Embed Size (px)

Citation preview

THE CITY OF NEW YORKOFFICE OF THE COMPTROLLER

September 20, 2017

COMMON INVESTMENT MEETINGPublic Session

QUARTERLY PERFORMANCE OVERVIEWQ2 2017

Asset Class IndexSecond

Quarter 2017Fiscal Year To

Date 3 Year 5 Year Expected*

Equities - U.S. Russell 3000 3.0% 18.5% 9.1% 14.6% 7.8%Equities - Developed Intl MSCI EAFE 6.1% 20.3% 1.2% 8.7% 8.9%Equities - Emerging Intl MSCI EMF 6.3% 23.8% 1.1% 4.0% 11.0%Debt - US Govt Long Duration Citigroup Treasury 10+ 4.0% -7.4% 5.7% 2.8%Debt - US Government NYC Treas/Agency +5 2.3% -4.6% 3.6% 2.0% 2.8%Debt - Investment Grade NYC IG Credit 2.3% 1.9% 3.4% 3.7% 3.4%Debt - High Yield Citigroup BB & B 2.1% 11.5% 4.1% 6.2% 6.1%

Market Returns: Q2-2017

Source: State Street

*Average of consultant long-term arithmetic expected returns, as of 2016

3

U.S. Equities FY Ending 6/17

Asset Class Benchmark Index

U.S. Equities 18.5% Russell 3000

Asset Class Benchmark Index

Small Cap 24.6% Russell 2000Mid Cap 18.6% S&P 400Large Cap 18.0% Russell 1000Russell 3000 Value 16.2% Russell 3000 ValueRussell 3000 Growth 20.7% Russell 3000 Growth

Top 2 Sectors 1 Year Return IndexFinancials 41.6% S&P 500Information Technology 38.4% S&P 500

Bottom 2 Sectors 1 Year Return IndexEnergy -1.6% S&P 500Telecommunication Services -10.9% S&P 500

Source: State Street

4

International Equities FY Ending 6/17

Asset Class Benchmark Index

International Equities 20.3% MSCI EAFE

Top 2 Countries 1 Year Return ($) 1 Yr Return (Local Currency) Weight

Austria 64.95% 60.7% 0.24%

Spain 38.39% 34.8% 3.42%

Bottom 2 Countries 1 Year Return ($) 1 Yr Return (Local Currency) Weight

Israel -2.32% -5.97% 0.69%

Belgium 2.08% -0.57% 1.14%

Top 3 Weighted Countries 1 Year Return ($) 1 Yr Return (Local Currency) Weight

Japan 19.18% 30.53% 23.44%

U.K. 13.35% 16.65% 15.76%

France 28.14% 24.82% 10.24%

Source: MSCI

5

Emerging Markets Equities FY Ending 6/17

Asset Class Benchmark Index

Emerging Markets Eq 23.7% MSCI EM

Top 2 Countries 1 Year Return ($) 1 Yr Return (Local Currency) Weight

Greece 50.41% 46.50% 0.39%

Hungary 44.43% 37.75% 0.33%

Bottom 2 Countries 1 Year Return ($) 1 Yr Return (Local Currency) Weight

Philippines -6.18% 0.63% 1.18%

Qatar -2.29% -1.78% 0.67%

Top 3 Weighted Countries 1 Year Return ($) 1 Yr Return (Local Currency) Weight

China 32.19% 32.81% 23.73%

South Korea 34.88% 33.98% 15.61%

Taiwan 32.85% 25.28% 12.48%

Source: MSCI

6

Core Fixed Income FY Ending 6/17

Asset Class Benchmark Index

Core Fixed Income -0.21% Core Plus Five

Government Return Index

Short Duration (1-3 years) -0.09% Citigroup USBIG Treasury 1-3 YearIntermediate Duration (1-10 years) -1.25% Citigroup USBIG Treasury/Agency 1-10 YearLong Duration (10+ years) -7.41% Citigroup Treasury 10+Investment Grade 1.90% NYC - Investment Grade CreditMortgage -0.09% Citigroup Mortgage Index

