Embed Size (px)

Citation preview

2018

Prepared by

for

City Water, Light, and Power of Springfield, Illinois

Integrated Resource Plan

i

This page is intentionally left blank.

ii

Table of Contents

List of Tables ..................................................................................................................................................................... v

List of Figures .................................................................................................................................................................... v

Executive Summary ........................................................................................................................................................ 8

Introduction and Objectives .................................................................................................................................. 8

Study Methodology .................................................................................................................................................. 9

Key Considerations and Risk Factors .................................................................................................................. 9

Assumptions .............................................................................................................................................................. 10

Findings....................................................................................................................................................................... 10

Reference Case .................................................................................................................................................... 10

Reference Case Solution 4 .............................................................................................................................. 11

Scenarios ............................................................................................................................................................... 12

Recommendations ............................................................................................................................................. 14

Disclaimer ................................................................................................................................................................... 14

Section 1: Introduction ............................................................................................................................................... 15

Integrated Resource Planning ............................................................................................................................ 15

IRP Development ................................................................................................................................................ 15

Methodology ....................................................................................................................................................... 16

CWLP Overview ........................................................................................................................................................ 17

Demand ................................................................................................................................................................. 18

Existing Resources ............................................................................................................................................. 18

Reserve Margins and the Need for Generating Capacity ................................................................... 18

Fuels ........................................................................................................................................................................ 18

Market Environment .............................................................................................................................................. 20

Potential Impact of Laws and Regulations .................................................................................................... 21

Energy Efficiency ................................................................................................................................................. 21

Renewable Resource Mandates .................................................................................................................... 21

Fuel Diversity ........................................................................................................................................................ 22

Carbon Dioxide Emissions Mitigation ........................................................................................................ 22

Other Emissions Constraints .......................................................................................................................... 23

Electric Vehicle Incentives ............................................................................................................................... 23

Federal, State, and Local Tax Credits and Incentives ............................................................................ 24

iii

Section 2: Existing Power Supply Resources ...................................................................................................... 26

Existing Supply-Side Resources ......................................................................................................................... 26

Energy Efficiency and Demand-Response Programs ................................................................................ 26

20-year Demand and Resource Balance ........................................................................................................ 27

Transmission and Distribution System ............................................................................................................ 28

Section 3: Supply and Demand Requirements Analysis ................................................................................ 29

Overview of Customers ......................................................................................................................................... 29

Historical Demand .................................................................................................................................................. 29

Demand and Energy Forecast ............................................................................................................................ 29

Section 4: Fuel Price Projections ............................................................................................................................. 32

Overview ..................................................................................................................................................................... 32

Natural Gas ................................................................................................................................................................ 32

Coal ............................................................................................................................................................................... 33

Fuel Oil ........................................................................................................................................................................ 33

Section 5: Future Resource Options ...................................................................................................................... 34

Resource Options Included in IRP .................................................................................................................... 34

Overview of Available Resources and Technologies ................................................................................. 34

Steam Units .......................................................................................................................................................... 34

Simple Cycle Gas Turbines .............................................................................................................................. 35

Simple Cycle Gas Turbine with Intercooler ............................................................................................... 35

Combined Cycle .................................................................................................................................................. 36

Reciprocating Internal Combustion Engine ............................................................................................. 36

Wind and Solar Generation ............................................................................................................................ 36

Energy Storage .................................................................................................................................................... 38

Distributed Energy Resources ....................................................................................................................... 41

Demand-Side Resources ................................................................................................................................. 42

Combined Heat and Power ............................................................................................................................ 43

Energy Efficiency ................................................................................................................................................. 44

Electric Vehicles .................................................................................................................................................. 45

Cost and Operational Abilities of Included Supply-Side Resources .................................................... 47

Operation and Maintenance Costs .............................................................................................................. 49

Capital Cost .......................................................................................................................................................... 49

Time Value of Money ....................................................................................................................................... 50

iv

Levelized Annual Capital Costs ..................................................................................................................... 50

Qualification ......................................................................................................................................................... 50

Potential Energy Efficiency and Demand-Response Programs ............................................................. 51

Section 6: Reference Case Assumptions and Assessment ............................................................................ 52

Description of the Reference Case ................................................................................................................... 52

Model Topology ...................................................................................................................................................... 52

Reference Case Results ......................................................................................................................................... 53

Capacity and Energy ......................................................................................................................................... 53

Environmental Impacts .................................................................................................................................... 55

Costs and Revenues .......................................................................................................................................... 55

Reference Case Alternate Solutions ................................................................................................................. 56

Reference Case Solutions 2 and 3 ............................................................................................................... 57

Reference Case Solution 4 .............................................................................................................................. 57

Section 7: Comparison of Scenario Results ........................................................................................................ 59

Description of the Scenarios ............................................................................................................................... 59

Scenario Results – MTEP Scenarios .................................................................................................................. 60

Scenario 1 – Accelerated Fleet Change ..................................................................................................... 60

Scenario 2 – Limited Fleet Change .............................................................................................................. 61

Scenario 3 – Distributed and Emerging Technologies ......................................................................... 62

Scenario Results – Locally Controlled Scenarios ......................................................................................... 62

Scenario 4 – High CWLP Coal Price ............................................................................................................. 63

Scenario 5 – Flat CWLP Coal Price ............................................................................................................... 63

Scenario 6 – Keep Dallman 3 and 4 ............................................................................................................ 64

Scenario 7 – High CWLP Renewables ......................................................................................................... 64

Scenario Results – Non-Impactable Scenarios............................................................................................. 64

Scenario 8 – NYMEX Gas Price ...................................................................................................................... 64

Scenario 9 – Seasonal Extremes ................................................................................................................... 65

Scenario 10 – Stricter Environmental Regulations ................................................................................. 66

Section 8: Conclusions and Recommendations ................................................................................................ 67

Conclusions ............................................................................................................................................................... 67

Recommendations .................................................................................................................................................. 69

Key Risk Factors ....................................................................................................................................................... 70

Disclaimer ................................................................................................................................................................... 71

v

Bibliography ................................................................................................................................................................... 72

Appendices ..................................................................................................................................................................... 74

Appendix A: Definitions ........................................................................................................................................ 74

Appendix B: Unit Types Excluded from the Study ...................................................................................... 77

Appendix C: Levelized Cost of Energy ............................................................................................................. 78

Appendix D: Scenario Annual Revenue Requirements ............................................................................. 79

List of Tables

Table 1: CWLP Overview ............................................................................................................................................... 8

Table 2: New Supply-Side Resource Options .................................................................................................... 10

Table 3: Wind and Solar Federal Income Tax Credits ..................................................................................... 25

Table 4: Existing Supply Resources........................................................................................................................ 26

Table 5: New Resource Options ............................................................................................................................. 48

Table 6: List of Scenarios ........................................................................................................................................... 59

List of Figures

Figure 1: Reference Case Fuel Price Forecast .................................................................................................... 10

Figure 2: Reference Case Load and Capacity Balance .................................................................................... 11

Figure 3: Ref Sol 4 Load and Capacity Balance ................................................................................................. 12

Figure 4: Scenario Results and Decisions Overview ........................................................................................ 13

Figure 5: Typical IRP Process Diagram ................................................................................................................. 16

Figure 6: Fuel Mix of Net Generation and Purchases ..................................................................................... 19

Figure 7: Existing EE Program Details ................................................................................................................... 27

Figure 8: Demand and Resource Balance ........................................................................................................... 27

Figure 9: Total Energy Usage ................................................................................................................................... 31

Figure 10: Peak Demand ........................................................................................................................................... 31

Figure 11: Natural Gas Price Forecast at Henry Hub ...................................................................................... 32

