Embed Size (px)

Citation preview

China & Hong Kong Latest Transfer Pricing Developments

www.pwc.com/tp

Navigating through the complexity

June 2015

Disclaimer

The materials of this seminar/workshop/conference are intended to

provide general information and guidance on the subject concerned.

Examples and other materials in this seminar/workshop/conference are

only for illustrative purposes and should not be relied upon for technical

answers. The Hong Kong Institute of Certified Public Accountants (The

Institute), the speaker(s) and the firm(s) that the speaker(s) is

representing take no responsibility for any errors or omissions in, or for

the loss incurred by individuals or companies due to the use of, the

materials of this seminar/workshop/conference.

No claims, action or legal proceedings in connection with this

seminar/workshop/conference brought by any individuals or companies

having reference to the materials on this seminar/workshop/conference

will be entertained by the Institute, the speaker(s) and the firm(s) that

the speaker(s) is representing.

PwC

Agenda

3

1Introduction and recent developments of Base Erosion and Profit Shifting (BEPS)

2 Recent developments in transfer pricing regulations and enforcement in China

3 Advance Pricing Arrangement regime in China and Hong Kong

4 In a nutshell

PwC

Introduction and recent developments of Base Erosion and Profit Shifting (“BEPS”)

PwCPwC 5

BEPS

Overview

Current updates

OECD’s Actions and Deliverables

in 2014

The Impact

SAT’s response

Recent BEPS

update

PwC

In the headlines…

6PwC

PwC

BEPS: Base erosion and profit shifting

Commissioned by G20 and devised by the OECD

Domestic and international tax rules fail to keep pace with changing business models. Lack of coherence of tax rules between countries. TP rules permit separation of profits from economic substance.

• Shifting profits in ways that erode the taxable base to locations with favourable tax treatment

• No or unduly low tax

• Consensus driven approach involving alignment of domestic rules, changes to Model DTAs and Commentary and Transfer Pricing Guidelines

What is BEPS?

How to address BEPS?

Wh

o i

s d

riv

ing

th

e B

EP

S p

ro

jec

t?

Wh

y d

oe

s B

EP

S a

ris

e?

PwC 8PwC

BEPS

Overview

Current updates

OECD’s Actions and Deliverables

in 2014

The Impact

SAT’s response

Recent BEPS

update

PwC

Addressing Base erosion and profit shifting

Current update……

• G20 summit

• <Addressing Base Erosion and Profit Shifting> (12 February 2013)

• <Action Plan on Base Erosion and Profit Shifting> (19 July 2013)

• Any new update?

9

Addressing Base Erosion and Profit Shiftinghttp://www.oecd-ilibrary.org/taxation/addressing-base-erosion-and-profit-shifting_9789264192744-en

Action Plan on base Erosion and Profit shiftinghttp://www.oecd.org/tax/beps.htm

PwC 10PwC

BEPS

Overview

Current updates

OECD’s Actions and Deliverables

in 2014

The Impact

SAT’s response

Recent BEPS

update

PwC

OECD 15 Actions and 7 Deliverables for 2014

11

1 Addressing the tax challenges of the digital economy

2 Neutralising the effects of hybrid mismatch arrangements

3 Strengthening CFC rules

4 Limiting base erosion via interest deductions and other financial payments

5 Countering harmful tax practices more effectively, taking into account transparency and substance

6 Prevent treaty abuse

7 Artificial avoidance of PE status

PwC

OECD 15 Actions and 7 Deliverables for 2014

12

8 Align TP outcomes with value creation: intangibles

9 Align TP outcomes with value creation: risks and capital

10 Align TP outcomes with value creation: other high risk transactions

11 Establish methodologies to collect and analyse data on BEPS and the actions to address it

12 Require taxpayers to disclose their aggressive tax planning arrangements

13 Re-examine TP documentation

14 Make dispute resolution mechanisms more effective

15 Develop a multilateral instrument

PwC 13PwC

BEPS

Overview

Current updates

OECD’s Actions and Deliverables

in 2014

The Impact

SAT’s response

Recent BEPS

update

PwC

Impact of BEPS…

14

Nexus

• Review of the taxation principles applicable to the digital business

• Widening the definition of PE

Transfer pricing

• Substance.

