Embed Size (px)

Citation preview

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 1/77

Asymptotics

Helle Bunzel

Iowa State University

September 26, 2008

Bunzel (ISU) Asymptotics September 26, 2008 1 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 2/77

Asymptotics: What and Why? I

We study the asymptotic behavior of sequences of random variables.

Typical sequence: X 1, 12 (X 1 + X 2) ,

13 ∑

3i =1 X i , ....,

1n ∑

ni =1 X i

Asymptotics: What happens when n ! ∞.

Why is this interesting?

n = ∞ : The largest possible amount of informationFinite sample vs asymptotic distributions.

Many types of convergence concepts for random variables:

1 Convergence in distribution2 Convergence in probability3 Mean square convergence4 Almost sure convergence

Bunzel (ISU) Asymptotics September 26, 2008 2 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 3/77

Convergence in distribution I

De…nition

Let fY ng be a sequence of random variables and let fF ng be the sequenceof associated CDFs. If there exists a CDF F , such that F n (y ) ! F (y ) forall y where F is continuous, then F is called the limiting CDF of fY ng andletting Y have CDF F , we say that Y n converges in distribution to the r.v.

Y .

Also called "convergence in law"

Denoted Y nd ! Y or Y n

L! Y or Y n ) Y or Y nd ! F etc.

If Y is degenerate, we say that Y n converges in distribution to aconstant.

Often we can …nd F , but not F n .

How does this help us?

Bunzel (ISU) Asymptotics September 26, 2008 3 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 4/77

Convergence in distribution II

Sometimes the density is su¢cient to establish convergence indistribution:

Theorem

Let fY ng be a sequence of either co ntinuou s or non-negative, integer valued, discrete random variables, and let ff ng be the corresponding sequence of pdfs. If there exists a density function f such that f n (y ) ! f (y ) , except perhaps on a set of points A such that

P Y (A) = 0, where Y f . Then Y nd ! Y .

Bunzel (ISU) Asymptotics September 26, 2008 4 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 5/77

Convergence in distribution III

A consequence of convergence in distribution is that the mean andthe variance of X n converge to the mean and the variance of X .

Simplistic example: If we sample form a normal distribution, thenX n N µ,

σ 2

n

.

The limiting distribution of X is the degenerate distribution with meanµ and variance 0.

Bunzel (ISU) Asymptotics September 26, 2008 5 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 6/77

Convergence in distribution IExample

Let

fX n

g be a sequence of r.v.s. X n

N (0, 1)

8n.

Let fZ ng be a sequence of r.v.s where Z n =

3 + 1n

X n + 2n

n1 .

Then Z n N

2nn1 ,

3 + 1

n

2

and Z nd ! N (2, 9)

Bunzel (ISU) Asymptotics September 26, 2008 6 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 7/77

Convergence in probability I

De…nition

The sequence of random variables fX ng converges in probability to therandom variable X i¤

a. Scalar case: limn!∞ P (jx n x j<

ε) = 1 8ε>

0b. Matrix case: limn!∞ P (jx n [i , j ] x [i , j ]j < ε) = 1 8ε > 0, 8 i and j

The notation we use is X nP ! X or plim(X n ) = X .

For large enough n, outcomes of X can serve as approximations of outcomes of X n .

Bunzel (ISU) Asymptotics September 26, 2008 7 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 8/77

Convergence in probability. Examples. I

Example 1:

Let fY ng have an associated sequence of density functionsf n (y ) = n1I f0g (y ) +

1 n1

I f1g (y )

Then limn!∞ P (jy n 1j = 0) = limn!∞

1 n1

= 1 and

plimY n = 1

Example 2:

Let fY ng be such that E (Y n ) =

23

and V (Y n ) = 1

n

2 11 1

.

Then, using Markov’s inequality:

P (jy n [1] 2j < ε) 1 2 1n

ε2 )

limn!∞

P (jy n [1] 2j < ε) limn!∞

1 2 1

n

ε2

! = 1

Bunzel (ISU) Asymptotics September 26, 2008 8 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 9/77

Convergence in probability. Examples. II

and

P (jy n [2] 3j < ε) 1 1n

ε2 )

limn!∞

P (jy n [2] 3j < ε) limn!∞

1 1n

ε2

! = 1

So, Y nP !

23 .

Bunzel (ISU) Asymptotics September 26, 2008 9 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 10/77

Convergence in probability I

Theorem

If limn!∞E (X n ) = µ and limn!∞V (X n ) = 0 then plimX n = µ

Prove using Chebychev’s inequality.

Events or distributions. What is the di¤erence?

Many di¤erent experiments can have the same distributions.Convergence in probability talks speci…cally about the probability of speci…c events.

Bunzel (ISU) Asymptotics September 26, 2008 10 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 11/77

Convergence in probability II

TheoremLet X n

P ! X , and let g be a functio n which is continuous, except perhaps on a set of points with probability 0. Thenplim g (X n ) = g (plim (X n )) .

EXTREMELY useful theorem.

Consider example from before where plimY n [1] = 2.

Using the theorem we know that plim 1Y n [1]

= 12 .

But we couldn’t do the calculations from scratch since we don’t knowE

1Y n [1]

.

Bunzel (ISU) Asymptotics September 26, 2008 11 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 12/77

Convergence in probability, Examples I

Let fX ng be a strictly positive valued r.v. such that X nP ! 3. Then

Y n = g (X n ) = ln (X n ) +p

X nP

!ln (3) +

p 3 = 2.8307

Let fX ng : k 1 be such that X nP ! X N (0, I k ) and let

Y n = g (X n ) = X 0nX n . Then Y nP ! X 0X χ2 (k )

Bunzel (ISU) Asymptotics September 26, 2008 12 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 13/77

Convergence in probability IProperties

For conformable r.v.s X n , Y n and constant matrix A :

1 plim AX n = A plimX n

2 plim ∑ mi =1 X n [i ] = ∑ mi =1 plimX n [i ]3 plim ∏

mi =1 X n [i ] = ∏

mi =1 plimX n [i ]

4 plim X nY n = plimX n plimY n

5 plim X 1n Y n = (plimX n )1

plimY n

Bunzel (ISU) Asymptotics September 26, 2008 13 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 14/77

Convergence in probability, Examples I

Let A = 2 11 1 and let fX ng be such that plim X n =

25 . Then

plim AX n = A plim X n =

2 11 1

25

=

97

and

plim (X n [1] + X n [2]) = plim X n [1] + plim X n [2] = 2 + 5 = 7

and

plim (X n [1] X n [2]) = (plim X n [1]) (plim X n [2]) = 2 5 = 10

Bunzel (ISU) Asymptotics September 26, 2008 14 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 15/77

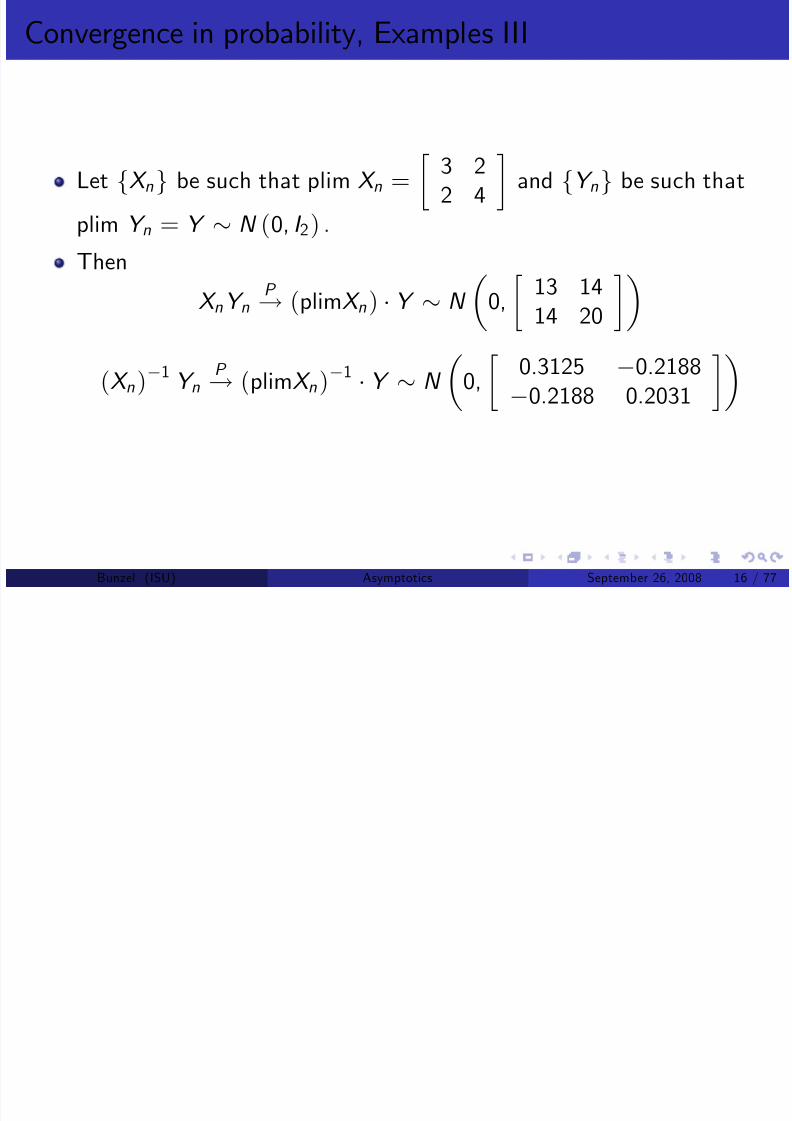

Convergence in probability, Examples II

Let fY ng be such that plim Y n =

1 22 1

and fX ng be such that

plim X n =

3 12 1

.

Then

plimX nY n = plimX n

plimY n = 3 1

2 1 1 2

2 1 = 5 7

4 5

plim (X n )1 Y n = (plimX n )1 plimY n = 3 12 1

1

1 22 1

=

1 12 3

1 22 1

=

1 14 1

Bunzel (ISU) Asymptotics September 26, 2008 15 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 16/77

C i b I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 17/77

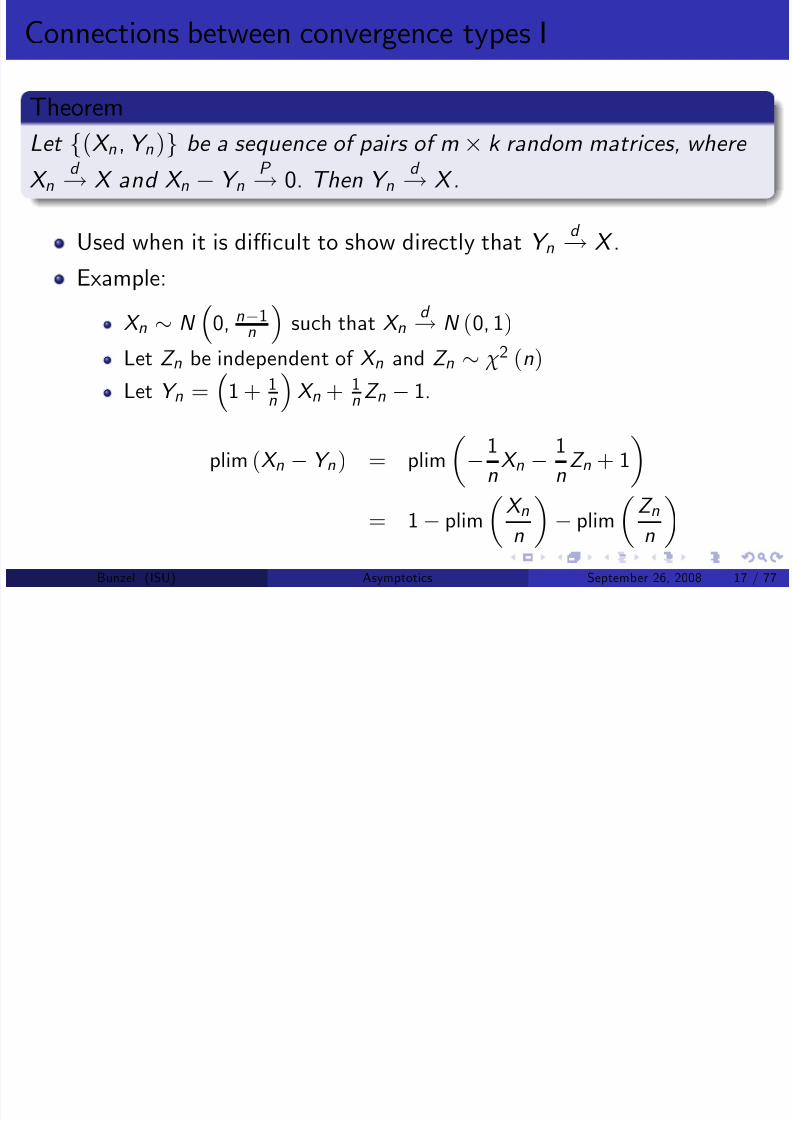

Connections between convergence types I

Theorem

Let f(X n , Y n )g be a sequence of pairs of m k random matrices, where X n

d ! X and X n Y nP ! 0. Then Y n

d ! X .