Figure 12: CWLP Delivered Coal Price Forecast ................................................................................................ 33

Figure 13: Distillate Fuel Oil Price Forecast ........................................................................................................ 33

Figure 14: Evolving U.S. Wind and Solar Generation Capacity Forecasts ............................................... 37

Figure 15: Cost of EV Batteries ................................................................................................................................ 39

Figure 16: Unsubsidized Levelized Cost of Storage ........................................................................................ 40

vi

Figure 17: DER Example Diagram........................................................................................................................... 41

Figure 18: CHP Example Diagram .......................................................................................................................... 43

Figure 19: US Annual Electricity Consumption per Year ............................................................................... 44

Figure 20: EV Inventory Forecast through Time (2010-2030) ...................................................................... 45

Figure 21: EV and ICE Fuel Cost .............................................................................................................................. 46

Figure 22: Potential EE Program Details .............................................................................................................. 51

Figure 23: Decision Summary .................................................................................................................................. 53

Figure 24: Load and Capacity Balance ................................................................................................................. 54

Figure 25: Energy Production by Resource ........................................................................................................ 54

Figure 26: Seasonal NOx Emissions by Resource ............................................................................................. 55

Figure 27: Reference Case Annual Revenue Requirements ......................................................................... 55

Figure 28: Solution Comparison ............................................................................................................................. 56

Figure 29: Ref Sol 4 Load and Capacity Balance .............................................................................................. 57

Figure 30: Ref Sol 4 Energy Production by Resource ..................................................................................... 58

Figure 31: Ref Sol 4 Annual Revenue Requirements ...................................................................................... 58

Figure 32: MTEP Scenarios Result Comparison ................................................................................................ 60

Figure 33: CO2 Production in AFC Scenario ....................................................................................................... 61

Figure 34: Locally Controlled Scenarios Result Comparison ....................................................................... 63

Figure 35: Non-Impactable Scenarios Result Comparison ........................................................................... 65

Figure 36: Scenario Results and Decisions Overview ..................................................................................... 67

Figure 37: Scenario LCOE and NPV Comparison.............................................................................................. 68

Figure 38: AFC Scenario Annual Revenue Requirements .............................................................................. 79

Figure 39: LFC Scenario Annual Revenue Requirements .............................................................................. 80

Figure 40: DET Scenario Annual Revenue Requirements .............................................................................. 80

Figure 41: FLC Scenario Annual Revenue Requirements .............................................................................. 81

Figure 42: HC Scenario Annual Revenue Requirements ................................................................................ 81

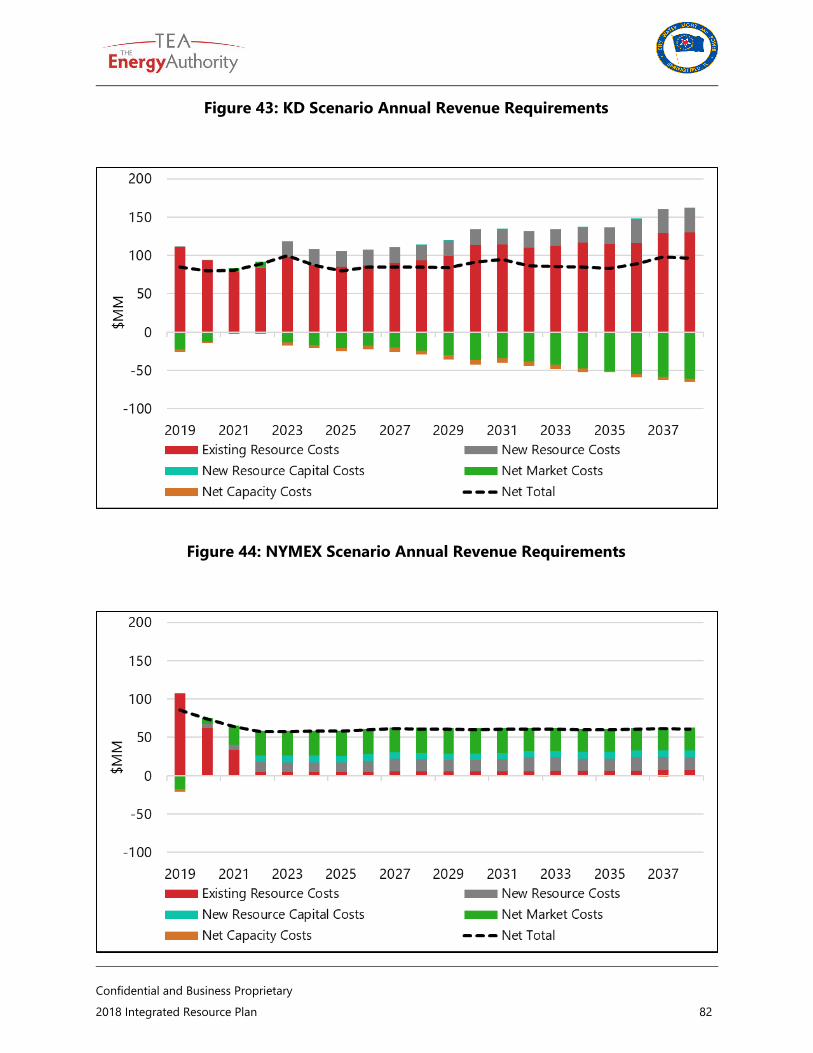

Figure 43: KD Scenario Annual Revenue Requirements ................................................................................ 82

Figure 44: NYMEX Scenario Annual Revenue Requirements ....................................................................... 82

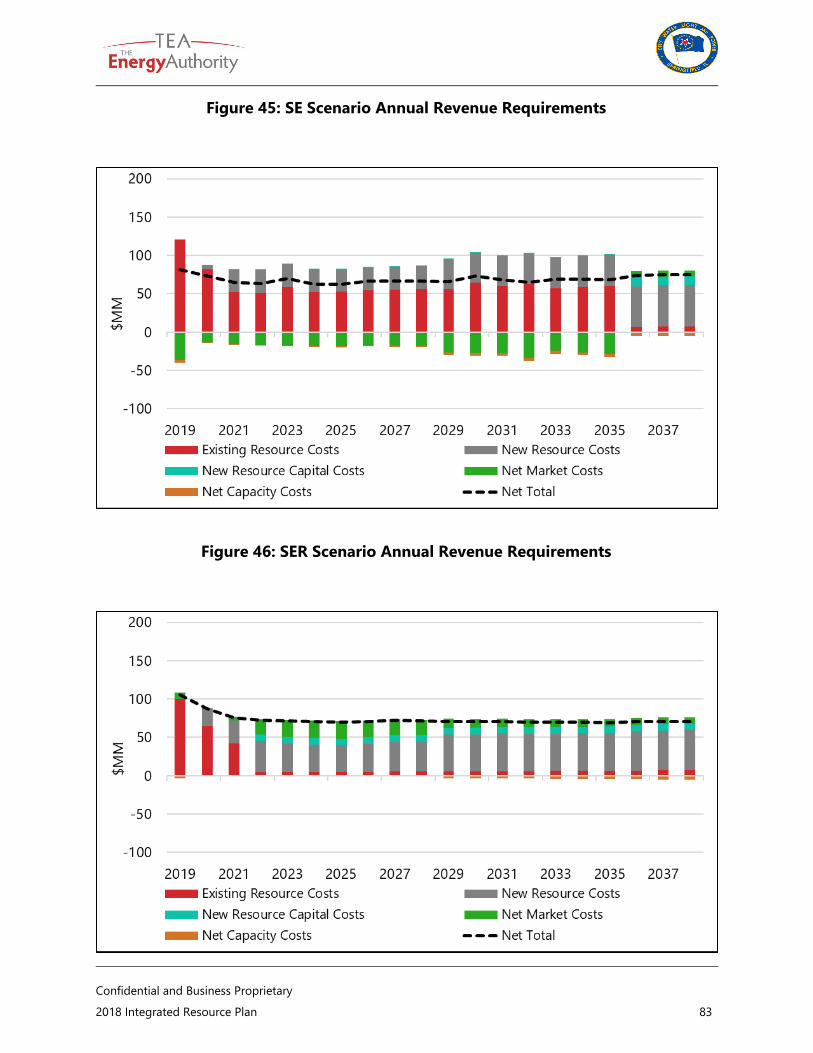

Figure 45: SE Scenario Annual Revenue Requirements ................................................................................. 83

Figure 46: SER Scenario Annual Revenue Requirements .............................................................................. 83

Confidential and Business Proprietary

2018 Integrated Resource Plan 7

This page is intentionally left blank.

