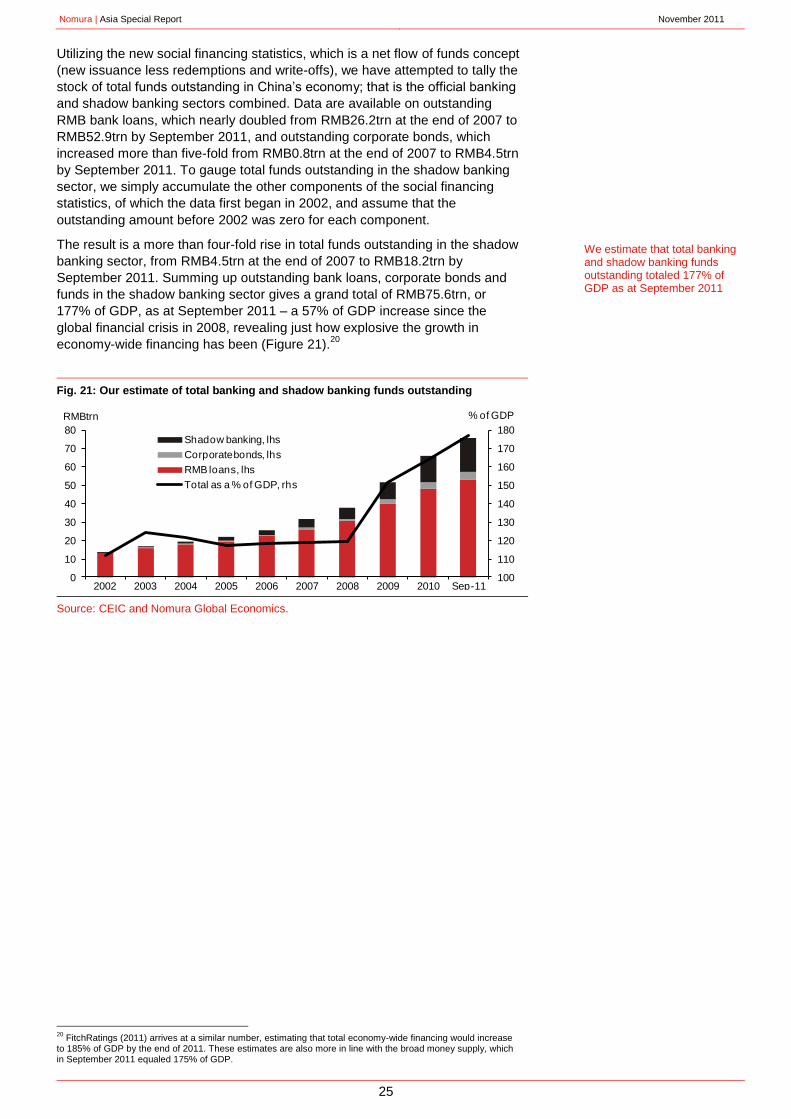

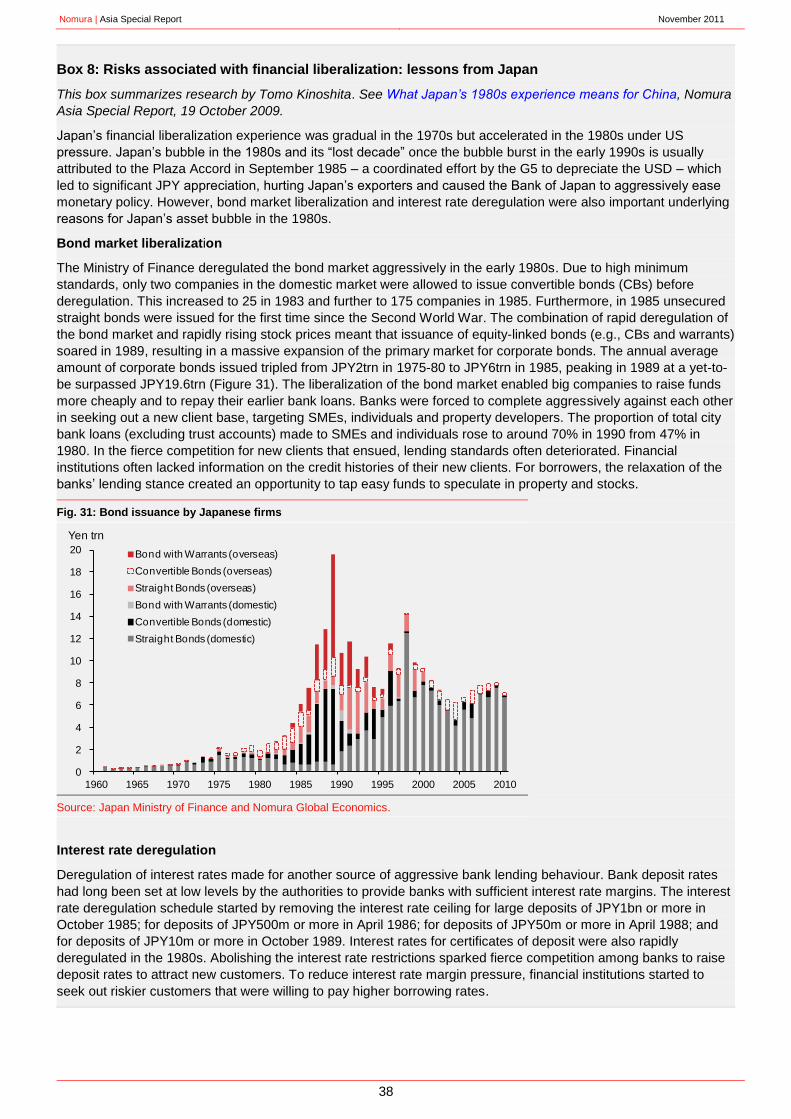

Embed Size (px)

Citation preview

China risks

We attach a one-in-three probability to China

experiencing a hard economic landing commencing before the end of 2014.

We define “hard landing” as an abrupt slowdown in real GDP growth to an average of 5% y-o-y or less over four consecutive quarters.

We discuss six key reasons why the risk of a China hard landing happening in the next three years appears to have increased.

We launch Nomura’s China Stress Index (CSI), which uses 18 indicators to summarize the macro risks in a single measure.

Our global strategy teams conduct a “what if” exercise, discussing trading recommendations and stock ideas for this non-trivial risk scenario.

GLOBAL ECONOMICS AND

STRATEGY

Novem ber 2011

AN

CH

OR

RE

PO

RT

Any portion of this report that has

been prepared by a trading desk

analyst is not a product of the

Fixed Income Research

Department and is not covered by

the Research Analyst certification

provided in Appendix A-1. For

additional information concerning

the role of Trading Desk Analysts,

please see the important conflicts

disclosures beginning at page

101 of this report.

November 2011

Research analysts

Economist

Rob Subbaraman

+852 2536 7435

Strategist

Kevin Gaynor

[email protected] +44 (0) 20 710 27800

China economy

Nomura | Asia Special Report November 2011

2

Foreword ........................................................................................................... 3

Executive summary ......................................................................................... 4

Introduction – Six reasons to worry .............................................................. 5

Defining a hard economic landing ................................................................. 8

Defining a “hard landing” ................................................................................ 8

Triggers and timing ........................................................................................ 8

Policy responses ............................................................................................ 8

Perceived likelihood ..................................................................................... 10

Nomura’s China Stress Index (CSI) ............................................................. 11

1. Overinvestment and excessive credit ..................................................... 13

Box 1: Fuzzy numbers .............................................................................. 14

Box 2: China‟s challenging GDP arithmetic .............................................. 17

Box 3: Lessons from Japan on the return and cost of capital .................. 19

2. Rudimentary monetary architecture ........................................................ 22

Box 4: Shadow banking in the US and China compared ......................... 26

3. The privileged state-owned enterprises .................................................. 28

Box 5: Investment is high, but savings are even higher ........................... 30

Box 6: The Akerlof market for lemons problem applied to China ............. 31

4. Unintended consequences of financial liberalization ............................ 33

Box 7: A chronology of China‟s capital account liberalization .................. 34

Box 8: Risks associated with financial liberalization: lessons from Japan 38

5. The Lewis turning point ............................................................................ 39

6. The setting in of growing pains ............................................................... 43

Demographic challenges .............................................................................. 43

Box 9: China‟s hukou household registration system .............................. 46

Rising inequality and an aspiring middle class ............................................ 46

Resource and environmental strains ........................................................... 51

Pricing a China hard landing – Strategy perspectives .............................. 56

Global macro perspectives ........................................................................... 59

Global equity perspective ............................................................................. 64

Asia-ex Japan FX perspective ..................................................................... 67

Implications for Asia regional equities…………………………………………69

China equities – the risk…………………………………………………….......73

Chinese credits – already reflecting the risks of a China hard landing ........ 91

References ...................................................................................................... 94

Appendix: The Construction of Nomura‟s China Stress Index ....................... 97

Nomura | Asia Special Report November 2011

3

Foreword

We are pleased to present Nomura‟s Anchor report on China, in which our

economists, strategists, equity and political analysts assess the medium-term

risk of a hard landing – a critical issue for today‟s global economy.

