Embed Size (px)

Citation preview

DiGi – 2007 and beyondNovember 2007

Confidential

CONFIDENTIAL

DiGi in the Malaysian mobile market

Total market subscriptions (Total market subscriptions (‘‘000)000) Mobile penetrationMobile penetration

78.2%72.3%74.1%

56.5%

43.9%36.9%

2002 2003 2004 2005 2006 1H2007

195451945419511

14611

111249053

2002 2003 2004 2005 2006 1H2007

61165312

4795

32392207

1616

2002 2003 2004 2005 2006 3Q2007

Source: MCMC

DiGi subs & revenue market shareDiGi subs & revenue market share

24.6% 24.8% 25.3% 25.6%

27.3%28.1% 28.4%

22.5%23.5%

24.6% 24.4% 24.4%25.4%

Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007

Subscriber Share Mobile Revenue Share

Source: MCMC

DiGi subscriber base (DiGi subscriber base (‘‘000)000)

CONFIDENTIAL

DiGi in Q307

3

1113

526

1058

502

273250 241

93

Revenue (RM mil) EBITDA (RM mil)

PAT (RM mil) Net Adds (‘000)

Q207 Q307 Q207 Q307

Q207 Q307 Q207 Q307

47.4% 47.3%

Strong revenue growth momentum

on increasing MOU and stable ARPU

solid EBITDA margin

Healthy gross activations

added 93k new customers

prepaid impacted by rotational churn

steady postpaid growth

Ongoing focus:strengthen key market offerings

operational excellence

upgrade of core technology platforms

CONFIDENTIAL

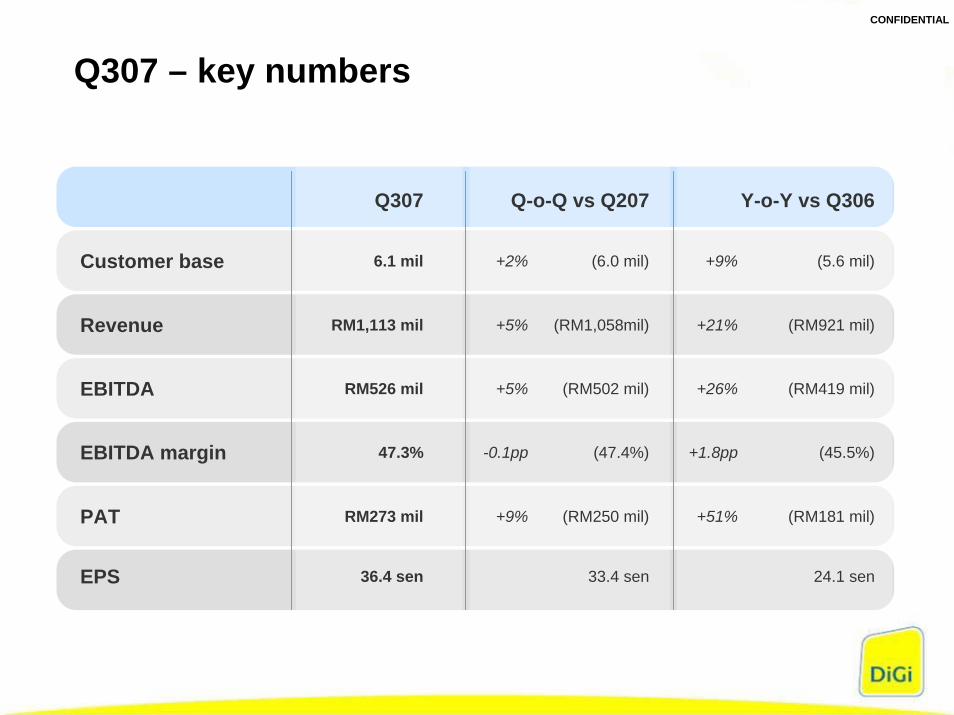

Q307 – key numbers

Q307 Q-o-Q vs Q207 Y-o-Y vs Q306

Customer base 6.1 mil +2% (6.0 mil) +9% (5.6 mil)

(RM1,058mil) (RM921 mil)

(RM419 mil)

(45.5%)

(RM181 mil)

24.1 sen

(RM502 mil)

(47.4%)

(RM250 mil)

33.4 sen

Revenue RM1,113 mil +5% +21%

EBITDA RM526 mil +5% +26%

EBITDA margin 47.3% -0.1pp +1.8pp

PAT RM273 mil +9% +51%

EPS 36.4 sen

CONFIDENTIAL

Current propositions by DiGi

1Plan and 1LFR reinforcing simplicity and best value position

Strengthening brand affinity – YCF and True Value postpaid prepaid campaigns

Launched DiGiRemit –international mobile cash remittance

CONFIDENTIAL

Strong financial performance YTD

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

YTD2006

YTD2007

EBITDA / Margin (RM mil)EBITDA / Margin (RM mil)Revenue (RM mil)Revenue (RM mil)

