Embed Size (px)

Citation preview

Dalmia Cement (Bharat) Ltd.

Annual Report 2007-08

InsideManagement Discussion & Analysis 24

Directors' Report 38

Corporate Governance Report 45

Standalone Financials 58

Consolidated Financials 87

Letter from Vice Chairmen 02

Key Financial Highlights 04

Directors’ Profile 06

Session with the Managing Director 10

Accelerating Growth 14

Today's successful businesses have set a clear goal for themselves. They continuously focus on creating and delivering value to their stakeholders. Something that can only be measured in terms of company's strategic relevance to its stakeholders.

The last few years have seen Dalmia Cement (Bharat) Ltd. (DCBL) move from strength to strength. Our revenues have more than doubled; volumes have grown; and brand awareness has improved considerably. All of this has been made possible by an astute business plan, careful execution and extensive market mapping.

This is also a result of back-breaking efforts put in by our 3300 employees, all of whom have not just believed in the DCBL story, but also in its culture of excellence, and in the future that it is walking fast towards...

To us, growth is a sustained activity. Our achievements in the past year are just the stepping stones towards the future that we have envisioned for the Company and its stakeholders.

This past year has seen strategic restructuring keeping in view our future goals. We have launched large scale projects in cement, accepted key business challenges, explored diversification opportunities, took initiatives towards organization building and brought about process and system improvements.

Accelerating Growth

01

Evening view of our cement plant at Dalmiapuram

Dear Shareholder,

Financial Year 2008 was a year of challenges and accomplishments for your Company. On many counts, it was a landmark year as the accelerated growth momentum continued for a major part of the year. As a proof of economy with sound fundamentals, India achieved a GDP growth rate which is amongst the best in the global arena.

Having clocked over 9% growth in the preceding two years, India has again logged a GDP growth of 9% in FY 2008 . With a CAGR of 8.8% in the past 5 years, our belief is that the economy shall continue to grow at a higher CAGR in the coming 5 years.

With an accelerated rate of GDP growth, improving infrastructure, rising per capita income and overall consumption and burgeoning success of small and medium enterprises, Indian economic growth momentum is further going to establish its importance globally. The bottleneck though, could be the rising inflation and interest costs and the over dependence on imported petroleum products. The government, with the participation of concerned institutions and private organisations is taking effective steps to address these concerns.

Letter from Vice Chairmen

02

The India growth story is being augmented by both manufacturing and services sectors. Manufacturing sector has consistently grown at 9%. This coupled with 12% growth in services sector has led to a veritable construction boom across the country. Over a sustainable period of three years, growth of the construction sector has outpaced that of the GDP.

This boom has been beneficial for cement industry. In the last five years, the Indian cement industry had added 49 MnTPA capacities and its production has grown by 60 MnTPA, registering a CAGR of 6% and 9% respectively. Going forward, we firmly believe that cement demand will grow at a double digit CAGR on a long term basis even though yearly growth numbers may be a bit volatile.

From being a highly fragmented and a bit localised industry some decades ago, cement industry is registering rapid transition into a more consolidated industry with key players making pan India manufacturing and sales presence. As the anticipated demand growth looks promising in medium to long term, cement players are investing heavily in rapidly expanding capacities.

Having been in the industry for almost seven decades, your Company has envisaged the future of cement industry much in advance and undertook capacity addition program in the year gone by. After adding 2 MnTPA capacity at its plant at Dalmiapuram, it initiated Greenfield expansion in Andhra Pradesh and Tamil Nadu. Having identified the southern region (in context of demand supply situation) amongst the most promising areas and leveraging its brand strength amongst customers, your Company will be amongst the frontrunners to benefit from the booming cement demand in years to come. Construction and developmental activity at both these projects is in full swing and we expect the same to be completed well within the stipulated time. To expand its footprint from Southern region towards Eastern India, your Company acquired 21.7% stake in the equity capital of OCL India Ltd., consequent upon amalgamation of it’s subsidiary, Dalmia Cement (Meghalaya) Limited.

Other area of your Company's operation – Sugar is also expected to witness a sweeter time ahead. Sugar production in the current sugar season of 2007-08 is expected to be 25 MnT after sitting on the record production in previous fiscal which led to lower realisations. This is likely to continue in coming years as the availability of sugar cane is expected to reduce on account of reduced acreage of cultivation. Based on these macro parameters, we envisage the domestic sugar prices to firm up. Value added segments of power co-generation and distillery from the by products shall add to the bottom line of integrated players like your Company.

Let us now share with you your Company's excellent financial performance for FY 2008, highlights of which are given below.

?Net Revenue from your Company's operations increased by 50% to Rs.14,807 million.

?Profit before depreciation, interest and taxes (PBDIT) increased by 56% to Rs. 6,334 million.

?Profit before tax (PBT) grew by 46% to Rs. 4,341 million.

?Profit after tax (PAT) grew by 52% to Rs. 3,472 million.

These are creditable results in the distinctly different economic environments of your Company's two dominant business segments, cement and sugar, both of which are cyclical plays. The entire credit goes to the Company fraternity for their untiring efforts in making this possible. Needless to say, we are grateful to all our stakeholders for their faith and trust reposed in us.

03

Jai Hari Dalmia Yadu Hari Dalmia

Key Financial Highlights

Particulars

Total Income Rs. Mn 4,017 4,743 6,506 11,426 16,452

Operating Profit (PBDIT) Rs. Mn 789 785 1,603 4,054 6,334

Cash Profits Rs. Mn 433 535 1,267 3,403 4,673

Profits before Tax (PBT) Rs. Mn 309 357 1,089 2,964 4,341

Profit after Tax (PAT) Rs. Mn 254 309 848 2,289 3,472

Share Capital Rs. Mn 77 77 77 85 162

Reserves & Surplus Rs. Mn 3,407 3,507 4,199 7,449 11,310

Loan Funds Rs. Mn 2,825 4,988 6,832 10,146 15,833

Gross Block Rs. Mn 7,049 7,691 10,446 16,971 18,830

Net Current Assets Rs. Mn 1,783 2,130 2,199 1,752 4,536

Operating Profit Margin 20% 17% 25% 35% 39%

Net Profit Margin 6% 7% 13% 20% 21%

Return on Average Net Worth 7% 9% 22% 39% 37%

Debt Equity Ratio x 0.81 1.39 1.60 1.35 1.38

Interest coverage x 2.1 2.6 5.6 6.5 4.8

Current Ratio x 2.89 2.38 1.93 1.35 1.68

#EPS (fully diluted) Rs. 4.27 4.91 11.78 29.18 42.87 #Cash EPS (fully diluted) Rs. 7.29 8.52 17.60 43.40 57.70

Dividend per share Rs. 5* 5* 2 3 4

Dividend Rate 50% 50% 100% 150% 200%

Share Price Rs. 287.9* 392.0* 264.5 361.3 284.8

Market Capitalization Rs. Mn 2,203 2,999 10,119 15,438 23,020

FY 2004 FY 2005 FY 2006 FY 2007 FY 2008

Clinker

Cement

1,04

3

1,29

3

1,15

1 1,40

5

1,26

2 1,56

9

2,00

5

2,73

7

2,44

4

3,29

4

FY 04

CEM

ENT

& C

LIN

KER

PR

OD

UC

TIO

N

(�000T)FY 05 FY 06 FY 07 FY 08

89

73 84

108

246

FY 04

SU

GA

R P

RO

DU

CTI

ON

(�000T)FY 05 FY 06 FY 07 FY 08

*Face Value Rs 10 per share, split to Rs 2 per share in FY 06. #Based on shares at year end.outstanding

04

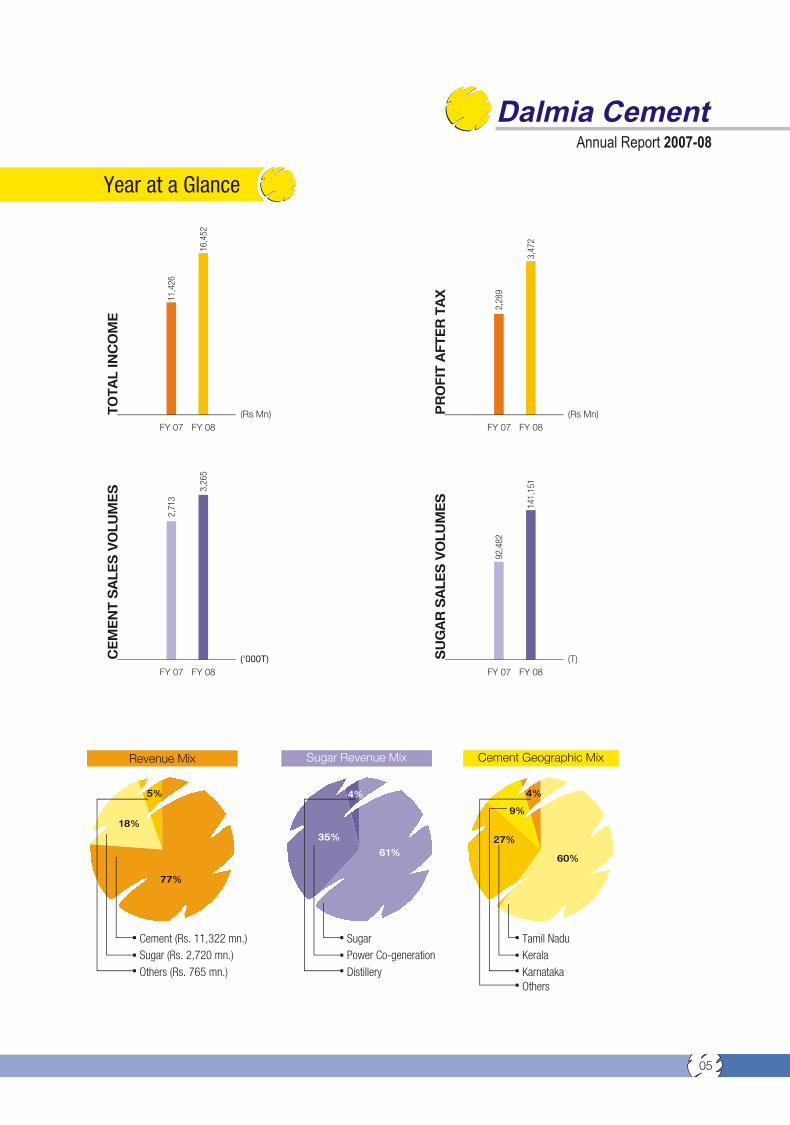

Year at a Glance

Revenue Mix

5%

18%

77%

Cement (Rs. 11,322 mn.)

Sugar (Rs. 2,720 mn.)

Others (Rs. 765 mn.)