Source: State Street

7

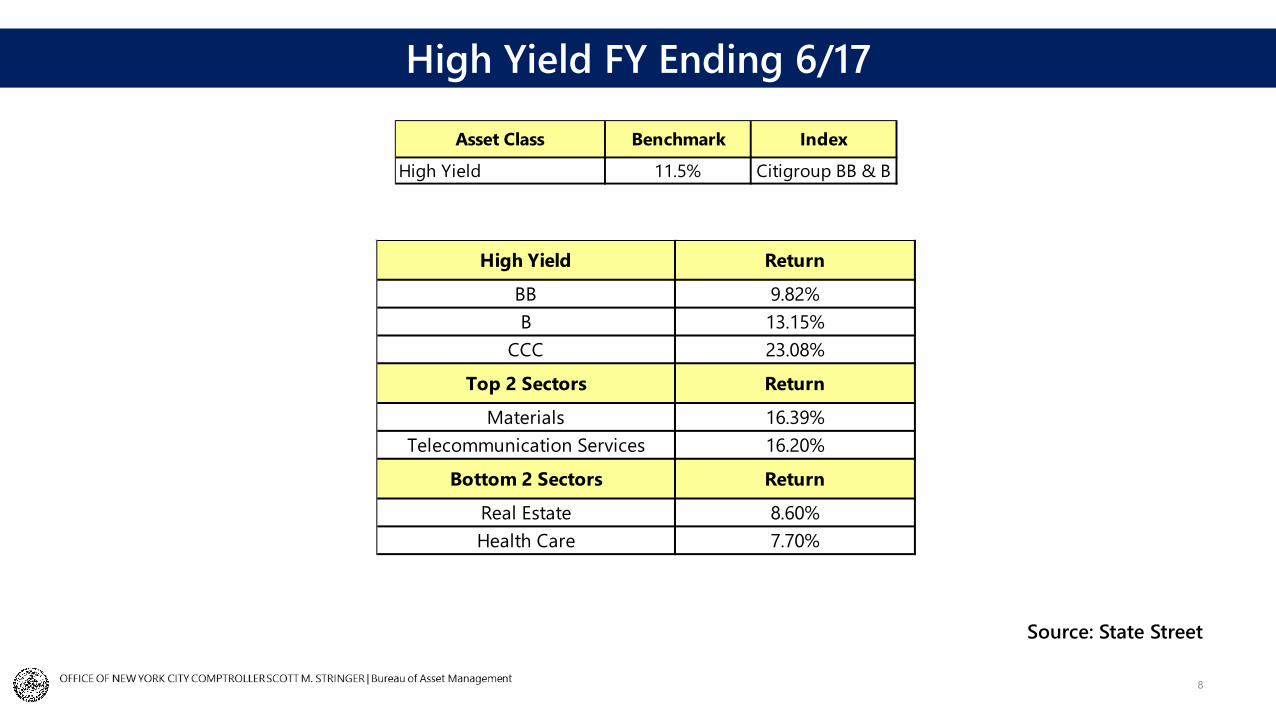

High Yield FY Ending 6/17

Asset Class Benchmark Index

High Yield 11.5% Citigroup BB & B

High Yield Return

BB 9.82%B 13.15%

CCC 23.08%

Top 2 Sectors Return

Materials 16.39%Telecommunication Services 16.20%

Bottom 2 Sectors Return

Real Estate 8.60%Health Care 7.70%

Source: State Street

8

• Domestic– Probability, timing and specifics on US tax and spending policies– Federal Reserve – impact on markets of interest rate increases and Federal Reserve

balance sheet normalization– Change in Fed Chairperson and new Fed governors– US equity market – valuations given stronger earnings with historically high PE ratios

• International– European Central Bank (ECB) – further reduction and end to QE, potential for interest rate

increases– UK-EU separation negotiations– North Korea concerns– China policies post 19th Party Congress in October ‘17– Middle East tensions

Current Global Macro Issues

9

• Change in Global QE– Fed expected to begin balance sheet normalization– ECB expected to further reduce pace of QE purchases in January

2018 and stop completely in 2H 2018• Policy rates remain historically low• U.S. Budget deficit likely to increase both short and long

term

Potential Regime Shift in Interest Rates

10

• US, Europe, UK and Japan government net bond issuance, issuance minus central bank purchases.

