Embed Size (px)

Citation preview

Deutsche Bank German & Austrian Corporate Conference

21 May 2010, Frankfurt

Dr Eckhard Cordes, CEO

1Deutsche Bank German & Austrian Corporate Conference

This presentation contains forward-looking statements which are based on certain expectations and assumptions at the time of publication of this presentation and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed in these materials. Many of these risks and uncertainties relate to factors that are beyond METRO GROUP’s ability to control or estimate precisely, such as future market and economic conditions, the behaviour of other market participants, the ability to successfully integrate acquired businesses and achieve anticipated cost savings and productivity gains as well as the actions of government regulators. Readers are cautioned not to place undue reliance on these forward-looking statements, which apply only as of the date of this presentation. METRO GROUP does not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of these materials.

This presentation merely serves the purpose of providing information. It neither represents an offer for sale nor for subscription of securities in any country including the USA. This presentation does not include an official offer of shares; an offering circular will not be published.

This presentation is not allowed to be reproduced, distributed or published without prior agreement of METRO GROUP.

All numbers are before special items, unless otherwise stated.

Please note that new accounting standards have been applied. More information regarding the application of accounting methods refer to the notes to the Annual Report 2009.

Extra’s activities are disclosed as discontinued operations in 2007 and 2008. Figures at Other are adjusted for Adler’s activities in 2007, 2008 and 2009.

The figures in this presentation are rounded to provide a better overview. The calculation of deviations is based on figures incl. fractions. Therefore rounding differences can occur.

Disclaimer and Notes

2Deutsche Bank German & Austrian Corporate Conference

In Q1 Return to Profitable Growth - First Earnings Increase since 2008

€ million Q1 2009 Q1 2010 Change

Metro Cash & Carry 10 25 150.0%

Real -53 -24 53.4%

Media Markt and Saturn 79 81 3.1%

Galeria Kaufhof -27 -19 28.9%

Real Estate 132 138 4.7%

Other -56 -67 -19.6%

Consolidation 3 3 -

METRO GROUP 87 136 55.9%

Q4

-0.1%

Q3

-0.1%

Q2

0.0%

Q1

1.1%

Sales development (in local currency)

2009 2010

� Total sales grew by 2.3% to€15.5 billion(pre-currency: +1.0%)

-0.1%

Q1

1.0%

� Adjusted EBIT increased significantlyby 55.9% to €136 million

3Deutsche Bank German & Austrian Corporate Conference

Strategy of Profitable Growth

Customer Orientation

+ International Expansion

+ Efficiency

4Deutsche Bank German & Austrian Corporate Conference

New METRO GROUP

� First step:

- Dissolving of central structures

- Undivided responsibility for the

divisions

� Second step:

- New organisational structure for

Metro Cash & Carry:

Two business units with different

strategic priorities

- Integration of Metro Cash & Carry

and METRO AG headquarters

Real Estate

NewGroup Structure

Europe/MENAAsia/New Markets

5Deutsche Bank German & Austrian Corporate Conference

Leveraging Strong International Presence as Platform for Further Growth

3.5%24.1%31.9%40.5%Share of sales

75 (+10)439 (+38)596 (+21)1,017 (-53)No. of stores (∆ YTD)

2,320

∆€: +4.8%; ∆LC: +0.6%

15,766∆€: -12.8%; ∆LC: +1.4%

20,932

∆€: -0.3%; ∆LC:+0.3%

26,511 ∆: -0.6%

Sales (€ million)

-35 (-2)765 (-263)708 (+99)587 (-40)EBIT* (€ million) (∆ YoY)

Asia / AfricaEastern EuropeWestern EuropeGermany

1 12 14 6Countries

As at 31 December 2009* pre-consolidation

2009

6Deutsche Bank German & Austrian Corporate Conference

EBIT 2012Market conditions,

price investments

Additional EBIT

potential 2012

1,500

EBIT 2009

2,024

Shape contribution

Market conditions,

price investments

Expansion

800

700

208-405

2,222 -1

EBIT 2008

illustrative

Shape Contributed €208 million already in 2009

€ million

� €1.5 billion EBIT potential targeted by 2012

� €800 million in cost savings to be largely effective in 2011

€700 million in productivity gains fully effective in 2012

Cost savings

Productivity gains

7Deutsche Bank German & Austrian Corporate Conference

Shape 2012 Well on Track

17%

14%

13%29%

21%16%

Q1 2010Q4 2009

108%

18%

15%

40%

Q3 2009

98%

7%

15%

30%

Q2 2009

56%

Q1 2009

0%

42%

116%

28%

17%

5 Effective

4 Implemented

3 Approved

2 Evaluated

1 Idea

Achievement of Shape 2012 Targets

Implementation Levels:

