:

xit t xi,t−1 rit

Erit|xi,t−1,xi,t−2, . . . ,xi0 0

∙ Then EΔxit|xi,t−1o EΔxit t, and IV in a model with

time effects fails.∙ One solution to the weak instrument problem is to searchfor more moment conditions.

6

∙ Arellano and Bover (1995) suggested adding

CovΔxit′ ,ci 0, t 2, . . . ,T.

∙ Suppose xit follows

xit fi rit

Then sufficient is

Covrit,ci 0, t 1, 2, . . .

∙ Covfi,ci is unrestricted.

7

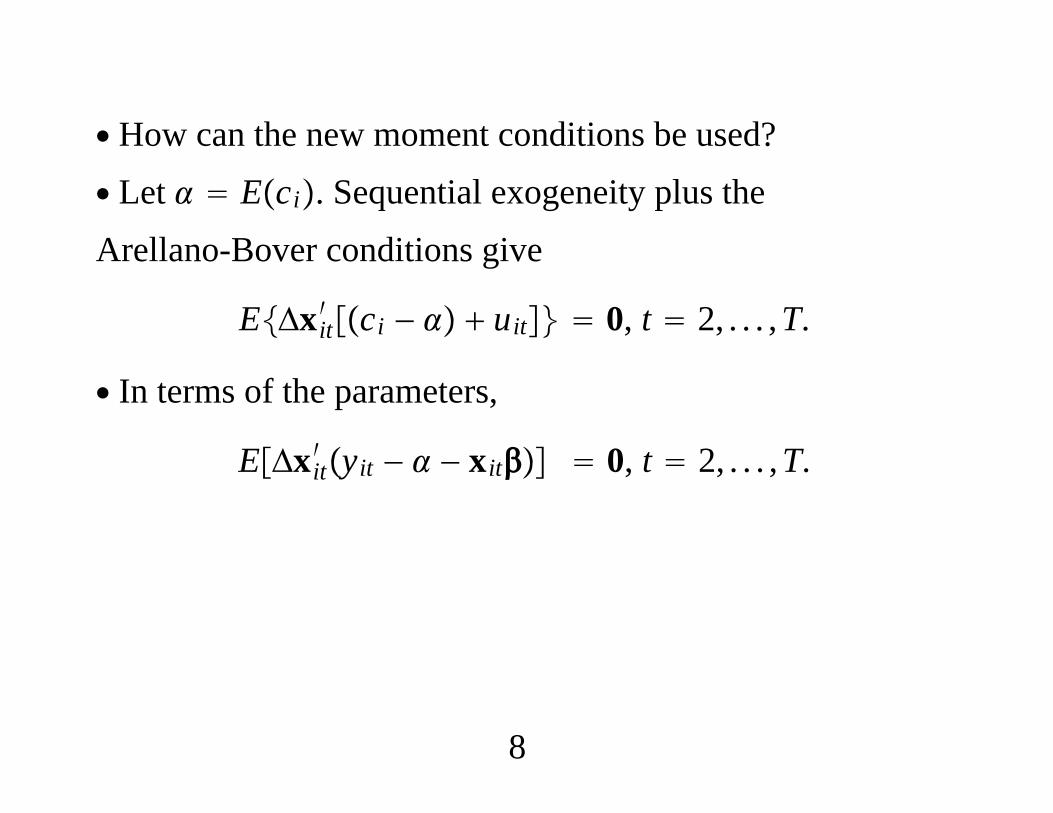

∙ How can the new moment conditions be used?∙ Let Eci. Sequential exogeneity plus theArellano-Bover conditions give

EΔxit′ ci − uit 0, t 2, . . . ,T.

∙ In terms of the parameters,

EΔxit′ yit − − xit 0, t 2, . . . ,T.

8

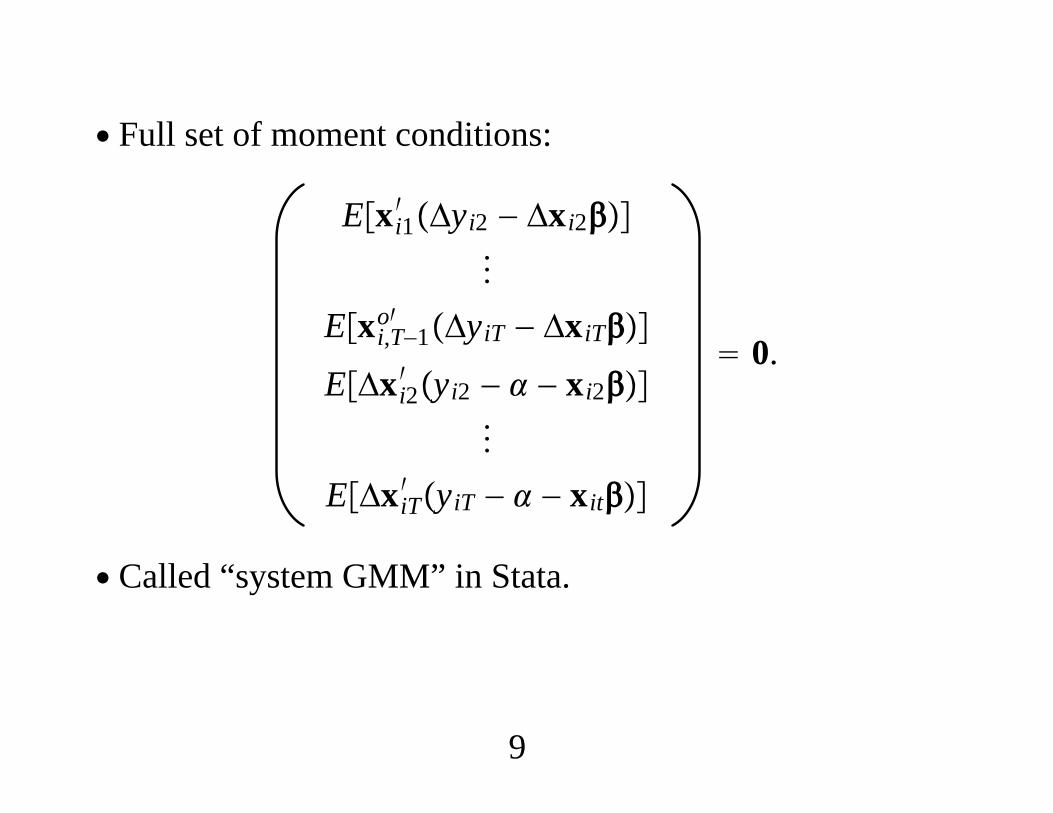

∙ Full set of moment conditions:

Exi1′ Δyi2 − Δxi2

Exi,T−1o′ ΔyiT − ΔxiT

EΔxi2′ yi2 − − xi2

EΔxiT′ yiT − − xit

0.

