Embed Size (px)

DESCRIPTION

Â

Citation preview

Today investors are presented with a number of surprisingevents that many thought impossible. Oil dropped from over$107 a barrel in June of 2014 to less than $50 a barrel today.Further, interest rates continue to drop with the 10-yearTreasury yield approaching 2% as we write this. And mostsurprising, the 30-year Treasury bond now yields a paltry 2.5%.

How low can rates and oil go? The key to remember is mosttrends last much longer than most think possible. The drop inoil prices is very logical – we have increased productionglobally via new technologies. So supply and demand is atplay here. Further, it seems like the big run-up in oil for aboutten years was simply a temporary price spike. The cause ofthis change: innovation and new technology in drillingefficiency and capabilities. Further, we are diversifying away from tradition oil and gasthrough conservation and alternative energy like solar, wind and electric vehicles. The keymessage: we are in a world of rapid innovation deployment – much of this innovation isrooted in our computational ability from computer power. Expect this type of progress inmany industries. Healthcare, transportation, energy, industrial companies and more are allexperiencing an explosion of new technologies and innovation. Get used to change – it willcome faster with more impact to many more industries over the coming decade.

So, how low will interest rates go? Could they drop even lower in the coming year? Yes – ifinflation is disappearing, the likelihood of the yields on bonds is disappearing too. Of course,there will be a reversal; however, rates could stay low a great deal longer than many expect.Today the German 10-year government bond trades at .45% and yields in Japan have all butdisappeared. Could yield in the United States continue to decline? Yes. Until the FederalReserve ends its accommodative period and until we see a real pick-up in inflation, then it isunlikely we will see interest rates rise much and they could even trade lower. With oildropping, we expect to see the CPI Index continue to trend lower and remain very bondfriendly. When will the interest rate bubble burst? No one knows for sure. We have to be onthe lookout for indications of a change – because when the change comes it could be rapidand dramatic.We are enthusiastic about the prospects for the United States economy. We areliving in a period of great prosperity and are the beneficiaries of incredible entrepreneurialinnovation and wealth creation. We know it will not be a smooth ride for all of 2015; however,we believe it will be a year of progress.

We are pleased to continue serving as stewards ofyour family’s wealth. Thank you for yourcontinued confidence in our team.

Best wishes,

Robert T. LuttsPresident and Chief Investment Officer

QUARtERLY REVIEWFOURtH QUARtER 2014

Cabot Wealth Management, Inc.216 Essex Street

Salem, MA 01970978-745-9233 / 800-888-6468

eCabot.com

Log on to eCabot.com

for our latest articles, interviews and reports. Email

if you would like to receive Cabot updates.

eCabot.com

In tHIS ISSUE

1PRESIdEnt’S MESSAGE

2015 Outlook

2-3WEALtH

MAnAGEMEnt

Charitable Giving

2015 Tax Update

4InVEStMEnt

MAnAGEMEnt

Is it Time to Bring

Your Money Home?

5CLIEnt SERVICES

Staying Connected

6MEEt tHE tEAM

Nick Burwell, Fixed-Income

Interns & Opportunities

7CABOt In tHE

COMMUnItY

Lutts Appointed

to Board of Trustees

Wilson Accepts

Volunteer Award

8

AROUnd CABOt

Cabot Kids Color Our Hearts

Save the Date

GEt COnnECtEd

Follow us@cabotwealthmgmt

for our latest updates,articles, and media clips.

Follow our company or join our group

Wealth Management

with Cabot

216 ESSEX STREET, P.O. BOX 150, SALEM, MA 01970 / 978-745-9233 / 800-888-6468

This quarterly newsletter is intended for information purposes only. Articles, graphs, charts and discussions should not be construed as specific investment advice. Individuals should personally consult with a financial professional to review their own specific situation in light of any information discussed here. Cabot is not under any obligation to update the information and while every attempt is made to insure that it is accurate,we are not responsible for misstatements or inaccuracies. This quarterly is intended for dissemination in the United States and is not intended forcirculation elsewhere. It is important to note that any performance reporting or implied performance is not indicative of future results. Investmentsare not insured and may lose value. Asset allocation and diversification does not protect against loss. For complete disclosures, please contact usat (800) 888-6468 or [email protected] to receive a copy of our Form ADV and privacy statement.

Like us on Facebookto see what’s happening

around Cabot.

January 2015

Friday, September 25, 2015

Join us for Cabot’s 26th Annual Wealth Management Conference at the HawthorneHotel in historic downtown Salem, Massachusetts. Presentations will focus on currenteconomic events and relevant wealth management topics. Attendees have the opportunityto have their questions and concerns addressed directly by members of the Cabot Team.

Cabot’s kids had the opportunityto color our hearts during our2nd Annual Holiday CardContest in November. Literally.Children of our staff submittedholiday-inspired works of“heart” to warm the hearts ofclients and colleagues during theholiday season. Winning heartsfeatured came from CarlottaGasparello (age 6), AbbyStevens (age 9), Cooper andParker Wassung (ages 6 and 8).In addition, all of our pint-sizedparticipants received acertificate of recognition, acoloring book, and had theirartwork displayed in Cabot’sCaboteria breakroom. Visit ourFacebook page to see all of theirworks of “heart”.

For more information or to RSVP :

Call (978) 745-9233 or email [email protected].

Mark your Calendar!

Autumn in New England!

In lieu of gifts this holiday season,Cabot Wealth Management has contributedto causes close to our homes and our hearts.

