Embed Size (px)

Citation preview

Determinants Determinants of Prices of Agriculturalof Prices of Agriculturaland Mineral Commoditiesand Mineral Commodities

Jeffrey Frankel,Jeffrey Frankel, Harvard University, &Harvard University, & Andrew Rose,Andrew Rose, University of California, BerkeleyUniversity of California, Berkeley

First draft of a paper for the Reserve Bank of Australia. First draft of a paper for the Reserve Bank of Australia. To be presented at pre-conference, 16 June, 2009, To be presented at pre-conference, 16 June, 2009,

Westfälische Wilhelms University Münster, Germany;Westfälische Wilhelms University Münster, Germany;Co-sponsored also by CAMA, Australia, Co-sponsored also by CAMA, Australia,

& VERC, Wilfred Laurier University, Canada& VERC, Wilfred Laurier University, Canada

22

The determination of prices for oil and The determination of prices for oil and other mineral & agricultural other mineral & agricultural commoditiescommodities

falls predominantly in the province of falls predominantly in the province of microeconomics. microeconomics.

But in periods when many commodity But in periods when many commodity prices are moving far in the same prices are moving far in the same direction at the same time, it becomes direction at the same time, it becomes difficult to ignore the influence of difficult to ignore the influence of macroeconomics. macroeconomics. The decade of the 1970s. The decade of the 1970s. The decade of the 2000s.The decade of the 2000s.

33

► ► A rise in the price of oil A rise in the price of oil might be explained by might be explained by “peak oil” fears, a risk “peak oil” fears, a risk premium on Gulf premium on Gulf instability, or political instability, or political developments in Russia, developments in Russia, Nigeria or Venezuela. Nigeria or Venezuela.

► Some farm prices ► Some farm prices might be explained by might be explained by drought in Australia, drought in Australia, shortages in China, or shortages in China, or ethanol subsidies in the ethanol subsidies in the US.US.

44

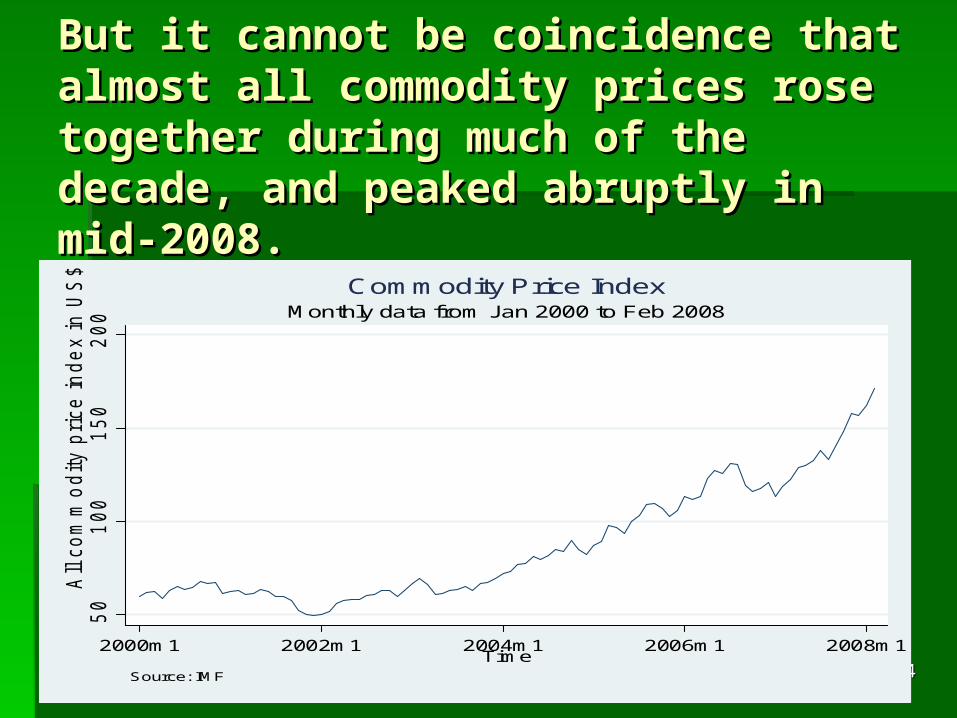

But it cannot be coincidence that But it cannot be coincidence that almost all commodity prices rose almost all commodity prices rose together during much of the together during much of the decade, and peaked abruptly in decade, and peaked abruptly in mid-2008.mid-2008.

