Embed Size (px)

Citation preview

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED

JUNE 30, 2011

ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDEO SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

TABLE OF CONTENTS

Pages

PART I - FINANCIAL SECTION

Independent Auditors' Report....................................................................................... 1-2

Management's Discussion and Analysis ...................... .................................................. 3-15

Basic Financial Statements:

Government - Wide Financial Statements:

Statement of Net Assets............................................................................................... 16

Statement of Activities .................................................................................................. 17

Fund Financial Statements - Governmental Funds

BalanceSheet ............................................................................................................. 18

Reconciliation of the Governmental Funds Balance Sheet to Statement of Net Assets............................................................................................... 19

Statement of Revenues, Expenditures, and Changes in Fund Balances........................ 20

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balance of Governmental Funds to the Statement of Activities ........................ 21

Notes to Basic Financial Statements ............................................................................. 22-44

PART II- REQUIRED SUPPLEMENTARY INFORMATION

Budgetary Comparison Schedule - General Fund......................................................... 46

Notes to Budgetary Comparison Schedule - General Fund.......................................... 47

ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

TABLE OF CONTENTS (CONTINUED)

Pages

PART III - SINGLE AUDIT SECTION

Schedule of Expenditures of Federal Awards ................................................................ 49

Notes to Schedule of Expenditures of Federal Awards ................................................. 50

Independent Auditors' Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based and on Audit of Financial Statements Performed in Accordance with Government Auditing Standards.............. 51-52

Independent Auditors' Report on Compliance with Requirements that Could Have a Direct and Material Effect on Each Major Program and on Internal Control over Compliance in Accordance with 0MB Circular A-i 33 ........ ..................... 53-54

Schedule of Findings and Questioned Costs ................................................................ 55-56

Schedule of Status of Prior Year Audit Findings and Questioned Costs.. ...................... 57

ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

PART I - FINANCIAL SECTION

ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

Ortiz, Rivera, Rivera & Co. Certified Public Accountants and Business Advisors

CPA Orlando Luis Ortiz Cabrera CPA Marco Antonio Rivera Zidiga CPA Luis Rivera Zddiga CPA Zoraida Cruz Claudio

Members: American Institute of Certified Public Accountants (AICPA)

Puerto Rico Board of Certified Public Accountants

INDEPENDENT AUDITORS REPORT

To the Honorable Mayor and Municipal Legislature Municipality of Fajardo Fajardo, Puerto Rico

We have audited the accompanying financial statements of the governmental activities, each major fund and the aggregate remaining fund information of the Municipality of Fajardo, as of and for the year ended June 30, 2011, which collectively comprise the Municipality's basic financial statements, as listed in the table of contents. These financial statements are the responsibility of the Municipality's management. Our responsibility is to express opinions on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United

IStates of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the

I financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and the significant estimates made by

I management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions.

I

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund and the aggregate remaining fund information of the Municipality of Fajardo as of June 30, 2011, and the respective changes in financial position thereof for the fiscal year then ended in conformity

Iwith accounting principles generally accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued our report dated February10, 2012 on our consideration of the Municipality's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, grants, agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

Suite 152, P0 Box 70250, San Juan, P.R. 00936-7250 • Phone (787) 756-8524, Fax (787) 274-0562

The Management's Discussion and Analysis on pages 3 through 15, and the Budgetary Comparison Schedule on page 46 are not a required part of the basic financial statements but

I are supplementary information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding methods of measurement and presentation of

I the required supplementary information. However, we did not audit the information and express no opinion on it.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Municipality of Fajardo's financial statements as a whole. The accompanying schedule of expenditures of federal awards is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is not a required part of the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements, and in our opinion, the information is fairly stated, in all material respects, in relation to the basic financial statements taken as a whole.

I San Juan, Puerto Rico February 10, 2012

I

The stamp El 8906 was affi to the originat of this

I

-2-

ORTIZ, RIVERA, RIVERA & CO. CBRTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO

IMUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

IFOR THE FISCAL YEAR ENDED JUNE 30, 2011

IThe following discussion and analysis of the Municipality of Fajardo' financial performance provides an overview of the Municipality's financial activities for the fiscal year ended June 30,

I 2011. Please read it in conjunction with the financial statements which foiw this section.

FINANCIAL HIGHLIGHTS

I Highlights for Government-wide Financial Statements

The government-wide financial statements report information about the Municipality as a whole

I using the economic resources measurement focus and accrual basis of accounting:

The assets of the Municipality, on a government-wide basis, exceeded its liabilities at the

I close of fiscal year 2011 by $140,023,905 (net assets). Revenues decreased by $1,384,106 and expenses increased by $6,414,136 in comparison with year 2010, as restated.

I. Net change in net assets amounted to $ 13,357,504, an increase with respect to prior

year (2010) net change.

IHighlights for Fund Financial Statements

The fund financial statements provide detailed information about the Municipality's most significant funds using the current financial resources measurement focus and modified accrual

I basis of accounting:

At the close of the current fiscal year, the Municipality's governmental funds reported

I combined ending fund balances of $60,766,970 an increase of $5,987,790 in comparison with the prior year.

. The General Fund reported an excess of revenues over expenditures and other

I financing uses of $ 1,053,571 and an unassigned fund balance of $14,882,326. Unassigned fund balances decreased by $1 ,236,268 from prior year.

IGeneral Financial Highlights

The investment in net capital assets as of June 30, 2011 was $85,026,207(net of related - debt).

Long term debt general and special obligations decreased by $2,205,000 approximately 4% with respect to prior year balance.

I. Other long term debts decreases and net reductions from payments amounted to

$2,489,651, respectively. On a budgetary basis, actual revenues exceeded actual expenditures by $17,864,347, revenues increase was mainly due to over estimate of $2,519,654 in miscellaneous

I revenues, although Municipality realized economies, principally in general administration $2,637,598.

1 -3-

I COMMONWEALTH OF PUERTO RICO

MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

I FOR THE FISCAL YEAR ENDED JUNE 30, 2011

I OVERVIEW OF THE FINANCIAL STATEMENTS

The Municipality's basic financial statements comprise three components: (1) management

I

discussion and analysis (presented here), (2) basic financial statements, and (3) required supplementary information.

MPO ETS' - • STT1Ef'TS

-S

I H

: I The Municipality's basic financial statements consist of two kinds of statements, each with a

different view of the Municipality's finances. The government-wide financial statements provide

I

both long-term and short-term information about the Municipality's overall financial status. The fund financial statements focus on major aspects of the Municipality's operations, reporting those operations in more detail than the government-wide statements:

Basic Financial Statements

. Government-Wide Financial Statements

The government-wide statements report information about the Municipality as a whole

I

using accounting methods similar to those used by private-sector businesses. They are prepared using the flow of economic resources measurement focus and the accrual basis of accounting. The first government-wide statement - the Statement of Net Assets

I

- presents information on all of the Municipality's assets and liabilities, with the difference between the two reported as net assets. Over time, increases or decreases in the Municipality's net assets are an indicator of whether its financial health is improving

I

or deteriorating. Other non-financial factors such as the condition of the Municipality's roads and other infrastructure may need to be considered to assess the overall health of the Municipality. The second statement - the Statement of Activities - presents information showing how the net assets changed during the year. All of the current

I

year's revenues and expenses are taken into account in the statement of activities regardless of when cash is received or paid.

-4-

I COMMONWEALTH OF PUERTO RICO

I MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

I FOR THE FISCAL YEAR ENDED JUNE 30, 2011

The government-wide statements reports as governmental activities the Municipality's basic services such as public safety, public works, health and sanitation, culture and recreation, solid waste disposal, human services and welfare, and community development;education and general administration. These activities are primarily financed through property taxes, other local taxes and intergovernmental revenues. Included in the governmental activities are the governmental funds.

. Fund Financial Statements

The fund financial statements provide more detailed information about the Municipality's most significant funds. Funds are accounting devices that the Municipality uses to keep track of specific sources of funding and spending for particular purposes. Some funds are required by Federal and Commonwealth regulations, as well by bond covenants.

The Municipality's basic services are included in governmental funds, which are used to account for essentially the same functions reported as governmental activities in the government-wide statements. However, unlike the government-wide statements, the governmental funds are prepared using the flow of current financial resources measurement focus and the modified accrual basis of accounting. Under this approach the financial statements focus on near-term inflows and outflows of external resources, as well on balances of expendable resources available at year end. Consequently, the governmental fund statements provide a detailed short-term view that helps the reader determine whether there are more or fewer financial resources that can be spent in the near future to finance the Municipality's programs. Because this information does not encompass the additional long-term focus of the government-wide statements, additional information is provided on a subsequent page that explains the relationship (or differences) between the government-wide and fund statements.