• Attribution of profit to the PE

• Intangibles: Legal ownership vs economic ownership

• Further documentation obligations

Financing

• Hybrids

• Further attention to financial transactions with related parties.

• Limitations to deduct interest expenses

Anti-abuse

• Additional anti-abuse legislation is expected.

• Tax inspection could focus more in the review of anti-abuse legislation.

PwC 15PwC

BEPS

Overview

Current updates

OECD’s Actions and Deliverables

in 2014

The impact

SAT’s response

Recent BEPS

update

PwC

China SAT’s Responses and Opinions

16

SAT Announcement on 17 September 2014

SAT Propaganda Conference on BEPS

Project on 25 September 2014

• Showing strong supportive gesture to the OECD’s BEPS project

• Establishing a BEPS task force within the SAT

• Taking this opportunity to improve China's domestic tax rules and international tax administration capabilities

• Identifying 15 unacceptable tax practices

• Emphasizing SAT’s view of the OECD recommendations

• Providing the SAT’s observations on specific BEPS Action Plans

• Sharing the SAT’s action plans on an international level and domestic level to address BEPS timetable

PwC

15 Unacceptable Tax Practices (1/2)

17

SAT’s official identified 15 unacceptable tax practices, which reflect the SAT’s determination to tackle BEPS issues in China:

Base Erosion and Profit Shifting

Double / Multiple Non-taxation

Aggressive Tax Planning

Tax Regimes that are not Transparent

Holding Structures or Transactional Arrangements

without Economic Substance

Deduction of Inappropriate Costs

Loss incurred by Chinese

Subsidiaries with Single / Simple

Functions

Treaty Abuse

PwC

15 Unacceptable Tax Practices (2/2)

18

SAT’s official identified 15 unacceptable tax practices, which reflect the SAT’s determination to tackle BEPS issues in China:

Unreasonable Over-pricing of

Intangibles

Remuneration Inconsistent with

Function and Contribution to Value Creation

High-Tech Company with Low

Profit Margins

China's Location Specific Advantages

not Observed

Losses Transferred from Foreign Entities to the

Chinese Subsidiaries

Refusal to Provide Data / Information /

Documentation to Chinese Tax Bureaux

upon Request

Hybrid Mismatch Arrangements for the Purpose of Tax

Avoidance

PwC

SAT’s increased focus on Anti-avoidance

19

In a recent public seminar, an SAT official has reiterated the SAT’s increased focus on anti-avoidance. The following trend shown during the seminar shows the increase in tax revenue from SAT’s continuous and relentless effort in combating and cracking down the cross border tax avoidance and evasion:

Published by SAT during a public seminar in April 2015

2014年中国反避税贡献税款523亿元

PwCPwC

Jiangsu State Tax Bureau’s Recent Development on International Taxation Administration

Jiangsu STB is the first and only provincial tax bureau, which had established a specific branch to centralise the transfer pricing investigation and APA administration.

• Jiangsu State Tax Bureau (“Jiangsu STB”) is well known for its sophistication and aggressiveness in transfer pricing investigation.

• In June 2014, Jiangsu STB issued a paper entitled <Administrative Plan on international tax compliance for 2014-2015>, summarizing their current stance towards the BEPS Action Plan and highlighting the most important tax risks in an international context for MNEs.

