Embed Size (px)

Citation preview

COVER SHEET

A S O 9 1 1 9 6 2 0 6 S.E.C. REGISTRATION NUMBER

S P L A S H C O R P O R A T I O N

(COMPANY’S FULL NAME)

H B C C O R P O R A T E C E N T R E

5 4 8 M I N D A N A O A V E N U E C O R .

Q U I R I N O H I G H W A Y

Q U E Z O N C I T Y

(Business Address: No. Street/City/Town/Province)

ATTY. MA. LOURDES B. RODRIGUEZ 984-5555 Contact Person Company Telephone Number DECEMBER 31 Definitive Information Statement 3rd Saturday of June ___________ ______________ ________________________ ____________ _____________ Month Day Form Type Month Day Fiscal Year Annual Meeting

____________________________________________ Secondary License Type, If Applicable

Corporation Finance Department ___________________________________ ____________________________________ Department Requiring this Document Amended Articles Number / Section Total Amount of Borrowings _____________________ __________________ _________________ Total no. of Subscribers Domestic Foreign ----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

TO BE ACCOMPLISHED BY SEC PERSONNEL CONCERNED

File Number ______________________________________________ LCU

Document I.D. ______________________________________________ Cashier

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 20 - IS

1. Date of Report : May 19, 2009 2. SEC Identification Number: ASO91-196206. 3. BIR Tax Identification No: 001-096-221 4. Exact name of issuer as specified in its charter Splash Corporation 5. Province, country or other jurisdiction of incorporation 6. Industry Classification Code: (SEC Use Only) 7. Address of principal office: 3F HBC Corporate Centre Mindanao Ave., Q.C. 1116 8. Issuer's telephone number, including area code: (02) 984-5555 9. Former name or former address, if changed since last report NA 10.Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the

RSA Number of Shares of Common Stock Common Shares listed in the Philippine 223,848,107 common shares Stock Exchange 11. Indicate the item numbers reported herein:

Submission of the Definitive Information Statement

SIGNATURE Pursuant to the requirement of the Securities Regulation Code, the issuer has duly caused this report to be signed on its behalf by the undersigned, duly authorized for the purpose. SPLASH CORPORATION By: ATTY. MA. LOURDES B. RODRIGUEZ Compliance Officer

May 19, 2009 Disclosure Department The Philippine Stock Exchange, Inc. Philippine Stock Exchange Centre Exchange Road, Ortigas Center Pasig City

Attention: Ms. Janet A. Encarnacion Head, Disclosure Department

Subject: Filing of Splash Corporation’s Definitive

Information Statement under SEC Form 20-IS

Gentlemen: Please be informed that Splash Corporation (SPH) hereby discloses the filing of its Definitive Information Statement (SEC Form 20-IS) with the Securities and Exchange Commission. Thank you. Very truly yours, ATTY. MA. LOURDES B. RODRIGUEZ Corporate Secretary cc : Director Justina F. Callangan Corporate Finance Department

Securities and Exchange Commission

1

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

TO ALL STOCKHOLDERS: Notice is hereby given that the Annual Meeting of the Stockholders of Splash Corporation will be held on Saturday, June 20, 2009, at nine o’clock in the morning at the Crowne Plaza Galleria Manila, ADB Avenue, Pasig City to consider and act upon the following matters:

1. Certification on sending of notices and quorum 2. Annual Report of the President and Chief Operating Officer 3. Ratification of the Actions of the Board of Directors and the Corporate Officers for the

year 2008 4. Ratification of the Annual Report and Ratification of the Actions of the Board of Directors

and Corporate Officers 5. Declaration of Dividends 6. Appointment of External Auditors 7. Election of Directors 8. Adjournment Only stockholders of record as of May 20, 2009 will be entitled to attend and vote at the

meeting. For this purpose, the Stock and Transfer Books of the Corporation will be closed on May 20, 2009. Please be advised that we are not soliciting your proxy FOR THE BOARD OF DIRECTORS

MA. LOURDES R. BANTEGUI- RODRIGUEZ

Corporate Secretary

2

Instructions

We are not soliciting your proxy. However, if you would be unable to attend the meeting but would like to be represented thereat, you may accomplish the proxy form herein provided below for the purpose and submit the same to the Office of the Secretariat at Stock Transfer Service, Inc. (STSI), Tel. Nos. (632) 898-7555 / 898-7611, c/o Mr. Richard D. Regala, Jr., Assistant Manager-Operations Head, 8th Floor, Phinma Plaza, 39 Plaza Drive, Rockwell Center, 1211 Makati City on or before June 5, 2009. This Proxy, when properly executed, will be voted in the manner as Directed herein by the Stockholder. If no direction is made, this Proxy will be voted “FOR” the election of all nominees, “FOR” the ratification of all previous acts and resolutions of the outgoing Board of Directors and Management, and “FOR” such other matters as may properly come before the meeting. Revocability of Proxy A stockholder giving a proxy has the power to revoke it at any time prior to its exercise by giving written notice to the Corporate Secretary at least six (6) working days prior to the Annual Meeting or by personal presence of the stockholder at the said meeting.

SPLASH CORPORATION P R O X Y

I/WE hereby name and appoint __________________________________, or in his/her absence, the Chairman of the Meeting, as my/our proxy at the annual stockholders’ meeting of SPLASH CORPORATION to be held at the Crowne Plaza Galleria Manila, ADB Avenue, Pasig City on Saturday, June 20, 2009 at 9:00 A.M. and at any postponement or adjournment thereof. _____________________________ ______________________________ Place Date __________________________________________ Printed Name & Signature Number of shares held: __________________

3

SPLASH CORPORATION

INFORMATION STATEMENT PURSUANT TO RULE 20 OF THE SECURITIES REGULATION CODE

A. GENERAL INFORMATION

Item 1 - Date, Time and Place of Meeting

The Annual Meeting of Stockholders of Splash Corporation is scheduled on June 20, 2009 at 9:00 A.M. at the Ruby Ballroom, Crown Plaza Galleria Manila, ADB Avenue, Pasig City. The complete mailing address of the principal:

Office of the Secretariat at Stock Transfer Service, Inc. (STSI) c/o Mr. Richard D. Regala, Jr. Assistant Manager-Operations Head 8th Floor, Phinma Plaza, 39 Plaza Drive, Rockwell Center, 1211 Makati City Tel. Nos. (632) 898-7555 / 898-7611

The information statement and form of proxy is targeted to be mailed to the stockholders on or before May 29, 2009

Item 2 - Dissenter’s Right of Appraisal

There are no corporate actions or matters that will be taken up during the meeting that will entitle dissenting stockholders to exercise their right of appraisal under Section 81 of the Corporation Code of the Philippines, which provides as follows: Any stockholder of a corporation shall have the right to dissent and demand payment of the fair value of his shares in the following instances: 1. In case any amendment to the Articles of Incorporation has the effect of changing or

restricting the rights of any stockholder or class of shares, or of authorizing preferences in any respect superior to those of outstanding shares of any class, or of extending or shortening the term of corporate existence;

2. In case of sale, lease, exchange, transfer, mortgage, pledge or other disposition of all or

substantially all of the corporate property and assets as provided in this Code; and 3. In case of merger or consolidation.

Item 3 - Interest of Certain Persons or Opposition to Matters to be Acted Upon

The Registrant is not a party to any arrangement with any person with regard to any matter to be acted upon at the meeting. No director has informed the Registrant that he intends to oppose any action intended to be taken by the Registrant. Neither has any director or executive officer of the corporation, or nominee for director, or any associate of the foregoing persons have any substantial interest, direct or indirect, in any matter to be acted upon, other than election to office.

4

B. CONTROL AND COMPENSATION INFORMATION

Item 4 - Voting Securities and Principal Holders

There are 691,290,326 shares of Splash Corporation common stock issued and outstanding and entitled to vote at the Annual Meeting. Only stockholders of record as of May 20, 2008, will be entitled to notice of and to vote at the Annual Meeting. An agenda item at the Annual Meeting is the election of directors for the ensuing year. Article II, Section 6 of the Company’s Amended By-Laws, provides:

VOTING – At all meetings of the stockholders, each stockholder shall be entitled to one vote for each share of stock outstanding in his name in the stock transfer books of the Corporation. In the election, a stockholder may vote his shares in person or by proxy for all the nominees for directors, or he may cumulate said shares and give one nominee as many votes as the number of directors to be elected multiplied by the number his shares shall equal, or he may distribute them on the same principle among as many nominees as he shall see fit. Provided, however, that the whole number of votes cast by him shall not exceed the number of shares outstanding in his name in the stock transfer books of the Corporation multiplied by the number of directors to be elected.

Discretionary authority to cumulate votes is not solicited. Security Ownership of Certain Record and Beneficial Owners of more than 5%: The following table is a list of the top stockholders as of December 31, 2008 including stockholders with beneficial ownership of more than 5%.

5

Rank

Stock- holder

Number Name and Address Citizenship Holdings %1 1 SPLASH HOLDINGS INC.

