Embed Size (px)

Citation preview

'ED 276 956

TITLE

INSTITUTION

REPORT NOPUB DATENOTEAVAILABLE FROM

PUB TYPE

DOCUMENT RESUME

CG 019 573

Medigap Insurance: Law Has Increased Protectionagainst Substandard and Overpriced P6Iidies. Reportto the Subcommittee on Health, Committee on Ways andMeans, House of Representatives.General Accounting Office, Washington, D.C. Div. ofHuman Resources.GAO/HRD-87-87 Oct 8648p.U.S. General Accounting Office, P.O. Box 6015,Gaithersburg, Maryland 20877 (1-5 copies, free; 6-99copies, $2.00/copy; 100 or more, 25% discount).Reports - Descriptive (141)

EDRS PRICE MFOI/PCO2 Plus Postage.DESCRIPTORS *Compliance (Legal); *Federal LegisIaticiii; *Health

Insurance; *Older Adults; State Programs; *StateStandardsMedicare; *Medigap InsuranceIDENTIFIERS

ABSTRACTThis report reviews certain aspectO of the

effectiveness of'the Public Law 96-265 provisions (Section 1882_ofthe Social Security Act) designed to protect the elderly againstsubstandard and overpriced health insurance policies supplementingMedicare. This document on Medigap policies indludes an executivesummary and five chapters. Chapter 1 looks at the Medicare program;the Baucus Amendment; state regulation of insurance industry; theMedigap market; and the objectives, scope, and methodology of thereport. Chapter 2 examines state regulatory programs, almost all Ofwhich met minimum federal standards. Chapter 3 discusses the 06liciesreviewed by the_General Accounting Office, Which generally metstandards. Chapter 4 explains loss ratio and presents_findings thatloss ratio experience of Medigap policies is mixed and generally notused by states to evaluate premiums. Chapter 5 examines federal andstate efforts to curb sales abuse through education and penalties.Because the report found that Section 1882, when combined with stateefforts, appeared to be meeting its objectives of protecting theelderly against substandard Medigap policies and providing theM Withinformation on how to select Medigap policies, no recOmmenditions forchange are included. Four tables and one figure are indluded;Company-Wide Loss Ratio Experience for Medicare SupplementalInsurance is appended. (NB)

************************************************************************ Reproductions supplied by EDRS are the best that can be made ** from the original document. *

***********************************************************************

Unittd StatesGeneral Accounting OfficeWashington, D.C. 20548

Human Resources Division

B-223317

Oetober 17, 1986

The Honorable Fortney H. (Pete) StarkChairman, Subcommittee on HealthCommittee on Ways and MeansHouse of Representatives

The Honorable WilliS D GradiSon, Jr.Ranking Minority MemberSubcommittee on HealthCommittee on Ways and MeansHouse of Representatives

This report is in response to your February 25,1986, request to review certainaspects of the efftctiveness of the Public Law 96-265 provisions designed to protectthe elderly against substandard and overpriced health insurance p-oliciessupplementing Medicare. The law set minimum Standards for policies that insurersmust meet to market them as Medicare supplementals and creaWd a voluntarycertification program for such imlicies.

As requested by your office, we did not obtain comments on this reriort. UnteSS youpublicly releaw its contents earlier, we plan no further distribution of this report for30 days. At that time, we will send copies to Senator Max Baucus, the Secretary ofHealth and Human Services, and other interested parties and make copiei availableto others on request.

Richard L. FogelAssistant Comptroller General

Medicare pays much of the health care costs of the elderly, but they areresponsible for deductibles and coinsurance, which sometimes representlarge out-of-packet coSts. Almost from the beginning of Medicare, pri-vate insurers have offered policies- called Medigap goliciegthat sup-plement Medicare benefits.

In 1980 the Congress amended the Social Security Act to provide stan-dards for policies that are marketed as Medigap insurance. In FebruvAry1986, the Chairman and Ranking Minority Member, Subcommittee onHealth, House Committee on Ways and Means, requested GAO to deter;mine if the law's objectives were being achieved. These oWectivog are toprotect the elderly from golicieS that do not provide a irtinimum level ofbenefits at a reasonable pfice and from deceptive advertising of policiesand to give the elderly information to enable them to select amongpolicies.

Section 1882 of the Social Security Act, added by Public Law 96-265,June 9, 1980, established standar& for Medigap policies requiring thatthey provide at least a minimum level of benefitt coverage and incluci3certain provisions. The law also wt minimum expected levels of benefitpayoutscalled loss ratios. Medigap policies sold to individuals musthave an anticipated return to policyholders as benefits of at least 60percent of the premiumscollected, and this minimum loss ratio was setat 75 percent for policies told to groups. Section 1882 also establishedfederal criminal penalties for engaging in abusive sales and marketingpractices for Medigap golicieg.

The statute incorporated by reference the Medigap standards containedin a model regulatory program developed by the National Association ofInsurance Commissioners and set forth two procedures for determiningwhether insurance policies meet the federal standardt. First, if a statehas adopted laws and/or regulations that are at least as stringent as theassociation's model and the federal loss ratio requirement, policies regu-lated by the state are deemed to meet the federal requirements.

cond, the statute established a voluntary certification program underwhich insurance companies could market policies as Medigap insurancein stateS that do not have laws and regulations equivalent to the associa-tion's model. Insurers can submit policies and supporting documentationto the Secretary of Health and Human Services (inis). If the Secretary

Pawe 2 4GAO/BED-874 Medigitp lnaurance

determines that a submitted policy meets federal requirements, it is cer=tilled and can_bt marketed aS Medigak). Only twn policies have been sub-mitted to the Secretary, and neither had been certified as of September1986.

To evaluate if policies being marketed as Medigap insurance meet therequirements of section 1882, GAO visited nine state& and the District ofColumbia that had laws and/or regulations at least as stringent as theassociation's mixlel and two states that did not. GAO review6d 142 pOlides for compliancY with the federal standards and obtained loss ratiodatafor 394 individual and 4 _group golicies &old by 92 commercial firmsand 13 Blue Cross/Blue Shield plan& Premiums cbllected nationwide onthese 394 individual polides totaled over $2.1 billion in 1984. The totalestimated Medigap market in that year %Vat about $5 billion.

Other types of health insur ance &old to the elderlysuch as hospitalindemnity, dread disease, and nursing home insuranceare not techni-cally Medigap policies and do not fall under section 1882. They were notcovered by GAO's review.

Results in Brief ction 1882 has encouraged state adoption of Medigap insurance regu-lato 7 programs at least as stringent as the association's model, and onlyfour states had not done so as of September 1986. ThiS, in turn, hasresulted in more uniform regulation of Medigap insurance and increasedprotection for the elderly against substandard and overpriced policieS

Medigap policies sold by commercial insurers that had more than $50million in premiums and Blue Cro&S/Blue Shield plans generally met theloss ratio requirements of section 1882. However, over 60 percent of thecommercial insurance Nlicies with premiums under $50 million in 1984did not meet those requirements. The loss ratio for all individual polidesstudied meant that about 60 cents of every premium dollar %Vat rew.uniedas btnefits or added to reserves.

Many Medigap policies covered more than the minimum required bene-fit& Differences in benefit coverage and loss ratiOS among policies illus-trate the importance of comparison shopping. ro assist the elderly, thefederal and state governments have made available information usefulin shopping for Medigap insurance.

Abuses still occur in the sale of Medigap policies. But many states haveattempted to prevent abu&e through such actiohs as itiohitotihg Sales

Page 3 5 GAO/M1D-87-8 Medlgaii Iniarance

and advertising practices and revokingor susrending insurance agentlicenses arid issuing cease and desist orders to itsurers.

When section 1882 was enacted, 9 states had laws and regulations per-taining ariecifically to Medigap insurance; currently, 46 States, PuertoRico, and the District of Columbia have laws and regulations that meetthe section's minimum requirement& Thus, the states are primarilyresponsible for awning that the federal standards for marketingMedigap insurance are met (See p. 14.)

GAO compared a sample of 142 policies with the association'S minimumstandard& In GAO'S opinion, 49 of them did not meet all of the standardsfor coverage. Forty of those policies fell short on only one standard. Themoat frequent shortcoming concerned the Medicare blood deductible-28 policies failed that standard, because they would not pay the full costof the first three pints of blood, which Medicare dots not cover. Theidentified shortcomings were relatively minor problem. (See pp. 21-24.)

On the other hand, 137 of the 142 golicies exceeded the mntum start-dards in some resptct venty-eight of them would cover the $492part A dtductible for inpatient services, and 63 would pay the $75annual part B deductible for physician and medical supplier services.Sixty=seven policies would cover the part A coinsurance for the 21stthrough 100th day of necessary skilled nursingcare. (Medicare pays thefull cost for the first 20 days.) (Ste pp. 22-23.)

The loss ratios of most policies were below the section 1882 targets;however, the loss ratios of the policies of the BlueCross/Blue Shieldplans and the Prudential Life Insurance Company were generally abovethe targets. (See p. 28.) Tb ese are the policies most commonly pur-chased. The Blue Cross/Blue Shield individual policies GAO reviewed had1984 premium- of $77616 million arid an aggregate loss ratio of 81.1 per-cent; the commercial individual policies includtd in GAO'S analysis hadnationwide 1984 premiums of $12 billion, and Prudential (with a 1984loSS ratio of 77.9 percent) had almost 25percent of that butineSs. (SeeaPP. I.)