Used when it is di¢cult to show directly that Y nd ! X .

Example:

X n N

0, n1

n

such that X n

d ! N (0, 1)

Let Z n be independent of X n and Z n χ2 (n)

Let Y n = 1 + 1nX n + 1

n Z n

1.

plim (X n Y n ) = plim

1

nX n 1

nZ n + 1

= 1 plimX nn plim

Z nn

Bunzel (ISU) Asymptotics September 26, 2008 17 / 77

C i b II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 18/77

Connections between convergence types II

Now, E

X nn

= 0, V

X nn

= n1

n3 ! 0 so plim

X nn

= 0

E Z nn = 1, V Z n

n = 2n

!0 so plimZ n

n = 1

This implies that plim(X n Y n ) = 0 and theref ore Y nd ! N (0, 1)

Theorem

Y nP

! Y ) Y nd

! Y

Previous theorem with X n = Y 8n.

Bunzel (ISU) Asymptotics September 26, 2008 18 / 77

C i b III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 19/77

Connections between convergence types III

Theorem

Y nd

! c ) Y nP

! c

Not true unless the limit is a constant.

Proof:

Y nd

! c ) F n (y ) ) F (y ) = 1fy c g (y )P (jy n c j < ε) = F n (c + ε) F n (c ε) ! 1

Theorem

Let fX ng : k m, fY ng : l q , and fang : j p be such that X nd

! X ,Y n

P ! Y and an ! a. Let B be such that P X (B ) = 1 and let the randomvariable g (X n , Y n , an ) be de…ned by a function g that is continuous at

every point in B y a. Then g (X n , Y n , an ) d ! g (X , Y , a)

Bunzel (ISU) Asymptotics September 26, 2008 19 / 77

C ti b t t E l I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 20/77

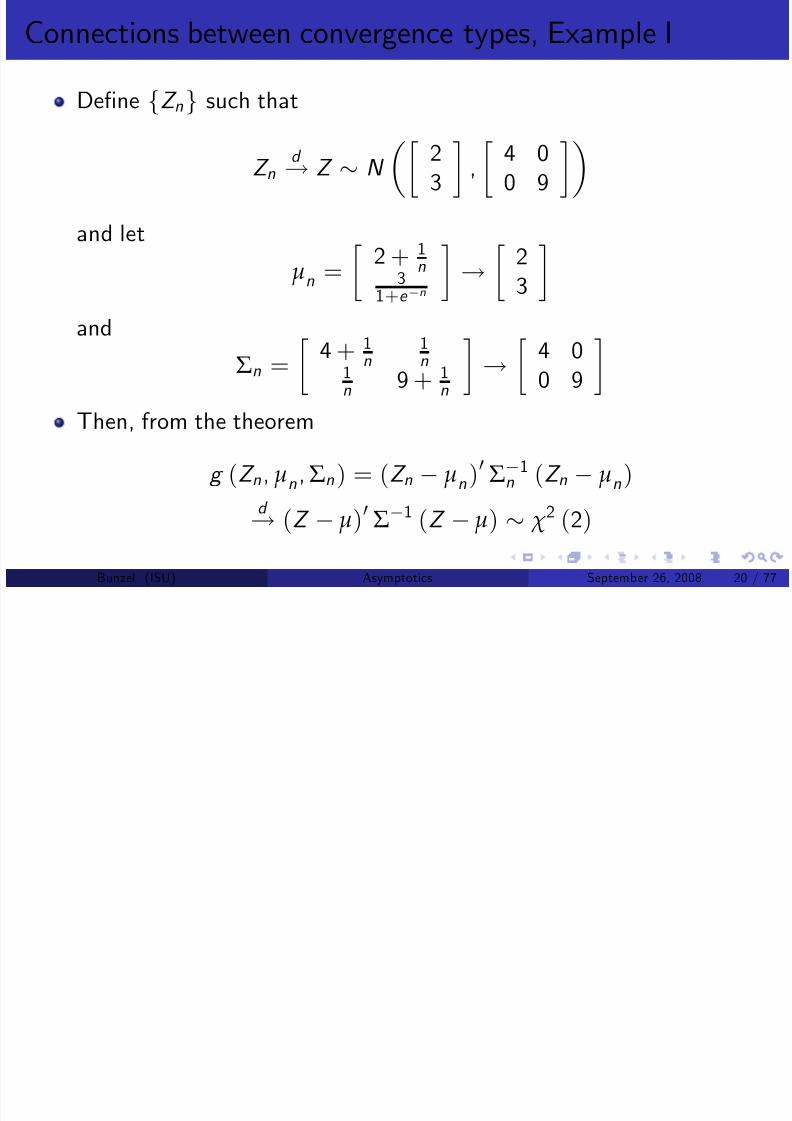

Connections between convergence types, Example I

De…ne fZ ng such that

Z nd ! Z N

23

,

4 00 9

and let

µn = 2 + 1

n

31+e n ! 2

3

and

Σn =

4 + 1

n1n

1n 9 + 1

n

!

4 00 9

Then, from the theorem

g (Z n , µn ,Σn ) = (Z n µn )0Σ1

n (Z n µn)

d ! (Z µ)0Σ1 (Z µ) χ2 (2)

Bunzel (ISU) Asymptotics September 26, 2008 20 / 77

C ti b t t I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 21/77

Connections between convergence types I

Theorem

Slutsky’s Theorems: Let X nd ! X and Y n

P ! c . Then, for conformable X nand Y n

a. X n + Y n d ! X + c b. Y n X n

d ! cX

c. Y 1n X n

d ! c 1X

All special cases of previous theorem.

Bunzel (ISU) Asymptotics September 26, 2008 21 / 77

Order of magnitude in probability I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 22/77

Order of magnitude in probability I

De…nition

Let fX ng be a sequence of random scalars. Thena. The sequence fX ng is said to be at most of order nk in probability,denoted by O P nk i¤ for every ε > 0 there exists a corresponding positive

constant c (ε) < ∞ such that P

nk

jX n j c (ε) 1 ε for all n.

b. The sequence fX ng is said to be of order smaller than nk in probability,

denoted by o P

nk

i¤ nk X nP ! 0.

Main use: Find out which terms are irrelevant as n increases.O P (1) : Bounded in probability.

Bunzel (ISU) Asymptotics September 26, 2008 22 / 77

Example I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 23/77

Example I

Let fX ng be such that X i N (0, 1) 8i and all the X i areindependent.

Let fZ ng be de…ned as Z n = ∑ ni =1 X i .

What are the orders of X n and Z n?

Note that we can always …nd a c (ε) large enough that

P (jX n j c (ε)) = 2

Z c (ε)

0N (x ; 0, 1) dx 1 ε

So, X n = O P (1)Consider Z n :

Z n =n

∑ i =1

X i N (0, n)

Bunzel (ISU) Asymptotics September 26, 2008 23 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 24/77

Mean Square Convergence I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 25/77

Mean Square Convergence I

Also called Convergence in Quadratic Mean.

De…nition

The sequence of random variables fY ng converges in mean square to therandom variable Y i¤ a. Scalar case: limn!∞ E (Y n Y )2 = 0b. Matrix case: limn!∞ E (Y n [i , j ] Y [i , j ])2 = 0 8i , j

Notation: Y n m! Y

Bunzel (ISU) Asymptotics September 26, 2008 25 / 77

Mean Square Convergence II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 26/77

Mean Square Convergence II

Theorem

Y nm! Y i¤

a. E (Y n [i , j ]) ! E (Y [i , j ])b. V (Y n [i , j ]) ! V (Y [i , j ])b. Cov (Y n [i , j ] , Y [i , j ])

!V (Y [i , j ])

Proof, scalar case only.

Y nm! Y ) a. b. and c.

a.

jEY n EY j = jE (Y n Y )j E jY n Y j h

E jY n Y j2i 1

2 ! 0

Bunzel (ISU) Asymptotics September 26, 2008 26 / 77

Mean Square Convergence III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 27/77

Mean Square Convergence III

b.V (Y n ) = E (Y n EY n )2 = E

Y 2n

(EY n )2

E

Y 2n

= E (Y n Y )2 + E

Y 2

+ 2E (Y (Y n Y ))

By Cauchy-Schwartz

jE (Y (Y n

Y ))

j hE Y 2E ((Y n

Y ))2i12

,

h

E

Y 2

E

((Y n Y ))2i 1

2 E (Y (Y n Y ))

hE Y 2 E ((Y n Y ))2

i12

and therefore

E (Y n Y )2 + E

Y 2

2h

E

Y 2

E

((Y n Y ))2i 1

2 E

Y 2n

E (Y n

Y )2 + E Y 2 + 2 hE Y 2 E ((Y n

Y ))2i

12

Bunzel (ISU) Asymptotics September 26, 2008 27 / 77

Mean Square Convergence IV

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 28/77

Mean Square Convergence IV

Taking limits:

E Y 2 lim

n!∞

E Y 2n E Y 2 ,

limn!∞

E

Y 2n

= E

Y 2

limn!∞

V (Y n ) = limn!∞

E

Y 2n

lim

n!∞(EY n )2 = E

Y 2

(EY )2 = V (Y )

c. We know that

E (Y n Y )2 = E

Y 2n

+ E

Y 2

2E (Y nY ) ! 0

By de…nition

Cov (Y n,

Y ) = E [(Y n EY n ) (Y EY )] = E (Y n Y ) EY n EY ,E (Y n Y ) = Cov (Y n , Y ) + EY n EY

2E (Y n Y ) = 2Cov (Y n , Y ) 2EY n EY

Bunzel (ISU) Asymptotics September 26, 2008 28 / 77

Mean Square Convergence V

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 29/77

Mean Square Convergence V

E (Y n Y )2 = E

Y 2n

+ E

Y 2 2Cov (Y n , Y ) 2EY n EY ! 0

Taking limits on the left side:

2E

Y 2

2 limn!∞

Cov (Y n , Y ) 2 (EY )2 = 0

limn!∞Cov (Y n,

Y ) = V (Y )

Now prove that a. b. and c. imply Y nm! Y .

E (Y n Y )2 = E Y 2n + E Y 2 2E (Y nY )

= E

Y 2n

+ E

Y 2 2Cov (Y n , Y ) 2EY nEY

! 2E

Y 2

2V (Y ) 2 (EY )2 = 0

Bunzel (ISU) Asymptotics September 26, 2008 29 / 77

Mean Square Convergence, Example I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 30/77

Mean Square Convergence, Example I

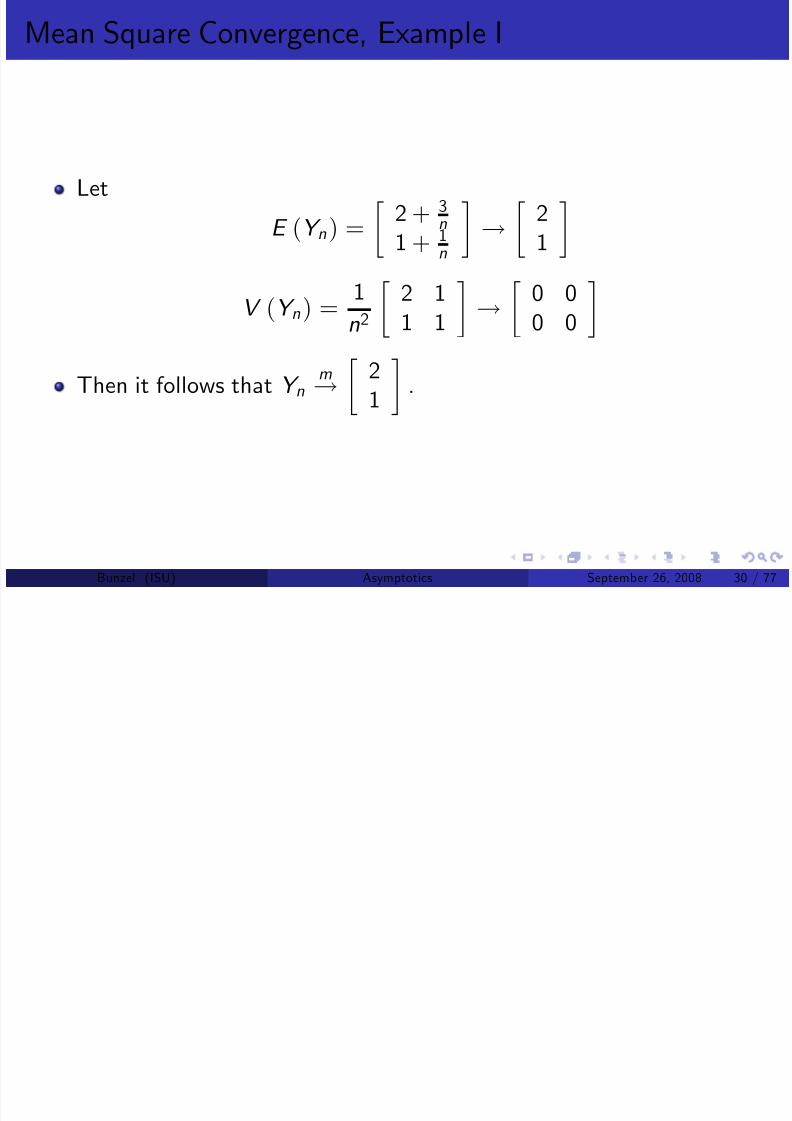

Let

E (Y n ) =

2 + 3

n1 + 1

n

!

