Embed Size (px)

Citation preview

Do institutional investors mitigate social costs ofprivatization? Evidence from prisons

Eyub Yegen∗

November 2020

Abstract

This paper examines whether institutional investors mitigate social costs that arisewhen government services are outsourced to private enterprises. Using hand-collecteddata on U.S. prisons, I find that privatization is associated with an increase in prisonersuicides by up to 39%. However, institutional investors of public companies managingprivate prisons decrease suicide rates by one third. These effects are stronger for long-term institutional investors since failing to internalize social externalities negativelyimpacts the long-term success of portfolio firms. Evidence from a tax reform thatexogenously increases institutional ownership of prison management companies suggeststhat the relationship between ownership and social outcomes is causal. To explain theseresults, I show that institutional investors have incentives to be socially responsible dueto litigation and reputation risks.

Keywords: Institutional Investors, Corporate Social Responsibility, Social Welfare

JEL: A13, G23, G32, H11, L33

∗Rotman School of Management, University of Toronto. E-mail: [email protected]. I wouldlike to express my gratitude to Pat Akey, Susan Christoffersen, Craig Doidge, Ray Fisman, and Mike Simutinfor their invaluable guidance and support. I also want to thank Anat Admati, Matthew Baron, MarianneBertrand, Matilde Bombardini, Mahfuz Chy, Peter Cziraki, Alexander Dyck, David Goldreich, Todd Gorm-ley, Denis Gromb, Oliver Hart, Camille Hebert, Charles Martineau, Paola Sapienza, Denis Sosyura, MatthewShaffer, Ana-Maria Tenekedjieva (discussant), Karamfil Todorov, Francesco Trebbi, Abhishek Varma (discus-sant), Hannes Wagner (discussant), Irene Yi, Luigi Zingales and participants at the Chicago Booth PoliticalEconomy of Finance conference, Columbia GRASFI conference, Conference on Green and Ethical Finance atSMU, FMA Annual Meetings, and Bank of Canada for fruitful discussions. The Clarkson Centre for BusinessEthics provided generous funding to support this project.

1 Introduction

Over the past three decades, outsourcing government services to the private sector has

become a popular tool for policymakers worldwide due to the benefits of privatization [Meg-

ginson and Netter (2001), Kamerman and Kahn (2014)]. Although there may be noticeable

efficiency gains of privatizing government services, a large body of literature in economics

suggests that privatization may impose social costs.1 Prior studies highlight the trade-off

that private enterprises have incentives to cut on costs, which may sacrifice quality [Hart,

Shleifer, and Vishny (1997)]. Reducing spending on resources that impact the quality of

outsourced government services may also harm individuals who rely on these services.

Despite the potential for private prison management companies to maximize profits by

neglecting to offer adequate resources to inmates, the United States government has increas-

ingly relied on private companies to provide prison services.2 In particular, from 2000 to 2016

the number of inmates in private prisons (immigration detention centers) increased by 47%

(442%), whereas the total number of prisoners rose by only 10% [Gotsch and Basti (2018)].

During the same period, the ownership structure of public companies that manage private

prisons has also changed dramatically; institutional ownership in these public companies has

risen by over 60%. The interest of institutional investors in prisons even went to the point

that delegated asset managers, such as BlackRock, have purchased their own prisons.3

In this paper, I examine a previously unstudied mechanism through which social costs

of privatization may be mitigated by shareholders of public companies that manage private

prisons in the United States. Recent theoretical studies highlight that the role of shareholders

may be instrumental in determining whether managerial decisions internalize social exter-

nalities [e.g., Benabou and Tirole (2010); Hart and Zingales (2017)]. Also, recent empirical

studies find that institutional investors may drive corporate social responsibility outcomes

[e.g., Dyck, Lins, Roth, and Wagner (2019); Chen, Dong, and Lin (2020)]. However, relatively

less is known whether institutional investors have a direct impact on social welfare.

1See, for example, Hart, Shleifer, and Vishny (1997), Lopez-de Silanes, Shleifer, and Vishny (1997),Shleifer (1998), Besley and Ghatak (2001), Baland and Francois (2005), Hart (2017).

2The New York Times article titled “Inside a Private Prison: Blood, Suicide and Poorly Paid Guards”summarizes the inadequate conditions in private prisons.

3For details, see the Reuters article titled “BlackRock-owned Mexican prison opens in Coahuila.”

1

To examine whether the poor prison conditions due to privatization are affected by insti-

tutional ownership, I have compiled a novel dataset on U.S. prisons by filing 51 state-specific

Freedom of Information Act requests and by hand-collecting other information from various

government documents.4 Without taking the ownership structure of the prison management

companies into account, I first empirically examine the main theoretical prediction of Hart,

Shleifer, and Vishny (1997) on whether prison privatization leads to a rise in social costs.

In particular, when the contract between the government and private prison operator

is incomplete, owners of the private enterprise have the residual right to make decisions

on the non-contracted dimensions. Due to an incentive to maximize profits, Hart, Shleifer,

and Vishny (1997) predict that private operators have incentives to cut on costs on the

non-contracted dimensions by ignoring to take negative externalities into account. These

externalities are more severe in less competitive industries, such as the prison industry, where

cutting on the quality of resources may have a detrimental impact on the lives of prisoners.

Consistent with Hart, Shleifer, and Vishny (1997), I find empirical evidence that privati-

zation of prisons is associated with an increase in inmate suicides, by up to 39%, even after

including prison fixed effects. As in Fisman and Wang (2015, 2017), I use mortality rates as

a proxy for social costs. Mortality rates are difficult to monitor, and the government does

not specify an upper limit on mortality rates in contracts signed with prison management

companies. Another reason for using this proxy is that if prisons are well managed and of-

fer adequate rehabilitation services, the probability of committing suicide may also decrease

[see, e.g., Hayes (1995); Cramer, Wechsler, Miller, and Yenne (2017); Fazel, Ramesh, and

Hawton (2017)]. However, the results are not sensitive to the choice of the outcome variable,

and I derive similar conclusions when I use alternative proxies, such as unexpected deaths,

total deaths, total rehabilitation programs offered in prisons, and the number of correctional

officers hired per inmate.

To examine my main question of whether institutional investors mitigate social costs of

privatization (when the government fails to write complete contracts), I take into account

the ownership structure of publicly traded companies that manage prisons. After controlling

4Washington D.C. has its own department of corrections and a D.C.-specific Freedom of InformationAct. After exchanging over 830 emails and contacting numerous senior state officials, such as governors andlegislators, I have obtained data on prisons from all states, except the state of Hawaii.

2

for an increasingly demanding set of fixed effects, including prison fixed effects, and time-

varying demographic factors that may impact the ex-ante likelihood of prisoners committing

suicide, I find a statistically significant negative association between institutional ownership

and suicides. In particular, a 1% increase in institutional ownership is associated with a

reduction in suicides by up to 1.2%. These magnitudes are economically significant since

they offset one third of the social costs that are observed in private prisons.

Building on Hart and Zingales (2017), I examine whether different types of institutional

investors pay more attention to social outcomes by breaking down institutional ownership

into more granular levels. Institutional investors with a long-term holding horizon pay more

attention to the long-term success of the firm and have incentives to internalize social exter-

nalities, whereas short-term investors may not have such incentives [Brochet, Loumioti, and

Serafeim (2015)]. Benabou and Tirole (2010) highlight the importance of long-term investors

by stating that corporate social responsibility “is about taking a long-term perspective to

maximizing profits” and “socially responsible investors should position themselves as long-

term investors who monitor management and exert voice to correct short-termism.”

Given that cutting costs may boost short-term profits, institutional investors with a short-

term holding horizon have an incentive to influence managers to implement cost reductions.

Such cost reductions that boost short-term profits, however, are likely to negatively impact

the overall prison conditions, leading to a rise in social costs. As well, institutional investors

with a long-term holding horizon pay more attention to long-term firm value [see, e.g., Bushee

(2001); Brochet, Loumioti, and Serafeim (2015)]. Hence, long-term investors are more likely

to monitor firms to ensure managers do not overly focus on short-term profits and take actions

to boost long-term firm value. Managers who are not overly focused on the short-term are

more likely to internalize consequences of cost reductions that impact prison conditions since

a drastic increase in suicides (or other social outcomes) may impact the renewal of long-term

prison contracts, and therefore negatively impacting long-term firm value.

Consistent with this argument, I find a statistically significant negative (positive) rela-

tionship between ownership by long-term (short-term) institutional investors and suicides

in prisons. In particular, I find that a 1% increase in long-term (short-term) ownership is

associated with a decrease in suicides by 1.2% to 1.5% (increase in suicides by 1.8% to 1.9%),

3

with the results being the strongest in the within-prison tests.

Given that holding duration is not randomly assigned to investors, I use an alternative

proxy for long-term and short-term ownership in addition to a novel identification strategy.

Prior studies [e.g., Bushee (1998, 2001); Gutierrez and Philippon (2018)] find that transients

and quasi-indexers have short and long holding horizons, respectively.5 Using this alternative

proxy for holding horizon, I find that a 1% rise in quasi-indexer (transient) ownership is

associated with a decrease in suicides by 2.5% to 2.7% (rise in suicides by 1.1% to 1.5%).6

However, within the long-term investor category, there is still a large heterogeneity in

the types of investors. The attentiveness to social outcomes may differ across types of long-

term investors. By using the granular investor types provided by Bushee (2001), I further

break down the long-term ownership levels to capture variation in attentiveness to social

outcomes. This may play a role in explaining why there is a positive relationship between

long-term ownership and improvements in prison conditions. I find that there are differential

effects of long-term ownership on social outcomes depending on the type of investor. The

effects are largest among independent investment advisors and companies, such as mutual

funds. Consistent with this finding, Bushee (2001) documents that ownership by independent

investment advisors and companies is positively associated with long-term firm valuation.

The results in my paper so far highlight the importance of making use of the heterogeneous

investor types to capture the social responsibility of shareholders that may impact prison

outcomes differently. These results, however, do not provide any causal evidence in regard

to the effects of long-term institutional ownership on social outcomes. Identifying the causal

effects of long-term institutional ownership on prison outcomes comes with an empirical

challenge. OLS regressions measure only the association between institutional ownership

and prison outcomes rather than examining a casual relationship. To examine the causal

relationship, I develop a new identification strategy that exogenously increases the exchange-

traded fund (ETF) ownership levels in publicly traded companies managing prisons.

In particular, at the end of 2012, the Internal Revenue Service reclassified publicly traded

5The annual portfolio turnover of quasi-indexers is only 33%, whereas the one of transients is 70%.6Quasi-indexers have incentives to monitor firms that are included in their portfolios due to index tracking

since it may improve firm fundamentals that will also have a positive impact on the value of assets undermanagement [for more details, see Appel, Gormley, and Keim (2016, 2018)].

4

prison management companies as Real Estate Investment Trusts (REIT) since these public

companies met the definition to be legally considered a REIT company. This reclassification

led to doubling ETF ownership levels since these prison management companies entered into

more ETFs that track the real estate sector. I make use of this exogenous increase in the

ETF ownership levels as an identification strategy to draw causal inferences on the possible

direct impacts of long-term institutional ownership on social outcomes. Furthermore, related

to the exclusion restriction, the tax reform is unlikely to be implemented to have a positive

impact on prison outcomes, but rather the improved prison conditions are more likely to be

driven by exogenous changes in long-term institutional ownership.

Using an instrumental variable (IV) approach, where I instrument the ETF ownership

levels by the exogenous increase in ETF ownership due to the REIT reclassification, I find that

long-term ownership has a causal negative impact on suicides. The economic magnitudes are

similar to the uninstrumented results. Using alternative outcome variables in lieu of mortality

rates, I confirm that long-term ownership leads to improvements in prison conditions.

Next, I examine why institutional investors may have an incentive to monitor prison man-

agement companies. Arena and Julio (2015) provide empirical evidence that the litigation

environment in the United States plays an important role for decisions made by firms and

shareholders. Corporate litigation is costly to firms and shareholders both from a valuation

and reputation perspective. Institutional investors are more likely to be attentive to social

outcomes if prisons harm the reputation of the institution, and have an indirect impact on

fund flows. For example, various social advocacy groups urge citizens to contact institu-

tional investors that manage their retirement plans, which include prison stocks, to be more

socially responsible with their investments. Otherwise, these advocacy groups urge that cit-

izens should opt to different providers. These calls typically rise when there are lawsuits

against prisons. Hence, if institutional investors indeed partially offset the social costs of

prison privatization, they are more likely to act when there are higher litigation risks.

Following this argument, I first examine whether the long-term ownership effects are

stronger in prisons which are located in states with judicial systems that make it easier for

plaintiffs to successfully sue corporations. As in Colonnello and Herpfer (2019), I use a state-

level proxy for litigation risk by obtaining data from the U.S. Chamber Institute for Legal

5

Reform. This institution publishes an annual ranking of the friendliness of a given state’s law

system to corporations. Using this proxy for litigation risk, I show that the ownership results

are strongest for prisons in states with higher litigation risks (i.e., prisons in plaintiff-friendly

states). I also show that the litigation risk results are robust to using the litigation risk proxy

of Arena and Julio (2015) (i.e., using lawsuits of peer prisons).

Given that the litigation and reputation risk results make use of endogenous ownership

levels, I use the REIT reclassification as an exogenous source of variation in long-term own-

ership levels and interact it with the 2012 state litigation rankings. It is unlikely that the

litigation risk proxies are impacted by the REIT reclassification in 2012 since this ownership

shock is completely unrelated to a state’s litigation ranking (i.e., rankings are orthogonal to

the ownership shock). Using an IV approach, I show that there is a monotonically increas-

ing, negative effect of long-term ownership on suicides in prisons that are located in more

plaintiff-friendly states. This suggests that long-term investors are more attentive to monitor

when there are higher litigation risks. Therefore, litigation risk provides a possible explana-

tion on why long-term investors have an incentive to internalize social costs since not taking

social outcomes into account is costly both from a valuation and reputation perspective.

