Embed Size (px)

Citation preview

Institutional Presentation

TIM PARTICIPAÇÕES

4th QTR 2014

• Global Telecom Landscape 4

• Brazilian Telecom Landscape 6

• TIM Brasil 10

• TIM’s Strategy 16

• Operational Data 20

Network Evolution 25

Fixed Business 29

• Regulatory Update 33

• Financial Data 36

• Perspectives 39

AGENDA

*Click on the page number to access the section

Global Telecom Landscape

240%

182%

173%

161%

158%

141%

Hong-Kong

Finlândia

Rússia

Portugal

Singapura

Brasil

189

138

71

29

26

EUA

China

Japão

Brasil

Reino Unido

1,278

927

349

283

257

China

Índia

EUA

Brasil

Indonésia

68%

65%

63%

59%

50%

32%

Japão

Hong Kong

Coréia

Austrália

Nova Zelândia

Brasil

73%

70%

69%

69%

64%

34%

Hong Kong

Noruega

Singapura

Coréia

Dinamarca

Brasil

57

49

47

46

41

9

Canadá

EUA

Noruega

Suíça

Japão

Brasil

GLOBAL LANDSCAPE

O Brazilian market is reaching maturity but there is still room for user profitability and the main opportunity is in data

Customer Base Ranking (Mln)

Service Revenues Ranking (U$ Bln)

4th 4th

Data / ARPU Ranking (%)

25th

Mobile Penetration Ranking (%)

14th

ARPU Ranking (U$)

38th

Smartphone Penetration Ranking (%)

28th

4

India

USA

Brazil

Indonesia

USA

China

Japan

Brazil

United Kingdom

Japan

Hong Kong

Korea

Australia

New Zeland

Brazil

Hong Kong

Finland

Russia

Portugal

Singapore

Brazil

Source: Merrill Lynch – Global Wireless Matrix 4Q14 (3Q14 data) | Top 5 + Brazil

Canada

USA

Norway

Switzerland

Japan

Brazil

Hong Kong

Norway

Singapore

Korea

Denmark

Brazil

Brazilian Telecom Landscape

51.9 51.6 53.5 55.6

64.8 69.9 72.4 71.9

2011 2012 2013 2014

43.0 44.3 44.9 45.0

242.2 261.8 271.1 280.7

16.5 19.0 21.7 23.4 12.7 16.2 18.0 19.6

314.4 341.3 355.7 368.7

2012

BRAZILIAN LANDSCAPE| TELECOM OVERVIEW Customer Base (R$ Mln)

Total Net Revenues (R$ Bln)

2014 / 2013

Fixed, data and TV

Mobile

Total

2011 2012 2013 2014

Mobile 77.0% 76.7% 76.2% 76.1%

Fixed 13.7% 13.0% 12.6% 12.2%

Fixed broadband 5.2% 5.6% 6.1% 6.3%

Pay TV 4.1% 4.7% 5.1% 5.3%

2014 / 2013

Fixed

Mobile

Fixed broadband

Total (fixed + mobile)

Pay TV

2014 2011 2013

2011 2012 2013 2014

Mobile 55.1% 57.5% 57.5% 56.4%

Fixed, data and TV 44.1% 42.5% 42.5% 43.6%

6

117.6 121.5 125.9 127.5

In 2014, the mobile market generated R$ 71.9 billion in revenues (56.4% of total). Fixed broadband and pay TV access gained share in the total market

Source: Anatel, Operator’s balance and Teleco website Notes: Total market base | Main operators revenues | Oi’s and Claro’s adjusted revenues

TIM represents 26% of the industry mobile revenue2 while has 28% of the market share

BRAZILIAN LANDSCAPE|MAIN GROUPS

7

TIM

Source: Anatel and Players balance sheet

Vivo

Claro Oi

Mobile Fixed1 Fixed BB Pay-TV Group

Customers 4Q14 (000´s) 74,721 657 153 n.a. 76,531

Market share 4Q14 27.0% 1.4% 0.5% n.a. ---

Net Adds 12M (000´s) 2,289 25 64 n.a. 2,378

Net Revs FY14 (R$ Mln) 18,919 579 19,498

ARPU 4Q14 18.0 n.a. n.a. n.a. ---

Mobile Fixed1 Fixed BB Pay-TV Group

Customers 4Q14 (000´s) 79,938 10,939 4,102 770 95,749

Market share 4Q14 28.5% 23.9% 17.1% 3.9% ---

Net Adds 12M (000´s) 2,693 502 -205 176 2,665

Net Revs FY14 (R$ Mln) 23,740 11,260 35,000

ARPU 4Q14 24.6 n.a. n.a. n.a. ---

Mobile Fixed1 Fixed BB Pay-TV Group

Customers 4Q14 (000´s) 71,107 11,519 7,523 10,182 100,331

Market share 4Q14 25.3% 25.2% 31.4% 52.0% ---

Net Adds 12M (000´s) 2,403 1,463 941 525 3,868

Net Revs FY14 (R$ Mln) 13,078 22,525 35,603

ARPU 4Q14 15.3 n.a. n.a. n.a. ---

Mobile Fixed1 Fixed BB Pay-TV Group

Customers 4Q14 (000´s) 50,918 16,692 6,554 1,303 75,467

Market share 4Q14 18.1% 36.5% 27.3% 6.7% ---

Net Adds 12M (000´s) 702 -1,742 20 474 1,196

Net Revs FY14 (R$ Mln) 9,290 19,132 28,422

ARPU 4Q14 17.4 n.a. n.a. n.a. ---

The mobile segment represents 78% of the industry access growth

1 - Fixed Access numbers refers to 3Q14

Fixed / Mobile Fixed BB Fixed voice & BB / TV Mobile

Fixed BB/ TV Fixed Mobile Fixed / Mobile

/ 2 - Mobile revenue considers only the 4 major players

MOBILE MARKET | OVERVIEW

Source: Anatel, IBGE

Regional Overview (Dec/14)

Penetration per Estate

(Dec/14)

8

68.1 26.8 24.8 18.7 16.6 15.4 13.0 11.7 9.3 8.9 9.1 6.9 6.7 5.2 4.4 4.7 4.7 4.2 3.8 4.2 4.2 2.7 2.4 2.0 0.9 0.9 0.5

154%

129% 150%

123%

147% 138% 140% 131%

115% 136% 134%

241%

97%

131% 113%

146% 137%

107%

145% 131% 125% 120%

139% 134% 114% 123%

102%

SP MG RJ BA RS PR PE CE PA GO SC DF MA PB ES MT RN AM MS PI AL SE RO TO AC AP RR

Base Móvel (MM) Penetração (base/pop)

