Embed Size (px)

Citation preview

Still an open road

China wind

Joseph Lam, CFA – NIHK+852 2252 [email protected]

Thomas Tang – NIHK+852 2252 [email protected]

Scott Chui – NIHK+852 2252 [email protected]

June 2014

Connecting Markets East & West

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Any authors named on this report are research analysts unless otherwise indicated.

Equity Research

Stocks for action – Overall bmanufacturers to operators

Stocks for action

Source: Bloomberg, Nomura research. Pricing as on 17 June 2014

Positive on sector fundamentals, given: Strong wind power capacity growth ahead, with the 12th FYP wind cap

112/210GW). Continuous improvement in the wind curtailment issue, with the accele

release of Renewable Portfolio Standard, as well as other government Prefer wind equipment to wind farm operators

Wind equipment makers as the direct beneficiary with immediate earni Wind farm operators can also benefit from the recovery in wind sector f

contribution, as well as a potential wind power tariff cut. Prefer mixed players given their solid cash inflow and diversified risk

Quality cash inflows generated from traditional fuel sources (coal/hydro Diversify the policy/climate risk on single fuel source.

Stock picks: CHST (658 HK) – Positioned as an industrial conglomerate: 1) the recove

y-y in 2014F); and 2) a turnaround for loss-making new businesses (includ Huadian Fuxin (816 HK) – A diversified and well balanced portfolio across

universe, with strong capacity growth ahead (17.6% 2013-15 CAGR across

Company Ticker RatingWind equipmentCHST 658 HK Buy 7.30 Goldw ind 2208 HK Buy 9.67

Wind operatorsHuadian Fuxin 816 HK Buy 5.30 China Longyuan 916 HK Buy 9.50 Huaneng RE 958 HK Buy 2.90 Datang RE 1798 HK Reduce 1.00

Price target (HKD)

1

bullish, prefer equipment

pacity target of 100/200GW by 2015/20F likely to be beaten (our estimate of

ration of UHV transmission lines’ construction and approval, potential policies regarding clean energy.

ngs impact for wind power capacity growth.fundamentals, but this requires capex investment first before any earnings

k portfolio: o/nuclear) support the rapid growth of renewable business (wind/solar)

ry of the wind gearbox business with strong sales volume growth ahead (at 23.3% ing CNC and LED sapphire substrates) in 2014F.s different fuel mix (wind, hydro, coal, nuclear, etc.), which is unique in the s different fuel types). Relatively low equity financing risk.

China wind: Major sector-specific news flow and regulatory development/

Source: Nomura research

4 Dec 2012MOF announced supplemental renewable tariff payment for Oct 2010 - Apr 2011

12 Dec 2012MOF announced advances for supplemental renewable tariff in 2012

18 Dec 2012Supplemental 2nd batch preliminary approval for wind power projects (8.5GW)

8 Jan 2013NEA targets to add 18GW wind power capacity in 2013

25 Jan 2013SREC established surplus wind power trading mechanism from Northeast China to North China

1 Feb 2013SERC requested higher wind/solar power dispatch to alleviate pollution levels

10 Mar 2013NEA andSERC merged under NEA

19 Mar 2013- 3rd batch preliminary approval for wind power projects (28.7GW)- NEA announced that it will take measures to promote wind power dispatch in 2013

22 Mar 2013NEA announced initiatives to promote heat generation using wind power

4 Apr MoF aadvancsupplerenew(unspe

24N20inof

Continuous governmental su

2

/proposals

14 Apr 2014NEA published notice to urge related parties to secure the absorption of wind power output

2013announced ces for emental

wable tariff ecified period)

4 Jan 2014EA released014 wind power nstallation target f 18GW

28 Feb 20144th batch preliminary approval for wind power projects (27.6GW)

15 May 2013NEA delegated wind power approval authority to local governments

13 Sep 2013State Council published the Action Plan of Air Pollution Control, promoting clean energy

4 Jun 2014NEA signed task paper with State Grid and South Grid to promote the construction of 12 new UHV lines

16 May 2014NDRC published the notice to push the air pollution control in energy industry, with 2015/17 wind capacity target of 100/150GW

upport and favorable policies

30 46

61 75

93

112 130

148

168

189

210

13

17

14 15

18 19 18 18 20

21 21

-

5

10

15

20

25

-

50

100

150

200

250

2010 2011 2012 2013 2014F 2015F 2016F 2017F 2018F 2019F 2020F

GWGW

Wind power capacity - LHS Annual addition - RHS

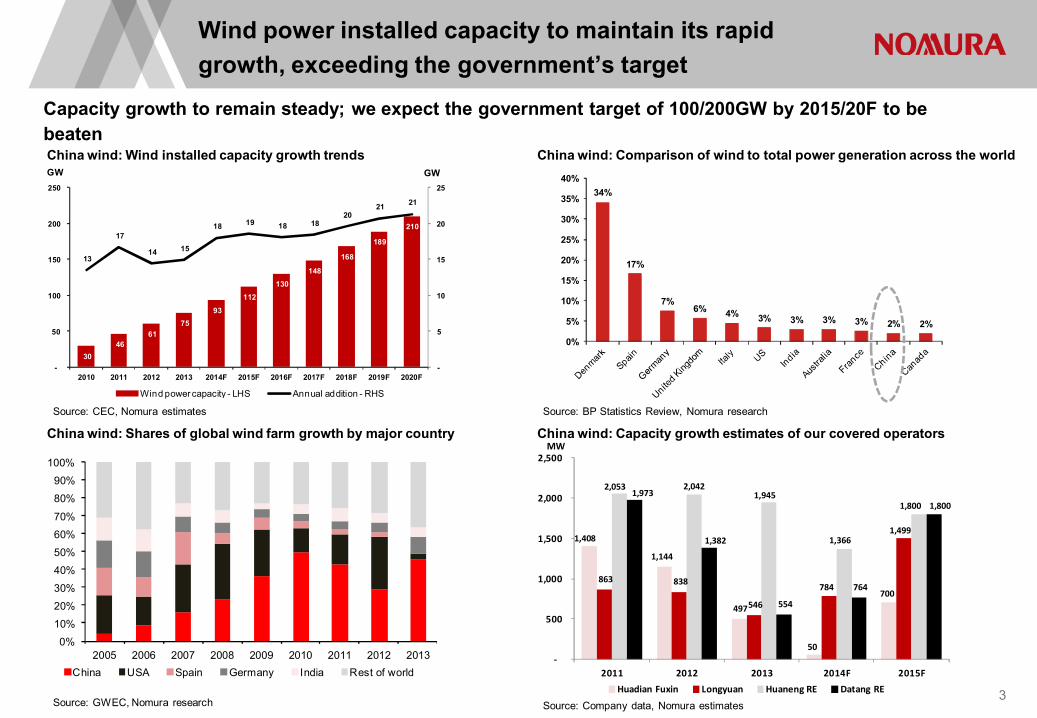

Wind power installed capacigrowth, exceeding the gover

Capacity growth to remain steady; we expect the govebeatenChina wind: Wind installed capacity growth trends

Source: CEC, Nomura estimates

China wind: Shares of global wind farm growth by major country

Source: GWEC, Nomura research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013China USA Spain Germany India Rest of world

34%

17%

7%6% 4% 3% 3% 3% 3% 2% 2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1,408

1,144

497

50

700 863 838

546

784

1,499

2,053 2,042 1,945

1,366

1,800 1,973

1,382

554

764

1,800

‐

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014F 2015F

MW

Huadian Fuxin Longyuan Huaneng RE Datang RE

ty to maintain its rapid rnment’s target

ernment target of 100/200GW by 2015/20F to be

3

China wind: Comparison of wind to total power generation across the world

Source: BP Statistics Review, Nomura research

China wind: Capacity growth estimates of our covered operators

Source: Company data, Nomura estimates

To avoid curtailment, and to enjoy the higher FiT, wind capacitYunnan, Guizhou, Guangdong, Fujian provinces.

China wind: Map of China’s wind resources and each provinces’ share of China’s total 75.5GW end-2013 cumulative wind installed capacity

Source: CEC, GWEC, Nomura research

Hainan0.4

Inner Mongolia23.8

Beijing0.2

Hebei10.4

Tianjin0.3

Jiangs3.4Anhui

0.7Zhejia

0.6

Henan0.4

Hubei0.5

Shaanxi0.8

Ningxia4.0

Qinghai0.1

Xinjiang6.6

TibetSichuan

0.1

Yunnan2.2 Guangxi

0.5

Guizhou1.8

Fujian1.9

Hunan0.4

Jiangxi0.4

Shanxi4.2 Shandong

6.6

Taiw

Liao7.