My paper contributes to two bodies of literatures. First, I contribute to the literature

that examines the role of institutional ownership in corporate social responsibility (CSR)

outcomes. Prior studies [e.g., Starks, Venkat, and Zhu (2017); Dyck et al. (2019); Krueger,

Sautner, and Starks (2020)] find a positive association between institutional ownership and

CSR outcomes.7 Complementing Chen et al. (2020) that provides empirical evidence on the

casual effect of institutional ownership on CSR outcomes, I show that a particular set of

institutional investors drives CSR outcomes. Not all types of institutional investors, such

as short-term investors, positively impact CSR outcomes. Consistent with the theoretical

prediction of Benabou and Tirole (2010), I find that long-term institutional investors have an

incentive to positively impact CSR outcomes. Therefore, I contribute to the CSR literature

by raising the importance of using granular investor classifications to capture heterogeneity in

7Relevant studies in the institutional investors literature include Aghion, Van Reenen, and Zingales (2013),Schmidt and Fahlenbrach (2017), Bebchuk and Hirst (2019), Crane, Michenaud, and Weston (2016); Crane,Koch, and Michenaud (2019), Chattopadhyay, Shaffer, and Wang (2020), and in the CSR literature includeMcguire, Sundgren, and Schneeweis (1988), Fisman, Heal, and Nair (2005), Shiller (2013), Bartling, Weber,and Yao (2015), Lins, Servaes, and Tamayo (2017), Liang and Renneboog (2017).

6

shareholders’ attentiveness to social outcomes, as highlighted by Benabou and Tirole (2010)

and Hart and Zingales (2017), to study the effects of ownership on CSR outcomes. To the

best of my knowledge, this paper is also the first study to provide causal evidence on the

direct effects of institutional ownership on society (in the form of human costs).

Second, I add to the literature on privatization. Prior studies, starting with the seminal

theoretical work by Hart, Shleifer, and Vishny (1997) as well as Lopez-de Silanes, Shleifer,

and Vishny (1997), Shleifer (1998), Besley and Ghatak (2001), Hart (2017) provide evidence

that there may be negative consequences of privatization. However, none of the prior studies

take into account whether the private enterprises’ ownership structure may mitigate the so-

cial costs of privatization. For instance, Banerjee, Hanna, Kyle, Olken, and Sumarto (2019)

experimentally examines the success of privatizing subsidized food distributions in Indone-

sia. Although they find that privatization leads to positive outcomes without the sacrifice of

quality (given that the non-contracted dimensions do not impact social costs), the ownership

structure of the private firms is not taken into account. Eaton, Howell, and Yannelis (2019)

find that private equity buyouts in private secondary schools lead to negative effects on con-

sumers.8 However, none of the prior studies examine whether the public ownership structure

may mitigate social costs of privatization. I fill in the gap in this literature by highlighting

the importance of the ownership structure of private firms, especially in less competitive

industries where the quality of non-contracted outcomes may impact social outcomes.

2 Sample and summary statistics

2.1 Data sources and sample construction

I construct a novel panel of prison-level data on inmate deaths (i.e., suicides, unexpected

deaths, and total deaths), programs offered in prisons (e.g., suicide-prevention programs,

educational programs, health programs), number of correctional officers hired per inmate,

institutional ownership in prisons, and other prison-specific information. My starting point is

the entire set of prisons in the United States of America between 2000 to 2018. To construct

this dataset, I have filed state-specific Freedom of Information Act (FOIA) requests to obtain

8Other relevant studies include Bayer, Hjalmarsson, and Pozen (2009) and Mukherjee (2020).

7

various information about prisons. The information I requested from each state is identical

to ensure comparability of data that each state provides.

To obtain the prison data, I have exchanged over 830 emails with state officials, paid fees

to fulfill my FOIA requests, and had to file complaints with certain states’ commissioner,

governor, and/or legislator. Information on annual mortality data for each specific prison

were obtained from all states, except of the state of Hawaii.9

With this data in hand, I analyze various official reports and databases provided on

each department of corrections’ website to identify whether the given prison was privately

managed and identify the prison management company. In addition, I analyze 10-K files

of prison management companies that are publicly-traded to verify the list of prisons that

are managed by these private enterprises. Similarly, I go over thousands of various official

reports and datasets provided by the department of corrections to hand collect the data

that is needed to construct the control variables.10 The definition of each control variable

is provided in Table 1. The information on various programs offered in the prisons are

also collected in the same manner although some of the department of corrections provided

directly information on programs offered in prisons (e.g., California).

For information on ownership, I use data from the Center for Research in Stock Prices

(CRSP), SEC Edgar, Thomson Reuters, and WRDS SEC Analytics. To construct the in-

stitutional onwership measures, I use 13-F holdings that are required to be disclosed by

institutional investors with at least $100 million assets under management. To obtain the

missing 13-F institutional holdings during the post-2012 period in Thomson Reuters, I fol-

low Ben-David, Franzoni, Moussawi, and Sedunov (2020) and Yegen (2019).11 As well, given

that the 13-F holdings are disaggregated, I follow the approach suggested by Lewellen and

Lewellen (2018) to aggregate the holdings to the parent-level. Following that, I aggregate the

13-F holdings to the annual-level and use outstanding shares from CRSP to construct the

fraction of shares held by various institutional investor types in a given firm that manages

private prisons. To define the fraction of shares held by short-term versus long-term investors,

9The exclusion of Hawaii does not affect substantially the sample size since it has only four prisons. Also,to focus on the within and across state variation, I exclude immigration detention centers and federal prisons.

10I do not automate this process since most reports are provided in varying formats across states and time.11I also verify that no institutional holdings data are missing by using institutional ownership data from

the Bloomberg Terminal.

8

I use the holding duration measure of Lan, Moneta, and Wermers (2019) and the investor

classification data provided by Bushee (1998, 2001) (i.e., transients and quasi-indexers). To

be precise, I use the following definition to construct the various institutional ownership

measures:

Institutional Ownershipi,j,t =

J∑j=1

vi,j,t × AUMj,t

Market Capitalizationi,t

(1)

where j stands for the institutional investor (of the given investor classification type)

that has ownership in the given publicly-traded prison management company i, vi,j,t is the

weight of the given stock in the portfolio of institutional investor j (i.e.,Holding V aluei,j,t

AUMj,t),

AUMj,t stands for given institutional investor j’s total assets under management (AUM),

and Market Capitalizationi,t is the market capitalization of prison management company i.

The average of the quarterly institutional ownership measures are then taken to obtain an

annual ownership number since the prison-level variables are provided at the annual-level.

Similarly, to construct the exchange-traded fund (ETF) ownership variables, I use data

from CRSP, ETF Global, and Thomson Reuters. Following Ben-David, Franzoni, and Mous-

sawi (2018) and Azim (2019), I start by identifying the ETFs in CRSP. By using the CRSP

Mutual Fund database, I obtain all ETF that have an ETF flag and drop ETFs that have a

regional description that is outside of North America using the Lipper Class Name. Follow-

ing that, I use the CRSP Portfolio Holdings database to obtain the holdings data for each

ETF. To ensure that no holdings data is missing, following Azim (2019), I link the CRSP

ETF data with Thompson Reuters Mutual Fund Holdings using the Mutual Fund linkages.

Then, I obtain all of the holdings from Thomson Reuters for each ETF that is identified from

the CRSP database. Following Ben-David, Franzoni, and Moussawi (2018), for each prison

management company I construct the following ETF ownership variable which measures the

average fraction of shares of the firm that are being held in ETFs during the given year:

ETF Ownershipi,j,t =

J∑j=1

wi,j,t × AUMj,t

Market Capitalizationi,t

(2)

9

where j stands for the ETF holding stocks in the given prison management company i, wi,j,t

is the weight of the given stock in the given ETF j (i.e.,Holding V aluei,j,t

AUMj,t), AUMj,t stands for

given ETF j’s AUM, and Market Capitalizationi,t is the market capitalization of firm i.

The average of the ETF ownership measure is taken to obtain an annual number since the

prison-level variables are provided at the annual-level.

Given that holdings are missing in the Thomson Reuters data, I use the ETF Global

dataset for the period starting in 2012. The ETF Global dataset focuses only on ETFs and

has a better coverage. Since this dataset only starts in 2012, I use the ETF Global dataset for

the period starting in 2012 and the CRSP-Thomson Reuters dataset prior to 2012. However,

using the CRSP-Thomson Reuters dataset for the entire sample does not significantly impact

the results. I follow the same approach of constructing the ETF ownership variable for the

period starting in 2012.

Lastly, I combine the ETF Ownership data, institutional ownership data, and the prison

data by matching the datasets on the common firm and year identifiers. This final step

yields a dataset that is at the prison level and contains annual information about a prison’s

population, mortality rates, correctional officers hired, and ownership structure.

2.2 Summary statistics

Table 1 provides the descriptive statistics. Approximately, 13% of the distinct 1,453

distinct prisons (12.2% of prison-year observations) that are included in my sample are man-

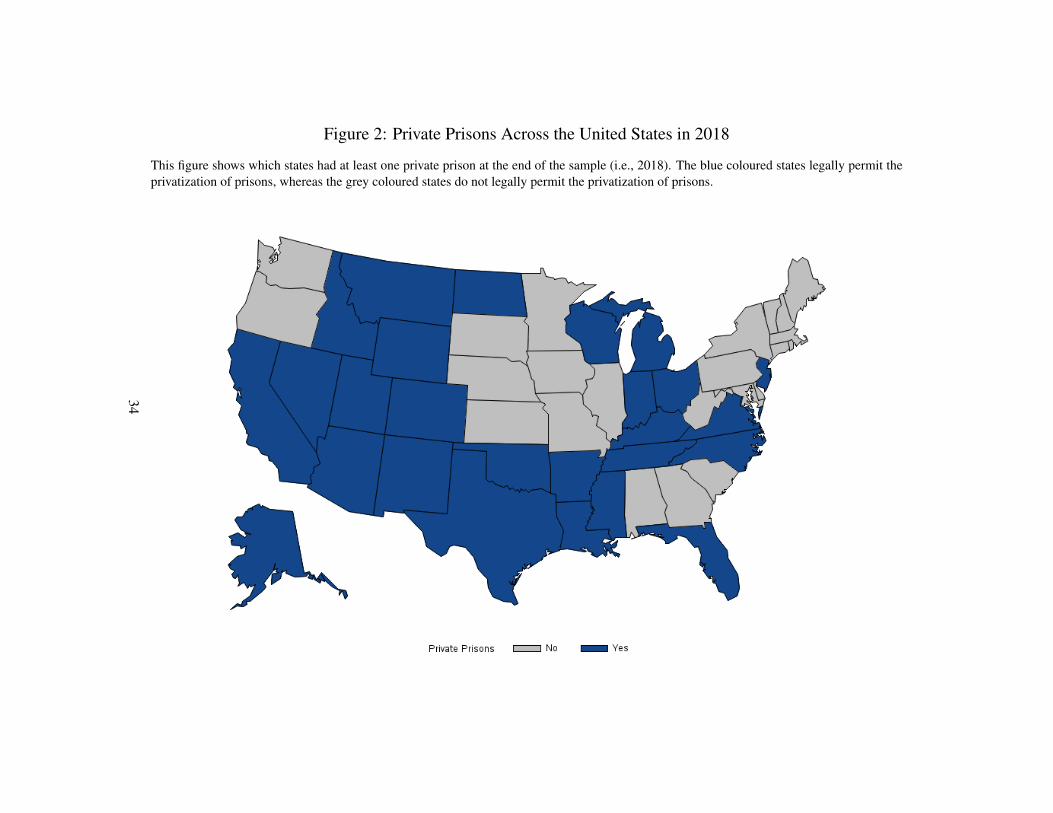

aged by a private enterprise. Figures 1 and 2 also provide some further information on which

states have at least one private prison at the beginning and end of the sample (i.e, 2000 and

2018), respectively. The average long-term and short-term institutional ownership, which

are defined by the quasi-indexers and transient classifications of Bushee (2001), are 0.028

and 0.016, respectively, whereas the ETF ownership is around 0.013. The average number

of total suicides, unexpected deaths, and all types of deaths that occur during a given year

is 0.673, 1.746, and 3.824, respectively. By scaling the mortality numbers with the average

number of inmates housed in the given prison, I construct alternative mortality measures,

such as suicide rates, unexpected death rates, and total death rates. The average suicide

rates, unexpected death rates, and total death rates are 0.001, 0.002, and 0.006, respectively.

10

As well, the average number of programs that are related to suicide-prevention is 4.379,

whereas the average number of programs offered in prisons is 29.977.

Furthermore, there is a significant difference, both economically and statistically, in out-

comes of prisons that are managed by a non-government institution (i.e., private firm) com-

pared to the ones that are managed by the government. For instance, the total number of

suicides, unexpected deaths, and all types of deaths are higher in privately-managed prisons

by 0.436, 0.576, and 1.007, respectively. This implies that an inmate is more likely to commit

suicide if the prisoner is housed in a privately-managed prison. Similar patterns appear with

the mortality rates when one scales the average number of moralities by the average number

of inmates housed in the given prison.

3 Empirical methodology

3.1 Regression specification

As a starting point, I first empirically examine the theoretical prediction of Hart, Shleifer,

and Vishny (1997) that privatization of prisons may lead to a rise in social costs when con-

tracts are incomplete. As in Fisman and Wang (2015, 2017), I use mortality rates as a

proxy for social costs. Although various outcomes may be specified in the contract between

the government and the private enterprise, putting a limitation (i.e., upper bound) on the

number of suicides, unexpected deaths, and total deaths that occur during the given year is

not feasible due to ethical and legal restrictions (i.e., mortality rates are non-contracted out-

comes).12 Therefore, in the main specifications, I use suicides as a proxy for social outcomes

that are difficult to monitor and are not contracted on.

In addition to using alternative empirical models (e.g., poisson models), I regress the

logarithmic transformation of one plus the number of suicides on whether the prison is

12By examining dozens of contracts I was able to obtain, I am able to confirm that there are no specificstatements being made in contracts that put a specific upper bound or a target number on the numberof suicides, unexpected deaths, or total deaths that may occur in prisons. Due to ethical constrains, it isimplausible to put a specific upper limit to suicides or other types of deaths. However, when prisons aremanaged well, the number of suicides is also likely to decrease as a result of improved prison conditions [see,e.g., Cramer et al. (2017); Fazel et al. (2017)]. Furthermore, the definition of suicides and other mortalityrates is the same across all states, making it easier to compare the number of suicides across states.