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

YTD2006

YTD2007

2686

31861219

1525

904 921 967 1015 1058 1113 410 419 476 497 502 526

45.4%45.3% 45.5%49.2% 49.0% 47.4%

47.3%47.9%

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

YTD2006

YTD2007

Profit After Tax (RM mil)Profit After Tax (RM mil) Free Free CashflowCashflow (RM mil)(RM mil)(FCF = EBITDA – Capex)

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

YTD2006

YTD2007

210 181 240 246 250 273

770566

293 205 183 396 403 367 761

1167

CONFIDENTIAL

73 sen net special dividend

Committed to a more efficient capital structure

Cash dividend (net sen/share) : paying progressively higher dividends

CR1 CR2 IntDiv FinDiv IntDiv SpDiv10/05 4/06 7/06 4/07 7/07 10/07

75 sen

60 sen

38.5 sen

50.0 sen

42.0 sen

73 sen

Capital Repayment (CR)

Dividends (interim/final)

Special Dividends

YTD FY 2007 FY 2006

Total borrowings RM300 mil RM300 mil

Cash & cash equivalents

RM931 mil RM870 mil

ROE 42.0% 46.0%

ROCE 43.1% 43.8%

*FCF/share 49.0 sen 24.4 sen

* FCF = EBITDA - Capex

Total pay-out RM2.5bn

7

CONFIDENTIAL

Competitive and industry situation

SIM activations and tariffsprepaid registration low barrier to rotational churn

some pressure on core tariffs

flat price models stimulating higher usage

# of players will increase3 player market today

MVNOs coming into the market

U Mobile preparing for launch

Competition intensifyinghigh marketing activity level

preparing for MNP and potential new entrants

handset subsidies and commitment plans more prevalent as retention/acquisition tools

Low broadband uptake slow growth of 3G services

also slow uptake of other broadband services

possible review and reallocation of spectrum in 2008

CONFIDENTIAL

Raising 2007 guidance

Revised guidance

Revenue growth (%) high teens

EBITDA margin (%) around 47% - 48%

Capex RM600 mil - RM700 mil

PAT / EPS growth (%) high 20’s

9

CONFIDENTIAL

DiGi going forward

Aim for higher market sharemore segmented/niche offerings

focus where we have further potential

continued strong branding

Still opportunities for growthgood potential in segments where we are currently weak : postpaid, business, rural and high-end

MNP and nationwide coverage remove main barriers for DiGi’s growth in these segments

further potential in MOU and data

Operational excellenceprocess re-design and cost focus

planned investments in network quality, capacity and upgrades

enhanced customer experience

strong focus on human capital

Capital management initiativesongoing focus to right-size balance sheet

single-tier tax system has removed tax credit constraint

committed to return excess cash

development

CONFIDENTIAL

High level 2008 Guidance

Guidance

Revenue growth (%) high single digit

EBITDA margin (%) mid-40’s

Capex RM700 mil - RM900 mil

PAT / EPS growth (%) high single digit

11

CONFIDENTIAL

Investing in DiGi

above industry averagerevenue growth

strong cash-flow generation and high yield

narrowed coverage gap

competitive & innovative

gaining market sharestrong support

strong branding

Pure M’sianmobile player

balance sheet strength

CONFIDENTIAL

Telenor in the emerging markets

CONFIDENTIAL

488

645724

613540516

435

683 724

1,097

921

418

Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

EBITDA CAPEX

146

Grameenphone - Bangladesh

Challenging environment

9971,133

1,229 1,152 1,155 1,170

49%57% 59% 53% 47%

36%

Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

Revenues (NOKm)/EBITDA%

Revenue growth of 15% in local currency

Compensation charge of NOK 146 million in Q3

Underlying EBITDA margin of 48%

Interconnect rates reduced from 1 Oct

Mandatory registration of subscriber base by mid Dec 2007

48%

CONFIDENTIAL

1,893 2,041 2,158

2,960 2,999 2,981

37% 36% 37%30% 29% 28%

Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

DTAC - Thailand

Increased tariffs in Q3Revenues (NOKm)/EBITDA%

698 732795

872 864 828

543 565

737

534432 428

Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

EBITDA CAPEX

Net adds of 400k to 14.9 million

Revenue growth of 5% in local currency excluding interconnect

Underlying EBITDA margin of 30%

Revised outlook 2007:

Revenue growth of 5-10%

EBITDA margin of 28-30%

CONFIDENTIAL

265333

486

686

841 887

17%7%

Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

-117 -87 -47

-3 59

1,013

150

880742754 701

847

Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

EBITDA CAPEX

Revenues (NOKm)

