Embed Size (px)

Citation preview

COST CONCEPTS, ANDCLASSIFICATIONS

IEG2H2-w2 1

COST ESTIMATING USED TO

Provide information used in setting a selling price forquoting, bidding, or evaluating contracts

Determine whether a proposed product can be madeand distributed at a profit (EG: price = cost + profit)

Evaluate how much capital can be justified forprocess changes or other improvementsprocess changes or other improvements

Establish benchmarks for productivity improvementprograms

IEG2H2-w2 2

Cost Viewpoints

Manufacturing Cost StructureViewpoint

Fixed/Variable Viewpoint

Past/Future Viewpoint

Life Cycle Viewpoint

IEG2H2-w2 3

DirectMaterials

DirectLabor

ManufacturingOverhead

Manufacturing Costs

The ProductThe Product

IEG2H2-w2 4

Direct Materials

Those materials that become an integral part of theproduct and that can be conveniently traced directly

to it.

Example: A radio installed in an automobile

IEG2H2-w2 5

Direct Labor

Those labor costs that can be easily traced toindividual units of product.

Example: Wages paid to automobile assembly workers

IEG2H2-w2 6

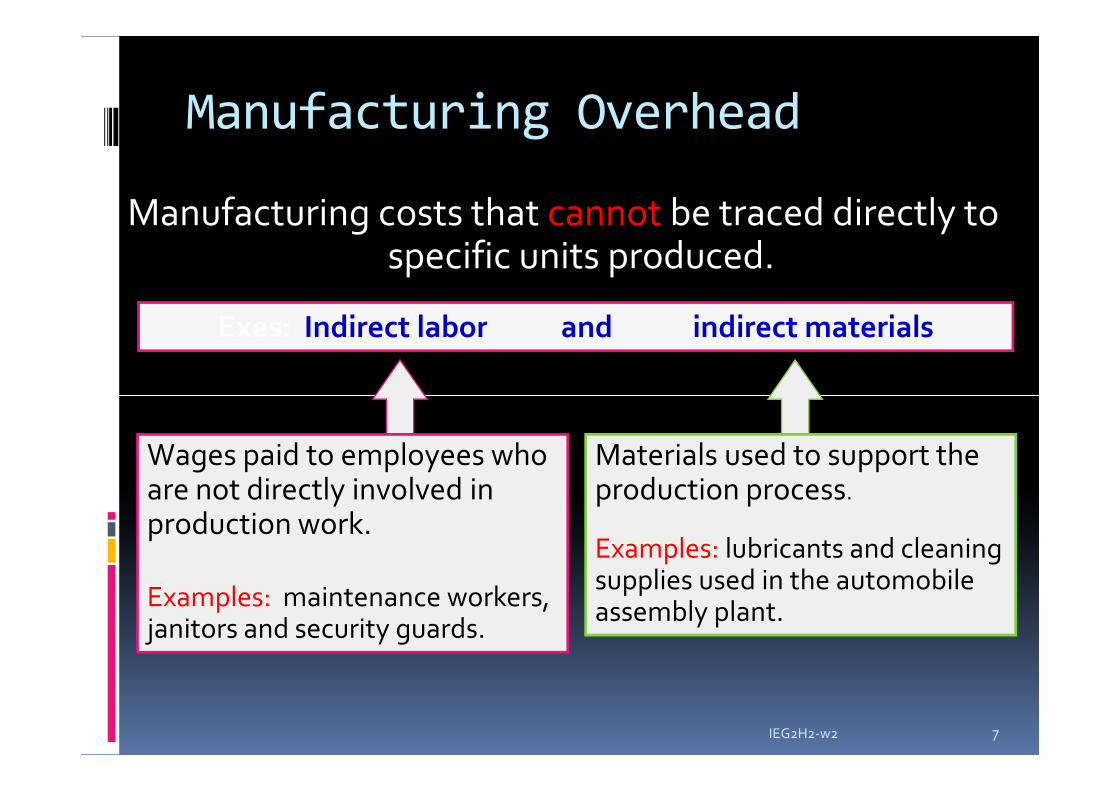

Manufacturing costs that cannot be traced directly tospecific units produced.

Manufacturing Overhead

Exes: Indirect labor and indirect materials

Wages paid to employees whoare not directly involved inproduction work.

Examples: maintenance workers,janitors and security guards.

Materials used to support theproduction process.

Examples: lubricants and cleaningsupplies used in the automobileassembly plant.

IEG2H2-w2 7

Nonmanufacturing Costs

Marketing and SellingCost

Administrative Cost

Costs necessary to get the orderand deliver the product.

All executive, organizational, andclerical costs.