11

managed by a private entity after controlling for time-invariant heterogeneity at the state-

level as well as year-level, and time-variant prison-level factors that may impact the mortality

rates.13 For instance, one may claim that private prisons ex-ante select inmates who are less

likely to commit suicide. Therefore, following the literature [e.g., Hayes (1995); Fazel et al.

(2017); Cramer et al. (2017)], I control for time-varying factors that represent the overall

prison population type and are relevant to suicides to address possible concerns that a change

in the overall demographics of the prisoner population may drive the results.14 The regression

specification is as follows:

Log(1 + Suicidesi,t) = β0 + β1 1(Privatei,t) + βvXi,t + βwXi + αt + γs + εi,t (3)

where t indexes year, i indexes the given prison, and s indexes the given state. Furthermore,

Xi,t is a vector of relevant control variables that vary overtime for each prison and may

impact mortality rates, whereas Xi is a vector of control variables at the prison-level that do

not vary overtime (e.g., prison security type), but may have an impact on mortality rates.

Year fixed effects are αt, whereas γs are state fixed effects. Given that actual suicide rates

may be incorrectly classified as non-suicide deaths, I use unexpected deaths and total deaths

as alternative dependent variables.

There may, however, still be some unobservable variation at the prison level that drives

some of the results. I, therefore, run a stricter version of the baseline regression by including

prison fixed effects in addition to time fixed effects. This specification captures the within-

prison effects of privatization on suicides. In particular, by including prison fixed effects

one eliminates the time-invariant heterogeneity at the prison-level [following the argument of

Gormley and Matsa (2014)]. Therefore, by taking away the prison-specific effects on inmate

13The reason why I use the logarithmic transformation of one plus the number of suicides rather than thelogarithmic transformation of the number of suicides is due the fact that prisons with no suicides (i.e., zerosuicides) will be automatically dropped out from the regressions since the log of zero is undefined. However,an annual total number of zero suicides does capture relevant information important to the inference I amseeking to draw. Therefore, I use the one plus suicides logarithmic transformation to include such cases.In robustness tests, I also use poisson and negative bionomial regressions that allow me to capture the zerocases without having to do the logarithmic transformation of one plus suicides.

14Inmates are typically assigned to a given prison the judge or the Department of Corrections. In general,a strategic selection of inmates by the prison operator is less likely to occur.

12

mortalities, I run the following fixed effects regressions:

Log(1 + Suicidesi,t) = β0 + β1 1(Privatei,t) + βvXi,t + αt + θi + εi,t (4)

where the notations are the same as in equation (3) and θi are prison fixed effects.

Furthermore, given that prior studies, such as Hart and Zingales (2017) and Benabou

and Tirole (2010), highlight the role of shareholders, such as institutional investors, who

may impact corporate social responsibility outcomes, I take the ownership structure of prison

management companies into account to capture heterogeneity in shareholders’ attentiveness

to social outcomes in prisons. As well, prior studies that examine the consequences of privati-

zation do not take into account the fact that there may be a different impact of privatization

on social outcomes when one takes the ownership structure of the private operator into ac-

count. Therefore, I first examine whether there is a relationship between total institutional

ownership and prison outcomes, and then break down the institutional ownership levels into

more granular levels. In particular, it is possible that certain types of institutional investors

may play an important monitoring role in mitigating the social costs that arise as a result of

prison privatization, which was raised as a possible concern of prison privatization by Hart,

Shleifer, and Vishny (1997).

To capture such heterogeneity in investors’ attentiveness to social outcomes, I first break

down the total institutional ownership levels to ownership by short-term and long-term in-

vestors. Benabou and Tirole (2010) empathize the important role of long-term investors

by stating that corporate social responsibility “is about taking a long-term perspective to

maximizing profits”, and that “socially responsible investors should position themselves as

long-term investors who monitor management and exert voice to correct short-termism.”

In addition, Bushee (2001) provides empirical evidence that there is a positive relationship

between long-term ownership and long-term firm value, whereas there is a positive associ-

ation between short-term ownership and short-term firm value. It is likely that long-term

investors monitor the prison management company to ensure that long-term firm value is

maximized and managers incorporate social outcomes. Failing to incorporate social out-

comes so may impact the renewal of contracts, and therefore impact the long-term value of

13

the firm. Short-term investors are, however, more likely to influence the prison management

company to implement managerial decisions that increase short-term profits, but may not

take into account the long-term consequences of a rise in social costs due to a reduction

in quality. I define long-term versus short-term ownership by following Lan, Moneta, and

Wermers (2019).

Given that holding duration is not randomly assigned, I use a proxy for holding duration.

In particular, I use the quasi-indexer and transient classification as a proxy for long-term

versus short-term ownership, respectively, since Bushee (2001) finds that quasi-indexers have

a short holding horizon, whereas transients have a short holding horizon. For instance, the

annual portfolio turnover of quasi-indexers is 33%, whereas the annual portfolio turnover of

transients is 70%.

To examine the role of institutional investors, I use the same regression specification

as in equations (3) and (4), except that I include variables that captures the variation in

institutional ownership types in the given prison as follows:

Log(1 + Suicidesi,t) = β0 + β1 1(Privatei,t) + β2 Institutional Ownershipi,t

+ βvXi,t + βwXi + αt + γs + εi,t

(5)

where the indexes are the same as in equation (3). Institutional Ownershipi,t is the aver-

age annual total institutional ownership level (or institutional ownership level by type) in

the private operator that manages the given prison. It is also important to note that I in-

clude 1(Privatei,t) in the regressions since there is a difference between non-publicly traded

privately managed prisons that have no institutional ownership and non-privately managed

prisons (i.e., managed by the government) that needs to be controlled for (which cannot be

distinguished when institutional ownership is zero). In robustness tests, I run a similar spec-

ification by only including private prisons (i.e., by excluding all government prisons) since

the baseline results measure both the extensive and intensive margins.

To examine the impact of institutional ownership on prison outcomes after removing any

time-invariant prison-specific unobservables, I run the following regression with prison fixed

14

effects and include the institutional ownership variable(s) as follows:

Log(1 + Suicidesi,t) = β0 + β1 1(Privatei,t) + β2 Institutional Ownershipi,t

+ βvXi,t + θi + αt + εi,t

(6)

where the indexes are the same as in equation (4).

Given that Benabou and Tirole (2010) theoretically predict that long-term investors may

play a more important role in social outcomes compared to other investors, I further examine

whether there are differences in the attentiveness to social outcomes among long-term investor

types. I break down the long-term institutional ownership levels into more granular investor

types, such as ownership by pension fund or independent investment advisor. Lastly, as I

describe in the next section, since my identifications strategy relies on the exogenous change

in ETF ownership, I run the same regressions of (5) and (6) using ETF ownership levels to

provide the uninstrumented baseline results for comparison.

Similarly, in the robustness test section, I follow the same regression specification as in

equations (5) and (6) when examining the effects of various ownership types on alternative

social outcome variables, such as the total number of rehabilitation programs offered in a

given prison during a given year, correctional officer hired per inmate, or overcrowding in the

prison. I do not re-write the specifications since they are identical to the ones from before

except that I use the aforementioned variables as alternative dependent variables to measure

the overall prison conditions.

3.2 Identification strategy

Identifying the causal effect of long-term institutional ownership on prison outcomes

comes with an empirical challenge. Without an identification strategy, one may not be able

to examine the causal relationship between institutional ownership and social outcomes in

prisons. There are two reasons that may lead to biased results. First, institutional investors

may be self-selecting into prison management companies that run prisons in an ethical man-

ner. Therefore, the relationship between ownership and prison outcomes may be driven by a

self-selection of institutional investors who are able to pick stocks well. Second, there may be

15

an omitted time-varying factor that is correlated with both long-term institutional ownership

and prison outcomes. Not including such an omitted factor may also lead to biased results.

To overcome this empirical challenge, I develop a new identification strategy that ex-

ogenously increased the long-term ownership levels in public companies that manage pris-

ons.15 At the end of 2012, the publicly-traded private prison management companies were

re-classified by the Internal Revenue Agency (IRS) as Real Estate Investment Trusts (REITs)

due to the fact that these private prison management companies were managing and owning

real estates (i.e., the prison facilities).16 The reclassification of private prison management

companies as REITs led to a sudden increase of the ETF ownership levels. This increase

was due to the fact that the publicly-traded prison management companies were included

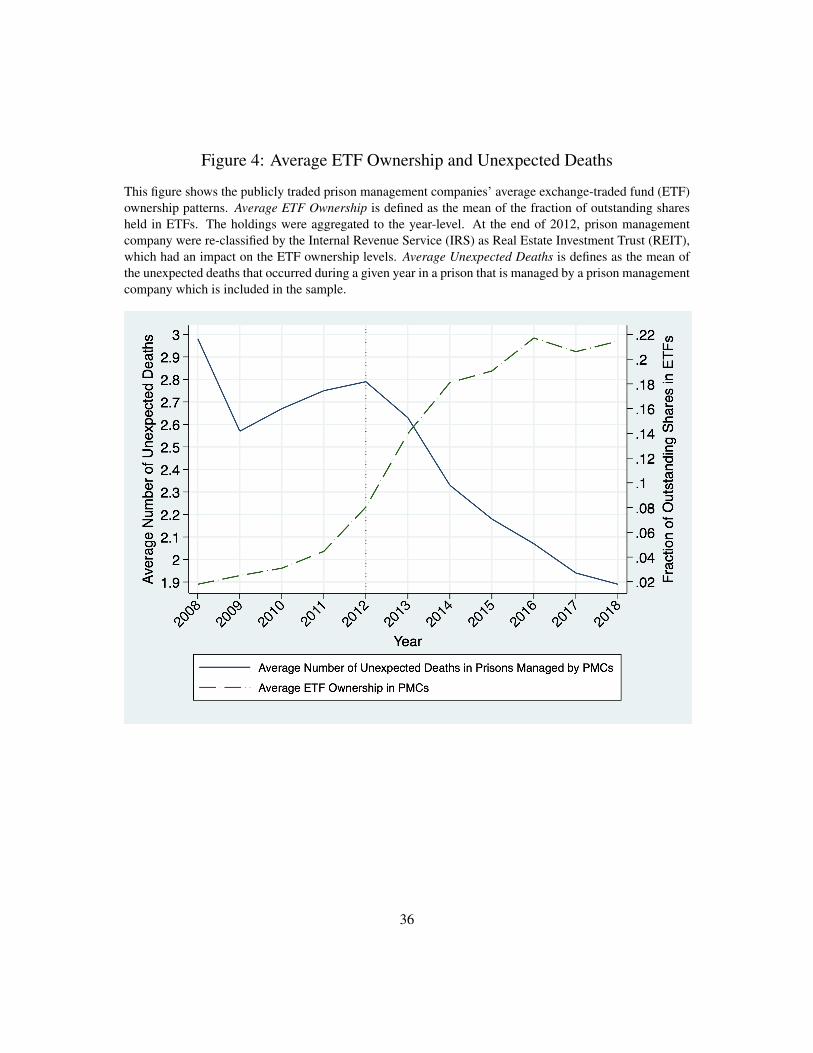

in ETF that track the real estate industry. Figures 3, 4, and 5 plot ETF ownership levels

and average suicides, unexpected deaths, and suicide rates, respectively. Figures 7 plots the

ETF ownership of prison stocks and non-prison stocks around the REIT reclassification to

illustrate that the sudden increase in ETF ownership levels during the post-2012 period oc-

cur only in prison management companies. These figures show that there was a significant

increase in ETF ownership after the reclassification.

In order to draw a causal link between long-term ownership and social outcomes in pris-

ons, I use the REIT reclassification as an exogenous shock to long-term ownership in prisons

managed by public companies. The reason why this shock is a plausible and reliable identi-

fication strategy is due to the following reason. It is unlikely that the IRS reclassified prison

management companies with the intention to have a positive impact on prison outcomes,

but rather the improved prison conditions are more likely due to the exogenous increase in

long-term institutional ownership levels in public prison management companies (i.e., due to

the monitoring role of long-term investors). The exclusion restriction, therefore, is likely to

be met.

To examine the relevance condition, I analyze whether there is an increase in ETF own-

ership in the treated group due to the REIT reclassification. The treated group contains

15To the best of my knowledge, there are no prior studies that use the REIT reclassification of prisonmanagement companies that are publicly traded as an instrument for ETF ownership.

16See the Forbes article titled “Why Would A Prison Corporation Restructure As A Real Estate Company?”written by Matt Stroud in January 2013 for a discussion of this reclassification.

16

the set of prisons that are managed by a public prison management company prior to the

REIT reclassification of the given public company (i.e., all prisons that are impacted by this

exogenous shock), whereas the control group contains the remaining set of prisons (i.e., all

other prisons that are not managed by publicly-traded companies, and hence not impacted

by the REIT reclassification).17

In particular, I instrument ETF ownership by the treatment effect. The strictest fixed

effects version of the first-stage regression of the instrumental variable approach is as follows:

ETF Ownershipi,t = β0 + β1 1(Treatedi) × 1(Postt) + β2 1(Postt)

+ β3 1(Privatei,t) + βvXi,t + θi + εi,t

(7)

where t indexes year and i indexes the given prison, whereas Xi,t is a vector of relevant

time-varying prison-level control variables that may impact mortality rates and θi represent

prison fixed effects. Since I include prison fixed effects, the treated binary variable cannot

be separately estimated.

After estimating the first-stage regression, I use the estimated values of ETF ownership

in the second-stage regression. In particular, I run the following regression specification:

Log(1 + Suicidesi,t) = β0 + β1 ETF Ownershipi,t + β2 1(Postt)

+ β3 1(Privatei,t) + βvXi,t + θi + εi,t

(8)

where the notations and control variables are the same ones as in the first-stage regression.

4 Results

4.1 Negative consequences of privatization on society

In this section, I explore the relationship between prison privatization and social out-

comes. By controlling for an increasingly demanding set of fixed effects, I first examine the

relationship between privatization and suicides in Table 3. Consistent with the theoretical

17The treated prisons have a non-zero ETF ownership level prior to the REIT reclassification, but the ETFownership levels in these prisons doubles during the post-period due to the exogenous shock.

