Embed Size (px)

Citation preview

European EnvironmentEur. Env. 12, 257–268 (2002)Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/eet.298

COST OF COMPLIANCEASSESSMENTS AND THEWATER INDUSTRY INENGLAND AND WALES

Paul McMahon*

Southern Water, Brighton, UK

Environmental compliance costassessments (CCAs) are being increasinglydemanded and used in the water industry,in order to allow regulators to balanceconflicting objectives. The 1999 periodicreview of water company price limitsconcerned massive environmentalexpenditures, and consequently major useof CCAs. There were major differencesbetween Ofwat (the economic regulator)and the water companies relating to thecompliance costs submitted. Theassumptions used by Ofwat vis-a-visfuture efficiency savings and the cost ofcapital are notable causes of thedifferentials. There are a number of otherreasons why this differential might havearisen, including gaming. However, theprincipal cause might be more a real lackof knowledge on the part of companies offuture efficiencies and the actual costs ofprojects. The CCAs produced in the waterindustry have had massive impact onpolicy design. A number of specificimprovements to CCA are identified.

* Correspondence to: Paul McMahon, Southern Water, SouthernHouse, Lewes Road, Falmer, BN1 9PY, UK.E-mail: [email protected]

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment.

These changes relate to increasedcollaboration between industry andregulators in working groups todesign/approve, inter alia, regulatorymethodologies for use in the periodicreview. More detailed guidance isrequired for preparation of a CCA.Further use of compliance cost databasesis recommended. The entire processwould be facilitated by increased trainingand awareness raising of economics forthe engineers largely responsible forpreparation of CCAs. Copyright 2002John Wiley & Sons, Ltd and ERPEnvironment.

Received 14 December 2001Accepted 8 July 2002

INTRODUCTION

The abstraction of water from the environ-ment and the return of (treated) wastew-ater to the environment are subject to a

vast, complex and increasingly stringent arrayof environmental legislation. England andWales are no exception to this and water com-panies incur significant capital and operatingcosts in meeting this legislation. Indeed, giventhe absolute and comparative magnitude of

P. McMAHON

these costs we might even describe a mod-ern water company as an environmental man-agement company with water distributionand wastewater collection facilities, in thesame way that Freddy Heineken describedthe eponymous beer company as a ‘marketingcompany with a beer production facility’. Therole of compliance cost assessment (CCA) hasbecome increasingly prominent and importantin the period since privatization of the waterindustry in 1989 given the intense and contin-uing tensions between prices and investmentlevels. As such the water industry provides auseful case study for students of CCA. Thispaper considers the following four questions.

1. Why are CCAs increasingly being deman-ded and used in the water industry?

2. Are the costs of compliance objectively‘discoverable’ or subjective and politi-cally motivated?

3. What influence are CCAs having onpolicy design?

4. How can the CCA process be improved?

An important caveat is that in somerespects the water industry is unique:because of the magnitude of environmen-tal compliance expenditure and the indus-trial/regulatory structure CCAs are intimatelywrapped up with the economic and environ-mental regulation of the industry. Because ofthis, any conclusions cannot automatically begeneralized.

The paper is structured as follows. A briefoverview of the water industry and theregulatory structure in England and Wales isprovided in the next section. Thereafter thefour questions are addressed in turn. Finally,conclusions will be drawn.

INDUSTRIAL AND REGULATORYSTRUCTURE

Industrial structure

The ten Regional Water Authorities in Englandand Wales that controlled all aspects of the

water cycle were privatized in 1989. These tencompanies are responsible, as virtual regionalmonopolies, for the provision of public watersupply and wastewater (sewerage) servicesto virtually all households and businessesin England and Wales. There are also 12small water only companies. In 1999/00 totalindustry revenue was approximately £7 billion(Ofwat, 1999). All of these companies operateunder licences granted by the Office of WaterServices (Ofwat), the economic regulator ofthe industry. Continuation of the license issubject to acceptable performance, as judgedby Ofwat. Due to the nature of the industryand the services provided, the water (andsewerage) companies differ from other privatefirms. Specifically, they operate as monopoliesin their respective markets and there is a rangeof statutory duties that they must fulfil.