3/F HBC CORPORATE CENTER 548 MINDANAO AVE. QUEZON CITY

2 9 PCD NOMINEE CORP.(FIL.) THE ENTERPRISE BLDG. AYALA AVE. MAKATI CITY

3 10 PCD NOMINEE CORP. (NON-FIL.) THE ENTERPRISE BLDG. AYALA AVE. MAKATI CITY

4 483 YAO ALFREDO M. 84 DAPITAN STREET QUEZON CITY

5 20 ENRILE WILLIAM T. VICENTE MADRIGAL AVENUE CORINTHIAN GARDEN, QUEZON CITY

6 481 BAYOG ROMEO D. 4420 SCARLET STREET SUNVALLEY SUBD. BRGY. SUNVALLEY PARANAQUE CITY

7 479 YAO ANNIKA SHERRYN 158 SUERTE STREET PASAY CITY

8 482 KHO DAVID LIMQUECO 35 QUEZON AVENUE QUEZON CITY

9 19 DUY WINSTON L. J.P. CABAGUIO AVENUE DAVAO CITY

10 485 REYES ANNA KARENINA E. BLK 1 LOT 37 SUGARTOWNE SUBD. BATASAN HILLS QUEZON CITY

11 488 OLIVEROS FEDERICO S. JR. 10 PEARL STREET SEVERINA DIAMOND SUBDPARANAQUE CITY

12 489 SOLOMON ANTONINA SABLAN 17-D REYNADO STREET TIERRA BELLA HOMETANDANG SORA QUEZON CITY

13 21 SANTOS ALFREDO M. 40 AUGUST STREET, VISTA VERDE VILLAGE CAINTA RIZAL

14 469 ALMIRA PILAR P. 135 ANONAS EXTENSION SIKATUNA VILLAGEQUEZON CITY

15 487 HWANG DAVID Y. 1209 ACACIA ROAD DASMARINAS VILLAGE MAKATI CITY

16 12 CHERYL LADD CHING OR CHRISTOPHER CHIN103 KAMUNING ROAD KAMUNING QUEZON CITY

17 11 JOSE A. FERRIOLS &/OR EDUARDO A. FERRIO1612 TAYUMAN STREET STA. CRUZ MANILA

18 478 YU KEVIN &/OR EMMA CONCEPCION YU UNIT 3 101 4TH STREET NEW MANILA QUEZON CITY

19 17 AGUAS RENE Q. 491 KAYUMANGI STREET PLAINVIEW MANDALUYONG CITY

20 16 TIO ELSON A. ELSON AUTO SUPPLY R. MAGSAYSAY AVENUE, DAVAO CITY

Total Top 20 Shareholders 691,248,821 99.99%

Other 41,505 0.01%

Total Outstanding Shares 691,290,326 100.00%

0.00%

0.00%

0.00%

0.00%

0.00%

0.00%

0.00%

0.00%Filipino 5,000

Filipino

Filipino

5,000

5,000

Filipino 10,000

Filipino 10,000

Filipino

Filipino 5,000

Filipino 5,000

5,000

Filipino23,000

Filipino20,000

Filipino10,000

0.00%

0.00%

0.00%

Filipino 50,000

Filipino 50,000

Filipino 50,000

0.01%

0.01%

0.01%

Filipino 599,000

Filipino 320,000

Filipino 56,000

0.09%

0.05%

0.01%

Filipino

Filipino

Foreign

492,009,214

93,031,107

104,980,500

71.17%

13.46%

15.19%

6

Security Ownership of Management

Name Citizenship Shareholdings % to TotalRolando B. Hortaleza, M.D., Chairman and Chief Executive Officer

Filipino 1 0.0000001%

Sinforoso Jesus R. Soriano, President Filipino 20,000 0.0028931%

Item 5 – Directors and Executive Officers

1. Directors

The following table lists the Directors of the Company, and following this table are profiles of each Director

Name PositionRolando B. Hortaleza, M.D. ChairmanRosalinda A. Hortaliza, M.D. Vice‐ChairmanSinforoso Jesus R. Soriano DirectorAllue Krisanne A. Hortaleza DirectorMaurice P. Ligot DirectorRizalino D. Rivera, Independent Director Independent DirectorJimmy T. Yaoksin, Independent Director Independent Director

Rolando B. Hortaleza, M.D. Dr. Hortaleza, 50, Filipino, is the Chairman of the Board and Chief Executive Officer of Splash Corporation which he co-founded with his wife, Rosalinda, also a medical doctor, in 1985. He is a scion of the Hortaleza family which pioneered the Hortaleza Vaciador and Beauty Supplies, a trail-blazing chain of stores that sells cosmetic products, nippers, scissors and other beauty salon supplies. Dr. Hortaleza also sits as Chairman of Splash Holding, Inc. and Vice-Chairman of the following corporations: HBC, Inc., World Partners Bank and World Partners Finance Corporation. He is also Vice-Chairman of Splash Foundation, Inc. Dr. Hortaleza graduated with a Bachelor of Science degree in Preparatory Medicine (Pre-Med) from the University of the East and obtained his degree in Medicine from Our Lady of Fatima University in 1984. Dr. Hortaleza also attended the Owners and Presidents Management Program at the Harvard Business School in Boston, Massachusetts from 1997 to 1998. Rosalinda Ang-Hortaleza, M.D. Dr. Ang-Hortaleza, 51, Filipino, is the Vice-Chairman of Splash Corporation. She also sits as Vice Chairman of Splash Holdings, Inc., and is the Chairman and Chief Executive Officer of HBC, Inc., Splash Foundation, Inc., World Partners Bank, and World Partners Finance Corporation. She graduated with a Bachelor of Science degree in Medical Technology from the University of Santo Tomas in 1980. She obtained her degree in Medicine from Our Lady of Fatima University in 1984. She attended the Advanced Management Program at the Harvard Business School in Boston, Massachusetts in 2000.

7

Sinforoso Soriano. Mr. Soriano, 46, Filipino, is the President and Chief Operating Officer of Splash Corporation. He is also heads the Company’s Investor Relations. He joined Splash in 2005. He was formerly the President/COO of Splash Nutraceutical Corporation until June 2006. Thereafter, he held the President/COO position of Splash Holdings, Inc. until his appointment to Splash Corporation in August 2007. Prior to joining Splash, Mr. Soriano spent his entire professional career with Eli Lilly (Philippines), Inc. where he started as a Professional Medical Sales Representative in 1987. He was assigned to various positions in the Eli Lily’s sales and marketing organization in the Philippines and the United States, highlighted by his appointment as Asia-Pacific Area Operations Manager (Sales) based in Singapore and as National Sales Director for the Philippines, a position he held until he left the company in February 2004. Mr. Soriano graduated from the University of Santo Tomas with a Bachelor of Science degree in Pharmacy. He passed the Pharmacy Licensure Examinations in 1986. He obtained his Master in Business Administration degree from St. Louis College. Allue Krisanne A. Hortaleza. Ms. Hortaleza, 24 Filipino, is the eldest daughter of Drs. Rolando and Rosalinda Hortaleza and was elected to the Board in 2007. She obtained her Bachelor of Science degree in Management from the Ateneo de Manila University in March 2007. She is currently the Executive Assistant to the Chairman/CEO of HBC, Inc. Maurice P. Ligot. Ms. Ligot, 57, Filipino, has been a Director of Splash Corporation since 2002 and President and Chief Operating Officer of Splash Foundation, Inc. since 1997. Ms. Ligot is also a member of the Board of Directors of World Partners Finance Corporation and HBC, Inc. Prior to her present positions, she was with Splash Manufacturing Corporation as Production Manager, Quality Assurance Manager and then Total Quality Manager. Ms. Ligot obtained her Bachelor of Science degree in Pharmacy from the Centro Escolar University (CEU) where she was Outstanding Alumna of the School of Pharmacy in 2000 and Centennial Awardee in 2007. She earned units in Master of Science in Pharmacy from the University of the Philippines. She also obtained diplomas in Creating Value in CSR from the Asian Institute of Management in Indonesia; Triple Bottomline: Operationalizing The Doing Good from Asian Institute of Management, Philippines; and Corporate Governance from the University of the Philippines. Ms. Ligot was Trustee and Treasurer of the League of Corporate Foundations in 2003 – 2007 and currently, a trustee of Ninoy and Cory Aquino Center for Leadership. Rizalino D. Rivera. Mr. Rivera, 47 Filipino, was elected to the Board of Splash Corporation on 1 October 2007. He is in charge of Management Planning for Digital Alliance which is a group of companies involved in ICT and Broadcast. He is President of Change Consultants, Inc. which offers consultancy services to top business corporations as well as government organizations, the academe, and development work. Mr. Rivera is the Faculty Chair for the Human Resource Cluster of the Ateneo Graduate School of Business. He is also involved with the Institute of People Power and Development of the Benigno S. Aquino, Jr. Foundation and is a member of the advisory team to former President Corazon C. Aquino. Mr. Rivera has been a senior consultant on human resource management and organizational development for several companies which include Nestle Philippines, Kraft Foods, Jollibee Foods Corporation, Wyeth Philippines, Pfizer, La Farge Cement, HBC, Inc. and the Asian Development Bank. Mr. Rivera has a Bachelor of Arts degree in Political Science from the University of the Philippines. He is a candidate for the Master of Arts in Counseling Psychology program of the Ateneo de Manila University as well as the Master of Science in Organization Development program of the Pepperdine University, U.S.A.

Jimmy T. Yaokasin. Mr. Yaokasin, 40, Filipino, was elected to the Board of Splash Corporation on October 1, 2007. He is currently the Chairman of the Board of Trustees of the Development Academy of the Philippines in his capacity as the representative of the Office of the President. He is also a member of the Board of Directors of MRC Allied, Inc., Menlo

8

Capital, Leyte Cable TV Network, Inc. and the YKS Group of Companies. Mr. Yaokasin is an active member of civic and community organizations – Paul Harris Fellow of Rotary International, Gideons International and former National President of the Philippine Jaycees. Mr. Yaokasin obtained his degree in Business Administration major in Accountancy (Magna cum Laude) from the University of the Philippines. He obtained his Master in Business Administration (MBA) under the joint Executive MBA program of the Kellogg School of Management of Northwestern University, Chicago and the Hongkong University of Science and Technology. Mr. Yaokasin is a Certified Public Accountant. Independent Directors: Among the seven (7) Directors, Messrs. Rizalino D. Rivera and Jimmy Tiu Yaokasin, Jr. are the independent directors of the company, having been as such pursuant to Article III, Section 1(a) of the By-Laws of the Corporation. For 2009, the following have been nominated by the stockholders as independent Directors: Nominees as Independent Directors: Messrs. Rizalino D. Rivera and Jimmy Tiu Yaokasin, Jr. were nominated by Splash Holdings, Inc., represented by Dr. Rolando B. Hortaleza. Messrs. Rivera and Yaokasin have no family or business relationships with the person who nominated them, and have accepted their nominations to again serve as Independent Directors. They possess the qualifications and none of the disqualifications of an Independent Director. The Certification of Independent Director Rizalino D. Rivera was submitted to the Securities and Exchange Commission on July 18, 2009 while the Certification of Independent Director Jimmy Tiu Yaokasin, Jr. was filed with the said Office on July 21, 2009. Nominations for Directors and Independent Directors will be received during the period May 1 to 7, 2009, all of which are compliant with Art. III, Sec. 2(a) of the By-Laws of the Corporation requiring submission of same in writing to the Corporate Secretary not later than thirty (30) days prior to the date of the regular meeting of stockholders for the election of directors. The Nominations Committee evaluated the qualifications of the seven (7) nominees and concluded that they have more than the required qualifications and have none of the disqualifications for directorship as set out in the Corporation’s By-Laws and Manual on Corporate Governance which are based on SRC Rule 38-1. The Committee submitted the list of qualified nominees to the Board on May 15, 2009, in compliance with the By-Laws requiring submission of same at least 30 days before the Annual Meeting.

