Embed Size (px)

Citation preview

DUBAI REAL ESTATE MARKET OVERVIEW

Q3 2017

REAL ESTATE SERVICES

2

FOREWORD ADIB Real Estate Services comprises a comprehensive real estate banking and advisory platform providing the full range of professional services from a single provider. Our services include:-

�� Real estate financing�� Strategic development advisory�� Investment advisory�� Asset management�� Project management

�� Valuation�� Agency�� Market research�� Property management�� Facilities management

Residential

�� Approximately 3,600 new units, the total residential stock of Dubai reached 510,000 units as of Q3 2017. During the nine months of 2017, c.14,500 units were added with 75% being apartments and 25% villas/townhouses.

�� During the quarter residential rents soften by 1% while year-on-year the decline was 6%. Multiple factors like addition of new residential units, increase in ownership and constrained job opportunities are impacting the rental rates and occupancy levels.

�� During the quarter, sale rates for villas and apartments recorded a marginal decline of 1% and 4.5% year-on-year. Within the villas segment, Arabian Ranches recorded the highest decline of 6.5% year-on-year while Downtown Dubai recorded a decline of 7% year-on-year within the apartment segment.

�� During the quarter over 9,000 new off-plan properties were launched. The Cityscape Global, the annual real estate exhibition further fueled launch of new properties. Moreover, for the first time developers were allowed to sell properties during the event and resulted in transaction of AED870 million worth of property during the three day event.

Office

�� The total office stock of Dubai reached 96 million sq.ft. during Q3 2017, with the addition of 1.1 million sq.ft. of office space being added in this quarter. New additions include office tower from One Central development, First Abu Dhabi bank building in Al Jadaf and low-rise office towers from Umm Al Sheif area.

�� Average office rents dropped by 4% year-on-year, while quarter-on-quarter the rates remained unchanged.

Leasing enquiries during the quarter mostly emanated from existing companies looking to migrate to newer buildings that offer quality space and market aligned rental rates.

�� Office sale rates remained stable during the quarter and registered a 3% drop year-on-year. In terms of rental decline by location development, Downtown Dubai recorded the highest annual drop of 7% followed by Barsha Heights at 5%.

Retail

�� With the addition of 9600,000 sq.ft. of gross leasable area (GLA), during Q3 2017 the total retail stock of Dubai account to 35.5 million sq.ft. GLA, as of end Q3 2017. During the quarter, Marsa Al Seef by Meraas located along the creek, a new retail destination, opened its door to public.

�� Challenging economic conditions, softening sales of luxury segment, rise in supply and online shopping penetration are putting pressure on the mall operators to review existing leases, as retailers are looking to downsize / consolidate their operations.

Hospitality

�� Hotel performance continues to be under pressure during the quarter, as a result of continued pricing competition in the market to retain desired occupancy levels during the summer period. On an average ADR’s dropped by around 10% during the quarter, as operators continue to focus on the overall revenue growth / stability.

�� With the addition of 585 rooms during the quarter, the total hotel supply of Dubai reached to 107,000 rooms and apartments. Looking at the ongoing construction activity, we expect c.800 rooms to enter during the last quarter of the year.

3

CONTENTSDemand Drivers 4

Macro Trends 6

Residential Sector 8

Project Focus 14

Office Sector 16

Retail Sector 22

Hospitality Sector 24

Definitions & Methodology 26

Contact Information 27

Supply - Photo Gallery 28

Development Location Map 30

MPM PROPERTIES FACTS AND FIGURES

TOTAL UAE STAFF PROPERTY MANAGEMENT STAFF ADVISORY STAFF

UNITS UNDER MANAGEMENT

LEASING & SALES STAFF LANDLORD CLIENTS

COMBINED MARKET VALUE OF PROPERTIES VALUED SINCE JANUARY 2012

MORTGAGE VALUATIONS SINCE JANUARY 2012

DEDICATED VALUATION PROFESSIONALS

OCCUPANCY RATE

LARGEST ABU DHABI MAINLAND PORTFOLIO

160+

7,600+

No.1

98.5%20+

30+

90bn

35+

23,500+

95+

1,700

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

4

DEMAND DRIVERS

REAL ESTATE AND CONSTRUCTIONHEALTHY INVESTOR INTEREST FOR LARGE AND SMALL ASSETS

�� Damac Properties awarded AED628 million contract to Arabtec for building 1,296 villas in Akoya Oxygen development located between Emirates Road and Al Qudra Road. The masterplan development is spread across 55 million sq.ft. offering residential, retail, hospitality and entertainment components along with a 18 hole golf course. The construction is expected to commence in Q3 2017, with completion in 24 months.

�� Belhasa Engineering & Contracting Company

has won AED600 million contract from Deyaar Properties PJSC to build two districts of the Midtown project in Dubai Production City. The two districts of Afnan and Dania offer a total of 1,238 residential units comprising of studio, one, two and three bedroom units. The construction period for the two districts is expected to be completed within 29 months. The Midtown project comprises of a total of 27 buildings spread across six districts on a 1.2 million sq.ft. plot and is expected to have a built-up area of c.5 million sq.ft. on completion.

FREEZONES SIGNING UP NEW TENANTS; CREATING EMPLOYMENT OPPORTUNITIES

�� DMCC Freezone, master developer of Jumeirah Lakes Towers (JLT) announced construction of a 10 million sq.ft development ‘Uptown Dubai’ located in close proximity to JLT. The development comprises of seven towers atop seven levels of podium offering Grade A office space, 3,000 luxury apartments, 200 retail and F&B outlets along with luxury hotels. The development is expected to create over 10,000 new job opportunities.

�� Jebel Ali Freezone recorded a 17% growth across

non-oil foreign trade reaching 27.9 million tonnes in 2016 compared to 23.9 million tonnes in 2015. Machinery, electronics and electrical goods dominated the trade with a share of 49% followed by petrochemical, oil and gas sector 16% and food and FMCG at 8%. The total value of non-oil foreign trade valued at US$80.2 billion. In terms of trade by region, trade with Asia Pacific region accounted at US$32.4 billion followed by the Middle East at US$27.2 billion, the Europe US$9.9 billion, the Americas US$5.5 billion and Africa at US$5 billion.

GOVERNMENT INITIATIVESATTRACTING ENTREPRENEURS; IMPROVING EASE OF DOING BUSINESS

�� The President, His Highness Sheikh Khalifa bin Zayed Al Nahyan, has issued the Federal Law No. 7 of 2017 for Tax Procedures. The Law defines a clear set of common procedures and rules to be applied to all tax laws in the UAE and clearly states the respective rights and obligations of the Federal Tax Authority and the taxpayer. The Law covers tax procedures, audits, objections, refunds, collection, and obligations - which include tax registration, tax-return preparation, submissions, payment and voluntary disclosure rules - in addition to tax evasion and general provisions.