TIM vice líder em Market Share

TIM líder em Market Share

A1 e A2: SP

* Population 44.2 Mln

* Mobile Base 68.1 Mln

* Penetration 154.1 %

* TIM Market Share 27.8 %

A3: RJ/ES

* Population 20.4 Mln

* Mobile Base 29.2 Mln

* Penetration 142.9 %

* TIM Market Share 15.1 %

A4: MG

* Population 20.8 Mln

* Mobile Base 26.8 Mln

* Penetration 129.0 %

* TIM Market Share 26.7 %

A5: PR/SC

* Population 17.9 Mln

* Mobile Base 24.4 Mln

* Penetration 136.7 %

* TIM Market Share 51.5 %

A6: RS

* Population 11.2 Mln

* Mobile Base 16.6 Mln

* Penetration 147.4 %

* TIM Market Share 13.5 %

A7: CO

* Population 19.4 Mln

* Mobile Base 29.7 Mln

* Penetration 153.6 %

* TIM Market Share 15.8 %

A8: NO

* Population 20.1 Mln

* Mobile Base 21.6 Mln

* Penetration 107.3 %

* TIM Market Share 31.8 %

A9: BA/SE

* Population 17.4 Mln

* Mobile Base 21.4 Mln

* Penetration 123.1 %

* TIM Market Share 21.4 %

A10: NE

* Population 32.1 Mln

* Mobile Base 42.9 Mln

* Penetration 133.7 %

* TIM Market Share 33.1 %

Mobile Base (Mln) Penetration (base/pop)

TIM: Market share leader

TIM: 2nd position in market share

TIM Brasil

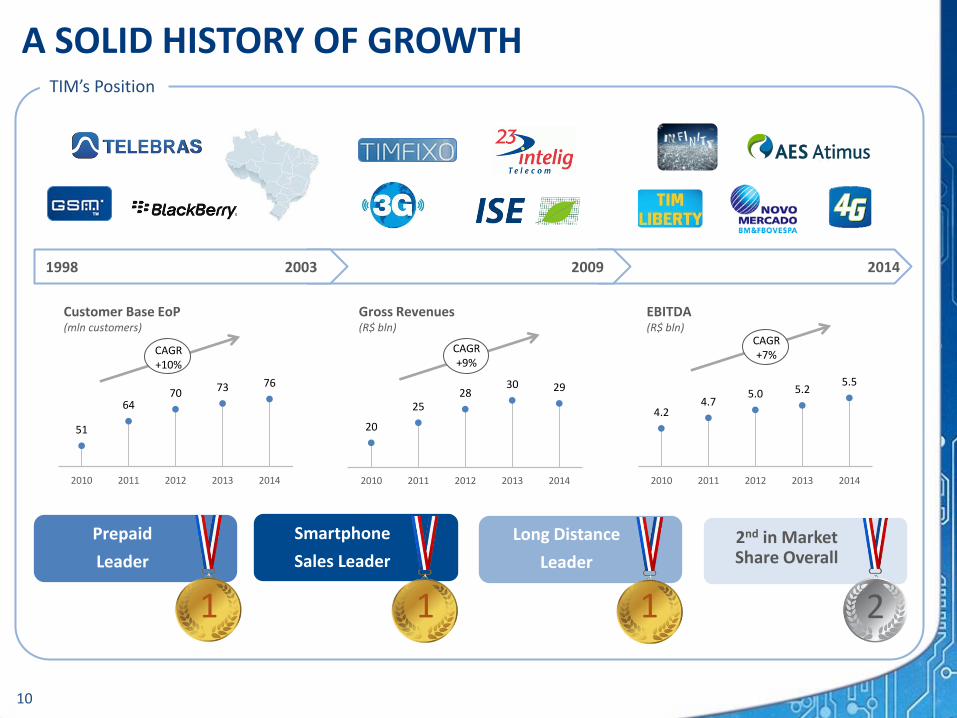

A SOLID HISTORY OF GROWTH TIM’s Position

1998 2003 2009 2014

CAGR+9%

CAGR+7% CAGR

+10%

20

25 28

30 29

2010 2011 2012 2013 2014

51

64 70 73 76

2010 2011 2012 2013 2014

4.2 4.7

5.0 5.2 5.5

2010 2011 2012 2013 2014

10

Gross Revenues (R$ bln)

Customer Base EoP (mln customers)

EBITDA (R$ bln)

Long Distance

Leader

2nd in Market Share Overall

Smartphone

Sales Leader

Prepaid

Leader

1 2 1 1

KNOWING TIM BETTER TIM: A Huge Brazilian Company

74.7 million customers (27% Share)

The 2nd Player - Market and rev. share

More than 465,000 points of sales

More than 170 own stores

15 Customer Care Centers (16k attendants)

~14,000 antennas

3,433 cities covered

95% of urban population covered

54,000 km of optical fiber network

~13,000 employees

23,000 indirect jobs

R$3.9 billion invested in 2014 (excluding licenses)

Sales

Network

Social & Economic

TIM Celular S.A. Intelig

100%

TIM Brasil Serv. e Part. S.A. Free Float

Telecom Italia International N.V.

Telecom Italia

100%

TIM Participações S.A.

ON: 33% (809,062,533) ON: 67% (1,611,969,946)

100% 100%

Purpose

Care about the costumer

Transparency

15,000 km of optical fiber

5,500 km of optical fiber

Recent Acquisions

Commitment

Innovation Agility

Values

11

Shareholders’ Structure

Presence in Brazil since 1998

16th largest Private Company in Brazil (source: Exame Magazine – 2013)

