Embed Size (px)

Citation preview

The Association of Cost Engineers

ACOSTE CONFERENCE 2012

www.acoste.org

Earned Value Project Control

Steve Wake Chairman APM Planning Monitoring and Control SIG

Company Logo

Introduction to Earned Value Management

2

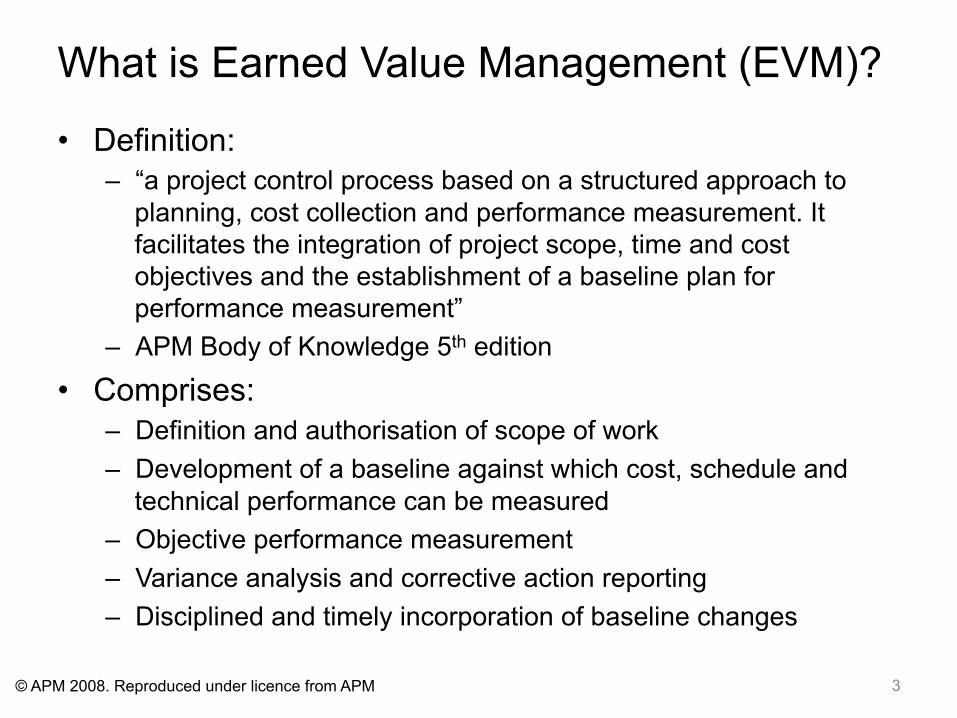

What is Earned Value Management (EVM)?

• Definition: – “a project control process based on a structured approach to

planning, cost collection and performance measurement. It facilitates the integration of project scope, time and cost objectives and the establishment of a baseline plan for performance measurement”

– APM Body of Knowledge 5th edition

• Comprises: – Definition and authorisation of scope of work – Development of a baseline against which cost, schedule and

technical performance can be measured – Objective performance measurement – Variance analysis and corrective action reporting – Disciplined and timely incorporation of baseline changes

3 © APM 2008. Reproduced under licence from APM

Why use Earned Value Management?

• Helps management by: – Enabling an objective measure of project status – Providing basis for estimating final cost – Predicting when the project will be complete – Supporting effective management of resources – Providing a means of managing and controlling change

• Also provides – Verifiable status reports – Clear objective analysis – Considered reasoning – Accountability in the decision-making process – Awareness of impact on the schedule and cost – Visibility of results

4 © APM 2008. Reproduced under licence from APM

Where can EVM be applied?

5

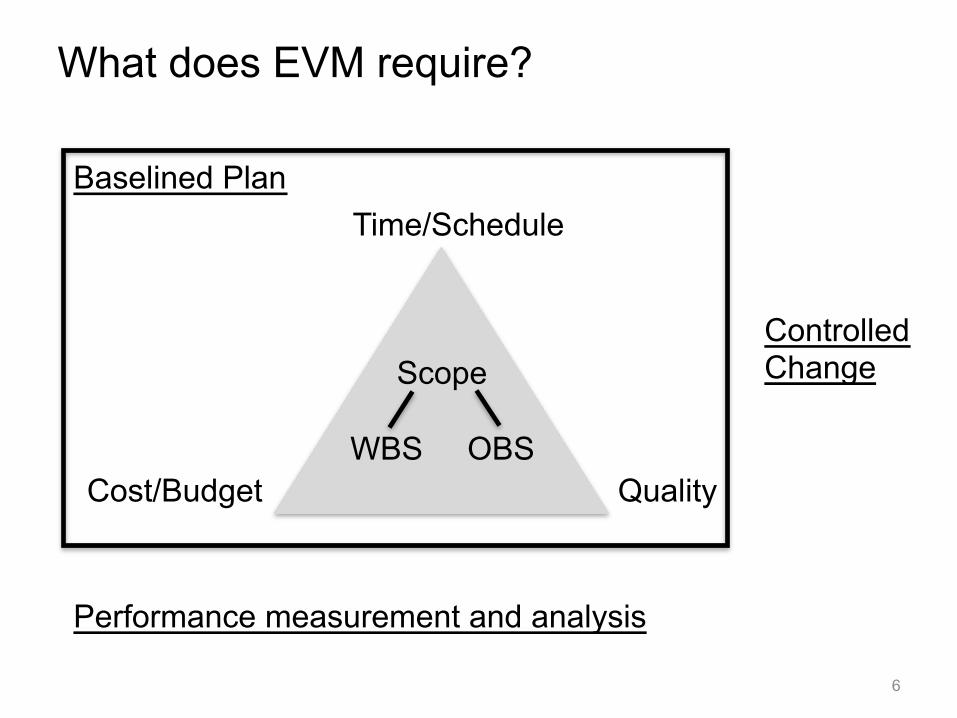

What does EVM require?

