Embed Size (px)

Citation preview

PRIVATE HEALTH INSURANCE OMBUDSMAN

STATE OF THE HEALTH FUNDS REPORT

PRIVATE HEALTH INSURANCE OMBUDSMAN

STATE OF THE HEALTH FUNDS REPORT

Relating to the financial year 2016ndash17Report required by 20D (c) of the Commonwealth Ombudsman Act 1976

This work is copyright Apart from any use permitted under the Copyright Act 1968 no part may be reproduced without written permission

Requests concerning reproduction and rights should be addressed to the Commonwealth Ombudsman copy Commonwealth of Australia 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 3

FOREWORDI am pleased to present the 13th annual State of the Health Funds Report relating to the financial year 2016ndash17 The Commonwealth Ombudsman Act 1976 (Cth) requires that the Private Health Insurance Ombudsman (PHIO) publish the report after the end of each financial year to provide comparative information

on the performance and service delivery of all health funds1 during that financial year

The information in the report supplements information available on PHIOrsquos consumer website privatehealthgovau The consumer website provides a range of information to assist consumers to understand private health insurance and to select or update their private health insurance policies The information on the consumer website together with the State of the Health Funds Report itself makes it easier for consumers to choose health insurance policies that better meet their individual needs

1 For the purposes of this report Australian registered private health insurers are referred to as lsquohealth fundsrsquo

The purpose of this report is to provide consumers with additional information to assist them to make decisions about private health insurance For existing policyholders the report details information that allows them to compare the performance of their fund with all other health funds For those considering taking out private health insurance for the first time the report provides an indication of the services available from each fund and a comparison of some service and performance indicators at the fund level

The range of issues and performance information contained in the report has been chosen after taking into account the availability of reliable data and whether the information is reasonably comparable across funds The information included in the report is based on data collected by the Australian Prudential Regulation Authority (APRA) as part of its role in undertaking statistical reporting and monitoring of the financial management of health funds I would like to thank APRA for their assistance and advice in relation to the report

Mr Michael Manthorpe PSM Commonwealth Ombudsman March 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 4

CONTENTS

Foreword 3

Using this report to compare funds 6

About the data used in this report 8

Key consumer issues 9

Health fund listing and contact details 14

Service performance 16

Hospital 20

Medical gap schemes 22

General treatment (extras) 25

Finances and costs 29

Health fund operations by state or territory 32

About the Private Health Insurance Ombudsman 41

Your health insurance checklist 42

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 5

List of Figures

Figure 1 Total complaints and enquiries by year 9

Figure 2 privatehealthgovau visitors per year 10

Figure 3 Information complaints 11

List of Tables

Table 1 Health funds listing and contact details 14

Table 2A Membership retention and complaints

(greater than 05 per cent market share) 18

Table 2B Smaller funds (less than 05 per cent national market share) 19

Table 3 Hospital 21

Table 4A Medical services with no gap 23

Table 4B Medical services with no gap or where known gap payment made 24

Table 5A General treatment (extras) 26

Table 5B General treatment (extras) Average amount of

costs covered by service 27

Table 6 Finances and costs 31

Table 7A New South Wales 33

Table 7B Victoria 34

Table 7C Queensland 35

Table 7D South Australia 36

Table 7E Western Australia 37

Table 7F Tasmania 38

Table 7G Australian Capital Territory 39

Table 7H Northern Territory 40

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 6

USING THIS REPORT TO COMPARE FUNDS

Disclaimer

bull Nothing contained in this report should be taken as a recommendation by the Private Health Insurance Ombudsman in favour of any particular health fund or health insurance policy

bull No single indicator should be used as an indicator of overall fund performance In most cases a seemingly poor performance on one indicator will be offset by a good performance on other factors

bull The information used in this report in order to compare health funds is based on data collected for regulatory purposes This information is the most appropriate independent and reliable data available

bull This report is intended to help you decide which health funds to consider though it wonrsquot necessarily indicate which of the fundrsquos policies to purchase Virtually all funds offer more expensive policies that can be expected to provide better than average benefits as well as cheaper policies that provide less

The State of the Health Funds Report

The State of the Health Funds Report (SOHFR) compares how health funds perform across the following criteria

bull service performance

bull hospital benefits

bull medical gap schemes

bull general treatment (extras) benefits

bull financial management

bull health fund operations

You can use the information contained in this report to identify possible funds to join or to assess your existing fundrsquos performance if yoursquore reviewing your current needs

You can use the range of indicators included in this report as a menu to choose the factors of most importance to youmdashnot all factors will be of equal importance to every individual or family

For instance if you prefer to do business with a health fund in person then you should consider the availability of retail offices to be an important consideration However if you prefer to do as much of your business as possible online the range of services available through the fundsrsquo websites will be more important than the branches

More information about particular indicators is provided in the explanations preceding each of the tables in this report

If yoursquore considering taking out private health insurance for the first time we suggest you use the report to identify a number of fundsmdashpreferably at least threemdashfor further investigation

Where to find more information about selecting a policy

The PHIO brochure lsquoHealth Insurance Choice Selecting a Health Insurance Policyrsquo includes important advice on what to consider and what questions to ask when selecting a hospital cover policy It also includes information on government incentives relating to hospital cover such as the lsquoMedicare Levy Surcharge Exemptionrsquo and lsquoLifetime Health Coverrsquo

These brochures as well as other publications can be found at ombudsmangovau Some brochures can be obtained in hard copy on request from the Ombudsmanrsquos Office

This report does not include detailed information on price and benefits for particular health insurance policies Information on specific policies is available from the Ombudsmanrsquos consumer website privatehealthgovau where you can search for and compare information about every health fund and policy in Australia

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 7

Fund names

Throughout this report health funds are referred to by an abbreviation of their registered name rather than any brand name that they might use This abbreviated name appears on the left side of the heading for each fund in the Health Fund Listing section Some funds use several different brand names

Current and recent brand names

Brand name Fund AAMI NIB

APIA NIB

Australian Country Health Medibank

Australian Health Management Medibank

Country Health Medibank

CY Health HBF

Druids GMHBA

Federation Health Latrobe

FIT GMHBA

Frank GMHBA

GMF Health HBF

Goldfields HBF

Government Employees Medibank

Grand United Australian Unity

HBA BUPA

Healthguard HBF

Illawarra Health Fund Medibank

IOOF NIB

IOR HCF

Manchester Unity HCF

MBF BUPA

Mutual Community BUPA

Mutual Health Medibank

NRMA Health BUPA

Qantas Assure NIB

RACT GMHBA

Suncorp NIB

SGIC (SA) BUPA

SGIO (WA) BUPA

Unihealth Teachers Health

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 8

ABOUT THE DATA USED IN THIS REPORT

Open and restricted membership health funds

Membership of lsquoopenrsquo health funds is available to everyone

lsquoRestricted membershiprsquo health funds have certain membership criteria which mean they arenrsquot available to all consumers For example membership may be restricted to employees of certain companies or occupations or members of particular organisations

Where applicable open and restricted membership funds are listed separately in each of the tables in this report

Information about policies

The information included in the report on fund contributions and benefits indicates the average outcomes across all of a fundrsquos policies and so canrsquot be taken as an indicator of the price or benefit levels that can be expected for any particular policy

Virtually all funds offer more expensive policies that can be expected to provide better than average benefits and most also offer cheaper policies that provide less

This report can help you to decide which health funds to consider but wonrsquot necessarily help you to decide which of the fundsrsquo policies to purchase

For information about specific policies the website privatehealthgovau enables you to view standard information outlining the main features of any health insurance policy You can compare Standard Information Statements for any policy available for purchase from any fund including the level of cover excess and price The website is also a good resource of independent and reliable information about private health insurance

Data collection

The need to obtain independent reliable data has been a key consideration in putting together the report The data selected by the Ombudsman as the most appropriate available is collected by the industry regulator the Australian Prudential Regulation Authority (APRA) APRA has supplied most of the data published in this report

Funds report to APRA for regulatory purposes and not all of the data is publicly available Some of this information is useful to consumers and is therefore reproduced in this report You should note that the data is collected primarily for regulatory purposes and not for the purposes of the State of the Health Funds Report Accordingly it is important to read the accompanying text explaining the data in conjunction with the tables

As funds differ in size most of the statistical information is presented as percentages or dollar amounts per membership for easier comparison No attempt has been made to weight the importance of various indicators as these are subjective judgements very much dependent on your particular circumstances preferences and priorities For this reason it would not be valid to average all the scores indicated to obtain some form of consolidated performance or service delivery score

The report provides you with additional information about the benefits that were paid by each fund over the last year The report also provides information about the extent of cover provided for hospital medical and general treatment and any state-based differences in coverage The selection of indicators used in this report is not intended to represent the full range of factors that should be considered when comparing the performance of health funds The range of indicators has been limited to those for which there is reliable comparative information available

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 9

KEY CONSUMER ISSUES

High levels of private health insurance complaints in 2016ndash17

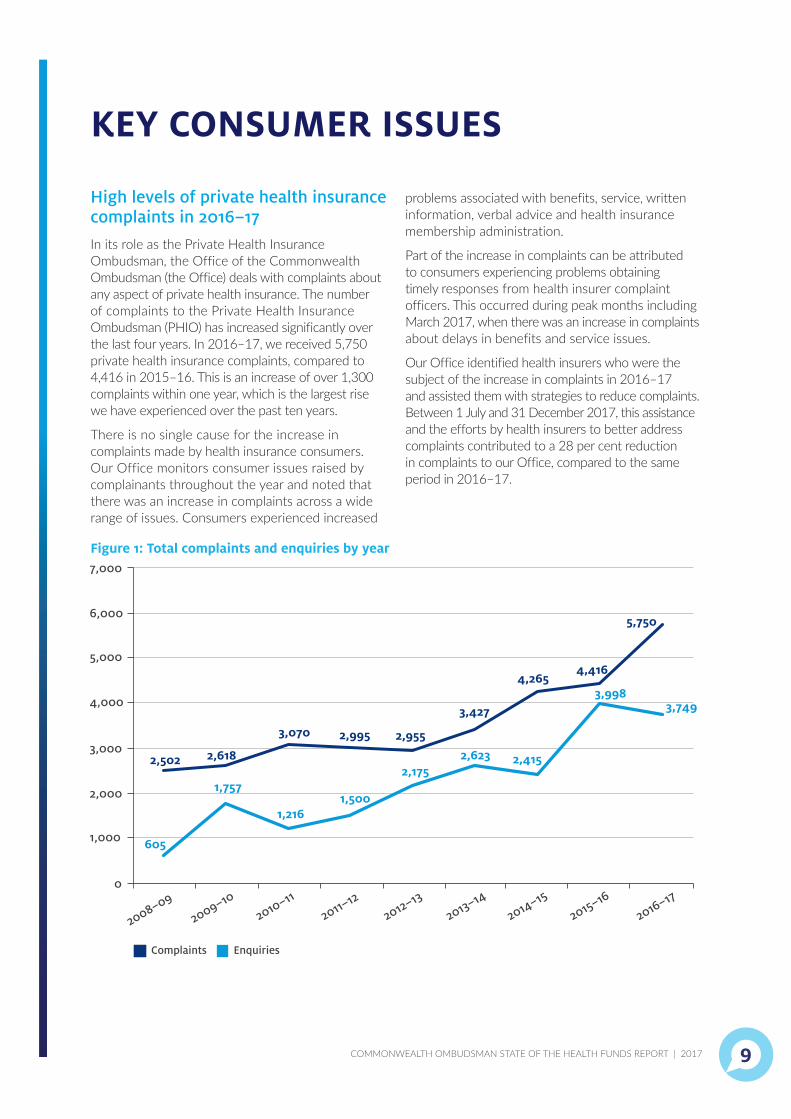

In its role as the Private Health Insurance Ombudsman the Office of the Commonwealth Ombudsman (the Office) deals with complaints about any aspect of private health insurance The number of complaints to the Private Health Insurance Ombudsman (PHIO) has increased significantly over the last four years In 2016ndash17 we received 5750 private health insurance complaints compared to 4416 in 2015ndash16 This is an increase of over 1300 complaints within one year which is the largest rise we have experienced over the past ten years

There is no single cause for the increase in complaints made by health insurance consumers Our Office monitors consumer issues raised by complainants throughout the year and noted that there was an increase in complaints across a wide range of issues Consumers experienced increased

problems associated with benefits service written information verbal advice and health insurance membership administration

Part of the increase in complaints can be attributed to consumers experiencing problems obtaining timely responses from health insurer complaint officers This occurred during peak months including March 2017 when there was an increase in complaints about delays in benefits and service issues

Our Office identified health insurers who were the subject of the increase in complaints in 2016ndash17 and assisted them with strategies to reduce complaints Between 1 July and 31 December 2017 this assistance and the efforts by health insurers to better address complaints contributed to a 28 per cent reduction in complaints to our Office compared to the same period in 2016ndash17

Figure 1 Total complaints and enquiries by year

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 10

Private health insurance reforms and the future of privatehealthgovau

In 2017 the Government announced significant reforms to health insurance and implementation of these reforms will commence in 2018 A key aim of the reforms is to make health insurance simpler for consumers to understand by introducing common health insurance terms and classifying policies into simpler categories The consumer website privatehealthgovau will be updated and improved as part of these reforms

Privatehealthgovau was launched on 1 April 2007 and since then the website has been regularly updated to improve the search features and respond to changes in health insurance Usage of the website by consumers has increased annually with 1297851 unique visitors in 2016ndash17 as shown in the figure below

The available data suggests that general growth in the sitersquos usage is due to the site becoming better known via recommendations and search results our Officersquos own initiatives to promote the website to consumers and regular reminders of the sitersquos existence in annual mailings of Standard Information Statements and Lifetime Health Cover letters

Our Office has a consumer information and advice role which included responding to 3749 individual enquiries last year Over two-thirds of our enquiries are received via the website

The website is the only independent source of health insurance information in Australia which includes all health insurers and insurance policies available A consumer can search and compare policies based on levels of benefits included and excluded services and premiums An important principle of the website comparison feature is that it does not favour any particular type of policy The website comparison feature is based on the individual being able to choose what is appropriate for their circumstances

Due to the large number of policies available for purchase website users are often presented with a large number of choices This indicates that private health insurance in Australia is competitive and there are a large number of choices for consumers but it also makes the task of sorting through policies more complex

We have commenced the project to upgrade the consumer website to reflect the announced reforms This is expected to be available from April 2019

Figure 2 privatehealthgovau visitors per year

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 11

Providing high quality information to consumers

The reforms aim to reduce health insurance complaints in the future by simplifying health insurance and providing better information to consumers In the meantime our Office considers that the complaints about health insurance information particularly verbal advice could be reduced if health insurers focused on improving their own practices within their organisations

In 2016ndash17 we received 599 complaints about health insurance information and of those 408 related to verbal advice In a typical case there will be an allegation of incorrect or unhelpful advice being provided during a customer service phone call which has resulted in an insured person

incurring an unexpected cost Investigating a complaint involves checking what records can be provided about the phone call and forming a view as to whether the advice was reasonable or not

Our Office works with health insurers to better understand the causes of complaints about verbal advice and we focus attention on those insurers that experience higher numbers of complaints What seems evident is that the quality of training and accuracy of verbal advice provided by health insurer customer service staff varies between insurers For those insurers that have a higher incidence of complaints about verbal advice it seems reasonable to question whether the training of staff provision of resources such as internal guidelines and levels of quality monitoring are sufficient

Figure 3 Information complaints

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 12

The performance of private health insurers

During 2016ndash17 the health insurance industry returned 86 per cent of contributions to policy holders through paying benefits towards hospital and general treatment costs This result is marginally lower than the previous year where 861 per cent of contributions were returned2

Some insurers performed better than the average of 86 per cent by returning well over 90 per cent of contributions to policyholders as benefits

The percentage of overall benefits returned to policyholders is an easy to understand method of comparing different health insurers and how they have performed in meeting the needs of their consumers Although some of the variance in results can be attributed to an insurerrsquos geographic location and customer profile this is perhaps the best measurement available to compare one insurerrsquos performance against another or against the industry See Table 6 on page 31 for the benefits as a percentage of contributions for each insurer

Our Office also tracks and compares the performance of health insurers using complaint data collected through the investigation of consumer complaints We compare an insurerrsquos share of total complaints against their market share to see if they have an average share of complaints

An incident of complaint which is higher than an insurerrsquos market share indicates that consumers are experiencing a higher level of problems with the service benefits and administration of the insurer See Table 2 on page 18 for the complaint performance results for each insurer

Our Office also produces quarterly updates on the complaint performance of each insurer3 Regular complaint reporting helps identify any problems within individual health insurers and any potential systemic problems early If a health insurerrsquos complaint share is reported as higher than average in a quarter there is a solid incentive for the organisation to take action to address complaints and change practices to reduce the causes of complaints The insurer can then track the success of their action to address consumer problems by seeing whether the insurerrsquos complaint performance improves in subsequent reports

2 Australian Prudential Regulation Authority Operations of the Private Health Insurers Report 2015ndash16 and 2016ndash17 apragovauPHIPublicationsPagesOperations-of-Private-Health-Insurers-Annual-Reportaspx

3 Private Health Insurance Ombudsman Quarterly Bulletins available at ombudsmangovauaboutprivate-health-insuranceprivate-health-insurance-publicationsprivate-health-insurance-quarterly-bulletin

Helping consumers understand private health insurance

In addition to the resources available on privatehealthgovau our Office provides a number of resources that enable consumers to better understand their health insurance and assist them in making informed choices about their health care These consumer information services help address the key causes of complaints as expressed by complainants to our Office

Our Office helps consumers understand their benefit entitlements so they are more knowledgeable about their cover and can make more informed choices about their health insurance and medical treatment Our Officersquos factsheets and brochures aim to address common causes of complaints by providing advice to consumers based on our complaint-handling experience These are available at ombudsmangovau4

Our Office has developed a number of brochures including

bull The Right to Change a consumer guide to transferring from one health insurance product to another

bull Health Insurance Choice choosing a Health Insurance Policy

bull Privatehealthgovau Australiarsquos leading independent source of information about private health insurance

bull Doctors Bill managing doctorrsquos bills and potential out-of-pocket costs

bull Waiting Periods for Health Insurance how and why waiting periods work including pre-existing conditions

4 See Private Health Insurance Publications available at ombudsmangovauaboutprivate-health-insuranceprivate-health-insurance-publications

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 13

Our Office has also developed a number of fact sheets including

bull Obstetrics and Pregnancy questions to ask your fund if yoursquore planning to start a family

bull Premium Increases the reasons and processes behind premium increases

bull Informed Financial Consent your right to ask about fees when going to hospital

bull Membership Arrears keeping your policy payments up to date

bull Policy Exclusions and Restrictions what isnrsquot covered on your policy

bull Mental Health Treatment and Health Insurance cover for psychiatric services rehabilitation and psychology

bull Plastic and Reconstructive Surgery items your policy may not cover

bull Clearance Certificates what to do if transferring between funds

bull Assisted Reproductive Services what can be covered for IVF GIFT and related services

bull Podiatric Surgery cover for surgical treatment from podiatric surgeons

bull The Pre-Existing Conditions Rule how it applies and the Officersquos role in complaints

bull Dental and Oral Surgery how private health insurance covers dental surgery

bull Orthodontic Treatment what it involves and how itrsquos covered by private health insurance

bull Insulin Pumps how private health insurance covers insulin pumps

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 14

HEALTH FUND LISTING AND CONTACT DETAILS

The following tables list all Australian registered health funds The lsquoopenrsquo membership funds provide policies to the general public The lsquorestrictedrsquo funds provide policies only through specific employment groups professional associations or unions

Table 1 Health funds listing and contact details

Open membership health funds Abbreviation Full name or other names Phone number Website

Australian Unity Australian Unity Health Ltd 132 939 australianunitycomau

BUPA Bupa HI Pty Ltd 134 135 bupacomau

CBHS Corporate

CBHS Corporate Health Pty Ltd 1300 586 462 cbhscorporatehealthcomau

CDH CDH Benefits Fund 02 4990 1385 cdhbfcomau

CUA Health CUA Health Ltd 1300 499 260 cuacomauhealth

GMHBA GMHBA Ltd Frank 1300 446 422 gmhbacomau

GU Corporate Grand United Corporate Health 1800 249 966 guhealthcomau

HBF HBF Health Ltd 133 423 hbfcomau

HCF Hospitals Contribution Fund of Australia

131 334 hcfcomau

HCI Health Care Insurance Ltd 1800 804 950 hciltdcomau

Healthcomau Healthcomau 1300 199 802 healthcomau

Health Partners Health Partners Ltd 1300 113 113 healthpartnerscomau

HIF Health Insurance Fund of Australia Ltd

1300 134 060 hifcomau

Latrobe Latrobe Health Services 1300 362 144 latrobehealthcomau

MDHF Mildura Health Fund Ltd 03 5023 0269 mildurahealthfundcomau

Medibank Medibank Private Ltd Australian Health Management

132 331 134 246

medibankcomau ahmcomau

MO Health [1] MyOwn Health Insurance 1300 300 338 myowncomau

NIB NIB Health Funds Ltd Qantas Assure APIA

131 463 nibcomau

Onemedifund National Health Benefits Australia Pty Ltd

1800 148 626 onemedifundcomau

Peoplecare Peoplecare Health Insurance Limited

1800 808 690 peoplecarecomau

Phoenix Phoenix Health Fund Ltd 1800 028 817 phoenixhealthfundcomau

QCH Queensland Country Health Fund Ltd

1800 813 415 qldcountryhealthcomau

St Lukes St Lukes Health 1300 651 988 stlukescomau

Transport Health Transport Health Pty Ltd 1300 806 808 transporthealthcomau

Westfund Westfund Limited 1300 937 838 westfundcomau

[1] MO Health commenced operations after the end of the reporting period (1 July 2016 to 30 June 2017) and for this reason does not appear elsewhere in the report

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 15

Table 1 Health funds listing and contact details

Restricted membership health funds Abbreviation Full name or other names Phone number Website

ACA ACA Health Benefits Fund 1300 368 390 acahealthcomau

CBHS CBHS Health Fund Ltd 1300 654 123 cbhscomau

Defence Health Defence Health Ltd 1800 335 425 defencehealthcomau

Doctorsrsquo Health The Doctorsrsquo Health Fund 1800 226 126 doctorshealthfundcomau

Emergency Services

Emergency Services Health Pty Ltd

1300 703 703 eshealthcomau

Navy Navy Health Ltd 1300 306 289 navyhealthcomau

Nurses and Midwives

Nurses and Midwives Health Pty Ltd

1300 344 000 nmhealthcomau

Police Health Police Health 1800 603 603 policehealthcomau

Reserve Bank Reserve Bank Health Society Ltd 1800 027 299 myrbhscomau

RT Health Fund Railway and Transport Health Fund Ltd

1300 886 123 rthealthfundcomau

Teachers Health Teachers Health Fund 1300 728 188 teachershealthcomau

TUH Teachersrsquo Union Health Fund 1300 360 701 tuhcomau

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 16

SERVICE PERFORMANCEThe level of complaints that the PHIO receives about a fund relative to its market share is a reasonable indicator of the service performance of most funds

Whether a fund can attract new members and more importantly retain members is also an indicator of member satisfaction

Member retention

The member retention indicator is used as one measure of the comparative effectiveness of health funds and their level of member satisfaction This indicator measures what percentage of fund members (hospital memberships only) have remained with the fund for two years or more Figures are not adjusted for policies that lapse when a member dies as these are not reported to APRA

Most restricted membership funds rate well on this measure compared to open membership funds This may be due to the particular features of restricted membership funds especially their links with employment

Membership change

The membership change indicator shows the change in the number of policy holders over the year from 30 June 2016 to 30 June 2017 Both the percentage change and number are included Negative figures indicate that the fund has experienced a net reduction in membership over the period As indicated above member deaths would contribute to this figure

PHIO complaints in context

The number of complaints received by the PHIO is very small compared to fund membership

There are a number of factors (other than service performance) that can influence the level of complaints the PHIO receives about a fund These include the information provided to fund members about the PHIO through general publicity or by the fund and the effectiveness of the fundrsquos own complaint-handling process

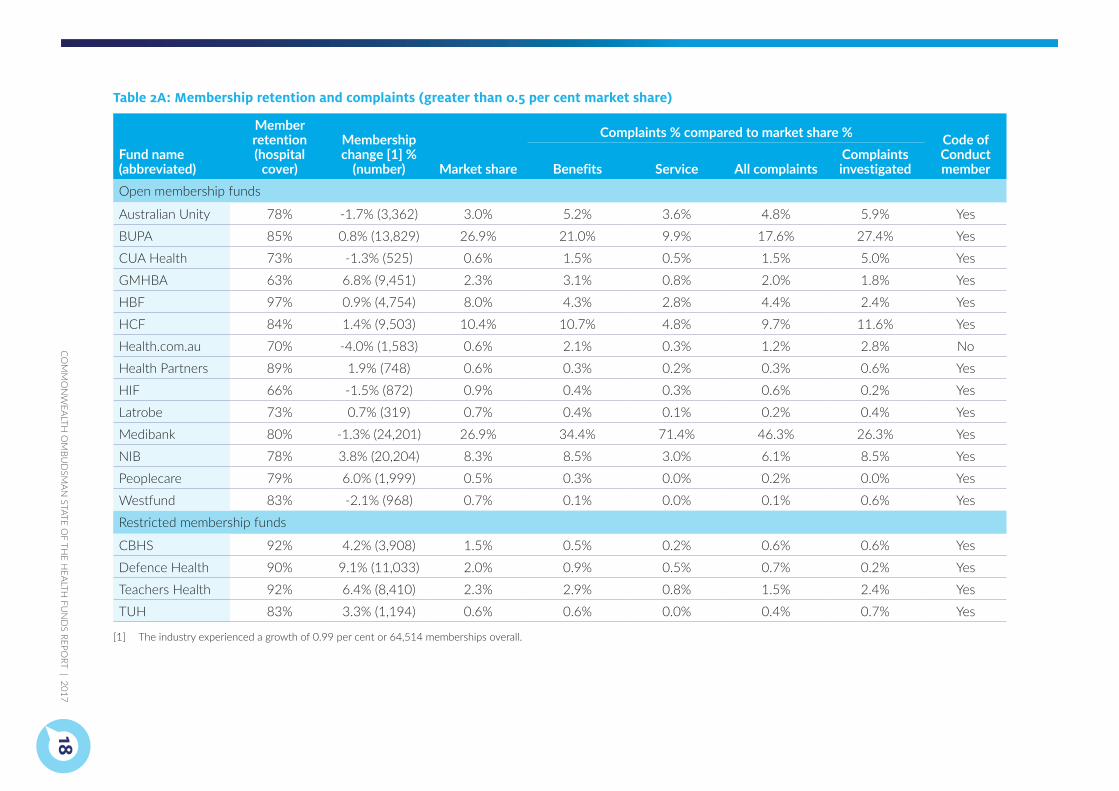

Complaints percentage compared to market share percentage

The first table (2A) includes all funds with a national market share of 05 per cent or more

In that table each fundrsquos market share (as at 30 June 2017) is shown in the market share column Subsequent columns show the percentage of PHIO complaints in various categories received about each fund These percentages should be compared with the market share percentage If a fund has a higher complaints percentage than its market share it indicates that members of that fund are more likely to complain than the average of all fund members

The table also indicates what percentage of Benefit and Service complaints are received about each fund

Benefit complaints include problems of non-payment delayed payment the level of benefit paid or the gap paid by the member

Service complaints are about the general quality of service provided by fund staff the quality of customer service advice and premium payment problems

All complaints takes account of all complaints received by the PHIO about the fund All complaints includes complaints investigated as well as complaints that were finalised without the need for investigation

Complaints investigated is a measure of how many complaints required a higher level of intervention from the Ombudsman Most complaints to the Ombudsman can be finalised by referring the matter to fund staff to resolve or by the PHIO staff providing information to the complainant Complaints which fund staff have not been able to resolve to a memberrsquos satisfaction are investigated by the Ombudsmanrsquos Officemdashso the rating on complaints investigated is an indicator of the effectiveness of each fundrsquos own internal complaints-handling

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 17

Smaller funds (less than 05 per cent national market share)

For these smaller funds it is not practical to show the percentage of complaints in each of the above categories because of the very small numbers of complaints

This separate table (2B) therefore shows the actual number of all complaints received and the number of complaints investigated as well as whether the number is below the number expected based on the fundrsquos market share

While these funds have a very low national market share many are nevertheless very significant in a particular state or region

Code of Conduct

The self-regulatory code for health funds deals with the quality of advice provided to consumers and sets standards for training of health fund staff and others responsible for advising consumers about private health insurance It also requires funds to have effective complaint-handling procedures Funds that have completed the compliance processes for becoming a signatory to the code are indicated in the table (as at January 2018)

For more information about the Code of Conduct please see privatehealthcareaustraliaorgaucodeofconduct

CO

MM

ON

WEALTH

OM

BUD

SMAN

STATE OF TH

E HEALTH

FUN

DS REPO

RT | 201718

Table 2A Membership retention and complaints (greater than 05 per cent market share)

Fund name (abbreviated)

Member retention (hospital

cover)

Membership change [1]

(number) Market share

Complaints compared to market share Code of Conduct memberBenefits Service All complaints

Complaints investigated

Open membership funds Australian Unity 78 -17 (3362) 30 52 36 48 59 Yes

BUPA 85 08 (13829) 269 210 99 176 274 Yes

CUA Health 73 -13 (525) 06 15 05 15 50 Yes

GMHBA 63 68 (9451) 23 31 08 20 18 Yes

HBF 97 09 (4754) 80 43 28 44 24 Yes

HCF 84 14 (9503) 104 107 48 97 116 Yes

Healthcomau 70 -40 (1583) 06 21 03 12 28 No

Health Partners 89 19 (748) 06 03 02 03 06 Yes

HIF 66 -15 (872) 09 04 03 06 02 Yes

Latrobe 73 07 (319) 07 04 01 02 04 Yes

Medibank 80 -13 (24201) 269 344 714 463 263 Yes

NIB 78 38 (20204) 83 85 30 61 85 Yes

Peoplecare 79 60 (1999) 05 03 00 02 00 Yes

Westfund 83 -21 (968) 07 01 00 01 06 Yes

Restricted membership funds CBHS 92 42 (3908) 15 05 02 06 06 Yes

Defence Health 90 91 (11033) 20 09 05 07 02 Yes

Teachers Health 92 64 (8410) 23 29 08 15 24 Yes

TUH 83 33 (1194) 06 06 00 04 07 Yes

[1] The industry experienced a growth of 099 per cent or 64514 memberships overall

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 19

Table 2B Smaller funds (less than 05 per cent national market share)

Fund name (abbreviated)

Member retention (hospital

cover)

Membership change [1]

(number)

Number complaints

received

Below market share

Number complaints

investigated

Below market share

Code of Conduct member

Open membership funds CBHS Corporate

na na 1 Yes 1 No No

CDH 89 -29 (77) 0 Yes 0 Yes No

GU Corporate 66 05 (154) 23 No 6 No Yes

HCI 89 302 (1437) 1 Yes 0 Yes Yes

MDHF 89 21 (316) 2 Yes 0 Yes No

Onemedifund 90 16 (91) 0 Yes 0 Yes Yes

Phoenix 86 98 (747) 4 Yes 0 Yes Yes

QCH 85 94 (2062) 1 Yes 0 Yes Yes

St Lukes 88 65 (1821) 8 Yes 0 Yes Yes

Transport Health

59 -135 (1277) 9 No 0 Yes Yes

Restricted membership funds ACA 92 09 (44) 1 Yes 0 Yes Yes

Doctorsrsquo Health 88 108 (1613) 10 Yes 3 No Yes

Emergency Services

na na 0 Yes 0 Yes No

Navy Health 88 52 (993) 4 Yes 2 No Yes

Nurses and Midwives

na na 1 Yes 0 Yes No

Police Health 92 36 (744) 3 Yes 1 Yes Yes

Reserve Bank 91 08 (19) 0 Yes 0 Yes Yes

RT Health Fund 89 28 (634) 21 No 2 No Yes

[1] The industry experienced a growth of 099 per cent or 64514 memberships overallNote lsquonarsquo indicates no data as insurer commenced operations during 2016ndash17

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 20

HOSPITALTable 3 provides a general comparison of health insurance for private hospital treatment A higher percentage indicates that on average the fundrsquos members are covered for a higher proportion of hospital charges

Itrsquos important to remember most funds offer a choice of different policiesmdashthe percentages indicated in this table arenrsquot indicative of any single policy but are an average of all policies offered by the fund

Hospital policies

This table provides a general comparison of health insurance for private hospital treatment (hospital policies) provided by each fund

Hospital policies provide benefits towards the following costs if you elect to be a private patient in a private or public hospital

bull hospital fees for accommodation operating theatre charges and other charges raised by the hospital

bull the costs of drugs or prostheses required for hospital treatment and

bull fees charged by doctors (surgeons anaesthetists pathologists etc) for in-hospital treatment

Most funds offer a range of different policies providing hospital cover These policies may differ on the basis of the range of treatments that are covered to what extent those treatments are covered the level of excess or co-payments you may be required to pay if you go to hospital and the price and discounts available to you

Hospital charges covered

This column indicates the proportion of total charges associated with treatment of private patients covered by each fundrsquos benefits This includes charges for hospital accommodation theatre costs prostheses and specialist fees (not including the Medicare benefit) excesses or co-payments and associated benefits

The figures shown are average outcomes across all of each fundrsquos hospital policies Higher cost policies will generally cover a greater proportion of charges than indicated by this average Cheaper policies including those with higher excesses or co-payments may cover less

The use of an average figure applying across all of each fundrsquos policies will mean that funds with a high proportion of their membership in lower costrestricted and excluded benefit policies will have a lower average figure

Information is not provided for some funds in some states where there were insufficient numbers reported to APRAmdashgenerally this occurs in states where the fund does not have a large membership

The information provided in this table presents the position taking account of all of each fundrsquos policies It is not indicative of any individual policy offered by the fund but is an average for the total fund membership

Additional information

The separate Health fund operations by state or territory tables in this report includes information on the number of lsquoagreement hospitalsrsquo under contract to each fund in each state

For additional information on the medical gap benefits provided through hospital policies please refer to the separate Medical gap schemes section

The PHIO brochure lsquoHealth Insurance Choice Selecting a Health Insurance Policyrsquo includes important advice on what to consider and what questions to ask when selecting a hospital cover policy It also includes information on government incentives relating to hospital policies such as the Medicare Levy Surcharge Exemption and Lifetime Health Cover The brochure is available on ombudsmangovau and privatehealthgovau

PHIO consumer website

The privatehealthgovau website provides information about all private health insurance policies available in Australia including benefits prices and agreement hospitals for each health fund

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 21

Table 3 Hospital

Fund name (abbreviated)

hospital related charges covered [1]

ACT NSW VIC QLD SA WA TAS NTOpen membership fundsAustralian Unity 851 874 907 886 921 888 900 836BUPA 829 888 932 910 955 884 936 899CBHS Corporate na 598 1000 1000 na na na naCDH na 957 940 951 852 944 952 naCUA Health 740 888 911 925 904 895 918 935GMHBA 712 811 890 848 870 866 900 806GU Corporate 858 865 904 879 879 879 882 815HBF 838 894 938 916 933 960 951 912HCF 875 931 938 924 953 901 937 888HCI 844 883 942 892 947 957 958 953Healthcomau 775 809 849 845 871 833 872 871Health Partners 820 893 932 932 957 729 959 963HIF 734 882 908 911 922 926 950 936Latrobe 788 883 924 910 910 923 921 930MDHF 847 931 936 932 918 943 899 954Medibank 837 895 928 903 941 905 936 903NIB 760 876 860 845 907 844 903 827Onemedifund 978 930 953 928 968 951 966 naPeoplecare 756 912 928 915 918 932 932 958Phoenix 875 952 954 940 973 956 951 1000QCH 868 930 939 898 943 909 1000 904St Lukes 939 933 935 913 938 915 948 920Transport Health 760 909 949 901 914 951 957 naWestfund 873 938 957 922 973 963 961 916Restricted membership fundsACA 851 937 952 960 939 964 977 naCBHS 837 899 941 931 961 922 964 850Defence Health 854 913 940 926 952 935 949 925Doctorsrsquo Health 898 925 933 934 922 921 890 889Emergency Services na 662 1000 872 841 na na naNavy Health 864 918 930 927 952 933 974 921Nurses and Midwives 602 842 882 865 na na 943 na

Police Health 870 916 935 928 979 932 971 930Reserve Bank 752 924 976 957 993 965 979 naRT Health Fund 880 939 935 937 951 924 937 935Teachers Health 861 914 933 936 950 910 952 888TUH 83 91 93 92 87 92 91 87

[1] Includes charges for hospital accommodation theatre costs prostheses and specialist fees (not including the Medicare benefit) and associated benefits (after any excesses and co-payments are deducted)

Note lsquonarsquo signifies no activity in that state 100 per cent is likely to indicate small numbers (eg only one episode)

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 22

MEDICAL GAP SCHEMESHealth insurer lsquomedical gap schemesrsquo are designed to eliminate or reduce the out-of-pocket costs incurred by a patient for in-hospital medical services If a service is lsquono gaprsquo it means no cost was incurred by the patient as the full cost was covered by Medicare and the health fund A reduced cost is incurred by the patient for what is called a lsquoknown gaprsquo service

If a health fund has a higher percentage of services covered at no gap than other funds it indicates the fund has a more effective gap scheme in that state The figures provided are averagesmdashit is no guarantee that a particular doctor will choose to use the fundrsquos gap scheme

Fund gap schemes and agreements

Doctors are free to decide whether or not to use a particular fundrsquos gap cover arrangements for each individual patient Factors that can affect the acceptance of the scheme by doctors include

bull whether the fund has a substantial share of the health insurance market in a particular state or region

bull the level of fund benefits paid under the gap arrangements (compared with the doctorrsquos desired fee) and

bull the design of the fundrsquos gap cover arrangements including any administrative burden for the doctor

State-based differences

Information is provided on a state basis because the effectiveness of some fundsrsquo gap schemes can differ between states and these differences are not apparent in the national figures

Most differences are due to the level of doctorsrsquo fees which vary significantly between different states and between regional areas and capital cities In some states funds are able to provide more effective coverage of gaps because doctors charge less than the national average In addition where a doctorrsquos fee for an in-hospital service is at or below the Medicare Benefits Schedule fee there will be no gap to the fund member

If a health fundrsquos percentage of services with no gap is higher than that of a fund in another state it does not necessarily mean the fundrsquos scheme is more effective because state-based differences could be the cause

Information is not provided for some funds in some states as the numbers are not reported to APRA for states in which the fund does not have a sufficiently large membership (in which case these figures are included with figures for the state in which a fund has the largest number of members)

Comparing different gap schemes

If a health fund has a higher percentage of services covered at no gap (in the same stateterritory) compared with another fund it is an indicator of a more effective gap scheme in that state Over the whole fund it is more likely that a medical service can be provided at no cost to the consumer but it is no guarantee that a particular doctor will choose to use the fundrsquos gap scheme

Percentage of services with no gapsmdashthe proportion of services for which a gap is not payable by the patient after the impact of fund benefits schemes and agreements

Percentage of services with no gap or where known gap payment mademdashthis table includes both the percentage of no gap services and what is called lsquoknown gaprsquo services Known gap schemes are an arrangement where the fund pays an additional benefit on the understanding that the provider advises the patient of costs upfront

These tables take into account all of the fundrsquos policies The information in the tables is not indicative of any individual policy offered by the fund but is an average for the total fund membership

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 23

Table 4A Medical services with no gap

Fund name (abbreviated)

of services with no gapACT NSW VIC QLD SA WA TAS NT

Open membership fundsAustralian Unity 836 909 927 920 934 887 927 866BUPA 785 842 864 821 854 734 866 802CBHS Corporate na 700 1000 1000 na na na naCDH na 874 na na na na na naCUA Health 862 905 913 934 854 877 928 851GMHBA 583 763 769 819 770 715 749 741GU Corporate 787 878 921 883 923 855 923 936HBF 554 654 661 622 577 878 621 462HCF 809 910 893 920 903 852 908 863HCI 863 888 904 894 904 930 939 970Healthcomau 744 846 874 872 840 842 911 851Health Partners 767 883 915 930 938 852 815 940HIF 746 841 882 890 888 870 927 889Latrobe 508 757 799 814 767 763 680 580MDHF 832 806 818 830 863 723 615 694Medibank 798 884 846 876 903 736 922 816NIB 675 888 882 841 917 747 829 802Onemedifund 876 894 900 912 911 859 942 naPeoplecare 749 924 912 914 899 893 944 827Phoenix 741 922 912 922 943 865 954 1000QCH 316 922 921 918 899 857 927 861St Lukes 773 813 808 803 799 713 918 933Transport Health 593 874 922 893 899 590 991 naWestfund 669 860 846 854 913 862 769 629Restricted membership fundsACA 833 908 936 934 964 910 937 naCBHS 804 887 914 924 908 868 952 827Defence Health 793 892 917 927 907 882 933 885Doctorsrsquo Health 887 921 937 944 928 891 933 761Emergency Services na 600 na 519 1000 na na naNavy Health 787 898 921 913 927 871 926 890Nurses and Midwives 1000 857 761 382 na na 1000 naPolice Health 835 910 887 889 918 843 930 858Reserve Bank 581 899 935 940 961 906 922 naRT Health Fund 815 929 921 933 942 863 933 877Teachers Health 846 902 911 929 911 854 944 915TUH 783 888 920 926 906 895 919 809

Note lsquonarsquo signifies no activity or very low activity in that state 100 per cent is likely to indicate small numbers (eg only one episode)

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 24

Table 4B Medical services with no gap or where known gap payment made

Fund name (abbreviated)

of services with no gap or where known gap payment madeACT NSW VIC QLD SA WA TAS NT

Open membership fundsAustralian Unity 925 960 976 958 981 952 973 897BUPA 854 884 902 851 905 784 900 856CBHS Corporate na 1000 1000 1000 na na na naCDH na 973 na na na na na naCUA Health 939 962 986 978 972 955 989 1000GMHBA 829 908 894 930 928 855 854 920GU Corporate 894 941 978 942 974 935 968 987HBF 921 949 977 955 956 996 892 1006HCF 949 983 994 989 998 970 997 975HCI 954 951 982 950 995 975 992 1000Healthcomau 933 950 971 960 987 944 998 957Health Partners 905 949 979 967 997 970 972 970HIF 917 951 973 960 979 965 987 977Latrobe 991 992 998 996 990 1000 981 1000MDHF 921 977 977 928 972 936 890 958Medibank 929 959 934 934 989 887 981 938NIB 675 888 882 841 917 747 829 802Onemedifund 991 967 973 974 981 967 989 naPeoplecare 923 972 987 970 990 965 992 1000Phoenix 933 979 988 985 992 958 1000 1000QCH 491 972 990 977 977 962 967 962St Lukes 784 862 866 861 894 765 983 967Transport Health 846 975 979 962 1000 965 1070 naWestfund 794 907 979 931 960 949 820 682Restricted membership fundsACA 922 968 989 976 984 980 978 naCBHS 940 959 982 969 988 945 990 957Defence Health 938 964 988 977 996 961 989 965Doctorsrsquo Health 970 983 992 990 998 972 968 985Emergency Services na 600 na 731 1000 na na naNavy Health 935 965 985 973 994 962 988 954Nurses and Midwives 1000 956 1000 529 na na 1000 naPolice Health 974 959 978 966 995 937 981 954Reserve Bank 903 966 988 981 994 973 963 naRT Health Fund 960 978 985 977 989 954 998 988Teachers Health 955 967 985 979 996 950 991 966TUH 880 960 981 975 956 974 975 977

Note lsquonarsquo signifies no activity or very low activity in that state 100 per cent is likely to indicate small numbers (eg only one episode)

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 25

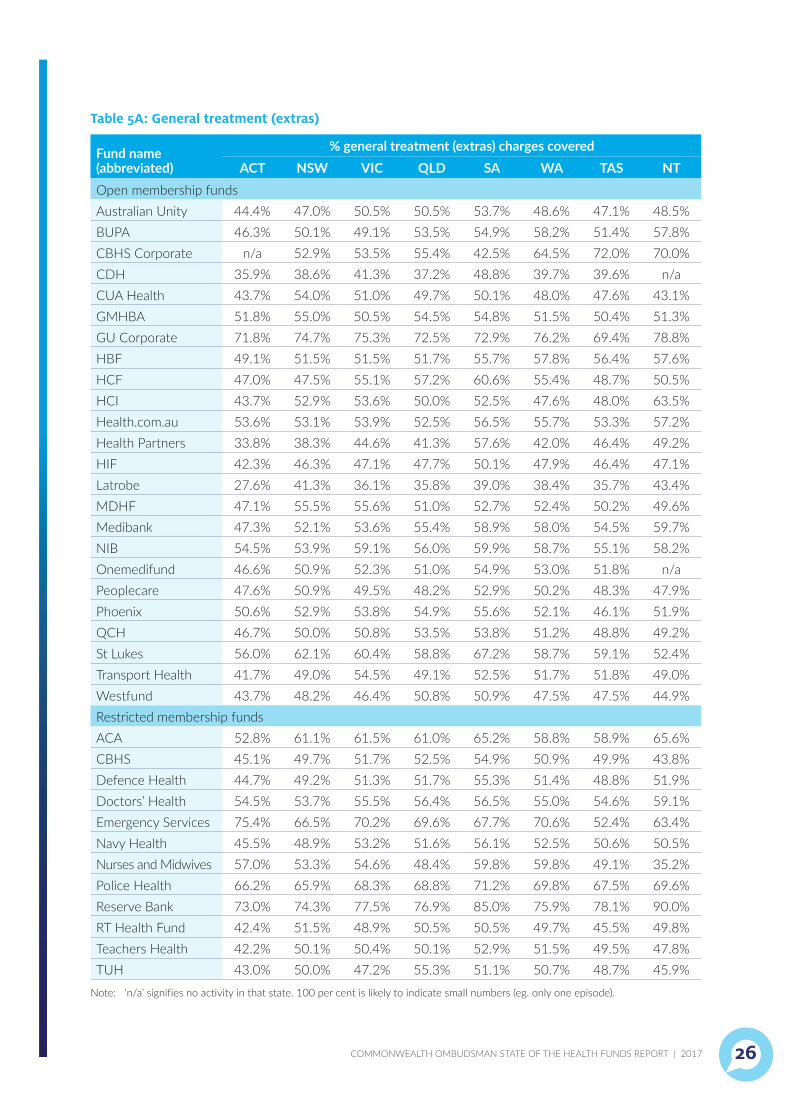

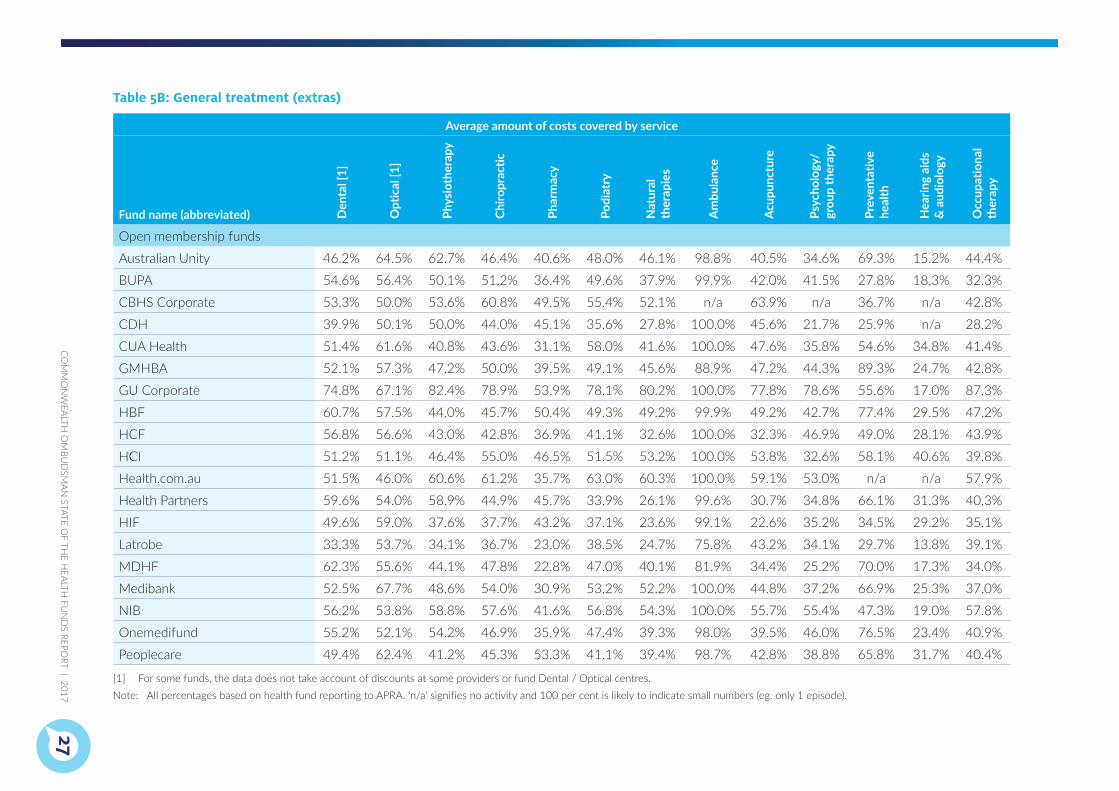

GENERAL TREATMENT (EXTRAS)General treatment or extras policies provide benefits towards a range of out-of-hospital health services The most commonly included services are dental optical physiotherapy and non-Pharmaceutical Benefits Scheme prescription medicines

The first table shows the average proportion of service charges covered by each fund per state (5A) for all their policies and services The second table (5B) shows the information according to the service being covered Generally higher-cost policies cover a higher proportion of charges

General treatment

General treatment policies also known as lsquoancillaryrsquo or lsquoextrasrsquo5 provide benefits towards a range of health-related services not provided by a doctor including but not limited to

bull dental fees and charges

bull optometry cost of glasses and lenses

bull physiotherapy chiropractic services and other therapies including natural and complementary therapies

bull prescribed medicines not covered by the Pharmaceutical Benefits Scheme

Percentage of charges covered all services by state

This table indicates what proportion of total charges associated with general treatment services is covered by each fundrsquos benefits This averages outcomes across all of each fundrsquos general treatment policies and services Higher cost policies will generally cover a greater proportion of charges than indicated by this average while cheaper policies may cover less

Average costs covered for each service type

This additional table provides information on the proportion of the total charge for each service type covered by each fund on average across all of the fundrsquos general treatment policies

5 Also known as lsquoessentialsrsquo cover in Western Australia

This is intended to provide a broad comparative indicator of fund general treatment benefits to allow comparisons between funds and should not be regarded as an indicator of how much of a bill for any particular service will be covered

Ambulance

Some funds do not provide ambulance cover through any of their general treatment policies but offer this as a component of hospital cover These funds show as lsquonarsquo under the ambulance column Most ambulance services in Queensland and Tasmania are provided free to residents of those states

Preferred providers

Many funds establish lsquopreferred providerrsquo or lsquoparticipating providerrsquo arrangements with some suppliers of general treatment services Those providers offer an agreed charge for fund members resulting in lower out-of-pocket costs for members after fund benefits are taken into account It is usually worth checking with your fund to see if a suitable preferred provider is available in your area

Fund dental and eyecare centres

In some states some funds operate their own dental and optical centres These are usually only located in capital cities or major population centres

Consumers who choose to use a fundrsquos own dental or optical centres will normally get services at a lower out of pocket cost

Additional information

The PHIO brochure lsquoHealth Insurance Choice Selecting a Health Insurance Policyrsquo includes important advice on what to consider and what questions to ask when selecting a general treatment policy The brochure is available at ombudsmangovau

The PHIOrsquos consumer website privatehealthgovau provides information about all private health insurance policies available in Australia including benefits prices and which hospitals a health fund has agreements with

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 26

Table 5A General treatment (extras)

Fund name (abbreviated)

general treatment (extras) charges coveredACT NSW VIC QLD SA WA TAS NT

Open membership fundsAustralian Unity 444 470 505 505 537 486 471 485BUPA 463 501 491 535 549 582 514 578CBHS Corporate na 529 535 554 425 645 720 700CDH 359 386 413 372 488 397 396 naCUA Health 437 540 510 497 501 480 476 431GMHBA 518 550 505 545 548 515 504 513GU Corporate 718 747 753 725 729 762 694 788HBF 491 515 515 517 557 578 564 576HCF 470 475 551 572 606 554 487 505HCI 437 529 536 500 525 476 480 635Healthcomau 536 531 539 525 565 557 533 572Health Partners 338 383 446 413 576 420 464 492HIF 423 463 471 477 501 479 464 471Latrobe 276 413 361 358 390 384 357 434MDHF 471 555 556 510 527 524 502 496Medibank 473 521 536 554 589 580 545 597NIB 545 539 591 560 599 587 551 582Onemedifund 466 509 523 510 549 530 518 naPeoplecare 476 509 495 482 529 502 483 479Phoenix 506 529 538 549 556 521 461 519QCH 467 500 508 535 538 512 488 492St Lukes 560 621 604 588 672 587 591 524Transport Health 417 490 545 491 525 517 518 490Westfund 437 482 464 508 509 475 475 449Restricted membership fundsACA 528 611 615 610 652 588 589 656CBHS 451 497 517 525 549 509 499 438Defence Health 447 492 513 517 553 514 488 519Doctorsrsquo Health 545 537 555 564 565 550 546 591Emergency Services 754 665 702 696 677 706 524 634Navy Health 455 489 532 516 561 525 506 505Nurses and Midwives 570 533 546 484 598 598 491 352Police Health 662 659 683 688 712 698 675 696Reserve Bank 730 743 775 769 850 759 781 900RT Health Fund 424 515 489 505 505 497 455 498Teachers Health 422 501 504 501 529 515 495 478TUH 430 500 472 553 511 507 487 459

Note lsquonarsquo signifies no activity in that state 100 per cent is likely to indicate small numbers (eg only one episode)

CO

MM

ON

WEALTH

OM

BUD

SMAN

STATE OF TH

E HEALTH

FUN

DS REPO

RT | 201727

Table 5B General treatment (extras)

Average amount of costs covered by service

Fund name (abbreviated) Den

tal [

1]

Opt

ical

[1]

Phys

ioth

erap

y

Chiro

prac

tic

Phar

mac

y

Podi

atry

Nat

ural

th

erap

ies

Am

bula

nce

Acup

unct

ure

Psyc

holo

gy

grou

p th

erap

y

Prev

enta

tive

heal

th

Hea

ring

aids

amp

aud

iolo

gy

Occ

upat

iona

l th

erap

y

Open membership funds

Australian Unity 462 645 627 464 406 480 461 988 405 346 693 152 444

BUPA 546 564 501 512 364 496 379 999 420 415 278 183 323

CBHS Corporate 533 500 536 608 495 554 521 na 639 na 367 na 428

CDH 399 501 500 440 451 356 278 1000 456 217 259 na 282

CUA Health 514 616 408 436 311 580 416 1000 476 358 546 348 414

GMHBA 521 573 472 500 395 491 456 889 472 443 893 247 428

GU Corporate 748 671 824 789 539 781 802 1000 778 786 556 170 873

HBF 607 575 440 457 504 493 492 999 492 427 774 295 472

HCF 568 566 430 428 369 411 326 1000 323 469 490 281 439

HCI 512 511 464 550 465 515 532 1000 538 326 581 406 398

Healthcomau 515 460 606 612 357 630 603 1000 591 530 na na 579

Health Partners 596 540 589 449 457 339 261 996 307 348 661 313 403

HIF 496 590 376 377 432 371 236 991 226 352 345 292 351

Latrobe 333 537 341 367 230 385 247 758 432 341 297 138 391

MDHF 623 556 441 478 228 470 401 819 344 252 700 173 340

Medibank 525 677 486 540 309 532 522 1000 448 372 669 253 370

NIB 562 538 588 576 416 568 543 1000 557 554 473 190 578

Onemedifund 552 521 542 469 359 474 393 980 395 460 765 234 409

Peoplecare 494 624 412 453 533 411 394 987 428 388 658 317 404

[1] For some funds the data does not take account of discounts at some providers or fund Dental Optical centres Note All percentages based on health fund reporting to APRA na signifies no activity and 100 per cent is likely to indicate small numbers (eg only 1 episode)

CO

MM

ON

WEALTH

OM

BUD

SMAN

STATE OF TH

E HEALTH

FUN

DS REPO

RT | 201728

Average amount of costs covered by service

Fund name (abbreviated) Den

tal [

1]

Opt

ical

[1]

Phys

ioth

erap

y

Chiro

prac

tic

Phar

mac

y

Podi

atry

Nat

ural

th

erap

ies

Am

bula

nce

Acup

unct

ure

Psyc

holo

gy

grou

p th

erap

y

Prev

enta

tive

heal

th

Hea

ring

aids

amp

aud

iolo

gy

Occ

upat

iona

l th

erap

y

Phoenix 576 617 513 497 401 535 355 977 412 424 488 420 437

QCH 531 588 480 617 351 657 398 na 454 476 421 376 407

St Lukes 643 678 513 543 420 491 423 782 450 504 524 450 484

Transport Health 553 593 471 560 352 538 426 1000 361 339 531 234 303

Westfund 528 490 397 560 380 408 402 999 372 364 537 381 564

Restricted membership funds

ACA 648 714 454 511 462 744 390 981 384 525 na 408 553

CBHS 508 531 534 615 427 459 449 969 469 424 362 352 357

Defence Health 500 524 527 552 469 527 403 1000 368 473 847 305 473

Doctorsrsquo Health 585 576 486 na 459 524 na na na 503 353 216 423

Emergency Services 712 530 771 761 443 666 406 na 800 694 na na na

Navy Health 479 576 549 610 469 527 467 993 na 418 1000 274 382

Nurses and Midwives 565 527 469 639 415 485 447 1000 388 489 637 429 579

Police Health 704 677 759 772 437 702 390 998 756 755 1000 339 706

Reserve Bank 764 737 721 743 608 785 784 1000 760 770 574 772 677

RT Health Fund 482 635 539 535 417 503 394 1000 556 232 467 351 344

Teachers Health 527 516 462 589 409 546 464 998 433 415 412 349 606

TUH 596 536 489 561 371 619 520 1000 456 432 512 414 385

[1] For some funds the data does not take account of discounts at some providers or fund Dental Optical centres Note All percentages based on health fund reporting to APRA na signifies no activity and 100 per cent is likely to indicate small numbers (eg only 1 episode)

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 29

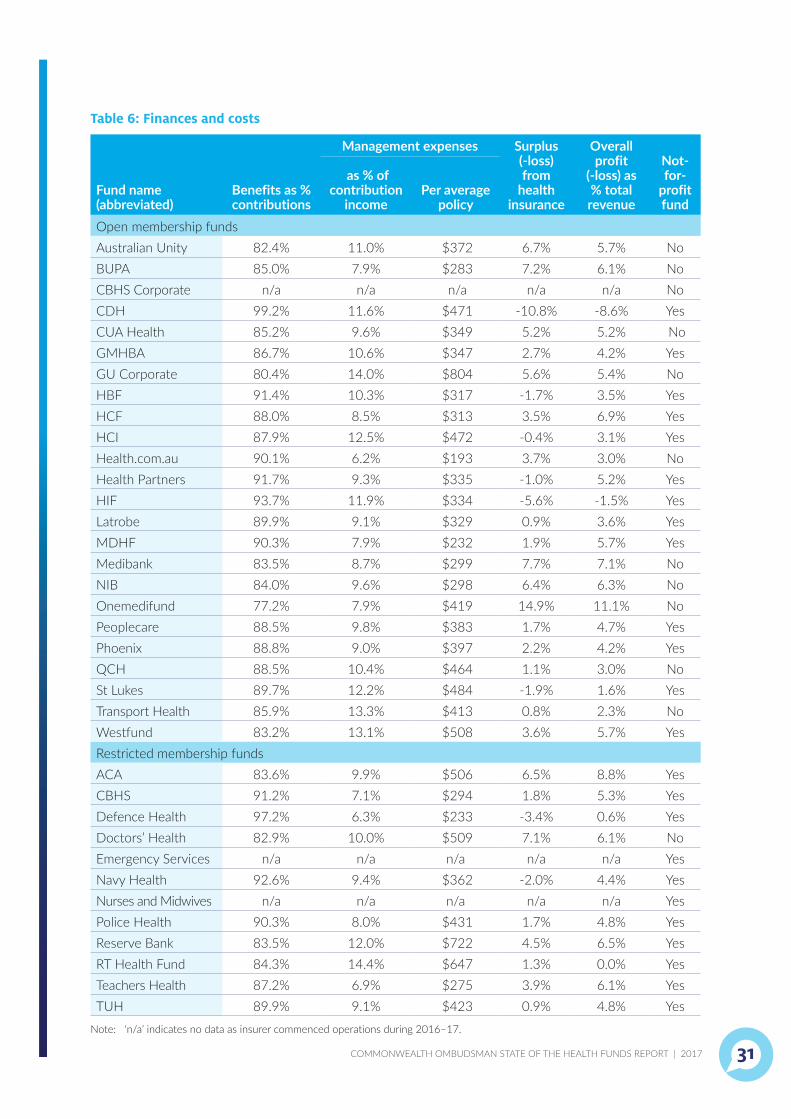

FINANCES AND COSTSAll health funds are required to meet financial management standards to ensure their membersrsquo contributions are protected Generally funds aim to set premium levels so their income from contributions covers the expected cost of benefits plus the fundrsquos administration costs

The percentage of contribution income which goes towards administration and management expenses is a key measure of fund efficiency

The regulation of health fund finances

The Private Health Insurance Act 2007 (the Act) specifies solvency and capital adequacy standards for funds to meet and outlines financial management and reporting requirements for all funds

The Private Health Insurance (Prudential Regulation) Act 2015 (the Prudential Regulation Act) ensures that private health insurers must comply with prudential standards made by APRA and with directions given by APRA APRA has monitoring and investigative powers in relation to private health insurers in order to monitor the financial performance of the funds and ensure that they meet prudential requirements

APRA produces an annual publication providing financial and operational statistics for the funds for each financial year6 Information included in the Financial Performance table (Table 6) is drawn from data collected by APRA for that purpose

6 The lsquoOperations of the Private Health Insurersrsquo report is available on the APRA website apragovau

Premium increases

Under the Act health funds require the approval of the Minister for Health before they can raise their premiums

The Minister assesses premium applications to ensure proposed increases are kept to the minimum necessary This takes into consideration fund solvency requirements forecast benefit payments and prudential requirements while also ensuring the affordability and value of private health insurance as a product

Benefits as a percentage of contributions

This column shows the percentage of total contributions received by the fund returned to contributors in benefits Funds will generally aim to set premium levels so that contribution income covers the expected costs of benefits plus the fundrsquos administration costs

A very high percentage of contributions returned as benefits may not necessarily be a positive factor for consumers particularly if it means that the fund is making a loss on its health insurance business This indicator should therefore be considered in conjunction with other factors such as the Surplus (-loss) and Management Expenses ratings

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 30

Management expenses

Management expenses are the costs of administering the fund They include items such as rent staff salaries and marketing costs

As a percentage of contribution income

This figure is regarded as a key measure of fund efficiency In this table management expenses are shown as a proportion of total fund contributions

Per average policy

A comparison of the relative amount each fund spends on administration costs is also demonstrated through provision of information on the level of management expenses per membership by each fund

On average restricted membership funds have lower management expenses as a proportion of benefits paid then open membership funds This is partially due to lower expenditure on marketing However unusually low management expenses by some restricted membership funds can also be the result of those funds receiving free or subsidised administrative services from the organisations with which they are associated

Surplus (-loss) from health insurance

The surplus or loss (indicated as a negative figure) made by the fund in 2016ndash17 from their health insurance business is expressed as a percentage of the fundrsquos contribution income This does not take account of additional income that the fund may derive from investment or other non-health insurance activities

All health funds maintain a sufficient level of reserves to cover losses from year to year However funds with high or continuing losses might be expected to have to increase premiums by a higher relative amount than other funds

Overall profit (-loss) as a percentage of total revenue

The overall profit or loss (indicated as a negative figure) takes account of additional income made by the fund mainly through investment This is shown as a percentage of all revenue received by the fund to allow a comparison of performance between funds of differing sizes Overall profit takes into account tax that is paid for a small amount of funds

Not-for-profit fund

If a health fund is listed as lsquonot-for-profitrsquo this means it is a mutual organisation with the premiums paid into the fund used to operate the business and cover benefits for members

lsquoFor-profitrsquo funds aim to return a profit to their owners (which may be another health fund or corporation) or shareholders

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 31

Table 6 Finances and costs

Fund name (abbreviated)

Benefits as contributions

Management expenses Surplus (-loss) from

health insurance

Overall profit

(-loss) as total revenue

Not- for-

profit fund

as of contribution

incomePer average

policy Open membership fundsAustralian Unity 824 110 $372 67 57 NoBUPA 850 79 $283 72 61 NoCBHS Corporate na na na na na NoCDH 992 116 $471 -108 -86 YesCUA Health 852 96 $349 52 52 NoGMHBA 867 106 $347 27 42 YesGU Corporate 804 140 $804 56 54 NoHBF 914 103 $317 -17 35 YesHCF 880 85 $313 35 69 YesHCI 879 125 $472 -04 31 YesHealthcomau 901 62 $193 37 30 NoHealth Partners 917 93 $335 -10 52 YesHIF 937 119 $334 -56 -15 YesLatrobe 899 91 $329 09 36 YesMDHF 903 79 $232 19 57 YesMedibank 835 87 $299 77 71 NoNIB 840 96 $298 64 63 NoOnemedifund 772 79 $419 149 111 NoPeoplecare 885 98 $383 17 47 YesPhoenix 888 90 $397 22 42 YesQCH 885 104 $464 11 30 NoSt Lukes 897 122 $484 -19 16 YesTransport Health 859 133 $413 08 23 NoWestfund 832 131 $508 36 57 YesRestricted membership fundsACA 836 99 $506 65 88 YesCBHS 912 71 $294 18 53 YesDefence Health 972 63 $233 -34 06 YesDoctorsrsquo Health 829 100 $509 71 61 NoEmergency Services na na na na na YesNavy Health 926 94 $362 -20 44 YesNurses and Midwives na na na na na YesPolice Health 903 80 $431 17 48 YesReserve Bank 835 120 $722 45 65 YesRT Health Fund 843 144 $647 13 00 YesTeachers Health 872 69 $275 39 61 YesTUH 899 91 $423 09 48 Yes

Note lsquonarsquo indicates no data as insurer commenced operations during 2016ndash17

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 32

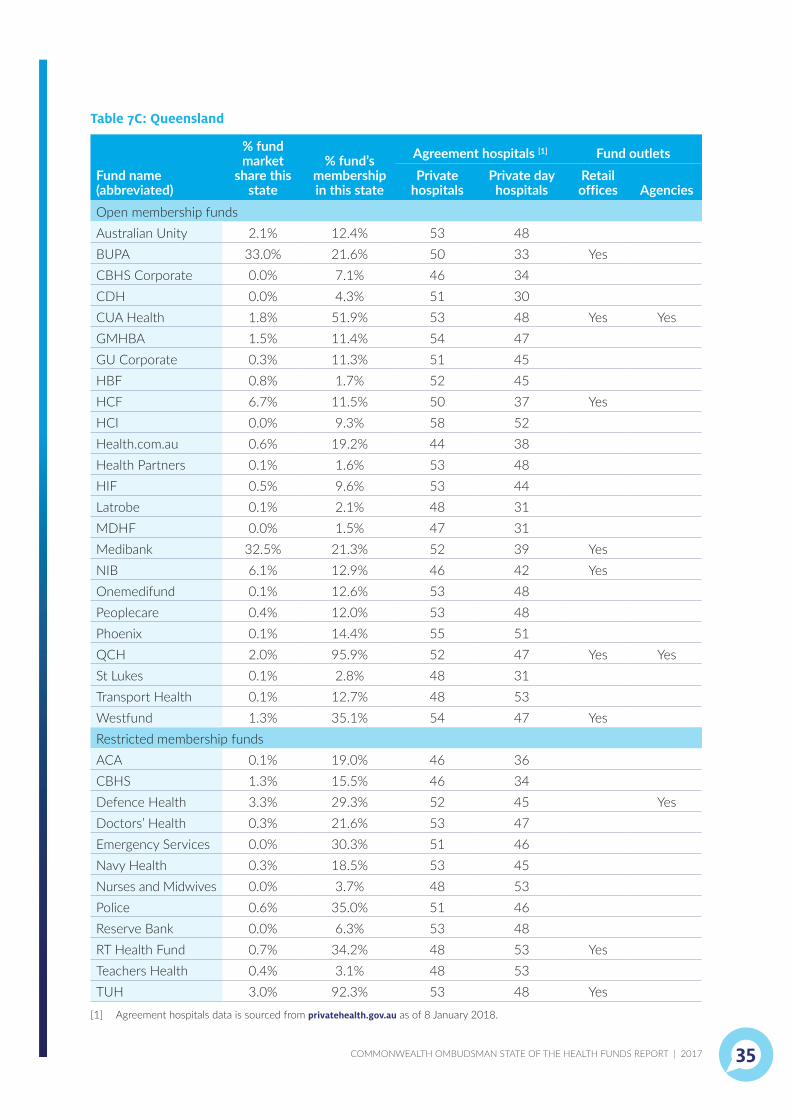

HEALTH FUND OPERATIONS BY STATE OR TERRITORYSome funds have little presence in most states but may have a large market share in one state or territory Every fund will still have agreements with hospitals throughout Australia even if they donrsquot have a local branch network or a significant proportion of policy holders in each state Australian health insurance policies are usually priced according to the policy holderrsquos state of residence but the benefits extend nation-wide

Health fund operations by state or territorySome funds have little presence in most states but may have a large market share in one state or territory Some funds use different brand names or offer different policies in different states and territories These separate tables for each stateterritory are therefore provided to give an indication of the extent and importance of each fundrsquos business in each area Most fund websites allow members to view fund information join or change their policy and submit claims Links to all health fund websites are available at privatehealthgovau

Percentage market shareThis column indicates how much of the total health insurance business within each state or territory each fund accounts for It is an indicator of the size and significance of each fund within each state Funds with a significant market share in the relevant state or territory can normally be expected to have more extensive networks of branch offices agencies agreement hospitals and preferred ancillary providers in those statesterritories They are also more likely to obtain the participation of doctors in their gap cover arrangements However funds participating in schemes such as the Australian Health Services Alliance (AHSA) will generally have access to a wide range of agreement hospitals in all states

Percentage of fundrsquos membership in stateThis column indicates how much of each fundrsquos health insurance membership is within each state It is an indicator of how significant that state is to each fundrsquos health insurance business

In general funds can be expected to design their policies (benefits conditions contracts etc) to suit the arrangements applying in the states in which they do a significant proportion of business However some nationally-based funds tailor their policies and prices to take account of different state arrangementsHealth fund costs differ from state to state which accounts for the variation in premiums across states

Agreement hospitals7

All health funds establish agreements with some or all private hospitals and day hospitals for the treatment of their members These agreements generally provide for the fund to meet all of the private hospitalrsquos charges for treatment of the fundrsquos members The member would then not be required to pay any amount to the hospital other than any agreed excess or co-payment and any incidental charges that may apply for certain extra services (eg television rental or internet)8

Where a fund has a comparatively low number of agreements with private hospitals or private day hospitals this is an indicator that consumer choice (as to where to be treated) may be more limited Treatment at a non-agreement hospital will mean a significantly higher out of pocket cost for the patientWhile funds do not have agreements with particular public hospitals all funds will fully cover hospital costs for treatment as a private patient in a public hospital unless the particular treatment is excluded under the individualrsquos policy or there is an extra charge for a private room or similar extra costs

Fund outletsmdashretail offices and agencies

Retail offices are full-service offices operated by health funds with staff employed by the fund