Key Topics

� Customer orientation

� Procurement

� Private labels

� New business models

� In-store and admin.

processes

� Logistics and supply chain

management

8Deutsche Bank German & Austrian Corporate Conference

Metro Cash & Carry

� Leading global Cash & Carry wholesaler

� B2B: Serves only professional customers

� Present in 30 countries

� Matchless international expansion:

international share of sales over 80%

� High operating RoCE (>35%) due to capital

efficient model

� Sales: Food 80%, Non-food 20%

9Deutsche Bank German & Austrian Corporate Conference

Market Entries

An Outstanding Success Story

Cumulated country population

~ 3.7 billion

2000 2001

437475

353

2002

384

+315

20092005

504584

2004

615

2006

544

2003 2007

668

2008

655

Stores

+46%

24.0

30.6

2006

26.425.1

20012000

22.7

2002

33.129.9

2008

31.7

21.0

20072004

28.1

2003 2005 2009

Sales

936963904

805716

641

200920052000

1,111

20082002 2006

1,013

2003

1,139

2001

1,243

2004 2007

EBIT€ million (since 2008 fully leased)

€ billionAsia/Africa

Eastern Europe

Western Europe

Germany

1964

Germany

1968

Nether-lands

1970

Belgium

1971

UK

1971

France

1971

Austria

1971

Denmark

1972

Spain

1972

Italy

1990

Turkey

1990

Portugal

1991

Morocco

1992

Greece

1994

Poland

1994

Hungary

1996

China

1996

Romania

1997

CzechRepublic

1999

Bulgaria

2000

Slovakia

2001

Russia

2001

Croatia

2002

Japan

2002

Vietnam

2003

Ukraine

2003

India

2004

Moldova

2005

Serbia

2007

Pakistan

2009

Kazakhstan

2010E

Egypt

10Deutsche Bank German & Austrian Corporate Conference

Different Business Units with Different Strategic Priorities

� Quality

� Freshness

� Availability

� Professional assortments

� Services

� Price

� Delivery

� Business Solutions

� Key account Management

� Customerproximity

+

+

USP

Priorities

Providing professional

solutions

Rapid

Expansion

Emerging Growing Developed

Asia/New Markets Europe/MENA

11Deutsche Bank German & Austrian Corporate Conference

� Satellite store supplied mainly by ‘mother store’with dedicated Trader focus

� Opened in October 2009in Tarnow, Poland

� Rapid expansion model to cover cities without further store potential

� Opened in October 2009 in Rodez, France,and managed by Toulouse store

� Online catalogue for food & non-food assortment

� Acquiring new high-ticket customers� Offering the full assortment in food and

non-food� Started in 2009

Delivery

Examples for Business Model Transformation

Metro Drive

Makro Punkt

12Deutsche Bank German & Austrian Corporate Conference

Productivity Gains are Gaining Traction

� Growing share of private label goods

Q4

31

Q3

29

Q2

27

Q1

17

Metro C&C Germany Delivery Services (€ m)

2009 2010

Q1

30

Q4

12.0%

Q3

11.7%

Q2

11.3%

Q1

11.4%

Private Label share development (total)

2009 2010

Q1

12.5%

� Sound development with new

delivery services

13Deutsche Bank German & Austrian Corporate Conference

China: Our Next Growth Driver

Targeted East Coast Expansion Areas

Suzhou

Wuxi

Dongguan

Shenzhen

Guangzhou

FoshanZhongshan

Zhuhai

Beijing

Tianjin

Shanghai

Shenyang

Harbin

Dalian

ZhengzhouXi’an

HefeiWuhan

Nanchang

Fuzhou

Xiamen

Quanzhou

Changsha

Chongqing

Chengdu

Kunming

Jiaxing

Changzhou

Nantong

Nanjing

Ningbo

Qingdao

Hangzhou

Metro New Stores

Metro Existing Store

ExistingPlanned

Bohai Bay (incl Beijing)

