Embed Size (px)

Citation preview

[Type the document title]

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 1

E- ISSN 2582-7251

Brindavan Journal of Management and Computer Science

National Conference Proceedings- December 2020

Volume 1, Issue 1, December 2020

Impact on Financial inclusion on economic Growth: A

Study with reference to Scheduled Commercial Banks

Sunita Chikkaveerayyanavar, Research Scholar, Karnataka State Akkamahadevi Women’s

University, Vijayapura

Dr. G. H. Kallimath, Research Guide, Karnataka State Akkamahadevi Women’s University,

Vijayapura

Brindavan Research Journal Volume 1, Issue 1, December 2020

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 2

Impact on Financial inclusion on economic Growth: A

study with reference to Scheduled Commercial Banks

Sunita Chikkaveerayyanavar, Research Scholar, Karnataka State Akkamahadevi Women’s

University, Vijayapura

Dr. G. H. Kallimath, Research Guide, Karnataka State Akkamahadevi Women’s University,

Vijayapura

Abstract: India is the fastest-growing economy in the world. Commercial banks act as

a vibrant sector in the economy and contribute significantly to the economic

development of the country. The success of commercial banks depends on effective

financial inclusion which boosts the improved and sustainable social and economic

growth of the country. Financial inclusion is an important driver of economic growth

and has attained national priority to enable the inclusive growth of financially

excluded weaker sections of the society. The paper attempts to study how financial

inclusion is linked with economic growth in India. The paper evaluates the impact of

financial inclusion on economic growth in India. Further explores the impact of

financial inclusion on economic growth in Karnataka. The study analysed to throw

light on economic growth indicator GDP and Financial inclusion indicators like bank

branch growth and Credit-Deposit ratio. To evaluate the impact correlation and

regression tools have been used.

The study reveals that GDP and Financial inclusion indicators are correlated. The

result shows that the branch growth and Credit-Deposit ratio have found positive

significant impact on GDP in Indian and Karnataka.

Keywords: Financial Inclusion, Commercial Banks, Economic growth, Gross

Domestic Product (GDP) and Credit-Deposit ratio

* Names of authors are listed alphabetically.

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 3

1. INTRODUCTION

Commercial banks play a pivotal role in the economic development of a country. Indian economy in

general and banking sector, in particular, have made tremendous progress in the last few years. The

Indian banking industry has achieved progress in terms of expansion of branch network, growth of

deposits and credit etc. Despite this admirable progress, certain groups of the population are unable to

access financial services such as bank accounts, credit and financial services. As per census 2011, only

58.7% of the population has access to banking services in India. World Bank Financial Access Survey

indicates that Financial Exclusion measured in terms of bank branch density, ATM growth and Credit –

Deposit ratio is quite low in India as compared to the most developed countries in the world.

In such a situation the term financial Inclusion gained enough attention to overcome these bottlenecks

to finance the financially excluded segment of the society. Financial inclusion plays a key role in the

process of economic development by enhancing the resource base of the financial system in terms of

saving among a large segment of the population in India (RBI report). GOI and RBI have designed

financial inclusion programmes through introducing several financial inclusion initiatives such as

Pradhan Mantri Mudra Yojana (PMMY), Pradhan Mantri Jan Dhan Yojana (PMJDY), Udyogini

Scheme etc. to provide finance unreached people. Apart from financial services several financial

education centres have established to provide education about banking and financial services. These

efforts resulted in a positive impact on the living standard of people and the economic development of

the country.

Definition of Financial Inclusion

Financial Inclusion is universal access to a wide range of financial services at a reasonable cost. These

include not only banking products but also other financial services such as insurance and equity

products (The committee on Financial Sector Reforms, Chairman: Dr Raghuram G Rajan). Financial

Inclusion is the process of ensuring access to appropriate financial products and services needed by all

sections of the society in general, and vulnerable groups such as weaker sections and low-income

groups in particular, at an affordable cost in a fair manner by regulated mainstream institutional players

(Chakrabarty, 2010). Financial inclusion is the absence of price or non-price barriers in the use of

financial services. They further add that it aims at improving access to financial services, which entails

improving the degree to which financial services are available to all at a fair price (Hannig and Jansen

2011).