Guangdong2.2

Chongqing0.1

Gansu9.3

Wind Power Density

200 w/m2 (high)

150-200 w/m2

100-150 w/m2

50-100 w/m2

50 w/m2 (low)

Numbers are in % of 2013 national wind power installed capacity

From North to South - The gcapacity growth tilted

ty addition has gradually migrated to southern regions such as

4

China wind: Total 4 batches of preliminary approved projects breakdown by regions

Source: NEA, CEC, Nomura research

China wind: Capacity growth by regions – 2013 and 1Q14

Source: CEC, Nomura research

Jilin5.0

u

Shanghai0.4

ang6

wan

Heilongjiang5.2

ning5

8,550 5,680 6,163 5,546

8,870

980 491 804

1,760

3,778 3,732 3,955

1,480

4,340 3,693 5,569

2,100

4,420 6,101 4,314

4,070

3,370

7,808 7,409

0

5,000

10,000

15,000

20,000

25,000

30,000

1st batch 2nd batch 3rd batch 4th batch

MW

Northern China Northeatern China Eastern ChinaCentral China Southern China Northwestern China

26,830

22,568

27,986 27,597

Region 2013 Capacity grow th 1Q14 Capacity growthNorthern China 17.8% 4.4%Northeatern China 13.8% 2.6%Eastern China 32.3% 5.6%Central China 125.0% 22.4%Southern China 39.1% 4.0%Northw estern China 32.0% 12.8%

geographical mix of wind

China wind: National installed and grid connected wind power generation capacity (2006-2013)

Source: GWEC, CEC, Nomura research

China wind : Annual wind farm installations by province (2009-13)

Source: CEC, Nomura research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013Inner Mong Gansu Liaoning Jilin Heilongjiang HebeiShandong Xinjiang Jiangsu Ningxia Shanxi GuangdongFujian Yunnan Zhejiang Others

2 49

16

30

45

61

75

3 612

26

45

62

75

91

23%

32%

25%

38%34%

28%

19%17%

0%

10%

20%

30%

40%

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012 2013

%GW Grid connected capacity (LHS)Installed capacity (LHS)% of capacity unconnected (RHS)

Wind supply and demand an

5

China: Power generation surplus over local power demand by province (2013)

Source: CEC, Nomura research

China wind: Wind farm operators current installed capacity by region

Source: NDRC, Nomura research

-150

-100

-50

0

50

100

150

bn kWh

19%

28%

44%

33%

21%

20%

24%

18%

40%

33%

21%

42%

20%

20%

11%

6%

0% 20% 40% 60% 80% 100%

Longyuan

Huaneng RE

Datang RE

Huadian Fuxin

In. Mongolia Northeastern Central and western Southeastern coastline

nalysis

China wind: Annual wind capacity installation by region

Source: LY, HN RE, DT RE, Nomura research

China wind: Annual wind power generation mix by region

Note: Huadian Fuxin does not disclose its annual power generation by regionsSource: Company data, Nomura research

512233

444 491248 110

338 892 341 297

147

38

214

647

849 744

1,075

913

140

230 419 510476

306

0

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012 2013

MW Longyuan

Inner Mongolia Northeastern

Central and Western Southeastern Coastline

0 0 0 0199 24950 63297

393

80

0

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012 2013

MW Huadian Fuxin

Inner Mongolia Northeastern

Central and Western Southeastern Coastline

19% 23% 29%22% 20% 23%

19%

30%29%

31% 28% 21%

31%

25% 21%18% 21% 33%

30%21% 20%

30% 31%23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012

LongyuanInner Mongolia NortheasternCentral and Western Southeastern Coastline

14%

35% 38%23%26%

41%

31% 24%

24%6%

11%

9% 17%

31%

100%

68%

33%24% 21% 23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012

Huaneng REInner Mongolia NortheasternCentral and Western Southeastern Coastline

Wind farm operators’ strateg

6

e

593

975

1490101

401

299

299

50 9998

387

678

306

56675

155

312

257

198

99

0

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012 2013

MW Huaneng RE

Inner Mongolia Northeastern

Central and Western Southeastern Coastline

527 494 399 293149 50

179 249 402

200

9899

95 50

379

342

19850

50 59

230

309

53

0

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012 2013

MW Datang RE

Inner Mongolia Northeastern

Central and Western Southeastern Coastline

54%70%

62% 63%52%

43%

34%

21%22% 22%

24%

23%

12% 9%10% 7%

13%20%

6% 8% 10% 13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012

Datang REInner Mongolia NortheasternCentral and Western Southeastern Coastline

gy – Heading south

Wind Power Density

200 w/m2 (high)

150-200 w/m2

100-150 w/m2

50-100 w/m2

50 w/m2 (low)

Yunnan

Guizhou

Sichuan

Guangxi

East Inner Mongolia

Wind Power Density

200 w/m2 (high)

150-200 w/m2

100-150 w/m2

50-100 w/m2

50 w/m2 (low)

Jiangsu

Xinjiang

Gansu

Guangdong

China wind: Wind farm operators’ guidance on near-term focus areas

Source: Company data, Nomura research

Huadian Fuxin

Huaneng RE

Wind farm operators’ strateg

Wind Power Density

200 w/m2 (high)

150-200 w/m2

100-150 w/m2

50-100 w/m2

50 w/m2 (low)

Zhejiang

Jiangsu

Shandong

Yunnan Guangxi

Wind Power Density

200 w/m2 (high)150-200 w/m2100-150 w/m250-100 w/m250 w/m2 (low)

Jiangsu

FujianYunnan

7

Longyuan

Datang RE

gy – Heading south

1,750

1,950

2,150

2,350

2,550

2,750Hrs 2010 2011 2012

2013 2014

1,000

1,500

2,000

2,500

3,000Hrs

2010 2011 20122013 2014

Wind utilisation recovered rolows… and likely to be stable

China wind: YTD (annualised) wind farm utilisation

Source: CEC, Nomura research

China wind: Monthly (annualised) wind farm utilisation

Source: CEC, Nomura research

NA

NA

20%

11%

8%

10%

14%

12%

6%

12%

21%

11%

NA

17%

21%

15%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013

Huadian Fuxin Longyuan Huaneng RE Datang RE

obustly in 2013 from 2012 e in 2014F

Weak wind speed in 4M14; but seeing recovery since May Policy and infrastructure initiatives NEA’s notice to ensure the wind power absorption in 2014 Excess wind power generation trading system

8

PRC wind farm operators’ reported wind power curtailment ratios

Source: Company data, Nomura research

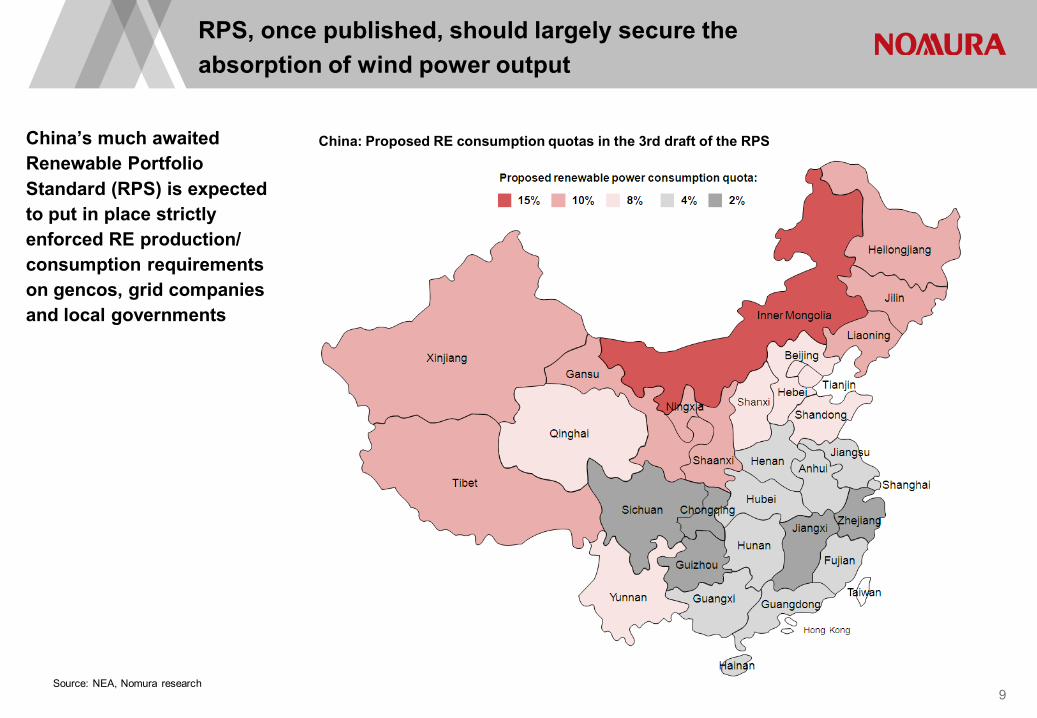

China: Proposed RE consump

Source: NEA, Nomura research

China’s much awaited Renewable Portfolio Standard (RPS) is expected to put in place strictly enforced RE production/ consumption requirements on gencos, grid companies and local governments