17

prediction of Hart, Shleifer, and Vishny (1997) that prison privatization may lead to poor

prison conditions due to incomplete contracts (i.e., mortality is difficult to contract on), I

find that there is a positive association between prison privatization and suicides.

The point estimates are statistically significant in each specification at the 1% level and

range from 0.276 to 0.387. Although the economic magnitudes are large in general, the

effects are especially stronger when prison fixed effects are included [i.e., columns (3) and

(6)]. This suggests that the impact of privatization on suicides is much larger when there

is a switch of management from the government to the private entity (or vice versa). As

well, the coefficients of the control variables are also consistent with prior studies [e.g., Hayes

(1995); Fazel et al. (2017); Cramer et al. (2017)]. It is also important to note that the

binary variables that measure the prison security types, which are time-invariant, cannot be

separately estimated in column 6 since I include prison fixed effects.

4.2 Institutional investors mitigate the negative consequences of

privatization

Although privatization leads to negative social outcomes in prisons, the ownership struc-

ture of the private enterprise may matter given that the owners of the private enterprise

have the residual right to make decisions on the non-contracted dimensions (i.e., social out-

comes) [Hart, Shleifer, and Vishny (1997)]. Benabou and Tirole (2010) and Hart and Zingales

(2017) highlight the importance of shareholders in social outcomes. In addition, prior em-

pirical studies, such as Dyck et al. (2019), find a positive association between institutional

ownership and corporate social responsibility outcomes. Therefore, to examine the role of

institutional investors when social costs arise due to privatization, I first take into account

the public ownership structure of the prison management company.

In Table 4, I document results that are consistent with the theoretical predictions of

Benabou and Tirole (2010) and Hart and Zingales (2017). In particular, there is a negative

relationship between total institutional ownership and social costs, suggesting that the neg-

ative consequences of privatization may be partially mitigated by an increase in institutional

ownership levels. The point estimates of total institutional ownership in Table 4 range be-

18

tween -0.010 and -0.012 where all of the point estimates are statistically significant at the 1%

level. It is also worthwhile to note that the point estimates are the largest when prison fixed

effects are included, suggesting that the results are primarily driven by prisons that had a

switch of management (i.e., from government to private or vice versa).

4.3 The role of long-term versus short-term investors

Benabou and Tirole (2010) raise the importance of long-term investors in corporate so-

cial responsibility outcomes by stating that “socially responsible investors should position

themselves as long-term investors who monitor management and exert voice to correct short-

termism.” To examine whether the role of long-term versus short-term investors is different

in regard to mitigating the negative consequences of privatization, I further break down total

institutional ownership to ownership by long-term versus short-term institutional investors.

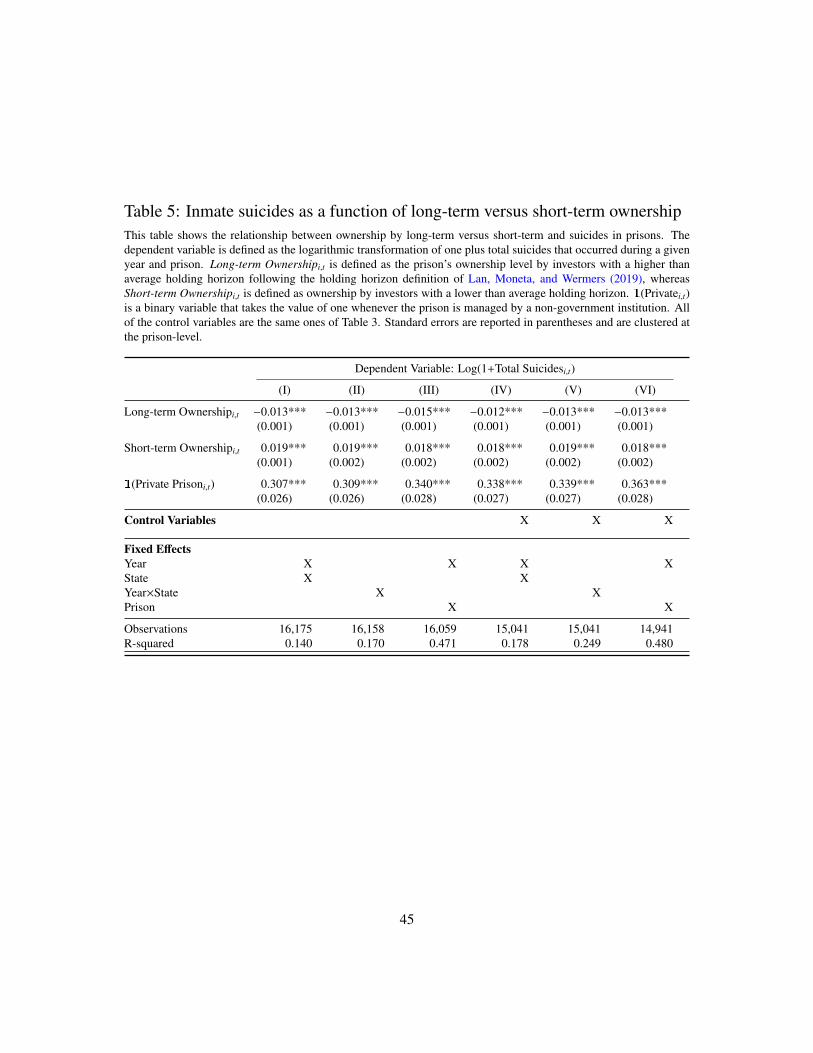

In Table 5, I first use the holding duration measure of Lan, Moneta, and Wermers (2019) to

identify long-term versus short-term institutional investors. Given that holding duration is

not randomly assigned to investors, I use an alternative proxy that does not solely rely on

holding duration to identify long-term versus short-term investors.

In particular, the quasi-indexers and transient investors classification of Bushee (2001)

takes holding duration and investment style into account. It is a good proxy for long-term

versus short-term ownership since the annual portfolio turnovers of quasi-indexers is 33%,

whereas the turnover of transient institutional investors is 70%. As well, Bushee (2001) also

provides empirical evidence that there is a positive relationship between ownership by quasi-

indexers and long-term firm value. This is consistent with the fact that quasi-indexers have

a longer holding horizon and have to hold the given firm in its portfolio due to, for instance,

indexing. Hence, it is likely that quasi-indexers will monitor the prison management company

to ensure that long-term firm value is maximized that may also incorporate social outcomes

[since doing so positively impacts the value of assets under management, as raised by Appel,

Gormley, and Keim (2016, 2018)]. This is also consistent with the theoretical predictions

of Benabou and Tirole (2010). Furthermore, transient investors who have a short holding

horizon are more likely to influence the prison management company to implement decisions

that increase short-term profits, but may not have an incentive to take into account the

19

long-term consequences of a rise in social costs.

Consistent with this argument, I document in Tables 5 and 6 that the positive role

of institutional investors in mitigating negative consequences of privatization is primarily

driven by long-term institutional investors. In fact, there is a positive association between

ownership by short-term investors and suicides, suggesting that short-term investors do not

pay much attention to social outcomes (i.e., human costs of short-termism). In particular, in

Table 5, the point estimates of ownership by long-term investors range between -0.012 and

-0.015, whereas the point estimates of short-term ownership range between 0.018 and 0.019.

I document similar results in Table 6 when I use the alternative proxy for long-term versus

short-term ownership levels. Specifically, in Table 6, the point estimates, which are significant

at the 1% significance level, of quasi-indexer (transient) ownership range between -0.025 and

-0.027 (0.012 and 0.015) with the point estimates being the strongest in the within-prison

tests.

These results suggest that holding duration plays an important role in social outcomes.

Lastly, to examine what fraction of the social costs that arise due to privatization are miti-

gated by institutional investors, in Figure 8, I provide the total effects of institutional own-

ership types on suicide rates. On average, institutional investors offset approximately one

third of the social costs that arise as a result of privatizing prisons.

4.4 Heterogeneity of effects across institutional investor types

In this section, I examine whether the type of long-term investor matters for social out-

comes. By making use of the granular investor types provided by Bushee (2001), I document

that the mitigation of negative consequences by long-term institutional investors also varies

by investor types. Bushee (2001) documents that there is a strong positive association be-

tween ownership by independent investment advisors and companies, such as mutual funds,

and long-term firm value. It is likely that these types of investors may be more attentive to

social outcomes given the theoretical predictions of Benabou and Tirole (2010) that long-term

investors may drive corporate social responsibility outcomes.

In Table 7, I provide empirical evidence that long-term independent investment advisors

and companies play the most important role in mitigating the social negative consequences

20

of privatization. The point estimates of the independent investment advisors (companies)

ranges between -0.078 and -0.092 (-0.044 to -0.052) with all being significant at the 1% level.

Ownership by pension funds does not have a large impact on suicides given the small point

estimates (possibly due to the fact that there is not high ownership by these investors due

to public pressure to divest from prison stocks). However, it is important to note that there

is a negative, although small, association between pension fund ownership and suicides.

Given that in the next section I will present the results of an instrumental variable test

that relies on exogenous variation in ETF ownership in prison management companies, I

provide next the uninstrumented results of the relationship between ETF ownership and sui-

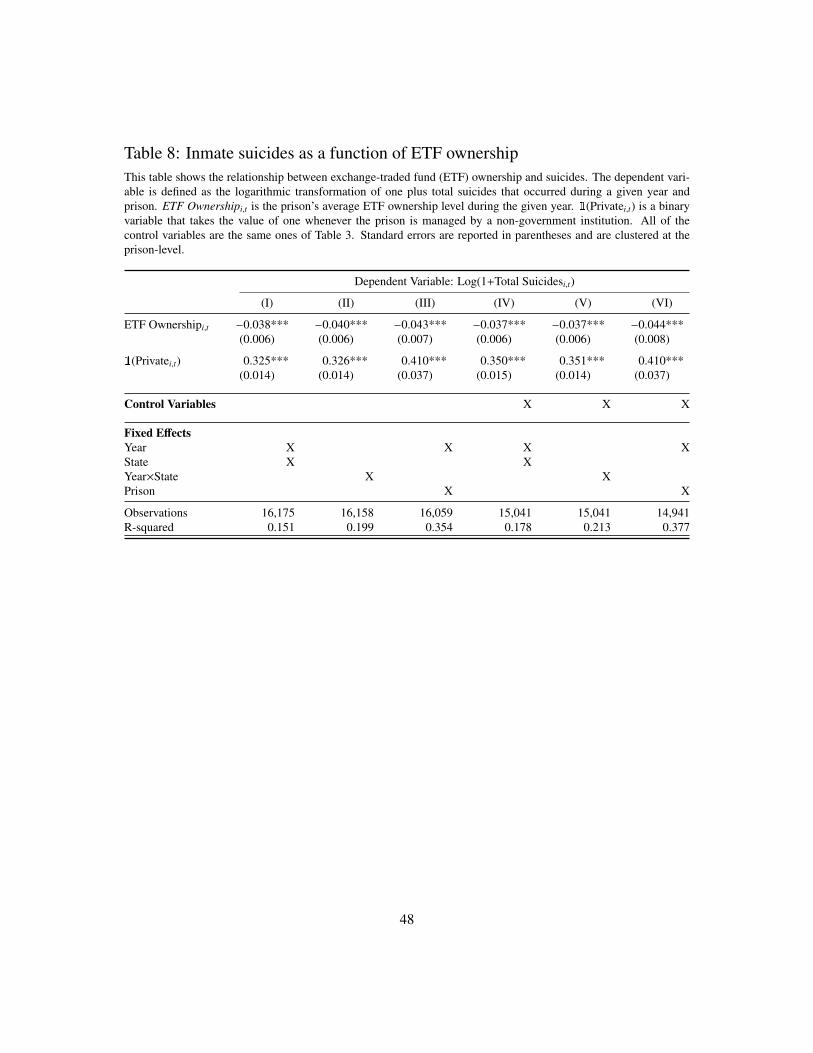

cides. In Table 8, I document that there is a negative relationship between ETF ownership

and suicides in prisons. This is consistent with the prior finding that long-term independent

investment advisors and companies, such as mutual funds, play an important role in miti-

gating the negative consequences of privatization. In particular, the point estimates of ETF

ownership range between -0.038 and -0.044 with the point estimates being the strongest in

the within-prison analysis.