6

Time/Schedule

Cost/Budget Quality

Scope

WBS OBS

Baselined Plan

Performance measurement and analysis

Controlled Change

Four key data elements

BCWS Budgeted Cost of Work Scheduled

Planned Value (PV)

ACWP Actual Cost of Work Performed

Actual Cost (AC)

BCWP Budgeted Cost of Work Performed

Earned Value (EV)

EAC Estimate at Completion

7 © APM 2008. Reproduced under licence from APM

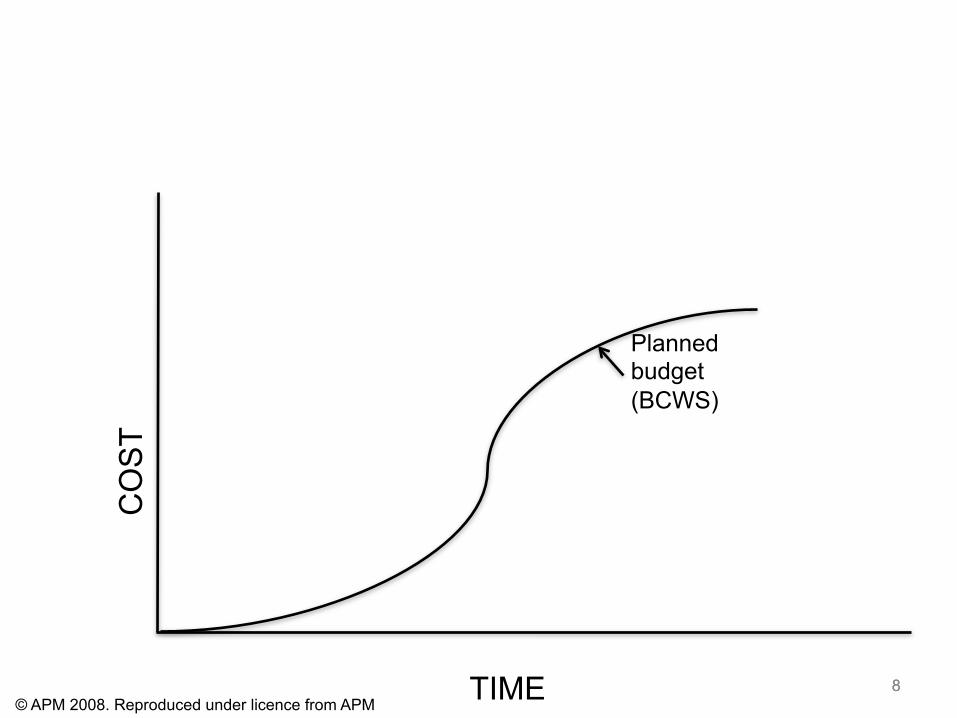

8 8 TIME

CO

ST

Planned budget (BCWS)

© APM 2008. Reproduced under licence from APM

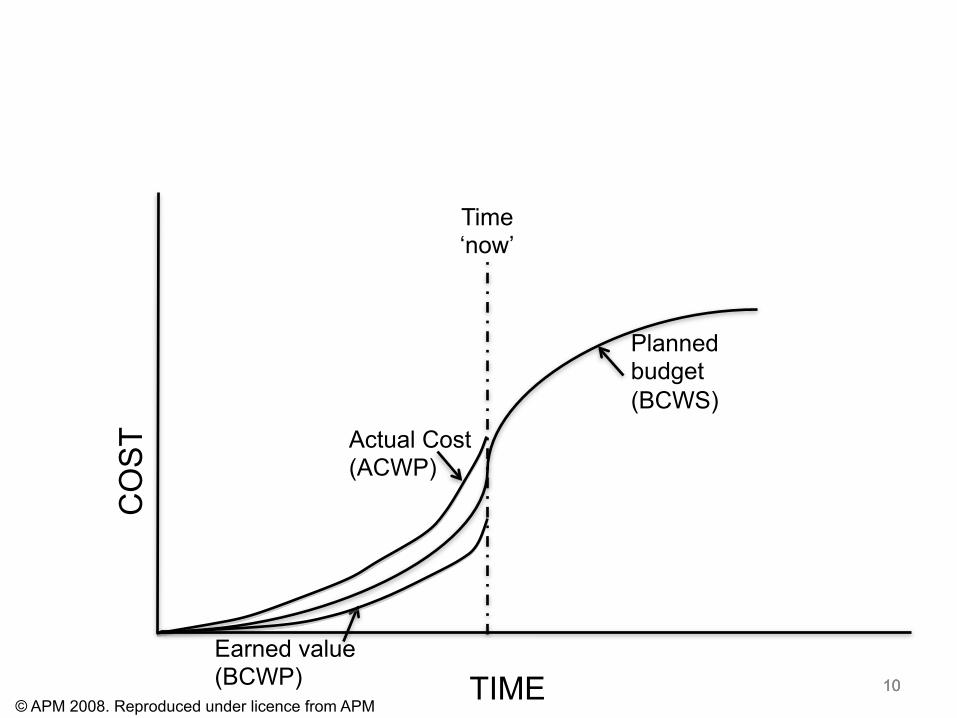

9

Time ‘now’

Actual Cost (ACWP)

9 9 TIME

CO

ST

Planned budget (BCWS)

© APM 2008. Reproduced under licence from APM

10

Earned value (BCWP)

Time ‘now’

Actual Cost (ACWP)

10 10 TIME

CO

ST

Planned budget (BCWS)

© APM 2008. Reproduced under licence from APM

EVM Process

11

EVM Process

12

1. Definition of scope

6. Risk Management

5. Change Management

2. Planning 4. Analysis, review, action

3. Data Collection

Definition of Scope

13

Definition of Scope

• Concerned with: – Defining the work to be done – WBS – Assigning work to parts of the project organisation – OBS – Aligning and combining the WBS and OBS – RAM

• Key activities: – Review the project requirements and establish key deliverables – Develop a Work Breakdown Structure (WBS) – Develop an Organisation Breakdown Structure (OBS) – Generate a Responsibility Assignment Matrix (RAM), identifying

control accounts – Produce a Work Breakdown Structure Dictionary (WBSD) down

to work packages and planning packages – Determine and agree flowdown of EVM into subcontracts

14 © APM 2008. Reproduced under licence from APM

Requirements and key deliverables

• Statement of Works – A narrative description of products or services to be delivered by

the project

• Defines the project scope • Includes:

– Overall requirements – Deliverables

• Forms the basis for allocating: – Work – Budget – Schedule

15 © APM 2008. Reproduced under licence from APM

Work Breakdown Structure

16

Project Scope

Component 2.1

High-level work

element 2

Component 2.2

Component 1.1

High-level work

element 1

Component 1.2

WBS Dictionary

• Purpose – Describe the entire scope of the work to be undertaken by the

project

• For each element of the WBS, should contain – Contract number – WBS number and title – WBSD issue number and date – Contract paragraph number – Statement of work

