Embed Size (px)

Citation preview

168

CHAPTER V

DATA ANALYSIS AND INTERPRETATION OF THE STUDY

5.1. Introduction

5.2. Scope of Analysis

5.3. Profile Analysis

5.3.1. Employee's position

5.3.2. Gender

5.3.3. Educational Qualification

5.4. Universal Analysis

5.4.1. A comparative study between the actual score and expected score

regarding components qualitative characteristics of financial reporting

in Indian banks.

5.4.2. A comparative study between the public and private sector banks

regarding components qualitative characteristics of financial reporting

information.

5.4.3. A comparative study between the public and private sector banks

regarding the compliance with RBI prudential norms.

5.4.4. A comparative study between the public and private sector banks

regarding the compliance with accounting standards.

5.5. Multiple Regression Analysis

5.5.1. Impact of RBI prudential norms on qualitative characteristics of

financial reporting information in Indian banks.

5.5.2. Impact of Accounting Standards on qualitative characteristics of

financial reporting information in Indian banks.

5.6. Conclusive Analysis

5.6.1. A comparative study between the actual score and expected score

regarding the qualitative characteristics of financial reporting in Indian

banks.

5.6.2. A comparative study between the public and private sector banks

regarding the qualitative characteristics of financial reporting

information.

5.7. Conclusive Universal Analysis

5.7.1. Actual score and expected score for the quality of financial reporting

information in Indian banks.

5.7.2. Quality of financial reporting information between public and private

sector banks in Indian

5.8. Conclusive Regression Analysis

5.8.1. Impact of the RBI prudential norms on quality of financial reporting

information in banks.

5.8.2. Impact of Accounting Standards on quality of financial reporting

information in banks

5.9. Conclusion

169

CHAPTER V

DATA ANALYSIS AND INTERPRETATION OF THE STUDY

5.1. Introduction

The present research investigates the qualitative characteristics of financial

reporting information system in Indian banking industry, a comparative study of public

and private sector banks. This chapter attempts to analyze and interpret the data

intended to determine and measure the quality of financial reporting information based

on the perceptions of top managers, senior managers and accountants. The survey helps

to: (i) identify gaps between the actual score and expected score regarding the quality of

financial reporting information by Indian banks; (ii) identify the difference between the

public sector banks and private sector banks regarding the quality of financial reporting

information; (iii) examine the impact of RBI prudential norms on quality of financial

reporting information in banks and (iv) examine the impact of Accounting Standards on

quality of financial reporting information in banks.

5.2. Scope of Analysis

The primary data required for the present study were collected from top managers,

senior managers and accountants in the public and private sector banks. Structured

questionnaire was developed for collecting the data from the sample respondents on

their perceptions about the qualitative characteristics of financial reporting information,

RBI prudential norms, and Accounting Standards related to financial reporting

information by banks.

The scope of analysis of the empirical research included profile analysis,

universal analysis, multiple regression analysis, and conclusive analysis with regard to

qualitative characteristics, RBI prudential norms, and Accounting Standards of financial

170

reporting information in banks. The analysis and interpretation of data covering the

above dimensions have been presented below.

5.3. Profile Analysis

Profile analysis covers three variables viz. employee's position; gender and

educational qualification.

5.3.1. Employee's position

The employee working position in the banks plays very important role in

enhancing or decrease the quality of financial reporting information. The primary data

required for the present study were collected from top managers, senior managers, and

accountants in the public and private sector banks, because this group of employee more

than related and within reach of financial information. Table 5.1 and Chart 5.1 present

the status of the sample respondents numbering 465.

Table No.5.1

Classification-Based on Position

Position Sector Banks

Total Public Private

Top Manager Nos. 94 22 116

Per cent 25% 24% 25%

Senior Manager Nos. 93 22 115

Per cent 25% 24% 25%

Second manager or Accountant

Nos. 188 46 234

Per cent 50% 52% 50%

Total Nos. 375 90 465

Per cent 100 100 100

Source: Filed Survey

171

Chart No.5.1

Response Rate of Employee's Position

Majority of the respondents were of public sector banks and the sample

respondents numbering 375 and representing 80% of total sample respondents. The first

group of the respondents included 94 top level managers which encompasses 25% of

the total sample respondents of public sector banks. Next in the respondents were 93

senior managers and comprises 25% while the third respondents were second level 188

managers or accountants which cover 50% of the total number of respondents from

public sector banks.