Financial Inclusion and Economic Growth

Financial Inclusion is the key driver of the economic growth of the nation. Financial inclusion provides

financial services to unbanked people through financial institutions to achieve sustainable development

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 4

and economic growth of the country. Financial institutions are the financial intermediaries that help to

strengthen the financial system of an economy. It generates economic activities by providing safe

custody of savings, sanction loan for multi-purposes to all segments of the society at an affordable rate.

Their effective and sound operations make the life of the people more comfortable and easier, which in

turn facilitates economic growth and development of the nation.

Financial inclusion is the burning issue in India and has been measured through commercial banks in

terms of opening new branches, Opening of new ATM centre, expanding ICT to rural areas, bank

lending advances and accepting deposits at an affordable cost to all segment of the society.

GDP is an indicator of the economic growth and development of the country. The service sector

contributes more than half of GDP in India. An increasing GDP is the indication of inclusive growth

which reflects in development of the people in the society. Further inclusive growth can be achieved

only when weaker sections of the society developed on par with other sections of the society in respect

of economic development.

In light of this scenario, the present study attempts to study the progress of financial inclusion in India

and Karnataka and analyzed the impact of financial inclusion on economic growth.

.

2. REVIEW OF LITERATURE

Josiah Aduda and Elizabeth Kalunda (2012) used a banking model to analyse the progress of

financial inclusion in Kenya. The study concluded that financial inclusion intervention measure should

continue with the array of products to promote financial inclusion effectively.

Anjali pathania (2016) focussed on financial inclusion indicators like the opening of new bank

branches, new ATM’s, covering unbanked villages etc. are the prerequisite for financial inclusion. In

addition to financial inclusion indicators, an effective and sound financial inclusion index must be

calculated by considering quality dimensions, which in turn gives a true picture of the level of financial

inclusion.

Dr Gudipati Vijayudu (2017) concluded that commercial banks have not benefitted from financial

inclusion in terms of deposits and business correspondence due to losses.Badar Alam Iqbala and Shaista

Sami (2017) conducted examines impact financial inclusion on the economic growth of the Indian

economy. Results of the study indicate a positive and significant impact of the number of branches and

credit-deposit ratio on GDP of the country.

Kehinde A Adetiloye (2017) conducted a study to highlight the relationship between financial

inclusion and economic growth. The study found that credit delivery to the private sector has an

insignificant impact on economic growth in Nigeria and financial inclusion has promoted poverty

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 5

alleviation through rural credit delivery. Dinabandhu Sethi and Debashis Acharya (2017) conducted a

study to highlight the linkage between financial inclusion and economic growth. The study used panel

causality test to find the direction of casualty between financial inclusion and growth of the economy.

The findings confirm that financial inclusion is one of the main drivers of economic growth of the

country.

Sanjay Kumar Singh (2018) in their study on Impact of Indian Commercial Banks in Financial

inclusion found that the important areas of financial inclusion like financial literacy, credit counselling,

BC model, KYC norms etc. yet to be performed by commercial banks in India. The study

recommended to the government to implement financial schemes at effective literacy level to enhance

knowledge of financial inclusion in India. Suman Dahiya and Manoj Kumar (2020) study are based on

secondary data extracted from the IMF and World Bank databases. The study findings show a

considerable positive relationship between economic growth and financial inclusion measures in India.

But financial inclusion index results were not satisfactory..

3. RESEARCH METHODOLOGY

3.1 Research methodology

The study is based on secondary data that has been collected from secondary sources like RBI report,

Economic Survey reports, Journals and other publications from 2014 to 2019. The data has been

analysed with the help of SPSS version 17.0. T-test, correlation and Multiple Regression Model has

been applied to achieve the objectives.

