Embed Size (px)

Citation preview

COUNTRY REPORT

Indonesia

1st quarter 1999

The Economist Intelligence Unit15 Regent Street, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newslettersto annual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

London New York Hong KongThe Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit15 Regent Street The Economist Building 25/F, Dah Sing Financial CentreLondon 111 West 57th Street 108 Gloucester RoadSW1Y 4LR New York Wanchai United Kingdom NY 10019, US Hong KongTel: (44.171) 830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288Fax: (44.171) 499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638E-mail: [email protected] E-mail: [email protected] E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU Electronic Publishing New York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Jeremy Eagle Tel: (44.171) 830 1183 Fax: (44.171) 830 1023

This publication is available on the following electronic and other media:

Online databases Microfilm

FT Profile (UK) NewsEdge Corporation (US) World Microfilms Publications (UK)Tel: (44.171) 825 8000 Tel: (1.781) 229 3000 Tel: (44.171) 266 2202

DIALOG (US)Tel: (1.415) 254 7000 CD-ROM

LEXIS-NEXIS (US) The Dialog Corporation (US)Tel: (1.800) 227 4908 SilverPlatter (US)

M.A.I.D/Profound (UK)Tel: (44.171) 930 6900

Copyright© 1999 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

ISSN 0269-5413

Contents

3 Summary

4 Political structure

5 Economic structure

6 Outlook for 1999-2000

11 Review11 The political scene22 Economic policy26 The economy30 Sectoral trends34 Finance and banking 37 Foreign trade and payments

43 Quarterly indicators and trade data

List of tables9 Forecast summary

11 Economic results and forecasts22 State budget23 Budget assumptions26 Gross domestic product growth by sector27 Consumer price index28 Monetary aggregates28 Money supply, 199829 Maximum guaranteed interest rates31 Manufacturing output, 199831 Manufacturing survey responses32 Shoe production33 Tourist arrivals through the main gateways, Jan-Nov37 Merchandise trade by value, Jan-Nov38 Non-oil and gas exports, Jan-Nov 199838 Exports by category, Jan-Sep39 Main trading partners, Jan-Sep40 Balance of payments40 Gross foreign assets41 Crossborder claims on selected Asian countries43 Quarterly indicators of economic activity44 Foreign trade

Indonesia 1

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

List of figures11 Gross domestic product11 Rupiah real exchange rates27 Inflation29 Interest rates and the exchange rate37 Import compression

2 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

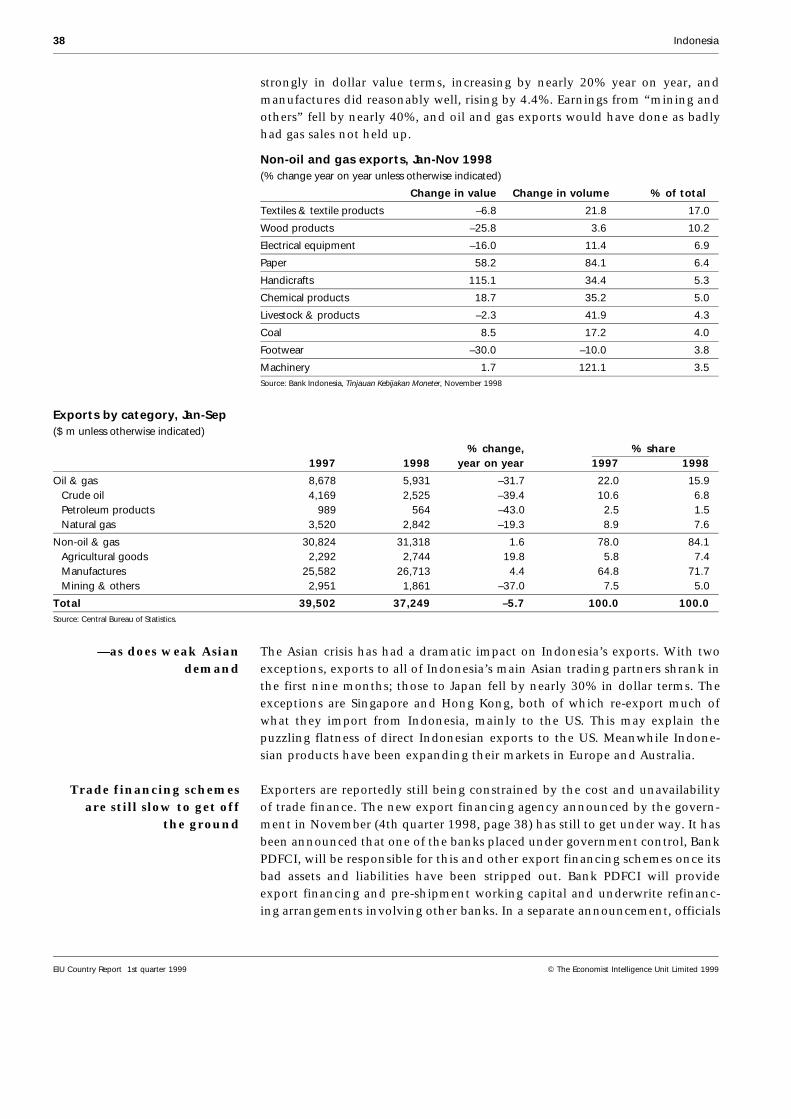

March 4th 1999 Summary

1st quarter 1999

Outlook for 1999-2000: In the current volatile political climate, the chancesof a stable outcome to the present transitional process have diminished but stillcannot be ruled out. GDP will contract again in 1999 as investment falls andexports grow only weakly. During the forecast period, despite high real interestrates, inflation will be higher than before the crisis. Severe import compressionwill continue to keep the current account in surplus.

The political scene: The political laws needed to hold more open parlia-mentary and presidential elections later this year have been passed. Golkar haslost another pillar of its traditional support. Mr Habibie’s star continues towane. Political parties have been mushrooming, but only a few are seriouscontenders for power. The unity of the Ciganjur group of opposition leadershas been tested. Suharto continues to play a political role from behind thescenes. Often violent social unrest shows no sign of abating, and there is someevidence that it is being manipulated for political ends. Separatist sentimenthas been mounting in Irian Jaya and Aceh. The government has offered EastTimor the option of independence.

Economic policy: The budget for 1999/2000 had a mixed reception, and wasamended slightly in parliament. Foreign financing looks like being adequate in1999/2000, and may be more than enough as a result of a reassessment of theimpact of the economic crisis. The government has lowered its unemploymentforecasts.

The economy: The economy shows no sign of having bottomed out. Afterseveral months of stability the rupiah has weakened, inflation has risen andinterest rates have nudged up. The monetary aggregates have remained undercontrol. Investors have been offered tax holidays as foreign investment approv-als slump.

Sectoral trends: Rice farmers are now facing problems of oversupply. Theimpact of the crisis on manufacturing has been uneven; textiles have faredbetter than footwear, for example. The car industry has been among the worsthit. Tourist arrivals fell sharply in 1998 and look like falling again in 1999.

Finance and banking: The bank recapitalisation plan has been delayed, andthe implications could be serious. The plight of the state banks is dire. Therehave been some false dawns on the Jakarta Stock Exchange.

Foreign trade and payments: Severe import compression has continued toboost the trade surplus. Weak prices and feeble Asian demand have hit exports,and trade financing is still scarce. The government expects another balance ofpayments surplus in 1999/2000. The reserves have been recovering. Externalprivate debt remains intractable.