Confidential and Business Proprietary

2018 Integrated Resource Plan 8

Executive Summary

INTRODUCTION AND OBJECTIVES

Given the ubiquity of electricity to modern society, long-term supply planning impacts everyone.

How customers consume and ultimately pay for this critical commodity in the future will be

driven by the decisions we make today. Power supply decisions have economic lives measured

in decades, and long-term planning is fraught with uncertainty, making it a complicated

undertaking. Technology development, electricity and commodity pricing, economic factors, and

cultural and social forces all present elements of risk to the long-term planning model.

The City Water, Light, and

Power of Springfield, Illinois

(CWLP) Integrated Resource

Plan (IRP) presents the results

of a detailed analysis of

alternatives CWLP may select

to meet the electrical energy

and demand requirements of

its retail electric consumers

for a 20-year period.

Generally, for decision-

making purposes, this period

is broken up into a near-term

actionable-decision period

and a long-term directional

period. This analysis includes

an assessment of existing

resources and alternatives for new and replacement resource options, including demand side

management alternatives. This executive summary provides a look at plan objectives,

methodology, existing resources, findings, and an overview of plan recommendations. The

complete document package includes a detailed description of the study.

The purpose of this study is to develop a robust resource plan, from a given set of input

assumptions, that:

Identifies the long-term, strategic needs of the utility, including any changes in supply-

side or demand-side resources.

Utilizes least-cost planning principles and estimates the magnitude of future power

supply costs and decisions.

Allows flexibility to respond to market changes.

Helps CWLP manage risk through a diverse mix of supply and demand-side resources.

Performs well over a range of economic, environmental, and regulatory scenarios.

Table 1: CWLP Overview

Location Springfield, Illinois

2013-2017

Average Peak

Demand

394 MW

Current

Generation

Resources

(Resource Name

– Fuel –

Maximum

Capacity – 2017

Capacity Factor –

Online Year)

Dallman 1 – Coal – 61 MW – 34.1% - 1968

Dallman 2 – Coal – 61 MW – 43.6% - 1972

Dallman 3 – Coal – 172 MW – 57.5% - 1978

Dallman 4 – Coal – 207 MW – 58.1% - 2009

Factory – Fuel Oil – 17 MW – 0.0%

Reynolds – Fuel Oil – 14 MW – 0.02%

Interstate – Fuel Oil & Natural Gas – 110

MW – 0.0% - 1997

Confidential and Business Proprietary

2018 Integrated Resource Plan 9

STUDY METHODOLOGY

A long-term generation expansion production cost model was used for this IRP to simulate

production cost and market price interaction. The optimization criterion is to minimize the

incremental Net Present Value of Revenue Requirements (NPVRR). For the purposes of this plan,

the NPVRR is the net cost that would need to be recovered for all resources in the utility's

portfolio, adjusted for the time value of money. It includes the capital costs for new or bettered

resources and any variable or ongoing fixed costs incurred during the study period. A number of

scenarios have been evaluated for this IRP. Results of each simulation have been aggregated in

the form of relative NPVRR and Levelized Cost of Energy (LCOE), along with the specific resource

retirements and additions resulting from each optimization. The LCOE is an industry-standard

metric for comparing scenarios with differing loads, calculated as total plan cost divided by

energy usage. Tools used in this study include, ABB’s PROMOD IV, Velocity Suite, Capacity

Expansion (CE), and Cambridge Energy Solution’s Dayzer.

KEY CONSIDERATIONS AND RISK FACTORS

This study is based on a set of inputs and assumptions, that, in TEA’s best judgement, will

provide CWLP with recommendations based on the most reasonable information available at

the time of this study. As time passes, some of the assumptions may not transpire as expected,

while other unexpected risk factors may become a reality. Some topics that could not be

reasonably modeled or expected at the time of the study – notably the 1100MW EmberClear

project, the possibility of fracking regulation, unanticipated environmental regulations, and

unforeseeable plant retirements close to CWLP – are not explicitly built-in to the study.

However, these possibilities are, to some degree, implicitly included by allowing power purchase

agreements, modeling multiple scenarios of varying natural gas prices, considering the High

Renewables scenario, and modeling increased renewable penetration scenarios.

Each of the plans, recommendations, actions, and potential futures discussed in this report have

the potential to impact or be impacted by regulatory, financial, market, and other types of risk.

While the CWLP Electric Division was founded with the intention of providing customers with

reliable and affordable energy, CWLP is also responsible for considering other factors such as

risk tolerance and reliability thresholds before making any decisions. For example, it is CWLP’s

responsibility to balance the potential for market risk against the potential financial risk of

acquiring additional debt servicing. The most significant risk factors which could impact the

recommendations include the following:

Rate of electric vehicle (EV) adoption and falling cost of new technology

Changes to federal, state, and local tax incentives

Changes in technological landscape over the course of the study period

Addition of large resources near CWLP’s system

Market-wide and CWLP-specific fuel diversity

Changes in environmental regulations and other public policy

Confidential and Business Proprietary

2018 Integrated Resource Plan 10

ASSUMPTIONS

Discount Rate: 3.4%

Energy Usage

Growth Forecast: -

0.8%

Demand Growth

Forecast: -0.7%

Forward Curve Mark

Date: 6/13/2018

Import/Export Limit:

325 MW/225 MW

Unforced Capacity

(UCAP) Planning

Reserve Margin

(PRM) Requirement:

8.4%

CWLP-Specific

Planning Reserve Margin Maximum to prevent costs and risks associated with excess

capacity: 50%

Data on CWLP’s existing resources and existing and potential energy efficiency (EE)

programs according to CWLP’s records and experiences

The table below provides a brief description of the supply-side resources selected by the model

in at least one scenario.

Table 2: New Supply-Side Resource Options

Resource Type Size

(MW)

Capacity

Planning

Factor

Capital

Cost

($/kW)

Fixed O&M

($/kW-Year)

Variable

O&M

($/MWh)

Conventional Combustion Turbine 198 94% $590 $18.02 $3.61

FEJA-Applicable Community Solar 1 50% $1,653 $20.00 -$85.79

Large Solar PPA 100 50% $0 $0.00 $39.00

Large Wind PPA 200 15% $0 $0.00 $26.30

Bilateral Capacity Contracts 5 100% $0 $24-$48 $0.00

FINDINGS

REFERENCE CASE

The reference case is the scenario to which all other scenarios are compared. Therefore, only

base assumptions are included. The plan resulting from this scenario is not necessarily the most

advantageous for CWLP or its ratepayers from a risk or least-cost perspective.

Figure 1: Reference Case Fuel Price Forecast

Confidential and Business Proprietary

2018 Integrated Resource Plan 11

In the

reference case

plan, CWLP’s

entire coal

fleet retires by

2022. Dallman

1, 2, and 3 all

retire in June

2020, which is

the first

month their

retirement

was allowed

due to

existing

capacity

transactions.