∙ Called “system GMM” in Stata.

9

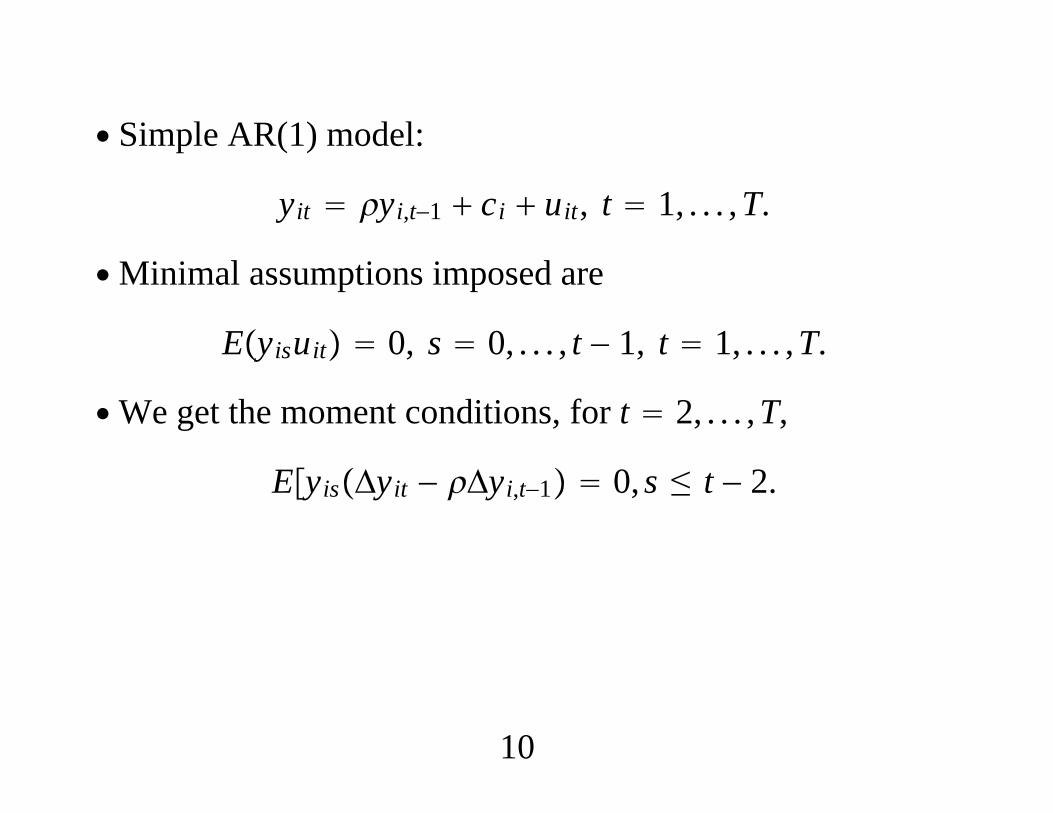

∙ Simple AR(1) model:

yit yi,t−1 ci uit, t 1, . . . ,T.

∙Minimal assumptions imposed are

Eyisuit 0, s 0, . . . , t − 1, t 1, . . . ,T.

∙We get the moment conditions, for t 2, . . . ,T,

EyisΔyit − Δyi,t−1 0, s ≤ t − 2.

10

∙ Can suffer from weak instruments when is close to unity.

∙ Blundell and Bond (1998) showed that if

Covyi1 − yi0,ci 0

is added then the Arellano and Bover condition holds:

EΔyi,t−1yit − − yi,t−1 0.

11

∙ Extensions of the AR(1) model,

yit yi,t−1 zit ci uit, t 1, . . . ,T

are easily handled using FD:

Δyit Δyi,t−1 Δzit Δuit, t 2, . . . ,TEyisΔuit 0, s ≤ t − 2

∙ Can use Δzit as own IVs if they are strictly exogenous.

12

∙ If zit is not strictly exogenous, can use zi,t−1, . . . ,zi1 asIVs, along with yi,t−2, . . . ,yi0 in the FD equation at time t.∙ And, we still might use, for t 2, . . . ,T, momentconditions on the levels:

EΔyi,t−1yit − − yi,t−1 − zit 0EΔzit

′ yit − − yi,t−1 − zit 0

∙ Airfare Example:

lfareit t lfarei,t−1 concenit cit uit

13

Dep. Var. lfare(1) (2) (3) (4)