At Nomura, we pride ourselves in producing research of the highest standard.

Historically, we have had a strong presence across Asia, and in recent years

we have increased our footprint in Europe and the United States to become

Asia‟s leading global investment bank. Our roots in Asia allow us to see first-

hand the breakneck speed at which the region‟s economies are emerging –

and contributing over half of global GDP growth.

China leads the world in the growth stakes, but the risks in our view have risen

and should no longer be ignored. Our base case is that China's economy will

average growth of about 8.5% in 2012-14, but we judge that the risks of a

temporary interruption that pushes growth far below potential are rising. We

define a so-called “hard landing” as an abrupt slowdown in real GDP growth to

average 5% or less for at least one year. This report discusses six key factors

that lead us to attach a one-in-three likelihood that China‟s economy

commences a hard landing before the end of 2014.

How would this non-trivial risk of a hard landing in China impact global

financial markets? Our global and Asian equity, FX, rates and credit strategy

teams assess the macro implications and present trading recommendations

and specific stock ideas to this risk scenario.

How can investors calibrate the risk of this hard landing scenario? In this

report we launch Nomura‟s China Stress Index (CSI) which we will update

quarterly. The exact probability of a hard landing is necessarily a matter for

investor judgment, but the CSI will give investors an important indication of risk.

Nomura‟s Anchor series of reports underscore our dedication to produce

thematic, long-term studies, involving cross-region and cross-division

collaboration among our global markets research teams.

We welcome your feedback as we continue our tradition of collaborative work

to deliver unique investment insight and ideas to our clients.

Hideyuki Takahashi Paul Norris

Head of Global Research Head of Global Markets Research

Nomura | Asia Special Report November 2011

4

Executive summary1

This study takes China‟s still enormous economic development

potential as a given and focuses on the risks and challenges that lie

ahead – for the economy‟s meteoric rise has been associated with a

build-up of fundamental imbalances.

We define a hard economic landing in China as an abrupt slowdown in

real GDP growth to an average of 5% y-o-y or less over four

consecutive quarters.

While our base case is that China's economy will average growth of

about 8.5% in 2012-14, we discuss six compelling reasons why the

risk of a hard landing has increased. We attach a one-in-three

likelihood that a hard landing commences before the end of 2014.

Overinvestment and excessive credit. China's investment is almost

half of GDP, while domestic credit is nearly 1.5x GDP, or 1.8x if the

shadow banking sector is included. Empirical literature shows that

investment booms are more likely to trigger a crisis if they are

associated with credit booms. China ticks both of these boxes.

A rudimentary monetary architecture, centered on controlling the

exchange rate is not very effective in managing an economy that is

rapidly becoming more open and sophisticated, and has resulted in a

cost of capital that is too low and a financial sector that is repressed.

The privileged state-owned enterprises receive preferential

government subsidies and bank financing, yet they are capital

intensive, inefficient and crowd out smaller private enterprises.

Unintended consequences of financial liberalization.

Internationalization of the renminbi is adding pressure for China to

accelerate financial liberalization, but this is not without risks, such as

falling credit standards as banks overly compete with one another.

The Lewis turning point, associated with a dwindling supply of

surplus labour from the countryside, is likely upon China, which could

trigger a serious outbreak of inflation.

The setting in of growing pains from worsening demographics and

increasing strains on natural resources and the environment. These

growing pains will almost certainly cause the economy's growth

potential to slow over this decade, making it more challenging to

implement structural reforms and address high income inequality.

China's economy is now so big and complex that many of its structural

problems are becoming more interrelated. Also, many of its critical

reforms are becoming unavoidably connected, making it more difficult

to continue undertaking individual reforms gradually and in isolation.

The government would no doubt do all in its power to respond, but the

question is how large, quick and effective a policy stimulus would be.

On all three counts, we judge that it would be less than in 2008.

We are well aware that picking the exact timing of a hard landing is

devilishly difficult. The key will be whether the risk of a hard landing

rises or falls in the future. Enter Nomura's new proprietary tool, our

China Stress Index, which uses 18 indicators to summarize the macro

risks in a single measure.

Please refer to the summary pages 56-58 for strategy perspectives,

trading recommendations and stock ideas should the non-trivial risk of

a China hard landing impact global financial markets.

1 The authors of particular parts are accredited in their respective sections, but specific mention should be made

of Zhiwei Zhang, Chi Sun, Alastair Newton, Simon Flint, Pradeep Mohinani, Michael Kurtz, Ian Scott, Chien-hua Chen and Qilong Zhang. We are grateful to Candy Cheung and Wendy Chen for data analysis; David Vincent and Kenneth Persing for editing; and Jay Chandrasekharan for coordinating the equity analysts. We are also indebted to Zhiwei Zhang, Paul Sheard and Paul Norris for providing helpful comments on early drafts.

Nomura | Asia Special Report November 2011

5

Introduction – Six reasons to worry

China has made remarkable achievements in development, but it

remains the largest developing country in the world. Population,

resources and the environment have put great pressure on our

economic and social development, and there is lack of adequate

balance, coordination or sustainability in our development.

President Hu Jinato, Boao Forum for Asia, Hainan, China, 15 April 2011.

China‟s economy has averaged 10% real growth since it launched its reforms

and began to open up in 1978. In 2010 it surpassed Japan to become the

world‟s second-largest economy (Figure 1).2 Yet China is still a poor country:

its nominal GDP per capita of USD4,400 in 2010 is similar to that of Japan in

1975, suggesting that there is still lots of room to urbanize, industrialize and

move up the value-added ladder (Figure 2).3 However, as China‟s leaders

readily admit, the economy‟s meteoric rise has been associated with a build-up

of fundamental problems: the export- and investment-led growth model is

reaching its limits; macro and industrial policies need a major overhaul; the

once seemingly endless supply of cheap rural labour migrating to the cities is

diminishing; and there are the growing challenges of worsening demographics,

high income inequality, resource shortages and environmental degradation.

Fig. 1: China’s long-run real GDP growth

Source: CEIC and Nomura Global Economics.

Fig. 2: Nominal GDP per capita: China vs Japan

Source: CEIC and Nomura Global Economics.

This study takes China‟s still enormous economic development potential as a

given and focuses on the macro risks and challenges that lie ahead.

Our base case is that China's economy will average growth of about 8.5% in

2012-14, but we judge that the risks of a temporary interruption that pushes

growth far below potential are rising. We define a so-called economic “hard

landing” as an abrupt slowdown in real GDP growth to an average of 5% y-o-y

or less over four consecutive quarters. Six factors lead us to attach a one-in-

three likelihood that a China hard landing commences before the end of 2014.

1. Overinvestment and excessive credit

2. Rudimentary monetary architecture

3. The privileged state-owned enterprises (SOEs)

4. Unintended consequences of financial liberalization

5. The Lewis turning point

6. The setting in of growing pains

2 To compare the sizes of economies we convert nominal GDP into USD at market exchange rates.

3 GDP per capita in constant prices is a more appropriate yardstick to compare real purchasing power, but such

data on a consistent basis are only available back to 1960. World Bank data show that in 1960, Japan's real GDP per capita (USD7,241) was still higher than China's real GDP per capita (USD2,423) in 2010, suggesting that China's current real average standard of living is more on par with Japan's before the 1960s.

-30

-20

-10

0

10

20

30

1950 1960 1970 1980 1990 2000 2010

% y-o-y

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1970 1975 1980 1985 1990 1995 2000 2005 2010

China

Japan

USD

China's economy still has lots of room to develop, but fundamental problems have built up

Six factors lead us to attach a one-in-three likelihood that a China hard landing commences before the end of 2014

Nomura | Asia Special Report November 2011

6

While there may be many tell-tale warning signs that a hard landing is coming,

the trickiest part is getting the timing right. The conventional wisdom seems to

be that, because of political incentives, a hard landing, should there be one,

would not occur until after the transition to China‟s fifth generation of leaders in

early 2013.4 The analysis of Eichengreen, Park and Shin (2011) adds some

support to this view. They analyse a sample of 41 fast-growing economies

over the period 1957 to 2007 and find that on average these economies slow

significantly when GDP per capita on a purchasing power parity basis hits

USD16,740 – which China is unlikely to reach until 2015, at the earliest.5

However, they also show that a low consumption-to-GDP ratio, higher and

more volatile inflation, a rising old-age dependency ratio and an undervalued

exchange rate are important features that typically increase the chances of a

sharp slowdown – and China has all of these.

While we are well aware that picking the exact timing of a hard landing is

devilishly difficult, we find some compelling reasons why the risk of it

happening in the next three years should no longer be ignored.