Regulatory structure

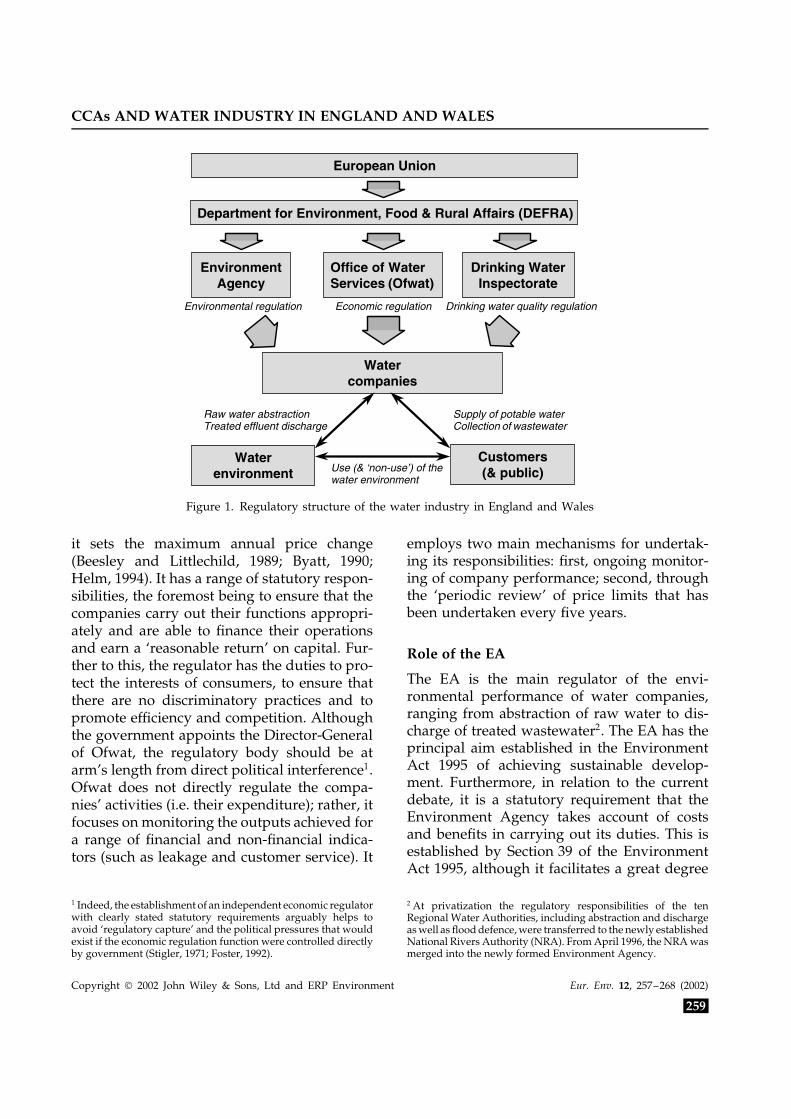

Figure 1 provides a stylized overview of theregulatory structure. There are five main reg-ulatory bodies of interest. At the highest levelthere are the European Union and the UK gov-ernment (principally the Department for Envi-ronment, Food and Rural Affairs–DEFRA). Inaddition to being responsible for transposingEU Directives into UK law, DEFRA is respon-sible for setting national environmental andquality standards, though this role is con-strained by EU directives. However, neitherthe EU nor DEFRA is involved in direct reg-ulation. This is undertaken by a triumvirateof the Office of Water Services (Ofwat); theEnvironment Agency (EA), the environmentalregulator; and the Drinking Water Inspectorate(DWI), the drinking water quality regulator. Inrelation to environmental legislation the role ofthe DWI is not of interest. The overall objectiveof the regulatory regime is to balance producerand consumer interests.

Role of Ofwat

Ofwat conducts economic regulation througha form of price-cap regulation under which

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

258

CCAs AND WATER INDUSTRY IN ENGLAND AND WALES

Office of WaterServices (Ofwat)

Watercompanies

Waterenvironment

Customers(& public)

Raw water abstractionTreated effluent discharge

Supply of potable waterCollection of wastewater

EnvironmentAgency

Drinking WaterInspectorate

Use (& ‘non-use’) of thewater environment

Department for Environment, Food & Rural Affairs (DEFRA)

European Union

Environmental regulation Economic regulation Drinking water quality regulation

Figure 1. Regulatory structure of the water industry in England and Wales

it sets the maximum annual price change(Beesley and Littlechild, 1989; Byatt, 1990;Helm, 1994). It has a range of statutory respon-sibilities, the foremost being to ensure that thecompanies carry out their functions appropri-ately and are able to finance their operationsand earn a ‘reasonable return’ on capital. Fur-ther to this, the regulator has the duties to pro-tect the interests of consumers, to ensure thatthere are no discriminatory practices and topromote efficiency and competition. Althoughthe government appoints the Director-Generalof Ofwat, the regulatory body should be atarm’s length from direct political interference1.Ofwat does not directly regulate the compa-nies’ activities (i.e. their expenditure); rather, itfocuses on monitoring the outputs achieved fora range of financial and non-financial indica-tors (such as leakage and customer service). It

1 Indeed, the establishment of an independent economic regulatorwith clearly stated statutory requirements arguably helps toavoid ‘regulatory capture’ and the political pressures that wouldexist if the economic regulation function were controlled directlyby government (Stigler, 1971; Foster, 1992).

employs two main mechanisms for undertak-ing its responsibilities: first, ongoing monitor-ing of company performance; second, throughthe ‘periodic review’ of price limits that hasbeen undertaken every five years.

Role of the EA

The EA is the main regulator of the envi-ronmental performance of water companies,ranging from abstraction of raw water to dis-charge of treated wastewater2. The EA has theprincipal aim established in the EnvironmentAct 1995 of achieving sustainable develop-ment. Furthermore, in relation to the currentdebate, it is a statutory requirement that theEnvironment Agency takes account of costsand benefits in carrying out its duties. This isestablished by Section 39 of the EnvironmentAct 1995, although it facilitates a great degree

2 At privatization the regulatory responsibilities of the tenRegional Water Authorities, including abstraction and dischargeas well as flood defence, were transferred to the newly establishedNational Rivers Authority (NRA). From April 1996, the NRA wasmerged into the newly formed Environment Agency.