Editor: Leo AbruzzeseAll queries: Tel: (44.171) 830 1007 Fax: (44.171) 830 1023

Indonesia 3

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

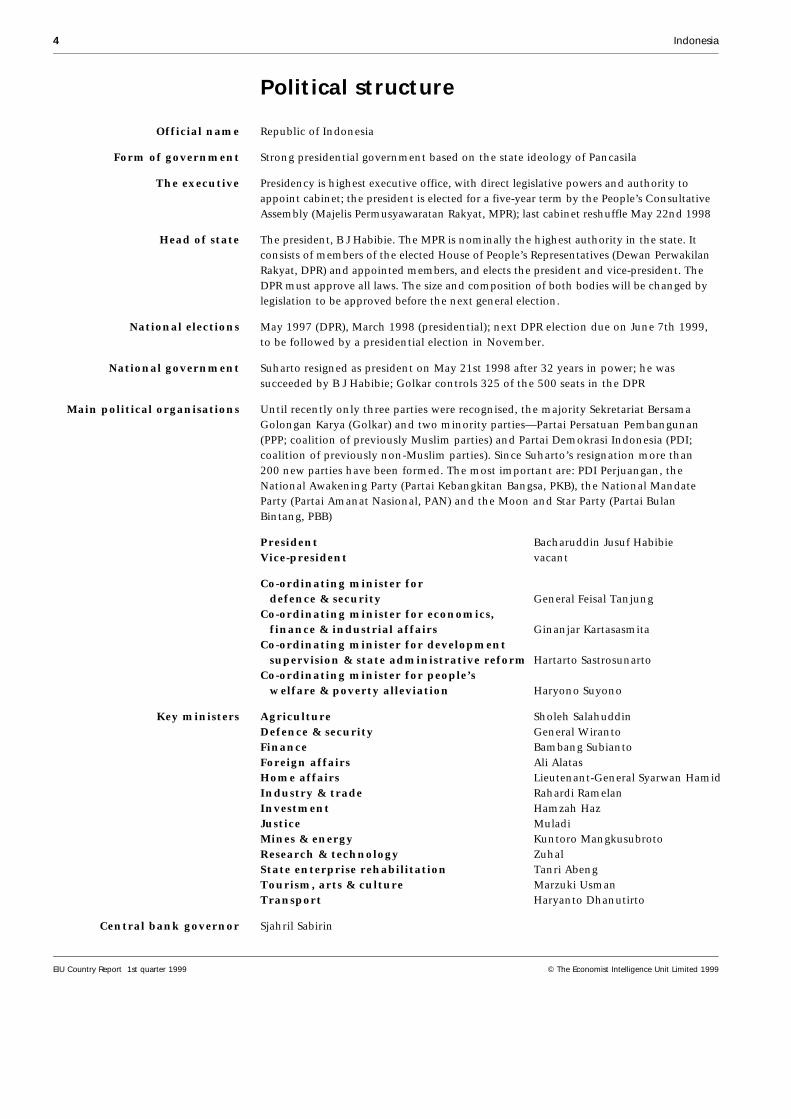

Political structure

Official name Republic of Indonesia

Form of government Strong presidential government based on the state ideology of Pancasila

The executive Presidency is highest executive office, with direct legislative powers and authority toappoint cabinet; the president is elected for a five-year term by the People’s ConsultativeAssembly (Majelis Permusyawaratan Rakyat, MPR); last cabinet reshuffle May 22nd 1998

Head of state The president, B J Habibie. The MPR is nominally the highest authority in the state. Itconsists of members of the elected House of People’s Representatives (Dewan PerwakilanRakyat, DPR) and appointed members, and elects the president and vice-president. TheDPR must approve all laws. The size and composition of both bodies will be changed bylegislation to be approved before the next general election.

National elections May 1997 (DPR), March 1998 (presidential); next DPR election due on June 7th 1999,to be followed by a presidential election in November.

National government Suharto resigned as president on May 21st 1998 after 32 years in power; he wassucceeded by B J Habibie; Golkar controls 325 of the 500 seats in the DPR

Main political organisations Until recently only three parties were recognised, the majority Sekretariat BersamaGolongan Karya (Golkar) and two minority parties—Partai Persatuan Pembangunan(PPP; coalition of previously Muslim parties) and Partai Demokrasi Indonesia (PDI;coalition of previously non-Muslim parties). Since Suharto’s resignation more than200 new parties have been formed. The most important are: PDI Perjuangan, theNational Awakening Party (Partai Kebangkitan Bangsa, PKB), the National MandateParty (Partai Amanat Nasional, PAN) and the Moon and Star Party (Partai BulanBintang, PBB)

President Bacharuddin Jusuf HabibieVice-president vacant

Co-ordinating minister for defence & security General Feisal TanjungCo-ordinating minister for economics, finance & industrial affairs Ginanjar KartasasmitaCo-ordinating minister for development supervision & state administrative reform Hartarto SastrosunartoCo-ordinating minister for people’s welfare & poverty alleviation Haryono Suyono

Key ministers Agriculture Sholeh Salahuddin Defence & security General WirantoFinance Bambang Subianto Foreign affairs Ali AlatasHome affairs Lieutenant-General Syarwan Hamid Industry & trade Rahardi Ramelan Investment Hamzah Haz Justice Muladi Mines & energy Kuntoro Mangkusubroto Research & technology ZuhalState enterprise rehabilitation Tanri AbengTourism, arts & culture Marzuki UsmanTransport Haryanto Dhanutirto

Central bank governor Sjahril Sabirin

4 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Economic structure

Latest available figures

Economic indicators 1994 1995 1996 1997 1998a

GDP at current market prices (Rp trn) 379.2 452.4 532.6 625.5 989.6

Real GDP growth (%) 7.5 8.2 8.0 4.9 –13.7

Consumer price inflation (av; %) 9.6 9.4 8.0 6.7 57.5

Population (m) 190.7 193.8 196.5 200.1 203.8

Exports fob ($ bn) 40.2 47.5 50.2 56.3 50.7

Imports fob ($ bn) 32.3 40.9 44.2 46.2 31.6

Current-account balance ($ bn) –2.79 –6.43 –7.66 –4.89 4.0

Reserves excl gold ($ bn) 12.13 13.71 18.25 16.59 22.71b

Total external debt (disbursed; $ bn) 107.82 124.40 128.94 135.59 155.93

Debt-service ratio, paid (%) 30.7 30.0 36.8 27.8 18.9

Exchange rate (av; Rp:$) 2,161 2,249 2,342 2,909 10,014b

March 4th 1999 Rp8,910:$1

Origins of gross domestic product 1997 % of total Components of gross domestic product 1997 % of total

Agriculture 16.1 Private consumption 62.2

Mining & quarrying 9.5 Government consumption 6.8

Manufacturing 25.6 Gross fixed capital formation 28.7

Construction 7.5 Change in stocks 2.9

Trade, hotels & restaurants 16.7 Exports of goods & services 27.9

Transport & communications 6.8 Imports of goods & services –28.5

GDP at market prices incl others 100.0 GDP at market prices 100.0

Principal exports fob 1997c $ m Principal imports cif 1997c $ m

Crude oil & products 6,783 Machinery & transport equipment 17,573

Natural gas 4,820 Other manufactures 6,491

Plywood 3,411 Chemicals 5,913

Ready-made garments 2,880 Fuels & lubricants 4,047

Textiles 2,389 Food, drinks & tobacco 3,223

Rubber 1,929 Raw materials 2,979

Total incl others 53,547 Total incl others 41,680

Main destinations of exports 1997 % of total Main origins of imports 1997 % of total

Japan 23.3 Japan 19.8

US 13.3 US 13.1

Singapore 10.2 Singapore 8.2

South Korea 6.6 Germany 6.3

China 4.1 Australia 5.8

Netherlands 3.4 South Korea 5.6

a EIU and official estimates. b Actual. c Customs basis.

Indonesia 5

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Outlook for 1999-2000

Politics remains highlyvolatile—

Politics in Indonesia is still in total flux, and predicting its direction over thenext two years is fraught with difficulty. A bewildering number of outcomes areconceivable, ranging from a stable solution to a nationwide breakdown of lawand order. Developing the worst of these scenarios is not difficult. State author-ity has been eroded to the point where it seems beyond the power of existingstate institutions to re-establish it. Political, ethnic and religious tensions haveincreased, and have often exploded into serious violence. The severe economiccrisis has heightened these problems, but the economy has not yet bottomedout and, despite a fragile stabilisation, several of the preconditions for recovery,including a functioning banking system and mechanisms for resolving thecorporate sector’s large external debt, are not yet in place.

—the government haslittle authority—

The president, B J Habibie, has not only failed to establish his legitimacy; hispolitical authority continues to wane. His always narrow political base is be-coming even narrower as he finds it increasingly difficult to accommodate itstwo main components, his Muslim allies and his backers within the armedforces, neither of whom is anyway prepared to give him more than conditionalsupport. He is not alone in being tainted by his long association with hispredecessor and mentor, Suharto. The key institutions of government, includ-ing the cabinet, the legislature and the armed forces (Angkatan BersenjataRepublik Indonesia, ABRI), are also still dominated by leftovers from theSuharto period.

Suspicion about the true loyalties of these people fuels the widely held view thatSuharto is still manipulating events from behind the scenes. This view gainscredibility from the new regime’s failure to bring the former president to acc-ount for the wealth he is alleged to have amassed during his time in office. It isalso widely believed that murky “status quo forces”, thought to be close toSuharto, if not actually acting on his behalf, are provoking some of the ethnicand religious violence in the hope of getting the parliamentary election sched-uled for June 7th called off and authoritarianism restored. The armed forces,overwhelmed by the nationwide epidemic of violence and discredited in theeyes of much of the population by the student killings of May and November1998 as well as by the revelation of earlier abuses committed during the Suhartoera, are themselves divided and seem powerless to stem the descent into chaos.

—and there are fears thatIndonesia’s break-up is

imminent

On top of the social and political divisions, separatist tendencies have beenintensifying, particularly in the provinces of Irian Jaya and Aceh. The newgovernment has recognised the need to dismantle the highly centralised powerstructure developed by Suharto, but its concessions are unlikely to allay separ-atist sentiment in the present inflamed climate, or even perhaps to satisfyresource-rich provinces which feel that they did not reap the benefits due tothem under Suharto’s development state.