The empirical literature on the causes of financial crises offers some pertinent

lessons to China. The first is that an extended period of high GDP growth can

mask the build-up of underlying financial problems, in part because the most

robust leading indicator of financial crises – the debt-to-GDP ratio – is flattered.

Lesson number two is that investment booms are more likely to trigger a crisis

if they are associated with credit booms. China ticks both of these boxes:

investment (public and private) comprises nearly half of GDP and domestic

credit is almost 1.5x GDP, or 1.8x if the shadow banking sector is included.

The second reason relates to China's stage of economic development – the

economy has become so big and complex that many of its structural problems

are becoming more interrelated. For example, a rudimentary monetary

architecture, centering on controlling the exchange rate, has resulted in a cost

of capital that is too low and a financial sector that is severely repressed. The

too-low cost of capital has fueled overinvestment, while the financial

repression has given rise to a flourishing shadow banking sector. Another

example is the generous government and bank support given to the less

efficient and capital-intensive state-owned enterprise (SOE) sector, which

leads to wasteful investment of scarce resources, environmental degradation

and credit rationing to private small to medium-sized enterprises (SMEs).

Rather than any one of these factors alone, we believe it is the combination of

various imbalances and interactions among them that increases the likelihood

of a major setback.

Third, increasing strains on natural resources and the environment, together

with demographic changes rapidly turning unfavorable, are causing growing

pains to set in that will almost certainly cause the economy's potential growth

to slow over the course of this decade and inflation to be structurally higher. In

an environment of slowing trend growth and higher structural inflation,

structural problems festering below the surface can bubble up to the surface,

and implementing reforms can be more challenging. For instance, removing

the generous government subsidies to SOEs, can become politically more

divisive as power and economic privilege needs to be wrested from local

governments, the SOEs and the banks.

Fourth, historically the government has implemented reforms incrementally.

However, China has reached a stage of development at which many of its

critical reforms are unavoidably connected, making it more difficult to

undertake individual reforms gradually and in isolation. For example,

internationalizing the renminbi and moving to a more flexible exchange rate

4 For example, according to a Bloomberg global survey on 29 September 2011, 1,031 of its subscribers were

asked about the chances of China‟s economy slowing below 5% growth: 12% of respondents believed it will happen within the next year, 47% within the next 2-5 years and the remainder thought longer than 5 years, or that it would never happen. 5 Specifically, the authors identify 43 cases where rapidly growing economies slow significantly – that is, real

GDP growth shifts down by at least 2 percentage points – and calculate that, on average, the tipping point is when GDP per capita (on a purchasing power parity basis) is USD16,740.

The empirical literature on the causes of financial crises offers some pertinent lessons to China

China‟s economy has become so big and complex that many of its structural problems are becoming more interrelated

Increasing strains on natural resources, the environment, and demographics are causing growing pains to set in

It is becoming more difficult to undertake individual reforms gradually and in isolation

Nomura | Asia Special Report November 2011

7

regime are adding pressure on China to press ahead with capital account

liberalization and interest rate deregulation. But without adequate safeguards,

financial deregulation can pressure banks to engage in overly aggressive

competition, lowering overall credit standards. Another example is China‟s

shrinking supply of young, rural surplus labour which is starting to accelerate

wage growth. One proposed reform is to relax the rigid hukou household

registration system, giving city migrants the same rights as locals so as to

encourage greater labour mobility and faster urbanization. But without other

reforms this could exacerbate other problems, such as environmental

degradation and social tensions. We see the pressure building to make more

broad-based wholesale reforms, but given growing inter-linkages of various

reforms, big changes will carry greater risks. Politically, it is hard to envisage

substantial change before the next generation of leaders takes the helm in

March 2013.

Nomura | Asia Special Report November 2011

8

Defining a hard economic landing

The term “China hard landing” is too often a throw-away line that means

different things to different people. We provide a precise definition of what we

regard as a hard economic landing in China. In addition – and with a large

dose of humility – we present our views on the likelihood, timing and

description of a hard economic landing, were it to occur.

Defining a “hard landing”

We define a hard economic landing in China as an abrupt slowdown in real

GDP growth to an average of 5% y-o-y or less over four consecutive quarters.

In economists‟ parlance we would regard this as a deep recession. On our

estimate of China‟s potential GDP growth being around 8%, our hard landing

definition means GDP growth being at least 3 percentage points (pp) below

potential, which we would regard as equivalent to a contraction in real GDP in

the US, on average, over four consecutive quarters. Note that under our

definition, China‟s real GDP growth could average 4.9% y-o-y for four quarters

in a row, or it could plunge to negative year-on-year growth in one quarter (a

low probability event, but one that we do not rule out) before rebounding to

over 5% y-o-y in subsequent quarters – but for the four quarters, averaging

below 5%. The last time China experienced a hard economic landing by this

definition was when real GDP growth slowed from 11.3% y-o-y in 1988 to

4.1% in 1989 and 3.8% in 1990, before rebounding to 9.2% in 1991. From Q4

1999, China started publishing quarterly real GDP data, and since then the

lowest average growth on a four-quarter rolling basis was 7.5% y-o-y in Q4

2001.

Triggers and timing

Although the advanced economies falling back into recession would hurt

China‟s exports, the economy is too domestic driven, in our view, for external

shocks to directly cause a hard landing. The more likely cause would be a

major pullback in investment from its current very high share of almost half of

GDP. Within gross capital formation, investments in property (24% of total)

and infrastructure (28% of total) appear the most vulnerable components.

Examples of potential triggers of an investment-led downturn include: 1) a

correction in what appears to be an overheated property market; 2) policy

mistakes, for instance the People‟s Bank of China (PBC) underestimating

inflation and having to play catch-up via aggressive tightening; 3) unforeseen

shocks, such as social unrest or a deadly pandemic; and 4) simply “investment”

fatigue setting in. Whatever the trigger, a major pullback in investment would

be likely to cause a steep rise in non-performing loans (NPLs) given that

China‟s domestic credit-to-GDP ratio is also at an extraordinarily high 1.5x, or

1.8x once the shadow banking sector is taken into account. Through losses of

wealth, confidence and jobs there would likely be large indirect knock-on

effects to household consumption.

It terms of timing, there is an argument that, because of political incentives, a

hard landing would not be allowed to happen until after the leadership

transition in March 2013. However, we would not rule out it happening earlier,

given: 1) the ratios of investment to GDP and credit to GDP are so high; 2)

support from exports is likely to be less than before; 3) the economy has

become so large and complex that many of the structural problems are

becoming more interrelated; and 4) policy responses are likely less effective

than before.

Policy responses

In response to the global financial crisis China implemented a RMB4trn (13%

of 2008 GDP) fiscal stimulus; put the steady appreciation of the CNY/USD

exchange rate, that has been in train since July 2005, on hold; cut the bank

Our definition is an abrupt slowdown in real GDP growth to an average of 5% y-o-y or less over four consecutive quarters

The most likely cause would be a major pullback in investment, but there are many potential triggers

Nomura | Asia Special Report November 2011

9

reserve requirement ratio (RRR) by 250bp; and cut the benchmark 1yr lending

rate by 216bp. We have no doubt that the government would again do all in its

power to respond to signs of a hard landing, but the question is how large,

quick and effective a policy stimulus would be. On all three counts, we judge

that it would be less than in 2008.

On monetary policy, we would expect aggressive cuts in the bank RRR and

CNY/USD appreciation to once again be halted (if there were to be large net

capital outflows rather than allowing CNY/USD depreciation, we would expect

the PBC to drawdown its USD3.2trn of FX reserves to keep CNY/USD stable).

On the other hand, we see a higher hurdle than in 2008 for the PBC to cut the

benchmark 1yr lending rate aggressively. One reason is because of greater

inflation pressures today, with CPI inflation currently much higher (6.1% y-o-y

in September 2011) than the 2.5% in 4Q 2008. Moreover, core CPI inflation,

which excludes food and energy items, has also risen steadily over the past

two years to 2.4% y-o-y in Q3 2011, the highest since the government began

publishing the data in 2005, suggesting that a structural inflation problem is

emerging (see Asia Special Report, China: The case for structurally higher

inflation. 21 September 2011). Another reason is what we believe is growing

recognition among China‟s policymakers that interest rates were set

fundamentally too low in the past, and that this cheap cost of capital

contributed to overinvestment. As such, we would expect to see greater official

resistance to rate cuts than in the past.

On fiscal policy, we would expect another stimulus package and, to avoid the

economy becoming more unbalanced, there would likely be more focus on

consumption-boosting measures. However, fiscal stimulus aimed at

consumption tends to be less effective than public investment, because any

increase in household income can be saved rather than spent.

Therefore, we would expect a fiscal stimulus package to again be dominated

by public investment, but again believe it would be less effective than that

seen in 2008-09, for three reasons.