Approximately R$25 billion of Market Capitalization

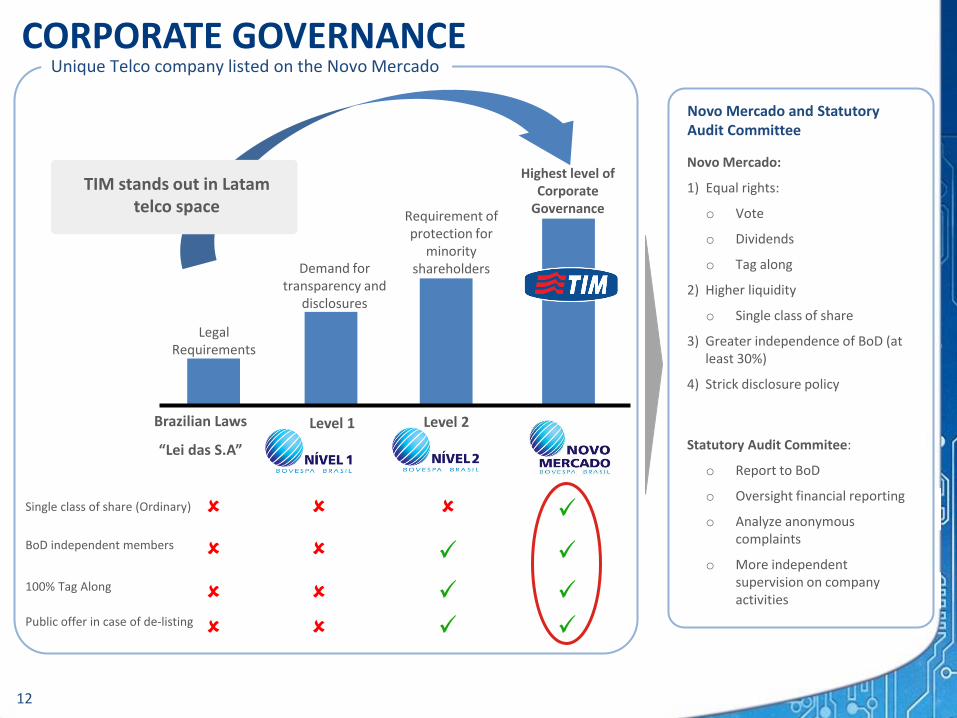

CORPORATE GOVERNANCE

12

Novo Mercado:

1) Equal rights:

o Vote

o Dividends

o Tag along

2) Higher liquidity

o Single class of share

3) Greater independence of BoD (at least 30%)

4) Strick disclosure policy

Statutory Audit Commitee:

o Report to BoD

o Oversight financial reporting

o Analyze anonymous complaints

o More independent supervision on company activities

Brazilian Laws

“Lei das S.A”

Legal Requirements

Demand for transparency and

disclosures

Highest level of Corporate

Governance Requirement of protection for

minority shareholders

Level 1 Level 2

Novo Mercado and Statutory Audit Committee

Unique Telco company listed on the Novo Mercado

TIM stands out in Latam telco space

Single class of share (Ordinary)

BoD independent members

100% Tag Along

Public offer in case of de-listing

In public schools

84,000 children and 2,700 professors

In museums and science and technology centers

More than 70,000 people

In public administration

Participatory Urban Caretaker

o 4 municipalities

Cultural maps

o 7 municipalities and RS & CE government

In the federal institutions of professional and technological education

TIM Tec

o MOOC platform

Partnership with 5 federal institutes

CORPORATE SOCIAL RESPONSABILITY

Founded in July, 2013

We are committed to creating and strengthening resources and

strategies for the democratization of science and innovation that

promote human development in Brazil, with mobile technology as

one of the main facilitators.

MISSION:

Commitment with the 2014-16 Social Investment Plan: R$45 million

President: Manoel Horacio F. da Silva

Director: Mario Girasole

13

Joined UN Global Compact in 2008

Member of ISE (Sustainability Index)

for 7 consecutive years

Member of ICO2 (Efficient Carbon Index) for 5 consecutive years

ISO 14001 certified since 2010, 1st Brazilian

telco Sustainability

TRANSPARENCY | PORTAS ABERTAS INICIATIVE

14

Portas Abertas Website www.tim.com.br/portasabertas

Portas Abertas Mobile app

App for mobile devices available at Apple Store and Google Play

Disclosure of Anatel’s Plan

Monitoring: o Network improvements

o Quality KPI’s

o Network incident and alerts

Real coverage footprint

New and Planed Antennas/Towers

Wi-Fi hotspots

TIM’s Strategy

Strategic Planning

TIM as a protagonist

Customer base appreciation

Quality mobile broadband (MBB)

infractructure

Strategic Options

STRATEGIC GUIDELINES

Differentiation in offerings, channels,

content and data applications

Take care of the customer experience

OneTIM project (best place to work)

16

MARKET: MOVING TOWARDS MOBILE DATA USAGE

17

Revenue Mix

Revenue Mix

27%

Mobile Market Revenues Evolution (Mobile Service Net Revenues; %)

• Most households without internet access • Mobile better suited to break price barrier

9.5

2.6

Jan-13 Nov-14

0.34 0.30 0.23

0.16 0.10 0.06 0.03 0.02

2012 2013 2014 2015 2016 2017 2018 2019

57%

4%

12%

1%

37%

2%

MTR Cut (R$)

Voice Incoming

Voice Outgoing

SMS

Internet 60%

• Maturing market: Customer base growth slowdown

• Consumption migrating from voice to data

2010 2020

SMS Traffic Sharp Decrease (billions of SMS sent)

Mobile Internet is the growth driver and will be the largest mobile market, although Voice remains important

Voice Decline

Internet Opportunities

Internet Market Evolution

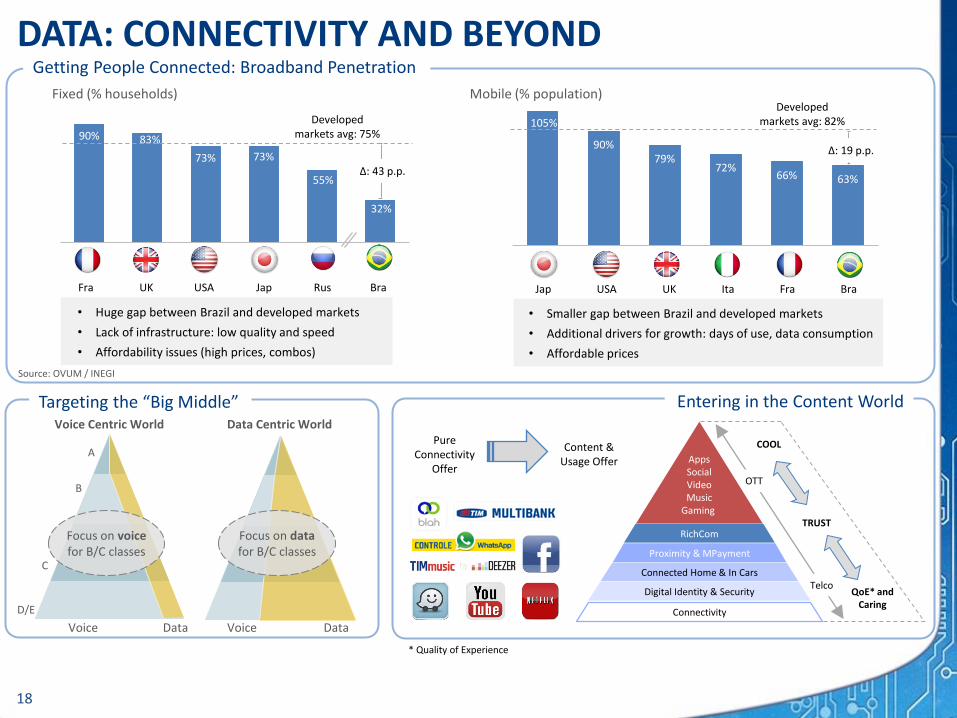

DATA: CONNECTIVITY AND BEYOND

18

105%

90% 79%

72% 66% 63%

• Huge gap between Brazil and developed markets

• Lack of infrastructure: low quality and speed

• Affordability issues (high prices, combos)