Expl. Var. FD-OLS FE FD-IV A-Blfare−1

.027−. 126

.032. 077

.062. 219

.055. 333

concen.053. 076

.053. 058

.056. 126

.040. 152

N 1, 149 1, 149 1, 149 1, 149

14

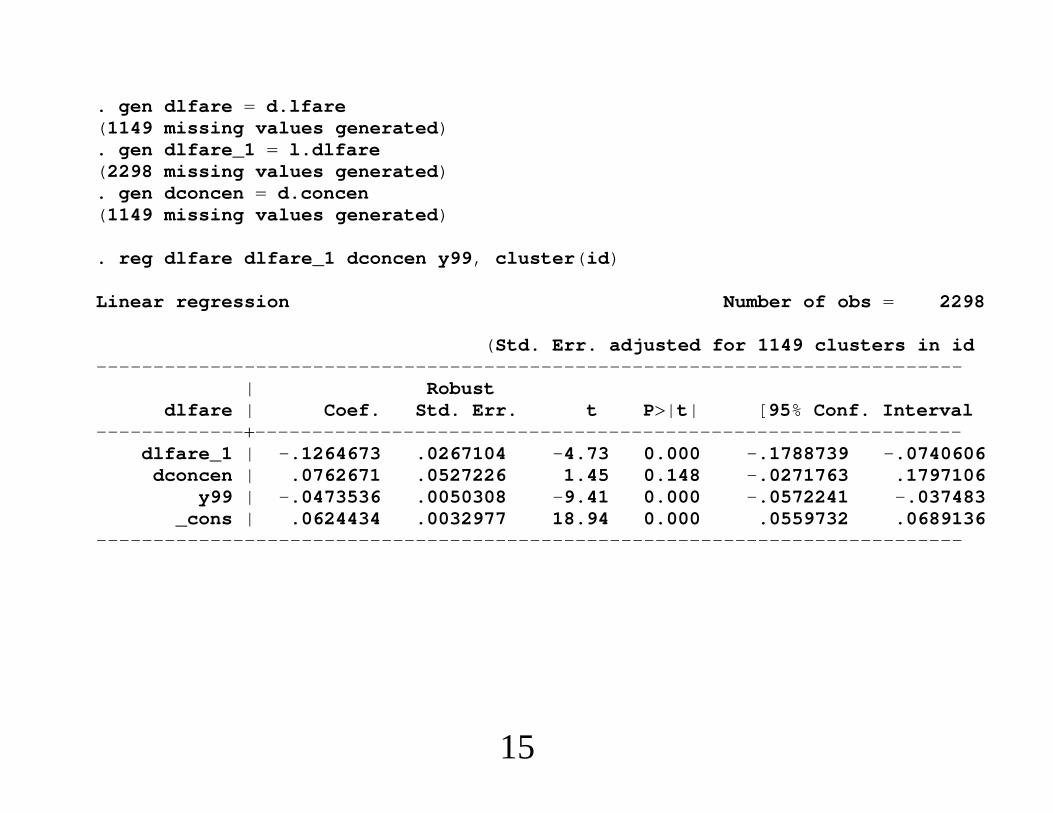

. gen dlfare d.lfare(1149 missing values generated). gen dlfare_1 l.dlfare(2298 missing values generated). gen dconcen d.concen(1149 missing values generated)

. reg dlfare dlfare_1 dconcen y99, cluster(id)

Linear regression Number of obs 2298

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| Robustdlfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------dlfare_1 | -.1264673 .0267104 -4.73 0.000 -.1788739 -.0740606

dconcen | .0762671 .0527226 1.45 0.148 -.0271763 .1797106y99 | -.0473536 .0050308 -9.41 0.000 -.0572241 -.037483

_cons | .0624434 .0032977 18.94 0.000 .0559732 .0689136----------------------------------------------------------------------------

15

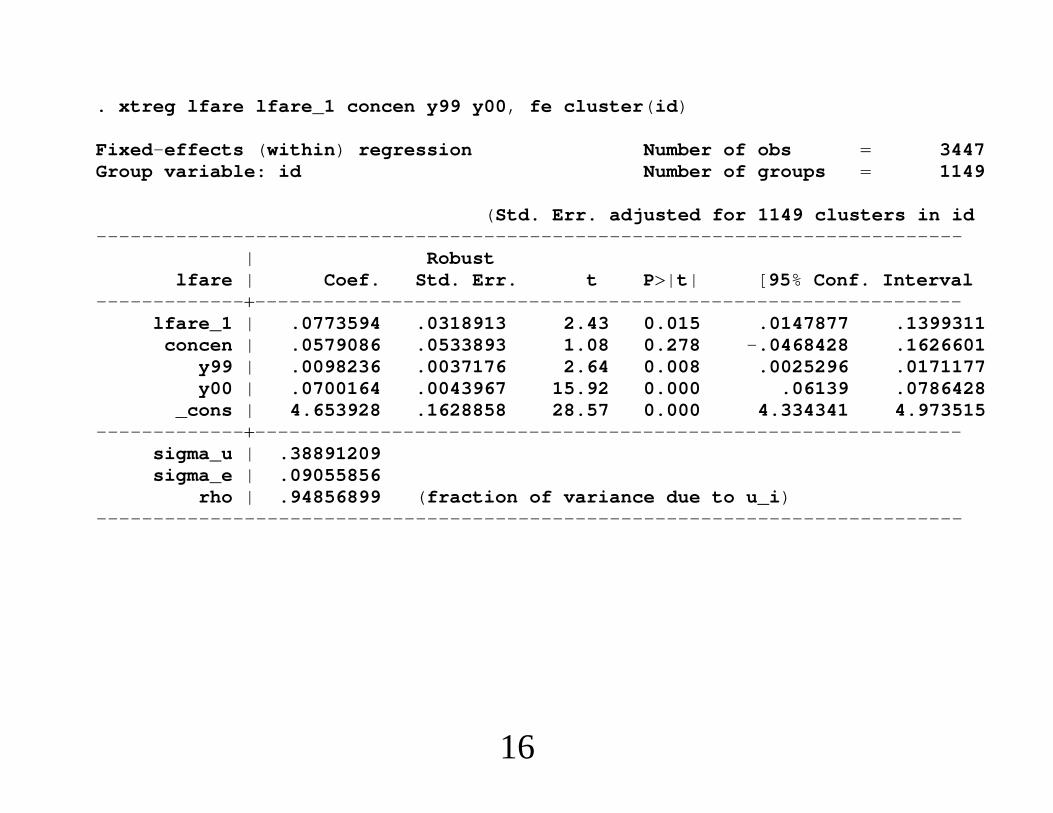

. xtreg lfare lfare_1 concen y99 y00, fe cluster(id)

Fixed-effects (within) regression Number of obs 3447Group variable: id Number of groups 1149

(Std. Err. adjusted for 1149 clusters in id----------------------------------------------------------------------------

| Robustlfare | Coef. Std. Err. t P|t| [95% Conf. Interval

---------------------------------------------------------------------------lfare_1 | .0773594 .0318913 2.43 0.015 .0147877 .1399311

concen | .0579086 .0533893 1.08 0.278 -.0468428 .1626601y99 | .0098236 .0037176 2.64 0.008 .0025296 .0171177y00 | .0700164 .0043967 15.92 0.000 .06139 .0786428