20PwC

PwC

Jiangsu STB’s Administrative Plan on international tax compliance for 2014 — 2015

21

• Establish off-shore structure to avoid tax jurisdiction• Base erosion by cross-border investment or financing• Erosion of the profit of domestic enterprise by overseas output of intangible

assets• No report or under-report of overseas income by overseas investing

enterprises• Functional restructure and mismatch of economic substance and profit level• Profit transfer by means of associated outbound payment• Lowering the tax burden of the whole group by off-setting intercompany

transactions• Profit transfer by means of purchasing overseas associated enterprise with

unreasonable price• Provide associated R&D service without responding gains or returns• Benefit the whole group by assuming implicit cost without corresponding

compensation• Tax avoiding transactions by means of shell company in tax heaven or

offshore account • Not report capital gains obtained by taking advantage of start-up period• Avoid non-resident tax obligation thorough three-party contract

Tax risks of cross-border taxation

PwC 22PwC

BEPS

Overview

Current updates

OECD’s Actions and Deliverables

in 2014

The impact

SAT’s response

Recent BEPS

update

PwC

Recent Updates

OECD 15 Actions and 7 Deliverables for 2014

23

1 Addressing the tax challenges of the digital economy

2 Neutralising the effects of hybrid mismatch arrangements

3 Strengthening CFC rules

4 Limiting base erosion via interest deductions and other financial payments

5 Countering harmful tax practices more effectively, taking into account transparency and substance

6 Prevent treaty abuse

7 Artificial avoidance of PE status

PwC

Recent Updates

OECD 15 Actions and 7 Deliverables for 2014

24

8 Align TP outcomes with value creation: intangibles

9 Align TP outcomes with value creation: risks and capital

10 Align TP outcomes with value creation: other high risk transactions

11 Establish methodologies to collect and analyse data on BEPS and the actions to address it

12 Require taxpayers to disclose their aggressive tax planning arrangements

13 Re-examine TP documentation

14 Make dispute resolution mechanisms more effective

15 Develop a multilateral instrument

PwCPwC

Issue date Action Plans Key message

31 March’15 Action 12 Require taxpayers to disclose their aggressive tax planning arrangements

Sets out a standard framework for a mandatory disclosure regimethat ensures consistency while providing sufficient flexibility to deal with country specific risks and to allow tax administrations to control the quantity and type of disclosure

3 April’15 Action 3Strengthen CFC Rules

Focuses on developing recommendations for the design of CFC rules to combat BEPS

16 April’15 Action 11Establish methodologies to collect and analyse data on BEPS and the actions to address it

Improve availability and analysis of data on BEPS, including to:

• monitor the implementation of the Action Plan and;

• evaluate effectiveness and economic impact of actions to address BEPS on an ongoing basis

29 April’15 Action 8Assuring that TP outcomes are in line with value creation Intangibles

To ensure contributions are tantamount to the benefits received under a CCA

15 May’15 Action 7Prevent the artificial avoidance of PE status

Expansion of scope of existing PE rules

22 May’15 Action 6Prevent Treaty Abuse

Includes a simplified Limitation on Benefits (LOB) Article for inclusion in the OECD Model Income Tax Convention and provides ‘conclusions and proposals’ on 20 targeted issues

Recent BEPS updates - At a glance

25PwC

PwCPwC

Discussion Draft on Revisions to Chapter VIII of the Transfer Pricing Guidelines on Cost Contribution Arrangements (“CCAs”)

• On 29 April 2015, the OECD released a discussion draft proposals under Action 8 of the BEPS Action Plan

26PwC

BEPS Update

• Proposed fundamental modifications to Chapter VIII of the OECD Transfer Pricing Guidelines with respect to measuring the value of contributions to CCAs and the tax characterisation of contributions, balancing payments and buy-in/ buy-out payments; and to make it consistent with other BEPS amendments including those addressing the fundamental issues on risk, capital, recharacterisation and intangibles

• Consistent with the underlying concept of BEPS initiative, the primary goal of the proposed revision – to ensure contributions are tantamount to the benefits received under a CCA

• The OECD invited targeted comments on these proposals by 29 May 2015 The input will be discussed during a public consultation on 6/7 July 2015

PwCPwC

OECD releases revised BEPS proposals on Permanent Establishments

• On 15 May 2015, the OECD released revised proposals on the Permanent Establishments (PE) rules in Article 5 of the OECD Model Tax Treaty