Objectives of the study

1. To examine the progress of financial inclusion of Scheduled Commercial Banks in India as well

as in Karnataka.

2. To study the impact of financial inclusion indicators on the economic growth of India.

To study the impact of financial inclusion indicators on the economic growth of Karnataka

3.2 Hypothesis

H1: There is a significant impact of financial inclusion on the economic growth of Indian

Economy.

Sub-hypothesis

H1.1: There is a significant impact of the number of bank branches on GDP in India.

H1.2: There is a significant impact of Credit-Deposit Ratio on GDP in India.

H2: There is a significant impact of financial inclusion on the economic growth of Karnataka

Economy.

Sub-hypothesis

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 6

H2.1: There is a significant impact on the number of bank branches on GDP in Karnataka.

H2.2: There is a significant impact of Credit-Deposit Ratio on GDP in Karnataka.

3.3 Research Design

The study design measure through dependent variable and independent variables and considered GDP

as the dependent variable and financial inclusion indicators like the number of bank branches and

credit-deposit ratio as independent variables. The data has been analysed to establish a relation between

financial inclusion and economic growth through multi-regression analysis from 2014 to 2019.

R represents the correlation between the dependent variable and independent variables. R2

is the

measure used to test the significance of the regression model in explaining the relationship between

GDP and financial inclusion indicators. P-value indicates to predict whether the relationship is

significant. The presence of autocorrelation in regression model raises questions about the validity of

the model. In this regard, Durbin-Watson test has been applied as a measure to test autocorrelation

between successive observations in the data. Further, a good regression model should be free from

multi co-linearity. The study examines the correlation between independent variables through multi co-

llinearity.

The Regression Model is as follows:

Y= b0 + b1 X1+b2 X2 + E

Y= GDP

b0 = Intercept Co-efficient

b1 and b2 = Co-efficient of for each independent variables.

X1= No. of Bank Branches

X2= Credit-Deposit Ratio

4. Results and Discussion

Impact of Financial Inclusion on Economic growth in India

Commercial banks have achieved success at the national level in terms of number of branches and