RPS, once published, shouldabsorption of wind power ou

9

ption quotas in the 3rd draft of the RPS

d largely secure the utput

China: UHV grid

Source: NDRC, NEA

The build-out of China’s power transmission infrastructu

6

12

345

7

Southeast Shanxi-Nan

Xiangjiaba – Shangha

Jinping – South Jiang

South Hami – Zhengz

Huainan – Shanghai 1

Xiluodu – West Zhejia

North Zhejiang – Fuzh

Huainan – Nanjing - S8

UHV grid lines – Constructio

After years’ of debate on the applied technology, the central government seems to have made its decision and preliminary approved a whole pack of 12 UHV grid lines to be built in the next 3-5 years in early 2014

Transmission lines Type Voltage Transmission forNingxia - Zhejiang DC ±800kv Wind pow erShanghaimiao - Shandong DC ±800kv Wind pow erXimeng - Jiangsu DC ±800kv Wind pow erXimeng - Shandong AC 1000kv Wind pow erWest Inner Mongolia - South Tianjin AC 1000kv Wind pow erSuizhong - Nothern China Grid DC ±500kv Coal-f iredShanxi - Hebei DC ±500kv Coal-f iredShenmu - Hebei DC ±500kv Coal-f iredShanxi - Zhejiang DC ±800kv Coal-f iredHuainan - Nanjing - Shanghai* AC 1000kv Coal-f iredYuheng - Weifang AC 1000kv Coal-f iredLijiang - Shenzhen DC ±800kv Coal-fired, Hydropow er

China: Details of the 12 UHV lines preliminary approved

Source: NEA, State Grid, Nomura research

10

d expansion plans before 2020

A, State Grid, Nomura research

ure is of crucial importance to the wind power industry...

Hainan

Inner Mongolia

Jilin

Beijing

HebeiTianjin

Jiangsu

Anhui Shanghai

Zhejiang

Henan

Hubei

Shaanxi

Ningxia

Qinghai

Xinjiang

TibetSichuan

Yunnan Guangxi

Guizhou Fujian

Hunan Jiangxi

ShanxiShandong

Taiwan

Heilongjiang

Liaoning

Guangdong

Chongqing

Gansu

1000kV UHVAC planned

± 800/±1000 kV UHVDC planned

± 800kV UHVDC completed

1000kV UHVAC completed

± 800kV UHVDC under construction

1000kV UHVAC under construction

10GW scale wind power bases

23

1

5

4

7

nyang – Jingmen 1000kv UHVAC

ai ±800kv UHVDC

gsu ±800kv UHVDC

zhou ±800kv UHVDC

1000kv UHVAC

6

ang ±800kv UHVDC

hou ±800kv UHVDC

Xinjiang Hami

Gansu Jiuquan

West Inner Mongolia

East Inner MongoliaJilin

Hebei

Shandong coastline

Jiangsu coastline

Shanghai 1000kv UHVAC

8

on accelerating

CNY 0.51/kWh Category I resource area

CNY 0.54/kWh Category II resource area

CNY 0.58/kWh Category III resource area

CNY 0.61/kWh Category IV resource area

China: The current four-tier wind FiT by region (incl. VAT)

Source: China wind power outlook (2010), Nomura research

Wind tariff – Generally stablenewly installed projects

We expect FiT for wind power will see a gradual decline – to be- The central government targets to reach grid-parity by 2020F;- The decline in equipment cost;- The further improvement of curtailment issue.

11

China wind: Wind operators’ blended wind tariffs (ex VAT)

Source: Company data, Nomura research

0.44

0.45

0.46

0.47

0.48

0.49

0.50

0.51

0.52

2013 2014F 2015F 2016F 2017F 2018F 2019F 2020F

CNY/kWhHuadian Fuxin Longyuan Huaneng RE Datang RE

e but may see tariff cut for

e cut by 5% every two years starting from 2015F to 2020F, given:

5,689 5,327 5,333

4,222 3,765 3,589 3,509

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013

CNY/kW

427

471

537 541

485 502 494

400

440

480

520

560

600

2007 2008 2009 2010 2011 2012 2013

CNY/kW

Goldwind: Trend of 1.5MW WTG ASP CHST: Trend of 1.5MW gearbox ASP

Source: Company data, Nomura research

385% 395%

342%366%

173% 182% 178% 177%187%

232%209%

242%

341%

409% 411%437%

150%

200%

250%

300%

350%

400%

450%

500%

2010 2011 2012 2013Huadian Fuxin Longyuan Huaneng RE

‐ Longyuan's placement & perp bond issuance‐Huadian Fuxin IPO

Datang RE IPOHuaneng RE IPO

Huaneng REplacement

1,408

1,144

497

50

700 863 838

546

784

1,499

2,053 2,042 1,945

1,366

1,800 1,973

1,382

554

764

1,800

‐

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014F 2015F

MW

Huadian Fuxin Longyuan Huaneng RE Datang RE

A trade-off between capacityrisk

China wind: Wind farm operators’ capacity addition – 2011-15F

Source: Company data, Nomura estimates

PRC wind farm operators: Net D/E profiles

Source: Company data, Nomura research

350%381%

183% 177%

289%

323%

453% 457%

2014F 2015FDatang RE

Huadian Fuxin placement

y growth and gearing / dilution

12

Source: Company data, Nomura research

4,397 6,000 2,727 2,458 2,305 2,753 1,813 2,111

52.4%45.9%

66.5%

85.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

1,000

2,000

3,000

4,000

5,000

6,000

Huadian Fuxin Longyuan Huaneng RE Datang RE

CNY mn

EBIT Net financial expenses % of net financial expenses to EBIT

China wind: Wind farm operators’ financial expenses to EBIT - 2013

R&M cost will surge due to tWTGs, while remains a relati

China wind: Wind farm operators’ cost breakdown – 2012-15F

Source: Company data, Nomura research

2012 y-y 2013 y-y 2014F y-y 2015FHuadian Fuxin - Depreciation (1,798) 44.5% (2,175) 21.0% (2,592) 19.2% (3,166) - Fuel cost (4,107) 104.4% (4,362) 6.2% (4,381) 0.4% (4,883) - Labor (801) 21.1% (955) 19.3% (1,139) 19.2% (1,322) - R&M (335) 99.3% (440) 31.3% (524) 19.2% (609)

- Administration (430) 89.8% (415) -3.5% (494) 19.2% (574) - Financial expenses (1,905) 58.6% (2,305) 21.0% (2,538) 10.1% (3,016) - Others (451) 219.2% (217) -51.9% 167 na 736 Total (9,826) 73.9% (10,869) 10.6% (11,501) 5.8% (12,833) Total expenses / revenue 86.6% 8.9ppt 82.1% -4.5ppt 77.3% -4.8ppt 73.7%

Longyuan - Depreciation (3,697) 29.9% (4,391) 18.8% (5,030) 14.5% (5,680) - Fuel cost (5,824) -14.0% (5,086) -12.7% (4,792) -5.8% (4,726) - Labor (925) 20.3% (1,115) 20.5% (1,193) 7.0% (1,244) - R&M (305) 20.2% (521) 71.0% (538) 3.2% (667)

- Administration (402) 36.6% (396) -1.3% (448) 13.2% (444) - Financial expenses (2,485) 61.8% (2,753) 10.8% (2,755) 0.1% (3,257) - Others (390) 15.4% (980) 151.5% (677) -30.9% (676) Total (14,027) 9.5% (15,242) 8.7% (15,432) 1.2% (16,694) Total expenses / revenue 81.1% 1.9ppt 79.7% -1.4ppt 74.7% -5.0ppt 74.1%