The circumstances in which the former Portuguese colony of East Timor be-came part of Indonesia were very different from those in which the Indonesianrepublic initially came into existence, and the annexation of the territory,which has never been recognised by the UN, has been a permanent obstacle to

6 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Indonesia’s hopes of achieving international respectability. Offering inde-pendence to East Timor, as the government did for the first time on January27th, boosts its chances of winning international support when for economicreasons it most needs it. If, as expected, the people of East Timor take up theoffer, an increasingly intolerable drain on Indonesia’s financial and militaryresources will be removed. Nonetheless, from a domestic point of view the offerof independence to East Timor carries risks: of intensified separatist feeling aswell as of a backlash among army officers and nationalists who believe thatIndonesia’s prized unity may be at risk. The most prominent leader to emergefrom the popular opposition to Suharto, Amien Rais, is not alone in warningthat a Soviet- or Yugoslav-style break-up is a real possibility.

A turbulent election is inprospect—

Against this turbulent background, the chances are that the election period willbe turbulent too. There are already grounds for fearing that, with inter-commu-nal tensions high, political debate will be poisoned by sectarianism, and thatpolitics will be contested along communal lines, as it largely was until Suhartoput a stop to politics altogether in 1965. With national and local legislativeelections scheduled to be held simultaneously in June, nationally and locallybased conflicts will feed off each other. In the current economic and politicalclimate “money politics” might well distort the electoral outcome, particularlysince it seems that if the governing party, Golkar, has any real assets left, theyare its access to financial resources, both its own and the state’s.

—and it may not producea stable solution

There is no guarantee that the election to the House of People’s Representatives(Dewan Perwakilan Rakyat, DPR) will produce a stable solution. There will beno outright winner at the polls and in the post-election period there will beintensive deal-making and coalition-building, particularly in the interim pe-riod between the parliamentary election in June and the meeting of the highestconstitutional body, the People’s Consultative Assembly (Majelis Permusya-waratan Rakyat, MPR) in October-November to elect a president. The horse-trading needed to elect a president will almost certainly result in the diffusionof power and a compromise. The outcome could be an intolerable level ofpolicy incoherence that will create further pressure for an authoritarian solu-tion. The coming elections could therefore end up creating new political uncer-tainty rather than dispelling it.

But elections will be held— As already noted, this scenario is not the only possible one. Six months ago theEIU set out a benign scenario under which two political blocs would emerge tocontend for parliamentary and presidential power on the basis of the acceptedrules of the game (3rd quarter 1998, pages 6-7). This scenario now looks lessplausible, but a variant of it is still conceivable. The necessary political lawshave been passed and it looks as though the electoral process will proceed totimetable.

It still looks unlikely that a state of martial law will be proclaimed, whichwould short-circuit this process. President Habibie has no incentive to hold onto power without the legitimacy of an election. Only as a reforming president,faithful to his own electoral timetable, does he stand any change of retainingpower. In fact his chances of winning the presidency next November are slim.The main opposition parties, which no longer regard him as a serious threat to

Indonesia 7

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

their own political ambitions, are more or less prepared to accept him as thefigure who will oversee the transition. The murky political forces which wouldlike to see the parliamentary election cancelled are unlikely to persuade thearmed forces high command that martial law is a politically feasible option: thearmed forces are too discredited and too divided and the momentum of theelectoral process now too strong.

—and a benign outcome isstill possible

Only a handful of the more than 200 political parties that have emerged sinceSuharto’s overthrow will actually contest the election, and even fewer are seri-ous contenders. Three are expected to be the largest vote-winners: MegawatiSukarnoputri’s PDI Perjuangan, Abdurrahman Wahid’s Partai KebangkitanBangsa (National Awakening Party, PKB) and Amien Rais’s Partai AmanatNasional (National Mandate Party, PAN). Others, including Golkar, the PartaiPersatuan Pembangunan (National Development Party) and Partai Bulan Bin-tang (PBB), may win a place at the bargaining table in the coalition-buildingperiod after the parliamentary election. The leaders of the three main partieshave all announced their intention of standing for the presidency in November.

Though there are tensions between them (particularly between AbdurrahmanWahid and Amien Rais), all three are moderates, who may in the end be willingto share power or even settle on an acceptable compromise candidate, such asthe sultan of Yogyakarta, the fourth signatory of the joint opposition mani-festo, the Ciganjur declaration, last November, which was effectively reaf-firmed in late January (see The political scene). As was shown in the days afterthe Ciganjur declaration, the greatest challenge to such a consensus will comefrom below. It still remains to be seen whether the Jakarta politicians, even onewith the evident popular appeal of Megawati Sukarnoputri, can control theirgrass-roots supporters.

The preconditions foreconomic recovery are not

yet in place—

The economy continues to suffer from the effects of the economic crisis thathit the country in the latter half of 1997. The collapse of the rupiah left muchof the corporate sector unable to service its massive offshore debts, and deliv-ered a fatal blow to many of the country’s already weakened financial institu-tions. By sharply increasing import costs and forcing the government to adopta tight monetary stance to contain inflationary pressures, it also underminedcorporate profitability and prevented firms from taking take advantage of theincreased competitiveness which the currency depreciation should in principlehave afforded them.

The political and social unrest, partly triggered by the crisis, has in turn intens-ified it. One serious consequence of the unrest has been the flight of manyethnic Chinese (who are the main source of the country’s entrepreneurialskills) together with their capital. Politics also threatens to undermine anyprogress made in stabilising the economy. Thus, after the rupiah strengthenedand inflation and interest rates fell in the final quarter of 1998, politics were areason for the partial reversal of these trends in January 1999. External factorswere at work too. The collapse of the Brazilian Real put emerging markets ingeneral under scrutiny once more, and created new pressures on the rupiah asthe US dollar strengthened and rumours of a Chinese devaluation once againgained ground.

8 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

—and more externalshocks cannot be ruled out

Although we do not believe that the Chinese will devalue in 1999, there arelikely to be further devaluation scares which will send shockwaves around theAsian region. Thus, although we expect the rupiah to strengthen in 1999, theimpact of this on inflation and on reaching an agreement over the privatesector’s external debt overhang will be less beneficial than might be hoped, aswe expect the exchange rate to fluctuate quite erratically during the year. Thereason for the generally upward trend of the rupiah will be a sound balance-of-payments position, based mainly on a strong current account and large inflowsof official capital, and secondarily (and more problematically) on much health-ier net private capital flows, as outflows continue to decline.

Forecast summary($ m unless otherwise indicated)

1997a 1998b 1999c 2000c

Real GDP (% change, year on year) 4.9 –13.7 –3.0 1.6

Consumer price inflation (av; %) 6.7 57.5 12.8 11.0

Merchandise exports fob 56,297 50,667 50,630 52,190

Merchandise imports fob 46,223 31,617 30,568 32,738

Current-account balance –4,890 4,046 6,272 4,406

Average exchange rate (Rp:$) 2,909 10,014a 8,000 7,619

a Actual. b EIU and official estimates. c EIU forecasts.

Investment will fall againin 1999—

GDP is officially estimated to have contracted by 13.7% in real terms in 1998.In expenditure terms the component most badly hit by the crisis was invest-ment, which we estimate fell by 38%. The collapse of the banking system andIndonesia’s unresolved private external debt problem starved business of capi-tal. The prospects for both recapitalising the banks and resolving the privatedebt overhang are at best clouded. In the absence of a functioning bankingsystem and the resumption of private capital inflows, the preconditions for arecovery of private investment in 1999 will not be present. Instead, whateverbuoyancy the economy shows this year will come from unaccustomed sources:through government schemes for the provision of working capital, by stimulat-ing agricultural production and by improving the absorption of social safetynet funds, for example. The urban-based, often export-oriented industrial andservices sectors which provided most of the momentum for growth over thedecade leading up to the crisis will show little sign of recovery.

—and exports will belanguid

We expect some of the constraints which prevented exports from growing in1998 will ease in 1999. The EIU expects world trade growth to slow further, to4.3% from 4.6% last year, mainly on the basis of weaker demand in the US andthe EU. Partly offsetting this downturn will be the beginnings of recovery else-where in Asia, including Japan. Trade finance will become more readily avail-able, but with interest rates still high its cost will continue to be prohibitive formany exporters. As the rupiah stabilises in nominal terms, much of the compet-itive advantage gained from its massive depreciation will be eroded by inflationand, with prices still weak, agricultural commodity exporters will not enjoyanother currency windfall. The continued political uncertainty will further re-duce the number of tourists. We do, however, expect exports to be the onlydemand component to grow in 1999, even though by only 2%. Improving

Indonesia 9

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

external demand and the establishment of the domestic conditions for recoverywill permit a further, moderate acceleration of export growth in 2000.