17 © APM 2008. Reproduced under licence from APM

Organisation Breakdown Structure

18

Project Organisation

Team Manager

2.1

Function/Department

2

Team Manager

2.2

Team Manager

1.1

Function/Department

1

Team Manager

1.2

Control Account

Control Account

Control Account

Control Account

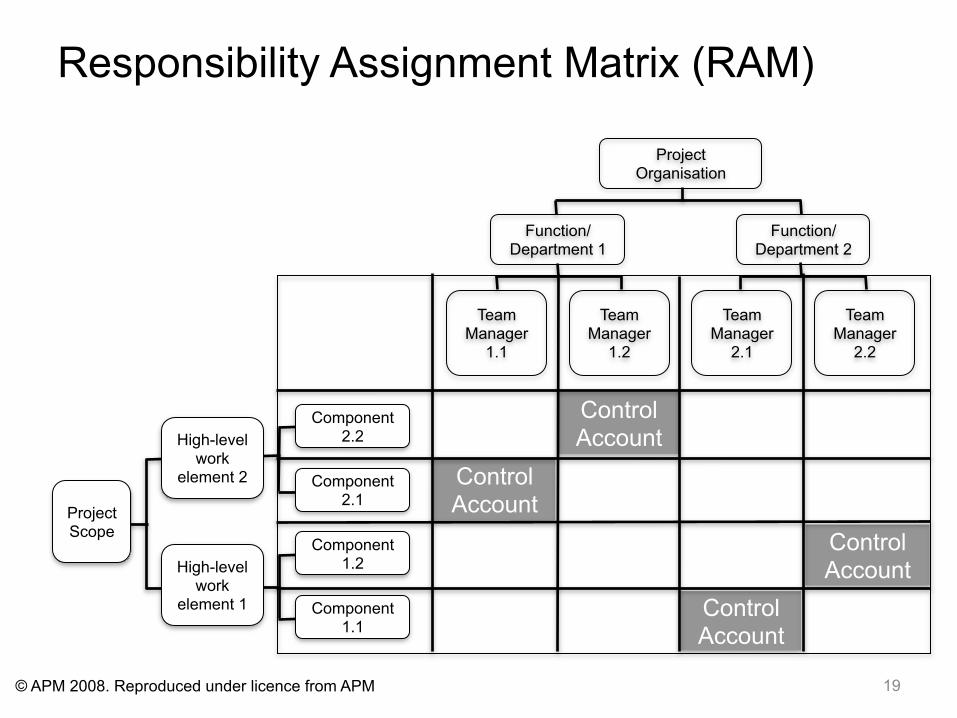

Responsibility Assignment Matrix (RAM)

19

Project Organisation

Team Manager

2.1

Function/Department 2

Team Manager

2.2

Team Manager

1.1

Function/Department 1

Team Manager

1.2

Project Scope

Component 2.1

High-level work

element 2

Component 2.2

Component 1.1

High-level work

element 1

Component 1.2

© APM 2008. Reproduced under licence from APM

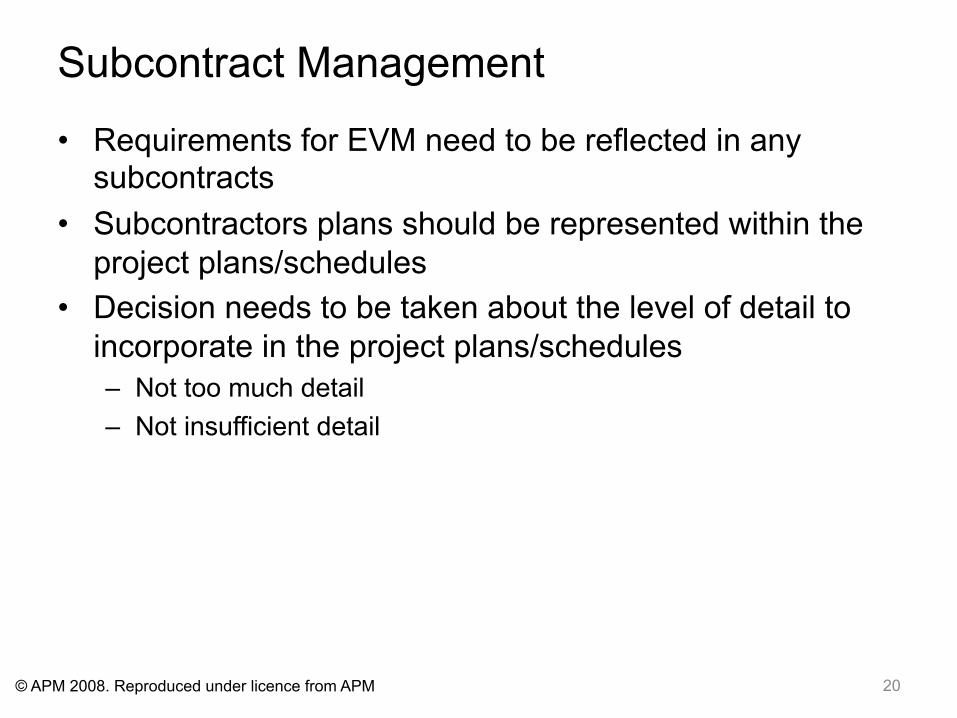

Subcontract Management

• Requirements for EVM need to be reflected in any subcontracts

• Subcontractors plans should be represented within the project plans/schedules

• Decision needs to be taken about the level of detail to incorporate in the project plans/schedules – Not too much detail – Not insufficient detail

20 © APM 2008. Reproduced under licence from APM

Planning

21

Planning

• Concerned with: – Establishing a baseline for performance measurement

encompassing: • A plan of logically scheduled activities • Agreed and assigned budgets and resources • Defined objective achievement measures

• Key activities: – Identify master milestones and deliverables – Develop activities with logical dependencies and durations – Group activities into work packages and planning packages – Apply resources to activities – Distribute the budget to work packages and planning packages – Determine the earned value type for the work packages – Establish performance measurement baseline