9

2. Executive Officers

Name PositionRolando B. Hortaleza, M.D. Chief Executive OfficerSinforoso Jesus R. Soriano President and Chief Operating OfficerRamon G. Trajano Chief Financial OfficerEdgardo I. Patron General Manager for International OperationsDeogracia G. Orpilla General Manager for Domestic OperationsAtty. Ma. Lourdes Bantegui‐Rodriguez Corporate SecretaryHiginio P. Porte, Jr. Head ‐ Research and Supply Chain ManagementTeodulo L. Manlubatan Head ‐ Corporate ServicesTeresa M. Conde Head ‐ Marketing and Brand Development Rico B. Lavalle Head ‐ Customer and Business DevelopmentGaryzalde O. Morales Head ‐ Brand Activation GroupKriskyril Peteilhard M. Lapitan Head ‐ Human ResourcesMenchie P. Sadornas Head ‐ FinanceArthur P. Bautista Head ‐ Splash Research InstituteLoida S. de Vera Head ‐ Strategic ProcurementEmyl B. Rendon Head ‐ Plant Operations and Logistics DivisionGrace D. del Rosario Head ‐ Regulatory AffairsLoida E. Moreno Head ‐ Market Research

Ramon G. Trajano, 53, Filipino, Chief Financial Officer. Mr. Trajano joined Splash in August 2008. Prior to Splash he was Finance Director of APAC Manila (a Nasdaq-listed BPO company) , CFO of Globalstride Corp (a Philippine call center), and finance head of two Ayala Corporation companies: CFO of Ayala Health Care and Finance Director of Ayala Life. Mr. Trajano graduated with degrees of Bachelor of Arts (Economics) and Bachelor of Science in Commerce (Accounting) from De La Salle University, Manila. He obtained his M.B.A. from the Wharton School of the University of Pennsylvania. He is a Certified Public Accountant. Deogracia G. Orpilla, 38, Filipino, EVP and General Manager for Domestic Operations. Mr. Orpilla joined Splash in 2006. Prior to joining Splash, he was Sales Director of Reckitt Benckiser from 2004 to 2006. He was National Sales Manager in Master Foods (Mars, Inc.) from 1996 to 2004. Mr. Orpilla graduated with a Bachelor of Arts degree in Public Administration from the University of the Philippines, Diliman, Quezon City. Edgardo I. Patron, 50, Filipino. EVP and General Manager for International Operations. Mr. Patron joined Splash in January 2005. Prior to joining Splash, he was with Kraft Foods International from 2000 to 2004 where he held senior positions in the company’s Southeast Asian operations, his last position being General Manager for Thailand. Mr. Patron completed the Management Development Program of the Asian Institute of Management and obtained his Bachelor of Science degree in Commerce from San Sebastian College, Manila.

10

Ma. Lourdes R. Bantegui-Rodriguez, 53, Filipino, Head of Corporate Legal Affairs and Corporate Secretary. Atty. Rodriguez joined Splash Corporation in January 2007. Prior to joining Splash she was the Corporate Counsel and the Corporate Secretary of Araneta Properties, Inc. Atty. Rodriguez graduated cum laude with a Bachelor of Arts degree in Mass Communications from the Far Eastern University where she also obtained her Bachelor of Laws. Higinio P. Porte, 46, Filipino, Vice President and Head of the Research and Supply Chain Management Division. Prior to joining Splash, he was with Interphil Laboratories, Inc. from 1987 to June 2000 where he last position was Division Head for Logistics and Materials Management. Mr. Porte obtained his Bachelor’s degree in Chemical Engineering from the University of the Philippines. He was a Director’s Awardee of the Management Development Program, Ateneo Professional Schools. Teodulo L. Manlubatan , 48, Filipino, Vice President and Head of Corporate Services. Mr. Manlubatan also worked for Lamoiyan Corporation as Senior Assistant Vice-President for Supply Chain Management. He holds a bachelors degree in Chemical Engineering from the University of the Philippines where he also completed academic requirements for a Masters degree in Chemical Engineering.

Teresa M. Conde, 36, Filipino, Head of Marketing and Brand Development. Ms. Conde was Infant Food Category Manager for Philippine Health Food Center, Inc. (a subsidiary of Unilab) from 1998 to 2001; and Senior Product Manager for RFM Swift Foods Inc. from 1994 to 1998. Ms. Conde graduated with a Bachelor of Science degree in Commerce from St. Paul’s College (Quezon City) and obtained her Master in Business Administration degree from the De La Salle University. Rico Ramon B. Lavalle, 39, Filipino, Head of Customer and Business Development. Mr. Lavalle was with the Pure Foods Corporation sales organization from 1993 to 1997. He also worked for Mead Johnson Philippines. He holds a Bachelors Degree in Commerce, major in Economics from the Central Philippine University in Iloilo. He is likewise a holder of a Diploma in Business Administration from the Ateneo Graduate School of Business Arthur P. Bautista, 34, Filipino. Head of Splash Research Institute. Before joining Splash, he was Faculty Member and Department Chairman of the Industrial Pharmacy Department of the College of Pharmacy, University of the Philippines, Manila. Mr. Bautista obtained his Bachelor of Science degree in Industrial Pharmacy from the University of the Philippines. Loida S. De Vera., 50, Filipino, Head of Strategic Procurement. Prior to joining Splash, she was the Strategic Sourcing Manager of Stephan Phils. Inc.. Ms. De Vera obtained her Bachelor of Science in Chemical Engineering from the University of Sto. Tomas.

Emyl B. Rendon. 36, Filipino, Head of Plant Operations and Logistics Division. Prior to joining Splash, Mr. Rendon was the Warehouse and Distribution Manager for Red Ribbon Bakeshop Inc. He and holds a Bachelor’s Degree in Electrical Engineering from the Mapua Institute of Technology and is a Registered Electrical Engineer. Grace S. Domingo-Del Rosario, 53, Head of Regulatory Affairs. Filipino. Before joining Splash, she was Senior Vice-President of Federal Chemicals, Inc. Ms. Del Rosario graduated from the University of the Philippines where she obtained her Bachelor of Science degree in Chemistry.

11

Loida E. Moreno, 33, Filipino, Head of Market Research Prior to joining Splash, Ms. Moreno was International Relations Assistant of PRTC Inc. She obtained her Bachelor of Arts degree in Psychology from De La Salle University.

3. Relationships and Related Transactions

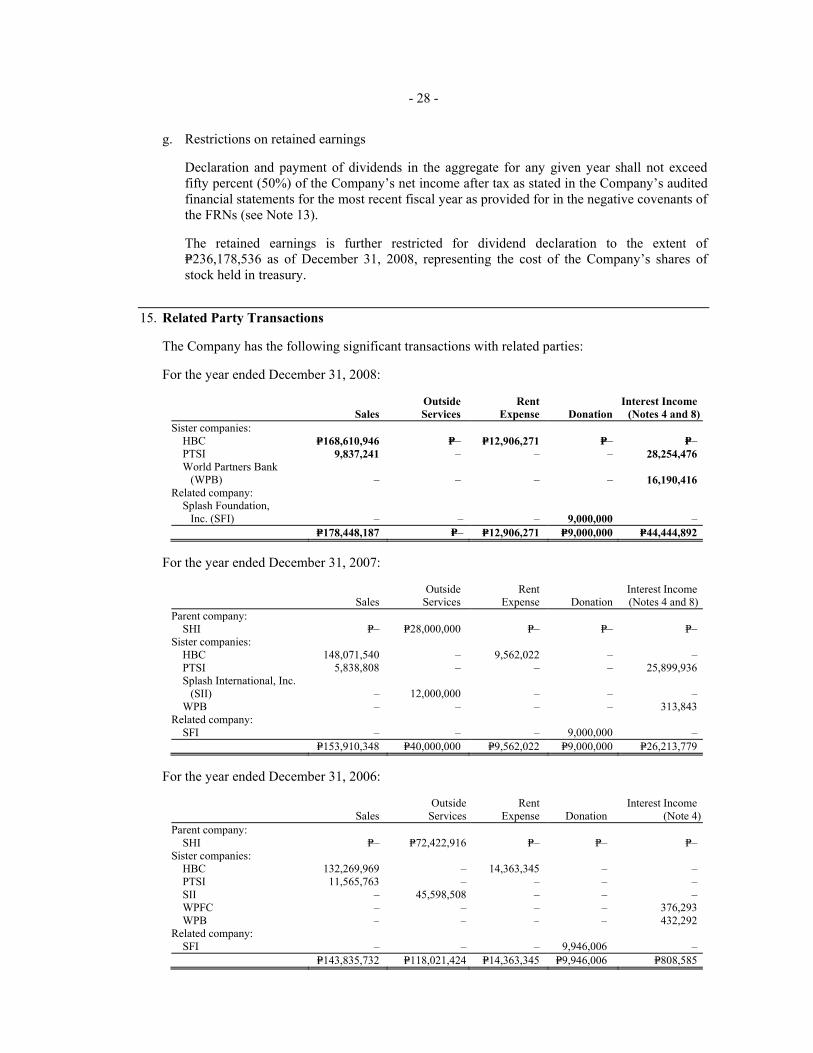

The Registrant sells to the following affiliates: HBC, Inc. and PT Splash Indonesia (PTSI), companies owned by Splash Holdings, Inc. where Dr. Rolando B. Hortaleza, Dr. Rosalinda Ang-Hortaleza, and Allue Krisanne A. Hortaleza are members of the Board of Directors and/or executive officers. The Company sells to HBC, Inc. and PTSE on an arm’s length basis. HBC accounted for 4.3% of total Company sales while PTSI accounted for 1.3%. There are no material transactions which were negotiated by Splash Corporation with parties whose relationship with the Corporation fall outside the definition of “related parties” under SFA/IAS No. 24 but with whom Splash Corporation has relationship that enables such parties to negotiate terms that may not be available from other, more clearly independent parties on an arm’s length basis. With the exception of the spouses Dr. Rolando B. Hortaleza and Dr. Rosalinda Ang-Hortaleza and their eldest daughter Allue Krisanne A. Hortaleza who are the Chairman, Vice-Chairman, and Director, respectively, of the Company, there are no family relationships either by consanguinity or affinity up to the fourth (4th) civil degree among the directors, executive officers and nominees for election as directors.