Dallman 4

retires as soon as a replacement resource can be built to satisfy the transmission requirements

Dallman 4 currently serves. The replacement resource is a 198 MW Conventional Combustion

Turbine, with an approximately $120 million overnight construction cost. This plan meets CWLP’s

remaining capacity requirements through a combination of fixed-priced renewable Power

Purchase Agreements (PPAs) and capacity purchased from the market.

Although they do not provide capacity credit, the plan also includes the following economically

selected EE programs: Multi-Family All-Electric (MFAC), Social Behavior Change, and A/C Rebate.

These programs are in addition to the programs currently in place, which economically remained

online throughout the simulation. These are Heat Pump Rebate, Heat Pump Water Heater

Rebate, Home Energy Audit, Helping Homes, and City Lights. Combined, these EE programs are

projected to save CWLP about 95 gigawatt-hours (GWh) per year by 2039. This is approximately

6% of CWLP’s 2038 energy demand.

The NPVRR is $1,012 million and the levelized cost of energy (LCOE) is $43.98 per MWh.

REFERENCE CASE SOLUTION 4

Using the Multiple-Integer Programming (MIP) capabilities of CE, TEA also examined alternate

solutions based on the reference case assumptions. These results are known as Reference Case

Solutions 2, 3, and 4. All of these solutions are examined in Figure 4, but Reference Case

Solution 4 (Ref Sol 4) is of particular importance to this IRP and requires further discussion.

Though certain assumptions and dates may differ when implemented into a real-world scenario,

Ref Sol 4 includes all the same capacity decisions as the recommendations, with the exception of

retiring Factory. The only significant difference between this plan and the one resulting from the

reference case is that, instead of retiring Dallman 4 in 2022 and replacing it with a CT, this plan

retains Dallman 4 for the whole study period. According to the model, the additional generation

provided by Dallman 4 allows CWLP to return to its current status as a net seller in 2028.

Figure 2: Reference Case Load and Capacity Balance

Confidential and Business Proprietary

2018 Integrated Resource Plan 12

Dallman 4’s retention increased the 20-year NPVRR by $30 million, which is $1.31/MWh in terms

of levelized cost. The total NPVRR and LCOE are $1,042 million and $45.29/MWh, respectively.

SCENARIOS

This study considered a total of 10 scenarios, and ultimately modeled nine. The list below

compares their assumptions to the reference case, and Figure 4 compares the results in terms of

the near-term actionable and long-term direction decision periods discussed above.

Midcontinent Independent System Operator (MISO) Transmission Expansion Plan (MTEP)

2018 Scenarios:

o Accelerated Fleet Change (AFC)

Adds more EE, demand-response (DR), and renewables

Uses higher load and gas price forecasts

Applies carbon reduction constraint of 20%

o Limited Fleet Change (LFC)

Retires fewer coal and nuclear resources

Installs fewer EE and renewable resources

Uses lower load and gas price forecasts

o Distributed & Emerging Technologies (DET)

Increased EE, energy storage, and renewables

Energy forecast adjusted to account for EV adoption

Locally controlled scenarios

o Flat CWLP Coal Price (FLC)

Maintains current coal price in nominal dollars throughout study

o High CWLP Coal Price (HC)

Increases coal price by 25% after current contract expiration

Disallows retirement of Dallman 4

Figure 3: Ref Sol 4 Load and Capacity Balance

Confidential and Business Proprietary

2018 Integrated Resource Plan 13

o Keep Dallman 3 & 4 (KD)

Disallows retirement of Dallman 3 and 4

o High CWLP Renewables (HR)

Requires 30% of CWLP’s energy to be served by renewables

Conditions were ultimately satisfied in the reference case

Non-impactable Scenarios

o NYMEX Gas Price (NYMEX)

Uses the NYMEX forward curve for Henry Hub

All other assumptions match the reference case

o Seasonal Extremes (SE)

Adjusts load for extreme weather events occurring every five years

All other assumptions, except the carbon dioxide (CO2) emissions

constraint, align with AFC

o Stricter Environmental Regulations (SER)

Adds carbon penalty pricing based on Regional Greenhouse Gas Initiative

(RGGI) Cost Containment Reserve price

Uses market topology of the AFC scenario with the load and gas price

assumptions of the reference case

Figure 4: Scenario Results and Decisions Overview

Retire

D1-2

Retire

D3

Add

EE

Replace

D4

Build FEJA

Solar

Add

PPAs

Add

PPAs

Retire

Factory

Retire

Interstate

Replace

D4

LCOE

($/MWh)

LCOE

Delta

NPVRR

($M)

NPV

Delta

Reference ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ NA $43.98 - $1,012 -

AFC ✔ ✔ ✔ ✔ ✔ ✔ ✔ $43.36 $0.62 $998 $14

LFC ✔ ✔ ✔ ✔ ✔ ✔ NA $41.25 $2.73 $931 $81

DET ✔ ✔ ✔ ✔ ✔ ✔ ✔ $43.99 -$0.01 $1,063 -$51

FLC ✔ ✔ ✔ ✔ ✔ ✔ $42.78 $1.20 $985 $28

HC ✔ ✔ ✔ NA ✔ ✔ ✔ ✔ NA $46.85 -$2.87 $1,079 -$66

HR - - - - - - - - - - - - - -

KD ✔ NA ✔ NA ✔ ✔ ✔ ✔ NA $53.39 -$9.41 $1,252 -$240

NYMEX ✔ ✔ ✔ ✔ ✔ NA $39.31 $4.67 $905 $108

SE ✔ ✔ ✔ ✔ ✔ ✔ ✔ $43.11 $0.87 $992 $20

SER ✔ ✔ ✔ ✔ ✔ ✔ ✔ NA $46.90 -$2.92 $1,073 $61

Ref Sol 2 ✔ ✔ ✔ ✔ ✔ ✔ ✔ NA $44.19 -$0.21 $1,017 -$5

Ref Sol 3 ✔ ✔ ✔ ✔ ✔ ✔ ✔ NA $45.09 -$1.11 $1,038 -$26

Ref Sol 4 ✔ ✔ ✔ ✔ ✔ ✔ ✔ $45.29 -$1.31 $1,042 -$30

Key: ✔ = Selected - = Not studied NA = Not Applicable

Near-Term Actionable 20-Year MetricsLong-Term Directional

See Appendix A for definitions.

Confidential and Business Proprietary

2018 Integrated Resource Plan 14

RECOMMENDATIONS

The recommendations resulting from this study are based on the economics of each decision

according to the inputs determined by The Energy Authority, Inc. (TEA). These inputs were

selected according to TEA’s best judgment based on industry experience, private and

government research, vendor information, and CWLP records.

Retire Dallman 1, 2, and 3 as soon as feasible given each unit’s current capacity

obligations. No scenario economically retained these units. Through the KD scenario, this

study shows that retaining Dallman 3 adds $210 million to the 20-year NPVRR.

Issue Request for Proposal (RFP) to meet expected capacity needs. The majority of

lower-cost PPAs included in this analysis have been backed by renewable generation, but

CWLP may also consider non-renewable PPAs, forward market purchases delivered to

CWLP, or pure capacity contracts. Any one or combination of these options may be the

best fit when considering contract price, market prices, congestion risk, and other factors.

Retain Dallman 4 until at least the next IRP cycle begins in three to five years. Retaining

this unit maintains fuel diversity and dispatch optionality and provides a hedge against

the predominantly gas-driven market. Additionally, the incremental cost of retiring the

unit ranged from +4% to -3% in comparable scenarios. The margin is insufficient to

conclusively determine the impact of this decision on CWLP.