27PwC

BEPS Update

• On 15 May 2015, the OECD released revised proposals on the Permanent Establishments (PE) rules in Article 5 of the OECD Model Tax Treaty

• Scope of dependent agent rule is expanded (including narrowing the scope of independent agent rule)

• Scope of specific activity PE exemptions is narrowed

• Proposed anti-fragmentation rule to prevent abuse of the PE rules by segregating activities across associated entities

• Expansion of the scope of existing PE rules

PwC

Recent developments in transfer pricing regulations and enforcement in China

PwC 29PwC

TP in China

China TP regulations

Intangibles

Intra-group

services

Investments in/ out of

China

Location Specific

Advantages

PwC

Briefly, SAT’s recent focus area of international tax development in China:

30

• To take part in international tax rules formulation along the principle of “profits should be taxed in the location where economic activities take place and values are created”

• To improve domestic tax laws and systems• Revision of Tax Collection and Administration Law and Individual

Income Tax Law (in 2 or 3 years)• Tax regulations recently issued: SAT Order No.31, SAT Public Notice

[2015] No.7, SAT Public Notice [2015] No.16• To formulate detailed tax rules regarding controlled foreign

corporation and hybrid mismatch

• To strengthen anti-avoidance measures and Exchange of Information

PwC

Briefly, SAT’s recent focus area of international tax development in China:

31

• To help taxpayers by:• Making tax regulations more transparent and clarify about taxpayers

rights and obligations;• Soliciting feedback from different stakeholders in respect of tax reform in

China

• To help developing countries to upgrade their tax administration and collection capabilities, consistent with China’s One Belt One Road strategy

• Following issuance of OECD discussion draft on CCAs, SAT issued State Council Circular [2015] No. 27 effecting the below:• Remove approval requirement on a series of tax matters, including Cost

Sharing Agreement; • Cancelling the non-administrative approval of 49 items and adjusting the

approval authority of 84 items that requires government internal approval

PwC 32PwC

TP in China

China TP regulations

Intangibles

Intra-group

services

Investments in/out of

China

Location Specific

Advantages

PwC

Definition of IntangiblesOECD Perspective

33

Commercial intangibles

• Either used for the production of a good or the provision of a service.

• Or business assets transferred to customers or used in the operation of business (e.g. software)

Trade intangibles

• Often created through risky and costly R&D activities.

• E.g. patents, know-how, designs, and models

Marketing intangibles

• Product of market research or sales activities and aids in commercial exploitation or have an important promotional value.

• E.g. trade names, trademarks, customer lists, distribution channels and unique packaging

(OECD Transfer Pricing Guidelines, paragraph 6.2)

PwC

HNTE• Are the “contract manufacturing” companies

allowed to be entitled to HNTE status or to enjoy super deduction of R&D expense?

• Higher return is expected if R&D related activities are performed?

Royalty• Can the rate of royalty sustain after China’s

contribution to the value of IP becomes more notable?

34

China’s perspective: Jiangsu State Tax Bureau’s official opinions on High/New Tech Enterprise (HNTE) and royalty

PwC 35PwC

TP in China

China TP regulations

Intangibles

Intra-group

services

Investments in/out of

China

Location Specific

Advantages

Services fee for shareholder activities not deductibleSAT submitted official Response to the United Nations regarding intra-group services and management fees, reaffirming the importance of arm’s length principle on intra-group services payment

Profit shifting via outbound payments The State Tax Bureau of the Jiangsu Province issued the Administrative Plan on international tax compliance for 2014-2015, highlighted the most important tax risks in an international context for MNEs were related to BEPS

Six-point testsOutlined a ‘six-point test’ to determine whether transfer pricing adjustment is required

Scrutiny on outbound service fee and royalty feeWith the released of Circular 146, The SAT requested local-level bureaus to launch a comprehensive tax examination on the significant service fee and royalty fee payments made by Chinese enterprises to their overseas related parties

Four types of “non-deductible” payments The SAT issued Public Notice 16: Certain Corporate Income Tax Matters on Outbound Payments to Overseas Related Parties provided guidance on outbound payments to foreign related parties

