Embed Size (px)

Citation preview

DEA Deutsche Erdoel AG

Group Management Report

and

Consolidated Financial Statements

Fiscal Year

1 January - 31 December 2016

Management Report of the DEA Group

as at 31 December 2016

1. Group structure and business

The DEA Group (DEA) is an international independent oil and gas company with full lifecycle capabilities

across exploration, development and production. Our primary mission is the secure, environmentally-

conscious and sustainable production of crude oil, natural gas and natural gas liquids. Our core produc-

tion and development assets are located in Germany, Norway, Denmark, Egypt and Algeria. Addition-

ally, we own large-scale underground natural gas storage facilities in Germany for storage of third-party

gas.

DEA is both operator and an active but non-operating partner in international joint ventures. We cover

the entire value chain from exploration to development and production of hydrocarbons. In addition to

its operations, DEA Deutsche Erdoel AG oversees the control and financing of activities of its subsidi-

aries. For purposes of internal management control within the DEA Group, production, EBITDAX and

liquidity are the key metrics used. Reporting to the shareholder is carried out by the following regions:

Germany/Denmark, Norway, North Africa (comprising Egypt and Algeria) and Other.

DEA Deutsche Erdoel AG (DEA AG), headquartered in Hamburg, is the parent company of the DEA

Group, comprising a total of 23 enterprises. DEA Deutsche Erdoel AG is a wholly owned subsidiary of

L1E Acquisitions GmbH, Hamburg which, via L1 Energy Capital Holdings S.A., Luxembourg, is a wholly

owned subsidiary of LetterOne Holdings S.A., Luxembourg. A domination and profit and loss transfer

agreement is in place between DEA Deutsche Erdoel AG and L1E Acquisitions GmbH.

Following a resolution adopted at the Annual General Meeting of 17 April 2015 and the entry in the

Commercial Register on 22 April 2015, DEA Deutsche Erdoel AG declared a short fiscal year for the

period from 1 April 2015 – 31 December 2015. Owing to the short fiscal year of the parent company,

financial statements were also prepared for the DEA Group for that short fiscal year. After 31 December

2015, the financial year once again corresponds to the calendar year. Since the current fiscal year com-

prises a 12-month period, a comparison with the 9-month period for the prior year is of limited value.

This report therefore focuses on the year-on-year comparison. The pro-forma figures for the consoli-

dated income statement as well as for the consolidated cash flow statement for the calendar year 2015

comprise the two short fiscal years 2015.

DEA Group will prepare consolidated financial statements as well as a group management report as at

31 December 2016 and will arrange for these to be disclosed in the German Government Gazette (Bun-

desanzeiger).

- 2 -

2. Strategy

Grow production and execute key projects

By focusing on proactive portfolio optimisation and utilising our strengths, we plan to continue to

strengthen and expand our presence in our core operating geographies, in particular in Northwestern

Europe. Our vision is to grow our daily production by safely and efficiently optimising the performance

of existing assets, successfully completing development projects, engaging in near-field exploration pro-

grams and undertaking strategic acquisitions in our core operating regions.

We have a diverse portfolio of producing Northwestern European assets located in OECD member

countries that are supported by established fiscal and regulatory regimes. We believe our position in

Northwestern Europe is underpinned by a long-standing business history in Germany and Norway. We

are committed to maintaining and strengthening our position in this region. We believe that our focus on

Northwestern Europe reduces our exposure to certain operational and geopolitical risks. Additionally,

we believe that focusing on this region enables us to benefit from significant synergies. We aim to further

expand our activities in this region through optimisation of production, future developments and near-

field exploration activities supplemented by strategic asset acquisitions. At the same time, we plan to

grow our production in North Africa through the completion of our West Nile Delta and Reggane Nord

development projects in Egypt and Algeria, respectively.

Increase value through balanced organic and inorganic growth

Regular portfolio management and enhancement are integral aspects of our exploration, development

and production strategy, through which we seek to realise value at an appropriate point in the lifecycle

of an asset. We continuously review macroeconomic, technical and competitive data with respect to our

exploration portfolio. Exploration is important to our operations and supports our plan to increase future

production. However, to complement our organic growth strategy, we also consider selective strategic

acquisitions of companies and/or interests in licences in our core and non-core operating regions as

well as other regions. As a result, we continue to monitor new opportunities for exploration and produc-

tion internationally.

Focus on costs and capital efficiency

We aim to maintain a conservative financial profile and strong balance sheet with ample liquidity. We

expect to fund exploration and development activities from a combination of cash flows from operating

activities, proceeds from debt issuances, and potentially through the proceeds of any portfolio manage-

ment activities, such as farm-downs or sales. Our financial policy is to target net debt / EBITDAX of

2.0 – 2.5x at the mid-point of the cycle. We intend to maintain a conservative approach to acquisitions;

potential future acquisitions need to satisfy this policy.

- 3 -

We also seek to monetise certain assets through divestments or farm-downs. This enables us to mon-

etise value early in the lifecycle of an asset and de-risk our interests by reducing our exposure to an

asset and associated development and other expenditures.

Continue to deliver high Quality, Health, Safety and Environment (QHSE) standards and sustainability

of operations

We are committed to sustainable business development. We continue to focus on maintaining high

safety and operational standards, which we believe are a prerequisite to doing business in our markets.

We are focused on continuing to strengthen our customer relationships, and aim to become the partner

of choice based on our technical and commercial excellence, environmental consciousness and sus-

tainable business development.

- 4 -

3. Economic fundamentals and climate

Economic environment

According to current forecasts of the International Monetary Fund, global economic output in 2016 in-

creased by approx. 3.1 % and will be slightly below the previous year’s figure of approx. 3.2 %. This is

essentially due to unexpected political and economic events such as “Brexit” as well as lower economic

growth in the threshold and emerging market countries. For the euro area, Gross Domestic Product is

currently expected to rise by 1.7 %, compared to 2.0 % in 2015.

Crude oil prices

After approximately four years of averaging around USD 100 per barrel, crude oil prices have fallen

significantly since 2014, reflecting strong production growth in the United States, increases in global

supply elsewhere and weaker global demand. The price decline continued in early 2016 due to ongoing

expectations of a market surplus, but subsequently recovered due to forecasts of growing oil demand

and production outages in Canada, Nigeria and Libya. Prices increased further after OPEC and some

non-OPEC countries like Russia agreed to cut oil production. At the beginning of December, prices

increased to more than 50 USD per barrel after the final OPEC decision to reduce its oil production by

1.3 million barrels per day, effective as of January 2017. This decision marked the first reduction in oil

production since 2008. Later in December, several non-OPEC countries (like Russia) agreed to a further

output cut of about 0.55 million barrels per day.

Our oil sales are primarily priced against the Brent crude oil benchmark. The average crude oil quoted

price for “Brent dated” decreased by 16 % from USD 54 per barrel for the calendar year ended 2015 to

USD 45 per barrel for the year ended December 31, 2016.

USD/barrel Jan. - Dec.

2016 Jan. - Dec.

2015

Average Brent price for the period1 45.13 53.60

1 Source: Bloomberg

- 5 -

Gas prices

On the back of falling crude oil prices, the traded UK NBP gas price has also come down from its level

over the past few years of around 25 EUR/MWh to just below 15 EUR/MWh. Most of that decline hap-

pened over the course of 2015, reflecting a certain time lag in the indexation of gas prices to oil product

prices in European long-term import contracts. However, gas prices have seen a recovery in the second

half of 2016, reaching almost 20 EUR/MWh towards year end. Some of the reasons for this rally include

a price recovery in the coal market following coal market consolidation, and an unplanned shutdown of

French nuclear power generation.

Our gas sales are based on UK NBP and TTF in the Netherlands. Average UK NBP prices decreased

by 28 % to 4.69 USD/mscf in 2016 compared to 6.49 USD/mscf in 2015. The Dutch TTF index, which

is the basis for the majority of our German gas sales, has fluctuated similarly to the UK NBP. Average

TTF gas prices decreased by 26 % to 4.76 USD/mscf for 2016, compared to 6.41 USD/mscf in 2015.

USD/mscf Jan. - Dec.

2016 Jan. - Dec.

2015

Average UK NBP price for the period 4.69 6.49

Average TTF price for the period 4.76 6.41

Foreign currency translation

The EUR/USD exchange rate decreased slightly at the beginning of the year 2016 and increased to-

wards the end of the year. On an annual average, it was unchanged at USD 1.11/€. At the end of 2016,

it was trading at USD 1.05/€ (31 December 2015: USD 1.09/EUR).

The Egyptian Pound fell substantially in value over the course of 2016 compared to the US dollar. In

March 2016 Egypt’s Central Bank devalued the Egyptian Pound by almost 13% to around 8.8 Egyptian

Pounds per USD. In November 2016, the Egyptian Pound was officially floated, with the intention of

helping to strengthen the country’s economy. As a consequence, the Egyptian Pound fell further in value

from 8.8 Pounds per USD to 18.2 Pounds per USD at the end of 2016.

- 6 -

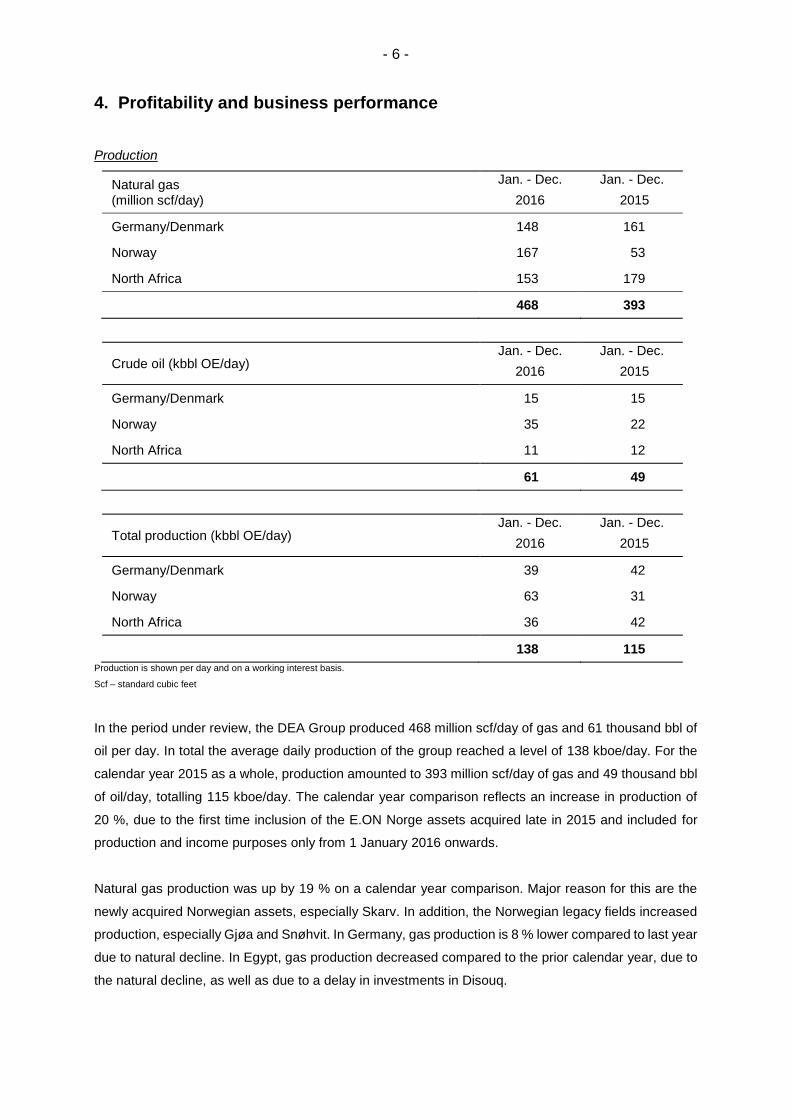

4. Profitability and business performance

Production

Natural gas (million scf/day)

Jan. - Dec.

2016

Jan. - Dec.

