Embed Size (px)

Citation preview

COUNTRY REPORT

Switzerland

3rd quarter 1996

The Economist Intelligence Unit

15 Regent Street, London SW1Y 4LR

United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 40 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newslettersto annual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

London New York Hong KongThe Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit15 Regent Street The Economist Building 25/F, Dah Sing Financial CentreLondon 111 West 57th Street 108 Gloucester RoadSW1Y 4LR New York Wanchai United Kingdom NY 10019, USA Hong KongTel: (44.171) 830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288Fax: (44.171) 499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638

Electronic deliveryEIU Electronic Publishing New York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Moya Veitch Tel: (44.171) 830 1007 Fax: (44.171) 830 1023

This publication is available on the following electronic and other media:

Online databases CD-ROM Microfilm

FT Profile (UK) Knight-Ridder Information World Microfilms Publications (UK)Tel: (44.171) 825 8000 Inc (USA) Tel: (44.171) 266 2202

DIALOG (USA) SilverPlatter (USA)Tel: (1.415) 254 7000

LEXIS-NEXIS (USA)Tel: (1.800) 227 4908

M.A.I.D/Profound (UK)Tel: (44.171) 930 6900

Copyright© 1996 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author�s and the publisher�s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

Symbols for tables�n/a� means not available; ��� means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

ISSN 0269-6169

Summary

Switzerland 3rd quarter 1996

August 30, 1996

Political and economic structures pages 2-3

Outlook: Growing public unease may lead to protests but employers will keep

the upper hand. Voters� nervousness will slow progress on EU bilateral talks.

Wide-ranging reform and liberalisation is planned. The recovery, led by exports,

will be feeble and unemployment will rise. The franc will provide no respite for

exporters to Europe. Tourism income will be weak but the current account will

remain strong. pages 4-8

The political scene: EU talks are dragging but a vote on EU and EEA member-

ship is possible in 1998. A cheese scandal has been uncovered. Swiss beef is still

banned by some countries. Forced repatriation of Bosnians has been postponed.

Heavier regulation of IVF practices is likely. A new sex equality law has come

into force. pages 8-12

Economic policy: Revenue is running lower than budgeted and cutbacks will

hit the public sector and the unemployed. The cartel law has come into force.

There is resistance to the liberal labour law. Funding for social security and

sickness insurance is causing disquiet. Energy is to be liberalised and reforms of

rail are planned. Expansionary monetary policy continues. pages 12-19

The economy: Private consumption has been stagnant and capital equipment

growth has slowed, but export growth has been better than expected. The

inflation rate has fallen, but unemployment has gone up. pages 19-23

Foreign trade and payments: Export and import values have increased and

the services surplus has risen, although tourism income has dropped sharply.

The franc eased but then rebounded in July. pages 23-25

Financial news: Large-scale restructuring is due for the big banks. The elec-

tronic bourse is on stream. Money-laundering rules are to be tightened again. A

deeper investigation into Holocaust victims� accounts is under way.

pages 25-28

Business news: Power firms are to offer a telephone service. Von Roll has sold

its steelmaking to von Moos. Swissair has bought into duty-free businesses and

casinos and has antitrust immunity for a multi-company marketing alliance.

Klaus Jacobs has extended his chocolate empire. ABB has encountered problems

with its Malaysian dam project. pages 28-31

Statistical appendices pages 32-34

Editor:

All queries:

Fiona Mullen

Tel: (44.171) 830 1007 Fax: (44.171) 830 1023

Switzerland 1

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

Political structure

Official name: Swiss Confederation

Form of state: federal republic

Legal system: based on constitution of 1874

National legislature: bicameral Federal Assembly (parliament), comprising the National Council and Council

of States. National Council of 200 members directly elected by proportional representation using the

Hagenbach-Bischoff quota, except in the smallest cantons where the single representative is elected by the

plurality (first-past-the-post) system. Council of States of 46 members representing the cantons. Any law passed

by both houses may be submitted to a referendum if demanded by eight cantons or 50,000 citizens

Electoral system: universal direct suffrage over age 18

Last federal election: October 22, 1995

Next federal election due: October 1999

Head of state: the de facto head of state is the president of the Federal Council, although constitutionally this

role is filled by the council as a whole

State legislatures: each of the 26 cantons and half-cantons has a parliament elected by universal suffrage and

a government whose organisation varies from canton to canton. In five, the principle of universal sovereignty is

exercised directly through assemblies of all voters. The cantons are sovereign in all areas not specifically

entrusted to the federal government

National government: Federal Council (the executive authority) of seven members elected for a four-year

term by, but not necessarily from, the Federal Assembly. The president and vice-president are elected for a

one-year term which is not immediately renewable. Since 1959 the Federal Council has contained two members

each of the Social Democratic Party, the Radical Democratic Party, and the Christian Democratic Party, and one

member from the Swiss People�s Party. The Federal Council was re-elected in December 1995

Main political parties: Radical Democratic Party (RDP); Social Democratic Party (SDP); Christian Democratic

Party (CDP); Swiss People�s Party (PP); Liberal Party; Ecology Party; Independent Alliance

The Federal Council

President & minister of public economy Jean-Pascal Delamuraz (RDP)

Vice-president & minister of justice & police Arnold Koller (CDP)

Ministers

defence Adolf Ogi (PP) finance Kaspar Villiger (RDP)

foreign affairs Flavio Cotti (CDP) interior & environment Ruth Dreifuss (SDP) transport, communications & energy Moritz Leuenberger (SDP)

Central bank president Hans Meyer

2 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

Economic structure

Latest available figures

Economic indicators 1991 1992 1993 1994 1995

GDP at market prices Swfr bn 331.1 338.8 342.9 351.9 359.4

Real GDP growth % 0.0 �0.3 �0.8 1.2 0.7

Consumer price inflation % 5.9 4.0 3.3 0.9 1.8

Population m (mid-year) 6.79 6.90 6.94 6.99 7.04

Exportsa fob $ bn 74.3 79.9 75.4 82.6 93.6b

Importsa fob $ bn 78.9 80.2 73.9 79.3 92.3b

Current accounta $ bn 10.4 14.2 17.8 18.5 19.9b

Reserves excl gold $ bn (Dec) 29.0 33.3 32.6 34.7 36.4

Gross public debtc % of GDP 33.7 38.3 43.7 46.4 48.0

Exchange rate (av) Swfr:$ 1.43 1.41 1.48 1.37 1.18

August 30, 1996 Swfr1.20:$1; Swfr0.81:DM1

Origins of gross domestic product 1990d % of total Components of gross domestic product 1994 % of total

Agriculture 3.1 Private consumption 58.8

Industry 26.3 Government consumption 14.3

Construction 8.4 Fixed investment 22.8

Services 62.2 Stockbuilding �0.6

Total at factor cost 100.0 Exports of goods & services 36.2

Imports of goods & services �31.5

Total 100.0

Principal exports 1995 $ m Principal imports 1995 $ m

Machinery 23,217 Machinery 17,350

Chemicals 19,988 Chemicals 11,002

Precision instruments, watches & jewellery 12,665 Vehicles 8,983

Metals & metal manufactures 7,073 Metals & metal manufactures 7,553

Textiles, clothing & shoes 3,350 Agriculture, forestry products & fish 6,839

Total incl others 77,976 Textiles, clothing & shoes 6,710

Precision instruments, watches & jewellery 4,743

Total incl others 76,928

Main destinations of exports 1995 % of total Main origins of imports 1995 % of total

EU-15 62.6 EU-15 80.8

Germany 24.5 Germany 34.8

France 9.7 France 11.7

Italy 7.8 Italy 10.5

UK 5.2 UK 4.4

USA 8.4 USA 5.8

Japan 3.9 Japan 3.3

EFTA4 0.6 EFTA4 0.4

a IMF source; not comparable with some national sources. b EIU estimate. c National definitions. d OECD figures. Switzerland does not publish

figures on GDP by origin.