50

100

150

200

All c

om

mo

dity p

rice in

de

x in U

S$

2000m1 2002m1 2004m1 2006m1 2008m1Time

Source: IMF

Monthly data from Jan 2000 to Feb 2008Commodity Price Index

55

Three theories competed to explain Three theories competed to explain the ascent of commodity prices in the ascent of commodity prices in 2003-08.2003-08.

1.1. Most standard: the Most standard: the global demand growth global demand growth explanationexplanation, emphasizing especially , emphasizing especially growth in China, India, etc. growth in China, India, etc.

2.2. Also highly popular: Also highly popular: destabilizing speculationdestabilizing speculation. .

1.1. Storability & homogeneity Storability & homogeneity => asset-like speculation. => asset-like speculation.

2.2. But destabilizing? But destabilizing?

3.3. Expansionary monetary policyExpansionary monetary policy1.1. low low real interest ratesreal interest rates2.2. expected expected inflationinflation..

66

Counter-evidence to claims of Counter-evidence to claims of destabilizing speculationdestabilizing speculation

1. Futures price of oil initially lagged behind 1. Futures price of oil initially lagged behind spot price.spot price.

2. High volume of trading 2. High volume of trading ≠≠ net short position net short position

3. Commodities that lack futures markets are 3. Commodities that lack futures markets are as volatile as those that have them. as volatile as those that have them.

4. Historical efforts to ban speculative futures 4. Historical efforts to ban speculative futures markets have failed to reduce volatility. markets have failed to reduce volatility.

77

The real interest rate The real interest rate explanationexplanation

1.1. Some argue that high prices for oil & other Some argue that high prices for oil & other commodities in the 1970s were not exogenous, commodities in the 1970s were not exogenous, but rather a result of easy monetary policy.but rather a result of easy monetary policy. [1][1]

2.2. Conversely, a rise in US real interest rates in the Conversely, a rise in US real interest rates in the early 1980searly 1980s. . helped drive commodity prices downhelped drive commodity prices down ..[2][2]

3.3. The Fed cut real interest rates sharply,2001-04, The Fed cut real interest rates sharply,2001-04, and again in 2008-09. and again in 2008-09. My claim: it helped push up commodity prices.My claim: it helped push up commodity prices. [3][3]

[1][1] Barsky & Killian (2001). Barsky & Killian (2001).

[2] [2] Frankel (1985). Frankel (1985).

[3][3] Frankel (2008). Frankel (2008).

88

High interest ratesHigh interest ratesLower inventory demand;Lower inventory demand; andand

encourage faster pumping of oil,encourage faster pumping of oil, mining of deposits, harvesting of crops, etc.,mining of deposits, harvesting of crops, etc., because owners can invest the proceeds at interest rates higher because owners can invest the proceeds at interest rates higher

than the return to saving the reserves.than the return to saving the reserves.

Both channels – fall in demand & rise in supply – Both channels – fall in demand & rise in supply – work to lower the commodity price.work to lower the commodity price.

A 3A 3rdrd channel goes the same direction -- channel goes the same direction -- trading in contracts (“the carry trade”): trading in contracts (“the carry trade”): Low interest rates induce a “search for yield” Low interest rates induce a “search for yield” among investors, who go long in commodities among investors, who go long in commodities (just as FX, emerging markets., (just as FX, emerging markets., etc.)etc.)