CEO Corner:

Rob Lutts is now in the midst of putting

on paper the lessons learned and

techniques he uses to lead the

investment team at Cabot. He is

writing a book which will

revolve around the key

factors in identifying

successful businesses,

and hence, winning

investments.

Around Cabot

Abby Stevens, 9, proudly displays

her certificate for submitting her

polka-dot inspired heart.

Cabot Kids Color Our Hearts for the Holidays

Establishing a high level plan for charitable giving can be very complex.

High-net-worth investors have many options when it comes to charitable giving. Here

are three vehicles our clients use regularly:

1. donor Advised Fund (dAF)A DAF gives the grantor the benefit of a charitable deduction in the year it is made. Sincethe funding vehicle itself will qualify as a 501(c)(3) charitable entity, any stock sales donein the portfolio are tax free. As a result, many investors in DAFs choose to make theircontributions with stock that has a low cost basis. The proceeds of the stock sale areprofessionally managed and distributions are made to charities of your choice.

2. Private Charitable Foundation (PCF)A Private Charitable Foundation is an entity established by families solely for the purposesof charitable giving. A PCF will typically develop a mission statement to guide the purposeand long-term charitable goals of the organization. The management of the foundation isoverseen by appointed officers and a board of directors (in many cases, family members).These individuals are tasked with managing the affairs of the foundation, including whengrants are made and how the funds in the foundation are to be invested and managed by aprofessional advisor. A PCF is required to distribute at least 5% of its assets each year forcharitable purposes.

3. Charitable trusts (CRt/CLt)Charitable Trusts offer a great option for investors to fund either current or future charitablegrants. A Charitable Remainder Trust (CRT) is an arrangement in which a donor providesfor a charitable bequest of assets in the future while still retaining an income stream fromthose assets while they are alive. The donor gets the benefit of a tax deduction in the yearthey fund the trust based on the projected “remainder interest” that goes to charity.

A Charitable Lead Trust (CLT) works in the opposite way of a CRT. In a CLT arrangement,a charity receives yearly distributions from the trust while the donor is alive (or for theterm dictated by the trust). When the donor passes away, their heirs receive whatever isleft.

As with other charitable arrangements, sale of stock within charitable trusts is not subjectto capital gains tax which makes these a great vehicle to fund with stock holdings that havea low cost basis. As with the other entities, the portfolio can be professionally managedand overseen by the grantor/donor.

As you can imagine, I’ve only scratched the surface within this article. I would

encourage anyone interested in learning more about charitable giving to contact your

attorney, accountant or your Cabot advisor for a more detailed explanation of your

options.

WEALtH

MAnAGEMEnt

CABOt WEALtH MAnAGEMEnt, InC. CABOt WEALtH MAnAGEMEnt, InC.

Cabot in the Community Charitable Giving AROUnd

CABOt

Greg Stevens, CFP ®, CRPS ®

Principal, Senior Wealth Advisor

Mikki Wilson was recognized at Salem StateUniversity’s 2014 Alumni Weekend Jazz brunch for herwork on the Alumni Association Board of Directors’civic engagement committee, as well as for her effortswith the Northeast Arc Adopt-a-Home program. In2012, Salem State’s Alumni Association teamed up withNortheast Arc, adopting a home that houses fourindividuals with disabilities who are learning to liveindependent lives. Through the alumni association’scivic engagement committee, a strong relationship hasformed between Salem State’s alumni and bothresidents and support staff. For her wonderfulcontributions to these endeavors, Mikki was presentedwith the George Ellison Sr. Volunteer of the Year Award.

Rob Lutts was appointed the newest member of theSalem State University Board of Trustees by formergovernor Deval Patrick on November 24. Lutts bringsover 30 years of investment management experience tothe board, and according to university president Dr.Patricia Maguire Meservey, “will be an important assetto Salem State in a variety of important and very criticalareas.”

“Rob’s interest in—and passion for—the university,”she continued, “is well known. His long anddistinguished service as a member and past presidentof the Salem State Foundation has given him a deepfamiliarity with the operations of a robust and growinguniversity as well as many of the challenges we face. Iam delighted to welcome him to our board of trustees.”

Commenting on his appointment, Rob noted that he is “thrilled to join the trustee leadership at Salem State University.This vitally important institution needs to be nurtured and cultivated so that it continues to support the excellent educationopportunities in our backyard.”

Salem State University, established in 1854, is a comprehensive, public institution of higher learning located approximately15 miles north of Boston, Massachusetts. The university enrolls 10,000 undergraduate and graduate students representing44 states and 61 nations, and is one of the largest state university in the Commonwealth of Massachusetts.

Rob Lutts named to Salem State University Board of trustees

Mikki Wilson Presented With Volunteer of the Year Award

Mikki proudly accepts her award from university

president Dr. Patricia Maguire Meservey and Dr. Erik

Champy, past president of SSU’s Alumni Association.

President Dr. Patricia Maguire Meservey and

Rob Lutts stand for a photo op inside SSU’s

Bertolon School of Business.

CABOt WEALtH MAnAGEMEnt, InC. CABOt WEALtH MAnAGEMEnt, InC.