�� Dubai Holding has appointed Tecom Group to develop the Emirates Business Park project. The AED 5 billion mixed use project, includes four high rise towers and a number of other buildings. The new business park will offer premium office space along with three five-star hotels, plus food and beverage units, and a space dedicated to host events and other functions. Project is expected to start by the end of 2017 with completion due within four years.

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

5

TOURISM INITIATIVES �� The Roads and Transport Authority (RTA) opened

a new bridge located at the intersection of Airport Road and Marrakech Street. The RTA has also awarded the second contract of Airport Road Improvement project valued at AED404 million which is expected to be completed by end of the year. The project includes an overpass on the Airport Road, with three lanes in each direction, a direct ramp from the bridge heading to Terminal 3 and building a two-lane tunnel to serve traffic heading left from Airport Road towards Marrakech Street.

�� A new station, Al Ittihad Park station opened along the Palm Monorail. The station is located

near the Shoreline apartments and offers direct access to the Palm Jumeirah’s central park and the Golden Mile Galleria mall. The Palm Monorail station network is expected to expand further with new stations been planned at the upcoming developments of Nakheel Mall and the Pointe.

�� Dubai International Airport handled 8.2 million passengers in August 2017, up by 6.6% compared to 7.7 million passengers in August 2016. YTD August 2017, passenger traffic increased by 6.3% to 59.3 million passengers, up from 55.8 million passengers during the same period last year.

TRANSPORTATION IMPROVING ACCESSIBILITY AND REACH IN DUBAI; CREATING JOBS

�� The UAE Cabinet approves visa on arrival at all ports to Indian passport holders carrying a valid EU or UK residency visa. An agreement was also signed between the UAE and the Pacific Island nation of Vanuatu exempting UAE nationals carrying diplomatic, private, VIP and regular passport holders and nationals of Vanuatu carrying diplomatic and private passports from obtaining pre-entry visas.

�� Figures from the Department of Tourism and Commerce Marketing (Dubai Tourism) indicate

a 8.2% rise in visitors to Dubai YTD August 2017 versus the same period last year. During the period YTD August 2017, Dubai had 10.4 million overnight visitors with 21% of the visitors originated from GCC countries, 20% from Western European countries, and 18% from South Asia. In terms of top source market, India ranks top with 1.32 million visitors followed by Saudi Arabia with 1.09 million visitors and the United Kingdom remained third with 0.81 million.

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

6

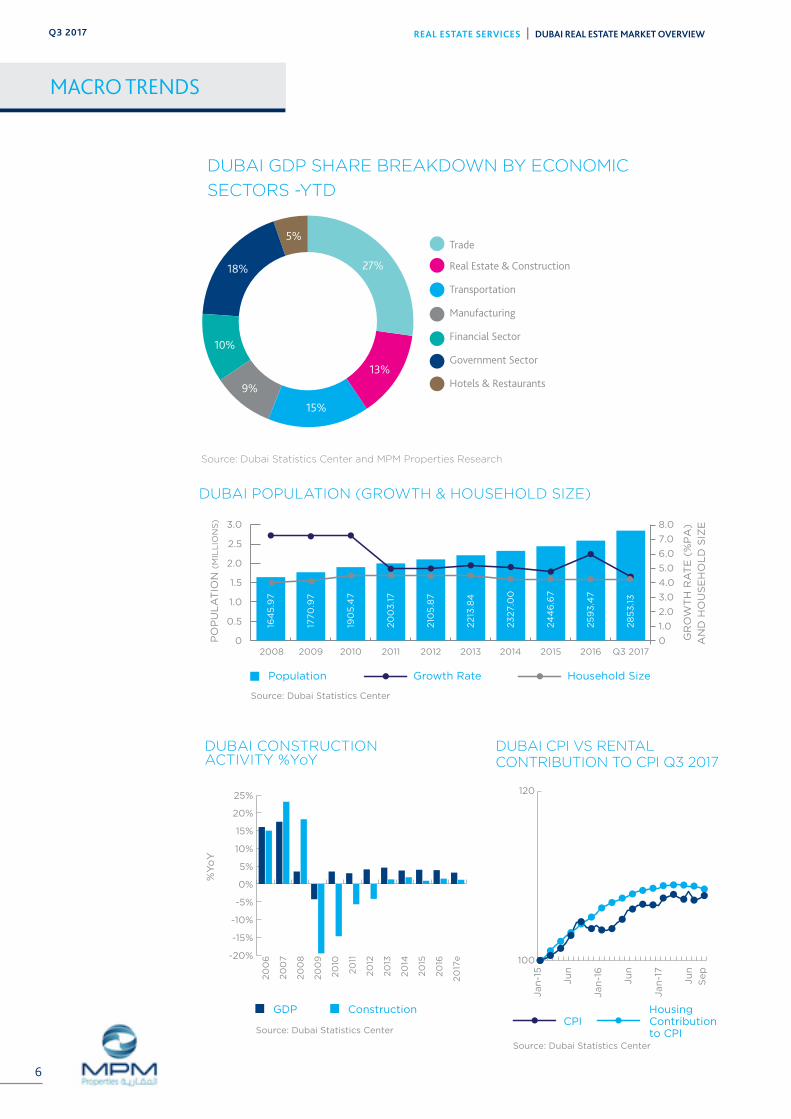

MACRO TRENDS

DUBAI POPULATION (GROWTH & HOUSEHOLD SIZE)

Population Growth Rate

2008

16

45

.97

1770

.97

19

05

.47

20

03

.17

210

5.8

7

2213

.84

23

27.0

0

24

46

.67

25

93

.47

28

53

.13

2009 2010 2011 2012 2013 2014 2016 Q3 20172015

3.0

2.5

2.0

1.5

1.0

0.5

0

8.0

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0PO

PU

LA

TIO

N (

MIL

LIO

NS

)

GR

OW

TH

RA

TE

(%

PA

)

AN

D H

OU

SE

HO

LD

SIZ

E

Household Size

Source: Dubai Statistics Center

DUBAI CONSTRUCTIONACTIVITY %YoY

GDP Construction

%Y

oY

DUBAI CPI VS RENTALCONTRIBUTION TO CPI Q3 2017

CPIHousingContributionto CPISource: Dubai Statistics Center

Source: Dubai Statistics Center

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17e

Jan

-15

Jan

-16

Jan

-17

Sep

Ju

n

Ju

n

Ju

n

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

100

120

Source: Dubai Statistics Center and MPM Properties Research

DUBAI GDP SHARE BREAKDOWN BY ECONOMIC

SECTORS -YTD

5%

27%

13%

15%

9%

10%

18%

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

7

INVESTOR ANALYSIS

2012 2013 2014 2015 2016 2017-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Valu

e (

in M

illio

ns)