99

Inverse correlation between Inverse correlation between real interest rate and real real interest rate and real

commodity price index commodity price index (DJ, 1950-(DJ, 1950-2008)2008)

Dow Jones Commodity Price Index vs. Real Interest Rate

Annual, 1950-2008

-0.5

0

0.5

1

1.5

-7.5% -5.0% -2.5% 0.0% 2.5% 5.0% 7.5% 10.0%

Real Interest Rate

Lo

g R

ea

l C

om

mo

dit

y P

ric

e I

nd

ex

1010

Counter-argument that applies to both the Counter-argument that applies to both the destabilizing-speculation & easy-money destabilizing-speculation & easy-money theoriestheories (Krugman(Krugman, 2008, 2008, & Kohn, & Kohn, 2008, 2008):):

Inventories of oil & other commodities were Inventories of oil & other commodities were said to be low in 2008, contrary to the theory.said to be low in 2008, contrary to the theory.

Perhaps inventory numbersPerhaps inventory numbers do not capture all inventories, ordo not capture all inventories, or are less relevant than (larger) reserves.are less relevant than (larger) reserves.

King of Saudi Arabia (2008): King of Saudi Arabia (2008): “we might as well leave the reserves “we might as well leave the reserves in the ground for our grandchildren.” in the ground for our grandchildren.”

1111

But in 2008, enthusiasm for theories (2) & But in 2008, enthusiasm for theories (2) & (3), the speculation & interest rate theories, (3), the speculation & interest rate theories, rose, at the expense of theory (1), the global rose, at the expense of theory (1), the global

boom.boom. The sub-prime mortgage crisis The sub-prime mortgage crisis

hit the US in August 2007. hit the US in August 2007. Thereafter, forecasts of growth fell, not just Thereafter, forecasts of growth fell, not just

for the US but globally, including China.for the US but globally, including China. Meanwhile commodity prices, far from Meanwhile commodity prices, far from

declining as one might expect from the global declining as one might expect from the global demand hypothesis, accelerated. demand hypothesis, accelerated.

For the year following August 2007, at least, For the year following August 2007, at least, the global boom theory was not relevant. the global boom theory was not relevant.

That left explanations (2) and (3). That left explanations (2) and (3).

1212

DefinitionsDefinitions

ss ≡ the spot price, ≡ the spot price, S ≡ its long run equilibrium, S ≡ its long run equilibrium, p p ≡ the economy-wide price index, ≡ the economy-wide price index, q ≡ s-pq ≡ s-p, the real price of the commodity, , the real price of the commodity,

andand Q Q ≡ ≡ the long run equilibrium real price of the long run equilibrium real price of

the commodity;the commodity; all in log form. all in log form.

1313

Derive the relationship Derive the relationship between between qq & & rr from two from two equations:equations:

Regressive expectations:Regressive expectations: E (Δs) = - θ (q-Q)E (Δs) = - θ (q-Q) + + E(ΔpE(Δp). ). (2) (2)

Arbitrage condition between inventories & bonds:Arbitrage condition between inventories & bonds: E Δs + c = i,E Δs + c = i, (3)(3)

where where c ≡ cy – sc – rp .c ≡ cy – sc – rp . cycy ≡ ≡ convenience yield from holding the stock (e.g., the convenience yield from holding the stock (e.g., the

insurance value of having an assured supply of a critical input in insurance value of having an assured supply of a critical input in the event of a disruption)the event of a disruption)

scsc ≡≡ storage costs (e.g., rental rate on oil tanks, etc.) storage costs (e.g., rental rate on oil tanks, etc.)

rp rp ≡ ≡ E Δs – (f-s) E Δs – (f-s) ≡≡ risk premium, risk premium, >0 if being long in commodities is risky, and>0 if being long in commodities is risky, and

ii ≡≡ the interest rate the interest rate

1414

Combining (2) & (3) Combining (2) & (3) gives the relationship:gives the relationship:

q - Q = - (1/q - Q = - (1/θθ) (i - E() (i - E(ΔΔpp) – c) .) – c) .(5)(5)

This inverse relationship between q & r has This inverse relationship between q & r has been supported by:been supported by: Event studies Event studies (monetary announcements)(monetary announcements) The graphsThe graphs Regressions of Regressions of q q against against rr in Frankel (2008):in Frankel (2008):

Significant for half of the individual commoditiesSignificant for half of the individual commodities and in a panel studyand in a panel study and for various aggregate commodity price indicesand for various aggregate commodity price indices

But much is left out of this equation. Esp. variation in But much is left out of this equation. Esp. variation in c.c.