For the 376 individual policies of commercial inturers studied, the lossratio was 60.2 r*rcent for 1984. In other words, $770 million in benefitswere returned for the $1.3 billion in premiums paid. That, for every

Page 4 GAO/M1D-874i Meillga,0 Insurance

$1 in premiums, 60 cents was returned as claims payments or used toincrease reserves, and 40 cents represented administrative and mar-keting costs and profits. The same figures for the Blue Cross/Blue Shieldplans studied are 81 cents in benefita to 19 cents in costs and profits.

The loss ratio provision of section 1882 is a target to strive for, not arequirement //or actual performance. Thus, according to mis's interpreta-tion of the law (which GAO fmds reasonable), states are not required tomonitor loss ratio experiehce.

Monitoring of Sales andAdvertising

Penalties for Medigap sales abuse generally have been the prerogativeof the states because they are primarily responsible for regulating theinsurance industry. All states GAO visited have a formal complaintsystem, within either the state insurance department or the Statedepartment of elderly affairs. State actions to stop abuses have includedfmes, cease and desist orders, and the revocation andsuspension ofagent li Ames. All states GAO visited also monitor the advertising prac-tices of insurance companies. Generally, the states rely on the public toalert state officials to problems, through the established complaintsystem. (See p. 34.)

Information Activities HHS and the aSSociation jointly published the Guide to Health Insurancefor People With Medicare, which contains much helpful advice foranyone shopping for Medigap insurance. Florida and Washington havepublished a shopper's guide for Medigap insilrance, and a Maryland offi-cial told GAO the state was developing such a guide. These guides givethe elderly valuable information to help them obtain Medigap insurance.(See pp. 32-34.)

ecommendations Section 1882, when combined with state efforts, appears to be rneeits objectives of protecting the elderly against substandard Medigap rol=icies and providing them with information on how to select Medigap pol-icies. Thus, GAO is making no recommendations.

Agency Comments GAO sought the views of federal and state agency officials during itSwork. Their views are incorporated in the report where appropriate.

Page 5 GAG/MD-87-8 Mecligap Insurance

1111111

Ekettitive Summary

Chapter 1Introduction

Chapter 2Almost All StateRegulatory ProgyanisMeet Minirnum FederalStandards111MINW

Chapter 3Policies ReViewedGenerally MetStandards

Chapter 4Loss Ratio Experienceof Medigap PoliciesMixed, and GetierallyNot Used by States toEvaluate Premiums

8The Medicare Program 8The Baucus Amendment 9State Regulation of Insurance Industry 10The Medigap Market 11Objectives, Scop, and Methodoi ..)gy 12

14certified Regul-tory Programs Meet Minimum Standards 14Some State Regulations Are More Restrictive Than 15

Minimum StandardsStates Not Certified by the Panel 15Conclusions 16

18The Minimum Standards 18Policies Reviewed by GAO 21Conclusions 23

24Explanation of Loss Ratios 24Loss Ratio Experience Generally Not Evaluated by States 25States to Receive Data That Can Be Used to Monitm Loss 29

Ratio ExperienceConclusions 30

Chapter 5State and Federal.Agencies Have Med toCurb Sales AbuseThrough Educationand Penalties

Federal EffortSMany States Support Efforts to Aid and Educate the

Elderly With Medigap Insurance DecisionsInveStigation and SanctionsConclusions

323233

3436

Appendix Appendix I: Company-Wide Logs Ratio Experience forMedicare Supplemental Insurance

38

Tables

Figure1111111N

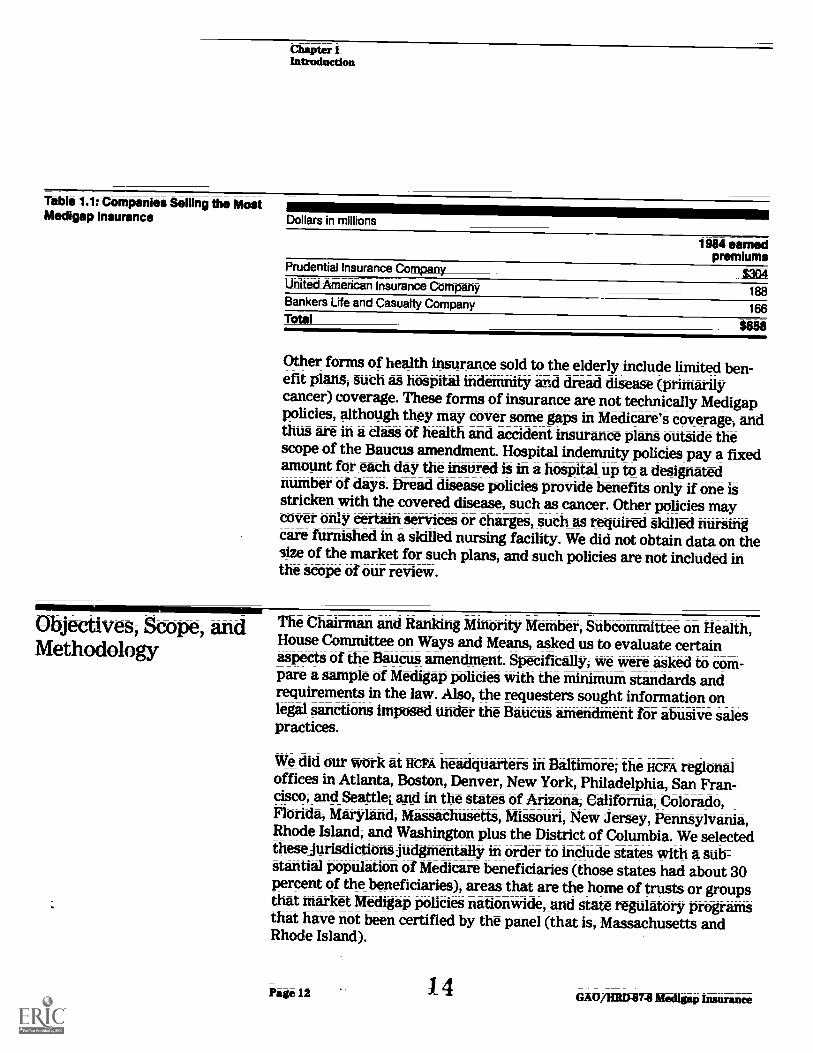

Table 1.1: Companies Selling the Most Medigap InsuranceTable 3.1: Schedule of Benefit Coverage Provided by

Medicare and Requimd by Medigap MinimumRequirements

Table 3.2: Medigap Policies That Did Not Meet All NAICStandards

Table 4.1: Loss Ratio Experience of Selected MedigapInsurance Policies

1220

22

28

Figure 4.1: Cumulative Loss Ratios for Medigap Policiesby Amount of 1984 Earned Premiums

29

Abbreviations

GAO

HCFA

misNAIC

Page 7

General Accounting OfficeHealth Care Financing AdministrationDepartment of Health and Human ServicesNational Association of Insurance Cot missioners

9 GAO/HRD.87-8 Media* huguranft

On February 25, 1986; the Chairman and Ranking Minority Member,Subcommittee on Health, House Committee on Ways and Means,requested that we review compliance with federal standar& regardingMedicare supplemental insurance policies sold by the private sector tothe elderly. These policies often referred to as Medigap insuranceare designed primarily to pay deductible and/or coinsurance amountsfor hospital, medical, and surgical expenses covered by Medicare. Therequesters asked us to compare policies with the federal minimum stan-dards for Medigap insurance and to develop information on legal sanc-tions imosed for abuses in the sale of such insurance.

The Medicare Progr Wdicare is a federal program that pays much of the health care costsfor eligible personsalmost all persons 65 and older and some disabledpersons. Mdicare was established by title XVIII of the Social &curityAct and became effective on July 1, 1966. The program provides twobasic forms of prowction:

Part A Hospital-Insurance, is financtd primatily by Social Security pay-roll taxes. It covers inpatient hospital services, posthospital care inskilled nursing facilities, and care provided in patients' homes and byhospices. Part A benefitS are paid on the basis of benefit periods. A ben=efit period begins when the beneficiary receives Medicare-covered ser-vices in a hospital and ends when he or she has been out of a hospital orskillal nursing facility for 60 consecutive days. For any benefit period,part A pays for all covered services for the firSt 60 days of inpatienthospital care except for the inpatient deductible ($492 in 1986) and thefirSt three pints of blood used. For the next 30 days, the beneficiary isresponsible for coinsurance equal to one qukrter of the deductibleamount per day ($123 per day in 1986). Every person enrolled in part Aalso has a 60-day, nonrenewable, lifetime reterve for inpatient hospitalcare that can I* drawn from if more than 90 days are needed hi a btri;efit period. When reserve days are used, the btneficiary is reSponsiblefor coinsurance equal to one-half of the deductible amount per day($246 ptr day in 1986). For medicallynecessary inpatient care in askilled nursing facility, after a hospital hipatient stay of at least 3 daysand within 30 days of discharge from the hospital, part kpays for allcovered services for the first 20 days in alYenefit ptriod. For the next 80days, the beneficiary is responsible for one-eighth of the hospitaldaluctible each day ($61.50 per day hi 1986), and part A pays theremainder. Part A pays the entire cost of all mWically necessary homehealth visits, and it pays for hospice services forbeneficiaries who havea terminal illness and elect hospice care.

