Embed Size (px)

Citation preview

Clean Energy Technology, R&D Clean Energy Technology, R&D and Innovationand Innovation

Dr. Harlan WatsonSenior Climate Negotiator and Special Representative

U.S. Department of State

Climate Change and Sustainable Development:An international workshop to strengthen research

and understandingSession 5: “Options for Response Measures”

Magnolia Hall, Indian Habitat CentreNew Delhi, India

April 8, 2006

OverviewOverview• Stabilization of greenhouse gas [GHG] concentrations in the

atmosphere—the “ultimate objective of the UNFCCC confronts several realities, including:

Reality 1—Stabilizing GHG Atmospheric Concentrations Is a Long-Term Issue.Reality 2—Fossil Fuels Will Remain the Dominant Energy Source for Decades.Reality 3—Can’t Expect Developing Countries to Reduce Energy Consumption for the Foreseeable Future.Reality 4—No “Silver Bullet”: Broad Portfolio of Technologies Required. Reality 5—Challenge is Formidable

• U.S. domestic and international efforts to develop and deploy cleaner technologies.

Reality 1Reality 1——Stabilizing GHG Atmospheric Stabilizing GHG Atmospheric Concentrations is a LongConcentrations is a Long--Term IssueTerm Issue

• Stabilizing atmospheric concentrations of GHGs is a very long-term issue—decades to a century or more time scale.

• Stabilization means that GLOBAL emissions must peak in the decades ahead and then decline indefinitely thereafter.

Source: Jae Edmonds (Battelle)

Reality 2Reality 2——Fossil Fuels Will Remain the Fossil Fuels Will Remain the Dominant Energy Source for DecadesDominant Energy Source for Decades

• ScenariosWorld Energy Demand ProjectionsWorld EnergyWorld Energy--Related CORelated CO22 Emissions ProjectionsEmissions Projections

• Plentiful Fossil Fuels Means Problem Will Not Go Away On Its Own.

Oil

Natural gas

Coal

Nuclear powerHydro power

Other renewables

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

1970 1980 1990 2000 2010 2020 2030

Mto

e

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

1970 1980 1990 2000 2010 2020 2030

Mto

eIEA World Energy Outlook 2004Reference Scenario:

Source: Fatih Birol (IEA)Fatih Birol (IEA)

• Fossil fuels account for almost 90% of the ~60% growth in energy demand between now and 2030.

World Primary Energy DemandWorld Primary Energy Demand

IEA World Energy Outlook 2004Reference Scenario:

Source: Fatih Birol (IEA)Fatih Birol (IEA)

• Global emissions projected grow 62% between 2002 & 2030, and developing countries’emissions overtaking OECD’s in the 2020s.

World EnergyWorld Energy--Related CORelated CO22 EmissionsEmissions

0

4 000

8 000

12 000

16 000

20 000

1970 1980 1990 2000 2010 2020 2030

Mt o

f CO

2

OECD Transition economies Developing countries

2

Plentiful Fossil Fuels Means Problem Will Plentiful Fossil Fuels Means Problem Will Not Go Away On Its OwnNot Go Away On Its Own

Unconventional Liquids and Gases

Coal

14

Carbon Reservoirs

BiomassBiomass~500 ~500 GtCGtC

SoilsSoils~1,500 ~1,500 GtCGtC

Atmosphere 800 GtC (2004)

OilOil~270 ~270 GtCGtC2

N. GasN. Gas~260 ~260 GtCGtC

Unconventional Fossil Fuels: 15,000 to 40,000 GtC

CoalCoal5,000 to 8,000 GtC5,000 to 8,000 GtC

Sources: Jae Edmonds (Battelle) and NebojNebojšša Nakia Nakiććenovienovićć (IIASA)(IIASA)

Reality 3Reality 3——CanCan’’t Expect Developing t Expect Developing Countries to Reduce Energy Consumption Countries to Reduce Energy Consumption

for the Foreseeable Futurefor the Foreseeable Future

• Overriding priority for developing countries, is poverty reduction => Economic growth => Increase in Energy Consumption => Increase in Emissions.

In 2030, if no major new policies are implemented, there will still be 1.4 billion people without electricity.Source: Fatih Birol Fatih Birol

(IEA)(IEA)

Reality 4Reality 4——No No ““Silver BulletSilver Bullet””: Broad : Broad Portfolio of Technologies RequiredPortfolio of Technologies Required

Assumed Advances In• Fossil Fuels• Energy intensity• Nuclear• Renewables

The “Gap”

“Gap” Technologies• More of All of the

Above• Biological

Sequestration• Carbon Capture and

Disposal• Hydrogen and

Advanced Transportation

• Biotechnologies

Source: Jae Edmonds (Battelle)

Atmospheric GHG Concentrations Stabilized

Global Carbon Emissions

Reality 5Reality 5——ChallengeChallenge is Formidableis Formidable

Source: Rob Socolow (Princeton)

Actions that Provide 1 Gigaton/year of Mitigation• Coal: Carbon capture and storage at 800 1 GW coal power plants.