Sugar Revenue Mix

Sugar

Power Co-generation

Distillery

4%

61%

35%

Cement Geographic Mix

Tamil Nadu

Kerala

KarnatakaOthers

4%

60%

27%

9%

FY 07FY 08

11,4

26

16,4

52

TOTAL INCOME

(Rs Mn)

92,4

82

141,

151

FY 07FY 08

SUGAR SALES VOLUMES

(T)

2,28

9

3,47

2

FY 07FY 08

PROFIT AFTER TAX

(Rs Mn)

2,71

3

3,26

5

FY 07FY 08

CEMENT SALES VOLUMES

('000T)

05

Mr. Pradip Kumar Khaitan, 67, has been associated with the cement

industry for over 41 years. He was co-opted as a Director of the Company

in 1996. He holds an LL.B. degree from the University of Calcutta. As a

partner of Khaitan & Co., Solicitors and Advocates, he has extensive

experience in legal and commercial matters. He is a Director of several

leading public limited companies in India.

Chairman and Non-Executive Director

Pradip Kumar Khaitan

Mr. J. H. Dalmia, 63, holds a B.E. degree in electrical engineering from

Jadavpur University and a Master's degree in electrical engineering from

the University of Illinois, Urbana Champagne. He has more than 36 years

of experience cutting across various industries which includes wide

knowledge and experience of refractory, sugar and cement businesses.

Mr. J.H. Dalmia has vast experience in research and development having

personally received several patents for the Company's businesses and

has been instrumental in establishing the Company’s research and

development efforts more than 20 years ago.

Vice-Chairman

Jai Hari Dalmia

Mr. Y. H. Dalmia, 60, holds a B.Com (Hon) degree from Delhi University

and is a Fellow Member of the Institute of Chartered Accountants of India.

He has more than 35 years of experience in the cement industry. Mr. Y.H.

Dalmia has served as President of the Cement Manufacturers Association

and is a known figure in the cement industry.

Vice-Chairman

Yadu Hari Dalmia

Directors' Profile

06

Mr. Mridu Hari Dalmia, 66, is a gold medallist in chemical engineering from

Jadavpur University. He was co-opted as a Director of the Company in

2005. In his present capacity he is the President and CEO of OCL having

been associated with the Company since 1970. He brings with him wealth

of over 38 years of experience in the cement industry and has led the

Group in various sectors in national and international operations. He has

held leadership positions in various Indian business associations and has

been associated with various industry organisations in the past including

those as Managing Committee member of the Federation of Indian

Chambers of Commerce and Industry, President of Indian Refractories

Manufacturers Association, Cement Manufacturers Association and

National Council for Cement and Building Materials. Currently he is a

member of the Management Committee and the Expert Committee on

Direct Taxes of the Associated Chambers of Commerce and Industry.

Non-Executive Director

Mridu Hari Dalmia

Mr. Puneet Dalmia, 35, holds a B.Tech. degree from the Indian Institute of

Technology, Delhi and is a gold medalist from the Indian Institute of

Management, Bangalore in strategy and marketing. He has eleven years

of experience in the industry having started his career as the co-founder

and Chairman of one of the most profitable e-recruitment websites in India,

JobsAhead.com, which was later acquired by Monster.com, a Nasdaq-

listed multinational company. Mr. Puneet Dalmia conceptualized the

growth strategy and governance architecture for the Company to focus on

its core businesses and is spearheading the growth plans for the group.

Managing Director

Puneet Dalmia

Mr. Gautam Dalmia, 40, holds B.S. and M.S. degrees in electrical

engineering from Columbia University. He has 15 years of experience in

the cement and sugar industries. He was part of the team that led the

diversification of the Company into sugar business in 1994. He was

personally responsible for implementing a new strategy to turnaround the

sugar business. He has led the effort to design and implement the

Company’s integrated sugar, ethanol and cogeneration business. He is

directly responsible for managing the sugar business and is leading all

operations and execution of cement projects besides providing leadership

to the commercial functions for the group.

Joint Managing Director

Gautam Dalmia

07

Directors' Profile

Mr. Nil Ratan Khaitan, 71, holds an LL.B. degree from the University of

Calcutta. He has over 22 years of experience in the cement industry. He

was co-opted as a Director of the Company on August 24, 1979. He is an

advocate by profession and has extensive experience in legal, taxation

and commercial matters. He holds directorships in two public companies,

namely, Universal Conveyor Belting Limited and Jay Cylinders Limited.

Independent Non-Executive Director

Nil Ratan Khaitan

Mr. M. Raghupathy, 71, holds an M.A. degree in Economics from Madras University, with Statistics as the special subject. He was Co-opted as a Director of the Company in 1997. He is the Chairman of the Audit Committee and Shareholders' Committee of the Company. He joined the Indian Administrative Service (IAS) in 1960 and has held various positions in the Government of Tamilnadu such as Deputy Secretary to Government in the Revenue Department, Collector of Salem District, Director of Rural Development, Managing Director of TamilNadu Dairy Development Corporation, Commissioner of Animal Husbandry Department, Commissioner & Secretary to Government of TamilNadu in various departments like Transport, Housing and Urban Development, Agriculture (as Agriculture Production Commissioner) & Textiles, Principal Commissioner of Land Administration, Land Reforms and Revenue departments of the Government of Tamilnadu, Chairman of Thiruvalluvar Transport Corporation Limited, Chairman of the Tamilnadu Transport Development Finance Corporation, Chief Electoral Officer of Government Of Tamilnadu, Principal Vigilance Commissioner and Principal Commissioner of Revenue Administration. He has over 11 years of experience in the cement industry.

Independent Non-Executive Director

M. Raghupathy

Mr. J. S. Baijal, 77, holds an M.A. degree in economics from Allahabad University. A senior fellow in Harvard University, USA, he joined the Indian Administrative Service (IAS) in 1954 and has held the posts of Secretary, Finance, Government of Orissa; Joint Secretary to the Government of India, Ministry of Finance, Department of Economic Affairs; Director of National Fertilizers Limited, IFFCO; Minister Economic, Embassy of India, Washington D.C.; Chairman of the Industrial Development Corporation of Orissa; Officer on Special Duty with the Reserve Bank of India; Secretary, Irrigation & Power, Government of Orissa; Additional Secretary to the Government of India, Health & Family Welfare; Additional Secretary to the Government of India, Ministry of Finance, Department of Economic Affairs; Ex-officio Director of the Mineral & Metals Trading Corporation of India Limited, ONGC Limited, and Punjab National Bank; Secretary to the Government of India, Planning Commission; and Executive Director, World Bank, International Finance Corporation, and International Development Association, Washington. After his retirement, he has held positions as Director of HDFC Bank Limited, before being appointed as a Director of the Company on May 31, 1999. He is a Trustee of Morgan Stanely Mutual Fund since 1994 and has over eight years of experience in the cement industry.

Independent Non-Executive Director

J. S. Baijal

08

Mr. N.Gopalaswamy, 76, holds a B.Sc. degree in chemistry from Madras

University and a B.E. degree in chemical engineering from Annamalai

University. Having joined the company in 1980 he was co-opted as a

Whole-time Director in 1989. He is a member of the Institute of Industrial

Engineers, USA, the Indian Institution of Industrial Engineering, the Indian

Institute of Chemical Engineering, and the Institution of Engineers (India).

Having held the position of President for 25 years, since last year, he is a

Council Member of the Tiruchirapalli Productivity Council. He has over 40

years of experience in the cement industry. He ceased to be a Whole-time

Director of the Company and was appointed as an Additional Director with

effect from 1-8-2007.

Non-Executive Director

N. Gopalaswamy

Mr. Donald Peck, 54, holds an M.A. degree and a doctorate in economic

history from Oxford University. He was nominated as a Director of the

Company in July, 2006. Mr. Peck's expertise lies in emerging markets

investing, both in the equity investment/fund management business,

experience in which was acquired by him when he was with International

Finance Corporation in Washington and prior to that in the investment

banks of Lloyds Bank and Morgan Grenfell. He joined CDC Capital

Partners and was responsible for helping it to develop its equity investment

business and setting up its fund management business worldwide. He

went on to become a Director in 1999. Having run the CDC/Actis private

equity business in India from 1995 to 2007, Mr Peck became one of the

senior founding partners in Actisin 2004.

Independent Non-Executive Director

Donald Peck

Mr. T. Venkatesan, 55 years, Whole-time Director, is a B.A. (Economics) and a fellow member of the Institute of Chartered Accountants of India. He brings with him a rich experience of over 28 years having commenced his career with Thiru Arooran Sugars Limited in the finance and accounts department. He has worked with reputed companies such as Eicher Tractors Limited, Triveni Engineering Limited and the Aditya Birla group. In his previous assignment with the Sterlite Group, he was instrumental in spearheading the expansion from 180 KTPA to 400 KTPA, as CEO for Sterlite Industries' copper business. In addition he was also holding additional charge as CEO and director on the Board of Vedanta Alumina Limited and has successfully implemented a Rs. 5000 crores project in the State of Orissa. His expertise lies in accelerating growth and building organisational capability to ensure delivery of business goals. In his present capacity he is responsible for operations and future growth of cement segment.

Whole Time Director

T. Venkatesan

09

What is the vision of your company in global business environment?

Globally, India is the second largest producer in both our lines of business, second to China in cement and second to Brazil in sugar. Considering the low per capita consumption of cement in India and the energy based opportunity in sugar business, India is a high growth market for the two industries.

While we are leveraging the best of knowledge, technology and practices available globally; our growth will be dictated by the manner in which the Indian economy is going to unfold. We at Dalmia Cement have utmost faith in the India growth story. We have participated for almost seven decades in the nation building activity and have grown consistently over these years gaining traditional wisdom in these markets.

To us the single most important challenge is to build scale in both the businesses. Our mid term aim is to break into top five producers in both our businesses. While we are chasing the capacity build program in cement, we are also practicing strict discipline on return on capital employed. We aspire to attain profitable growth. This discipline on returns restrains us from pursuing every possible opportunity and helps us identify and grab opportunities which will help us outperform the industry and create greater stakeholders' return on sustainable basis.

In sugar business we follow the integrated model, which helps us manage the market vagaries better. Ethanol and Power enhance the profitability in good times and protect bottom-lines in down cycles. We consider our ability to access high yield variety sugarcane as the foremost focus of our sugar business. Going beyond rhetoric development work with farmers in our region, our recovery is amongst the best in the industry and our endeavour is to consistently enhance accessing high quality cane.

With the third generation of the family taking the anchoring role, we are making conscious efforts to bring about a cultural shift in the way our businesses will be managed. We are fast transiting from 'family run' to 'family owned, professionally managed' company with designated heads for the two main business lines. We are empowering people to take appropriate decisions at various levels. Many platforms for interaction are being created whereby employees can communicate and discuss ideas openly; cutting across the hierarchy.

Session with the Managing Director

10

What are the value systems of your company? Why do you think they are important for any organisation?

How do you view your company's performance in FY 2008?