• Smaller gap between Brazil and developed markets

• Additional drivers for growth: days of use, data consumption

• Affordable prices

90% 83%

73% 73%

55%

32%

Fixed (% households) Mobile (% population)

Content & Usage Offer

Pure Connectivity

Offer

Developed markets avg: 75%

Developed markets avg: 82%

Connectivity

Proximity & MPayment

Connected Home & In Cars

RichCom

OTT

Telco

COOL

TRUST

QoE* and Caring

Fra UK USA Jap Rus Bra Jap USA UK Ita Fra Bra

Δ: 43 p.p.

Δ: 19 p.p.

* Quality of Experience

Getting People Connected: Broadband Penetration

Entering in the Content World

Apps Social Video Music

Gaming

Digital Identity & Security

A

B

C

D/E

Voice Centric World Data Centric World

Data Data Voice Voice

Focus on voice for B/C classes

Focus on data for B/C classes

Targeting the “Big Middle”

Source: OVUM / INEGI

Operational Data

MAIN OFFERS Postpaid

TIM Pay Express: pay for purchases and receive payments

through mobile phone

Fast and safe platform

v

Hibrid Plan Other Services

20

Prepaid

o Unlimited local and long distance calls (using 41 code) to TIM customers

o Unlimited calls to radios for R$12.90/month used

o Package of minutes to other operators and fixed numbers (in accordance with the chosen plan: from 50 to 800 minutes)

o Internet package (in accordance with the chosen plan: from 300MB to 50GB)

o Unlimited SMS to all operators for R$13.90/month used

o Pay per day concept: • R$0.75 to local and long distance (using 41 code) TIM customers • R$0.99 data + SMS • R$0.50 unlimited music through TIMmusic app

+ • R$0.70 per unlimited call to local fixed numbers

o Infinity Web + Torpedo for R$0.75/day used • 10MB of Internet/day with max. speed of 1mbps on 3G network

and 5mbps on 4G network • Unlimited SMS to all operators

o With an unique concept in the market, the plan provides unlimited access to WhatsApp without consuming data from the packed hired

o Additionally to the unlimited WhatsApp access, the plan includes 300Mb of internet, unlimited SMS and R$10 on credits for the total cost of R$29.90/month

o First postpaid plan on the market that does not require a voice package

o A plan that combines postpaid freedom and prepaid control

Brazil’s largest digital music provider

>32 mln downloaded songs

TIM Chip for soccer fans: free content of soccer teams

International long distance plans in the 5 continents

Voice and data usage for a single value per 24 hours of usage

RECENT INNOVATIONS SHOWING RESULTS

Customer Base (mln users)

PREPAID MOBILE ACCOUNT/ MONEY

o Partnership: TIM, Mastercard and Caixa Econômica Federal

o Focus on unbanked population ( >50% of prepaid base)

NEW MUSIC PLATFORM

o Partnership TIM and Deezer (top global streaming platform)

o More than 35 million music available for download

o Maintaining leadership position in the mobile music industry in Brazil

Source: ANATEL

3G Market Share (%; mln users)

4G Market Share (%; thd users)

Source: ANATEL Source: ANATEL

INTERNET SHARING PLANS

o Up to 4 devices

o No additional charges

WEEKLY SERVICE PACKAGE o Voice + Data + SMS o R$ 7 per week

R$ 0.75 DAILY OFFER

o Expansion to new regions: PR, SC, MA, RJ

o Covering most of the country

Adding Value Through Innovation

NEW APP FOR LANGUAGE COURSES o Games and quizzes help

students developing English skills

blah COMMUNICATION APP

o Integrated communication (VOIP, IM, SMS) App

o First ad campaign

21

CONTROLE WHATSAPP PLAN o Unlimited app use for chat,

phoos, videos and audio

41%

39%

31% 30%

17%

20%

11%

8%

23% 25%

24% 26%

37% 34%

12% 13%

76.1 77.2 79.9

70.4 73.5 75.7

65.2

69.0 71.1

49.2 50.5 51.2

4Q12 4Q13

TIM

4Q14

P1

P3

P4

Dec/13 Dec/14

36.2

37.5

49.6

19.3

145 mln

Dec/13 Dec/14

TIM

2.6

2.0

1.3

0.5

6.8 mln

TIM

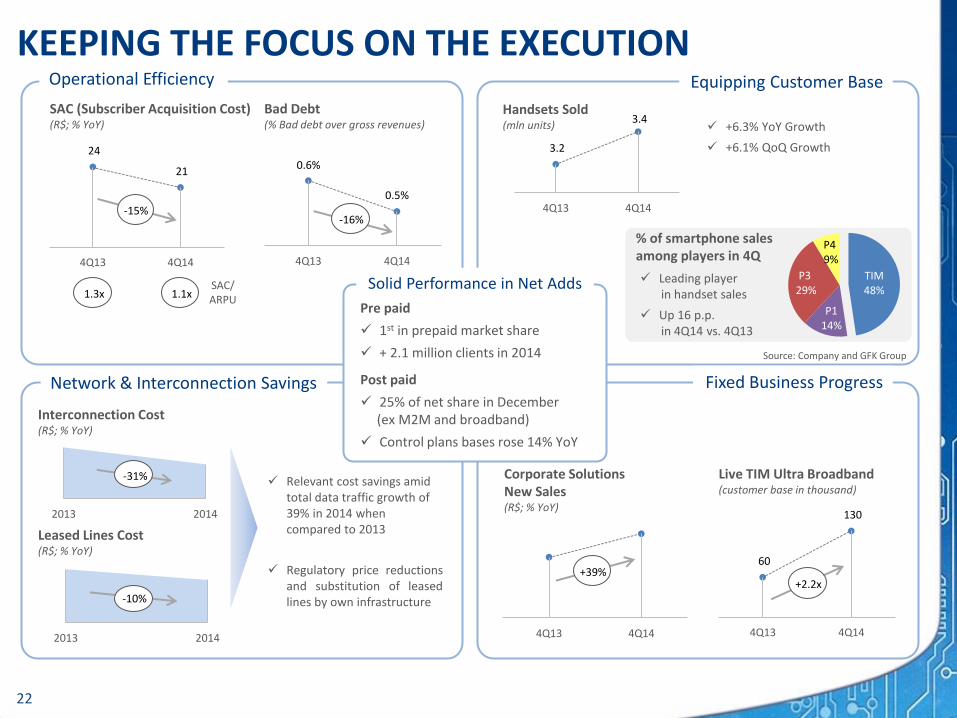

KEEPING THE FOCUS ON THE EXECUTION

22

2013 2014

2013 2014

-31%

Network & Interconnection Savings

Interconnection Cost (R$; % YoY)