The governmental fund statements focus on major funds. The Municipality's major funds are the general fund (which accounts for the main operating activities of the Municipality) and funds that complies with a minimum criterion (percentage of the assets, liabilities, revenues or expenditures). Funds that do not comply with this criterion are grouped and presented in a single column as other governmental funds.

. Notes to the Financial Statements

Provides integral information needed to explain the basis for the numbers used within the Basic Financial Statements and provide more detailed data.

Required Supplementary Information

Provides additional information to better understand the financial position of the Municipality and contains the Budgetary Comparison Schedule for the General Fund.

-5-

Table 1 Commonwealth of Puerto Rico

Municipality of Fajardo, Puerto Rico Statement of Net Assets

As of June 30, 2011

2011 2010 Current and non-current assets................ $78,069,026 $ 68,141,379 Capital assets (As Restated) .................... 89,772,020 90,914,132

Total Assets .................................... 167,841,046 159,055,511 Current liabilities....................................... 902,804 1,107,961 Deferred revenues.................................... 6,145,063 6,899,843 Long-term liabilities (As Restated) 20,769,274 24,244,024

Total Liabilities................................ 27,817,141 32.251,828 Investment in capital assets, Net of

Related Debt..................................... 85,026,207 82,857,737 Restricted.............................................. 42,322,055 27,056,139 Unrestricted (As Restated) ................... 12,675,643 16,752,525

Total Net Assets.............................. $ 140.023.905 $ 126.666 .401

I COMMONWEALTH OF PUERTO RICO

I MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

I FOR THE FISCAL YEAR ENDED JUNE 30, 2011

I FINANCIAL ANALYSIS OF THE MUNICIPALITY AS A WHOLE

Net Assets

I The following table presents a summary of the Statements of Net Assets as of June 30, 2011 and 2010:

I Net assets (assets over liabilities) may serve over time as a useful indicator of a government's financial position. Net assets for the year decreased, with respect to prior year as restated. The most significant changes were an increase in restricted assets of $ 15,265,916

The largest portion of the Municipality's net assets reflects its investment in capital assets (e.g., land, buildings, equipment, and infrastructure) for $85,026,207 total capital assets ($89,772,020) less accumulated depreciation ($42,460,921) and less any related outstanding debt ($745,813) used to acquire or construct those assets. The Municipality uses these assets to provide services to its citizens and consequently, these assets are not available for future spending. The resources needed to repay the debt related to these capital

assets must be provided from other sources, because capital assets are not generally liquidated for the purposes of retiring debt.

Restricted net assets represent resources that are subject to external restrictions on how they may be used.

Unrestricted net assets are the part of the net assets that can be used to finance day-to-day operations without constrains established by debt covenants, enabling legislation or other legal requirements.

I As of June 30, 2011 the Municipality presented unrestricted net assets of $12,675,643 This balance was affected by long term obligations such as compensated absences $1 ,968,774 and

I

other debts for the amount of $520,877 for which the Municipality did not provide funding in previous budgets. Historically, such obligations have been budgeted on a pay as you go basis without providing funding for their future liquidation.

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Changes in Net Assets

The following table summarizes the changes in net assets for the years ended June 30, 2011 and 2010:

Table 2 Commonwealth of Puerto Rico

Municipality of Fajardo, Puerto Rico Changes in Net Assets

For Fiscal Years Ending June 30, 2011 and 2010

2011 2010 Revenues: Program Revenues:

Capital Grants and Contributions $ - $ 2,395,225 Operating Grants and Contributions 9,217,241 7,304,077

General Revenues: Property Taxes................................... 11,397,583 12,842,417 Volume of Business Taxes................. 8,408,328 5,388,135 Sales and Usage Taxes 3,730,994 4,377,562 Construction Taxes............................. 535,228 1,811,044 Intergovernmental............................... 1,775,359 2,236,701 Other General Revenues 995,870 1,089,548 Total revenues ................................. 36,060,603 37,444,709

Expense ................................................ General Administration....................... 11,885,109 13,492,383 Public Safety ...................................... 834,861 954,192 Public Works ...................................... 2,803,382 2,141,482 Culture and Recreation and Instruction 845,109 1,178,175 Health and Sanitation......................... 194,315 4,664,811 Human Services and Welfare............. 1,302,247 1,361,001

Public Instruction 4,324,413 4,664,811 Urban Development............................... - 1,696,180

Interest Cost....................................... 513,663 505,881 Total expenses.............................. 22,703,099 29,117,235

Changes in net assets ......................... 13,357,504 8,327,474 Net assets - beginning, as Restated* 126666,401 118,338,927 Net assets - ending ............................. $1 40.023.905 $1 26.666.401

-7-

14,000,000 r' -- '- 12 000000

10,000,000 - 8,000,000 6,000,000 - 4,000,000 2,000,000

- -.

.,

C, / ' i-,,

2 , Q

,

2010 2011

2011 2010

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

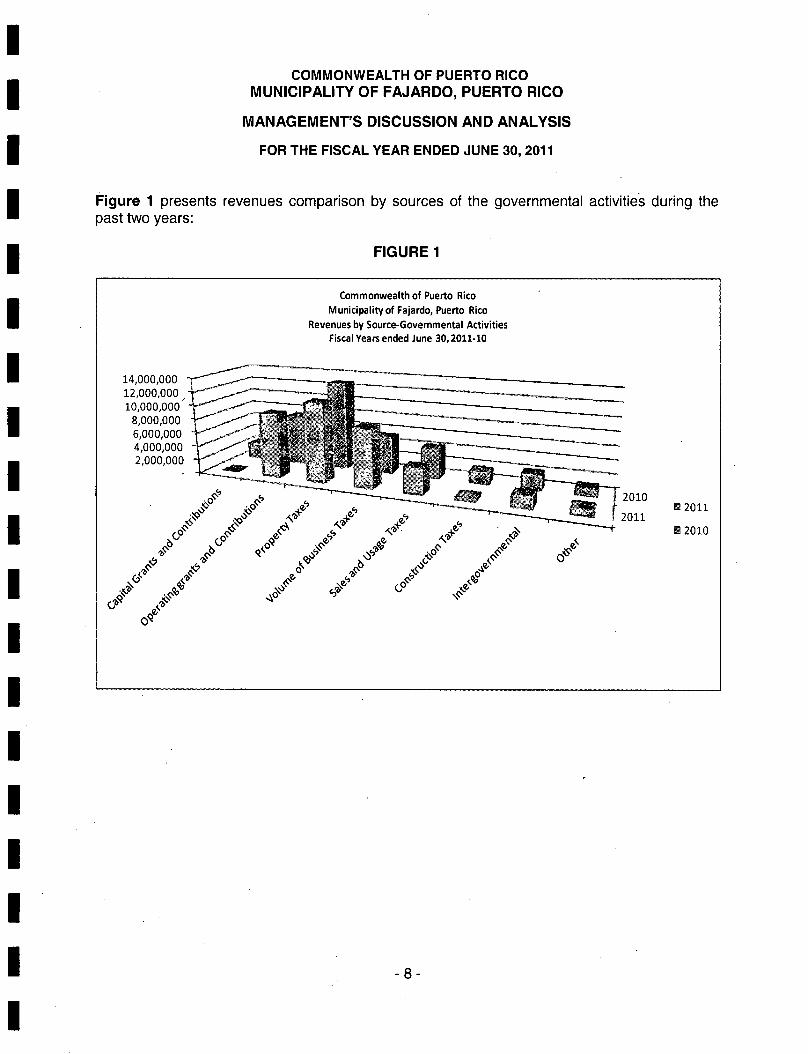

Figure 1 presents revenues comparison by sources of the governmental activities during the past two years:

FIGURE 1

Commonwealth of Puerto Rico Municipality of Fajardo, Puerto Rico

Revenues by Source-Governmental Activities Fiscal Years ended June 30,2011-10

I COMMONWEALTH OF PUERTO RICO

MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Figure 2 presents expenses by function of the governmental activities during the fiscal year 2010-2011:

I FIGURE 2

Commonwealth of Puerto Rico

Municipality of Fajardo, Puerto Rico Expenses by Function

Fiscal Year 2011 (In Dollars)

14,000,000

12,000,000

10,000,000

8,000,000 -

6,000,000 H 4,000,000

77 2,000,000

( 4-

4- 'b q Q qQ / ,

/

(p

Approximately 5% of the Municipality's revenues came from intergovernmental, 32% from property taxes, and 3% from other sources. The Municipality's expenses cover a range of services. The largest expenses are general administration with 52%, public works with 12%, health and sanitation with 1%, public safety with 4%, and human services and welfare with 6%. Program revenues of the Municipality covered 20% of total expenses.

With respect to prior year, revenues decreased by approximately $1,384,106 or 4%, principally on capital grants and contributions, property taxes and construction taxes.

Expenses decreased 22% or $6,414,136 in comparison with 2010 year. Significant increases wereregistered on benefits to employees, and donations and services incurred for the benefit of the community.