1515

Inverse correlation between real Inverse correlation between real interest rate and real commodity interest rate and real commodity

price indexprice index (Moody’s, (Moody’s, 1950-20081950-2008))Moody's Commodity Price Index vs.

Real Interest Rate Annual, 1950-2008

-0.5

0

0.5

1

1.5

-7.5% -5.0% -2.5% 0.0% 2.5% 5.0% 7.5% 10.0%

Real Interest Rate

Lo

g R

ea

l C

om

mo

dit

y P

ric

e I

nd

ex

1616

Translate convenience yield, Translate convenience yield, storage costs, & risk premium from storage costs, & risk premium from equation (6) into empirically usable equation (6) into empirically usable form, form, with 4 or 5 measurable factors: with 4 or 5 measurable factors:

1. Inventories.1. Inventories. Storage costs rise with the extent to which Storage costs rise with the extent to which inventory holdings strain existing storage inventory holdings strain existing storage capacity: capacity: sc = Φ (INVENTORIES).sc = Φ (INVENTORIES).

Can estimate an inventory equation:Can estimate an inventory equation:

INVENTORIES INVENTORIES = Φ = Φ-1-1 (sc) = Φ (sc) = Φ-1-1 (cy-i–(s-f)) (cy-i–(s-f)) (8)(8)

1717

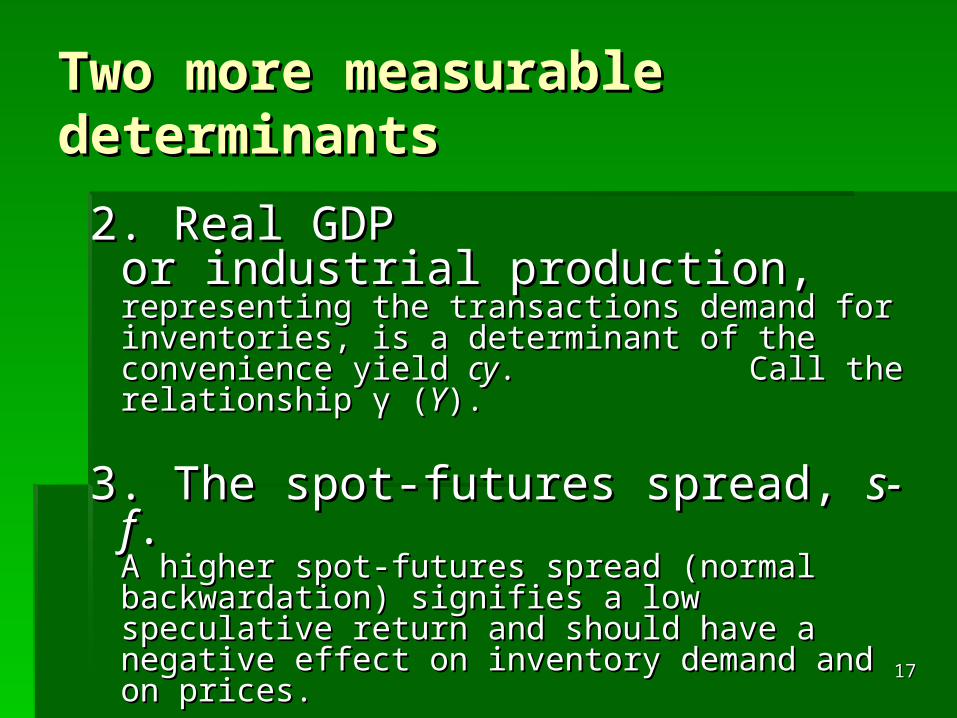

Two more measurable Two more measurable determinantsdeterminants

2. Real GDP 2. Real GDP or industrial production,or industrial production, representing the transactions demand for representing the transactions demand for inventories, is a determinant of the convenience inventories, is a determinant of the convenience yield yield cycy. Call the relationship γ (. Call the relationship γ (YY).).