Inflation will remainabove pre-crisis levels

In the final quarter of 1998 month-on-month inflation settled to moderatelevels from the extremely high rates seen earlier in the year. As a result, bothaverage and end-year inflation came in at levels just below those that had beenassumed by the government and the IMF. The stronger rupiah, the easing ofrice shortages and the stabilisation of money-supply growth, as injections ofliquidity assistance by Bank Indonesia (the central bank) into the banks and tosubsidise staples procurement tapered off, all helped bring inflation down. Anupturn in the consumer price index in January may have been a seasonal blip.

Domestic demand will remain weak throughout the forecast period. However,as developments in 1998 demonstrated, that alone will not guarantee lowinflation. Fiscal and monetary discipline could easily be lost as the electionsapproach, particularly if the government succeeds in catching up on the vastbacklog of aid-financed social security spending. We are assuming that realinterest rates will be kept strongly positive, not least because of the need tomaintain the banking system’s liquidity, as it undergoes another crisis of con-fidence that seems an almost inevitable consequence of the type of radicalrecapitalisation programme required to restore it to health.

Further exchange-rate instability and the resumption of high inflation wouldsimply add to the pressure for interest rates to remain high. Another burst ofmoney creation—possibly related to the election, possibly required by thedemands of the ailing banking system—could set inflation off again. Furthercuts in subsidies, including those on fuel and electricity, are possible later inthe year. And when the recovery begins, it will create new inflationary pres-sures. Replenishing stocks of imported goods will be costly in rupiah terms. Therecovery is likely to be uneven, leading to inflationary mismatches betweensupply and demand. We therefore forecast that inflation will fall sharply fromthe average rate of 57.5% recorded in 1998, but will remain in double digits,above pre-crisis levels,.

There will be furthersurpluses on thecurrent account

The crisis has had a superficially beneficial impact on Indonesia’s externaltrade and payments performance. However, this is largely the result of severeimport compression. As a result, the customary current-account deficit turnedinto a large surplus in 1998. We expect this pattern to persist in 1999 as exportsstagnate and imports contract further. On this basis we are forecasting that thetrade surplus will widen slightly and that, with trade-related services paymentsstable (the largest component on the invisibles side), the current-account sur-plus will widen again. This contrasts with the government’s forecast for1999/2000 which, on the basis of forecasts of more buoyant export and (moreimportant) import growth, projects a narrower surplus. We believe that only in2000 will the surplus begin to erode, as economic recovery stimulates a slowincrease in imports to more normal levels.

10 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Economic results and forecasts(Rp bn; constant 1993 market prices; % change year on year in brackets unless otherwise

indicated)

1997a 1998b 1999c 2000c

Private consumption 273,793 252,711 243,866 245,085 (5.5) (–7.7) (–3.5) (0.5)

Government consumption 31,850 27,710 26,463 26,463 (0.6) (–13.0) (–4.5) (0.0)

Gross fixed capital formation 134,133 83,162 77,341 76,954(4.5) (–38.0) (–7.0) (–0.5)

Change in stocks 4,733 1,500 2,500 5,500 (0.2)d (–0.7)d (0.3)d (0.8)d

Exports of goods & services 119,445 117,653 120,006 123,847 (6.3) (–1.5) (2.0) (3.2)

Imports of goods & services –129,858 –108,042 –106,745 –108,453 (6.6) (–16.8) (–1.2) (1.6)

GDP 434,096 374,694 363,431 369,396 (4.9) (–13.7) (–3.0) (1.6)

a Official data. b EIU estimates. c EIU forecasts. d As a percentage of GDP in the previous year.

Review

The political scene

The political laws arepassed on deadline—

Another important milestone en route to this year’s parliamentary and pres-idential elections was passed on January 28th, when the House of People’sRepresentatives (Dewan Perwakilan Rakyat, DPR) approved the three politicallaws changing the rules under which the parliamentary election scheduled forJune 7th will be fought. Differences emerged over three contentious matterscovered in the bills—whether active civil servants should be allowed to bemembers and officers of political parties; what sort of electoral system shouldbe used; and the number of DPR seats to be allocated to the armed forces—and

40

50

60

70

80

90

100

110

120

1990 91 92 93 94 95 96 97 98 99 2000

Rupiah real exchange rates (c)1990=100

Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$Rp:$

Rp:¥

Rp:$

Rp:¥Rp:¥

Rp:DMRp:DMRp:DM

Rp:$

Rp:¥

Rp:$

Rp:¥Rp:¥

Rp:DMRp:DMRp:DM

97 98(a) 99(b) 2000(b)

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:$

Rp:¥

Rp:DM

97 98(a) 99(b) 2000(b)97 98(a) 99(b) 2000(b)97 98(a) 99(b) 2000(b)97 98(a) 99(b) 2000(b)97 98(a) 99(b) 2000(b)

-15

-10

-5

0

5

10

1996 97(a) 98(a) 99(b) 2000(b)

Indonesia

Asia excl Japan

Gross domestic product% change, year on year

(a) EIU and official estimates. (b) EIU forecasts. (c) Nominal exchange rates adjusted for changes in relative consumer prices.Sources: EIU; IMF, International Financial Statistics; World EconomicOutlook.

Indonesia 11

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

there was some doubt whether the January 28th deadline for passing the legis-lation would be met.

—after Golkar makesconcessions

Despite its overwhelming majority in the DPR, Golkar in the end yielded to theopposition of all the three other parliamentary “fractions” (including the armedforces—Angkatan Bersenjata Republik Indonesia, ABRI—fraction), as well asthreats from extra-parliamentary groups, and accepted that the country’s 4.1mcivil servants should no longer be allowed to play an active role in politics. Thestrongest opposition to the three bills—on political parties, the electoral systemand the composition of the national and local legislatures—came from theUnited Development Party (Partai Persatuan Pembangunan, PPP). Havingwrung concessions from Golkar on civil servants and the less contentious issueof the electoral system, the PPP dropped its other objections, including itsdemand for a much reduced number of ABRI seats. The final law gives ABRI 38seats in the DPR (down from the current 75), and 10% of the seats in localassemblies. Many parties not represented in the DPR continue to argue that anyABRI presence in the house is unconstitutional. The electoral system—propor-tional representation (PR) based on the province—is a variant of the old one thattended to favour locally based candidates The government had originally pro-posed a first-past-the-post system based on the second tier of local government,the district, and then came out in favour of a district-based PR system. The otherfractions had argued that the latter system would favour Golkar which, becauseof the discriminatory provisions of the old law on political parties, is believed tohave the most developed organisation at local level.

Main points of the political laws

• The election will be run on a multiparty system.

• To be eligible to contest the DPR election a party has to be represented in at leastnine provinces and in half of the districts in each of these nine provinces.

• The DPR will have 500 members (as now) and the MPR 700 (previously 1,000),comprising the 500 members of the DPR, 135 regional representatives and 65representatives of social and mass organisations.

• ABRI, whose members will not vote in elections, will automatically receive 38 seatswith voting rights.

• Civil servants may not join political parties, unless with the approval of theirimmediate superiors, and must take leave of absence if they wish to take part inpolitical activities.

• The voting system will be proportional representation based on the province, butto be elected candidates must gain a plurality in their constituencies.

• The national election committee shall consist of five government representativesand one representative of each political party eligible to contest the election.

12 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Golkar continues tocrumble—

The political laws probably dealt another blow to Golkar’s prospects in theforthcoming election. Tainted by its close association with the old regime,since May 1998 Golkar has also lost the two main forces which used to ensureit massive votes in DPR elections, the armed forces and the bureaucracy. Themilitary high command has declared its neutrality in the elections. Many ofthe retired senior officers, who used to form the backbone of the Golkar execu-tives in the provinces, have deserted the party for the newly created PartaiKeadilan Persatuan, led by a former defence minister, Edi Sudradjat. Mr Sudrad-jat lost the battle for the Golkar chairmanship last July to Mr Habibie’s statesecretary, Akbar Tanjung (3rd quarter 1998, page 15). The support of the armedforces commander, General Wiranto, was probably vital to Mr Akbar’s victory.However, Mr Akbar with his modernist Muslim background is not a naturalbedfellow for the secular nationalist General Wiranto, who appears more com-fortable with like-minded politicians such as the leader of PDI Perjuangan,Megawati Sukarnoputri. Another powerful military man, the minister of homeaffairs, Lieutenant-General Syarwan Hamid, has affirmed the neutrality of thecivilian bureaucracy, which under the old system was required to vote forGolkar.

The election timetable

February 1st-March 1st: Registration of parties.

March 1st-April 15th: Registration of candidates for the DPR and localassemblies (DPRD).

March 16th-April 17th: Registration of voters.

May 18th-June 6th: The election campaign.

June 7th: Election day.