Switzerland 3

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

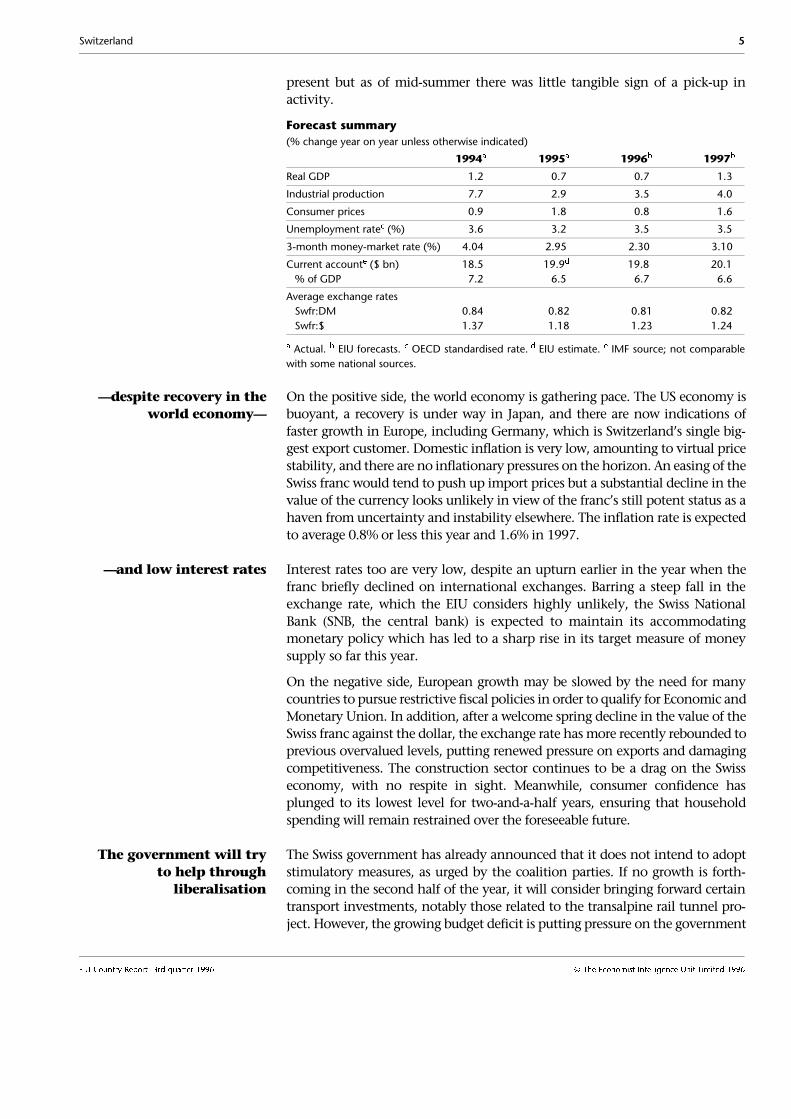

Outlook

Unease may lead to

protest�

Although Switzerland remains one of the strongest economies in the world, two

lean years of slow growth, rising unemployment and wide-scale restructuring

have made the Swiss increasingly nervous about their future. Companies are

now asking workers to accept cuts in wages in further efforts to increase compet-

itiveness, but it appears that Swiss workers have had enough. While it is true

that, notwithstanding their high levels of productivity, Swiss workers are among

the highest paid in the world, companies� efforts to claw back in this way profit

margins lost to the strong franc are beginning to meet with resistance, even

from government (see The political scene).

However, although there will be protests, they are unlikely to lead to strikes,

which are rare in Switzerland. Also, as workers may be faced with the chance of

pay cuts or no job at all, in general employers will have the upper hand.

�and further delay to EU

bilateral talks

Another manifestation of voters� unease is that they are more likely than ever

to resist pressure to open up Swiss markets to the EU. The government will

continue to argue that integration with the EU is in Switzerland�s best interests,

but persuading the electorate will take a long time. Thus, the bilateral talks

with the EU are unlikely to be formally over, with referendum and parlia-

mentary approval, until after 1997.

Fiscal tightening will

target expenditure�

The federal deficit in 1996 is threatening to exceed the budgeted Swfr4bn

($3.4bn), about 1.1% of GDP. This is particularly alarming for the authorities in

view of the fact that in 1994 and 1995 the government did succeed in pushing

the deficit below budget. A sluggish economy has dampened revenue, while

higher unemployment in the first half of the year, compared with the year-

earlier period, has pushed up unemployment payments. Fiscal policy will

therefore be tightened over the next two years and the finance minister, Kaspar

Villiger, is already seeking an immediate Swfr1.6bn cut in spending in 1996.

Federal expenditure is likely to be the principal target for immediate cuts and

there will probably be restrictions on pay rises and staff reductions in the public

sector. The unemployed will also be affected, as the five-day delay before a

person can collect benefit is likely to be extended.

�and reforms to the

public sector and social

security

The lower house of parliament, the National Council, has called for a balanced

budget by 2000, one year earlier than planned. The government has already

embarked on a programme to keep expenditure down in the long term.

Agricultural subsidies will be reduced; funding for social security will be

increased through a possible mixture of value-added tax (VAT), energy taxes

and increased contributions; the retirement age for women may be raised to 65;

and Swiss Railways is to be restructured (see Economic policy).

Recovery will be feeble� The current stagnation of the Swiss economy reflects the continuing strength

of the franc and the difficult situation in the important construction industry.

Slow growth in Europe, Switzerland�s biggest export market, has also been an

important factor, as have efforts by federal and local government to put their

finances in order. The conditions for a recovery towards the end of 1996 are

4 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

present but as of mid-summer there was little tangible sign of a pick-up in

activity.

Forecast summary

(% change year on year unless otherwise indicated)

1994a 1995a 1996b 1997b

Real GDP 1.2 0.7 0.7 1.3

Industrial production 7.7 2.9 3.5 4.0

Consumer prices 0.9 1.8 0.8 1.6

Unemployment ratec (%) 3.6 3.2 3.5 3.5

3-month money-market rate (%) 4.04 2.95 2.30 3.10

Current accounte ($ bn) 18.5 19.9d 19.8 20.1

% of GDP 7.2 6.5 6.7 6.6

Average exchange rates

Swfr:DM 0.84 0.82 0.81 0.82

Swfr:$ 1.37 1.18 1.23 1.24

a Actual. b EIU forecasts. c OECD standardised rate. d EIU estimate. e IMF source; not comparable

with some national sources.

�despite recovery in the

world economy�

On the positive side, the world economy is gathering pace. The US economy is

buoyant, a recovery is under way in Japan, and there are now indications of

faster growth in Europe, including Germany, which is Switzerland�s single big-

gest export customer. Domestic inflation is very low, amounting to virtual price

stability, and there are no inflationary pressures on the horizon. An easing of the

Swiss franc would tend to push up import prices but a substantial decline in the

value of the currency looks unlikely in view of the franc�s still potent status as a

haven from uncertainty and instability elsewhere. The inflation rate is expected

to average 0.8% or less this year and 1.6% in 1997.

�and low interest rates Interest rates too are very low, despite an upturn earlier in the year when the

franc briefly declined on international exchanges. Barring a steep fall in the

exchange rate, which the EIU considers highly unlikely, the Swiss National

Bank (SNB, the central bank) is expected to maintain its accommodating

monetary policy which has led to a sharp rise in its target measure of money

supply so far this year.

On the negative side, European growth may be slowed by the need for many

countries to pursue restrictive fiscal policies in order to qualify for Economic and

Monetary Union. In addition, after a welcome spring decline in the value of the

Swiss franc against the dollar, the exchange rate has more recently rebounded to

previous overvalued levels, putting renewed pressure on exports and damaging

competitiveness. The construction sector continues to be a drag on the Swiss

economy, with no respite in sight. Meanwhile, consumer confidence has

plunged to its lowest level for two-and-a-half years, ensuring that household

spending will remain restrained over the foreseeable future.

The government will try

to help through

liberalisation

The Swiss government has already announced that it does not intend to adopt

stimulatory measures, as urged by the coalition parties. If no growth is forth-

coming in the second half of the year, it will consider bringing forward certain

transport investments, notably those related to the transalpine rail tunnel pro-

ject. However, the growing budget deficit is putting pressure on the government

Switzerland 5

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

to make expenditure restraint a priority, so the speeding up of such investment

projects is by no means guaranteed. The government�s main way of aiding the

economy will be by liberalisation of cartels, labour laws, agriculture, pharma-

ceuticals and energy. Lower company taxes are also in prospect (see Economic

policy).

The recovery will be led

by exports�

Switzerland will once again trail at the bottom of the west European league table

in terms of real GDP growth rates. The recovery will be led by exports, which

have remained remarkably buoyant despite the strong franc and weak growth in

Europe and should profit from improvements in both. Better than expected

growth in exports has led us to revise up our GDP growth forecast slightly, to

0.7% in 1996 and 1.3% in 1997. Domestic demand will also increase, propelled

mainly by a high level of investment spending on plant and equipment.

Consumer spending will rise feebly as households continue to be worried about

jobs and income security. These fears have been exacerbated by recent

announcements of wage cuts in the public sector and big job losses in a series of

mergers and company cutbacks (see Economic policy). Although real incomes

are expected to rise by about 1% this year and next, the gains will be eroded by

higher health insurance premiums. Savings will remain high.

A 15% annual drop in new construction orders in the first quarter, and an 11%

fall in building permits issued, point to a continued fall in construction invest-

ment this year and into next. Vacant residential and commercial property still

overhangs the market and little stimulus is likely from the public sector. The

decline in construction may be more pronounced in the German-speaking

part of the country where the industry has so far suffered less than in French-

speaking areas.

�but unemployment will

remain high by historical

standards

Most investment spending will continue to be aimed at rationalisation and

efficiency gains designed to improve productivity. Coupled with slow

economic growth, this means that employment will rise only slightly next year

and unemployment remain high by historical standards. Small and medium-

sized companies, which dominate the Swiss economy, have fallen behind the

big multinationals in restructuring their activities to take account of the strong

franc and other competitive pressures. Surveys suggest that this sector expects

to shed many more jobs this year after delaying hard decisions in the hope of

an early economic recovery. We expect the unemployment rate, on OECD

standardised definitions, to rise to 3.5% in 1996-97. On national definitions,

the rate is likely to be in the region of 4.6%.