22 © APM 2008. Reproduced under licence from APM

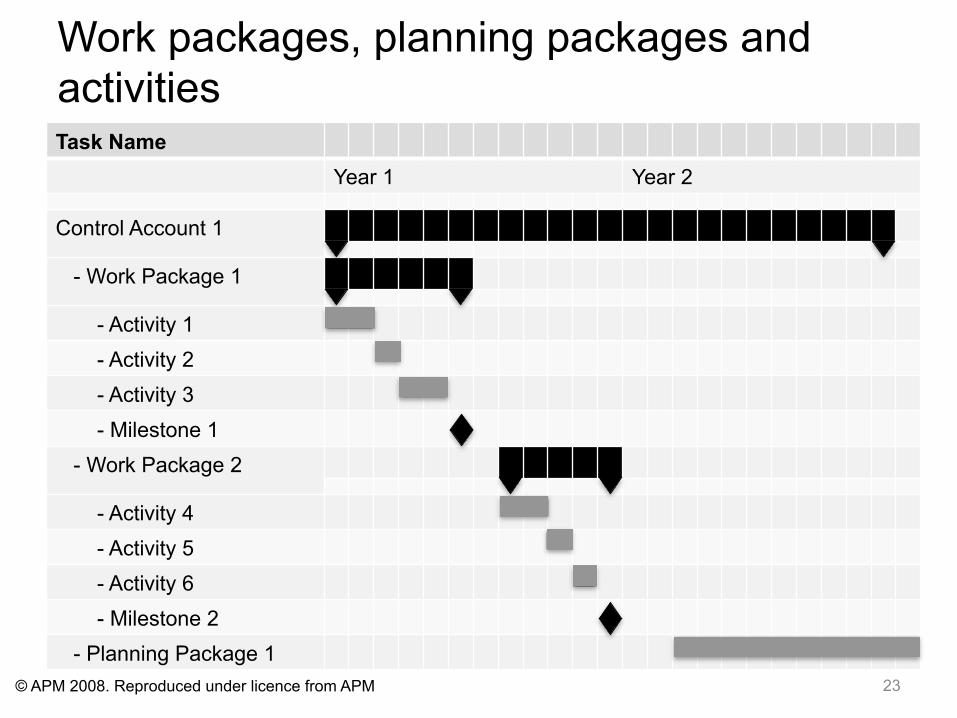

Work packages, planning packages and activities

23

Task Name Year 1 Year 2

Control Account 1

- Work Package 1

- Activity 1 - Activity 2 - Activity 3 - Milestone 1 - Work Package 2

- Activity 4 - Activity 5 - Activity 6 - Milestone 2 - Planning Package 1

© APM 2008. Reproduced under licence from APM

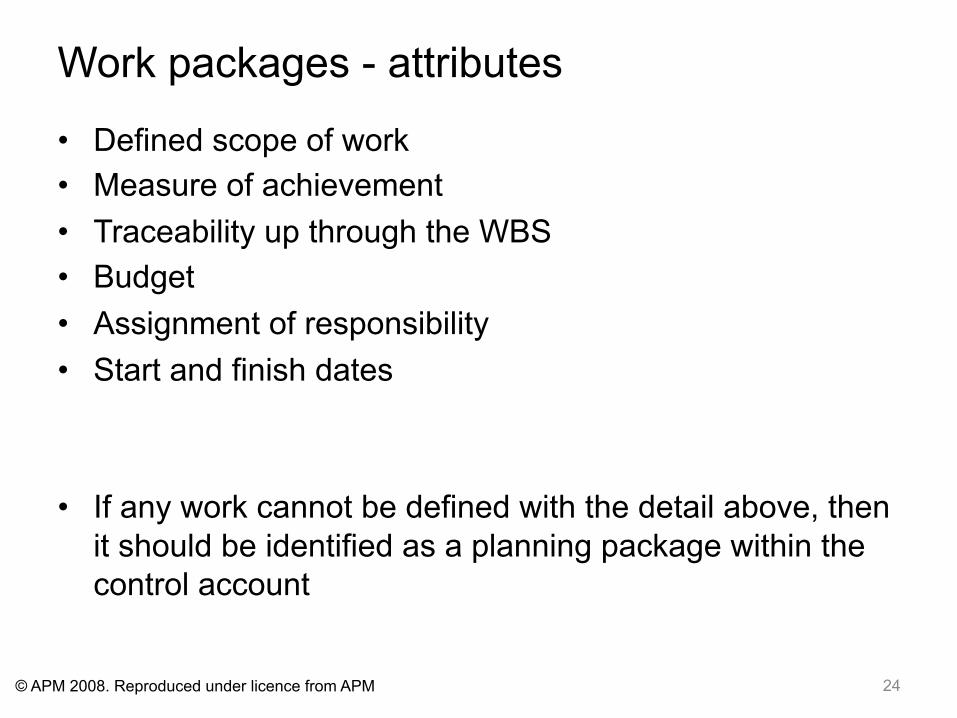

Work packages - attributes

• Defined scope of work • Measure of achievement • Traceability up through the WBS • Budget • Assignment of responsibility • Start and finish dates

• If any work cannot be defined with the detail above, then it should be identified as a planning package within the control account

24 © APM 2008. Reproduced under licence from APM

Schedules

• Definition – The timing and sequence of tasks within a project, as well as the

project duration. The schedule consists mainly of tasks, dependencies among tasks, durations, constraints, resources and time-oriented project information

• Key points – Form the basis for assessing actual progress – Should include contractual milestones – Need to identify activities on the critical path – Permits the integrated planning of project resources with the cost

and schedule objectives of the project

• The plans of any subcontractor should detail an appropriate number of activities/milestones, and these should be integrated into the project schedule