Sales Transactions

Tra

nsa

cti

on

s

DUBAI LAND TRANSACTIONSVOLUME vs VALUE

Sales Value

4,000

2,000

0

6,000

8,000

10,000

12,000

0

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014 2015 2016 2017

DUBAI LAND TRANSACTIONSQoQ% CHANGE

Sales Transactions

Source: DLD and MPM Properties Research

* Established Real estate

Source: DLD and MPM Properties Research

TOP NATIONALITIES INVESTING IN DUBAI PROPERTY (JAN 2016 - JUN 2017)

0

200

400

600

800

1,000

Tra

nsa

cti

on

Valu

eA

ED

mill

ion

TOP LOCATIONS - RESIDENTIAL TRANSACTION VALUE

Q2 2017 Q3 2017

Source: DLD

Bu

sin

ess

Bay

Ju

meir

ah

Vill

ag

e

Du

bai

Sp

ort

s C

ity

Ju

meir

ah

Lakes

To

wers

Ara

bia

nR

an

ch

es

Palm

Ju

meir

ah

Ju

meir

ah

Beach

Resi

den

ce

Du

bai

Mari

na

Do

wn

tow

nD

ub

ai

Em

irate

sL

ivin

g

Valu

e (

AE

D' B

illio

ns)

LebanonUSAChinaEgyptJordanPakistanUnitedKingdom

SaudiArabia

IndiaUAE0

5

10

15

20

25

30

35

40

Source: DLD

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

8

RESIDENTIAL SUPPLY �� With the addition of over 3,600 new units,

the total residential stock of Dubai reached 510,000 units as of Q3 2017. During the nine months of 2017, c.14,500 units were added with 75% being apartments and 25% villas/townhouses.

�� Looking at the ongoing construction activity, we expect a further 4,000 new units to be added during the last quarter of the year. Few of the projects that are expected to be handed over during the last quarter include Manara Tower, Reef Residence, Hub Canal 2, Zahra townhouses, Glitz 1 and 2, Yasmin and Samara villas.

�� Real estate projects offering over 9,000 new off-plan properties were launched during

this quarter. Launch of such high number of properties was due to Cityscape Global, the annual real estate exhibition. Furthermore, for the first time developers were allowed to sell properties during the event which led several developers to launch properties at the same time. According to the Dubai land department, AED870 million worth of off-plan properties was sold during the three day event.

�� A few of the projects launched include Azizi Riviera and MAG Eye in Meydan City, Parkland Residences and Views in Dubai South, Seven Residences on the Palm Jumeirah, IGO101 in Jumeirah Lakes Towers, Spanish and Arabian towers in Dubai Sports City.

0

100

200

300

400

500

600

2014 2015 2016 Q42017

Q32017

H12017

2018 2019

Source: MPM Properties Research

Supply Apartments

RESIDENTIAL SUPPLY BY UNITS 2013-2019

Existing Supply Villas +% Change

1.9% 2.7% 3.1% 2.2% 0.7% 1.1% 5.0% 3.8% YoY 3.1%

2013

444 452 469 481 496 507 511 516 542

8.5 14 11 11 8 3 173 1.2 4.2 34

4215

RESIDENTIAL SECTOR

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

9

SAMPLE OF RESIDENTIAL UPCOMING PROJECTS

SAMPLE OF ANNOUNCED PROJECTS IN Q3 2017

NAME OF PROJECT TYPE DEVELOPER LOCATION

Bait Al Aseel Villa Damac Akoya Oxygen

Azizi Riviera Apartments Azizi Meydan

Bin Ghatti Stars Apartments Bin Ghatti Dubai Silicon Oasis

Spanish and Arabian Towers Apartments Dubai Sports City Dubai Sports City

J One Apartments RKM Durar Business Bay

O2 Apartments Tiger Properties Jumeirah Village Circle

Icon Bay Apartments Emaar Dubai Creek Harbour

Parklane Residences Apartments Dubai South Dubai South

Parklane Views Apartments Dubai South Dubai South

Al Haseen Residences Apartments City Properties Dubai Industrial Park

The Life Villa/Townhouses Jumeirah Luxury Living Jumeirah Golf Estates

IGO 101 Apartments Jumeirah Lakes Towers IGO

Seven Residences Apartments Seven Tides Palm Jumeirah

MAG Eye Villa/Townhouses MAG Meydan

Aston Plaza & Residences Apartments Aston Dubai Science Park

LOCATION PROPERTY NAME

Business Bay The Pad

Dubai Motor City OIA Residence

Dubai Studio City Glitz 1 & 2

Manara Tower Jumeirah Village Triangle

Reef Residence Jumeirah Village Circle

Piccadily Green Damac Hills

Zahra Townhouses Townsquare

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

10

RESIDENTIAL SECTOR

Th

eG

reen

s

Ju

meir

ah

Beach

Resi

den

ce

Bu

sin

ess

Bay

Du

bai

Mari

na

Th

eV

iew

s

Palm

Ju

meir

ah

DIF

C

Old

To

wn

Do

wn

tow

nD

ub

ai

APARTMENT AVERAGE SALES PRICES (Q3 2017)AND PERCENTAGE CHANGE

AE

D/s

q.ft.

Source: MPM Properties Research

-1.2% -1.4% 0.0% -1.7% 0.0% 0.0% -1.9% -0.8%0.0% QoQ

YoY -7% -8% -3% -8% -2% -2% -6% -2%-6%

0

500

1,000

1,5002,000

2,500

2,0

00

1,775

1,75

0

1,5

00

1,4

75

1,3

75

1,23

0

1.3

00

1,20

0

SALE PRICES �� The total residential transactions (off-plan and

completed properties) during Q3 2017 were valued at AED13.87 billion. Of these, off-plan properties accounted for 70% of the transactions (AED9.81 billion) and the rest 30% towards completed properties.

�� Transactions for completed properties recorded a year-on-year increase of 4% in value terms and a marginal decline in volume. During Q3 2017 a total of 2,401 transactions were recorded at a value of AED4.06 billion compared to AED3.89 billion during the same period last year. However, quarter-on-quarter the decline has been substantial at 18.6%. Historically transactions during the third quarter of the year remain sluggish due to holiday and festive period.

�� In terms of transactions by unit type, apartments accounted for 65% valued at AED2.62 billion

while villas and townhouses accounted for 35% of the total transaction value at AED1.44 billion.

�� During the quarter, sale rates for villas and apartments recorded a marginal decline of 1% and 4.5% year-on-year. Within the villas segment, Arabian Ranches recorded the highest decline of 6.5% year-on-year while Downtown Dubai recorded a decline of 7% year-on-year within the apartment segment.