Change in Global QE

-1,000

-500

0

500

1,000

1,500

2012 2013 2014 2015 2016 2017e 2018e

US ($ bn) Japan ($ bn) UK ($ bn) Euro ($ bn)

USD, bn

Increase in net issuance

Decrease in net issuance

11

• Fed Funds RealRate at historicallylow level

-Fed Funds rate(yellow) at 1.25%

-ECB policy rate(blue) at -0.4%

-UK policy rate(red) at 0.25%

-BOJ policy rate(green) at -0.1%

Policy Rates Remain Historically Low

Fed Funds Rate Euro Depo Rate UK Base Rate BOJ Policy Rate

Source: Bloomberg 12

• Tax cuts and infrastructurespending will furtherincrease the deficit.

• Increased federal spending(Medicare and socialsecurity outlays) willincrease deficit meaningfullyover time.

U.S. Budget Deficit (% of GDP)

Source: PGIM

13

• Higher yields – impacts valuations of all fixed income securities

• Lower Price-Earnings (PE) multiples – impacts values of domestic and international equities, as well as private equity

• Increased volatility across all asset classes – implications for fixed income, equity, FX and private assets

Market Implications of Rising Interest Rates

14

Net of fees in public asset classes

(SSB P p.23; N, F p.24; T p.24; B p.31)

NYC Pension SystemPortfolio Std

Dev - 1 yr2Q 2017 FY 2017 Three Year

BERS 3.8% 3.6% 15.3% 6.0%TRS 3.7% 3.0% 12.7% 5.6%FIRE 3.4% 3.1% 12.8% 5.7%POLICE 3.3% 3.0% 13.2% 6.0%NYCERS 3.3% 3.0% 13.0% 5.8%Public Mkt Equiv 35 (43/22/35 index) 3.1% 12.0% 5.2%Median Fund - TUCS 3.2% 12.9% 6.0%

15

Total NYC Pension Fund Performance as of 6/30/2017

Source: State Street

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

16

Asset Allocation Second Quarter 2017 - Growth

Source: State Street

Relative Mix to Adjusted New Policy Weights (SSB F, T, N p.8; P p.10; B p.12)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

17

Asset Allocation Second Quarter 2017 – Inflation Protection

Source: State Street

Relative Mix to Adjusted New Policy Weights (SSB F, T, N p.8; P p.10; B p.12)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

18

Asset Allocation Second Quarter 2017 - Deflation Protection

Source: State Street

Relative Mix to Adjusted New Policy Weights (SSB F, T, N p.8; P p.10; B p.12)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

19

Treasury Duration Actual Vs. Target

10.9

8.3

11.0 10.5

7.6

17.8

10.9

17.8 17.8

10.9

7.066.72

8.04 8.28

5.42

0.0

3.0

6.0

9.0

12.0

15.0

18.0

21.0

6/30/17 Durations Target Durations 3/31/17 DurationsNYCERSTRS POLICE FIRE BERS

Source: State Street

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

20

Fiscal Year to Date Return – Total Portfolio

-1600

-1400

-1200

-1000

-800

-600

-400

-200

0

200

400

600

800

1000

1200

1400

1600

FYTD Portfolio FYTD Benchmark FYTD Excess

bps

TRS

NYCERS

Police

Fire

BERS

Basis Points of Excess Return (SSB T, P p.12; F p.13; N p.15; B p.19)

Source: State StreetPREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

7% AAR

21

Fiscal Year to Date Excess Return – Total Portfolio

-600

-400

-200

0

200

400

600

FYTD Total Excess Return FYTD Asset Allocation FYTD Manager Value Added

bps

TRS

NYCERS

Police

Fire

BERS

Source: State Street

Basis Points of Excess Return (SSB T, P, F p.14; N, p.17; B p.21)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

22

Fiscal Year to Date Manager Value Added - Total Portfolio

-600

-400

-200

0

200

400

600

FYTD 3 Year Trailing

TRS

NYCERS

Police

Fire

BERS

bps

Basis Points of Excess Return (SSB T, P, F p.14; N, p.17; B p.21)

Source: State Street

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

23

Value Added – Total U.S. Equities

-600

-400

-200

0

200

400

600

FYTD 3 Year Trailing

TRS: 30.21%NYCERS: 31.19%POLICE: 34.97%FIRE: 31.92%BERS: 35.48%

Source: State Street

Weights as of6/30/2017

bps

Basis Points of Excess Return (SSB P p.23; N, F p.24; T p.24; B p.31)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