Pearl River Delta(incl. Guangzhou)

Yangtze River Delta

(incl. Shanghai)

� First priority to achieve

critical mass by focusing

on three targeted

expansion areas

(major long-term growth

potential due to high

population density)

� Still highly fragmented

market with no

established #1 player

� EBIT margin on store

level between 2%-3%

ExistingPotential

.

14Deutsche Bank German & Austrian Corporate Conference

Expansion Programme Subject to Signficant Ramp-up

2012 E

~50

2011 E

~40

2010 E

~30

2009

18

2008

40

2007

32

2006

41

2005

43

2004

33

2003

39

MCC Europe/MENAMCC Asia/New Markets

New Store Openings 2003 - 2009 Planned New Store Openings 2010 - 2012

15Deutsche Bank German & Austrian Corporate Conference

Real

� Leading player in Germany’s

hypermarket sector

� Presence in five Eastern European

countries

� Large range of fresh produce

complemented by attractive non-

food assortment

� Sales: food 70% and non-food 30%

� Range of up to 80,000 products

16Deutsche Bank German & Austrian Corporate Conference

� Adjusted for changes in store network outperformance in German hypermarkets (-0.7% vs. -1.9%*)

� Former Walmart stores turned positive

� Share of private label increasedto 16%; including fresh >22%

� EBIT margin improved by 40bps; in Germany EBIT margin at 1%

* Source: Nielsen Umsatzmonitor, adj. for store changes

Real: German EBIT Margin Improved to 1% in 2009

EBIT margin

2009

0.3%

Margin mixProductivity gains

Cost savings/ network

streamlining

EBITmargin2008

1.0%

Real Germany

Germany (€ million) 2008 2009 Change

Sales 8,750 8,573 -177

EBIT 23 83 +60

Margin 0.3% 1.0% +0.7 pp

17Deutsche Bank German & Austrian Corporate Conference

Value-for-money

Availability of

products

Choice/

range of

products

Quality of

products

Store atmosphere

Cleanliness/

store hygiene

Staff

expertise

Staff

friendliness

Real 2008

Real 2009

A Sharper Brand

� Higher attractiveness in all dimensions

� Only hypermarket with clear improvement in price perception

� Further ramp-up of private labels

Price Perception(2009 vs. 2007)

Retailer 3Retailer 1 Retailer 2Real

∅ -3

points

-3

-7-6

2

ne

ga

tive

po

sit

ive

Private Label

Articles[as at 31/03/2010]

870

1,500

220

60

18Deutsche Bank German & Austrian Corporate Conference

� 614 new concept modules in 2009

� Positive customer response after

concept module implementation

� Further 400 concept modules to be

implemented in 2010

c.80 conceptmodules

Q1

c.110 conceptmodules

Q2

c.130 conceptmodules

Q3

c.80 conceptmodules

Q4

∑c.400 concept

modules

Roll-out 2010

167

125

785446353331

2520

TOTAL

614

Beauty & More

OthersWine & Spirits

Service Centre

TextileHouse-hold

Electr.DIYF&VIntern. Spec.

Focus in 2010 on Further Concept Enhancements to Drive Customer Frequency and Basket

Concept Modules Implemented in 2009

19Deutsche Bank German & Austrian Corporate Conference

Media Markt and Saturn

� Pan-European market leader in consumer

electronics retailing

� Top market positions

� Consistent dual-brand strategy with

superior brand recognition

� Multi-channel approach:

e-commerce piloted in 2 countries

� Large-scale, full assortment and

highly capital efficient

� Aggressive pricing

� Store managers are partners:

