Embed Size (px)

Citation preview

COMPANY OVERVIEW AS OF Q2 2017

Forward Looking Statements This presentation contains, and the above referenced conference call may contain, forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, including but not limited to statements relating to the Company’s strategic initiatives and adjusted net income per diluted share. Forward-looking statements typically are identified by use of terms such as “may,” “will,” “should,” “plan,” “project,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. These forward-looking statements are based upon the Company's current expectations and assumptions and are subject to various risks and uncertainties that could cause actual results and performance to differ materially. Some of these risks and uncertainties are described in the Company's filings with the Securities and Exchange Commission, including in the “Risk Factors” section of its Annual Report on Form 10-K for the fiscal year ended January 28, 2017. Included among the risks and uncertainties that could cause actual results and performance to differ materially are the risk that the Company will be unsuccessful in gauging fashion trends and changing consumer preferences, the risks resulting from the highly competitive nature of the Company’s business and its dependence on consumer spending patterns, which may be affected by weakness in the economy that continues to affect the Company’s target customer, the risk that the Company’s strategic initiatives to increase sales and margin are delayed or do not result in anticipated improvements, the risk of delays, interruptions and disruptions in the Company’s global supply chain, including resulting from foreign sources of supply in less developed countries or more politically unstable countries, the risk that the cost of raw materials or energy prices will increase beyond current expectations or that the Company is unable to offset cost increases through value engineering or price increases, and the uncertainty of weather patterns. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date they were made. The Company undertakes no obligation to release publicly any revisions to these forward-looking statements that may be made to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

SAFE HARBOR STATEMENT

• $1.8 billion in revenue, strong brand awareness and market share

• Strategic plan being executed based on four pillars: 1) superior product, 2) business transformation through technology, 3) global growth through alternate channels of distribution and 4) store fleet optimization

• Successful execution of this strategy is driving operating margin expansion, robust capital returns and increasing shareholder value

• Experienced and talented management team focused on consistent execution and operational excellence

• As of July 29, 2017, the Company operated 1,026 stores in the United States, Canada and Puerto Rico, online stores in the US and Canada at www.childrensplace.com and had 161 international points of distribution in 19 countries, open and operated by its 7 franchise partners and Tmall.

3

INVESTMENT HIGHLIGHTS #1 pure play children’s specialty apparel retailer in North America, realizing the benefits of a multi-year business transformation strategy

• Deep knowledge of core customer results in consistent delivery of trend-right product, with an attractive price/value proposition, increasing brand reach by introducing extended sizes

• Inventory management transformation began mid 2015. Deployment of several tools continues to drive margin expansion, with significant runway ahead

• Developing a personalized customer contact strategy based upon three areas of focus: 1) customer insights, 2) customer strategy and 3) digital delivery, consisting of omni channel initiatives and digital architecture upgrades

• Re-launched an enhanced loyalty program and introduced a new private label credit card program, increasing customer engagement, revenue and profitability

• Growing alternate channels of distribution with significant international and wholesale opportunities

• Closed 156 stores since 2013 as part of ongoing store fleet optimization initiative

4

INVESTMENT HIGHLIGHTS (CONTINUED) #1 pure play children’s specialty apparel retailer in North America, realizing the benefits of a multi-year business transformation strategy