�� Substantial increase of off-plan properties is adversely affecting the sales of completed properties. Developers are not only incentivizing the customers with flexible payment plans but also agents with above market norm, commission structure in order to boost the sales.

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

11

RENTS�� During the quarter residential rents soften by 1% while

year-on-year the decline was 6%. Multiple factors like addition of new residential units, increase in ownership and constrained job opportunities are impacting the rental rates and occupancy levels.

�� The highest rental decline within the leasehold areas was recorded across the traditional residential bases of Bur Dubai, Oud Metha, Al Barsha and Al Nahda, wherein the rates have dropped by over 7% year-on-year.

�� The highest brunt was noticed in Bur Dubai area with a 9% rental drop which was primarily due to migration of tenants from ageing structures that offer limited or lack facilities and amenities that are demanded by the tenants. The studio and two bedroom apartments recorded a decline of 11% year-on-year. The two bedroom apartments are currently achieving a rent of AED 82,000-110,000 per unit per annum as compared to AED95,000-120,000 per unit per annum in Q3 2016.

�� Within the freehold areas the highest drop was recorded across the developments of Palm Jumeirah, Downtown Dubai, Discovery Gardens and International City which saw

rents dropping by over 7% year-on-year. The rental decline has been largely noticed across high-end and affordable market segments while the mid-market segment recorded a modest drop.

�� Across the villa segment, Dubai Silicon Oasis, Palm Jumeirah, Springs and Jumeirah Park recorded a decline of over 7% year-on-year. The highest decline was in Jumeirah Park wherein rates dropped by 9% year-on-year, this is mainly due to high rental rates that prevailed at the start of handover and are currently adjusting to the market levels. The four bedroom units within the development dropped from AED190,000-240,000 per unit per annum in Q3 2017 to AED225,000-275,000 per unit per annum in Q3 2016.

�� The residential sector in terms of rental and occupancy performance is expected to remain under stress as substantial new supply is expected to enter the market over the course of next 15 months.

LOCATION STUDIO 1BR 2BR 3BR Q-ON-Q Y-ON-Y

Business Bay 60 78 115 153 -1.33% -6.61%

DIFC 78 105 138 205 -0.58% -5.85%

Discovery Gardens 44 65 90 - -2.29% -7.22%

Downtown Dubai 68 100 150 205 -1.29% -7.28%

Dubai Marina 60 88 130 183 -0.34% -5.32%

Greens 64 83 123 150 -0.88% -6.53%

International City 31 46 65 87 -1.30% -7.79%

Jumeirah Beach Residence

74 100 128 168 -1.71% -4.03%

Jumeirah Lakes Towers 57 85 113 145 -1.40% -3.93%

Palm Jumeirah 78 113 145 182 -1.32% -9.53%

Barsha Heights 57 75 98 130 -3.00% -6.82%

AVERAGE APARTMENT ANNUAL RENTS Q3 2017

Source: MPM Properties Research

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

12

RESIDENTIAL SECTOR

PROJECT 2 BEDROOM 3 BEDROOM 4 BEDROOM 5 BEDROOM Q.O.Q Y.O.Y

Al Furjan - 155 - 215 -1.38% -2.14%

Arabian Ranches 138 175 225 280 -0.98% -6.78%

Dubai Sports City - 168 188 260 -1.60% -7.32%

Jumeirah Park - - 215 273 -1.59% -9.19%

Jumeirah Village 138 145 158 185 0.00% -6.47%

Meadows - 208 235 270 -0.40% -6.07%

Palm Jumeirah - 305 415 455 -1.31% -6.26%

Springs 120 163 - - -0.76% -7.42%

Jumeirah Islands - - 275 350 -0.70% -6.87%

Jumeirah Golf Estates - 235 290 360 -2.10% -10.54%

0

500

1,000

1,500

2,000

2,500

Al F

urj

an

Ju

meir

ah

Vill

ag

e

Sp

rin

gs

& M

ead

ow

s

Ju

meir

ah

Park

Ara

bia

nR

an

ch

es

Du

bai

Sp

ort

s C

ity

Th

eL

akes

Palm

Ju

meir

ah

AVERAGE VILLA SALE PRICE AED/ sq.ft. Q3 2017

AE

D/s

q.ft

Source: MPM Properties Research

0.0%

-3.0%

-2.0%

-7.0%

0.0%

-4.0%

-2.0%

-5.0%

0.0%

-5.0%

0.0%

-4.0%

-2.0%

-5.0%

0.0%

-4.0%

QoQ

YoY

2,4

00

1,275

1,10

0

1,0

50

1,0

50

1,0

00

95

0

975

AVERAGE VILLA ANNUAL RENTS Q3 2017

Source: MPM Properties Research

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

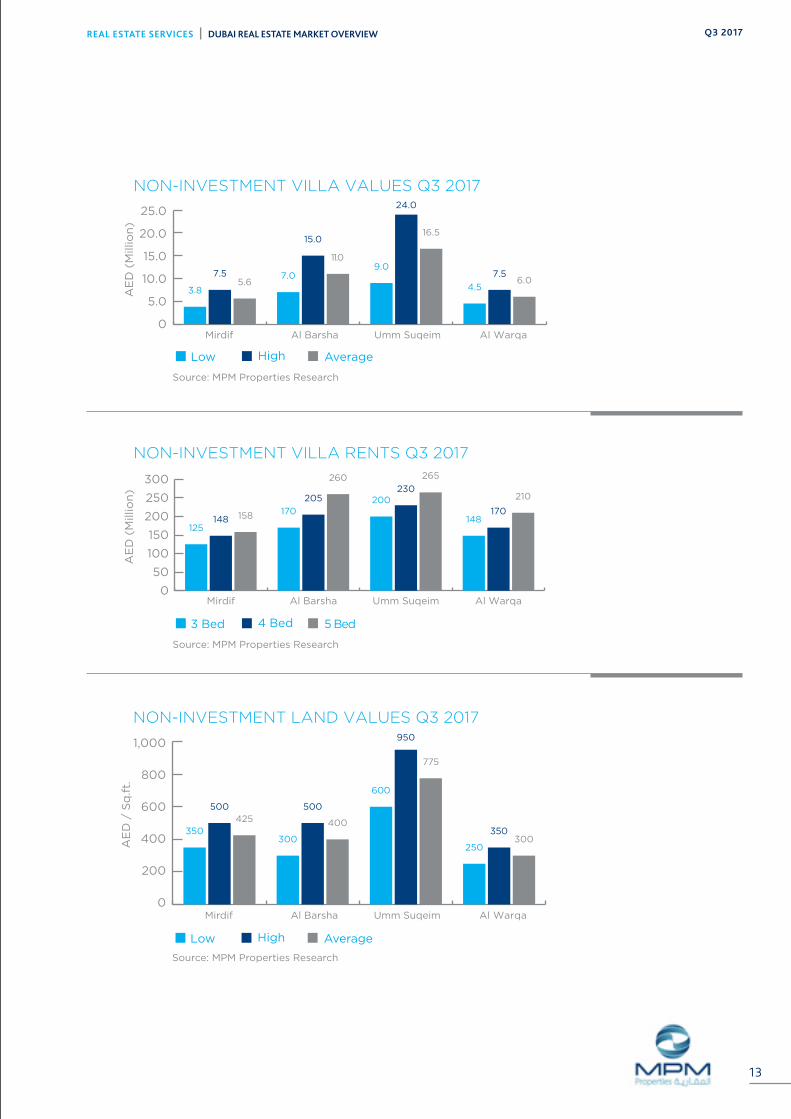

13

350

500425

300

500

400

600

950

775

250

350300

NON-INVESTMENT LAND VALUES Q3 2017

1,000

800

600

400

200

0

AE

D /

Sq

.ft.