_cons | 4.653928 .1628858 28.57 0.000 4.334341 4.973515---------------------------------------------------------------------------

sigma_u | .38891209sigma_e | .09055856

rho | .94856899 (fraction of variance due to u_i)----------------------------------------------------------------------------

16

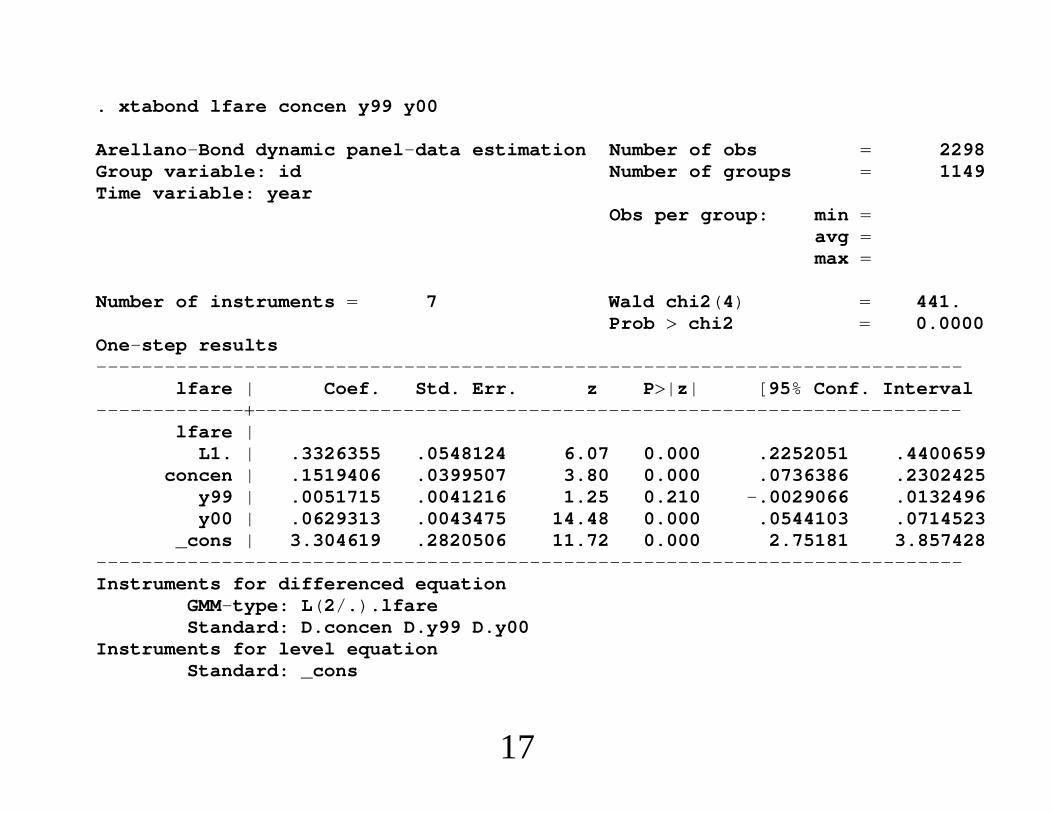

. xtabond lfare concen y99 y00

Arellano-Bond dynamic panel-data estimation Number of obs 2298Group variable: id Number of groups 1149Time variable: year

Obs per group: min avg max

Number of instruments 7 Wald chi2(4) 441.Prob chi2 0.0000

One-step results----------------------------------------------------------------------------

lfare | Coef. Std. Err. z P|z| [95% Conf. Interval---------------------------------------------------------------------------

lfare |L1. | .3326355 .0548124 6.07 0.000 .2252051 .4400659

concen | .1519406 .0399507 3.80 0.000 .0736386 .2302425y99 | .0051715 .0041216 1.25 0.210 -.0029066 .0132496y00 | .0629313 .0043475 14.48 0.000 .0544103 .0714523

_cons | 3.304619 .2820506 11.72 0.000 2.75181 3.857428----------------------------------------------------------------------------Instruments for differenced equation

GMM-type: L(2/.).lfareStandard: D.concen D.y99 D.y00

Instruments for level equationStandard: _cons

17

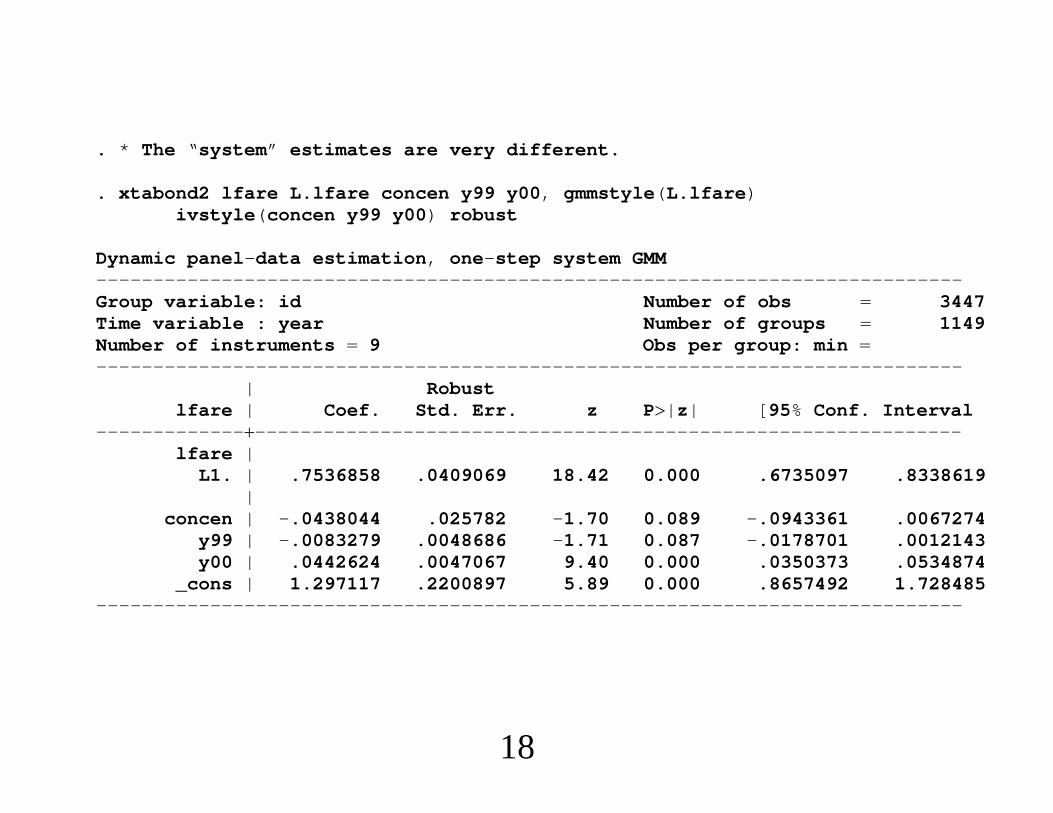

. * The “system” estimates are very different.