5

STRONG FINANCIAL PERFORMANCE YTD Q2 FY17 YTD Q2 FY16 FY16 FY15 FY14

Comp Sales +4.7% +3.8% +4.9% +0.4% +0.4%

Gross Margin GAAP 36.9%

30 bps leverage 36.6% 37.6%

140 bps leverage 36.2%

90 bps leverage 35.3%

Adjusted* 37.0% 40 bps leverage

36.6% 37.6% 140 bps leverage

36.2% 90 bps leverage

35.3%

SG&A GAAP 27.2%

30 bps leverage 27.5% 25.4%

180 bps leverage 27.2%

50 bps deleverage 26.7%

Adjusted* 26.5% 100 bps leverage

27.5% 25.4% 80 bps leverage

26.2% 10 bps leverage

26.3%

Operating Margin

GAAP $45.5 or 5.6% 100 bps leverage

$36.7 or 4.6% $147.4 or 8.3% 310 bps leverage

$90.1 or 5.2% 70 bps leverage

$80.0 or 4.5%

Adjusted* $53.5 or 6.6% 160 bps leverage

$39.3 or 5.0% $151.7 or 8.5% 210 bps leverage

$110.8 or 6.4% 80 bps leverage

$99.1 or 5.6%

EPS GAAP $2.76

Up 123% $1.24 $5.40

Up 93% $2.80 Up 8%

$2.59

Adjusted* $2.82 Up 114%

$1.32 $5.43 Up 51%

$3.60 Up 18%

$3.05

*YTD Q2 FY17 EPS increase includes $0.87 benefit resulting from the new accounting rules for the income tax impact on share-based compensation *Adjusted measures are non-GAAP and exclude transactions that are not indicative of the performance of the core business. A reconciliation of GAAP and non-GAAP measures is provided in the Company’s earnings releases which are available at http://investor.childrensplace.com

6

CONTINUED STRONG FINANCIAL METRICS Q2 FY17 Results vs Prior Year Drivers

Comp Sales +3.1%

• Superior product offering • Increased AUR & ADS • Enhanced inventory management capabilities • Fleet optimization

Gross Margin GAAP 100 bps leverage

• Ten consecutive quarters of merchandise margin leverage • Leverage due to increases in AUR and merchandise margin

from strong product acceptance and inventory management inclusive of impact of higher penetration of ecommerce business which runs at lower gross margin

Adjusted* 100 bps leverage

SG&A GAAP 10 bps leverage

• Disciplined cost control • Decreased store expenses including lower store

compensation expenses and credit card fees • Leverage due to strong comparable sales • Continued investment in growth drivers

Adjusted* 30 bps leverage

Operating Margin GAAP $3.2 million or 0.9%

vs. ($2.9) million LY • Operating margin expansion for ten consecutive quarters

• Adjusted operating income increase of $5.0 million vs. LY Adjusted* $5.1 million or 1.4% vs. $0.1 million LY

EPS GAAP $0.79 vs. ($0.11) LY

Adjusted* $0.86 vs. ($0.01) LY

*Q2 FY17 EPS includes $0.68 benefit resulting from the new accounting rules for the income tax impact on share-based compensation *Adjusted measures are non-GAAP and exclude transactions that are not indicative of the performance of the core business. A reconciliation of GAAP and non-GAAP measures is provided in the Company’s earnings releases which are available at http://investor.childrensplace.com

7

STRATEGIC INITIATIVES Realizing the benefits of a company-wide, multi-year business transformation focused on a four pillar strategy

Built upon a strong foundation of operational excellence driven by an experienced and talented management team

SUPERIOR PRODUCT

BUSINESS TRANSFORMATION THROUGH TECHNOLOGY

GLOBAL GROWTH THROUGH ALTERNATE CHANNELS OF DISTRIBUTION

STORE FLEET OPTIMIZATION

»

• Consistently strong customer response to product offering

• Continue to significantly differentiate and upgrade the look of our merchandise

• Trend-right and age-appropriate assortments, increasing reach with extended sizes

• Strive to have the right product, in the right channels of distribution, at the right time

• Balancing fashion and fashion basics with more frequent, wear now deliveries

• We also offer a full line of accessories and footwear so busy moms can quickly and easily put together head-to-toe outfits

8

SUPERIOR PRODUCT Highly talented design, merchandising and sourcing teams are core strengths, delivering a superior product offering

9

BUSINESS TRANSFORMATION THROUGH TECHNOLOGY Technology enhancements with focused execution in the areas of Digital, Customer Engagement, Inventory Management, and Alternate Channels of Distribution are driving significant improvement in operating performance, with significant runway still ahead.