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

259

P. McMAHON

of flexibility with regard to how costs and ben-efits are calculated and used in the decisionmaking process (see e.g. EA, 1996). Section 39has generated a significant amount of contro-versy and debate (McMahon and Moran, 2000),although this has tended to relate to ‘bene-fits’ (i.e. environmental valuation). The EA hasbecome enmeshed in the issue of benefits andreceived significant criticism for this. For sure,the methodological issues relating to measur-ing cost are much more mundane and betterunderstood, meaning that it is not as attractivea research field as benefits. In addition, legisla-tion generally includes clauses on using costsin regulation, albeit the scope is quite tightlyrestricted. Cost has been widely overlooked inthe regulatory work of the EA for a numberof reasons:

(i) because the requirement for a CCA is notalways obligatory;

(ii) a lack of training and understanding byEA staff of why CCAs are important;

(iii) a lack of confidence by EA staff in dealingwith what is perceived to be an area wherefirms have expertise and

(iv) environmental regulators seeing the issueof compliance costs as an unneces-sary issue, and one that if embracedwill remove their professional discretionand/or belief to maximize environmen-tal quality.

Nonetheless, on the matter of costs somegood work has been undertaken in the areaof industrial pollution, developing a cost ofcompliance database and CCA methodologies.

THE DEMAND FOR AND USE OFCOMPLIANCE COST ASSESSMENTS

Levels of CCA

Two broad levels of CCA can be discerned.Firstly, there is the CCA that is, or should be,conducted at the policy design stage to supportdesign of the most efficient legislative solution

(taking into account other policy objectives).This applies equally to both the Europeanand national levels. However, completion of aCCA at the policy design level (‘policy CCA’),however comprehensive, does not reduce therelevance of a second level of CCA, namely‘project CCA’. It virtually goes without sayingthat aggregate costs (and benefits) estimatedfor the purposes of policy design will notnecessarily hold for each individual firm. Thestandard on the ground could be more orless stringent. Thus a project CCA shouldalways be required when the national policyor European Directive is implemented andimpacts individual firms. Project CCA needsto be the means by which flexibility is builtinto legislation. Typically, such project CCAis not required–with the reliance on blanketstandards, although recent developments suchas the requirements for economic analysis inthe IPPC Directive are encouraging.

Driver for CCA 1: reducing the regulatoryburden

From the 1980s the UK government, follow-ing in the footsteps of the USA, developed anincreased attention to ensuring ‘efficiency’ and‘value for money’ across the private and publicsectors. A key aspect of this was the objectiveto minimize the regulatory burden on business,which led to the requirement for all UK gov-ernment regulatory proposals that will affectthe private sector to be subjected to a regu-latory impact assessment (RIA) incorporatinga CCA (Baldwin and Cave, 1999, pp. 87–88).This is a familiar and general topic that is notof particular concern here.

Driver for CCA 2: economic regulation ofmonopoly power

In the water industry in the UK, some formof project level CCA has been required as anessential and legitimate part of the regulatorycontract and the periodic review process. It iswholly justified by the nature of the industrialstructure of the water industry, where all

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

260

CCAs AND WATER INDUSTRY IN ENGLAND AND WALES

water company expenditure is submitted toand scrutinized by Ofwat, as the determinerof price limits of privatized monopolists undera continual regulatory process, as a proxy fortrue market competition3,4.

Driver for CCA 3: reconciling regulatoryobjectives

The third driver for CCAs in the water industryis the need to weigh costs against other factorsin determining the overall balance between thevarious regulatory objectives. The regulatorsmust set environmental standards and pricelimits to reconcile

(i) firm interests (e.g. profit/return on capital,revenue sufficiency for customer serviceand asset maintenance),

(ii) customer interests (e.g. low (fair?) prices,levels of service),

(iii) environmental impact and(iv) ‘political’ concerns (e.g. social/equity con-

siderations).

In order to inform this process it is essentialthat water company costs are visible to theregulators so that the costs and benefits can becompared. This necessitates the use of CCAs5.

3 Under the pure form of price-cap regulation, with infiniteregulatory lag, there is no contractual use of cost data. As suchthe regime is unlikely to lead to optimal outcomes unless theregulator has good knowledge of costs and demand conditions(see e.g. Laffont and Tirole, 1993).4 Of course, the cost submissions to Ofwat cover all aspects of thefirms’ expenditures and activities, not just those that would becovered by a conventional CCA for environmental legislation.5 It is established in the economics of regulation that whenenvironmental and quality regulation is separate from economicregulation, there are risks that the regulatory tensions and trade-offs will not be appropriately balanced. That is, imposition ofstandards without consideration of the costs and benefits ofmeeting them will lead to economically inefficient outcomes dueto the regulators having different, conflicting, objectives andinformation (Baron, 1985; Cowan, 1993). On the other hand,separation of the economic and environmental regulatory rolesbetween Ofwat and the EA improve transparency and helps toavoid ‘regulatory capture’ and the political pressures that wouldexist if the economic regulation function were controlled directlyby government (Foster, 1992).