Agencies are generally limited service outlets operated by the fund or under arrangements with pharmacies credit unions etc

The table indicates whether the fund operates retail offices andor agencies in the state or territory

7 According to privatehealthgovau 8 January 2018 or as supplied by the fund

8 These agreements do not apply to fees charged by private doctors for in-hospital treatment these medical fees may be covered by a fundrsquos medical gap scheme arrangements

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 33

Table 7A New South Wales

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies

Open membership fundsAustralian Unity 17 189 98 88BUPA 258 315 87 74 YesCBHS Corporate 00 673 79 65CDH 01 899 75 53 YesCUA Health 05 258 101 91 YesGMHBA 10 153 99 90GU Corporate 06 490 98 90HBF 08 35 96 85HCF 196 620 83 86 YesHCI 00 104 100 100Healthcomau 06 358 85 74Health Partners 00 14 100 89HIF 03 124 99 91Latrobe 02 79 77 51MDHF 01 108 80 51 YesMedibank 230 282 88 74 Yes YesNIB 137 543 88 91 YesOnemedifund 01 409 100 89 YesPeoplecare 07 458 100 89 YesPhoenix 02 483 99 98 YesQCH 00 16 81 72St Lukes 00 36 79 48Transport Health 01 152 89 100Westfund 13 620 99 90 YesRestricted membership fundsACA 01 580 79 66 YesCBHS 20 449 79 65Defence Health 11 181 99 90 YesDoctorsrsquo Health 03 391 99 90 YesEmergency Services 00 189 99 92Navy Health 03 298 98 89Nurses and Midwives 00 591 100 89Police 00 16 99 92Reserve Bank 01 611 100 89 YesRT Health Fund 06 516 89 100 YesTeachers Health 48 696 100 89 YesTUH 01 37 100 89

[1] Agreement hospitals data is sourced from privatehealthgovau as of 8 January 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 34

Table 7B Victoria

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies

Open membership fundsAustralian Unity 77 608 78 75 YesBUPA 242 212 75 59 YesCBHS Corporate 00 142 73 50CDH 00 38 74 64CUA Health 04 175 78 77 Yes YesGMHBA 61 640 78 76 Yes YesGU Corporate 04 224 77 76HBF 13 37 77 71HCF 65 149 70 45 YesHCI 01 249 79 79Healthcomau 08 330 71 64Health Partners 01 34 78 75HIF 06 151 77 76Latrobe 25 880 76 62 Yes YesMDHF 08 848 76 63 Yes YesMedibank 330 289 68 53 YesNIB 74 209 71 68 YesOnemedifund 01 249 78 75Peoplecare 07 323 78 75 YesPhoenix 01 192 78 82QCH 00 09 74 58St Lukes 01 55 75 62Transport Health 04 672 75 78Westfund 00 09 78 76Restricted membership fundsACA 00 129 73 50CBHS 15 247 73 50Defence Health 25 301 78 76 Yes YesDoctorsrsquo Health 03 301 78 76Emergency Services 00 223 76 77Navy Health 04 275 78 75 YesNurses and Midwives 00 280 78 74Police 00 24 77 77Reserve Bank 00 231 78 75RT Health Fund 02 104 75 78Teachers Health 14 146 78 74 YesTUH 01 29 78 75

[1] Agreement hospitals data is sourced from privatehealthgovau as of 8 January 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 35

Table 7C Queensland

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies

Open membership fundsAustralian Unity 21 124 53 48BUPA 330 216 50 33 YesCBHS Corporate 00 71 46 34CDH 00 43 51 30CUA Health 18 519 53 48 Yes YesGMHBA 15 114 54 47GU Corporate 03 113 51 45HBF 08 17 52 45HCF 67 115 50 37 YesHCI 00 93 58 52Healthcomau 06 192 44 38Health Partners 01 16 53 48HIF 05 96 53 44Latrobe 01 21 48 31MDHF 00 15 47 31Medibank 325 213 52 39 YesNIB 61 129 46 42 YesOnemedifund 01 126 53 48Peoplecare 04 120 53 48Phoenix 01 144 55 51QCH 20 959 52 47 Yes YesSt Lukes 01 28 48 31Transport Health 01 127 48 53Westfund 13 351 54 47 YesRestricted membership fundsACA 01 190 46 36CBHS 13 155 46 34Defence Health 33 293 52 45 YesDoctorsrsquo Health 03 216 53 47Emergency Services 00 303 51 46Navy Health 03 185 53 45Nurses and Midwives 00 37 48 53Police 06 350 51 46Reserve Bank 00 63 53 48RT Health Fund 07 342 48 53 YesTeachers Health 04 31 48 53TUH 30 923 53 48 Yes

[1] Agreement hospitals data is sourced from privatehealthgovau as of 8 January 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 36

Table 7D South Australia

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies

Open membership fundsAustralian Unity 15 38 25 25BUPA 504 144 26 22 YesCBHS Corporate 00 33 27 19CDH 00 09 22 15CUA Health 01 12 26 25GMHBA 04 15 26 25GU Corporate 01 18 26 24HBF 05 05 24 23HCF 61 46 25 17 YesHCI 00 23 27 28Healthcomau 02 27 27 23Health Partners 75 926 25 25 Yes YesHIF 03 25 26 26Latrobe 00 06 22 14MDHF 01 22 22 14Medibank 219 63 26 20 Yes YesNIB 33 30 23 22Onemedifund 01 51 25 25Peoplecare 03 50 25 25Phoenix 02 132 27 28QCH 00 03 27 21St Lukes 01 16 22 14Transport Health 00 17 25 25Westfund 00 05 26 25Restricted membership fundsACA 00 33 27 21CBHS 09 47 27 19Defence Health 21 83 27 26 YesDoctorsrsquo Health 01 32 26 25Emergency Services 00 137 26 25Navy Health 02 55 26 24Nurses and Midwives 00 27 25 24Police 15 361 26 25 YesReserve Bank 00 37 25 25RT Health Fund 01 13 25 25Teachers Health 18 62 25 24TUH 00 02 25 25

[1] Agreement hospitals data is sourced from privatehealthgovau as of 8 January 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 37

Table 7E Western Australia

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies

Open membership fundsAustralian Unity 05 23 20 22BUPA 114 56 19 15 YesCBHS Corporate 00 43 16 11CDH 00 03 18 15CUA Health 01 21 21 24 YesGMHBA 09 56 20 24GU Corporate 04 133 20 24HBF 543 900 23 21 Yes YesHCF 27 34 18 11 YesHCI 00 13 21 26Healthcomau 02 56 18 18Health Partners 00 04 22 23HIF 39 588 21 23 Yes YesLatrobe 00 04 18 14MDHF 00 03 18 14Medibank 199 98 20 18 Yes YesNIB 27 43 19 20Onemedifund 01 112 22 23Peoplecare 01 27 22 23Phoenix 00 32 21 25QCH 00 06 17 15St Lukes 00 06 17 14Transport Health 00 17 23 22Westfund 00 05 20 24Restricted membership fundsACA 00 45 16 11CBHS 08 71 16 11Defence Health 06 43 20 24 YesDoctorsrsquo Health 00 21 20 24Emergency Services 00 57 20 24Navy Health 02 74 20 24Nurses and Midwives 00 13 22 23Police 03 140 20 24Reserve Bank 00 34 22 23RT Health Fund 00 12 23 22Teachers Health 05 29 22 23TUH 00 02 22 23

[1] Agreement hospitals data is sourced from privatehealthgovau as of 8 January 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 38

Table 7F Tasmania

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies

Open membership fundsAustralian Unity 10 07 5 3BUPA 360 27 8 4 YesCBHS Corporate 00 09 8 2CDH 00 03 6 7CUA Health 01 03 8 3GMHBA 11 10 8 3GU Corporate 01 05 8 3HBF 08 02 8 3HCF 30 06 5 3HCI 23 510 8 5 YesHealthcomau 02 07 8 3Health Partners 01 02 5 3HIF 02 06 8 4Latrobe 02 05 8 6MDHF 00 01 8 6Medibank 288 22 5 3 YesNIB 23 06 5 2Onemedifund 02 51 5 3Peoplecare 02 07 5 3Phoenix 00 06 8 5QCH 00 02 8 3St Lukes 189 857 8 6 Yes YesTransport Health 00 05 3 5Westfund 01 02 8 3Restricted membership fundsACA 00 14 8 2CBHS 11 16 8 2Defence Health 11 11 8 3Doctorsrsquo Health 01 09 8 3Emergency Services 00 17 8 4Navy Health 02 14 8 3Nurses and Midwives 00 34 5 3Police 05 30 8 4Reserve Bank 00 11 5 3RT Health Fund 01 04 3 5Teachers Health 12 11 5 3TUH 01 03 5 3

[1] Agreement hospitals data is sourced from privatehealthgovau as of 8 January 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 39

Table 7G Australian Capital Territory

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies

Open membership fundsAustralian Unity 16 11 6 7BUPA 224 17 5 4 YesCBHS Corporate 00 24 5 4CDH 00 04 5 6CUA Health 03 10 6 7 YesGMHBA 12 11 6 7GU Corporate 03 15 6 7HBF 09 02 6 7HCF 142 28 5 6 YesHCI 00 08 6 8Healthcomau 07 24 6 6Health Partners 01 03 6 7HIF 03 08 6 7Latrobe 01 04 5 6MDHF 00 01 5 6Medibank 290 22 5 4 YesNIB 153 37 6 7 YesOnemedifund 00 02 6 7Peoplecare 03 13 6 7Phoenix 01 08 6 7QCH 00 02 6 7St Lukes 00 02 5 6Transport Health 01 09 7 6Westfund 02 07 6 7Restricted membership fundsACA 00 08 5 4CBHS 10 14 5 4Defence Health 72 73 6 7 YesDoctorsrsquo Health 03 26 6 7Emergency Services 00 23 6 7Navy Health 13 89 6 7Nurses and Midwives 00 13 5 7Police 01 04 6 7Reserve Bank 00 12 6 7RT Health Fund 01 06 7 6Teachers Health 24 22 5 7TUH 01 03 7 6

[1] Agreement hospitals data is sourced from privatehealthgovau as of 8 January 2018

COMMONWEALTH OMBUDSMAN STATE OF THE HEALTH FUNDS REPORT | 2017 40

Table 7H Northern Territory

Fund name (abbreviated)

fund market

share this state

fundrsquos membership in this state

Agreement hospitals [1] Fund outlets Private

hospitalsPrivate day

hospitalsRetail offices Agencies