Embed Size (px)

Citation preview

Copyright 2014 by Diane S. Docking 1

Interest Rate Risk Management:DGAP

Learning Objectives

Define the duration gap measure of interest rate risk

Understand the process of DGAP management

Copyright 2014 by Diane S. Docking 2

Copyright 2014 by Diane S. Docking 3

Duration GAP

Why look at Duration GAP? ISGAP does not fully take into account the

effect of changing interest rates on bank’s capital.

Immunize Financial Institution Balance sheet

4Copyright 2014 by Diane S. Docking

Duration Gap Analysis

Recall: The basic equation for determining the change in market value for assets or liabilities is:

% Change in Value = – DUR x [Δi / (1 + i)]

or

Change in Value = – DUR x [Δi / (1 + i)] x Original Value

Copyright 2014 by Diane S. Docking 5

Immunizing a Bank’s Balance Sheet

Use duration to immunize bank assets and liabilities, in effect the capital. Duration is an attractive measure because it is

_____________across assets and liabilities.

If duration of capital = , the bank will not be affected by changes in interest rates.

Copyright 2014 by Diane S. Docking 6

Dollar-Weighted Average Duration of an Asset Portfolio

n

1iiA iA Dx w D

Where:

wi = the dollar amount of the ith asset divided by total assets

DAi = the duration of the ith asset in the portfolio

001TA

i

iDTA A

Copyright 2014 by Diane S. Docking 7

Dollar-Weighted Average Duration of a Liability Portfolio

n

1iLiL i

D x w D

Where:

wi = the dollar amount of the ith liability divided by total liabilities

DLi = the duration of the ith liability in the portfolio

001TL

i

iDTL L

Copyright 2014 by Diane S. Docking 8

Leverage-Adjusted Duration Gap (DGAPK)

TA

TL x D - D DGAP LAK

where:TA or A= total assets of an investment portfolio or a bankK = total capital of the bank or net worth of the

investment portfolioTL or L = total liabilities of an investment portfolio or a bank

Copyright 2014 by Diane S. Docking 9

Duration Gap

DGAP models focus on managing net worth (capital) or the net market value of the portfolio, recognizing the timing of all individual cash flows.

Management’s goal is to stabilize or increase net worth or the value of the portfolio.

If Fund/Bank expects interest rates to increase (decrease), then it will want a negative (positive) DGAP

Copyright 2014 by Diane S. Docking 10

Change in the Value of a Bank’s Capital

TA i) (1

Δi DGAPΔK K

Copyright 2014 by Diane S. Docking 11

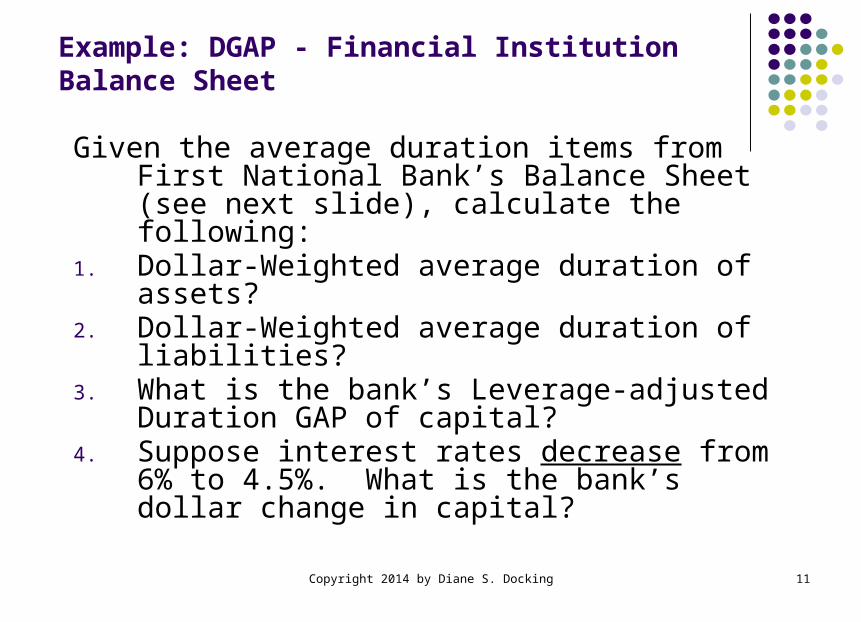

Example: DGAP - Financial Institution Balance Sheet

Given the average duration items from First National Bank’s Balance Sheet (see next slide), calculate the following:

1. Dollar-Weighted average duration of assets?2. Dollar-Weighted average duration of liabilities?3. What is the bank’s Leverage-adjusted Duration

GAP of capital?4. Suppose interest rates decrease from 6% to

4.5%. What is the bank’s dollar change in capital?