Page 8 GAWIMI)87-8 Medigap Insurance

Chapter 1_Iiitraduction

Part B, Supplementary-Medical-Maumee, is a voluntary programfmanced by enrollee premiums and federal contributions. Enrollee pre-miums currently account for 25 percent of total part B costs. Part Bcovers physician services and many other health services, such as labo-ratory and physical therapy services. For each calendar year, the benezficiary is responsible for the first $75 of approved charges (the part Bdeductible), after which the program pays 80 percent of approvedcharges for covered services during the rest of the year. The beneficiaryis responsible for 20 percent of the approved charges (the part Bcoinsurance), plus any charges in excess of the Medicare-approvedcharge on claims for which the physician or supplier does not acceptassigiunew)

The BaucusAmendment

Public Law 96-265, enacted in 1980; added section 1882 to the &icialSecurity Act. Thisprovision is commonly referred to as the Baucusamendment after Senator Max Baucus, the amendment's chief wonsorin the Senate. This law was a response to marketing and advertisingabuses in the sale of Medigap insurance to the elderly. Many abuseswere detailed in hearings before the House Select Committee on Aging in1978 and summarized in published hearings and a committee staffstudy.2

The Baucus amendment defines minimum standards for policies thatmust be met before companies can market them as Medigap policies. Thestandards are_contained in a model regulation approved by theNationalAsaociation of Insurance Commissioners (NAic) on June 6, 1979, andincorporated in section 1882 by reference. These standards (1) requiresuch policies to cover Medicare's coinsurance amounts within certanilimits; (2) require that purchasers of a policy have a "free look" period,during which they may return an unwanted policy for cancellation andreceive a full refund of any premium paid; (3) standardize many of theterms used hi policies; (4) limit the peri6d for which coverage may bedenied for preeidating conditions; and (5) require cancellation and termiznation clauses to be prominently displayed. The standar& for Medigappolicies apply only to those sold to persons who qualify for Medicare by

1When phymc ans and suppliers accept assigrunent they agree to accept Medicare's determination ofa remoryable charge as payment in full and not to bill beneficiaries for charges in excess of the deter-Mined reasonable charge.

2Abuses in the We of-140.81danStiraneetathe-Elderly, hearingstefore the_House Select Committee onMit& Committee Publication 95-1654 _November 28; 1978, and Abuses in the &aleof liedlthliteianeeto the Elderlyin Supplertuaitation of Medicare A National-Seandat a staff study of the House SelectComitiittee on Aghig, Committee Publicadon Number 96-160, November 28; 197&

Page 9 1 1 GAO/HM.874 Medigrap Insurance

Chapter 1Introduction

State Regulation ofInsurance Industry

reason of age. In addition, the Baucus amendment established loss ratiotargets for Medigap policies that set a goal for the percentage of insur-ance premiums to be returned to policyholders in the form of benefits.Medigap policies must be expected to pay benefits at least equal to 60p-ercent of the earned premiums for individual policies and 75 percentfor group policies.

Because insurance regulation has historically been a state responsibility,the Baucus amendment relies primarily on the states to enforce theMedigap standards. Federal responsibilities involve determiningwhether state laws and regulations are equivalent to the Baucus amend-ment standards and certifying policies on a voluntary basis in statesthat do not have equivalent laws and regulations. "t r the Mcarran-Ferguson Act (Public Law 79-15), enacted in 194b, : e Congressexpressed its desire that the states continue to have primary responsi-bility for regulating the insurance industry. When the Baucus amend-ment was enacted, nine states had rules and regulations specificallygoverning Medigap policies.

The amendment established the Supplemental Health Insurance Panel,consisting of the Secretary of Health and Human Services (rris) and fourstate insurance commissioners or superintendents of insuranceappointed by the President. The panel is responsible for reviewing eachstate's insurance regulatory program and certifying those that meet theminimum standards contained in the Baucus amendment. ht states thatdo not obtain panel certification, insurers may submit their policies tothe Secretary of mis for approval. mis's Health Care Financing Adminis-tration (HcFA), which administers Medicare and supports the panel, hasreported that only two insurers had submitted policies to the Secretaryand neither had been approvtd as of September 1986.

Finally, the Baucus amendment contains federal sanctions, consisting offmes and/or imprisonment, for (1) furnishing false information to obtainthe Secretary's certification, (2) posing as a federal agent to sell Medigappolicies, (3) knowingly selling policies that duplicate coverage the indi-vidual already has, and (4) selling supplemental policies by mail instates that have not approved, or are deemed not to have approved,their sale.

Regulating the insurance industry has traditionally been a state func-tion, accomplished through the office of the state insurance commis-sioners. The state commissioners are linked through Nix for the

Chapter 1Intrtvduction

purposes of discussing common problems, standardizing the annualrepirting of financial information by insurance companies, and devel-oping model legislative acts for adoption by the individual states.

State regulatory processes and procedures generally include

prior approval of policies after a review of such features as policy read-ability and standardization of policy terms,premium rate control, andmonitoring of unfair or deceptive acts through unfair trade practiceregulations.

Health and accident insurance, of which Medigap is a part, is regulatedthrough the same mechanisms mentioned above, except that premiumrates are not directly regulated. Most states require premium rates forhealth and accident policies to be filed with the state and will disap-prove any policy whose benefits provided are not considered reasonablein relation to the premiums charged. The requirement for a reasonablerelationship between premiums and benefits paid (claims incurred) ledNAIC to develop loss ratio benchmarks. A loss ratio is stated as a per-centage. For example, a policy earning $1 million on premiums andincurring claims of $600,000 has a loss ratio of 60 percent.

The major sources of Medigap insurance are Blue Cross/Blue Shieldplans and commercial insurance companies. The Blue Cross and BlueShield Association told us that, nationwide, the premiums for its Medi-care complementary insurance sold to individuals totaled about $3.7 bil-lion3 in 1984. Earned premiums of commercial Medigap insurance for1984 totaled over $1.2 billion. These policies were sold by over 90 dif-ferent companies, but the following three companies accounted for over50 percent of the earned premiums:

3Th1s figure includes Medirap policies plus some other policies sold to complement Medicare. Theassociation could notprovide data solely for Medigappolicies, but an association representative toldus most of these premiums would be for plans that meet or exceed Baucus amendment standards.

13 GAO/HRD-8743 Med Ito Insurance

Table 1.1: Companies Selling the MostMedigap insurance

Objectives, ScoMethodology

Dollars in millions

1984 earnedpremiums

Prudential Insurance Company

UnittA_American Insurance ComrianyBankers Life and Casuelty CompanyTOtal

166

8858

Other forms of health insurance sold to the elderly include limited ben-efit plans, such as hoapital indemnity &Yid dread disease (primarilycancer) &overage. These forms of insurance are not technically Medigappolicies, although they may cover some gaps in Medicare's coverage, andthus are in a class of health and accident insurance plans outaide thescope of the Baucus amendment Rospital indemnity policies pay a fixedamount for each day the insured is in a hospital up to a designatednumber of days. Dread disease golicies provide benefits only if one isstricken with the covered digeaSe, such as cancer. Other policies maycover only certain sefvices or charges, such as required skilled nursingcare furnished in a skilled nursing facility. We did not obtain data on thesize of the market for such plans, and such policies are not included inthe scope of our review.

The Chairman and Ranking Minority Member, Subcommittee on Health,House Committee on Ways and Means, asked us to evaluate certainaspects of the Baucus amendment. Spetifically, we were asked to com-pare a sample of Medigap pblicies with the minimum standards andrequirements hi the law. Also, the requesters sought information onlegal sanctions imgcrxed under the Baucus amendment for abusive salespractices.

We did our work at HCPA headquarters in Baltimore; the HCFA regionaloffices in Atlanta, Boston, Denver, New York, Philadelphia, San Fran-cisco, and Seattle; and in the states of Arizona, California, Colorado,Florida, Maryland, Massachusetts, Missouri, New Jersey, Pennsylvania,Rhode Island, and Washington plus the Dittrict of Columbia. We selectedthese jurisdictionS judgmentally in order to include states with a sub=stantial population of Medicare beneficiaries (those states had about 30percent of the treneficiaries), areat that are the home of trusts or groupsthat market Medigap policies nationwide, and state regulatory programsthat have not been certified by the panel (that is, Massachusetts andRhode Island).

Page 12 14GAO/EMIR:174 Med !gap Insurance

In the states visited, we did our work at the state insurance department,where we collected data maintained on the premiums collected andclaims paid for all policies that we could identify as Medigap insuranceand for which data were available. A total of 398 polkies were coveredby the dat.% which we used to compute nationwide loss ratios for thosepolicies. In addition, hi all states except Missouri, we Selected all BlueCross/Blue Shield Medigap policies, the five commercial Medigap poli-cies with the highest value of earned premiums in 1984 (the latest yearfor which data were available), and a Sample of all other Medigap poli-cies for detailed review of the coverage offered. We reviewed the&elected policies (a total of 142) to determine jf they met the minimumstandards. In Missouri and the District of Columbia, our review focusedon policies sold nationwide through trusts or groups. (ee app. I for alist of all insurance companies for which data are included in thisreport.)

We contacted state insurance departments, offices of aging, consumeraffairs offices, and/or offices of attorneys general as appropriate toobtain data on complaints and prosecutions of cases of marketing abuseor illegal sales practices.

At HCFA headquarters and the regional offices, we obtained data on com-plaints about the marketing of Medigap policies. At headquarterS, wealSo reviewed LIM'S files on the operations of the Supplemental HealthInsurance Panel in certifying states and HCFA'S a.ctions to verify thatstate regulatory programs continue to meet the Baucus amendmentstandards.

Our fieldwork was performed from March through July 1986 in accor-dance with generally accepted government auditing standards. ASrequested by the Subcommittee office, we did not obtain written com-ments from the federal and state agencies involved. However the viewsof responsible federal and state officialS were Sought during our workand are incorporated in the report where appropriate.