2015

Germany/Denmark 148 161

Norway 167 53

North Africa 153 179

468 393

Crude oil (kbbl OE/day) Jan. - Dec.

2016

Jan. - Dec.

2015

Germany/Denmark 15 15

Norway 35 22

North Africa 11 12

61 49

Total production (kbbl OE/day) Jan. - Dec.

2016

Jan. - Dec.

2015

Germany/Denmark 39 42

Norway 63 31

North Africa 36 42

138 115

Production is shown per day and on a working interest basis.

Scf – standard cubic feet

In the period under review, the DEA Group produced 468 million scf/day of gas and 61 thousand bbl of

oil per day. In total the average daily production of the group reached a level of 138 kboe/day. For the

calendar year 2015 as a whole, production amounted to 393 million scf/day of gas and 49 thousand bbl

of oil/day, totalling 115 kboe/day. The calendar year comparison reflects an increase in production of

20 %, due to the first time inclusion of the E.ON Norge assets acquired late in 2015 and included for

production and income purposes only from 1 January 2016 onwards.

Natural gas production was up by 19 % on a calendar year comparison. Major reason for this are the

newly acquired Norwegian assets, especially Skarv. In addition, the Norwegian legacy fields increased

production, especially Gjøa and Snøhvit. In Germany, gas production is 8 % lower compared to last year

due to natural decline. In Egypt, gas production decreased compared to the prior calendar year, due to

the natural decline, as well as due to a delay in investments in Disouq.

- 7 -

In crude oil production, we recorded a 24 % increase in 2016 in relation to the calendar year 2015 due

to the addition of the newly acquired Norwegian assets as well as higher oil production in Denmark due

to improved uptime of the facilities and an additional well. In Germany we could compensate the natural

decline and maintain a stable production due to the continuous drilling mode. Oil production in the Gulf

of Suez in Egypt is down owing to the natural production decline.

Results of operations

Consolidated income Statement of the DEA Group

€ m Jan. - Dec.

2016 Apr. - Dec.

2015 Jan. - Dec.

2015

Sales and other operating revenues 1,483 1,115 1,449

Cost of sales -1,101 -673 -847

Gross profit 382 442 602

Exploration costs -119 -119 -206

General and administration expenses -149 -123 -171

Net impairment of assets -70 -229 -538

Operating Result 44 -29 -313

Financial income 129 64 120

Financial expenses -224 -161 -213

Result from continuing operations be-fore taxes

-51 -126 -406

Income taxes 18 -27 -10

Result from continuing operations -33 -153 -416

Result from discontinued operations -3 -241 -235

Net result -36 -394 -651

In order to present the income statement of an international E&P company in a more appropriate way

and to increase the comparability with other companies in the industry, the presentation of the income

statement has been changed from the total cost to the cost of sales method. The prior year figures have

been adjusted accordingly.

- 8 -

Jan. - Dec.

2016 Jan. - Dec.

2015

Average realised oil price including oil hedge result (in USD/bbl)

42.20 60.27

Average realised oil price excluding oil hedge result (in USD/bbl)

39.79 48.44

Germany/Denmark 38.60 46.04

Norway 41.16 50.82

North Africa 34.17 46.08

Average realised gas price (in USD/mscf) 4.96 5.80

Germany/Denmark 5.25 6.50

Norway 5.89 5.80

North Africa 2.67 2.80

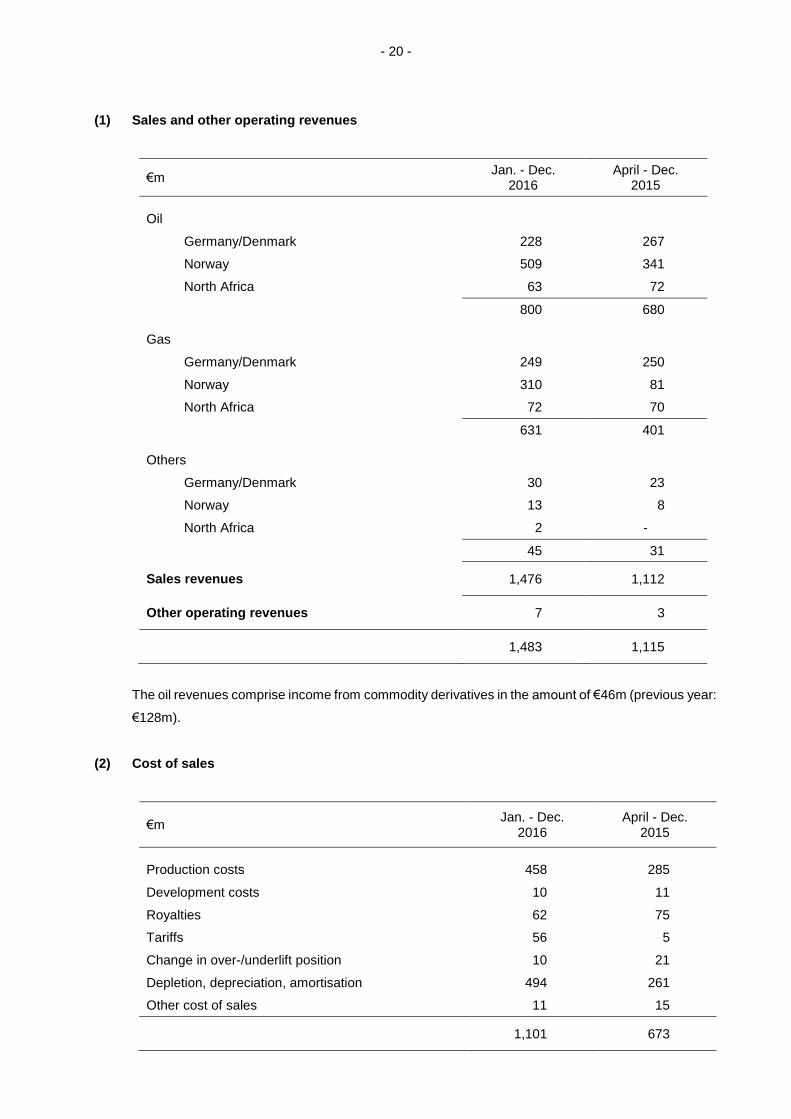

Sales and other operating revenues increased by € 34 million or 2 %, to € 1,483 million for 2016

compared to € 1,449 million for the calendar year 2015, primarily driven by higher sales volumes. This

was partially offset by the steep decline in commodity prices.

Oil sales decreased by € 55 million, or 6 %, to € 800 million for 2016 compared to € 855 million for the

whole year 2015, as 30% higher sales volumes were offset by an 18 % decline in oil prices. In addition,

we had lower results from oil commodity hedges in Germany and Norway, resulting in a negative effect

of € 124 million.

Gas sales increased by € 102 million (+19 %) to € 631 million for 2016 compared to € 529 million for

the calendar year 2015, as 25 % higher sales volumes were partly offset by a 15 % decline in prices.

In the period under review oil sales resulted in 54 % of total revenue (calendar year 2015: 60 %),

whereas gas sales contributed 43 % (calendar year 2015: 37 %).

Cost of sales increased year-on-year by € 254 million or 30 %, to € 1,101 million for 2016 compared to

€ 847 million for the calendar year 2015. Despite the decline in specific production costs in the context

of the expenditures reduction programs, the absolute production costs increased in parallel to the higher

production quantities. Same applies for scheduled depletion/depreciation/amortisation which increased

in line with the higher production. In addition, we incurred higher costs for tariffs and transportation in

Norway. This was partially offset by price-related reduced production royalties.

- 9 -

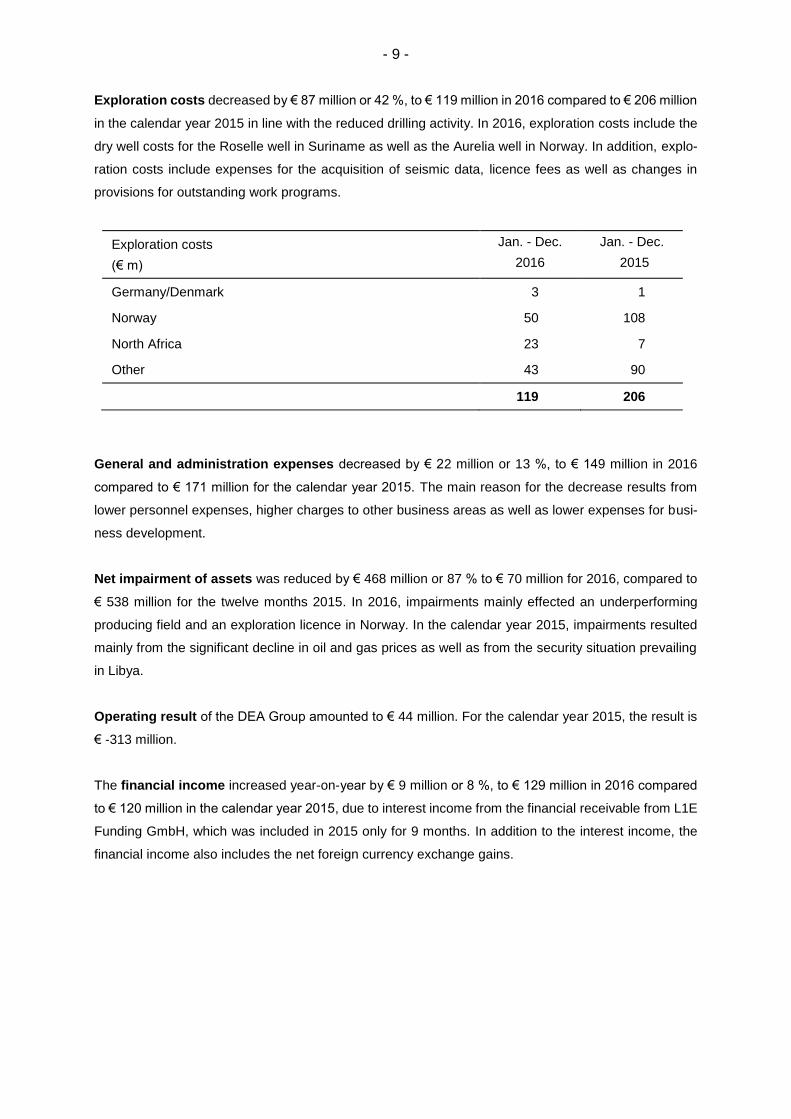

Exploration costs decreased by € 87 million or 42 %, to € 119 million in 2016 compared to € 206 million

in the calendar year 2015 in line with the reduced drilling activity. In 2016, exploration costs include the

dry well costs for the Roselle well in Suriname as well as the Aurelia well in Norway. In addition, explo-

ration costs include expenses for the acquisition of seismic data, licence fees as well as changes in

provisions for outstanding work programs.

Exploration costs

(€ m)

Jan. - Dec.

2016

Jan. - Dec.

2015

Germany/Denmark 3 1

Norway 50 108

North Africa 23 7

Other 43 90

119 206

General and administration expenses decreased by € 22 million or 13 %, to € 149 million in 2016

compared to € 171 million for the calendar year 2015. The main reason for the decrease results from

lower personnel expenses, higher charges to other business areas as well as lower expenses for busi-

ness development.

Net impairment of assets was reduced by € 468 million or 87 % to € 70 million for 2016, compared to

€ 538 million for the twelve months 2015. In 2016, impairments mainly effected an underperforming

producing field and an exploration licence in Norway. In the calendar year 2015, impairments resulted

mainly from the significant decline in oil and gas prices as well as from the security situation prevailing

in Libya.

Operating result of the DEA Group amounted to € 44 million. For the calendar year 2015, the result is

€ -313 million.

The financial income increased year-on-year by € 9 million or 8 %, to € 129 million in 2016 compared

to € 120 million in the calendar year 2015, due to interest income from the financial receivable from L1E

Funding GmbH, which was included in 2015 only for 9 months. In addition to the interest income, the

financial income also includes the net foreign currency exchange gains.