Splash Holdings, Inc (SHI) is the parent company of Splash Corporation (SC). SHI sold Php100 million of SC shares of stock to SC, and used the proceeds to partially pay P.T. Indonesia’s (PTSI) Notes Payable to SC. SHI is guarantor of this Notes Payable.

Item 6 - Compensation of Directors and Executive Officers All the members of the Board of Directors are entitled to P20,000.00 per diem for attendance in any regular or special meeting. The compensation table which follows summarizes total salaries, allowances and bonuses for the last two fiscal years (2007 and 2008) and estimated to be paid for 2009 to the principal executive, operating and financial officers.

Other than the election of directors, there is no action to be taken at the Annual Stockholders’ Meeting that will affect directors and executive officers relative to bonus, profit sharing, pension/retirement plan, granting or extension of any option, and warrants or rights to purchase any securities. The members of the Compensation Committee are Maurice P. Ligot as Chairman with Allue Krisanne A. Hortaleza and Rizalino D. Rivera (Independent Director), as members.

12

Salary Php Mil)

Rolando B. Hortaleza, M.D.Chiarman and Chief Executive OfficerSinforoso Jesus R. SorianoPresident and Chief Operating OfficerRamon G. TrajanoChief Financial OfficerDeogracia G. OrpillaEVP and GM for Domestic OperationsEdgardo I. PatronEVP and GM for International OperationsHiginio P. Porte, Jr.VP for Research and Supply Chain ManagementAtty. Ma. Lourdes Bantegui‐RodriguezAVP ‐ Corporate Legal / Corporate SecretaryTeresa M. CondeAVP ‐ Marketing and Brand Development

Actual 2007 39.473 9.929Actual 2008 60.028 13.170Projected 2009 60.510 13.917Actual 2007 25.847 6.502Actual 2008 31.727 6.948Projected 2009 37.691 8.669

*Senior Managers and above

Name and Principal Position Year Other Variable Pay (Php Mil)

CEO and most highly compensated Executive Officers

All other officers* as a group unnamed

Item 7 – Independent Public Accountant Sycip, Gorres, Velayo (SGV) is the Company’s independent external auditor and is proposed to be retained. There are no disagreements with SGV regarding accounting and financial disclosure. A representative of SGV will be at the annual general meeting and will have the opportunity to make a statement if they desire to do so, and, will respond to appropriate questions. The table below summarized fees billed by SGV in the past two years:

2007 2008Audit fees 2,395,646 3,531,336 Other audit related fees 69,930 263,298 Tax services fees 425,600 300,000 Other fees 246,400 246,400 Totals 3,137,576 4,341,034

The members of the Audit Committee are Jimmy Tiu Yaokasin, Jr. (Independent Director) of the corporation as Chairman with Rosalinda Ang-Hortaleza and Maurice P. Ligot as members.

13

C. NATURE AND SCOPE OF BUSINESS

1. Business Overview

Splash Corporation (the Company) was incorporated in the Philippines and registered with the Philippine Securities and Exchange Commission (SEC) on September 30, 1991 primarily to develop, manufacture, bottle, pack, and market cosmetics and other beauty products, and pharmaceutical products in the Philippines and abroad. On November 14, 2008, the Company’s Board of Directors (BOD) approved to amend the primary purpose of the Articles of Incorporation to include the development or acquisition of technology to manufacture and sell personal care, pharmaceuticals, food, health, home, household care and other ancillary products in the Philippines and abroad.

Before the Company listed its shares of stock with the Philippine Stock Exchange (PSE), the Company was a wholly owned subsidiary of Splash Holdings, Inc. (SHI). On November 15, 2007, the Company’s shares of stock were listed and traded in the PSE. After the IPO wherein the Company offered 30% of outstanding shares (both primary and secondary) to the public, the Company became 70% owned by SHI. On December 4, 2008, the BOD approved to buy back the Company’s shares of stock totaling 30.3 million shares held by SHI. After the buyback, SHI’s ownership of the company increased from 70% to 71.17% and SHI continues to exercise control over the Company.

The Company’s registered office address is HBC Corporate Centre, 548 Mindanao Avenue corner Quirino Highway, Quezon City.

2. Products and Brands

The Company markets and sells its products and brands in the Philippines (Domestic segment) and abroad (International segment). In turn, the Company’s products and brands sold in these two segments fall under the following categories:

• Hair care – Consists of hair care products, with sales derived from the following brands: Kolours (premium hair dye), Vitress (cuticle coat), and Control (hair dressing)

• Skin care – Products positioned to provide total skin care solution through the use of potent non-herbal active ingredients. Revenues are largely generated by Maxipeel (exfoliants) and Skin White (skin whitening). These brands each generate sales in excess of P1 billion.

• Naturals – Products with active ingredients derived from natural or herbal sources. Sales result from the following brands: Biolink VCO (Virgin Coconut Oil), Biolink Tea Tree Oil, Biolink Green Papaya, Extract (calamansi, papaya, avocado and cucumber), and Baby Spa.

• Health and wellness – Consists of products with naturally-derived ingredients which promote health and general well-being. Revenues are generated by Theraherb VCO.

14

The Skin care, Hair care and Naturals categories comprise the Personal care business of the Company. The following table shows the Company’s market leadership position tracked by A.C. Nielsen across several category/brand/product lines:

Splash Brand Market Share Market Standing

Maxi-peel Exfoliant Solution 82% Market LeaderSkinwhite Lotion 29% Market Leader Extract Lotion 4% Biolink GP Lotion 1%Total Splash (Whitening Lotion) 34%Skinwhite Soap 45% Market Leader Extract Soap 6% Biolink GP Soap 4%Total Splash (Whitening Soap) 55%Extract Facial Cleanser 10% Strong Challenger Biolink GP Facial Cleanser 3% Skinwhite Toner 1%Total Splash (Facial Cleanser) 14%Kolours Hair Dye 58% Market LeaderSource: AC Nielsen Retail Audit, 31 Dec 2008

3. Marketing

The Company is positioned as a marketer of innovative personal care products. This positioning combined with an effective communication, pricing, sales and distribution strategies, provide a compelling value proposition for the Philippine mass market. Through new product launches and product reformatting, the Company keeps market excitement for its brands and product lines at high levels, resulting in market share growth. The Company uses television, radio and print advertising as well as in-store activities and promotions to communicate the benefits and features of its products to consumers. In addition to nationwide advertising programs, regional campaigns are also undertaken to increase consumer demand in specific geographic markets. The Company develops annual brand marketing plans that are based on market studies, trend analyses, focus groups, surveys, and portfolio reviews. These marketing plans go through an intensive approval process that forms part of the Company’s strategic and annual business planning cycle. Post-implementation evaluation studies are done to assess the effectiveness of the marketing initiatives and approaches.

4. Selling and Distribution

The Company’s distribution network consists of in-house and third party distributors. The Company delivers directly to strategic accounts, or what it calls the National Accounts Group (NAG). These accounts are Super Value, Inc. and Super SM (of the SM Group), Mercury Drug Inc., Watson’s, Robinson’s, HBC and IDS Philippines Inc. . For other key accounts and outlets, Splash utilizes twenty-four (24) third party distributors which are assigned specific territories.

Apart from National Accounts, Splash products are also sold to two other major trade groups: Modern Trade and General Trade. Modern Trade consists of all large accounts outside of NAG such as the Gaisano Group, Ever Gotesco, Puregold, Cherry Foodarama, and The Landmark. General Trade is composed of small retail trade outlets including groceries, stand-alone drugstores, sari-sari stores and market stalls.

15

The table below summarizes percent contribution to sales, indicating relative balance of revenue sources. The largest contributor is General Trade which accounted for 41% of sales in 2008.

2008 2007

National Accounts 28% 29% Splash Corp.Modern Trade 31% 32%General Trade 41% 39%Totals 100% 100%

Account Group

Distributors

Contribution to Total SalesServed By

In Metro Manila, South Luzon, North Luzon, and the Samar-Leyte islands, goods are delivered over land using third party service providers. For the rest of Visayas and Mindanao regions, delivery is by sea using third party service providers. The Company employs demand-based production planning and inventory management systems. Each distributor maintains an optimal level of inventory which is automatically replenished whenever inventory levels fall to re-order point. The following diagram illustrates the Company’s distribution network in the Philippines:

Internationally, the Company has established market presence in 38 countries through its distributors and local consolidators. These countries include the ASEAN counties, China/Hong Kong, Japan, Korea, India, and countries in the Middle East (United Arab Emirates and Saudi Arabia among them) and in Africa (notably Nigeria).

5. Manufacturing Facilities

The Company’s industrial plant, where substantially all of its manufacturing are conducted, is situated at F. Lazaro Street, West Canumay, Valenzuela City with an estimated lot area of 29,410 square meters and buildings with a total floor area of 20,910 square meters. The properties and structures located in the plant include the following: Production Building, Finished Goods Warehouse, the Splash Research Institute Building, Chemical Storage Building, Soap Plant, Canteen, Power House, Engineering Building, Substation, Recovery Warehouse, Guard House, Multi-purpose Hall, Alcohol Storage, and the Waste Water Treatment Plant.