Small firms are feeling the full force of the strong Swiss franc as they have little

opportunity for production outside Switzerland. They are also at a disadvan-

tage because Switzerland is not a member of the EU. Switzerland�s big com-

panies have already restructured or are in the process of doing so (see Financial

news and Business news), shifting both production and sourcing abroad. This

in turn has put additional pressure on small Swiss-based suppliers. Industry

surveys show clearly that, for both goods and services, sectors dominated by

international firms have done far better than those where small firms are

concentrated. In services, for instance, banks and insurance companies have

6 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

posted good results in the past year or so, while hotels, restaurants and shops

have suffered.

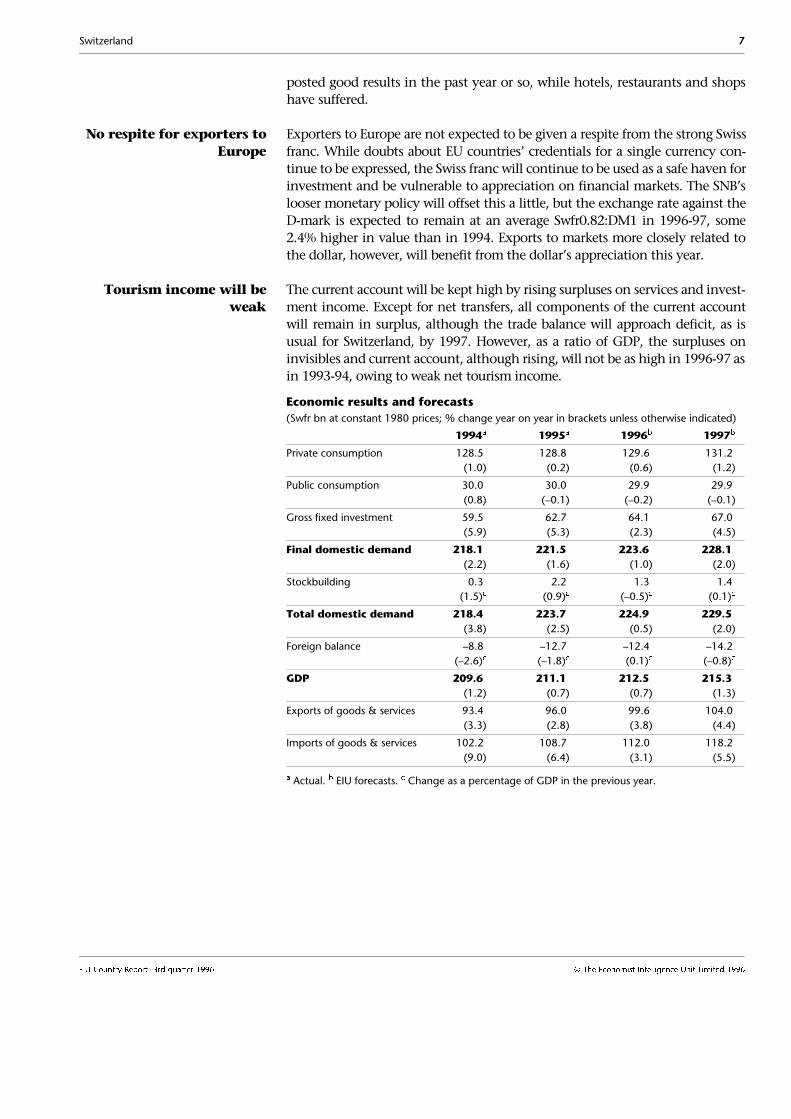

No respite for exporters to

Europe

Exporters to Europe are not expected to be given a respite from the strong Swiss

franc. While doubts about EU countries� credentials for a single currency con-

tinue to be expressed, the Swiss franc will continue to be used as a safe haven for

investment and be vulnerable to appreciation on financial markets. The SNB�s

looser monetary policy will offset this a little, but the exchange rate against the

D-mark is expected to remain at an average Swfr0.82:DM1 in 1996-97, some

2.4% higher in value than in 1994. Exports to markets more closely related to

the dollar, however, will benefit from the dollar�s appreciation this year.

Tourism income will be

weak

The current account will be kept high by rising surpluses on services and invest-

ment income. Except for net transfers, all components of the current account

will remain in surplus, although the trade balance will approach deficit, as is

usual for Switzerland, by 1997. However, as a ratio of GDP, the surpluses on

invisibles and current account, although rising, will not be as high in 1996-97 as

in 1993-94, owing to weak net tourism income.

Economic results and forecasts

(Swfr bn at constant 1980 prices; % change year on year in brackets unless otherwise indicated)

1994a 1995a 1996b 1997b

Private consumption 128.5 128.8 129.6 131.2

(1.0) (0.2) (0.6) (1.2)

Public consumption 30.0 30.0 29.9 29.9

(0.8) (�0.1) (�0.2) (�0.1)

Gross fixed investment 59.5 62.7 64.1 67.0

(5.9) (5.3) (2.3) (4.5)

Final domestic demand 218.1 221.5 223.6 228.1

(2.2) (1.6) (1.0) (2.0)

Stockbuilding 0.3 2.2 1.3 1.4

(1.5)c (0.9)c (�0.5)c (0.1)c

Total domestic demand 218.4 223.7 224.9 229.5

(3.8) (2.5) (0.5) (2.0)

Foreign balance �8.8 �12.7 �12.4 �14.2

(�2.6)c (�1.8)c (0.1)c (�0.8)c

GDP 209.6 211.1 212.5 215.3

(1.2) (0.7) (0.7) (1.3)

Exports of goods & services 93.4 96.0 99.6 104.0

(3.3) (2.8) (3.8) (4.4)

Imports of goods & services 102.2 108.7 112.0 118.2

(9.0) (6.4) (3.1) (5.5)

a Actual. b EIU forecasts. c Change as a percentage of GDP in the previous year.

Switzerland 7

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

Review

The political scene

Bilateral negotiations

with Brussels drag on

The Swiss government has become increasingly impatient with the slow pace of

bilateral talks with Brussels. Despite the adoption by Switzerland in April of a

more flexible negotiating position (2nd quarter 1996, pages 8-9), the discussions

have dragged on with little apparent progress and no firm date for their con-

clusion. EU officials have indicated that the end of this year could be realistic,

but this is not a target or deadline as the Swiss had hoped. In July EU foreign

ministers said only that progress had been made in the negotiations and called

for an agreement to be reached �as soon as possible�.

The bilateral talks, begun in December 1994 at Switzerland�s instigation, are

intended to ameliorate some of the disadvantages to Switzerland of the rejection

by Swiss voters in 1992 of membership of the European Economic Area (EEA)

which links the EU and three European Free Trade Association (EFTA) countries.

The negotiations cover seven topics: air and road transport, agriculture,

research, technical barriers to trade, government procurement and the free

movement of people.

The Swiss reject free

movement of persons�

The free movement of people, the most sensitive issue for Switzerland, remains

the main sticking-point. Brussels continues to insist on an agreed timetable for

scrapping Switzerland�s work permit quotas (although it is prepared to concede

a safeguard clause allowing the Swiss to reimpose immigration controls if there

is an unexpected influx of foreigners). However, Switzerland has refused to

concede the principle of free circulation. It has offered only to improve the lot

of the 800,000 EU citizens already living in Switzerland and to return to the

free circulation issue in five years� time.

�and insist on Alpine

freight taxes

On road transport, another difficult area for Switzerland, Brussels says that

Swiss road taxes designed to discourage transit freight traffic should be based

on costs and should not be out of line with taxes in neighbouring EU countries

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1993 94 95 96(a) 97(a)

Switzerland

EU

Gross domestic product % change on previous year

(a) EIU forecast. (b) Nominal exchange rates adjusted for changes

in relative consumer prices.Sources: EIU; IMF, International Financial Statistics.

70

80

90

100

110

120

1990 91 92 93 94 95 96(a) 97(a)

Swiss franc: real exchange rate (b)1990=100

Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$Swfr:$

Swfr:¥

Swfr:$

Swfr:¥Swfr:¥

Swfr:DMSwfr:DMSwfr:DM

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥Swfr:¥

Swfr:DMSwfr:DMSwfr:DM

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:$

Swfr:¥

Swfr:DM

8 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

such as Austria and France. In April the Swiss government said it would be

prepared to relax its 28-ton lorry weight limit progressively to 34 tons in 2001

and 40 tons in 2005, provided lorry taxes were raised by both sides to reflect

costs. To comply with a 1994 vote to force transit freight crossing the Alps to

switch to rail, Switzerland has reserved the right to impose a surcharge on

lorries for using its four Alpine passes: Gotthard, San Bernadino, Simplon and

Grand-Saint-Bernard.

In July the European Commission itself proposed changes in the taxation of

heavy goods vehicles to reflect costs, including a possible surcharge for the use

of �sensitive routes�. However, while the principles of the scheme closely

match Swiss plans, they have yet to be accepted by EU ministers and there is no

certainty that the costings will be the same.

In addition, Austria, France, Germany and the Netherlands want an immediate

concession from Switzerland to allow transport of goods using heavier trucks to

the main population centres. The Swiss government says this is out of the

question, a view reinforced by the decision of several environmental groups to

form a referendum committee to challenge any relaxation of the 28-ton limit.