Source: MPM Properties Research

Mirdif Al Barsha Umm Suqeim Al Warqa

HighLow Average

NON-INVESTMENT VILLA RENTS Q3 2017

AE

D (

Mill

ion

)

Source: MPM Properties Research

4 Bed3 Bed 5 Bed

0

50

100

150

200

250

300

Al WarqaUmm SuqeimAl BarshaMirdif

148170

210200230

265

170

205

260

125148 158

3.8

7.55.6

7.0

15.0

11.09.0

24.0

16.5

4.5

7.56.0

NON-INVESTMENT VILLA VALUES Q3 2017

25.0

20.0

15.0

10.0

5.0

0

AE

D (

Mill

ion

)

Source: MPM Properties Research

Mirdif Al Barsha Umm Suqeim Al Warqa

HighLow Average

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

14

IMPERIAL AVENUE

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

15

AMENITIES AND FACILITIES

PAYMENT PLAN

One of India’s oldest business conglomerates, Shapoorji Pallonji began as a humble infrastructure development company in 1865. Over the past 150 years, it has come a long way, created many a milestone and constructed world-renowned landmarks across the Indian subcontinent and beyond.

Imperial Avenue is the first real estate project by Shapoorji Pallonji outside India. Needless to mention, the company is

leaving no stone unturned to make exemplary statement with it. An exclusive collection of luxury homes, each in a class of its own, Imperial Avenue offers a chance to reside at the pinnacle of elegance in one of the world’s most celebrated neighbourhoods, Downtown Dubai. Located in a direct nod to Burj Khalifa, it is awe-inspiring, inside out. Right from its fluid design and sophisticated features to its unsurpassed amenities and prestigious location, it is a true jewel in the crown.

Dubai overtook London as the most preferred property investment location for 2017. This is testimony to the sector’s maturity and identity as a safe haven for investment, providing long-term returns. The total return analysis of real estate assets in Dubai stands between 5-11%.

An increase in the rate of economic expansion is expected in 2018 and 2019, underpinned by higher spending levels. For the country’s real estate markets, this is expected to translate into widespread stability and growth in some segments by the end of 2018.

We see a number of positive indicators for the UAE’s property market as we head towards the fourth quarter of 2017. While Expo 2020 is well documented as the shining light on the horizon, we view the government’s plan to introduce a formal tax regime as a tremendously positive step and are confident that it will help cement much-needed alternative revenue streams.

Cyrus EngineerManaging Director

�� 10,000 sq.ft. lobby

�� 2 Infinity pools

�� Apartments with Spacious Private decks

�� Grand Entrance

�� Indoor and outdoor kids play areas

�� Fitness Centre and Squash court

�� Exclusive Private AV room

�� Party Hall

�� 5% Down payment;

�� 40% during construction;

�� 55% on handover

17

UNIT TYPE AREA (SQ.FT.) STARTING PRICE (AED)

One bedroom 825 – 1,100 1.56 million

Two bedroom 1,350 – 1,750 2.5 million

Three bedroom 1,750 – 2,200 3.7 million

Four bedroom 3,065 – 5,100 7.6 million

Five bedroom 5,500 onwards 17.5 million

3,4,5 BR podium villa 3,710-5,935 7.7 million

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

16

OFFICE SUMMARY �� The total office stock of Dubai reached 96

million sq.ft. during Q3 2017, with the addition of 1.1 million sq.ft. of office space being added in this quarter. New additions include office tower from One Central development, First Abu Dhabi bank building in Al Jadaf and low-rise office towers from Umm Al Sheif area.

�� Average office rents dropped by 4% year-on-year, while quarter-on-quarter the rates remained unchanged. Leasing enquiries during the quarter mostly emanated from

existing companies looking to migrate to newer buildings that offer quality space and market aligned rental rates. There are several fully fitted office space in the market that are offered at attractive rates and targeted towards new entrants and SME’s, which avoid incurring capital expenditure towards office fit outs.

�� Looking at the ongoing construction activity, close to a million sq.ft. of office space is due for completion during the last quarter which in anticipated to further inflate the vacancy rates.

OFFICE SECTOR

0

20

40

60

80

120

100

DUBAI OFFICE STOCK (2008 - 2019)

Mill

ion

sq

.ft.

20092008 2010 2011 2012 2013 2014 2015 2016 H12017

Stock Expected

Source: MPM Properties Research

20192018

0.91.10.83.56.82.50.26.0

6.010.0

8.06.0

96

2.8

97

3.8

1009594918481817569595145

Q32017

Q42017

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

17

OFFICE SALES �� Office sale rates remained stable during the quarter

and registered a 3% drop year-on-year. In terms of rental decline by location development, Downtown Dubai recorded the highest annual drop of 7% followed by Barsha Heights at 5%. The sale rates in Downtown Dubai range from AED 1,700 – 2,400 per sq.ft. while in Barsha Heights it ranges between AED 750 – 1,050 per sq.ft.

�� During Q3 2017, office transactions were valued at AED453 million for a cumulative office space of 393,000 sq.ft. with an anticipated sale price of AED1,150 per sq.ft, an increase by 4.8% quarter-on-

quarter. The transaction activity remained strong for office with an area less than 2,500 sq.ft., accounting for 82% of the total transactions in Q3 2017.

�� The two business districts - Business Bay and Jumeirah Lakes Towers dominated the transaction market with over AED350 million worth of sales being concluded during the quarter. Business Bay recorded transactions worth AED254 million across 221,000 sq.ft. at an average of AED1,150 per sq.ft. while Jumeirah Lakes Towers saw transaction of 109,000 sq.ft. at a total value of AED102.4 million, at an average sale price / sq.ft. of AED940.

OFFICE SUPPLY �� The office rents remain flat during the quarter

while year-on-year the rates dropped by 4%. Few large office space enquiries are floating in the market from logistics, online trading companies and business centres who are looking for large floor space across consecutive floors in-close proximity to the metro network to facilitate easy movement for their workforce.