Background of Public Notice 16 (“PN16”)

Mar 2014

Apr 2014

Jun 2014

Aug 2014

Mar 2015

36

Arm’s Length Principle and Authenticity test

4 types of “non-deductible” payments

Key focus of Public Notice 16

37

• No approval is required in advance of any overseas related party payments

• The tax authority is empowered to request for contracts or agreements concluded with its overseas related party, and relevant documentation within a specified period, to test the arm’s length nature of the related party payment

• The tax authority is empowered to make special tax adjustments in cases of non-compliance with the arm’s length principle

Arm’s Length Principle and Authenticity test

Enterprises must comply with the arm’s length principle when making outbound payments to avoid special tax adjustments by the tax authority; the tax authority is empowered to request for relevant related party documentations to proof the authenticity and arm’s length nature of the transaction

PublicNotice

16

Adjustment period:

10 Years(commencing from year of

transaction)

Official interpretation

38

PwC

Unqualified service fee

Unqualified overseas related parties

Royalties paid to related

parties without contribution to value creation of underlying

intangible assets

Royalties paid for incidental benefits from financing or

listing activities

4 Types of “non-deductible” payments

Non-deductible

39

PwC 40PwC

TP in China

China TP regulations

Intangibles

Intra-group

services

Investments in/out of

China

Location Specific

Advantages

PwCPwC

Implications on MNC operations in China

Global value chain vs. Profit split method

• Historical trend: setting up of certain simple functions entities in China by MNCs

• Examples: Contract manufacturers involved in R&D process; High and New Technologies Enterprises (HTNEs) enjoying preferential tax rates but pay outbound royalty to parent company

• Key question: Which party to secure profits deriving from an integrated value chain?

• China perspective: assess the importance of the entities, to justify a higher return of the single function performed

• Indicative changes towards Profit Split concept in China’s tax landscape

• Potential usage of the profit split method will increase in China bringing additional income to the country

• Flip side: whether Chinese tax authority is willing to accept the losses from the implementation of the profit split method?

41PwC

PwCPwC

Implications on outbound investments from China

Principal structure model vs. Profit split method

• Historical trend:

• setting up of headquarters in lower tax jurisdictions by Chinese entities, economic activities remain in China

• Chinese operating company pays management fee/ royalty to offshore “headquarters”, which have no economic substance

• China perspective: challenge the substance of offshore “headquarters” and assess the importance of the economic activities of China operating company

• Key question: whether profit split method is appropriate to capture the contribution of Chinese operating companies?

42PwC

In a recent public seminar, the Deputy Director of SAT International Taxation Department (Ms. Wang Xiaoyue) has shared her the SAT’s agenda to enhance administration for outbound investments: formulating CFC implementation rules, Foreign Tax Credit management, Information Sharing System, expansion of knowledge database of more countries’ tax systems.

PwC 43PwC

TP in China

China TP regulations

Intangibles

Intra-group

services

Investments in/out of

China

Location Specific

Advantages

PwCPwC

The attribution of location savings and market premium

• OECD: location savings do not belong automatically to one party but must be allocated in line with the bargaining situation

- Need to determine the appropriate allocation of location savings: the arm’s length principle (based on bargaining positions)

- Due to lack of sufficient comparable data, need to conduct a vertical analysis of entities along the value chain

• Location savings and market premium are new transfer pricing (“TP”) challenges often seen in BRICS* economies with low cost, but booming economy and huge market, such as China and India

*BRICS: Brazil, Russia, India and China

44

Market premium: pull of sales volume and price

Location savings: reducing prices of factors of production

PwC

Quantification and allocation of location specific advantages

45

Unique features in China limiting relevance of non-Chinese companies as comparables

• Fast economic growth, rising income and a huge consumer base with great purchasing power creating imbalance of supply and demand

• Impact of government regulations and policies on production and consumption

• Consumer general preference to foreign brands

Location savings and market premium

China authorities apply LSAs in transfer pricing investigations and APA negotiations

PwC

Advance Pricing Arrangement (“APA”) regime in China and Hong Kong

PwC

SAT Reports China completed Eight Bilateral APAs, 11 Unilateral APAs, in 2013

47

Key development:

China’s SAT releases its annual APA

report for 2013

Key takeaway:China signs 8 BAPA and 11

Unilateral Agreements in

2013

What’s next:Demand for

BAPAs continues to outstrip the SAT’s limited staff resources

PwC

China APAs

48

1

2

3

4

In 2013, total of 11 unilateral APAs and 8 bilateral APAs, representing an all year high, among which 5 were signed with Asian countries, 2 were with European countries, 1 was with North American country.

5

From 2005 to 2013, 147 intentions of formal applications for bilateral APAs (of which 37 were concluded) were received. The number of APA applications will continue to increase.

By 31 December 2013, cumulative total of APAs signed is 104, 67 unilateral and 37 bilateral.

Due to lack of resources in SAT, significant requests for APA are waiting for acceptance.

For new APA application, different type of related party transactions (e.g. services, intangibles), an innovative application of TP method (e.g. profit split method), or a high-quality analysis for intangibles and market premium will get SAT’s attention and priority consideration.

PwC

2003 2005 2006 2007 2008 2010 2011 2012 2013 2014In

Progress

Hong Kong DTA Network

Belgium

Thailand

MainlandChina

Luxembourg

Vietnam

Brunei

Netherlands

Indonesia

Hungary

Kuwait

Austria

UnitedKingdom

Ireland

Liechtenstein

France

Japan

New Zealand

Portugal

Spain

Czech Republic

Switzerland

Malta

Jersey

Malaysia

Mexico

Canada

Italy

Guernsey

Qatar

Korea

SouthAfrica

United Arab

Emirates

Bahrain

Bangladesh

Finland

Germany

India

Israel

Latvia

Macao SAR

Mauritius

Pakistan

Romania

Russia

Saudi Arabia49

PwC

Hong Kong APA program’s development

50

HK APA is still progressing

• APA program was introduced in 2012 with cautious optimism in Hong Kong• Associated practical challenges were fully apprehended• APA is accepted as an effective dispute resolution mechanism

HK APA experience

• IRD is open to fair negotiations with enterprises• Shift in bilateral relationship between IRD and enterprise• Reduce TP audits and consequential adjustments and penalties

Snapshot of APA filings

• Trade: distribution, wholesaling, service, manufacturing, research and development

• BAPA partners: Mainland, Netherlands, Japan, Korea• TP methodology: TNMM-FCMU, TNMM-operating margin, cost plus, profit

split• Processing time of BAPA concluded: 15 to 24 months• Period of BAPA concluded: 5 years