June 20th-26th: Announcement of results of elections for district levelassemblies (DPRD II).

June 27th-July 2nd: Announcement of results of elections for provincial levelassemblies (DPRD I).

July 3rd-12th: Announcement of results of DPR election.

July 20th: DPRD II members sworn in.

July 25th: DPRD I members sworn in.

August 29th: DPR and MPR members sworn in.

October 28th-November 10th: MPR session to elect new president.

Indonesia 13

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Other groups have also deserted Golkar. A number of its component “func-tional groups” have also left for other parties. Several of its most effectivepoliticians, such Siswono Yudohusodo and Sarwono Kusumaatmadja, havejoined Megawati Sukarnoputri’s PDI Perjuangan. The party itself has cast outthe Suhartoists, (known as the Cendana group after the street where the Suhar-tos have their family house), which has meant the loss of an important sourceof funds (see below).

—and its two principalfactions—

What is left are two main factions, grouped around Mr Habibie and Mr Akbarrespectively. Their organisational bases are quite small: ICMI (Ikatan Cen-dekiawan Muslimin Indonesia, the Association of Muslim Intellectuals, theMuslim modernist organisation set up by Mr Habibie in 1991) supportsMr Habibie, and KAHMI (the alumni society of the Himpunan Mahasiswa Islam,a modernist Muslim student group, which peaked in the 1960s) and KNPI (thenational youth organisation) support Mr Akbar. There have been moves withinGolkar to break with Mr Habibie as the symbol of a past with which Golkar itselfneeds to break. (In January Mr Akbar, after much pressure from within the party,apologised for Golkar’s past “wrongdoings and mistakes”.) Mr Habibie has alsobeen trying to take a distinctive position: during the debates on the politicallaws, for instance, he took a more “presidential”, less partisan stance thanMr Akbar by coming out in favour of a neutral civil service.

—cannot agree on Habibiefor president

Perhaps the best indication of the party’s factionalisation is the large numberof candidates for the presidency and the vice-presidency being floated. Theyinvolve various permutations of Mr Habibie, Mr Akbar, General Wiranto, theco-operatives minister, Adi Sasono, the party chairman Marzuki Darusman andthe sultan of Yogyakarta. Faced with the prospect of a much reduced Golkarvote in the DPR election and uncertain of the party’s support, Mr Habibie hasbeen looking for support elsewhere. Feelers have been put out to three Muslimparties—the United Sovereignty Party (Persatuan Daulat Rakyat, PDR), theUnited Development Party (Partai Persatuan Pembangunan, PPP) and theMoon and Star Party (Partai Bulan Bintang, PBB). All of them are expected to doreasonably well in the election, and precisely for that reason may not want tolink their fates to that of Mr Habibie.

Mr Habibie’s starcontinues to wane

Mr Habibie is still regarded as Suharto’s creature, particularly after publicationof what is apparently a genuine transcript of a tapped telephone conversationwith his attorney-general about the ongoing investigation into Suharto’swealth (see below). His public attack on Suharto’s disgraced son-in-law, Lieu-tenant-General Prabowo Subianto, did not go down well with some of thelatter’s Muslim allies, who are influential in the PBB. Opinion polls takenbefore these two embarrassments for the president already showed him trailingas third or fourth choice for president with 10% or less of the vote. He is notregarded as a useful ally.

Mr Sasono keeps everyoneguessing

One great unknown is the political agenda of the populist (and popular) min-ister of co-operatives, Adi Sasono. Mr Sasono has received a lot of attention inthe press, chiefly for his promotion of a “people’s economy” (in the foreignpress he has been dubbed “Indonesia’s most dangerous man”, sometimes with

14 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

a question mark, sometimes without), but his political intentions remain un-clear. Mr Sasono is formally a Golkar chairman, who could have been an effec-tive vote-winner for the party. His political constituency is Muslim smalltraders, farmers and fishermen, and his ministry controls large amounts offunds earmarked for the needy. Adi Sasono has denied reports that he will leaveGolkar for the newly created Partai Daulat Rakyat (Sovereign People’s Party),which was formed by close associates to appeal to the same constituency as hedoes. But he has said that he will not campaign for Golkar, justifying hisdecision on the grounds that the funds at his disposal as a minister wouldcreate a conflict of interest.

Political parties havemushroomed—

Of the more than 200 parties that have come into existence since Suharto leftoffice, 141 registered at the Ministry of Justice during the registration periodthat ended on March 1st (see box: The election timetable). At most, 60 of theseare expected to cross the next hurdle—screening by an independent committeeto establish whether they truly meet the criteria set out in the political partieslaw. Some will then merge and others will collapse. The most common predic-tion is that 25-35 parties will actually contest the election.

—but only a few areserious contenders—

Of these only a handful will be serious contenders, capable of getting 5% ormore of the vote and thus winning a place at the bargaining table when itcomes to forming a coalition after the election. They are: Megawati Sukarnopu-tri’s PDI Perjuangan, Abdurrahman Wahid’s Partai Kebangkitan Bangsa (Nat-ional Awakening Party, PKB), Amien Rais’s Partai Amanat Nasional (NationalMandate Party, PAN), the former government vehicle Golkar, and perhaps twoMuslim parties, the PBB and the PPP. PDI Perjuangan is expected to win thelargest number of votes and its leader, Megawati Sukarnoputri, is the front-run-ner for the presidency.

—and even they will needto build coalitions

Most observers expect PDI Perjuangan to win 30-40% of the vote. The partyitself predicted in mid-February that it would win 210 of the 462 elective seats inthe DPR, or 45% of the vote. Even then, it would still need to build a coalitionto secure a majority. Party officials have said that a coalition involving the PKBor PAN or both was a possibility. The PAN leader, Amien Rais, has said that a PDIPerjuangan-PAN coalition is conceivable. But Megawati Sukarnoputri andAbdurraham Wahid are natural allies, whereas neither is with Amien Rais.

PAN sets out its stall At its national working meeting held in Bandung in December, PAN nomi-nated, Amien Rais, as its presidential candidate. Amien Rais became the leadingvoice of popular opposition during the demonstrations against Suharto lastyear. PAN was launched last August as a non-sectarian party, but because of itsleader’s own roots in the Muhammadiyah organisation it also has a Muslimbase. The urban elite and the Muslim modernists to whom PAN appeals are notalways easy bedfellows, and there have been signs of strain within the party.

Amien Rais’s reformist credentials remain more or less intact, however. He isstill prepared to take to the streets. He is steadfastly anti-Suharto and his NewOrder, including ABRI’s dwifungsi (its dual security and political function). Hebelieves that despite Suharto’s fall the power structure that he created is stillintact. He has been outspokenly critical of military abuses, most recently in

Indonesia 15

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Aceh. He has called for the replacement of the attorney-general, Andi Ghalib,for his half-hearted investigation into Suharto’s wealth. He has been eager topursue recent headline corruption cases. He is vulnerable for his espousal offederalism and possibly for his economic policies (he favours the redistributionof assets and a more inward-looking industrial strategy and is open to the ideaof a currency board).

The Ciganjur group’sunity is tested—

Harmony among the four signatories of the Ciganjur declaration was predict-ably brief. The declaration was signed by four major opposition figures—Abdurrahman Wahid, Amien Rais, Megawati Sukarnoputri, and the sultan ofYogyakarta, Sri Sultan Hamengku Buwono X—on the eve of last November’sMPR session (4th quarter 1998, pages 12-13). In particular AbdurrahmanWahid and Amien Rais have been airing their differences.

—and just about holds up In December Abdurrahman Wahid embarked on a series of controversial meet-ings, which some saw as an attempt to snatch the initiative from Amien Rais.In the name of national reconciliation Abdurrahman Wahid (Gus Dur) metGeneral Wiranto on December 9th, President Habibie on December 12th andthen most controversially Suharto on December 13th and again on December19th. He then called for a four-way meeting, involving Mr Habibie, GeneralWiranto and Suharto (“as a person with a large following”) as well as himself.He suggested that Suharto’s followers had been angered at seeing their mentor“cornered” and had provoked some of the worst of the recent violence inJakarta, West Timor, East Java and South Sulawesi (see below) in retaliation.This brought a sharp rebuke from Amien Rais, who accused Gus Dur of engag-ing in political manoeuvres on his own as well as breaching the Ciganjurdeclaration, one of whose ten points was an agreement to seek an investigationof the former president’s wealth. Amid mounting nationwide turmoil a newtruce between the opposition leaders, brokered by General Wiranto, came intobeing on January 24th, but strains persist.