. xtabond2 lfare L.lfare concen y99 y00, gmmstyle(L.lfare)ivstyle(concen y99 y00) robust

Dynamic panel-data estimation, one-step system GMM----------------------------------------------------------------------------Group variable: id Number of obs 3447Time variable : year Number of groups 1149Number of instruments 9 Obs per group: min ----------------------------------------------------------------------------

| Robustlfare | Coef. Std. Err. z P|z| [95% Conf. Interval

---------------------------------------------------------------------------lfare |

L1. | .7536858 .0409069 18.42 0.000 .6735097 .8338619|

concen | -.0438044 .025782 -1.70 0.089 -.0943361 .0067274y99 | -.0083279 .0048686 -1.71 0.087 -.0178701 .0012143y00 | .0442624 .0047067 9.40 0.000 .0350373 .0534874

_cons | 1.297117 .2200897 5.89 0.000 .8657492 1.728485----------------------------------------------------------------------------

18

2. Estimating Production Functions Using ProxyVariables∙ Olley and Pakes (1996) show how investment can be usedas a proxy variable for unobserved, time-varyingproductivity.∙ Productivity can be expressed as an unknown function ofcapital and investment (when investment is strictly positive).∙ Approach does not assume inputs are strictly exogenous(but omits firm heterogeneity).

19

∙ Levinsohn and Petrin (2003) suggest using intermediateinputs to proxy for unobserved productivity (to avoid thezero investment problem). Still OP estimation.∙ In implementing LP (or OP), convenient to use low-orderpolynomials. Petrin, Poi, and Levinsohn (2004) (PPL)suggest third-degree polynomials (programmed in Stata).

20

∙Wooldridge (2009, Economics Letters): Set up as atwo-equation system for panel data with the same dependentvariable, but where the set of instruments differs acrossequation.∙ Simpler, more efficient, leads to insights aboutidentification.

21

∙ Production function for firm i in period t:

yit lit kit vit eit, t 1, . . . ,T, (1)

yit logarithm of the firm’s outputlit 1 J vector of variable inputs (labor)

kit 1 K vector of observed state variables (capital)

∙ vit : t 1, . . . ,T is unobserved productivity andeit : t 1, 2, . . . ,T is a sequence of shocks.

22

∙ Key implication of the theory underlying OP and LP: Forsome function g, ,

vit gkit,mit, t 1, . . . ,T, (2)

where mit is a 1 M vector of proxy variables.∙ In OP, mit consists of investment; in LP, mit isintermediate inputs.∙ Can somewhat relax time invariance of g, .

23

∙ Under

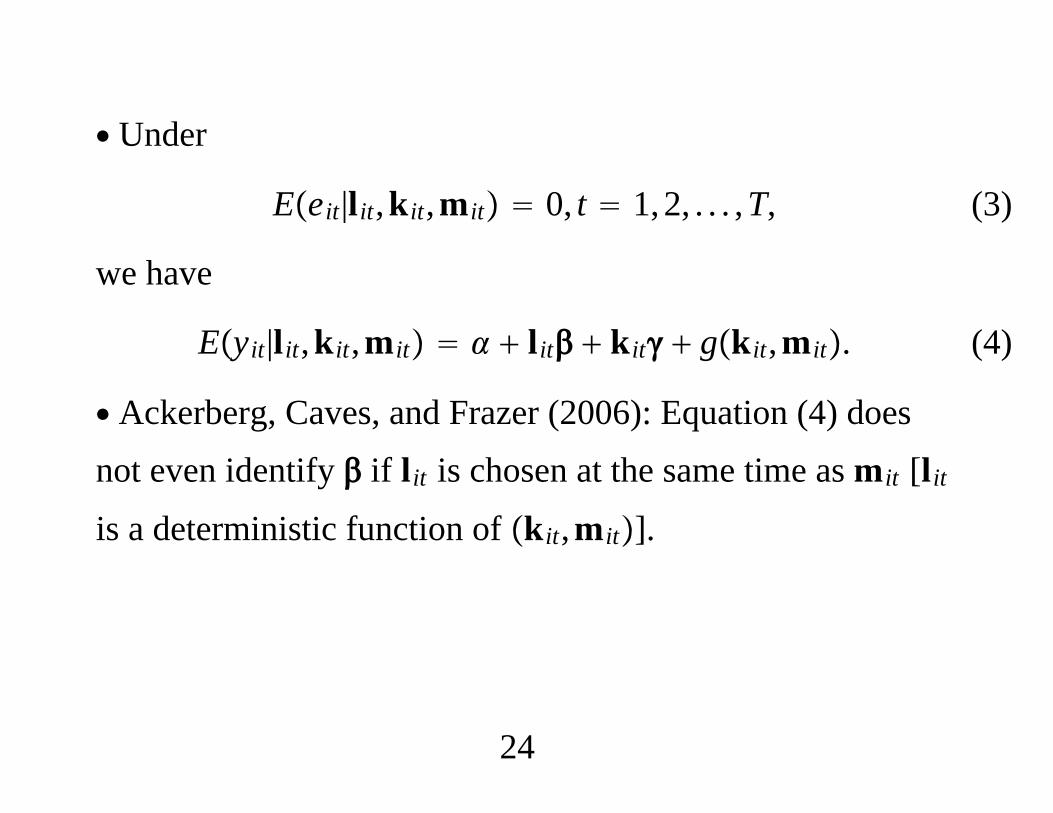

Eeit|lit,kit,mit 0, t 1, 2, . . . ,T, (3)

we have

Eyit|lit,kit,mit lit kit gkit,mit. (4)

∙ Ackerberg, Caves, and Frazer (2006): Equation (4) doesnot even identify if lit is chosen at the same time as mit [lit

is a deterministic function of kit,mit].