First, while China certainly has room for fiscal stimulus, it has less room than it

did before. Central government debt is still low at around 20% of GDP, but the

build-up of local government debt in recent years has lifted general

government debt (central plus local) to around 50% of GDP. On top of this are

the government‟s contingent future liabilities, including future losses related to

NPLs and unfunded pension liabilities which, if all were to be recognized in

2011, would lift the general government debt to 85% of GDP, according to the

IMF (2011a, p.47).

Second, the speed of implementation would likely be slower than in 2008-09.

Before the global financial crisis, the economy was overheating, forcing the

National Development Reform Commission (NDRC) to turn down a large

number of new investment projects by SOEs and local governments. So when

the global financial crisis hit, China had many large off-the-shelf investment

projects ready to go and so could boost investment quickly. This is no longer

the case.6

Third, given that government-influenced investment comprises about one-third

of total investment, to avoid a fall in total investment public investment must

grow by twice as much as any decline in private investment growth. The

government “doubling up” with another public-led investment boom could

heighten concerns over misallocated, wasteful investment, increasing fears of

an even bigger hard landing further out – the private response could be to pull

back investment even more.

6 The growth of newly started fixed-asset investment projects was 28.7% y-o-y in 2007, but the NDRC‟s rejection

of new projects caused the growth rate to plunge to -2.9% y-o-y in Jan-July 2008; the NDRC reversed course after the global financial crisis hit, and the pent-up demand caused the growth rate to rebound to over 80% y-o-y in Jan-Oct 2009. The growth of newly started fixed-asset investment projects was 23.1% y-o-y in Jan-Aug 2011, and there is now much less pent-up demand.

We see a higher hurdle than in 2008 for the PBC to cut the benchmark 1yr lending rate aggressively

Another public-led investment boom could heighten concerns over misallocated, wasteful investment

The speed of implementation would likely be slower than in 2008-09

China still has room for fiscal stimulus, but less than in 2008

Nomura | Asia Special Report November 2011

10

Perceived likelihood

Drawing together the strands of the analysis we have done on the six main

macro risks in China, our overall assessment is that the chance of a hard

economic landing has increased in recent years. We attach a one-in-three

probability of real GDP growth falling to an average of 5% y-o-y or less over

four consecutive quarters sometime between now and the end of 2014. While

our baseline modal (i.e., most likely outcome) forecast – to which we attach

the residual two-third probability – is for China‟s real GDP to grow by an

average of 8.5% in 2012-14. We are aware of the non-trivial tail risk of a much

worse outcome which, as we explain in the final chapter, would have severe

repercussions for the global economy and financial markets.

Interestingly, this year there has been a significant sell-off in China‟s equity

and credit markets, yet most China economists have not significantly

downgraded their GDP forecasts. For example, the latest 10 October survey of

18 market economists by Consensus Economics Inc. shows that the

consensus forecast of China‟s real GDP growth is 8.5% in 2012 and 8.4% in

2013, while the IMF‟s latest forecast (released in September) is 9.0% in 2012.

The way we would reconcile this gap is that economists forecast the modal, or

most likely, outcome, whereas the financial market tends to take a weighted-

average probability of different possible outcomes. If we apply our baseline

and hard-landing probabilities to the market method {(8.5*0.66)+(5.0*0.33)}, it

gives a weighted-average GDP growth forecast of at most 7.3% in 2012-14. In

other words, like-for-like, our forecasts are probably not that dissimilar to what

the market is pricing in – the key will be whether the risk of a hard landing rises

or falls going forward, which brings us to Nomura‟s new proprietary tool – our

China Stress Index (CSI).

We attach a one-in-three probability to our definition of a hard landing commencing sometime between now and the end of 2014

Nomura | Asia Special Report November 2011

11

Nomura‟s China Stress Index (CSI)

To more closely monitor the risks of a hard landing in China‟s economy, we

have constructed a macro China Stress Index, or CSI for short. The CSI is

made up of 18 indicators that quantify the macro risks in China into one

summary measure. We selected the 18 indicators by using two main criteria:

• Importance: Each indicator signals an important risk factor that we

believe is not fully captured by other indicators in the CSI. We try to capture,

among others, the risks associated with over- and mal-investment, particularly

in the property market; excessive credit and the problems created by the

rudimentary monetary architecture; structural inflation risks associated with the

Lewis turning point; and the increasing challenges arising from high income

inequality and environmental degradation.

• Availability: A challenge not only in China, but in all developing

economies is the paucity of the data. We chose indicators that are sourced

from official statistics and that have a time series of over a decade, so that the

CSI has a reasonably long history for statistical inference (the CSI begins in

January 2000). For the indicators that are available only on an annual or

quarterly basis, monthly series were interpolated from the longer-frequency

data.

To construct the CSI, the 18 indicators are first standardized and then

weighted. The weights, to some extent, are subjective, but they are grounded

in our analysis in the following chapter and international experience of the

common causes of emerging market crises. Most variables have weights of 3-

5%, while two have 8% weights (property loans/total loans and residential

property price index/long-run trend) and three have 10% weights (gross capital

formation/GDP, domestic credit/GDP and new shadow banking funding/ new

total social financing). The CSI is indexed to 100 in January 2000. For more

technical details on the methodology in constructing the CSI, please see the

Appendix: The construction of Nomura‟s China Stress Index.

The CSI indicates that risks in China‟s macro economy have been on a broad

uptrend, and more noticeably since the global financial crisis. In Q2 2011, the

CSI rose to its highest level since it was first compiled, but in Q3 it eased

slightly, mainly because of a decline in the flow of new shadow banking

funding (Figure 3). One limitation of the CSI is that it does not give a

probability of a hard economic landing. To do so would require a reference

variable measuring past episodes of hard economic landings in China, the

obvious one being real GDP. Yet in the past 20 years China‟s GDP growth has

not fallen below 5% and before then the causes of hard landings in GDP were

influenced heavily by social and political unrest.

We could have used panel data on GDP from other countries showing hard

economic landing experiences internationally, but in our view China‟s economy

is too special for this exercise to give credible results. So what the CSI tells us

is: 1) the direction of overall macro risk; and 2) how fast the risk has changed

compared to history.

The CSI is made up of 18 indicators that quantify the macro risks in China into one summary measure

The CSI indicates that risks in China‟s economy have been on a broad uptrend, more noticeably since the global financial crisis

Nomura | Asia Special Report November 2011

12

Fig. 3: Nomura’s China Stress Index

Note: The last data point is September 2011. Source: PBC; National Bureau of Statistics and Nomura Global Economics. For details of construction, see the Appendix: The construction of Nomura‟s China Stress Index

A closer look at the components reveals that rapid increases in residential

housing starts relative to sales, residential property prices, gross capital

formation, property loans and domestic credit have been the main recent

drivers (Figure 4). We are under no illusions that the CSI has its limitations and

needs to be treated with caution. The results of the CSI, which we will update

on a quarterly basis, should always be open to interpretation, and used as a

tool among many others for analysis of China macro risks.

Fig. 4: The five biggest drivers of the CSI over Jan 2007-Sep 2011 (contribution to the increase in the CSI index over this period)

Note: Unit is percentage point. Source: PBC; National Bureau of Statistics and Nomura Global Economics. For details of CSI construction, see Appendix: The construction of Nomura‟s China Stress Index.

Fig. 1

99.5

100.0

100.5

101.0

101.5

102.0

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

Jan 2000=100

0 0.05 0.1 0.15 0.2

Residential housing starts less sales

Residential property price deviation from long-run linear trend

Gross capital formation/GDP

Property loans/total loans

Domestic credit/GDP

Housing starts relative to sales, property prices, gross capital formation, property loans and domestic credit have been the main recent drivers

Nomura | Asia Special Report November 2011

13

1. Overinvestment and excessive credit

Since the early 1960s the share of total investment (public and private gross

capital formation) in China‟s GDP has trended upwards, a normal course of

economic development as poor countries start with a small capital stock

ensuring a high return on capital and hence a high rate of investment. Former

leader Deng Xiaoping endorsed this trend during his famous South China tour

in 1992, by espousing the benefits of an open economy, setting China firmly

on the path of export- and investment-led growth. China‟s share of investment

in GDP rose from 35.3% in 2000 to a relatively high 43.9% in 2008, before

surging to 47.5% in 2009 and to 48.6% in 2010 (Figure 5). By the end of 2010,

we estimate that more than half of China‟s total gross capital formation was

related to property (23.8%) and infrastructure (27.7%). This year, property

investment has continued to surge, to 13% of GDP in Q3 2011 (Figure 6).

Fig. 5: Investment and consumption shares of nominal GDP

Source: CEIC and Nomura Global Economics.

Fig. 6: Property investment share of nominal GDP

Source: China's NBS and Nomura Global Economics.