Switzerland wants �fifth

freedom� air rights

Switzerland is also disappointed with the EU position on air transport. Brussels

is offering little more than bilateral traffic rights rather than fifth freedom

rights, which would allow Swiss airlines to fly onward connections within the

EU for flights originating in Switzerland: Geneva-Milan-Rome, for example.

The Swiss say the EU offer is ungenerous in view of the planned �open skies�

policy in Europe next year. Brussels retorts that reciprocal rights in Switzerland

would not be worth a great deal to EU airlines.

A pro-European initiative

will be put to a vote

A people�s initiative to begin immediate talks on EU membership has obtained

the required 100,000 signatures. The Federal Council (Switzerland�s executive

ruling body) now has two years to take a position on the initiative and it could

be put to a vote in 1998. Two other initiatives on Europe, one demanding a

second vote on the EEA and the other requiring a referendum to approve any

talks with Brussels on joining the EU, have already secured the requisite signa-

tures, but a referendum date has yet to be fixed.

Government reform plans

are rejected by voters�

Proposals to lighten the load on government ministers by creating a second-tier

of ten state secretaries to assist them were rejected by 61% of voters in a referen-

dum in June. The turnout was 31%. The proposals were backed by a majority of

French- and Italian-speakers but decisively thrown out by German-speakers,

who are traditionally more suspicious of the federal government. The Federal

Council must now decide whether to proceed with an attenuated reform

programme or accelerate more ambitious plans already under consideration for

a thorough shake-up of the federal administration. Switzerland has by far the

fewest ministries in western Europe�seven compared with Austria�s 15,

Germany�s 18 and France�s 24. The number has not changed since 1848, despite

the huge increase in the workload.

German 63.6

French 19.2

Italian 7.6Romansch 0.6

Other 8.9

Resident population by first language% of total, 1990 census

Source: Département fédéral de l'économie publique, La Vieéconomique.

Switzerland 9

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

�but constitutional

amendment on

agriculture is accepted�

On the same day, a proposed constitutional amendment on agriculture was

accepted by 78% of voters, following rejection of an earlier amendment in

March 1995. Last year�s refusal stemmed from concerns that industrial farming

was unduly favoured. The approved amendment, by contrast, anchors in the

constitution the principle that direct payments to farmers can be made only for

environmental reasons. It also stipulates a �multi-functional� agricultural sector

responsible for feeding the population, protecting the environment and main-

taining rural communities.

�and more agricultural

reforms on the way�

Later in June, the Federal Council approved a second tranche of agricultural

reforms designed to make the sector more market-oriented and environmentally

sensitive. The programme, dubbed �Agriculture 2002", sets out a detailed plan of

implementation for the seven years to 2002. In the important dairy sector, the

price of milk will no longer be guaranteed, although border protection will

continue. The government will continue to support butter- and cheese-making.

However, it will stop subsidies for cheese exports to the EU, while maintaining

export subsidies for other markets. There will also be reductions in support for

wheat.

�which will benefit

consumers

Consumers will be the main beneficiaries, saving Swfr1.4bn ($1.1bn) over the

seven years in lower prices for food in the shops. The federal government will

save Swfr530m ($431m) in price guarantees over the period but will pay out

Swfr1.2bn more in direct payments to farmers. However, these payments will

only partly compensate farmers for the loss of Swfr1.9bn in price supports. The

government is hoping that the deficiency of Swfr700m left in their finances will

be eliminated by lower costs of production. To that end, it plans to introduce a

subsidy for farm investment and to change existing inflexible laws on farm

property and rents. Switzerland subsidises its farmers more generously than

almost any other OECD country, paying out $6.1bn in 1995, amounting to 81%

of the value of production.

A cheese scandal is

uncovered

The Swiss government has nominated a former federal prosecutor, Hans Walder,

to investigate alleged corruption in the Swiss Cheese Union, a semi-government

agency responsible for buying in and marketing Emmental, Gruyère and Sbrinz.

The administrative inquiry will run parallel to the criminal investigation already

under way, which has resulted in the arrest and brief detention of the former

marketing director of the Swiss Cheese Union, Walter Rüegg. The allegations

relate to abuse of the system under which the EU charges duty on Swiss cheese

sold below a minimum level set by Brussels. To help in offloading stocks, the

Swiss Cheese Union is said to have paid some Swfr26m to an Italian cheese firm,

allowing it to buy cheese at prices below the minimum, with false invoices to

avoid paying tariffs. Mr Rüegg is alleged to have received gifts of at least

Swfr350,000 in connection with the affair. Italy is Switzerland�s biggest cheese

importer, taking nearly 40% of Swiss exports of Emmental, Gruyère and Sbrinz

last year.

Swiss officials have raised the prospect that as much as Swfr200m might have to

be paid to the EU in restitution and fines. The scandal is also likely to hasten the

demise of the Swiss Cheese Union, now renamed Swiss Cheese, whose future

was already in doubt because of plans to dismantle the comprehensive system of

10 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

dairy price supports. Subsidies for marketing the three above-mentioned hard

cheeses, which together account for two-thirds of Swiss cheese production, will

amount to more than Swfr450m this year. Over the past decade, exports of Swiss

cheese sold at normal prices have tumbled, while cut-price sales now account for

nearly one-quarter of the total. To make matters worse, the EU has refused to

give Swiss Emmental protected status, forcing the cheese to compete with ge-

neric EU �Emmental� produced at lower cost. With less generous subsidies in

the future, Swiss farmers will have no alternative but to cut cheese production

drastically in line with what can be sold on the open market.

The boycott on Swiss beef

continues

Some 16 countries are maintaining an embargo on Swiss beef, beef products and

dairy goods such as chocolate, ice-cream and powdered milk because of fears of

�mad cow� disease (2nd quarter 1996, page 11). They include Germany and

Austria among EU countries; the others are Algeria, Turkey, Yugoslavia (Serbia-

Montenegro), Slovakia, Argentina, Syria, Ukraine, Peru, Russia, Czech Republic,

Morocco, Singapore, Tunisia and Poland. The European Commission has again

demanded that Germany and Austria lift the ban on Swiss beef imposed at the

end of March after the UK government admitted a possible link between mad

cow disease and a rare form of human brain disease. Subsequently, an EU

investigation suggested that the source of mad cow disease in Swiss cows was

infected feed from the UK. Although it concluded that the disease was under

control, the German and Austrian governments remain to be convinced.

The return of Bosnian

refugees is postponed

The Swiss government has postponed the repatriation of a first group of 8,000

Bosnian refugees, initially planned for the end of August 1996, to April 30 next

year. The decision, which concerns single people or couples without children,

is in line with similar positions taken by Austria, Sweden, Denmark and the

Netherlands. The return of Bosnian families with children, involving about

13,000 people, is still planned for August 31, 1997. So far this year, only

350 refugees have gone back voluntarily. Most of the refugees in Switzerland

are Muslims from areas now controlled by the Bosnian Serbs.

The government proposes

new controls on test-tube

babies

The Federal Council has proposed new controls on in vitro fertilisation (IVF), in

response to a people�s initiative deposited in 1994 which calls for a ban on the

practice. Surrogate mothers and the donation of embryos are already forbidden

in Switzerland. But the government plans to go further in limiting to three the

number of embryos which can be reinserted into the mother�s womb and for-

bidding the preservation of embryos for future use. The Federal Council also

proposes to ban certain techniques that may become possible in the future,

including the removal of a fertilised egg for testing for genetic anomalies before

being reimplanted, the modification of genes in sperm, eggs or embryos, and

cloning.

Donations of sperm will be permitted but not those of eggs, a discriminatory

move that may not survive parliamentary scrutiny. Children fathered by a

sperm donor will have the right to know his identity once they reach the age

of 16, but the donor will not be able to claim fatherhood rights. Assisted

procreation will be available only to heterosexual couples in a �stable�

relationship and in a position to raise the child to adulthood. A national ethics

commission will be set up to monitor the new legislation, which partly

Switzerland 11

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

implements a constitutional change on procreation and genetic engineering

approved in a 1992 referendum.

A new sex equality law

enters into force

A new law on sex equality that came into force on July 1 bans all forms of sex

discrimination including that relating to wages. Some groups of women public

employees in the canton of Zurich, including nurses and physiotherapists, have

already announced that they plan court actions to force the cantonal authorities

to put them in a higher wage bracket. However, at a national level no one is

expecting a rush of court cases of this kind. The new legislation also outlaws

sexual harassment, allows class actions by groups of women and reverses the

burden of proof in court cases so that discrimination is presumed unless the

employer can demonstrate the contrary.

A report on sex equality issued in June by the Federal Statistical Office shows

that Switzerland, like other countries, is far from granting women equal status.

Women remain concentrated in �women�s jobs� and in lower levels of the job

hierarchy. On average they earn 30% less than men, which partly reflects their

lower educational levels, a difference more marked in Switzerland than else-

where in Europe. In addition, working women spend more than 23 hours a

week on domestic tasks, while men spend just ten hours.