credit-deposit ratio to uplift the economic growth of the nation

Table-1

GDP and Financial Inclusion Indicators in India

Year GDP(crores) No. Of Bank

Branches

Credit-Deposit Ratio

2014 1867407 120965 79.0

2015 2073714 130482 77.1

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 7

2016 2294787 134858 78.4

2017 2492967 140216 73.8

2018 2609016 141909 76.7

2019 2786855 145374 78.3

Source: RBI published reports

Figure 1: Growth of GDP in India from 2014 to 2019

Figure 2: Growth of Branches of Scheduled Commercial Banks from 2014 to 2019

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 8

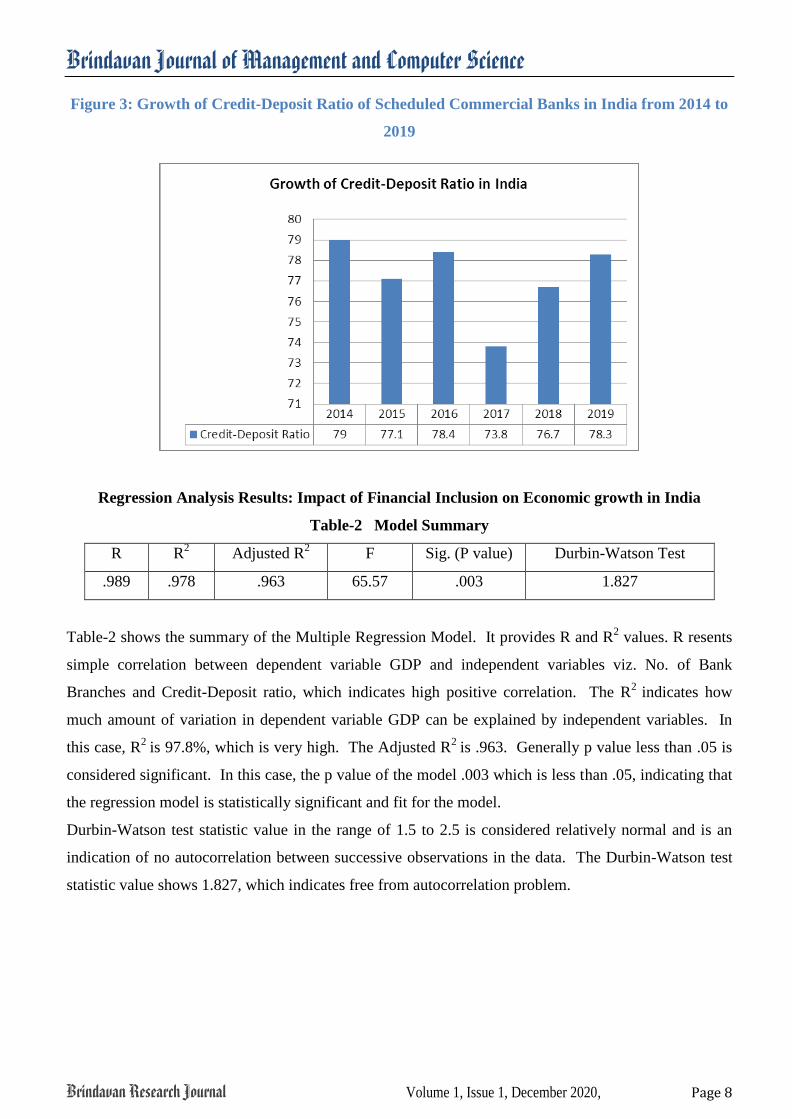

Figure 3: Growth of Credit-Deposit Ratio of Scheduled Commercial Banks in India from 2014 to

2019

Regression Analysis Results: Impact of Financial Inclusion on Economic growth in India

Table-2 Model Summary

R R2

Adjusted R2 F Sig. (P value) Durbin-Watson Test

.989 .978 .963 65.57 .003 1.827

Table-2 shows the summary of the Multiple Regression Model. It provides R and R2 values. R resents

simple correlation between dependent variable GDP and independent variables viz. No. of Bank

Branches and Credit-Deposit ratio, which indicates high positive correlation. The R2

indicates how

much amount of variation in dependent variable GDP can be explained by independent variables. In

this case, R2

is 97.8%, which is very high. The Adjusted R2

is .963. Generally p value less than .05 is

considered significant. In this case, the p value of the model .003 which is less than .05, indicating that

the regression model is statistically significant and fit for the model.

Durbin-Watson test statistic value in the range of 1.5 to 2.5 is considered relatively normal and is an

indication of no autocorrelation between successive observations in the data. The Durbin-Watson test

statistic value shows 1.827, which indicates free from autocorrelation problem.

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 9

Table-3

Regression Co-efficient

Variables Unstandardised

Co-efficient

B

Standardised

Co-efficient

t-

values

Sig. (p

value)

Tolerance VIF H1

Rejected/

Accepted

Constant -4.482 -2.786 .69

No. Of Bank

Branches

39.595 1.027 10.826 .02 .828 1.208 Accepted

Credit-

Deposit ratio

18976.626 .104 1.095 .354 .828 1.208 Rejected

Dependent Variable: GDP

Table-3 portrays regression analysis financial inclusion indicators and GDP of the economy of India.

The results show that in case of No. of Bank Branches, the Beta value is 39.595 and p value is .02,

which is less than .05 at 5% significance level, indicates a positive significant impact on GDP. Further,

the analysis reveals that the Beta value of Credit-Deposit ratio is 18976.626 and the p value is .354,

which is more than .05, indicates the positive statistically insignificant impact on GDP.