How are your two Greenfield expansion projects in Andhra Pradesh and Tamil Nadu progressing?

At Dalmia Cement, we are committed “to constantly create value for our stake-holders” while practicing integrity. In our endeavour to create a forward marching DCBL, we have adopted a set of values which will govern all our actions, create differentiation and make us a respectable employer for leaders of tomorrow. Forming the very basis of our vision, these values are Learning, Pursuit of Excellence, Speed and Teamwork.

Learning: The world around us is continuously evolving and changing. Past knowledge is becoming obsolete at a pace faster than ever before. In order to excel and propel us to greater heights, our leaders must possess child like curiosity and humility to learn from anyone at any level.

Pursuit of excellence: Competing in a global environment, we aspire to set and surpass global benchmarks on key value drivers. We will continuously inculcate the habit of taking impossible challenges before creating possible solutions. Our channels of communication are open across hierarchy to allow for free flow of knowledge and innovation.

Speed: In the fast changing competitive business environment, the big may not necessarily beat the small but fast will definitely lead the slow. We choose our professional leaders to carry on the entrepreneurial culture, based on their passion for growth. We empower them to take quick decisions taking due cognizance of the possible risks involved.

Teamwork: We believe that sustainable growth can not be achieved by an individual but is an outcome of collaborative efforts and ideas of a group. We create options for people to network across businesses, locations and functional teams to achieve excellence. At Dalmia Cement, we encourage people to display high level of mutual trust and respect for colleagues.

FY 2008 was an exciting year of performance at Dalmia Cement (Bharat) Limited. Results were pretty satisfactory across multiple areas of financial performance, operational efficiency, project implementation and organisational transformation. I can see the passion of our people to achieve results quickly across various performance metrics. The Year’s financial performance reflects improved operational efficiency of our company as is depicted below.

?Gross sales of Rs. 16,908 million, registered an impressive year on year growth of 51%.

?Profit before tax grew by 46% to reach Rs. 4,341 million.

?Net Profit grew by 52% to reach Rs. 3,472 million.

?In cement, we achieved over 20% volume growth backed by high 94% capacity utilisation.

?As for sugar, the three plants ran on enhanced capacity for the first full financial year andderived benefits from volume growth of 128% in production and 53% in sales.

Of the two Greenfield projects, Cudappa plant of 2.25MnTPA Cement capacity at Andhra Pradesh is expected to be commissioned in second half of CY2008. The main plant and machinery had been ordered well in time in financial year 2007. Major achievement of the group has been the construction of Pre Heater tower with a height of over 139 meters within 10 months, against an industry standard of 12-14 months.

For an equivalent cement capacity project in Ariyalur, Tamil Nadu; the group now has requisite expertise and the methodologies for achieving its target of commissioning in first half of CY2009.

The company is facing challenges in terms of skilled manpower across managerial and operational levels but we are confident of project completion well within time lines and costs.

11

There are diverse opinions on Indian cement sector's prospects. How does your company see the sector in near future?

In the fast paced competitive environment, one national agenda being ignored is that of community development. What are your views on this issue?

We believe in India growth story. And hence we are making significant investments in India. Being an emerging markets frontrunner, India is expected to remain an attractive cement destination. MNCs and Indian Cement players are responding to the increased demand opportunity in the country by expanding capacities. In our view, capacity expansion will bear a significant mark in India's development considering that the sector employs 70,000 people directly and almost 10 million people indirectly.

Demand for cement is growing consistently. For the quantum of housing units, hotels, malls, SEZs and office space needed; kilometers of roads/rail tracks/metros to be constructed & renovated across highways and hinterland; industrial expansion in key sectors including steel and power; scope of improvement in port and aerodrome network; we see a favourable demand supply situation for cement manufacturers in times to come, with some volatility, here and there.

Indian cement industry is expected to be on fast track of consolidation. Players with smaller capacities and localised presence will be dominated by national players having capacities in excess of 20 MnTPA. Hence it is imperative for smaller companies to grow at a rapid pace and have national presence to be amongst significant players in the industry.

At Dalmia Cement, we are responsible for carrying on the traditional legacy of inclusive growth for all. Our commitment to be a good corporate citizen with conscience has two focus areas of community development and concern for environment.

On community development front, we focus on providing basic education and healthcare to the communities we operate in. Our educational initiatives benefit thousands of students pursuing their primary and secondary education. We also have investments in Industrial Training Institutes that prepare workers on technical skills required for getting better job opportunities. Our plants have been set up in villages which did not even have basic economic or social infrastructure. The Company has consistently invested to uplift these areas in both aspects.

As for our environment protection, we follow the best practices towards controlling emission, water conservation and efficient energy consumption. The company has used technology and appropriate structures to reduce dust emissions. The company ensures zero chemical discharges through water treatment plants, using recycle water for plantation. Initiatives for afforestation and plantation have been undertaken at our cement manufacturing plant to contribute towards a greener environment.

Realising that much more needs to be done, the company has plans to allocate upto 2% of its annual profits to Dalmia Foundation to undertake CSR activities across all its regional facilities.

12

Bankers

AXIS Bank LimitedBank of IndiaBNP ParibasCanara BankCorporation BankICICI Bank LimitedIndian BankPunjab National BankState Bank of IndiaState Bank of TravancoreUnion Bank of IndiaYES Bank Limited

Head Office

11th & 12th Floors, 'Hansalaya'15, Barakhamba RoadNew Delhi 110001

Registered OfficeDalmiapuram 621 651District Tiruchirapalli(Tamilnadu)

AuditorsStatutory : S.S. Kothari Mehta & Co.Internal : KPMG & Axis Risk Consulting

Services Pvt. Ltd.

Company Information

13

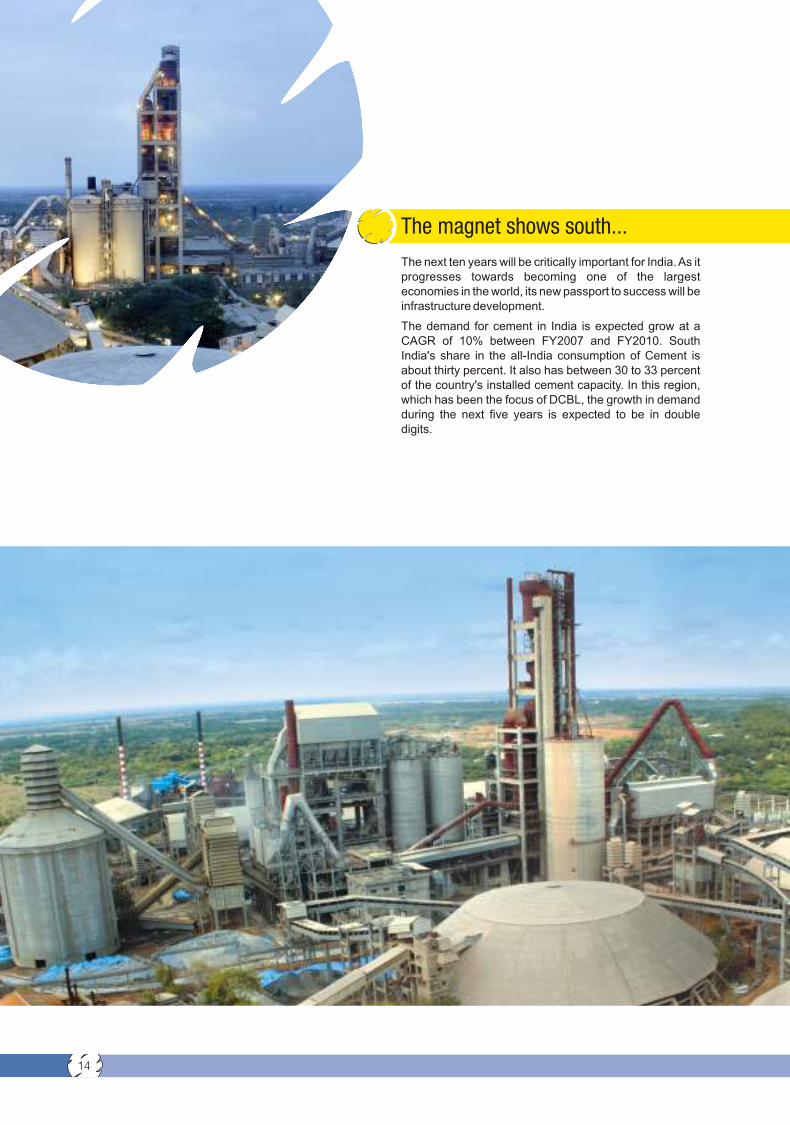

The next ten years will be critically important for India. As it progresses towards becoming one of the largest economies in the world, its new passport to success will be infrastructure development.

The demand for cement in India is expected grow at a CAGR of 10% between FY2007 and FY2010. South India's share in the all-India consumption of Cement is about thirty percent. It also has between 30 to 33 percent of the country's installed cement capacity. In this region, which has been the focus of DCBL, the growth in demand during the next five years is expected to be in double digits.

The magnet shows south...

14

It may be added that the Southern region enjoys amongst the highest realizations in the country on account of favorable cement demand supply scenario.

The states which account for about 60% of the off take in the South, namely Andhra Pradesh and Tamil Nadu are likely to grow in teens, driven by government projects, SEZs, Infrastructure projects, and IT Parks.

Thus, DCBL's already commissioned 2 MnTPA brownfield expansion, as well as the upcoming 4.5 MnTPA Greenfield projects under implementation are favorably timed. By responding to the demand escalation with rapid expansion, the Company is well-poised to achieve higher sales volume in its core markets in Southern India.

15

Aerial view of our cement plant at Dalmiapuram

DCBL, being in a cyclical industry such as Cement, where the demand-supply position alternates between deficit and glut over a period of time, has diversified into Sugar, Ethanol and Power industries. In recent past, it tripled its capacity in Sugar to 22500 TCD at three locations in state of Uttar Pradesh.

Diversified for stability

16

It also set up a 80 KLPD Ethanol plant next to one of its Sugar plants. It has installed 79 MW cogeneration power plants across the three Sugar units for captive consumption & export of surplus power. DCBL has access to power for its Cement plants from thermal power plant and wind farm in South. These measures help to mitigate the risk during a downside period in the Cement industry's cycles.

The consistency in its corporate performance is adequately reflected in its track record over the years of growth with profitability.

17

Integrated Sugar Plant at Jawaharpur

Importance of people as assets can not be undermined in any organization, and especially in a company embarking on an accelerated growth path. With increasing scale of operations, people capacity and capabilities need to be enhanced at an equally rapid pace. We follow a rigorous selection procedure across operational and managerial cadre so that we attract talent which matches our value systems.

People, Performance and Progress.

18

Each group has exhibited capability to deliver up to the challenges and performed well, accomplishing operational and process improvements of the growing Company. Various annual awards have been instituted to recognize exemplary performers across all locations and levels.