24

US Equities FY 2017 Excess in Basis Points

Source: State Street

Mandate Type Manager FY 2017 Excess in Bps:NYCERS TRS Police Fire BERS

Small Core Active Wellington 178 - - - - Mid Cap Active Iridian - 480 466 - Mid Cap Active Wellington 435 434 436 Small Growth Active Brown AM 297 260 260

Small Core Active DFA - - (189) - - Large Core Quant. VTL SP500 (156) - (149) - - Small Core Quant. RAFI (344) - (337) - - Large Core Quant. RAFI (421) - (428) - - Small Value Active Ceredex (1,306) - (1,305) (1,294) - Small Value Active Dalton Greiner (396) (396)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

25

Value Added – Total International Equities

-800

-600

-400

-200

0

200

400

600

800

FYTD 3 Year Trailing

TRS: 22.35%NYCERS: 22.02%POLICE: 16.88%FIRE: 16.79%BERS: 23.6%

Source: State Street

Weights as of6/30/2017

bps

Basis Points of Excess Return (SSB P p.25; T, F, p.26; N, p.29; B p.33)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

26

Developed Equities FY 2017 Excess in Basis Points

Source: State Street

Mandate Type Manager FY 2017 Excess in Bps:NYCERS TRS Police Fire BERS

EFA Growth Active Baillie Gifford 1,323 1,152 1,476 1,476 1,476 Global Active Generation 1,227 - 1,227 - - EFA Small Core Quant. Acadian 307 572 398 398 398 EFA Growth Active Walter Scott 164 139 142 142 -

EFA Value Active Sprucegrove (80) (175) (136) (136) (133) EFA Small Value Active Pyramis (173) (181) (190) (181) - EFA Value Active Causeway (251) (370) (301) (301) -