• Nuclear: 700 GW (twice current capacity) displacing coal power

• Geologic Sequestration: 3,500 Sleipners @1 MtCO2/yr (~100 x U.S. CO2injection rate for EOR).

• Biofuels: Two billion 60 mpg cars running on biofuels 250 million hectares of high-yield crops (one sixth of world cropland)

• Efficency: 2 billion cars at 60 mpg instead of 30 mpg.

• Wind: One million 2-MW windmills displacing coal power. (Today~50,000 MW).

• Solar PV: 2000 GWpeak (700 times current capacity) and 2 million hectares of land.

U.S. Climate Change U.S. Climate Change Policy Policy ComponentsComponents

• Slowing the Growth of Net Greenhouse Gas (GHG) Emissions.

National Goal: Reduce GHG Intensity by 18% Over 10-Year Period (2002-2012).

140

150

160

170

180

190

2000 2002 2004 2006 2008 2010 2012 2014

Year

No Improvement (183 tons in 2002)

Current Efforts (14%)

National Goal (18% decline to

151 tons in 2012)

Met

ric T

ons C

arbo

n Eq

uiva

lent

Per

M

illio

n D

olla

rs G

DP,

200

1 D

olla

rs

• Laying the Groundwork for Current and Future Action: Investments in Science and Technology.

Climate Change Science Program (~$2 billion/year)Climate Change Technology Program (~$3 billion/year)

• Promoting International Cooperation.

Address climate change within a broader development agenda—one that promotes economic growth, reduces poverty, provides energy security, reduces air pollution, and mitigates greenhouse gas emissions.

NearNear--Term Domestic ActionsTerm Domestic Actions• More than 60 Federal mandatory, incentive-based, and voluntary programs

designed to help reduce emissions by more than 500 million metric tons of carbon-equivalent from BAU through 2012. Examples of mandatory and incentive-based programs include:

Fuel Economy Standards Clean Air RulesEnergy Efficiency Standards Biological SequestrationRenewable Energy/CHP Tax Incentives Nuclear Plant RelicensingHybrid/Fuel Cell Vehicle Tax Incentives Nuclear Power 2010

• Numerous U.S. Department of Energy (DOE) and U.S. Environmental Protection Agency (EPA) voluntary programs to help consumers andcorporations reduce their GHG emissions, such as:

ENERGY STAR Methane Programs CHP* Partnership SmartWay Transport Partnership Climate Leaders Climate VISION

• U.S. Fiscal Year 2007 budget request of about $5 billion for climate change programs plus energy tax incentives:

Supports the near-term objective and future actions through major investments in science and technology.

*Combined Heat and Power

Domestic Clean Air PolicyDomestic Clean Air Policy• CLEAR SKIES: Reduce Power Plant Pollution (Sulfur Dioxide, Nitrogen

Oxides, and Mercury) by 70% below 2003 levels by 2018Market-Based Cap and Trade SystemUS Fleet of Coal-Fired Power Plants — 1,300 NationwideTwo Phases Provides Regulatory Certainty for Capital Planning Decisions Promotes Technology Innovation and Cost ReductionPromotes Clean Coal and Relieves Pressure On Natural Gas Usage$50+ Billion in Pollution Controls, Efficiency Upgrades$100+ Billion Health SavingsHigh Compliance — Low BureaucracyMinimal electricity price impact (~ 1,7-3%)

• CLEAN DIESEL RULES — Reduce Diesel Engine Pollution by 90%+Performance Standard — Promotes InnovationFuel Sulfur Dioxide Reduced 99+% in 2007New Engine Nitrogen Oxide Reduced 90%Large Trucks, Construction and Farm Equipment, Locomotives, Marine Vessels Commercially Feasible TimelinesAssures Reliability and Affordability of New EnginesEnables Larger U.S. Market in Fuel Efficient Vehicles (up to 30% improved fuel economy)