3. The spot-futures spread, 3. The spot-futures spread, s-fs-f. . A higher spot-futures spread (normal A higher spot-futures spread (normal backwardation) signifies a low speculative backwardation) signifies a low speculative return and should have a negative effect on return and should have a negative effect on inventory demand and on prices. inventory demand and on prices.

1818

The last two are uncertainy The last two are uncertainy measuresmeasures

4. Medium-term volatility4. Medium-term volatility (σ), measured (σ), measured either as the standard deviation of the spot either as the standard deviation of the spot price or as the implicit forward-looking price or as the implicit forward-looking expected volatility that can be extracted from expected volatility that can be extracted from options prices. options prices. Volatility is a determinant of convenience yield, Volatility is a determinant of convenience yield,

cy; cy; and so of commodity pricesand so of commodity prices It may also be a determinant of the risk It may also be a determinant of the risk

premium.premium.

1919

5. Risk5. Risk (political, financial, & economic), (political, financial, & economic), in the case of oil, in the case of oil, e.g.,e.g., is measured by a weighted is measured by a weighted average of average of (inverse)(inverse) political risk political risk for 12 top oil producers. for 12 top oil producers.

The theoretical sign is ambiguous: The theoretical sign is ambiguous: Risk is another determinant of Risk is another determinant of cycy (esp. fear of (esp. fear of

disruption of availability), whereby it should have a disruption of availability), whereby it should have a positive effect on commodity prices. positive effect on commodity prices.

But it is also a determinant of the risk premium But it is also a determinant of the risk premium rprp, , whereby it should have a negative effect on prices.whereby it should have a negative effect on prices.

2020

The equation works for oil The equation works for oil inventories:inventories:

INVENTORIESINVENTORIES = Φ = Φ -1-1 (cy - i– (cy - i– (s-f)(s-f)) ) ------------------------------------------------------------------------------------------------------------------------------------------------------------log_inventories | Coef. Std. Err. t log_inventories | Coef. Std. Err. t P>|t| P>|t| -----------------------+-----------------------------------------------------------------------------+------------------------------------------------------ Real interest rate| -.00056 Real interest rate| -.00056 .00033 -1.71 .00033 -1.71 0.09 0.09 Oil spot-forward | -.00079 Oil spot-forward | -.00079 .00013 -5.98 .00013 -5.98 0.000.00 Log industr.prod. | .05222 Log industr.prod. | .05222 .01968 2.65 .01968 2.65 0.01 0.01 risk risk | .00013 | .00013 .00018 0.69 .00018 0.69 0.491 0.491

Lag log inv Lag log inv | .93105| .93105 00976 95.39 00976 95.39 0.0000.000 counter counter | -.00003 | -.00003 .00001 -2.21 .00001 -2.21 0.0270.027 counter2 counter2 | | -2.78e-09 5.13e-09-2.78e-09 5.13e-09 -0.54 -0.54 0.588 0.588 _constant | .18380 _constant | .18380 .09458 1.94 .09458 1.94 0.0520.052 ------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

2121

The same macro variables work The same macro variables work to determine real oil price:to determine real oil price:

------------------------------------------------------------------------------------------------------------------------------------------------ Log real oil p | Coef. Std. Err. t P>|t| Log real oil p | Coef. Std. Err. t P>|t| ------------------+-----------------------------------------------------------------------+----------------------------------------------------- Log ind.prod. | 3.445 .239 Log ind.prod. | 3.445 .239 14.44 0.00 14.44 0.00 log inventory | .455 log inventory | .455 .119 .119 3.82 0.00 3.82 0.00 Real int.rate | -.052 Real int.rate | -.052 .004 -13.24 0.00 .004 -13.24 0.00 Oil risk | .037 .002 16.25 0.00Oil risk | .037 .002 16.25 0.00 s-f spread | .026 .002 s-f spread | .026 .002 15.94 0.00 .15.94 0.00 . counter | -.006 .0002 -34.82 0.00 counter | -.006 .0002 -34.82 0.00 counter2 | counter2 | 2.84e-06 6.23e-082.84e-06 6.23e-08 45.52 0.00 45.52 0.00 constant | -19.673 1.143 -17.21 0.00 constant | -19.673 1.143 -17.21 0.00 --------------------------------------------------------------------------------------------------------------------------------------------------