2015 tax UpdateMeet the team WEALtH

MAnAGEMEnt

Tom Vautin, CPA, CFA, CFP ®

Senior Financial Planner

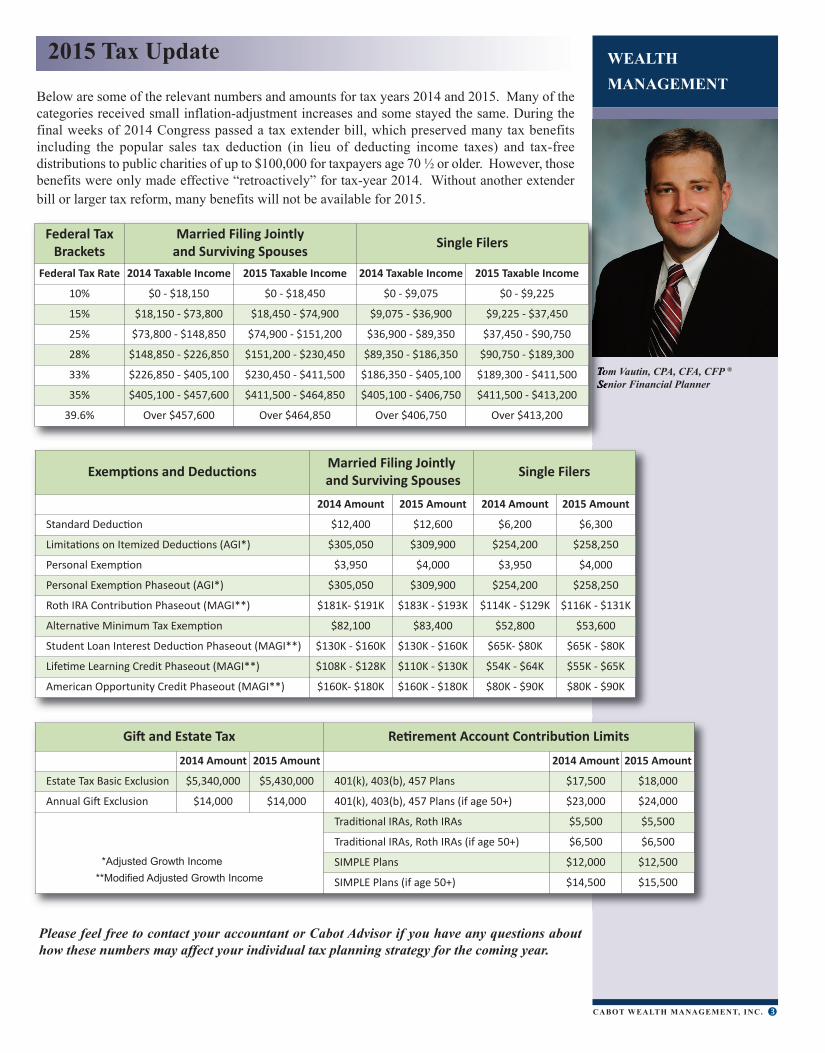

AROUnd

CABOtBelow are some of the relevant numbers and amounts for tax years 2014 and 2015. Many of thecategories received small inflation-adjustment increases and some stayed the same. During thefinal weeks of 2014 Congress passed a tax extender bill, which preserved many tax benefitsincluding the popular sales tax deduction (in lieu of deducting income taxes) and tax-freedistributions to public charities of up to $100,000 for taxpayers age 70 ½ or older. However, thosebenefits were only made effective “retroactively” for tax-year 2014. Without another extender

bill or larger tax reform, many benefits will not be available for 2015.

Cabot is proud to provide hands-on and interactive learning experiences for graduating studentsin our community. By partnering with colleges and universities, we are able to offer internshipopportunities during the fall and spring semesters so that these young adults can build their re-sume, network and gain relevant work experience within their area of study. Our goal is to providethem with an experience that will take them far beyond the classroom and will form the foundation

for a lasting career.

Alexander Aparo is an accounting intern and senior at SalemState University. Majoring in both Accounting and PoliticalScience, he is excited to graduate with Salem State’s Class of2015. While interning at Cabot, Alex has become familiar withthe use of tax software and filling in government tax formscorrectly. He has put theory into practice by gaining real worldtax experience with guidance from Steve Davis. Alex hasalready secured a job after his graduation in May at Johnson,O’Connor, Feron & Carucci, LLP, a public accounting firm in

Wakefield, where he will serve as a staff accountant working with audits and tax

accounts.

Parker dodd is a portfolio management intern and a seniorcurrently majoring in finance and economics at Salem StateUniversity. Taken under the wings of portfolio managers DennisWassung and Craig Goryl, Parker has learned the selectionprocess for securities and gained a broader view on gatheringresearch information. Not sure of his plans after graduating inMay 2015, Parker intends to pursue his Series 7, 63 and 66licenses.

nick Burwell Joins Portfolio Management team

We are pleased to announce the addition of nick Burwell toCabot’s portfolio management team. Nick will be responsible formanaging Cabot’s fixed-income portfolios and he is currently aCFA Level III candidate. He previously worked for ICC CapitalManagement in Orlando, Florida, an institutional firm with over$500 million in assets under management.

Nick obtained his undergraduate degree in businessadministration from Stetson University in Florida and nowcurrently resides in Watertown, Massachusetts. He has a strongunderstanding of the asset management industry, passion forfinancial markets and demonstrated ability to master complex concepts and deliver highlevel performance. Welcome to the team Nick!

Mikki L. Wilson,

Director of Marketing

and Business Development

Please feel free to contact your accountant or Cabot Advisor if you have any questions about

how these numbers may affect your individual tax planning strategy for the coming year.