Leased Lines Cost (R$; % YoY)

Relevant cost savings amid total data traffic growth of 39% in 2014 when compared to 2013

Regulatory price reductions and substitution of leased lines by own infrastructure -10%

3.2

3.4

4Q13 4Q14

Equipping Customer Base

Handsets Sold (mln units)

% of smartphone sales among players in 4Q

+6.3% YoY Growth

+6.1% QoQ Growth

Source: Company and GFK Group

TIM 48%

P1 14%

P3 29%

P4 9%

Leading player in handset sales

Up 16 p.p. in 4Q14 vs. 4Q13

0.6%

0.5%

4Q13 4Q14

Operational Efficiency

Fixed Business Progress

SAC (Subscriber Acquisition Cost) (R$; % YoY)

Bad Debt (% Bad debt over gross revenues)

SAC/ ARPU

24

21

4Q13 4Q14

-15%

1.3x 1.1x

-16%

Corporate Solutions New Sales (R$; % YoY)

Live TIM Ultra Broadband (customer base in thousand)

4Q13 4Q14

+39% 60

130

4Q13 4Q14

+2.2x

Solid Performance in Net Adds

Pre paid

1st in prepaid market share

+ 2.1 million clients in 2014

Post paid

25% of net share in December (ex M2M and broadband)

Control plans bases rose 14% YoY

MAINTAINING STRONG PACE IN DATA

...Remodeling the Business Profile

% over revenues

Strong Progress on Data...

+22% +20% +23% +28%

40 mln to come! 34 mln data users

Customer base: 75.7 mln

20 mln of untapped market

Usage Growth

Penetration Increase

13 mln w/ enabled devices

Data Opportunities on Data in the Customer Base

23

Data Customer Base (as % of total base)

Smartphone Penetration (% of smartphones over customer base)

14.9%

29.4%

49.5%

2012 2013 2014

Smartphone sales over 80% in 4Q14

+35 p.p.

30.3%

36.4%

44.6%

2012 2013 2014

1Q14 2Q14 3Q14 4Q14

Mix of Gross Data Revenues (% YoY)

SMS

Web

Content & Others

+29% +39%

+45% +80%

+33%

+72%

+47%

+82%

1,500 1,578 1,677 1,862

+1.2% -19% -8.2% -24%

Data ARPU (% YoY Growth)

18%

20% 21%

25%

1Q14 2Q14 3Q14 4Q14

+7.2 p.p

Data Revenues Penetration (% Gross VAS Revs / Gross Mobile Service Revs )

25.2%

27.2%

28.7%

30.9%

1Q14

2Q14

3Q14

4Q14

Network Evolution

...UNDERSCORING QUALITY IMPROVEMENT

25

3,093

3,013

2,930

2,845

TIM P4 P3 P1

Source: Anatel

Source: Company’s survey of national satisfaction

TIM

P1 P3 P4

Customers Satisfaction

¹ Voice Network (repair and call completion) ² Data Network: Estimated by TIM and composed by a subset group of Additional Services complaint

Total Demands at Consumer’s Protection Agency (Procon) (Per economic group, in thousands)

Source: SENACON/MJ

10.6 14.0

23.6 27.2

42.2 46.3

21.4

28.0

4Q13 1Q14 2Q14 3Q14 4Q14

TIM

P1

P3

P4

Data Evolution

Data Accessibility Ranking (3G) in SP

4G Sites in State Capital Cities

Anatel

Average Satisfaction with Coverage and Quality of Calls (score assigned by the customer)

Least claimed company at

Procon

7.80 7.80

Nov-12 May-13 Nov-13 May-14 Nov-14

Network Complaints (number of complaints)

Voice network¹

Data network²

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Voice network 2014 vs. 2013

-27%

Data network 2014 vs. 2013

-11%

Anatel Metrics

Customers Demands

Source: Anatel

Access

Anatel

Access

Access

Access

Access

99.24%

98.93%

99.20%

99.57%

98.88%

INFRASTRUCTURE EVOLUTION…

26

2.5 GHz 2.1 GHz

1.8 GHz 850 MHz 700 MHz

radius (km)

0.458 0.61

Innovative Coverage

Investment Profile

Site Densification

Cell coverage characteristics (Urban coverage simulation)

Capital allocation on innovative services:

Fiber (metropolitan + LD): expansion to ~55k Km in 2014

2G (voice)

3G+4G (data)

Number of 4G Sites Number of 3G Sites

4Q13 4Q14

1.9k

3.7k

4Q13 4Q14

9.1k

10.4k

Indoor coverage deployment

DAS (Distributed Antenna Systems) Solution

Femto Cells (corporate)

Wifi (consumers)

+92% +14%

R$3.9 bln Organic Capex +

R$2.9 bln (4G License & Clean up)

=

R$6.85 billion in 2014

Deployment in:

0.363 1.413 1.685

Rio de Janeiro Curitiba Brasília Manaus Natal São Luís

51%

87%

49%

13%

2013 2014

Band 850 MHz 900 MHz 1800 MHz

2100 MHz

2500 MHz

700 MHz

Possible Technologies

2G/3G 2G/3G 2G/4G 3G 4G 4G

Efficient Use of Spectrum Portfolio

Wifi and Small Cells

> 100% YoY

Fistel exemption

approved in Jan/15

Mobile Broadband Evolution (cities)