- 10 -

The financial expenses increased € 11 million (+5 %) to € 224 million in 2016 compared to € 213 million

in the calendar year 2015. Interest expenses for the RBL facility as well as for the shareholder loans

increased, since they were included in the prior calendar year only for 9 and 10 months, respectively. In

addition, interest expenses increased in line with a higher LIBOR. In addition to the interest expenses,

the financial expenses also include the net losses from financial derivatives as well as for the calendar

year 2015 the net foreign currency exchange losses.

Result from continuing operations before taxes amounted to € -51 million in 2016, and to € -406

million for the full calendar year 2015. In the reporting period, DEA had in a total tax income of € 18

million. Current income tax expense, resulting from the fact that various expenses are not tax deductible,

was compensated by deferred tax income, due to temporary differences mainly in Norway. In 2016, tax

rate was 35 %.

Result from continuing operations amounted to € -33 million.

Result from discontinued operations for 2016 comprises adjustments in regard to the sale of our

British activities. In 2015, it included the complete result of the British activities sold. In addition to the

operating result, this also comprised necessary impairments due to the sales price, the costs of the sale

as well as deconsolidation effects.

Net result came to € -36 million, considerably better than the value for the calendar year 2015.

All in all, the DEA Group is in an environment of continuously low oil and gas prices, which imposed a

substantial burden on results despite rising production volumes in the reporting period.

EBITDAX

EBITDAX is the factor used for internal management control purposes within the DEA Group. As a key

ratio of the income statement it is determined as earnings before interest, taxes, depletion/deprecia-

tion/amortisation and exploration expenditure for the last 12 months; in addition, adjustments are made

for realised and unrealised gains/losses arising from derivatives and exchange rate fluctuations as well

as non-recurring effects.

In 2016, EBITDAX amounted to € 776 million, down by € 52 million compared to the calendar year 2015.

Revenues increased only slightly due the offsetting effects of higher sales volumes and significantly

lower commodity prices. Despite the decline in specific production costs in the context of the expendi-

tures reduction programs, the absolute production costs increased in parallel to the higher production

quantities. In addition, we incurred higher costs for tariffs and transportation in Norway. This was partially

offset by price-related reduced production royalties.

- 11 -

5. Net asset position

Balance sheet of the DEA Group

Assets (€ m) 31-12-2016 31-12-2015

Intangible assets/ property, plant and equip-ment/ investment property

3,097 3,039

Financial receivables/financial investments 2,210 2,166

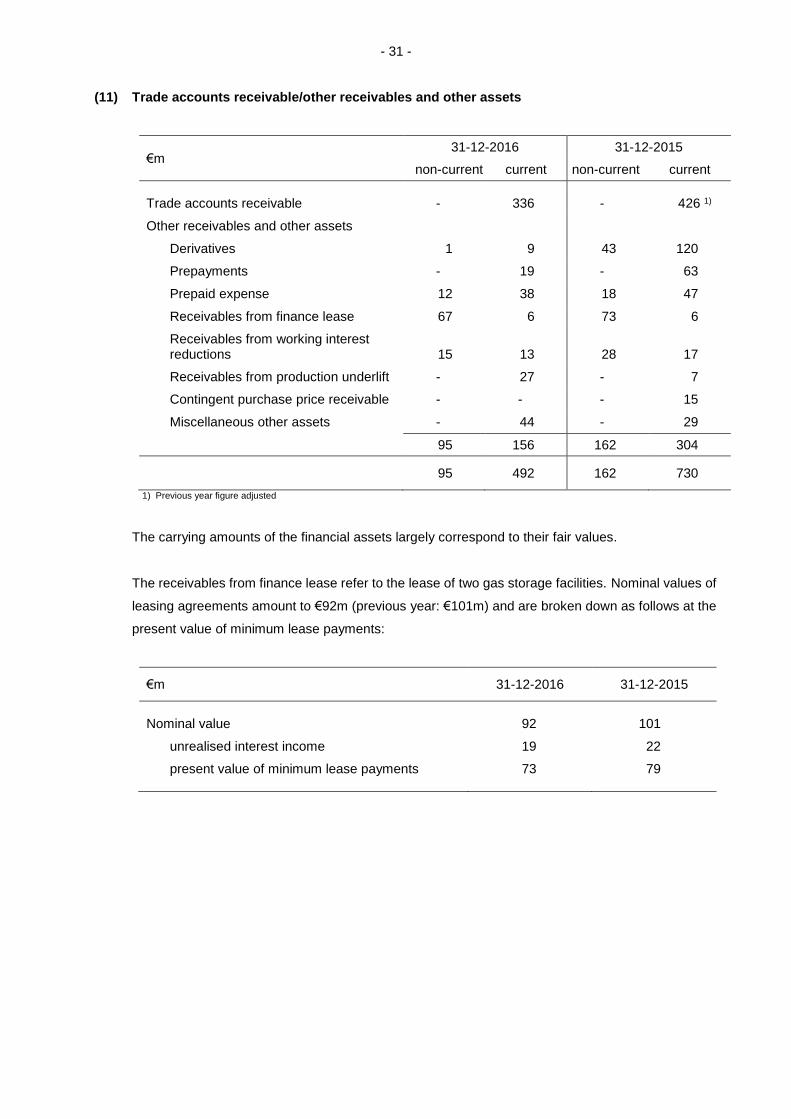

Other receivables and other assets 95 162

Deferred tax assets 85 74

Non-current assets 5,487 5,441

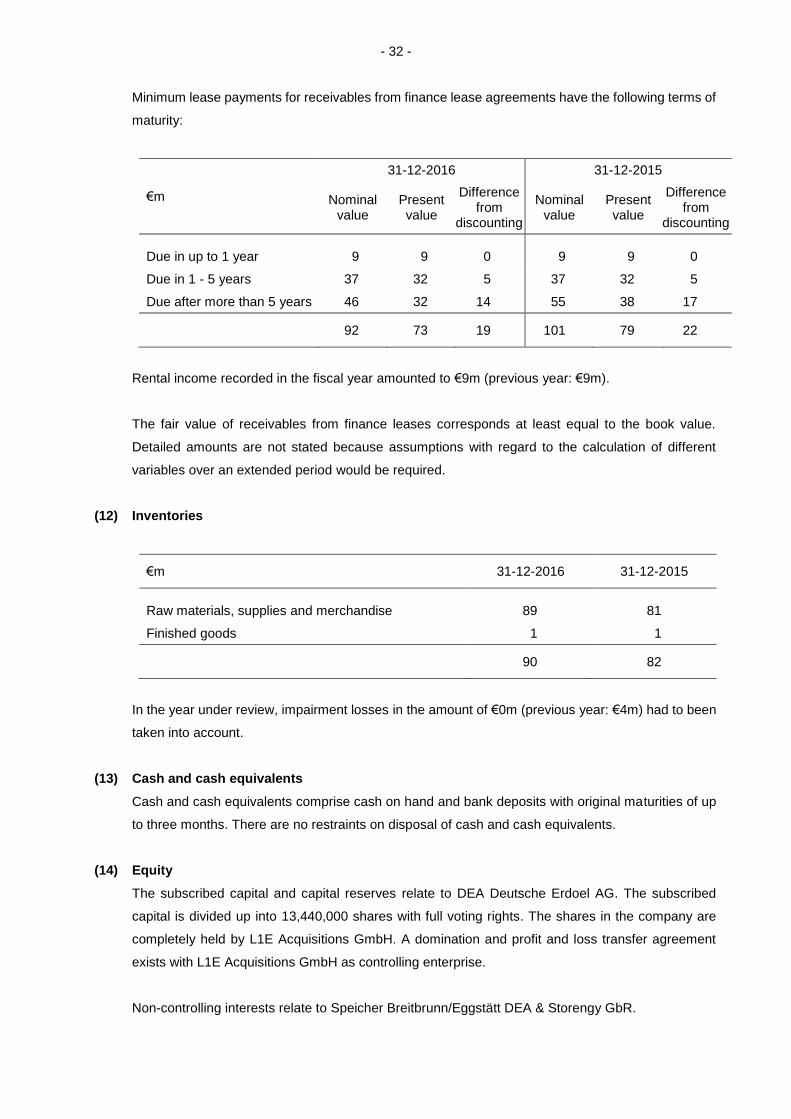

Inventories 90 82

Financial receivables1 - 340

Trade accounts receivable1 336 426

Other accounts receivables, other assets and income tax assets

157 316

Cash and cash equivalents 101 320

Current assets 684 1,484

Assets 6,171 6,925

1 As from the reporting period profit and loss transfers are recognised under financial receivables or financial liabilities, respectively. The previous year's disclosure as trade accounts receivable (€340m) has been adjusted accordingly.

- 12 -

Equity and liabilities (€ m) 31-12-2016 31-12-2015

Equity 1,904 1,958

Provisions 616 665

Debt to banks 1,494 2,021

Financial debt 1,018 779

Other liabilities/income tax liabilities 40 34

Deferred tax liabilities 431 512

Non-current liabilities 3,599 4,011

Provisions 209 242

Debt to banks 3 5

Financial debt 16 283

Trade accounts payable 308 306

Other liabilities/income tax liabilities 132 120

Current liabilities 668 956

Equity and liabilities 6,171 6,925

Liquidity

As of December 31, 2016, our cash and cash equivalents amounted to € 101 million. Our principal

sources of liquidity are operating cash flows from our producing assets, debt financing through drawings

under the RBL, other external borrowings via related parties and shareholder loans. Our liquidity is used

to cover working capital, capital expenditures, debt service requirements and other liquidity requirements

that may arise from time to time, including repayments of outstanding debt, acquisitions and other in-

vestment opportunities, funding exploration and development projects and other payments in the ordi-

nary course of business. A firm liquidity risk management program is in place to ensure that the DEA

Group is in a position to meet its payment obligations at all times.

Both, internal credit lines made available by the shareholder and external credit facilities by banks are

not fully drawn. Additional immediately available liquidity under credit lines with third parties amounts to

775 million USD.

- 13 -

Effective as of 2 April 2015, DEA Deutsche Erdoel AG and various subsidiaries became parties to an

existing loan agreement for up to USD 2.3 billion between L1E Funding GmbH and a syndicate of banks

(reserve-based lending or RBL facility). Under this loan agreement, DEA has the option to borrow addi-

tional external resources for Group funding purposes as long as the credit facility is collateralised by

productive assets.

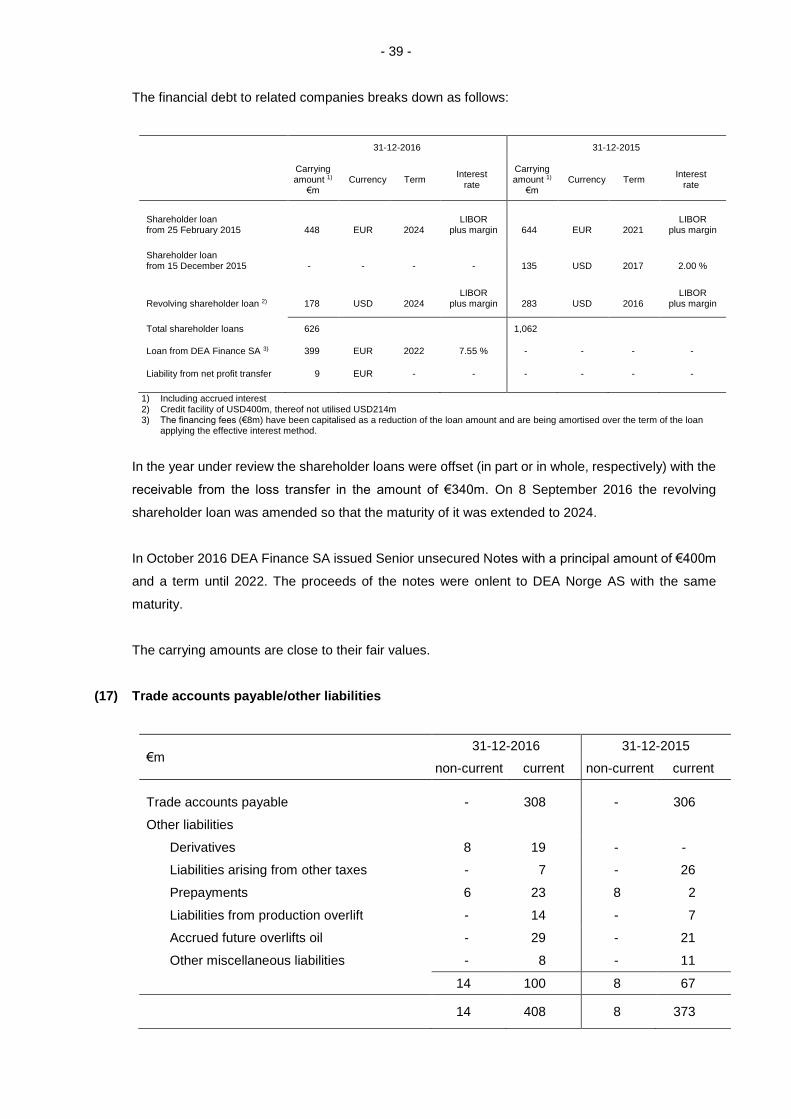

In October 2016 DEA Finance SA, a related party to DEA Deutsche Erdoel AG, issued Senior unsecured

Notes with a principal amount of € 400 million and a term until 2022. DEA AG and its major subsidiaries

became guarantors of the notes. The proceeds of the notes were onlent to DEA Norge AS with the same

maturity.