2222

Complete equation,Complete equation, from (5) and (8):from (5) and (8):

q = Q - (1/q = Q - (1/θθ) r ) r + + (1/ (1/θθ)) γγ(Y) + (1/(Y) + (1/θθ)Ψ )Ψ ((σσ)) - (1/ - (1/θθ) ) Φ Φ (INVENTORIES) (INVENTORIES) (9)(9)

We now test it on 12 commodities, We now test it on 12 commodities, with data from 1960s to 2008.with data from 1960s to 2008.

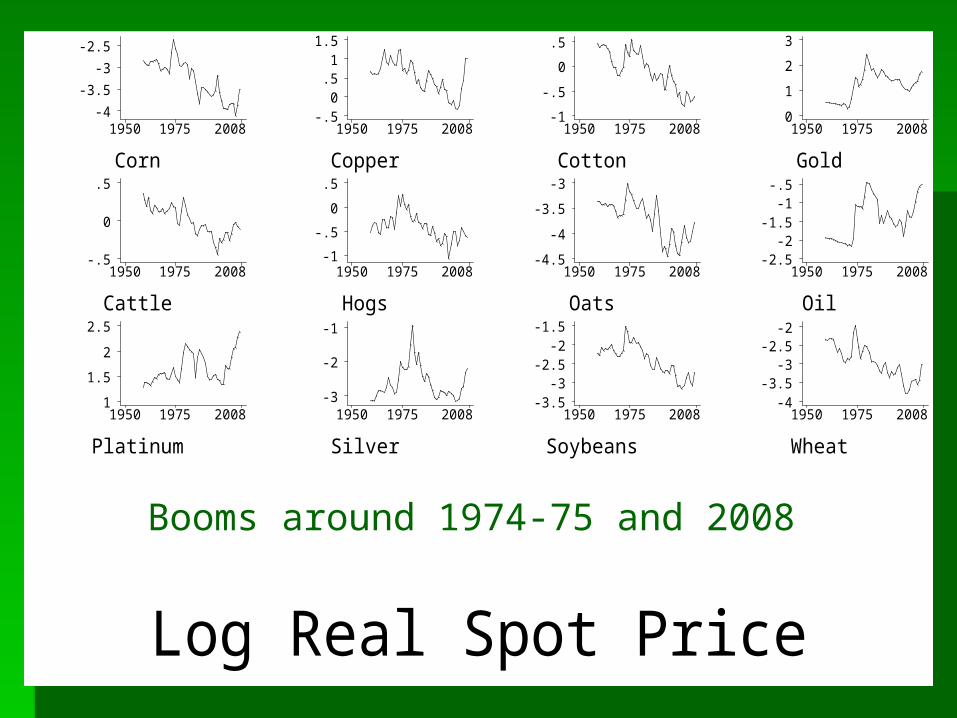

2323Log Real Spot Price

Corn

1950 1975 2008-4

-3.5

-3

-2.5

Copper

1950 1975 2008-.5

0.51

1.5

Cotton

1950 1975 2008-1

-.5

0

.5

Gold

1950 1975 20080

1

2

3

Cattle

1950 1975 2008-.5

0

.5

Hogs

1950 1975 2008-1

-.5

0

.5

Oats

1950 1975 2008-4.5

-4

-3.5

-3

Oil

1950 1975 2008-2.5

-2-1.5

-1-.5

Platinum

1950 1975 20081

1.5

2

2.5

Silver

1950 1975 2008-3

-2

-1

Soybeans

1950 1975 2008-3.5

-3-2.5

-2-1.5

Wheat

1950 1975 2008-4

-3.5-3

-2.5-2

Booms around 1974-75 and 2008

2424

Table 3b -- Panel Results, Table 3b -- Panel Results, for for lnln of real commodity prices, of real commodity prices,

with risk included. Annual data.with risk included. Annual data.