In international and historic terms, China is now an outlier: no other large

economy has had such a high investment-to-GDP ratio for so long. The

highest investment ratio in the US since 1929 was 26.2% in 1941. Surveying

Japan, Korea, Singapore and Thailand, four Asian countries that have

experienced rapid economic take-offs, their highest investment ratios typically

lasted seven to eight years – and none ever reached the levels seen in China

(Figure 7). 2011 will be the ninth consecutive year that China‟s investment

ratio has been over 40%. Undoubtedly there are questions marks over the

quality of Chinese data – some claim that China‟s official investment ratio is

overstated because the services sector and hence consumption are likely

underestimated; on the other hand, aggregating the investment data for

China‟s 31 provinces suggests that the official national investment-to-GDP

ratio could be 7pp too low (see Box 1: Fuzzy numbers).

10

20

30

40

50

60

70

1954 1962 1970 1978 1986 1994 2002 2010

Investment

Household consumption

% GDP

3

6

9

12

15

Sep-97 Sep-99 Sep-01 Sep-03 Sep-05 Sep-07 Sep-09 Sep-11

% of GDP

The share of investment in China‟s GDP has risen to almost half

China is now an outlier: no other large economy has had such a high investment-to-GDP ratio for so long

Nomura | Asia Special Report November 2011

14

Fig. 7: Asian investment-to-GDP ratios – during economic take-off periods

Note: t=numbers of years from the starting year, eg. For China, the starting year is 2002. The data are in nominal terms and investment is the sum of public and private gross capital formation. Source: China Statistical Yearbook; CEIC and Nomura Global Economics.

Fig. 2

Box 1: Fuzzy numbers

The quality of China‟s statistics is improving, but large gaps remain. Following the completion of its first Financial

Stability Assessment Program (FSAP) of China in July 2011, the IMF noted that a “full assessment of these various

risks is, however, hampered by serious data gaps, weakness in the infrastructure and constraints on the FSAP

team‟s access to confidential data”, IMF (2011a, p.11). Some of the glaring examples include the official urban

unemployment rate hovering within such a tight range of 4.0-4.3% for the past nine years, and how in 2010 real

GDP growth in 29 of the 31 provinces was above the national GDP growth of 10.3%. There have also been several

sizable upward revisions to China‟s GDP, mainly due to under-reporting of the size of the services sector and

hence consumption. The biggest revision was in 2005 after the first national economic census, when 2004 nominal

GDP was revised up by 16.8% in one fell swoop, with the share of services in GDP revised up from 31.9% to

40.7%. It is possible that the services sector and consumption will be revised up again, and the investment-to-GDP

ratio revised down, but then again it is also possible that the starting position is a higher investment-to-GDP ratio

than officially reported. GDP data are available by province and aggregating the gross capital formation and the

GDP data for the 31 provinces, we arrive at an investment-to-GDP ratio of 55.7% in 2010, a full 7pp higher than the

national investment-GDP ratio (see Figure 8).

Fig. 8: An alternative measure of the investment-to-GDP ratio

Source: CEIC and Nomura Global Economics.

Fig. 3

The recent jump in China's investment ratio to almost half of GDP was driven

by a conscious policy response to the global financial crisis, but the

fundamental reason why the investment ratio has been so high for so long has

more to do with serious factor cost distortions.

The high priority on internal rebalancing of the economy – that is, lowering the

investment ratio and raising the consumption ratio – is not a new initiative; in

fact it was a key goal of the 11th Five-Year Plan (2006-10) unveiled in early

20

25

30

35

40

45

50

t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10

China, 2002 -11e

Japan, 1966 -75

Korea, 1988 -98

Singapore, 1978 -88

Thailand, 1989 -98

% of GDP

0

10

20

30

40

50

60

1954 1962 1970 1978 1986 1994 2002 2010

Sum of provinces

National

% GDP

Nomura | Asia Special Report November 2011

15

2006. However, the global financial crisis of 2008 was a huge unexpected

shock, causing China‟s export performance to swing from 23% y-o-y growth in

Q3 2008 to a 24% y-o-y contraction in Q2 2009. Fearing major knock-on

effects to the domestic economy from firms cutting jobs and capex, the

authorities gave the go-ahead to a credit-financed investment boom. China's

real estate developers, SOEs and local governments took heed, ramping up

investment in property and infrastructure, putting rebalancing efforts in China

firmly on the back burner.

However, the more fundamental reason for China's persistently high

investment-to-GDP ratio is the large difference between the return on, and

cost of, capital. The bank lending rate has historically been artificially

controlled far below the return on capital needed to support an industry-led,

export-orientated growth model. A simple approximation of the return on

capital is nominal GDP growth, which averaged 18.5% in the 1990s and 14.6%

in the 2000s, compared with the benchmark 1yr bank lending rate of 9.4% in

the 1990s and 5.8% in the 2000s. This large gap gave producers a big

incentive to invest. To more formally estimate China's return on capital, we

follow a similar methodology to the Bank of Japan (2011) and Bai et al (2006).

Qualitatively, the results are similar to that of using nominal GDP growth,

indicating the large wedge between the return on, and cost of, capital of over

10pp over the past three decades (Figure 9). Even five years ago, Aziz (2006)

found that China‟s low cost of capital was quantitatively an important factor in

explaining why the investment-to-GDP ratio was high, and back in 2006 the

ratio was “only” 42%.7

Fig. 9: The difference between the return on, and cost of, capital

Note: The aggregate return on capital is measured using approximated data on the share of capital in total income, the capital stock-to-output ratio and the depreciation rate of capital. The cost of capital is estimated using the 1yr bank lending rate. Source: CEIC; China Statistical Yearbook; Development and Research Center under the State Council; and Nomura Global Economics.

The big question is not if, but when, China‟s investment and consumption

ratios re-balance – and will it happen in a gradual, policy-controlled way, or will

the process involve one or more episodes that are abrupt and beyond the

control of policymakers, causing major disruptions to the economy and

markets? International experience shows that rebalancing is never easy, as it

usually means redistributing income and power from vested interests that have

benefited from the old model – in China, notably large SOEs and local

governments (see chapter: The privileged state-owned enterprises). Of all the

main components in GDP, investment is typically the largest swing factor and

in most Asian countries it usually contracts at least one year each decade. Yet

7 The flipside of China's high investment-to-GDP ratio is a low consumption-to-GDP ratio, which is partly

because Chinese households have a high motive for precautionary saving, but also the share of wages in national income is low relative to profits. SOEs historically provided generous social welfare benefits to their workers, so the downsizing of SOEs in the late 1990s meant that workers needed to save more of their income to pay for their own healthcare, education and pensions. Also, while urbanization has boosted incomes of rural migrant workers, the stringent hukou household registration system has provided them with scant social welfare benefits in the cities where they live, increasing their precautionary savings. The very low or negative real interest rate on bank saving deposits has also forced households to save more than they otherwise might have.

0

5

10

15

20

25

30

% Difference (percentage points)

Return on capital

Cost of capital

The fundamental reason for the high investment-to-GDP ratio is the large difference between the return on, and cost of, capital

At almost half of GDP, China‟s investment is now so large that were it to stop growing it would cut real GDP growth in half

Nomura | Asia Special Report November 2011

16

China's investment has not fallen since 1990 in volume terms and not since

1976 in value terms (Figure 10). At almost half of GDP, China‟s investment is

now so large that were it to stop growing, let alone turn negative, it would cut

real GDP growth in half (see Box 2: China‟s challenging GDP arithmetic). The

timing of rebalancing is also now less favourable for China, as besides

investment and consumption, the third engine of growth – exports – is unlikely

to be firing on a full cylinder given the crisis-scarred economies of the US and

Europe.

Fig. 10: Identifying the years when real gross capital formation contracted

1940s 1950s 1960s 1970s 1980s 1990s 2000s

China Nominal n.a. 1955: -2% 1967:-25% 1976:-7%

1960-62:-95% 1972:-3%

Real* n.a. 1955:-2% 1967-68: -27% 1976: -9% 1981: -2% 1990: -1%

1960-62:-109% 1972: -2%

Hong Kong Real n.a. n.a. 1966-68: -38% 1989: -5% 1998-99: -32% 2008: -1%

1985: -5% 1996: -3% 2005: -1%

1982-83: -7% 2001: -5%

India Real n.a. 1957-59: -8% 1967-68: -9% 1979: -10% 1981: -4% 1996: -1% 2008: -6%

1952: -26% 1961: -2% 1974: -10% 1991: -16% 2000-01: -6%

Indonesia Real n.a. n.a. n.a. 1988: -5% 1998-99: -62% 2002: -4%

Japan Real n.a. 1974-75: -12% 1983: -3% 1998-99: -16% 2008-09: -23%

1980: -1% 1992-94: -10% 2001-03: -13%

Korea Real n.a. n.a. n.a. 1975: -4% 1980: -17% 1997-98: -32% 2009: -13%

1972: -10% 1992: -1%

Malaysia Real n.a. n.a. n.a. n.a. 1985-87: -32% 1998-99: -47% 2008-09: -17%

2005: -2%

2003: -2%

2001: -9%

Philippines Real 1956: -1% 1962: -1% 1970: -4% 1984-85: -69% 1998-99: -29% 2009: -9%

1952: -3% 1960: -11% 1980: -4% 1991: -17% 2006: -15%

1949-50: -30% 2004: -2%

Singapore Real n.a. n.a. 1964: -3% 1977: -4% 1988: -3% 1998: -24% 2009: -19%

1975: -5% 1985-86: -18% 2001-03: -57%

Taiwan Real n.a. 1955: -15% 1975: -7% 1985: -8% 2007-09: -30%

1982: -5% 2001: -24%

Thailand Real n.a. n.a. n.a. n.a. 1985-86: -8% 1997-98: -73% 2009: -25%

1982: -7% 2006: -4%

Source: CEIC and Nomura Global Economics. Note: The shaded areas are decades when real gross capital formation falls. For China, official data on real gross capital formation are not available and so Nomura‟s proxy is nominal gross capital formation deflated by the fixed-asset investment deflator back to 1990 and before that, deflated by the GDP deflator.