Additionally, DEA has a USD 50 million working capital facility for intra-month cash management pur-

poses that remains undrawn.

Development of net assets

Non-current assets amount to 89 % of total assets, and stand at € 5,487 million, up by € 46 million in

relation to 31 December 2015. The significant capital expenditures were partially offset by depletion/de-

preciation/amortisation, impairments and asset disposals. The non-current financial receivables slightly

increased and comprise mainly the financial receivable to L1E Funding GmbH in correspondence for

the assumption of the RBL facility in 2015. The decrease in the other non-current receivables and assets

mainly relates to lower assets from commodity derivatives.

Current assets decreased significantly compared to 31 December 2015. This is mainly due to the

settlement of financial receivables under the domination and profit & loss transfer agreement (DPLTA),

which were off-set against financial liabilities owed to the direct shareholder L1E Acquisitions GmbH. In

addition, trade accounts receivables decreased compared to the end of last year due to lower prices. In

the other receivables and assets, the derivatives decreased due to scheduled maturity of hedging trans-

actions and revaluation effects. The level of cash holdings decreased compared to last year due to

voluntary partial repayments under the RBL.

The equity capital ratio of the DEA Group amounted to 31 % as at the balance sheet date (previous

year: 28 %). As at 31 December 2016, equity amounted to € 1,904 million.

A substantial proportion of non-current provisions and liabilities, at € 3,599 million, is accounted for

by debt to banks, comprising the RBL credit facility. To optimise the interest costs and increase financial

flexibility, we reduced the drawn amount under the facility in the course of 2016. Other non-current

financial debt increased year-on-year, mainly due to the proceeds loan from DEA Finance SA to DEA

Norge AS. This was partially compensated by an overall decrease in shareholder loans between DEA

AG and L1E Acquisitions GmbH due to the offsetting with receivables under the DPLTA despite the

effect of the reclassification from current to non-current liabilities after the amendment of the maturity of

- 14 -

the shareholder loans. In addition, € 616 million is accounted for by pension provisions and decommis-

sioning provisions, as well as other provisions. On the whole, the extent of provisions decreased, espe-

cially for decommissioning, owing to the higher interest rate year-on-year. On the contrary, pension

provisions increased due the decrease of the applicable interest rate. The decrease in deferred tax

liabilities is the result of a higher netting with deferred tax assets.

Current provisions and liabilities are down by € 288 million or 30 % year-on-year, essentially due to

the reclassification of shareholder loans. In addition, other provisions slightly decreased year-on-year

due to lower provisions related to personnel and outstanding work programs.

- 15 -

6. Financial position

Jan. - Dec.

2016 Apr. - Dec.

2015 Jan. - Dec.

2015

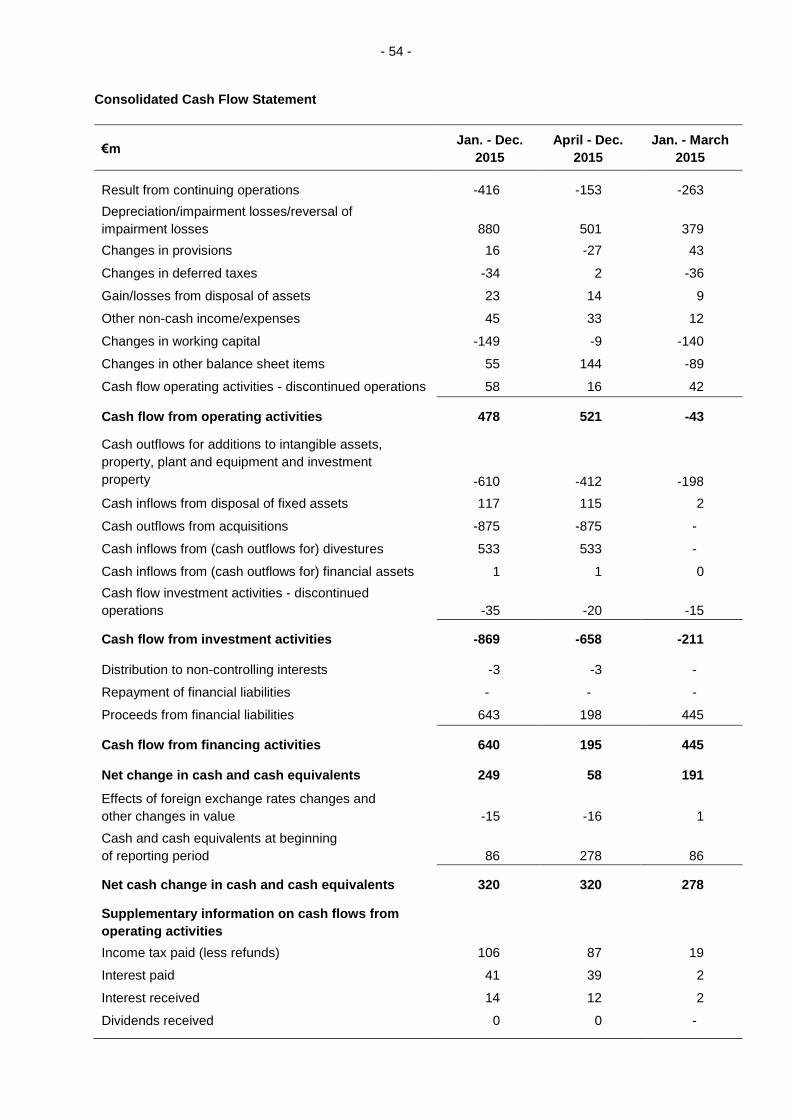

Cash flow operating activities 626 521 478

Cash flow from investment activities -558 -658 -869

Cash flow from financing activities -287 195 640

Cash flow from operating activities

Cash inflow from operating activities increased by € 148 million to € 626 million for 2016 from € 478

million for the calendar year 2015. The increase is mainly driven by the higher results from operations

before depletion/depreciation/amortisation. In addition, the changes in the working capital had a positive

impact on the cash flow from operating activities, mainly driven by lower accounts receivable. Besides

that, the calendar year 2015 was negatively affected by cash settlements of foreign currency hedges

with our previous parent in the course of the sale of DEA.

Cash flow from investment activities

Cash outflow from investment activities amounted to € 558 million for 2016, compared to € 869 million

for the calendar year 2015 (including € 35 million for investment in the discontinued UK assets). The

decrease in cash outflow from investment activities was mainly driven by lower acquisitions, as the

calendar year 2015 included the acquisition of shares in E.ON Norge, as well as due to lower proceeds

from divestments, due the sale of the UK business in 2015. In contrast, we had higher organic invest-

ments.

Investments (€ m)

Jan. - Dec. 2016

Jan. - Dec. 2015

Capital expenditures (net of acquisitions)

Germany/Denmark 53 85

Norway 158 204

North Africa 444 302

Other 1 19

656 610

Acquisitions 0 875

Total 656 1,485

- 16 -

Our expenditures for tangible and intangible assets increased year-on-year by 8 %, due to the capex for

our current development projects in the Egyptian West Nile Delta and Reggane in Algeria. In total, our

capital expenditures (excluding acquisitions) reached € 656 million. In addition to the spendings for the

development projects, key capex investments were made in existing producing fields in Germany and

Norway.

Cash flow from financing activities

Cash flow from financing activities amounted to € -287 million, compared to a cash flow of € +640 million

in the twelve months 2015. Cash flow from financing activities in the reporting period mostly reflects

outflow from the net repayment of the RBL and of shareholder loans, partly compensated by the cash

inflow from the proceeds loan from DEA Finance SA. The cash inflow from financing activities in 2015

resulted from additional shareholder loans in the amount of € 643 million.

- 17 -

7. Employees

The average number of employees of the DEA Group decreased from 1,433 (Ø 1 April – 31 December

2015) by 95, to 1,338 (Ø 1 January – 31 December 2016) full-time equivalents (FTEs). The main driver

for the reduction are the various measures for cost reduction and efficiency improvement on all DEA

sites. The average number of employees at the German companies decreased by approx. 6 %. In Nor-

way the number of employees started to decrease after the merger of the two Norwegian companies by

43 FTE. The number of employees in Egypt on 31 December 2016 declined by 49 FTE. In Libya the

workforce was reduced by about 3 employees, in Turkmenistan by 9 employees.

On 31 December 2016, DEA Deutsche Erdoel AG had 17 apprentices and trainees; as at 31 December

2015 there were 19. As a supplementary strategy, within the scope of a training sponsorship program

DEA supports 7 trainees engaged in small to medium-scale enterprises.

A key factor in achieving success internationally is the quality of staff, both locally and on an international

scale. Despite the restructuring programs, DEA still sends expatriates to other countries and brings also

employees of the foreign companies to work in Hamburg and at other locations. On 31 December 2016,

2 impatriates from other countries worked in Germany, 1 was employed in Turkmenistan, 7 in Norway

and 18 in Egypt. We meanwhile have 149 employees on an international scale that do not have the

nationality of the countries in which they work. This represents a share of over 11 %. This enables us to

achieve a better understanding amongst our employees of foreign cultures in general, and of special

aspects pertaining to the different locations in which we operate.

Effective as of 1 February 2016, DEA Deutsche Erdoel AG and the IG Bergbau, Chemie, Energie (the

German trade union for employees in the mining, chemical and energy industries) had entered into a

new Company Collective Agreement with a minimum term until 31 January 2017. An essential element

of the Collective Agreement was a freeze in collective wages and salaries and in trainee remuneration.

Nevertheless, it was agreed to grant each full time employee an one-off payment of gross € 400.

Through our employer-funded company pension scheme, we make a contribution to our employees’

retirement provision and support them in the event of invalidity or bereavement. Our company pension

scheme provides for a personal pension to be paid to each employee of DEA Deutsche Erdoel AG once

the waiting period has elapsed. The extent of this company pension depends on the years of service

and remuneration paid. In supplementation of the employer-funded pension scheme, our employees

also have the option of providing for retirement themselves by means of a remuneration conversion,

thus additionally securing their standard of living after retirement. At DEA Deutsche Erdoel AG, employ-

ees have a choice of investing components of their gross remuneration in pension insurance funds,

pension funds, direct life insurance and direct commitments. Our employees also benefit from pension

plans in a number of our foreign companies.

