Embed Size (px)

Citation preview

Disasters Implied by Equity Index Options

David Backus (NYU), Mikhail Chernov (LSE & LBS),and Ian Martin (Stanford)

Boston University | February 11, 2011

This version: February 10, 2011

Backus, Chernov, & Martin (NYU) Disasters in options 1 / 34

Summary

The idea

I Problem: disasters infrequent ⇒ hard to estimate their distributionI Solution: infer from option prices

What we find

I Disasters apparent in options dataI More modest than disasters in macro data

Why this is harder than we thought

I Barro data gives us “true” distribution of consumption growthI Option prices give us “risk-neutral” distribution of returns

Backus, Chernov, & Martin (NYU) Disasters in options 1 / 34

Outline

Preliminaries: entropy, cumulants, plan

Disasters in macroeconomic models

Digression: risk-neutral probabilities

Disasters in option models

Comparing models

Backus, Chernov, & Martin (NYU) Disasters in options 2 / 34

Preliminaries

Entropy

Hans-Otto Georgii (quoted by Hansen and Sargent):

When Shannon had invented his quantity and consultedvon Neumann on what to call it, von Neumann replied:“Call it entropy. It is already in use under that name and,besides, it will give you a great edge in debates becausenobody knows what entropy is anyway.”

Backus, Chernov, & Martin (NYU) Disasters in options 3 / 34

Preliminaries

Entropy bound

Entropy is a measure of dispersion: for x > 0

L(x) ≡ log Ex − E log x ≥ 0

Pricing relation: there exists m > 0 such that

Et (mt+1rt+1) = 1

Entropy bound

L(m) ≥ E(log r − log r1

)

Backus, Chernov, & Martin (NYU) Disasters in options 4 / 34

Preliminaries

Cumulants

Cumulant generating function

k(s; x) = log Eesx =∞∑j=1

κj(x)sj/j!

Cumulants are almost moments

mean = κ1

variance = κ2

skewness = κ3/κ3/22

(excess) kurtosis = κ4/κ22

Backus, Chernov, & Martin (NYU) Disasters in options 5 / 34

Preliminaries

Entropy and cumulants

Entropy of pricing kernel

L(m) = log Ee logm − E logm

= k(1; logm)− E logm =∞∑j=2

κj(logm)/j!

Zin’s “never a dull moment” conjecture

L(m) = κ2(logm)/2!︸ ︷︷ ︸(log)normal term

+κ3(logm)/3! + κ4(logm)/4! + · · ·︸ ︷︷ ︸high-order cumulants (incl disasters)

Backus, Chernov, & Martin (NYU) Disasters in options 6 / 34

Preliminaries

Plan of attack

Modeling assumptions

I iidI Tight link between consumption growth and equity returnsI Representative agent with power utility [if needed]

Parameter choices

I Match mean and variance of log consumption growthI Ditto log equity returnI Base “disasters” on Barro’s macroeconomic evidenceI Or on equity index options

Compare macro- and option-based examples

Backus, Chernov, & Martin (NYU) Disasters in options 7 / 34

Macro disasters

Macro disasters: environment

Consumption growth and “equity” return are iid

gt+1 = ct+1/ct

dt = cλt

log r et+1 = constant + λ log gt+1

Power utility

logmt+1 = log β − α log gt+1

Backus, Chernov, & Martin (NYU) Disasters in options 8 / 34

Macro disasters

Macro disasters: the bazooka

Cumulant generating functions

k(s; logm) = k(−αs; log g)

Yaron’s “bazooka”

κj(logm)/j! = κj(log g)(−α)j/j!

Backus, Chernov, & Martin (NYU) Disasters in options 9 / 34

Macro disasters

Macro disasters: Poisson-normal mixture

Consumption growth

log gt+1 = wt+1 + zt+1

wt+1 ∼ N (µ, σ2)

zt+1|j ∼ N (jθ, jδ2)

j ≥ 0 has probability e−ωωj/j!