24

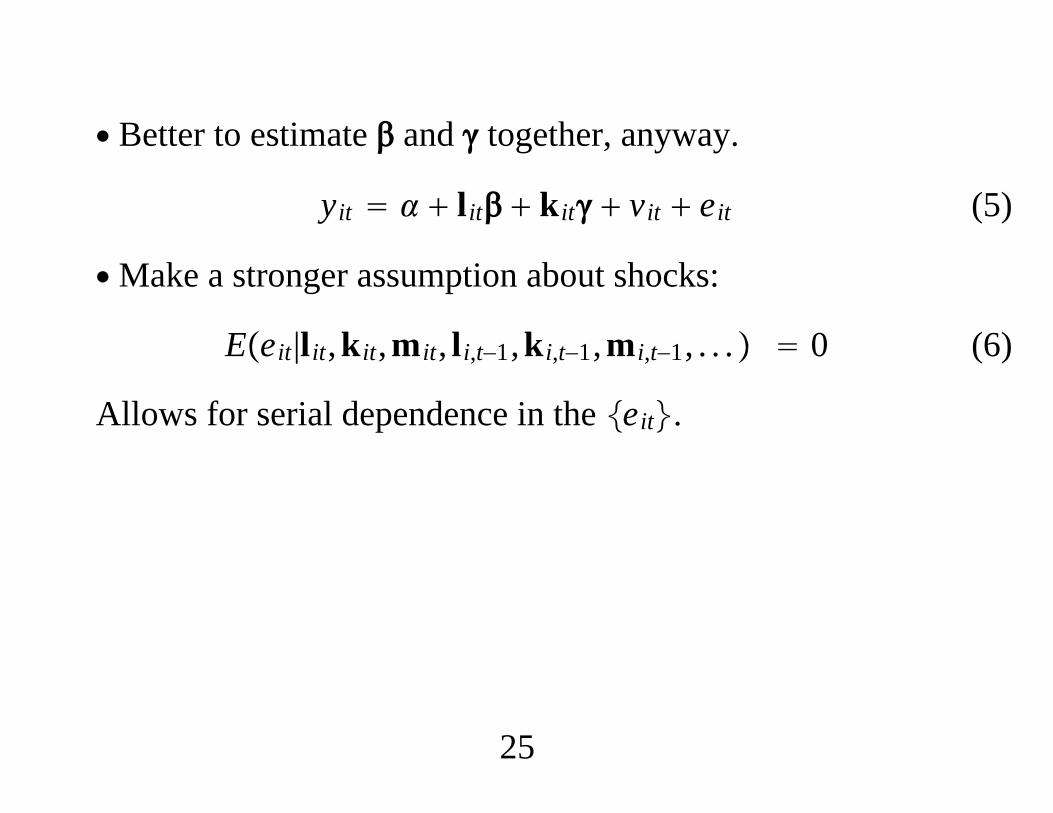

∙ Better to estimate and together, anyway.

yit lit kit vit eit (5)

∙Make a stronger assumption about shocks:

Eeit|lit,kit,mit, li,t−1,ki,t−1,mi,t−1, . . . 0 (6)

Allows for serial dependence in the eit.

25

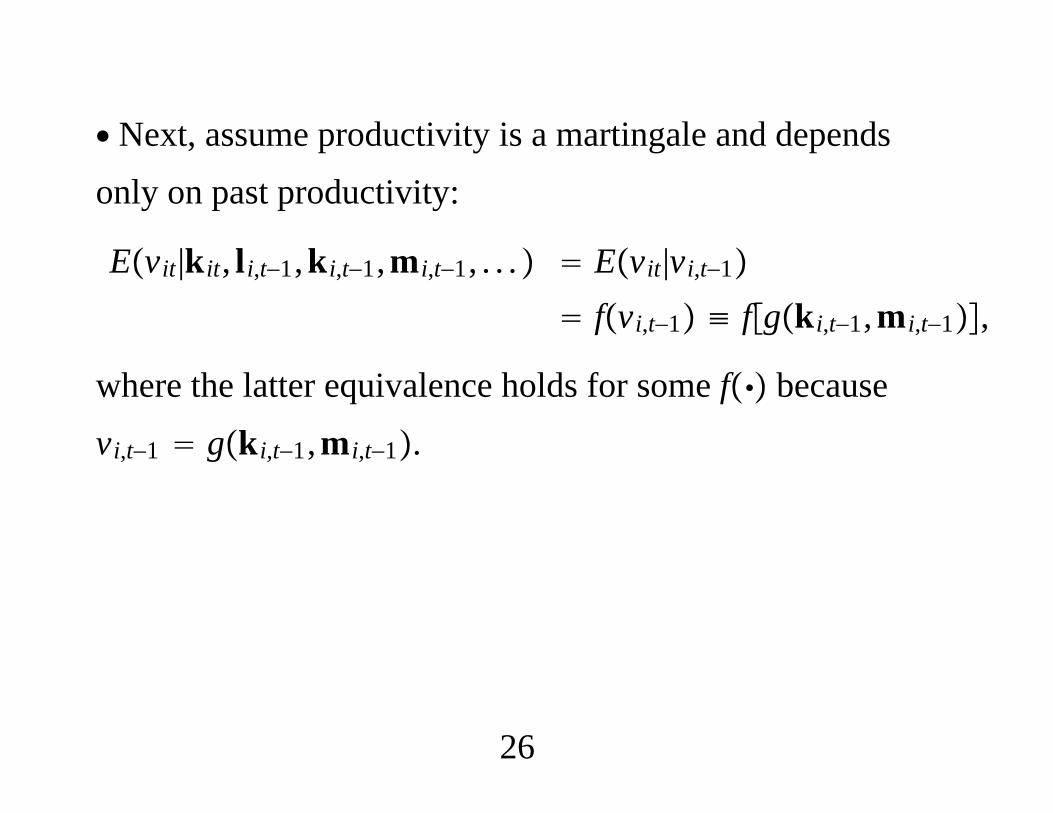

∙ Next, assume productivity is a martingale and dependsonly on past productivity:

Evit|kit, li,t−1,ki,t−1,mi,t−1, . . . Evit|vi,t−1

fvi,t−1 ≡ fgki,t−1,mi,t−1,

where the latter equivalence holds for some f becausevi,t−1 gki,t−1,mi,t−1.