I COMMONWEALTH OF PUERTO RICO

MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

I FOR THE FISCAL YEAR ENDED JUNE 30, 2011

I The following table focuses on the cost of each of the Municipality's largest functions/programs as well as each functions/program's net cost (total cost less fees generated by the programs and program—specific intergovernmental aid):

I TABLE 3

Net Cost of Municipality's Governmental Activities Fiscal years ended June 30, Total Cost of Services Net Cost of Services

Functions/Programs 2011 2010 2011 2010

General Administration $11,885,109 13,492,385 $8,775,884 $13,330,213 Public Safety 834,861 954,192 834,861 954,192 Public Works - 2,141,482 - 2,141,482 Culture and Recreation 845,109 1,178,175 845,109 1,178,175 Health and Sanitation 194,315 3,123,128 194,315 Human Services and Welfare 1,302,247 1,361,001 1,302,247 630,881 Urban Development 2,803,382 1,696,180 1,019,779 142,843 Other 4,838,076 505,881 513,663 851,805

$22,703,099 $29,117,235 $13,485,858 $21,162,560

Some of the cost of governmental activities in 2011 was paid by those who directly benefited from the programs and other governments and organizations that subsidized certain programs with grants and contributions The $13,485,858 net cost of services was substantially covered by other general revenues including property, volume of business license taxes and intergovernmental.

FINANCIAL ANALYSIS OF THE MUNICIPALITY'S FUNDS

Governmental Funds

The focus of the Municipality's governmental funds is to provide information on near-term inflows,outflows and balances of resources available for spending. Such information is useful in assessing the Municipality's financing requirements. In particular, unreserved fund balance may serve as a useful measure of a Municipality's net resources available at the end of a fiscal year.

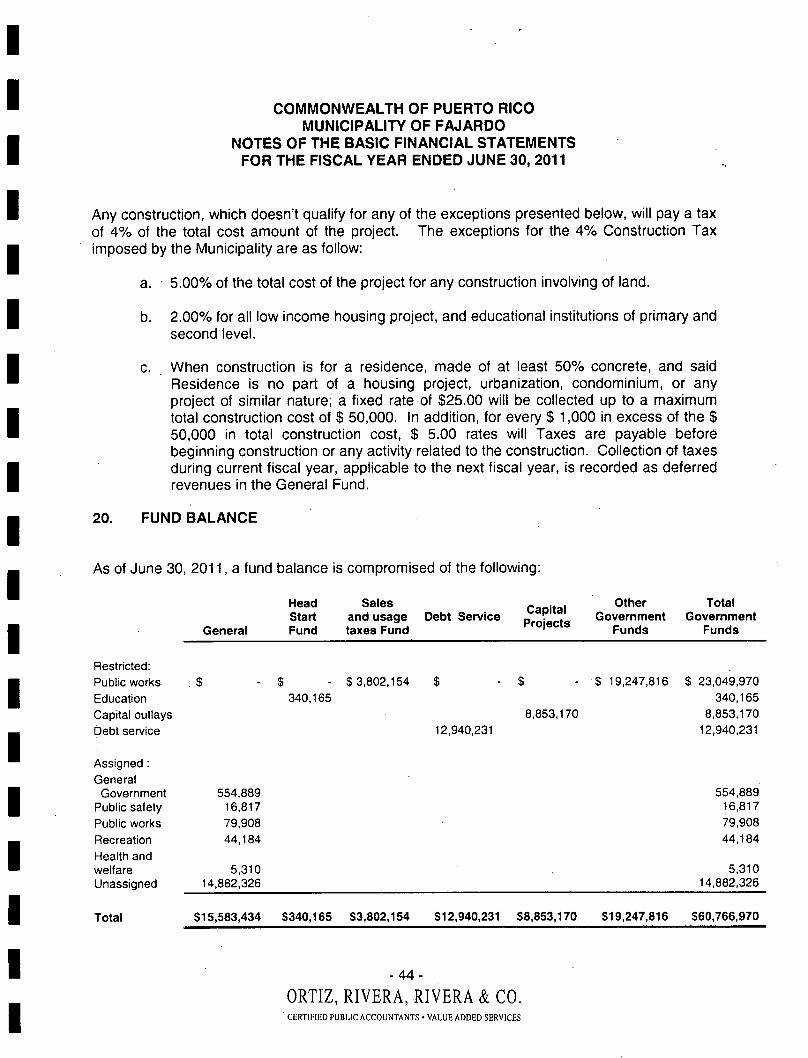

For the Fiscal year ended June 30, 2011, the governmental funds reported combined ending fund balances of $60,766,970, a net increase of $5,967,790 in comparison with the prior year. This increase was caused primarily by a net change in the non-major funds corresponding to the uses of prior years fund balance. Of total combined fund balances, 14,882,326 constitutes unassigned fund balance of general fund which was financed by the used of state assignments fund. The remainder of fund balance is reserved to indicate that is not available for new spending.

- 10-

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

IMANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

I The general fund is the operating fund of the Municipality. Unassigned fund balance of the general fund represents approximately 26% of total ending general fund balance (deficit). For

I the year ended June 30, 2011, the fund balance (deficit) of the general fund increased by $1 ,053,571 when compared with the prior year. The principal component of the net increases is an excess of revenues over expenditures.

GENERAL FUND BUDGETARY HIGHLIGHTS

The general fund original budget for the fiscal period 2010-2011 presented an increase of 5%

Iwith respect to prior year budget. During the fiscal year budget revenues were increased by $731 ,787 due to a revision of original estimate of property taxes and intergovernmental revenues. The Municipality does not included as an amendment to the budget the reduction on

I projected revenues in property taxes and miscellaneous revenues. Budget expenditures were amended during the year in accordance with additional revenues and functions estimates (see Figure 3 below).

FIGURE 3

The negative variance of $3,972,496 between revised budget and actual expenditures was due mainly to reduction in revenue as explained in the preceding paragraph in excess of economies in some functions. The Municipality reported less expenditure than appropriations in those functions for payments to purchase of supplies, professional and nonprofessional services, and solid waste disposal.

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

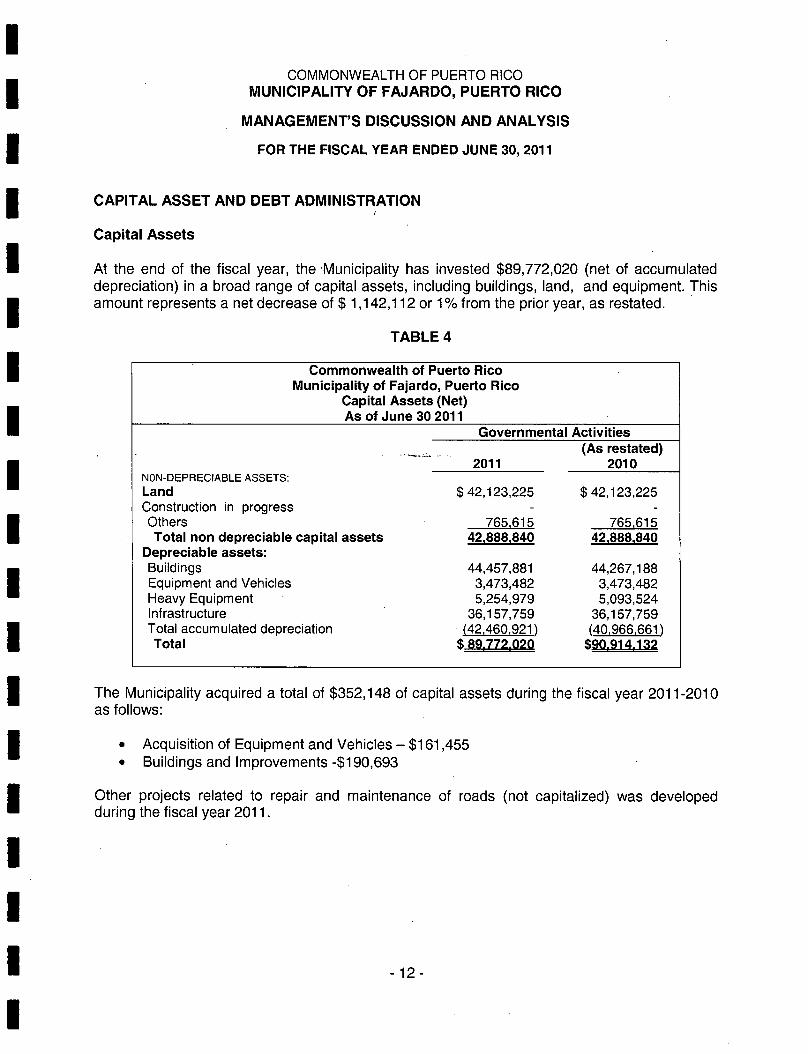

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets

At the end of the fiscal year, the Municipality has invested $89,772,020 (net of accumulated depreciation) in a broad range of capital assets, including buildings, land, and equipment. This amount represents a net decrease of $1,142,112 or 1% from the prior year, as restated.