9

2014 2015 2016 2017

Foundational • SAP ERP Deployed • Global Supplier Portal

Digital

• Ecommerce Re-Platform

• Mobile Launch

• Digital Order Management

• Organic Search Enhancements

• E-Receipt Launch

• Re-launched Loyalty Program

• Launched New Private Label Credit Card

• Personalized Customer Contact Strategy: • Customer Insights • Customer Strategy • Digital Delivery –Digital Architecture

Upgrades • Rollout Buy Online Pickup in Store Omni-

Channel Initiative to All Stores

Inventory Management

• Assortment Planning • Allocation & Replenishment

• Order Planning & Forecasting • Size & Pack Optimization

• Store Tiering

Channel Expansion

• EDI for Wholesale • Product Development

Enhancements

• Launched Amazon Replenishment

• Entered China via Tmall • Developed Global UPC

10

GROWTH THROUGH ALTERNATE CHANNELS OF DISTRIBUTION

• Nearly 20% of total sales in fiscal 2016, an increase of approximately 200 basis points compared to 2015

• Enhancing end-to-end user experience

• Mobile application enhancements

• Investing in digital architecture and capabilities

North American E-Commerce

• Operating in 19 countries through 7 franchise partners and Tmall in China

• Stores, shop in shops and e-commerce launched in key markets

• Focused on large markets with favorable demographics (India, China and Mexico)

• Currently online in India and China

• Added 6 points of distribution in Q2 2017, resulting in 161 points of distribution (including Tmall) at the end of Q2 2017

International

• Continued growth in replenishment program with Amazon in addition to existing wholesale business

• Focus on the growing off-price and club channels

Wholesale

Canada

USA

Mexico

Costa Rica

Panama

Venezuela

Curacao

Puerto Rico Dom. Republic Egypt

Israel

Saudi Arabia Oman

UAE India

Indonesia

China

Kazakhstan

Georgia

Guatemala

Kuwait Bahrain

Qatar

2017

11

GLOBAL OMNI-CHANNEL RETAILER Have 161 international points of distribution (including Tmall) in 19 countries at the end of Q2 2017 outside U.S./Canada, consisting of brick and mortar stores, shop-in-shops and e-commerce. Announced new franchise agreement with Gill Capital in the 2nd Quarter; Gill Capital plans to open 25 stores in Indonesia, followed by openings in Singapore, Thailand and the Philippines.

2012 2013 2014 2015 2016

Oman Saudi Arabia

UAE

Bahrain Qatar

Egypt Israel

Kuwait Panama

Dominican Republic Georgia

Guatemala India

Kazakhstan Mexico

Venezuela

China Costa Rica Curaçao

Indonesia

• 156 stores closed in the period 2013 through Q2 2017, with a target of a minimum of 300 closures by 2020

• Realization of more than 20 percent sales transfer rate to nearby stores and e-commerce business in the first 12 months after closure

• Average of 300 lease renewals annually over the next 4 years

• Average lease term of less than 3 years and reduced occupancy cost on renewals

12

STORE FLEET OPTIMIZATION Targeting 200 basis points of operating margin accretion from 2013 through 2020 from this initiative

Fleet Facts

Malls 57%

Non-Mall 43%

1,026 Stores in North America

United States 88%

Canada 12%

13

STRONG BALANCE SHEET AND CASH FLOW

$183

$199

$75 $71

$141

$164

$59

$48

$10

$30

$50

$70

$90

$110

$130

$150

$170

$190

$210

2015 2016 YTD Q2 2016 YTD Q2 2017

Operating Cash ($mm)

Free Cash Flow ($mm)

Generating increased operating and free cash flow

• Operating cash increased 9% in 2016 vs 2015

• Free cash flow increased 16% in 2016 vs 2015

• At the end of Q2 2017: – $258 million in cash and short-term

investments, compared to $246 million at the end of Q2 2016.