26

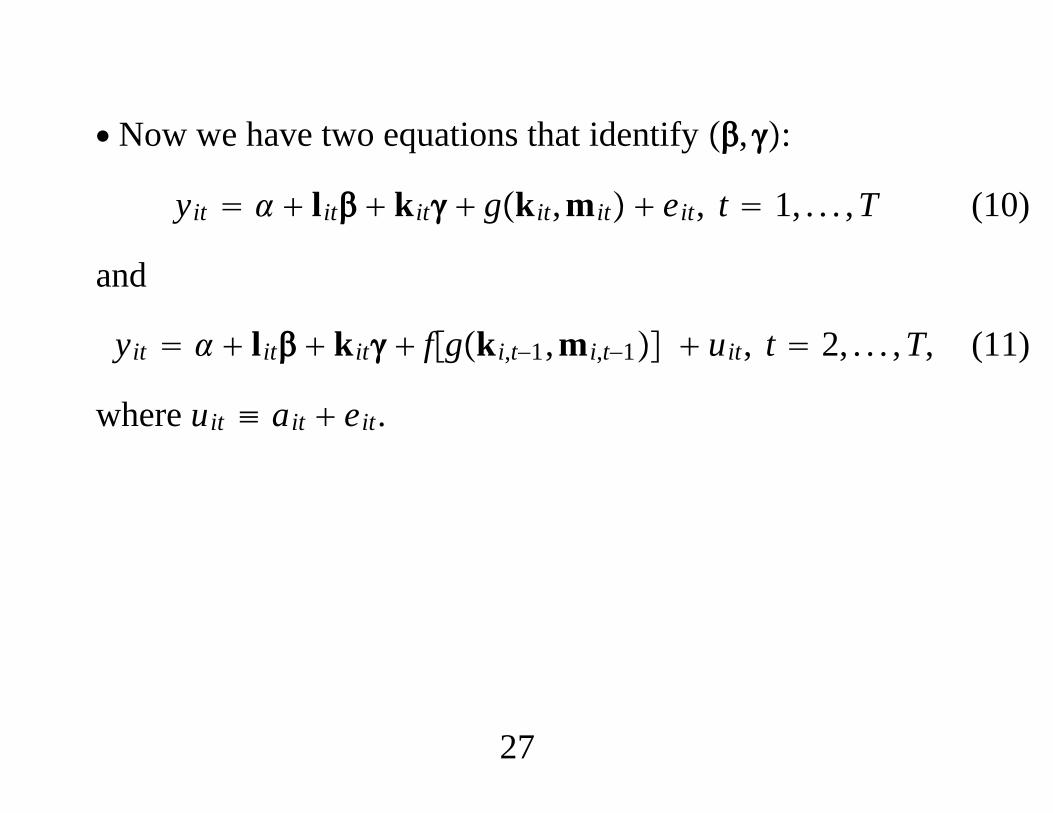

∙ Now we have two equations that identify ,:

yit lit kit gkit,mit eit, t 1, . . . ,T (10)

and

yit lit kit fgki,t−1,mi,t−1 uit, t 2, . . . ,T, (11)

where uit ≡ ait eit.