Economic policy

The federal deficit may

exceed the budgeted

Swfr4bn in 1996�

A shortfall in expected tax revenue in the first half of 1996 has led to fears that

the budgeted Swfr4bn ($3.4bn, or 1% of GDP) federal deficit for 1996 may be

exceeded. This would be unusual, for the government in the last two years has

managed to cut the actual deficits to less than those that had been targeted in

the budget. The recession is to blame for most of the shortfall: receipts from

federal income tax and petrol duties have been lower than expected. In addi-

tion, higher than anticipated unemployment is expected to cost �some hundred

millions� of francs, according to the Federal Finance Department. (This shows in

the federal accounts as increased lending to the unemployment insurance

fund.) Interest payments on government debt and allotments to the cantons are

also expected to be higher than budgeted. Additional expenditure approved by

the Federal Assembly (parliament), Swfr600m ($488m) in the first half of 1996,

is running at three times last year�s level.

�and the 1997 budget is

looking gloomy

Spending plans by the federal government point to a budget deficit next year of

Swfr7.5bn, or Swfr3.5bn more than the budgeted deficit for 1996. More than

half the deficit increase is attributable to changes in accounting rules: Swfr900m

in loans to the Swiss Federal Railways will be included in the government

accounts for the first time instead of being outside the budget, while the near-

Swfr1bn surplus of the Federal Pension Fund (the civil service pension fund) will

be excluded. However, the finance minister, Kaspar Villiger, says he is seeking

Swfr1.6bn in immediate cuts to limit the budget deficit next year to Swfr6bn.

One likely candidate for cuts is next year�s inflation adjustment to the pay of

federal civil servants; there could also be staff reductions. Other possibilities

include increasing the present five-day delay before the unemployed can collect

benefit and a reduction, without compensation, in milk production quotas.

12 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

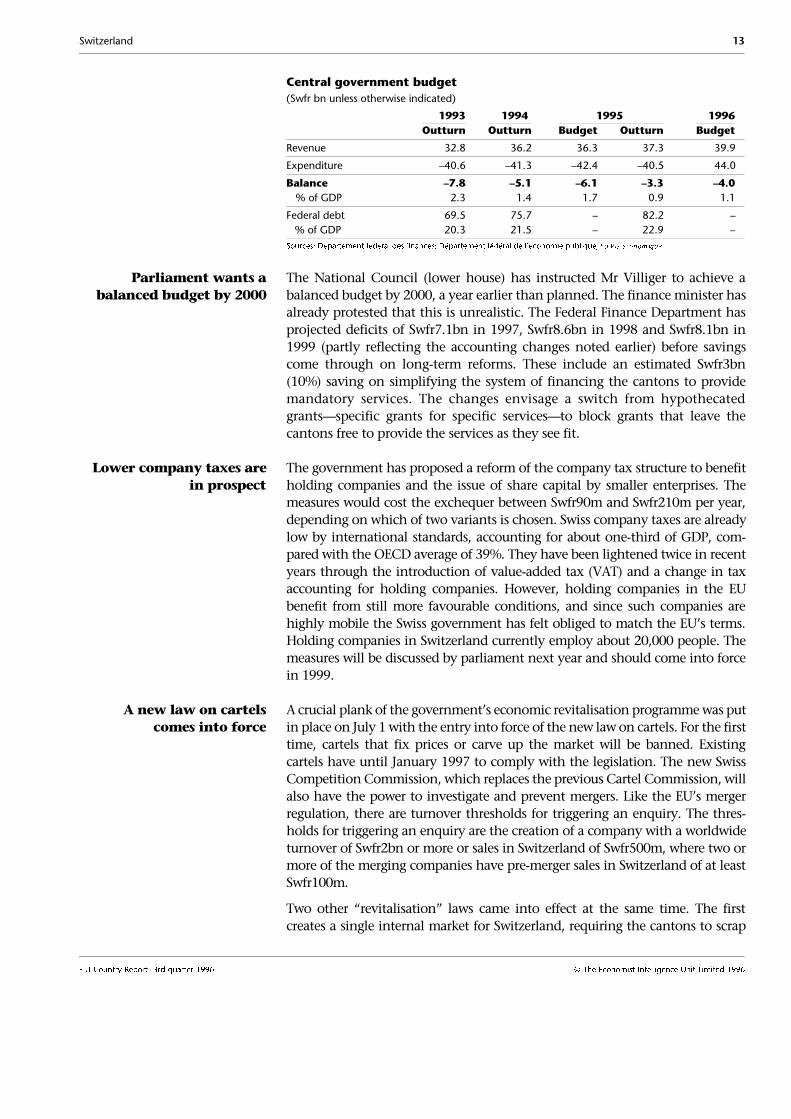

Central government budget

(Swfr bn unless otherwise indicated)

1993 1994 1995 1996

Outturn Outturn Budget Outturn Budget

Revenue 32.8 36.2 36.3 37.3 39.9

Expenditure �40.6 �41.3 �42.4 �40.5 44.0

Balance �7.8 �5.1 �6.1 �3.3 �4.0

% of GDP 2.3 1.4 1.7 0.9 1.1

Federal debt 69.5 75.7 � 82.2 �

% of GDP 20.3 21.5 � 22.9 �

Sources: Département fédéral des finances; Département fédéral de l�économie publique, L a V ie é conom ique .

Parliament wants a

balanced budget by 2000

The National Council (lower house) has instructed Mr Villiger to achieve a

balanced budget by 2000, a year earlier than planned. The finance minister has

already protested that this is unrealistic. The Federal Finance Department has

projected deficits of Swfr7.1bn in 1997, Swfr8.6bn in 1998 and Swfr8.1bn in

1999 (partly reflecting the accounting changes noted earlier) before savings

come through on long-term reforms. These include an estimated Swfr3bn

(10%) saving on simplifying the system of financing the cantons to provide

mandatory services. The changes envisage a switch from hypothecated

grants�specific grants for specific services�to block grants that leave the

cantons free to provide the services as they see fit.

Lower company taxes are

in prospect

The government has proposed a reform of the company tax structure to benefit

holding companies and the issue of share capital by smaller enterprises. The

measures would cost the exchequer between Swfr90m and Swfr210m per year,

depending on which of two variants is chosen. Swiss company taxes are already

low by international standards, accounting for about one-third of GDP, com-

pared with the OECD average of 39%. They have been lightened twice in recent

years through the introduction of value-added tax (VAT) and a change in tax

accounting for holding companies. However, holding companies in the EU

benefit from still more favourable conditions, and since such companies are

highly mobile the Swiss government has felt obliged to match the EU�s terms.

Holding companies in Switzerland currently employ about 20,000 people. The

measures will be discussed by parliament next year and should come into force

in 1999.

A new law on cartels

comes into force

A crucial plank of the government�s economic revitalisation programme was put

in place on July 1 with the entry into force of the new law on cartels. For the first

time, cartels that fix prices or carve up the market will be banned. Existing

cartels have until January 1997 to comply with the legislation. The new Swiss

Competition Commission, which replaces the previous Cartel Commission, will

also have the power to investigate and prevent mergers. Like the EU�s merger

regulation, there are turnover thresholds for triggering an enquiry. The thres-

holds for triggering an enquiry are the creation of a company with a worldwide

turnover of Swfr2bn or more or sales in Switzerland of Swfr500m, where two or

more of the merging companies have pre-merger sales in Switzerland of at least

Swfr100m.

Two other �revitalisation� laws came into effect at the same time. The first

creates a single internal market for Switzerland, requiring the cantons to scrap

Switzerland 13

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

restrictions on the free circulation of goods and services and recognise profes-

sional qualifications granted by other cantons. The second allows the govern-

ment to minimise technical barriers to trade by relaxing excessively tight norms

and standards or harmonising them with international or European standards.

Two immediate targets are food hygiene rules and car safety tests.

A recent report on Switzerland by the World Trade Organization (WTO) said

that lack of domestic competition had resulted in a price level 50% above the

EU average. The report counted 20 cartels operating restrictions in the markets

for energy, insurance, transport and communications.

New labour laws will be

challenged in a

referendum

Trade unions, backed by the Social Democratic Party, have collected 150,000

signatures to force a referendum on the new labour law passed by parliament in

March. The vote will probably be held on December 1. The main focus of

complaint is the extension of �normal� working hours from 8pm to 11pm and

the absence of any legal requirement for employers to pay overtime or even give

compensating time off for night work and Sunday working. Compensation was

refused by the bourgeois majority (the Radical Democratic Party, the Christian

Democratic Party and the Swiss People�s Party) in parliament, against

the government�s recommendation, on the grounds that it was a matter for

collective bargaining.

Employers have welcomed the new law, arguing that it will increase the flexi-

bility of the Swiss labour market, improve competitiveness and create jobs.

Other provisions of the legislation remove restrictions on night work by

women in industry (no such restriction has ever been in force for the service

sector), enable shops to open six Sundays a year, and allow firms to operate

double shifts without special authorisation.

The trade unions are incorporating in their referendum campaign strategy a

wholesale attack on what they claim is a drive by employers to dismantle the

social welfare system and destroy the gains achieved by workers in the period

since the Second World War. Slow economic growth and rising unemployment

has meant that Swiss voters already fear for their future prosperity and in June

they were shocked by the news that Switzerland�s biggest employer, Swiss

Federal Railways, was considering pay cuts of 2-4% to help curb its massive

deficit. The next day the canton of Zurich announced that it planned to reduce

the wages of its employees by 5%; some other cities have indicated that they

may follow suit. Until now the public sector has been largely insulated from

the wage pressures already felt by workers in private industry, pressures which

have resulted in a general stagnation of real incomes over the past few years.