21

V (Y n) = 1n2

2 11 1

!

0 00 0

Then it follows that Y nm!

21 .

Bunzel (ISU) Asymptotics September 26, 2008 30 / 77

Mean Square Convergence I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 31/77

Mean Square Convergence I

Corollary

Y nm

! Y ) ρ (Y n [i , j ] , Y [i , j ]) ! 1 when V (Y [i , j ]) > 0 8i , j .

Intuition. Outcomes perfectly correlated with equal variances.

Bunzel (ISU) Asymptotics September 26, 2008 31 / 77

Mean Square Convergence II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 32/77

q g

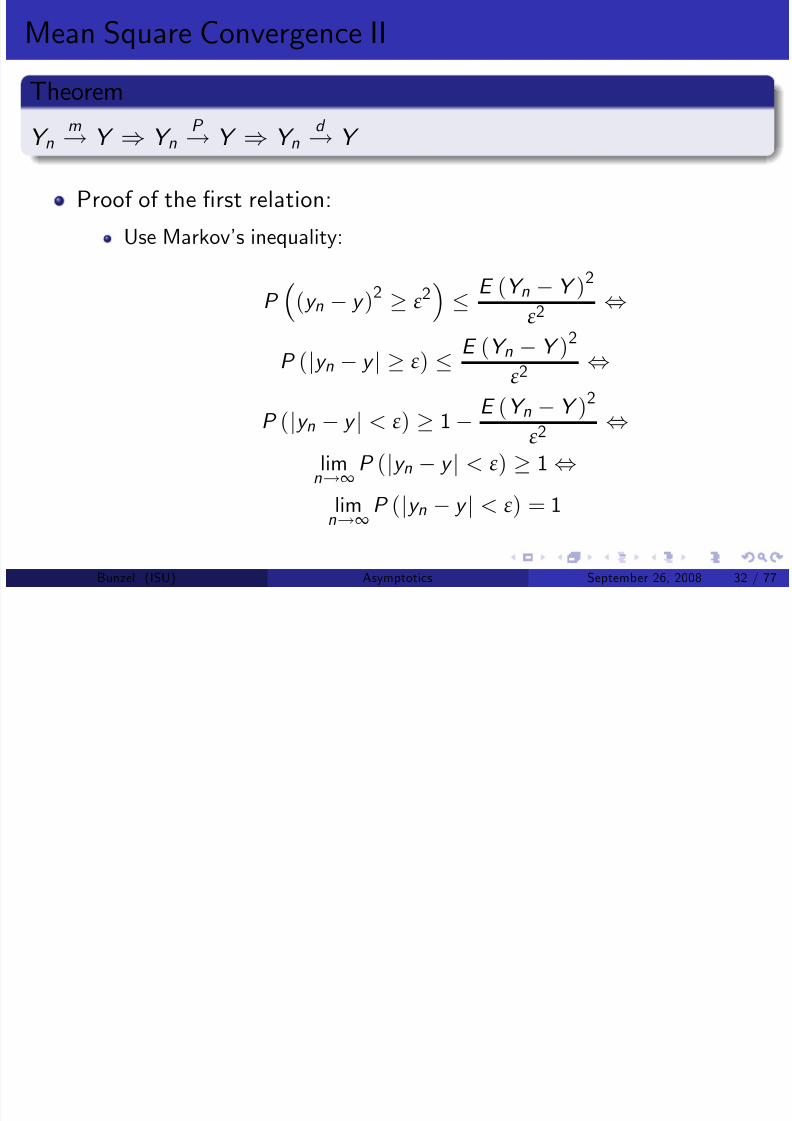

Theorem

Y n

m

! Y ) Y n

P

! Y ) Y n

d

! Y

Proof of the …rst relation:

Use Markov’s inequality:

P

(y n y )2 ε2

E (Y n Y )2

ε2 ,

P (jy n y j ε) E (Y n Y )2

ε2 ,

P (jy n y j < ε) 1 E (Y n

Y )2

ε2 ,lim

n!∞P (jy n y j < ε) 1 ,

limn!∞

P (jy n y j < ε) = 1

Bunzel (ISU) Asymptotics September 26, 2008 32 / 77

Mean Square Convergence, Example I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 33/77

q g , p

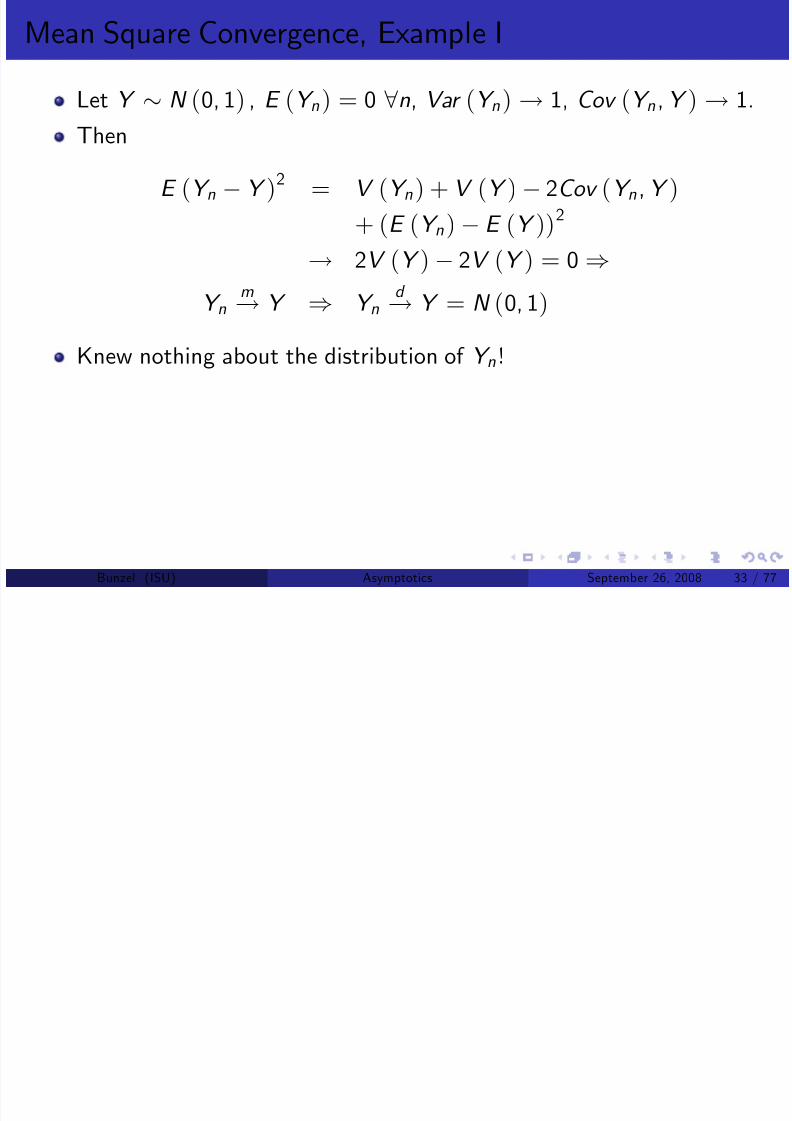

Let Y N (0, 1) , E (Y n ) = 0 8n, Var (Y n ) ! 1, Cov (Y n , Y ) ! 1.

Then

E (Y n Y )2 = V (Y n ) + V (Y ) 2Cov (Y n , Y )

+ (E (Y n ) E (Y ))2

! 2V (Y )

2V (Y ) = 0

)Y nm! Y ) Y n

d ! Y = N (0, 1)

Knew nothing about the distribution of Y n !

Bunzel (ISU) Asymptotics September 26, 2008 33 / 77

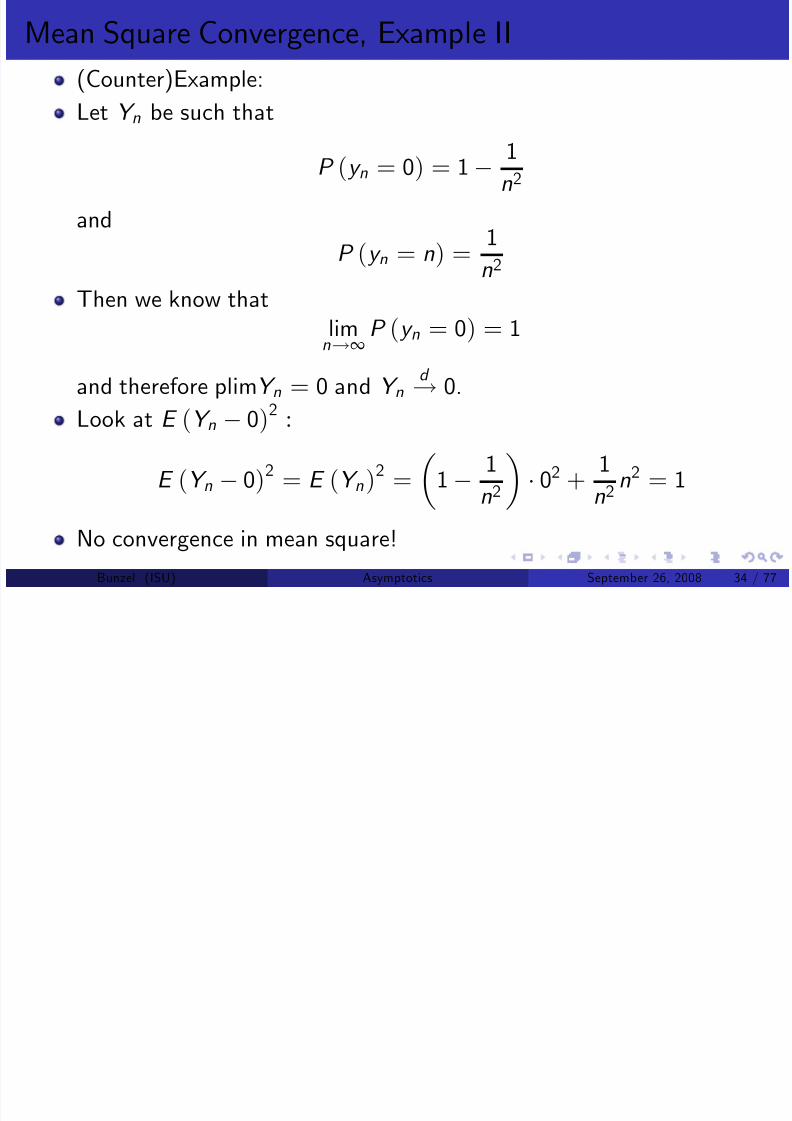

Mean Square Convergence, Example II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 34/77

q g p

(Counter)Example:

Let Y n be such that

P (y n = 0) = 1 1n2

and

P (y n = n) = 1

n2

Then we know thatlim

n!∞P (y n = 0) = 1

and therefore plimY n = 0 and Y nd ! 0.

Look at E (Y n 0)2

:

E (Y n 0)2 = E (Y n)2 =

1 1

n2

02 +

1

n2n2 = 1

No convergence in mean square!

Bunzel (ISU) Asymptotics September 26, 2008 34 / 77

Almost sure convergence I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 35/77

g

Almost sure convergence is the convergence of outcomes .

De…nition

The sequence of random variables fY ng converges almost surely to therandom variable Y i¤ a. Scalar case: P (limn

!∞ y n = y ) = 1

b. Matrix case: P (limn!∞ y n [i , j ] = y [i , j ]) = 1 8i , j

The notation is Y na.s .! Y .

Note that each sequence of random variables has MANY possible

sequences of outcomes.

Note that Y np ! c ; that limn!∞ y n exists. Why?

For limn!∞ y n = c , it must be the case that8n N (ε) , jy n c j < ε.

Bunzel (ISU) Asymptotics September 26, 2008 35 / 77

Almost sure convergence II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 36/77

A.s. convergence provides this limit with probability 1.

Y n p ! c , P (jy n c j < ε) ! 1 8ε.

This corresponds to

8n N (δ) : 1 P (jy n c j < ε) < δ

or 8n N (δ) : P (jy n c j < ε) > 1 δ

So, for big n, the probability that y n is close to c is high, but not 1. ForNO …xed n is the probability 1, so it certainly isn’t for all n greaterthan N .

Thus, convergence in probability does NOT imply almost sureconvergence.