Parameter values

I Match mean and variance of log consumption growthI Jump probability (ω = 0.01), mean (θ = −0.3), and variance

(δ2 = 0.152) [similar to Barro, Nakamura, Steinsson, and Ursua]

Backus, Chernov, & Martin (NYU) Disasters in options 10 / 34

Macro disasters

Macro disasters: entropy

Cumulant generating functions

k(s; log g) ≡ log Ees log g = k(s;w) + k(s; z)

k(s;w) ≡ log Eesw = sµ+ (sσ)2/2

k(s; z) ≡ log Eesz = ω(esθ+(sδ)2/2 − 1

)Entropy

L(m) = (−ασ)2/2 + ω(e−αθ+(αδ)2/2 − 1

)+ αωθ,

Backus, Chernov, & Martin (NYU) Disasters in options 11 / 34

Macro disasters

Macro disasters: entropy

0 2 4 6 8 10 120

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

Risk Aversion α

Ent

ropy

of P

ricin

g K

erne

l L(m

)

Alvarez−Jermann lower boundnormal

Backus, Chernov, & Martin (NYU) Disasters in options 12 / 34

Macro disasters

Macro disasters: entropy

0 2 4 6 8 10 120

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

Risk Aversion α

Ent

ropy

of P

ricin

g K

erne

l L(m

)

Alvarez−Jermann lower boundnormal

disasters

Backus, Chernov, & Martin (NYU) Disasters in options 12 / 34

Macro disasters

Macro disasters: entropy

0 2 4 6 8 10 120

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

Risk Aversion α

Ent

ropy

of P

ricin

g K

erne

l L(m

)

Alvarez−Jermann lower boundnormal

disasters

booms

Backus, Chernov, & Martin (NYU) Disasters in options 12 / 34

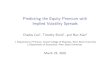

Macro disasters

Macro disasters: cumulants

2 3 4 5 6 7 8−1

0

1

2x 10

−3

Cum

ulan

t

2 3 4 5 6 7 80

1

2

3x 10

−3

Con

trib

utio

n

risk aversion α=2

2 3 4 5 6 7 80

0.05

0.1

Con

trib

utio

n

Order j

risk aversion α=10

Backus, Chernov, & Martin (NYU) Disasters in options 13 / 34

Macro disasters

Macro disasters: cumulants

High-Order Cumulants

Model (α = 10) Entropy Variance/2 Odd Even

Normal 0.0613 0.0613 0 0Poisson disaster 0.5837 0.0613 0.2786 0.2439Poisson boom 0.0266 0.0613 –0.2786 0.2439

Backus, Chernov, & Martin (NYU) Disasters in options 14 / 34

Macro disasters

Macro disasters: equity premium

0 2 4 6 8 10 12−0.5

0

0.5

1

1.5

2

Risk Aversion α

Ent

ropy

and

Equ

ity P

rem

ium

sample mean = lower bound equity premium

entropy

Backus, Chernov, & Martin (NYU) Disasters in options 15 / 34

Risk-neutral probabilities

Digression: risk-neutral probabilities

Notation: states x have (true) probabilities p(x)

Risk-neutral probabilities p∗

p∗(x) = p(x)m(x)/q1

m(x) = q1p∗(x)/p(x)

q1 = Em (1-period bond price)

Entropy (aka “relative entropy” or “Kullback-Leibler divergence”)

L(m) = L(p∗/p) = E log(p/p∗)

Backus, Chernov, & Martin (NYU) Disasters in options 16 / 34

Risk-neutral probabilities

Risk-neutral probabilities: power utility

Normal log consumption growth

I If log g ∼ N (µ, σ2) (true distribution)I Then risk-neutral distribution also lognormal with

µ∗ = µ− ασ2, σ∗ = σ

Poisson log consumption growth

I Jumps have probability ω and distribution N (θ, δ2)I Risk-neutral distribution has same form with

ω∗ = ω exp[−αθ + (αδ)2/2], θ∗ = θ − αδ2, δ∗ = δ

Backus, Chernov, & Martin (NYU) Disasters in options 17 / 34

Option disasters

Option disasters: overview

Options an obvious source of information ...