To add to these worries, a series of highly publicised mergers and company

cutbacks has resulted in planned job losses totalling 13,300 in the first six

months of the year, among them 3,500 at Credit Suisse (see Financial news),

1,200 at Swissair and 3,500 at the science group, Novartis. These events have

contributed to an unprecedented sense of insecurity in Switzerland; seven in

ten Swiss workers fear unemployment or wage cuts, according to an opinion

poll published in July.

In June the Federal Council (Switzerland�s executive ruling body) went so far as

to issue a statement expressing its concern about the confrontation between

14 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

trade unions and employers, arguing that �only a constructive dialogue will

permit us to find solutions to current problems�. Mr Villiger also spoke out

against generalised wage reductions, arguing that these would simply worsen

the economic situation by depressing consumption.

The main employers� groups deny there is any general intention to cut wages

or demolish social benefits. However, employers appear to be gaining the

upper hand both in their dealings with the trade unions and in restraining

social welfare provision. Several trade unions have recently been obliged to

abandon sectoral bargaining for company agreements, for example in the

chemicals industry and banking. A number of employers have cancelled and

renegotiated collective agreements. Swissair has just agreed pay cuts with its

pilots (see Business news) and unions in other industries have also accepted

wage reductions. Rules for claiming unemployment benefits have been tough-

ened and the Swiss Employers� Association, which has taken the hardest line

on social issues, has called not only for a halt to all future social security

projects but also for a review of some benefits.

Funding for social security

stirs passions

In June a government working group published its report on the future financ-

ing needs of the social security system, suggesting a worrying shortfall in future

funding. The report estimates that spending on social insurance benefits will

rise from Swfr73bn in 1995 to Swfr103bn in 2010 and Swfr124bn in 2025. This

will mean finding extra funds of Swfr30bn to finance benefits in 2010 and

Swfr51bn in 2025. However, according to the government�s assumption of

average economic growth of 1.3% per year, the financing gap in 2010 would be

about Swfr5bn, concentrated on the state pension and invalidity schemes. For

the pension scheme, this sum could be recouped either by extra contributions

equivalent to 1.9% of earnings or by increasing VAT by 2.5 percentage points.

Funding the invalidity scheme would require either an extra 1% of earnings in

contributions or 1.3 percentage points on VAT. For all ten social insurances,

including sickness insurance, the working group estimates that the equivalent

of a 6.8 percentage point increase in VAT would be needed. However, it recom-

mends mixed financing, including the possibility of an energy tax. Another

government working group has now been charged with devising a financing

scheme and looking at possible future changes in benefits.

The Swiss Employers� Association said that the report demonstrated the need to

halt expansion of the welfare state. The three bourgeois coalition parties also

voiced disquiet. But the socialist home affairs minister, Ruth Dreifuss, argued

that the costs were manageable and that there was no need to overdramatise

the situation. There was no question of dismantling the social welfare system;

on the contrary, it should be consolidated and the gaps filled, a reference to the

long-promised introduction of maternity benefit. Ms Dreifuss noted that social

charges in Switzerland were lower than in the EU (although they have more

than doubled to one-quarter of GDP since the 1950s) and said that most of

those in charge of the economy �cared about social cohesion�.

Certainly there is a split in the ranks of employers between those advocating

liberal views which put market forces in the driving seat and those who

believe enterprises have responsibilities to workers and society as well as to

shareholders. Guido Richterich of Roche, the Basle chemicals giant, who is

Switzerland 15

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

president of the Swiss Employers� Association, advocates a social moratorium,

deregulation, cuts in government spending, labour-market flexibility and a

reduction in the role of trade unions. Against that, Hans-Dieter Vontobel of

Vontobel Bank in Zurich, one of Switzerland�s biggest private banks, has criti-

cised those �who want to reduce society to a vulgar and one-dimensional

liberalism� and Robert Studer, the president of Union Bank of Switzerland

(UBS), Switzerland�s biggest bank, argues that companies cannot devote them-

selves exclusively to shareholders� interests.

Trade unions and

ecologists call for a lower

retirement age

Two separate initiatives calling for flexible retirement from the age of 62 have

collected the required 100,000 signatures needed for a national vote. One is

sponsored by the Swiss Ecology Party and the other by trade unions. The Greens

want the cost of the plan�put at around Swfr500m�financed by a tax on

energy while the trade unions favour a mixture of higher VAT and increased

contributions. Critics claim the cost could run as high as Swfr3bn. Yet another

initiative, deposited last year by the main trade union federation, calls for a

reversal of the decision in the tenth revision of the state pension scheme to raise

the retirement age for women from 62 to 64.

Like other countries in Europe, Switzerland has an ageing population. In 1950,

two years after the introduction of the state pension scheme, there were

6.2 people employed for every pensioner. In 1995 the ratio was 2.9:1 and it will

be close to 2:1 by the year 2000. The next revision of the state pension scheme

will concentrate on financing and the possible revision of benefits. Ms Dreifuss

says that the revision will also contain proposals for flexible retirement that

treat men and women equally.

Meanwhile, a working group of the right-wing Swiss People�s Party has called

for drastic measures to cut retirement benefits, including raising the retirement

age for women to 65, the same as for men. The working group, whose report

has not yet been accepted by the party, also advocates means-testing for state

pension benefits and a wait of a month before unemployed people can claim

benefits.

Sickness insurance is still

causing disquiet

Unhappiness with the new law on sickness insurance that came into force this

year looks likely to continue, with the announcement by several insurers

of further steep increases in premiums of between 10% and 30% next year.

Premiums rose sharply in 1996 on introduction of the law, which requires

insurers to charge the same premium for basic treatment, regardless of age,

sex or state of health. At the same time, state subsidies were trimmed and

reallocated to the poorest families, with the result that middle-income families

have had to pay much more.

The federal government has ruled out urgent changes in the law, arguing that

provisions on reducing health costs will eventually mitigate premium costs.

But it has acted to lessen the pain for households in western Switzerland where

premiums are highest. These cantons will get extra money to reduce premiums

next year out of the Swfr2.7bn total set aside for this purpose. Not content with

this, the far-left Swiss Workers� Party has launched a people�s initiative

that would require the federal government to meet half the costs of sickness

insurance.

16 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

In July insurers Helvetia and Artisana announced a merger, creating a new

company, Helsana, which will come into operation from the beginning of next

year. Helsana will be Switzerland�s biggest health insurer, with 1.5 million

contributors. The merger decision follows the break-up last year of a holding

company, Swisscare, created in 1993 to link Helvetia with two other health

insurers, Concordia and KFW. One of Helsana�s priorities, like that of Swisscare,

will be to try to reduce medical charges, especially for private hospital care

where doctors� fees can be exorbitant. A hospital childbirth that costs

Swfr2,500-3,000 ($2,000-2,400) with a bed in a communal ward may cost

Swfr20,000 privately, according to Helsana.

The OECD calculates that Switzerland has the highest health spending of any

member country after the USA, at 9.3% of GDP in 1994. Spending per person

was $2,294, compared with $3,516 for the USA and $1,965 for Austria, the

runner-up in Europe.

The cost of medicines in Switzerland is also much higher than in neighbouring

countries, reflecting high margins on drugs sold at mandatory fixed prices. The

protection afforded by these margins has led to a rise of one-fifth in the number

of pharmacies in Switzerland over the past ten years to more than 1,600�to

which must be added about 900 drugstores selling non-prescription drugs.

Many will not survive the deregulation planned for the sector. Next year

medicine prices will be partially liberalised, paving the way for full deregulation

after the year 2000, which should bring prices down closer to the European

average. This is simply recognition of the inevitable, as the fixed-price system is

clearly incompatible with the law outlawing price cartels that came into force on

July 1.

The pharmacies currently have about 60% of the Swfr4bn drugs market in

Switzerland, with doctors and hospitals dispensing another third. However, the

supermarket chain, Migros, has expressed interest in selling over-the-counter

medicines. In addition, the association regulating pharmacies has recently

agreed to offer sickness insurance companies a rebate on the cost of medicines,

following news that some health insurers plan to distribute drugs themselves to

patients suffering from chronic ailments.

A national debate on

energy policy is planned

The energy minister, Moritz Leuenberger, plans a national debate this autumn

on energy policy after the year 2000 when the existing programme �Energy

2000" expires. Mr Leuenberger has already made clear his support for the

principle that energy prices should reflect true costs. According to an expert

report published in July, including environmental and health costs, and the

costs of ancillary infrastructures, would mean consumers paying an extra

Swfr11bn-16bn per year. This idea is unlikely to go down well with industry,

which already complains that energy costs in Switzerland are too high by

comparison with competitors.

Paradoxically, government plans to liberalise the electricity market to be pre-

sented later this year are expected to result in lower electricity prices. The

government intends to follow the EU in allowing big industrial consumers to

choose their suppliers, although complete liberalisation will have to await a

restructuring of the industry. About 1,200 electricity producers, mostly publicly

Switzerland 17

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

owned, share the Swiss market, a fragmentation that is clearly inefficient. How-

ever, consolidation is likely to be bitterly opposed by the cantons and com-

munes, which take about a fifth of the final price of electricity in taxes.