Suharto remains at thecentre of politics

It is widely believed that Suharto is still pulling strings with a view to disrupt-ing the transition process—as well as the investigations into his and his fam-ily’s wealth. On May 21st last year, the day Suharto resigned, the armed forcescommander, General Wiranto, publicly pledged to protect him. Some, includ-ing Mr Habibie and his attorney-general, Andi Ghalib, have called for publicrestraint in the treatment of Suharto out of respect for his age and achieve-ments, and are thought to have set an example by themselves showing re-straint in their handling of the ex-president. It is widely presumed that Suhartois being protected from prosecution by officials who themselves have some-thing to hide. Hence the power of the veiled threat issued by Suharto’s lawyerlast December that, if a case were brought against Suharto, it would also dragdown “government officials, ex-officials and all the cronies also suspected ofimproper gains through corruption, collusion and nepotism”.

Abdurrahman Wahid, who is also the leader of the traditionalist Muslim organ-isation Nahdlatul Ulama, has also taken a conciliatory stance, though for dif-ferent reasons (see below). This restraint is being shown despite the passage bythe MPR (constitutionally the highest political institution) last November of aresolution calling for Suharto’s wealth to be investigated. Other family mem-

16 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

bers have been summoned for questioning by the Attorney-General’s Office,including most recently Siti Hardiyanti Rukmana (Tutut) on February 4th toanswer questions about one of her charitable foundations. However only oneimmediate member of the family, the former president’s youngest son,Hutomo (Tommy) Mandala Putra, looks in danger of prosecution.

Mr Habibie’s failure to set up an independent commission to investigateSuharto’s wealth following the MPR resolution (4th quarter 1998, page 16) wasseen as a sign of his half-heartedness. More damning confirmation thatMr Habibie was going easy on Suharto came in the weekly magazine, PanjiMasyarakat, on February 22nd. The magazine published what purported to bethe transcript of a telephone conversation between the president and AndiGhalib. The two discussed the attorney-general’s questioning of Suharto onDecember 9th 1998 in terms that suggested that neither man took the investig-ation entirely seriously. The content of the conversation was important—someMPs wanted to question the president to see if he had violated the MPR resolu-tion, which would be possible grounds for impeachment. But no less strikingwas the fact that the tape appeared to be authentic, meaning that there werepeople tapping the president’s phone and leaking the results to the press,something inconceivable in Suharto’s day.

The shaming of GeneralPrabowo continues—

While the authorities have been proceeding gingerly in the case of Suharto,there has been a concerted high-level campaign to discredit further his son-in-law, Lieutenant-General Prabowo Subianto. General Prabowo was dismissedfrom the army in August 1998, after an inquiry found that he had orchestratedsome of the worst violence during the Jakarta riots of May 1998. The trial of 11soldiers accused of the abduction of political activists in the months leading upto Suharto’s overthrow, in which General Prabowo has already been implic-ated, has been under way since December. In February Mr Habibie accusedGeneral Prabowo of having surrounded the presidential palace with troops onthe day after he was sworn in as president, with the aim of forcing him out ofoffice. General Prabowo issued a detailed riposte from exile in Jordan. His alliessay that he is being made a scapegoat for the armed forces’ transgressions in theperiod around the downfall of Suharto.

On January 4th the military high command announced a large-scale reshuffle,involving 100 senior officers and clearly aimed at consolidating the position ofGeneral Wiranto and at helping to restore ABRI’s reputation. Among thoseremoved were a number of highly placed Prabowo supporters, most with strongIslamic leanings, including the ABRI general chief of staff (the armed forces’number three job), Lieutenant-General Fachrul Razi, and the head of militaryintelligence, Major-General Zacky Anwar Makarim. Their replacement—by theformer army deputy chief of staff, Lieutenant-General Sugiono, and the formercommander of the Central Java Diponegoro division, Major-General TyasnoSudarto—did not reassure those who continue to see the controlling hand ofSuharto in all things. Both men, like General Wiranto himself, had been adju-tants to the former president. Two regional commanders who had failed tocontain violence in their areas (East Java and North Sumatra) were also removed.

Indonesia 17

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

—as ABRI seeks toreposition itself—

Within ABRI there has been some soul-searching about its role under Suharto’sNew Order. The need to rethink the doctrine of dwifungsi (the double functionof the armed forces which gives it a socio-political as well as a security role) hasbeen acknowledged. Dwifungsi became the pretext for many of the less savouryaspects of New Order politics under Suharto: the armed forces’ direct manipula-tion of political activity (including the use of terror), the ubiquitous internalsecurity apparatus, the military’s extensive business activity and a commandstructure that exactly mirrored (and shadowed) the structure of the civilianbureaucracy. There have been few opportunities for calm reflection about theprocess of (in official jargon) “redefining, repositioning and reactualising” ABRIin the current turbulent climate. Five key members of the 23-strong cabinet areactive senior officers, as are about 40% of the country’s provincial governors.

—and cope with mountingunrest

Instead, beleaguered by violence of various kinds throughout the archipelago,ABRI has been casting around vainly to find a response. Changes in structure,such as the separation of the police from the armed forces, to take effect inApril, seem almost irrelevant. Partly because the military’s reputation has beenso badly sullied by its past and recent conduct, many of its responses to thecrisis, such as a plan to set up a 40,000-strong civilian auxiliary force or theissuing of orders to shoot rioters, are widely presumed to be in bad faith. (Theuse of civilian “volunteers” to assist with security during the MPR session inNovember undoubtedly aggravated the violence on that occasion and was apublic relations disaster for General Wiranto—4th quarter 1998, pages 11-12).

A few senior officers are reported to have been pressing for the imposition ofmartial law. Probably reckoning that it would be deeply unpopular (not leastbecause forcing the government to declare martial law was said to be an objec-tive of the Suharto group and therefore would be regarded as tending to con-firm suspicions that Suharto was still controlling events) and would not restorestability anyway, the majority of the high command is against such a move.Instead, General Wiranto has taken measures to quell rioting that fall someway short of a declaration of martial law, although one of them—a plan an-nounced on February 4th to set up a Special Task Force Unit with extra-legalpowers—sounded to some like martial law in disguise. The new unit, under thecommand of the national police chief, General Roesmanhadi, is a 3,300-strongforce drawn from the army, navy and air force and from police special units.On March 1st a battalion from the rapid-reaction force was despatched toAmbon to try to control the escalating violence there.

Social unrest takes manyforms—

Elite politics continues to be conducted against a backdrop of intense socialunrest, much of it violent, which takes a bewildering variety of forms, rangingfrom gang warfare to separatist movements. There was a partial lull duringRamadan, which was most fully observed by the students, but the violencepicked up with a vengeance once the fasting month was over. During the daysof Lebaran, the holiday celebrating the end of Ramadan, several incidents werereported. Some were for reasons related to the holiday, such as workers notreceiving the usual annual bonus.

Economic desperation still drives much of the unrest. Aside from pure crimi-nality—the plundering of plantations, forests and shrimp farms, highway rob-

18 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

bery and so on—there are protests and occupations relating to land disputes.Suppressed economic grievances, for example of communities that have suf-fered the effects of polluting factories, have also been surfacing, as in Porsea,North Sumatra, where protests against Indorayon’s textile plant have turnedviolent. Protests against local officials continue to take place on a massive scale.In the district of Cirebon in the six months to February, protests were heldagainst 81 of the 421 village heads accused of corruption, collusion and nepo-tism, (korupsi, kolusi dan nepotisme, KKN).

Even in apparently clear-cut instances, where religion (as in the Christian-Muslim violence in eastern Indonesia) or separatism (as in Aceh, North Suma-tra) is apparently the trigger for the violence, other factors are at play. Theinter-communal violence between Christians and Muslims in Ambon andneighbouring islands was triggered by a fight on January 19th between a Mus-lim migrant and a local Christian minibus driver. However, murky politicalmanoeuvring, economic grievances, ethnic tensions, gang rivalries and separ-atist sentiment all seem to have played a part in the ensuing violence which bythe end of February had taken at least 160 lives. Ethnic, religious and economicgrievances as well as the desire to avenge human rights abuses committed bythe military under the previous regime (3rd quarter 1998, page 21) are all fuel-ling the separatist movement in Aceh.

—including a political one There are grounds for thinking that the violence will feed into the elections.Already there have been reports of clashes between supporters of rival parties—between Golkar and PDI Perjuangan supporters in Bali and between PPP andPKB supporters on the north coast of Java. In late February in Lampung PDIPerjuangan supporters attacked the chairman of Partai Demokrasi Indonesia,Budi Hardjono. There is also a danger that communal differences and griev-ances will be channelled through political parties. Leaders of the main partieshave already fallen into line with the government’s proposal that outdoorrallies be kept to a minimum during the campaign.

Fears of election violence are increased by the widely held belief that much ofthe current violence is being manipulated for political ends, and is aimed atgetting the DPR election either cancelled or, if held, discredited. The finger hasbeen pointed at various groups, among them:

• Suharto supporters, either acting spontaneously or at his behest, to discreditthe reform process, and protect the Suharto family’s economic interests;

• extreme Muslim supporters of President Habibie seeking to discredit hisopponents and give him a justification to crack down on them;

• dissident elements within the armed forces seeking to weaken the authorityof the current military leadership and General Wiranto in particular, possiblywith a view to taking over control of the government;

• unscrupulous political leaders seeking to improve their chances in the elec-tions; and

• discontented elements seeking to create chaos and instability for their ownparticular reasons.