Ln(G-7 Ln(G-7 Real Real GDP)GDP)

VolatilityVolatility RiskRisk Spot-Spot-Futures Futures SpreadSpread

Inven-Inven-toriestories

Real Real interest interest raterate

.82*.82* 2.242.24 .21.21 -.021** -.021** -.16**-.16** .02.02

(.38) (.38) (1.57) (1.57) (.11) (.11) (.006) (.006) (.04)(.04) (.04)(.04)

.57*.57* 1.75*1.75* -.06-.06 -.003* -.003* -.15**-.15** .00.00

(.21) (.21) (.58) (.58) (.04) (.04) (.001) (.001) (.03)(.03) (.01)(.01)

Pooled

Commodity effects

** (*) => significantly different from zero at .01 (.05) significance level. Robust standard errors in parentheses; Intercept & trend included, not reported.

2525

Other testsOther tests

6 Major commodity price indices.6 Major commodity price indices.

Unit root testsUnit root tests Philips-Perron on individual commoditiesPhilips-Perron on individual commodities & panel& panel

Co-integration testsCo-integration tests Johanson on individual commoditiesJohanson on individual commodities PanelPanel Vector error correctionVector error correction

2626

Overall conclusions Overall conclusions (as of now)(as of now)

The commodity-specific explanatory factors The commodity-specific explanatory factors work surprisingly well:work surprisingly well: Inventory holdingsInventory holdings Spot-futures spreadSpot-futures spread VolatilityVolatility

In the latest results, the macroeconomic In the latest results, the macroeconomic variables work surprisingly poorly:variables work surprisingly poorly: Economic activityEconomic activity Real interest ratesReal interest rates

2727

Possible extensionsPossible extensions

Explore other measures of real interest Explore other measures of real interest rate and economic activity.rate and economic activity.

Try survey data as a direct measure of Try survey data as a direct measure of expectations.expectations.

Estimate simultaneous system Estimate simultaneous system in inventories, expectations or spread, in inventories, expectations or spread,

and commodity prices, and commodity prices, tied directly to the theory.tied directly to the theory.