OBJECTIVITY OF COSTS OFCOMPLIANCE ASSESSMENTS

The periodic review process

The periodic review process is the principalmeans by which the ex ante compliance costsare revealed. The periodic review is basedupon submissions by companies to Ofwat oftheir strategic business plans, which containforecasts of expenditure requirements for thesubsequent five-year period in order to meet,inter alia, environmental legislation6. Based onthe business plans, findings of the annual mon-itoring, in addition to further analysis (e.g.econometric modelling has been used, Stew-art, 1993), Ofwat imposes maximum annuallimits on customer bill increases for the sub-sequent five-year period7. This annual pricerise for each company, known as K, is addi-tional to the retail price index (RPI). K canbe decomposed into three sub-components.(i) New environmental and quality legislationnecessitates new investment that needs to befunded (Q). (ii) Closely related to this areinvestments necessary to improve standards(S). (iii) Expected efficiency savings (over thosethat may be subsumed in RPI) (X). Hence theprice limit K is given by K = Q + S – X.

In the absence of real market competitionfor their services Ofwat determines the relativeefficiency of each of the separate companies bycomparison of their performance, known ascomparative competition (note that the com-panies do effectively compete in the capitalmarkets). Mimicking the effects expected in acompetitive market, inefficient firms are penal-ized in their price limits at each periodic reviewand this provides an incentive for companiesto improve their efficiency. During each five-year period companies have the incentive toimprove efficiency by being allowed to retainthe benefits for a five-year period, before recov-ery at the subsequent periodic review, as well

6 The investment plans are based on long term forecasts, e.g. tobalance supply and demand for water over a 25 time horizon.7 Strictly, the price limit relates to the average of a basket ofproduce prices.

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

261

P. McMAHON

as receiving higher K values (i.e. there is no‘catch-up’ element, as applied to a compara-tively inefficient company).

The ex post costs of environmentalcompliance in the privatized water industry?

Since privatization two periodic reviews ofprice limits have been completed (1994and 1999). Between 1989 and 2000 newcapital investment in the water industryhas amounted to approximately £37 billion(1999/00 prices). This represented between 2and 3% of total capital investment in Englandand Wales over this period. Of this, half hasbeen related to environmental improvements.Taking account of the additional operatingcosts associated with these investments meansthat just this environmental compliancewas equivalent to a cost of £70 perhousehold in England and Wales, fromthe average household bill for water andwastewater services in 1999/00 of £248.In total, environmental compliance couldpossibly account for more than half of thecosts of providing these essential services8.These average household bills for water andwastewater services have risen, in real terms,by approximately 40% between 1989 and 2000.

Because of the nature of economic regulationof the water industry, as we have seen above,and in theory at least, the regulator shouldsee the costs of the company, which willinclude costs for environmental compliance.The issue of asymmetric information betweenthe regulator and the firm is the most importantissue in regulatory economics and it is farbeyond the scope of this paper to discuss thisin any detail. There are problems of both moralhazard and adverse selection. Suffice it to saythat the nature of price-cap regulation meansthat the company faces risks by not submittingthe correct costs to the regulator (given theassumption that asymmetry exists).

For instance, whilst under ‘conventional’rate of return regulation over-investment (and

8 Hence the analogy with Heineken drawn in the introduction.

hence reporting of higher costs) is encouraged(the familiar Averch–Johnson effect, Averchand Johnson, 1962), under the UK form ofprice-cap regulation with comparative compe-tition the firm is penalized with lower pricelimits (K values). Under-reporting of costs tomake the firm appear more efficient in compar-ison with peers inflates the measure of profitthat will then be reduced by the regulator at asubsequent price review.

However, this is not to say that there isno scope for companies to alter the level ofcosts accounted to different activities in theirregulatory submissions. However, it is a zerosum game and appearing more efficient ina certain service area necessitates appearingworse in another. Assuming that Ofwat hascorrectly balanced penalties and rewards thenthere should be no benefit, save for non-financial (i.e. political) reasons. More generally,whilst in theory the scope for doing this shouldbe no less than for companies in other sectorsnot subject to detailed economic regulation, inpractice firms in other sectors have far moreleeway to benefit from asymmetric informationand strategic adjustment and submission ofcompliance costs.

The scope for the regulated water companiesto present ‘strategically adjusted’ CCAs isrestricted and depends on possible collusion inthe industry, which the regulatory regime, ofcomparative competition with a large numberof comparators under a price-cap, is designedto avoid (Armstrong et al., 1994).