Huaneng RE - Depreciation (1,612) 37.9% (1,931) 19.8% (2,223) 15.1% (2,799) - Labor (151) 28.0% (205) 36.0% (268) 30.5% (331) - R&M (50) 68.3% (91) 80.7% (96) 5.0% (168)

- Administration (127) 7.7% (146) 15.4% (191) 30.5% (236) - Financial expenses (1,530) 50.2% (1,813) 18.5% (2,206) 21.7% (2,931) - Others (104) 12.8% (420) 303.8% (202) -51.8% (265) Total (3,574) 40.4% (4,607) 28.9% (5,185) 12.6% (6,730) Total expenses / revenue 88.8% 9.1ppt 79.5% -9.3ppt 77.0% -2.5ppt 76.1%

Datang RE - Depreciation (1,857) 36.4% (2,201) 18.5% (2,445) 11.1% (2,716) - Labor (265) 41.1% (353) 33.2% (295) -16.3% (328) - R&M (83) 19.6% (121) 45.6% (175) 45.0% (223)

- Material costs (24) -21.0% (65) 171.7% (46) -29.2% (51) - Financial expenses (1,934) 46.8% (2,111) 9.2% (2,171) 2.8% (2,387) - Others (294) 19.8% (374) 27.1% (390) 4.3% (440) Total (4,457) 38.8% (5,224) 17.2% (5,522) 5.7% (6,144) Total expenses / revenue 102.0% 18.2ppt 92.8% -9.2ppt 91.9% -0.8ppt 90.7%

he increasing out-of-warranty ively small portion

13

China wind farm operators: Proportion of out-of-warranty WTG

y-y 2012-15F CAGR

22.1% 20.8%11.5% 5.9%16.1% 18.2%16.1% 22.0%

16.1% 10.1%18.8% 16.6%

na na11.6% 9.3%

-3.6ppt

12.9% 15.4%-1.4% -6.7%4.3% 10.4%

24.0% 29.8%

-0.9% 3.4%18.2% 9.4%-0.2% 20.1%8.2% 6.0%

-0.6ppt

25.9% 20.2%23.4% 29.9%76.3% 49.6%

23.4% 22.9%32.9% 24.2%31.4% 36.7%29.8% 23.5%

-0.9ppt

11.1% 13.5%11.0% 7.3%27.0% 38.9%

11.0% 28.7%10.0% 7.3%12.8% 14.4%11.3% 11.3%

-1.2ppt

Source: Company data, Nomura research

7%

53%

4%

15%21%

57%

18%

39%35%

61%

35%

44%

0%

10%

20%

30%

40%

50%

60%

70%

Huadian Fuxin Longyuan Huaneng RE Datang RE

2013 2014F 2015F

Why R&M cost will surge? A typical warranty period for WTG is 3-5 years; Generally, it will cost 3-4 times for R&M

expenses when a WTG’s warranty is expired.

Wind farm operators: CDM income profiles and contribution to PBT

CER and EUA price trends

Source: Bloomberg, Nomura research

0

5

10

15

20

25

17-J

un-0

9

17-O

ct-0

9

17-F

eb-1

0

17-J

un-1

0

17-O

ct-1

0

17-F

eb-1

1

17-J

un-1

1

17-O

ct-1

1

17-F

eb-1

2

17-J

un-1

2

17-O

ct-1

2

17-F

eb-1

3

17-J

un-1

3

17-O

ct-1

3

EUR/ ton EUA Future CER Futur

CDM income – An old-time fa

118 210 392 727 742 54

19%

11%

12%

20% 20%

2%

0%

5%

10%

15%

20%

25%

0

100

200

300

400

500

600

700

800

2008 2009 2010 2011 2012 2013

CNY mn

LongyuanCDM income - LHS % of PBT - RHS

31 75 155 134 -

5%

8%

21%

8%

0%0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

120

140

160

180

2008 2009 2010 2011 2012 2013

CNY mn

Huadian FuxinCDM income - LHS % of PBT - RHS

Source: Company data, Nomura research

14

17-F

eb-1

4

17-J

un-1

4

e

airy tale

%

%

%

%

16 29 165 484 105 -

17%

9%

26%

42%

17%

0%0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013

CNY mn

Huaneng RECDM income - LHS % of PBT - RHS

72 137 229 371 61 58

30%

36%

31%

37%34%

16%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

50

100

150

200

250

300

350

400

2008 2009 2010 2011 2012 2013

CNY mn

Datang RECDM income - LHS % of PBT - RHS

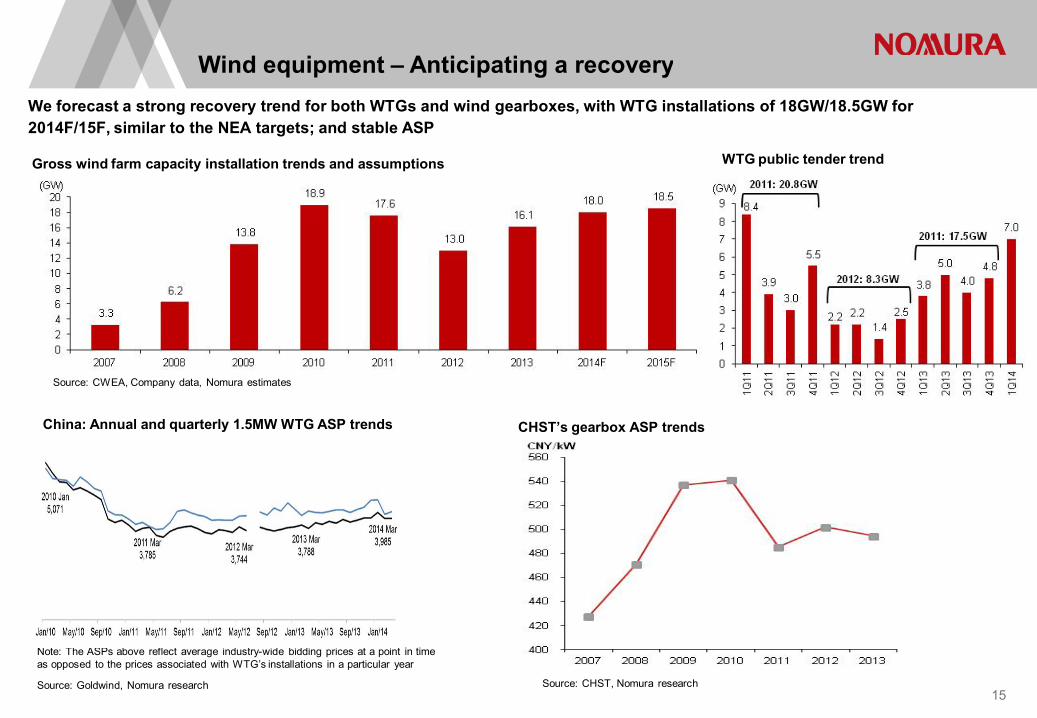

Gross wind farm capacity installation trends and assumptions

We forecast a strong recovery trend for both WTGs and wind gea2014F/15F, similar to the NEA targets; and stable ASP

Wind equipment – Anticipati

Source: Goldwind, Nomura research

Note: The ASPs above reflect average industry-wide bidding prices at a point in time as opposed to the prices associated with WTG’s installations in a particular year

China: Annual and quarterly 1.5MW WTG ASP trends

Source: CWEA, Company data, Nomura estimates

15

arboxes, with WTG installations of 18GW/18.5GW for

ng a recovery

Source: CHST, Nomura research

WTG public tender trend

CHST’s gearbox ASP trends

Positioned as an industrial conglomerate Diversified business with six segments, namely: 1) gearbox (including wind, tr

computer numerical controlled (CNC) system; 4) coal mining machinery; 5) lig

Wind gearbox: On a strong recovery trend with sales volume to grow Domestic market: 15%-plus sales volume growth given the improving wind p Overseas market: 50% sales volume growth due to the strong demand from

New businesses (CNC, coal mining machines and LED): we expect t CNC: marginally breakeven in 2013FY, and expecting a slight profit in 2014F. Coal mining machines: remain cautious given the challenging environment. LED: At early stage of the business with loss making situation in 2013FY, but

profit in 2014F when it achieves economies of scale (current production at ~0

Valuation: Attractive valuation vs peers At HKD5.42, the stock is trading at attractive 2014F P/E and P/B of 15.6x and

P/B.