Nomura | Asia Special Report November 2011

17

Box 2: China’s challenging GDP arithmetic8

With investment making up almost half of GDP, China‟s economy is vulnerable to an investment slump for

whatever reason: a banking crisis; the central bank hiking aggressively having fallen behind the curve in fighting

inflation; unforeseen shocks, such as social unrest or a deadly pandemic; or simply because “investment” fatigue

sets in. To illustrate China‟s challenging GDP arithmetic consider the numbers. We expect real investment to grow

by 11.3% in 2011, contributing 5.5pp to GDP growth of 9.2%. However, if real investment were to grow by only 5%

it would contribute 2.4pp and, assuming (conservatively) unchanged contributions from net exports and

consumption, GDP growth would be just 6.1%. If real investment growth were to slow to 0%, it would make no

contribution to GDP and so GDP growth would more than halve to 3.7%.

However, carefully calibrating a rebalancing of GDP growth toward consumption is no easy feat. To illustrate, for

the share of household consumption in GDP to rise, consumption growth must outpace GDP growth. Yet we

estimate that real household consumption has grown at a double-digit rate in only three of the past 14 years and

over the past decade has averaged about 9% growth, whereas real GDP has averaged 10.3% growth. To raise the

household consumption-to-GDP ratio from 34% in 2010 to 40% by 2020, and assuming real GDP grows 8% pa this

decade, then real household consumption would need to grow consistently by 10% pa over 2010-20. To turn

consumption into an engine of growth, China needs to do more than simply beef up social welfare spending to

reduce precautionary household savings. It needs to transfer a massive amount of income from the still heavily

state-subsidized corporate sector to households (see chapter: The privileged state-owned enterprises) and end

financial repression, which has given rise to negative real deposit rates (see chapter: Rudimentary monetary

architecture).

As Japan's experience shows, the large positive gap between the return on,

and the cost of, capital does not last forever (see Box 3: Lessons from Japan

on the return and cost of capital). China‟s large gap could soon start to narrow,

possibly quite sharply, because of a simultaneous fall in the return on capital

and a rise in the cost of capital. The return on capital could start falling simply

because the enormity of investment is causing the capital stock to accumulate

at such a rate that capital is rapidly becoming less scarce. Total nominal

investment (i.e. gross capital formation) is set to total some USD3.5trn in 2011,

3x larger than in 2006 and 7x larger than in 2001. Another reason to expect

the return on capital to soon start to fall is the strong international evidence

that investment booms are often associated with a misallocation of capital,

especially in emerging markets. This seems a particular risk in China given: 1)

the banking sector does not have much experience in gauging credit risk; 2) a

massive shadow banking sector has emerged, which is difficult to measure, let

alone regulate; and 3) the fact that much of the investment in recent years has

been government-led, which tends to be less productive than private

investment, and in big infrastructure projects, which can take many years to

break even.9 A third reason is that China's heavy investment can also run into

diminishing returns from a social perspective, as capital intensive industries

pollute the environment and create fewer job opportunities.

Meanwhile, China's cost of capital has been increasing and we expect it to rise

further. The benchmark 1yr bank lending rate has risen from 5.31% in October

2010 to 6.56%, and this likely understates the effective cost of capital as banks

are charging a record 61.2% of their new loans above the benchmark lending

rate; in the shadow banking sector borrowing costs can be several times

higher. While the central bank has paused its rate hiking cycle, we expect it to

resume hiking in 2012. China needs higher interest rates to contain what we

see as structural inflation problems caused by accelerating labour costs (see

chapter: The Lewis turning point); the urgent need for the government to

8 The phrase “China‟s challenging GDP arithmetic” was coined by Paul Sheard, Nomura‟s global chief economist,

back in 2009 (see the Global Letter, “China‟s challenging GDP arithmetic” in the Global Economic Weekly Monitor, 25 September 2009). 9 A good micro example is China building – in just three years – the world‟s longest and fastest high-speed rail

network, which according to data from the International Union of Railways extends to 6,300km, an achievement that had produced considerable national pride. The collision of two new high-speed trains outside the city of Wenzhou on 23 July, which killed 40 and injured 191, stoked public anger and a media frenzy that the breakneck development of high-speed rail had cut corners – indeed, China‟s Railways Ministry is the manufacturer, operator and regulator of the network. As a result, Beijing has suspended approvals of new high-speed lines and its original ambitious program of having a further 4,339km of high-speed rail under construction by 2012 – more under construction over this period than that of the rest of the world put together – is now unlikely to be achieved.

As Japan's experience shows, the large positive gap between the return on, and the cost of, capital does not last forever

Nomura | Asia Special Report November 2011

18

unwind generous subsidies to SOEs and to stop underpricing factor inputs

such as land, water and energy; and a likely continued multi-year surge in food

prices (see our Special Report, The coming surge in food prices, 8 September

2010). Higher interest rates would also be a natural result of accelerating the

evolution of China's monetary policy framework, from administrative measures

to more market-price-based instruments (see chapter: Rudimentary monetary

architecture). A key risk is policy errors, for example falling behind the curve in

fighting inflation and needing to catch up via aggressive rate hikes, leading to

a sharp rise in the cost of capital at a time when the return on capital could be

falling.10

10

Firms should adjust their capital stock so that its marginal productivity equals its user cost. As interest rates increase, firms scale back investment for which the expected return is insufficient to cover the higher financing costs. Using micro data on listed Chinese firms over 2002-07, Conway, Herd and Chalaux (2010) found empirically that capital spending is negatively influenced by higher interest rates.

Nomura | Asia Special Report November 2011

19

Box 3: Lessons from Japan on the return and cost of capital

Similar to China in the last two decades, Japan achieved high GDP growth over the period 1955 to 1970, averaging

9.7% and, like China today, Japan‟s economy became increasingly unbalanced, with a rising investment-to-GDP

ratio and falling consumption-to-GDP ratio, reaching 35.5% and 59.7% respectively in 1970 (Figure 11). Domestic

rebalancing in Japan began after 1970. According to a recent study by researchers Fukumoto and Muto (2011) at

the Bank of Japan, the main trigger of rebalancing was a decline in the return on capital and a rise in the cost of

capital. In the 1950s, Japan had a small capital stock and so the return on capital was higher than 20%, but the

rapid accumulation of capital drove down the marginal productivity of capital. An undeveloped financial sector led to

some misallocation during the investment boom, while the development “catch up” to advanced foreign technology

was virtually complete in the early 1970s. All these factors contributed to a decline in the return on capital in the

late 1960s and early 1970s.

Meanwhile, the bank lending rate was highly regulated in the 1950-60s and was kept very low to support an

industry-led growth model. However, in the early 1970s Japan experienced an outbreak of inflation, in part driven

by the 1973-74 oil crisis, but also the flow of surplus rural labour moving to the cities started to diminish in the

1960s, leading to increased worker bargaining power and a surge in real wages, the so-called Lewis turning point

(Minami, 1973). All this led to monetary policy tightening and a rise in bank lending rates and the cost of capital. So

in the early 1970s, Japan faced a marked narrowing in the difference between the return and cost of capital,

significantly reducing firms‟ incentives to maintain high rates of investment (Figure 12).

Fig. 11: Japan's investment and consumption shares of GDP

Source: Bank of Japan (2011).

Fig. 12: Japan’s difference between the return and cost of capital

Source: Bank of Japan (2011).