- 18 -

Declaration of corporate governance according to § 289a HGB

In accordance with the [German] Act for equal treatment of women and men in leadership positions in

the private sector and the civil service (Gesetz für die gleichberechtigte Teilhabe von Frauen und Män-

nern an Führungspositionen in der Privatwirtschaft und im öffentlichen Dienst) the Supervisory Board of

DEA AG adopted a resolution in 2015 to establish a target quota of 0 % for women on the Company’s

Supervisory Board and also 0 % for women on the Board of Management for the first performance period

defined pursuant to this Act, i.e. up to 30 June 2017. These quotas correspond to the then current quota

of women in the two management bodies.

The Board of Management has defined a target quota of 5 % for the first managerial level below the

Board of Management and a target quota of 16 % for the second managerial level. This corresponds to

the current quota of women at these managerial levels at the time of defining these targets. These

quotas are planned to be met by 30 June 2017.

- 19 -

8. Risk management

Risk management system

Overall responsibility for the group wide risk management system sits with the Board of Management of

DEA Deutsche Erdoel AG. It establishes the rules and minimum standards and determines how much

risk the company is willing to take. Our Risk Committee is in charge of monitoring and refining the risk

management system. It is composed of the full Board of Management of DEA Deutsche Erdoel AG, the

managing directors of the operating subsidiaries and the heads of the following departments of DEA AG

which are accountable for the entire group: Treasury, Controlling, Accounting/Tax, Audit, QHSSE and

Commercial Development & Infrastructure. The Treasury Department bears responsibility for the con-

trol, steering and co-ordination of the risk management system. This department regularly reports on

the Group’s risk situation to both the Risk Committee and the Audit Committee of the Supervisory Board

of DEA Deutsche Erdoel AG.

It is our business policy to make optimum use of opportunities and contain risks at the same time. All

risks and opportunities are monitored and controlled by means of a risk management system in place

throughout the Group. It is supported by a documented risk management system and gives appropriate

consideration to the risk aspect in all decisions and business processes of DEA through ongoing early

identification, standardised recording, assessment, control, and monitoring. We gain an overview of our

opportunities and risks once every three months by performing a bottom-up analysis. The executive and

supervisory bodies are updated on the risk exposure within the scope of the quarterly reporting. The

term “risk” is defined in a way to ensure that the long-term strategic objectives are attained and to pro-

duce an adequate depiction of the entire risk portfolio. The risks and the key figures and ratios for risk

measurement are aligned with the control parameters of the DEA Group. We analyse the material indi-

vidual risks of the Group using a matrix in which the risks’ probability of occurrence and potential net

damage are represented. We can derive from this whether there is need for action and the scope of

such action. Actions in place are as well reported and evaluated in this process as possible future actions

to mitigate the risk. We assess risks based on how they affect our EBITDAX/equity and/or how they

impact our liquidity.

Commodity price risks and opportunities

As an upstream enterprise, we are exposed to the risks but also stand to benefit from the opportunities

arising from the level of oil and gas prices on the international markets. These are constantly analysed,

quantified and reported on a regular basis. As part of our mid-term planning, we also calculated the

sensitivities of commodity price. A change in the oil price by USD -10/bbl would have an influence of

approx. € -124 million on EBITDAX or approx. € -81 million on the free cash flow in 2017. A change in

the gas price by -10 % would result in a change to EBITDAX in 2017 of approx. € -28 million and to

approx. € -19 million to the free cash flow. Rising oil and gas prices lead to opportunities in EBITDAX

and free cash flow for DEA Group, respectively.

- 20 -

The Risk Committee meets regularly to discuss the policies to be applied in the face of all risks, espe-

cially commodity price risks. These essentially consist of risks arising from operations (payments to be

received for future sales revenues from future production) as well as from financing processes. Com-

modity-price swaps and fixed price marketing agreements are in place to hedge price risks. The terms

of such transactions are based on the term of the underlying transaction and are therefore predominantly

short to medium-term. All hedging transactions serve the exclusive purpose of covering the risk from

operational and financial transactions as well as underlying transactions accounted for or expected with

a high degree of probability. Oil and gas prices are to be hedged in order to stabilise our future cash

flows and the RBL borrowing base. The extent of the volumes to be hedged depends on the economic

exposures and the prevailing oil and gas prices. Owing to the current level of oil and gas prices, com-

modity-price swaps were concluded for the calendar years 2017 - 2019. For the calendar year 2017,

approx. 20 % of the oil production exposed to market price risks is hedged by commodity-price swaps.

This is in line with the target defined in our hedge policy and covers 50 % of the economic exposure

after taxes. The oil hedge ratio for 2018 is currently at approx. 15 % and for 2019 at approx. 10 %. Gas

price risks for 2017 are hedged at approx. 28 % by fixed price agreements against gas price fluctuations.

The gas hedge ratio is currently for 2018 at approx. 12 % and for 2019 at approx. 10 %. We continue to

actively hedge our 2018 and 2019 production in line with our hedging policy.

Risks and opportunities from exchange rate fluctuations

As an international active group, we are also exposed to the risks and stand to benefit from the oppor-

tunities arising from movements in exchange rates on the international markets, especially changes in

USD/EUR, USD/NOK and NOK/GBP. These risks are managed in the DEA Group by means of system-

atic risk management procedures and broadly matching currency structure of assets and liabilities, using

short-term currency swaps, amongst other solutions. According to our current mid-term planning, a

change to the USD/€ exchange rate of USD 0.1/€ would lead to a change in EBITDAX of approx.

€ -92 million and approx. € -40 million in the free cash flow. Decreasing exchange rate ratios lead to

opportunities in EBITDAX and free cash flow for DEA Group, respectively.

Specific risks of the E&P industry

As an international active E&P group, our operations are subject to all risks common in our industry (e.g.

blow out, oil spills). To protect our core business against loss and liability to third parties we maintain

insurance that we believe is consistent with customary industry practices in the jurisdictions in which we

do business.

DEA faces also risks that involve above all the possible misinterpretation of geological structures and

the resultant dry wells drilled. We contain such risks through state-of-the-art technology and systematic

quality assurance.

Reserve estimates may undergo positive or negative changes in the course of time and exert an influ-

ence on current depreciation and amortisation as well as the value of the company’s assets. In general,

estimates of economically recoverable oil and gas reserves are based on a number of factors and as-

sumptions made as of the date on which the reserves estimates were determined, such as geological

- 21 -

and engineering estimates, historical production from the properties, the assumed effects on regulation

by governmental agencies and estimates of future commodity prices and operating costs, all of which

may vary considerably from actual results. Our policy regarding internal controls over the recording of

reserves is structured to objectively and accurately estimate our oil and gas reserve quantities and val-

ues in compliance with 2007 SPE/AAPG/WPC/SPEE PRMS. Our Petroleum Reservoir Simulation De-

partment maintains oversight and compliance responsibility for our internal reserve estimate process

and provides appropriate data to our independent reserves auditors for the annual estimation of our

year-end reserves.

The timely execution within the planned cost budget of our large development projects receives high

attention in the Risk Committee to enable possible countermeasures.

Financial risks

The development of oil and gas prices influences the RBL credit facility. If prices fall over a defined

period of time below a certain price deck used by the banks for the latest calculation of the available

facility amount, a recalculation of the facility amount is triggered which could lead to a (partial) short-

term repayment of the drawn facility amount, if not compensated by other measures such as the inclu-

sion of new reserves. In case of potentially necessary partial repayments of the outstanding loan DEA

has other financing opportunities that need to be used.

DEA Group is subject to restrictive debt covenants. In the reporting period, DEA was in compliance with

its obligations under all financing arrangements.

We closely monitor liquidity risk through cash flow forecasts and sensitivity analyses. We manage our

credit risk by assessing the creditworthiness of potential counterparties before entering into transactions

and through ongoing creditworthiness evaluations with respect to ongoing transactions.

Political risks

In the course of its foreign operations, DEA is exposed to the political risks prevailing in the various

countries. Our investments in North Africa are secured by federal German government guarantees. In

addition, our risk management activities also call for us to monitor the security situation in the countries

in which we ourselves or our subsidiaries are engaged very closely. The prevailing security situation in

Libya still prevents any operational activities in that country. We will continue to monitor developments

very closely and will react at short notice and take preventive measures to protect our employees and

their families.

- 22 -

Risk assessment of DEA Group

The assessment of the general situation of the risk environment is the result of a consolidated analysis

of all material individual risks. The focus was primarily on the significant market risks owing to fluctua-

tions in commodity prices. By deferring investment or portfolio optimisation decisions, DEA takes the

appropriate action to cope with the ongoing low level of prices. Furthermore, an organisational cost

reduction study is under way to increase efficiency. From today’s perspective, there are no risks threat-

ening the continued existence of the DEA Group as a going concern.

- 23 -

9. Environmental protection and safety

Quality, health, safety and environmental excellence is imperative to our business. We actively manage

the safety of all personnel working across our operations, including the application of health and safety

standards, the implementation of security measures at our facilities and internal and external audits of

health and safety standards. One of the performance measures we track is the recognised industry

metric, lost time injury (“LTI”) and lost time injury frequency (“LTIF”). We monitor our injury rates and

currently benchmark them on a regional basis due to the varying lost time injury criteria across the

countries in which we operate. On Germany our LTIF in 2015 was approximately 2 % of the German

industry average. Overall, our LTIF was 0.32 per million working hours in 2016. We encountered 1 LTI

in Germany in the calendar year 2016.

We carefully manage our impact on the environment and strive to uphold the highest international envi-

ronmental, health and safety standards. We undertake a wide range of construction-related and opera-

tional measures for the conservation of soil and water resources. These include the shielding of local

environments by means of special catchment tanks and monitoring facilities. Additionally, one of the

critical objects of our environmental policy is the avoidance of water pollution. To achieve this objective,

we define a number of water pollution control measures during the planning phase, prior to the under-

taking of any development activity.

We operate in jurisdictions with stringent regulatory regimes, including Germany and Norway. To ensure

compliance with relevant legislations and regulations, we routinely monitor our activities and constantly

adapt our operations to incorporate new innovations and safety measures.

We spent € 23 million on environmental protection in the period under review, with investments in envi-

ronmental protection amounting to € 52 million.

- 24 -

10. Research and development

Our Company’s activities in the exploration and development of hydrocarbon reservoirs are typical for

our industry. To support these activities, we have our own laboratories in our Geo Support Centre for

production engineering and geo-sciences, for example. The focus of our research activities quite natu-

rally is on the ongoing improvement of our methods for the exploration, development and production of

hydrocarbon deposits.

The personnel of the “F&E and Special Projects” Department comprises of 4 employees. For execution

and efficient handling of R&D projects, we continue to rely on the proactive support of project attendants

from the relevant functional departments. Our expenditure on development in 2016 came to a total of

€ 3 million. We succeeded in maintaining our participation in key R&D projects and programs. This was

possible to achieve on the one hand through in-kind services, i.e. the performance of cost-equivalent

own services, as well as through increased use of shared research, such as in Deutsche Wissenschaft-

liche Gesellschaft für Erdöl, Erdgas und Kohle (DGMK) [German Society for Petroleum and Coal Sci-

ence and Technology] or joint industry projects (JIP) on the other.

The focus in the period under review was on our participation in application-oriented development pro-

jects together with DGMK. By ensuring timely implementation, these projects lead to improved and more

efficient production processes and to minimised exploration risks. Via the research fund of our industrial

association BVEG, we also support projects to do with basic research.

- 25 -

11. Comparison with previous outlook and 2017 guidance

In the 4th quarter 2016, the new mid-term planning (MTP) of the DEA Group for the following five years

was prepared and adopted. Our guidance for 2017 is based on this MTP.

The following reference criteria are used:

“slight” represents a change of 1 - 10 %

“considerable” applies for changes of 11 % or higher.

In total, we expect for 2017 a slight decrease in production and a slight increase in commodity prices.

We face the current environment in the E&P industry with further measures to optimise the structure of

the DEA group.

Underlying assumptions

On average, the Brent oil price quoted in US dollars developed below our last year’s guidance due to

the further decline of prices in the first quarter 2016. On average, the European NBP and TTF gas prices

of key importance to our business likewise turned out to be below our last year’s guidance. Regarding

the exchange rate between US dollar and EUR, the actual development was in line with the guidance.