China High Speed Transmis

CHST: Wind gearboxes sales volume (2008CHST: Wind gearboxes sales volume (2008--15F)15F)

2,506

5,474

8,156 7,266 4,777 5,719 6,624 7,115

704

954

1,083 1,362

1,901 1,613

2,419 3,024

-30%

0%

30%

60%

90%

120%

150%

0

2,000

4,000

6,000

8,000

10,000

12,000

2008

2009

2010

2011

2012

2013

2014

F

2015

F

(MW) Domestic (LHS)Export (LHS)y-y growth (RHS)

Source: CWEA, NEA, Company data, Nomura estimates

raditional, high-speed locomotives, etc); 2) marine gearbox; 3) ght-emitting diode (LED) sapphire substrates; and 6) mechatronics.

w 23.3% y-y in 2014Fpower generating environment in China since 2H13GE in the US.

to see a turnaround.

CHST is expecting the business to break even or achieve a slight .3mn units / month vs. end-2014F target of 0.8mn units / month).

0.8x, respectively, vs Goldwind (2208 HK, Buy) at 26.0x P/E and 1.4x

16

ssion (658 HK, Buy)

CHST’s gearbox ASP trendsCHST’s gearbox ASP trends

Note: The ASPs disclosed are blended across both domestic and export sales and exclude PRC VAT at 17%

WTG sales: a direct beneficiary of expected wind power market reb Solid WTG sales volume growth due to: 1) most of the wind farm projects a

Goldwind has a homefield advantage in the Hami Wind Farm Project Phase and 4) the NEA also targets 18GW of new wind installed capacity in 2014, up

Limited upside potential in margin expansion: the ASP for wind turbines t

Wind power services: only a small earnings contributor 20% revenue growth and a slight pick up in GPM given revenue mix will shift Limited opportunity from ex-warranty installed base, given: 1) usually on

maintenance services; and 2) many mid-to-large wind farm operators have a

Wind farm development: gaining importance as a wind farm operat 700MW new capacity each year for 2014-15F, thanks to 3.1GW project pipel The company will pursue more on a “build-and-operate” strategy instead of a

Valuation: High valuation justified, but CHST is our preferred play Trading at 2014F P/E of 26.0x and P/B of 1.4x, Goldwind shares are at a pre

which trades at 15.6x P/E and 0.8x P/B. We believe the high valuation is just

Xinjiang Goldwind (2208 HK

Goldwind: WTG sales volume Goldwind: WTG sales volume (2007(2007--16F)16F)

China: 1.5MW WTGChina: 1.5MW WTGpublic bidding pricpublic bidding pric

Source: Company data, Nomura estimates

boundapproved by the NEA under the four batches are still pending construction; 2) II; 3) we see mid- to long-term potential for offshore wind farm development; p 11.8% y-y from 16.1GW in 2013.to remain flattish to slightly, with limited cost reduction esp. for 1.5MW WTGs

t to higher-margin maintenance service instead of lower-margin EPC.nly wind farms installed with Goldwind’s wind turbines will use Goldwind’s already set up their own internal teams for maintenance.

torline under the four batch of NEA approvals

a “build-and-sell” strategy

emium valuation to peers and more specifically to wind equipment peer CHST, tified by a three-year EPS CAGR of 37.3%. Buy.

17

K, Buy)

G monthly average G monthly average ce (CNY/kW)ce (CNY/kW)

GoldwindGoldwind: Market share of the : Market share of the WTG sales in ChinaWTG sales in China

Wind farm operators – Rapidprefer players with diversifie

Huadian Fuxin (816 HK, Buy, TP HKD5.30) – A diversified clean ene A diversified and well balanced portfolio of generation assets across differen Strong capacity growth ahead: At 17.6% 2013-15 CAGR across different fue Low equity financing risk Valuation: Trading at 13.1x 2014F P/E (at the lower end of its peers’ range o Initiated coverage at Buy with TP of HKD5.3 on 15 May 2014.

Longyuan (916 HK, Buy, TP HKD9.50) – Premium for its balance sh The strongest balance sheet across peers: Low dilution risk A mix of coal-fired and wind power generation portfolio: Risk diversification a Steady and quality wind capacity growth: Mediocre capacity growth across p

exposure in overseas market and first-mover advantage in low-wind-speed r Valuation: Trading at 16.3x 2014F P/E (at the higher end of its peers’ range o

strong balance sheet.

Huaneng RE (958 HK, Buy, TP HKD2.90) – Wind blowing with sunsh Strong capacity growth: Fastest wind capacity growth among peers at 1.8GW More emphasis on solar power business: ~200MW in new solar capacity pa Dilution risk remains given high gearing: Strong capacity growth comes with Valuation: Trading at 12.8x 2014F P/E (at the low end of its peers’ range of 1

of 38.9%.

Datang RE (1798 HK, Reduce, TPHKD1.00) – Choked by high gearin Slowest wind capacity growth: With 0.6-0.8GW annual capacity additions for Curtailment eases but remains high vs peers Heavy financial burden given high gearing: With net gearing ranges between

largely eroded by interest expenses, and a potential equity financing exercis Valuation: Trading at 16.9x 2014F P/E (at the high end of its peers’ range of

18

d capacity growth ahead; ed exposure

ergy exposurent fuel mix (wind, hydro, coal, nuclear, etc.): Unique in the universeel types

of 12.8x-16.9x) and 1.9x P/B. Attractive

heet strength

across different fuels.peers, but with potential margin and curtailment improvement, thanks to its regions.of 12.8x-16.9x) and 1.6x P/B; at a premium to peers but justifiable given its

hineW pa, implying a 25.6% 2013-15F CAGR.at a decent IRR of 12-15%.high capex needs; seeing potential equity financing in the mid- to long-term.

12.8x-16.9x) and 1.3x P/B; undemanding, given its strong 2013-16F EPS CAGR

ngr 2014/15F, implying a 11.6% 2013-15F CAGR, the lowest among peers.

n 430-460% in 2014-16F per our estimates, we see the company’s profit being e in the near-term is more likely than peers.12.8x-16.9x) and 0.6x P/B; demanding.

Wind Power Density

200 w/m2 (high)

150-200 w/m2

100-150 w/m2

50-100 w/m2

50 w/m2 (low)

Southeastern Coastline1,224MW windInstalled capacity(20% of portfolio)

Inner Mongolia1,716MW windInstalled capacity(28% of portfolio)

Central and Western 2,034MW windInstalled capacity(33% of portfolio)

Northeastern China1,247MW windInstalled capacity(20% of portfolio)

Wind Power Installed

Power plant type

Wind Power Density

200 w/m2 (high)

150-200 w/m2

100-150 w/m2

50-100 w/m2

50 w/m2 (low)

Southeastern Coastline222MW windInstalled capacity(6% of portfolio)

Inner Mongolia1,170MW windInstalled capacity(33% of portfolio)

Central and Western 1,469MW windInstalled capacity(42% of portfolio)

Northeastern China640MW windInstalled capacity(18% of portfolio)

Wind Power Installed

Power plant type

China wind: Wind farm operators’ 2013 capacity distribution

Source: Company data, Nomura research

Huadian Fuxin

Huaneng RE

Wind farm operators’ currenLongyuan poised at a better

Wind Power Density

200 w/m2 (high)

150-200 w/m2

100-150 w/m2

50-100 w/m2

50 w/m2 (low)

Southeastern Coastline650MW windInstalled capacity(11% of portfolio)

Inner Mongolia2,507MW windInstalled capacity(44% of portfolio)

Central and Western 1,187MW windInstalled capacity(21% of portfolio)

Northeastern China1,375MW windInstalled capacity(24% of portfolio)

Wind Power Installed

Power plant type

Wind Power Density

200 w/m2 (high)150-200 w/m2100-150 w/m250-100 w/m250 w/m2 (low)

Power plant type

Wind Power InstalledCoal Power

Southeastern Coastline2,427MW wind installed capacity(20% of portfolio)

Inner Mongolia2,285MW wind installed capacity(19% of portfolio)

Central and Western4,709MW wind installed capacity(40% of portfolio)

Northeastern2,489MW wind installed capacity(21% of portfolio)

19

Longyuan

Datang RE

t capacity distribution –position

Note: Pricing as of 17 June 2014; ratings and price targets are as of the date of the most recently publishSource: Company data, Bloomberg, Nomura estimates

Valuation comparison I

ReportingCompany Ticker currency FY end RatingWind equipmentCHST 658 HK CNY Dec 1,635 BuyGoldw ind 2208 HK CNY Dec 2,695 BuyWind equipment average

Wind operatorsHuadian Fuxin 816 HK CNY Dec 7,980 BuyChina Longyuan 916 HK CNY Dec 8,036 BuyHuaneng RE 958 HK CNY Dec 9,029 BuyDatang RE 1798 HK CNY Dec 7,274 Reduce

Wind operators average

Company 2013 2014F 2015F 2013 2014FWind equipmentCHST 0.00 0.00 0.07 na naGoldw ind 0.08 0.08 0.12 1.1% 1.2%

Wind equipment average 0.04 0.04 0.09 1.1% 1.2%

Wind operatorsHuadian Fuxin 0.04 0.05 0.06 1.2% 1.5%China Longyuan 0.05 0.08 0.09 0.7% 1.2%Huaneng RE 0.02 0.03 0.04 0.9% 1.5%Datang RE 0.00 0.01 0.01 0.3% 0.9%

Wind operators average 0.03 0.04 0.05 0.8% 1.3%

No. of shares (mn)

DPS (Reporting $) Yield (%)

20

hed report (http://www.Nomura.com) rather than the date of this document.