Moreover, the Tolerance level and Variance Inflation Factor (VIF) measures used to indicate the multi

co-linearity. As a rule of thumb, if VIF value lies between 1 and 10, shows no multi co-linearity and if

VIF values lie between <1 or>1, shows sign of multi co-linearity. Based on the regression co-efficient

output, the VIF obtained is1.208, indicating that the VIF obtained value is between 1 and 10, it can be

concluded that there are no multi co-llinearity symptoms.

The Regression equation was as follows:

Y=-4.482+ 39.595X1 + 18976.626 X2 + E

Testing Hypothesis and Interpretation

From the analysis p value is .003, which s less than the .05. Therefore, the alternative hypothesis is

accepted. It is found that the strong significant impact of financial inclusion indicators on economic

growth in India.

Impact of Financial Inclusion on Economic growth in Karnataka

Sadhan Kumar (2011) conducted a study on the index of financial inclusion based on penetration,

availability and usage. The results of this study indicate that only three states have achieved high

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 10

financial inclusion. Karnataka is one of those 3 states.

Table-4

GDP and Financial Inclusion Indicators in Karnataka

Year GDP(lakhs) No. Of Bank

Branches

Credit-Deposit Ratio

2014 3481860 8625 76.5

2015 3976689 9365 72.6

2016 4538028 9640 75.4

2017 4788732 10037 71.2

2018 5056379 10041 75.7

2019 5294029 10285 75.1

Source: RBI published reports

Figure 4: Growth of GDP in Karnataka from 2014 to 2019

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 11

Figure 5: Growth of Branches of SCBs in Karnataka from 2014 to 2019

Figure 6: Growth of Credit-Deposit Ration of SCBs in Karnataka from 2014 to 2019

Regression Analysis Results: Impact of Financial Inclusion on Economic growth in Karnataka

Table-5 Model Summary

R R2

Adjusted R2 F Sig. (P value) Durbin-Watson Test

.998 .996 .993 379.449 .0004 2.291

Table-4 reveals the summary of multiple regression models. It shows R and R2 values. R represents a

simple correlation between the dependent variable and independent variables. The value of R is .993,

which indicates a high positive correlation between GDP and financial inclusion indicators i.e. No. of

Bank Branches and Credit-Deposit Ratio. The R2 indicates how much amount of variation in

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 12

dependent variable GDP can be explained by independent variables i.e. financial inclusion indicators.

In this case, R2 is 99.6%, which is very high. Adjusted R

2 is .993. The p value of the model is .0004

which is less than .05. It indicates the regression model is statistically significant and fit for the model.

Durbin-Watson test used to test autocorrelation. The test statistic value of Durbin-Watson test shows

2.291, which indicates free from autocorrelation problem.

Table-6

Regression Coefficient

Variables Unstandardised

Co-efficient

B

Standardised

Co-efficient

t-

values

Sig.

(p

value)

Tolerance VIF H1

Rejected/

Accepted

Constant -1.204 -

10.527

.002

No. Of Bank

Branches

1175.696 1.043 27.365 .0003 .903 1.107 Accepted

Credit-Deposit

ratio

69854.307 .210 5.507 .012 .903 1.107 Accepted

Dependent Variable: GDP

Table-6 portrays regression analysis of financial inclusion indicators and economic growth in

Karnataka. The regression analysis results show that the Beta value of No. Of Bank, Branches is

1175.696 and p value is .0003, which is less than .05 at 5% significance. It indicates a positive

significant impact on GDP. Further, the analysis reveals that the beta value of Credit-Deposit Ratio is

69854.3 and p value .012, which is less than .05 as the rule of thumb. It reveals that Credit-Deposit

Ratio has positive significant impact on GDP.