Our guidance 2017 is based on forwards and consensus of analyst estimates for commodity prices and

exchange rate:

We assume Brent prices in a range of 50 – 55 USD/bbl and UK NBP prices in a range of 5.0 –

5.5 USD/mscf for 2017

We assume the USD/EUR exchange rate to be in a range of 1.05 – 1.15.

Production is based on our latest production profiles for the respective fields.

Production

Our total production in the calendar year was slightly below the level of our last year’s guidance. For oil,

production was slightly below guidance due to lower production in the Gulf of Suez in Egypt and slightly

lower production in Norway, whereas production in Germany was in line with the guidance. Gas produc-

tion was also slightly below our guidance due to lower production volumes in Egypt and Germany,

whereas Norway slightly exceeded the guidance.

For the year 2017, we assume that our production will be at a range of 120 – 130 kbbl OE/d as the

decline in the already producing fields is expected to be partially compensated by the production start

of the development projects in the West Nile Delta and Reggane in Egypt and Algeria, respectively.

DEA Deutsche Erdoel AG

Consolidated Financial Statements

Fiscal Year

1 January - 31 December 2016

- 2 -

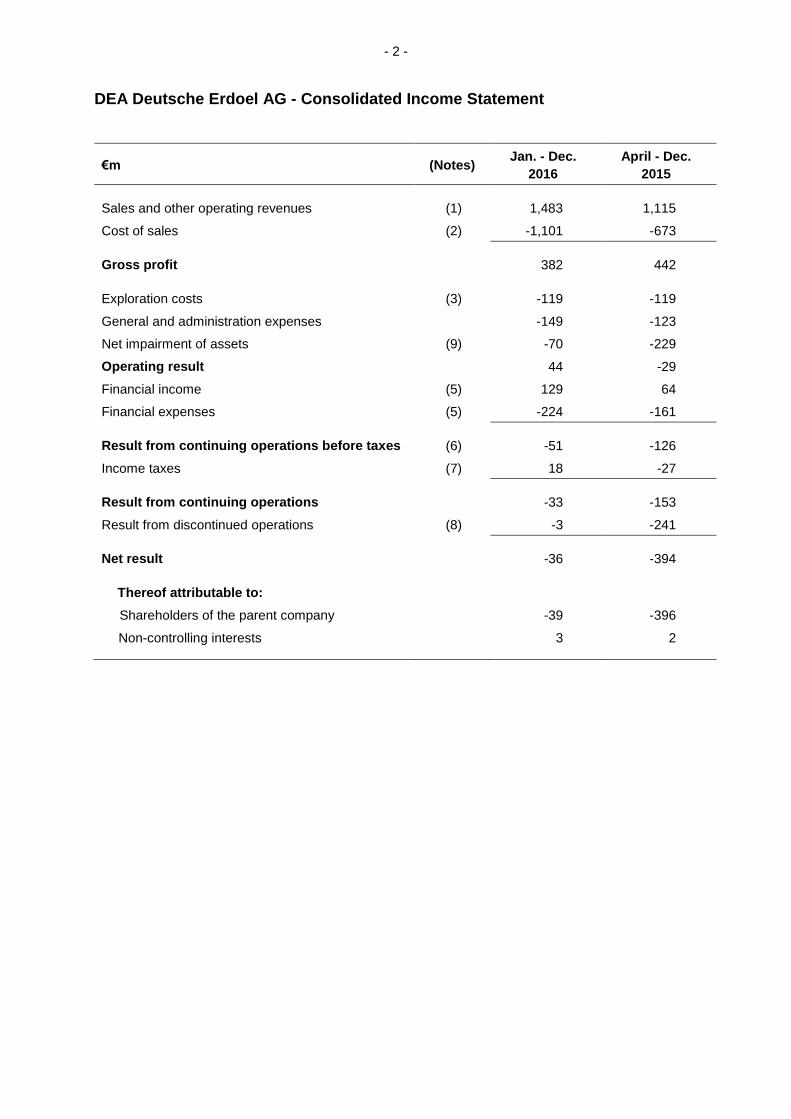

DEA Deutsche Erdoel AG - Consolidated Income Statement

€m (Notes) Jan. - Dec.

2016

April - Dec.

2015

Sales and other operating revenues (1) 1,483 1,115

Cost of sales (2) -1,101 -673

Gross profit 382 442

Exploration costs (3) -119 -119

General and administration expenses -149 -123

Net impairment of assets (9) -70 -229

Operating result 44 -29

Financial income (5) 129 64

Financial expenses (5) -224 -161

Result from continuing operations before taxes (6) -51 -126

Income taxes (7) 18 -27

Result from continuing operations -33 -153

Result from discontinued operations (8) -3 -241

Net result -36 -394

Thereof attributable to:

Shareholders of the parent company -39 -396

Non-controlling interests 3 2

- 3 -

DEA Deutsche Erdoel AG - Consolidated Statement of Comprehensive Income

€m Jan. - Dec.

2016

April - Dec.

2015

Net result -36 -394

Items that may be reclassified to profit or loss

Currency translation adjustments 17 -16

Fair valuation of financial instruments

in hedge relationship

-12

3

Fair valuation of financial assets available

for sale

-48

-2

Items that will not be reclassified to profit or loss

Remeasurement of defined benefit plans -17 34

Other comprehensive income (after taxes) -60 19

Total comprehensive income -96 -375

Thereof attributable to:

Shareholders of the parent company -99 -377

Non-controlling interests 3 2

- 4 -

DEA Deutsche Erdoel AG - Consolidated Balance Sheet

Assets (€m) (Notes) 31-12-2016 31-12-2015

Non-current assets

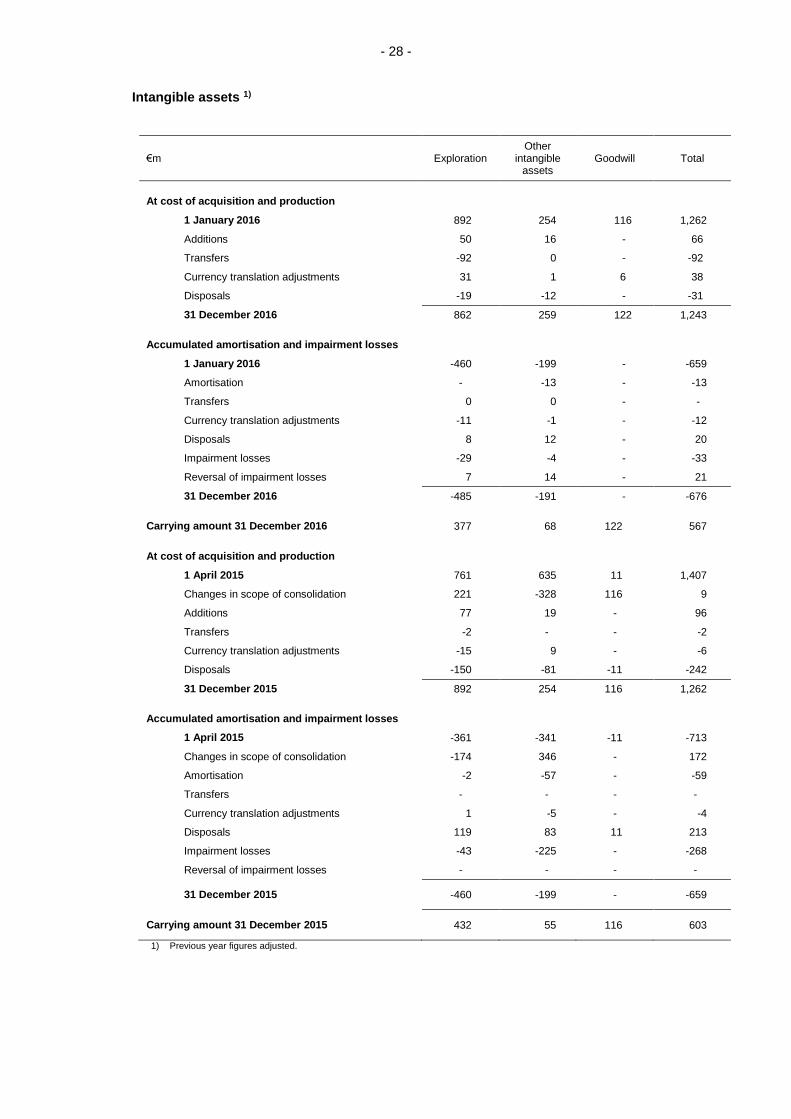

Intangible assets 1) (9) 567 603

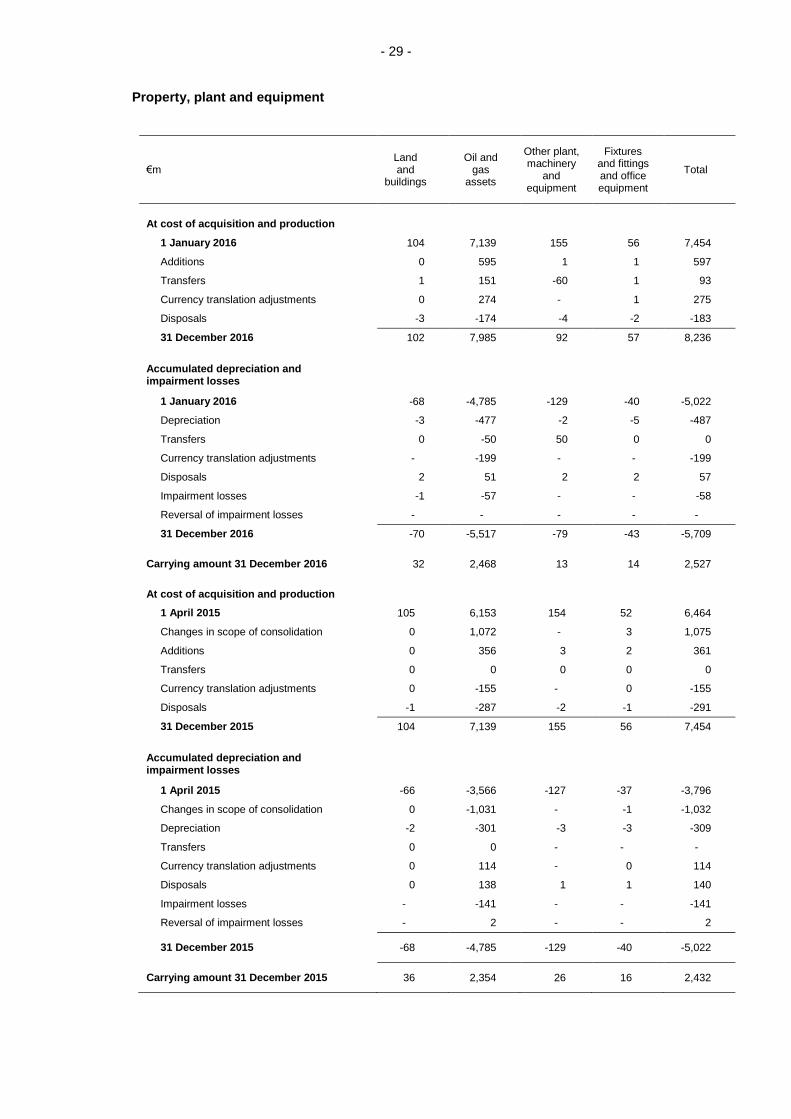

Property, plant and equipment (9) 2,527 2,432

Investment property 3 4

Financial investments 1 1

Financial receivables (10) 2,209 2,165

Other receivables and other assets (17) 95 162

Deferred tax assets (7) 85 74

5,487 5,441

Current assets

Inventories (12) 90 82

Financial receivables 2) (10) 0 340

Trade accounts receivable 2) (11) 336 426

Other receivables and other assets (11) 156 304

Income tax assets (7) 1 12

Cash and cash equivalents (13) 101 320

684 1,484

6,171 6,925

Equity and Liabilities (€m) (Notes) 31-12-2016 31-12-2015

Equity (14)