Page 13 15 GAO/IIRD17-8 Mangey Insurance

Almost All State Regulatory Programs M

The Supplemental Health Lnsturance Panel, established by the Baucusamendment, reviewed state regulatou programs and then certifid 46states, the District of Columbia, and Puerto Rico as having Medigap reg-ulatory programs that met minimum federal standards. The Baucusamendment encouraged states to adopt the minimum standards. As of&ptemb-er 1986, about N percent of the nation's population lived injurisdictions with replatory programs that meet Baucus amendmentstandards, up from 35 percent in states with Medigap regulatory pro-grams when the law was enaxted in 1980.

Certified RegulatoryPrograms MeetMinimum Standards

The Supplemental Health Insurance Panel is responsible for reviewingstate regulatory programs and certifying those that incorporate stan-dards equal to or more stringent than those contained in the NAIC modelregulation and meet the loss ratio requirementS of the Baucus amend-ment. In a university study in 1979, before the Baucus amendment wasenacted, only nine states were identified as having minimum standardsgoverning Wdigap policies.

The panel was assisted in its work by HCFA staff, who reviewed the lawsand regulations of the states and compared them with the NAIC model.The staff prepared recommendations of approval or nonapproval forthe panel's consideration. The panel held its first meeting in December1980.

The panel had approved 10 state regulatory progxams by November1981, but other states had to enact legislation or adopt regulations tobring their program into compliance with the minimum standards. ByJuly 1982, the panel had certified 30 additional states. Five more statesand the District of Columbia and Puerto Rico were certified by January1984. Finally, New Jersey was certified in 1985. Thus, as of Septemlxr1986, the panel had certified 46 states plus the District of Columbia andPuerto Rico.

In support of the panel, HCFA has establisheii a procedure to obtainammal updates from the states on their continued compliance with theBaucus amendment. HCFA does this through annual recertification lettersto the states. In those letters, a state official responsible for adminis-tering the state's regulatory program is asked to sign an attestation thatno substantive changes were made in the state's regulatory programthat would cause it to lose its certification.

Page 14 16 GAO/HRD-874 Mftgap Insurance

ChcpWr 2Almost All State Rego lately A ()grams MeetMinimum Federal Standards

We reviewed HCFA'S annual recertification fileS. In the 1984 file, wecould not locate recertification letters from Alaska and Utah, but thosestates did submit such letters in 1985. In the 1985 file, we could notlocate recertification letters from Temiessee, Montana, Washington, andthe District of Columbia; however, each of them attested in 1986 thatthere were no changes to their regulatory programs. By August 1986,WM had received recertification letters from all but five states. A HCFA

representative told us that follow-up letters had been Sent to those fivestates, requesting a reply by September 30, 1986.

Some State RegulationsAre More RestrictiveThan MinimumStandards

Some of the certified states we visited have adopted more restrictiverequirements than those in the Baucus amendment. For eXample:

In Pentisylvania; insurers must offer coverage of the part A deductible(the NAIC model does nOt require CoVerage of thiS deductible); and theMaximum part B deductible under Medigap policies is $75 p-er year (themodel allows for a maximum part B dtductible of $200).In Mandaild, all Medigap policies must cover the part A deductible.Also; insurers must offer coverage of the part B deductible, either in theRoney or through an optional rider. In 1986; Maryland amended itsstatute to require Medigap policies to pay up to $100 for an annual IOWdose mammograph for the detection Of Occult breast dancer,Washington and New Jersey require anticipated loss ratios of 65 percentfor individual policies instead of the 60 percent required by the Baticusamendment.Both Colorado and Washington require a 30-day "free look" period fOrall policies during which the policyhOlder Can cancel and obtain a returnOf premium. The NficIC model sets a 10-day period for policies solddirectly by agents.

States Not Certified bythe Panel

Massachusetts, New York, Rhode Island, and Wyoming have notreceived panel certification. To obtain information on regulatory pro-grams of these noncertified states, we reviewed documents availablethrough HCFA on why the states were not certified, and we visited Mu=sachusetts and Rhode Island. According to theae documents, the regula-tions of the noncertified states did not include many of the minimumstandards, but some contained features that exceed the NAIC model insome respects.

Massachusetts' regulatory program did not meet three of the Baucusamendment standards. Massaxhusetts (1) does not require insurers to

17GAO/HRD-874 Medigap Insurance

pay the blood deductible;1 (2) does not require coverage for an addi-tional 365 days of 90 percent of part A expenses after the beneficiary'sMedicare coverage is exhausted (MassachuSetts requires payment of100 iyercent of part A expenses for a total of 365 days); and (3) allowsthe insurer to exclude coverage for some part B services, Such asdurable medical equipment, doctor's charges outside of a hospital, med-ical supplies, ambulance services, and dental services outside of ahospital.

In other respects, Massachusetts requires coverage at leaSt equal to thatrequired under the NAIC model regulation, and in some areas the state'sstandar& are higher than the model. For example, Massachusettsrequires policies to meet an anticipated loss ratio of 65 percent and tocover the part B coinsurance without a dollar limit, whereas the modelallows a $5,000 annual limit.

New York State regulations did not meet three of the minimum stan-dards. Specifically, New York's regulationt did not (1) require insurersto supplement part B expenses when the beneficiary is not hospitalized,(2) require delivery of a buyer's guide, and (3) require a receipt for theoutline of coverage. N:Av York regulations require policies sold to indi-viduals over age 65 to meet an anticipated loss ratio of 65 percent,which is more restrictive than the Baucut amendment target.

Wyoming failed to meet two minimuzn standards. The State'S regulations(1) allowed the sale of part A only and part B only supplemental policiesand (2) allowed reasonable charges to be based on the insurer's determi-nation rather than on Medicare's reasonable charge determination.

Rhode Island did not meet the Baucns amendment standards in severalrespects. The state's regulations did not meet the minimum standardsconcerning (1) payment of the Medicare part A coinsurance, (2) thelimits on coverage of preexisting conditions, and (3) defirdtions of manystandard terms. Also, the Rhode Island regulations did not cover grouppolicies.

Conclusioris Since the enactment of the BaucuS amendment, all but four states haveadopted the NAIC model regulation for Medigap golicies. We believetheamendment was effective in encouraging the States to bring a degree of

'Under Medicare; the beneficiary is_responsible for the cost of the first three oat of bltkid -dr mayarrange for the replatement of the first three pints.

Page 16 GAWIERD-87-6 Mecligap Insurance

18

CWtetAlmost All State Regulate*. Programs MeetMinimum Federal Standards

standardization to their regulatory progranis for NWdigap inSuranc-e.Nevertheless, state regulatory programs for these policies are not iden-tical. Several states have standards that exceed the minimum federalrequirements, and as discussed in the nekt chapter, Medigap policiesprovide varying degrees of coverage.

Page 19

19

A.

GAO/HRD47-8 Medlgap Insurance

This chapter discuSSes compliance with the Balms amendment stan-dards eiccept for those related to loss ratios, which are discussed inchapter 4. We reviewed a sample of 142 Medicare supplemental policiesand found that f.n nearly all cases their met the minimum standards pro=vided for in the Baucus amendment.

A number of Medigap policies also provide coverage beyond what isrequired. For example, 78 of the 142 policies providedcoverage forMedicare's $492 hoSpital deductible, and 63 of the 142 covered the $75part B deductible.

Few, if any, of the policies provide coverage that could I* termed cata-strophic, and coverage is usually limited to the same services that Medi-care covers.

The MinimumStandaits

For a policy to be marketed as a Medigap policy, the NAIC model regula-tion requires the following:

Conditions for renewability must be stated on the first page of therfgolicT.If a policy is sold as "noncancellable" or "guaranteed renewable," itmust provide coverage for the insured'S sOuse after coverage of theinsured ends if premiums are paid.A policy that is terminated must continue coverage for illnesses or acci-dents that occurred while the policy was in force, except that such cov-erage may be predicated on the continuous total disability of theinsured, limited to the duration of a stated benefit period, or limited tothe payment of maximum benefits.The purchaser must lm allowed a "free look" periOd during which thepurchaser may return the policy and get a full refund ofany rremiumpaid; this period must be at least 10 days for_golicies sold throughneents and at least 30 days for policies Sold through the mail.The coverage in the policy must automatically change as Medicare'sdeductibles and coinsurance requirements change.The policy may not define preekisting conditions more restrictively thanas a condition that was diagnosed or treated within 6 months before theeffective date of the po:icy, and benefitS -nay be denied for preexistingconditions for no more than 6 months from the effective date of thepolicy.The policy must cover treatment for accidents and illnesses equally.

Page 18 20 GA0/1111.1)-87-8 Medlgap Insurance

Ch-opUer 3Policies Reviewed enerally Met Standards

o Terms used in the golicy,such as physician, hospital, sickness, and acci-dent, may be defmed within vertain limits, and Medicare must bedefmed in the policy.The policy must cover all of the Medicare part A inpatient coinsurancefor the 61st through 90th day in the hospital, and the 91st through150th day while the beneficiary uses his or her lifetiMe reserve days,plus 90 percent of covefed hospital inpatient expenses for a lifetimemaximum of up to 365 days after the insured has exhausted his or herMedicare benefits.The policy must cover the Medicare part B coinsurance, but this may besubject to a deductible of $200 and a maximum benefit of $5,000 peryear.The policy must cover the parts Aand B blood deductible&The policy must have an outline of coverage, which shows what Medi-care covers; what the beneficiary is resp:insible for, and what the sup-plemental policy covers.

In addition, the NAIC standards include a requirement that insurers givebeneficiaries a buyer's guide. This guide must be given to the benefi-ciary at the time he or she applies for insurance or, in the case of poli-cies sold through the mail, at the time the policy is deEvered to thebeneficiary. HCFA and NAIC have jointly developed a guide that describesMedicare, Medigap, and other health insurance plans.