27

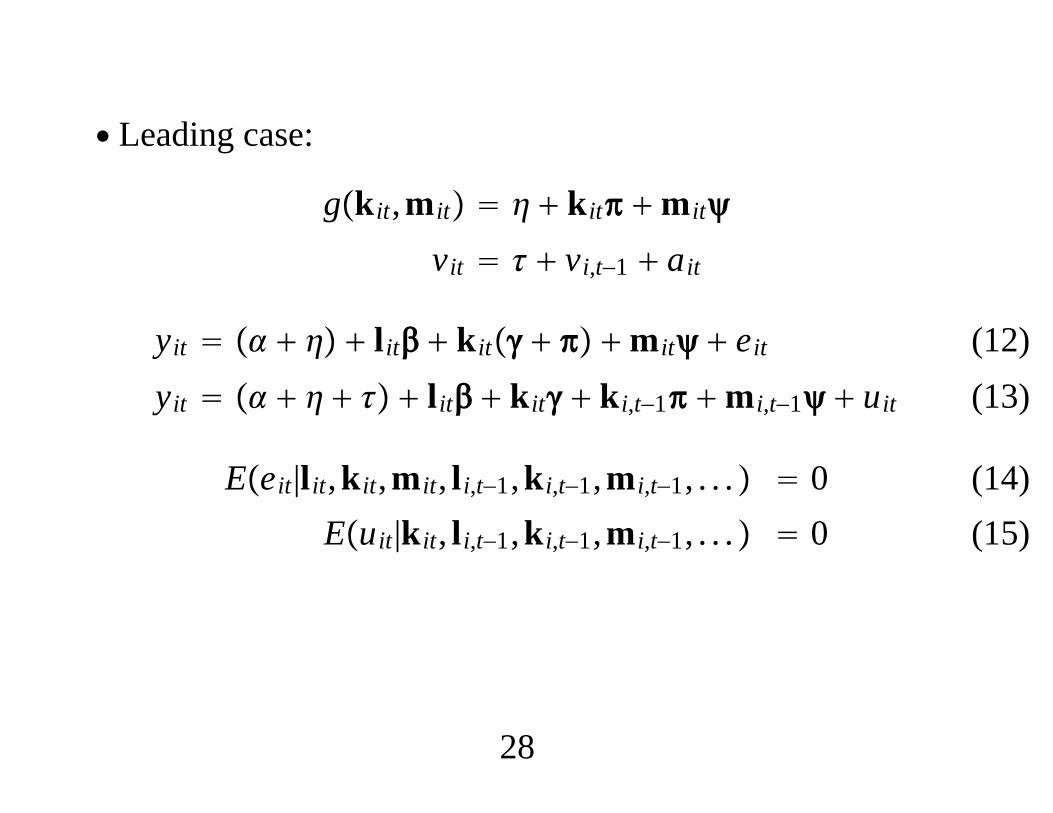

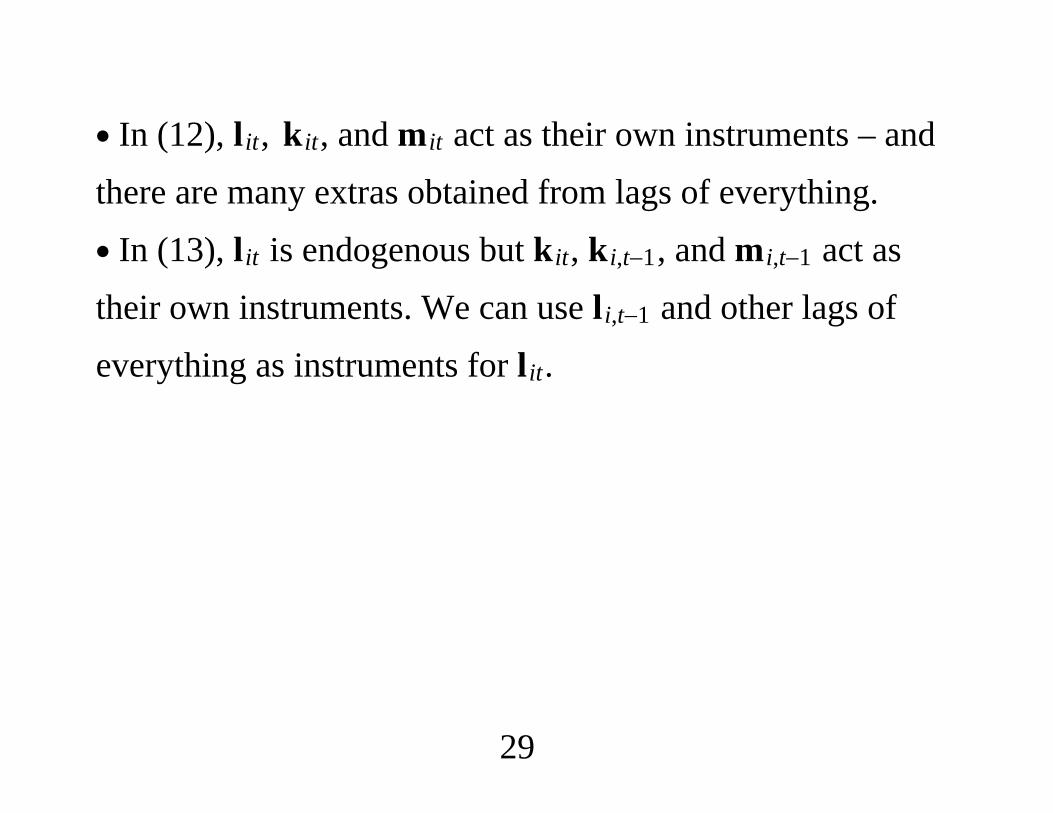

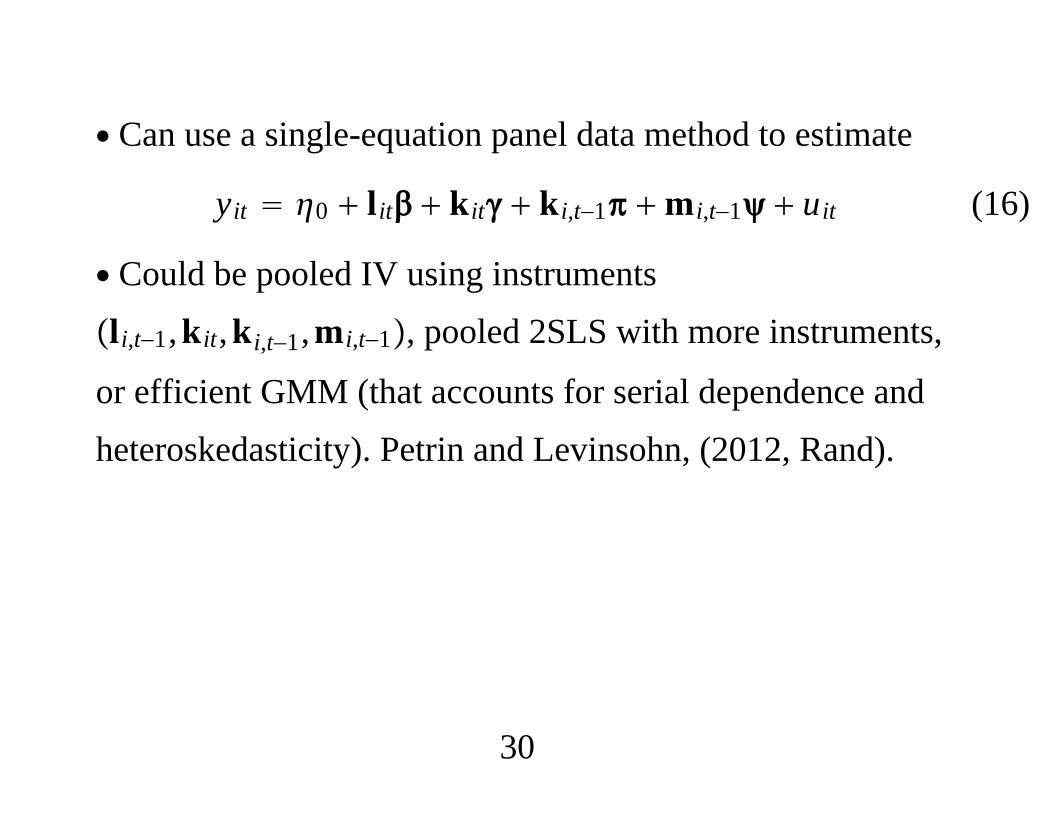

∙ Leading case:

gkit,mit kit mit

vit vi,t−1 ait

yit lit kit mit eit

yit lit kit ki,t−1 mi,t−1 uit

(12) (13)