What accentuates the macro risks of China's investment boom is the credit

boom associated with it. One of the relatively few robust findings to emerge

from the empirical literature on leading indicators of banking crises is that rapid

domestic credit growth increases the likelihood of a problem (Kaminsky and

Reinhart, 1999). In a survey of credit booms in 28 emerging market economies

during 1970-2002, the IMF (2004) estimates that about 75% of the credit

booms were associated with a banking crisis. More pertinent to China, Borio

10

20

30

40

50

60

70Gross fixed capital formation

Consumption

% of nominal GDP

0

5

10

15

20

25

30

35

%Difference (percentage points)

Return on capital

Bank lending rate

What accentuates the macro risks of China's investment boom is the credit boom associated with it

Nomura | Asia Special Report November 2011

20

and Lowe (2002) use annual data since 1960 for 34 countries to show

empirically that an investment boom by itself may pose little threat to the

stability of the financial system. Rather, it is the combination of various

imbalances, in particular the simultaneous interactions of rapid credit growth,

rapid increases in asset prices and an investment boom – rather than any one

of these alone – that increases the likelihood of problems.

Analysis of China's recent credit boom has tended to focus on local

government borrowing, where the data are opaque. Local governments are not

allowed to directly incur debt, and so finance infrastructure projects by

borrowing from banks. To do so, they set up over 6,500 Local Government

Financing Vehicles (LGFVs). The latest official estimate of local government

debt outstanding was RMB10.7trn, or 27% of 2010 GDP, as at June 2011 by

the State Audit Office, although some private estimates are much higher.11

Whatever the true figure of local government debt is, a broader analysis can

be gleaned from IMF data which show that total domestic credit (private and

government) surged from 121% of GDP in Q4 2008 to 147% in Q2 2011, a

level that is not far from the peak in 2003 (Figure 13). Moreover, China's

credit-to-GDP ratio stands as an outlier compared with other countries of a

similar income level (Figure 14).

Fig. 13: Domestic credit-to-GDP ratio

Source: IMF; CEIC and Nomura Global Economics.

Fig. 4

Fig. 14: Credit-to-GDP ratio versus GDP per Capita

Source: IMF Global Financial Stability Report, September 2011.

Fig. 5

China's credit boom over 1998-2003 led to a banking crisis. As far as we know,

the earliest official data on the NPL ratio of the major commercial banks was

23.6% in 2002, but this excludes a large volume of bad loans, of over 15% of

GDP, that were carved out and transferred to newly created asset

management companies a few years earlier.12

Since 2002, the official NPL

ratio has steadily declined and by June 2011 stood at just 1.0% for all

commercial banks. However, given that China's credit-to-GDP ratio has

surged to just shy of the record high in 2003, there is little doubt that the NPL

ratio will rise again –the question is by how much.

Reflecting the paucity of data and the uncertainties involved, estimating how

high NPLs may rise and the potential fiscal cost of recapitalizing the banks can

vary widely.13

To be sure, compared to a decade ago China‟s banks today are

better capitalized, have higher loan-loss provisioning and face more stringent

11

In July 2010, the China Banking Regulatory Commission (CBRC) first estimated total local government debt outstanding at RMB7.7trn but raised its estimate in November 2010 to RMB9.1trn. The latest estimate in June 2011 by the State Audit office was even higher, at RMB10.7trn, or 27% of 2010 GDP – albeit still far short of the RMB20trn projected by Professor Victor Shih at Northwestern University. 12

Before the establishment of asset management companies, unofficial estimates put the peak NPL ratio in 1999-2000 at about 40%, or higher. The OECD estimates that the total cost to the government of recapitalizing the banking sector in the early 2000s was some 30% of GDP (OECD 2005). 13

The State Audit Office sent a warning in June 2011, when after a lengthy audit of the five major banks it found that RMB58bn, or 17% of total loans outstanding, violated regulations, such as new loans granted for unapproved projects or used to repay existing debt. Rating agency Moody‟s expects China‟s NPL ratio to rise to 8-12% in coming years. In July 2011, the official auditor of Liaoning province reported in a speech that 85% of LGFVs in Liaoning had insufficient income in 2010 to cover debt-servicing payments.

50

60

70

80

90

100

110

120

130

140

150

160

Jun-81 Jun-86 Jun-91 Jun-96 Jun-01 Jun-06 Jun-11

% of GDP

China

Cyprus

0

50

100

150

200

250

300

350

0 10 20 30 40 50 60 70

Cre

dit to

GD

P, e

nd

-2010

(%

)

GDP per capita, 2009 (PPP, thousands of US$)

China's credit-to-GDP ratio stands as an outlier compared with other countries of a similar income level

China‟s banks today are better capitalized, have higher loan-loss provisioning, but…

There is little doubt that the NPL ratio will rise again – the question is by how much

Nomura | Asia Special Report November 2011

21

regulations and supervision.14

But on the other hand, we see two important

reasons for concern: 1) a big and largely unregulated shadow banking sector

has emerged in recent years, estimated to be almost as large as the official

banking sector (see chapter: Rudimentary monetary architecture); and 2) this

time, both local governments and property developers are heavily indebted,

which raises the risk of a vicious spiral if there is a major correction in property

prices given that 30-40% of local government revenue is made up of proceeds

from land sales and other property-related activities.15

According to official

data, nationwide property prices have risen 60% since the end of 2006 (IMF

2011c). This has fueled speculative property investment and an ominous sign

is the large gap that has opened up between the combined floor space of

residential, office and commercial property that builders have started work on,

compared to the floor space sold (Figure 15).16

In a back-of-the-envelope exercise simply to illustrate how much estimates can

vary, if we assume that China's NPL ratio rises from 1% to 10% and that 70%

of these loans could be recovered, then the cost to the banking sector – or

failing that, the government – would be RMB1.6trn, or 3.6% of 2011 GDP

(Figure 16). However, under more drastic scenarios of higher NPLs and lower

recovery rates, it is possible that the total cost could be over 30% of 2011 GDP.

Fig. 15: Difference between floor space started and floor space sold:

Source: CEIC and Nomura Global Economics.

Fig. 16: Assessing the cost of potential financial sector problems, % of GDP

Loan recovery rate, %

30 40 50 60 70

NPL

ratio,

%

10 8.3 7.1 5.9 4.7 3.6

20 16.6 14.2 11.8 9.5 7.1

30 24.9 21.3 17.8 14.2 10.7

40 33.1 28.4 23.7 18.9 14.2

50 41.4 35.5 29.6 23.7 17.8

Note: % of estimated 2011 GDP. Source: CEIC and Nomura Global Economics.

14

In May 2011, the CBRC ordered systemically important banks to have bad-loan provisions that are no less than 2.5% of total outstanding credit by the end of 2013 and 150% of non-performing debt. 15

This year, tighter credit conditions have led property developers to seek other, more expensive, forms of financing in the shadow banking sector, notably new entrusted loans. Lucy Fung, Nomura‟s China Bank analyst, estimates that of the RMB702.8bn of new entrusted loans in Jan-Jun 2011, 46% were granted to property developers at an average interest rate of 15.8% and at an average duration of 11.3 months. Stress tests by ratings agency Standard & Poor‟s (2011) estimate that the property developers could absorb a 10% decline in property sales in 2012. But if property sales fell by 30% in 2012, more than half of the 30 developers rated by S&P would have “weak liquidity”, which according to S&P‟s definition means overarching credit risk and an issuer credit rating at the “B” level or lower. 16

The increasing use of desperate sales gimmicks by property developers is one micro-level sign that property supply has moved ahead of demand. For example, at this year's Shanghai Autumn Property Exhibition, to exploit the law which prohibits the purchase of more than two residential apartments, so-called “Soho” apartments – offices equipped with private bathroom and kitchens – have been marketed as they are not classed as homes (South China Morning Post, 6 October 2011).

0

500

1,000

1,500

2,000

2,500

Dec-96 Dec-99 Dec-02 Dec-05 Dec-08 Dec-11

Floor space started

Floor space sold

Millions of Sq. meters, 12m rolling sum

… a big and largely unregulated shadow banking sector has emerged in recent years

Nomura | Asia Special Report November 2011

22

2. Rudimentary monetary architecture

China‟s monetary policy, by evolving too slowly toward market price-based

instruments, is losing its effectiveness in managing an economy that is rapidly

becoming more open and sophisticated. In the words of the OECD, “after three

decades of liberalization, product markets have become increasingly

competitive and market forces are now generally the main determinant of price

formation and market behaviour”, OECD (2005, p.102). The PBC needs to

place less emphasis on quantity-based instruments such as the bank reserve

requirement ratio (RRR), central bank bill issuance, credit quotas and bank

window guidance, and instead adopt the interest rate as the primary policy tool.

A precondition for this is a more flexible exchange rate. Market-based

instruments are less distortionary and can have powerful indirect economy-

wide effects by enhancing competition, efficiency and risk management.