25 © APM 2008. Reproduced under licence from APM

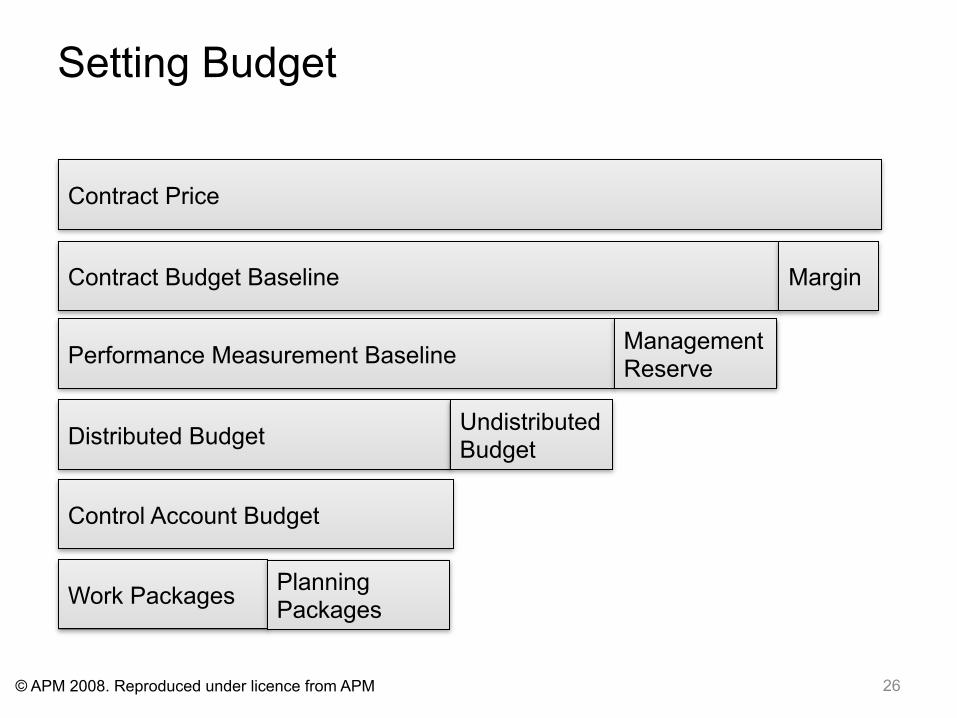

Setting Budget

26

Contract Price

Contract Budget Baseline

Performance Measurement Baseline

Distributed Budget

Control Account Budget

Work Packages

Margin

Management Reserve

Undistributed Budget

Planning Packages

© APM 2008. Reproduced under licence from APM

Objective Measures of Progress

• Applies to work packages that are planned to be or are actually in progress

• Earning method may be objective or subjective • Objective – measurement is straightforward and can be

automated • Subjective – manual assessment will be necessary • Short work packages make assessment easier, but avoid

arbitrary breaks in job planning and scheduling

27 © APM 2008. Reproduced under licence from APM

Earned Value Techniques

• To be agreed for each work package

• Milestones complete • Percentage complete • Equivalent units • Formula method • Level of effort • Apportioned effort

• Earned value for materials?

28 © APM 2008. Reproduced under licence from APM

Baselining the Project

• The plan is baselined (frozen) when it is sufficiently developed and stable

• Becomes the agreed Performance Measurement Baseline (PMB)

• PMB forms the basis for measurement • Should include all elements of the project • Should only be changed through a formal approval

process

29 © APM 2008. Reproduced under licence from APM

Data Collection

30

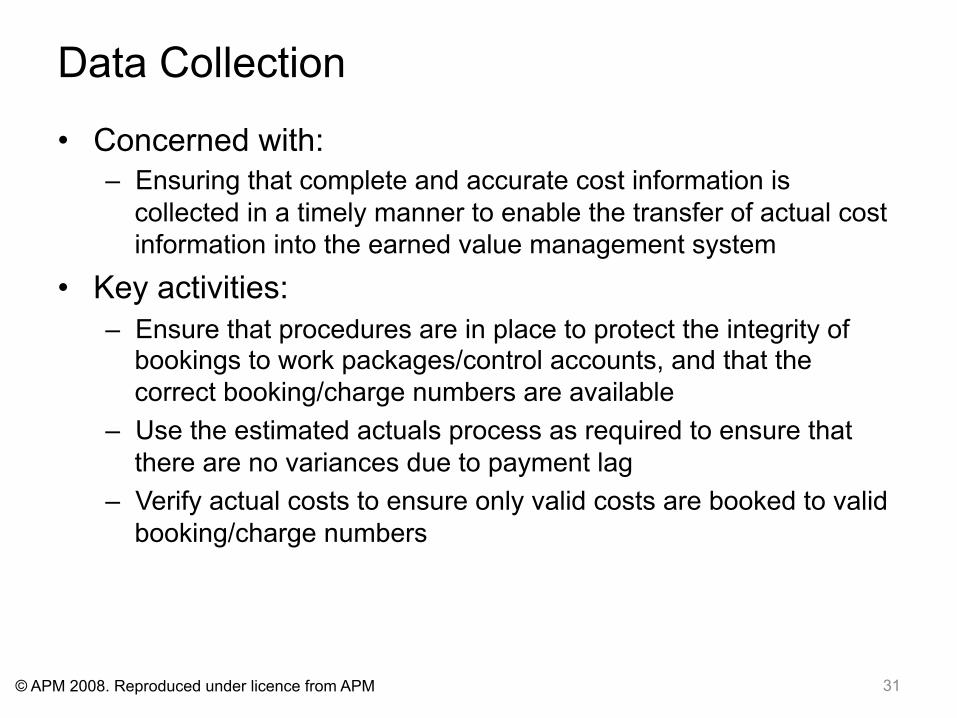

Data Collection

• Concerned with: – Ensuring that complete and accurate cost information is

collected in a timely manner to enable the transfer of actual cost information into the earned value management system

• Key activities: – Ensure that procedures are in place to protect the integrity of

bookings to work packages/control accounts, and that the correct booking/charge numbers are available

– Use the estimated actuals process as required to ensure that there are no variances due to payment lag

– Verify actual costs to ensure only valid costs are booked to valid booking/charge numbers

31 © APM 2008. Reproduced under licence from APM

Measuring costs and committed costs

• Actual cost of work performed (ACWP) include: – Labour costs (direct and indirect costs) – Direct expenses – Materials costs – Subcontractor costs for work done

• ACWP should be: – Collected at a level that will identify cost elements and factors

contributing to cost variance – Recorded in a manner consistent with the budget and include all