Retain peaking units until at least the next IRP cycle. According to the fixed costs

reported by CWLP, these units cost less to maintain than they earn in capacity revenue.

Fund existing and additional EE Programs, including the MFAC, Social Behavior

Change, and A/C Rebate Programs.

Construct a 2 MW community solar facility eligible to receive funding from the Future

Energy Jobs Act (FEJA) program. This legislation is currently under appeal and municipal

utilities may not be eligible to receive funding. TEA recommends consulting legal counsel

on the likelihood of receiving FEJA funding prior to taking action on this project.

DISCLAIMER

This document was prepared by TEA, solely for the benefit of CWLP. TEA hereby disclaims (i) all

warranties, express or implied, including implied warranties of merchantability or fitness for a

particular purpose, and (ii) any liability with respect to the use of any information,

recommendations, or methods disclosed in this document. Any unauthorized commercial use of

this document by third parties is prohibited. The recommendations resulting from this study are

based on the economics of each decision according to the inputs available to TEA. The

recommendations are subject to change as the underlying facts and assumptions change.

CWLP’s final action plan may reasonably differ from the TEA’s recommendations due to various

local, organizational, or other considerations not factored into these recommendations.

Confidential and Business Proprietary

2018 Integrated Resource Plan 15

Section 1: Introduction

INTEGRATED RESOURCE PLANNING

An Integrated Resource Plan (IRP) is the result of a comprehensive planning study, which

provides a recommended mix of supply- and demand‐side resources a utility may use to meet

its customers’ future electricity needs. An IRP should include:

A demand forecast over a 20-year time horizon.

An assessment of supply‐side generation resources.

An economic appraisal of renewable and non‐renewable resources.

An assessment of feasible conservation and efficiency resources.

A least-cost plan for meeting the utility’s requirements.

An action plan.

This IRP should guide City Water, Light, and Power of Springfield, Illinois (CWLP) in making

decisions about the capacity resources it will use to meet future load and reserve obligations.

Having a long-range resource plan enables CWLP to provide affordable, reliable electricity to the

people it serves well into the future and may better equip it to meet many of the challenges

facing the electric utility industry.

The IRP process is an effort to anticipate key challenges which CWLP may face within 20 years.

Primarily, this means determining how much capacity CWLP may need and when it may be

needed. These projections are used to identify the optimum mix of energy and capacity

resources to meet such demands. Evolving technology, and regulations have implications for the

best path forward for CWLP, but each component of the plan will take time to implement.

CWLP must allow adequate time to properly study, engineer, site, and conduct environmental

reviews to modify existing resources or build additional generation and transmission

infrastructure. Given the long lead times required to plan, permit, and build new resources, the

IRP demand forecasts typically involve 10- to 20-year outlooks. CWLP will use a 20-year time

horizon.

All of these activities entail varying levels of risk and uncertainties, which this IRP attempts to

account for in its analysis and recommendations. To reduce the risks associated with relying too

much on a specific fuel type or resource type, it is important that CWLP maintains a mix of

energy resource options, including natural gas, energy efficiency, and renewables.

IRP DEVELOPMENT

A typical IRP process is diagramed in Figure 5. The process begins with an evaluation of existing

resources and a load forecast, which are used to determine if new or replacement resources are

required to meet system reliability requirements. Next, the IRP process evaluates which supply-

and demand-side alternatives best meet plan objectives under a variety of possible scenarios.

This stage also considers risk limitations on the basis of physical, policy, regulatory, financial, and

non-financial risks. The Energy Authority, Inc. (TEA) evaluates potential resources based on

physical feasibility and cost. The process ends with the presentation of TEA’s recommendations

Confidential and Business Proprietary

2018 Integrated Resource Plan 16

and this report. As part of the IRP process, CWLP may develop an action plan that identifies the

steps that should be taken over the next three to five years to implement the IRP

recommendations.

METHODOLOGY

This study uses a long-term generation expansion production cost model to aid in identifying

the most cost effective generation replacement and expansion plan. The Capacity Expansion1

(CE) electricity production cost model was used to simulate CWLP’s production cost and electric

market interaction. This model includes features which optimize future resource choices from a

given set of input alternatives and constraints.

The optimization criterion is to minimize the incremental Net Present Value of the Revenue

Requirements (NPVRR or NPV) for the identified revenue requirements while honoring system

and regulatory constraints. For the purposes of this plan, the NPVRR is the net cost that would

need to be recovered for all resources in the utility's portfolio, adjusted for the time value of

money. The NPVRR includes the capital costs for new or bettered resources and any variable or

ongoing fixed costs incurred during the study period. It does not include variable or ongoing

fixed costs incurred more than 10 years after the study period, costs that would be avoided by a

1 Capacity Expansion is licensed from ABB Group and part of the e7 platform.

Figure 5: Typical IRP Process Diagram

Confidential and Business Proprietary

2018 Integrated Resource Plan 17

retirement suggested in the plan, or sunk costs such as the cost of existing debt servicing. Sunk

costs are not included because they cannot be avoided by any action CWLP could take following

the IRP. Potential changes or improvements to CWLP’s transmission and distribution system are

beyond the scope of this IRP, except where necessary to facilitate retirement of existing units. In

these instances, such transmission upgrade costs have been incorporated at rates provided by

CWLP staff.

The model provides the mathematically optimal selection of future resources based on a set of

input assumptions, a list of alternative resource types and sizes, and certain constraints such as

import limits and minimum required reserve margin. CE facilitates multi-area economic dispatch

and unit commitment zones.

A number of scenarios have been evaluated for this IRP. Results of each simulation have been

aggregated in the form of relative incremental NPVRR along with the specific resource additions

resulting from each optimization. For all projects which are completed or can no longer be

canceled, the capital investments in existing resources are a sunk cost and thus are not included

in the forward-looking resource plan. This IRP does, however, incorporate future fixed and

variable operations and maintenance (O&M) cost for existing resources and planned capital

expenses which will not be performed if the unit is retired. While many of these fixed costs are

not avoidable in the short-run, they can be avoided entirely if the existing resources can be

retired and replaced with new, more cost-effective options.

Other tools used in this study include, ABB’s PROMOD IV, Velocity Suite, and Cambridge Energy

Solution’s Dayzer.

While NPV is a generally accepted method to compare the economics of various alternatives, it

does present some limitations which require consideration:

Different investments (various size, type and timing) which have the same present value

may have significantly different project lives and different salvage values (costs).

Investments with the same net present values may have different cash flows within the

study period.

Assumptions of future cash flows, interest rates, and investment costs cannot be known

with certainty.

Although the portfolio selection does account for costs and benefits continuing 10 years

beyond the study period, the NPV calculation included herein does not.

CWLP OVERVIEW

CWLP is a division of the City of Springfield, Illinois, providing both electric and water services to

the community. It currently owns and operates four coal units which provide over 500 MW of

generating capacity, along with 141 MW of combustion turbines. The fleet is dispatched by the

Midcontinent Independent System Operator (MISO) market, but it primarily exists to serve

CWLP’s peak demand and energy requirements.

Confidential and Business Proprietary

2018 Integrated Resource Plan 18

DEMAND

CWLP has experienced a growth rate of -1.3% per year from 2007-2017, before weather

adjustment. TEA projects CWLP’s total load will continue to grow at a rate of -0.8% per year.

CWLP’s highest system peak occurred in 2006 at 451 MW and the average peak for 2013-2017

was 394 MW. TEA projects a 386 MW peak load in 2019, with a forecasted growth rate of -0.7%

per year. Summer and winter peaks are highly dependent on the weather.

The demand and energy forecasts are discussed further in Section 3.