At the root of the problem is China‟s inflexible exchange rate, which

significantly hinders the PBCs ability to tailor monetary policy to domestic

objectives. The essential problem stems from Professor Robert Mundell‟s

“Impossible Trinity”: that a country can simultaneously choose two, but not all

three, of a managed exchange rate, an open capital account and monetary

policy autonomy. With capital flowing more freely, China risks losing more

control over its monetary policy if it continues to heavily manage the exchange

rate. A rigid exchange rate reduces the central bank‟s ability to use market

instruments such as interest rates to manage aggregate credit growth and

instead perpetuates a reliance on administrative measures such as credit

quotas, hindering efforts to make the banking system more commercially

orientated.

China‟s inflexible exchange rate regime requires the PBC to conduct

substantial open market operations to sterilize, or “mop up” excess domestic

liquidity arising from FX intervention, which has increased FX reserves to an

extraordinary USD3.2trn as at September 2011.17

The sterilization measures

include aggressively issuing low-yielding central bank bills and raising the

RRR of large banks 12 times since January 2010, from 15.5% to 21.5%, an

all-time high.18

Meanwhile, the benchmark 1yr bank lending interest rate has

been increased only five times, from 5.31% to 6.56% (Figure 17). While the

PBC is successfully sterilizing its FX intervention, it is repressing the free-

functioning intermediation role of the banking sector.

Fig. 17: Bank reserve requirement ratio and the benchmark bank lending rate

Source: CEIC and Nomura Global Economics.

17

The massive accumulation of FX reserves to USD3.2trn is not necessarily costless. The larger the stock of FX reserves the greater the potential quasi-fiscal cost if the return earned on the foreign assets is less than the interest paid on the PBC‟s sterilization bills. The PBC could also incur substantial capital losses on its balance sheet if USD was to crash, leaving it with negative capital. The PBC could try and recapitalize itself by earning profits from increased seigniorage, i.e. printing more currency; or it could be recapitalized by the government but at the cost of losing some of its monetary policy independence and heightening the risk of a major inflation problem. 18

Combining these two sterilization measures, we estimate that the PBC has effectively "locked up" nearly one-quarter of total bank deposits that otherwise could have been used for more profitable commercial business, such as lending.

0

5

10

15

20

25

Oct-91 Oct-95 Oct-99 Oct-03 Oct-07 Oct-11

Benchmark 1yr bank lending rate

Bank reserve requirement ratio

%

China‟s monetary policy is losing its effectiveness in managing an economy that is rapidly becoming more open and sophisticated

While the PBC is successfully sterilizing its FX intervention, it is repressing the free-functioning intermediation role of the banking sector

At the root of the problem is China‟s inflexible exchange rate

Nomura | Asia Special Report November 2011

23

Fig. 6 The PBCs sterilization operations impose considerable cost on the banking

sector. China maintains an interest rate ceiling on bank deposits, which

currently ranges from 3.50% for 1yr savings deposits to 5.50% for 5yr deposits.

So, the requirement that 21.5% of deposits for large banks be reserved at the

PBC earning only 1.62% interest is akin to an implicit tax on the banking sector,

restricting banks from allocating a larger portion of their portfolios to higher-

yielding loans and investments.

One way to help ease this financial repression is to allow a wide margin

between the benchmark bank lending and deposit rates, which traditionally is

what China has done. In the last decade, the spread between the 1yr bank

lending and saving deposit rates averaged 3.4% – substantially higher than

the 1.4% average in the 1990s. However, fat margins simply shift the cost of

financial repression from the banks to depositors, which means most

households given a lack of alternative investment opportunities. This has been

particularly onerous on depositors in the past year because of the sharp rise in

inflation. For a third time in the past eight years (after 2004 and 2008) the real

rate of return on 1yr bank saving deposits has sunk deep into negative territory,

averaging -2.5% in Jan-Sep 2011 (Figure 18). The IMF (2011a, p.34) finds that

a 1pp increase in the real rate of return on bank deposits lowers the urban

household saving rate by 0.6pp.

Fig. 18: 1yr inflation-adjusted real deposit rate

Source: CEIC and Nomura Global Economics.

Fig. 7

It should come as no surprise then, that despite waves of macro-prudential

tightening measures, it has proved difficult to cool speculation in the property

market. Moreover, with negative inflation-adjusted returns, banks have been

finding it more difficult to attract deposits and so are turning to wealth-

management products, which typically are loans repackaged as short-term

investment vehicles and are held off-balance sheet. These products are

typically short term, maturing within one month, and can offer annualized

returns of about 8%, more than double that on 1yr bank deposits. According to

Xinhua news agency, by mid-2011 China had RMB7trn in outstanding wealth

management products, triple the amount at the end of 2010. With bank assets

mainly tied to longer-term loans, there is a growing problem of duration

mismatch between bank assets and liabilities.

Perhaps in response, in this latest tightening cycle the PBC has hiked interest

rates on longer-term bank deposits by a larger magnitude, which has shifted

some of the costs of financial repression back to the banks. For example,

since September 2010 the 1yr bank deposit rate been increased by 125bp,

and the 5yr rate by 190bp, while the benchmark 5yr or longer lending rate has

been increased by only 114bp. Interestingly, this seems to be forcing banks to

price credit risk more actively by charging borrowing rates that are higher than

official benchmark rates on more of their loans: in June 2011, a record-high

61.2% of loans were priced above benchmark rates, versus 44.3% in

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

Sep-97 Sep-99 Sep-01 Sep-03 Sep-05 Sep-07 Sep-09 Sep-11

% p.a.

One way to help ease this financial repression is to allow a wide interest rate margin, but this shifts the repression from the banks to depositors

Negative real bank deposit rates have contributed to property market speculation and the explosion of wealth-management products

Nomura | Asia Special Report November 2011

24

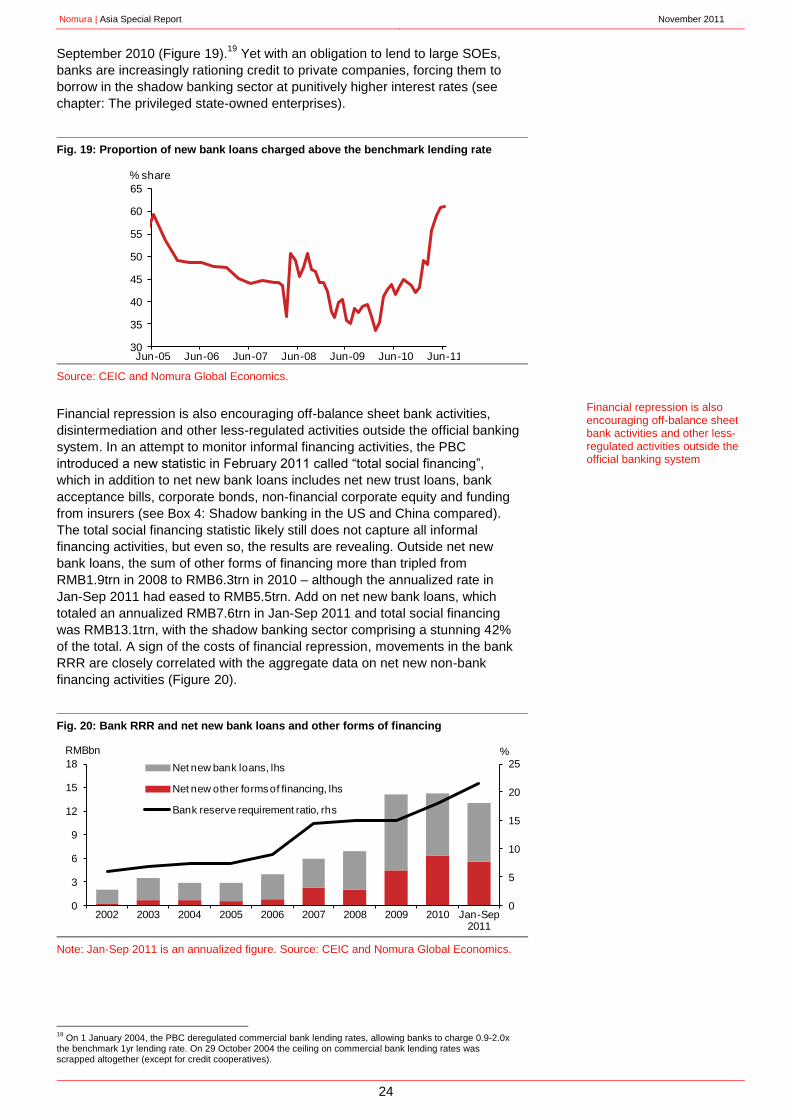

September 2010 (Figure 19).19

Yet with an obligation to lend to large SOEs,

banks are increasingly rationing credit to private companies, forcing them to

borrow in the shadow banking sector at punitively higher interest rates (see

chapter: The privileged state-owned enterprises).

Fig. 19: Proportion of new bank loans charged above the benchmark lending rate

Source: CEIC and Nomura Global Economics.

Fig. 8

Financial repression is also encouraging off-balance sheet bank activities,

disintermediation and other less-regulated activities outside the official banking

system. In an attempt to monitor informal financing activities, the PBC