expenditure

• Ensure that BCWS, BCWP and ACWP are created in the same time frame

32 © APM 2008. Reproduced under licence from APM

Analysis Review and Action

33

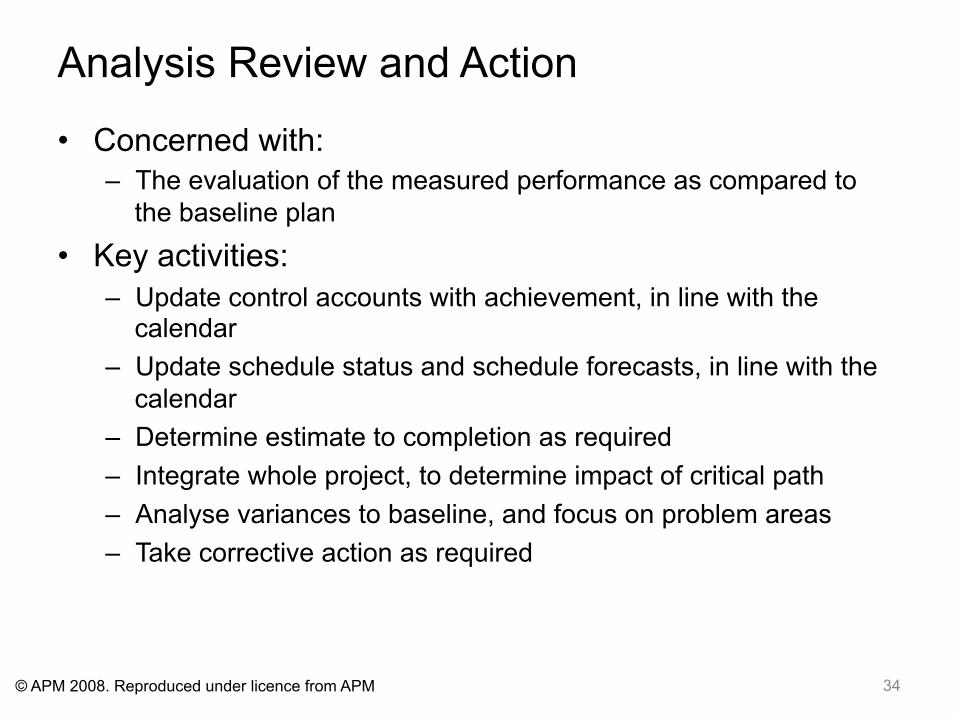

Analysis Review and Action

• Concerned with: – The evaluation of the measured performance as compared to

the baseline plan

• Key activities: – Update control accounts with achievement, in line with the

calendar – Update schedule status and schedule forecasts, in line with the

calendar – Determine estimate to completion as required – Integrate whole project, to determine impact of critical path – Analyse variances to baseline, and focus on problem areas – Take corrective action as required

34 © APM 2008. Reproduced under licence from APM

Schedule Status

• When updating schedule status, consider: – Activity actual start/finish dates – Estimate of the time remaining to complete the task – Estimated start and finish dates of future activities

• Schedule status is determined by comparing how much time the activity is ahead or behind the baseline schedule

• Aspects of schedule assessment: – Review of the critical path activities – Review of schedule against key milestone forecasts – Review of future resource requirements

35 © APM 2008. Reproduced under licence from APM

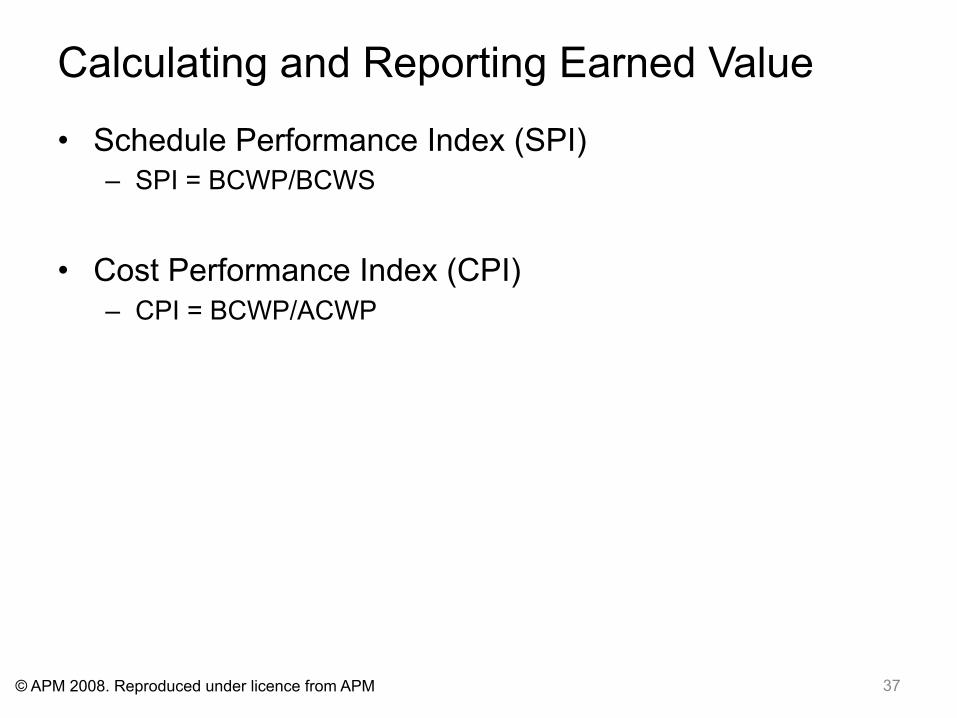

Calculating and Reporting Earned Value

• Schedule Variance (SV) – SV = BCWP – BCWS – SV% = (SV/BCWS) X 100

• Cost Variance (CV) – CV = BCWP – ACWP – CV% = (CV/BCWP) X100

• Variance at Completion (VAC) • VAC = BAC – EAC • VAC% - (VAC/BAC) X100

36 © APM 2008. Reproduced under licence from APM

Calculating and Reporting Earned Value

• Schedule Performance Index (SPI) – SPI = BCWP/BCWS

• Cost Performance Index (CPI) – CPI = BCWP/ACWP

37 © APM 2008. Reproduced under licence from APM

Reporting Graphs

38 TIME

CO

ST

Planned completion

Planned Budget

BAC

Planned budget (BCWS)

BAC Budget at completion BCWS Budgeted Cost of Work Scheduled

© APM 2008. Reproduced under licence from APM

Reporting Graphs

39 TIME

CO

ST

Planned completion

Planned Budget

BAC

Planned budget (BCWS)

Earned value (BCWP)

Time ‘now’

BAC Budget at completion BCWS Budgeted Cost of Work Scheduled OD Original Duration planned ATE Actual Time Expended ACWP Actual Cost of Work Performed BCWP Budget Cost of Work Performed

OD ATE

Actual Cost (ACWP)

© APM 2008. Reproduced under licence from APM

Reporting Graphs

40 TIME

CO

ST

Planned completion

Planned Budget

BAC

Planned budget (BCWS)

Actual Cost (ACWP)

Earned value (BCWP)

OD ATE

Time ‘now’

BAC Budget at completion BCWS Budgeted Cost of Work Scheduled OD Original Duration planned ATE Actual Time Expended ACWP Actual Cost of Work Performed BCWP Budget Cost of Work Performed EAC Estimate Cost at Completion ETC Estimate Time at Completion

Schedule Variance (time)

Schedule Variance (cost)