- Up to 10% ownership of their stores

- Local entrepreneur: determines assortment, pricing and staffing

- Remuneration directly linked to the store’s success

20Deutsche Bank German & Austrian Corporate Conference

Market Shares Gained in Every Country

Source: GfK

Market

position2008 2009

∆-

points

Austria # 1 22.7% 24.5% 1.8%

Germany # 1 18.3% 19.7% 1.4%

Hungary # 1 17.3% 19.3% 2.0%

Poland # 1 16.5% 17.6% 1.1%

Italy # 1 13.0% 15.2% 2.2%

Luxemburg Newcomer 5.7% 14.9% 9.2%

Netherlands # 1 14.0% 14.3% 0.3%

Switzerland # 2 11.5% 13.1% 1.6%

Spain # 1 10.0% 11.0% 1.0%

Belgium # 1 9.0% 10.4% 1.4%

Sweden Early stage 5.5% 8.7% 3.2%

Greece # 2 6.1% 8.6% 2.5%

Portugal # 4 6.4% 6.8% 0.4%

Turkey Newcomer 1.5% 3.1% 1.6%

Russia Early stage 1.6% 2.7% 1.1%

France Relaunch 2.0% 2.2% 0.2%

21Deutsche Bank German & Austrian Corporate Conference

Multi-Channel Approach

� Complementing the store base

� Addressing and interacting directly with the

customers along all touchpoints

� Extending the assortment with content, services

and bundles

� Media Markt Pilot-Webshops now available in

the Netherlands and Austria

22Deutsche Bank German & Austrian Corporate Conference

China: Huge growing market with unique window of opportunity

� Chinese consumer electronics retail market* of~€82 billion to grow to more than €180 billion

over the next five years

� Consumer electronics market very fragmented with the market leader commanding currently~7% market share

� Entering the Chinese market with a joint venturepartner is the most efficient solution

from 2013

Phase 1: Pilot Phase

Phase 2:Expansion

Timeline:

# stores:(cum. market share):

2010 - 2012

~10(~8% in Shanghai)

>100

January 2012: Evaluation of options

+ target achievement

2010: 100% focus on Shanghai

(ultimate test of competitiveness)

2–Phase Approach to start in Shanghai and finetune the Chinese Business Model

* Source: Euromonitor 29/01/2010

23Deutsche Bank German & Austrian Corporate Conference

Galeria Kaufhof

�Concept and systems leader in Germany’s department store segment and market leader in Belgium

�Sales 2009: €3.5 billion

�EBIT 2009: €119 million

� 141 stores in Germany and Belgium

� Focus on mid-market and lifestyle orientation (sharper brand and private label portfolio)

� Strong cost and stock management

� Strong customer retention programme

� Sales: Food 10%; Non-food 90%

�Non-strategic asset

24Deutsche Bank German & Austrian Corporate Conference

Sales growth

EBIT(before special items)