Telenor Pakistan

Increasing market shareTelenor Pakistan

Increasing market share

Net adds of 1.9 million subscriptions in Q3 to 12.6 million

Market share from 17% to 18%*

EBITDA affected positively by discount on leased line

Average price decline of 6% in Q3

*PTA figures

CONFIDENTIAL

From two to three players

Net adds of 118k in Q3

ARPU increased by 7% in local currency

Campaigns targeting summer roamers and contract subscribers

Telenor Serbia

Increased competition

175

551669

723804

37% 38% 39% 35%

Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

Revenues (NOKm)/EBITDA%

103

206252

281 279

49

114 108

167

267

Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

EBITDA CAPEX

CONFIDENTIAL

Mobile Operations

ARPU development (USD)

4.64.9

5.4

6.36.57.2

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

Grameenphone

4.34.64.64.54.3

4.8

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

Telenor Pakistan

17.417.017.316.115.515.8

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

DiGi

11.412.0

12.8

10.510.911.2

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

DTAC

15.014.413.7

13.0

Q4 2006 Q1 2007 Q2 2007 Q3 2007

Telenor Serbia

FX as at 30.09.2007

CONFIDENTIAL

214

247

213241 252 245

0.03 0.03 0.03 0.02 0.02 0.02

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

Grameenphone Telenor Pakistan DiGi

DTAC

MoU APPM (USD)

Mobile Operations

MoU/APPM development

123

153146132

142154

0.03 0.04 0.03 0.03 0.03 0.03

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

162

194

163173

193 187

0.10 0.10 0.09 0.09 0.09 0.09

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

314

365327 329

403 396

0.03 0.03 0.03 0.03 0.03 0.03

Q22006

Q32006

Q42006

Q12007

Q22007

Q32007

76

87 8590

0.150.18 0.17 0.17

Q4 2006 Q1 2007 Q2 2007 Q3 2007

Telenor Serbia

CONFIDENTIAL

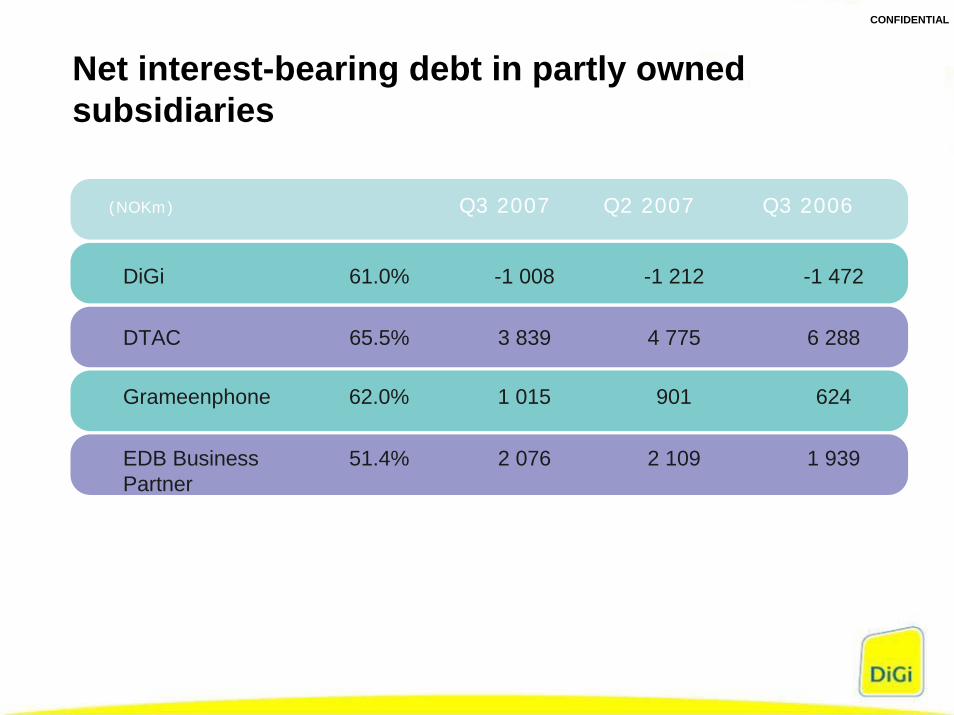

Net interest-bearing debt in partly owned subsidiaries

(NOKm) Q3 2007 Q2 2007 Q3 2006

DiGi 61.0% -1 008 -1 212 -1 472

DTAC 65.5% 3 839 4 775 6 288

Grameenphone 62.0% 1 015 901 624

EDB Business Partner

51.4% 2 076 2 109 1 939

Thank You

Confidential