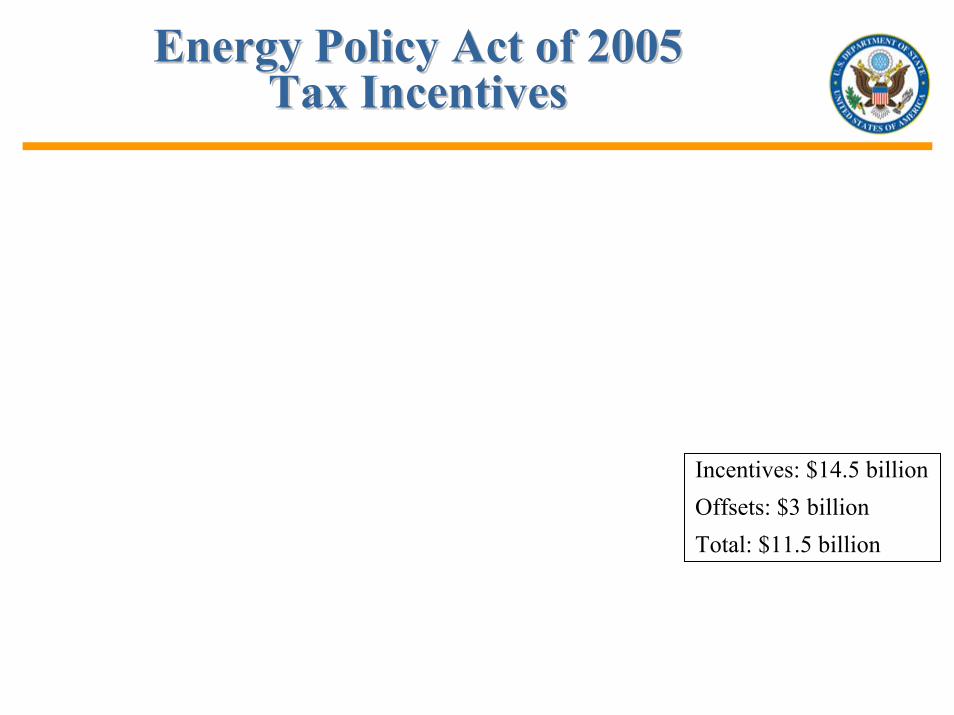

Energy Policy Act of 2005Energy Policy Act of 2005Tax IncentivesTax Incentives

Incentives: $14.5 billionOffsets: $3 billionTotal: $11.5 billion

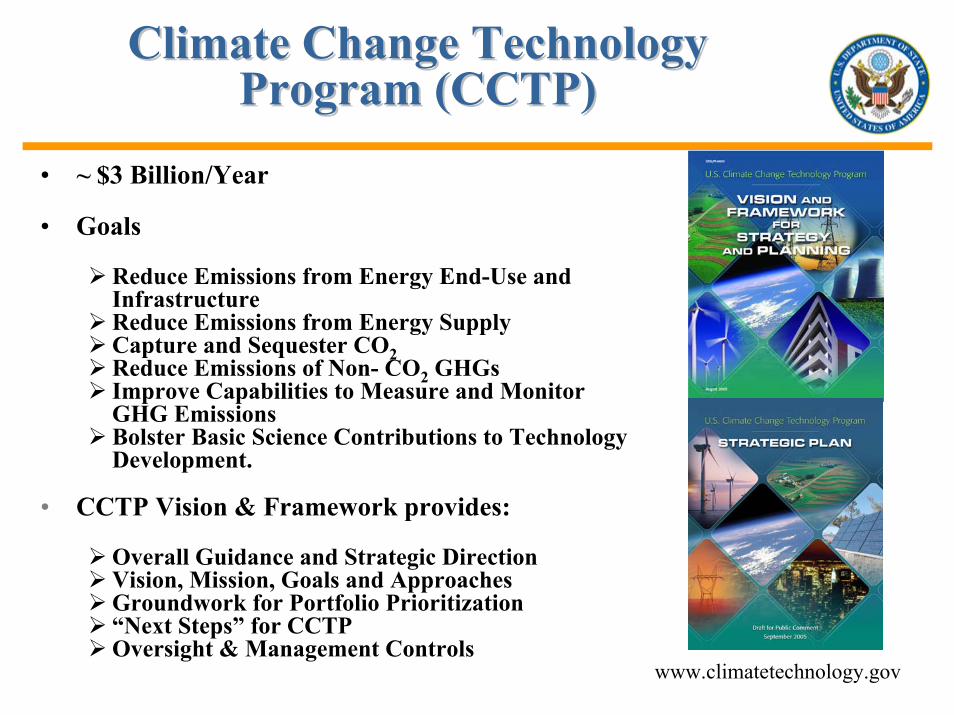

Climate Change TechnologyClimate Change TechnologyProgram (CCTP)Program (CCTP)

• ~ $3 Billion/Year

• Goals

Reduce Emissions from Energy End-Use and InfrastructureReduce Emissions from Energy Supply Capture and Sequester CO2Reduce Emissions of Non- CO2 GHGsImprove Capabilities to Measure and Monitor GHG EmissionsBolster Basic Science Contributions to Technology Development.