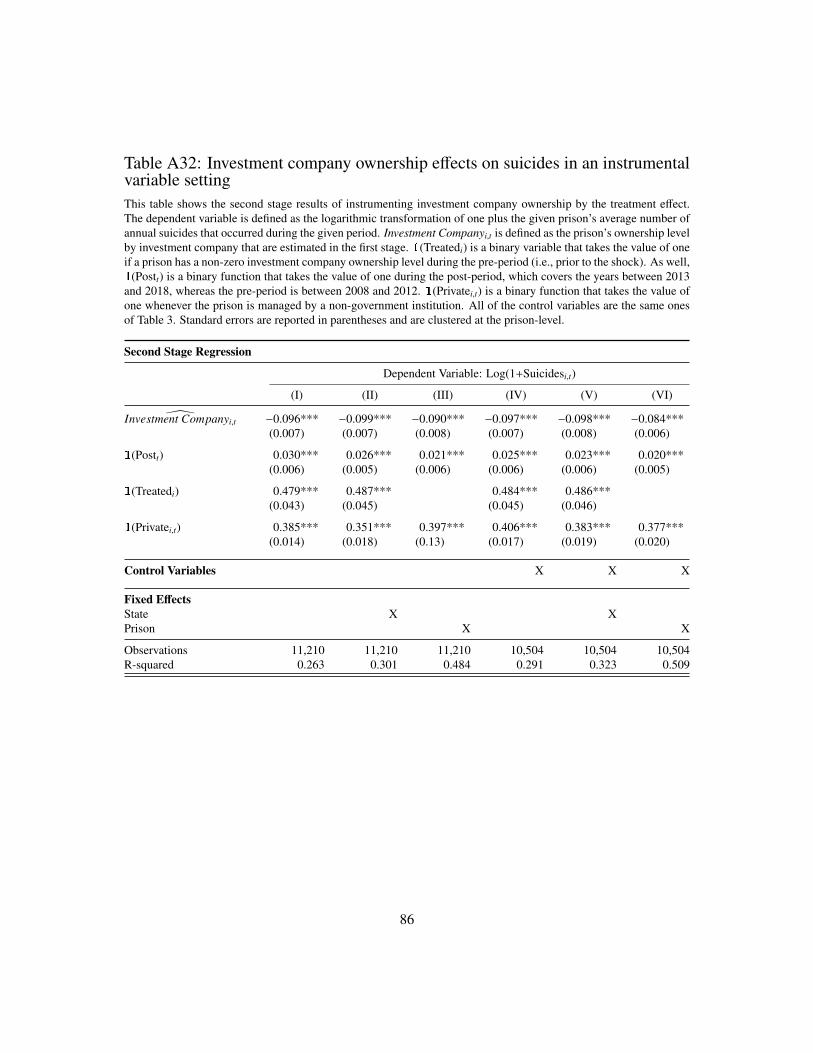

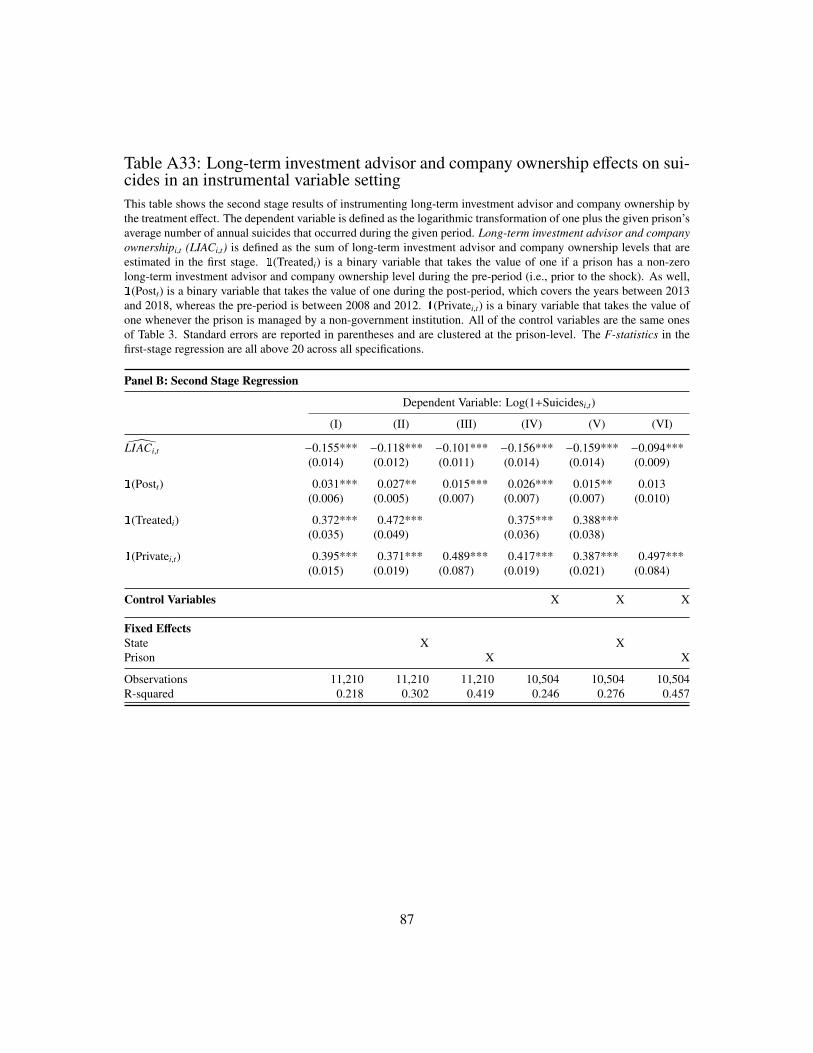

4.5 Instrumental Variable Approach

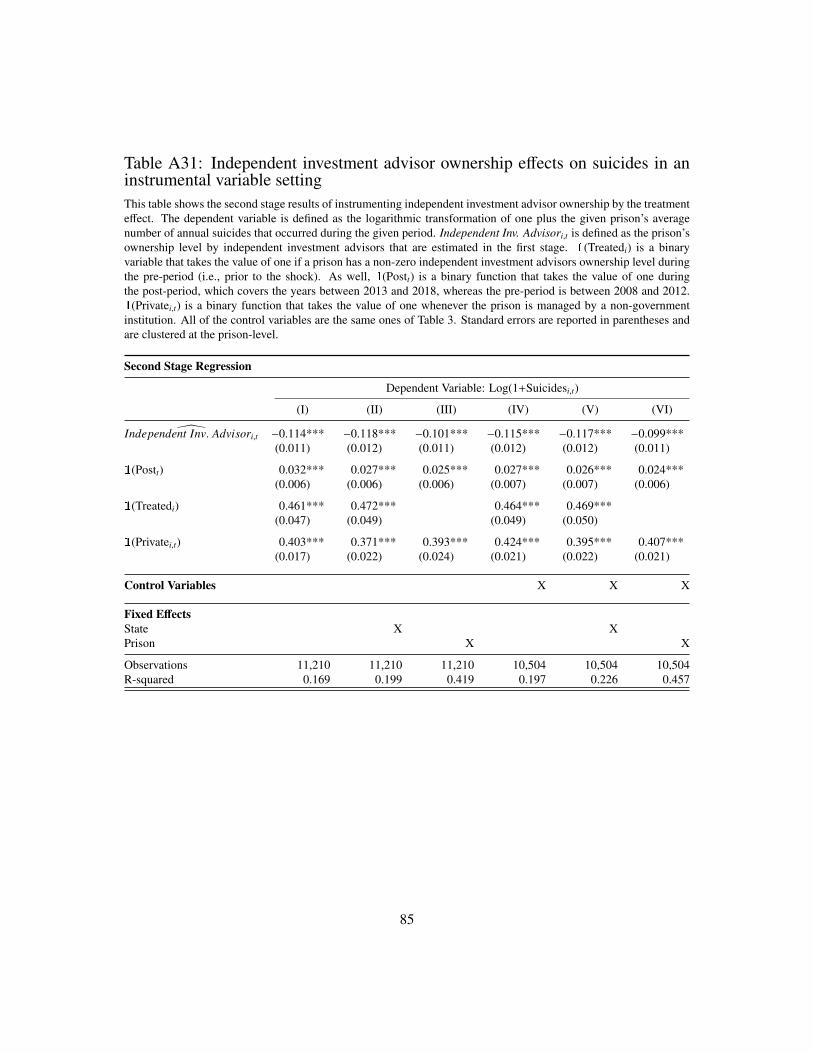

In this section, by using a novel identification strategy, I study the causal relationship

between long-term ownership and suicides. In particular, to examine the causal relation-

ship between ETF ownership and suicides, I instrument the ETF ownership levels by the

treatment effect using an instrumental variable approach. The first-stage regression results

are provided in Table 9, Panel A. The point estimates of the treatment effect are statisti-

cally significant at the 1% level across all specifications. The economic magnitudes are also

large, ranging from 7.578 to 7.626. The first-stage F-statistics on the instrument is also

large (much larger than the conventional benchmark of 10), suggesting that the relevance

condition is met.

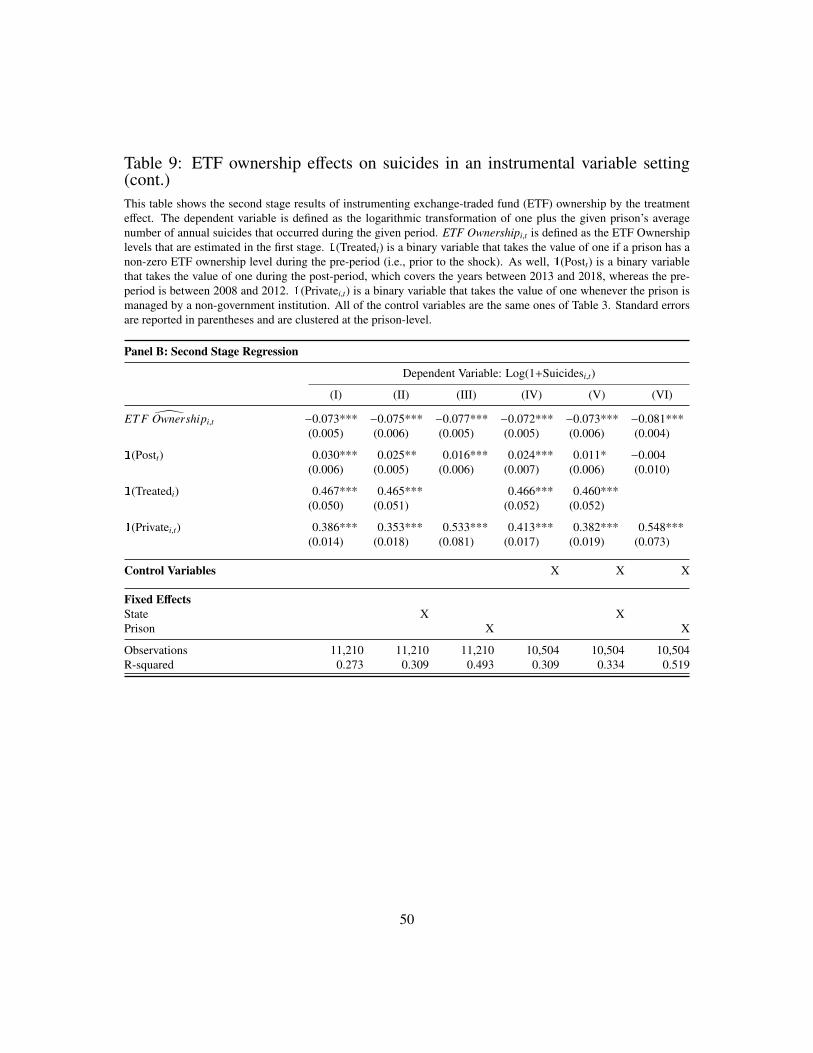

Furthermore, Table 9, Panel B provides the estimates of the second-stage regression. The

point estimates are between -0.072% and -0.081%, suggesting that a one percent increase in

ETF ownership reduces the average number of suicides by 7.2% to 8.1%. The magnitudes

are also the largest when prison fixed effects are included. As well, all of the point estimates

21

are statistically significant at the 1% level across all specifications. It is also important to

note that the prison fixed effects absorb the treated binary variable.

Lastly, the point estimates of the second-stage of the instrumental variable approach are

comparable to the point estimates in the baseline results provided in Table 8. Jiang (2017)

states that the economic magnitudes of the instrumental variable estimates of 255 articles

published in leading finance journals is, on average, 9.2 times larger than the magnitudes of

the OLS estimates. The magnitudes in the instrumental variable estimates reported in Table

9, Panel B are only around 1.8 times larger than the magnitudes of the OLS estimates.

5 The Mechanism

In this section, I examine why institutional investors may have an incentive to monitor

prison management firms that are held in their portfolios. In particular, I analyze a possible

channel that may provide a rational explanation on why an increase in the institutional

ownership leads to improvements in the social outcomes of prisons (e.g., reduction in suicides).

Prior studies, such as Arena and Julio (2015), provide empirical evidence that litigation

risk impacts corporate decisions. As well, corporate litigation is costly to firms both from a

valuation and reputation perspective.18 Until Congress passed the Prison Litigation Reform

Act in 1996, the high number of lawsuits against prisons, mostly based on frivolous reasons,

created a crisis in the federal court system [Belbot (2004)]. To resolve this crisis, Congress

engaged in legislative action to make it more challenging (e.g., by increasing administrative

fees) for inmates to sue for irrelevant cases (e.g., the famous case of an inmate filing a lawsuit

for not getting “peanut butter” in prison).19 The lawsuits that have been filed post-1996,

therefore, are more likely to be based on a legitimate reasons, such as poor prison conditions.

Given the endogenous nature of lawsuits (e.g., omitted variable bias), I use a proxy for

litigation risk following Colonnello and Herpfer (2019). The U.S. Chamber Institute for Legal

18Large shareholders of private prison management companies, such as BlackRock and Vanguard, are oftenmentioned in newspapers when the given private enterprise fails to provide humane conditions to inmates.For instance, see the Financial Times article titled “US investors confront home truths about private prisonholdings” published on Feb 26, 2020.

19For more details, see the statement regarding the “Peanut Butter Case” that Senator Dole raises regardingfrivolous prisoner-brought lawsuits in 141 Cong. Rec. S14413 (September 27, 1995).

22

Reform published an annual ranking of state courts in regard to the friendliness of the given

state’s law system to corporations [for more details, see Colonnello and Herpfer (2019)].

I use the ranking provided by the U.S. Chamber Institute for Legal Reform to examine

whether the relationship between institutional ownership and social outcomes are stronger

for prisons that are located in more corporation unfriendly states (i.e., plaintiff friendly

states). The reason of using such a proxy is due to the fact that if a prison is located in a

state in which it is easier to sue corporations, prisoners or their families are more likely to sue

prison management companies for poor prison conditions or negligence by management that

contributed to the success of a suicide. To avoid costly settlements, therefore, institutional

investors have an incentive to monitor private prison management companies to ensure that

management does not cut on important costs that negatively impact prison conditions and

increase the probability of being sued.

As well, institutional investors are more likely to be attentive to social outcomes if prisons

harm the reputation of the institution, and have an indirect impact on fund flows. Various

social advocacy groups, for instance, urge citizens to contact institutional investors that

manage their retirement plans to be more socially responsible with their prison investments.

If institutional investors are not socially responsible, these advocacy groups urge that citizens

should opt to different providers. Such calls typically rise when there are lawsuits against

prisons. Hence, if institutional investors indeed partially offset the social costs of prison

privatization, they are more likely to act when there are higher litigation risks.