Table 3.1 compares hospital and physician benefit coverage for pay-ments by Medicare, the amount the beneficiary is responsible for, andthe minimum coverage required of Medigap insurance.

21GAO/HRD-87-8 Medigsp Insurance

Chspter 3Policies IV:viewed Geweitilly

Tab 140.1: Schedule of Serofit Mverage ForcitikWd*AladicaranndRequired by Med %pp MinimumRequirementsIMadkJaiy Minimum requirenwsitBenefit WHIkare pays* responsible foe for Meagan Insurance_

Medicare (Part A): Hospital insuranceCovered Benefit PedalH jtalIzithsemiprivate room andbeard general nursingand_miscellaneoushospital services andsupplies

First 60 days

61st to 90th day

91tt to 150th day

Beyond 150 days

All but the $492deductible__ _

All but the $123 a daycoinsuranceAll but the $246 a daycoinsuranceNothing

$492

$123 a day

$246 a day

All charges

None

$123 a day

$246 a day

90 percent of coveredcharges up to 365 days

SihospitatikHiednursing facility carein a.facility appreVed byMedicare it the beneficiaryhas been in a hospital forat least 3 days and entersthe facility within 30 daysafter hospital discharge

First 20 days

Additional 80 days

Beyond 100 days

100 percent of costs

All but $61.50 a day

Nothing

Nothing

$61.50 a day

All charges

Home health care Unlimited visits asmedically necessary

Full cost Nothing

Hospice date Two gaiday periods and All but limited coinsurance Limited ceSt Sharing_forone 30-day period for Outpatient drugs and outpatient drugs and

inpatient respite care inpatient respite careBiedd Blood All but first 3 pints FirSt 3 pints

None

None

None

None

None

First S pints

Medicare (Part 13): Medical Frieurancered ServIcespeuealendar YearHealth expenses Medicare pays for healthphysicians' services, services in or out of theoutpatient health services hospitaland supplies, physicaland speech therapy,ambulance, etc.

80 percent_ofMedicare-approvedemount (after$75 deductible)

$75_deductible plus 20percent of balance ofapproved amount (plusany charge aboveapproved amount onunassigned claims)

All Medicare- approvedchargee net Covered byMedicare. This benefit__may be limited to $5,000per year and may besubject to an annualdeductible of $200.

Home health dare UnliMited visits asmedinally necessary

Full cost Nothing Nene

Outpatient hospitaltreatment

Unlimited as medicallynecessary

80 percent of approvedamount (after $75deductible)

$75 deductible plus 20peteent of balance ofapproved amount(assignment is required)

Soma as kir healthexpenses

Bleed Blood 80 percent of approvedarnountAafter $7_5_deductible and startingwith 4th pint)

Fire 3 OM plus 20percent of approvedamount (par $75deductible)

Same as forhealthexpenses, pliis fiett 3pints

Clinical laboratory Unlimited as medicallynecessary

Full cost (on assignedclaims)

-----.-Nothing_on assignedclaims. Different('bAween Medicarepayment and charges onunassigned claims

Same as for healthexpenses (on unassignedclaims)

'Based on calendar year 1986 Medicare deductible and coinsuranbeamounts.

Chapter 3Policies Reviewed Generally Met Standards

As can be seen in the table, Medigap policies are not required to paysome items, such as the part A deductible. Also, under part B, a Medigappolicy may have its own deductible of up to $200 per year and may alsolimit benefits to $5,000 per year. As discussed below, some policies pro-vide coverage beyond these minimum requirements.

A person who is shopping for Medigap insurance snould be aware of thecoverage options available. The buyer's guide jointly published by IICFAand NKIC includes a table similar to the one above plus other helpfulhints for Med:care beneficiaries shopping for health inturance. Also,each Medigap policy must contati an outline of coverage, in a formatsimilar to the table above, which describes the coverages of the golicy.Comparing policies and reading the buyer's guide should give a Medicarebeneficiary considerable informatkm to help in choosing a golicy. Inaddition, as discussed in chapter 5, we found that several states publishtheir own shopper's guides for Medigap insurance sold there.

Policies Reviewed byGAO

We reviewed 142 policies to determine whether the provisionS and cov=erage of each were in compliance with the 11.alcus amendment standardslisted above. From the 398 policies on which we obtained earned pre=faium and incurred claims data, we selected 142 goliciei, which includedin each state the five commercial policies with the highest earned pre-miums in 1984, all Blue Cross/Blue Shield plans in the stalk, and arandom selection of other policies. Our objective was to select policiesthat would cover most of the business (the Blue Cross/Blue Shield plansand high-volume commercial policies) plus Some lower volume policies.

Although the basic purpose of our review was to determine compliancewith Baucus amendment standards, we also noted policy coverages thatexceed the minimum standards.

Minor Shortcomings Notedin Certain Policies

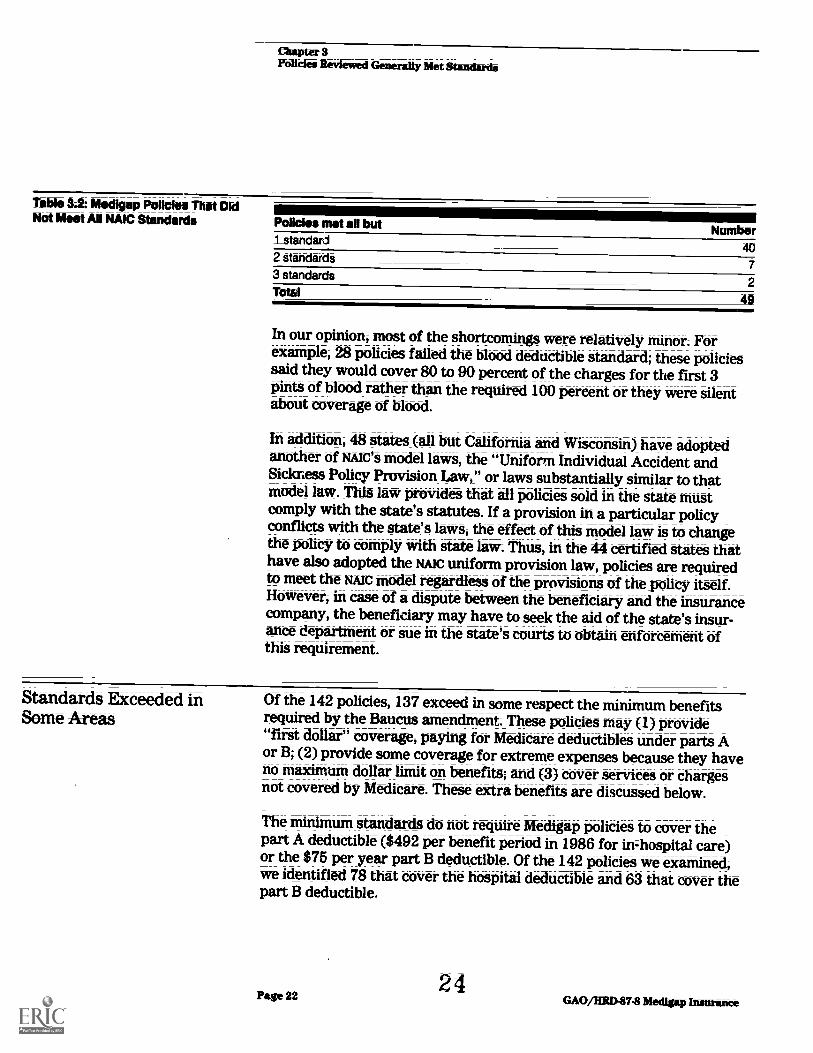

In our opinion, 49 of the 142 golicies we reviewed did not meet all of thefederal standardS. Generally, the policies fell short on one of the stan-dards, as shown in table 3.2.

Page 2123

GA0/RED./37-S Medipp Insorwoce

Table 3.2: Madigan Ponchos That DklNot Meet All NAM Standards POliales

istandard2 Static lardS

3 standardsTotal

Number40

7

2

49

In our opinion, most of the shortcomings were relatively minor. Forexample, 28 policies failed the bloOd deductible standard; these policiessaid they would cover 80 to RO percent of the charges for the firSt 3pints of blood rather than the required 100 percent or they were silentabout coverage of bleo-d.

In addition, 48 states (all but California and Wisconsin) have adoptedanother of Nmc's model laws, the "Uniform Individual Accident andSickness Policy Provision Law," or laws substantially similar to thatmodel law. This law provides that all policies sold in the state mustcomply with the state's statute& If a provision in a particular policyconflicts with the state's laws, the effect of this model law is to changethe policy to comply with state law. Thus, in the 44 certified States thathave also adopted the rim uniform provision law, policies are requiredto meet the mic mOdel regardless of the provisions of the golicy itself.However, in case of a dispute txtween the beneficiary and the insurancecompany, the Iseneficiary may have to seek the aid of the state's insur=ance department or sue in the state's courts to obtain enforcement ofthis requirement.

Standards Exceeded inSome Areas

Of the 142 policie& 137 exceed in some respect the minimum benefitsrequired by the Baucus amendment._These Rolicies may (1) provide"first dollar" coverage, paying for Medicare deductibles under parts Aor B; (2) provide some coverage for extremeexixnses because they haveno maximum dollar limit on benefits; and (3) cover services or chargesnot covered by Medicare. These extra benefits are discussed below.

The minimum standards do not require Medigap policies to cover thepart A deductible ($492 per benefit period in 1986 for in=hospital care)or the $75 per year part B deductible. Of the 142 policies we examined,we identified 78 that cover the hospital deductible and 63 that cover thepart B deductible.