PwC

Hong Kong APAs

HK IRD very encouraging of APA

applications

Five APA applications accepted by the HK IRD

to date

Two concluded negotiations with

Netherlands and Japan

Open and transparent approach is one of the

key success factors

Source: Information as at 31 October 2014 per IRD comments at a public seminar

51

PwC

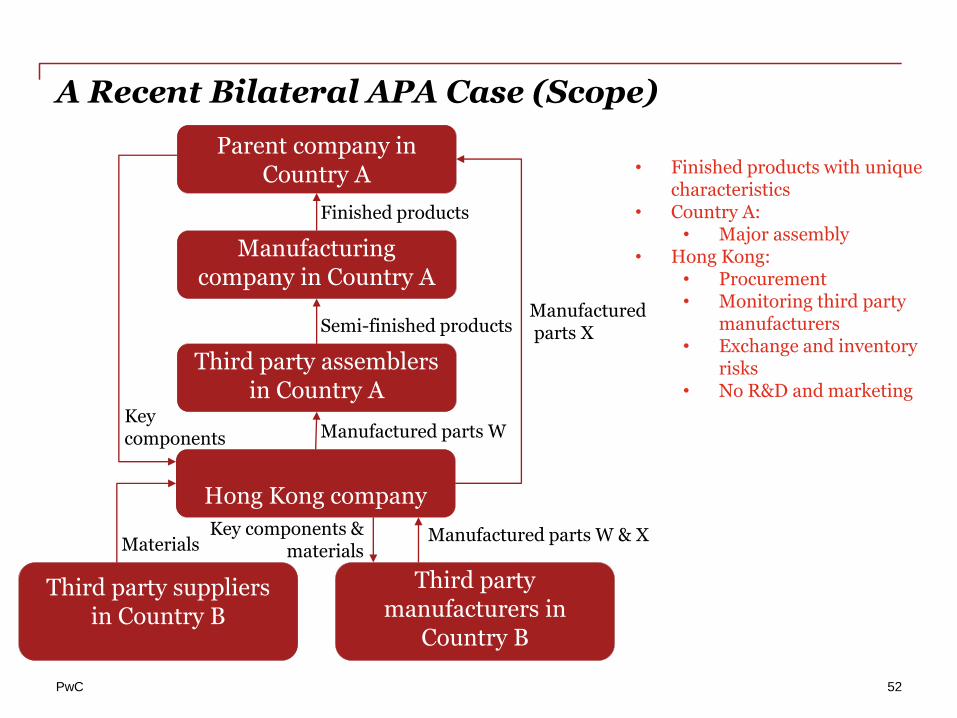

A Recent Bilateral APA Case (Scope)

52

Parent company in Country A

Manufacturing company in Country A

Third party assemblers in Country A

Hong Kong company

Third party suppliers in Country B

Third party manufacturers in

Country B

Finished products

Semi-finished products

Manufactured parts W

Manufacturedparts X

Manufactured parts W & XKey components & materials

Key components

Materials

• Finished products with unique characteristics

• Country A:• Major assembly

• Hong Kong:• Procurement• Monitoring third party

manufacturers• Exchange and inventory

risks• No R&D and marketing

PwC

A Recent Bilateral APA Case (Technical Issues)

53

• Business nature: wholesaler or contract manufacturer

• Review of possible internal comparables

• TNMM – Full Cost Mark-Up

• Exclusion of “extraordinary loss” from FCMU for a particular year

• Determining the arm’s length range

• Weighted average approach

• Pooled approach

• Compensating adjustment

• Term adjustment

• Year-by-year adjustment

PwC

In a nutshell

PwC

Managing TP risks

55

(a) Review the current risk profile, identify “high risk” areas and take immediate actions

(b) Review the economic substance along the value chain and whether the tax arrangement is consistent with the economic substance

Proper TP documentation in place to get ready for a potential transfer pricing investigation

Effective & efficient communication maintained with local level tax bureaus

(a) Sound ongoing internal tax risk control and improve charges mechanism

(b) Sustainable intra-group charges structure

PwC

Tax function in China – Being aware of the reality

56

Be pro-active!What are the high risk areas?

Be flexible!SAT views are also development, be open-minded and adapt to the changes

Be prepared!Be aware and get ready to address unique challenges in China

Be sustainable!Tax arrangement follows economic substance, build sound tax internal control system

01 02 03 04

PwC

Thank you!

© 2015 PricewaterhouseCoopers Ltd. All rights reserved. PwC refers to

PricewaterhouseCoopers Ltd which is a member firm of PricewaterhouseCoopers International

Limited and may sometimes refer to the PwC network. Each member firm of which is a

separate legal entity. Please see www.pwc.com/structure for further details.

The information contained in this presentation is of a general nature only. It is not meant to be

comprehensive and does not constitute the rendering of legal, tax or other professional advice

or service by PricewaterhouseCoopers Ltd or any other entity within the PwC network. PwC

has no obligation to update the information as law and practices change. The application and

impact of laws can vary widely based on the specific facts involved. Before taking any action,

please ensure that you obtain advice specific to your circumstances from your usual PwC

client service team or your other advisers.

The materials contained in this presentation were assembled in April 2015 and were based on

information available at that time.