TABLE 4

Commonwealth of Puerto Rico Municipality of Fajardo, Puerto Rico

Capital Assets (Net) As of June 30 2011

Governmental Activities (As restated)

2011 2010 NON-DEPRECIABLE ASSETS:

Land $42,123,225 $42,123,225 Construction in progress - - Others 765,615 765,615 Total non depreciable capital assets 42,888,840 42,888,840

Depreciable assets: Buildings 44,457,881 44,267,188 Equipment and Vehicles 3,473,482 3,473,482 Heavy Equipment 5,254,979 5,093,524 Infrastructure 36,157,759 36,157,759 Total accumulated depreciation (42,460,921) (40,966,661) Total $_89.772.020 $90,914,132

The Municipality acquired a total of $352,148 of capital assets during the fiscal year 2011-2010 as follows:

Acquisition of Equipment and Vehicles - $161,455 Buildings and Improvements -$190,693

Other projects related to repair and maintenance of roads (not capitalized) was developed during the fiscal year 2011.

- 12-

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Figure 4 below present the components of capital assets during the fiscal years 2011 and 2010:

FIGURE 4

Commonwealth of Puerto Rico

Municipality of Fajardo, Puerto Rico Components of Capital Assets

(In Dollars)

50,000,000

45,000,000

40,000,000

35,000,000

30,000,000

25,000,000

20,000,000

15,000,000

10,000,000

5,000,000

P2011

2010

Land Others Buildings Equipment Heavy Infrastructure

and Vehicles Equipment

Long-Term Debt

At year-end, the Municipality had $18,212,000 in general and special obligation bonds, an decrease of 2.83% with respect to prior year. The following is a summary of the Municipality's outstanding debt as of June 30, 2011 and 2010:

-13-

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

TABLE -5

Commonwealth of Puerto Rico Municipality of Fajardo, Puerto Rico

Outstanding Long-term Dbt AsofJune30 2011

Governmental Activities 2011 2010

General and Special Obligation Bonds $19,348,000 $20,417,000 Property Taxes - 6 Department of Labor and Human Resources 257,634 310,574 LIMS 62,634 159,471 Law 42 200,609 209,569 Others - 101,227 Compensated Absences 1,968,774 3,046,177 Total $21,837,651 $24,244,024

The decrease in the others debts is due to recognition of unemployment benefits. More detailed information about the Municipality's long term liabilities is presented in Note 10 to the financial statements.

Figure 5 presents the components of long-term debts during the fiscal year 2011 and 2010:

FIGURE 5

Commonwealth of Puerto Rico Municipality of Fajardo, Puerto Rico

Outstanding Long-Term Debts (in dollars)

30,000,000

25,000,000

20,000,000

15,000,000

10,000,000

5,000,000

132011

82010

General and Property Department LIMS Law 42 Others Compensated Special Taxes of Labor and Absences

Obligations Human Bonds Resources

-14-

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

MANAGEMENT'S DISCUSSION AND ANALYSIS

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

ECONOMIC FACTORS AND NEXT YEAR'S BUDGET

The Municipality's selected and appointed officials considered many factors when setting the fiscal year 2010-2011 budget. One of these factors is the economy. Among economic areas considered are the population growth estimates, personal income, housing statistics and unemployment rates. The Municipality's unemployment rate now stands at 10.2%, which compares with the Commonwealth rate of 14.1%.

The Municipality applied a conservative approach in development budget estimates. Amounts available for appropriations in the General Fund for the fiscal year 2011 are $19 million, approximately $1,000,000 thousand more than the fiscal year 2011. The Municipality expects an increase in revenues for the next years due to a new sales tax enacted by state legislature and Municipality ordinance during fiscal year 2010-2011. Budgeted expenditures are expected to stabilize accordingly to the projected revenues. Among planned projects, this budget may be adjusted in accordance with economic injection projected when the construction project promoted by the Municipality and others private projects were develop during the year.

CONTACTING THE MUNICIPALITY'S FINANCIAL MANAGEM ENT

I This financial report is designed to provide our citizens, taxpayers, and creditors with a general overview of the Municipality's finances and to demonstrate the Municipality's accountability for the money it receives. If you have questions about this report or need additional information,

I

contact the Municipality's Finance Department at (787) 863-1802 or P0 Box 865, Fajardo, Puerto Rico 00738.

-15-

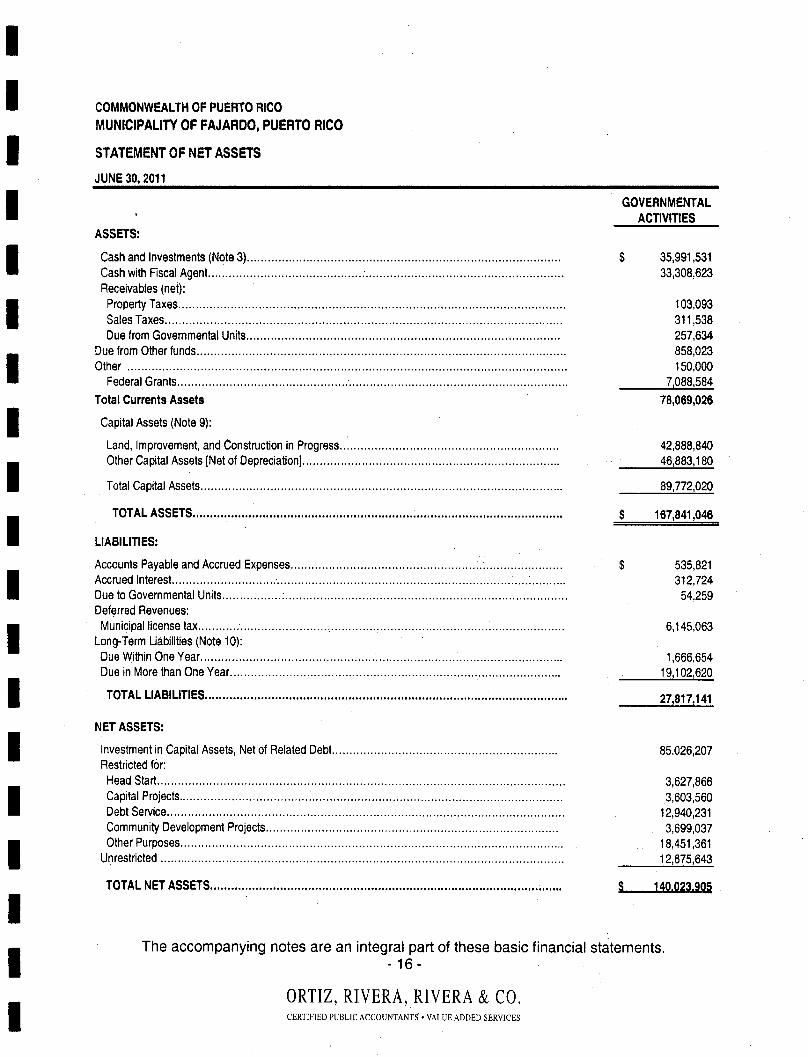

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

STATEMENT OF NET ASSETS

JUNE 30,2011

I GOVERNMENTAL

ACTIVITIES ASSETS:

Cash and Investments (Note 3).......................................................................................... $ 35,991,531 Cash with Fiscal Agent ....................................................................................................... 33,308,623 Receivables (net): Property Taxes............................................................................................................... 103,093

I SalesTaxes.................................................................................................................. 311,538 Due from Governmental Units.......................................................................................... 257,634

858,023 Due from Other funds............ ...... .. .... ........ ....... .. ..... ............................................................ Other..............................................................................................................................

I 150,000

FederalGrants ................................................................................................................ 7,088,584 Total Currents Assets 78,069,026

ICapital Assets (Note 9):

Land, Improvement, and Construction in Progress............................................................... 42,888,840 Other Capital Assets [Net of Depreciation] .......................................................................... ... 46,883,180

I Total Capital Assets .............................................................................................. .... ....... 8,772,020

TOTALASSETS ............... ................................................ . ........................................... $ 167,841,046

I LIABILITIES:

Accounts Payable and Accrued Expenses .............................................................................. . $ 535,821

I Accrued Interest ............................... .................................................................................... 312,724 Due to Governmental Units................................................................................................... 54,259 Deferred Revenues:

Municipal license tax .......................................... . ............................................................... 6,145,063 Long-Term Liabilities (Note 10): I DueWithin One Year........................................................................................................ 1,666,654 Due in More than One Year ............................................................................................... .19,102,620

ITOTAL LIABILITIES ........................................................................................................ 27,817,141

NET ASSETS:

Investment in Capital Assets, Net of Related Debt................................................................. 85,026,207 Restricted for:

3,627,866 Head

I

Start....... .... . ............. ............................................................................................ Capital Projects .............................................................................................................. 3,603,560 DebtService.................................................................................................................. 12,940,231 Community Development Projects.................................................................................... 3,699,037 Other Purposes .............................................................................................................. . 18,451,361

Unrestricted..................................................................................................................... I 12,675,643

TOTALNET ASSETS .....................................................................................................