Cost variance

© APM 2008. Reproduced under licence from APM

Variance Thresholds

41

CPI > 1, SPI < 1 Under spent and late

CPI < 1, SPI > 1 Over spent and early

CPI > 1, SPI > 1 Under spent and early

CPI < 1, SPI < 1 Over spent and late

COST PERFORMANCE

INDEX (CPI)

SCHEDULE PERFORMANCE

INDEX (SPI)

1

1

© APM 2008. Reproduced under licence from APM

Performance Trend Charts

42

VARIANCE

Positive

Negative

TIME

Schedule Variance

Cost Variance

© APM 2008. Reproduced under licence from APM

Estimates at Completion

• EAC = ACWP Cumulative + ETC (Estimate to completion)

• Based on the best estimates of the costs still to be incurred

43 © APM 2008. Reproduced under licence from APM

Simple Tests of Reasonableness

• Current performance indicators (SPI and CPI) should be compared with the anticipated performance to achieve either the BAC or the EAC

• To complete performance index (TCPI) provides a means of doing this comparison

• TCPI (BAC) = BAC – BCWP BAC – ACWP

• TCPI (EAC) = BAC – BCWP

EAC – ACWP

44 © APM 2008. Reproduced under licence from APM

TCPI Period

1 2 3 4 5 BCWS 10 20 50 80 120 BCWP 10 10 20 60 100 ACWP 12 15 30 80 110

BAC 120 120 120 120 120 EAC 120 130 160 150 130

CPI 0.83 0.67 0.67 0.75 0.91

TCPI(BAC) 1.02 1.05 1.11 1.50 2.00 TCPI(EAC) 1.02 0.96 0.77 0.86 1.00

45 © APM 2008. Reproduced under licence from APM

Checking forecast costs and dates

• To extrapolate future cost assuming past performance:

• EAC = BAC / CPI

• ETC = (BAC – BCWP) CPI

• To extrapolate future dates assuming past performance:

• Forecast Completion = Original Completion / CPI

46 © APM 2008. Reproduced under licence from APM

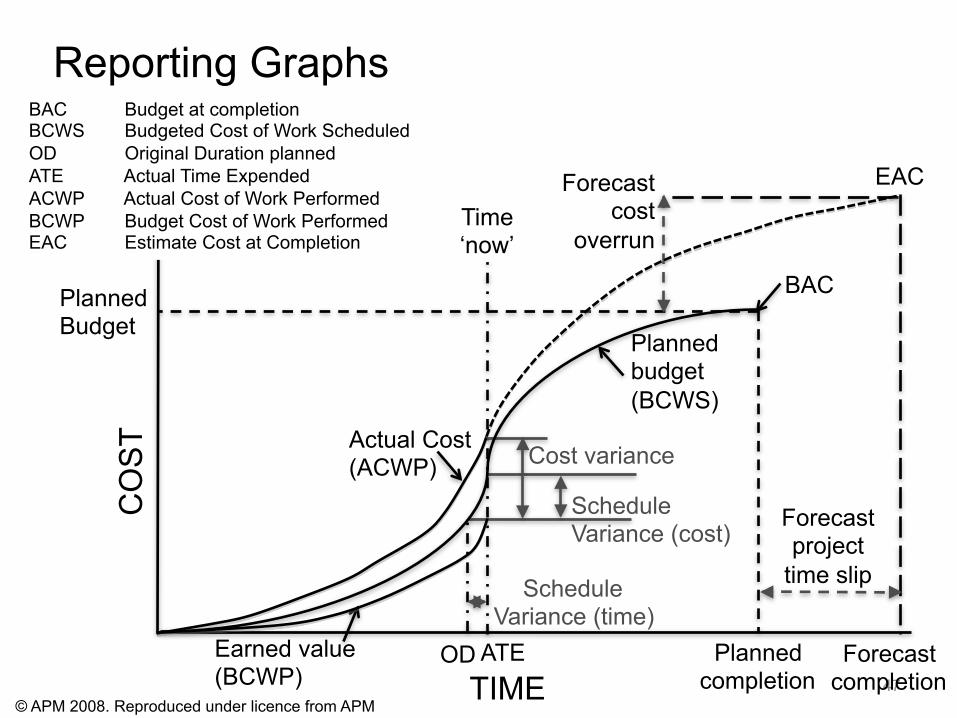

47

Reporting Graphs

TIME

CO

ST

Planned completion

Planned Budget

BAC

Planned budget (BCWS)

EAC

Forecast project

time slip

Actual Cost (ACWP)

Earned value (BCWP)

OD ATE

Forecast cost

overrun Time ‘now’

BAC Budget at completion BCWS Budgeted Cost of Work Scheduled OD Original Duration planned ATE Actual Time Expended ACWP Actual Cost of Work Performed BCWP Budget Cost of Work Performed EAC Estimate Cost at Completion

Schedule Variance (time)

Schedule Variance (cost)

Cost variance

Forecast completion

© APM 2008. Reproduced under licence from APM

Change Management

48

Change Management

• The change management process ensures change is assessed and incorporated into the project baseline in a timely and controlled manner

• Key activities: – Identify and raise necessary changes to the control account – Integrate, where applicable, change to associated risks – Ensure that all changes to the performance measurement

baseline (PMB) are reflected within the associated forecast plans – Ensure that changes are embodied within all elements of

management systems (toolset, documentation, reports etc) – Seek appropriate approval for change.

49 © APM 2008. Reproduced under licence from APM

Maintaining Integrity

• Changes to past, present and future information should be embodied in the PMB in an orderly and and documented manner

• Approved project baseline is the time-phased budget against which progress and performance are measured and reported (BCWS)

• Current baseline must be traceable back to the original baseline

50

Contract Budget Baseline (CBB)

Performance Measurement Baseline (PMB)