The 125 cities of the MBB project

represent 50% of the total network

traffic 39

53

66

83

125

4Q13

1Q14

2Q14

3Q14

4Q14

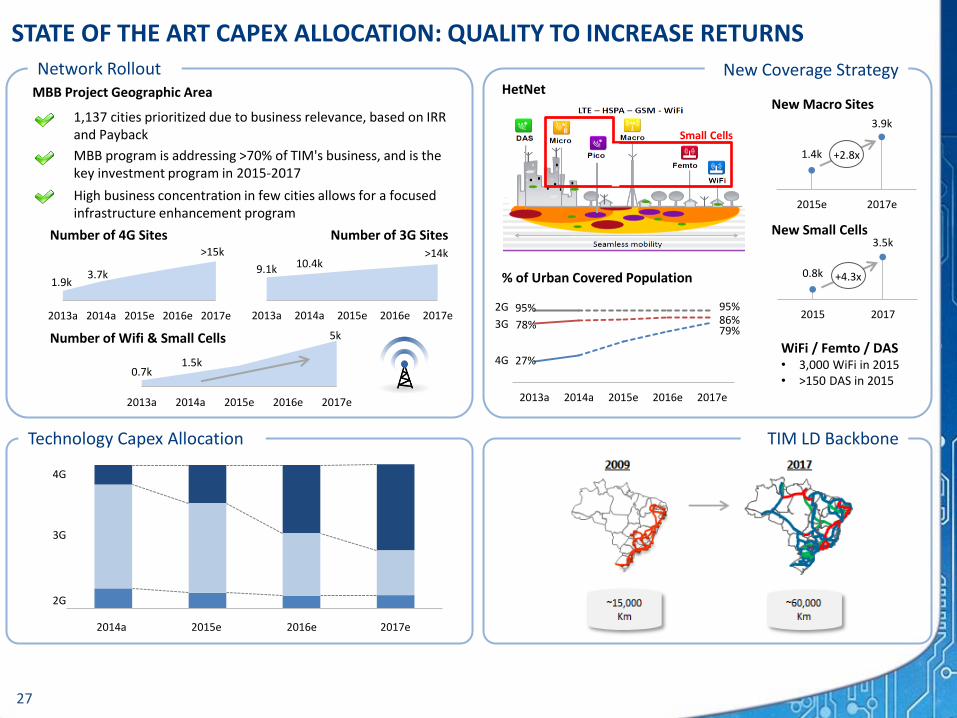

STATE OF THE ART CAPEX ALLOCATION: QUALITY TO INCREASE RETURNS

27

2014 Actual 2015 Bdg 2016 Plan 2017 Plan

MBB Project Geographic Area

Small Cells

New Macro Sites

WiFi / Femto / DAS • 3,000 WiFi in 2015 • >150 DAS in 2015

1,137 cities prioritized due to business relevance, based on IRR and Payback

HetNet

% of Urban Covered Population

2G

3G

4G

2014a 2015e 2016e 2017e

MBB program is addressing >70% of TIM's business, and is the key investment program in 2015-2017

High business concentration in few cities allows for a focused infrastructure enhancement program

1.9k 3.7k

>15k

2013a 2014a 2015e 2016e 2017e

Number of 4G Sites

9.1k 10.4k >14k

2013a 2014a 2015e 2016e 2017e

Number of 3G Sites

0.7k 1.5k

5k

2013a 2014a 2015e 2016e 2017e

Number of Wifi & Small Cells

2G

3G

4G

95% 95%

78% 79%

27%

86%

2013a 2014a 2015e 2016e 2017e

Network Rollout New Coverage Strategy

Technology Capex Allocation TIM LD Backbone

1.4k

3.9k

2015e 2017e

New Small Cells

0.8k

3.5k

2015 2017

+2.8x

+4.3x

Fixed Business

TRANSFORMING THE FIXED INFRASTRUCTURE

29

SP

Rio

National fiber Backbone: 10 POPs and 14,500 km

National Voice Backbone: 9 switching voice centrals and 150 interconnection points

International Interconnection: two nodes in RJ and SP managing international traffic

Satelite networks links in 9 cities

AES Atimus acquisition in 2011, later called TIM Fiber

Extensive optical fiber network with 5.5 thd km

Coverage in metropolitan areas of RJ and SP

Potential market of 8.5 million households and 550 thd

companies in 21 cities

Central Switch Fiber Network Satelite Station Central ATM and IP network Submarine cable MAN – Metropolitan Network Presence

Intelig Atimus

ACCELERATING FIXED BUSINESS PERFORMANCE

30

2013 2014

3.4

3.3

2.9

Live TIM

GVT

NET

4Q13 4Q14

2014 business remodeling recap:

Customer base management

Multiservice network launch

Sales team reorganization

Brand repositioning

Re-designed service portfolio

Fixed + mobile integration for corporate clients

2013 2014

+3.5x

EBITDA Net Revenues (with intercompany)

Revenues from New Sales (YoY)

Outstanding product performance… (ISP speed ranking - Mbps)

…with solid operational and financial results

60

130

4Q13 4Q14

Customer Base (000 users)

+2.2x

ARPU (R$; YoY%)

+24%

New Line Payback (months)

21

14

4Q13 4Q14

1

15.9

8.9

8.8

Live TIM

NET

GVT

37

21

Download

Upload

1

1,490

2,194

1,069

1,503

4Q13 4Q14

Coverage (000 Households)

+41%

Addressable Households

Homes passed

+1.0%

2013 2014

+2.7x

-33%

FIXED CORPORATE SOLUTIONS & LIVE TIM POSITIVE TRENDS

31

60k

130k

>500k

2013a 2014a 2015e 2016e 2017e

2013a 2014a 2015e 2016e 2017e

Customer Base (thousands customers)

EBITDA Revenues from New Sales (R$; YoY)

2013a 2014a 2015e 2016e 2017e

FIXED

MOBILE

CONVERGED SOLUTIONS

2015-2017 Drivers:

• Revenue and EBITDA rebound

• Sales team resizing and training

• Customer care unification (F+M)

• Improvement on service level

• Fine tuning mobile portfolio

• Launch of new convergent solutions

+9x

Investments (R$; YoY)

2013a 2014a 2015e 2016e 2017e

+3x +9x

From option value to reality:

• Accelerate growth through incremental investment

• Focus on keeping customer experience leadership

• Introduction of new services (Voice and Bluebox)

• Support the discussion on “Banda Larga Para Todos” program

Corporate Solutions as a Sustainable Business

Live TIM Plan: Accelerating Growth

Regulatory Update

MAIN REGULATORY TOPICS FOR 2015

33

Internet “Marco Civil da Internet” (Brazilian Civil Rights Framework for the Internet): Law nº. 12,965 provides Decrees/Regulations on topics such as net neutrality and privacy. Public Consultations will be launched involving the Comitê Gestor da Internet (CGI), MinCom and ANATEL

Broadband “Programa Banda Larga para Todos” (Broadband for All) and review of PGMU (Universal Service goals): The President Dilma intends to launch a universal broadband program, with 90% of households connected at 25Mbps.

Licensing “PL das Antenas” (SCD 293): Approved by the House of Representatives. Still needs to be voted in the Senate. Main points: simplification of licensing in environmental bodies and municipal governments; 60 days “positive silence”; right of passage in public lands.

Exemptions

Fistel (Law nº. 13.097/2014): Enacted on 20.01, by President Dilma Rousseff. FISTEL full exemption for Small Cells with power <5W and reduction to 10% with power <10W. REPNBL: Regulates tax exemption for Telecommunications Network Deployment. Update approved by Minicom on 01.14.2015, reducing the % of national technology.