Supermarkets

Department Stores GT

24 National Distributors

Splash Factory or Warehouse

Minimarts MT

Convenience Stores

Small Pharmacies

National Accounts

16

6. Manufacturing Facilities

The Company established the Splash Research Institute (SRI) to continuously develop, by employing cutting-edge technology, new products that will meet the growing needs of the personal care market. It adopted the “open innovation” concept whereby the Company collaborates with its suppliers to come up with new and better product formulations in a cost effective manner. It also developed a flexible brand and product creation process that allows it to quickly respond to changes in consumer preferences. The Company strives to have at least two (2) years worth of new products in the pipeline at any given time. SRI departments (Product Research and Development, Packaging Innovations, Product Testing and Documentation, and Skin Research) work interdependently towards creating innovative products which address the felt and latent needs of consumers.

17

D. OTHER MATTERS

1. Legal Proceedings

During the past 5 years, 2004-2008, there has been no pending Legal Proceeding, Bankruptcy petition, or conviction by final judgment, against any Director and Executive Officer of the Registrant that is material to an evaluation of their ability or integrity to become a Director or Executive Officer of the Company. Neither has any of them been subject to any Order, Judgment, or Decree, nor involved in any proceeding for violation of a Securities or Commodities law. There are pending legal cases against the Company that are being contested by the Company and its legal counsels. Management and its legal counsels believe that the final resolution of these cases will not have material effect on the financial position and operating results of the Company.

2. Vote on Certain Matters

The Board of Directors recommends a vote on the following matters: (i) Election of the seven (7) members of the Board who are indicated above. (ii) Appointment of External Auditor. (iii) The President’s Report, Annual Report and the Financial Report as of December 31,

2008 will be submitted to the stockholders for their approval. Likewise, the stockholders will be asked to confirm and ratify the resolutions or actions of the outgoing Board of Directors and the Management of the Company in 2008, on matters related to budget, cost control and cost reduction measures, and marketing strategies. The resolutions adopted by the Board in 2008 pertain to: a) Approval to sell the shares of stock of the Corporation in Professional Services, Inc.; b) Approval of Share Buy Back Program; c) Approval of the Amendment of the Articles of Incorporation by a majority of the Board

of Directors and the Stockholders; d) MOU with IDS Philippines, Inc.; e) Approval to buy back shares owned by Splash Holdings, Inc.; f) Approval for a new subsidiary in Indonesia; g) Authority to open or close bank accounts, and designation of authorized signatories;

and h) Authority to sell used motor vehicles.

(iv) Declaration of Dividends for stockholders on record as of May 20, 2009.

3. Voting Procedures

The voting procedure for election and approval of corporate action in which Stockholders’ approval will be required shall be by “viva voce” unless voting by balloting is demanded by the stockholders representing at least 20% of the outstanding capital stock entitled to vote. (i) The vote required for approval

The approval of any corporate action shall require the majority vote of all stockholders present either in person or represented by proxy in the meeting, if constituting a quorum, except the Amendment to the Articles of Incorporation which shall require two-thirds vote. For election of Directors, Section 24 of the Corporation Code shall apply.

18

(ii) The methods by which vote will be counted

Except in cases where voting by ballot is required by law, voting and counting shall be by “viva voce”. If by ballot, counting shall be supervised by external auditors.

19

SIGNATURE PAGE

After reasonable inquiry and to the best of my knowledge and belief, I certify that the information set

forth in this report is true, complete and correct. This report is signed in the City of Quezon City on May

18, 2009

By: RAMON G. TRAJANO Chief Financial Officer

20

MANAGEMENT REPORT

1. Audited Financial Statements and Interim Financial Statements

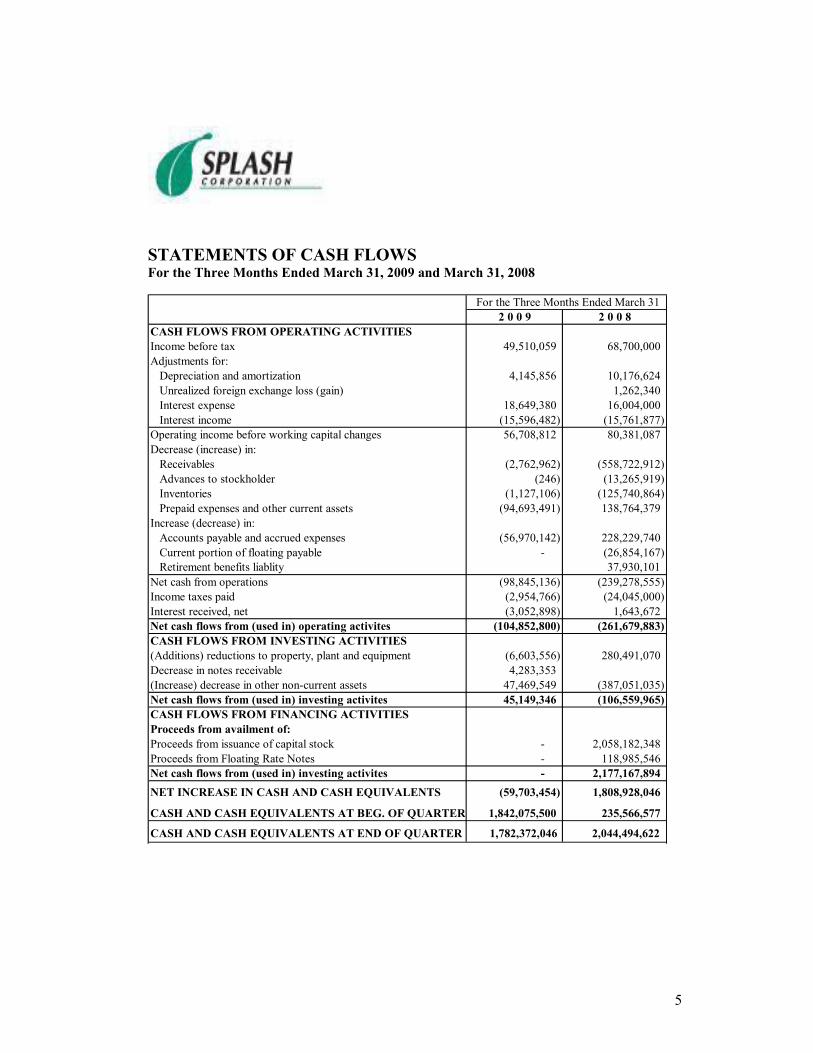

Registrant incorporates by reference the Annual Report containing the financial report of the corporation as of December 31, 2008, and other related information. Accompanying this Annual Report is the Statement of Management’s Responsibility for Financial Statements The Annual Report will be handed to stockholders together with this Information Statement and copies of the Minutes of the June 21, 2008 Annual Stockholders’ Meeting. The interim financial statements for the first quarter of 2009 are also provided.

2. Management’s Discussion and Analysis

21

Revenues Net sales in 2008 was Php3.165 million, Php154.4 million or 5.1% higher than last year. In spite of adverse economic conditions marked by record oil price increases and the global financial crisis in 2008, revenue growth was achieved by sustained marketing activities and new product introductions.

Amounts in Php 000s 2008 2007 2006

Net sales 3,165,224 3,010,832 2,399,082Change 154,392 611,750 ‐294,233 % 5.1% 25.5% ‐10.9%

The Company introduced the following new products in 2008:

• Extraderm New Generation Sunblock Cream

• Maxi-Peel Facial Cleanser

• Maxi-Peel Exfoliant Neck & Body Lotion

• Maxi-Peel Exfoliant Soap

• Maxi-Peel Exfoliant Cream

• Skin White Power Whitening Lotion

• Skin White Power Whitening Bath Soap

• Skin White Power Whitening Face Cream Powder

• Skin White Milk Soap

• Skin White Glutathione Lotion

• Skin White Glutathione Bath Soap

• Skin White Gluta Capsules

• Extract Whitening Face Cream Sales from these new products contributed 23% of revenues in 2008.

22

Business Segments and Market Performance The tables below shows shares in the domestic and international segments, broken down further by product category. The split of domestic to international sales (92% to 8%) remained unchanged in 2008 and 2007. In the core skin care category, share of domestic sales was 91% in 2008, up from 87% in 2007. This resulted from the 40% growth in domestic sales of skin care products from Php1.481 billion in 2007 to Php2.066 billion in 2008 (when Skin White and Maxi-Peel reached P1 billion in sales). For hair care, share of domestic sales was virtually relative flat year on year (98% in 2008 versus 99% in 2007)

Personal Care: Skin Care 2,066,794 91% 209,238 9% 2,276,032 100% Hair Care 511,662 98% 9,887 2% 521,549 100% Naturals 266,903 85% 46,459 15% 313,362 100% Other 8,489 100% ‐ 0% 8,489 100% Total Personal Care 2,853,848 91% 265,583 9% 3,119,431 100%Health and Wellness 45,004 98% 789 2% 45,793 100%Totals 2,898,852 92% 266,372 8% 3,165,224 100%

TotalNet Sales ‐ 2008 (Amounts in Php 000s)

Product CategoryDomestic Int'l

Personal Care: Skin Care 1,481,295 87% 213,487 13% 1,694,782 100% Hair Care 536,414 99% 7,143 1% 543,557 100% Naturals 628,519 97% 19,866 3% 648,385 100% Other 105,000 100% ‐ 0% 105,000 100% Total Personal Care 2,751,228 92% 240,496 8% 2,991,724 100%Health and Wellness 13,812 72% 5,302 28% 19,114 100%Totals 2,765,040 92% 245,798 8% 3,010,838 100%

Product CategoryNet Sales ‐ 2007 (Amounts in Php 000s)

TotalDomestic Int'l

In 2008, the lead brands of the skin care category continue to maintain market leadership as shown by market share data from AC Nielsen summarized in the preceding table (Products and Brands).