Federal Tax

Brackets

Married Filing Jointly

and Surviving SpousesSingle Filers

Federal Tax Rate 2014 Taxable Income 2015 Taxable Income 2014 Taxable Income 2015 Taxable Income

10% $0 - $18,150 $0 - $18,450 $0 - $9,075 $0 - $9,225

15% $18,150 - $73,800 $18,450 - $74,900 $9,075 - $36,900 $9,225 - $37,450

25% $73,800 - $148,850 $74,900 - $151,200 $36,900 - $89,350 $37,450 - $90,750

28% $148,850 - $226,850 $151,200 - $230,450 $89,350 - $186,350 $90,750 - $189,300

33% $226,850 - $405,100 $230,450 - $411,500 $186,350 - $405,100 $189,300 - $411,500

35% $405,100 - $457,600 $411,500 - $464,850 $405,100 - $406,750 $411,500 - $413,200

39.6% Over $457,600 Over $464,850 Over $406,750 Over $413,200

Exemptions and DeductionsMarried Filing Jointly

and Surviving SpousesSingle Filers

2014 Amount 2015 Amount 2014 Amount 2015 Amount

Standard Deduction $12,400 $12,600 $6,200 $6,300

Limitations on Itemized Deductions (AGI*) $305,050 $309,900 $254,200 $258,250

Personal Exemption $3,950 $4,000 $3,950 $4,000

Personal Exemption Phaseout (AGI*) $305,050 $309,900 $254,200 $258,250

Roth IRA Contribution Phaseout (MAGI**) $181K- $191K $183K - $193K $114K - $129K $116K - $131K

Alternative Minimum Tax Exemption $82,100 $83,400 $52,800 $53,600

Student Loan Interest Deduction Phaseout (MAGI**) $130K - $160K $130K - $160K $65K- $80K $65K - $80K

Lifetime Learning Credit Phaseout (MAGI**) $108K - $128K $110K - $130K $54K - $64K $55K - $65K

American Opportunity Credit Phaseout (MAGI**) $160K- $180K $160K - $180K $80K - $90K $80K - $90K

Gift and Estate Tax Retirement Account Contribution Limits

2014 Amount 2015 Amount 2014 Amount 2015 Amount

Estate Tax Basic Exclusion $5,340,000 $5,430,000 401(k), 403(b), 457 Plans $17,500 $18,000

Annual Gift Exclusion $14,000 $14,000 401(k), 403(b), 457 Plans (if age 50+) $23,000 $24,000

Traditional IRAs, Roth IRAs $5,500 $5,500

Traditional IRAs, Roth IRAs (if age 50+) $6,500 $6,500

SIMPLE Plans $12,000 $12,500

SIMPLE Plans (if age 50+) $14,500 $15,500

*Adjusted Growth Income

**Modified Adjusted Growth Income

Interns & Opportunities

InVEStMEnt

MAnAGEMEnt

CABOt WEALtH MAnAGEMEnt, InC. CABOt WEALtH MAnAGEMEnt, InC.

CLIEnt

SERVICES

time to Bring Your Money Home? Staying Connected

Natalie Rubel

Client Services Specialist

At Cabot we pride ourselves in providing exceptional client service while protectingnonpublic personal information. We strongly believe that our relationship with ourclients is our greatest asset. In order to maintain our high level of service and stayconnected with our clients, it is important that we maintain accurate, current recordsof client contact information.

Please help us by reviewing the name, address, telephone, email and other informationyou see on your account statements and correspondence from Cabot. If there are anychanges or corrections that need to be made, please contact us at (800) 888-6468.Doing so will allow us to reach you regarding important account and/or marketinformation.

In addition, we strongly encourage you to provide a preferred email address. This willprovide you with online access to account information and is key to using certain toolsthat will make it easier to transact service requests. It will also allow you to receiveCabot’s quarterly newsletter right to your inbox as well as any notifications forupcoming events and industry updates.

Arguably the most important reason to keep your contact information current is fraudprevention. If we suspect unauthorized access to your account, we need to contactyou. It is imperative that we have your most recent phone numbers and email address.

You’ve entrusted us with your personal information, and we use it wisely as weperform the tasks you request. Simply put, we do not share your personal informationwith anyone, except as authorized by you. Our employees are trained on handlingprivate financial information and keeping your information private. We use firewallsand encryption technology to protect personal information on our computer systems.

Foreign stock indices have trailed US stocks for 3 of the last 4 years. In 2014, foreign stocks (bothemerging and developed markets) lost money while US large caps achieved double-digit returns.Headlines were equally lopsided: The US created almost 3 million jobs in 2014 and posted 5%GDP growth in the fourth quarter. Meanwhile Europe deflated, Russia crumbled, Africa battledEbola, Japan seesawed, and China slowed dramatically.

So, is it time to bring all your money home? We don’t think so. There are some good argumentsthat the pendulum has swung too far, and that foreign markets are poised to outperform the USin 2015. First, what happened in 2014? In the US a true recovery took hold, allowing our centralbank to stop some of the more extraordinary measures it had taken to stimulate growth. But outsideour borders, economic growth disappointed investors. As stocks adjusted to these surprises, the

US market dramatically outperformed.

Why do we like foreign stocks today?

History suggests the gap between US stocks and the rest of the world has grown too wide.

The performance gap between the US and foreign markets is now the widest in 18 years. Thelast 4 times the disparity between US and foreign stocks was this wide (going back to 1970),foreign stocks beat the S&P by an average of 14% the next year. Investors need to rememberthat modern global economies are linked. Either the rest of the world will catch up to ourrecovery, or drag us back into the mud.

the herd is running to US large caps. Watch CNBC for a day and see if you can find anystrategists recommending foreign stocks. The US is almost universally considered to be thebest place to invest for both safety and growth. Money flows reflect this. The top three ETFsfor inflows in 2014 all mimic the S&P 500 index. Following the crowd is rarely a successfulinvestment strategy.