On the face of it, therefore, compliance costswould seem to be ex post objective. It is proba-bly fair to say that given the regulatory report-ing and monitoring regime the costs of com-pliance for the major environmental legislation(such as the EU Urban Waste Water TreatmentDirective) can be fairly accurately obtained.However, undoubtedly even in undertakingthese calculations numerous assumptions andinterpretations of the raw data will have been(or would have to be) made. Many costs willbe joint or shared (Kahn, 1988) and prior mis-allocation of costs may have taken place for

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

262

CCAs AND WATER INDUSTRY IN ENGLAND AND WALES

financial, regulatory or political reasons byOfwat and/or the water companies. For exam-ple, anyone who has worked with financialreporting packages and project budgets willknow how tempting (necessary, even) it is tomiscode costs.

Ex ante revelation of environmentalcompliance costs?

Looking back over a 12 year period to deter-mine costs ex post, whilst important, is lessimportant than the ex ante discovery of compli-ance costs in the periodic review process. Thishas been an important issue in the water indus-try since privatization (see e.g. Ofwat, 1993)9.

In the run-up to the 1999 periodic reviewof price limits a huge amount of effort wentinto the preparation and analysis of CCAs andother regulatory submissions. Ofwat issuedreporting requirements regarding the type andformat of information that companies neededto prepare. Over an intensive two/three yearperiod there was a process whereby companiessubmitted costs and other data to Ofwat (andthe EA) regarding costs to meet given envi-ronmental (and other) objectives, and thesedata were assessed by reporters (auditors) andOfwat, and in many cases challenged.

The company submissions will have beenprepared by in-house engineers and/or engi-neering consultants. There are a number ofcost estimating databases developed and main-tained by consultants that are extensively usedby the water companies, including for the 1999periodic review10. Arguably, these databasescan only provide initial estimates of cost. Theactual costs will be influenced by a range ofspecific risks and uncertainties that cannot beknown a priori, including

9 Indeed, the reasons for the 1989 privatization of the water com-panies were significantly related to the costs of environmentalcompliance. First there was a shortfall in investment in infras-tructure during the 1980s, and second large increases in futureinvestment were required to catch up with asset maintenanceand, more importantly, to meet new environmental and qualitylegislation.10 Chiefly, ICEMATE developed by CSSP; WATCOST developedby Faithful and Gould; and TR61 developed by WRc.

(i) errors and omissions in project design,(ii) delay and changes in project design as

a function of: planning approval (includ-ing public inquiry), ground conditions,weather conditions, archaeological inves-tigations, environmental studies and landacquisition/access,

(iii) delay and changes in design due tolegislation,

(iv) variation in the cost of capital and(v) efficiency gains and new techniques/tech-

nologies.

Generally, these databases and the engineerspreparing the CCAs have endeavoured todeal with risk and uncertainty in projectdesign and costing, but this has tended to besimplistic (e.g. assuming that project risk canbe adequately covered by earmarking a sumfor contingency). Companies may, as would beexpected, have adopted a risk averse position.On the other hand, Ofwat may have adoptedan overly optimistic view of future costs.Further to this the high level of the initial watercompany produced CCAs compared with thefinal values determined by Ofwat might beexplained by

(i) differences in views (between Ofwatand the companies) regarding the costof capital,

(ii) risk averse costing by the companies(versus optimistic assumptions usedby Ofwat?),

(iii) gaming and regulatory uncertainty(Ofwat flagged up potential reductionsin the level of the price limits well inadvance of the 1999 periodic review;initial high ‘bidding’ can be seen asa means of establishing a ‘bargaining’position in the face of uncertainty),

(iv) use of historic precedent rather than trueforward looking assessments,

(v) difficulty in predicting future costsavings (efficiencies) in water industrycosts given the comparatively rapidly

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

263

P. McMAHON

changes in the industry structure fromprivatization,

(vi) insufficient training of engineers ineconomics/costing,

(vii) inadequate guidance from Ofwat and(viii) poor auditing (by Ofwat reporters).

The role of reporters is important. Thereporters act as (company appointed) auditorsof regulatory submissions on behalf of Ofwat,both of the data assumptions and compliancewith guidelines. This should facilitate robustCCAs from each company that can be used forcomparison purposes by Ofwat.

INFLUENCE OF COMPLIANCE COSTASSESSMENTS ON POLICY DESIGN

Influence at the national and supra-nationallevel

There has been notably little use of CCAs (andmore generally, cost–benefit analysis (CBA)and regulatory impact assessment (RIA)) inpolicy design at the European level for muchof the major legislation that has driven invest-ment by the water industry from the 1990s(Pearce, 1998). Design of many of these direc-tives stems from the 1970s and 1980s, when,by definition, cost did not constitute a majorconcern for environmental policy makers.Arguably, if comprehensive CCA/CBA/RIAhad been undertaken then the resulting pol-icy (standards) would have been materi-ally different.

Whilst there has been major progress sincethen in conducting CCAs at these levels and arelated and parallel increase in the productionof guidance (see e.g. EEA, 1999; Cabinet Office,1998), this does not mean to say, of course, thatthe present process is faultless. For example,consideration of the EU’s Water FrameworkDirective suggests that the process of CCAhas not moved on substantively. There was,seemingly, little input by way of CCA intothe formulation of the directive. RIA (andtherein CCA) continues to appear to be little

more than an after the fact ‘tick in the box’process rather than a core element of policydevelopment, which runs counter to RIA bestpractice (Deighton-Smith, 1997).