Expenses As shown by the cost summary table below, total cost and operating expenses increased by Php221 million (8.2%) to Php2.908 billion in 2008. (By comparison, total costs rose by Php535 million to Php2.687 billion in 2007). The increase in 2008 was largely due to the Php192 (15.9%) million rise in operating costs. Cost of goods sold increased by Php29 million (2%) to Php1.504 billion in 2008 Operating expenses increased in 2008 mainly as a result of the Php194 million (26.9%) rise in advertising and promotions (Php916 million in 2008) as the Company intensified its marketing and brand building initiatives in 2008. Increases in personnel costs (Php47 million:27%) and transportation and travel expenses (Php25 milllion: 37%) were largely offset by declines in other expense categories notably outside services (down Php43 million or 59.5%), and bad debts expense (lower by Php15 million or 76.3%).

23

Amounts in Php 000s 2008 2007 2006Net Sales 3,165,224 3,010,832 2,399,082 Cost of goods sold 1,504,004 1,475,161 1,093,979

% to Net sales 47.5% 49.0% 45.6%Advertising and promotions 916,440 722,013 648,145 Personnel costs 221,093 174,049 122,300 Transportation and travel 92,229 67,327 43,681 Outside services 29,250 72,136 124,682 Taxes and licenses 22,521 18,071 17,338 Rent 20,583 11,939 8,173 Depreciation and Amortization 20,477 16,278 32,151 Insurance 13,032 13,663 10,020 Communication, light and water 11,234 11,895 6,561 Membership, dues and subscriptions 5,628 7,173 1,774 Provision for doubtful accounts 4,732 19,948 3,000 Repairs and maintenance 3,849 4,257 3,200 Research and development 3,404 11,050 6,068 Supplies 2,571 7,548 5,826 Product samples and give‐aways 1,964 7,511 3,757 Others 34,668 46,535 20,729 Total operating expenses 1,403,677 1,211,395 1,057,403

% to Net sales 44.3% 40.2% 44.1%

Total COGS and expenses 2,907,680 2,686,556 2,151,382 % to Net sales 91.9% 89.2% 89.7%

Profitability Gross profit margin improved to 10.5% of sales in 2008, from 4.1% in 2007 as a result of lower costs of goods. With higher operating expenses however, operating profit margin declined to 8.1% in 2008 from 10.8% the previous year. Net income margin of 9.4% in 2008 is virtually flat to 9.3% for 2006 and 2007

Amounts in Php 000s 2008 2007 2006Net sales 3,165,224 3,010,832 2,399,082Cost of goods sold 1,504,004 1,475,161 1,093,979Gross profit 1,661,221 1,535,671 1,305,103 Margin 10.5% 4.1% 19.3%Operating expenses 1,403,677 1,211,395 1,057,403

Operating profit 257,544 324,276 247,700 Margin 8.1% 10.8% 10.3%

Net income after tax 297,734 279,271 223,607 % to net sales 9.4% 9.3% 9.3%

24

. The following two tables summarize segment profitability. The domestic business segment accounted for 90% of gross profits in 2008, unchanged from the previous two years; and delivered 67% of operating profit in 2008 and 2007.

2008 2007 2006 Domestic 1,498,467 90% 1,380,735 90% 1,175,144 90% International 162,754 10% 154,936 10% 129,959 10%Totals 1,661,221 100% 1,535,671 100% 1,305,103 100%

Business SegmentGross Profit (Amounts in Php 000s)

2008 2007 2006 Domestic 172,283 67% 217,796 67% 170,612 69% International 85,261 33% 106,480 33% 77,089 31%Totals 257,544 100% 324,276 100% 247,701 100%

Operating Profit (Amounts in Php 000s)Business Segment

Key Indicators The table which follows summarizes the Company’s key financial and market share measures. It shows that year on year, net sales grew by 5.1%; net income after tax (NIAT) improved by 6.6%; and EBITDA increased by 1.3%. EBITDA margin was 10.9% in 2008 versus 11.3% in 2007. Turnover of both trade receivables and inventory declined: 3.5 for receivables in 2008 (from 5.0 the previous year); 4.2 for inventory in 2008 (from 5.8 in 2007)

Key Indicators 2008 2007 Change

Amounts in Php millionsNet Sales 3,165.2 3,010.8 5.1%Sales of new products 736.9 482.0 52.9%Net income after tax 297.7 279.3 6.6%EBITDA 346.0 341.4 1.3% Margin 10.9% 11.3% ‐0.4%

Trade receivables turnover 3.5 5.0 ‐1.5Inventory turnover 4.2 5.8 ‐1.5

Market shares of core brands* Maxi-peel Exfoliant 82% 81% 1.0% Skin White Lotion 29% 25% 4.0% Skin White Soap 45% 36% 9.0% Extract Facial Clenser 10% 11% ‐1.0% Kolours Hair Dye 58% 49% 9.0%*Source: AC Nielsen Retail Audit, 31 Dec 2008

25

Liquidity and capital resources

The Company remains liquid with current assets more than four times current liabilities, resulting in current ratios of 4.2 and 4,4 in 2008 and 2007, respectively. Net cash flow from operations was Php321 million in 2008 compared to Php103 million in 2007, while cash flow from investing activities was Php 26 million in 2008 compared to a net outflow of Php128 million the previous year.

Total equity was relatively flat at Php2.677 billion in 2008 versus Php 2.712 billion in 2007. Debt to equity ratio was steady at 0.7 in both years.

Amounts in Php millions 2008 2007

Current assets 3,548.3 3,547.7Current liabilities 850.3 809.5 Current ratio 4.2 4.4

Cash flow from operations 320.9 103.3Cash flow from investing activities 26.4 (127.5)

Total Equity 2,676.7 2,711.8Debt to equity 0.7 0.7

3. Market Information

The Company’s common shares are traded at the Philippine Stock Exchange. The table below summarizes the monthly high, low and closing prices for the months of Q4/2008, as well as the closing share prices for the first nine months of 2008:

Q4/2008 High Low CloseOctober 6.10 3.00 3.40November 3.45 2.60 3.40December 3.65 2.70 3.00

Q1 to Q4/2008 CloseJanuary 6.30February 6.20March 5.30April 4.50May 4.80June 4.40July 3.85August 3.70September 5.60

26

4. Stockholders

The following table is a list of the top stockholders as of April 30, 2009

Rank

Stock- holder

No. Stockholder Citizenship Holdings %1 1 SPLASH HOLDINGS INC. FILIPINO 492,009,214 71.17%2 9 PCD NOMINEE CORP.(FIL.) FILIPINO 92,655,107 13.40%3 10 PCD NOMINEE CORP. (NON-FIL.) FOREIGN 104,980,500 15.19%4 483 YAO ALFREDO M. FILIPINO 599,000 0.09%5 20 ENRILE WILLIAM T. FILIPINO 320,000 0.05%6 498 COBANKIAT JOHNNY FILIPINO 111,000 0.02%7 495 GOTIANSE PAUL L. FILIPINO 100,000 0.01%8 481 BAYOG ROMEO D. FILIPINO 56,000 0.01%9 482 KHO DAVID LIMQUECO FILIPINO 50,000 0.01%

10 19 DUY WINSTON L. FILIPINO 50,000 0.01%11 479 YAO ANNIKA SHERRYN FILIPINO 50,000 0.01%12 500 QUALITY INVESTMENTS & SECURITIES CORPORATION FILIPINO 50,000 0.01%13 501 ZANTUA NILO C. FILIPINO 50,000 0.01%14 502 SOLINAP GERONIMO A. FILIPINO 30,000 0.00%15 485 REYES ANNA KARENINA E. FILIPINO 23,000 0.00%16 488 OLIVEROS FEDERICO S. JR. FILIPINO 20,000 0.00%17 497 PABLO DELLA LOUISE A. FILIPINO 15,000 0.00%18 499 GO IRENE CHAN FILIPINO 10,000 0.00%19 489 SOLOMON ANTONINA SABLAN FILIPINO 10,000 0.00%20 21 SANTOS ALFREDO M. FILIPINO 10,000 0.00%

Total Top 20 Shareholders 691,198,821 99.99%Other 91,505 0.01%Total Outstanding Shares 691,290,326 100.00%

5. Dividends

Below are details of cash dividends declared and paid in 2007 and 2008: Declaration Date Dividend per Share Amount Record Date August 31, 2007 P 1.59 P 350,000,000 August 31, 2007

June 19, 2008 P 0.18 134,308,864 May 22, 2008

Declaration and payment of dividends in the aggregate for any given year shall not exceed 50% of the Company’s net income after tax as stated in the Company’s audited financial statements for the most recent fiscal year as provided for in the negative covenants of its Floating Rate Note (FRN) Agreement.

6. Sales of unregistered securities

There were no recent sales of unregistered or exempt securities including recent issuance of securities constituting an exempt transaction.

27

7. Governance Practices

a) The Company’s Manual of Corporate Governance and the 2008 Corporate Governance Scorecard for Publicly Listed companies prepared by the Institute of Corporate Directors in collaboration with the Philippine Stock Exchange and the Securities and Exchange Commission serve as the bases of an evaluation system established by the Company to measure or determine the level of compliance of the Board of Directors and top-level management with good governance practices

b) Measures consistently undertaken by the Company to fully comply with leading practices

in good corporate governance include:

i. The offer of equitable shares of the profits or cash dividends to the shareholders; ii. The shareholders’ opportunity to elect each board member individually through voting

by ballots during the Annual General Meeting; iii. The observance of at least two (2) weeks for the notice to call shareholders for the

Annual General meeting; iv. Adequate information on the individual profile of the new directors and the returning

directors; v. Adequate public information on the Company’s ownership structure; vi. The opportunity of the shareholders to ask questions/raise issues in the Annual

General Meeting and on meetings duly constituted for the purpose; vii. The prompt disclosure to the Philippine Stock Exchange and the Securities and

Exchange Commission of material information or events occurring in the Company; viii. The provision of a retirement fund for its employees which is held in a trust fund with

Metrobank; ix. The continuous honoring of the Company’s debt agreements and timely payment of

its debt obligations; x. The recognition by the Company of its broader obligations to society and/or the

community through the projects and activities of the Splash Foundation, Inc.; xi. The existence of an internal audit operation as a separate unit in the Company

c) There has been no deviation from the Company’s Manual of Corporate Governance as of

31 December 2008. d) As the need arises or in compliance with other leading governance practices, the

Company intends to adopt other measures which will improve its corporate governance. The Company undertakes to provide without charge to each person, on the written request of any such person, a copy of its annual report on SEC Form 17-A, indicating in the copy the name and address of the requesting person.