IEG2H2-w2 8

Manufacturing Cost Flows

Work inDirect Labor

Balance SheetCosts Inventories

IncomeStatementExpenses

Material Purchases Raw Materials

Selling andAdministrative

Period Costs

FinishedGoods

Cost ofGoods

Sold

Selling andAdministrative

ManufacturingOverhead

Work inProcess

Direct Labor

IEG2H2-w2 9

Indirectlabor cost

IndirectOthers cost

Overh

ead

cost

Manufa

ctu

ring

cost

Adm.cost

Sellingcost

taxes

Profit

Se

llin

ga

nd

Ad

min

istr

ati

ve

Pro

duction

Cost

Sellin

gPrice

Cost

IEG2H2-w2 10

Pri

me

Cost

DirectLabor

DirectMaterial

labor cost

IndirectMaterial cost

Overh

ead

cost

Manufa

ctu

ring

cost

Pro

duction

Cost

Sellin

gPrice

Cost component

Cost structure base on product manufacturing

0

Cost Classifications forPredicting Cost Behavior

How a cost will react toHow a cost will react tochanges in the level of

business activity.

Total variable costs Total variable costschange when activitychanges.

Total fixed costs remainunchanged when activitychanges.

Fixed and Variable Viewpoint

A Fixed Cost (FC) is any cost that does not vary inproportion to the quantity of output. Examples include rent, depreciation, lighting, and

supervisor salaries.

Fixed Costs are commonly fixed only over a certain range of Fixed Costs are commonly fixed only over a certain range ofproduction, called the relevant range.

For example supervisor salaries or lighting are fixed for oneshift operation but step to a new higher level for two shiftoperation.

Successive relevant ranges are often representedgraphically as a step function.

IEG2H2-w2 12

A Variable Cost (VC) is a cost that varies inproportion to the quantity of output.

Common examples include direct materials and directlabor.labor.

Variable Costs are often represented as a linearfunction of output

VC(x) = rate * x; where x is the level of production

Total Cost is the sum of fixed costs and variablecosts

TC(x) = FC + VC(x)

IEG2H2-w2 13

Example: Total Variable Cost

Your total long distance telephone bill isbased on how many minutes you talk.

Minutes Talked

Tota

lLo

ng

Dis

tan

ceTe

lep

ho

ne

Bill

IEG2H2-w2 14

Variable Cost Per Unit

The cost per long distance minute talked isconstant. For example, 10 cents per minute.

Minutes Talked

Pe

rM

inu

teTe

lep

ho

ne

Ch

arg

e

IEG2H2-w2 15

Total Fixed Cost

Your monthly basic telephone bill probably doesnot change when you make more local calls.

Number of Local Calls

Mo

nth

lyB

asic

Tele

ph

on

eB

ill

IEG2H2-w2 16

Fixed Cost Per Unit

Mo

nth

lyB

asic

Tele

ph

on

eB

ill

The average cost per local call decreases as morelocal calls are made.

Number of Local Calls

Mo

nth

lyB

asic

Tele

ph

on

eB

illp

er

Lo

calC

all

IEG2H2-w2 17

Cost Classifications forPredicting Cost Behavior

Behavior of Cost (within the relevant range)

Cost In Total Per Unit

Variable Total variable cost changes Variable cost per unit remainsVariable Total variable cost changes Variable cost per unit remains

as activity level changes. the same over wide ranges

of activity.

Fixed Total fixed cost remains Fixed cost per unit goes

the same even when the down as activity level goes up.

activity level changes.

IEG2H2-w2 18

The Past/Future Viewpoint

The Past/Future viewpoint focuses on when costsand revenues occur relative to “time now”.

A past cost is any cost that occurred prior to “timenow”.now”.

A future cost is any cost that is expected to occursubsequent to “time now”.

Similar interpretations apply to past revenue andfuture revenue.

IEG2H2-w2 19

Opportunity Costs

The potential benefit that is givenup when one alternative isselected over another.

Example: If you wereExample: If you werenot attending college,you could be earning$15,000 per year.Your opportunity costof attending college forone year is $15,000.

Costs Related to Decision Making

Opportunity Costs - costs when taking one actionrequires giving up the opportunity to earn profitsfrom a different action

Nike Inc. has limited production capacity. What Nike Inc. has limited production capacity. Whatwould be Nike’s opportunity cost of accepting aspecial order from the military for combat boots?

If Nike accepts the special order, they may not beable to produce enough product for other sales.So, Nike would lose the profit from the other sale.

IEG2H2-w2 21

Sunk Costs

Sunk costs cannot be changed by any decision. They arenot differential costs and should be ignored when

making decisions.