• CCTP Vision & Framework provides:

Overall Guidance and Strategic DirectionVision, Mission, Goals and ApproachesGroundwork for Portfolio Prioritization“Next Steps” for CCTPOversight & Management Controls

www.climatetechnology.gov

Near-Term Mid-Term Long-TermCCTP GoalsGoal #1 Energy End-Use& Infrastructure

Goal #2 Energy Supply

Goal #3 Capture, Storage& Sequestration

Goal 4 Other Gases

• Hybrid & Clean Diesel Vehicles• High-Efficiency Appliances• High-Performance Buildings• High-Efficiency Industrial

Processes & Boilers• Modernized Grids

• Wind, Hydro, Solar & Geothermal

• Biomass, Biodiesel, Clean Fuels• Distributed Electric Generation • IGCC Coal Plants• Stationary H2 Fuel Cells • Enhanced Nuclear Power

• CSLF & Regional Partnerships• Oxy-Fuel Combustion• Enhanced Oil Recovery• Reforestation• Soils Conservation

• Methane to Markets• Alternatives to High GWP

Gases• Bioreactor Landfill Technology

• H2 Fuel Cell Vehicles• High-Efficiency Aviation• Net-Zero Buildings • Expanded Solid-State Lighting• Transformational Technologies for

Energy-Intensive Industries• Advanced Energy Storage &

Controls

• Large-Scale Wind Power• Community-Scale Solar• Bio-Fuels, Bio-Refineries• Advanced Bio-Refining of Cellulose

& Biomass• FutureGen Scale-Up• Gen IV Nuclear Energy

• Improved CO2 Capture• Safe Geologic Storage • Environmental Guidelines• Bio-Based & Recycled Products• Soils Uptake & Land Use

• Methane Emissions Reduction• Precision Agriculture• PFC Substitutes

• Net-Zero Communities• Low-Emission Intelligent Transport

Systems• Low-Emission Industrial Production• Closed-Cycle Products & Materials• Low-Loss Energy Transmission &

Distribution

• Widespread Renewable Energy• Bio-Inspired Energy & Fuels• Zero-Emission Fossil Energy• H2 & Electric Economy• Widespread Safe Nuclear Energy• Fusion Power Deployment

• CO2 as Commodity Chemical • Large Global CO2 Storage• Large-Scale Sequestration• Carbon-Based Products & Materials

• Low Emissions of Other GHGs• Low-Emission Agriculture• Genetically Designed Forages &

Bacteria

Roadmap for CC Technology DevelopmentRoadmap for CC Technology Development

H2 + Fuel Cells

Clean Fossil

Sequestration

Nuclear Energy

Fusion Energy, ITEREnergy Efficiency RD&D

Transmission & Distribution

Renewable Energy

Other CCTP RD&D Areas

Deployment**

CCTP Fiscal Year 2007 Budget Request*Portfolio of RD&D and Deployment: $2.987 Million

($649 M)

($25 M)

($395 M)

($103 M)

($320 M)($319 M)

($397 M)

($137 M)

($321 M)

($322 M)

** Deployment is 79% Energy Efficiency*All CCTP Federal Agencies Fiscal Year 2007 Budget Request

Fiscal Year 2007 Budget Request:Fiscal Year 2007 Budget Request:CCTP PortfolioCCTP Portfolio

International PartnershipsInternational Partnerships• Carbon Sequestration Leadership Forum (CSLF)―22 members:

Focused on CO2 capture & storage technologies.

• International Partnership for the Hydrogen Economy (IPHE)―17 members: Organizes, coordinates, and leverages hydrogen RD&D programs.

• Generation IV International Forum (GIF)―1 members: Devoted to R&D of next generation of nuclear systems.

• Methane to Markets Partnership―17 members: Recovery and use of methane from landfills, mines, and oil & gas systems.

• ITER―7 members: Project to demonstrate the scientific and technological feasibility of fusion energy.

• Renewable Energy and Energy Efficiency Partnership (REEEP)―17 countries working to enhance the delivery of clean and secure energy through the use of renewable resources and energy efficiency programs in the developed and developing world.