Price Market cap(HKD) % upside (USD mn) 2013 2014F 2015F

7.30 5.42 34.7% 1,144 0.05 0.27 0.359.67 9.20 5.1% 3,199 0.16 0.27 0.38

2,171 0.10 0.27 0.37

5.30 4.18 26.8% 4,304 0.19 0.25 0.329.50 8.55 11.1% 8,866 0.26 0.41 0.472.90 2.73 6.2% 3,181 0.10 0.17 0.221.00 1.09 -8.3% 1,023 0.03 0.05 0.06

4,343 0.15 0.22 0.27

2015F 2013 2014F 2015F 2013 2014F 2015F

1.7% 0.0% 0.0% 20.0% 5.21 5.48 5.821.6% 50.4% 30.0% 30.0% 4.96 5.15 5.46

1.6% 25.2% 15.0% 25.0% 5.08 5.32 5.64

2.0% 20.8% 20.0% 20.0% 1.47 1.72 1.991.4% 18.6% 20.0% 20.0% 3.85 4.21 4.602.0% 20.3% 20.3% 20.3% 1.54 1.67 1.851.1% 9.2% 15.0% 15.0% 1.28 1.32 1.38

1.6% 17.2% 18.8% 18.8% 2.03 2.23 2.45

Price target (HKD)

EPS (Reporting $)

Dividend payout (%) BVPS (Reporting $)

Valuation comparison II

Note: Pricing as of 17 Jun 2014; Ratings and price targets are as of the date of the most recently publishSource: Company data, Bloomberg, Nomura estimates

Company 2013 2014F 2015F 2013Wind equipmentCHST 91.2 15.6 12.0 0.8Goldw ind 45.9 26.0 18.4 1.4Wind equipment average 68.6 20.8 15.2 1.1

Wind operatorsHuadian Fuxin 17.2 13.1 10.2 2.2China Longyuan 26.6 16.3 13.9 1.7Huaneng RE 20.9 12.8 9.4 1.4Datang RE 26.6 16.9 13.5 0.7Wind operators average 22.8 14.8 11.8 1.5

Company 2013 2014F 2015F 2013Wind equipmentCHST 84.7% 84.8% 79.8% 0.8%Goldw ind 27.6% 49.0% 65.4% 3.3%Wind equipment average 56.1% 66.9% 72.6% 2.0%

Wind operatorsHuadian Fuxin 365.7% 350.4% 380.9% 13.5%China Longyuan 177.7% 177.4% 183.2% 6.8%Huaneng RE 209.2% 241.8% 289.5% 6.9%Datang RE 410.9% 437.3% 453.0% 2.6%Wind operators average 290.9% 301.7% 326.6% 7.4%

P/E (x) P/B (

Net Gearing (%) RoE (

21

hed report (http://www.Nomura.com) rather than the date of this document.

2014F 2015F 2013 2014F 2015F

0.8 0.7 12.3 9.1 8.11.4 1.3 12.3 6.4 5.91.1 1.0 12.3 7.7 7.0

1.9 1.6 10.7 9.7 9.01.6 1.4 10.7 9.2 8.41.3 1.1 10.2 9.4 8.60.6 0.6 10.2 9.9 9.31.3 1.2 10.4 9.5 8.8

2014F 2015F 2013 2014F 2015F

5.0% 6.1% 2.8% 4.4% 5.1%5.4% 7.2% 1.4% 3.9% 4.6%5.2% 6.7% 2.1% 4.1% 4.8%

15.6% 17.0% 7.1% 7.6% 7.9%10.1% 10.7% 6.3% 7.2% 7.7%9.8% 12.0% 5.8% 6.3% 6.8%3.8% 4.6% 4.5% 4.7% 5.0%9.8% 11.1% 5.9% 6.4% 6.8%

(x) EV/EBITDA (x)

(%) RoA (%)

Source: Company data, Bloomberg, Nomura estimates

CHSTCHST GoldwindGoldwind

LongyuanLongyuan Huaneng REHuaneng RE

P/E comparison

22

Huadian FuxinHuadian Fuxin

Datang REDatang RE

Source: Company data, Bloomberg, Nomura estimates

P/B comparison

CHSTCHST GoldwindGoldwind

LongyuanLongyuan Huaneng REHuaneng RE

23

Huadian FuxinHuadian Fuxin

Datang REDatang RE

Appendix A-1Any Authors named on this report are Research Analysts unless otheAnalyst Certification We, Joseph Lam, Yuwen Tang and Scott Chui, hereby certify (1) that the views expressed in this Researeferred to in this Research report, (2) no part of our compensation was, is or will be directly or indirectlyour compensation is tied to any specific investment banking transactions performed by Nomura Securiti

Issuer Specific Regulatory Disclosures The term "Nomura Group" used herein refers to Nomura Holdings, Inc. or any of its affiliates or subsidia

Materially mentioned issuers Issuer Ticker Price Price date China Datang Renewable Power 1798 HK 1.08 HKD 18-Jun-2014China High Speed Transmission 658 HK 5.43 HKD 18-Jun-2014China Longyuan Power 916 HK 8.41 HKD 18-Jun-2014Huadian Fuxin 816 HK 4.28 HKD 18-Jun-2014Huaneng Renewables Corporation 958 HK 2.7 HKD 18-Jun-2014Xinjiang Goldwind 2208 HK 9.2 HKD 18-Jun-2014

Important Disclosures

Online availability of research and conflict-of-interest disclosures Nomura research is available on www.nomuranow.com/research, Bloomberg, Capital IQ, Factset, MarkImportant disclosures may be read at http://go.nomuranow.com/research/globalresearchportal/pages/di5752. If you have any difficulties with the website, please email [email protected] for help. The analysts responsible for preparing this report have received compensation based upon various factUnless otherwise noted, the non-US analysts listed at the front of this report are not registered/qualifiedbe subject to FINRA Rule 2711 and NYSE Rule 472 restrictions on communications with covered comp Nomura Global Financial Products Inc. (“NGFP”) Nomura Derivative Products Inc. (“NDPI”) and NomuraNational Futures Association (NFA) as swap dealers. NGFP, NDPI, and NIplc are generally engaged in Any authors named in this report are research analysts unless otherwise indicated. Industry Specialistsresponsible for the sales and trading effort in the sector for which they have coverage. Industry Speciali Distribution of ratings (Global) The distribution of all ratings published by Nomura Global Equity Research is as follows: 45% have been assigned a Buy rating which, for purposes of mandatory disclosures, are classified as a44% have been assigned a Neutral rating which, for purposes of mandatory disclosures, is classified as11% have been assigned a Reduce rating which, for purposes of mandatory disclosures, are classified Group*. As at 31 March 2014. *The Nomura Group as defined in the Disclaimer section at the end of this report.

24

rwise indicated

arch report accurately reflect our personal views about any or all of the subject securities or issuers y related to the specific recommendations or views expressed in this Research report and (3) no part of ies International, Inc., Nomura International plc or any other Nomura Group company.

aries, and may refer to one or more Nomura Group companies.