Influence at the water industry capitalinvestment programme level

The composition of the discretionary (national)environmental programme was determined onthe basis of the relative cost–benefit of eachscheme proposed by the EA, although therewas only limited use of formal cost–benefitanalysis). This analysis was overshadowed bya higher level (political) trade-off betweenthe overall impact on prices and the relativeapportionment of expenditure between differ-ent environmental objectives. The role of CCAwas therefore crucial in this process.

Arising from the 1999 periodic review,the forecast investment in the ‘qualityenhancement programme’ necessary to meetenvironmental legislation requirements was£7.38 billion, which equates to an averageof £335 for each household in England andWales over the period 2000/01 to 2004/0511.For instance, over £5 billion of the qualityprogramme is related to wastewater activities,with £1.3 billion earmarked for completion ofthe Urban Waste Water Treatment Directiveand £1.7 billion to be invested in improvingcombined sewer overflows. For the investmentin ‘clean’ water related activities of £2.3 billion,comparatively little is strictly related tocompliance with environmental legislation12.£110 million is earmarked to (i) reduce over-abstraction at sites that are designated underthe European Habitats and Birds Directives(£50 million), (ii) reduce abstractions affectingUK Sites of Special Scientific Interest

11 In addition to this, around £1 billion of expenditure is notinitially included in price limits, which relates schemes that arebeing reviewed and for the sum of £700 million that is a provisionfor new obligations that may arise during AMP3.12 Over £1 billion is intended for renovation of water distributionsystems to address water quality problems and nearly£500 million is to be invested in improvements to water treatmentworks to reduce the risk from cryptosporidium, neither of whichis ‘environmental’.

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

264

CCAs AND WATER INDUSTRY IN ENGLAND AND WALES

(£10 million) and (iii) reduce abstractions onlow flow rivers (£50 million). Maintainingthe balance between supply and demandfor water has been projected to cost over£1.1 billion, which will have implications forwater abstraction and hence the environmentin its own right.

The sum of £7.38 billion is nearly £3 billionless than that included in the companies’strategic business plans. The final total wasprincipally influenced by the efficiency gainsthat Ofwat assumed companies could realize inboth capital procurement and operations, andthe cost of capital Ofwat deemed appropriate13.As discussed, the assumptions used in thefinal price determinations by Ofwat were basedon the companies’ own submissions, studiesby consultants for Ofwat and standardizedcosts for generic capital projects reported toOfwat by certain water companies, whichwere used as the benchmark for industrywide comparison.

The issues of future efficiency gains and costof capital and their impact on price levelswere arguably the most prominent aspect ofthe 1999 periodic review (Ofwat, 1998; Clifton,1999; Bostock, 1999; Ofwat, 1999; Weeden,1999). This issue, which overshadowed the1999 periodic review, has continued to rumbleon against the backdrop of redundancies andindustry restructuring.

IMPROVING THE COMPLIANCECOST ASSESSMENT PROCESS

Which side was ‘correct’, if any, in estima-tion of compliance costs in the 1999 periodicreview may never be known given the indus-try restructuring believed by many companiesto be unavoidable as a consequence of the pricelimits for 2000/01–2004/05. In addition, theindustry landscape is continually changing, inparticular relating to competition, which will

13 A comparatively small element of the difference was related toOfwat’s view that certain schemes (required by the EA) were notcost effective.

affect the actual out-turn costs for environmen-tal legislation compliance projects. Nonethe-less, some improvements to the CCA processcan be proposed.

Timely, joint Ofwat–water companypreparation of regulatory approaches

The 1999 periodic review generated heateddebate between the companies and Ofwat inrelation to methods and assumptions as wellas the conclusions. The entire process will havebeen very costly for all parties concerned (bothdirect financial costs as well as, arguably, interms of trust). There is already extensive col-laboration between the various regulators andthe companies in the preparation of guide-lines for certain regulatory submissions (forinstance, the methodology used to appraiseand select schemes to address water resourcedeficits, see UKWIR and EA, 199614). Consider-ation should be given to the further extensionof joint working groups that allow detaileddiscussion on relevant issues to take placebetween relevant parties in sufficient time toapprove assessment methodologies for use inthe periodic review process. This would allowthe hard work to be undertaken up front,engendering buy-in by all parties, minimizingthe amount of work and scope for disagree-ment in the actual periodic review process,when time pressures and politics put pres-sure on the process. In addition, some external(independent or ‘non-aligned’?) representationon these collaborative groups needs to be con-sidered to foster cross sectoral consistency inregulation, which is vital when companies(from different sectors) are competing in thecapital markets.

14 Ofwat were also represented on the steering group for thisproject. The guidelines are currently being reviewed, againwith the steering group comprised of representatives of watercompanies, EA and Ofwat.