Shareholder's equity 1,900 1,954

Non-controlling interests 4 4

1,904 1,958

Non-current liabilities

Provisions (15) 616 665

Debt to banks (16) 1,494 2,021

Financial debt (16) 1,018 779

Income tax liabilities (7) 26 26

Other liabilities (17) 14 8

Deferred tax liabilities 1) (7) 431 512

3,599 4,011

Current liabilities

Provisions (15) 209 242

Debt to banks (16) 3 5

Financial debt (16) 16 283

Trade accounts payable (17) 308 306

Income tax liabilities (7) 32 53

Other liabilities (17) 100 67

668 956

6,171 6,925

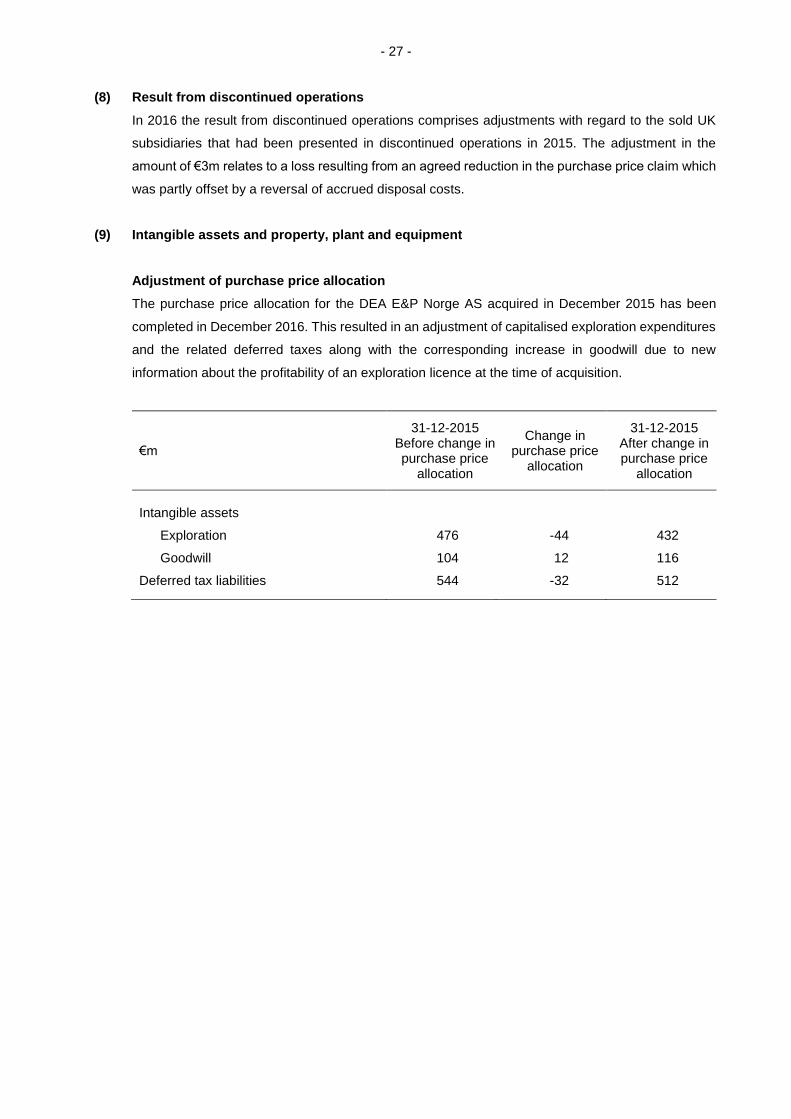

1) Previous year figures adjusted due to amended purchase price allocation. 2) As from the reporting period profit and loss transfers are recognised under financial receivables or financial liabilities, respectively. The previous year's disclosure as trade accounts receivable (€340m) has been adjusted accordingly.

- 5 -

DEA Deutsche Erdoel AG - Consolidated Cash Flow Statement

€m Jan. - Dec.

2016

April - Dec.

2015

Result from continuing operations -33 -153

Depreciation/impairment losses/reversal of impairment losses 570 501

Changes in provisions -10 -27

Changes in deferred taxes -94 2

Gain/losses from disposal of assets 5 14

Other non-cash income/expenses 14 33

Changes in working capital 46 -9

Changes in other balance sheet items 128 144

Cash flow from operating activities - discontinued operations - 16

Cash flow from operating activities 626 521

Cash outflows for additions to intangible assets, property,

plant and equipment and investment property

-656

-412

Cash inflows from disposal of fixed assets 23 115

Cash outflows for acquisitions - -875

Cash inflows from (cash outflows for) divestures 69 533

Cash inflows from (cash outflows for) financial assets 6 1

Cash flow from investment activities - discontinued operations - -20

Cash flow from investment activities -558 -658

Distribution to non-controlling interests -3 -3

Repayments of debt to banks -772 -

Proceeds from debt to banks 203 -

Repayments of financial liabilities -110 -

Proceeds from financial liabilities 395 198

Cash flow from financing activities -287 195

Net change in cash and cash equivalents 1) -219 58

Effects of foreign exchange rates changes and other changes

in value

0

-16

Cash and cash equivalents at beginning of reporting period 320 278

Cash and cash equivalents at end of reporting period 101 320

Supplementary information on cash flows from

operating activities

Income tax paid (less refunds) 1 87

Interest paid 60 39

Interest received 6 12

Dividends received 1 0

1) This includes changes from discontinued operations (April - Dec. 2015: €-4m).

- 6 -

DEA Deutsche Erdoel AG - Consolidated Statement of Changes in Equity from 1 January to 31 December 2016

€m Subcribed

capital Capital reserve

Retained earnings

Currency translation

adjustments

Fair valuation of financial instruments

Shareholder's equity

Non- controlling interests

Total

As at 01-04-2015 344 980 653 -61 42 1,958 5 1,963

Fair value of derivative financial instruments with no impact on profit or loss

3

3

3

Fair value of financial assets available for sale with no impact on profit or loss

-2

-2

-2

Currency translation adjustments

0

-14

-2

-16

-16

Remeasurement of defined benefit plans

34

34

34

Other comprehensive income 34 -14 -1 19 19

Net result -396 -396 2 -394

Total comprehensive income -362 -14 -1 -377 2 -375

Profit transfer/distribution 373 373 -3 -370

Other changes

As at 31-12-2015/01-01-2016 344 980 664 -75 41 1,954 4 1,958

Fair value of derivative financial instruments with no impact on profit or loss

-48

-48

-48

Fair value of financial assets available for sale with no impact on profit or loss

-12

-12

-12

Currency translation adjustments

0

16

1

17

17

Remeasurement of defined benefit plans

-17

-17

-17

Other comprehensive income -17 16 -59 -60 -60

Net result -39 -39 3 -36

Total comprehensive income -56 16 -59 -99 3 -96

Loss transfer/distribution 45 45 -3 42

Other changes 4 -4

As at 31-12-2016 344 980 657 -63 -18 1,900 4 1,904

- 7 - About this report

DEA Deutsche Erdoel AG is a German limited company and is headquartered at Überseering 40 in 22297

Hamburg, Germany. It is registered at the Hamburg local court under HRB 6882. The nature of the

operations and principle activities of DEA Deutsche Erdoel AG are described in the management report.

The presented consolidated financial statements as at 31 December 2016 were approved for publication

by the Board of Management of DEA Deutsche Erdoel AG on 2 February 2017. In accordance with the

resolution adopted at the annual general meeting, PricewaterhouseCoopers Aktiengesellschaft

Wirtschaftsprüfungsgesellschaft audited the consolidated financial statements and the consolidated

management report of DEA Deutsche Erdoel AG and issued its unqualified audit opinion. The consolidated

financial statements are available from DEA Deutsche Erdoel AG, Überseering 40, 22297 Hamburg and at

www.dea-group.com. The consolidated financial statements are filed electronically with the operator of the

German Government Gazette and promulgated therein after the filing.

Basis of preparation

The consolidated financial statements were prepared in accordance with the International Financial

Reporting Standards (IFRS) applicable in the EU, as well as in accordance with the supplementary

accounting regulations applicable pursuant to Section 315a, Para. 3 of the German Commercial Code

(HGB). All figures for the previous year were determined in conformity with the same principles unless new

accounting methods have been used prospectively for the reporting period.

The financial statements are prepared in euro (€). The amounts, including prior-year figures, are generally

reported in million euro (€m). If necessary, amounts are disclosed in thousand euro (€k). This rounding

effect does not produce a loss of information. Various items of the Income Statement and the Balance

Sheet are combined to improve the transparency of presentation. These items are shown and explained

separately in the Notes. In order to present the income statement of an international E&P company in a

more appropriate way and to increase the comparability with other companies in the industry, the

presentation of the income statement has been changed from the total cost to the cost of sales method.

Moreover, foreign currency gains and losses as well as income and expenses form financial derivatives are

no longer shown in the operative result, but are instead recognised under financial result. The prior-year

figures have been adjusted accordingly.

The financial statements have been prepared under the historical cost convention, except for derivative

financial instruments and certain other financial assets and financial liabilities, which have been measured

at fair value.

In the previous year the DEA Group created a second short fiscal year for the period from 1 April to

31 December 2015 in order to bring the financial year back into line with the calendar year. Since the current

fiscal year comprises a 12-month period, a comparison with the 9-month period of the short fiscal year is

of limited value.

- 8 - Summary of significant accounting policies

Scope of consolidation

The consolidated financial statements include the accounts of DEA Deutsche Erdoel AG and its

subsidiaries over which the company has control. DEA AG controls an investee if it has power over the

investee. In addition, DEA AG is exposed to, or has rights to, variable returns from the involvement with the

investee and DEA AG has the ability to use its power over the investee to affect the amount of DEA AG's

return. A subsidiary is de-consolidated from the date that control ceases. There are 20 consolidated

companies (previous year: 18), 4 of them foreign (previous year: 5). In the reporting period DEA E&P Norge

AS was merged into its direct parent company, DEA Norge AS. Furthermore, 3 companies (incorporated in

Germany) were newly founded. Participation in 3 foreign subsidiaries (previous year: 3) of minor importance

to the DEA Group are reported at fair value in accordance with IAS 39. In total, these subsidiaries account

for less than 1 % of the consolidated revenue and income as well as of consolidated debt.

Consolidation principles

The financial statements of the domestic and foreign companies included in the Consolidated Financial

Statements of DEA Deutsche Erdoel AG are drawn up in conformity with uniform accounting and valuation

methods. Expenses and earnings as well as accounts receivable and payable between the consolidated

subsidiaries are eliminated. Intercompany gains or losses are eliminated, unless they are negligible. Capital

consolidation is performed by offsetting the carrying amounts of subsidiaries against their underlying equity.

Depreciation charged in the companies' individual statements on shares in, and loans to, consolidated

subsidiaries are reversed.

Business combination

Cost of an acquisition is measured at the fair value of the assets given and liabilities incurred or assumed

at the date of exchange. Identifiable assets acquired and liabilities assumed in a business combination

(including contingent liabilities) are measured initially at their fair values at the acquisition date, irrespective

of the extent of any non-controlling interest. Non-controlling interest in a subsidiary represents the portion

of the subsidiary not owned by DEA Deutsche Erdoel AG. The results of the subsidiaries acquired or

disposed of during the year are included in the consolidated statement of income from the date of

acquisition or until their disposal, respectively.

Joint arrangements

Joint arrangements are classified as either joint operations or joint ventures depending on the contractual

rights and obligations of each investor. There are joint arrangements at DEA Group in course of

development and production activities. They are classified as joint operations since the arrangements

transfer the rights and obligations relating to the assets and liabilities to the investors. The Group's shares

in joint operations are accounted by recognising its respective share in assets and liabilities as well as its

income and expenses.