Stock rating Previous rating Date of change Sector rating 4 Reduce Neutral 23-Jul-2013 N/A 4 Buy Suspended 15-May-2014 N/A 4 Buy Neutral 12-Dec-2011 N/A 4 Buy Not Rated 15-May-2014 N/A 4 Buy Neutral 15-May-2014 N/A 4 Buy Suspended 15-May-2014 N/A

kitHub, Reuters and ThomsonOne. sclosures/disclosures.aspx or requested from Nomura Securities International, Inc., on 1-877-865-

tors including the firm's total revenues, a portion of which is generated by Investment Banking activities. as research analysts under FINRA/NYSE rules, may not be associated persons of NSI, and may not

panies, public appearances, and trading securities held by a research analyst account.

a International plc. (“NIplc”) are registered with the Commodities Futures Trading Commission and the the trading of swaps and other derivative products, any of which may be the subject of this report.

identified in some Nomura International plc research reports are employees within the Firm who are sts do not contribute in any manner to the content of research reports in which their names appear.

a Buy rating; 42% of companies with this rating are investment banking clients of the Nomura Group*. s a Hold rating; 54% of companies with this rating are investment banking clients of the Nomura Group*. as a Sell rating; 26% of companies with this rating are investment banking clients of the Nomura

Explanation of Nomura's equity research rating system in Europe, Middle East and AfThe rating system is a relative system, indicating expected performance against a specific benchmark idan assessment of the current intrinsic fair value of the stock based on an appropriate valuation methodocash flow analysis, expected return on equity and multiple analysis. Analysts may also indicate expecteprice)/current price. STOCKS A rating of 'Buy', indicates that the analyst expects the stock to outperform the Benchmark over the nexthe Benchmark over the next 12 months. A rating of 'Reduce', indicates that the analyst expects the stothe rating, target price and estimates have been suspended temporarily to comply with applicable regula'No rating' are not in regular research coverage. Investors should not expect continuing or additional inUnited States/Europe/Asia ex-Japan: please see valuation methodologies for explanations of relevanhttp://go.nomuranow.com/research/globalresearchportal/pages/disclosures/disclosures.aspx; Global Emmethodology; Japan: Russell/Nomura Large Cap. SECTORS A 'Bullish' stance, indicates that the analyst expects the sector to outperform the Benchmark during thewith the Benchmark during the next 12 months. A 'Bearish' stance, indicates that the analyst expects thrated' or shown as 'N/A' are not assigned ratings. Benchmarks are as follows: United States: S&P 500ex-Asia. Japan/Asia ex-Japan: Sector ratings are not assigned. Explanation of Nomura's equity research rating system in Japan and Asia ex-Japan pSTOCKS Stock recommendations are based on absolute valuation upside (downside), which is defined as (TargeTarget Price will equal the analyst's 12-month intrinsic valuation of the stock, based on an appropriate vindicates that potential upside is 15% or more. A 'Neutral' recommendation indicates that potential upsidownside is 5% or more. A rating of 'Suspended' indicates that the rating and target price have been scircumstances including when Nomura is acting in an advisory capacity in a merger or strategic transacshown as 'No rating' are not in regular research coverage of the Nomura entity identified in the top bansecurities and/or companies. SECTORS A 'Bullish' rating means most stocks in the sector have (or the weighted average recommendation of thstocks in the sector have (or the weighted average recommendation of the stocks under coverage is) a weighted average recommendation of the stocks under coverage is) a negative absolute recommendati Target Price A Target Price, if discussed, reflects in part the analyst's estimates for the company's earnings. The achother risks related to the company or the market, and may not occur if the company's earnings differ fro

25

frica, US and Latin America, and Japan and Asia ex-Japan from 21 October 2013dentified for each individual stock, subject to limited management discretion. An analyst’s target price is ology determined by the analyst. Valuation methodologies include, but are not limited to, discounted d absolute upside/downside relative to the stated target price, defined as (target price - current

xt 12 months. A rating of 'Neutral', indicates that the analyst expects the stock to perform in line with ock to underperform the Benchmark over the next 12 months. A rating of 'Suspended', indicates that ations and/or firm policies. Securities and/or companies that are labelled as 'Not rated' or shown as formation from Nomura relating to such securities and/or companies. Benchmarks are as follows: t benchmarks for stocks, which can be accessed at: merging Markets (ex-Asia): MSCI Emerging Markets ex-Asia, unless otherwise stated in the valuation

e next 12 months. A 'Neutral' stance, indicates that the analyst expects the sector to perform in line he sector to underperform the Benchmark during the next 12 months. Sectors that are labelled as 'Not 0; Europe: Dow Jones STOXX 600; Global Emerging Markets (ex-Asia): MSCI Emerging Markets

rior to 21 October 2013

et Price - Current Price) / Current Price, subject to limited management discretion. In most cases, the valuation methodology such as discounted cash flow, multiple analysis, etc. A 'Buy' recommendation ide is less than 15% or downside is less than 5%. A 'Reduce' recommendation indicates that potential uspended temporarily to comply with applicable regulations and/or firm policies in certain

ction involving the subject company. Securities and/or companies that are labelled as 'Not rated' or nner. Investors should not expect continuing or additional information from Nomura relating to such

he stocks under coverage is) a positive absolute recommendation. A 'Neutral' rating means most neutral absolute recommendation. A 'Bearish' rating means most stocks in the sector have (or the ion.

hievement of any target price may be impeded by general market and macroeconomic trends, and by m estimates.

Disclaimers This document contains material that has been prepared by the Nomura entity identified at the top or bowhose employees and their respective affiliations are specified on page 1 herein or identified elsewhereaffiliates or subsidiaries and may refer to one or more Nomura Group companies including: Nomura SecInternational, Inc. ('NSI'), New York, US; Nomura International (Hong Kong) Ltd. (‘NIHK’), Hong Kong; Nregistered with the Korea Financial Investment Association ('KOFIA') can be found on the KOFIA Intrane197201440E, regulated by the Monetary Authority of Singapore); Nomura Australia Ltd. (‘NAL’), Australand holder of an Australian financial services licence number 246412; P.T. Nomura Indonesia (‘PTNI’), Taiwan; Nomura Financial Advisory and Securities (India) Private Limited (‘NFASL’), Mumbai, India (ReMumbai- 400 018, India; Tel: +91 22 4037 4037, Fax: +91 22 4037 4111; CIN No : U74140MH2007PTC231299034, MCX: INE261299034) and NIplc, Madrid Branch (‘NIplc, Madrid’). ‘CNS Thailand’ next to aCapital Nomura Securities Public Company Limited (‘CNS’) to provide research assistance services to NTHIS MATERIAL IS: (I) FOR YOUR PRIVATE INFORMATION, AND WE ARE NOT SOLICITING ANY ASOLICITATION OF AN OFFER TO BUY ANY SECURITY IN ANY JURISDICTION WHERE SUCH OFFSOURCES THAT WE CONSIDER RELIABLE, BUT HAS NOT BEEN INDEPENDENTLY VERIFIED BYNomura Group does not warrant or represent that the document is accurate, complete, reliable, fit for anresulting from use of this document and related data. To the maximum extent permissible all warrantiesfor the use, misuse, or distribution of this information. Opinions or estimates expressed are current opinions as of the original publication date appearing on thchange without notice. Nomura Group is under no duty to update this document. Any comments or stateNomura Group. Clients should consider whether any advice or recommendation in this report is suitableNomura Group does not provide tax advice. Nomura Group, and/or its officers, directors and employees, may, to the extent permitted by applicable or sell, the securities, commodities or instruments, or options or other derivative instruments based thermaker or liquidity provider (within the meaning of applicable regulations in the UK) in the financial instrugiven to it by specific laws and regulations of the US or other jurisdictions, this will be separately disclosThis document may contain information obtained from third parties, including ratings from credit ratings prohibited except with the prior written permission of the related third party. Third party content providerratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cexpress or implied warranties, including, but not limited to, any warranties of merchantability or fitness foincidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legtheir content, including ratings. Credit ratings are statements of opinions and are not statements of fact securities or the suitability of securities for investment purposes, and should not be relied on as investmAny MSCI sourced information in this document is the exclusive property of MSCI Inc. (‘MSCI’). Withoutreproduced, re-disseminated or used to create any financial products, including any indices. This informinformation. MSCI, its affiliates and any third party involved in, or related to, computing or compiling the merchantability or fitness for a particular purpose with respect to any of this information. Without limitingrelated to, computing or compiling the information have any liability for any damages of any kind. MSCI Russell/Nomura Japan Equity Indexes are protected by certain intellectual property rights of Nomura Senot guarantee the accuracy, completeness, reliability, or usefulness thereof and do not account for busiInvestors should consider this document as only a single factor in making their investment decision andmay be associated with any investment decision. Nomura Group produces a number of different types otrading ideas; recommendations contained in one type of research product may differ from recommendamethodologies or otherwise. Nomura Group publishes research product in a number of different ways ingroups of clients may receive different products and services from the research department depending Ideas platform (Retina) at http://go.nomuranow.com/equities/tradingideas/retina/ Figures presented herein may refer to past performance or simulations based on past performance whicfuture performance, such forecasts may not be a reliable indicator of future performance. Moreover, simfuture distribution of returns.