Regulatory evolution

“Revisão do modelo de Concessão de STFC”: Asset reversibility and duration, Universal Service (Presidential Decree nº. 7.512/2011): possibly relieving voice universal service goals, changes in Law nº. 9.472/1997 (General Telecommunication Law), extending the concession beyond 2025.

Spectrum 1,800 MHz Renewal: Anatel approved the renewal process for the 1,800 MHz band for an additional period of 15 years.

LTE AUCTION DETAILS

34

1st Round (10+10) MHz cap

Block 4 (10+10) MHz

Block 5 (10+10) MHz

Block 6 (10+10) MHz

Block 2 (10+10) MHz

Block 3 (10+10) MHz

Block 1 (10+10) MHz Total

R$ mln Regional National

Minimum Price 1,893 30 5 1,928 1,928 1,928 7,712

Winning Bid Unsold 30 Unsold 1,947 1,928 1,947 5,852

Premium - 0.02% - 0.99% 0.00% 1.00% 38

Final Public Price (Anatel) - 26 - 1,739 1,720 1,739 5,224

EAD 887.59 13.86 2.48 903.93 903.93 903.93 3,616

EAD w/ unsold blocks obligations

- 18.9 - 1,119 1,119 1,119 3,616

Clean-up Cost Road Map*

700MHz Auction Results

Auction totaled R$5.85 billion, 24% lower then the R$7.7 billion expected for minimum prices for all blocks

EAD Contribution of R$890.1 million related to unsold blocks will be distributed proportionately among the participants and will be discounted of the Public Price

0.52 0.78 0.83 1.07 1.13 1.18 1.22 1.28 1.29 1.29 1.48

2.58

DEN NZL Spain Brazil GER PORT EUA Taiwan Italy France AUS Canada

Average = 1.22

Oi and Sercomtel did not participate in the auction

Spectrum acquisition at fair price (Price in USD/MHz/Pop. adjusted for GDP)

UPLINK Central Band

TV Channels Guard Band Private Limited Service

4 2 3 1

Central Band 5

6

30% in April 2015

30% in January 2016

30% in January 2017

10% in January 2018

R$1,199 million

~R$360 million

~R$360 million

~R$360 million

~R$120 million

Total Amount:

* Values will be adjusted by the IGP-DI index.

Financial Data

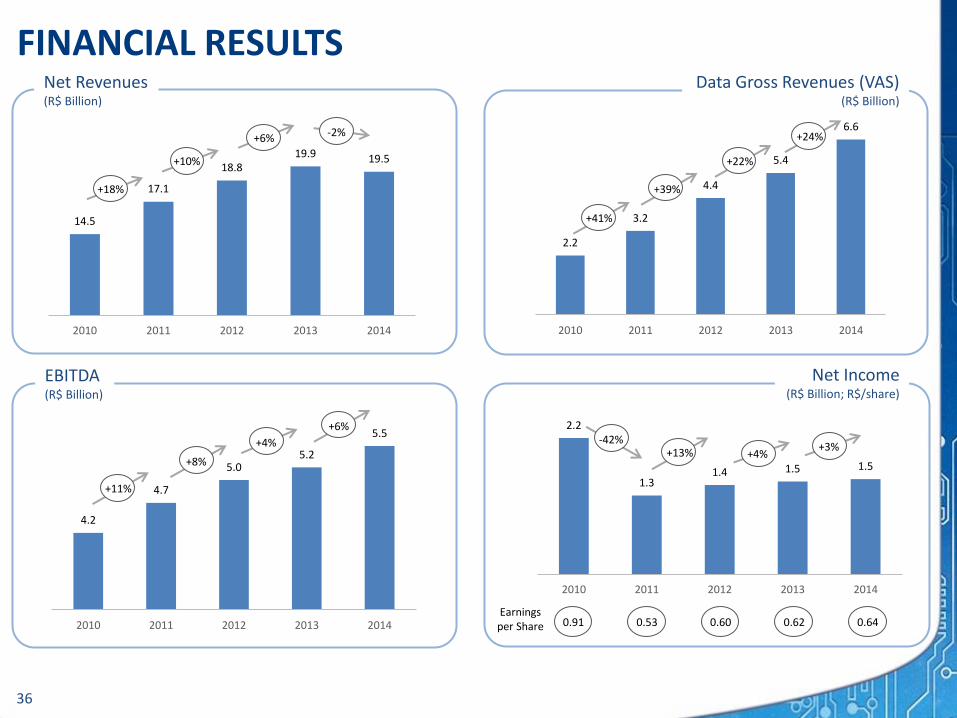

2.2

1.3 1.4 1.5 1.5

2010 2011 2012 2013 2014

4.2

4.7

5.0 5.2

5.5

2010 2011 2012 2013 2014

2.2

3.2

4.4

5.4

6.6

2010 2011 2012 2013 2014

14.5

17.1

18.8 19.9 19.5

2010 2011 2012 2013 2014

Net Income (R$ Billion; R$/share)

EBITDA (R$ Billion)

Data Gross Revenues (VAS) (R$ Billion)

Net Revenues (R$ Billion)

FINANCIAL RESULTS

Earnings per Share

+18%

+10%

+6%

+41%

+39%

+22%

+11%

+8%

+4% -42% +13% +4%

0.91 0.53 0.60 0.62 0.64

36

-2% +24%

+6%

+3%

NET FINANCIAL POSITION DETAILS

37

BNDES 58%

BB 6%

BEI 19%

BofA ML 5%

KFW 4%

Cisco 4%

Others 5%

Higher cash yield and debt cost due to CDI increase in the period Bigger gap between cash yield and debt cost due to smaller cost of new loans

Δ: 62 bps

4,279 4,867

6,507

2,000

2012 2013 2014

Cash & Debt Evolution

Cash Yield vs. Debt Cost (% per year)

Net Financial Position (R$ mln)

BNDES new disbursements

Short term debt

Better Profile: Less Short Term Debt

Debt by Lender in 2014 end (% of total loans)

Debt Position (R$ mln; % of total debt in short term)

Cash Position (R$ mln)

4,431

5,288 1,742

2012 2013 2014

4G payment

5,233

Improved group liquidity margin

9.58% 7.69%

8.58%

9.78%

10.20%

7.09%

9.50%

11.25%

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Δ: 147 bps

Cash yield

Debt cost

Excluding 4G payment -151

-421

1,274

-468

Net debt/

EBITDA 12M 0.23x -0.08x -0.03x

2012 2013 2014

20% 21% 21%

Perspectives

32.0%

34.9%

2012 2013 2014 2015e

Delivering important operational and financial results

Strong market positioning for growth

Renewed culture of innovation, quality and caring

Staying power and commitment with long term, with recognized

institutional leadership

Best governance in the industry: Novo Mercado

MBB (cities)