37

38

*SGVMC308954*

Splash Corporation (A Subsidiary of Splash Holdings, Inc.)

Financial Statements December 31, 2008 and 2007 and Years Ended December 31, 2008, 2007 and 2006 and Independent Auditors’ Report SyCip Gorres Velayo & Co.

A S 0 9 1 9 6 2 0 6

SEC Registration Number

S P L A S H C O R P O R A T I O N

( A S u b s i d i a r y o f S p l a s h

H o l d i n g s , I n c . )

(Company’s Full Name)

H B C C o r p o r a t e C e n t r e

5 4 8 M i n d a n a o A v e n u e c o r n e r

Q u i r i n o H i g h w a y , Q u e z o n C i t y

(Business Address: No. Street City/Town/Province)

Mr. Ramon G. Trajano 984-5555 (Contact Person) (Company Telephone Number)

1 2 3 1 A A F S 0 4 1 9Month Day (Form Type) Month Day

(Calendar Year) (Annual Meeting)

Not Applicable (Secondary License Type, If Applicable)

Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings

153 Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S Remarks: Please use BLACK ink for scanning purposes.

COVER SHEET

SPLASH CORPORATION (A Subsidiary of Splash Holdings, Inc.) BALANCE SHEETS December 31

2008

2007(As restated,

Note 2)ASSETS Current Assets Cash and cash equivalents (Notes 4 and 15) P=1,842,075,488 P=1,975,037,566Receivables - net (Notes 5, 8, 11 and 15) 1,087,810,564 1,024,454,563 Current portion of note receivable (Notes 8 and 15) 54,215,416 50,030,502 Advances to a stockholder (Note 15) 137,370,246 137,370,246 Inventories - net (Note 6) 381,756,239 328,675,357 Prepaid expenses and other current assets (Note 7) 45,023,355 32,155,443 Total Current Assets 3,548,251,308 3,547,723,677 Noncurrent Assets Note receivable- net of current portion (Notes 8 and 15) 150,091,505 200,122,007 Property, plant and equipment - net (Note 9) 272,065,531 294,573,396 Available-for-sale investments (Note 10) 215,945,000 219,770,000 Land for development (Note 11) 141,956,454 141,956,454 Deferred income tax assets (Note 20) 33,193,965 37,045,274 Other noncurrent assets (Note 20) 56,948,398 56,422,097 Total Noncurrent Assets 870,200,853 949,889,228TOTAL ASSETS P=4,418,452,161 P=4,497,612,905 LIABILITIES AND EQUITY Current Liabilities Accounts payable and accrued expenses (Note 12) P=803,343,598 P=762,491,968 Current portion of floating rate notes payable (Note 13) 46,923,404 46,990,002 Total Current Liabilities 850,267,002 809,481,970 Noncurrent Liabilities Floating rate notes payable - net of current portion (Note 13) 891,503,397 938,426,801 Retirement benefits liability (Note 18) – 37,930,101 Total Noncurrent Liabilities 891,503,397 976,356,902 Total Liabilities 1,741,770,399 1,785,838,872 Equity (Note 14) Capital stock 746,160,357 746,160,357Additional paid-in capital 1,676,712,406 1,676,712,406 Unrealized valuation gain on available-for-sale investments (Note 10) 718,100 4,543,100 Cumulative actuarial gain (loss) on defined benefit plan (Note 2) 13,962,294 (27,524,027)Treasury stock (236,178,536) – Retained earnings (Note 2) 475,307,141 311,882,197Total Equity 2,676,681,762 2,711,774,033 TOTAL LIABILITIES AND EQUITY P=4,418,452,161 P=4,497,612,905 See accompanying Notes to Financial Statements.

SPLASH CORPORATION (A Subsidiary of Splash Holdings, Inc.) STATEMENTS OF RECOGNIZED INCOME AND EXPENSE FOR THE YEARS ENDED DECEMBER 31, 2008, 2007 AND 2006 December 31 2008 2007 2006

Actuarial gain (loss) on defined benefit plan (Notes 2, 18 and 22) P=73,227,686 (P=6,524,288) (P=27,957,832)Adjustment on asset ceiling (Notes 18 and 22) (21,454,563) – –Effect of deferred income tax (10,286,802) (1,512,917) 9,835,789Net actuarial gain (loss) on defined benefit plan

and adjustment on asset ceiling 41,486,321 (8,037,205) (18,122,043)Unrealized gain (loss) on available-for-sale

investments (3,825,000) 5,520,000 1,400,000

NET INCOME (EXPENSE) RECOGNIZED DIRECTLY IN EQUITY 37,661,321 (2,517,205) (16,722,043)

NET INCOME FOR THE YEAR 297,733,808 279,270,860 223,606,843

TOTAL RECOGNIZED NET INCOME FOR THE YEAR P=335,395,129 P=276,753,655 P=206,884,800

See accompanying Notes to Financial Statements.

SPLASH CORPORATION (A Subsidiary of Splash Holdings, Inc.) STATEMENTS OF INCOME Years Ended December 31

2008

2007 (As restated,

Note 2)

2006 (As restated,

Note 2)

NET SALES (Notes 11 and 15) P=3,165,224,133 P=3,010,832,030 P=2,399,082,430

COST OF GOODS SOLD (Notes 11 and 16) 1,504,003,578 1,475,161,239 1,093,979,127

GROSS PROFIT 1,661,220,555 1,535,670,791 1,305,103,303

OPERATING EXPENSES (Note 17)

(1,403,676,775)

(1,211,395,081)

(1,057,402,607)

INTEREST INCOME (Notes 4, 8, 15 and 19)

96,206,842

36,022,712

2,580,950

INTEREST EXPENSE (Notes 13 and 19) (73,015,901) (74,509,990) (62,655,776)

OTHER INCOME (CHARGES) Foreign exchange gain (loss) - net (Note 7) 14,515,826 (14,836,325) (7,330,087)Provision for probable loss (Note 27) (12,000,000) – – Reversal of excess provision (Note 12) – – 60,461,525 Others 13,583,176 7,619,896 3,328,078

INCOME BEFORE INCOME TAX 296,833,723 278,572,003 244,085,386

PROVISION FOR (BENEFIT FROM) INCOME TAX (Note 20)

(900,085)

(698,857)

20,478,543

NET INCOME P=297,733,808 P=279,270,860 P=223,606,843

Earnings Per Share (Note 23) P=0.40 P=0.98 P=2.08 See accompanying Notes to Financial Statements.

SPLASH CORPORATION (A Subsidiary of Splash Holdings, Inc.) STATEMENTS OF CASH FLOWS Years Ended December 31 2008 2007 2006 CASH FLOWS FROM OPERATING ACTIVITIES Income before income tax P=296,833,723 P=278,572,003 P=244,085,386 Adjustments for: Interest income (Note 19) (96,206,842) (36,022,712) (2,580,950) Interest expense (Note 19) 73,015,901 74,509,990 62,655,776 Depreciation and amortization (Notes 9 and 17) 47,348,669 50,731,775 78,113,226 Provision for probable loss 12,000,000 – – Unrealized foreign exchange loss (gain) (9,010,630) 12,220,520 1,040,176 Dividend income (3,785,844) – – Gain on sale of property and equipment (2,109,119) (814,489) (736,742) Reversal of excess provision (Note 12) – – (60,461,525)Operating income before working capital changes 318,085,858 379,197,087 322,115,347 Decrease (increase) in: Receivables (54,600,894) (329,449,802) (179,231,185) Inventories (53,080,882) (146,216,699) 60,270,048 Prepaid expenses and other current assets (2,280,625) (49,497,453) 4,540,752 Increase (decrease) in: Accounts payable and accrued expenses 22,557,793 274,989,605 (34,433,608) Retirement benefits liability (Note 18) 13,843,022 (15,593,621) (120,328)Net cash generated from operations 244,524,272 113,429,117 173,141,026 Interest received 92,456,323 3,756,502 2,580,950 Income taxes paid (16,122,695) (13,918,678) (19,514,404)Net cash flows from operating activities 320,857,900 103,266,941 156,207,572 CASH FLOWS FROM INVESTING ACTIVITIES Collection of note receivable (Note 8) 45,845,588 – – Additions to property, plant and equipment (Note 9) (24,887,804) (20,585,127) (2,901,900)Dividends received 3,785,844 – – Increase in other noncurrent assets (526,300) (1,175,477) (665,880)Proceeds from sale of property and equipment 2,156,119 1,424,276 1,067,375Cash advances to a stockholder – (117,012,421) (52,986,905)Decrease in other investments – 9,835,205 – Net cash flows from (used in) investing activities 26,373,447 (127,513,544) (55,487,310)CASH FLOWS FROM FINANCING ACTIVITIES Acquisition of treasury stock (Note 14) (236,178,536) – – Payments of: Dividends (134,308,864) (350,000,000) – Interest (66,642,984) (70,431,990) (62,655,776) Floating rate notes (46,990,002) – – Bank loans – (640,000,000) (220,000,000)Proceeds from issuance of capital stock - net (Note 14) – 2,058,182,348 – Proceeds from availment of: Floating rate notes – 985,416,803 433,500,000 Bank loans – 280,000,000 270,000,000 Payment of long-term debt – (367,173,612) (499,826,389)Net cash flows from (used in) financing activities (484,120,386) 1,895,993,549 (78,982,165)EFFECT OF EXCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS 3,926,961

(8,569,832) (137,747)

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS (132,962,078)

1,863,177,114 21,600,350

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 1,975,037,566

111,860,452 90,260,102

CASH AND CASH EQUIVALENTS AT END OF YEAR (Notes 4 and 15) P=1,842,075,488 P=1,975,037,566 P=111,860,452 See accompanying Notes to Financial Statements.