There are also longer-term benefits to owning stocks. (At Cabot we use a combination of foreignshares, US-traded stocks of foreign companies, ETFs and mutual funds to invest globally.)

Geographic diversification lowers risk. This is a counter-intuitive conclusion for manyinvestors. Often one market is up when another is down. So having money outside the USlowers the volatility (that is, risk) of your overall portfolio. Every investor loves return. Riskcontrols go unappreciated in a bull market, but are a vital component of wealth management.

Geographic diversification enhances returns. The past few years nothwithstanding, thereare powerful trends that favor foreign markets. Emerging markets offer better economic growthfrom the powerful effect of a rapidly growing middle class. Developed markets like Japan andEurope, following our own Fed’s recovery playbook, will see a cyclical recovery. Bothemerging and developed stocks are priced at a discount to US peers. US stocks are among themost expensive in the world.

Craig E. Goryl, CFA®

Portfolio Manager

Staying connected and secure is a partnership. Please help us by advising

us of any changes to your contact information. Contact us toll-free at

(800) 888-6468 to speak with your Client Services Specialist.

Visit:http://ecabot.com/?p=1105

to see a larger image of this chart.

the Importance of Updating Your Contact Information

InVEStMEnt

MAnAGEMEnt

CABOt WEALtH MAnAGEMEnt, InC. CABOt WEALtH MAnAGEMEnt, InC.

CLIEnt

SERVICES

time to Bring Your Money Home? Staying Connected

Natalie Rubel

Client Services Specialist

At Cabot we pride ourselves in providing exceptional client service while protectingnonpublic personal information. We strongly believe that our relationship with ourclients is our greatest asset. In order to maintain our high level of service and stayconnected with our clients, it is important that we maintain accurate, current recordsof client contact information.

Please help us by reviewing the name, address, telephone, email and other informationyou see on your account statements and correspondence from Cabot. If there are anychanges or corrections that need to be made, please contact us at (800) 888-6468.Doing so will allow us to reach you regarding important account and/or marketinformation.

In addition, we strongly encourage you to provide a preferred email address. This willprovide you with online access to account information and is key to using certain toolsthat will make it easier to transact service requests. It will also allow you to receiveCabot’s quarterly newsletter right to your inbox as well as any notifications forupcoming events and industry updates.

Arguably the most important reason to keep your contact information current is fraudprevention. If we suspect unauthorized access to your account, we need to contactyou. It is imperative that we have your most recent phone numbers and email address.

You’ve entrusted us with your personal information, and we use it wisely as weperform the tasks you request. Simply put, we do not share your personal informationwith anyone, except as authorized by you. Our employees are trained on handlingprivate financial information and keeping your information private. We use firewallsand encryption technology to protect personal information on our computer systems.

Foreign stock indices have trailed US stocks for 3 of the last 4 years. In 2014, foreign stocks (bothemerging and developed markets) lost money while US large caps achieved double-digit returns.Headlines were equally lopsided: The US created almost 3 million jobs in 2014 and posted 5%GDP growth in the fourth quarter. Meanwhile Europe deflated, Russia crumbled, Africa battledEbola, Japan seesawed, and China slowed dramatically.

So, is it time to bring all your money home? We don’t think so. There are some good argumentsthat the pendulum has swung too far, and that foreign markets are poised to outperform the USin 2015. First, what happened in 2014? In the US a true recovery took hold, allowing our centralbank to stop some of the more extraordinary measures it had taken to stimulate growth. But outsideour borders, economic growth disappointed investors. As stocks adjusted to these surprises, the

US market dramatically outperformed.

Why do we like foreign stocks today?

History suggests the gap between US stocks and the rest of the world has grown too wide.

The performance gap between the US and foreign markets is now the widest in 18 years. Thelast 4 times the disparity between US and foreign stocks was this wide (going back to 1970),foreign stocks beat the S&P by an average of 14% the next year. Investors need to rememberthat modern global economies are linked. Either the rest of the world will catch up to ourrecovery, or drag us back into the mud.

the herd is running to US large caps. Watch CNBC for a day and see if you can find anystrategists recommending foreign stocks. The US is almost universally considered to be thebest place to invest for both safety and growth. Money flows reflect this. The top three ETFsfor inflows in 2014 all mimic the S&P 500 index. Following the crowd is rarely a successfulinvestment strategy.

There are also longer-term benefits to owning stocks. (At Cabot we use a combination of foreignshares, US-traded stocks of foreign companies, ETFs and mutual funds to invest globally.)

Geographic diversification lowers risk. This is a counter-intuitive conclusion for manyinvestors. Often one market is up when another is down. So having money outside the USlowers the volatility (that is, risk) of your overall portfolio. Every investor loves return. Riskcontrols go unappreciated in a bull market, but are a vital component of wealth management.

Geographic diversification enhances returns. The past few years nothwithstanding, thereare powerful trends that favor foreign markets. Emerging markets offer better economic growthfrom the powerful effect of a rapidly growing middle class. Developed markets like Japan andEurope, following our own Fed’s recovery playbook, will see a cyclical recovery. Bothemerging and developed stocks are priced at a discount to US peers. US stocks are among themost expensive in the world.