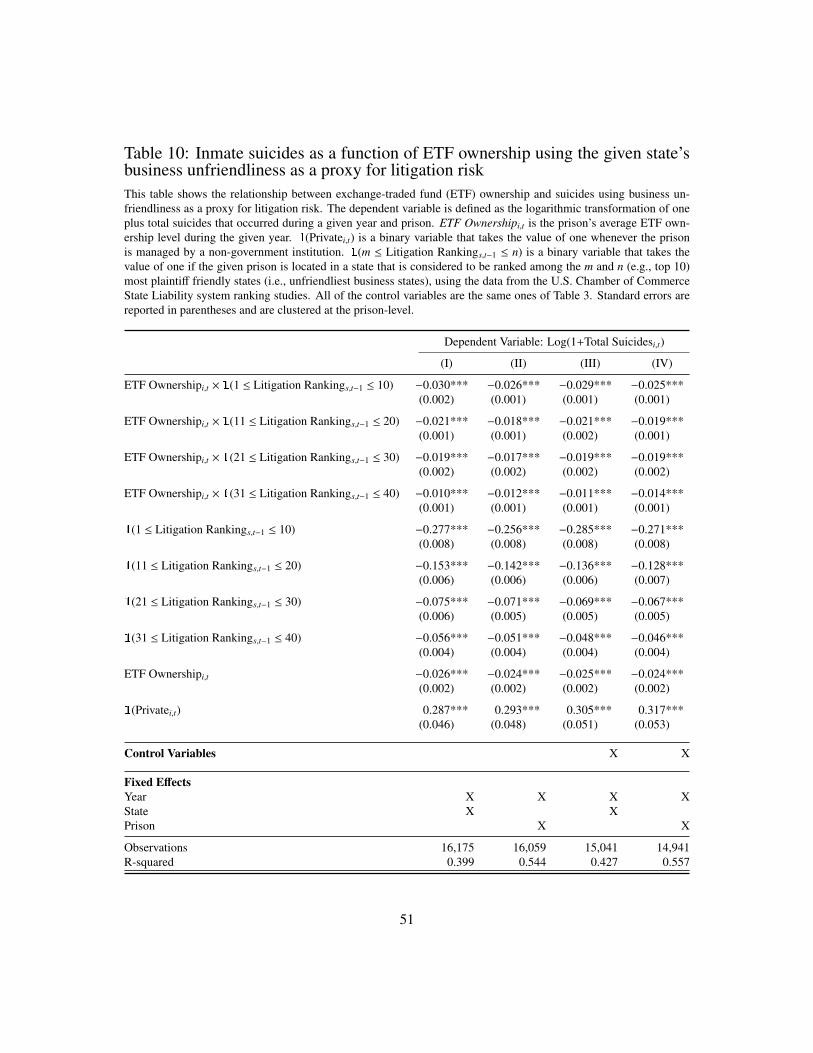

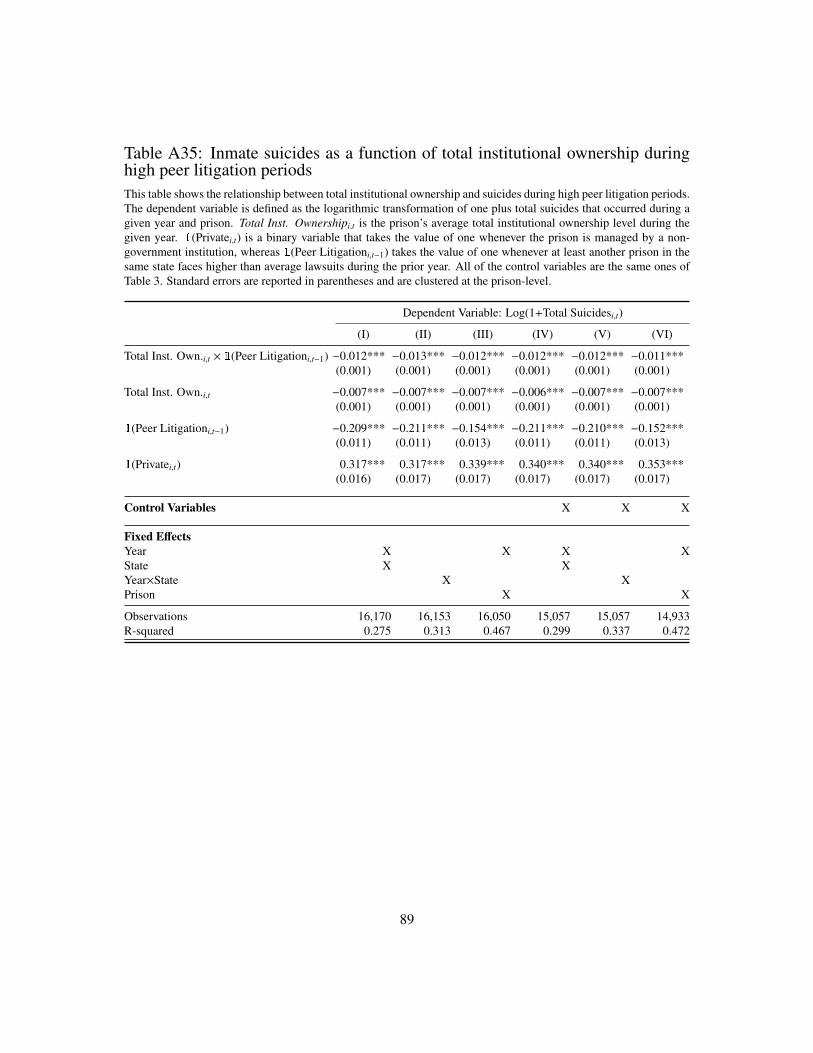

Using the litigation proxy, in Table 10, I document that the association between suicides

and long-term ownership, proxied by ETF ownership, is stronger for prisons that are located

in more plaintiff friendly (i.e., business unfriendly) states. The relationship is monotonically

stronger with the litigation ranking. For instance, the point estimates of the interaction term

between ETF ownership and the top 10 most friendly plaintiff state range between -0.025

and -0.030, whereas the interaction between the next highest ranked states (i.e., 11 to 20)

have point estimates ranging between -0.018 and -0.021. As well, I do not include state times

year fixed effects since the litigation ranking is at the state-year level.

Given that the litigation and reputation risk results make use of endogenous ownership

levels, I use the REIT reclassification as an exogenous source of variation in long-term own-

23

ership levels and interact it with the 2012 state litigation rankings. It is unlikely that the

litigation risk proxies are impacted by the REIT reclassification in 2012 since this ownership

shock is completely unrelated to a state’s litigation ranking (i.e., rankings are orthogonal to

the ownership shock). I use an instrumental variable approach by interacting the ETF own-

ership levels with the litigation rankings in 2012 (i.e., pre-period). In particular, in the first

stage regressions, I use the interaction between treatment (as defined before) and the given

ranking quartile (e.g., top 10) as an instrument for the interaction between ETF ownership

and the given ranking quartile. Each of the five first stage regressions have a F-Statistics

greater than 10 across all specifications.

Table 11 presents the second-stage results in which I use the predicted values from the

five first stage regressions in lieu of the interaction between ETF ownership and the litigation

ranking quartilem. The point estimates of the interaction term are monotonically increasing

in the ranking score quartile and the point estimates are two times of magnitude of the

uninstrumented point estimates. These results suggest that the long-term ownership effects

on suicides are much stronger for prisons that are located in states that have a judiciary

system which is more friendly to plaintiffs. In particular, prisons in such states are more

likely to be successfully sued for negligence by management that contributes to the given

inmate committing suicide. Hence, the monitoring effects are larger in such states given that

there is a higher potential monetary and reputation cost. As in Arena and Julio (2015), I

also use an alternative proxy for litigation risk, peer prison litigation, and document similar

results. The findings are provided in Tables A35 and A36 of the Appendix.

6 Robustness

I perform a variety of additional robustness checks for the baseline specification. For

instance, one may be concerned that actual suicides are misclassified as non-suicides. Instead

of using the total number of suicides, I use different dependent variables. In particular, I

use unexpected deaths, which is defined as the sum of the number of suicides, homicides,

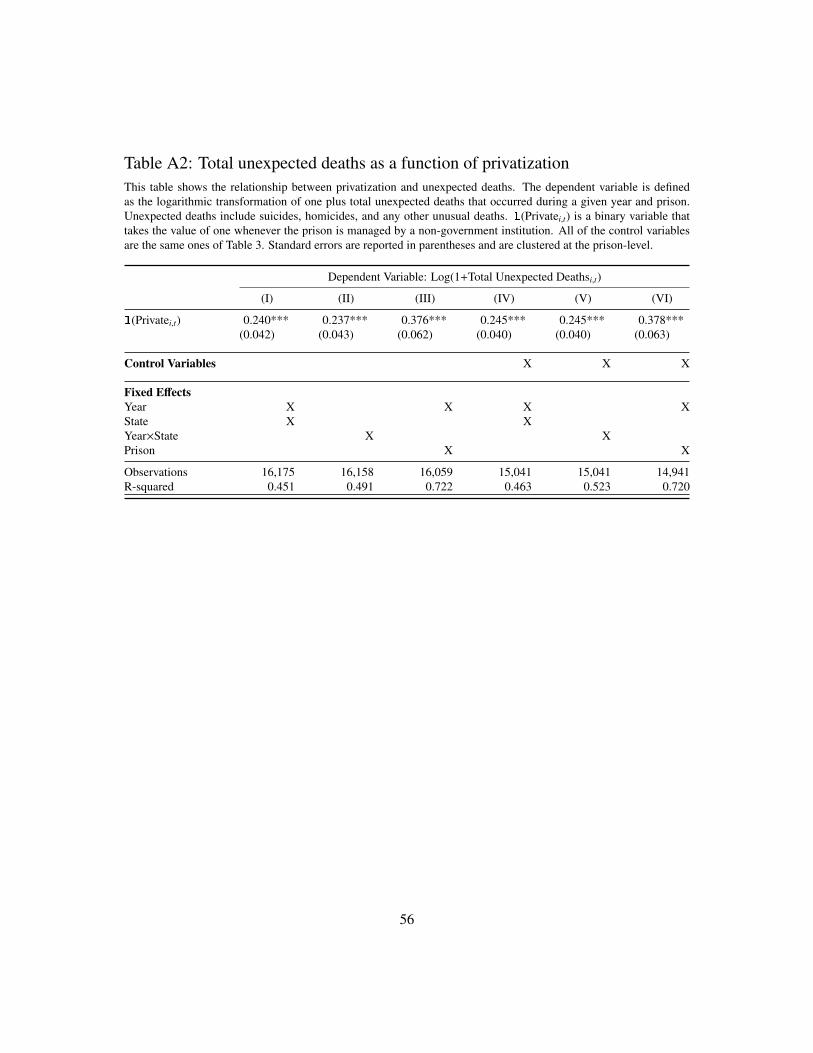

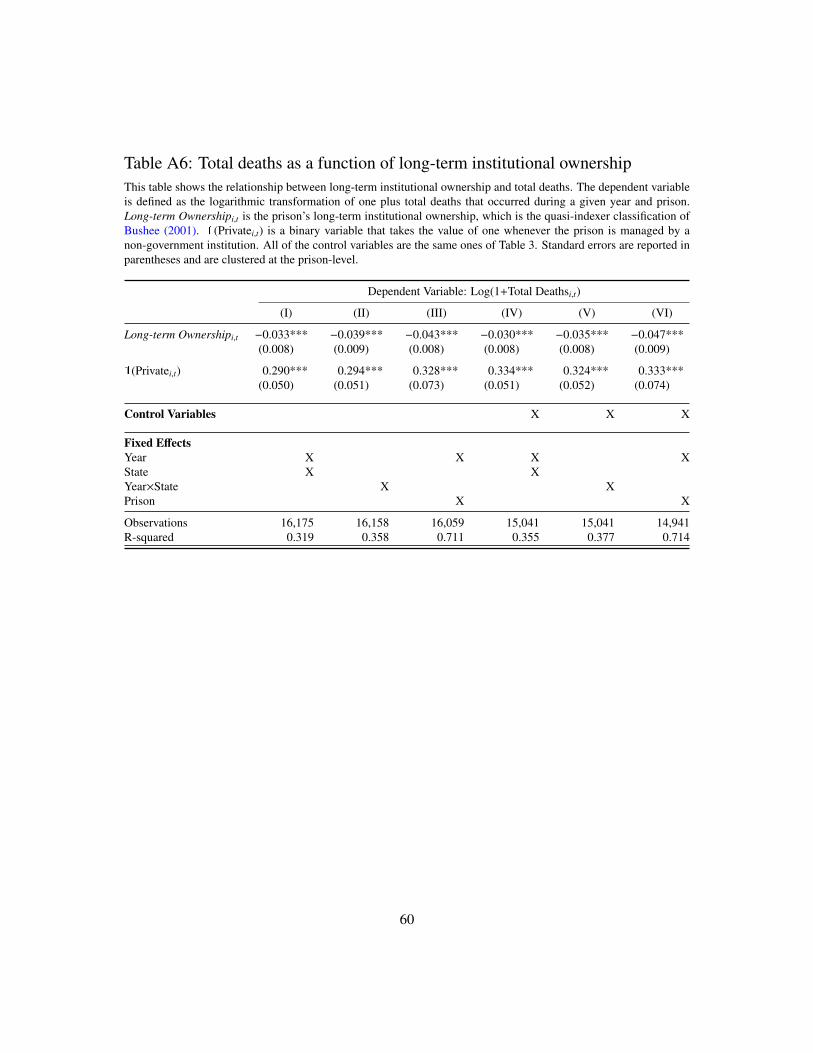

accidents, and unnatural deaths, and also total deaths as dependent variables. Tables A2

to A7 of the Appendix provide the results of using alternative definitions of mortality. The

24

results are similar to the ones reported in the main tables.

As well, since the total number of suicides may be correlated with the average number of

inmates housed in a given prison, I use an alternative definition of suicides. Specifically, in

Tables A8 to A10 of the Appendix, the dependent variable is suicide rates, which is defined

as total suicides scaled by the average number of inmates housed in the given prison during

the given year. The results are similar to the baseline results of Tables 3 to 8.