Whether in carving out career and development plans to take them forward in work and life or tying up with global institutes such as Indian Institute of Management, Ahmedabad and Centre for Creative Leadership for upgrading their skills and knowledge; the focus is on strengthening individual assets so that they not only contribute towards the growth of the Company but also spur a culture of excellence in society at large.

19

Customer acceptance of quality is an important aspect of building market-share and DCBL's brands have upheld customer confidence in the markets in which they are currently available.

Stronger Brand Strength

20

The Company has a formidable reputation for its specialty Cements for niche applications. Both the range of products manufactured and the brand support activities regularly undertaken, play a significant role in maintaining a positive and substantial mind-share for DCBL's brands.

Each niche brand has a strong back up both at retailer and distribution levels. Regular brand promotions have ensured loyalty and acceptance of DCBL's brands amongst a growing base of quality and brand-conscious customers.

21

As a concerned corporate, we are conscious of our responsibilities towards the communities in whose midst our manufacturing and business operations are conducted. Our community development initiatives are undertaken to improve the quality of life of people in the surrounding areas. Notable thrust areas of some of these initiatives are education, community development and cultural enrichment.

Our might to empower communities

22

Cane crop ready for harvesting

In education for the young, the company endeavours to provide for basic study material, midday meals and even entire school infrastructure. It also runs an industrial training institute for up-skilling and providing vocational training for the workers.

For the development of the farming community around its sugar business, DCBL helps farmers with superior farming techniques to aid them to increase their farm output and thereby their income. From extending loans to farmers, to organising experience and knowledge sharing fairs, it all forms part of the company’s CSR activities.

To enrich cultural lives of the communities the company strives to host annual festivals, provides for festivities during the season, sponsors dramas and music programmes.

Through these efforts DCBL has endeavored to maintain a harmonious relationship with the environment and its social surroundings by adding value to the bio-system of which it is an integral part.

23

Afforestation in mining area Afforestation in mining area

Indian Economy Overview

What proved to be a challenging year for the global economies turned out to be a year of manifestation of might for the Indian economy. While there were increased global uncertainties and fear of slow down of the US economy with crude oil prices reaching all time highs, Indian Economy maintained its growth momentum in FY 2008.

According to the data released by the Central Statistical Organisation, Indian Economy has posted GDP growth of 9%. As per the said report, manufacturing registered growth of 8.8%, agriculture 4.5% and construction 9.8%. Services, contributing almost 63% to the GDP recorded another year of double digit growth.

Despite the overall pressure of global uncertainties and the inflation reaching beyond 7%, this GDP growth is a true reflection of the sound fundamentals and the maturity of our economy. We, at Dalmia Cement, believe that our economy will sustain its growth momentum over the next three to five years.

Management Discussion and Analysis

24

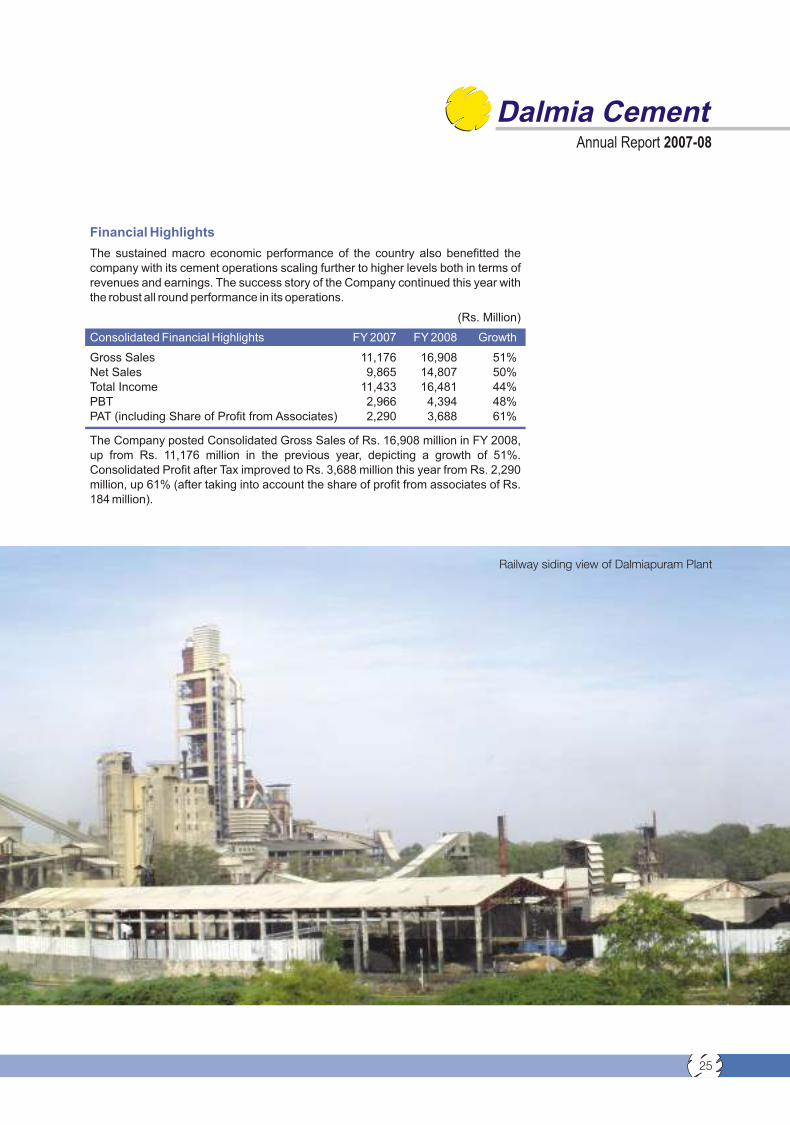

Financial Highlights

The sustained macro economic performance of the country also benefitted the company with its cement operations scaling further to higher levels both in terms of revenues and earnings. The success story of the Company continued this year with the robust all round performance in its operations.

(Rs. Million)

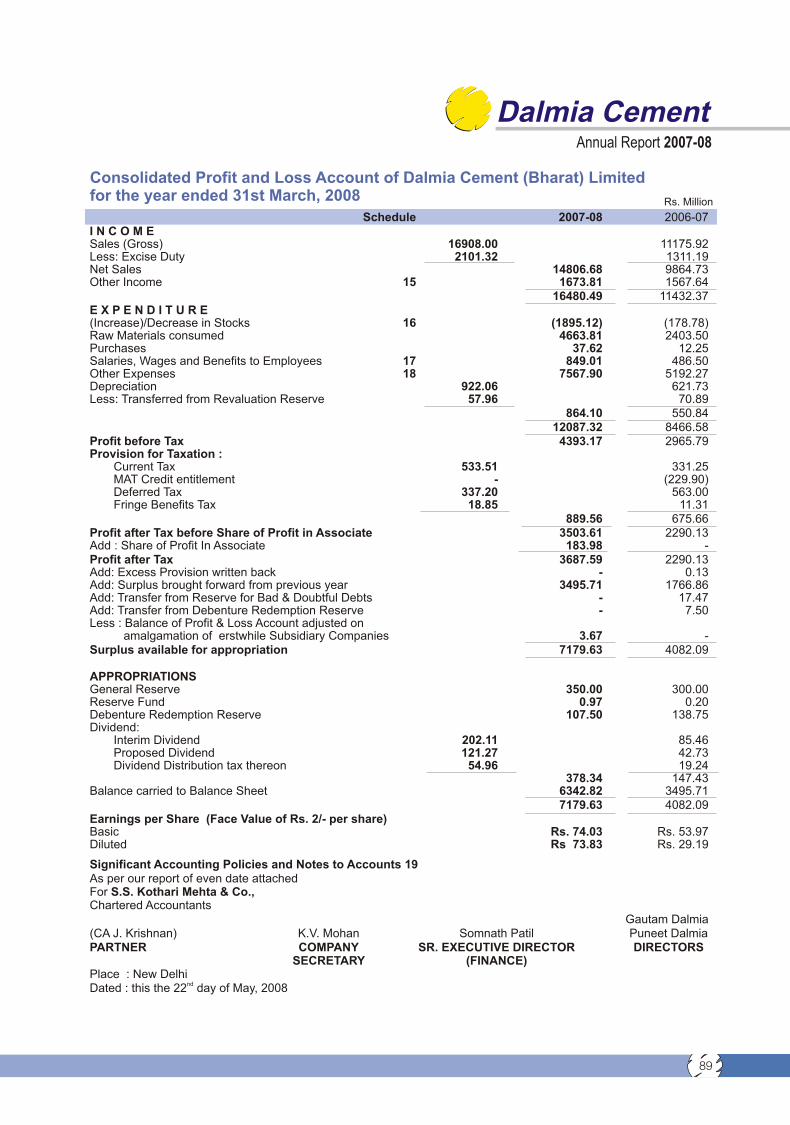

Gross Sales 11,176 16,908 51%Net Sales 9,865 14,807 50%Total Income 11,433 16,481 44%PBT 2,966 4,394 48%PAT (including Share of Profit from Associates) 2,290 3,688 61%

The Company posted Consolidated Gross Sales of Rs. 16,908 million in FY 2008, up from Rs. 11,176 million in the previous year, depicting a growth of 51%. Consolidated Profit after Tax improved to Rs. 3,688 million this year from Rs. 2,290 million, up 61% (after taking into account the share of profit from associates of Rs. 184 million).

Consolidated Financial Highlights FY 2007 FY 2008 Growth

25

Railway siding view of Dalmiapuram Plant

6,33

4

4,05

4

FY 07FY 08

EBITDA

(Rs Mn)

Stand alone Net Sales in FY 2008 were up from Rs. 9,865 million to Rs. 14,807 Million for the Company. EBITDA for the Company grew from Rs. 4,054 million to Rs. 6,334 million, depicting a growth of 56%.

Share of contribution at Net Sales level of each business to the total net sales has not changed much over last year. However, EBITDA contribution from the cement business has significantly improved, as is evident from the table above.

The net sales of cement business grew by 49% to Rs. 11,322 million in FY 2008. Net Sales from the integrated sugar business of the Company increased to Rs. 2,720 million in FY 2008, up 61%. Net Sales from other businesses, which include magnesite and refractory amongst others, were up from Rs. 556 million in FY 2007 to Rs. 765 million.

In the Earnings Before Interest, Tax and Depreciation, huge surge was witnessed in cement and integrated sugar businesses in FY 2008 as compared to previous year. Cement EBITDA has grown last year on account of higher volumes as well as improved realisations taking margins to 44% from 37% last year. Sugar business EBITDA improved due to profitability contribution from the co-generation unit.