Page 22 GAO/IIRD-87-8 MedIwp Wier:nee

Chapter 3Policies Reviewed Generally Met Standards

Medigap policies are required to pay 90 percent of the in-hospital dailycosts for up to 365 days, after the beneficiary's Medicare benefits areexhausted. This tyge of coverage could be considered a limited form of"cataStrophic" health insurance. The policies we reviewed generally donot provide coverage beyond the 365-day requirements, but 61 of thegolicies exceeded the minimum requirements by covering 100 percent ofthese daily hospital costs. However, few Medigap beneficiaries woulduse this benefit. HCFA data show that only 0.6 percent of p-ersons aged 65years and greater hospitalized during 1984 used any of their lifetimereserve days. HCFA estimates that since the beginning of Medicare, aliout0.3 percent of all enrollees exhausted their 60 lifetime reserve days, atwhich point this benefit would apply.

Six policies paid more or permitted payment ofmore than the required20-percent part B coinsurance. Four of the six golicieS paid from 24 to30 percent of the Medicare:approved charge for part B services, and twopolicies paid some portion of the difference between a supplier's chargefor a service and the Medicare-approved amotmt for that service.

Fifteen policies provided coverage for private duty nutting, which is aservice not covered by Medicare Sixty-seven of the Medigap policies wereviewed covered the part A coinsurance ($61.50 per day in 1986) forthe 21st through 100th day of necessary skilled nursing care, which isnot required by the minimum benefit standards.

A Medicare beneficiary can buy Medigap insurance in the certifiedstates with reasonable assurance that the policy either meets the min-imum benefit standards of the NAIC model regulation or is required bystate law to be in compliance with the standards. However, an indi-vidual may still face significant out-of-pocket costs even if he or she hasa Medigap policy, lyecause such policies are not required to pay thedeductibles under parts A or B, may limit coverage of part B coinsur-ance to $5,000 per year, usually do not cover any costs that exceedMedicare's approved charges, and usually do not cover services (such asnursing home care) that are not covered by Medicare.

We also noted that many Medigap policies provide at least some cov-erage beyond the minimum requirements.

Page 23 25 GAO/MD-874 Medigap Insurance

Chapter 4

Loss Ratio Experience of Medigap Policiesed, and Generally Not Used by States to

aluate Premiums

The actual loss ratio experience of many individual policies did not meetthe tarpt loss ratios of the Baucus amendment, but the actual lossratios of the policies with the largest volumes of earned premiums wereabove the targets. However, loss ratios for a particular year can be diffl=cult to interpret for a number of reasons. For example, a new policy mayhave a low loss ratio, but the ratio may rise as the policy matures. Ala°,policies that experience a high turnover in policyholders may have a lowloSS ratio because of such factors as the 6=month exclusion for new poli-cyholders for treatmentS associated with preexisting conditions.

The loss ratio in the l3aucus amendment is the "expected" ratio betweenpremiums and benefits paid, not a ratio that must actually be met. Thus,if the insurer demonstrates to the state that it anticipates paying outenough in tenefits to meet the specified loss ratios, it has met the lossratio requirement. Accordingly. MIS believes the States are not requiredto evaluate whether the actual loss ratio experience of Medigap policiescomplies with the target. We believe that mis's interpretation isreasonable.

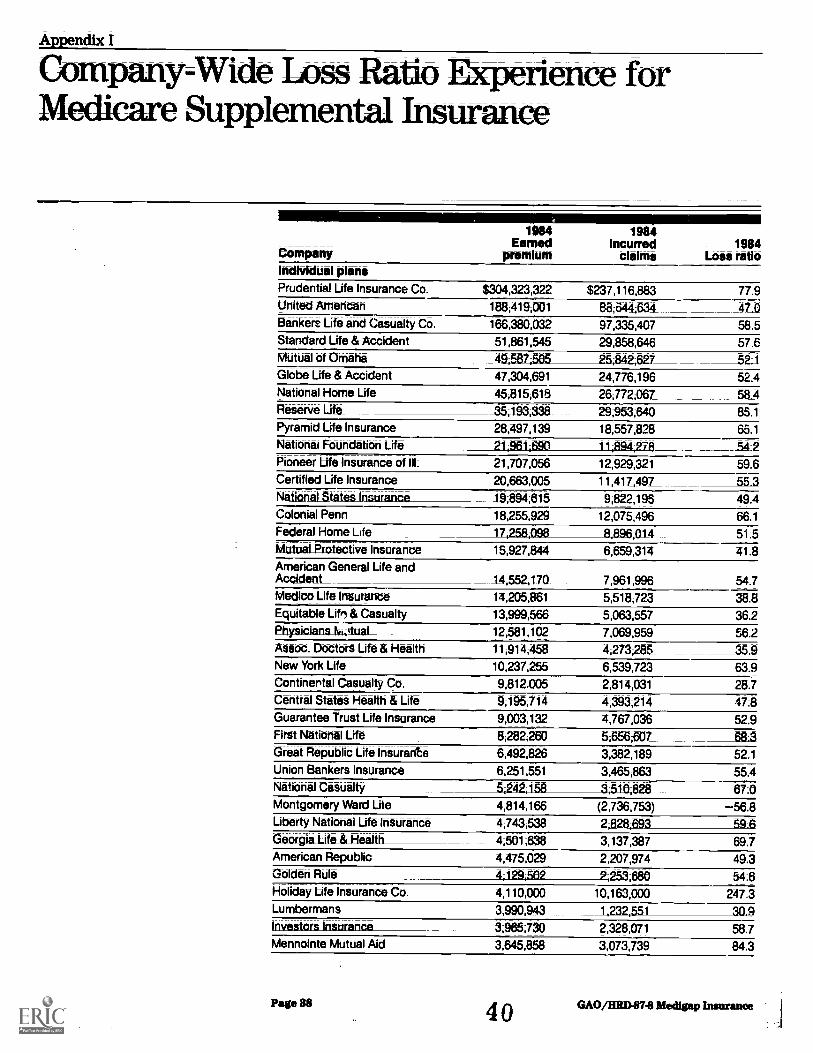

Appendik I lists the annual earned premiums and loss ratios forMedigap insurance for 98 commercial firms and 13 Blue Cross/BlueShield organizations that issued the 398_golicies covered by our review.The loss ratio data cover the period 1982-84. The commercial companyinformation is nationwide data for policies for which data were avail-able, whereas the Blue Cross/Blue Shield data are statewide. The 92commercial companies for which the 1984 loss ratio was obtained hadan aggregate loss ratio for 1984 of 60.2 gement. This loSs ratio was sub-stantially influenced by the experienceof the Prudential Life InsuranceCompany, which had nearly one-fourth of the earned premium amountand a loss ratio of 77.9 percent. The 13 Blue Cross/Blue Shield organiza-tions had an aggregate loss ratio of 81.1 percent during 1984.

Explanation of LossRatios

The loss ratio for a policy represents the Nrcentage of premiums col-lected that are paid in benefits; it is computed by dividing the amount ofincurred claims by the amount of earned premiums for the reportingperiod. The result of this computation is usually expressed as a per-centage. Incurred claims include not only paid claims but also re&ervesfor claims for services enrollees received durirmg the period that have notyet been settled by or reported to the inSurer. The earned premium forthe wriod for which a loss ratio is computed is an estimate of (1) thegortion of total premiums assumed to have been uSed for incurredclaims plus (2) the portion of earned premium that is available for

Page 24 2 6 GAOAMD-87-8 MedItIP Insurance

Cluipter 4Loss Ratio Experience of Medigap PoliciesMixed; and Generally Not Used by States toRI lima* Premiums

profit, paying dividends, and such expenses as administration, salescommissions, and advertising.

LOSS ratios, which are used in the insurance industry as a method ofinterpreting the amount of benefits returned to policyholders, are some-times considered a way of measuring the policy's value. Generally, stateregulators told us that loss ratios must be interpreted with care and thata loss ratio that falls below the minimum required should mark thebeginning of research to determine the reasons for the variance from thetarget.

In addition, several state insurance department staffs told us that lossratios are useful only when dealing with "mature" policies, but theyhave different opinions on whether a mature policy is one that has beenin force for 2, 3, or 4 years. Factors that can affect the maturity of apolicy are the &month waiting perk5d for claims involving treatment forpreexisting conditions and the expectation that policyholders will needmore medical services as they grow older and thus will submit moreclaims the longer they hold a policy.

The Baucus amendment requires an "expected" loss ratio of 60 percentfor policies sold to individuals and 75 percent for policies sold to mem-bers of groups. The states we visited all had requirements for Medigappolicies to have an anticipated loss ratio at least equal to the Baucusamendment targets. When companies apply for policy approval from thestate insurance commissioner, the states require companies to includewith the application their actuarial estimateS for the policy's anticipatedloss ratio.

His has interpreted the amendment as not requiring state regulators tomonitor the actual loss ratios of Medigap wlicies, but we collected datasubmitted by insurance companies to the state insurance departmentsand computed loss ratios for 394 individual and 4 group Medigap poli-cies. The loss ratios of 254 of the policies were below the targett.

Regarding loss ratios, the Baucus amendment provides:

"The Secretary shall certify.. . . any medicare supplemental policy, or continue certi-fication of such a policy, only if he finds that such policy-

"(2) tan be expected (as estimated for the entire period for which rates are com-puted tip provide coverage, on the basis of incurred claims experience and earnedpremiums for such period and in accordance with accepted actuarial principles and

Page 25 z, 27 GAWERD-87-8 Medigap Insurance

(MAW& 4Loss Ratio Experietts_of Medigap PoliciesMixon% and Gencndly Not (Wed by !Retell toEfthinte Peeininms

practices) to return to_policyholders in the form of aggregate benefits providedunder the policy; at least 75 percent of the aggregate amount of premiums collectedin the case of group policies and at least 60 percent of the aggregitth dinount of pre-Mitittit ttillected in the case of individual policies.