Capex

New storeopenings

2009 2010Medium-

Term

-3.6% 0 – 6% > 6%

€2.0 billion > €2.0 billion > 10%

€1.5 billion

18

12

50

~ €1.9 billion > €2.2 billion

~ 30

~ 5

~ 60

~ 40

~ 15

> 70

Outlook

25Deutsche Bank German & Austrian Corporate Conference

METRO GROUP: Key Messages

� Portfolio of strong retail brands with diversified regional presence

� Efficiency- and value-enhancing programmeShape 2012 well on track

� METRO GROUP well positioned for future profitable growth

Deutsche Bank German & Austrian Corporate Conference

21 May 2010, Frankfurt

Dr Eckhard Cordes, CEO

Appendix

28Deutsche Bank German & Austrian Corporate Conference

€ million 2007 2008 2009 Change

Sales 64,210 67,955 65,529 -3.6%

EBITDAR - 4,451 4,335 -2.6%

EBITDAR margin (%) - 6.5% 6.6% -

EBITDA 3,343 3,540 3,328 -6.0%

EBITDA margin (%) 5.2% 5.2% 5.1% -

EBIT 2,078 2,222 2,024 -8.9%

EBIT margin (%) 3.2% 3.3% 3.1% -

EPS from continuing operations (€)* 2.77 3.04 2.10 -31.0%

Total assets 33,862 33,814 33,667 -0.4%

Equity ratio (%) 19.2% 17.9% 17.8% -

Capex 2,154 2,423 1,517 -37.4%

Capital Employed - 16,888 16,277 -3.6%

Dividend per ordinary share (€) 1.18 1.18 1.18 -

* After minority interests

Key Data

29Deutsche Bank German & Austrian Corporate Conference

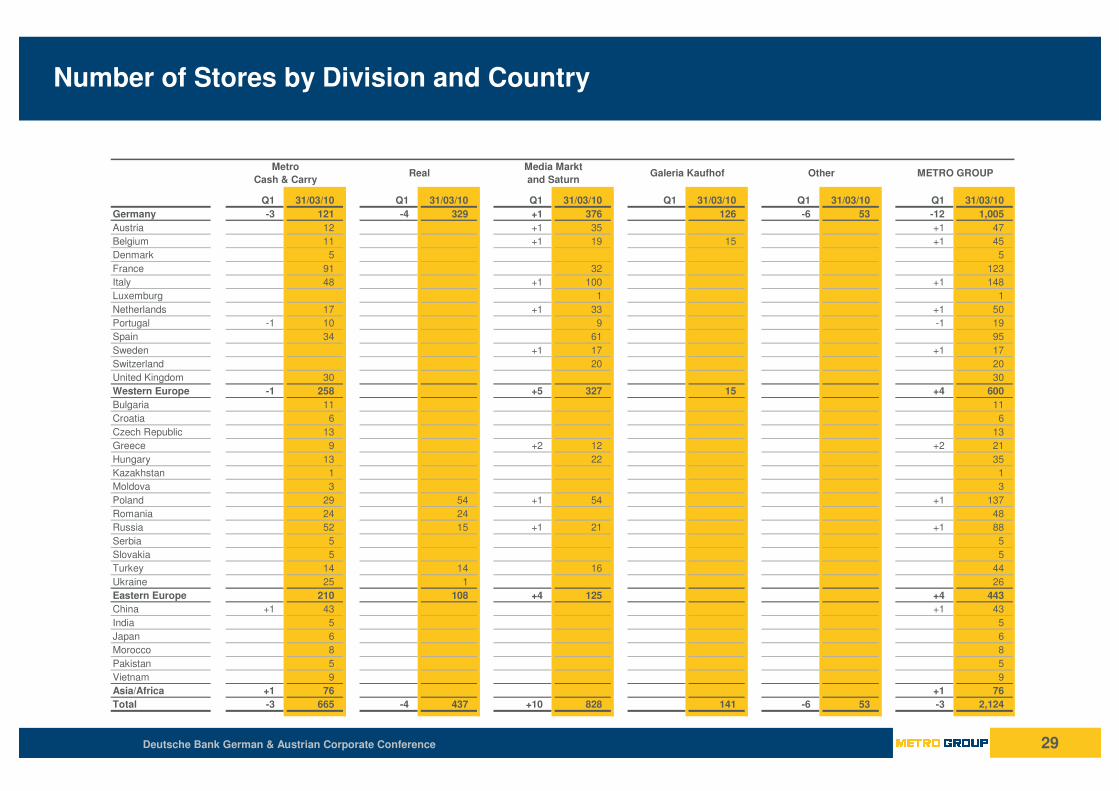

Number of Stores by Division and Country

Q1 31/03/10 Q1 31/03/10 Q1 31/03/10 Q1 31/03/10 Q1 31/03/10 Q1 31/03/10

Germany -3 121 -4 329 +1 376 126 -6 53 -12 1,005

Austria 12 +1 35 +1 47

Belgium 11 +1 19 15 +1 45

Denmark 5 5

France 91 32 123

Italy 48 +1 100 +1 148

Luxemburg 1 1

Netherlands 17 +1 33 +1 50

Portugal -1 10 9 -1 19

Spain 34 61 95

Sweden +1 17 +1 17

Switzerland 20 20

United Kingdom 30 30

Western Europe -1 258 +5 327 15 +4 600

Bulgaria 11 11

Croatia 6 6

Czech Republic 13 13

Greece 9 +2 12 +2 21

Hungary 13 22 35

Kazakhstan 1 1

Moldova 3 3

Poland 29 54 +1 54 +1 137

Romania 24 24 48

Russia 52 15 +1 21 +1 88

Serbia 5 5

Slovakia 5 5

Turkey 14 14 16 44

Ukraine 25 1 26

Eastern Europe 210 108 +4 125 +4 443

China +1 43 +1 43

India 5 5

Japan 6 6

Morocco 8 8

Pakistan 5 5

Vietnam 9 9

Asia/Africa +1 76 +1 76

Total -3 665 -4 437 +10 828 141 -6 53 -3 2,124

Metro

Cash & CarryReal METRO GROUPOtherGaleria Kaufhof

Media Markt

and Saturn