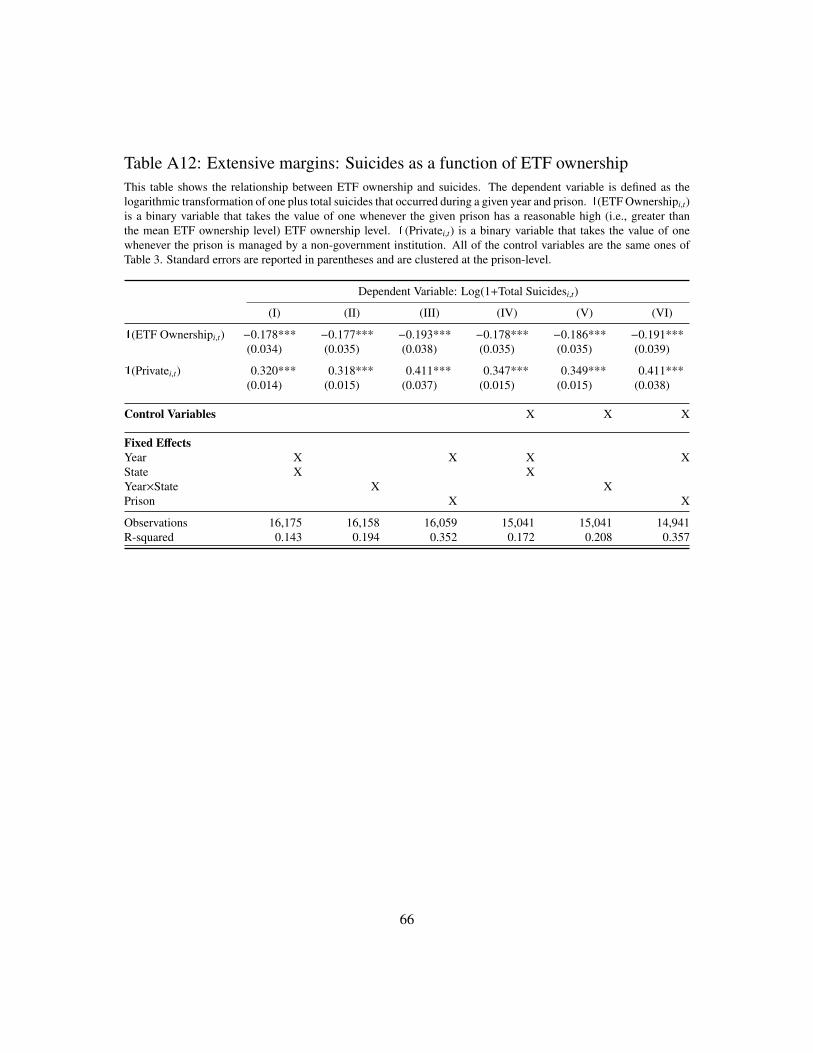

Furthermore, Tables A11 and A12 of the Appendix provides the extensive margin of

long-term ownership and ETF ownership on suicides. In other words, this table examines

the association between having at least some long-term ownership and ETF ownership on

suicides. In Table A11 of the Appendix, the point estimates of long-term ownership effects

range from -0.183 to -0.197, whereas in Table A12 of the Appendix, the point estimates

of ETF ownership range from -0.177 to -0.193. All of the point estimates are statistically

significant at the 1%.

I also use a variety of other outcomes variables that measure the prison conditions. In

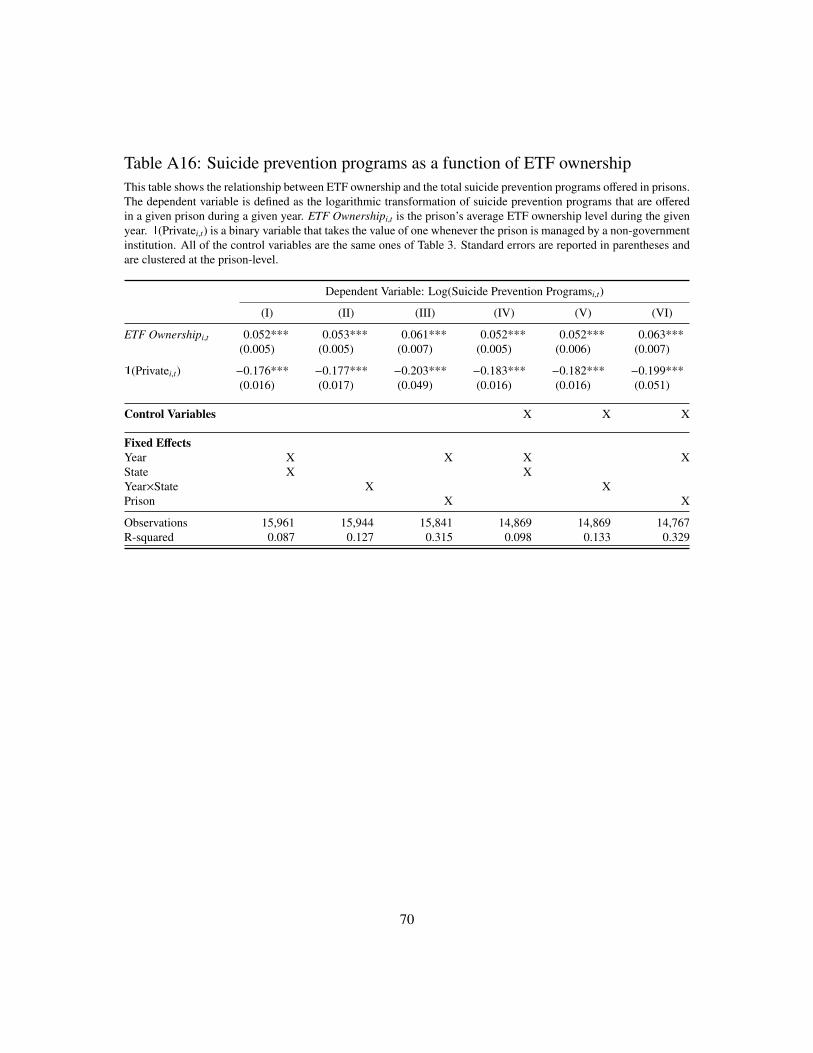

Tables A15 and A16 of the Appendix, I use suicide prevention programs, whereas in Tables

A17 and A18, I use the total number of rehabilitation programs offered in prisons. I find

similar results as the baseline findings that long-term ownership and ETF ownership leads

to improvements in prison conditions. I also use an overcrowding outcome variable in Tables

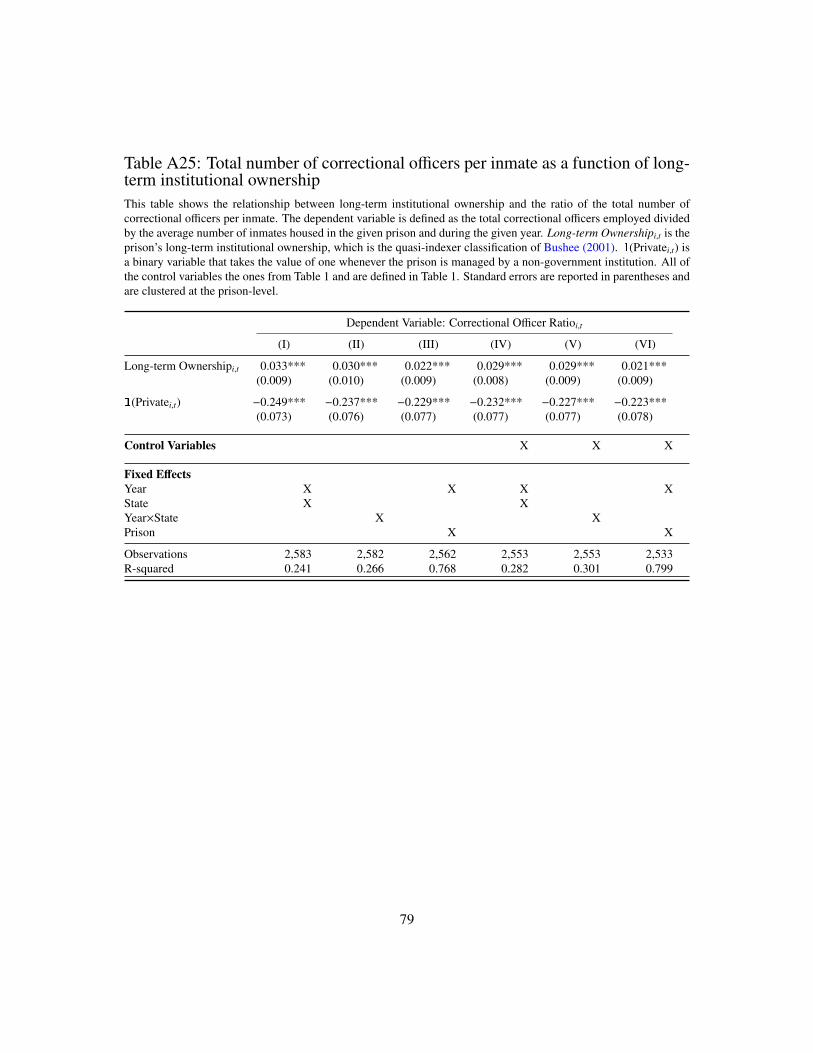

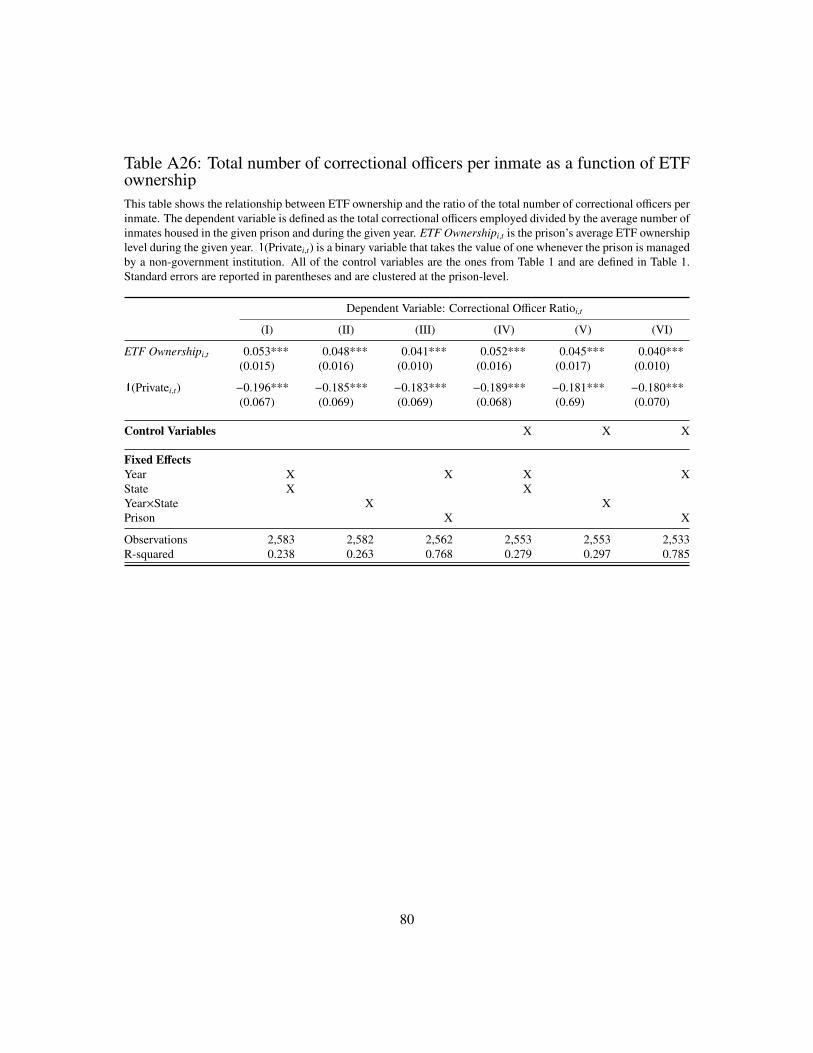

A23, A24, and A27, and use total number of correctional officers hired per inmate in Tables

A25, A26, and A28. Moreover, when I break down long-term ownership and use alternative

outcome variables in Tables A29 to A33, I obtain similar results as the main results that

long-term investment advisors and companies have the strongest positive effects on prison

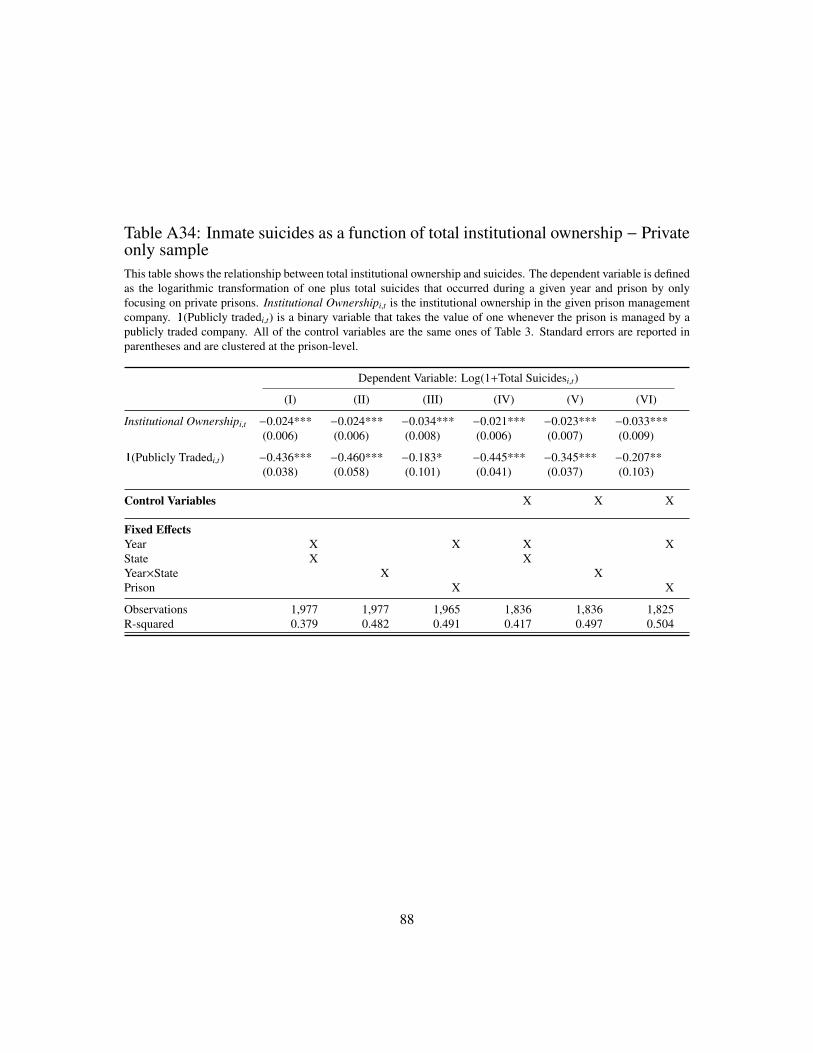

outcomes. In Table A34, I examine whether the baseline results are robust to excluding the

prisons managed by the government. I document similar results as the baseline findings.