• 49.0% of World GDP (Purchasing Power Parities)

•• 45.4% of World Population

• 46.2% of World Total Primary Energy Consumption

• 50.2% of World CO2 Emissions from the Fossil Fuel Consumption and Flaring

Six Partners in 2003: (Australia, China, India, Japan,Republic of Korea, and the United States) accounted for:

• 64.4% of World Coal Production

• 63.6% of World Coal Consumption

• 45.6% of World Petroleum Consumption

• 49.3% of World Total Net Electricity Generation

• 49.4% of World Total Net Electricity Consumption

Sources: International Energy Agency, CO2 Emissions for Fuel Combustion: 1971-2003. 2005 Edition; and Energy Information Administration, International Energy Annual 2003

AsiaAsia--Pacific Partnership on Clean Pacific Partnership on Clean Development and ClimateDevelopment and Climate

Asia-Pacific Partnership on Clean Development and Climate

• Voluntary practical measures taken by these six countries in the Asia-Pacific region to create new investment opportunities, build local capacity, and remove barriers to the introduction of clean, moreefficient technologies.

• Help each country meet nationally-designed strategies for improving energy security, reducing pollution, and addressing the long-term challenge of climate change.

• Promote the development and deployment of existing and emerging cleaner, more efficient technologies and practices that will achieve practical results in areas such as:

Energy EfficiencyClean CoalNatural GasBioenergy

Methane Capture/UseCivilian Nuclear PowerGeothermalAgriculture/Forestry

Rural/Village Energy SystemsAdvanced TransportationHydro/Wind/Solar PowerBuilding/Home Construction/Operation

• Seek opportunities to engage the private sector.

FocusFocus

Asia-Pacific Partnership on Clean Development and Climate

Policy and Implementation Committee(USA, Chair)

CleanerFossil

EnergyTask Force

Australia (Chair)China

(Co-Chair)

PowerGeneration

AndTransmission

USA(Chair)China

(Co-Chair)

AluminiumTask Force

Australia(Chair)

USA(Co-Chair)

Coal MiningTask Force

USA(Chair)India

(Co-Chair)

RenewableEnergy

and DistributedGenerationTask Force

Korea(Chair)

Australia(Co-Chair)

SteelTask Force

Japan(Chair)India

Co-Chair)

CementTask Force

Japan(Chair)

BuildingsAnd

AppliancesTask Force

Korea(Chair)

USA(Co-Chair)

Administrative Support Group(USA)

OrganizationOrganization

Asia-Pacific Partnership on Clean Development and Climate

Next StepsNext Steps• Policy and Implementation Committee and Task Forces will meet April

18-21 in Berkeley, California.

• Task Forces to begin development of Action Plans — “blueprints” for action — for the private sector and governments.

Strategic framework for identifying opportunities (technologies and practices) and implementing priority actions to advance clean development and climate goals.Identification of specific opportunities (technologies and practices) for cooperation and barriers to these opportunities.Establishment of ambitious and realistic results-oriented goals for both immediate and medium-term specific actions, with measurement systems to gauge progress toward achieving the goals.

• We are seeking actions that are both broad and deep, including both technology development and deployment.

• Action Plans to be completed by mid-2006, with implementation to begin at start of Fiscal Year 2007 (October 1, 2006).

SummarySummary• Stabilization of greenhouse gas [GHG] concentrations in the atmosphere—the

“ultimate objective of the UNFCCC confronts several realities, including:

Reality 1—Stabilizing GHG Atmospheric Concentrations Is a Long-Term Issue.Reality 2—Fossil Fuels Will Remain the Dominant Energy Source for Decades.Reality 3—Can’t Expect Developing Countries to Reduce Energy Consumption for the Foreseeable Future.Reality 4—No “Silver Bullet”: Broad Portfolio of Technologies Required.Reality 5—Challenge is Formidable.

• U.S. addresses climate change within a broader development agenda—one that promotes economic growth, reduces poverty, provides energy security, reduces air pollution, and mitigates greenhouse gas emissions.

• Seeks to accelerate near-term deployment of cleaner technologies through a mix of mandatory, incentive-based, and voluntary programs, and working through international partnerships, with emphasis on public-private partnerships.

• Seeks to develop “breakthrough” cleaner technologies through government-funded RD&D programs domestically, and working through international partnerships, again emphasizing public-private partnerships where feasible.

Room for Optimism: U.S. Experience Room for Optimism: U.S. Experience with Air Pollutionwith Air Pollution

• Air Pollution Down 54% Since 1970:

Down 10% in 2001-2004

Economy Up 187%

Vehicle Miles Up 171%

Energy Use Up 47%

Population Up 40%