Example: You bought an automobile that costExample: You bought an automobile that cost$10,000 two years ago. The $10,000 cost is sunkbecause whether you drive it, park it, trade it, or sellit, you cannot change the $10,000 cost.

IEG2H2-w2 22

LIFE-CYCLE COSTLIFE-CYCLE COST

Life-cycle cost is the summation of all costs,both recurring and nonrecurring, related to aproduct, structure, system, or service duringits life span.

Life cycle begins with the identification of

Life-cycle cost is the summation of all costs,both recurring and nonrecurring, related to aproduct, structure, system, or service duringits life span.

Life cycle begins with the identification ofLife cycle begins with the identification ofthe economic need or want ( therequirement ) and ends with the retirementand disposal activities.

Life cycle begins with the identification ofthe economic need or want ( therequirement ) and ends with the retirementand disposal activities.

IEG2H2-w2 23

The Life Cycle viewpoint focuses on when cashflows occur within the life cycle of an asset’s (orproject’s) service life.

Investment cost is the capital (money) required formost activities of the acquisition phase;

Operating and Maintenance (O&M) Costs Operating and Maintenance (O&M) Costs

Salvage Value / disposal cost includes non-recurringcosts of shutting down the operation;

IEG2H2-w2 24

LCC-Investment Costs

Investment cost are the costs required toplace the asset in service.

Purchase Cost

Training Cost Training Cost

Shipping and Installation Cost

Initial Tooling Cost

Supporting Equipment Cost

Site Preparation

IEG2H2-w2 25

LCC- O&M Costs

Operating and Maintenance (O&M) Costs are theroutine costs required to keep the asset inservice.

A wide variety of costs may be considered here A wide variety of costs may be considered heredepending on the situation.

Energy Costs

Routine Maintenance (lubricants, filters, etc.)

Indirect Labor

etc.

IEG2H2-w2 26

LCC-Salvage Value

Salvage Value is the net cash flow resulting fromdisposing of the asset or terminating the project.

Salvage Value may be positive or negative.

Salvage Value is determined by deducting the Salvage Value is determined by deducting thecost of disposal from the market value of theasset at the time of disposal.

Salvage value is typically one of the most difficultvalues to estimate.

IEG2H2-w2 27

COST, VOLUME, and BREAKEVENPOINT RELATIONSHIP

IEG2H2-w2 28

Price-Demand Relationship

Price•Perfect Competition

IEG2H2-w2 29

p = a - bD

Units of Demand

Price•Perfect Competition

•Product Substitution

Monopoly

Oligopoly

Total Revenue Function

Tota

lR

even

ue

TR = Price x Demand

Substitute p = a - bD

TR = aD - bD2

Demand that will produce max revenue?

dTR/dD = a-2bD = 0

IEG2H2-w2 30

Demand

Tota

lR

even

ue

dTR/dD = a-2bD = 0

D’ = a/2b

How would you guarantee that D’

maximizes total revenue?D’=a/2b

* Maximum profits may not be obtained by maximizing revenue

PROFIT MAXIMIZATION D*

Occurs where total revenue exceeds totalcost by the greatest amount;

Occurs where marginal cost = marginal Occurs where marginal cost = marginalrevenue;

Occurs where dTR/dD = d Ct /dD;

IEG2H2-w2 31

PROFIT MAXIMIZATION D*

Total Revenue

CT

C

Profit

Max Profit

CT = CF + Cv

Cv = (cv) (D) where cv is the variable cost per unit

Case 1:

Demand is function of price

D1 , D2 = breakeven points; Total Rev = Total Cost

D* = Optimal demand for maximum profit

IEG2H2-w2 32

Volume (Demand)

CF

Cv

D1 D* D2

D* = Optimal demand for maximum profit

Profit(loss) = total revenue - total costs

= (aD-bD2) - (CF + cvD)

Take derivative and set to zero

Optimal D* =

b

aD0

2b

vca

How would you check profit maxima vs. profit minima?