Lastly, I use a Poisson model to estimate the baseline tests. Tables A19 and A20 of the

Appendix are comparable to Tables A5 and A8, respectively, except that I use a Poisson

model rather than an OLS model given the count nature of the dependent variable. In Table

19, the incidental-rate ratios of long-term ownership range between 0.953 and 0.960. An

incidental-rate ratio below one represents a negative relationship between the given indepen-

dent variable and dependent variable. The unreported point estimates of the Poisson (i.e.,

25

the natural logarithmic transformations of the incidental-rate ratios) are similar to the point

estimates of Table 5. The point estimates of Table A20 are also similar to the ones reported

in Table 8.

Similarly, to determine whether a standard Poisson model or a zero-inflated Poisson model

is more appropriate, in unreported tests I compared the Akaike information criterion (AIC)

and Bayesian information criterion (BIC) of the estimations. The standard Poisson model

appears to be the more appropriate model (since both the AIC and BIC are smaller). I

also examined whether there was over dispersion (or under dispersion) since a Poisson would

not be appropriate in such a case, and compared the goodness of fit of Poisson model to

the negative binomial model (another alternative model that works better when there is

dispersion). Again, the standard Poisson model appears to be the better model. Given the

similar point estimates of the Poisson model and baseline results (in regard to economic

magnitudes and statistical significance), therefore, the choice of the empirical model does

not drive the results. Lastly, to ensure that my model estimates are robust given there are

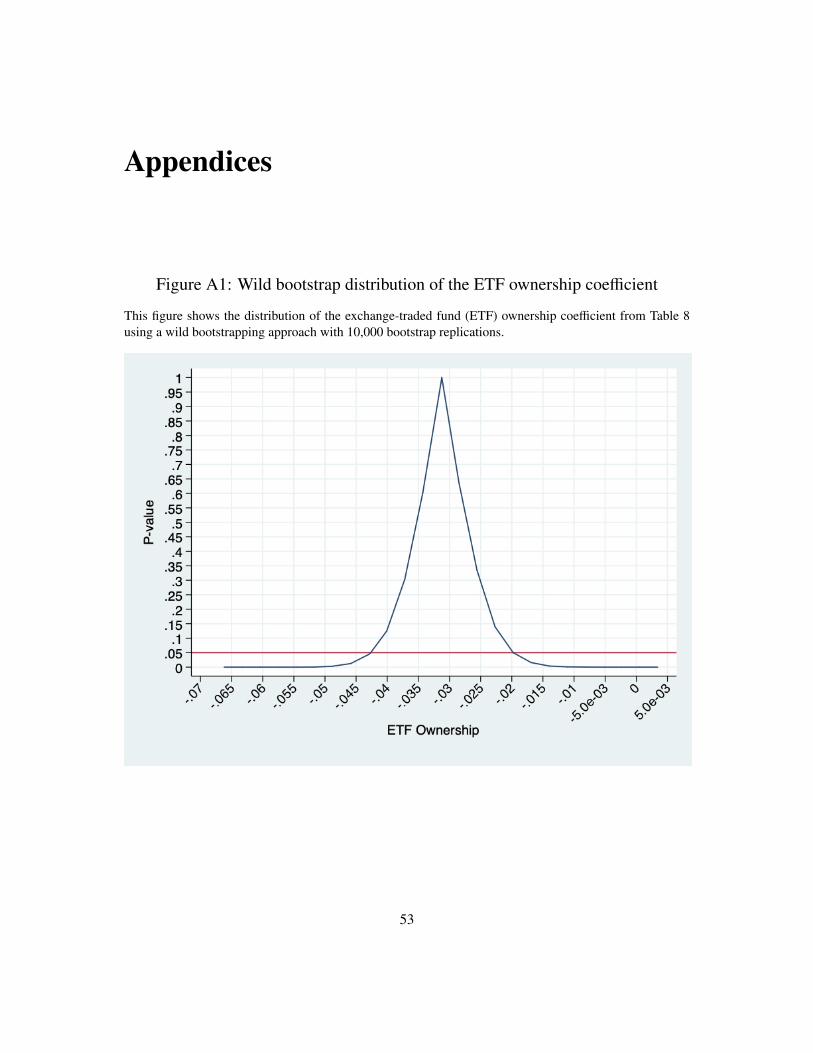

not significantly many private prison management companies, I use a wild bootstrapping

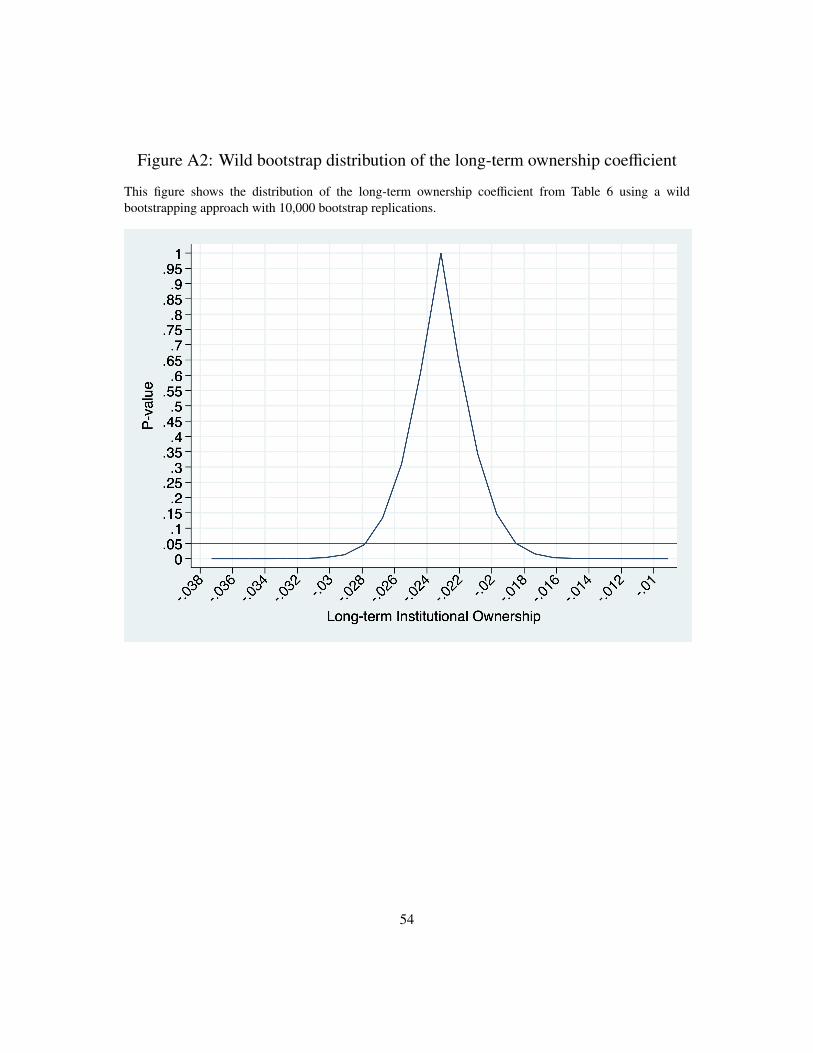

method with 10,000 bootstrap replications and plot the results in Figures A1 and A2.

7 Conclusion

Over the past three decades, with the increasing evidence of the weaknesses of in-house

government service provisions, there has been a shift to privatize important public services,

such as prisons. Prior studies, such as the seminal work by Hart, Shleifer, and Vishny (1997),

suggest that privatizing prisons may lead to a rise in social costs since private operators

may have incentives to reduce costs that negatively impact the qualify of prisoner lives.

None of the prior studies, however, take into account the public ownership structure of the

private enterprise that may play an important role in examining the social consequences of

privatization.

By taking into account the ownership structure of private prisons, I find empirical evidence

that institutional investors play an important role in mitigating the social cost associated

with privatization. The effects of institutional ownership, however, depend on the type of

26

investor since the attentiveness of shareholders to corporate social responsibility outcomes

differs across investor type.

To capture the heterogeneity in the attentiveness of shareholder to social outcomes, I first

break down the ownership levels into one of the most commonly used institutional ownership

categories: ownership by short-term versus long-term investors. I find evidence that the

positive social effects of institutional ownership are primarily driven by long-term investors

given that these investors are more attentive to the long-term value of the firm, providing

empirical evidence to support the theoretical predictions of Hart (2017) and Benabou and

Tirole (2010). To further examine the attentiveness to social outcomes across different long-

term institutional investors, I further break down long-term ownership into ownership by

granular long-term investor types. In particular, I find that the positive social effects of long-

term institutional ownership are primarily driven by investment advisors and companies, such

as mutual funds. I also show that the relationship between social outcomes and ownership

by long-term institutional investors is causal by developing a new identification strategy.

Long-term institutional investors, such as investment advisors and companies, often hold

stocks due to tracking an index. Such institutional investors may not be able to use exit

as a voice if managers of portfolio firms fail to maximize long-term value and act socially

responsibly. In this paper, I find that institutional investors may be able to use their voice

(i.e., monitoring role) to exert influence on managers to ensure that firms operate more

socially responsibly.

Furthermore, in order to determine why institutional investors may have an incentive to

monitor portfolio firms, I find a novel economic mechanism that provides a possible expla-

nation. Given that lawsuits are costly to firms and shareholders, both from a valuation and

reputation perspective, I find that the institutional ownership results are stronger in prisons

that are located in states where it is more likely to successfully sue corporations. By using a

proxy for litigation risk, I find evidence that investors are more attentive to social outcomes

when there is higher litigation risk since failing to do so has a harm to the reputation of the

institutional investors. Failing to be socially responsible may, therefore, impact fund flows.

Overall, my paper highlights the importance of institutional investors in society since they

improve the quality of outsourced government services. Prisons as well as the conditions in

27

which prisoners are rehabilitated play an important role in society and overall welfare. Al-

though privatization of prisons may lead to a rise in social costs due to incomplete contracts,

such social costs are partially mitigated, on average, by factor of one third, by the moni-

toring role of institutional investors. Forcing institutional investors, such as pension funds

or investment advisors, to divest from public prison management companies may lead to

unintended consequences, such as a rise in social costs.

28

References

Aghion, P., J. Van Reenen, and L. Zingales (2013). Innovation and Institutional Ownership. TheAmerican Economic Review 103 (1), 277–304.

Appel, I. R., T. A. Gormley, and D. B. Keim (2016). Passive investors, not passive owners. Journalof Financial Economics 121 (1), 111–141.

Appel, I. R., T. A. Gormley, and D. B. Keim (2018). Standing on the Shoulders of Giants: TheEffect of Passive Investors on Activism. The Review of Financial Studies 32 (7).

Arena, M. and B. Julio (2015). The Effects of Securities Class Action Litigation on CorporateLiquidity and Investment Policy. Journal of Financial and Quantitative Analysis 50 (1-2), 251–275.

Azim, M. (2019). Passive Demand but Active Pay: The Effect of ETF Flows on CEO Stock OptionCompensation. Rotman School of Management Working Paper .

Baland, J.-M. and P. Francois (2005). Commons as insurance and the welfare impact of privatiza-tion. Journal of Public Economics 89 (2), 211–231.

Banerjee, A., R. Hanna, J. Kyle, B. A. Olken, and S. Sumarto (2019). Private outsourcing andcompetition: Subsidized food distribution in Indonesia. Journal of Political Economy 127 (1),101–137.

Bartling, B., R. A. Weber, and L. Yao (2015). Do Markets Erode Social Responsibility. TheQuarterly Journal of Economics 130 (1), 219–266.

Bayer, P., R. Hjalmarsson, and D. Pozen (2009). Building criminal capital behind bars: Peer effectsin juvenile corrections. The Quarterly Journal of Economics 124 (1), 105–147.

Bebchuk, L. A. and S. Hirst (2019). Index funds and the future of corporate governance: Theory,evidence, and policy. Columbia Law Review 119 (8), 2029–2146.

Belbot, B. (2004). Report on the Prison Litigation Reform Act: What have the courts decided sofar? The Prison Journal 84 (3), 290–316.

Ben-David, I., F. Franzoni, and R. Moussawi (2018). Do ETFs Increase Volatility? The Journal ofFinance 73 (6), 2471–2535.

Ben-David, I., F. A. Franzoni, R. Moussawi, and J. Sedunov (2020). The Granular Nature of LargeInstitutional Investors. Managemment Science, forthcoming .

Benabou, R. and J. Tirole (2010). Individual and corporate social responsibility. Econom-ica 77 (305), 1–19.

Besley, T. and M. Ghatak (2001). Government Versus Private Ownership of Public Goods. TheQuarterly Journal of Economics 116 (4), 1343–1372.

Brochet, F., M. Loumioti, and G. Serafeim (2015). Speaking of the Short-Term: Disclosure Horizonand Managerial Myopia. Review of Accounting Studies 20 (3), 1122–1163.

29

Bushee, B. J. (1998). The influence of institutional investors on myopic R&D investment behavior.The Accounting Review 73 (3), 305–333.

Bushee, B. J. (2001). Do Institutional Investors Prefer Near-Term Earnings over Long-Run Value?Contemporary Accounting Research 18 (2), 207–246.

Benabou, R. and J. Tirole (2010). Individual and Corporate Social Responsibility. Econom-ica 77 (305), 1–19.

Chattopadhyay, A., M. Shaffer, and C. Wang (2020). Governance through shame and aspiration:Index creation and corporate behavior. Journal of Financial Economics 135 (3), 704–724.

Chen, T., H. Dong, and C. Lin (2020). Institutional shareholders and corporate social responsibility.Journal of Financial Economics 135 (2), 483–504.

Colonnello, S. and C. Herpfer (2019). Do Courts Matter for Firm Value? Evidence from the U.S.Court System. Emory University Working Paper .

Cramer, R. J., H. J. Wechsler, S. L. Miller, and E. Yenne (2017). Suicide Prevention in CorrectionalSettings: Current Standards and Recommendations for Research, Prevention, and Training.Journal of Correctional Health Care 23 (3), 313–328.