Stand Alone Financial Highlights FY 2007 FY 2008 Growth % Mix % Mix (FY 2007) (FY 2008)

Net Sales*Cement 7,620 11,322 49% 77% 77%Sugar 1,689 2,720 61% 17% 18%Others 556 765 38% 6% 5%

9,865 14,807 50% 100% 100%EBITDA*

Cement 2,830 5,063 79% 70% 80%Sugar 207 373 80% 5% 6%Others 1,017 898 -12% 25% 14%

4,054 6,334 56% 100% 100%

PAT 2,289 3,472 52% 100% 100%

(Rs. Million)

* Cement includes Wind-Farm: Sugar includes Co-generation and Distillery unit financials.

2,07

7 2,49

6

2,31

1

2,98

13,48

2

3,54

7

3,63

3 4,14

5

NET SALES

(Rs Mn)Q1Q2Q3Q4

FY 07FY 08

44%

37%

FY 07FY 08

CEMENT EBITDA M

ARGIN

S

(%)

26

Cement Business

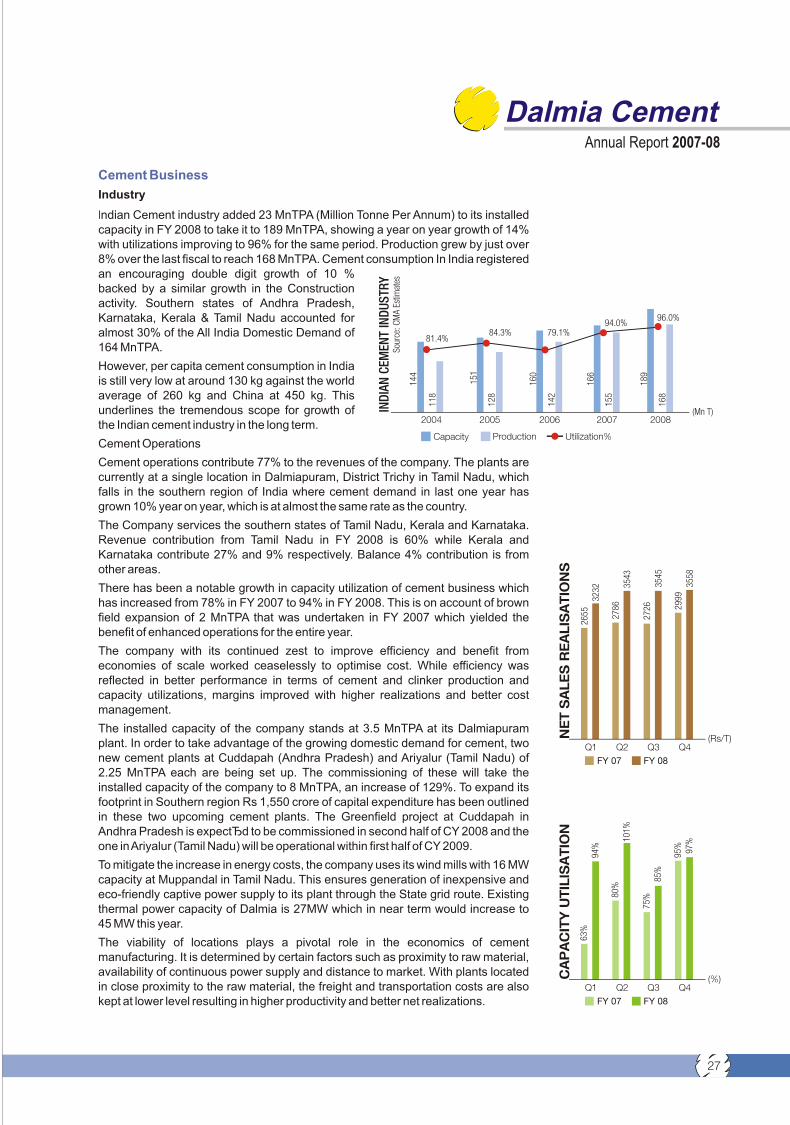

Industry

Indian Cement industry added 23 MnTPA (Million Tonne Per Annum) to its installed capacity in FY 2008 to take it to 189 MnTPA, showing a year on year growth of 14% with utilizations improving to 96% for the same period. Production grew by just over 8% over the last fiscal to reach 168 MnTPA. Cement consumption In India registered an encouraging double digit growth of 10 % backed by a similar growth in the Construction activity. Southern states of Andhra Pradesh, Karnataka, Kerala & Tamil Nadu accounted for almost 30% of the All India Domestic Demand of 164 MnTPA.

However, per capita cement consumption in India is still very low at around 130 kg against the world average of 260 kg and China at 450 kg. This underlines the tremendous scope for growth of the Indian cement industry in the long term.

Cement Operations

Cement operations contribute 77% to the revenues of the company. The plants are currently at a single location in Dalmiapuram, District Trichy in Tamil Nadu, which falls in the southern region of India where cement demand in last one year has grown 10% year on year, which is at almost the same rate as the country.

The Company services the southern states of Tamil Nadu, Kerala and Karnataka. Revenue contribution from Tamil Nadu in FY 2008 is 60% while Kerala and Karnataka contribute 27% and 9% respectively. Balance 4% contribution is from other areas.

There has been a notable growth in capacity utilization of cement business which has increased from 78% in FY 2007 to 94% in FY 2008. This is on account of brown field expansion of 2 MnTPA that was undertaken in FY 2007 which yielded the benefit of enhanced operations for the entire year.

The company with its continued zest to improve efficiency and benefit from economies of scale worked ceaselessly to optimise cost. While efficiency was reflected in better performance in terms of cement and clinker production and capacity utilizations, margins improved with higher realizations and better cost management.

The installed capacity of the company stands at 3.5 MnTPA at its Dalmiapuram plant. In order to take advantage of the growing domestic demand for cement, two new cement plants at Cuddapah (Andhra Pradesh) and Ariyalur (Tamil Nadu) of 2.25 MnTPA each are being set up. The commissioning of these will take the installed capacity of the company to 8 MnTPA, an increase of 129%. To expand its footprint in Southern region Rs 1,550 crore of capital expenditure has been outlined in these two upcoming cement plants. The Greenfield project at Cuddapah in Andhra Pradesh is expect? d to be commissioned in second half of CY 2008 and the one in Ariyalur (Tamil Nadu) will be operational within first half of CY 2009.

To mitigate the increase in energy costs, the company uses its wind mills with 16 MW capacity at Muppandal in Tamil Nadu. This ensures generation of inexpensive and eco-friendly captive power supply to its plant through the State grid route. Existing thermal power capacity of Dalmia is 27MW which in near term would increase to 45 MW this year.

The viability of locations plays a pivotal role in the economics of cement manufacturing. It is determined by certain factors such as proximity to raw material, availability of continuous power supply and distance to market. With plants located in close proximity to the raw material, the freight and transportation costs are also kept at lower level resulting in higher productivity and better net realizations.

Capacity Production Utilization%

81.4%84.3% 79.1%

94.0%96.0%

144

151

160

166

189

118

128

142

155

168

2004 2005 2006 2007 2008

IND

IAN

CEM

ENT

IND

US

TRY

(Mn T)

Sour

ce: C

MA

Estim

ates

63%

80%

75%

95%

94%

101%

85%

97%

CAPACITY U

TILIS

ATIO

N

(%)Q1Q2Q3Q4

FY 07FY 08

27

2726 29

99

3545

3558

2655 27

86

3232 35

43

NET SALES R

EALIS

ATIO

NS

(Rs/T)Q1Q2Q3Q4

FY 07FY 08

The Company continued to enjoy goodwill in its market place and its brands such as Dalmia Superroof and Vajram continued to be preferred products and commanded premium over other products in the market. The most prominent aspect of company's market is its significant presence in infrastructure applications which includes cement used for constructing airstrips, oil wells and railway sleepers. The Company's oil well cement is the first cement in the country to receive the prestigious American Petroleum Institute (API) certification. It is used for cementing the walls of on-shore and off-shore oil wells of ONGC, Reliance and other oil exploration companies.

Outlook

Realty will continue to play a major role as the development of commercial space including malls, hotels, SEZs will go on full swing. Residential realty has seen a slight moderation in demand as the cost and availability of retail finance has adversely impacted its growth. This slowdown is momentary. Recommended pay hike of government employees by the Sixth Pay Commission and the otherwÿse rising prosperity of the Indian middle class segment with improved economic conditions will drive the growth momentum of the retail realty sector.

Going forward, dedicated rail freight corridor, rapid expansion of airport network to cover tier II & III cities, ongoing up-gradation of important ports and airports, slew of capacity expansion in steel, power and other manufacturing sectors and 2010 Commonwealth Games to be held in Delhi will all continue to augment the growth momentum in key infrastructure areas. The country is likely to double its infrastructure spending over the next five years towards creating and modernising its infrastructure and sustaining its growth momentum.

In light of above and based on the last 3 year CAGR of 10% in cement demand, the Company estimates that the industry shall continue to see double digit demand growth.

The Cement Manufacturers Association estimates addition of over 75 MnTPA capacity spread across India, in next two years. This would take the country's cement capacity to over 260 MnTPA, to meet its rising demand growth. The Company would endeavour to maintain its market share in its core geographies and expand network in its new market, State of Andhra Pradesh.

77%

66%

FY 07FY 08

PPC

(%)

1.39

1.30

FY 07FY 08

Cement Clinker Ratio

28

Sugar Business

Industry

India continues to remain the largest consumer of sugar followed by China, Brazil and USA. In fact consumption in above countries is growing at a rate higher than the world average. Consequently these topographies are expected to play a pivotal role in global sugar trade in coming years.

Sugar is now perceived as an energy crop owing to derivation of ethanol which is increasingly being used as a mixture in petrol. With rising crude prices but softer sugar prices, Brazil has been increasingly diverting the sugarcane juice for manufacture of ethanol. Currently about 55-56 % of the total sugarcane production of Brazil is used for manufacturing ethanol.

The Indian Sugar industry is the country's second largest agro processing industry with an estimated production of 27 MnT (Million Tonnes) in the 2007-08 sugar season. This sector is a key driver of rural development, supporting India's economic growth. The industry, in the past two to three seasons has shown respectable growth in terms of quantities produced. This was primarily on account of good climatic conditions, remunerative sugar cane prices, setting up of new production capacities and on time payments to farmers. The cane acreage grew by 4.4% in 2007-08 across India and by 7% in UP where the company operates its three units.

In FY 2008, sugar prices remained slightly soft as production in India was at 28.3 MnT in sugar season 2006-07. Delayed commencement of crushing on account of uncertainty in cane prices and lower per hectare yield of sugar cane has moderated production estimates for the season. Crushing days reduced significantly in 2007-08 season and is expected to favourably impact the realisations.