Bunzel (ISU) Asymptotics September 26, 2008 36 / 77

Almost sure convergence III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 37/77

Theorem

P (limn!∞ y n = y ) = 1 ,limn!∞ P (jy i y j < ε i n) = 1, 8ε > 0.

Alternative de…nition.

Theorem

Y na.s .! Y ) Y n

P ! Y

Proof:

We know that 8ε > 0 limn!∞ P (jy i y j < ε i n) = 1

Bunzel (ISU) Asymptotics September 26, 2008 37 / 77

Almost sure convergence IV

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 38/77

Note that jy i y j < ε i n ) jy n y j < ε, so

P (jy i y j < ε i n) P (jy n y j < ε) )limn!∞P (jy n y j < ε) limn!∞P (jy i y j < ε i n) = 1 8ε ,

limn!∞

P (jy n y j < ε) = 1

Bunzel (ISU) Asymptotics September 26, 2008 38 / 77

Almost sure convergence, (Counter)Example I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 39/77

Let fY ng be a sequence of independent random variables such that

Y n f n (y ) =

1 1

n

I f0g (y ) +

1

nI f1g (y )

Convergence in distribution:

f n (y ) ! f (y ) = I f0g (y ) )Y n

d ! 0

Convergence in probability:Since Y n converges in distribution to a constant, we know that

Y nP ! 0

Bunzel (ISU) Asymptotics September 26, 2008 39 / 77

Almost sure convergence, (Counter)Example II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 40/77

Mean square convergence:

E (Y n 0)2 =

1 1n

02 +

1n 12 =

1n ! 0

Almost sure convergence:

8ε 2 (0,

1) and 8s >

n,

s integer

P (jy i j < ε, n i s )

=s

∏i =n

1 1

i

=

s

∏i =n

i 1

i

=

n 1n

n

n + 1

n + 1n + 2

...

s 2s 1

s 1

s

=

n 1

s ! 0 as s ! ∞

Bunzel (ISU) Asymptotics September 26, 2008 40 / 77

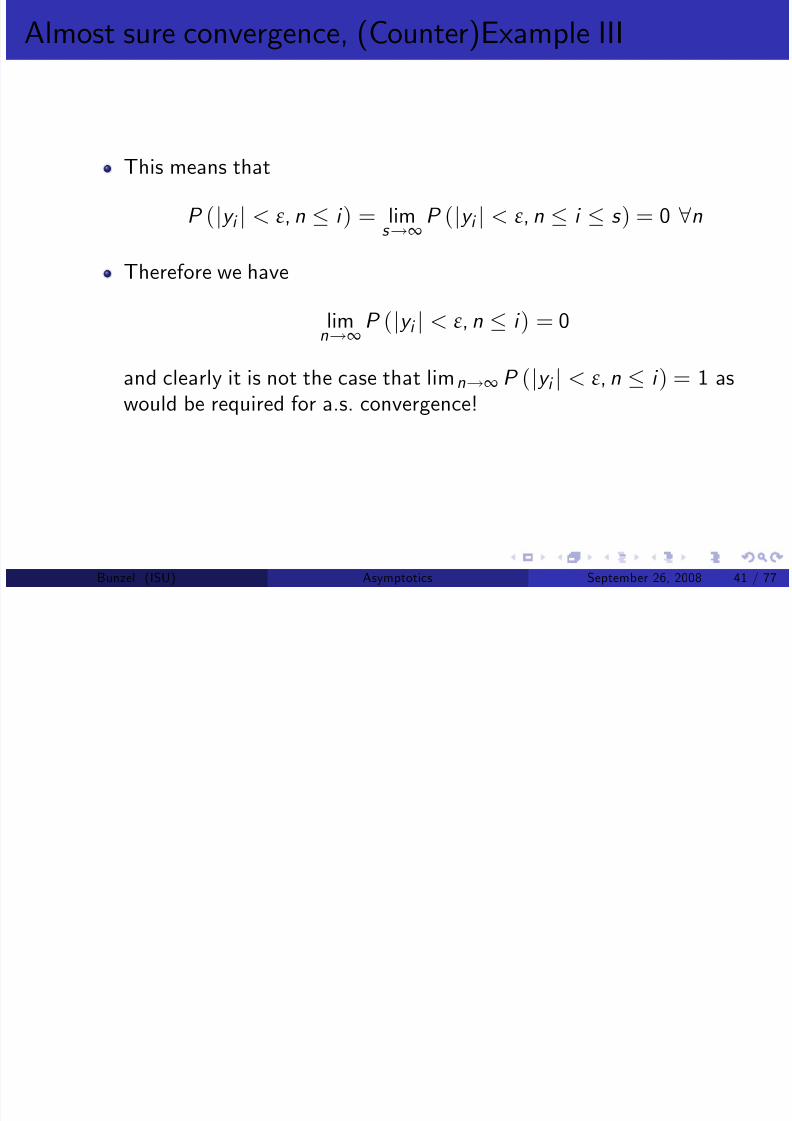

Almost sure convergence, (Counter)Example III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 41/77

This means that

P (jy i j < ε, n i ) = lims !∞

P (jy i j < ε, n i s ) = 0 8n

Therefore we have

limn!∞

P (jy i j < ε, n i ) = 0

and clearly it is not the case that limn!∞ P (jy i j < ε, n i ) = 1 aswould be required for a.s. convergence!

Bunzel (ISU) Asymptotics September 26, 2008 41 / 77

Almost sure convergence, (Counter)Example I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 42/77

Y na.s .! Y ; Y n

m! Y

Let

fY n

g be a sequence of independent random variables such that

Y n f n (y ) =

1 1

n2

I f0g (y ) +

1

n2I fng (y )

8ε

2(0, n) and

8s > n, s integer

P (jy i j < ε, n i s )

=s

∏i =n

1 1

i 2

=

s

∏i =n

i 2 1

i 2

= n2

1

n2 (n+1)2

1

(n+1)2 (n+2)2

1

(n+2)2

... (s

1)2

1

(s 1)2 s 2

1

s 2

=

(n1)(n+1)n2

n(n+2)

(n+1)2

(n+1)(n+3)

(n+2)2

...

(s 3)2s

(s 1)2

(s 1)(s +1)

s 2

= (n 1) (s + 1)

ns Bunzel (ISU) Asymptotics September 26, 2008 42 / 77

Almost sure convergence, (Counter)Example II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 43/77

So

P (jy i j < ε, n i ) = (n 1)n

limn!∞

P (jy i j < ε, n i ) = 1

Which proves that Y na.s .

! Y

Now, note that E (Y n ) = 1n ! 0 but

V (Y n ) =

1 1

n2

1

n2 +

1

n2

n 1

n

2

=

1 1

n2 1

n2 +n2 + 1

n2

2

n2 ! 1

Then, Y n does not converge in mean square.

Bunzel (ISU) Asymptotics September 26, 2008 43 / 77

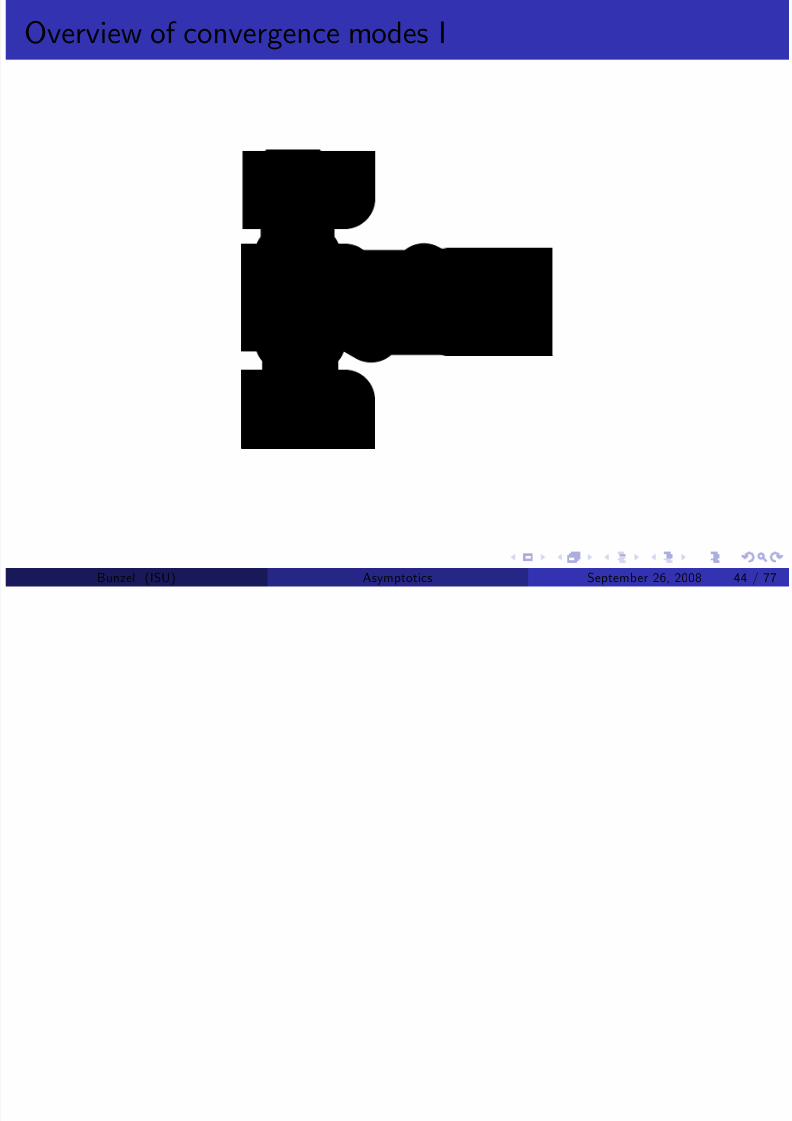

Overview of convergence modes I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 44/77

Yn Ya.s.

Yn YP Yn Yd

Yn Ym

y = c

Bunzel (ISU) Asymptotics September 26, 2008 44 / 77

Almost sure convergence I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 45/77

Theorem

Let X n

a.s .

! X and let the random variable g (X ) be de…ned by a functiong (x ) that is continuous, except perhaps on a set of points assigned

probability 0 by the distribution of X . Then g (X n ) a.s .! g (X ) .

Same as for plim

Example:

Let X na.s .!

21

. Then

g 1 (X n ) =

X n [2]

X n [1]a.s .

! 1

2

g 2 (X n ) = X n [2] X n [1] a.s .! 1

g 3 (X n ) = g 1 (X n ) g 2 (X n ) a.s .! 1

2

Bunzel (ISU) Asymptotics September 26, 2008 45 / 77

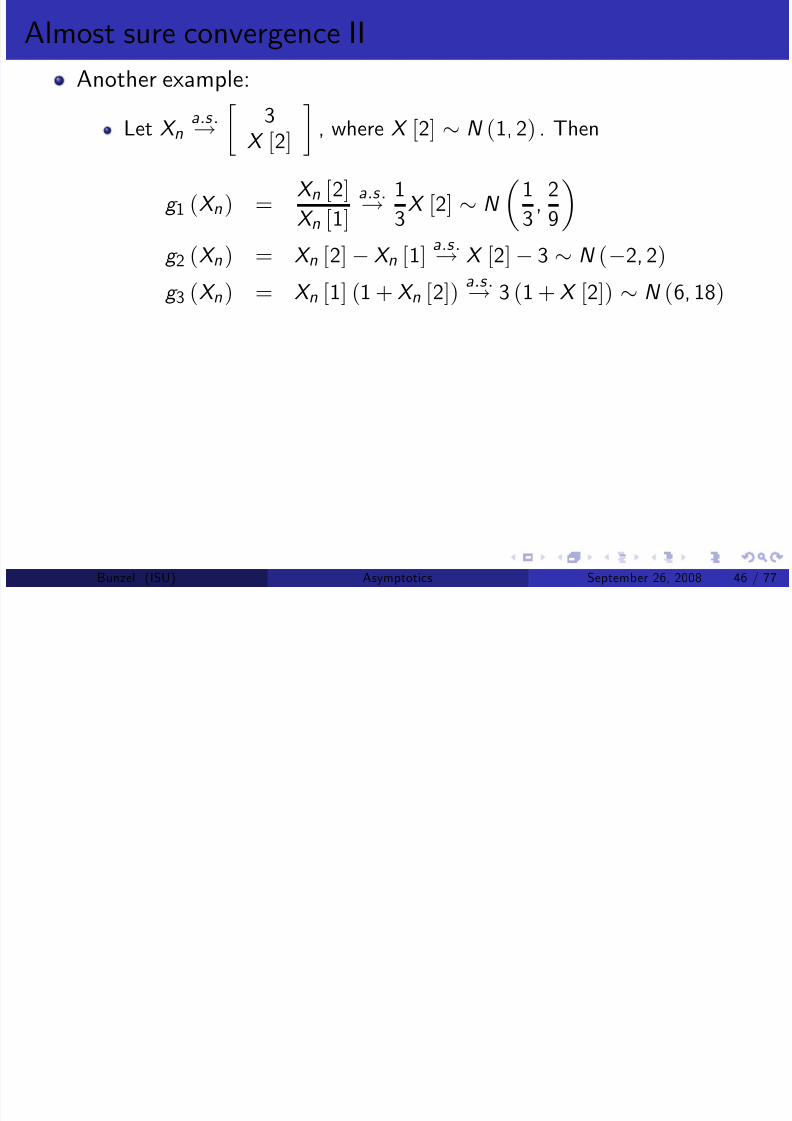

Almost sure convergence II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 46/77

Another example:

Let X na.s .