SPLASH CORPORATION (A Subsidiary of Splash Holdings, Inc.) NOTES TO FINANCIAL STATEMENTS 1. Corporate Information General Splash Corporation (the Company) was incorporated in the Philippines and registered with the

Philippine Securities and Exchange Commission (SEC) on September 30, 1991 primarily to develop, manufacture, bottle, pack, and market cosmetics and other beauty products, and pharmaceutical products in the Philippines and abroad. On March 4, 2009, the SEC approved the Company’s amendment of the primary purpose of the Articles of Incorporation to include the development or acquisition of technology to manufacture and sell personal care, pharmaceuticals, food, health, home, household care and other ancillary products in the Philippines and abroad. Before the Company listed its shares of stock with the Philippine Stock Exchange (PSE) on November 15, 2007, the Company is a wholly-owned subsidiary of Splash Holdings, Inc. (SHI).

On November 15, 2007, the Company’s shares of stock were listed and traded in the PSE. After

the Initial Public Offering (IPO) wherein the Company offered 30% of its outstanding shares (both primary and secondary) to the public, the Company became 70%-owned by SHI. On December 4, 2008, the BOD approved to buyback the Company’s shares of stock totalling 30.30 million shares held by SHI (see Note 14f). After the buyback, SHI’s ownership in the Company increased from 70% to 71.17%, and SHI continues to exercise control over the Company (see Note 14).

The Company’s registered office address is HBC Corporate Centre, 548 Mindanao Avenue corner Quirino Highway, Quezon City.

The accompanying financial statements were authorized for issuance by the BOD on April 14, 2009.

2. Summary of Significant Accounting and Financial Reporting Policies

Basis of Financial Statement Preparation The accompanying financial statements have been prepared under the historical cost basis, except for derivative financial instruments and available-for-sale (AFS) financial assets which have been measured at fair value. The financial statements are presented in Philippine peso, which is the Company’s functional currency.

Statement of Compliance The Company’s financial statements have been prepared in conformity with Philippine Financial Reporting Standards (PFRS).

Changes in Accounting Policies and Disclosures The accounting policies adopted are consistent with those of the previous financial year, except for the following: • PFRS 8, Operating Segments. The Company early adopted PFRS 8 which will become

effective on January 1, 2009. PFRS 8 replaces PAS 14, Segment Reporting, and adopts a full management approach to identifying, measuring and disclosing the results of an entity’s

- 2 -

operating segments. The information reported is that which management uses internally for evaluating the performance of operating segments and allocating resources to those segments. Such information may be different from that reported in the balance sheet and statement of income, and the Company will provide explanations and reconciliations of the differences, if any. The adoption of this standard resulted in a change in the reportable segments from business segments consisting of naturals, skin care and hair care to geographical areas where the Company’s products are sold. Comparatives for 2007 and 2006 have been restated. The changes of disclosures relating to segment information are fully discussed in Note 21 to the financial statements.

• In 2008, the Company changed its accounting policy for actuarial gains or losses from

immediate recognition as income or expense to full recognition directly in equity under the statement of recognized income and expense (SORIE). This is to align the Company’s accounting policy with comparable companies within the industry.

The change in accounting policy was accounted for retroactively which resulted in the following:

Increase (Decrease)

December 31,

2007December 31,

2006 January 1,

2006 Retained earnings P=8,037,205 P=18,122,043 P=1,364,779 Actuarial loss on defined benefit plan 8,037,205 18,122,043 1,364,779 Retirement benefits cost (6,524,288) (27,957,832) – Provision for income tax - deferred (1,512,917) 9,835,789 –

Additional disclosures required as a result of the change in accounting policy were made in the financial statements (see Notes 18 and 22).

The following Philippine Interpretations International Financial Reporting Interpretations Committee (IFRIC) interpretations which became effective on January 1, 2008 and an amendment to an existing Philippine Accounting Standard (PAS) that became effective on July 1, 2008 are determined by management to be not relevant and not applicable to the Company. • Philippine Interpretation IFRIC 11, PFRS 2, Group and Treasury Share Transactions

This Interpretation addresses issues relating to whether transactions should be accounted for as equity-settled or as cash-settled under PFRS 2 and issues concerning share-based payment arrangement involving entities within the same group. The Company has no share-based payments.

• Philippine Interpretation IFRIC 12, Service Concession Arrangements

This Interpretation applies to contractual arrangements whereby a private sector party participates in the development, financing, operation and maintenance of infrastructure for public sector services. The Company has no service concession arrangements.

• Philippine Interpretation IFRIC 14, PAS 19 - The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction Philippine Interpretation IFRIC 14 addresses how to assess the limit under PAS 19, Employee Benefits, on the amount of the pension scheme surplus that can be recognized as an asset in balance sheet, in particular, when a minimum funding requirement exists. This Interpretation has no impact on the Company’s financial statements.

- 3 -

• Amendments to PAS 39, Financial Instruments: Recognition and Measurement, and PFRS 7, Financial Instruments: Disclosures - Reclassification of Financial Assets Entities are not permitted to reclassify financial assets in accordance with the amendments before July 1, 2008. Any reclassification of a financial asset made in periods beginning on or after November 15, 2008 will take effect only from the date the reclassification is made. The amendments to PAS 39 permit an entity to: (1) reclassify non-derivative financial assets (other than those designated at fair value through profit or loss by the entity upon initial recognition) out of the fair value through profit or loss category if the financial asset is no longer held for the purpose of selling or repurchasing it in the near term in particular circumstances; and (2) transfer from the available-for-sale category to the loans and receivables category a financial asset that would have met the definition of loans and receivables (if the financial asset had not been designated as available-for-sale), if the entity has the intention and ability to hold that financial asset for the foreseeable future. This amendment had no impact on the Company’s financial statements.

New Accounting Standards, Interpretations and Amendments to

Existing Standards Effective Subsequent to December 31, 2008 The Company will adopt the following standards, amendment to existing standard and Interpretations enumerated below when these become effective. Except as otherwise indicated, the Company does not expect the adoption of these new and amended PFRS and Philippine Interpretations to have significant impact on its financial statements.

Effective in 2009

• PFRS 1, First-time Adoption of Philippine Financial Reporting Standards - Cost of an Investment in a Subsidiary, Jointly Controlled Entity or Associate The amended PFRS 1 allows an entity, in its separate financial statements, to determine the cost of investments in subsidiaries, jointly controlled entities or associates (in its opening PFRS financial statements) as one of the following amounts: a) cost determined in accordance with PAS 27; b) at the fair value of the investment at the date of transition to PFRS, determined in accordance with PAS 39; or c) previous carrying amount (as determined under generally accepted accounting principles) of the investment at the date of transition to PFRS.

• PFRS 2, Share-based Payment - Vesting Condition and Cancellations The standard has been revised to clarify the definition of a vesting condition and prescribes the treatment for an award that is effectively cancelled. It defines a vesting condition as a condition that includes an explicit or implicit requirement to provide services. It further requires non-vesting conditions to be treated in a similar fashion to market conditions. Failure to satisfy a non-vesting condition that is within the control of either the entity or the counterparty is accounted for as cancellation. However, failure to satisfy a non-vesting condition that is beyond the control of either party does not give rise to a cancellation.

• Amendments to PAS 1, Presentation of Financial Statements

These Amendments introduce a new statement of comprehensive income that combines all items of income and expenses recognized in the profit or loss together with “other comprehensive income” (OCI). Entities may choose to present all items in one statement, or to present two linked statements, a separate statement of income and a statement of comprehensive income. These amendments also require additional requirements in the presentation of the balance sheet and owner’s equity as well as additional disclosures to be included in the financial statements.

- 4 -

• PAS 23, Borrowing Costs

The standard has been revised to require capitalization of borrowing costs when such costs relate to a qualifying asset. A qualifying asset is an asset that necessarily takes a substantial period of time to get ready for its intended use or sale. In accordance with the transitional requirements in the standard, the Company will adopt this as a prospective change. Accordingly, borrowing costs will be capitalized on qualifying assets with a commencement date after January 1, 2009. No changes will be made for borrowing costs incurred to this date that have been expensed.

• Amendments to PAS 27, Consolidated and Separate Financial Statements - Cost of an

Investment in a Subsidiary, Jointly Controlled Entity or Associate Amendments to PAS 27 will be effective on January 1, 2009 which has changes in respect of the holding companies separate financial statements including: (a) the deletion of “cost method”, making the distinction between pre- and post-acquisition profits no longer required; and (b) in cases of reorganizations where a new parent is inserted above an existing parent of the group (subject to meeting specific requirements), the cost of the subsidiary is the previous carrying amount of its share of equity items in the subsidiary rather than its fair value. All dividends will be recognized in profit or loss. However, the payment of such dividends requires the entity to consider whether there is an indicator of impairment.

• Amendment to PAS 32, Financial Instruments: Presentation and PAS 1 Presentation of

Financial Statements - Puttable Financial Instruments and Obligations Arising on Liquidation These amendments specify, among others, that puttable financial instruments will be classified as equity if they have all of the following specified features: (a) the instrument entitles the holder to require the entity to repurchase or redeem the instrument (either on an ongoing basis or on liquidation) for a pro rata share of the entity’s net assets; (b) the instrument is in the most subordinate class of instruments, with no priority over other claims to the assets of the entity on liquidation; (c) all instruments in the subordinate class have identical features; (d) the instrument does not include any contractual obligation to pay cash or financial assets other than the holder’s right to a pro rata share of the entity’s net assets; and (e) the total expected cash flows attributable to the instrument over its life are based substantially on the profit or loss, a change in recognized net assets, or a change in the fair value of the recognized and unrecognized net assets of the entity over the life of the instrument.

• Philippine Interpretation IFRIC 13, Customer Loyalty Programmes This Interpretation requires customer loyalty award credits to be accounted for as a separate component of the sales transaction in which they are granted and therefore part of the fair value of the consideration received is allocated to the award credits and realized in income over the period that the award credits are redeemed or expire.

• Philippine Interpretation IFRIC 16, Hedges of a Net Investment in a Foreign Operation