30Deutsche Bank German & Austrian Corporate Conference

Metro Cash & Carry

Sales

20062000 2001 2005200420032002

5,000

35,000

30,000

25,000

20,000

15,000

10,000

200920082007

Sales (€ million)

2009 Regional Sales Breakdown

Asia/Africa

7%

EasternEurope

36%

WesternEurope

40%

Germany

17%

Financials (€ million) 2000 2001 2002 2003 2004 2005 2006 2007 2008* 2009*

Sales 21,032 22,726 23,972 25,093 26,442 28,087 29,907 31,698 33,143 30,613

Change yoy in % 8.0% 8.1% 5.5% 4.7% 5.4% 6.2% 6.5% 6.0% 4.6% -7.6%

Change yoy in % - pre-currency 7.2% 8.8% 6.4% 7.7% 5.6% 4.4% 6.2% 5.7% 5.4% -2.5%

Change yoy in % - lfl (LC) - - 1.4% 1.6% 1.1% -0.3% 1.9% 2.2% 2.4% -4.9%

EBITDA 873 972 1,078 1,200 1,280 1,377 1,510 1,631 1,406 1,165

Change yoy in % 9.9% 11.4% 10.9% 11.2% 6.7% 7.6% 9.6% 8.0% - -17.2%

EBITDA margin 4.2% 4.3% 4.5% 4.8% 4.8% 4.9% 5.0% 5.1% 4.2% 3.8%

EBIT** 641 716 805 904 963 1013 1,111 1,243 1,139 936

Change yoy in % 6.9% 11.7% 12.4% 12.3% 6.5% 5.1% 9.7% 11.9% - -17.8%

EBIT margin 3.0% 3.2% 3.4% 3.6% 3.6% 3.6% 3.7% 3.9% 3.4% 3.1%

Capital Employed - - - - - - - - 2,565 2,605

RoCE - - - - - - - - 44.4% 35.9%

Capex 577 839 750 737 619 900 880 859 336 220

* New segment reporting structure

** until 2003: EBITA

Operating Statistics 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Number of stores 353 384 437 475 504 544 584 615 655 668

Selling space (1,000 sqm) 2,972 3,182 3,423 3,725 3,952 4,218 4,507 4,875 5,176 5,291

Change yoy in % 6.6% 7.1% 7.5% 8.8% 6.1% 6.7% 6.9% 8.2% 6.2% 2.2%

Average store size (sqm) 8,419 8,287 7,832 7,841 7,841 7,754 7,717 7,927 7,902 7,921

Sales/Øsqm (€) 7,304 7,386 7,259 7,021 6,889 6,876 6,856 6,757 6,595 5,849

31Deutsche Bank German & Austrian Corporate Conference

Real

-1%

0%

1%

2%

3%

4%

2003200220012000

6,000

4,000

2,000

0

200920082007200620052004

12,000

8,000

10,000

EBIT margin

Sales

EasternEurope

24%

Germany

76%

Sales and EBIT Margin

2009 Regional Sales Breakdown

Financials* (€ million) 2000 2001 2002 2003 2004 2005 2006 2007 2008** 2009**

Sales 8,166 8,375 8,198 8,205 8,182 8,192 8,775 11,003 11,635 11,298

Change yoy in % 2.4% 2.6% -2.1% 0.1% -0.3% 0.1% 7.1% 25.4% 5.8% -2.9%

Change yoy in % - pre-currency 2.3% 3.0% -1.1% 1.2% 0.0% -1.2% 7.1% 25.0% 5.4% 1.3%