! 3

X [2] , where X [2]

N (1, 2) . Then

g 1 (X n ) = X n [2]

X n [1]a.s .! 1

3X [2] N

1

3,

2

9

g 2 (X n ) = X n [2] X n [1] a.s .! X [2] 3 N (2, 2)

g 3 (X n ) = X n [1] (1 + X n [2]) a.

s .

! 3 (1 + X [2]) N (6, 18)

Bunzel (ISU) Asymptotics September 26, 2008 46 / 77

Almost sure convergence III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 47/77

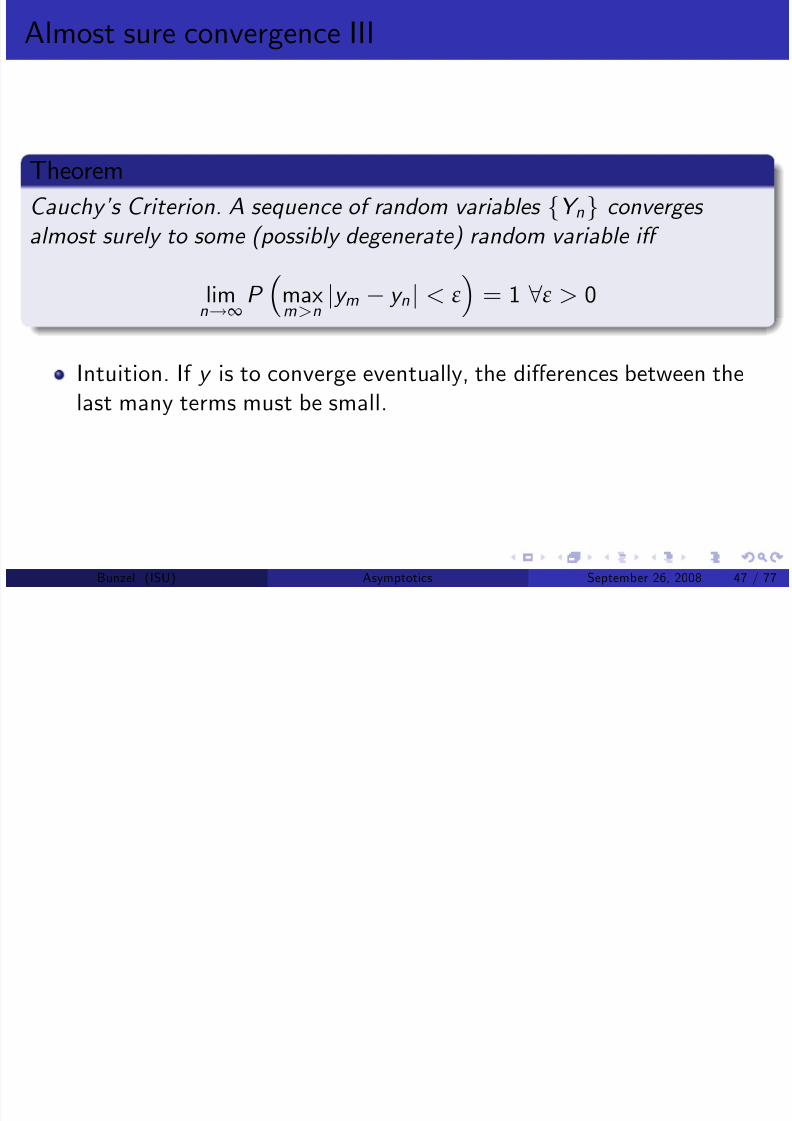

Theorem

Cauchy’s Criterion. A sequence of r andom variables fY ng converges almost surely to some (possibly degenerate) random variable i¤

limn!∞P

maxm>n jy m y n j < ε

= 1 8ε > 0

Intuition. If y is to converge eventually, the di¤erences between thelast many terms must be small.

Bunzel (ISU) Asymptotics September 26, 2008 47 / 77

Laws of Large Numbers I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 48/77

Laws of large numbers give results f or the convergence of sequences

fX ng , where

X n = 1

n

n

∑ i =1

X i

If data is generated by f

X ng

,

fX n

g is the sequence of sample means.

Convergence in probability: Weak Laws of Large Numbers (WLLN)

Almost Sure Convergence: Strong Laws of Large Numbers (SLLN)

Two types of Laws of Large Numbers:

1 If E (X i ) = µ 8i , ¯

X n ! µ2 If E (X i ) = µi (not the same for all i ), X n µn ! 0, where

µn = 1n ∑

ni =1 µi

Bunzel (ISU) Asymptotics September 26, 2008 48 / 77

WLLN I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 49/77

Weak Laws of Large Numbers, basic idea:Impose conditions such that the limiting distribution of Y n = 1

n ∑ ni =1 (X i µi ) is degenerate on 0.

This happens when ∑ ni =1 (X i µi ) = o P (n)

Suppose X i are iid with mean µ and variance σ 2?

BUT: Neither iid nor existence of variance is required.

Theorem

(Khinchin’s WLLN) Let fX ng be a sequenc e of iid random variables, and suppose E (X i ) = µ < ∞, 8i . Then X n

P ! µ.

Bunzel (ISU) Asymptotics September 26, 2008 49 / 77

WLLN, Examples I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 50/77

Let fX ng be a sequence of random variables such thatX i p x (1 p )1x 1f0,1g (x ) 8i . Then E (X i ) = p 8i and by

Khinchin’s WLLN X nP ! p .

Let f (x ) = 2x 31[1,∞) (x ) and suppose the sequence of random

variables fX ng is iid such that X i f (x ) . Then

E (X i ) =Z ∞

∞x 2x 31[1,∞) (x ) dx =

Z ∞1

2x 2dx

= 2x 1∞1 = 2

By Khinchin’s WLLN X nP ! 2.

Bunzel (ISU) Asymptotics September 26, 2008 50 / 77

WLLN, Examples II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 51/77

BUT: Note that

V (X i ) = E

X 2i 4

= Z ∞

∞x 22x 31[1,∞) (x ) dx

4

=Z ∞

12x 1dx 4

= [2 ln (x )]∞1 4 ! ∞

Bunzel (ISU) Asymptotics September 26, 2008 51 / 77

WLLN I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 52/77

Theorem

(Convergence in Probability of Relat ive Fre quency) Let A be any event in

the sample space. Let an outcome N A be the number of times that anevent occurs in n independent and identical repetitions of the experiment.

Then the relative frequency of event A occurring is such that N An

P ! P (A)

The relative frequence can be used as a measure of the probability asn ! ∞.

Now relax iid assumption. Cost: Assume existence of variances.

Bunzel (ISU) Asymptotics September 26, 2008 52 / 77

WLLN II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 53/77

Theorem

Let fX ng be a sequence of random variable s with …nite variances, and let fµng be the corresponding sequence of expected values. Then

limn!∞

P (jx n µn j < ε) = 1, 8ε > 0

i¤

E

" ( X n µn )

2

1 + ( X n µn )2

#! 0

Usage: Any conditions which imply that E

( X nµn )2

1+( X nµn )2

! 0 will

provide a WLLN.

Bunzel (ISU) Asymptotics September 26, 2008 53 / 77

WLLN III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 54/77

Theorem

(WLLN for non-iid case) Let fX ng be a seq uence of random variables with

…nite variances, and let fµng be the corresponding sequence of expected values. If Var ( X n ) ! 0, then ( X n µn )

P ! 0.

Bunzel (ISU) Asymptotics September 26, 2008 54 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 55/77