In June the lower house of parliament followed the upper house in approving an

increase in the price paid to mountain cantons for the use of their water for

hydroelectricity from Swfr54 to Swfr80 per kw, raising their income from this

source from Swfr270m to Swfr400m per year (2nd quarter 1996, page 15). Ind-

ustry representatives have hinted that they may launch a referendum campaign

against the increase which will add 0.2 centimes to the price of a kilowatt-hour.

Nuclear wastes may still

go to Wellenberg

On expert advice, the government is leaning towards creating a dump at

Wellenberg in the canton of Nidwald to take low-level and medium-level

radioactive wastes from its five nuclear power stations. This is despite last year�s

local referendum opposing the move. The experts say that technically and

geologically Wellenberg offers the safest location for lodging the wastes. The

Federal Council, which is due to take a decision later in the year, is legally

entitled to override the referendum vote, but will probably decide on extra

safety and other precautions to lessen local objections.

Reforms are planned for

Swiss Federal Railways

The Federal Council has proposed a framework law governing the railway

system which would, among other things, oblige the Swiss Federal Railways to

create separate divisions for infrastructure and operations. The railways would

be able to charge private operators of freight and certain passenger services

wanting to use the infrastructure, subject to some fairly strict conditions giving

priority to a coordinated railway transport system. The public authorities

would also have to pay for the maintenance of loss-making lines or lose the

services. However, freight transport would continue to be subsidised as long as

road transport does not pay its true costs. The Swiss Federal Railways would be

given full management autonomy as a public corporation, subject to parlia-

mentary approval every four years of a level of service provision and a broad

financial package. Railway staff will no longer be treated as civil servants. At the

same time, the railways� accumulated losses�likely to be around Swfr1bn by

January 1988�will be written off, and government loans of Swfr12bn will be

converted into share capital of Swfr8bn.

The Federal Railways made a record loss of Swfr496m in 1995, due partly to

special charges including the introduction of VAT, restructuring costs, and

capital write-offs for the sale of stakes in its freight forwarding arm, Cargo

Domicile, and Hotelzug (railway hotels). Receipts for passenger traffic were

down by 7.3% and for freight traffic by 8%.

The SNB continues an

easier monetary policy

Adjusted central bank money, the target measure of the Swiss National Bank

(SNB, the central bank), has grown rapidly this year as the bank has responded

to depressed economic activity and the strength of the franc. At the end of July,

the bank injected extra funds into the money markets, a rare move that followed

nervousness in the foreign exchange markets in thin summer trading. The bank

said that it considered the Swiss franc to be massively overvalued and that there

was no sound economic basis for it.

18 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

Money supply

(% change, year on year)

1994 1995 1996

Year 1 Qtr 2 Qtr 3 Qtr 4 Qtr Year 1 Qtr

Cash in circulation 1.7 0.5 0.6 0.3 0.3 0.9 2.3

Money supply (M1) 5.6 1.7 4.2 7.0 9.9 6.9 17.1

Money supply (M2) 10.2 1.7 4.0 7.2 9.7 5.1 16.7

Seasonally adjusted central

bank moneya 0.6 1.5 1.8 1.9 1.4 1.4 4.8

a Swiss National Bank target measure.

Source: Département fédéral de l�économie publique, L a V ie é conom ique .

The discount rate remains at 1.5%. However, money-market rates have begun

to rise, reflecting markets� expectations of faster growth in demand and slightly

higher inflation. Nevertheless, both short-term and long-term rates remain

below equivalent rates in the EU�s hard-core, which at mid-August stood at

3.25% and 6.25% respectively, 150-200 basis points above Swiss rates.

Interest rates

(%; period averages unless otherwise indicated)

1995 1996

1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr

Official discount ratea 3.00 3.00 2.00 1.50 1.50 1.50

3-month Euro-deposits 3.79 3.25 2.75 2.02 1.63 2.07

Confederation bonds 5.18 4.72 4.37 3.78 4.08 4.19

a End-period.

Source: Département fédéral de l�économie publique, L a V ie é conom ique.

SNB�s investment policy is

to be examined

A joint working party of the SNB and the Swiss finance ministry is to examine

the bank�s investment policy, currency management and profit transfers. In

April the bank announced that it would transfer only Swfr142m of its profits

for 1995 to the federal and cantonal governments, the first time such transfers

had fallen below Swfr600m since they began in 1991. The reduction drew

criticism from some commentators that the bank was not managing its reserves

efficiently. The bank itself wants a change in the rules which now bar it from

investing currency reserves for a maturity of more than 12 months.

The economy

The economy may have

bottomed out�

Switzerland�s gross domestic product fell by an annualised 0.1% in real terms

between the fourth quarter of 1995 and the first quarter of 1996, the fourth

consecutive quarter-on-quarter decline. However, the quarter-on-quarter drop

was only slight compared with previous quarters, which suggests that the

contraction in economic activity which began in the second quarter of 1995

may be coming to an end. However, the GDP figures have also been revised

downwards for previous quarters, revealing a sharper decline than previously

thought. Over the year to the first quarter 1996, the drop was 0.7%, compared

with 0.3% in the fourth quarter of 1995. Domestic demand is at a low ebb:

household spending is feeble, government spending is down in real terms and,

Switzerland 19

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

for the first time in over two years, fixed investment has also fallen on an

annual basis. The foreign balance made a small positive contribution to growth

in the first quarter, with the rise in exports exceeding that of imports.

Trends in components of gross domestic product

(% real change, year on year)

1994 1995 1996

Year 1 Qtr 2 Qtr 3 Qtr 4 Qtr Year 1 Qtr

Private consumption 1.0 �0.2 1.0 0.5 �0.3 0.2 0.5

Public consumption 0.8 0.1 0.1 �0.3 �0.1 �0.1 �0.3

Fixed investment 5.9 10.4 6.1 2.9 2.6 5.3 �1.3

Construction 3.2 0.0 �0.7 �1.9 �3.1 �1.5 �4.0

Equipment 11.0 25.2 18.3 12.4 13.1 17.2 1.8

Exports of goods & services 3.3 2.2 5.0 3.0 1.2 2.8 3.0

Goods 4.9 5.2 7.0 4.5 0.7 4.2 3.2

Services �2.4 �8.6 �2.8 �1.7 4.1 �2.6 2.4

Imports of goods & services 9.0 11.0 7.5 3.3 4.2 6.4 2.5

Goods 9.5 11.4 7.8 3.0 3.9 6.5 2.2

Services 3.8 5.3 4.3 4.6 8.6 5.4 7.8

GDP 1.2 1.7 1.1 0.4 �0.3 0.7 �0.7

Source: Département fédéral d l�économie publique, L a V ie é conom ique.

�but consumer spending

is still stagnant�

Consumer spending rose by 0.5% in real terms between the first quarters of

1995 and 1996, but this partly reflects the early Easter in 1996 and the extra

Leap Year day in February. Some estimates put the effect of an extra day�s

production at 1-1.5%, at least in theory. Retail sales remain depressed but

spending on services, with the notable exception of leisure and tourism, rose in

the quarter. The number of hotel nights spent in Swiss hotels has fallen steadily

since 1991, while spending on holidays abroad tapered off in the first quarter.

New car registrations also declined in the three months to March after having

picked up at the end of 1995. Meanwhile, consumer confidence has sunk to its

lowest level for two-and-a-half years, according to the government�s quarterly

survey in April, with households even less ready to make big purchases than

they were before. Fears about job insecurity are the main reason.

�and investment fell� Fixed investment fell by 1.3% in the year to the first quarter 1996, as the boom

in spending on plant and equipment levelled off. Investment in new equipment

rose by just 1.8% in the 12 months to the first quarter, after a 13.1% rise in the

fourth quarter and an increase of 17.2% for 1995 as a whole, when it accounted

for a record 12% of GDP. However, the low first-quarter increase partly reflects

the very high annual growth of over 25% in the final quarter of the previous

year. Spending on office machinery and commercial vehicles continued to be

strong, as was investment in new aircraft. Nevertheless, more than three-quar-

ters of investment expenditure is spent on imports rather than benefiting dom-

estic producers. The Swiss machinery industry suffered a big drop in orders in

the first quarter, from foreign as well as from domestic customers.

Meanwhile, construction investment continued to fall, by 4% in the year to the

first quarter. There is no sign that the declining trend for most of last year is

about to be reversed. Housebuilding has been particularly depressed after a

shortlived boom in 1994. Deliveries of bricks and cement fell by 10% in the first

quarter of 1995 compared with 12 months earlier. New construction orders,

20 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

registered by members of the Swiss Entrepreneurs� Association that groups build-

ing employers, were 15% lower in nominal terms in the first quarter than in the

same period of 1995. All types of building were affected.

�although exports

remain healthy

Despite the strong Swiss franc and sluggish growth in the rest of Europe,

exports of goods have been remarkably buoyant. They rose by 3.2% in real

terms in the year to the first quarter after stagnating in the fourth quarter.

Exports of jewellery, chemicals and pharmaceuticals, machinery and electronic

goods were all up from last year, although exports of textiles and watches fell.