EXISTING RESOURCES

CWLP’s current generation portfolio consists of four coal-fired steam turbines (ST), two oil-fired

combustion turbines (CT), and one dual-fuel CT capable of burning oil and natural gas. The four

STs constitute the Dallman Power Station and serve as the primary generating resources serving

CWLP’s load. In total, they provide a maximum capacity of 506 MW. The largest and newest unit,

Dallman 4, provides 207 MW of that total. The three CTs, with a total capacity of 141 MW, serve

as peaking resources to both CWLP and MISO as a whole. CWLP’s portfolio does not currently

contain any renewable resources, but CWLP does manage or have plans to manage 13 energy

efficiency (EE) and demand response (DR) programs designed to reduce costs and total energy

served. All of these resources and programs are described in further detail in Section 2: Existing

Power Supply Resources.

RESERVE MARGINS AND THE NEED FOR GENERATING CAPACITY

Generating capacity is the maximum electric output an electric generator can produce under

specific conditions. Since customer demand for electrical energy varies by season and time of

day, only a portion of generating capacity resources may need to be operating at any particular

time, with the remaining capacity resources shut-down or on stand-by for the periods when

electrical demand is high and/or other generation resources are unable to operate due to

equipment malfunctions. When considering its ability to serve demand, an electric utility should

also consider the amount of electricity actually produced by the generator, or its energy

production. If a utility owns enough resources to meet its capacity requirements but those

resources are rarely dispatched by the market, then the utility will still be exposed to market risk

for its energy requirements beyond any actual energy its resources have produced.

Requirements for capacity and energy are determined by regulatory requirements and the

market in which a utility operates. CWLP, as a Balancing Authority (BA), Distribution Provider

(DP), Generation Owner (GO), Transmission Owner (TO), Transmission Operator (TOP), and

Resource Planner (RP), is bound by the reliability standards and requirements of North American

Electric Reliability Corporation (NERC) and SERC Reliability Corporation (SERC). As a member of

MISO, CWLP is currently required to maintain a planning reserve margin of 8.4% of unforced

capacity (UCAP) above its peak load, which is described in more detail in Section 2.

FUELS

In a long-term plan, the utility should consider the costs of both construction and energy

production over the life of the resource. Different types of generating resources rely on different

Confidential and Business Proprietary

2018 Integrated Resource Plan 19

fuel types and technologies resulting in a wide range of overall costs throughout the useful lives

of the resources. Over-reliance on a single fuel or resource type presents both price and

business risks; therefore, an effective resource planning process should include consideration of

fuel and resource diversity.

Coal

CWLP procures Illinois Basin (IB) coal for its Dallman Power Station from Arch Coal’s Viper mine

located approximately 15 miles from Dallman in Williamsville. The utility arranges for the coal to

be delivered by truck. CWLP’s current practice is to maintain approximately 15 days of coal

inventory on site at Dallman prior to the summer and winter seasons. For the purposes of this

study, CWLP expects to continue to burn exclusively IB coal from the Viper mine.

Natural Gas

CWLP purchases interruptible natural gas supply for its combustion turbine unit at its Interstate

plant. The natural gas is delivered to CWLP’s Interstate unit through a Panhandle Eastern

Pipeline Company lateral. CWLP also maintains fuel oil as a secondary fuel at Interstate.

CWLP uses natural gas at its Dallman plant for unit startups and building heat. Dallman gas is

supplied on the retail market by Ameren Illinois, Springfield’s natural gas local distribution

company (LDC).

Fuel Oil

CWLP procures distillate fuel oil for use in its peaking units located at the Factory and Reynolds

facilities. Fuel oil also serves as a backup fuel to natural gas at Interstate. Since CWLP uses very

little fuel oil, it maintains its reserves using infrequent, as-needed spot purchases.

Fuel Mix

Figure 6 shows CWLP’s fuel mix as a percentage of its 2.7 million MWh of net generation and

purchases for calendar year 2017. This energy provided for CWLP’s local power demand of 1.8

Figure 6: Fuel Mix of Net Generation and Purchases

Confidential and Business Proprietary

2018 Integrated Resource Plan 20

million MWh and additional demand from the MISO market. CWLP’s coal generation located at

the Dallman Power Station provided 90% of the energy. Purchases of wholesale power provided

approximately 9% of the energy and natural gas delivered the remaining 1% of CWLP’s energy

requirements.

MARKET ENVIRONMENT

Electric utilities in the United States have been undergoing profound changes in the way they

provide electrical energy to consumers over the last five decades. Fuel choice preferences have

shifted from oil, coal and nuclear in the 1960s and 1970s to natural gas and renewables in recent

years. Federal policies in the 1970s banned the use of natural gas for boiler fuel and mandated

generating units that were under construction to burn coal. These 1970s policies have shifted in

recent years to policies which greatly encourage renewable energy sources and discourage the

use of coal.

Technological changes have dramatically impacted fuel choices. These include evolution of

highly efficient advanced technology gas turbine generators and combined cycle units along

with unprecedented advances in the methods used to extract natural gas and oil from shale

rock, leading to a surplus of supplies and relatively low prices for these fuels. These fundamental

market shifts have caused natural gas to be the fuel of choice for nearly all new thermal

generation in the last ten years.

The physical infrastructure required to produce and transmit electricity is capital intensive and

long-lived. Utilities have made large investment in power generation and transmission systems

based on expected useful lives exceeding 30 years.

CWLP’s market environment for wholesale electricity is primarily defined by the Midcontinent

Independent System Operator (MISO) Regional Transmission Organization (RTO) and its Open

Access Transmission Tariff (OATT), Operating Agreement and Reliability Assurance Agreement

(RAA). CWLP is party to these agreements. Its wholesale purchase and sale transactions are

governed by these agreements.

CWLP also owns and operates electric generation, transmission and distribution systems which

are used to provide electrical service to its retail electric customers. This IRP addresses long-term

plans for its wholesale energy and capacity market, and potential changes to the transmission

and distribution system are beyond the scope of this IRP. See Methodology starting on page 16

for more information.

MISO is a not-for-profit member-based organization that ensures reliable, least-cost delivery of

electricity across all or parts of 15 U.S. states and one Canadian province. In cooperation with

stakeholders, MISO manages approximately 65,000 miles of high-voltage transmission and

200,000 MW of power-generating resources across its footprint. The market serves more than

42 million people.

MISO facilitates a number of important functions to coordinate operation and planning of the

wholesale electric grid within its service territory. It is a stakeholder-driven organization, with

decision-making and conflict resolution achieved through a stakeholder committee structure.

Specifically, the RTO market includes:

Confidential and Business Proprietary

2018 Integrated Resource Plan 21

Congestion hedging via Financial Transmission Rights (FTR) and Auction Revenue

Rights (ARR) which enable entities to mitigate basis risk surrounding the generation-

to-load relationship.

Ancillary service markets which procure operating reserves such as regulation,

spinning, and supplemental reserves necessary to maintain system reliability. These

ancillary services are co-optimized with energy requirements and cleared in the most

economical manner across the footprint.

Capacity markets which allow utilities to purchase capacity for the upcoming

planning year in order to meet market or governmental reserve guidelines. This

short-term market can be used to defer a major decision, but it is a short-term

tactical plan and not a long-term strategic solution.

Because MISO manages an electric transmission grid which crosses state boundaries and

involves wholesale power transactions, it is subject to federal regulation under the Federal

Power Act. MISO’s primary governing regulatory body is the Federal Energy Regulatory

Commission (FERC), with input from state regulators when appropriate. All tariffs, rates, and

operating agreements associated with this wholesale market are subject to FERC approval,

including any changes which are made to these important agreements.