I

S 140.023.905

The accompanying notes are an integral part of these basic financial statements.

I -16-

ORTIZ, RIVERA, RIVERA & CO. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

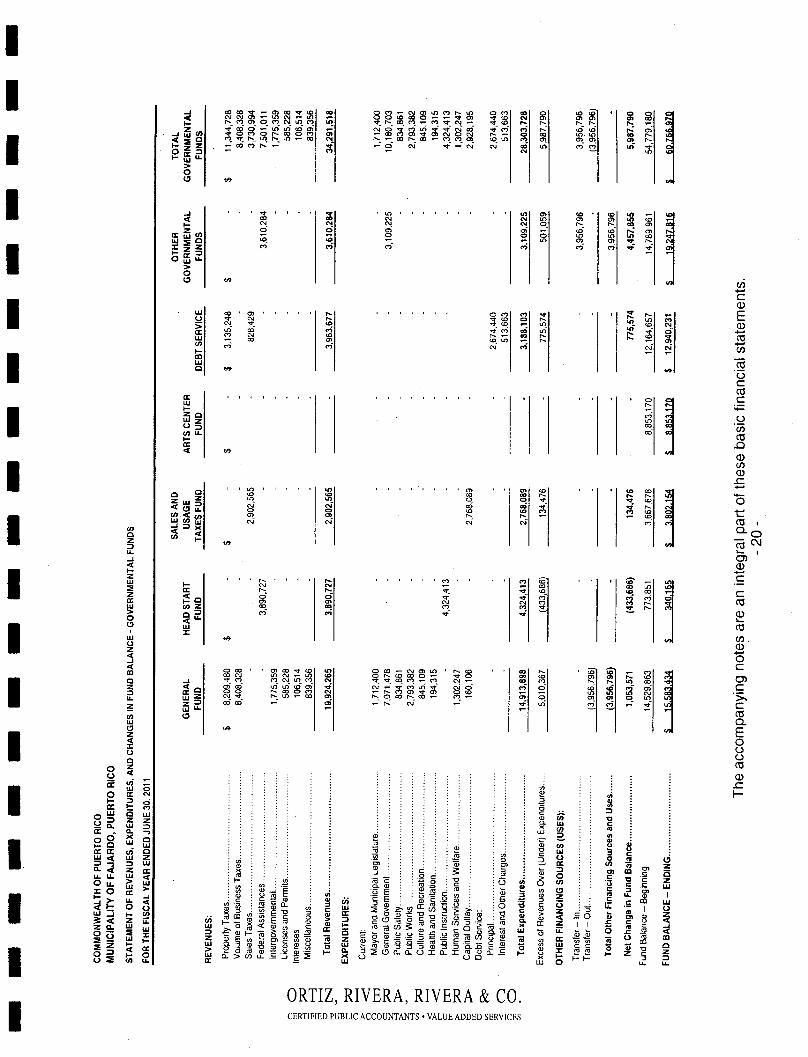

I

CL C LU >

z

I

0 cc C.)

Of I— d cc Cv) LU Lu

z —a. — -71

00 I- a LU — UJ< — Z

LU Q_ pcc u_u. ou_ < Lu

L —J I- __JI— .d I

LU U LU

0() UJ X — I— I—z <

0 1-0 o2 cn u

0

C)COCO

IN Cv) C) I!)

R C

C)C) N ))

co CO —

C) CO CO C)

)

C

CvC'O)J

In 'C)

— U) 0C))

C IN Cv

C L.

Cv

0 N- U Cv)

CO O

Cv C'1 C)

CO Cv) CO Cv) CO C CO IN — IN

U) 1 I I I 1 Cl)

Lt) C) C) C' CO IN C) C' 06 C) CO C'.J

cli cc

U) :

U) O . o E?cii U)

CL

I— ci)ci)

U)

Oci) 55U)c

. :

C) C) — C'J C) U) Cv) N- Cv) 0) ci) U) U) ci) : C) C) CO CO C) — CO

N- COCv)v— Cv)INC 0) S C

ci) ci) U, 0 — IN IN co U) IN > i— p— — C 11)

N- Cv) C) vt C) IN C) T—.--COCO—C)Cv)U) C)

N- 0 C cciOC

Cci . IN C.,. -

U) (L3 —

0

ca

:cci • :

—ci) C.) -

. :OC -- E — > ciC

0.0 CO C c 'E3 E :Cci G)

E ')0) C — Dci) C/)3

C) 0oCOC)C E cicci ) 2 E

ØQ C Io

—

ORTJZ, RIVERA, RIVERA & CO.

CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

(a

0

I o

cn

--J c < LU o

LU cc 00 z I- 0 1 CC I LU w< >

' 0 u_U_ 0 u_

LU >- LU

LU _j in < LU c.i 0. C)

CD 0 Z Lu

(_)

0 N) a)

NJ N)

(C

N) N) 0 0 N) c')NJ ONJ

I- a,IO sqqo. z co

I- Z U)N) <' N-- 0I

N, - 00 co N-

LU IL > 0

(a

_J C,- 100, 0 co cs 0)

0(0 - N--

u20 Z 00

a,- NJ

I- cc O WU 0

(C

LU C)

NJ (0 N) In 0) a) co. q

LUZ cn c,j - N, I_u_ 7t - ca (C LU 0 (C (a

I Ui I- N-

N) I"

cnu_ I- I

0 2 (0

(DU. 0,

U)<U) C

UJUj N)

(1)

0 (0 a,

ON, ONJ

C. 0 N- U)

0 NJ Lq

NJ 0 0) N) N) (0 N- 0 NJ (0 NJ 0) 0 N- NJ 0

NJC0 N- N) U) (0

0 NJ N) 0 *C'J Cq N)

NJ- 10 U)

'9

- N) NJ_ NJ 0

0 -

NJ 0 0 ( U) 0 -

N- NJ a, U) cli

NJ

N-

-

(C

ONJ . 0_N-.

NJ

(ONJ 0 -N)

(a

(C

0 ......

N) 0

li

a,

F-) N, (00) .

(a

. C)

NJ U)

co_ NJ 010 F- NJ

N, a, 0)

NJ 0) 16

IM

(00(0 0 N)0C\J N-(0,-N) 0) N,.-cs (0 000 (0 N- 10 "r

C:,

(0 (0

N NJ N cc

N-

th C w

N, N,

NJ_ 0 cm

0 9l cu U)

J(U 0 C (U

0 0 01 C N- N-

F-) co- N)l 0 U) co a, 0 U) 9 (fl 0 001 (U

I -a 0) U) 0)

• i 0 Ni 0 NJ 0 Nil 01 C, cq

N

1 a co

(CI 0) 0) C a, •

2 a, (01

C 0 (U

I (U

0) 0 C

0 (0NJ O NJ N) C

N-0a,

ca

E 0 0 0 co 0)

I—

• : ,- (0 0 •

• UI C,) Z C

a : C

- c CC : 0 Z -

lu :2a,ja. 0 C C w

(O( .,

-°> •

C C • 0 CQ(5 Z < LLCOC C > 10 (0 C CCC C

0 = - C = - < CC

_oWOECS U) (0> .i Ei

i . -I C0( -2 1

2 Lu

<00 2 ,2 -J -J OIL

-

ORTIZ, RIVERA, RIVERA & Co.

CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

$ 42,888,840

53,186,342

36,157,759 (42,460,921)

1,343,862

3,287,701 1,227,818

6,145,063

257,634

(18,212,000) (1,136,495)

(205,089)

(58,154) (257,634)

(2,907,791)

89,772,020

12,262,078

(22,777,163)

$ 140,023,905

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO, PUERTO RICO

RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET TO THE STATEMENT OF NET ASSETS

JUNE 30, 2011

Total Fund Balances - Government Funds ....................................... . ................................. S 60,766,970

Amount reported for Governmental Activities in the Statement of Net Assets

are different because:

I Capital assets used in governmental activities are not financial resources and therefore

are not reported in the funds. In the current period, these amounts are:

I. Non Depreciable Capital Assets..........................................................................

Depreciable Capital Assets.....................................................................................

Infrastructure Assets.............................................................................................. Accumulated Depreciation......................................................................................

ITotal Capital Assets.......................................................................................

Some of the Municipalitys revenues will be collected after year-end but are not available

soon enough to pay for the current period's expenditures and therefore are deferred in the funds:

I CDBG ................................................................................................................. HeadStart Program ...............................................................................................