Change yoy in % - lfl (LC) - - -1.4% 0.1% -2.2% -4.7% -2.5% -0.1% 4.4% 0.0%

EBITDA 276 353 372 384 352 -121 192 160 191 235

Change yoy in % 13.6% 28.0% 5.3% 3.1% -8.3% - 45.4% -16.7% - 22.1%

EBITDA margin 3.4% 4.2% 4.5% 4.7% 4.3% -1.5% 2.2% 1.5% 1.6% 2.1%

EBIT*** 138 202 228 242 219 -2 19 -16 6 52

Change yoy in % 15.2% 46.0% 13.5% 5.9% -9.3% - - - - -

EBIT margin 1.7% 2.4% 2.8% 2.9% 2.7% 0.0% 0.2% -0.2% 0.1% 0.5%

Capital Employed - - - - - - - - 2,942 2,674

RoCE - - - - - - - - 0.2% 1.9%

Capex 323 248 160 174 110 255 854 345 250 193

* excluding Extra

** New segment reporting structure

*** until 2003: EBITA

Operating Statistics* 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Number of stores 276 277 278 289 306 328 442 434 439 441

Selling space (1,000 sqm) 2,006 2,016 2,019 2,078 2,135 2,242 3,158 3,103 3,148 3,184

Change yoy in % 0.6% 0.5% 0.1% 3.0% 2.7% 5.0% 40.9% -1.7% 1.4% 1.1%

Average store size (sqm) 7,267 7,279 7,262 7,192 6,977 6,835 7,145 7,150 7,171 7,220

Sales/Øsqm (€) 4,058 4,165 4,063 4,005 3,884 3,743 3,250 3,515 3,723 3,569

32Deutsche Bank German & Austrian Corporate Conference

Media Markt and Saturn

Sales and EBITDA Margin

0%

1%

2%

3%

4%

5%

6%

7%

2009

7,500

5,000

20,000

17,500

15,000

12,500

10,000

Ø +11.1% p.a.

200820072006200520042003200220012000

EBITDA marginSales (€ million)

Eastern Europe

10%

WesternEurope

44%

Germany46%

2009 Regional Sales Breakdown

Financials (€ million) 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Sales 7,619 8,341 9,583 10,563 12,210 13,306 15,156 17,444 18,993 19,693

Change yoy in % 24.0% 9.5% 14.9% 10.2% 15.6% 9.0% 13.9% 15.1% 8.9% 3.7%

Change yoy in % - pre-currency 23.8% 9.1% 14.8% 11.0% 15.8% 8.5% 13.9% 14.2% 8.4% 5.5%

Change yoy in % - lfl (LC) - - 3.2% 0.9% 4.6% -1.4% 3.0% 2.6% -2.1% -0.4%

EBITDA 375 368 431 506 612 679 776 818 839 851

Change yoy in % 17.9% -1.9% 17.0% 17.6% 20.8% 11.0% 14.4% 5.4% - 1.4%

EBITDA margin 4.9% 4.4% 4.5% 4.8% 5.0% 5.1% 5.1% 4.7% 4.4% 4.3%

EBIT* 272 228 290 360 452 510 587 610 603 608

Change yoy in % 17.8% -16.1% 27.0% 24.3% 25.5% 12.8% 15.2% 3.9% - 0.8%

EBIT margin 3.6% 2.7% 3.0% 3.4% 3.7% 3.8% 3.9% 3.5% 3.2% 3.1%

Capital Employed - - - - - - - - 960 795

RoCE - - - - - - - - 62.8% 76.4%

Capex 267 264 350 229 261 315 370 463 402 353

* until 2003: EBITA

Operating Statistics 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Number of stores 314 357 386 436 503 558 621 702 768 818

Selling space (1,000 sqm) 852 976 1,129 1,307 1,514 1,704 1,914 2,213 2,439 2,633

Change yoy in % 16.9% 14.6% 15.6% 15.8% 15.8% 12.6% 12.3% 15.6% 10.2% 8.0%

Average store size (sqm) 2,714 2,735 2,925 2,999 3,010 3,054 3,082 3,152 3,176 3,219