I ... about risk-neutral distribution of equity returns

Critical ingredients

I Option pricesI Merton modelI Estimated parametersI Implied volatilities

Backus, Chernov, & Martin (NYU) Disasters in options 18 / 34

Option disasters

Option disasters: information in option prices

Put option (bet on low returns)

qpt = q1t E∗t (b − r et+1)

+

Strategy

I Estimate p∗ by varying strike price b (cross section)

Black-Scholes-Merton benchmark

I Quote prices as implied volatilities (high price ⇔ high vol)I Horizontal line if lognormalI “Skew” suggests disasters

Backus, Chernov, & Martin (NYU) Disasters in options 19 / 34

Option disasters

Option disasters: Merton model

Equity returns iid

log r et+1 = log r1 + wt+1 + zt+1

wt+1 ∼ N (µ, σ2)

zt+1|j ∼ N (jθ, jδ2)

j ≥ 0 has probability e−ωωj/j!

Risk-neutral distribution: ditto with *s

Backus, Chernov, & Martin (NYU) Disasters in options 20 / 34

Option disasters

Option disasters: parameter values

Set (ω∗, θ∗, δ∗) to match option prices

I Jumps: ω∗ = ω, θ∗ = −0.0482, δ∗ = 0.0981I Set σ∗ = σI Set µ∗ to satisfy pricing relation (q1E∗r e = 1)

Later: choose (µ, σ, ω, θ, δ) to match distribution of equity returns

I Jumps: ω = 1.512, θ = −0.0259, δ = 0.0229I Equity premium: µ+ ωθI Variance of equity returns: σ2 + ω(θ2 + δ2)

All from Broadie, Chernov, and Johannes (JF, 2007)

Backus, Chernov, & Martin (NYU) Disasters in options 21 / 34

Option disasters

Option disasters: implied volatility

−0.06 −0.04 −0.02 0 0.02 0.04 0.060.19

0.195

0.2

0.205

0.21

0.215

0.22

Moneyness

Impl

ied

Vol

atili

ty (

annu

al)

estimated Merton model

smaller jump mean θ*

smaller jump standard deviation δ*

Backus, Chernov, & Martin (NYU) Disasters in options 22 / 34

Comparing models

Comparing macro and option models

Approach 1: compare pricing kernels

I Required: estimated p from daily data on equity returns

Approach 2: compare consumption growth distributions

I Required: connections between g and r e , p and p∗

Approach 3: compare option prices

I Required: connections between g and r e , p and p∗

Backus, Chernov, & Martin (NYU) Disasters in options 23 / 34

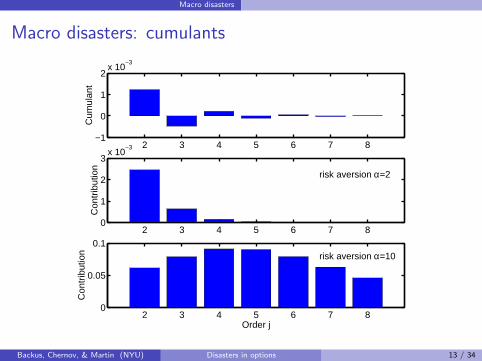

Comparing models

Comparing pricing kernels: components of entropy

High-Order Cumulants

Model Entropy Variance/2 Odd Even

Consumption-based modelsNormal (α = 10) 0.0613 0.0613 0 0Poisson (α = 10) 0.5837 0.0613 0.2786 0.2439Poisson (α = 5.38) 0.0449 0.0177 0.0173 0.0099