�� The office rents in the CBD area remained unchanged during the quarter, while a drop of 2% was recorded year-on-year. Average rents in the area range between AED85-240 per sq.ft. per annum (all inclusive).

�� The Business Bay area which accounts for 14% of the total existing office space, with majority being strata office space, recording a decline of 2% quarter-on-quarter and 7% year-on-year. The prevailing office rents range between AED65-190 per sq.ft. per annum (all inclusive).

�� Within the DIFC district, office space managed by the DIFC authority continues to record high occupancy and top-end rental rates. The worst impacted segment has been the strata owned office space within the area, which are currently being offered at an all-inclusive rate starting from AED125 per sq.ft. per annum.

Sheikh Mohamed Bin Zayed Rd.

Sheikh Mohamed Bin Zayed Rd.

Sheikh Mohamed Bin Zayed Rd.

Al Khail Road

Al Khail Road

daoR mi equS

mm

U

Sheikh Zayed Rd.

Sheikh Zayed Rd.

Sheikh Zayed Rd.

Arabian RanchesDubai

Land

DubaiLand

DubaiLand

DubaiLand

DubaiLand

Nad AlSheba 2

Nad Al Sheba

DubaiSilicon Oasis

InternationalCity

DragonMark

MushrifNational Park

Murdif

FestivalCity

TOSHARJAH

TOHATTA & OMAN

TOAL AIN

TOABU DHABI

TheLagoons

Business Bay Za’abeel

Garhoud

Al Qusais

Port Saeed

Rigga

Ras Al Khor

Al Marqadh

LegendsAl Barari

City of ArabiaGlobal Village

MotorCity

DubaiSport City

DubaiInvestment

Park 1

Jumeirah GolfEstates

Jumeirah GolfEstates

IMPZ

DubaiInvestment

Park 2

JumeirahVillage

JumeirahVillage South

The Meadows

Emirates Hills

The Springs

TheGardens

Jebel Ali Village

Jebel Ali Port

Jebel Ali Freezone

Jebel AliIndustrial Area

Dubai World Central Airport

DiscoveryGardens

JumeirahPark

JumeirahIslands

BarshaHeightsThe

Lakes

TheGreens

Naif

Al Raffa

SatwaJumeirah

Al WaslAl Safa

Umm Suqeim

The PalmJumeirah

Al SufouhMedia / Internet

CityJumeirah Lake

Towers

Dubai Marina

Burj Al Arab

The World

The Palm Deira

Al QuozIndustrial Area

Al Barsha

Al Quoz

Emirates Towers

DIFCBurj Khalifa

Karama

OudMetha

Al Mamzar

Port Rashid

DubaiInternational

Airport

OFFICE SECTOR

0

50

100

150

200

250

300

350

DIC

& D

MC

Bars

ha

Heig

hts

Ju

meir

ah

Lake T

ow

ers

Bu

sin

ess

Bay

Sh

eik

hZ

ayed

Rd

Do

wn

tow

nD

ub

ai

DIF

C

OFFICE RENTS AED/sq.ft. Q3 2017

AE

D/s

q.ft.

High Low

Source: MPM Properties Research

125

34

0

130

24

0

85

180

65 13

5 190

55

70 11

0

120 17

5

SHEIKH ZAYED RD.RENT = AED 85 - AED 180 /sq.ft.

DIC & DMCRENT = AED 120 - AED 175 /sq.ft.

BARSHA HEIGHTSRENT = AED 70 - AED 110 /sq.ft.AVG. SALE = AED 900 /sq.ft.

JUMEIRAH LAKES TOWERSRENT = AED 55 - AED 190 /sq.ft.AVG. SALE = AED 975 /sq.ft.

DOWNTOWN DUBAIRENT = AED 130 - AED 240 /sq.ft.AVG. SALE = AED 2,050 /sq.ft.

DIFCRENT = AED 125 - AED 340 /sq.ft.AVG. SALE = AED 1,750 /sq.ft.

BUSINESS BAYRENT = AED 65 - AED 135 /sq.ft.AVG. SALE = AED 1,050 /sq.ft.

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

18 21

0

500

1,000

1,500

2,000

2,500

BarshaHeights

JumeirahLake Towers

BusinessBay

DubaiMarina

DIFCDowntownDubai

OFFICE AVERAGE SALE PRICES Q3 2017

AE

D /

sq

.ft.

-1.0%

-7.0%

0.0%

-3.0%

-1.0%

-1.0%

0.0%

0.0%

0.0%

-3.0%

0.0%

-5.0%

QoQ YoY

2,0501,750

1,4651,050 975 900

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

19

RETAIL SECTOR

PRIME SHOPPING MALL AVERAGE RENTS – Q3 2017

An

ch

ors

Cin

em

a

Hyp

erm

ark

et

Min

i M

ajo

rs

Fla

gsh

ips

Rest

au

ran

ts

Fo

od

Co

urt

Lin

e S

ho

ps

1,2001,1001000900800700600500400300200100

0

AE

D/s

q.ft.

Source: MPM Properties Research

�� With the addition of 960,000 sq.ft. of gross leaseable area (GLA), the total retail stock of Dubai account to 35.5 million sq.ft. GLA, as of end Q3 2017. During the quarter, Marsa Al Seef by Meraas located along the creek, a new retail destination, opened its door to public.

�� Challenging economic conditions, softening sales of luxury segment, rise in supply and online shopping penetration are putting pressure on the mall operators to review existing leases, as retailers are looking to downsize / consolidate their operations. However, the impact remains marginal

across Grade “A” assets which continue to record strong occupancy and footfall figures. Secondary retail centres continue to struggle in their attempt to hold healthy occupancy and rental rates.

�� Looking at the current challenging market environment, it is important for properties under stress to review their retail mix and diversify the use of retail space to other related use in order to remain competitive in the market, while growing the revenues to desired levels.

RETAIL SUMMARY

22

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

20

Source: MPM Properties Research

0

10

20

30

50

40

24.5 27.1 27.9 28.4 28.7 30.0 32.6 34.5 34.5

1.0

35.5

0.6

36.1

3.2

39.3

2.9

42.2

3.4

DUBAI RETAIL MALL STOCK (2010 - 2020)

GL

A s

q.ft.

(Mill

ion

s)

Stock Expected - *Includes all retail malls with a GLA greater than 25,000 sq.ft.