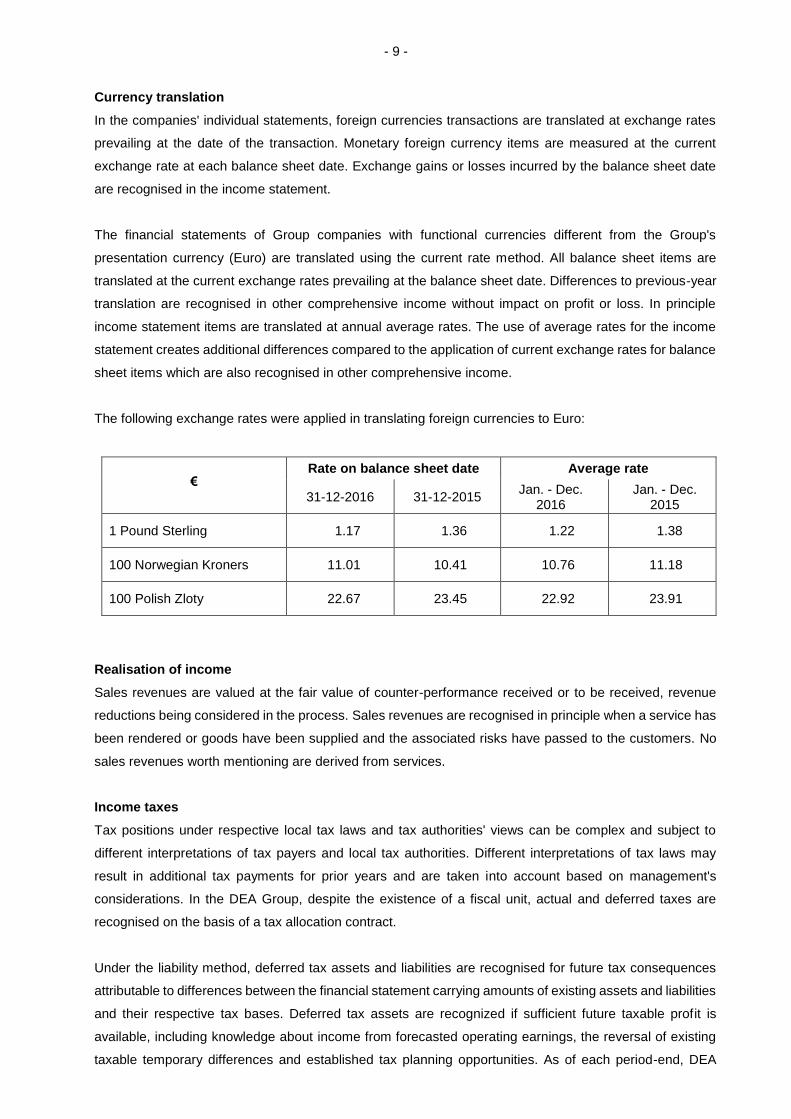

- 9 - Currency translation

In the companies' individual statements, foreign currencies transactions are translated at exchange rates

prevailing at the date of the transaction. Monetary foreign currency items are measured at the current

exchange rate at each balance sheet date. Exchange gains or losses incurred by the balance sheet date

are recognised in the income statement.

The financial statements of Group companies with functional currencies different from the Group's

presentation currency (Euro) are translated using the current rate method. All balance sheet items are

translated at the current exchange rates prevailing at the balance sheet date. Differences to previous-year

translation are recognised in other comprehensive income without impact on profit or loss. In principle

income statement items are translated at annual average rates. The use of average rates for the income

statement creates additional differences compared to the application of current exchange rates for balance

sheet items which are also recognised in other comprehensive income.

The following exchange rates were applied in translating foreign currencies to Euro:

€ Rate on balance sheet date Average rate

31-12-2016 31-12-2015 Jan. - Dec.

2016 Jan. - Dec.

2015

1 Pound Sterling 1.17 1.36 1.22 1.38

100 Norwegian Kroners 11.01 10.41 10.76 11.18

100 Polish Zloty 22.67 23.45 22.92 23.91

Realisation of income

Sales revenues are valued at the fair value of counter-performance received or to be received, revenue

reductions being considered in the process. Sales revenues are recognised in principle when a service has

been rendered or goods have been supplied and the associated risks have passed to the customers. No

sales revenues worth mentioning are derived from services.

Income taxes

Tax positions under respective local tax laws and tax authorities' views can be complex and subject to

different interpretations of tax payers and local tax authorities. Different interpretations of tax laws may

result in additional tax payments for prior years and are taken into account based on management's

considerations. In the DEA Group, despite the existence of a fiscal unit, actual and deferred taxes are

recognised on the basis of a tax allocation contract.

Under the liability method, deferred tax assets and liabilities are recognised for future tax consequences

attributable to differences between the financial statement carrying amounts of existing assets and liabilities

and their respective tax bases. Deferred tax assets are recognized if sufficient future taxable profit is

available, including knowledge about income from forecasted operating earnings, the reversal of existing

taxable temporary differences and established tax planning opportunities. As of each period-end, DEA

- 10 - Group evaluates the recoverability of deferred tax assets, based on projected future taxable profits. Based

upon the level of historical taxable income and projections for future taxable income over the periods in

which the deferred tax assets are deductible, DEA Group believes it is probable the company will realise

the benefits of these deductible differences. As future developments are uncertain, assumptions are

necessary to estimate future taxable profits as well as the period in which deferred tax assets will recover.

Estimates are revised in the period in which there are sufficient evidence to revise the assumption.

Intangible assets

Intangible assets include capitalised exploration expenditures, other intangible assets such as cost

recovery rights, licence rights in the production phase, commercial and technical software as well as

goodwills. They are reported at amortised costs.

The exploration phase comprises the period from the receipt of exploration rights until their expiry or until

technical feasibility of a field development and economic viability have been demonstrated respectively.

The exploration expenditures capitalised during this phase include for example concession acquisition

costs, licences and exploration rights as well as exploration wells. Exploration wells are accounted for at

their historic cost of acquisition or production according to the successful efforts method, i.e. expenses

incurred on exploration wells are only capitalised in principle if they were successful, in the sense that they

led in particular to the discovery of crude oil and gas deposits. Once the reserves are proved and

commercial viability is established as well as the development is highly probable the exploration wells are

reclassified into property, plant and equipment and intangible exploration rights are reclassified into other

intangible assets. During the exploration phase, the exploration expenditures capitalised are not subject to

scheduled amortisation/depreciation. With the start of production they are amortised/depreciated according

to the unit-of-production method.

With the exception of goodwill, all intangible assets have a finite useful life and are therefore subject to

systematic linear or production-related depreciation. The useful life of concessions and other licence rights

corresponds to the contractual term or comprises the period until the end of economic production. Software

for commercial or technical applications is depreciated under the straight-line method over three years. The

useful economic life and amortisation methods are subject to annual review.

Goodwill is not subject to systematic amortisation. It is subject to an impairment test on an annual basis or

whenever there are indications of a diminution in value (impairment test). Goodwill is part of cash-

generating units. The goodwill impairment test is performed at the level of a cash-generating unit or a group

of cash-generating units. This is the lowest level at which goodwill is monitored for internal management

purposes.

Property, plant and equipment

Property, plant and equipment comprise land and buildings, oil and gas assets, other plant, machinery and

equipment as well as fixtures and fittings and office equipment. They are valued at amortised acquisition

or production cost. Borrowing costs that can be directly allocated to the acquisition or production of an asset

are capitalised as part of acquisition or production costs if a considerable period is necessary to convert

the asset into its intended state for use or sale ("qualified asset"). The cost of property, plant and equipment

- 11 - includes the estimated cost of de-installation or demolition and removal and of the reconditioning of the

asset under public or private law obligations, to the extent related provisions were set up. Maintenance and

repair costs are stated as expenses.

Oil and gas assets are generally depreciated using the unit-of-production method. Basically, in case of

capitalised wells the depreciation is based on the current production of the period in relation to proved

developed producing reserves and in case of acquisition costs and production facilities/support equipment

the current production of the period is set in relation to total proved reserves.

Other property, plant and equipment, with the exception of land and similar rights, is depreciated using the

straight-line method. The typical useful lives of the DEA Group's non-production-related property, plant and

equipment are as follows:

Years

Buildings 24 – 50

Gas storage 33

Technical plant and machinery 5 – 15

Factory and office equipment 3 – 20

Impairment test

An impairment loss is recognised for intangible assets as well as for property, plant and equipment and

investment properties if the recoverable amount of the asset is less than its carrying amount. Exploration

assets are required to be tested for impairment as soon as the technical feasibility and profitability of a

resource can be proven. The presence of facts and circumstances indicating an impairment also gives rise

to an impairment test. If the asset is part of a cash-generating unit (the smallest identifiable group of assets

generating cash flows, which are largely independent of the cash inflows of other assets or other groups of

assets), then an impairment is derived on the basis of the recoverable amount of the cash-generating unit.

In the event that the carrying amount of a cash-generating unit to which a goodwill was allocated exceeds

the recoverable amount, a resulting impairment loss is initially applied to the allocated goodwill. Any further

impairment loss required will be taken into account through a pro-rata reduction in the remaining carrying

amounts of the cash-generating unit. A reversal of an impairment loss up to the value of amortised cost is

made if the reasons for an earlier impairment are no longer existing. In this case, the increased book value

resulting from a reversal must not exceed the amortised cost of acquisition or production. Impairment losses

are reported net of reversals of impairment losses. Impairment losses on goodwill are not reversed.

Within the scope of the impairment test, the recoverable amount of the cash-generation unit is determined.

The recoverable amount is defined as the higher of fair value less cost to disposal or value in use. The fair

value represents the best possible estimate for the amount for which an independent third party would

acquire the cash-generating unit on the balance sheet date; the cost of disposal is deducted. Value in use

reflects the present value of the future cash flows which are expected to be generated with the cash-

- 12 - generating unit. If either of these amounts exceeds the carrying amount, it is not always necessary to

determine both amounts. These values are generally determined based on discounted cash flow

calculations which, in turn, are generally based on the current corporate planning. The cash flow forecasts

pertain to the life-of-field-period for the individual concession/licence or groups of concessions/licences.

The calculations are based on historical experiences as well as the expectations for future market trends.

The principal assumptions underlying the determination by management of recoverable amount are the

forecasts for market prices of crude oil and natural gas, the estimated reserves, the production forecast as

well as the discount rates. The discount rates applied are based on the weighted average capital costs

taking into consideration specific country risks. The calculation was not related to the actual capital structure

of the company but was generated as a derivation from Peer Group.

Financial assets

Financial assets are recognised in the balance sheet if a company is a party to a contract for the asset in

question. Market-conform purchases or sales of financial assets are recognised or derecognised,

respectively, on the day of trading. Financial assets are derecognised when the contractual rights to cash

flows from the asset expire or the entity transfers the financial asset. The latter applies when substantially

all the risks and rewards of ownership of the asset are transferred, or the entity no longer has control of the

asset.

Financial assets are allocated to the following valuation categories: “loans and receivables”, “available-for-

sale financial assets” and “financial assets at fair value through profit or loss” ("held for trading" or “held in

hedging relationship”).

Financial assets, with the exception of financial derivatives and available-for-sale financial assets, are

valued at amortised cost by applying the effective interest method, if necessary. Any impairments

necessary are determined by the actual risk of default. In the presence of appropriate indications, such as

the insolvency of a customer or disputed invoices, specific impairments are made. Receivables are

generally corrected via an allowance account. Impairments are reversed if payments are received or the

default risk is reduced accordingly. The reversal is recognised in the same expense item in which the

original impairment loss was recorded.

The available-for-sale financial assets are recognised initially and in the following periods at fair value as

long as such can be determined reliably. Unrealised gains and losses are stated as other comprehensive

income without impact on profit or loss. If there are objective and material indications of a reduction in the

value of an asset, an impairment loss is recognised in profit or loss.

Inventories

Inventories are carried at cost of acquisition or production or at the lower net realisable value. Production