Option-based modelOption model 0.7647 0.4699 0.1130 0.1819

Backus, Chernov, & Martin (NYU) Disasters in options 24 / 34

Comparing models

Comparing pricing kernels: cumulants

2 3 4 5 6 7 8 9 10−0.01

0

0.01

0.02

0.03

0.04Cumulants of equity return

2 3 4 5 6 7 8 9 10−0.2

0

0.2

0.4

0.6Contributions to entropy of pricing kernel

Order j

Backus, Chernov, & Martin (NYU) Disasters in options 25 / 34

Comparing models

Comparing consumption growth

Consumption Process Based on

Cons Growth Option Prices

α 5.38 10.07ω 0.0100 1.3864θ –0.3000 –0.0060δ 0.1500 0.0229Skewness –11.02 –0.31Excess Kurtosis 145.06 0.87Tail prob (≤ −3 st dev) 0.0090 0.0086Tail prob (≤ −5 st dev) 0.0079 0.0002

Backus, Chernov, & Martin (NYU) Disasters in options 26 / 34

Comparing models

Comparing option prices

−0.06 −0.04 −0.02 0 0.02 0.04 0.060.05

0.1

0.15

0.2

0.25

option−based model

Impl

ied

Vol

atili

ty (

annu

al)

Moneyness

Backus, Chernov, & Martin (NYU) Disasters in options 27 / 34

Comparing models

Comparing option prices

−0.06 −0.04 −0.02 0 0.02 0.04 0.060.05

0.1

0.15

0.2

0.25

option−based model

Impl

ied

Vol

atili

ty (

annu

al)

Moneyness

consumption−based model

Backus, Chernov, & Martin (NYU) Disasters in options 27 / 34

Comparing models

Comparing models

All of these comparisons point in the same direction

I Macro disasters more pronounced than option disasters

Backus, Chernov, & Martin (NYU) Disasters in options 28 / 34

Reconsidering

Reconsidering ...

Our models are based on

I iidI Tight link between consumption growth and equity returnsI Representative agent with power utility

Let’s take a closer look at the last two

Backus, Chernov, & Martin (NYU) Disasters in options 29 / 34

Reconsidering

Reconsidering power utility

“Risk aversion” implied by arbitrary pricing kernel

RA ≡ −∂ logm

∂ log g= −∂ log(p∗/p)

∂ log r e· ∂ log r e

∂ log g

Backus, Chernov, & Martin (NYU) Disasters in options 30 / 34

Reconsidering

Reconsidering power utility

−0.1 −0.05 0 0.05 0.12

3

4

5

6

7

8

9

10

Log Return on Equity

Impl

ied

Ris

k A

vers

ion

RA

Backus, Chernov, & Martin (NYU) Disasters in options 31 / 34

Reconsidering

Reconsidering the link between g and r e

−0.1 −0.05 0 0.05 0.1

−0.6

−0.4

−0.2

0

0.2

0.4

0.6

Log Consumption Growth

Log

Exc

ess

Ret

urn

on E

quity

Backus, Chernov, & Martin (NYU) Disasters in options 32 / 34

Reconsidering

Reconsidering the link between g and r e

−0.06 −0.04 −0.02 0 0.02 0.04 0.060.05

0.1

0.15

0.2

0.25

option−based model

Impl

ied

Vol

atili

ty (

annu

al)

Moneyness

consumption−based model

bivariate consumption−returns model

Backus, Chernov, & Martin (NYU) Disasters in options 33 / 34

Recapitulation

Barro, Longstaff & Piazzesi, Rietz

I Disasters contribute to equity premium [entropy]I Evident in macro dataI Range of opinion on magnitude

We look at options

I Smile/smirk suggests something like disastersI Prices available even for outcomes that don’t occur in sampleI Implied disasters less severe than macro dataI High entropy from options suggests it’s not enough to match equity

premium

Backus, Chernov, & Martin (NYU) Disasters in options 34 / 34