1417

.5

12.7

18.5

19.3

19.6

22.7

28.3

26.1

25.5

ProductionOfftake (incl exports)

2004 2005 2006 2007e 2008e

INDIAN SUGAR INDUSTRY

(Mn T)

13,1

08

13,0

95

13,3

75

14,0

72

Q1�08

SU

GA

R S

ALE

S R

EALI

SA

TIO

NS

(Rs/T)Q2�08 Q3�08 Q4�08

29

Sour

ce: I

SMA,

Indu

stry

Est

imat

es

Sugar Operations

Dalmia embarked on the manufacture of sugar in the mid-nineties and set up its first unit at Ramgarh (Distt. Sitapur) U.P. The installed capacity at the time of diversifying into sugar business was 2500 TCD (tonnes cane crushing per day), which has been expanded to 7500 TCD. From a single sugar-manufacturing unit the Company has now grown to three operational units with total installed capacity of 22500 TCD leading to sugar manufacturing of about 300,000 TPA. With co-generation capacity of 79MW and distillery capacity of 80 KL per day, it is a forward integrated sugar manufacturing set up.

The sale of sugar accounts for more than 10% of Company's revenues and it aims to build deep capabilities in this segment. The sugar manufacturing plants incorporate state-of-the-art technology that ensures high productivity and efficiency, across all plants. Due to emphasis on quality throughout the processes, the Company produces high quality sugar both in terms of grain size and colour, which leads to better realizations.

In this challenging business environment of huge sugar stocks and high administered sugarcane prices, the Company's sugar business performance is noteworthy.

Sugar

Sugar production and cane crushed has grown substantially in FY 2008 as compared to the previous year. Sugar production grew by 128% to 2.46 lac tons in FY 2008. Crushed cane increased by 142% to 24.45 lac tons. Volumes jumped due to the fact that two new sugar plants at Jawarharpur and Nigohi started operating at full scale in FY 2008. Though sugar recovery rate in FY 2008 was at 10.06%, the business saw 53% growth in sales volumes at 1.41 lac tones.

Co-generation

The Cogeneration plants at three locations Ramgarh, Jawaharpur and Nigohi with total installed capacity of 79 MW started operating at full scale last year. Power generated during FY 2008 was 299 million units and gross Power exported during the year was 201 million units. Cogeneration is major contributor to top and bottom line of business and it helped to pull up sugar contribution in the overall Company revenues and profits.

Distillery

Distillery plant at Jawaharpur (U.P.) with capacity of 80 KLPD too is now operational and contributing to the top-line of the Company. Distillery Production in FY 2008 touched 9557 KL and sales volume during this period was at 7490 KL

Being highly regulated, the performance of the sugar industry in India is largely dependent on Government policies and regulations. This year, free level of buffer stock of 20 million tonnes for free sale was released by the Government and it has impacted the realizations. Sugar prices which had fallen to historically low levels during last year have only recently shown slight signs of recovery.

2445

1009

20072008

CANE C

RUSHED

(�000 T)

13,4

60

16,7

66

20072008

SUGAR SALES R

EALIS

ATIO

NS

(Rs.T)

30

Outlook

This season, it is expected that sugar production would be lower in the range of 25-26 MnT against the earlier estimates of 30-31 MnT and this should bode well for sugar realisations to inch upwards.

The industry has been under tremendous pressure on various issues of cane sourcing, cane pricing and lower sugar realisations. Thorat Commission was set up by the Central Government to look into various aspects of sugar industry including cane prices, reservation of cane area, dispensing with monthly release mechanism, abolishing of levy sugar and distance criteria between the factories. The industry is hopeful that the issues would be resolved in a manner that is beneficial to all stakeholders.

Going forward the shift of sugar towards manufacture of ethanol would be crucial for the volume of sugar available for international market. Within our country, the government's fiat that with effect from 1st Oct'08, oil marketing companies will have to blend 10 per cent ethanol with petrol from existing 5% will provide value-addition to the sugar by-product, molasses. This will open up further opportunities for your company.

The overall financial position of the company continued to be healthy and promising. The snapshot of the financial performance of the company in FY 2008 vis-à-vis its performance in FY 2007 is presented below.

(Rs. Millions)

Net Sales from Operations 9,865 14,807 50%Other Income 1,561 1,645 5%

Total Income 11,426 16,452 44%

Material Costs adjusted for change in stocks 2,237 2,806 25%Salaries & Wages 486 849 75%Other Expenses 5,188 7,592 46%

Total Expenditure 7,911 11,247 42%

Profit before Depreciation and Tax (PBDT) 3,515 5,205 48% Depreciation 551 864 57%Profit before Tax (PBT) 2,964 4,341 46% Taxes 675 869 29%

Profit After Tax (PAT) 2,289 3,472 52%

The company witnessed increased turnover on account of growth in volumes in cement as well as sugar units. Improved realisations along with change in product mix led to higher profitability.

Total Expenses before Depreciation and Tax for the company are Rs. 11,247 Million, up from Rs. 7,911 Million last year. Power and Fuel costs are the highest contributor to the expenses of the company in FY 2008, at Rs. 2,887 million. Raw Material costs at Rs. 2,806 million are close to 25% of the expenditure. Freight & transportation charges along with Repairs & Maintenance contributed another 15% to the costs. Salaries and Wages contribute only 8% to the costs of the company at Rs. 849 million. Interest cost was 10% of expenses.

Financial Performance

Stand Alone Financials FY 2007 FY 2008 Growth

6%

28%

5%

10%

7%

18%

FY 2007

Raw Material

Salaries

Power & Fuel

Repair & Mtc

Freight &Trsptn

Interest

Others

26%

31

8%

25%

5%

10%

10%

16%

FY 2008

26%

Raw Material

Salaries

Power & Fuel

Repair & Mtc

Freight &Trsptn

Interest

Others

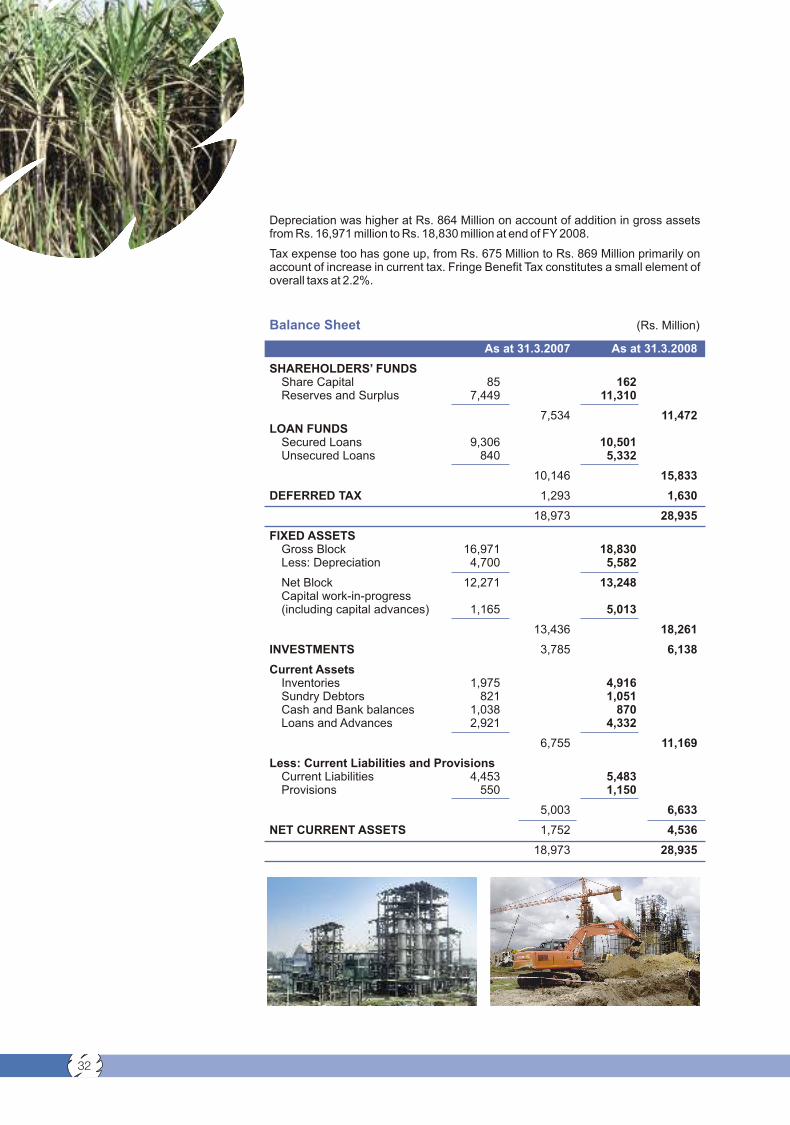

Depreciation was higher at Rs. 864 Million on account of addition in gross assets from Rs. 16,971 million to Rs. 18,830 million at end of FY 2008.

Tax expense too has gone up, from Rs. 675 Million to Rs. 869 Million primarily on account of increase in current tax. Fringe Benefit Tax constitutes a small element of overall taxs at 2.2%.

Balance Sheet (Rs. Million)

SHAREHOLDERS’ FUNDSShare Capital 85 162Reserves and Surplus 7,449 11,310

7,534 11,472LOAN FUNDS

Secured Loans 9,306 10,501Unsecured Loans 840 5,332

10,146 15,833

DEFERRED TAX 1,293 1,630

18,973 28,935

FIXED ASSETSGross Block 16,971 18,830Less: Depreciation 4,700 5,582

Net Block 12,271 13,248Capital work-in-progress (including capital advances) 1,165 5,013

13,436 18,261

INVESTMENTS 3,785 6,138

Current AssetsInventories 1,975 4,916Sundry Debtors 821 1,051Cash and Bank balances 1,038 870Loans and Advances 2,921 4,332

6,755 11,169

Less: Current Liabilities and ProvisionsCurrent Liabilities 4,453 5,483Provisions 550 1,150