There was a slight decline in deliveries to members of the EU, including

Germany, Switzerland�s largest single customer. However, exports to the USA,

Canada and Japan were buoyant, as were deliveries to OPEC countries and

Singapore, India and South Korea.

Exports of services were up by 2.4% in the first quarter compared with the

year-earlier period, with banking services particularly in demand. However,

earnings from tourism again declined in real terms.

Import growth slows Economic stagnation has slowed the growth of imports, which rose by only

2.5% in the year to the first quarter, the smallest increase since the third

quarter of 1993. Most of the growth was in consumer goods, where imports

rose by 6.2% over the year, notably for pharmaceuticals. Imports of household

goods and equipment, and jewels, were the only sectors to show a decline.

Imports of investment goods, which had notched up double-digit growth over

the eight quarters in 1994 and 1995, rose only slowly in the first quarter of

1996. This was partly due to the general economic effect mentioned earlier.

Imports of raw materials and semi-finished goods fell.

Industrial production

(% change year on year unless otherwise indicated)

1994 1995 1996

Year 1 Qtr 2 Qtr 3 Qtr 4 Qtr Year 1 Qtr

All industry 8 7 5 3 �2 3 n/a

of which:

textiles 12 2 �6 �9 �10 �5 n/a

chemicals 14 11 12 9 7 10 n/a

metallurgy 9 6 1 �3 �6 �1 n/a

machinery 6 4 5 11 �4 4 n/a

watchmaking �11 �6 1 4 �16 �4 n/a

Industry excl utilities 8 7 6 6 �2 4 n/a

New orders 9 4 �1 �1 �8 �1 n/a

Capacity utilisation (%) 83.7 85.1 85.3 85.2 85.0 85.2 84.0a

a Preliminary estimate.

Source: Département fédéral de l�économie publique, L a V ie é conom ique.

Production falters Official data on industrial production are not yet available for the first quarter.

However, the indications are that industrial production and orders contracted

year on year in the first quarter of 1996. Capacity utilisation sank to 84%, its

lowest level for two years. The fall-off in orders affected industries geared to

domestic production as well as those with large export markets. The investment

goods sector was particularly depressed, with lower production and orders in the

Switzerland 21

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

metalworking and machinery industries. The fortunes of the consumer goods

sector were more mixed. Orders rose for food, drink and tobacco and fell for

textiles, clothing and watches. Orders and production in the chemicals industry

stagnated, while output sank in the building materials sector.

Employment falls Employment continued to fall in the first three months of 1996, by 1.1% on

the year-earlier period according to the index that covers full-time work and

part-time employment of at least 50%. Worst affected was the construction

industry where employment fell by 4.2%, but there were also declines for

manufacturing and services. The latest figures mean that employment has

fallen more or less continuously since the second half of 1991, albeit at a slower

pace in the past two years.

Figures for total industrial employment also show a steady decline to below

3 million in the first quarter of 1996, a fall of 0.4% from the same period in

1995. Part-time working (over 50%) increased but not by enough to make up for

the loss of full-time jobs. In addition to 2,572,000 people working full-time,

417,000 people occupied part-time jobs of more than 50% of normal hours.

Another 436,380 people worked less than 50%. The economically active popul-

ation, which includes workers in agriculture and the self-employed, also fell by

0.4% over the year to the first quarter.

Unemployment, which increased in the early months of 1996, levelled off in

the summer for seasonal reasons, falling from 162,377 (4.5% of the workforce)

in May to 159,900 (4.4%) in June, according to national definitions. However,

at 4.5% in the second quarter, unemployment remains 0.3 percentage points

above its year-earlier level. Moreover, the federal employment office, which in

January was predicting an average of 140,000 jobless in 1996, is now expecting

a figure of around 163,000 (4.5%). Unemployment is predicted to fall to

155,000 on average in 1997 but this is still higher than last year�s

153,316 (4.2%).

Short-time working also rose in the first part of 1996, especially in the construc-

tion and metalworking industries.

Trend in employment by sector

(�000; % change year on year in brackets)

1994 1995 1996

Year 1 Qtr 2 Qtr 3 Qtr 4 Qtr Year 1 Qtr

Building industry 281 280 290 296 277 286 272

(�0.8) (2.5) (2.8) (1.0) (0.3) (1.6) (�2.8)

Machinery & vehicles 137 138 138 138 139 138 139

(�4.0) (1.6) (0.3) (0.8) (0.8) (0.9) (1.2)

Metals & metal manufactures 94 94 95 95 94 95 94

(�0.1) (0.4) (1.9) (�0.1) (�1.0) (0.3) (�0.6)

Chemicals 75 74 74 76 75 75 75

(2.3) (0.2) (�1.1) (0.7) (0.6) (0.1) (0.8)

Jewellery & watchmaking 37 37 37 37 37 37 37

(4.4) (3.5) (1.8) (0.4) (0.1) (1.4) (�0.4)

Total employment

incl others 3,776 3,782 3,787 3,801 3,761 3,783 3,766

(�0.2) (1.0) (0.5) (�0.5) (�0.3) (0.2) (�0.4)

Source: Département fédéral de l�économie publique, L a V ie é conom ique.

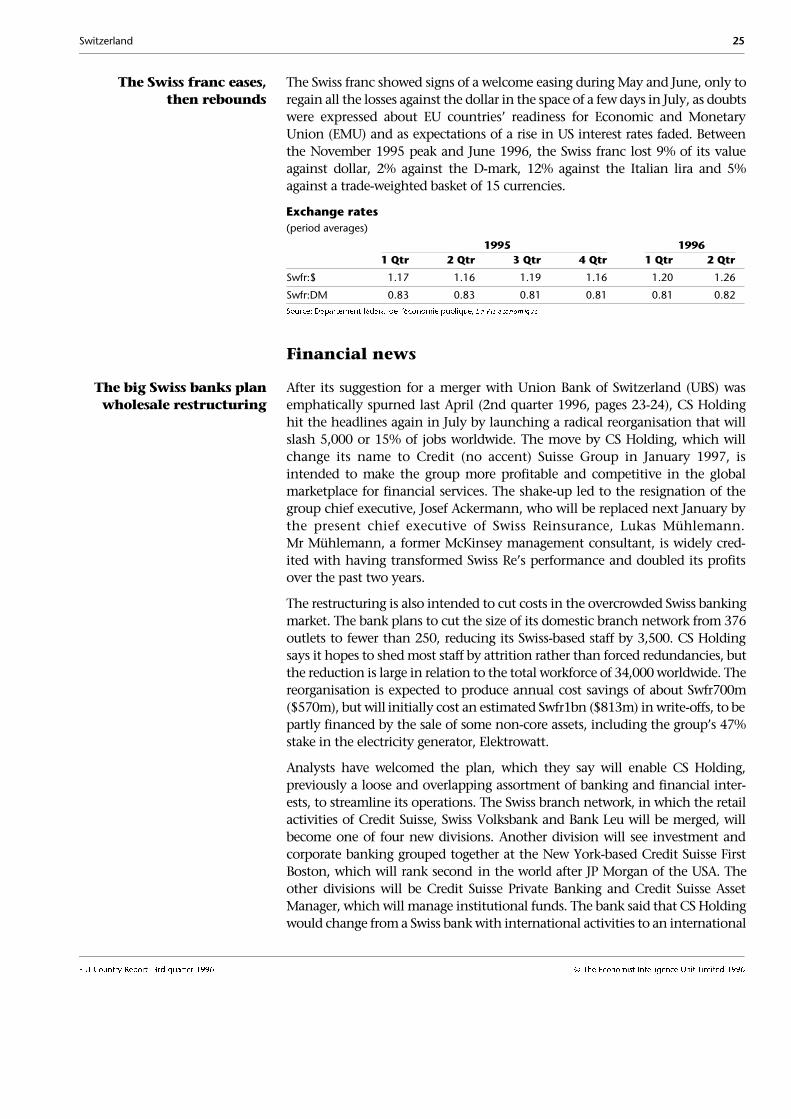

4.5

5.0

5.5

6.0

6.5

May. . Jul . . Oct . . Jan . . Apr

Unfilled vacancies'000, seasonally adjusted

Source: OECD, Main Economic Indicators.

199519951995199519951995199519951995199519951995199519951995199519951995199519951995199519951995 961995 961995 96961995 961995 961995 961995 961995 961995 961995 961995 961995 961995 961995 961995 961995 96

22 Switzerland

EIU Country Report 3rd quarter 1996 © The Economist Intelligence Unit Limited 1996

Unemployment

(period averages)

1995 1996

1 Qtr 2 Qtr 3 Qtr 4 Qtr Year 1 Qtr 2 Qtr

Number 164,647 151,662 145,096 151,860 153,316 165,354 162,164

Rate (%) 4.5 4.2 4.0 4.2 4.2 4.6 4.5

Source: Département fédéral de l�économie publique, L a V ie é conom ique.

Inflation remains low Inflation has remained low and broadly stable during 1996, helped by the

continuing strength of the Swiss franc, which has kept import prices down. The

consumer price index rose by 0.7% in the year to July, the same as in June,

compared with an annual inflation rate of 2% in July 1995. After an inflationary

bout in the early 1990s, Switzerland has squarely reclaimed its traditional rank-

ing as one of the industrialised world�s lowest inflation countries. The May