Craig E. Goryl, CFA®

Portfolio Manager

Staying connected and secure is a partnership. Please help us by advising

us of any changes to your contact information. Contact us toll-free at

(800) 888-6468 to speak with your Client Services Specialist.

Visit:http://ecabot.com/?p=1105

to see a larger image of this chart.

the Importance of Updating Your Contact Information

CABOt WEALtH MAnAGEMEnt, InC. CABOt WEALtH MAnAGEMEnt, InC.

2015 tax UpdateMeet the team WEALtH

MAnAGEMEnt

Tom Vautin, CPA, CFA, CFP ®

Senior Financial Planner

AROUnd

CABOtBelow are some of the relevant numbers and amounts for tax years 2014 and 2015. Many of thecategories received small inflation-adjustment increases and some stayed the same. During thefinal weeks of 2014 Congress passed a tax extender bill, which preserved many tax benefitsincluding the popular sales tax deduction (in lieu of deducting income taxes) and tax-freedistributions to public charities of up to $100,000 for taxpayers age 70 ½ or older. However, thosebenefits were only made effective “retroactively” for tax-year 2014. Without another extender

bill or larger tax reform, many benefits will not be available for 2015.

Cabot is proud to provide hands-on and interactive learning experiences for graduating studentsin our community. By partnering with colleges and universities, we are able to offer internshipopportunities during the fall and spring semesters so that these young adults can build their re-sume, network and gain relevant work experience within their area of study. Our goal is to providethem with an experience that will take them far beyond the classroom and will form the foundation

for a lasting career.

Alexander Aparo is an accounting intern and senior at SalemState University. Majoring in both Accounting and PoliticalScience, he is excited to graduate with Salem State’s Class of2015. While interning at Cabot, Alex has become familiar withthe use of tax software and filling in government tax formscorrectly. He has put theory into practice by gaining real worldtax experience with guidance from Steve Davis. Alex hasalready secured a job after his graduation in May at Johnson,O’Connor, Feron & Carucci, LLP, a public accounting firm in

Wakefield, where he will serve as a staff accountant working with audits and tax

accounts.

Parker dodd is a portfolio management intern and a seniorcurrently majoring in finance and economics at Salem StateUniversity. Taken under the wings of portfolio managers DennisWassung and Craig Goryl, Parker has learned the selectionprocess for securities and gained a broader view on gatheringresearch information. Not sure of his plans after graduating inMay 2015, Parker intends to pursue his Series 7, 63 and 66licenses.

nick Burwell Joins Portfolio Management team

We are pleased to announce the addition of nick Burwell toCabot’s portfolio management team. Nick will be responsible formanaging Cabot’s fixed-income portfolios and he is currently aCFA Level III candidate. He previously worked for ICC CapitalManagement in Orlando, Florida, an institutional firm with over$500 million in assets under management.

Nick obtained his undergraduate degree in businessadministration from Stetson University in Florida and nowcurrently resides in Watertown, Massachusetts. He has a strongunderstanding of the asset management industry, passion forfinancial markets and demonstrated ability to master complex concepts and deliver highlevel performance. Welcome to the team Nick!

Mikki L. Wilson,

Director of Marketing

and Business Development

Please feel free to contact your accountant or Cabot Advisor if you have any questions about

how these numbers may affect your individual tax planning strategy for the coming year.

Federal Tax

Brackets

Married Filing Jointly

and Surviving SpousesSingle Filers

Federal Tax Rate 2014 Taxable Income 2015 Taxable Income 2014 Taxable Income 2015 Taxable Income

10% $0 - $18,150 $0 - $18,450 $0 - $9,075 $0 - $9,225

15% $18,150 - $73,800 $18,450 - $74,900 $9,075 - $36,900 $9,225 - $37,450

25% $73,800 - $148,850 $74,900 - $151,200 $36,900 - $89,350 $37,450 - $90,750

28% $148,850 - $226,850 $151,200 - $230,450 $89,350 - $186,350 $90,750 - $189,300

33% $226,850 - $405,100 $230,450 - $411,500 $186,350 - $405,100 $189,300 - $411,500

35% $405,100 - $457,600 $411,500 - $464,850 $405,100 - $406,750 $411,500 - $413,200

39.6% Over $457,600 Over $464,850 Over $406,750 Over $413,200

Exemptions and DeductionsMarried Filing Jointly

and Surviving SpousesSingle Filers

2014 Amount 2015 Amount 2014 Amount 2015 Amount

Standard Deduction $12,400 $12,600 $6,200 $6,300

Limitations on Itemized Deductions (AGI*) $305,050 $309,900 $254,200 $258,250

Personal Exemption $3,950 $4,000 $3,950 $4,000

Personal Exemption Phaseout (AGI*) $305,050 $309,900 $254,200 $258,250

Roth IRA Contribution Phaseout (MAGI**) $181K- $191K $183K - $193K $114K - $129K $116K - $131K

Alternative Minimum Tax Exemption $82,100 $83,400 $52,800 $53,600

Student Loan Interest Deduction Phaseout (MAGI**) $130K - $160K $130K - $160K $65K- $80K $65K - $80K

Lifetime Learning Credit Phaseout (MAGI**) $108K - $128K $110K - $130K $54K - $64K $55K - $65K

American Opportunity Credit Phaseout (MAGI**) $160K- $180K $160K - $180K $80K - $90K $80K - $90K

Gift and Estate Tax Retirement Account Contribution Limits

2014 Amount 2015 Amount 2014 Amount 2015 Amount

Estate Tax Basic Exclusion $5,340,000 $5,430,000 401(k), 403(b), 457 Plans $17,500 $18,000

Annual Gift Exclusion $14,000 $14,000 401(k), 403(b), 457 Plans (if age 50+) $23,000 $24,000

Traditional IRAs, Roth IRAs $5,500 $5,500

Traditional IRAs, Roth IRAs (if age 50+) $6,500 $6,500

SIMPLE Plans $12,000 $12,500

SIMPLE Plans (if age 50+) $14,500 $15,500

*Adjusted Growth Income

**Modified Adjusted Growth Income

Interns & Opportunities

Establishing a high level plan for charitable giving can be very complex.