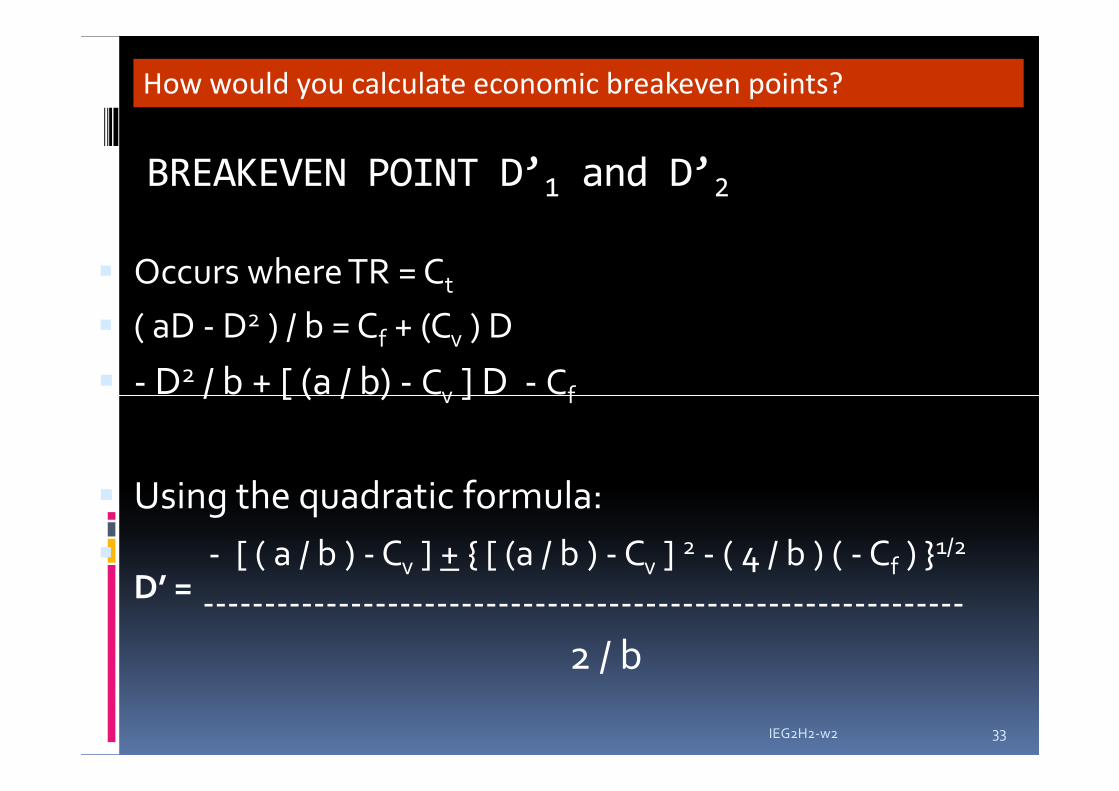

BREAKEVEN POINT D’1 and D’2

Occurs where TR = Ct

( aD - D2 ) / b = Cf + (Cv ) D

- D2 / b + [ (a / b) - Cv ] D - Cf

How would you calculate economic breakeven points?

- D / b + [ (a / b) - Cv ] D - Cf

Using the quadratic formula:

- [ ( a / b ) - Cv ] + { [ (a / b ) - Cv ] 2 - ( 4 / b ) ( - Cf ) }1/2

D’ = --------------------------------------------------------------

2 / b

IEG2H2-w2 33

Breakeven Point

TR

CT

Breakeven Point Profit

Case 2

When price is independent of demand

Total revenue = total cost

IEG2H2-w2 34

Volume (Demand)

Fixed Costs

Variable CostsCF

Loss

DcCDp vF

D’

D´ =CF

(p-cv)

Example: 2-7

A company produces an electronic timingswitch that is used in consumer andcommercial products made by several othermanufacturing firms. The fixed cost Cf is$73,000 per month, and the variable cost Cv is$83 per unit. The selling price per unit is$83 per unit. The selling price per unit isp=$180-0.02(D). For this situation,

a. Determine the optimal volume for this productand confirm that a profit occurs at this demand.

b. Find the volumes at which breakeven occurs;that is, what is the domain of profitable demand?

IEG2H2-w2 35

Contoh-3Sebuah perusahaan merencanakan membuat suatu produk;

Departemen penjualan mengestimasikan bahwa jumlah produkyang akan terjual sangat tergantung dari harga jual per unit. Bilaharga jual per unit naik maka jumlah yang terjual akan menurun.Secara numerik diformulasikan sbb:

P = 35000 - 20 Qdimana P = harga jual per unit.

Q = jumlah produk terjual per tahun

Dilain pihak, manajemen mengestimasikan bahwa rata-rata biaya

IEG2H2-w2 36

Dilain pihak, manajemen mengestimasikan bahwa rata-rata biayapembuatan dari produk tersebut akan menurun sesuai dengankenaikan jumlah unit terjual. Mereka mengestimasikan :

C = 4000 Q + 8 jutadimana C = biaya produksi dari penjualan Q per tahun.

Manajemen Perusahaan mengharapkan hasil produksi danpenjualan produk mencapai keuntungan yang maksimal. Berapajumlah produk yang direncanakan untuk dijual per tahun agarharapan tersebut tercapai.