WLLN, Example II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 56/77

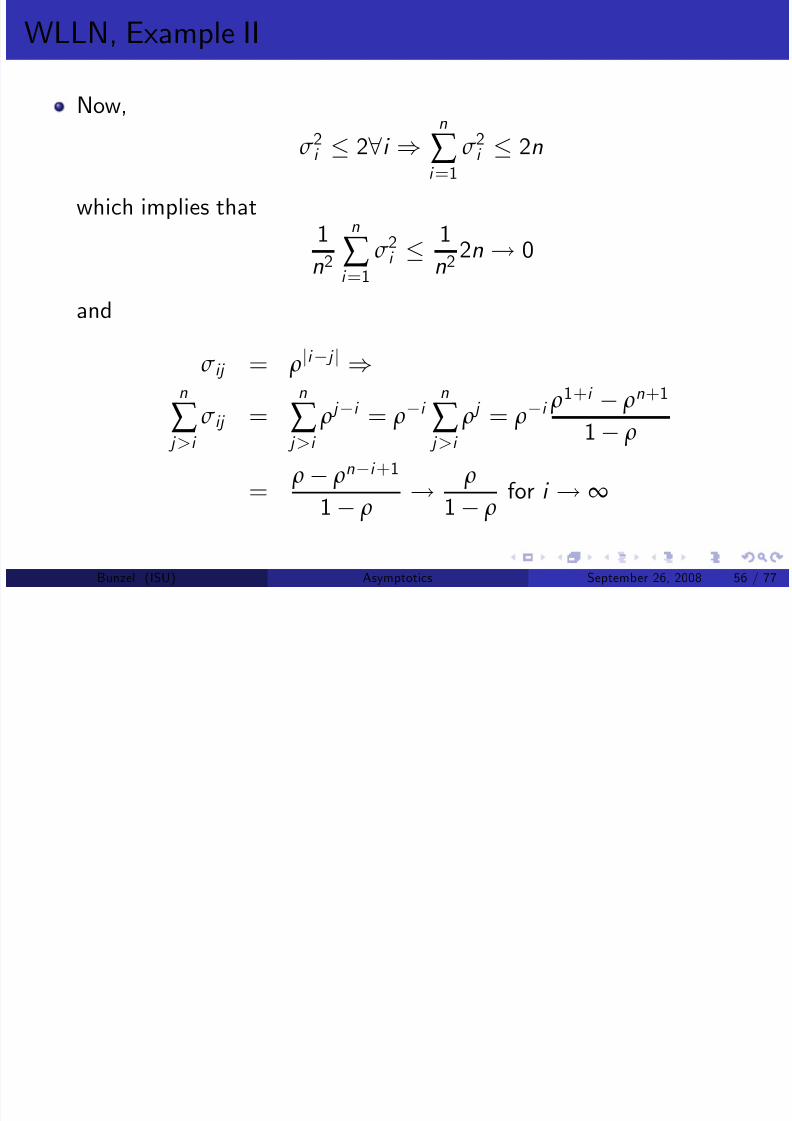

Now,

σ 2

i 28i )n

∑ i =1 σ 2

i 2n

which implies that1

n2

n

∑ i =1

σ 2i 1

n22n ! 0

and

σ ij = ρji j j )n

∑ j >i

σ ij =n

∑ j >i

ρ j i = ρi n

∑ j >i

ρ j = ρi ρ1+i ρn+1

1 ρ

= ρ ρni +1

1 ρ ! ρ

1 ρ for i ! ∞

Bunzel (ISU) Asymptotics September 26, 2008 56 / 77

WLLN, Example III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 57/77

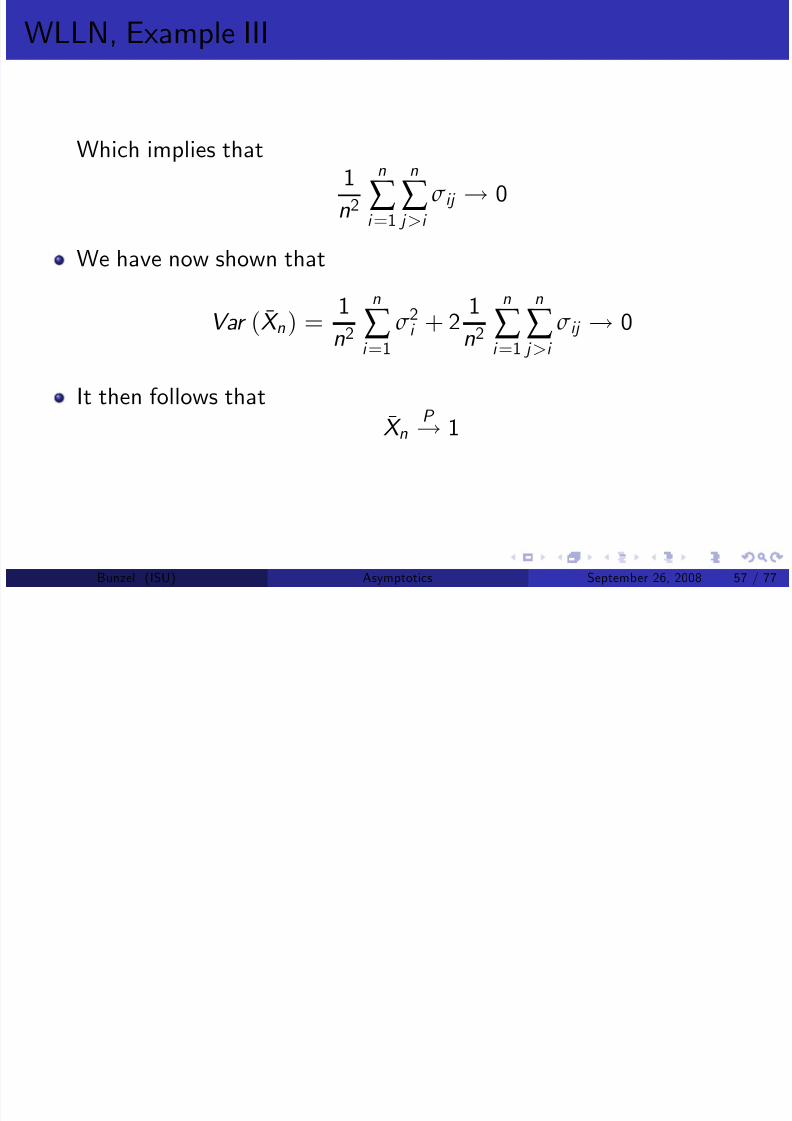

Which implies that 1

n2

n

∑ i =1

n

∑ j >i

σ ij ! 0

We have now shown that

Var ( X n ) = 1

n2

n

∑ i =1

σ 2i + 2 1

n2

n

∑ i =1

n

∑ j >i

σ ij ! 0

It then follows that¯

X nP

! 1

Bunzel (ISU) Asymptotics September 26, 2008 57 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 58/77

SLLN I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 59/77

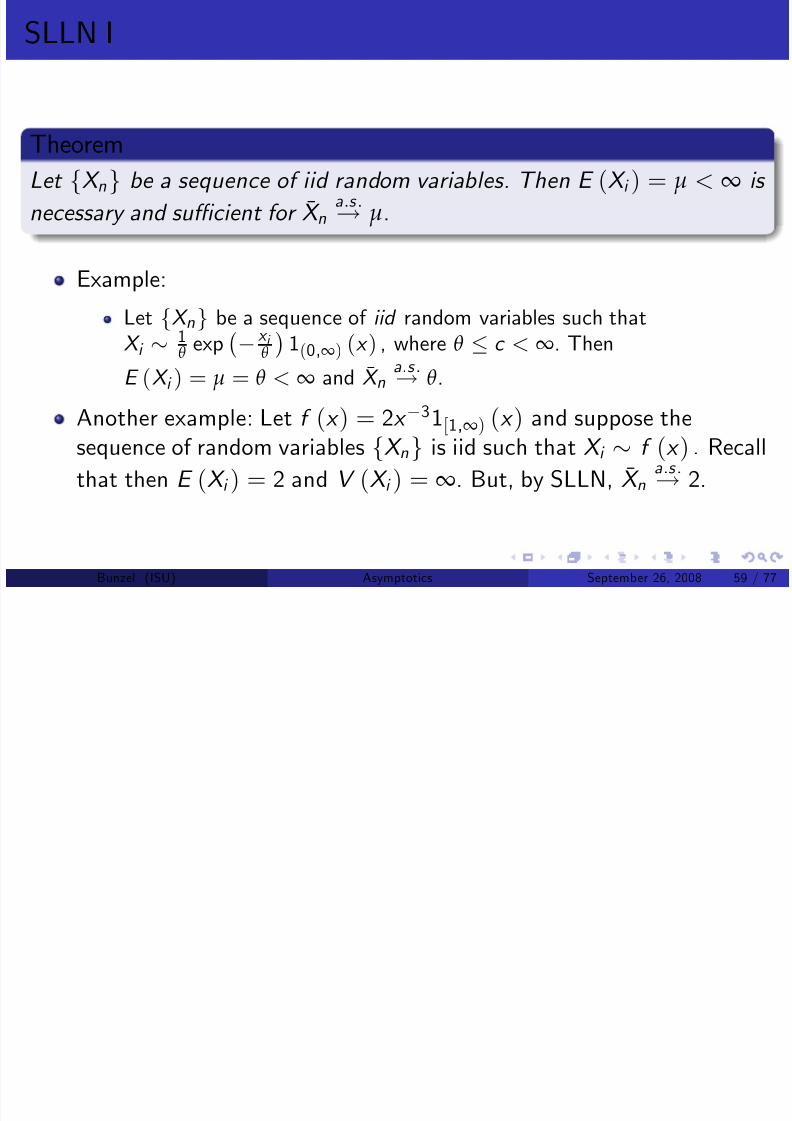

TheoremLet fX ng be a sequence of iid rand om variables. Then E (X i ) = µ < ∞ is

necessary and su¢cient for X na.s .! µ.

Example:

Let fX ng be a sequence of iid random variables such thatX i 1

θ exp x i

θ

1(0,∞) (x ) , where θ c < ∞. Then

E (X i ) = µ = θ < ∞ and X na.s .! θ.

Another example: Let f (x ) = 2x

31[1

,

∞) (x ) and suppose the

sequence of random variables fX ng is iid such that X i f (x ) . Recall

that then E (X i ) = 2 and V (X i ) = ∞. But, by SLLN, X na.s .! 2.

Bunzel (ISU) Asymptotics September 26, 2008 59 / 77

SLLN II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 60/77

Theorem

(A.s. convergence of relative freque ncy) Let A be any event in the sample space. Let an outcome N A be the number of times that an event occurs inn independent and identical repetitions of the experiment. Then the

relative frequency of event A occurring is such that N

An

a.s .

! P (A)

Theorem

If ( X n µn ) a.s .! 0 and µn ! c then X n

a.s .! c

Bunzel (ISU) Asymptotics September 26, 2008 60 / 77

Central Limit Theorems I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 61/77

CLT: Asymptotic distribution of sequences of random variables.

Typical CLT: Sequence of r.v.s such that

Y n = b 1n (S n an )

d ! N (0,Σ)

where

fS n

g is a sequence such that S n = ∑

ni =1 X i .

CLT provides restrictions on fX ng , fang, and fb ng such that theconvergence in distribution occurs.

Main usage: Distribution of parameter estimates and test statistics, if

Finite sample distribution is unknown, or

Finite sample distribution is hard to work with.

A good illustration:http://www.statisticalengineering.com/central_limit_theorem.htm

Bunzel (ISU) Asymptotics September 26, 2008 61 / 77

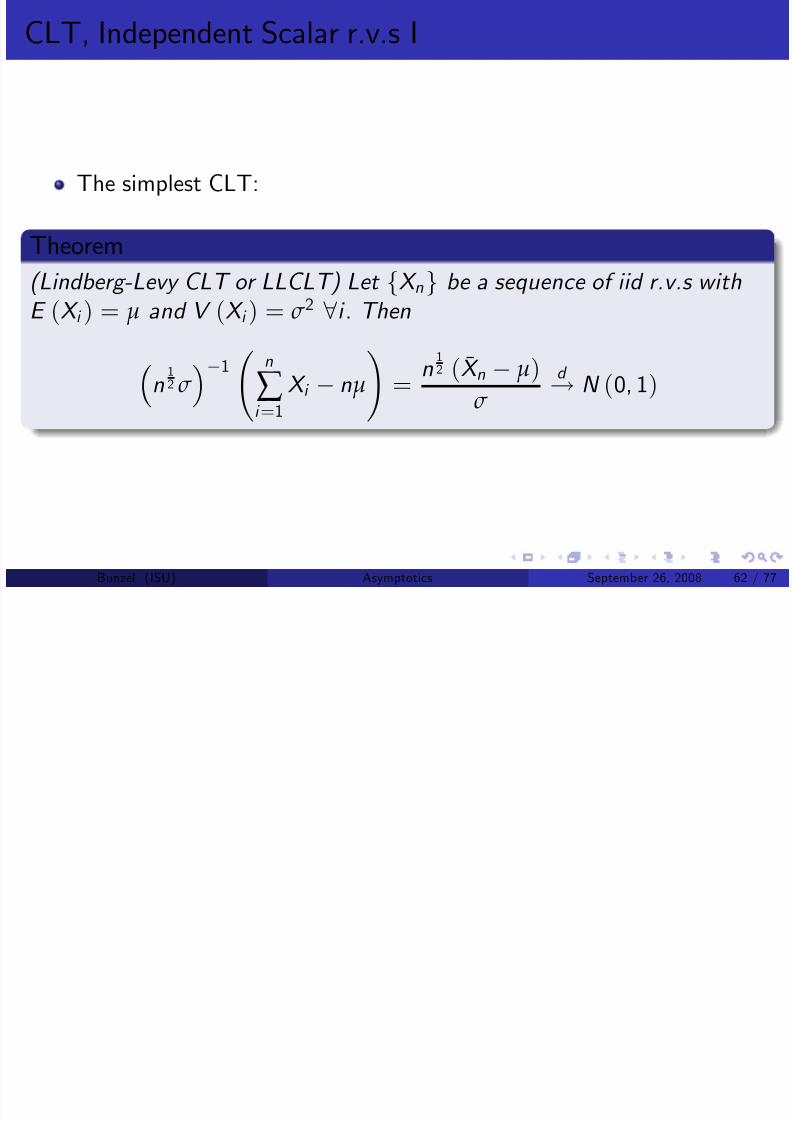

CLT, Independent Scalar r.v.s I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 62/77

The simplest CLT:

Theorem

(Lindberg-Levy CLT or LLCLT) Let f

X ng

b e a sequence of iid r.v.s withE (X i ) = µ and V (X i ) = σ 2 8i . Then

n

12 σ

1

n

∑ i =1

X i nµ

! =

n12 ( X n µ)

σ

d ! N (0, 1)

Bunzel (ISU) Asymptotics September 26, 2008 62 / 77

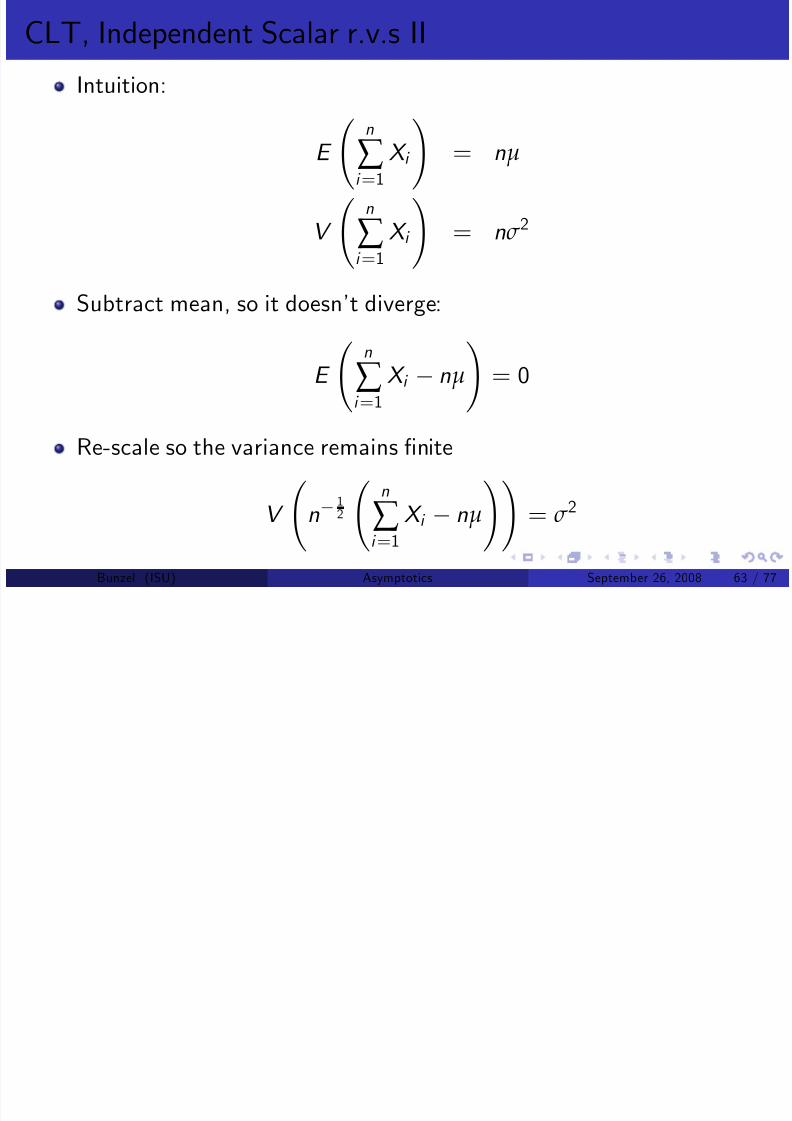

CLT, Independent Scalar r.v.s II

Intuition:

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 63/77

Intuition:

E n

∑ i =1 X i !