High-net-worth investors have many options when it comes to charitable giving. Here

are three vehicles our clients use regularly:

1. donor Advised Fund (dAF)A DAF gives the grantor the benefit of a charitable deduction in the year it is made. Sincethe funding vehicle itself will qualify as a 501(c)(3) charitable entity, any stock sales donein the portfolio are tax free. As a result, many investors in DAFs choose to make theircontributions with stock that has a low cost basis. The proceeds of the stock sale areprofessionally managed and distributions are made to charities of your choice.

2. Private Charitable Foundation (PCF)A Private Charitable Foundation is an entity established by families solely for the purposesof charitable giving. A PCF will typically develop a mission statement to guide the purposeand long-term charitable goals of the organization. The management of the foundation isoverseen by appointed officers and a board of directors (in many cases, family members).These individuals are tasked with managing the affairs of the foundation, including whengrants are made and how the funds in the foundation are to be invested and managed by aprofessional advisor. A PCF is required to distribute at least 5% of its assets each year forcharitable purposes.

3. Charitable trusts (CRt/CLt)Charitable Trusts offer a great option for investors to fund either current or future charitablegrants. A Charitable Remainder Trust (CRT) is an arrangement in which a donor providesfor a charitable bequest of assets in the future while still retaining an income stream fromthose assets while they are alive. The donor gets the benefit of a tax deduction in the yearthey fund the trust based on the projected “remainder interest” that goes to charity.

A Charitable Lead Trust (CLT) works in the opposite way of a CRT. In a CLT arrangement,a charity receives yearly distributions from the trust while the donor is alive (or for theterm dictated by the trust). When the donor passes away, their heirs receive whatever isleft.

As with other charitable arrangements, sale of stock within charitable trusts is not subjectto capital gains tax which makes these a great vehicle to fund with stock holdings that havea low cost basis. As with the other entities, the portfolio can be professionally managedand overseen by the grantor/donor.

As you can imagine, I’ve only scratched the surface within this article. I would

encourage anyone interested in learning more about charitable giving to contact your

attorney, accountant or your Cabot advisor for a more detailed explanation of your

options.

WEALtH

MAnAGEMEnt

CABOt WEALtH MAnAGEMEnt, InC. CABOt WEALtH MAnAGEMEnt, InC.

Cabot in the Community Charitable Giving AROUnd

CABOt

Greg Stevens, CFP ®, CRPS ®

Principal, Senior Wealth Advisor

Mikki Wilson was recognized at Salem StateUniversity’s 2014 Alumni Weekend Jazz brunch for herwork on the Alumni Association Board of Directors’civic engagement committee, as well as for her effortswith the Northeast Arc Adopt-a-Home program. In2012, Salem State’s Alumni Association teamed up withNortheast Arc, adopting a home that houses fourindividuals with disabilities who are learning to liveindependent lives. Through the alumni association’scivic engagement committee, a strong relationship hasformed between Salem State’s alumni and bothresidents and support staff. For her wonderfulcontributions to these endeavors, Mikki was presentedwith the George Ellison Sr. Volunteer of the Year Award.

Rob Lutts was appointed the newest member of theSalem State University Board of Trustees by formergovernor Deval Patrick on November 24. Lutts bringsover 30 years of investment management experience tothe board, and according to university president Dr.Patricia Maguire Meservey, “will be an important assetto Salem State in a variety of important and very criticalareas.”

“Rob’s interest in—and passion for—the university,”she continued, “is well known. His long anddistinguished service as a member and past presidentof the Salem State Foundation has given him a deepfamiliarity with the operations of a robust and growinguniversity as well as many of the challenges we face. Iam delighted to welcome him to our board of trustees.”

Commenting on his appointment, Rob noted that he is “thrilled to join the trustee leadership at Salem State University.This vitally important institution needs to be nurtured and cultivated so that it continues to support the excellent educationopportunities in our backyard.”

Salem State University, established in 1854, is a comprehensive, public institution of higher learning located approximately15 miles north of Boston, Massachusetts. The university enrolls 10,000 undergraduate and graduate students representing44 states and 61 nations, and is one of the largest state university in the Commonwealth of Massachusetts.

Rob Lutts named to Salem State University Board of trustees

Mikki Wilson Presented With Volunteer of the Year Award

Mikki proudly accepts her award from university

president Dr. Patricia Maguire Meservey and Dr. Erik

Champy, past president of SSU’s Alumni Association.

President Dr. Patricia Maguire Meservey and

Rob Lutts stand for a photo op inside SSU’s

Bertolon School of Business.

Today investors are presented with a number of surprisingevents that many thought impossible. Oil dropped from over$107 a barrel in June of 2014 to less than $50 a barrel today.Further, interest rates continue to drop with the 10-yearTreasury yield approaching 2% as we write this. And mostsurprising, the 30-year Treasury bond now yields a paltry 2.5%.