26

ottom of page 1 herein, if any, and/or, with the sole or joint contributions of one or more Nomura entities e in the document. The term "Nomura Group" used herein refers to Nomura Holdings, Inc. or any of its curities Co., Ltd. ('NSC') Tokyo, Japan; Nomura International plc ('NIplc'), UK; Nomura Securities

Nomura Financial Investment (Korea) Co., Ltd. (‘NFIK’), Korea (Information on Nomura analysts et at http://dis.kofia.or.kr); Nomura Singapore Ltd. (‘NSL’), Singapore (Registration number ia (ABN 48 003 032 513), regulated by the Australian Securities and Investment Commission ('ASIC') Indonesia; Nomura Securities Malaysia Sdn. Bhd. (‘NSM’), Malaysia; NIHK, Taipei Branch (‘NITB’),

egistered Address: Ceejay House, Level 11, Plot F, Shivsagar Estate, Dr. Annie Besant Road, Worli, C169116, SEBI Registration No: BSE INB011299030, NSE INB231299034, INF231299034, INE n analyst’s name on the front page of a research report indicates that the analyst is employed by NSL under a Research Assistance Agreement. CNS is not a Nomura entity. ACTION BASED UPON IT; (II) NOT TO BE CONSTRUED AS AN OFFER TO SELL OR A FER OR SOLICITATION WOULD BE ILLEGAL; AND (III) BASED UPON INFORMATION FROM Y NOMURA GROUP. ny particular purpose or merchantable and does not accept liability for any act (or decision not to act) and other assurances by Nomura group are hereby excluded and Nomura Group shall have no liability

his material and the information, including the opinions and estimates contained herein, are subject to ements made herein are those of the author(s) and may differ from views held by other parties within e for their particular circumstances and, if appropriate, seek professional advice, including tax advice.

law and/or regulation, deal as principal, agent, or otherwise, or have long or short positions in, or buy reon, of issuers or securities mentioned herein. Nomura Group companies may also act as market ments of the issuer. Where the activity of market maker is carried out in accordance with the definition

sed within the specific issuer disclosures. agencies such as Standard & Poor’s. Reproduction and distribution of third party content in any form is

rs do not guarantee the accuracy, completeness, timeliness or availability of any information, including cause, or for the results obtained from the use of such content. Third party content providers give no or a particular purpose or use. Third party content providers shall not be liable for any direct, indirect, al fees, or losses (including lost income or profits and opportunity costs) in connection with any use of or recommendations to purchase hold or sell securities. They do not address the suitability of

ment advice. t prior written permission of MSCI, this information and any other MSCI intellectual property may not be

mation is provided on an "as is" basis. The user assumes the entire risk of any use made of this information hereby expressly disclaim all warranties of originality, accuracy, completeness,

g any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in, or and the MSCI indexes are services marks of MSCI and its affiliates.

ecurities Co., Ltd. and Russell Investments. Nomura Securities Co., Ltd. and Russell Investments do ness activities and services that any index user and its affiliates undertake with the use of the Indexes. , as such, the report should not be viewed as identifying or suggesting all risks, direct or indirect, that of research product including, among others, fundamental analysis, quantitative analysis and short term ations contained in other types of research product, whether as a result of differing time horizons, ncluding the posting of product on Nomura Group portals and/or distribution directly to clients. Different on their individual requirements. Clients outside of the US may access the Nomura Research Trading

ch are not reliable indicators of future performance. Where the information contains an indication of mulations are based on models and simplifying assumptions which may oversimplify and not reflect the

Certain securities are subject to fluctuations in exchange rates that could have an adverse effect on theThe securities described herein may not have been registered under the US Securities Act of 1933 (thebeen registered under the 1933 Act, or except in compliance with an exemption from the registration reqexecuted via a Nomura entity in your home jurisdiction. This document has been approved for distribution in the UK and European Economic Area as investmeFinancial Conduct Authority and the Prudential Regulation Authority. NIplc is a member of the London Sapplicable regulations in the UK, or take into account the particular investment objectives, financial situacounterparties' or 'professional clients' for the purposes of applicable regulations in the UK, and may nobeen approved by NIHK, which is regulated by the Hong Kong Securities and Futures Commission, for NAL, which is authorized and regulated in Australia by the ASIC. This document has also been approveaccepts legal responsibility for the content of this document, where it concerns securities, futures and foor institutional investors as defined by the Securities and Futures Act (Chapter 289). Recipients of this ddocument. Unless prohibited by the provisions of Regulation S of the 1933 Act, this material is distributeaccordance with the provisions of Rule 15a-6, under the US Securities Exchange Act of 1934. The entitmake copies of such documents available to their clients. This document has not been approved for distribution to persons other than ‘Authorised Persons’, ‘ExemArabia (‘Saudi Arabia’) or 'professional clients' (as defined by the Dubai Financial Services Authority) in the Qatar Financial Centre Regulatory Authority) in the State of Qatar (‘Qatar’) by Nomura Saudi Arabiacopy thereof may be taken or transmitted or distributed, directly or indirectly, by any person other than t‘Authorised Persons’, ‘Exempt Persons’ or ‘Institutions’ located in Saudi Arabia or 'professional clients' idocument, you represent that you are not located in Saudi Arabia or that you are an ‘Authorised Personor a ‘Market Counterparty’ or ‘Business Customers’ in Qatar and agree to comply with these restrictionsArabia or Qatar. NO PART OF THIS MATERIAL MAY BE (I) COPIED, PHOTOCOPIED, OR DUPLICATED IN ANY FORMEMBER OF NOMURA GROUP. If this document has been distributed by electronic transmission, succould be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sendemay arise as a result of electronic transmission. If verification is required, please request a hard-copy ve Nomura Group manages conflicts with respect to the production of research through its compliance poliConfidentiality policies) as well as through the maintenance of Chinese walls and employee training. Additional information is available upon request and disclosure information is available at the Nhttp://go.nomuranow.com/research/globalresearchportal/pages/disclosures/disclosures.aspx Copyright © 2014 Nomura International (Hong Kong) Ltd. All rights reserved.

27

value or price of, or income derived from, the investment. ‘1933 Act’), and, in such case, may not be offered or sold in the US or to US persons unless they have quirements of the 1933 Act. Unless governing law permits otherwise, any transaction should be

nt research by NIplc. NIplc is authorised by the Prudential Regulation Authority and regulated by the Stock Exchange. This document does not constitute a personal recommendation within the meaning of ations, or needs of individual investors. This document is intended only for investors who are 'eligible ot, therefore, be redistributed to persons who are 'retail clients' for such purposes. This document has distribution in Hong Kong by NIHK. This document has been approved for distribution in Australia by

ed for distribution in Malaysia by NSM. In Singapore, this document has been distributed by NSL. NSL oreign exchange, issued by their foreign affiliates in respect of recipients who are not accredited, expert document in Singapore should contact NSL in respect of matters arising from, or in connection with, this ed in the US, by NSI, a US-registered broker-dealer, which accepts responsibility for its contents in ty that prepared this document permits its separately operated affiliates within the Nomura Group to

mpt Persons’ or ‘Institutions’ (as defined by the Capital Markets Authority) in the Kingdom of Saudi the United Arab Emirates (‘UAE’) or a ‘Market Counterparty’ or ‘Business Customers’ (as defined by

a, NIplc or any other member of Nomura Group, as the case may be. Neither this document nor any hose authorised to do so into Saudi Arabia or in the UAE or in Qatar or to any person other than n the UAE or a ‘Market Counterparty’ or ‘Business Customers’ in Qatar . By accepting to receive this

n’, an ‘Exempt Person’ or an ‘Institution’ in Saudi Arabia or that you are a 'professional client' in the UAE s. Any failure to comply with these restrictions may constitute a violation of the laws of the UAE or Saudi

RM, BY ANY MEANS; OR (II) REDISTRIBUTED WITHOUT THE PRIOR WRITTEN CONSENT OF A h as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information

er therefore does not accept liability for any errors or omissions in the contents of this document, which ersion.

icies and procedures (including, but not limited to, Conflicts of Interest, Chinese Wall and

omura Disclosure web page: