Embed Size (px)

DESCRIPTION

City of Cape Town Submission on EDIR. Challenges, Successes and Proposals 27/07/2012. Content. Background Challenges, Successes (Cape Town) Alternate models Proposals. 1. 2. 4. 3. 7. 8. 5. 10. 6. 11. 12. 9. 15. 14. 16. 13. 17. 18. 19. 20. 23. 26. 22. 25. 27. 28. - PowerPoint PPT Presentation

Citation preview

City of Cape TownSubmission on EDIR

Challenges, Successes and Proposals

27/07/2012

Content

1. Background

2. Challenges, Successes (Cape Town)

3. Alternate models

4. Proposals

1. Background

1

2

3

4

56

789

1011 12

1314

1516

1718

19 2022 23

24 25

26

27 28

2930

31 32 33 3435

36373839

40 41 424344 45 46 47484950

515253

M

54

5556

2. Challenges, Successes

Challenges EDIR was to address

1.Electricity tariffs

2.Ageing networks and capital requirements

3.Ageing skilled workforce

4.Importance/impact on Local Government finances

5.Legislative environment

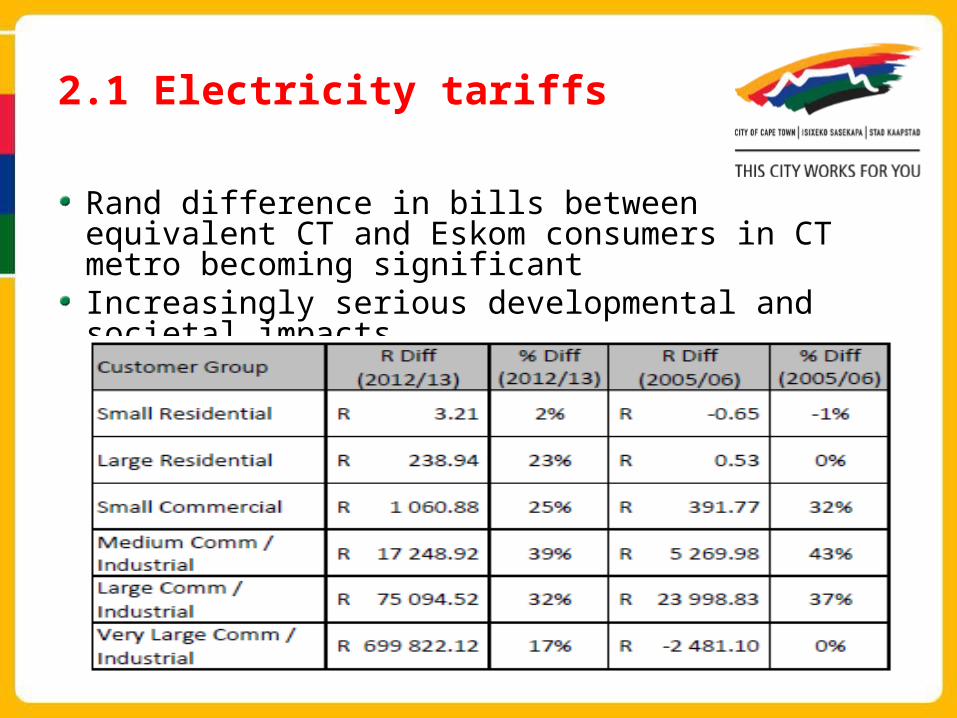

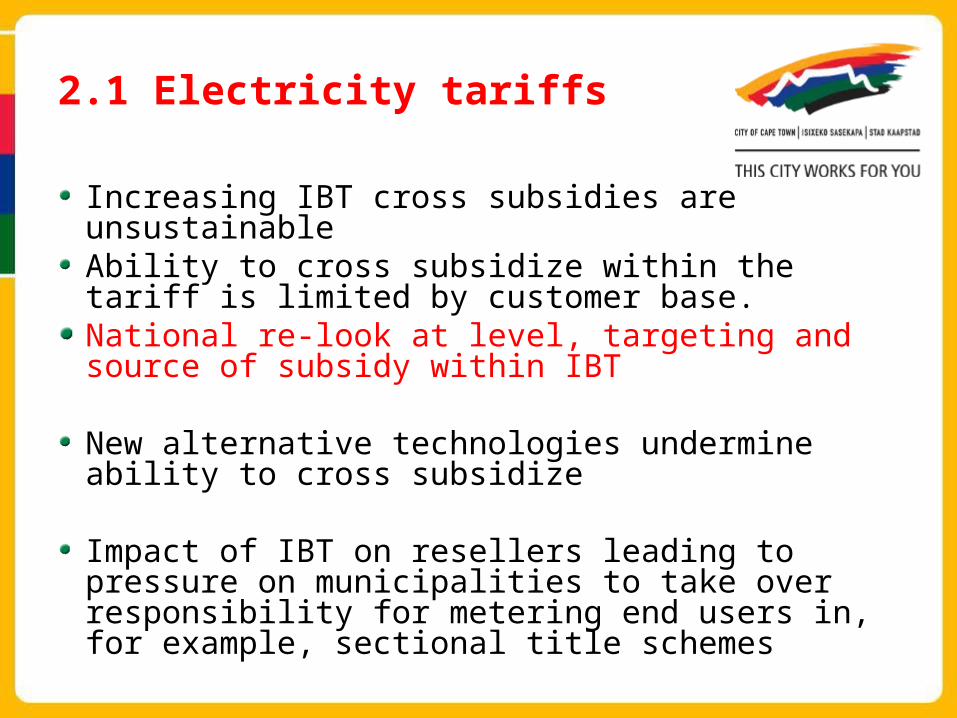

2.1 Electricity tariffs

Rand difference in bills between equivalent CT and Eskom consumers in CT metro becoming significantIncreasingly serious developmental and societal impacts

2.1 Electricity tariffs

Increasing IBT cross subsidies are unsustainableAbility to cross subsidize within the tariff is limited by customer base.National re-look at level, targeting and source of subsidy within IBT

New alternative technologies undermine ability to cross subsidize

Impact of IBT on resellers leading to pressure on municipalities to take over responsibility for metering end users in, for example, sectional title schemes

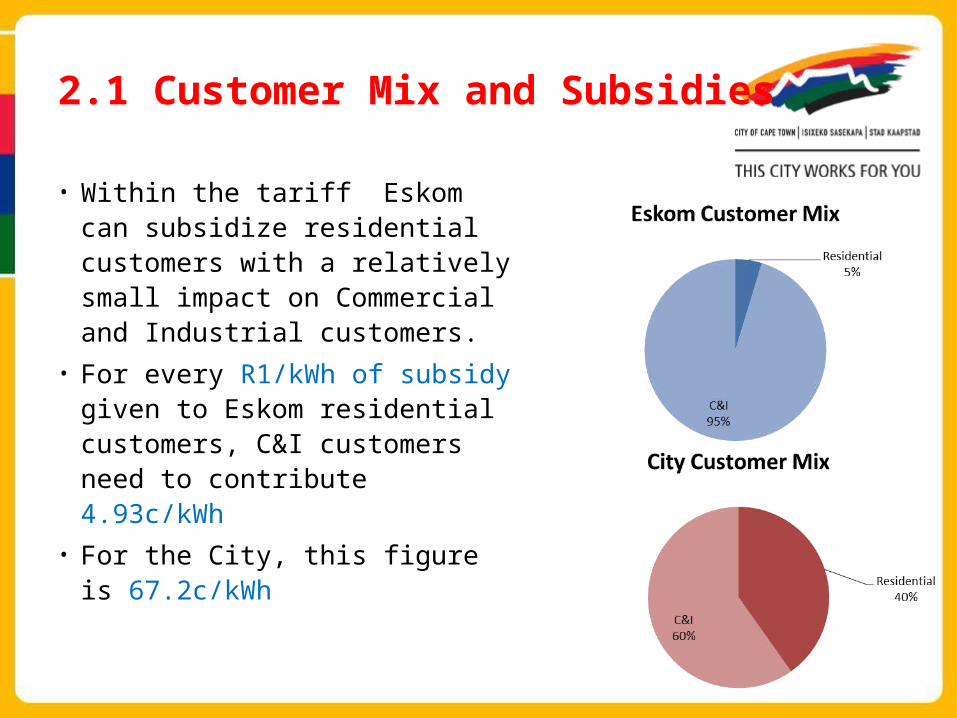

2.1 Customer Mix and Subsidies

• Within the tariff Eskom can subsidize residential customers with a relatively small impact on Commercial and Industrial customers.

• For every R1/kWh of subsidy given to Eskom residential customers, C&I customers need to contribute 4.93c/kWh

• For the City, this figure is 67.2c/kWh

2.1 Bulk Subsidy & Surcharge

Cross-subsidy in the municipal bulk tariff (to other Eskom customers)Removal of this cross subsidy in review of municipal tariffs

Eskom’s CT customers don’t pay for street-lightingEskom’s CT customers don’t contribute to City for other services (municipal surcharge)These services are beneficial to EDI and customers – roads, traffic services, fire & emergency servicesMunicipal Surcharge be introduced for Eskom customers

All CT metro customers supplied directly by same distributor

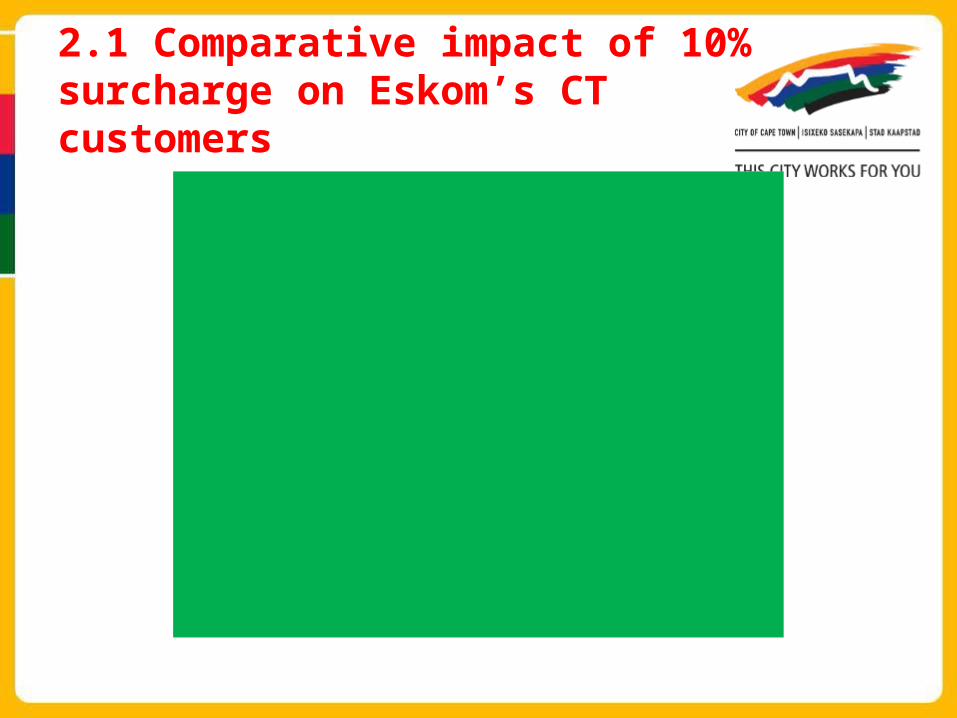

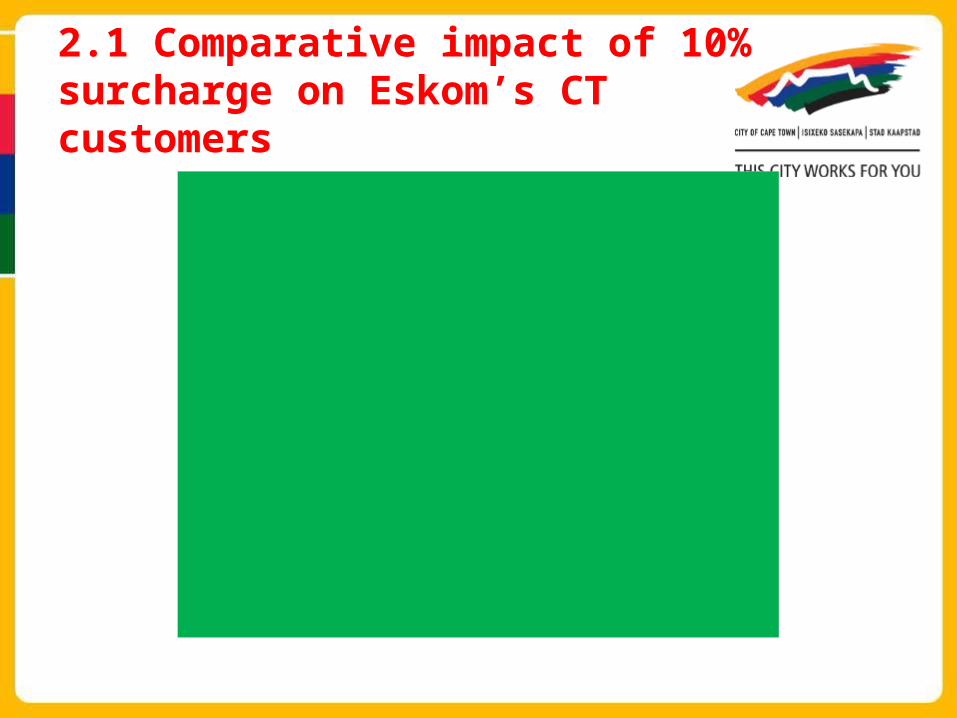

2.1 Comparative impact of 10% surcharge on Eskom’s CT customers

R -

R 200.00

R 400.00

R 600.00

R 800.00

R 1,000.00

R 1,200.00

R 1,400.00

Small Residential Large Residential

City

Eskom

Eskom +10%

R -

R 1,000,000.00

R 2,000,000.00

R 3,000,000.00

R 4,000,000.00

R 5,000,000.00

R 6,000,000.00

Large Commercial/Industrial Very Large Commercial/Industrial

City

Eskom

Eskom +10%

2.1 Comparative impact of 10% surcharge on Eskom’s CT customers

2.2 Ageing networks and capital requirements

National Infrastructure backlog

(R27bn+R2.5bn pa EDIH 2008)

Valuation of assets

Implementation of Enterprise Asset Management (EAM) on SAP Plant Maintenance Module

R100m pa MV switchgear programme

On-going ability to raise and recover capital through ring-fenced Electricity Services and tariffs

Capex requirements determined through EAM

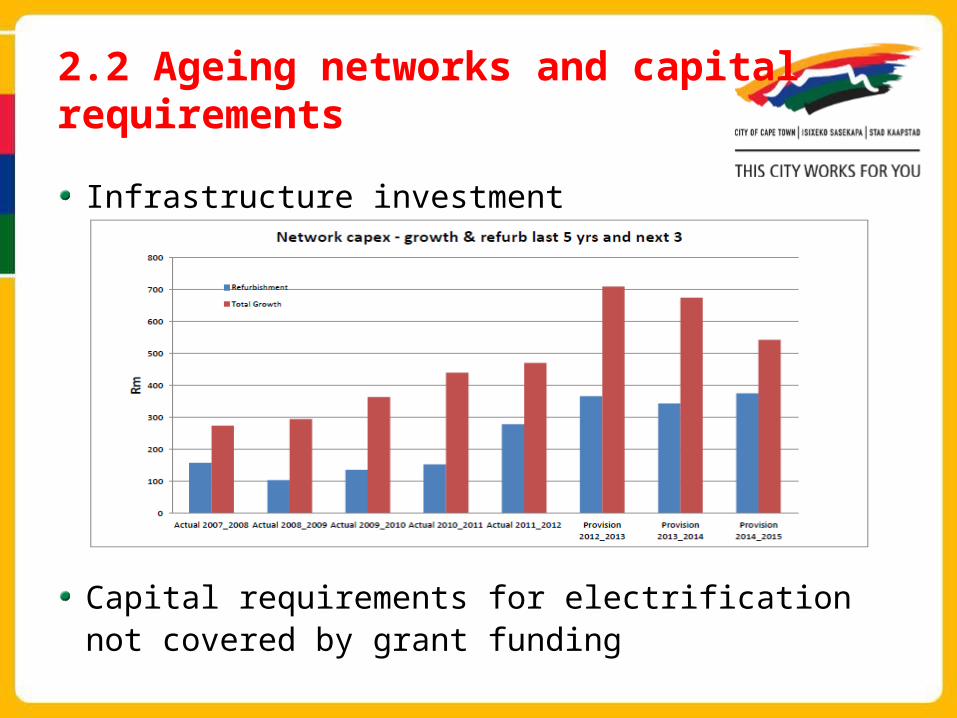

2.2 Ageing networks and capital requirements

Infrastructure investment

Capital requirements for electrification not covered by grant funding

2.3 Ageing skilled workforce

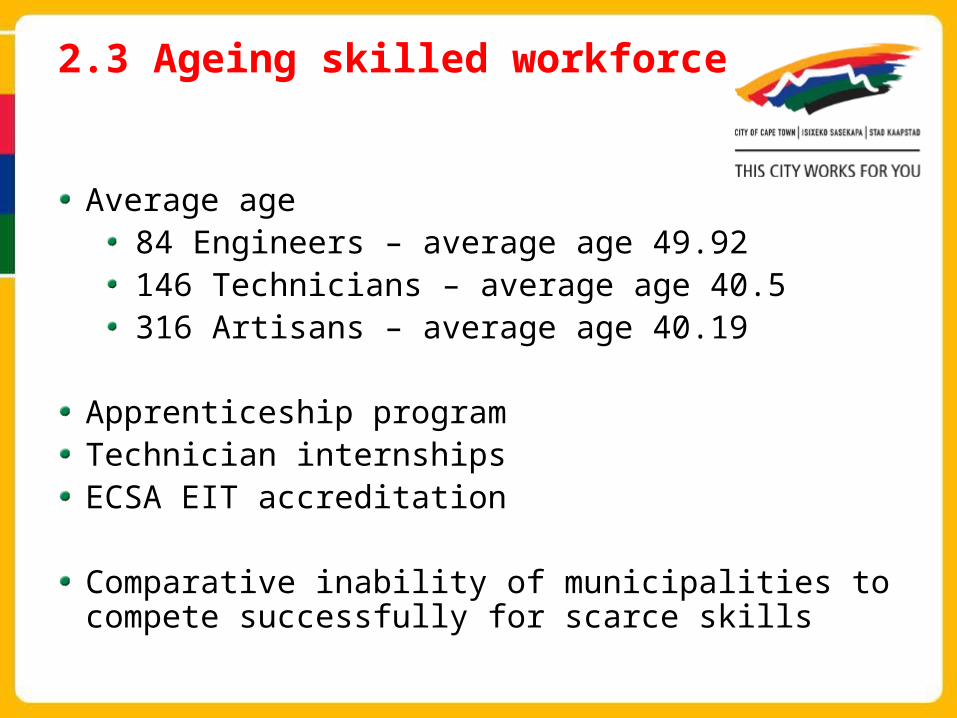

Average age84 Engineers – average age 49.92146 Technicians – average age 40.5316 Artisans – average age 40.19

Apprenticeship programTechnician internshipsECSA EIT accreditation

Comparative inability of municipalities to compete successfully for scarce skills

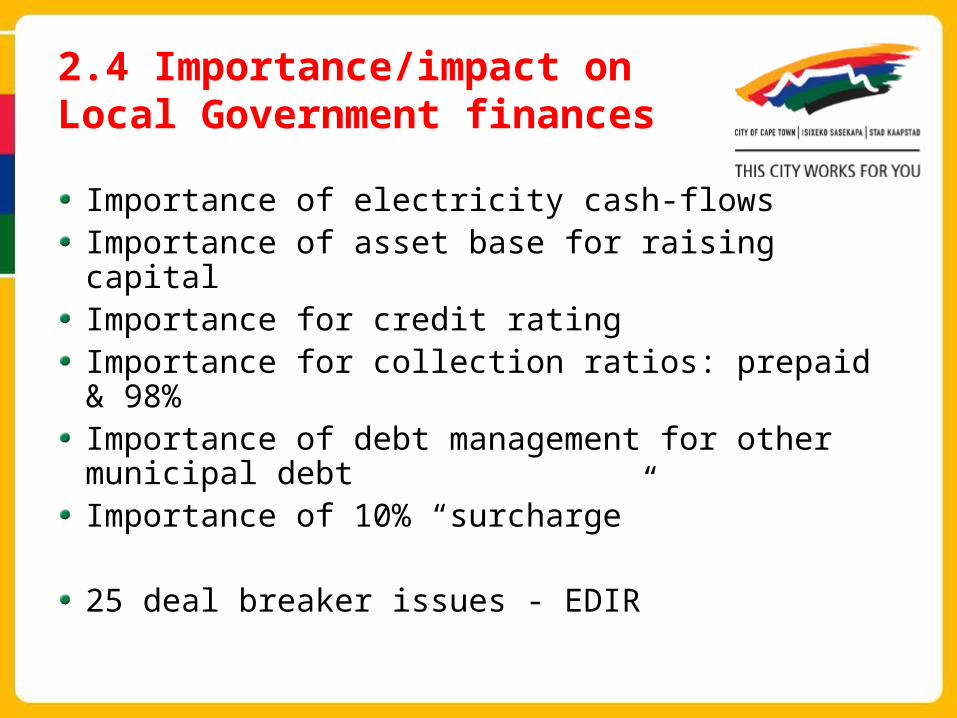

2.4 Importance/impact on Local Government finances

Importance of electricity cash-flowsImportance of asset base for raising capitalImportance for credit ratingImportance for collection ratios: prepaid & 98%Importance of debt management for other municipal debtImportance of 10% “surcharge”

25 deal breaker issues - EDIR

2.5 Legislative environment

Electricity reticulation is an exclusive Local Government power and function (Constitution of SA)

Tariff approval (Nersa vs Council)

Approval timeframes

Eskom has not signed SDA with municipalities

RRM vs NT chart of accounts

3. Alternate EDIR models

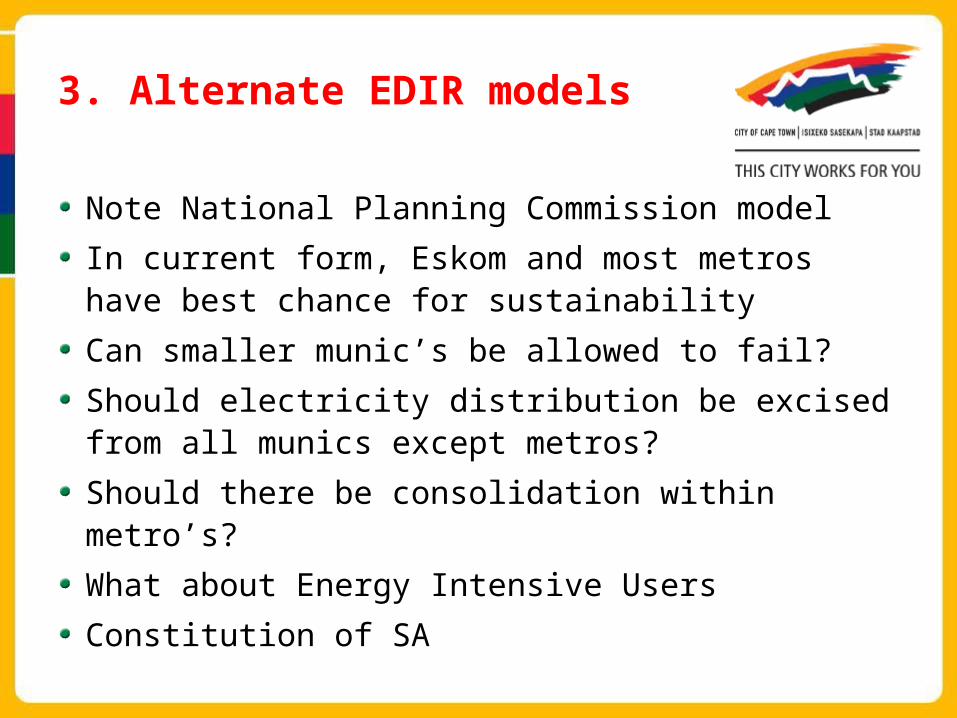

Note National Planning Commission model

In current form, Eskom and most metros have best chance for sustainability

Can smaller munic’s be allowed to fail?

Should electricity distribution be excised from all munics except metros?

Should there be consolidation within metro’s?

What about Energy Intensive Users

Constitution of SA

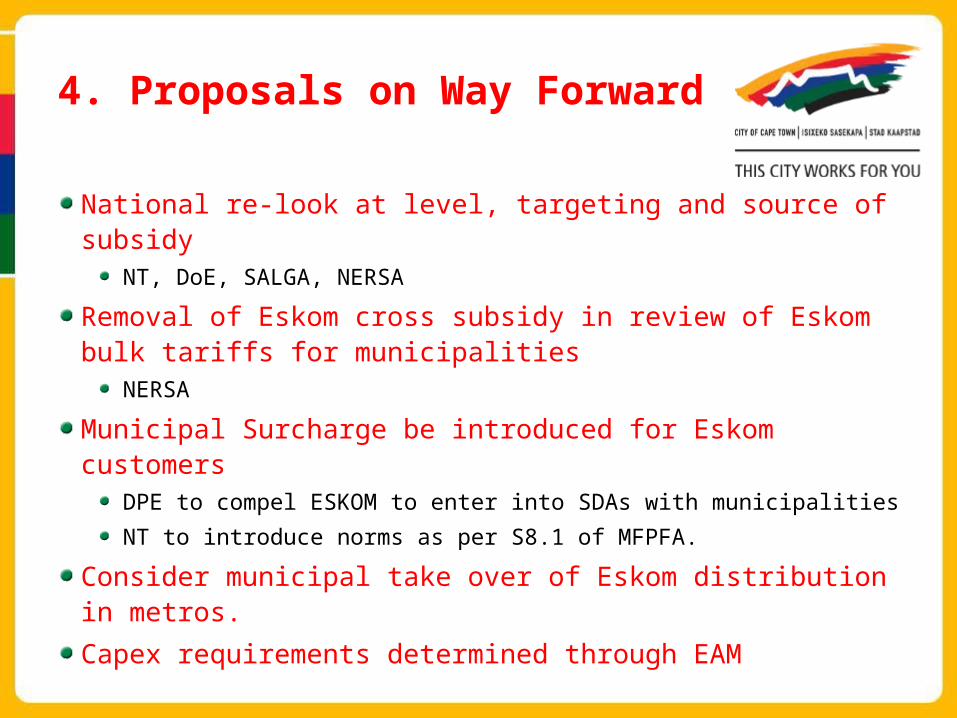

4. Proposals on Way Forward

National re-look at level, targeting and source of subsidyNT, DoE, SALGA, NERSA

Removal of Eskom cross subsidy in review of Eskom bulk tariffs for municipalities

NERSA

Municipal Surcharge be introduced for Eskom customersDPE to compel ESKOM to enter into SDAs with municipalities

NT to introduce norms as per S8.1 of MFPFA.

Consider municipal take over of Eskom distribution in metros.

Capex requirements determined through EAM

Thank you

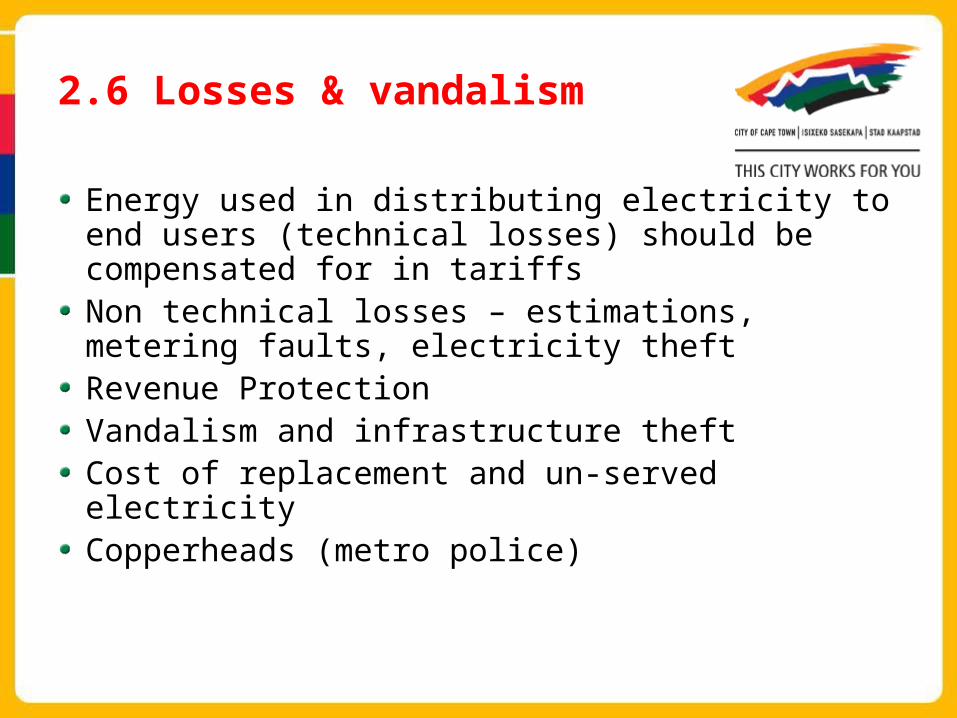

2.6 Losses & vandalism

Energy used in distributing electricity to end users (technical losses) should be compensated for in tariffsNon technical losses – estimations, metering faults, electricity theftRevenue ProtectionVandalism and infrastructure theftCost of replacement and un-served electricityCopperheads (metro police)

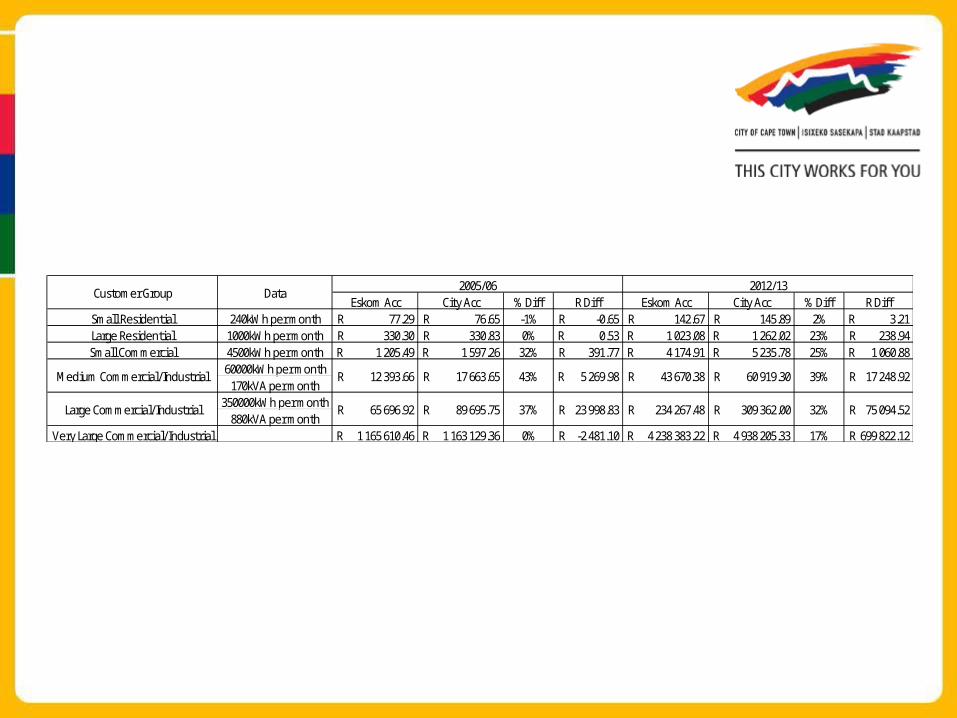

Eskom Acc City Acc % Diff R Diff Eskom Acc City Acc % Diff R DiffSmall Residential 240kWh per month 77.29R 76.65R -1% -0.65R 142.67R 145.89R 2% 3.21R Large Residential 1000kWh per month 330.30R 330.83R 0% 0.53R 1 023.08R 1 262.02R 23% 238.94R Small Commercial 4500kWh per month 1 205.49R 1 597.26R 32% 391.77R 4 174.91R 5 235.78R 25% 1 060.88R

60000kWh per month170kVA per month

350000kWh per month880kVA per month

Very Large Commercial/Industrial 1 165 610.46R 1 163 129.36R 0% -2 481.10R 4 238 383.22R 4 938 205.33R 17% 699 822.12R

2005/06 2012/13

Medium Commercial/Industrial

Large Commercial/Industrial

12 393.66R 17 663.65R 43% 5 269.98R 43 670.38R 60 919.30R

DataCustomer Group

39% 17 248.92R

65 696.92R 89 695.75R 37% 23 998.83R 234 267.48R 309 362.00R 32% 75 094.52R