Moreover, the tolerance level and VIF indicators used to measure multi co-linearity. As a rule of

thumb, if VIF values lie between 1 and 10, shows no multi co-linearity. Based on regression co-

efficient output, the VIF obtained value is 1.107, which lies between 1and 10 and it can be concluded

that the regression model is free from multi co-linearity symptoms.

The Regression equation was as follows:

Y=-1.204+ 1175.696 X1 + 69854.31 X2 + E

Testing Hypothesis and Interpretation

Based on regression analysis p value is .0004, which is less than .05. Therefore the alternative

hypothesis is accepted. It is found that the financial inclusion indicators like No. of bank branches and

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 13

Credit-Deposit ratio have a strong significant impact on economic growth in Karnataka.

5. CONCLUSION AND SUGGESTIONS

Financial inclusion plays a key role in building integrity and stability for the financial system and

channelizes the financial sectors to achieve sustainable growth. Commercial banks are the financial

intermediaries have shown substantial growth in the economic and social development of the country

through sound financial inclusion programmes. Financial inclusion acts as an engine for inclusive

economic growth. Due to potential benefits associated with financial inclusion, a developing country

like India is promoting financial inclusion in their economies.

The present study found that the number of bank branches has a positive significant impact on GDP of

the Indian economy. But another financial indicator credit-deposit ratio has shown a positive

insignificant impact on GDP. On other hand, the study also found that the financial inclusion indicators

number of branches and credit-deposit ratio have a positive impact on GDP of Karnataka economy.

Hence, the study observed that financial inclusion has a robust relationship with the economic growth

of the country. The results of the present study are also similar to that of Badar Alam Iqbala and Shaista

Sami (2017) where financial inclusion strongly associated with economic growth and development of

the country. Despite this success, there is a need to frame comprehensive financial inclusion plans and

implement effectively to access financial services and enhance the knowledge of financial literacy to

achieve inclusive growth

REFERENCES

1. Josiah Aduda1 and Elizabeth Kalunda (2012) Financial Inclusion and Financial Sector Stability

With Reference To Kenya: A Review of Literature. Journal of Applied Finance & Banking.

2. Suman Dahiya and Manoj Kumar (2020) Linkage between Financial Inclusion and Economic

Growth: An Empirical Study of the Emerging Indian Economy. in.sagepub.com/journals-

permissions-India.

3. Sanjay Kumar Singh (2018) Impact of Indian Commercial Banks in Financial Inclusion. The

International Research Journal of Social and Management.

4. Badar Alam Iqbala and Shaista Sami (2017) Role of banks in financial inclusion in India.

Transnational Corporations Review.

5. Kehinde A Adetiloye (2017) Financial Inclusion as a Strategy for Enhanced Economic Growth and

Development.. Journal of Internet Banking and Commerce, May 2017, vol. 22, no. S8.

6. Dr V. B. Khandare (2019) Financial Inclusion: Empirical Study of Brics Countries.

International Journal of Social Science and Economic Research ISSN: 2455-8834 Volume: 04,

Issue: 05 "May 2019"

7. Dinabandhu Sethi and Debashis Acharya (2017) Financial Inclusion and Economic Growth

Linkage: Some Cross Countries Evidence. Journal of Financial Economic Policy.

8. Hamad Omar Bakar and Zunaidah Sulong (2018) The Role of Financial Inclusion on Economic

Growth: Theoretical and Empirical Literature Review Analysis. Journal of Business &

Financial Affairs, ISSN: 2167-0234, Volume 7, Issue 4, 1000356.

Brindavan Journal of Management and Computer Science

Brindavan Research Journal Volume 1, Issue 1, December 2020, Page 14

9. Dr Gudipati Vijayudu (2014) Role of Indian Banks for Financial Inclusion. EPRA International

of Economic and Business Review.

10. Anajali pathania (2016) Quality Dimension Imperative for Innovative Financial Inclusion: A

Case Study of Selected Banks in J & K. Amity Business Review