5,003 6,633

NET CURRENT ASSETS 1,752 4,536

18,973 28,935

As at 31.3.2007 As at 31.3.2008

32

Capital Structure

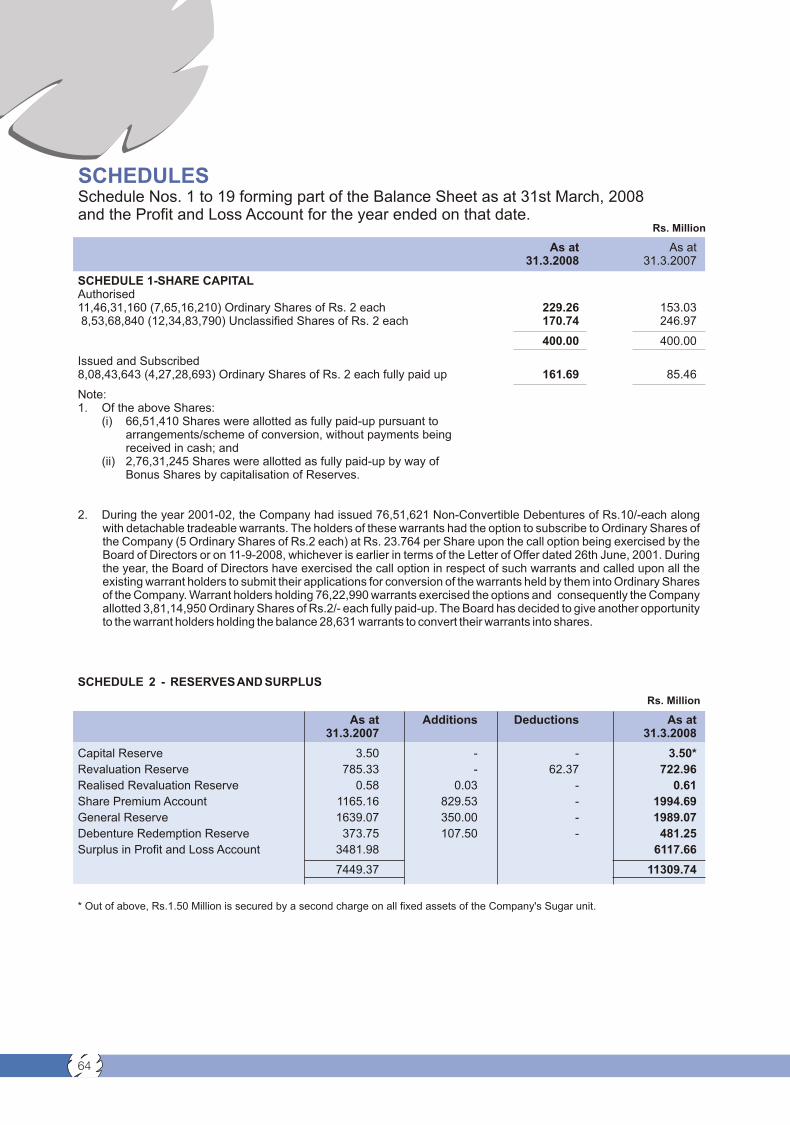

The Company’s equity capital increased to Rs. 162 million as on March 31, 2008 comprising 8,08,43,643 equity shares (4,27,28,693 shares) of Re. 2 each (fully paid up) on account of warrant conversion.

During the FY 2002, the Company had issued 76,51,621 Non-Convertible Debentures of Rs.10/-each along with detachable tradeable warrants. The holders of these warrants had the option to subscribe to Ordinary Shares of the Company (5 Ordinary Shares of Rs.2 each) at Rs. 23.76 per Share upon the call option being exercised by the Board of Directors on or before September 11, 2008, in terms of the Letter of Offer dated June 26, 2001. During the year, the Board of Directors have exercised the call option in respect of such warrants and called upon all the existing warrant holders to submit their applications for conversion of the warrants held by them into Ordinary Shares of the Company. Warrant holders holding 76,22,990 warrants exercised the option and consequently the Company allotted 3,81,14,950 Ordinary Shares of Rs.2/- each fully paid-up.

Reserves & Surplus

The Company’s reserves and surplus increased to Rs. 11,310 million in FY 2008. During the year under review, Share Premium Reserve has increased by Rs. 830 million, Debenture Redemption Reserve by Rs. 108 million while Revaluation Reserve has reduced by Rs. 62 million. General Reserve too increased by Rs. 350 million.

Loan Profile

The borrowed funds of the Company increased to Rs. 15,833 million in FY 2008. Secured loans at Rs. 10,501 million comprise 66% of the total loans. Average cost of funds of the Company is over 9% per annum.

Capital Employed

The capital employed by the Company in the business increased by 54% from Rs. 17,680 million in FY 2007 to Rs. 27,305 million in FY 2008. The Company’s Net fixed assets as a proportion of total capital employed were at 67% at the end of the year.

Gross Block and Depreciation

The 11% increase in gross block of the Company can be attributed to the installation of new plant and machinery of Rs. 1,640 million during the year. The Company continued to upgrade its infrastructure and technology across all its manufacturing facilities. It provided depreciation of Rs. 864 million for FY 2008. Capital Work in progress including the two green field cement projects is Rs. 5,013 million.

33

Investments

Cumulative investments of the Company at Rs 6,138 million include investments of Rs 2,000 million towards acquisition of 21.7% shares of de-merged OCL India Ltd.

Sundry Debtors

The debtors of the Company increased to Rs. 1,051 million in FY 2008, of which only 4% amounting to Rs. 47 million are more than six months old.

Loans and Advances

Loans and Advances comprised 39% of the Company’s current assets. Loans and Advances made by the Company were up at Rs. 4,332 million in FY 2008 due to increase in advance income tax payments and increased MODVAT credit availability on the new projects.

Your Company’s human resources continue to be its biggest asset. Carrying on the legacy of almost seven decades, the Company has endeavoured to always be a people-centric organisation. In the recent years, the Company has shifted from a family operated setup to a professionally managed one. The Company’s talented pool of over 3300 executives and workers is leading its growth plans through capacity expansion projects and improved systems and processes.

The Company believes that its ability to attract, train, reward and retain its human resources will play a critical role in its future success. This challenge is being addressed through several structured initiatives. The Company has also instituted a Variable Pay Plan and Performance Management System for evaluation purposes.

As always, the Company continued to enjoy healthy and mutually respectful industrial relations this year with excellent support from its trade unions.

Keeping pace with the ambitious expansion program and to bring in standardization at all levels of operations through IT, the company decided to migrate its existing Business Application into industry standard SAP, ECC 6.0 suite. In the first phase, core business modules of Finance, Costing, Sales and Distribution, Materials Management, Production Planning and Quality module of the SAP suite are being implemented. During the year the Company implemented industry specific ERP for its sugar units.

The Company took a major step in moving out its Data Centre from its own location to a Level 3 Data Centre so as to provide the Company world class hosting and bandwidth on demand facilities. During the year it invested in third party multi-engine SPAM and virus protection services for improving its existing email services across all locations.

The Company continued with expansion of its fully capable multi-service Voice / Video / Data IT network for new locations, Ariyalur, Cuddapah and Hyderabad by seamlessly integrating them with existing domain. All the current locations country-wide enjoy same level of point to multi-point video conferencing facilities in addition to integrated data network.

Human Resources

Information Technology

34

The company is also imparting extensive training to its employees to ensure smooth implementation of SAP operations.

The company has a robust system for identification of key risks to the business, assessment of the possible impact and formulating strategies to mitigate such risks in an appropriate manner. Such risks could arise as a result of the industry, environment, regulation, nature of operations and the company’s growth plans into the future. Given below is a brief on the underlying risks.

Market and Competition Risk

The company is aware that cement and sugar are commodities and, therefore, inherently cyclical in nature. Fluctuations in the demand supply gap in the future can have significant impact on the realisations and on the competitive scenario. The Company’s objective therefore is to understand measure and monitor these risks regularly, and take appropriate measures to minimise their impact.

The Company has taken several initiatives to mitigate the market risks associated with its operations. The cement business, over the years, has continuously invested in creating strong brands which have led to significant increase in market share in relevant markets. This has helped the Company to command a premium on its products, even in relatively adverse market conditions. The company has further initiated a detailed micro-market analysis to foresee the demand supply situation in different markets.

In the sugar business, the newly commissioned industrial alcohol/ethanol manufacturing capability will allow the Company to realise new business opportunities and, to that extent, insulate it from the sugar cycle. Its power generation capacity of 79 MW is also generating revenues by selling excess power to Uttar Pradesh Power Corporation Limited.

Regulatory Risk

There is a fair amount of regulatory control exercised by the Government on both the businesses i.e. Cement and Sugar. The cement sector has seen changes in the excise duty structure during FY 2008. However, the company has been able to pass on the impact of such duty structure changes to the user to some extent and have been able to sustain the bottom-line impact.

The sugar business has seen some impact as a result of the cane prices administration and withdrawal of incentives available to new units set up in the State of Uttar Pradesh. However, the company has been able to sustain reasonable profitability through its diversification into the Power Cogeneration and Ethanol businesses which have opened new avenues for the company to derisk the cyclical nature of Sugar business. Given the situation of unprecedented rise in crude prices worldwide, the company sees a big opportunity here.

Risks and Concerns

35

Project Execution Risk

The company is expanding its production capacities with a view to cater to the growing demand of cement in domestic market. The company is currently executing two green-field cement projects one in Cuddapah (Andhra Pradesh) and second at Ariyalur (Tamil Nadu). Project execution is largely dependent on varied factors as timely delivery of capital equipments by suppliers, timely completion of work by contractors etc. Adherence to their envisaged commissioning date and allocated budget poses a challenge in light of rising steel prices, huge demand for capital goods engineering and scarcity of reputed and experienced contractors in the construction industry.

The company has set up a dedicated and experienced Project Management and Commercial Team supported by experienced advisors and consultants. Further, the company believes in partnering well with its vendors and contractors thereby enabling the company to get priority in executing projects on time and better costs. Further, there exists a strong review mechanism at each level to ensure timely support for completion of the projects.

Raw Material Risk

Access to raw materials like limestone and coal is critical to the cement business of the Company. Further, FY 2008 has seen unprecedented increase in coal and gypsum prices which has led to significant increase in the variable cost for the industry. The company has initiated a process to augment its limestone reserves to ensure uninterrupted supply of raw material to the plants and is also evaluating alternate sources of fuel. Further, the company is maintaining reasonable inventories and has sufficient order booking to ensure smooth operations.

Shortage of sugarcane poses similar risks for the sugar business. Sugarcane is a perishable item, and the Government controls its price as well as the area allotted to sugar units for growing cane. The Company has engaged proactively with sugarcane farmers and has been able to significantly augment the area under cane for the new sugar units. Further, significant work is being done by the business to increase the yield per hectare of cane thereby making it lucrative for the farmers to grow cane instead of other options like wheat and paddy.

36

Currency risk

The Company’s exposure to currency risk arises out of the import of coal for its cement plants and project equipment imports for its Greenfield projects. The Company continuously monitors exchange rate movements and hedges major transactions in foreign currency by taking forward contracts in the currency market, as considered appropriate.

The Company has robust and adequate internal audit and control systems. The company has a strong and robust internal audit function and has a co-sourcing arrangement with reputed audit firms including the Big Fours. Every unit is subject to a quarterly internal audit as per the Audit plan approved by the Audit Committee of the Board.

The internal audits are conducted with a view to periodically evaluate adequacy of internal control systems in all spheres of the company’s operations namely financial, operations, compliance and projects. The audit plan is constantly reviewed to evaluate the risks posed by new ventures, polices and the environment and accordingly modified to provide reasonable assurance to the management on key risk areas regarding the effectiveness and efficiency of operations, reliability of financial reports, and compliance to applicable laws and regulations. There also exists a robust mechanism to ensure timely identification and reporting of fraud and negligence within the Company. The Internal Audit Head reports independently to the Audit Committee of the Board which is headed by a Non-Executive Director thereby ensuring fair amount of independence of the function and transparency of the process. The Committee meets every quarter to review the progress of the internal audit initiatives, significant audit observations and the action plans. Details on the composition and functions of the Audit Committee can be found in the chapter on Corporate Governance of the Annual Report.