POTENTIAL IMPACT OF LAWS AND REGULATIONS

ENERGY EFFICIENCY

The federal government has established a number of incentives and mandates to achieve

improvements in end-use EE. Programs such as appliance efficiency standards, interconnection

standards, low-income assistance, and loan and grant programs have helped decrease electrical

demand and retail energy sales. Much of these impacts are believed to be implicitly recognized

in load forecasts. However, rapid changes in these laws and regulations could shift CWLP’s

electrical demand higher or lower than the current forecast.

This IRP includes the possibility of expanding EE programs beyond current levels in lieu of

adding traditional energy-generating resources. While EE may be mutually beneficial for both

the end-use consumer and CWLP, it is important to recognize the larger long-term implications

for electric rates. Utilities tend to have high fixed costs which are largely recovered via variable

retail rates. If EE-influenced demand declines faster than fixed costs, utilities may have to change

their rate levels and structure to include either a higher fixed rate or higher variable rates,

although the consumer’s total bill may decline.

RENEWABLE RESOURCE MANDATES

Many states and/or local governments have established Renewable Portfolio Standards (RPS)

which mandate the local electric Load Serving Entities (LSE) to utilize renewable energy

resources such as solar, wind, and biomass for a specified percentage of its annual energy

requirements. Though such a requirement currently exists in the state of Illinois due to the

Illinois Power Agency Act of 2007, it does not apply to municipal utilities such as CWLP.

Although the reference case of this study does not include an RPS, the High Renewables

Confidential and Business Proprietary

2018 Integrated Resource Plan 22

scenario requires CWLP’s portfolio to consist of 30% renewable energy by 2030. This standard

and timeline is based on a variety of regional and international standards including but not

limited to the Illinois RPS and the Paris Climate Accords.

FUEL DIVERSITY

Risk Management principals suggest that having dependence of a single source of supply for

any commodity is a significant risk factor. This is particularly true for fuel supply for a utility’s

power generation facilities and even more so for fuels or resources that have other constraints,

such as the intermittency of renewables and the prioritization of natural gas service to firm

customers over non-firm transportation for electric generation.

CWLP’s current fleet runs on a combination of coal, fuel oil, and natural gas. CWLP’s service

reliability is enhanced by maintaining coal inventory on-site at the Dallman plant and by the

close proximity of Arch Coal’s Viper mine which supplies Dallman. Since CWLP has not

purchased firm transport of natural gas for economic reasons, it may not be able to receive

natural gas during very cold periods when end users with firm transport do not release any

excess capacity. Therefore, before adding additional gas-fueled resources or transitioning to a

mostly gas-fueled fleet, CWLP should consider the risk of being unable to purchase fuel when it

needs it most. CWLP estimates that natural gas is unavailable five hours out of the year, on

average. With a power import limit of 325 MW and existing non-gas resources, CWLP can

import enough power from the rest of MISO to support the majority of its load during most fuel

shortage and unavailability events.

CARBON DIOXIDE EMISSIONS MITIGATION

The discussion and debate on the potential impact of greenhouse gas (GHG) emissions on

climate change has moved the United States Congress and Environmental Protection Agency

(EPA) to consider laws or regulations to reduce anthropogenic carbon dioxide (CO2) emissions.

Though no nation-wide program currently exists, there is a possibility that some form of a GHG

emissions mitigation program will evolve in the future. The EPA recently put forth for

consideration the Affordable Clean Energy (ACE) rule, which would guide the development of

state plans to reduce CO2 emissions from existing units by setting performance standards for

those units. Meanwhile, some states have implemented their own programs to mitigate GHG

emissions, including California and several northeastern states participating in the Regional

Greenhouse Gas Initiative (RGGI).

This study is focused on finding the least-cost path forward for CWLP to meet its reliability and

capacity needs, and does not consider potential environmental or climate impacts of new or

existing resources or advocate for any alternative on the basis of potential impacts. It merely

attempts to help prepare a utility for how the social, political, and regulatory environment will

affect the cost and availability resources in the future. Given the political nature of this topic,

regulatory assumptions including tariffs, tax credits, portfolio requirements, and emissions

requirements can change quickly and often, so utilities should take care to account for this risk

when planning for their future.

For this IRP, two scenarios will examine the potential impact of a GHG mitigation requirement

on the portfolio. The first is the Accelerated Fleet Change (AFC) scenario, which includes all the

Confidential and Business Proprietary

2018 Integrated Resource Plan 23

market updates in and prices calculated from the MISO Transmission Expansion Plan (MTEP)

future of the same name. The second is the Stricter Environmental Regulations scenario, which is

based on the AFC but with differences discussed in Section 7. Since no CO2 emission restrictions

currently apply to CWLP, none have been modeled in the reference case.

OTHER EMISSIONS CONSTRAINTS

This study includes an examination of two key emissions constraints on CWLP’s system. Both of

these constraints are held constant throughout all scenarios.

The most significant and complex is the federal Cross-State Air Pollution Rule (CSAPR)2, which

restricts sulfur dioxide (SO2) and nitrogen oxide (NOx) emissions. The EPA divides the total

number of allowances into the country by state, and the state then disperses them further as it

sees fit. In Illinois, the allowances are assigned to each generator but may be used by any

generator in the same fleet. The rule sets allowances for both annual and seasonal emissions,

where the ozone season is defined as May through September. As emitting units retire, the

owner’s loses the allowances associated with that unit and the replacement of allowances

cannot be predicted or guaranteed. Therefore, this study assumes that the addition of a new

emitting resources will lead to no additional allowances, which may cause a decrease in

allowable generation.

The flue gas desulfurization systems equipped on all resources at the Dallman Power Station

mitigate the emissions of SO2, making NOx allowances the driving constraint of this regulation.

According to CSAPR, CWLP must not exceed its Assurance Provision of 500 tons of NOx per

ozone season. The Assurance Provision is a calculated emissions level which includes EPA

allowances and any additional allowances CWLP could reasonably purchase without incurring

the risk of penalties. Because allowances are allocated per unit, CWLP will lose a portion of its

allowances with each unit retirement. Allowances expire five years after the retirement of their

associated unit.

The other constraint is a cap on carbon monoxide (CO) emissions, which only pertains to

Interstate. Due to its classification as a synthetic minor source under Illinois law3, Interstate

cannot emit more than 249 tons of each NOx, CO, SO2, and other pollutants within any

consecutive 365 days. Of the pollutants included in this regulations, CO has the highest

emissions rate at Interstate and therefore drives when the unit can no longer generate.

ELECTRIC VEHICLE INCENTIVES

The rate of electric vehicle (EV) adoption may have a profound impact on how CWLP forecasts

load, as well as the need for additional supply-side resources and distribution-level upgrades to

the system. National, state, and local regulations could hinder or advance adoption of EVs.

CWLP should stay abreast of community interest and the actions of various governing bodies to

inform the need to further study EVs and their impact on CWLP’s future.

2 § 40 CFR Parts 51, 52, 72, 78, and 97 3 § 40 CFR 72.2

Confidential and Business Proprietary

2018 Integrated Resource Plan 24

On September 24th, 2018, the Illinois Commerce Commission issued a Notice of Inquiry (NOI)

regarding electric vehicles. This NOI is non-decisional, but may establish the groundwork for

future rulemaking. However, electric vehicle adoption in Illinois has been relatively slow to date,

and neither TEA nor CWLP anticipate significant EV-related impacts to load in the next few years.

However, quantified inclusion for load associated with EVs is included as part of the Distributed

& Emerging Technologies (DET) scenario, consistent with MISO’s approach.