Indonesia 19

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

The most commonly held view is that the current explosion of violence isbeing orchestrated by “status quo forces” (comprising Suhartoists and elementsof ABRI and the civilian bureaucracy). These suspicions are fanned by themilitary leadership’s habit of blaming provocateurs or conflicts among thepolitical elite for the violence, while rarely succeeding in attaching blame toanyone. An investigation by the traditionalist Muslim organisation, NahdlatulUlama, into the wave of mysterious killings in the Banyuwangi area of East Java(4th quarter 1998, page 12) found that the 239 identified killings there wereacts of “political terror”, involving senior ABRI and local government officialsas well as deserters from elite units. At the same time the recent reassessment ofthe impact of the crisis (see Economic policy) has put in question the conven-tional diagnosis that economic deprivation is the main reason for the currentexplosion of violence. There are of course still other explanations—forexample, that it is the explosion of anger at grievances allowed to fester over 30years of authoritarian government.

A dirty war breaks out inAceh—

Separatist feeling is strong, and growing, in the provinces of Irian Jaya andAceh, on the country’s eastern and western extremes. The Habibie governmentseems willing to offer some kind of enhanced autonomy but, as in the case ofEast Timor (see below), that may not be enough, particularly in the northSumatran province of Aceh. A cycle of kidnappings and killings by both armyand separatists has been under way there since the end of December. In the late1980s Aceh was made a Special Military Operations Zone (DOM) to allow themilitary to suppress an insurgent independence movement, Aceh Merdeka.The discovery last July of the mass graves of Aceh Merdeka fighters created anuproar, and forced the government to end Aceh’s DOM status. Amid risingtensions and increased activity by Aceh Merdeka, there has now been a build-up of troops again in the province. Tentative moves have been made to contactAceh Merdeka’s exiled leader, Hasan di Tiro, but his main objective seems to beto negotiate independence.

—and the Irianese test thenew regime’s political

limits

In Irian Jaya (called West Papua by independence forces) reformasi has beenconfronting old-style military repression. A popular “national dialogue” on theprovince’s future status is under way (sparked by a letter to Mr Habibie from agroup of US senators). Those taking part in the dialogue have been intimidatedand in some cases charged with rebellion. People involved in raising the flag ofan independent West Papua (3rd quarter 1998, page 21) have been chargedwith subversion. By contrast, on February 26th a 99-strong delegation of tribal,religious leaders and other notables from Irian Jaya held a meeting withMr Habibie in which several asked that the province be given independence.According to the government news agency, Antara, Mr Habibie reacted calmly.

An independence offer forEast Timor—

On January 27th the government made what sounded like a breakthroughoffer on East Timor, the former Portuguese colony which Indonesia invadedand annexed in 1975-76. If the East Timorese rejected Indonesia’s proposal ofbroad autonomy, the government would be willing to “let go” of the territorywithin a year. It would do this not, as had been proposed by pro-independenceEast Timorese, after an interim period of autonomy leading to a referendum,but as soon as it could gain the necessary approval of the MPR. Mr Habibie

20 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

subsequently made it clear that he wanted the Timor issue resolved one way orthe other by the end of this year. As a gesture of good faith the East Timorindependence leader, Xanana Gusmão, was released from prison to housearrest on February 11th.

This shift in policy took place on the eve of the latest round of UN-sponsoredtriangular talks, involving Indonesia, Portugal (which the UN still regards asthe administering power) and the UN. A government spokeswoman, DewiFortuna Anwar, explained that Australia’s announcement of its own majorpolicy change on East Timor on January 11th had been decisive. Australia,which had been the only Western country to recognise Indonesian sovereigntyover the territory, proposed instead that the people of East Timor should beallowed to vote on independence after a period of autonomy. According toMs Anwar, the Australian announcement pulled the diplomatic rug from un-der the Indonesians just as they were about to enter the talks.

—causes shock— The Indonesian offer was unexpected for two reasons. It had generally beenpresumed that no Indonesian government would offer East Timor inde-pendence: first, because of the precedent it would set for Indonesian provinceswith separatist leanings; second, because ABRI would veto it, on securitygrounds and for reasons of pride. The explosion of unrest throughout thearchipelago, including separatist unrest, has changed the security argument:the need for ABRI to deploy 20,000 troops in East Timor at a time when theyare needed elsewhere meant that holding on to East Timor actually made itmore likely that Indonesia would fragment. Publicly at least, the armed forcesseem willing to swallow their pride: General Wiranto has said they wouldcomply if it were decided that East Timor was no longer part of Indonesia.

—and some initialdisbelief—

The improbability of an Indonesia turnaround on East Timor caused many todoubt that the offer was being made in good faith, particularly as on theground pro-integration militias, issued with arms by the Indonesian military,were stepping up their activity. Although opening up the possibility of inde-pendence, the government made clear that its preference was that East Timorshould remain part of Indonesia with broad autonomy. The upsurge of militiaactivity was viewed by some observers as a warning that if East Timor chose tobe “let go” the outcome could be a bloody civil war, and therefore was anattempt to force the East Timorese to accept its offer of autonomy. The take-it-or-leave-it tone of the initial offer, including its apparent rejection of the pro-independence leadership’s call for an interim period of autonomy underIndonesian rule, tends to support the view of the Indonesians’ bad faith.

—and may still fall foul ofdomestic politics

Indonesia’s preferred outcome is likely to be overridden by the wishes of the US,Australia and the EU, which by late February were putting together the diplo-matic machinery to smooth East Timor’s transition to independence. The great-est obstacle to East Timor’s independence may now be the stance of MegawatiSukarnoputri’s PDI Perjuangan. Megawati, the current favourite to be Indone-sia’s next president, has come out against the government’s offer, although byearly March there were signs that her party was rethinking its position.

Indonesia 21

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

Economic policy

A non-transparent budgetfor 1999/2000—

On January 6th President Habibie introduced a budget for the 1999/2000 fiscalyear (April-March) in which expenditure was projected to fall 17.3% below thefinally budgeted amount for 1998/99. Since the 1998/99 outturn is likely todiffer greatly from the final 1998/99 budget, this comparison is not very useful.In the first half of 1998/99 domestic revenues were just about on target, butspending, and in particular capital spending, was way below it (4th quarter1998, page 19). If that trend continued to the end of the year, the budget wason track to record a surplus of 0.7% of GDP, rather the projected 8.5% deficit.There will certainly be some real cuts in expenditure in 1999/2000: the largestprojected fall in spending, on debt servicing, is explicable in terms of a strongerrupiah. But other “cuts”, such as the 9.7% reduction in capital spending, willprobably not turn out to be cuts at all. The likely large gap between the 1998/99budget and the 1998/99 outturn may explain why Mr Habibie suggested that itwas an expansionary budget which would allow public spending to be themotor of the economy.

State budget(Rp bn)

Budget Budget % change,1998/99 1999/2000 year on year

Oil & gas company taxes 49,711.4 20,965.0 –57.8

Non-oil & gas revenue 99,591.1 119,838.8 20.3 of which: income tax 25,846.2 40,626.0 57.2 value added tax 28,940.0 34,697.4 19.9 import duties 5,494.9 2,950.3 –46.3 excise duties 7,755.9 9,360.0 20.7 export tax 942.8 2,594.5 175.2 non-tax receipts 26,660.3 25,799.1 –3.2

Domestic revenue 149,302.5 140,803.8 –5.7

External funds 114,585.6 77,400.0 –32.5 Programme aid 74,044.7 47,400.0 –36.0 Project aid 40,540.9 30,000.0 –26.0

Total revenue 263,888.1 218,203.8 –17.3

Recurrent expenditure 171,205.1 134,555.5 –21.4 of which: personnel expenditure 24,781.4 32,037.1 29.3 domestic debt service 1,940.1 380.1 –80.4 foreign debt service 64,296.3 44,430.8 –30.9 fuel oil subsidy 27,534.0 9,985.8 –63.7

Capital expenditure 92,683.0 83,648.3 –9.7 Rupiah financed 52,142.1 53,648.3 2.9 Project aid 40,540.9 30,000.0 –26.0

Total expenditure 263,888.1 218,203.8 –17.3

Balance 0.0 0.0 0.0

Public savingsa –21,902.6 6,248.3 –

a Domestic revenue minus recurrent expenditure.

Source: Ministry of Finance; Business News.