"For purp-oSa of paragraph (2), policies issued as a result of solicitations of individ-uals through the maila dr by mass media advertising (including both print andbroadcast advertising) shall be deemed to be individual policies."

The amendment further provides that a state program mugt rricet thesame requirements in order to be certified.

On May 6, 1985, in reswnse to an inquiry from Senator Baucus con-cerning the Mcdigap legislation, the Secretary ofMIS interpreted thisprovision as follows:

"The statute requires that a Medigap policy have a minimum antieiPated loss ratio.It does not rwitiire that actual loss ratio merience be compared with What Wasanticipated. The Panel certified States on the basis that a minimum anticipated lea§ratio Wag required. consequently, there is not much information available aboutproblems in aatertaining loss ratios or on the impact the Medigap program hws hadon policies that had lower loss ratios than that required." (Emphasis supplied.)

Thus, according to Him, the states are not required to compare the lossratio experience of Meligap policies with the standards for the3e ratios.we found several states that, on their own, require insurance companieato furnish actual earned premium and incurrCid claim§ information.

Of the states we visited, Colorado, Maryland, Missouri, and Penn-sylvania were collcicting data that would allow them to monitor the lossratioS of Medigap policies.

Missouri monitored insurers doing business in that state, including cer=tain insurers who market policies nationwide through a truat arrange-ment within Missouri. In April 1986, Missouri wrote to 38 insurerswho-se loss ratios were below die targets, telling them that their loaaratios were too low and instructing them to lower their premiumsaccordingly. Five insurers lowered their premiums. The other 33itnsurers responded, and as of Septemlw 1986 the State had contractedwith an actuarial consultant to study those responses.

Colorado, Maryland, and Pennsylvania have be-en collecting data on lossratio-a, but as of August 1986, state officials had not concluded thataction was necessary. Colorado analyzed loss ratios for Medigap policies

Page 26 28 GAO/HRD-87-8 Medlgap Insurance

Chapter 4Loss Ratio_Experienceof Medlgap PoliciesHiked, lad Generally Not Used by States toEvaluate Premiums

and found that-the policies liad average statewide loss ratios of 54 per-cent and 58 percent for 1983 and 1984, resiRctively. As of June 1986,however, the state had not requestCd explanations from companieswhose loss ratios were below the standards. Maryland requires insur-ance companies doing business in the state to report annually theirexperience on policies sold to Maryland residents. If the company has sofew policies in force in the state that a statewide loss ratio is not cred-ible, the company may submit data on its nationwide experience. Mary-land requires data covering 5 years' experience, and Pennsylvaniarequires 4 years' experience.

The state of Washington plans to begin a loss ratio monitoring programin late 1986 for all health and accident insurance.

We obtained nationwide financial information on 398 policies for which1984 premium and claims information was reported by 92 commercialfirms and 13 Blue Cross/Blue Shield plans. Using the data availablefrom the states,' which varied from 1 to 5 years' experience, we com-puted a cumulative loss ratio for each policy. The four golicies withearned premiums in 1984 of over $100 million had loss ratios thatexceeded the target. Generally, the policies that were not meeting theloss ratio targets established in the Baucus amendment had less busi-ness, as shown in table 4.1.

'Data concerning policies sold by Prudential, National Home Life, and Colonial Pennwere not avail-able thrbiigh the states we Visited; those data were obtained through a private association. The datawere also reported to us on an aggregate basis for each company's Medigap business, not on a policy-by-policy Weds:

29

Page 2/. GAO/HM87-8 Medlgap hum:ante

cbapter 4Loss latioltaiwkwee able-MOOPolkiàMIS Td, Wesseridly Not Used by States toEvaluate Premiums

Rati. 111114 fufrhedpremhmtOver $100 million

$50-99 million

$149 enilliOn

TIM

CommercialBlve Cross/ Blue Shield

Number of policies with---Cttaltdativaitisa-tatkii-

Abovetarget

BOIOW_target

lndMduaiCommercialBILit Cross/ Blue Shield

CommercialBlue Cites/ Blue Shield

39

Group10

1

892

Under $1 millionCommercialBlue Cross/ Blue Shield

861

Gr Otip

1580

2Total 144 254

The total 1984 earned premiums for the 144 rolicies whose loss rati6Swere almve the tarpt was aWut $1.4 billion; for the 254 policies whoselots ratios were below the target, the 1984 earned premiums totaledabout $650 million.

The percentages of policies whose loss ratios were above and below theBaucus amendment targets, groupt.d according to volume of 1984earned premium, are shown in figure 4.1.

Pe& 28 GAO/HRD-8741 Medico Iiittaillite

CMS* r 4Loss Ratio Experience of M PoliciesIllixeck and Generally Not Used by &atm to&abate Prendums

Figura 4.1: cumulative Lou Ratios forlUticiFesp POIó by Amount of 1984Earned Premiums Percentage

lisTra th4it $100 $SO=119

Range of 1984 premium on millions

1-1Above target

Below target

4149 Loss than $1

In appendbc I, the loss ratios of the companies that sold the 398 policiesplus six additional companies that reported premium and claims infor-mation for years before 1984 are present&I on a company-wide basis forall policies for which data were available. Overall, the aggregate lossratios for the commercial companies ranged from 59.2 to 65.3 percent in1982=84; for Blue Cross/Blue Shield plans, the range of aggregate lossratios was 81.1 to 93.7 percent. The cumulative loss ratios of individualcommercial policies for which we had 3 or more years of data rangedfrom 18.6 to 85.3 percent. For Blue Cross/Blue Shield individual plans,the cumulative loss ratios ranged from 58.1 to 111.8 percent.

States to Receive DataThat Can Be Used toMonitor thss RatioExrerience

An NAM committee prepared a revised standard Medigap reporting formfor calendar year 1985 and later. NAIC recommends its reporting formsbut does not have the authority to require their use; nevertheless, a rep-re_entative of the industry told us that NAIC forms usually become theindustry-wide standard. These mix:tits are due from the insurance coin=panies by June 30 of the year following the year the data cover. The

Page 29 31 GAO/HRI878 bind100 huiUiiiià

Chapter 4Loss Rado_Expaknot of Medighp VolieW

WeiWrally Not Used by States toEvaluate Pm= lams

new Medigap form calls for loss ratio data to be regorted for the "lattcompleted calendar year" and "last three calendar yeafs." The newform also requires loss ratio data for "Experience in Reporting State"and "United States Totals." The impetus to develop and implement thisreporting form came from the stateS.

When we completed our work at the States in June 1986, they had notyet received data reported under this new framework, but the firstannual reports on the new form were due on June 30, 1986. Regulatoryofficials in the states we visited lelieved that historical data are neces-sary for the states to adequately monitor loss ratio experience.

State insurance regulatory officials told us that loss- ratios are a usefultool in analyzing insurance policy performance, but caution that theyare only a step in any analysis. Loss ratios must be interpretbi with carebecause of the factors that may affect the &utations. Early policyexperience may result in a relatively low loss ratio because of waitingperiods for certain conditions when the policy will not cover services.Also, new policyholders may be relatively healthy and file few claims,so a policy experiencing substantial amounts of new business mayexperience a relatively low loss ratio. ThuS, loss ratios should be viewedover the time that represents "mature" experience. State officials couldnot give us a clear definition of mature experience, but the new NAICreporting form requesta data covering 3 years' experience.

The Baucus amendment established WAS ratio targets of 60 percent forindividual Medigap policies and 75 percent for group Medigap policies.According to ios, there is no requirement for the States to determinewhether policies meet these targets. Beginning with data covering cal-endar year 1985, the states should receive standardized loss ratio infor-mation, which will aid them in monitoring loss ratio experience, if theychoose to do so.

We computed loss ratios from lata available in the states and through aprivate association. The loss ratios of 254 of the 398 volicies wereviewed were below the targetS, and theSe policies had about $650 mil-lion in earned premiums in 1984. Generally, the policies offered by coin;mercial firms with high volumes of earned premiuma and Blue Cross/Blue Shield plans had loss ratios that exceeded the targets.

Loss ratios reflect the combined experience of all policyholders, but thepurchase of a policy is a highly individual transaction. A relatively high

Page 80 32 GAO/HILDS741 bleAtm) Inuratice

Chapter 4 _

Lots Rado Experience of Medigip PoliciesMixed, and Generally Not Used by States toEvaluate Premiums

.loss ratio mdicates that the policyholders as a group are getting a fairreturn on their premiums but does not promise any particular return toan individual.

As discussed in chapter 3, the extent of bnefits provided underMedigap insurance varies among policies. This, combined with the widedifferences in loss ratios discusaed in this chapter, indicates to us that itis important for beneficiaries to shop for Medigap policies in order toobtain the best return on their premiumpayments. Chapter 5 diacusaesaome of the assistance available to beneficiaries when they are lookingfor a Medigap policy.