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

265

P. McMAHON

Issue detailed guidelines for calculatingenvironmental compliance costs

Following from the above, there is an urgentrequirement for a common set of guidelinessetting out how environmental compliancecosts should be drawn up. Detailed guidancein this area was missing for the 1999 peri-odic review. Their production and use wouldreduce uncertainty and make the auditing pro-cess more efficient. The precedent here is themethodological guidance issued by HMIP forIPC and more recently the EA for IPPC, aswell as the generic guidance for producingCCAs published by the European Environ-ment Agency (EEA, 1999). Key assumptions(or sets of assumptions) such as discount rateand time horizon can be agreed upon. Forinstance, submissions to Ofwat in the 1999 peri-odic review for water resource projects werediscounted at 6% over 30 years, whilst submis-sions to the EA were discounted at 7% over25 years.

In turn, this could be linked to thedevelopment of common, industry wide data-bases and studies of ex post costs of com-pliance as a springboard for ex ante anal-yses. Databases if appropriately designedand used facilitate the capture of institu-tional learning. Ideally, regulators and indus-try should share development. The commer-cial costing databases referred to above pos-sibly suffice here if they are also used bythe regulators.

It must be noted in relation to this andthe previous suggestion that what is notintended is de facto management of the day-to-day operations of the water companiesby the regulators or prescriptive choice ofcapital investment scheme. The benefits ofprice-cap regulation must not be lost: com-panies need to retain strong incentives toidentify lower cost options to meet legisla-tive and regulatory requirements relating toenvironmental standards and other objec-tives.

More sophisticated treatment of risk anduncertainty in CCAs

Whilst careful project selection and (initial)design and use of guidance and databasesshould minimize the variance between esti-mate and out-turn cost and between companyestimate and regulatory acceptance, risk anduncertainty is persistent. As a start, improvedmethods for producing and using CCAs arerequired that deal with risk and uncertaintyin a more explicit and sophisticated manner.Single point estimates are not sufficient in deal-ing with such major investment projects andprogrammes with the range of risks and uncer-tainties as discussed above. Approaches toeconomic analysis considering risk and uncer-tainty can begin to deal with this (see e.g. Dixitand Pindyck, 1994).

Extend training/awareness raising

The input of economists in CCA remains lim-ited. CCA would be improved by a betterunderstanding of economic/financial issues byengineers, who are mostly responsible for thepreparation of a CCA in the water industry.One could also argue that regulators (whetherenvironmental or economic) would similarlybenefit from increased understanding of thework of engineers and the water companies.Whilst the issues of risk and uncertainty aregaining increased attention in the water indus-try the understanding and use of risk assess-ment methodologies remains underdevelopedand this is an additional area that needs rectify-ing. Secondment is an obvious option, but theissues of commercial confidentiality and cap-ture might prove insurmountable. One wayof dealing with the training/awareness issueis through ongoing professional developmentrequired by institutions such as ICE (the Insti-tution of Civil Engineers) and CIWEM (theChartered Institution of Water and Environ-mental Management).

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

266

CCAs AND WATER INDUSTRY IN ENGLAND AND WALES

CONCLUSIONS

Regulating the environmental performanceof privatized water companies requires theregulators to obtain company estimates ofcompliance cost. The information problemgenerally is the most important and mostintractable in the economics of regulation.

CCAs are being increasingly demanded andused in the water industry as part of theregulatory process, principally as a means tobalance the, typically, conflicting objectives.At the simplest level, this constitutes a three-way balancing act: to maximize environmentalenhancement whilst ensuring that customercharges are minimized whilst addressing thelegitimate interests of the water company.

Because of the tightly regulated nature ofthe water industry, with extensive submissionand scrutiny of CCAs and other data, it islikely that the objective costs of complianceare more discoverable than in most industrialsectors. However, untangling costs for specificareas of legislation remains to some degreesubjective. In the water industry the chiefconcern is, of course, ex ante discovery ofcosts. The view of Ofwat is that companieshave overstated compliance costs. There area number of possible reasons for this. Thespecific assumptions used by Ofwat vis-a-visfuture efficiency savings and the cost of capitalare notable causes of the differentials betweencompany submissions and the final price limitsdetermined by Ofwat. There are a numberof other reasons why this differential mighthave arisen, including gaming. However, theprincipal cause might be less due to gamingand more a real lack of knowledge on thepart of companies of future efficiency savingsand the actual costs of projects. As MartinWeitzman has put it,

In most cases even the managers and engi-neers most closely associated with produc-tion will be unable to precisely specifybeforehand the cheapest way to generatevarious hypothetical output levels. Because

they are yet further removed from the pro-duction process, the regulators are likely tobe vaguer still about a firm’s cost function(Weitzman, 1978, p. 684).

Nonetheless, the CCAs produced in thewater industry have had, and continue tohave, massive impact on policy design, bothat the national/international levels and in rela-tion to the specific policy (strictly, programme)of environmental enhancements in the waterindustry. Given the magnitude of investmentinvolved it is vital that the preparation anduse of CCAs in the water industry is as opti-mal as possible. To this end, a number ofspecific improvements are identified. Theserelate to the more prosaic issue of the CCArather than changes to the regulatory frame-work. These changes relate to increased col-laboration between industry and regulatorsin working groups to design/approve regu-latory methodologies ahead of the periodicreview. In particular, more detailed guidance isrequired for preparation of a CCA. Further useof compliance cost databases is recommended.Finally, the entire process would be facilitatedby increased training and awareness raising ofdifferent disciplines, specifically economics bythe engineers largely responsible for prepara-tion of CCAs.