22 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

—gets a mixed reception— The largest expenditure items were wages, debt servicing and (controversially)bank recapitalisation. There was also a large increase in the total allocation forthe provinces, which under various headings were allocated Rp53.6trn (nearlyone-quarter of total spending). The sharp cut in fuel oil subsidies may portendlarge price increases (though part of the cut will be due to the lower assumedinternational oil price—see Budget assumptions table).

Some of the revenue projections look overoptimistic. In a depressed economicclimate value-added tax may not be as buoyant as expected. In 1998/99 incometax receipts were boosted by high interest income, but if interest rates resumetheir downward trend (as the government desires) takings may not be as high.Though generally well received (far better than Suharto’s disastrous first at-tempt at the 1998/99 budget in January 1998—1st quarter 1998, page 25),doubts such as these led some observers to question the budget’s assumptions.In particular, the assumed GDP growth rate and exchange rate came under thespotlight. There were other criticisms. One related to the Rp18trn allocation forbank recapitalisation, which is regarded by some members of the House ofPeople’s Representatives (Dewan Perwakilan Rakyat, DPR) as the misuse ofpublic money to bail out reckless bankers. Another condemned the budget astoo “populist”, particularly in its redirection of funds to the provinces. At thesame time it was also criticised for an increase in spending on personnel whichwas well below the rate of inflation.

Budget assumptions1998/99 1999/2000

GDP growth (%) –12.0 0,0

Consumer price inflation (%; year-end) 66.0 17.0

Crude oil price ($ per barrel) 13.00 10.50

Oil production ( ’000 barrels/day) 1,520 1,520

Exchange rate (Rp:$; year-end) 10,600 7,500Source: Ministry of Finance, Nota Keuangan dan RAPBN Tahun Anggaran 1999/2000.

—and some adjustmentsin the DPR

The budget was passed by the DPR on February 26th with a few changes thattook some of these criticisms into account. Overall budget spending was in-creased by Rp1.4trn to Rp219.6trn. Within this total there was a Rp1.5trn(4.8%) increase in spending on civil servants’ pay (from Rp32,037bn toRp33,569bn), which was offset by a Rp1trn cut in the appropriation for thebank recapitalisation programme and Rp500bn of cuts elsewhere. The Rp1.4trnoverall increase is to be covered by raising receipts from excise tax by Rp800bn,from Rp9.36trn to Rp10.16trn, with the rest coming from increased non-taxrevenues, mainly higher dividends from state enterprises.

Foreign financing lookslike being adequate—

In the 1999/2000 budget, unlike this year’s, public savings (domestic revenue minusrecurrent expenditure) are projected to be positive. However they will cover only7.5% of rupiah-financed development spending, leaving another large hole to befilled by aid. The budget projects an aid requirement of Rp77.4trn ($10.3bn at theassumed exchange rate of Rp7,500:$1), compared with the current fiscal year’sRp114.6trn ($10.8bn at the assumed Rp10,600:$1 rate).

By mid-February the government seemed well on the way to reaching this target:

Indonesia 23

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

• $2.4bn had been promised under Japan’s Miyazawa plan (of which $1.5bn isto come from the Japan Export-Import Bank and $900m from the OverseasEconomic Co-operation Fund—OECF);

• $1bn from the World Bank; and

• $1bn from the Asian Development Bank in 1999/2000—out of $1.52bn inpolicy-based loans which the Bank expects to commit to Indonesia this year.

The remaining $1.9bn was expected to be secured at the annual meeting ofIndonesia’s aid consortium, the Consultative Group on Indonesia (CGI), inJune. This amount could also be more than covered by the rescheduling of debtsdue for repayment in 1999/2000. The minister of finance, Bambang Subianto,told the DPR recently that the government wanted to reschedule $800m ofbilateral debt and $1.9bn of export credits due to mature in the coming fiscalyear. The Japanese government has said that it will start disbursing its newlycommitted funds before the June election. There have also been reports that theIMF too may make an additional commitment of quick-disbursing funds beforethe election. This apparent surfeit of capital will come in useful if (or when) therupiah comes under attack during and after the election.

—and may be more thanadequate—

It is possible that not all of this capital will flow, however, first, because it maynot all be needed and, second, because it may not all be disbursed. At a meetingof the CGI, held in Jakarta on January 25th, 80 representatives of bilateral andmultilateral donor organisations reviewed the progress of Indonesia’s reformprogramme and assessed the impact of international aid on the country. Denisde Tray, the country director of the World Bank, which chairs the CGI, saidthat all aspects of the reform programme—not just the social safety net pro-gramme but the corporate and financial sector programmes as well—must becarried out transparently and efficiently. In fact there are doubts about allaspects of the programme, from the bank recapitalisation plan to the provisionof a social safety net. The World Bank and the IMF may both defer loandisbursements if the bank recapitalisation programme does not go ahead soon(see Finance and banking).

—as the crisis’s impact isreassessed—

With regard to the social safety net, two recent developments particularly influ-enced thinking at the meeting. The first concerned the true social impact of theeconomic crisis; the second was the government’s slow disbursement of socialsafety net funds. Earlier doubts about assessments of poverty levels in the wakeof the crisis (4th quarter 1998, pages 26-27) have been supplemented by doubtsabout its impact on employment and education (on employment, see below).Both developments may cause Indonesia’s capital needs also to be reassessed.There was a hint of this when Mr de Tray said that Indonesia would need $9bnto finance its budget deficit rather than the $10.3bn initially projected.

—and aid disbursement isslow

The slow disbursement of aid for social projects has many causes. There havebeen allegations about the mishandling of aid from Japan and Singapore. Thereis also plenty of evidence of the maladministration of social safety net funds onthe ground. The International Non-Governmental Organisation Forum onIndonesian Development (INFID) has written to the World Bank president,James Wolfensohn, urging him to postpone the disbursement of the social

24 Indonesia

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

safety net fund until there is “a change in concept, design, target and method-ology”. A government-appointed monitoring committee has also been critical.The Bank has said that it is considering postponing delivery of funds until therequirements for independent monitoring, complaint mechanisms and trans-parency are in place. Barely 30% of the Rp17.79trn allocated for social safetynet spending during 1998/99 had actually been disbursed as of mid-February.On February 18th the government announced that donors and “independentparties” would be involved in monitoring the disbursement of social safety netfunds in the light of protests over lack of transparency and alleged corruption.

There were also allegations of the politicisation of the distribution processbecause the agencies charged with channelling funds had been packed withgovernment or Golkar supporters. There have even been suggestions that dis-bursements were purposefully delayed so that more funds could be distributedcloser to the election. To avoid the tainting of the programme by moneypolitics, opposition politicians have proposed that it should be suspended inthe two months leading up to the election.

The government scalesdown its unemployment

projections—

The government seems to have tacitly scaled down some of its own assess-ments. Last October the minister of manpower, Fahmi Idris, said that one-fifthof the workforce of 92.6m (about 18.5m) was then unemployed and that thetotal would rise to 20m (22% of the workforce) by the end of the year. Theministry arrived at these figures by using GDP/employment elasticity modelsrather than by actual surveys in the field. Such projections had already beencontested by, among others, the International Labour Organisation and theUN Development Programme, which in a joint report published in June 1998had argued that, although the crisis would result in large-scale labour displace-ment, this would not translate into big increases in open unemployment; in acountry such as Indonesia where wages are downwardly flexible and socialsafety nets are minimal, it would instead lead to the spread of work in theinformal sector. It therefore estimated that the number of openly unemployedpeople as of mid-1998 was no more than 6.7m, 7.2% of the labour force.

Surveys undertaken in the past year by government and international agencieshave borne out these conclusions: the proportion of the population in paidlabour seems to have risen, unemployment is up only slightly but real wageshave fallen sharply. Apparently accepting the thrust of this argument, onFebruary 18th Mr Idris told a seminar in Jakarta that unemployment was nowexpected to rise to 16.86m in 1999. The increase was expected largely becauseof the 3.2m people expected to enter the workforce this year.

—and offers a meagreincrease in the minimum

wage

One signal that real wages would fall again in 1998/99 came with the an-nouncement on February 18th that the regional minimum wage is to rise by anaverage of 16.1% in the year beginning April 1st, not nearly enough to make upfor the preceding year’s inflation. A ministry official said that the higher mini-mum wage would be sufficient to cover only 70% of workers’ daily minimumneeds (less than the 76% covered by the minimum wage rise of last October).Last year’s increase was just 15% and came into effect only on August 1st 1998because of the disruption caused by the economic and political crisis (3rdquarter 1998, page 27). For the first time the government is also to set sectoral

Indonesia 25

EIU Country Report 1st quarter 1999 © The Economist Intelligence Unit Limited 1999

minimum wages. So far 19 of the country’s 27 provinces have set sectoralminimum wages after discussions between employers’ and workers’ repre-sentatives. The sectoral minimum wage is intended to take into account whatindividual sectors can afford to pay in current circumstances.

The economy

The economy has not yethit bottom—