Margin

Management Reserve

© APM 2008. Reproduced under licence from APM

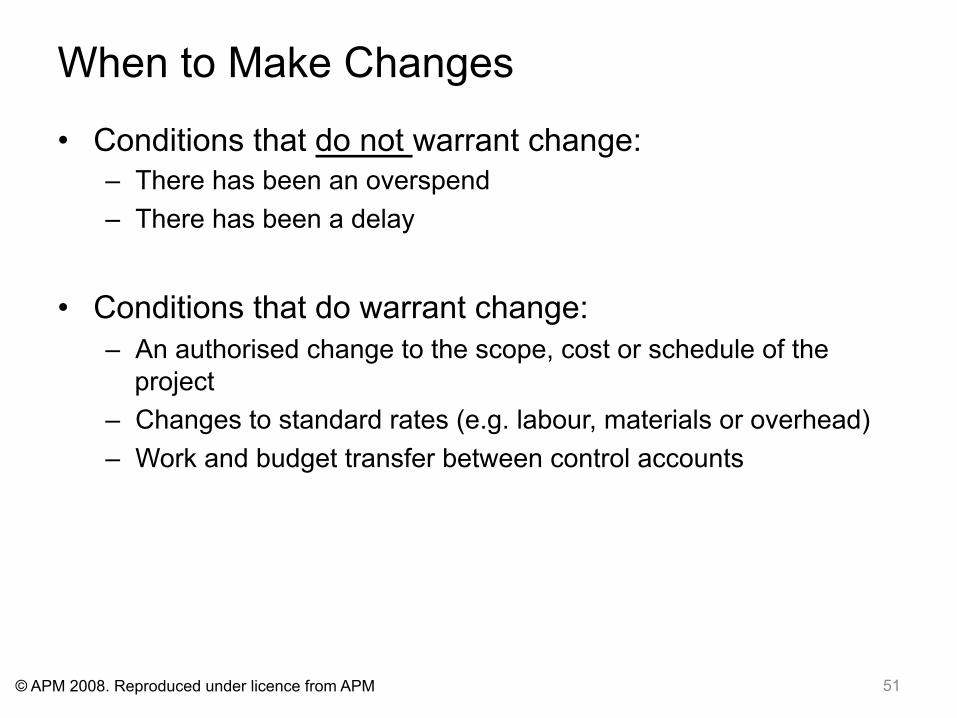

When to Make Changes

• Conditions that do not warrant change: – There has been an overspend – There has been a delay

• Conditions that do warrant change: – An authorised change to the scope, cost or schedule of the

project – Changes to standard rates (e.g. labour, materials or overhead) – Work and budget transfer between control accounts

51 © APM 2008. Reproduced under licence from APM

How to Make Changes

• Baselines are updated by either: – Adding extra budget for additional work scope, and/or – Transferring management reserve into the budget baseline

• Additional budgets can be incorporated by: – Generating new work packages – Closing existing work pages and opening new work packages

• Additional budget must not be assigned to closed work packages

52 © APM 2008. Reproduced under licence from APM

Risk Management

53

Risk Management

• The integration of EVM and risk management should provide more realistic earned value assessments and give a better estimate of the project completion cost and timescale

• Key activities: – Risk identification – Risk assessment – Produce response strategy

54 © APM 2008. Reproduced under licence from APM

Benefits of Risk Management

• More realistic business and project planning • Actions being implemented in time to be effective • Greater certainty of achieving business goals and project

objectives • Appreciation of, and readiness to exploit, all beneficial

opportunities • Improved loss control • Improved control of project and business costs • Increased flexibility • Greater control over innovation and business

development • Fewer costly surprises

55 © APM 2008. Reproduced under licence from APM

Integrating Risk Management with EVM

• Estimating project activities (cost and schedule) • Establishing management reserve budget • Creating and controlling the budget and schedule for the

risk management process • Scheduling • Including risk management activities in project

performance analysis • Developing forecasts • Change management

56 © APM 2008. Reproduced under licence from APM

System Review

57

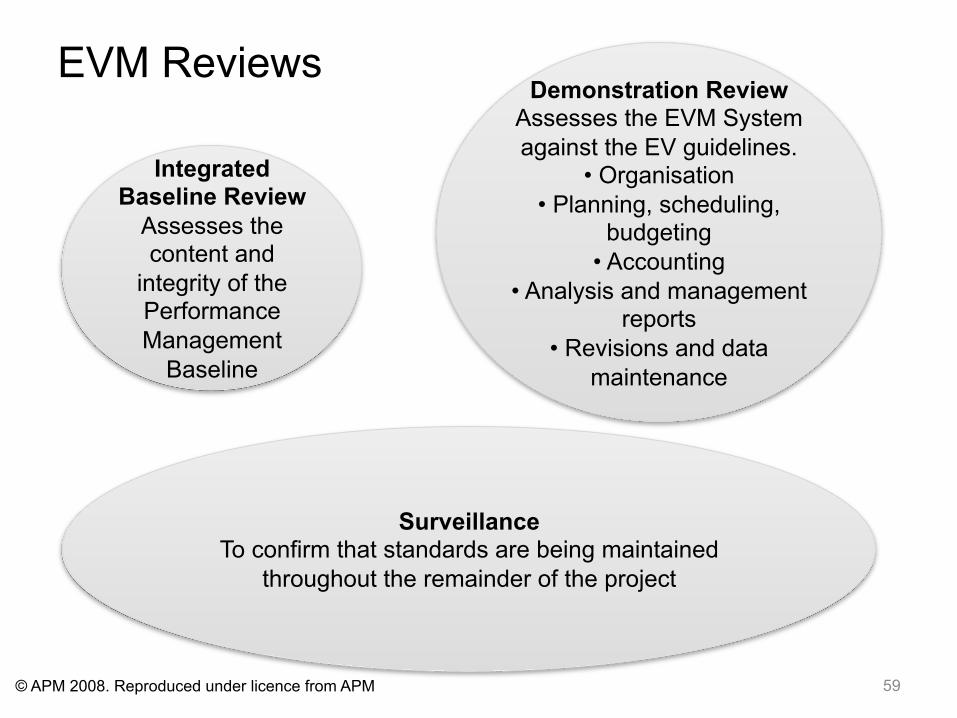

System Review

• Benefits – Confirm that an integrated project management system exists – Provide a fixed cut-off point to conclude the planning phase – Validate reliable performance data – Reduce risk – Ensure that experience from previous projects is captured – Put the focus on performance measurement

• Three main categories – Integrated baseline review (IBR) – Demonstration review – Surveillance

58 © APM 2008. Reproduced under licence from APM

EVM Reviews

59

Integrated Baseline Review

Assesses the content and

integrity of the Performance Management

Baseline

Surveillance To confirm that standards are being maintained

throughout the remainder of the project

Demonstration Review Assesses the EVM System against the EV guidelines.

• Organisation • Planning, scheduling,

budgeting • Accounting

• Analysis and management reports

• Revisions and data maintenance

© APM 2008. Reproduced under licence from APM

Steve Wake EVA booklet APM Guideline for EV PMI Practice standard

Foundation exan Practitioner exam Earned Schedule

EV Compass EV and Risk

60

Thanks

[email protected] 0788 764 4125

www.acoste.org

The Association of Cost Engineers

Company Logo