Otherfunds...........................................................................................................

I Municipal License Tax...........................................................................................

ChristmasBonus.................................................................................................. Total...........................................................................................................

I .Some liabilities are not due and payable in the current period and therefore are not reported in the funds. Those liabilities consist of:

I General Bonds and Special Bonds........................................................................... General Bonds and Special Bonds Interest................................................................. LawNumber 42-MRCC ...........................................................................................

MACCLiquidation..................................................................................................

I Christmas Bonus.................................................................................................

Compensated Absences.....................................................................................

Total Long-Term Liabilities...............................................................................

Total Net Assets of Governmental Activities ........................................................................

I The accompanying notes are an integral part of these basic financial statements.

-19-

I ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS VALUE ADDED SERVICES

I

00 0) (0 (01 (0 I I—

_J Lu (nl 40I

l 6(11 C

L'i

U).01 I)

Lu

>1 01

I I

_j I 41

......i (0 1co 'NI 1

ItcflI uJ0I

101

I ZZ

Lu I I >1 II 01 I I

IA II

uji 00) •••••1 NI

> It Ui1

N ICI

(01

In ! (0 at i—I IflI

I I Ic'1

I WI CI

I IA I

I I

It I (Li I I

I I I I

U,LI.I I I 1- I It I I

IA I

0 C).- 6(40)U) C') N U) 0 C) I (01 0) I 0 .- 0) 101 CM 1 'c'I C)I NI

611 0 ('4 N 01 01

r"t — C. cli a 0U)lc')IC)1

.0 ('I C(4 CM (01(4)1

1•1

U) • In C) U)

N CM 0

0) 0.-

0 0 0 U)

0(P) C., 10 0 N (0 U) N.- (0 N N

0 0)0) 0) 0 ID C-N (0(0 N C) (4)14) (0 N 0)0) 01 C-

(0 • (0 (4) C) 0) (4) (0 C- N 0•01 10 10 N C) (4) 4) 14) CC C) 0) ' N

Cl

-W

I

-It

• • N N - (0 CM

N 0,

C_(4 CM

U,

• 0 N

(4) 10 (0

10 u,I I lot Z ZIU I (01 ICUI LL 6•4 0 10)1 04U)I

WU,wI (3i c'1

0,1 16(11

Cfl IA I

• 0' (0 (41 (0 0 N (0 6 - (0 N (0

N CM CM

10 (0 N N

N (0

N ,

0 C') C,) ci CflZ

0 CU 1') C') J N C,, 4 1L.

LU Z

IA

00 0) (0 (0 (0 0 (0 ('4 C) U) • N 10 (0 C-

- (0 0) (00) (4) CC) C'.NUC' 10

N

0 N (000'- 0

'- C". N 0) (0 1') 0)1

NINI 0)1 N (0

4 0) (0 (OU'(00) C'4 C') U) CM 0 C') WZ ('4'1 N0 0 N° 0 N0 '- C".'- O)J 0) 0 U) z C) '- N CM ,- —

I

0)

Lu

I CC 2.

• O0U)

111 (4 ,_ ( C u.

Lu

(41 o I— It I I £

flilflfl HQH ij U I I j

ORTIZ, RIVERA, RIVERA & CO.

CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNiCIPALITY OF FMARDO, PUERTO RICO

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES, AND CHANGES IN FUND BALANCE OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTiVITIES

FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Net Change in Fund Balances - Gomment Funds ............................................................ $5,987,790

Amount reported for GoemmentaI Actities in the Statement of Actifties are different because:

Go'emmentaI funds report capital outlays as expenditures. Howe'er, in the Statement of Activities the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. In the current period, these amounts are:

Capital Assets ................................................................................................. $2,928,195 Depreciation Expense........................................................................................ (1,494,260)

Excess of Capital Assets over Depreciation Expense ........................................... 1433,935

Revenues in the Statement of Activities that do not provide current financial resources are reported as revenues in the funds:

Head Start Program........................................................................................... 3,080,013

Repayment of long-term principal is expenditure in the governmental funds, but issuing debt reduced Long-Term Liabilities in the Statement of Net Assets. In the current period repaymentswere...................................................................................................... . 2,674,440

Some expenses reported in the Statement of Activities do not require the use of current financial resouces and therefore are not reported as expenditures in governmental funds. These activities consist of:

ChristmasBonus.............................................................................................. 42,940 Decrease in Compensated Absences. .................................................................. 138,386 Total Additional Expenses.................................................................................. 181,326

Change in Net Assets of Governmental Activities .................................................................. $ 13,357,504

The accompanying notes are an integral part of these basic financial statements. - 21 -

ORTIZ, RIVERA, RIVERA & CO. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTESOF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

FINANCIAL REPORTING ENTITY

ORGANIZATION

The Municipality of Fajardo, Puerto Rico (Municipality) was founded in the year 1775, and

I

operates as a governmental unit of the Commonwealth of Puerto Rico, under the Law Number 81 of August 30, 1991, known as "Autonomy Municipalities Law of the Commonwealth of Puerto Rico". The governmental system of the Municipality is composed of the executive and

I

legislative bodies. The Mayor is the Chief Executive Officer and is elected every four years in the general elections of the Commonwealth of Puerto Rico. The legislative body consists of 14 Legislators also elected in the general elections of Puerto Rico for a four-year period.

I The Municipality provides services such as: health, public works, sanitation, aids and services to low-income and elderly citizens, public safety, housing and urban development, culture and recreation, planning, zoning and other general and administrative services.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accounting policies of the Municipality conform to accounting principles generally accepted in the United States of America as applicable to governmental units. The following is a summary of the more significant of such policies.

The accompanying basic financial statements of the Municipality have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP) as prescribed by the Governmental Accounting Standards Board (GASB). The GASB is thestandard -setting body for governmental accounting and financial reporting. The GASB periodically updates its codification of the existing Governmental Accounting and Financial Reporting Standards which, along with subsequent GASB pronouncements (Statements and Interpretations) constitutes GAAP for governmental units.

In June 1999, the GASB issued Statement Number 34, Basic Financial Statements-and Management's Discussion and Analysis-for State and Local Governments. This statement establishes new financial reporting requirements for state and local governments. The Municipality adopted the provisions of GASBS No. 34 as well as other statements referred to below as of July 1, 2002. They require new information and restructure much of the information that governments have presented in the past.

With the implementation of GASBS No. 34, the Municipality has prepared required supplementary information titled Management's Discussion and Analysis, which precedes the basic financial statements.

I The accompanying basic financial statements present the financial position and the results of operations of the Municipality and its various funds and fund types, and the cash flows of the proprietary funds. The basic financial statements are presented as of June 30, 2011, and for the

I -22-

I

ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTES OF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

fiscal year then ended. The more significant of these accounting policies are described below and, where appropriate, subsequent pronouncements will be referenced.

Financial Reporting Entity

The accompanying basic financial statements include all departments and organizations units whose funds are under the custody and control of the Municipality. In evaluating the Municipality as a reporting entity, management has addressed all the potential component units. The decision to include a potential component unit in the reporting entity was made by applying the provisions of GASBS No. 14.

The basic criteria for including a potential component unit within the reporting entity is if potential component units are financially accountable and other organizations for which the nature and significance of their relationship with the entity are such that exclusion would cause the Municipality's financial statements to be misleading or incomplete. The GASB has set forth criteria to be considered in determining financial accountability. These criteria include appointing a voting majority of an organization's governing body and (1) ability of the Municipality to impose its will on that organization or (2) the potential for the organization to provide specific 'nancial benefits to, or impose specific financial burdens on the Municipality.

The relative importance of each criterion must be evaluated in light of specific circumstances in order to determine which components units are to be included as part of the reporting entity. Our specific evaluations of the criteria applicable to the Municipality indicate no organizations meet the criteria to be included as component units. Accordingly, theses basic financial statements present only the Municipality as the reporting entity.

These financial statements present the respective financial position of the governmental activities, each major fund, and the aggregate remaining fund information of the Municipality, as of June 30, 2011, and the respective changes in financial position, where applicable, thereof for the fiscal year then ended.

Measurement Focus and Basis of Accounting

Government-wide Financial Statements

The government-wide financial statements (the Statement of Net Assets and the Statement of Activities) are reported using the economic resources measurement focus and the accrual basis of accounting. Revenue is recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Grant and similar items are recognized as revenue as soon as all eligibility requirements have been met.

Governmental Fund Financial Statements

The governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recorded when

- 23 -

0RTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTESOF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

susceptible to accrual; as soon as it is both measurable and available. "Available" means collectible within the current period or soon enough thereafter, normally within sixty (60) days, to beused to pay liabilities of the current period. Expenditures are generally recognized when the related liability is incurred.

The exception to this general rule is the principal and interest on general obligation long-term debt and compensated absences, if any, are recognized when due.