= nµ

V

n

∑ i =1

X i

! = nσ 2

Subtract mean, so it doesn’t diverge:

E

n

∑ i =1

X i nµ

! = 0

Re-scale so the variance remains …nite

V

n 1

2

n

∑ i =1

X i nµ

!! = σ 2

Bunzel (ISU) Asymptotics September 26, 2008 63 / 77

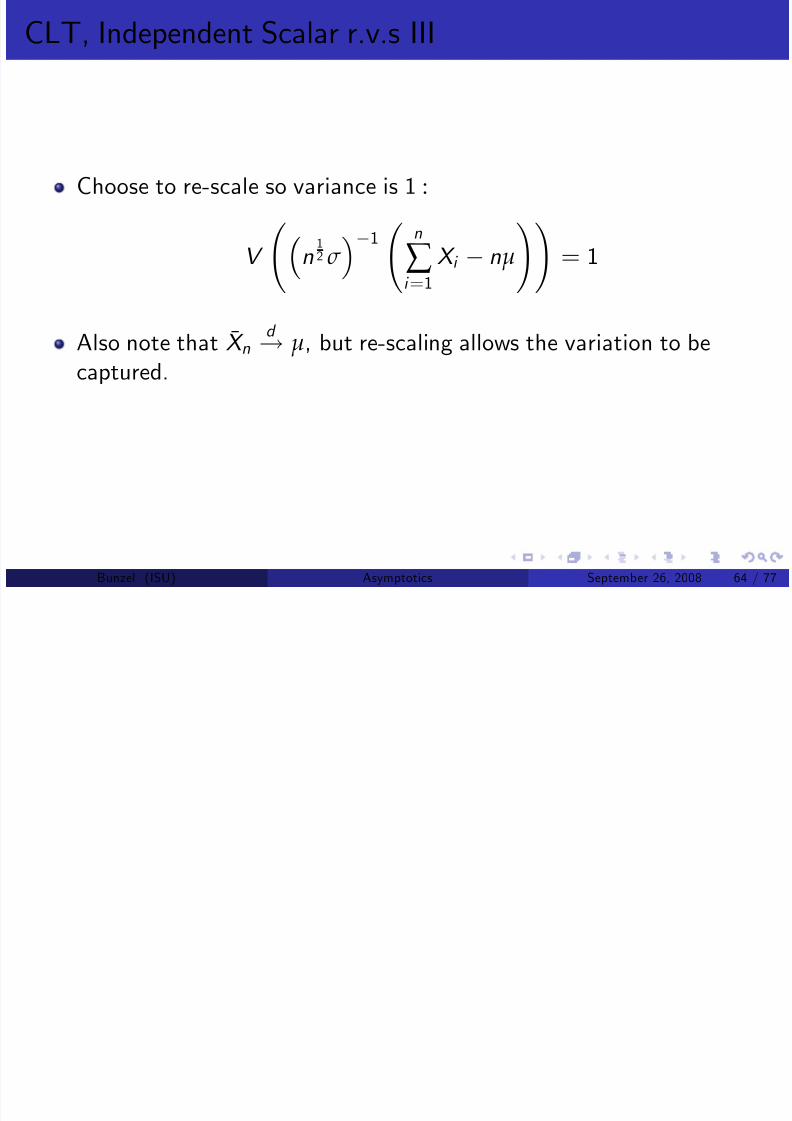

CLT, Independent Scalar r.v.s III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 64/77

Choose to re-scale so variance is 1 :

V

n

12 σ

1

n

∑ i =1

X i nµ

!! = 1

Also note that X nd ! µ, but re-scaling allows the variation to be

captured.

Bunzel (ISU) Asymptotics September 26, 2008 64 / 77

CLT, Independent Scalar r.v.s, Example I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 65/77

Let fX ng be a sequence of χ2 (1) variables. Then E (X i ) = 1 andV (X i ) = 2 and ∑

ni =1 X i χ2 (n) .

Then, by LLCLT

∑ n

i =1 X i nn

12 (2)

12

= ∑

n

i =1 X i n(2n)

12

d ! N (0, 1)

How good is the approximation? In reality we don’t know. There aresome theoretical bounds. Also we often use simulation techniques to

determine how big n should be for the approximation to work well.

Bunzel (ISU) Asymptotics September 26, 2008 65 / 77

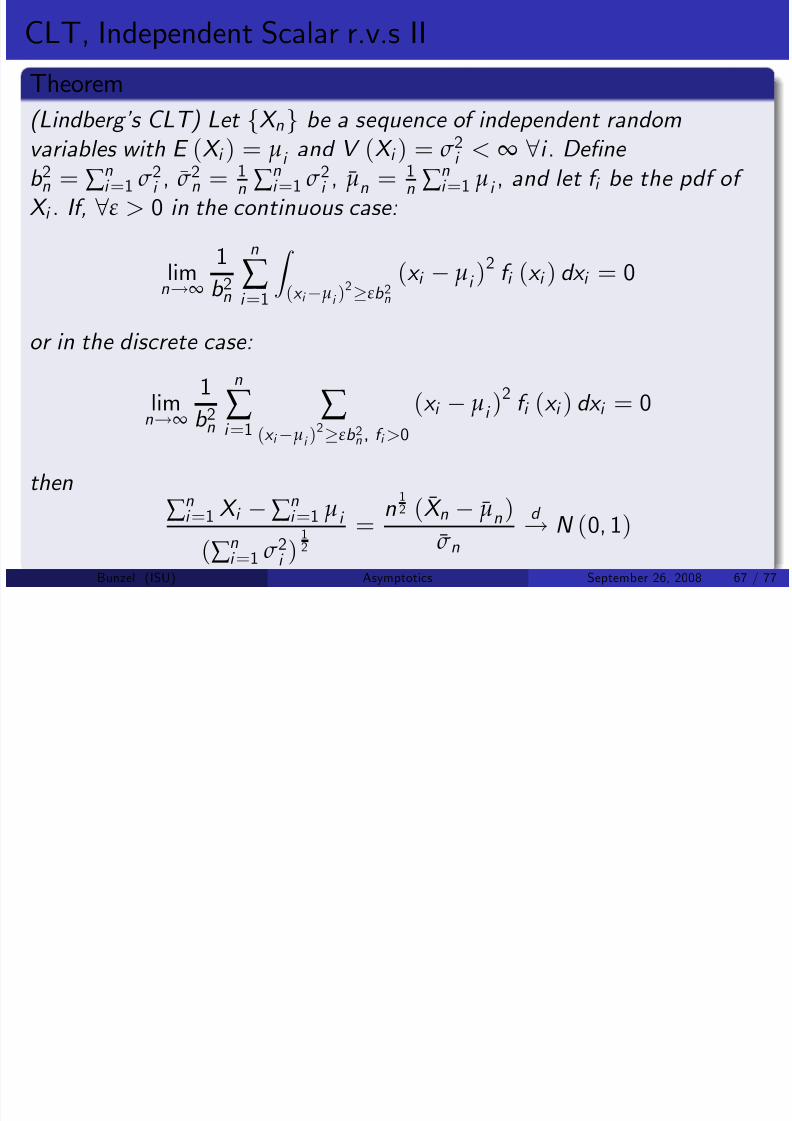

CLT, Independent Scalar r.v.s I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 66/77

A CLT where we don’t require that the variables be iid:

Bunzel (ISU) Asymptotics September 26, 2008 66 / 77

CLT, Independent Scalar r.v.s II

Theorem

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 67/77

(Lindberg’s CLT) Let fX ng be a seq uence o f independent random

variables with E (X i ) = µi and V (X i ) = σ 2

i < ∞

8i .

De…ne b 2n = ∑ ni =1 σ

2i , σ 2n = 1

n ∑ ni =1 σ

2i , µn = 1

n ∑ ni =1 µi , and let f i be the pdf of

X i . If, 8ε > 0 in the continuous case:

lim

n!∞

1

b 2n

n

∑ i =1

Z (x i µi )

2

εb 2n

(x i

µi )

2 f i (x i ) dx i = 0

or in the discrete case:

limn

!∞

1

b 2n

n

∑ i =1

∑ (x i µi )

2

εb 2n , f i >0

(x i µi )2 f i (x i ) dx i = 0

then∑

ni =1 X i ∑

ni =1 µi

(∑ ni =1 σ 2i )

12

= n

12 ( X n µn )

σ n

d ! N (0, 1)

Bunzel (ISU) Asymptotics September 26, 2008 67 / 77

CLT, Independent Scalar r.v.s I

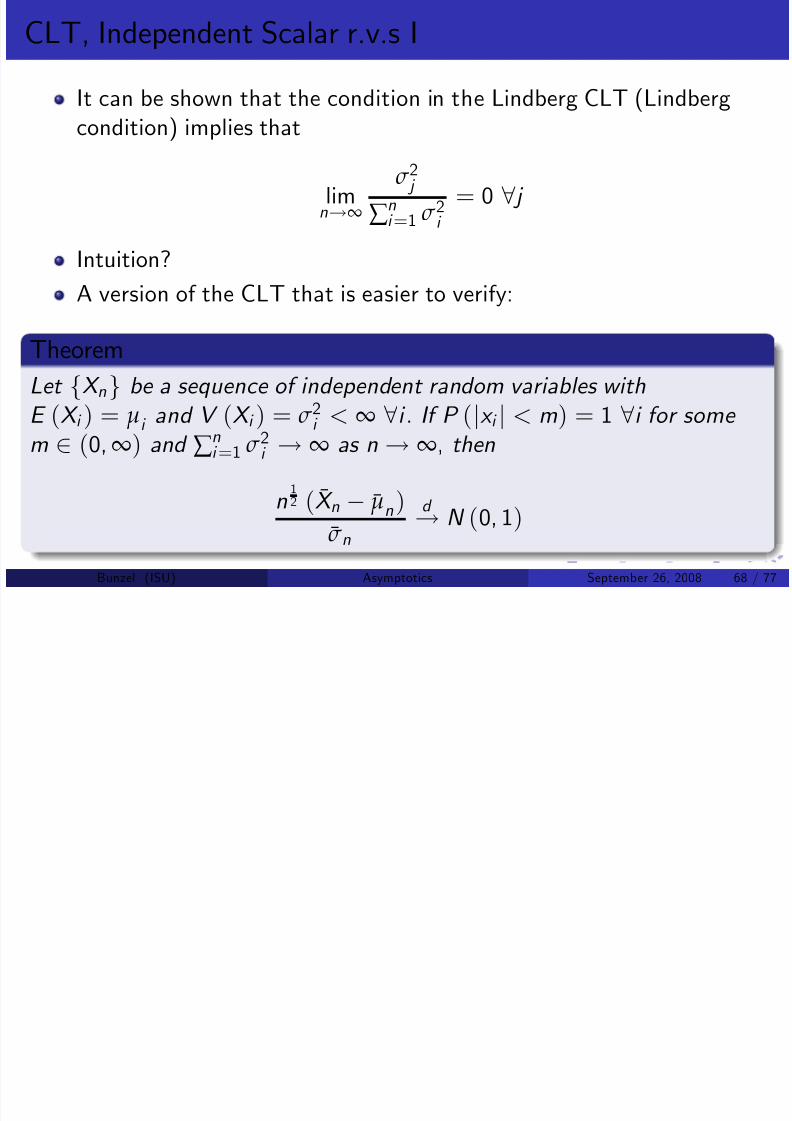

It can be shown that the condition in the Lindberg CLT (Lindberg

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 68/77

It can be shown that the condition in the Lindberg CLT (Lindbergcondition) implies that

limn!∞

σ 2 j

∑ ni =1 σ

2i

= 0 8 j

Intuition?