Source: MPM Properties Research

2010 2011 2012 2013 2014 2015 2016 H12017

Q32017

Q42017

2018 2019 2020

2.62.6 0.7 0.5 0.3 1.3

1.8 0.04

DUBAI RETAIL MALLS GLA BY AREA Q3 2017

12%

16%

14%

25%

33%

DUBAI RETAIL MALLS BY SIZE Q3 2017

DUBAI RETAIL SUPPLY (PRE-2010)

NEW SUPPLY DELIVERED 2010-Q3 2017

Neighborhood - 22%

Community - 14%

Regional - 16%

Sub-Regional - 18%

Super Regional - 30%

Neighborhood - 30%

Community - 20%

Regional - 18%

Sub-Regional - 6%

Super Regional - 23%

30%

20%18%

6%

23%22%

14%

16%18%

30%

19%

10%

13%

9%10%

4%

5%

6%3%

6%3%

8% 3%

Deira - 19%

Mirdif - 10%

Business Bay - 13%

Bur Dubai - 9%

Barsha - 10%

Dubailand - 4%

Dubai Marina - 5%

Jebel Ali - 6%

Jumeirah - 3%

Al Quoz - 6%

Al Wasl - 3%

Al Warsan - 8%

Other Areas - 3%

Neighborhood - 16%

Community - 12%

Regional - 14%

Sub-Regional - 25%

Super Regional - 33%

23

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

21

HOSPITALITY SECTOR

HOTEL SUMMARY �� With the addition of 585 rooms during the

quarter, the total hotel supply of Dubai reached to 107,000 rooms and apartments. Looking at the ongoing construction activity, we expect c.800 rooms to enter during the last quarter of the year.

�� Hotel performance continues to be under pressure during the quarter, as a result of continued pricing competition in the market to retain desired occupancy levels during the summer period. Beach and key central business district properties are performing on par, while properties in other areas are being

challenged by falling ADR’s. On an average ADR’s dropped by around 10% during the quarter, as operators continue to focus on the overall revenue growth / stability.

�� Continuous growth in tourism numbers is helping the hospitality sector and creating confidence among existing and new hotel operators on the future growth of the sector. We expect the performance to improve during the last quarter, as several tourism initiatives are been lined up which include the opening of Dubai Safari, Dubai Frame and the Global Village.

DUBAI HOTEL ROOMS SUPPLY (2012 - 2019)

No

. o

f R

oo

ms

('0

00

s)

Existing Supply New Supply

Source: MPM Properties Research

418 4.7

6.8 3.3 0.6

H12017

Q32017

Q42017

2018 2019201620152012 2013 20140

30

60

90

120

150

79 80 84 9297 104 107

2.5

107

8.0

110

7.5

118

24

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

22

0

200

400

600

800

1,000

1,200

DUBAI HOTELS PERFORMANCE - 2017 YTD

ADR RevPAR

Source: MPM Properties Research

Occupancy

100.0%90.0%80.0%70.0%60.0%50.0%40.0%30.0%20.0%10.0%0%

Jan

-14

May

Sep

Oct

Jan

-15

May

Sep

Jan

-16

May

Sep

Jan

-17

May

Sep

AE

D

Occu

pan

cy

HOTEL NAME LOCATION STAR DATE NUMBER OF KEYS

Mena Plaza Al Barsha 3 star Q3 2017 92

Omega Hotel Bur Dubai 4 star Q3 2017 238

The Retreat Palm Dubai Palm Jumeirah 5 star Q3 2017 255

HOTEL NAME LOCATION STAR DATE NUMBER OF KEYS

Waldorf AstoriaDubai International

Financial Centre5 star 2017 247

Creek Rotana & Arjaan Deira 4 star 2017 280

Bulgari Resort & Residences

Jumeirah Bay Island 5 star 2017 212

Park Inn by Radisson Motor City 4 star 2017 146

Renaissance Down-town Dubai

Business Bay 5 star 2017 298

HOTELS - NEW SUPPLY Q3 2017

SAMPLE OF UPCOMING SUPPLY

25

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

23

DEFINITIONS & METHODOLOGY

RESEARCH STUDY AREA

The geographic extent of the study area covers the key districts in Dubai.

RESIDENTIAL

New residential developments are classified as delivered and thus entered into the new supply category when they are made available for occupation. This is verified via a combination of site inspections and discussion with the developer and hence our supply numbers do take into consideration the phased release of large projects.

Rental and sales trend analysis is based on transactional data derived from the MPM Properties Agency team and data sourced from developers and owners.

OFFICES

New office developments are classified as delivered and thus entered into the new supply category when they are available for tenant fit-outs.

Given the general lack of transparency in the local market rents quoted are headline rents, thus exclude any rent free period of other financial

incentives that may have been negotiated between the parties. The rents quoted are also exclusive of service charges.

RETAIL

New retail developments are classified as delivered and thus entered into the new supply category when the first units are open and trading.

Our classification of malls is based on our own assessment having regard to size and the catchment area which the mall typically penetrates.

HOSPITALITY

New hotels are classified as delivered and thus entered into the new supply category when they are opened and trading. All trading performance data is provided by DTCM.

FUTURE SUPPLY PROJECTIONS

Our future supply projections across all sectors are based on a combination of regular site inspections and discussions with developers.

BESPOKE CLIENT RESEARCH ADDING VALUE TO YOUR PROPERTY INTERESTSThe ADIB Real Estate Services team covers all sectors of the real estate market. We provide bespoke market research to our valued clients to meet their specific requirements.

We provide reports, information and presentations derived from primary market data that directly assist our clients to save or make money from real estate and shape strategies to enhance value.

DISCLAIMER:

The information contained in this report has been obtained from and is based upon sources that MPM Properties believes to be reliable, however, no warranty or representation, expressed or implied, is made to the accuracy or completeness of the information contained herein, and same is submitted subject to errors, omissions, change of price, rental or other conditions, withdrawal without notice, and to any special listing conditions imposed by our principals. MPM Properties will not be held responsible for any third-party contributions. All opinions and estimates included in this report constitute MPM Properties, as of the date of this report and are subject

to change without notice. Figures contained in this report are derived from a basket of locations highlighted in this report and therefore represent a snapshot of the Dubai market. Due care and attention has been used in the preparation of forecast information. However, actual results may vary from forecasts and any variation may be materially positive or negative. Forecasts, by their very nature, involve risk and uncertainty because they relate to future events and circumstances which are beyond MPM Properties’ control. For a full in-depth study of the market, please contact MPM Properties team.