Sales/Øsqm (€) 9,638 9,126 9,105 8,671 8,656 8,270 8,379 8,454 8,166 7,765

33Deutsche Bank German & Austrian Corporate Conference

Galeria Kaufhof

EBITDA and EBIT Margin

91%

9%

Germany

WesternEurope

0

50

100

150

200

250

300

350

0%

1%

2%

3%

4%

5%

20052001 2002 20042003 20072000 2006 20092008

EBITDAEBIT margin

2009 Regional Sales Breakdown

Financials (€ million) 2000 2001 2002 2003 2004 2005 2006 2007 2008* 2009*

Sales 3,941 3,971 3,900 3,819 3,768 3,575 3,609 3,556 3,607 3,539

Change yoy in % -1.5% 0.8% -1.8% -2.1% -1.3% -5.1% 0.9% -1.5% -1.1% -1.9%

Change yoy in % - lfl 0.1% -3.7% -4.5% -2.2% -1.2% -4.8% -0.6% -1.7% -1.4% -2.2%

EBITDA 324 349 292 249 199 189 192 211 223 223

Change yoy in % 10.2% 7.9% -16.3% -14.7% -19.9% -5.4% 1.8% 10.0% - 0.2%

EBITDA margin 8.2% 8.8% 7.5% 6.5% 5.3% 5.3% 5.3% 5.9% 6.2% 6.3%

EBIT** 181 190 139 99 57 69 82 107 115 119

Change yoy in % 10.5% 4.8% -26.8% -28.4% -43.6% 21.8% 18.1% 31.3% - 3.4%

EBIT margin 4.6% 4.8% 3.6% 2.6% 1.5% 1.9% 2.3% 3.0% 3.2% 3.4%

Capital Employed - - - - - - - - 826 785

RoCE - - - - - - - - 13.9% 15.2%

Capex 167 202 120 104 120 96 151 107 128 57

* New segment reporting structure; since 2009 including Dinea

** until 2003: EBITA

Operating Statistics 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Number of stores 132 148 150 148 147 142 142 141 141 141

Selling space (1,000 sqm) 1,319 1,440 1,456 1,457 1,473 1,465 1,487 1,486 1,489 1,501

Change yoy in % 1.6% 9.1% 1.1% 0.1% 1.0% -0.5% 1.5% -0.1% 0.2% 0.7%

Average store size (sqm) 9,995 9,728 9,706 9,847 10,018 10,318 10,473 10,539 10,567 10,645

Sales/Øsqm (€) 3,011 2,879 2,693 2,622 2,572 2,434 2,445 2,392 2,363 2,367

34Deutsche Bank German & Austrian Corporate Conference

Real Estate

Asia/Africa

9%

EasternEurope

35%

WesternEurope

33%

Germany

23%

2009 Selling Space by RegionFinancials (€ million) 2008 2009

EBITDA 927 959

Change yoy in % - 3.4%

EBIT 538 551

Change yoy in % - 2.4%

Capital Employed 8,856 8,690

RoCE 6.1% 6.3%

Capex 1,060 580

35Deutsche Bank German & Austrian Corporate Conference

Long-Term Debt Maturity Profile

€ million

750

500

250

1,250

1,000

0

20172016201520142013201220112010

Refinancing already completed

7.625%EUR1,000,000,00005/03/201505/03/2009

4.250%EUR750,000,00022/02/201722/02/2010

5.750%EUR600,000,00014/07/201414/07/2009

9.375%EUR500,000,00028/11/201328/11/2008

11.550%RON23,800,00023/07/201223/07/2009

4.750%EUR500,000,00029/05/201229/05/2007

3.625%EUR350,000,00024/06/201124/06/2009

4.625%EUR750,000,00026/05/201126/05/2004

FRNEUR200,000,00008/09/201008/09/2006

CouponCurrencyNom. Outstanding (€)MaturityIssued

� Dependency on bank financing further reduced

� Well-balanced maturity profile

Bonds

Bonds

Promissory Notes (Schuldscheindarlehen)

36Deutsche Bank German & Austrian Corporate Conference

METRO Group

Investor Relations

Schlueterstrasse 1

40235 Duesseldorf

Germany

Tel.: +49 (0)211 6886-1936

Fax: +49 (0)211 6886-3759

Email: [email protected]

Internet: www.metrogroup.de

Contact