A version of the CLT that is easier to verify:

Theorem

Let fX ng be a sequence of independ ent random variables withE (X i ) = µi and V (X i ) = σ 2i < ∞

8i . If P (

jx i

j< m) = 1

8i for some

m 2 (0,∞) and ∑ ni =1 σ 2i ! ∞ as n ! ∞, then

n12 ( X n µn )

σ n

d ! N (0, 1)

Bunzel (ISU) Asymptotics September 26, 2008 68 / 77

CLT, Independent Scalar r.v.s, Example I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 69/77

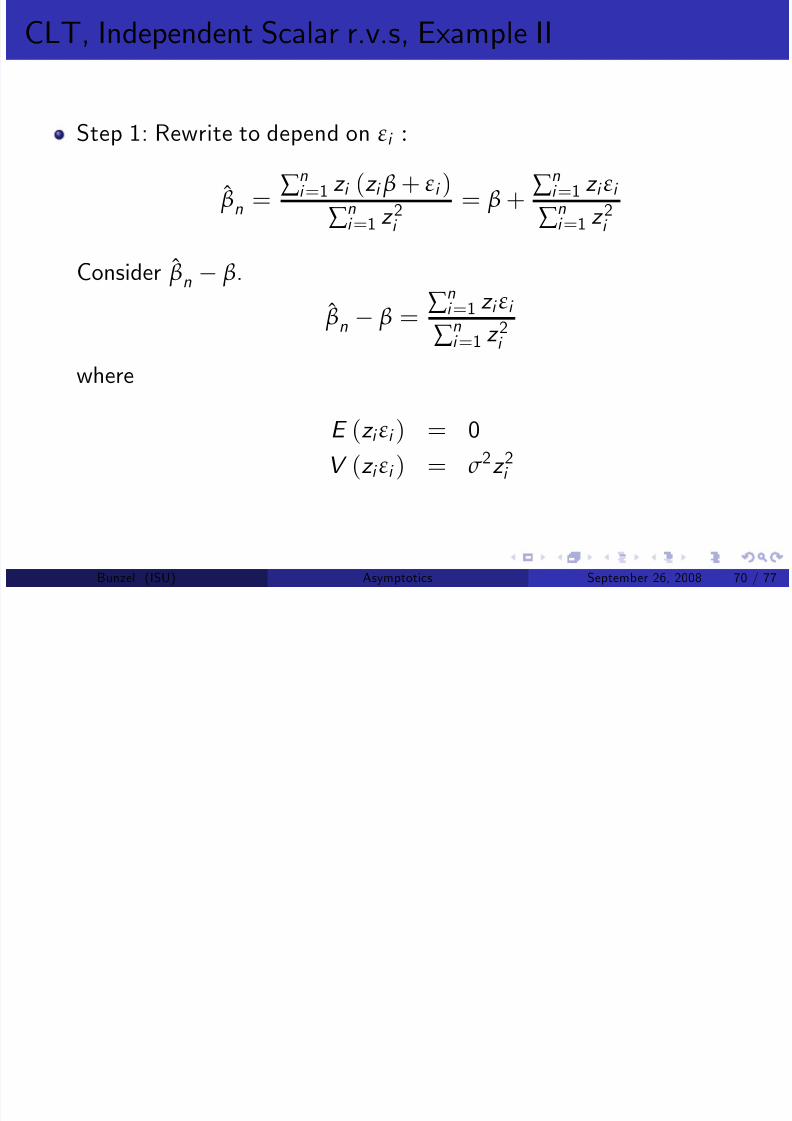

Let the sequence fY ng be de…ned by Y i = z i β + εi , where: β is a real number

z i is the i’th element in the sequence of real numbers fz ng , for which1n ∑

ni =1 z 2i > a > 0 and jz i j < d < ∞, 8i

εi is the i’th element in the sequence iid random variables

fεn

g, for

which E (εi ) = 0 and V (εi ) = σ 2 2 (0,∞) and P (jεi j m) = 1, 8i ,where m 2 (0,∞)

Find an asymptotic distribution of the least squares estimator of βde…ned by

ˆ βn = ∑

n

i =1 z i Y i ∑

ni =1 z 2i

Bunzel (ISU) Asymptotics September 26, 2008 69 / 77

CLT, Independent Scalar r.v.s, Example II

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 70/77

Step 1: Rewrite to depend on εi :

ˆ βn = ∑

ni =1 z i (z i β + εi )

∑ ni =1 z 2i

= β + ∑

ni =1 z i εi

∑ ni =1 z 2i

Consider ˆ βn

β.

ˆ βn β = ∑ ni =1 z i εi

∑ ni =1 z 2i

where

E (z i εi ) = 0V (z i εi ) = σ 2z 2i

Bunzel (ISU) Asymptotics September 26, 2008 70 / 77

CLT, Independent Scalar r.v.s, Example III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 71/77

Is z i εi bounded?

P (jz i εi j < dm) = P (jz i j jεi j < dm) P (jεi j < m) = 1

and dm

2(0,∞) .

Now check the sum of the variances:

n

∑ i =1

V (z i εi ) = σ 2n

∑ i =1

z 2i = nσ 2

1

n

n

∑ i =1

z 2i

!

> anσ 2

! ∞

Bunzel (ISU) Asymptotics September 26, 2008 71 / 77

CLT, Independent Scalar r.v.s, Example IV

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 72/77

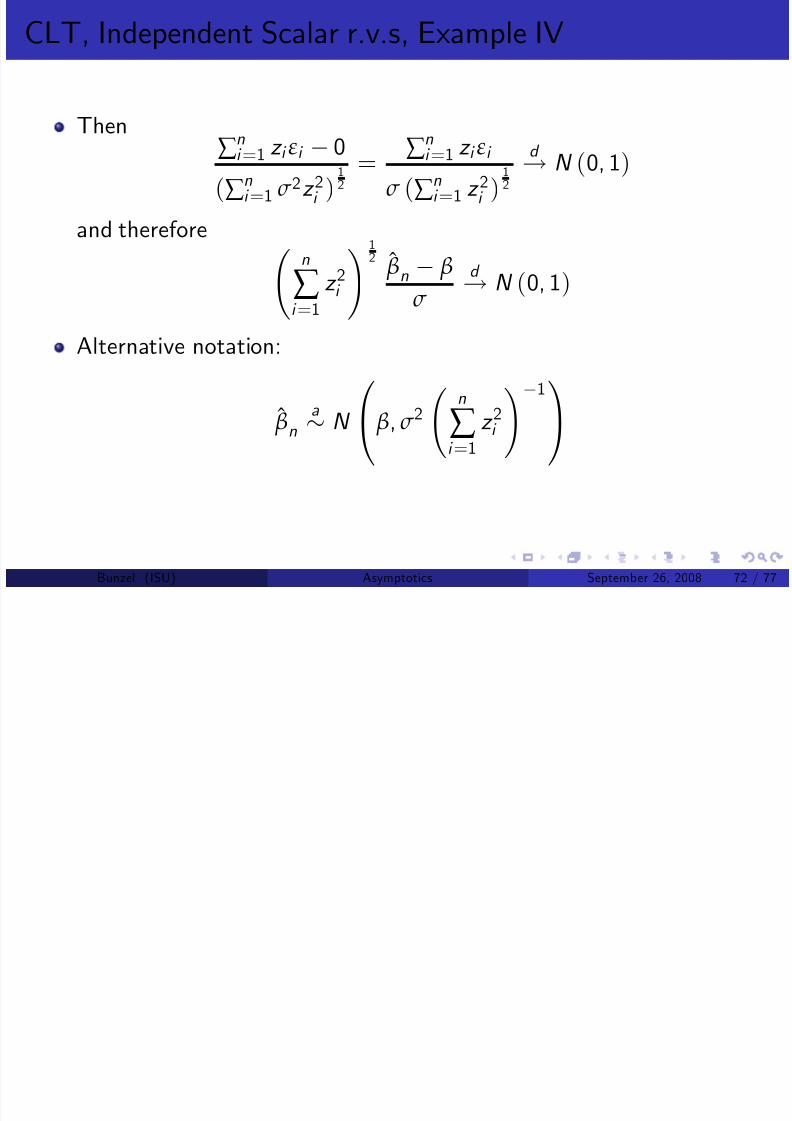

Then∑

n

i =1 z

i ε

i 0

(∑ ni =1 σ 2z 2i )

12

= ∑

n

i =1 z

i ε

i σ (∑ ni =1 z 2i )

12

d

! N (0, 1)

and therefore

n

∑ i =1

z 2

i !

12 ˆ βn β

σ

d

!N (0, 1)

Alternative notation:

ˆ βn

a

N 0@ β, σ 2 n

∑ i =1

z 2

i !

1

1A

Bunzel (ISU) Asymptotics September 26, 2008 72 / 77

Multivariate CLT I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 73/77

Theorem

(Multivariate Lindberg-Levy CLT) Let fX ng be a sequence of iid randomvariables with E (X i ) = µ and Cov (X i ) = Σ 8i , where Σ is a k k

positive de…nite matrix. Then

n12

1

n

n

∑ i =1

X i µ

! d ! N (0,Σ)

Bunzel (ISU) Asymptotics September 26, 2008 73 / 77

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 74/77

Multivariate CLT, Example II

Then

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 75/77

E (X i ) = p 1

p 2

Cov (X i ) =

p 1 (1 p 1) 0

0 p 2 (1 p 2)

Also let X n = 1n ∑ ni =1

X 1i X 2i

.

Then, by the multivariate LLCLT

n12 X n

p 1

p 2 d

!N 0, p 1 (1

p 1) 0

0 p 2 (1 p 2)

Suppose we’re interested in the di¤erence in failure rates.

That is X 1i X 2i or cX i , where c = [1, 1]

Bunzel (ISU) Asymptotics September 26, 2008 75 / 77

Multivariate CLT, Example III

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 76/77

Then

cn12

X n

p 1p 2

= n

12

c X n c

p 1p 2

= n12 (( X 1n X 2n ) (p 1 p 2))

d ! N

0, c

p 1 (1 p 1) 00 p 2 (1 p 2)

c 0

= N (0, p 1 (1 p 1) + p 2 (1 p 2))

Note the variance is what we’d expect when we’re subtracting two

independent variables.

Bunzel (ISU) Asymptotics September 26, 2008 76 / 77

Multivariate CLT I

8/10/2019 Detailed Notes on Asymptotics

http://slidepdf.com/reader/full/detailed-notes-on-asymptotics 77/77

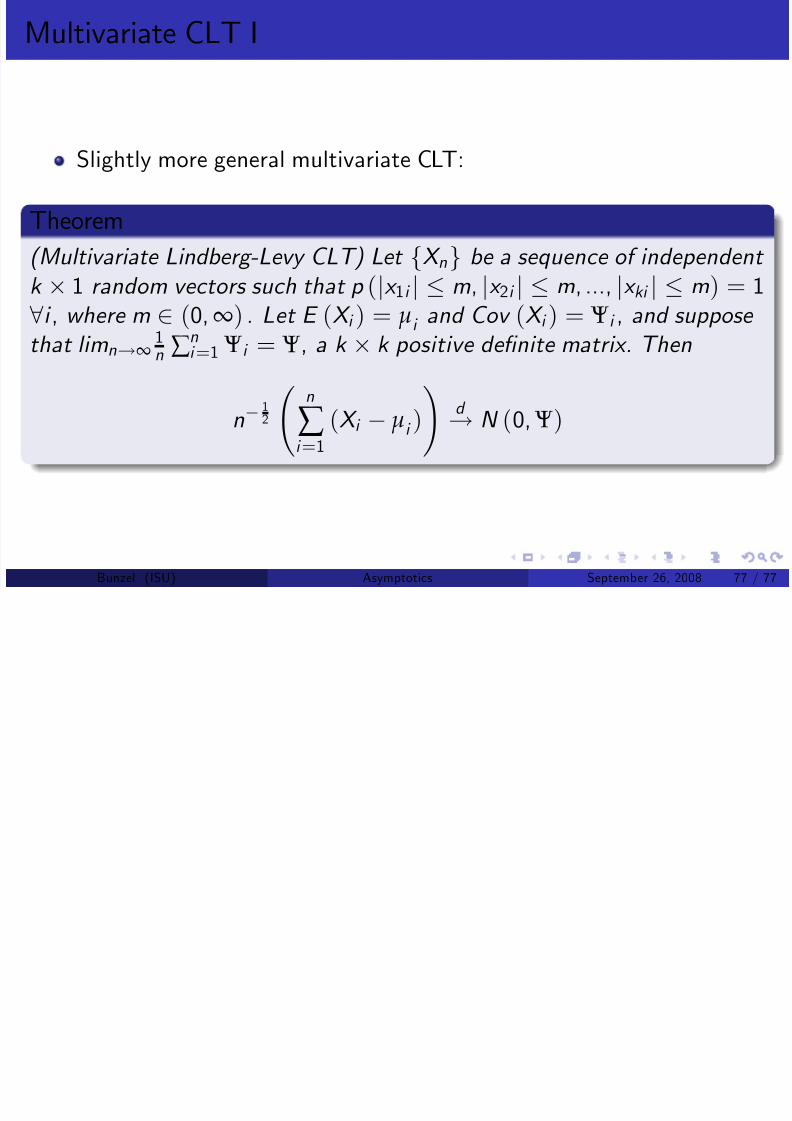

Slightly more general multivariate CLT:

Theorem

(Multivariate Lindberg-Levy CLT) Let fX ng be a sequence of independent k

1 random vectors such that p (

jx

1i j m,

jx

2i j m, ...,

jx

ki j m) = 1

8i , where m 2 (0,∞) . Let E (X i ) = µi and Cov (X i ) = Ψi , and suppose that limn!∞

1n ∑

ni =1 Ψi = Ψ, a k k positive de …nite matrix. Then

n 12

n

∑ i =1

(X i

µi )! d

!N (0, Ψ)

Bunzel (ISU) Asymptotics September 26, 2008 77 / 77