26

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEW Q3 2017

24

A collaborative team providing our integrated services

27

BALAJI NAGARAJ MSC MRICS Head of Residential Valuation Dubai & Northern Emirates T: +971 (0)4 371 9463 M: +971 (0)55 196 2396 [email protected]

CHARLES ANDREW CHAMBERS CEO T: +971 (0)2 610 0545 M: +971 (0)56 6773521 [email protected]

ABDULLAH SAID AL KUWEITI Business Development Director T: +971 (0)2 610 1554 M: +971 (0)50 623 5854 [email protected]

MOHAMMED FAHEEM Manager Strategic Advisory & Research T: +971 (0)4 371 9471 M: +971 (0)50 384 5220 [email protected]

WAHIDA KARAMA Head of Property Operations T: +971 (02) 610 0435 M: +971 (0)50 765 7679 [email protected]

STEPHEN DUNCAN FORBES Chief Operating Officer T: +971 (0)2 510 0687 M: +971 (0)54 777 3750 [email protected]

DOMINIC BARLOW Head of Retail, Hospitality & Leisure T: +971 (0)2 510 0655 M: +971 (0)56 288 1458 [email protected]

JUBRAN AL HASHMI Head of Property Services T: +971 (0)2 610 0232 M: +971 (0)50 122 0041 [email protected]

VINEET KUMAR Director of Agency – UAE T: +971 (0)4 371 9462 M: +971 (0)50 651 6491 [email protected]

VAIBHAV SHARMA MCOM; MDBA Chief Strategy Officer T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]

ALI ABDULLAH ABDUL RAHMAN Acting Regional Head – Northern Emirates T: 971 (0)6 597 2514 M: +971 (0)50 656 2486 [email protected]

MOHAMED AL ZOUBI Head of Development Advisory BSc Civil Engineering T: +971 (0)2 610 0564 M: +971 (0)50 310 3570 [email protected]

YOUSEF AL ZAROONI Regional Head – Al Ain T: +971 (0)3 708 8636 M: +971 (0)50 600 1002 [email protected]

PAUL MAISFIELD BSC (HONS) MRICS Head of UK Real Estate T: +44 (0) 20 7590 2234 M: +44 (0)7802 404868 [email protected]

SAMPLE OF UPCOMING PROJECTS – Q3 2017RESIDENTIAL

RETAIL

HOTEL

3 REEF RESIDENCE, JVC1 EMIRATES AIRLINES BUILDINGS

2 GLITZ 1 & 2, STUDIO CITY

4 ZAHRA TOWNHOUSES, TOWNSQUARE

OFFICE

4 THE EXCHANGE DIFC

1 DUBAI MALL EXTENSION DOWNTOWN DUBAI

2 NAKHEEL MALL PALM JUMEIRAH

3 PAVILLION BADRAH RESIDENCE

4 THE POINTE PALM JUMEIRAH

1 BULGARI RESORT & RESIDENCE

2 PARK INN MOTOR CITY

3 RENAISSANCE DOWNTOWN DUBAI

4 WALDORF ASTORIA DIFC

1 HSBC HQ DOWNTOWN DUBAI

2 THE COURT BUSINESS BAY

3 THE OPUS BUSINESS BAY

SUPPLY - PHOTO GALLERY

REAL ESTATE SERVICES | DUBAI REAL ESTATE MARKET OVERVIEWQ3 2017

28 29

NEW SUPPLY – Q3 2017RESIDENTIAL

RETAIL

HOTEL

3 SAFEER TOWER 2, BUSINESS BAY

4 SERENA, MAJAN2 MODELUX 1, INTL. CITY PHASE 2

1 CENTURION, DIP

OFFICE

1 FAB OFFICE BUILDING AL JADDAF

1 FIRST AVENUE MALL MOTOR CITY

2 MARSA AL SEEF BUR DUBAI

3 THE FAIRWAYS JGE

1 MENA PLAZA AL BARSHA

2 OMEGA HOTEL BUR DUBAI

3 THE RETREAT PALM DUBAI

2 OFFICE BUILDING UM AL SHEIF

3 OFFICE TOWER UM AL SHEIF

TOABU DHABI

Jebel Ali Port

Jebel Ali FreezoneBarshaHeights

Al Mamzar

Al Qusais

1

2

3

231

3

3

4

1

2

3

3

4 1

2

2

3

3

1

2

2

1

1

4

4

2

4

1

Residential

Offices

Retail

Hotels

Q3 2016 NEW SUPPLY

Residential

Offices

Retail

Hotels

UNDER CONSTRUCTION

Q3 2017

30 31

INTEGRATED SERVICES COVERING THE FULL PROPERTY LIFECYCLE

Property Management

Investment Advisory

Project Management and ESCROW

Research & Strategic AdvisoryAgency (Sales & Leasing)

Valuation

VAIBHAV SHARMA MCOM; MDBA Chief Strategy Officer T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]

ABU DHABI HEAD OFFICE 6th Floor, Al Wahda Tower P.O Box 114686 Abu Dhabi

Tel. +971 2 610 0252Fax. +971 2 610 0514 www.mpmproperties.ae

DUBAI OFFICE Office 2301,2303,2305 - Level 123 Arenco Tower, Dubai Internet City Dubai

Tel. +971 (0)4 371 9462

AL AIN OFFICE 201-204 ADIB Ladies Branch Building Oud Touba Street Al Ain

Tel. +971 (0)3 703 9521

SHARJAH OFFICE Sarh Al Emarat Tower Buheira CornicheSharjah

Tel. +971 (0)6 597 2555

Enhancing value for individual & institutional property owners:

�� Prompt leasing & debt collection

�� Effectively market & lease vacant units

�� Physical & technical maintenance of asset

�� Maintain tenant satisfaction

�� Timely lease renewals

�� Manage risk, insurance & litigation

�� Protect your interests and enhance value

Complete Project Management services at planning & construction stage:

�� Engineering Review & Scheduling

�� Cost Estimate & Procurement

�� Project Monitoring

�� Cost Control & Accounting

�� Assist with Permits & Licensing

�� Ensure appropriate fund movement for Escrow based on Project Assessment

Aiding developers and investors to maximize value:

�� Investment Advisory & Due Diligence

�� Investment Management

�� Disposal Strategy

�� Portfolio Review & Optimization

�� Deal Structuring & Capital Sourcing

�� Investment Sale

We work with developers, commercial tenants, retailers and individuals, offering:

�� Launch Strategy

�� Project Launch Handling

�� Project Marketing Events

�� Acquisitions

�� Leasing

�� Sales

We cover all sectors, including residential, commercial, industrial, retail, and land.

Bankable studies for your real estate and business needs:

�� Highest & Best Use

�� Market & Financial Feasibility

�� Development Strategy

�� Market Research

�� Corporate Real Estate Strategy

�� Master-plan and design review

Valuation reports for:

�� Mortgage & Loan Security

�� Securing Project Funding

�� Internal Accounting

�� Mergers & Acquisitions

�� Investment appraisal

�� Litigation

�� Inheritance

We cover all asset classes. Our reports are in compliance with the International Valuation Standards (IVS) and the RICS Professional Valuation Standards.

CHARLES ANDREW CHAMBERS CEO T: +971 (0)2 610 0545 M: +971 (0)56 6773521 [email protected]