2828

AppendixAppendix

Graphs of dataGraphs of data

2929Risk

Corn

1950 1975 200801234

Copper

1950 1975 20080

.5

1

1.5

Cotton

1950 1975 20080

1

2

3

Gold

1950 1975 20080

.5

1

1.5

Cattle

1950 1975 20080

.2

.4

Hogs

1950 1975 200801234

Oats

1950 1975 20080.51

1.52

Oil

1950 1975 200801234

Platinum

1950 1975 20080

1

2

3

Silver

1950 1975 20080.51

1.52

Soybeans

1950 1975 20080

2

4

Wheat

1950 1975 20080

.1

.2

.3

3030

Future-Spot Spread

Corn

1950 1975 2008-40-20

02040

Copper

1950 1975 2008-60-40-20

020

Cotton

1950 1975 2008-50

0

50

100

Gold

1950 1975 2008-20

0

20

40

Cattle

1950 1975 2008-40

-20

0

20

Hogs

1950 1975 2008-50

0

50

100

Oats

1950 1975 2008-40-20

02040

Oil

1950 1975 2008-50

0

50

100

Platinum

1950 1975 2008-50

0

50

100

Silver

1950 1975 2008-50

0

50

Soybeans

1950 1975 2008-40-20

02040

Wheat

1950 1975 2008-40-20

02040

3131

Log Inventory

Corn

1950 1975 200810.5

1111.5

1212.5

Copper

1950 1975 200811

12

13

14

Cotton

1950 1975 20089.5

10

10.5

11

Gold

195019752008-1-.5

0.51

Cattle

1950 1975 200811.2

11.4

11.6

11.8

Hogs

1950 1975 200810.710.810.9

1111.1

Oats

1950 1975 200811

12

13

Oil

1950 1975 20087.8

8

8.2

8.4

Platinum

1950 1975 2008-20246

Silver

1950 1975 200845678

Soybeans

1950 1975 2008789

1011

Wheat

1950 1975 200811

11.5

12

12.5

3232Volatility

Corn

1950 1975 20080

.05.1

.15.2

Copper

1950 1975 20080

.2

.4

Cotton

1950 1975 20080

.1

.2

.3

Gold

1950 1975 20080

.1

.2

.3

Cattle

1950 1975 20080

.05.1

.15.2

Hogs

1950 1975 20080

.05.1

.15.2

Oats

1950 1975 20080

.1

.2

Oil

1950 1975 20080

.2

.4

Platinum

1950 1975 20080

.1

.2

.3

Silver

1950 1975 20080.1.2.3.4

Soybeans

1950 1975 20080

.1

.2

.3

Wheat

1950 1975 20080

.1

.2

.3

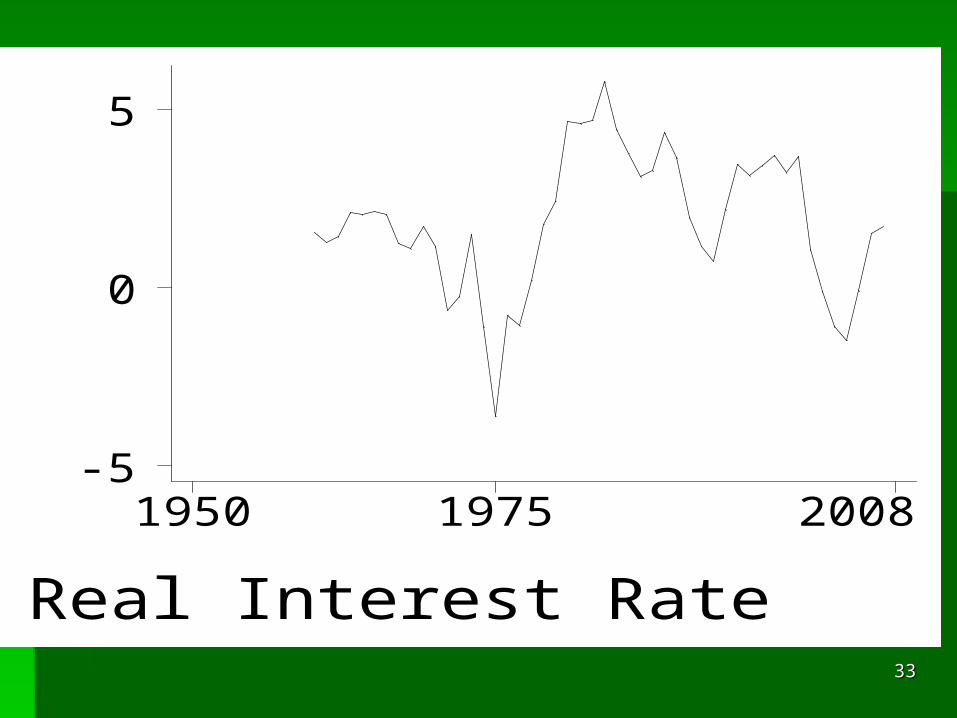

3333

Real Interest Rate

1950 1975 2008-5

0

5

3434

Log Real G-7 GDP

1950 1975 200829

29.5

30

30.5

31

3535

![[PPT]Energy Economics – II Jeffrey Frankel Harpel Professor ... · Web viewEnergy Economics – III Jeffrey Frankel Harpel Professor, Harvard University ADA Summer School, Baku,](https://img.dokumen.tips/doc/110x75/5ab0cb237f8b9abc2f8bdb54/pptenergy-economics-ii-jeffrey-frankel-harpel-professor-viewenergy-economics.jpg)