How low can rates and oil go? The key to remember is mosttrends last much longer than most think possible. The drop inoil prices is very logical – we have increased productionglobally via new technologies. So supply and demand is atplay here. Further, it seems like the big run-up in oil for aboutten years was simply a temporary price spike. The cause ofthis change: innovation and new technology in drillingefficiency and capabilities. Further, we are diversifying away from tradition oil and gasthrough conservation and alternative energy like solar, wind and electric vehicles. The keymessage: we are in a world of rapid innovation deployment – much of this innovation isrooted in our computational ability from computer power. Expect this type of progress inmany industries. Healthcare, transportation, energy, industrial companies and more are allexperiencing an explosion of new technologies and innovation. Get used to change – it willcome faster with more impact to many more industries over the coming decade.

So, how low will interest rates go? Could they drop even lower in the coming year? Yes – ifinflation is disappearing, the likelihood of the yields on bonds is disappearing too. Of course,there will be a reversal; however, rates could stay low a great deal longer than many expect.Today the German 10-year government bond trades at .45% and yields in Japan have all butdisappeared. Could yield in the United States continue to decline? Yes. Until the FederalReserve ends its accommodative period and until we see a real pick-up in inflation, then it isunlikely we will see interest rates rise much and they could even trade lower. With oildropping, we expect to see the CPI Index continue to trend lower and remain very bondfriendly. When will the interest rate bubble burst? No one knows for sure. We have to be onthe lookout for indications of a change – because when the change comes it could be rapidand dramatic.We are enthusiastic about the prospects for the United States economy. We areliving in a period of great prosperity and are the beneficiaries of incredible entrepreneurialinnovation and wealth creation. We know it will not be a smooth ride for all of 2015; however,we believe it will be a year of progress.

We are pleased to continue serving as stewards ofyour family’s wealth. Thank you for yourcontinued confidence in our team.

Best wishes,

Robert T. LuttsPresident and Chief Investment Officer

QUARtERLY REVIEWFOURtH QUARtER 2014

Cabot Wealth Management, Inc.216 Essex Street

Salem, MA 01970978-745-9233 / 800-888-6468

eCabot.com

Log on to eCabot.com

for our latest articles, interviews and reports. Email

if you would like to receive Cabot updates.

eCabot.com

In tHIS ISSUE

1PRESIdEnt’S MESSAGE

2015 Outlook

2-3WEALtH

MAnAGEMEnt

Charitable Giving

2015 Tax Update

4InVEStMEnt

MAnAGEMEnt

Is it Time to Bring

Your Money Home?

5CLIEnt SERVICES

Staying Connected

6MEEt tHE tEAM

Nick Burwell, Fixed-Income

Interns & Opportunities

7CABOt In tHE

COMMUnItY

Lutts Appointed

to Board of Trustees

Wilson Accepts

Volunteer Award

8

AROUnd CABOt

Cabot Kids Color Our Hearts

Save the Date

GEt COnnECtEd

Follow us@cabotwealthmgmt

for our latest updates,articles, and media clips.

Follow our company or join our group

Wealth Management

with Cabot

216 ESSEX STREET, P.O. BOX 150, SALEM, MA 01970 / 978-745-9233 / 800-888-6468

This quarterly newsletter is intended for information purposes only. Articles, graphs, charts and discussions should not be construed as specific investment advice. Individuals should personally consult with a financial professional to review their own specific situation in light of any information discussed here. Cabot is not under any obligation to update the information and while every attempt is made to insure that it is accurate,we are not responsible for misstatements or inaccuracies. This quarterly is intended for dissemination in the United States and is not intended forcirculation elsewhere. It is important to note that any performance reporting or implied performance is not indicative of future results. Investmentsare not insured and may lose value. Asset allocation and diversification does not protect against loss. For complete disclosures, please contact usat (800) 888-6468 or [email protected] to receive a copy of our Form ADV and privacy statement.

Like us on Facebookto see what’s happening

around Cabot.

January 2015

Friday, September 25, 2015

Join us for Cabot’s 26th Annual Wealth Management Conference at the HawthorneHotel in historic downtown Salem, Massachusetts. Presentations will focus on currenteconomic events and relevant wealth management topics. Attendees have the opportunityto have their questions and concerns addressed directly by members of the Cabot Team.

Cabot’s kids had the opportunityto color our hearts during our2nd Annual Holiday CardContest in November. Literally.Children of our staff submittedholiday-inspired works of“heart” to warm the hearts ofclients and colleagues during theholiday season. Winning heartsfeatured came from CarlottaGasparello (age 6), AbbyStevens (age 9), Cooper andParker Wassung (ages 6 and 8).In addition, all of our pint-sizedparticipants received acertificate of recognition, acoloring book, and had theirartwork displayed in Cabot’sCaboteria breakroom. Visit ourFacebook page to see all of theirworks of “heart”.

For more information or to RSVP :

Call (978) 745-9233 or email [email protected].

Mark your Calendar!

Autumn in New England!

In lieu of gifts this holiday season,Cabot Wealth Management has contributedto causes close to our homes and our hearts.

CEO Corner:

Rob Lutts is now in the midst of putting

on paper the lessons learned and

techniques he uses to lead the

investment team at Cabot. He is

writing a book which will

revolve around the key

factors in identifying

successful businesses,

and hence, winning

investments.

Around Cabot

Abby Stevens, 9, proudly displays

her certificate for submitting her

polka-dot inspired heart.

Cabot Kids Color Our Hearts for the Holidays