Changing Business Profile Focus on Execution Improving Profitability

Infrastructure Leveraging Growth

Revenue profile changing

Pre-paid data as key source of growth

TIM strategically well positioned with data focus on “big middle”

Business Generated Net Revenues Keeping costs under control, amid macroeconomic pressure

Keeping innovative offers:

• Infinity Day, Data Shared Plans, Controle Whatsapp plan, TIMmusic by Deezer, TIM Multibank (2015), Blue Box (2015)

Fixed turnaround completed: back to growth in 2015

Live TIM: from optionality to reality

TIM: A Solid Player

Building the Future

Tower sale

Big data analysis for Capex allocation

Investing Efficiently

4G LTE in 700MHz and 1,800MHz

EBITDA growth in 2014: +6.4% YoY

Margins expansion through opex savings and new revenues sources

(Voice & Other)

(Data & SMS)

Service EBITDA Margin (%; YoY)

+3.0 p.p.

2013 2014

39

125

Mobile broadband project

+86

2013 2014

74% 69% 64%

26% 31% 36%

2014 CONCLUSION

39

2014a 2017e

Leased Lines Cost (R$)

SAC (Subscriber Acquisition Cost) (R$)

Bad Debt (R$)

EBITDA Evolution (R$ without intercompany)

EBITDA - Capex

2013a 2014a 2015e 2016e 2017e

Data Traffic Expectation

3G Data Traffic

LTE Data Traffic

(in petabytes)

Mobile Customer Base (mln customers)

73.4

75.7

2013a 2014a 2015e 2016e 2017e

2014a 2017e 2014a 2017e

2014a 2015e 2016e 2017e

Business Growth

2014a 2017e

Operational Efficiency

Fixed Business Progress

MTR Path (R$)

0.34

0.02

2012 2014 2016 2018

SMS Market Revenues (R$)

2014a 2017e

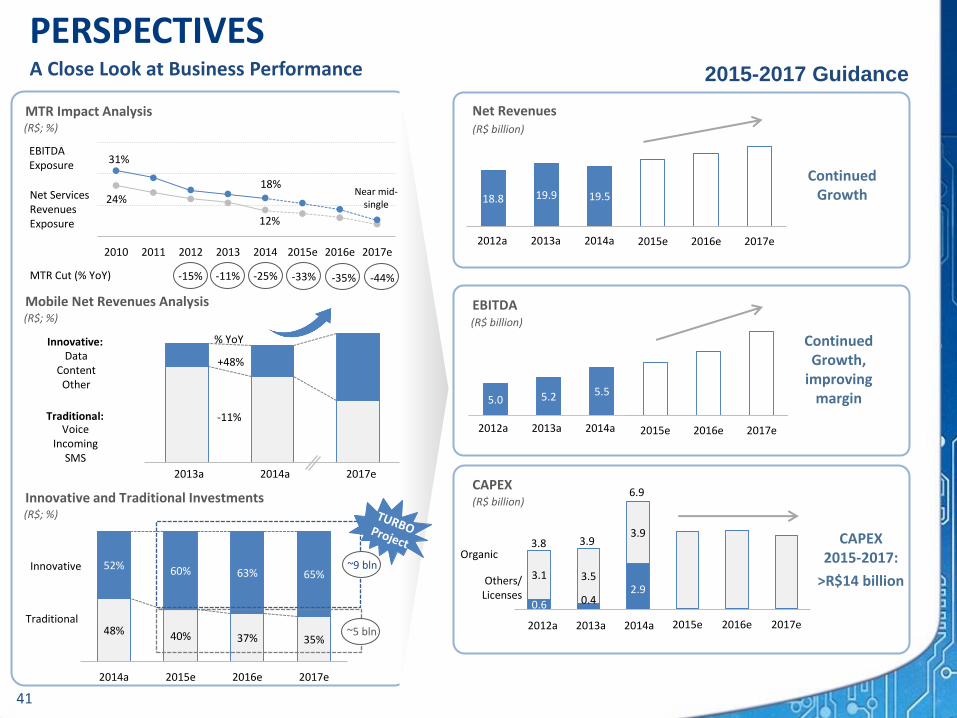

Network & Interconnection Savings COST EFFICIENCY

40

18.8 19.9 19.5

2012A 2013A 2014A 2015e 2016e 2017e

5.0 5.2 5.5

2012A 2013A 2014A 2015e 2016e 2017e

0.6 0.4 2.9

3.1 3.5

3.9

2012A 2013A 2014A 2015e 2016e 2017e

Organic

Others/ Licenses

3.8 3.9

6.9

Continued Growth

Continued Growth,

improving margin

CAPEX 2015-2017:

>R$14 billion

Net Revenues

EBITDA

CAPEX

48% 40% 37% 35%

52% 60% 63% 65%

2014a 2015e 2016e 2017e

Innovative

Traditional

Innovative and Traditional Investments (R$; %)

(R$ billion)

(R$ billion)

(R$ billion)

2015-2017 Guidance

MTR Impact Analysis (R$; %)

Mobile Net Revenues Analysis (R$; %)

A Close Look at Business Performance

24%

12%

31%

18%

2010 2011 2012 2013 2014 2015e 2016e 2017e

-15% -11% -25%

Net Services Revenues Exposure

EBITDA Exposure

-33% MTR Cut (% YoY)

2013a 2014a 2017e

Innovative:

Traditional:

Data Content

Other

Voice Incoming

SMS

+48%

-11%

% YoY

Near mid-single

-35% -44%

~5 bln

~9 bln

2012a 2013a 2014a

2012a 2013a 2014a

2012a 2013a 2014a

PERSPECTIVES

41

Safe Harbor Statements

TIM on the Web

Statements in this presentation, as well as oral statements made by the management of TIM Participações

S.A. (the “Company”, or “TIM”), that are not historical fact constitute “forward looking statements” that

involve factors that could cause the actual results of the Company to differ materially from historical results

or from any results expressed or implied by such forward looking statements. The Company cautions users

of this presentation not to place undue reliance on forward looking statements, which may be based on

assumptions and anticipated events that do not materialize.

TIM website: www.tim.com.br

Investor Relations website: www.tim.com.br/ir

TIM on Twitter: @TIMBrasil

Investor Relations Twitter: @TIM_RI

TIM on Facebook: www.facebook.com/timbrasil

TIM on YouTube: www.youtube.com/timbrasil

43