– $55 million drawn on $250 million ABL credit facility, maturity date of September 2020

14

DRIVING INCREASED CAPITAL RETURN Consistent track record of returning capital to shareholders

• Returned over $829 million to shareholders through share repurchases and dividends since 2009

• $306 million remaining on existing share

repurchase programs as of end of Q2 2017 • Increased dividend by over 200% since

inception in 2014

Cumulative Capital Returned to Shareholders ($mm)

2009 2010 2011 2012 2013 2014 2015 2016 2017 Q2

27.6 26.1 24.5 23.1 22.0 20.8 19.4 17.7 17.7

Shares Outstanding (mm)

Cumulative Dividends Cumulative Share Repurchase

$12 $24 $38 $52 $68 $159

$250 $339 $405

$481 $600

$752 $777

2009 2010 2011 2012 2013 2014 2015 2016 2017Q2

15

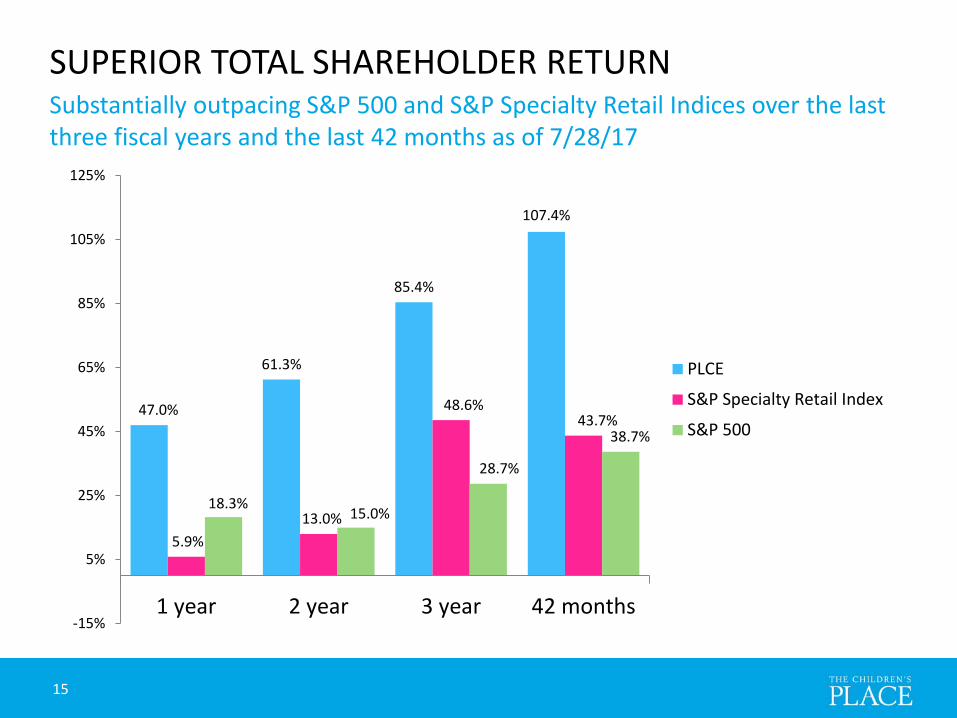

SUPERIOR TOTAL SHAREHOLDER RETURN Substantially outpacing S&P 500 and S&P Specialty Retail Indices over the last three fiscal years and the last 42 months as of 7/28/17

47.0%

61.3%

85.4%

107.4%

5.9% 13.0%

48.6% 43.7%

18.3% 15.0%

28.7%

38.7%

-15%

5%

25%

45%

65%

85%

105%

125%

1 year 2 year 3 year 42 months

PLCE

S&P Specialty Retail Index

S&P 500

![Q2 Result Presentation [Company Update]](https://img.dokumen.tips/doc/110x75/577ca7871a28abea748c70f6/q2-result-presentation-company-update.jpg)

![Earnings Presentation - Q2 FY16 [Company Update]](https://img.dokumen.tips/doc/110x75/577ca7491a28abea748c5346/earnings-presentation-q2-fy16-company-update.jpg)