Duration of First National Bank's Assets and Liabilities

First National BankAmount Duration($ millions) (years)

AssetsReserve and cash items 5 0.0Securities Less than 1 year 5 0.4 1 to 2 years 5 1.6 Greater than 2 years 5 5.5Residential mortgages Variable-rate 10 0.5 Fixed-rate (30-year) 10 6.0Commercial loans Less than 1 year 25 0.7 1 to 2 years 20 1.4 Greater than 2 years 5 2.3Physical capital 10 0.0 Total Assets 100

LiabilitiesCheckable deposits 5 0.1MMDAs 6 0.5Savings deposits 8 1.0CDs Variable-rate 3 0.5 Less than 1 year 5 0.2 1 to 2 years 15 1.9 Greater than 2 years 23 5.6Fed funds 5 0.0Borrow ings Less than 1 year 2 0.3 1 to 2 years 8 1.5 Greater than 2 years 15 5.3 Total Liabilities 95

Capital 5

Total Liabilities & Capital 100

Example: IDGAP - Financial Institution Balance Sheet

12Copyright 2014 by Diane S. Docking

Assume Macaulay duration

Example: DGAP - Financial Institution Balance Sheet

First National BankAmount Duration Weight Wtd.Duration($ millions) (years) (%) (years)

AssetsReserve and cash items 5 0.0 5% 0.000Securities Less than 1 year 5 0.4 5% 0.020 1 to 2 years 5 1.6 5% 0.080 Greater than 2 years 5 5.5 5% 0.275Residential mortgages Variable-rate 10 0.5 10% 0.050 Fixed-rate (30-year) 10 6.0 10% 0.600Commercial loans Less than 1 year 25 0.7 25% 0.175 1 to 2 years 20 1.4 20% 0.280 Greater than 2 years 5 2.3 5% 0.115Physical capital 10 0.0 10% 0.000 Total Assets 100 100% DA 1.595

LiabilitiesCheckable deposits 5 0.1 5% 0.005MMDAs 6 0.5 6% 0.032Savings deposits 8 1.0 8% 0.084CDs Variable-rate 3 0.5 3% 0.016 Less than 1 year 5 0.2 5% 0.011 1 to 2 years 15 1.9 16% 0.300 Greater than 2 years 23 5.6 24% 1.356Fed funds 5 0.0 5% 0.000Borrow ings Less than 1 year 2 0.3 2% 0.006 1 to 2 years 8 1.5 8% 0.126 Greater than 2 years 15 5.3 16% 0.837 Total Liabilities 95 100% DL 2.773 DGAPK -1.039

13

Copyright 2014 by Diane S. Docking

Copyright 2014 by Diane S. Docking 14

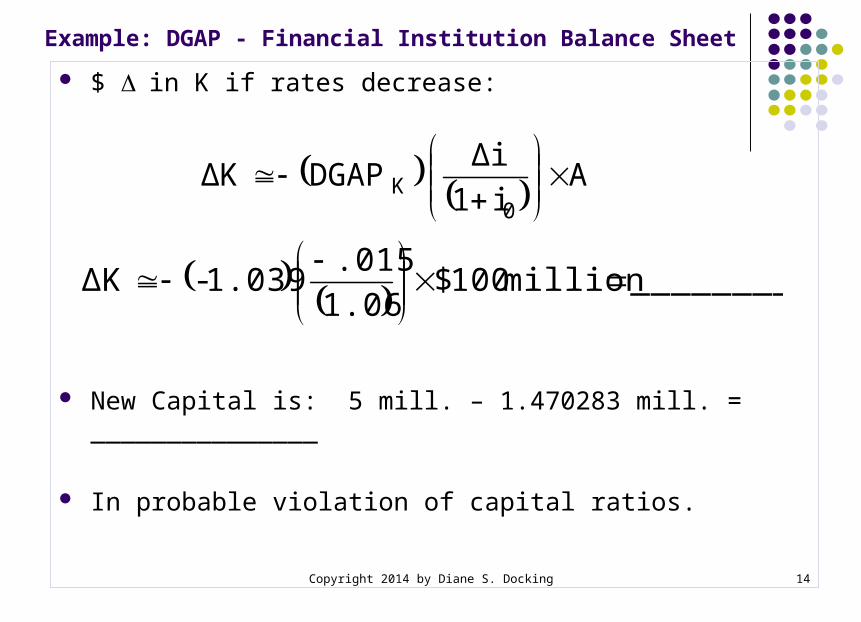

Example: DGAP - Financial Institution Balance Sheet

$ D in K if rates decrease:

New Capital is: 5 mill. – 1.470283 mill. = _______________

In probable violation of capital ratios.

Ai1

ΔiDGAPΔK

0K

_________million 100$1.06

.0151.039-ΔK

Copyright 2014 by Diane S. Docking 15

Impact of Changing Interest Rates on a Portfolio’s or Bank’s Capital

Sign of DGAP E(i) NW or Capital

Rise Decrease Positive DGAP

Fall Increase

Rise Increase Negative DGAP

Fall Decrease

Rise No Change Zero DGAP

Fall No Change

Copyright 2014 by Diane S. Docking 16

Problems with Duration Gap Analysis

1. Finding Assets and Liabilities of the Same Duration Can be Difficult

2. Some Assets and Liabilities May Have Patterns of CFs Not Well Defined

3. Customer Prepayments May Distort the Expected Cash Flows in Duration

4. Not a Linear Relationship Between Prices and Interest Rates5. Any duration analysis assumes that the yield curve is flat and

shifts in the level of interest rates imply parallel shifts of the yield curve. In reality, the yield curve is seldom flat, and short-term and long-term interest rates have different volatilities or shifts over time.

Copyright 2014 by Diane S. Docking 17

Problems with Duration Gap Management

6. Overly aggressive management that “bets the bank.” This happened to First Pennsylvania Corp. in late 1970s. With rates high at the end of an expansion, it bought long-term securities with short-term borrowed funds (negative dollar gap, positive duration gap). However, instead of rates falling, they shot up further, causing both negative NIMs and losses on equity leading to bankruptcy. Moral: don’t bet the bank on interest rates!

7. Average durations of assets and liabilities drift or change over time and not at the same rates. At one point the duration gap may be 2.0 but one year later it may be only 0.5. Some experts advise rebalancing to keep the duration gap in a target range over time.

Example: Immunize Financial Institution Balance Sheet

18

First National Bank

Amount Duration Weight Wtd.Duration

($ millions) (years) (%) (years)

Assets

Reserve and cash items 5 0.0 5% 0.000

Securities

Less than 1 year 5 0.4 5% 0.018

1 to 2 years 5 1.6 5% 0.073

Greater than 2 years 5 5.5 5% 0.252

Residential mortgages

Variable-rate 10 0.5 9% 0.046

Make 30-yr 5% mtgs. 9 11.4 9% 0.972

Fixed-rate (30-year) 10 6.0 9% 0.549

Commercial loans

Less than 1 year 25 0.7 23% 0.160

1 to 2 years 20 1.4 18% 0.256

Greater than 2 years 5 2.3 5% 0.105

Physical capital 10 0.0 9% 0.000 Total Assets 109 100%

DA 2.431

Liabilities

Checkable deposits 5 0.1 5% 0.005

MMDAs 6 0.5 6% 0.029

Savings deposits 8 1.0 8% 0.077

CDs

Variable-rate 3 0.5 3% 0.014

Attract 3% 90-day CDs 9 0.25 9% 0.022

Less than 1 year 5 0.2 5% 0.010

1 to 2 years 15 1.9 14% 0.273

Greater than 2 years 23 5.6 22% 1.235

Fed funds 5 0.0 5% 0.000

Borrowings

Less than 1 year 2 0.3 2% 0.006

1 to 2 years 8 1.5 8% 0.115

Greater than 2 years 15 5.3 14% 0.762 Total Liabilities 104 100%

DL 2.547 DGAPK 0.000

Copyright 2014 by Diane S. Docking

90/360

See next slide

Duration Calculation

19

rm = 5.00%

Calculation of monthly payment

Loan Amount 100,000.00

Annual Interest Rate 5.00%

Loan Period in Years 30

Number of Payments 360

Monthly Payment 536.8216

t CF PVCF at 5.0%/12 t x PVCF Duration

1 536.82 534.5941 534.5941

2 536.82 532.3759 1,064.7518

3 536.82 530.1669 1,590.5007

4 536.82 527.9670 2,111.8681

5 536.82 525.7763 2,628.8814

355 536.82 122.6791 43,551.0918

356 536.82 122.1701 43,492.5520

357 536.82 121.6632 43,433.7481

358 536.82 121.1583 43,374.6835

359 536.82 120.6556 43,315.3611

360 536.82 120.1550 43,255.7843

100,000.0000 13,718,611.7718 11.4322 yearsCopyright 2014 by Diane S. Docking

![(20/19. 06 DGAP/SET/1303/2017 DGAP/SET/10/2017 LL.] N01851/DGAP/SET/10/2017 - ALGERIE POSTE](https://img.dokumen.tips/doc/110x75/5e577db6c60636027e71c121/-2019-06-dgapset13032017-dgapset102017-ll-n01851dgapset102017.jpg)