Certain statements in this management discussion and analysis describing the Company’s objectives, projections, estimates and expectations may be ‘forward looking statements’ within the meaning of applicable laws and regulations. Forward looking statements are identified in this report, by using the words ‘anticipates’, ‘believes’, ‘expects’, ‘intends’ and similar expressions in such statements.

Although we believe our expectations are based on reasonable assumptions, these forward-looking statements may be influenced by numerous risks and uncertainties that could cause actual outcomes and results to be materially different from those expressed or implied. Some of these risks and uncertainties have been discussed in the section on ‘risks and concerns’. The Company takes no responsibility for any consequence of decisions made based on such statements and holds no obligation to update these in the future.

Internal Control Systems

Cautionary Statement

37

The Directors have pleasure in submitting the Annual Report and Audited Statements of Account of the Company for the styear ended 31 March 2008.

(Rs. Million)

2007-08 2006-07

Net Sales Turnover 14807 9865

Profit before interest, depreciation and tax (EBITDA) 6334 4054Less: Interest 1129 540

Profit before depreciation and tax (PBDT) 5205 3514Less: Depreciation 864 551

Profit before tax (PBT) 4341 2963Provision for current tax (net of MAT credit) 513 100Provision for deferred tax 337 563Fringe Benefit tax 19 11

Profit after tax (PAT) 3472 2289Add:

(i) Surplus brought forward 3482 1755 (ii) Transfer from Debenture Redemption Reserve - 7 (iii) Transfer from Reserve for Bad & Doubtful Debts - 17

Profit available for appropriation 6954 4068

APPROPRIATIONS:General Reserve 350 300Debenture Redemption Reserve 108 139Interim/Proposed Dividend 323 128Dividend Distribution tax thereon 55 19Balance carried forward 6118 3482

6954 4068

Your Directors had disbursed an interim dividend of 125 per cent amounting to Rs. 2.50 per equity share of face value of Rs.2/- each in February 2008. In addition to the interim dividend, your Directors have decided to recommend a final dividend of 75% amounting to Re. 1.50 per equity share of the face value of Rs. 2/- each, thus making the total dividend payout for the year Rs. 4/- per equity share on increased capital as against Rs. 3/- per share last year.

Your Directors exercised the call option in respect of the detachable tradeable warrants issued by the Company in September, 2001 along with the 6% Non-Convertible Secured Redeemable Debentures of Rs. 10/- each issued to the Shareholders on a Rights basis. Out of the 76,51,621 outstanding warrants, warrant holders holding 76,22,990 warrants opted for conversion of the warrants and were allotted 3,81,14,950 Equity Shares of Rs. 2/- each, which have been listed on the Stock Exchanges.

As a gesture of goodwill, your Directors have decided to permit the remaining warrant holders to opt for conversion of the outstanding warrants into equity shares of the Company and have addressed letters to each one of them to apply for the conversion of warrants held by them.

Please refer to the chapter on Management Discussion and Analysis for a detailed analysis of the performance of the Company during 2007-08. In addition, working results for key businesses have been provided as an annexure to this report (Annexure - A).

FINANCIAL RESULTS

DIVIDEND

SHARE CAPITAL

OPERATIONS AND BUSINESS PERFORMANCE

Directors’ ReportFor The Year Ended 31st March, 2008

38

CORPORATE GOVERNANCE

LISTING OF SHARES

INDUSTRIAL RELATIONS

EMPLOYEES' PARTICULARS

ENERGY CONSERVATION, TECHNOLOGY ABSORPTION AND FOREIGN EXCHANGE TRANSACTIONS

SUBSIDIARIES

FIXED DEPOSITS

DIRECTORS

The Company's corporate governance practices have been detailed in a separate chapter in this document. The Auditors certificate on the compliance of Corporate Governance Code embodied in Clause 49 of the Listing Agreement is attached as annexure and forms part of this Report.

thIn terms of the resolution passed by the Shareholders in the Annual General Meeting held on 27 September 2003, the Company applied for delisting of its securities from dealings on the Calcutta Stock Exchange. The Company's shares have since been delisted from the Calcutta Stock Exchange. The Company's shares continue to be listed on the Madras Stock Exchange, National Stock Exchange and Bombay Stock Exchange.

The industrial relations during the year under review remained harmonious and cordial. The Directors wish to place on record their appreciation for the excellent cooperation received from all employees at various units of the Company.

The statement giving particulars of employees who were in receipt of remuneration in excess of the limits prescribed under Section 217(2A) of the Companies Act, 1956 read with the Rules and Notifications made thereunder, is annexed. However, in terms of Section 219(1)(b)(iv) of the Companies Act, 1956 the Report and Accounts are being sent to the Shareholders excluding the aforesaid Annexure. Any Shareholder interested in obtaining copy of the same may write to the Company Secretary at the Registered Office.

A statement giving details of Conservation of Energy, Technology Absorption and Foreign Exchange transactions, in accordance with the Companies (Disclosure of particulars in the Report of the Board of Directors) Rules, 1988, forms a part of this report as Annexure - B.

Dalmia Cement (Meghalaya) Limited, a subsidiary of your Company, got amalgamated with OCL India Limited pursuant to the orders of the Gauhati High Court vide order dated 15-10-2007.

The Company has obtained exemption from the Central Government under Section 212(8) of the Companies Act, 1956, from attaching the Annual Reports of its subsidiaries vide letter No. 47/125/2008-CL-III dated 18-3-2008.

Accordingly, the Directors' Report and audited accounts of the Companies Subsidiaries, Kanika Investment Limited, Ishita Properties Limited, Shri Rangam Properties Limited, Geetee Estates Limited, D.I. Properties Limited, Avnija Properties Limited, Hemshila Properties Limited, Himshikhar Investment Limited, Arjuna Brokers & Minerals Limited, Shri Radha Krishna Brokers & Holdings Limited, Shri Rangam Brokers & Holdings Limited, Dalmia Minerals & Properties Limited, Seeta Estates & Brokers Limited, Sri Kesava Mines & Minerals Limited, Sri Shanmugha Mines & Minerals Limited, Sri Subramanya Mines & Minerals Limited, Sri Swaminatha Mines & Minerals Limited, Sri Madhava Minerals & Properties Limited, Sri Dhandauthapani Mines and Minerals Limited, Eswar Cements Private Limited, Sri Madhusudana Mines and Properties Limited, Sri Trivikrama Mines and Properties Limited, Dalmia Sugar Ventures Limited and Dalmia

stCement Ventures Limited for the year ended 31 March 2008 are not being enclosed with this annual report. Any Member desiring to inspect the detailed Annual Reports of any of the aforementioned subsidiaries may inspect the same at the Head Office of the Company and that of the subsidiaries concerned. In event a Member desires to obtain a copy of the Annual Report of any of the aforementioned subsidiaries, he may write to the Registered Office of the Company specifying the name of the subsidiary whose annual report is required. The Company shall supply a copy of such Annual Report to such Member.

stThe total amount of deposits remaining due for payment and not claimed by the depositors as on 31 March 2008 was Rs. 9.30 lakhs in respect of 14 depositors, out of which deposit amounting to Rs. 0.61 lakhs in respect of 1 depositor has since been paid.

Shri Jai H. Dalmia, was appointed as Vice-Chairman, of the Company effective 1-4-2007 in terms of the Resolution which was confirmed by the Shareholders by means of a Postal Ballot, the results of which were declared in March, 2007.

The following Directors retire by rotation at the ensuing Annual General Meeting:.

1. Shri M.H. Dalmia;2. Shri N. Khaitan; and3. Shri J.S. Baijal

39

Shri N. Gopalaswamy ceased to hold office as a Whole-time Director of the Company on 31-7-2007. Considering the service rendered by Shri Gopalaswamy during his tenure as a Whole-time Director, the Board co-opted him as an

stAdditional Director effective 1 August, 2007. The Company has received a Notice from a Shareholder as required under the provisions of Section 257 of the Companies Act, 1956 to the effect that he intends to propose the name of Shri N. Gopalaswamy to be appointed as a Director of the Company liable to retire by rotation.

stShri T. Venkatesan, was appointed as a Whole-time Director effective 1 November, 2007. The appointment of thShri T. Venkatesan was confirmed by the Shareholders in the Extra-ordinary General Meeting held on 18 January, 2008.

Shareholdings in the Company by its Directors as at 31-3-2008, are as under:

Name of the Director No. of Shares of each held

Shri N. Khaitan 6,665

Shri Jai H. Dalmia 16,35,010

Shri Y.H. Dalmia 6,02,380

Shri Gautam Dalmia 6,77,290

Shri Puneet Dalmia 7,42,055

Shri N. Gopalaswamy 6,665

Shri T. Venkatesan 1,800

OCL India Limited has become an associate of the Company upon the amalgamation of the Company's subsidiary, Dalmia Cement (Meghalaya) Limited with OCL India Limited effective 1-7-2007, and consequent allotment of shares by OCL India Limited to the extent of 21.71% of its issued and paid-up capital.

In compliance with the Accounting Standard 21 on Consolidated Financial Statements, this Annual Report also includes Consolidated Financial Statements for the financial year 2007-08.

As required under clause 49 of the Listing Agreement, the CEO/CFO's Report on the Accounts is attached.

In terms of the provisions of Section 217(2AA) of the Companies Act, 1956 your Directors declare that:

a) in the preparation of the annual accounts, the applicable Accounting Standards have been followed and no departures have been made there from;

b) the Directors had selected such accounting policies and applied them consistently and made judgements and estimates that are reasonable and prudent so as to give a true and fair view of the state of affairs of the Company at the end of the financial year and of the profit of the Company for that period;

c) the Directors had taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities; and

d) the Directors had prepared the annual accounts on a going concern basis.

M/s. S.S. Kothari Mehta & Co., Chartered Accountants, Auditors of the Company retire at the conclusion of the ensuing Annual General Meeting and are eligible for re-appointment. As required under Section 224 of the Companies Act, 1956, the Company has obtained from them a certificate to the effect that their re-appointment, if made, would be in conformity with the limits prescribed in the said Section.

For and on behalf of the Board

Place : New DelhindDated : 22 May, 2008

CHAIRMAN

Rs. 2/-

CONSOLIDATED FINANCIAL STATEMENTS

CEO/CFO REPORT ON ACCOUNTS

DIRECTORS RESPONSIBILITY STATEMENT

AUDITORS

40

ANNEXURE - A

2007-08 2006-07 2005-06

CEMENT DIVISION ('000 MT)Clinker Production 2444 2055 1262Cement Production 3294 2737 1569Cement Sales and Self Consumption 3265 2713 1577