Would these proposals help improve theregulatory process and facilitate better out-comes, that is a better balance of producer andconsumer interests? Only experience wouldshow for sure, but the proposals are relativelystraightforward, easy to implement and couldbe halted quickly if they did not work15. How-ever, improvement to the preparation of CCAsis required and proposals such as these aresurely worth further consideration.

ACKNOWLEDGEMENTS

The views in this paper represent those of the authoronly and do not necessarily reflect any position held

15 It is worth noting that they are also applicable to industrialsectors not subject to detailed economic regulation.

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

267

P. McMAHON

by Southern Water. The paper was prepared when theauthor was at the National Centre for Risk Analysis andOptions Appraisal, Environment Agency, London.

REFERENCES

Armstrong M, Cowan S, Vickers J. 1994. RegulatoryReform: Economic Analysis and British Experience. MITPress: Cambridge, MA.

Averch M, Johnson L. 1962. Behaviour of the firm underregulatory constraint. American Economic Review 52:1052–1069.

Baldwin R, Cave M. 1999. Understanding Regulation:Theory, Strategy and Practice. Oxford: Oxford UniversityPress.

Baron D. 1985. Noncooperative regulation of anonlocalized externality. RAND Journal of Economics16(4): 553–568.

Beesley M, Littlechild S. 1989. The regulation ofprivatized monopolies in the United Kingdom. RANDJournal of Economics 20(3): 454–472.

Bostock J. 1999. Cost base wrangle moves up a gear.Water Magazine 2 April.

Byatt ICR. 1990. UK Office of Water Services: structureand policy. Utilities Policy 1(2): 164–171.

Cabinet Office. 1998. The Better Regulation Guide andRegulatory Impact Assessment. Cabinet Office: London.

Clifton M. 1999. The final straw? Water Magazine 22October.

Cowan S. 1993. Regulation of several market failures: thewater industry in England and Wales. Oxford Reviewof Economic Policy 9(4): 14–23.

Deighton-Smith R. 1997. Regulatory impact analysis:best practices in OECD countries. In Regulatory ImpactAnalysis: Best Practices in OECD Countries. Organisationfor Economic Co-operation and Development: Paris.

Dixit AV, Pindyck RS. 1994. Investment UnderUncertainty. Princeton University Press: Princeton, NJ.

Environment Agency (EA). 1996. Taking Account of Costsand Benefits (Sustainable Development Publication Series).Bristol: EA.

European Environment Agency (EEA). 1999. Guidelinesfor Defining and Documenting Data on Costs of PossibleEnvironmental Protection Measures, Technical Report 27.Copenhagen: EEA.

Foster CD. 1992. Privatization, Public Ownership and theRegulation of Natural Monopoly. Oxford: Blackwell.

Helm D. 1994. British utility regulation: theory, practiceand reform. Oxford Review of Economic Policy 10(3):17–39.

Kahn AE. 1988. The Economics of Regulation: Principlesand Institutions. MIT Press: Cambridge, MA.

Laffont J-J, Tirole J. 1993. A Theory of Incentives inProcurement and Regulation. MIT Press: Cambridge,MA.

McMahon P, Moran D (eds). 2000. Economic Valuationof Water Resources: Policy and Practice. CharteredInstitution of Water and Environmental Management:London.

Office of Water Services (Ofwat). 1993. The Cost ofQuality: a Strategic Assessment of the Prospects for FutureWater Bills. Ofwat: Birmingham.

Office of Water Services (Ofwat). 1998. Prospects for Prices:a Consultation Paper on Strategic Issues Affecting FutureWater Bills. Ofwat: Birmingham.

Office of Water Services (Ofwat). 1999. FinalDeterminations: Future Water and Sewerage Charges2000–2005. Ofwat: Birmingham.

Pearce DW. 1998. Environmental appraisal andenvironmental policy in the European Union.Environmental and Resource Economics 11(3/4): 489–501.

Stewart M. 1993. Modelling Water Costs 1992–93: FurtherResearch into the Impact of Operating Conditions onCompany Costs, Ofwat Research Paper 2. Ofwat:Birmingham.

Stigler G. 1971. The theory of economic regulation. BellJournal of Economics 2: 3–21.

UK Water Industry Research Ltd (UKWIR), EnvironmentAgency (EA). 1996. Economics of Demand Management:Practical Guidelines. UKWIR–EA: London–Bristol.

Weeden R. 1999. It’s time to jump off the price escalator.Water Magazine 1 October.

Weitzman M. 1978. Optimal rewards for economicregulation. American Economic Review 68: 683–691.

Copyright 2002 John Wiley & Sons, Ltd and ERP Environment Eur. Env. 12, 257–268 (2002)

268