33Page 31, GAO/ERB-SU Medigap Insurance

Chapter 5

te and Federal Agencies Have Thed to CurbSales Abuse Through Education and Penalties

The purchase of Medigap insurance can be a complicated transaction1*.eause policy provisions, benefits, and loss ratios vary among policiesthat meet the minimum standards. HCFA and the states have made var-ious efforta to aid and educate the elderly to make informed insurancepurchase decisions. Sales abuses continue, but the states have takensome actions to deal with them through monetary penalties, cease anddesist orders issued by state insurance commissioners, and the revoca-tion and susimision of agent licenses. There have been no federal con-victions under the Baucus amendment; however, the Postal Service hasinvestigated Medigap insurance sale abuses under the mail fraud stat-utes. A June 1986 report, by the House Select Committee on Aging con-cluded that the states have done a gcod job in implementing regulatoryimprovements, but the report notes that abuses persist in the sale ofMedigap insurance.

Generally, federal and state agencies initiate actions in response to com-plaints about advertising or sales practices. Federal agencies tend toemphasize educational activit es, to help people make informed choices.While also supporting efforts to inform elderly persons about theoptions available to them, the states have been the primary enforcementarm against advertiSing and Sales abuses.

Federal Efforts To educate Medicare beneficiaries about purchasing private healthinsurance, HCFA and NAIC publish the Guide-to-Health Inturance forReople-With-Medicare. The guide includes suggestions to makepur-chasers aware of and to protect themselves from misrepresentations andabusive sales practices. The guide is made available, without charge,through Social Security offices, and it is published in English andSpanish.

HCFA also conducts a nationwide educational program for volunteerswho assist Medicare beneficiaries considering the purchase of Medigap

HCFA distributes its Medicare and Private Health-InsuranceTraining Text to course participants as an instructor's guide.

The Social Security Administration district offices, as a contact pointwith the elderly, may receive questions or complaints from Medicarebeneficiaries. These district offices record complaints and refer them toHCFA regional offices.

ICataStroPhie-Health-Insurance: " axeport by_the_Chairman; Subcommittee on Healthand Long-Term Care, House Select Committee on Aging, June 1986.

Pue 32 34 GAO/HRD-87-3 Medlgap Inaarance

Chmter 5State Ind Federal Agencies Have 'Med toCurb Sales Abuse Through EducationLnd PenVtles

HCFA'S regional offices have been involved with settling complaints fromconsumers about possible misrepresentation and other misleading salespractices of companies and agents. HCFA refers these complaints to theappropriate state insurance departments or to the MIS In Spector Generalfor digposition. During fiscal years 1982-84, HCFA received 63 complaintsof misrepresentation or sale of policies duplicating coverage underanother policy. HCFA referred 8 complaints to the inis Inspector Generaland 25 to the various state insurance departments for follow-up action.HCFA reviewed and dosed the other 30 complaints for lack of evidence.In Meal year 1985, HCFA received another 17 complaints. HCFA closed 13of the complaints because of a lack of evidence; the other 4 Werereferred to state insurance departments.

In 1982, HCFA cooperated with the U.S. attorney and the Federal Bureauof Investigation in charging four insurance agents in Pennsylvania withrepresenting themselves as federal employees while persuading elderlypeople to buy medical insurance. The Baucus amendment provides sanc-tions for posing as a federal agent to sell Mcdigap volicies. The chargesagainst these individuals were dropped becaute of difficulties in provingthat they represented themselves as government agents, but the state ofPennsylvania later wnalized one of them by suspending hig license tosell insurance.

The Postal Inspection &rvice alSo takeS preventive measures againstinsurance fraud through a consumer protection program directed at Wu=cating the elderly about potential Mail fraud SchemeS. According to the

rvice, many of its 100 inspectors assigned to crime prevention dutiesmake presentations to various senior citizen groups, and pamphlets onthe topic are provided at no coSt. The Service also has investigatedinsurance fraud cases directed against the elderly, although as of June1986 there were no current investigations ahned specifically at Medigapinsurance.

Many States SupportEfforts to NW andEtlucate the ElderlyWith MedigapInsurance Decisions

All the state insurance departments that we visited, except RhodeIsland's, had a consumer protection diviSion to help elderly citizensunderstand the sometimes confusing language of health insurance roll=cies and a group of investigators to handle complaintS received from thepublic. In Rhode Island, complaints about Medigap insurance arereferred to the state's department of elderiy affairs.

Some examples of state services to assist the elderly in makir,g Medigapinsurance decisions are

Page 58t 35 GAO/HR13417-43Medigap Insurance

Chapter 5StaW and Federkil Agendes Rave Tried toCurb Sales Abuse Through Educationand Penalties

shopper'E guides that compare_prices and coverages,education programs available for presentation at senior citizen meetings,andnetworks of Lounselors to help the elderly With inStirance decisions:

The state of Washington has a program that is Centered oh the seniorhealth insurance benefits advisors and includes a comparative shopper'sguide; The advisors train senior citizens and other volunteer8 te beaware of the variety Of medical proteetion services available to the eld-erly. These trained volunteers serve as advisors for seniors in their coin;munities. The office of aging staff in NeW JetSey said they trainedpeople tO counF2l senior citizens in a program similar to that ofWashington.

In Arizona the state Association of Life Underwriters created the SeniorCitizens Health Insurance Counselors program. ThiS pitgram was aresp-onse to the negative image given the industry as a result of thestate's "sting" operation, concluded in 1980, which dettiOnStrated thatagents had misrepresented the insurance they were selling; The objec-titre of the program, which is fmancially supported by the state, iS tOtram* volunteers to counsel senior citizens ne-editig ASSistatiCe in makingintelligent decisions about purchasing Medigap or other insurance.

Florida officials issued a shopper's guide, and they conduct Medigapworkshops at senior citizen association meetings arid condominiumcom-plexes. They credit these effortS with creating a better informed popula-dein who are able to make good choices of coverage. They also said thatthey have received fewer complaints about Mdigap itiSiitatide Sincethese efforts have been in force.

Maryland officials told us they were assembling a shopper's guide forMedigap irsurance available in that state.

All of the states we visited had established rules arid regulations gov-erning advertising practices and sales of insurance by agents, and theymonitor advertising and sales practices. All of them also had a formalinsurance complaint handling system, either thitugh the state's depart-hieing a f insurance or elderly affairs, that included recording corn-plaints; investigating the facts, and attempting tei rekihre the problems;Generally, the states respond primarily to complaints from the elderlyor their representatives. That is, the states are usually tiOt aWare Ofproblems unless they are brought to the attention of state officials.

Page 34 GAO/KRD-87-8 Medigap Insurance

Chapter 5State and Federal Agencies Have 'Med toCurb Sales Alm* Through Hducationand Pena lthia

Pennsylvania had records on the number of complaints about Medigapinsurance received and the disposition of those complaints for theperiod July 1, 1984, through March 31, 1986, and WaShington hadrecore . for the period January 1, 1985, through March 31, 1986. Penn-sylvania received 445 complaints, and the state's investigators consid=ered 234 to I* justified. Of the 504 complaints that WashingtonreCeived, its investigators considered 239 to be justified. In both states,most of the justified complaints dealt wi:h questionS regarding premiumrefunds, diSputed claim amounts, and claim delays. In Pennsylvania, 29of the justified complaints concerned misleading advertising and agentmisrepresentation; in Washington, 32 were about those problems. In theother states visited, either we could not separate complaints alYoutMedigap tclicies from complaints ahout other formS of insurance,or wecould not readily identify the number of complaints received and theirdisposition for a recent time period.

Although time did not permit us to catalog all actions taken by thestates, the following are examples of actionS taken during 1985 and1986:

1. Several states have acted to stop the use of mailings that were consid-ered misleading. For example:

The Washington state insurance commissioner's office issued a ceaseand desist order in January 1986. The order directed two groups to stopmailing information that attempted to deceive senior citizens. Thegroups involved were the "Senior Security Ilenefit &rvice" and the"National Senior Advisory Center." Both had the same Washington,D.C., address. The official-looking envelopes used, as well as the namesand addresses of the groups, led the State office to conclude that theywere deceiving people into thinking they were official government mail-ings, when the mailings were actually insurance marketing forma.An agreement and consent order in February 1985 betweenan insurancecompany and the Pennsylvania insurance commissioner called for thepayment of a $50,000 wttlement to the State. The Pennsylvania insur-ance department complained that the company's mail solicitations weremisleading and deceptive. The MassachusettS State division of inSuranceissued a cease and desist order against the same insurance company fora deceptive mail solicitation. The state complained that the company'Smailim suggested the purchase of the insurance was required by federallaw. Florida also fmed this company $5,000 for deceptivemailings.

P0,86 37 GA0/111W.117-8 Medigap Insurance

Chapter 5State and Federal AgencleaRave Tried toCurb Salei Abuse Through Educationand Penalties

2. In March 1986, the state of Florida fined an insurance company$25,000. This company was not renewing policies but rather offered pol-icyholders a new policy that started a new 6-month waiting period forbenefitt.

3. &ome states have dealt with insurance agent misrepresentation casesthrough fines and/or license revocation. For example, an agent in Penn-sylvania was fined for falsely representing himself as a Medicare offi-cial. This was not a first offense. In Florida, agent licenses have beenrevoked for Medigap sale abuses, according to state officials, but thenumber of revocations was not readily available. During 1984, Arizonasuspended or revoked the licenses of 15 insurance agents for violationsinvolving the sale of Medigap insurance.

4. In June 1986, Maryland completed an investigation and receivedagreement from an insurance company to notify its agents that theywere not to use unfair or high-pressure sales tactics or to misrepresentthemselves as agents of another company or Medicare. This investiga-tion grew out of consumer complaints that the company's agents soldMedigap and other health golicies that were essentially duplicativeb-ecause the policyholders already were covered by other insurance.

In June 1986 hearings before the House &lect Committee on Aging, Min-nesota's attorney general testified on current sales abuses and actionstaken by that state to stop abuses in the sale of Medigap insurance.Those actions included