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

27

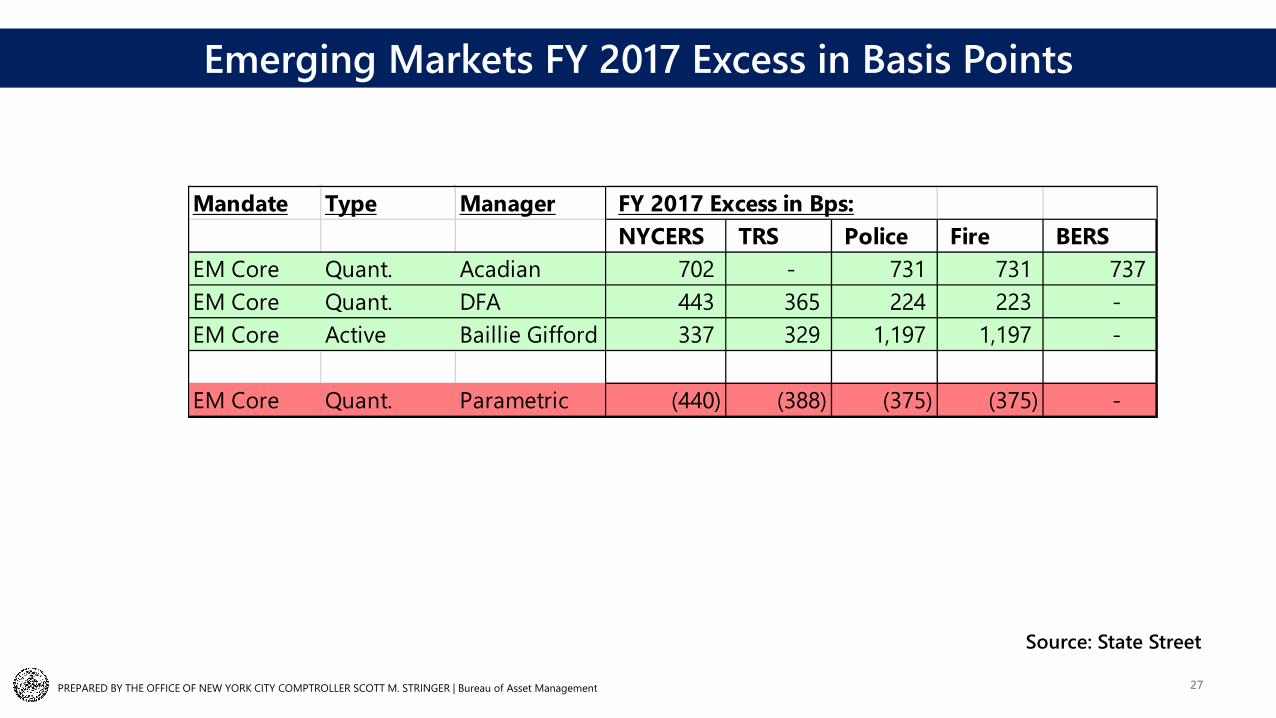

Emerging Markets FY 2017 Excess in Basis Points

Source: State Street

Mandate Type Manager FY 2017 Excess in Bps:NYCERS TRS Police Fire BERS

EM Core Quant. Acadian 702 - 731 731 737 EM Core Quant. DFA 443 365 224 223 - EM Core Active Baillie Gifford 337 329 1,197 1,197 -

EM Core Quant. Parametric (440) (388) (375) (375) -

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

28

Value Added – Investment Grade

-600

-400

-200

0

200

400

600

FYTD 3 Year Trailing

TRS: 6.01%NYCERS: 5.5%POLICE: 4.86%FIRE: 5.84%BERS: 5.21%

Source: State Street

Weights as of6/30/2017

bps

Basis Points of Excess Return

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

29

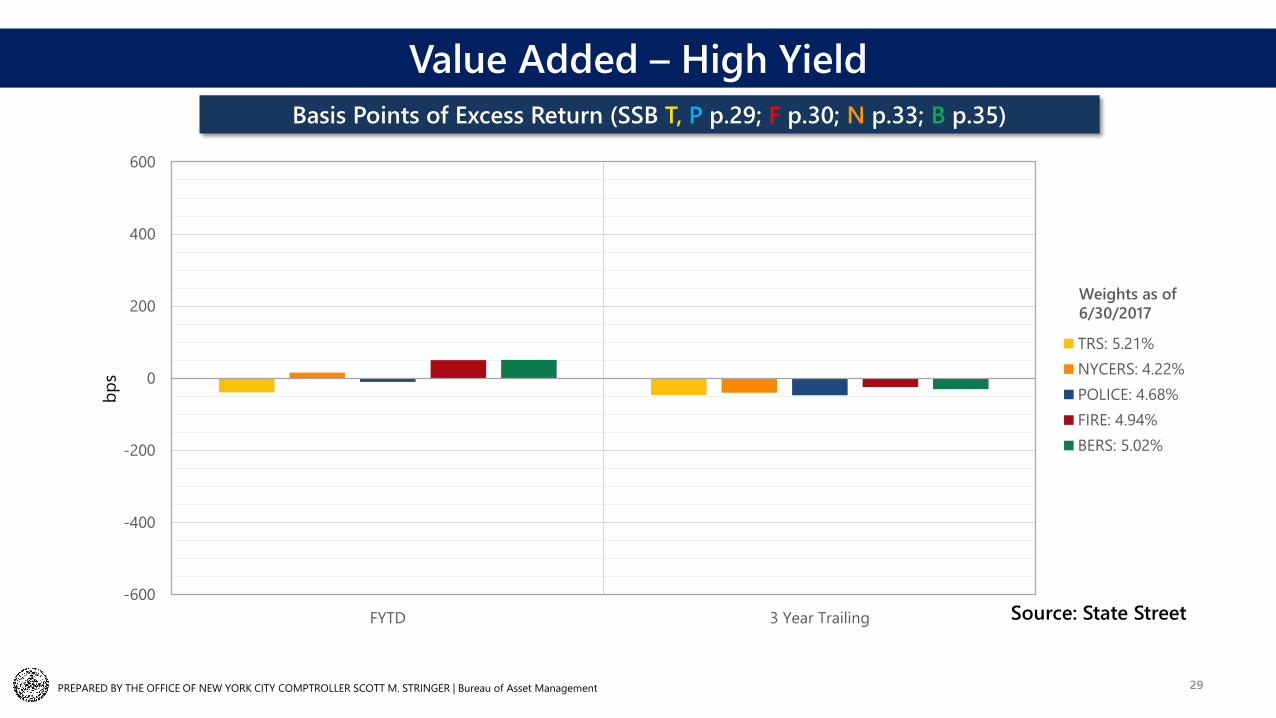

Value Added – High Yield

-600

-400

-200

0

200

400

600

FYTD 3 Year Trailing

TRS: 5.21%NYCERS: 4.22%POLICE: 4.68%FIRE: 4.94%BERS: 5.02%

Source: State Street

Weights as of6/30/2017

bps

Basis Points of Excess Return (SSB T, P p.29; F p.30; N p.33; B p.35)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