In applying the 'susceptible to accrual" concept to intergovernmental revenues (federal grants) pursuant to GASBS No. 33, Accounting and Financial Reporting for Non exchange Transactions (the Municipality may act as either provider or recipient), the provider should recognize liabilities and expenses and the recipient should recognize receivables and revenue when the applicableeligibility requirements including time requirements, are met. Resources transmitted before the eligibility requirements are met should, under most circumstances, be reported as advances by the provider and deferred revenue by the recipient.

There are essentially two types of revenue. For the majority of grants, moneys must be expended by the Municipality on the specific purpose or project before any amounts will be reimbursed. Revenue is, therefore, recognized as expenditures are incurred to the extent available. For the other revenue, moneys are virtually unrestricted and are generally revocable only for failure to comply with prescribed compliance requirements. These resources are reflected as revenue at the time of receipt or earlier if the susceptible to accrual criteria is met. Expenditures are generally recorded when a liability is incurred, as under accrual accounting. Modifications to the accrual basis of accounting include the following:

I . Employee's vested annual vacation and sick leave is recorded as expenditure when

utilized. The amount of accumulated annual vacation and sick leave unpaid at June 30, 2011, has been reported only in the government-wide financial statements.

I C. Financial Statement Presentation

I

The basic financial statements include both government-wide (based on the Municipality as a whole) and fund financial statements. While the previous financial reporting model emphasized fund types (the total of all funds of a particular type), in the new financial model the focus is on

I

either the Municipality as a whole, or major individual funds (within the basic financial statements). Both the government-wide and fund financial statements (within the basic financial statements) categorize primary activities as either governmental or business type.

I Government-wide Financial Statements

The government-wide financial statements (the Statement of Net Assets and the Statement of

I Activities) report information of all the activities of the Municipality. For most part, the effect of interfund activity has been removed from these government-wide financial statements. Governmental activities, which normally are supported by taxes and intergovernmental

I -24-

ORTIZ, RIVERA, RIVERA & Co.

I CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTESOF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

revenues, are reported separately fro business-type activities, which rely to a significant extent on fees and charges for support.

U The focus of the Statement of Net Assets is designed to be similar to bottom line results for the Municipality and its governmental activities. This statement, for the first time, combines and consolidates governmental fund's current financial resources (short-term expendable resources) with capital assets and long-term obligations.

The Statement of Net Assets presents the reporting entities' assets and liabilities, with the

I difference reported as net assets. Net assets are reported in three categories:

Invested in Capital Assets, Net of Related Debt - These consists of capital assets, net of

I

accumulated depreciation and amortization and reduced by outstanding balances for bonds, notes, and other debt that are attributed to the acquisition, construction, or improvement of those assets.

I • Restricted Net Assets - These result when constraints placed on net assets use are either externally imposed by creditors, grantors, contributors, and the like, or imposed by law

I through constitutional provisions or enabling legislation.

Unrestricted Net Assets - These consist of net assets which do not meet thedefinition of

I the two preceding categories. Unrestricted net assets often are designated, to indicate that management does not consider them to be available for general operations. Unrestricted net assets often have constraints on resources that are imposed by management, but can be

Iremoved or modified.

When both restricted and unrestricted resources are available for use, generally it is the Municipality's policy to use restricted resources first, then the unrestricted resources as they

I are needed.

The Statement of Activities is focused on both the gross and net costs per functional category.

I

The statement reduces gross expenses (including depreciation) by related program revenues, operating and capital grants. This is intended to summarize and simplify the user's analysis of cost of various governmental services.

I Governmental Fund Financial Statements

The fund financial statements (the Balance Sheet, the Statement of Revenues,

I Expenditures, and Changes in Fund Balances, the Statement of Net Assets) are, in substance, very similar to the financial statements presented in the previous financial reporting model. Emphasis here is on the major funds in the governmental category. Non-major funds are

I summarized into a single column.

I -25-

I ORTIZ, RIVERA, RIVERA & CO. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTESOF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Traditional users of governmental financial statements will find the Fund Financial Statements presentation more familiar. The focus is on Major Funds, rather than the previous financial

I model's fund types. The Governmental Major Fund Statements are presented on current financial resources and modified accrual basis of accounting. This is the manner in which these funds are normally budgeted. This presentation deemed most appropriate to (a) demonstrate

I

legal and covenant compliance, (b) demonstrate the source and use of liquid resources, and (c) demonstrate how the Municipality's actual experience conforms to the budgeted fiscal plan.

Since the governmental fund statements are presented in different measurement focus and basis of accounting than the government-wide statements, reconciliation is presented and separate explanation for each differences.

I The Municipality reports its financial position (Balance Sheet) and results of operations (Statement of Revenues, Expenditures and Changes in Fund Balance) in funds, which are considered separate accounting entities. The operations of each fund are accounted for within a

I set of self-balancing accounts. Fund accounting segregates funds according to their intended purpose and is used to aid management in demonstrating compliance with legal, financial, and contractual provisions.

I The model as defined in GASBS No. 34 established criteria (percentage of the assets, liabilities, revenues, or expenditures/expenses of either fund category in the governmental fund) for the determination of major funds. The non-major funds are combined in a single column in the fund

I financial statements. The Municipality reports the following major fund:

General Fund - This is the general operating fund of the Municipality. It is used to

I account for all financial resources, except those required to be accounted for in another fund.

I Head Start Fund - This is the fund used to account for all transactions of the Head Start Program. The objectives to this program are to provide comprehensive health, educational, nutritional, social and other developmental services primarily to

I economically-disadvantaged pre-school children and infants and toddlers so that the children will attain school readiness.

Sales and Usage Taxes Fund-This fund used to account for accumulation of resources for,

I and the payment of special purpose obligations.

IArts Center Fund- This is used to account for construction of an Arts center.

Debt Service Fund - This is used to account for the accumulation of resources for, and the payment of long-term debt principal and interests

I CDBG Fund - This is the fund used to account for all the transactions of the Community Development Block Grant Program. The primarily objectives of this program is to

I development of viable communities by providing decent housing, a suitable living

-26-

I

ORTIZ, RIVERA, RIVERA & CO. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTES OF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

development of viable communities by providing decent housing, a suitable living environment and expanded economic opportunities, principally for persons of low and moderate income.

D. Budgetary Data

The Municipality's annually adopts the Budget Resolution for all operating funds of the Municipality except for certain restricted accounts of Proprietary Funds and Special Revenue Funds. Budgetary control is legally maintained at the fund level. The budget is prepared using the modified accrual basis of accounting with encumbrance included as budgetary basis expenditures. The Municipality's Budget Resolution provides transfer authority (1) to the Mayor and the Management and Budget Director, within and between departments and funds, as long as the total budget of the Municipality (net of inter-fund transfers) is not increased; (2) to the Management and Budget Director to implement grant budgets as the grant applications are accepted by the Municipality; and (3) to the Management and Budget Director to amend (re-appropriate) each new year's budget, to the extent of outstanding encumbrances, and/or unexpended project/grant appropriations at year end. Municipality's Legislature action is required for (1) use of the budgeted Legislature contingency, and (2) the approval of a supplemental appropriation(s). During the year, several supplemental appropriations were necessary.

The budget columns (original and final budgets) of the Budgetary Comparison - General Fund reflect the original budget and the amended budget (which have been adjusted for legally authorized revisions of the annual budgets during the year). Appropriations, except remaining project appropriations, encumbrances, and unexpended grant appropriations, lapse at the end of each fiscal year.

Amendments to the budget, including transfers, require the approval of the Municipal

I Legislature. Unencumbered appropriations lapse at the end of the next fiscal year. The Municipality follows these procedures, in accordance with law, in order to establish the budgetary data reflected in the basic financial statements:

Prior of May 15 of each fiscal year, the Mayor submits to the Municipal Legislature a proposed budget for the fiscal year commencing the following July 1 in addition of a

Ibudget message.

The budget document is available for public inspection prior to its approval by the

IMunicipal Legislature.

The Commissioner of Municipal Affairs examines the budget to verify if it complied with the law's standards and sends it to the Mayor for any comments or recommendation

I before the limited date establishes by the Law.

Prior to June 13, the annual budget is legally enacted through passage of the annual

U appropriation ordinance.

- 27 -

I ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTES OF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

If a budget is not adopted prior to the end of the end of the fiscal year, the annual budget for the preceding fiscal year, as approved by the Municipal Legislature and the Mayor, is automatically renewed for the ensuing fiscal year until a new budget is approved. This permits the Municipality to continue making payments for its operating and other expenses until the new budget is approved.

Subsequent to the enactment of the annual appropriation ordinance, the Municipal Legislature has the authority to make necessary amendments made during the fiscal year and are reflected in the budget information included in the Budgetary Comparison Schedule - General Fund.