FEDERAL, STATE, AND LOCAL TAX CREDITS AND INCENTIVES

Though the federal government offers some loan and grant programs for those interested in

investing in renewables, the most significant incentives to encourage development of renewable

resources are the federal production tax credit (PTC) applicable to wind generation and

investment tax credit (ITC) applicable to solar generation.

Federal tax credits have served as one of the primary financial incentives for renewable energy

(RE) deployment in the United States over the past two decades. The PTC was first enacted as

part of the Energy Policy Act of 1992 and has historically played a significant role in supporting

wind energy. The ITC of 30% for solar projects was initially established in the Energy Policy Act

of 2005. Since their initial inceptions, federal renewable tax credits have been extended,

modified, and nearly expired numerous times. Historically, changes in federal tax policies have

been highly correlated with year-to-year variations in annual RE installations, particularly for

wind, where the U.S. wind industry has experienced multiple boom-and-bust cycles that

coincided with PTC expirations and renewals.4

Prior to the passage of the Consolidated Appropriations Act of 2016 in December 2015, the PTC

had expired and the ITC was set to decline at the end of 2016. The Consolidated Appropriations

Act of 2016 extended these ITC and PTC deadlines by five years from their prior scheduled

expiration dates, but included ramp downs in tax credit value during the latter years of the five-

year period. Notably, the act kept the commenced-construction provision for the wind PTC and

extended the provision to the ITC for utility-scale and commercial solar.

Table 3 summarizes the wind and solar tax credit schedule before and after the act was passed.

In the new policy, the dates for all categories except Residential Host-Owned Solar ITC change

from being based on “placed-in-service” dates to “commenced-construction” dates.

Due to the nature of the credit, non-taxable entities such as CWLP are unable to directly capture

the economic value associated with the federal PTC and ITC. As such, most assets eligible for tax

credits are attained through Purchased Power Agreements (PPAs) whereby the producer, who is

a taxable entity, retains the incentives and then offers a more competitive rate to the non-

taxable entity.

TEA does not closely monitor changes and updates to state and local incentives, laws, or

regulations. Therefore, we rely heavily on each client to inform us of any current or anticipated

items that would impact our studies. One such item considered in this study is the Illinois Future

4 Ryan Wiser et al., 2017 Wind Technologies Market Report, U.S. Department of Energy Office of Energy

Efficiency and Renewable Energy, August 2018, http://eta-

publications.lbl.gov/sites/default/files/2017_wind_technologies_market_report.pdf

Confidential and Business Proprietary

2018 Integrated Resource Plan 25

Energy Jobs Act (FEJA) which creates significant state-level payments for both utility-scale and

community solar development. The impact of FEJA has been included in resource assumptions

where appropriate.

Table 3: Wind and Solar Federal Income Tax Credits

2015 2016 2017 2018 2019 2020 2021 Future

Full Full 80% 60% 40% 0% 0% 0%

Utility 30% 30% 30% 30% 30% 26% 22% 10%

Commercial/Third-Party-Owned 30% 30% 30% 30% 30% 26% 22% 10%

Residential-Host-Owned30% 30% 30% 30% 30% 26% 22% 0%

0% 0% 0% 0% 0% 0% 0% 0%

Utility 30% 30% 10% 10% 10% 10% 10% 10%

Commercial/Third-Party-Owned 30% 30% 10% 10% 10% 10% 10% 10%

Residential-Host-Owned 30% 30% 0% 0% 0% 0% 0% 0%

The new policy schedules reflect "commenced-construction" dates for all categories except

Solar ITC Residential Host-Owned for which "placed-in-service" dates are shown. The prior

policy schedules reflect "placed-in-service" dates for all categories except for the wind PTC

which had a "commenced-construction" deadline of December 31,2014. The "Full" (100%) wind

PTC value is 2.3¢/kWh for electricity production over the first ten years.

Source: NREL

Solar ITC

Solar ITC

Ne

w P

oli

cyP

rio

r P

oli

cy

Wind PTC

Wind PTC

Confidential and Business Proprietary

2018 Integrated Resource Plan 26

Section 2: Existing Power Supply Resources

EXISTING SUPPLY-SIDE RESOURCES

CWLP’s current generation portfolio consists of four coal-fired STs and three CTs units. Two CTs

are oil-fired, and one is dual-fuel, capable of burning oil and natural gas.

The four STs constitute the Dallman Power Station and serve as the primary generating

resources serving CWLP’s load. Built in 2009, Dallman 4 is the largest unit and generates the

most electricity in the portfolio. Additionally, transmission studies performed by CWLP show that

a generating unit of this size is required to maintain the reliability and safety of the distribution

grid in Springfield. All four units at Dallman are equipped with flue gas desulfurization systems

to mitigate SO2 emissions and selective catalytic reduction (SCR) systems to reduce NOx

emissions.

The three CTs serve as peaking resources and are offered into the MISO market to provide

capacity and ancillary services. These resources are identified in CWLP’s System Restoration Plan,

meaning they are important to maintain the reliability and resilience of the CWLP system.

As of November 2018, the final remaining contract with NextEra Energy Resources, LLC for the

purchase of wind power capacity has expired, and CWLP’s generation portfolio consists of no

renewable generation or Purchased Power Agreements (PPAs).

ENERGY EFFICIENCY AND DEMAND-RESPONSE PROGRAMS

This IRP includes the following 6 EE and demand-response (DR) programs. For every program,

CWLP forecasted the energy reduction per year of funding.

CityLights replaces existing Springfield lighting with brighter and more energy

efficient LED lights.

Retro-Commissioning upgrades existing heating, cooling, and lighting resources to

newer, more efficient models.

Table 4: Existing Supply Resources

Generating

Unit

Prime

Mover Fuel

Max Capacity

(MW)

Min Capacity

(MW)

Online

Year

PY 2018

Capacity Factor

Dallman 3 ST Coal 172 90 1978 57.50%

Dallman 4 ST Coal 207 80 2009 58.00%

Dallman 1 ST Coal 61 46 1968 34.10%

Dallman 2 ST Coal 61 46 1972 43.60%

Factory CT Oil 17 17 1973 0.00%

Reynolds CT Oil 14 14 1970 0.02%

Interstate CT Gas and Oil 110 75 1997 13.30%

Confidential and Business Proprietary

2018 Integrated Resource Plan 27

Refrigerator Roundup provides an incentive for consumers to purchase newer

refrigerators with better than required efficiency ratings.

Helping Homes provides

insulation upgrades to low-

income members of the

Springfield community.

Home Energy Audit allows a

CWLP Energy Expert to

identify sources of unwanted

heat loss and gain and ways

to mitigate these issues.

Heat Pump Rebate and Heat

Pump Water Heater Rebate

are separate programs

providing rebates on the

corresponding technologies.

Figure 7 shows the cumulative

projected program costs and

energy reduction throughout the

study period.

20-YEAR DEMAND AND RESOURCE BALANCE

MISO currently requires CWLP to hold a planning reserve margin (PRM) of 8.4% of unforced

capacity (UCAP) above its peak load, which translates to about 17.1% of installed capacity (ICAP).

Though this requirement has historically changed every year, it has plateaued recently and is

expected to remain within a few percentage points of the current margin through the end of the

Figure 7: Existing EE Program Details

Figure 8: Demand and Resource Balance

Confidential and Business Proprietary

2018 Integrated Resource Plan 28

study period. CWLP’s ICAP currently exceeds its peak load by approximately 65% and its reserve

margin by approximately 41%. In UCAP, the corresponding numbers are about 51% and 39%.

TRANSMISSION AND DISTRIBUTION SYSTEM

CWLP’s electric transmission network can be categorized into two significant parts. The 138

kilovolt (kV) portion of the transmission network includes about 63 circuit miles of overhead

lines forming a complete loop around the service area. These lines serve nine of the system’s