30

Value Added – Bank Loans

-600

-400

-200

0

200

400

600

FYTD 3 Year Trailing

TRS: 2.53%NYCERS: 1.8%POLICE: 1.62%FIRE: 1.59%BERS: 2.15%

Source: State Street

Weights as of6/30/2017

bps

Basis Points of Excess Return (SSB T p.29; P p.30; F p.31; N p.33; B p.35)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

31

Value Added – Economically Targeted Investments

-600

-400

-200

0

200

400

600

FYTD 3 Year Trailing

TRS: 0.87%NYCERS: 1.27%POLICE: 0.98%FIRE: 0.72%BERS: 0.58%

Source: State Street

Weights as of6/30/2017

bps

Basis Points of Excess Return

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

Value Added- Hedge FundsBasis Points of Excess Return

-600

-400

-200

0

200

400

600

FYTD 3 Year Trailing

TRS: 0%

NYCERS: 0.16%

POLICE: 5.35%

FIRE: 5.41%

BERS: 0%

Source: State Street

Weights as of6/30/2017

32

bps

Value Added - Hedge FundsBasis Points of Excess Return (SSB F p.56; N p.58; P p.60)

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

PRIVATE MARKET DATA

34

Value Added – Private Equity

(600)

(400)

(200)

-

200

400

600

Excess Return Since Inception; PME Benchmark: Russell 3000 As of 3/31/17

TRS - 07/08/99

NYCERS - 03/29/99

Police - 03/29/99

Fire - 03/29/99

BERS - 07/20/06

Inception Date

300bps Target

Source: StepStone Group & Hamilton Lane

Basis Points of Cumulative IRR above Public Market Equivalent

bps

The PME Spread is the difference between the IRR and the PME Benchmark.

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

35

Value Added – Opportunistic Fixed Income (OFI)

-600

-400

-200

0

200

400

600

Excess Return Since Inception; PME Benchmark: 50% JP Morgan Global High Yield 50% CS Leveraged Loans as of 6/30/17

TRS - 10/24/2007

NYCERS - 10/24/2007

Police - 10/24/2007

Fire - 10/24/2007

BERS - N/A

Inception Date

300bps Target

Source: State Street

Basis Points of Cumulative IRR above Public Market Equivalent

bps

The PME Spread is the difference between the IRR and the PME Benchmark.

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

36

Value Added – Private Real Estate - Core

-600

-400

-200

0

200

400

600

Excess Return Since Inception; Core = 40% Equities- Russell 3000 /60% BarcAgg as of 3/31/17

TRS - 12/6/2002

NYCERS - 12/6/2002

Police - 12/6/2002

Fire - 12/6/2002

BERS - 12/13/2010

Inception Date

Source: State Street

Basis Points of Cumulative IRR above Public Market Equivalentbp

s

The PME Spread is the difference between the IRR and the PME Benchmark.

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

37

Value Added – Private Real Estate – Non-Core

-600

-400

-200

0

200

400

600

Excess Return Since Inception; Non-core = 60% Equities- Russell 3000/40% BarcAgg as of 3/31/17

TRS - 12/6/2002

NYCERS - 12/6/2002

Police - 12/6/2002

Fire - 12/6/2002

BERS - 12/13/2010

Inception Date

Source: State Street

Basis Points of Cumulative IRR above Public Market Equivalentbp

s

The PME Spread is the difference between the IRR and the PME Benchmark.

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

38

Value Added - Infrastructure

-900

-700

-500

-300

-100

100

300

500

700

900

Excess Return Since Inception; PME Benchmark: 50% R3000 & 50% Barclays Agg. as of 3/31/17

TRS - 11/19/2013

NYCERS - 11/19/2013

Police - 11/19/2013

Fire - 11/19/2013

BERS - 11/19/2013

Inception Date

Source: StepStone Group

Basis Points of Cumulative IRR above Public Market Equivalentbp

s

The PME Spread is the difference between the IRR and the PME Benchmark.

PREPARED BY THE OFFICE OF NEW YORK CITY COMPTROLLER SCOTT M. STRINGER | Bureau of Asset Management

Questions?