I 7. Budgetary data for the Special Revenue Fund has not been presented in the

accompanying basic financial statements as such funds are budgeted over the life of the respective grant or project and not on an annual basis.

I Since the budgetary basis differs from accounting principles generally accepted in the United States of America (GAAP), actual amounts for the General Fund in the accompanying

I

Budgetary Comparison Schedule, is presented on the budgetary basis to enhance comparability.

The principal differences between the budgetary and GAAP bases are the following:

Encumbrances are recorded as expenditures under the budgetary basis and as a

Ireserve of fund balances under GAAP.

The non-exonerated portion of the property tax advances are presented as revenue in the budgetary basis and as other financing sources under GAAP.

Inter-fund transactions of the General and Special Revenue Funds are not included in the budgetary basis.

Certain accrued liabilities and other debts are not included in the budgetary basis.

Certain revenues susceptible to accrual, i.e., both measurable and available, are not included in the budgetary data.

All encumbrance appropriations in the operating budget lapse at the end of the fiscal year. Property taxes collected during the current year by the Municipal Revenue Collection Center (Fiscal Agent) are presented as revenues in the accounting basis but are not considered in the

I

budgetary schedule.

The special funds of the Special Revenue Fund have not been included in the budgetary comparison because balances are not budgeted. Also the budget prepared for the Federal

I Finance Awards Programs included in the Capital Projects and Special Revenue Funds is

- 28 -

I

ORTIZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTES OF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

based on a program period which is not necessarily a year. Accordingly, it's not practical to present an annual comparison of budget for such programs.

E. Cash, Cash Equivalent, and Investment

Under Puerto Rico statutes, public funds deposited in commercial banks must be fully collateralized for the amount deposited in excess of federal depository insurance. All securities pledged as collateral are held by the Secretary of the Treasury of Puerto Rico. In addition, the Municipality maintains deposits with the Government Development Bank for Puerto Rico (GDB). The Municipality's bank balances in commercial banks of approximately $14.3 million in the general fund were fully collateralized at June 30, 2011. The deposits at GOB of approximately $5.6 million that are restricted principally for capital projects, and the $4.1 million in the debt service fund are unsecured and uncollateralized, as no collateral is required to be carried by governmental banks. The excess is covered by collateral provided by banks and held by the Treasury Department of the Commonwealth of Puerto Rico pursuant to applicable laws and regulations.

F.. Receivable

Receivable are stated nets of estimated allowances for uncollectible accounts, which are determined upon past collection experience and current economic conditions. Receivable from Federal Government represents amounts owed to the Municipality for reimbursement of expenditures incurred pursuant to federally funded programs.

Inventories

The General, Special Revenue and Capital Project Funds, purchases office and printing supplies, gasoline, oil and other expendable supplies held for consumption. The cost of purchases is recorded as expenditure in the appropriate fund and the inventory is not recorded in the basic financial statements.

Capital Assets

Property, plant and equipment purchased or acquired is carried at historical cost or estimated historical cost. Contributed assets are recorded at fair market value as of the date received. The Municipality's capitalization levels are $500 on personal property. For improvements other than buildings, the capital outlay must be greater than $10,000, extend the estimated useful life for ten years, and be greater than 10% of the original cost of the asset. Other costs incurred for repairs and maintenance is expensed as incurred.

- 29 -

ORTJZ, RIVERA, RIVERA & Co. CERTIFIED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTES OF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Depreciation on all assets is provided on the straight-line basis over the following estimated useful lives:

CAPITAL ASSETS

YEARS

I

Buildings 70 Improvement Other than Buildings 70 Infrastructure 10-70 Motor Vehicles 5

I Machinery and Equipments 5-10

II. Compensated Absences

The Municipality accrues accumulated unpaid vacation and sick leave and associated employee- related costs when earned (or estimated to be earned) by the employee. The

I Municipality's employees are granted 30 days of vacations and 18 days of sick leave annually. Vacations may be accumulated up to a maximum of sixty (60) days and sick leave up to a maximum of ninety (90) days. In the event of employee resignation, the employee is paid for

I

accumulated vacation days up to the maximum allowed. Separation from employment prior to use of all or part of the sick leave terminates all rights for compensation, except for employees with ten years of service who are entitled to sick leave pay up to the maximum allowed. The

IMunicipality accrued a liability for compensated absences, which meet the following criteria:

The Municipality's obligation relating to employee's rights to receive compensation for

Ifuture absences is attributable to employee's services already rendered.

The obligation relates to rights that vest or accumulate.

I 3. Payment of the compensation is probable.

4. The amount can be reasonably estimated.

I In accordance with the above criteria and requirements as established by GASBS No. 16; the Municipality has accrued a liability for compensated absences, which has been earned but not

I

taken by Municipality's employees. For the government-wide statements, the current portion is the amount estimated to be used in the following year. For the governmental funds statements, all of the compensated absences are considered long-term and therefore, are not a fund liability

Iand represents a reconciling item between the fund level and government-wide presentations.

J. Insurance

I The Municipality has insurance coverage for its public facilities, primarily to provide protection from catastrophic losses. Also, principal officials of the Municipality are covered under various surety bonds. The Secretary of the Treasury Department of the Commonwealth of Puerto Rico

I is the agent commissioned to place all of the Municipality's insurance coverage.

- 30 -

I

ORTIZ, RIVERA, RIVERA & CO. CERTIFIED PUBLIC ACCOUNTANTS • \'ALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTES OF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Corresponding premiums payable are withheld by the Municipal Revenue Collection Center from quarterly advances of annual property tax and subsidy send to the Municipality.

Inter-fund Transactions

Inter-fund transactions are reflected as loans, reimbursements or transfers. Loans are reported as receivables and payables as appropriate and are subject to elimination upon consolidation. Reimbursements occur when one fund incurs a cost, charges the appropriate benefiting fund and reduces its related cost as a reimbursement. All other inter-fund transactions are treated as transfers. Transfers between governmental or proprietary funds are netted as part of the reconciliation to the government-wide columnar presentation. The Municipality has the following types of transactions among funds:

Inter-fund Transfers - Legally required transfers that are reported when incurred as transfers-in by the recipient fund and as transfers-out by the disbursing fund, with receivables and payables presented as amounts due to and due from other funds. Advances between funds are also presented as amounts due to and due from other funds. However, these transfers and related amounts receivables and payables are considered internal balances and activities that have been eliminated in the government-wide financial statements.

Fund Balances

In the current year, the Municipality adopted the provisions of GASB Statement No. 54, Fund Balance Reporting and Governmental Fund Type Definitions (GASB No. 54), which enhanced the usefulness of fund balance information by providing clearer fund balance classifications that can be more consistently applied. This statement establishes fund balance classifications that comprise a hierarchy based primarily on the extent to which the Municipality is bound to observe constraints imposed upon the use of the resources reported in governmental funds.

Pursuant to the provisions of GASB No. 54, the accompanying fund financial statements report fund balance amounts that are considered nonspendable, such as fund balance associated with inventories. Other fund balances have been reported as restricted, committed, assigned, and unassigned, based on the relative strength of the constraints that control how specific amounts can be spent, as described as follows:

Nonspendable - Represent resources that cannot be spent readily with cash or are legally or contractually required not be spent, including but not limited to inventories, prepaid items, and long term balances of interfund loans and accounts receivable.

2. Restricted - Represent resources that can be spent only for the specific purposes stipulated by constitutional provisions, external resource providers (externally imposed by creditors or grantors), or through enabling legislation (that is, legislation that creates a new revenue source and restricts its use). Effectively, restrictions may be changed or lifted only with the consent of resource providers.

- 31 -

ORTIZ, RIVERA, RIVERA & Co. CERTIFJED PUBLIC ACCOUNTANTS • VALUE ADDED SERVICES

COMMONWEALTH OF PUERTO RICO MUNICIPALITY OF FAJARDO

NOTES OF THE BASIC FINANCIAL STATEMENTS FOR THE FISCAL YEAR ENDED JUNE 30, 2011

Committed - Represent resources used for specific purposes, imposed by formal action of the Municipal's highest level of decision making authority (Municipal Legislature through resolutions and ordinances) and can only be changed by a similar law, ordinance or resolution, no later than the end of fiscal year.

Assigned - Represent resources intended to be used by the Municipality for specific purposes but do not meet the criteria to be classified as restricted or committed (generally executive orders approved by the Mayor). Intent can be expressed by the Municipal Legislature, the Mayor or by an official or body to which the Municipal Legislature delegates authority in conformity with the Autonomous Municipalities Act of Puerto Rico, as amended. In governmental funds other than the general fund, assigned fund balance represents the remaining amount that is not restricted or committed.

Unassigned - Represent the residual classification for the Municipality's general fund and includes all spendable amounts not contained in the other classifications. In other funds, the unassigned classification is used only to report a deficit balance resulting from overspending for specific purposes for which amounts had been restricted, committed, or assigned.