In this study 90 respondents were from the private sector banks, representing 20

% of total sample respondents. The first group of the respondents was 22 top managers

representing 24% of the total number of respondents of private sector banks. The

second group of the respondents included 22 senior managers representing 24% and the

third group of the respondents comprises 46 second managers or accountants

representing 52% of the total number of respondents of private sector banks.

Top managwer

25%

Senior Manager

25%

Second manager or Accountant

50%

172

5.3.2. Gender

Table 5.2 and Chart 5.2 present the gender status of the sample respondents by

classifying than on the basis of gender.

Table No.5.2

Classification-Based on Gender

Gender Public Sector Banks Private Sector Banks

Total Top Manager

Senior Manager

Second manager

Top Manager

Senior Manager

Second manager

Male Nos. 84 85 161 15 17 33 395

Per cent

89% 91% 86% 68% 77% 72% 85%

Female Nos. 10 8 27 7 5 13 70

Per cent

11% 9% 14% 32% 23% 28% 15%

Total Nos. 94 93 188 22 22 46 465

Per cent

100% 100% 100% 100% 100% 100% 100%

Source: Filed Survey

Chart No.5.2

Response Rate of Gender

Majority of the respondents were males including 395 representing 85% of the

total sample as against 70 female representing 15%. Among male bankers, in the public

sector banks the percent of top managers, senior managers and accountants stood at

89%, 91% and 86% respectively, while in the private sector banks the percent of top

managers, senior managers and accountants stood at 68%, 77% and 72% respectively.

Male 85%

Female15%

173

Amid female, in the public sector banks the percent of top managers, senior

managers and accountants stood at 11%, 9% and 14% respectively, while in the private

sector banks the percent of top managers, senior managers and accountants stood at

32%, 23% and 28% respectively.

5.3.3. Educational Qualification

Education is one of main factors to help the employee for better understanding of

the situation and decision making. Level of the education can change the employee’s

attitudes, efficiency and supple in the working environment. It leads to update, learning

and adjusts in the changing of the technology and the prudential norms based banking

sector. Table 5.3 and Chart 5.3 highlight the grouping of respondents based on

educational qualification.

Table No.5.3

Classification- Based on Education

Gender Public Sector Banks Private Sector Banks

Total Top Manager

Senior Manager

Second manager

Top Manager

Senior Manager

Second manager

Bachelor Nos. 44 47 101 2 4 16 231

Per cent 47% 51% 53% 9% 18% 35% 50%

Master Nos. 21 19 35 8 9 14 92

Per cent 22% 21% 18% 36% 41% 30% 20%

Professional Nos. 25 19 40 9 7 12 110

Per cent 27% 21% 21% 41% 32% 26% 23%

Other Nos. 4 7 13 3 2 4 32

Per cent 4% 7% 8% 14% 9% 9% 7%

Total Nos. 94 92 189 22 22 46 465

Per cent 100% 100% 100% 100% 100% 100% 100%

Source: Filed Survey

174

Chart No.5.3

Response Rate of Educational Qualification

Majority of the respondents were bachelor's degree holders and their number

stood at 231 representing 50% as against professionals numbering 110 and representing

23%, master's degree holders numbered 92 and represented 20 % while others

numbered 32 and represented 7%. Among bachelors, in the public sector banks the

percent of top managers, senior managers and accountants stood at 47%, 51% and 53%

respectively, while in the private sector banks the percent of top managers, senior

managers and accountants stood at 9%, 18% and 35% respectively.

Amidst professionals, in the public sector banks the percent of top managers,

senior managers and accountants stood at 27%, 21% and 21% respectively, while in the

private sector banks the percent of top managers, senior managers and accountants

stood at 41%, 32% and 26% respectively. Among the masters, in the public sector

banks the percent of top managers, senior managers and accountants stood at 22%, 21%

and 18% respectively, while in the private sector banks the percent of top managers,

senior managers and accountants stood at 36%, 41% and 30% respectively.

Bachelor50%

Master20%

Professional23%

Other7%

175

Amid others, in the public sector banks the percent of top managers, senior

manager and accountants stood at 4%, 7% and 8% respectively, while in the private

sector banks the percent of top managers, senior managers and accountants stood at

14%, 9% and 9% respectively.

5.4. Universal Analysis

The universal analysis encompasses the perceptions of all the sample respondents

about; gap between the actual score and the expected score regarding the component of

qualitative characteristics of financial reporting in banks and difference between the

public sector banks and private sector banks regarding the component of qualitative

characteristics of financial reporting.

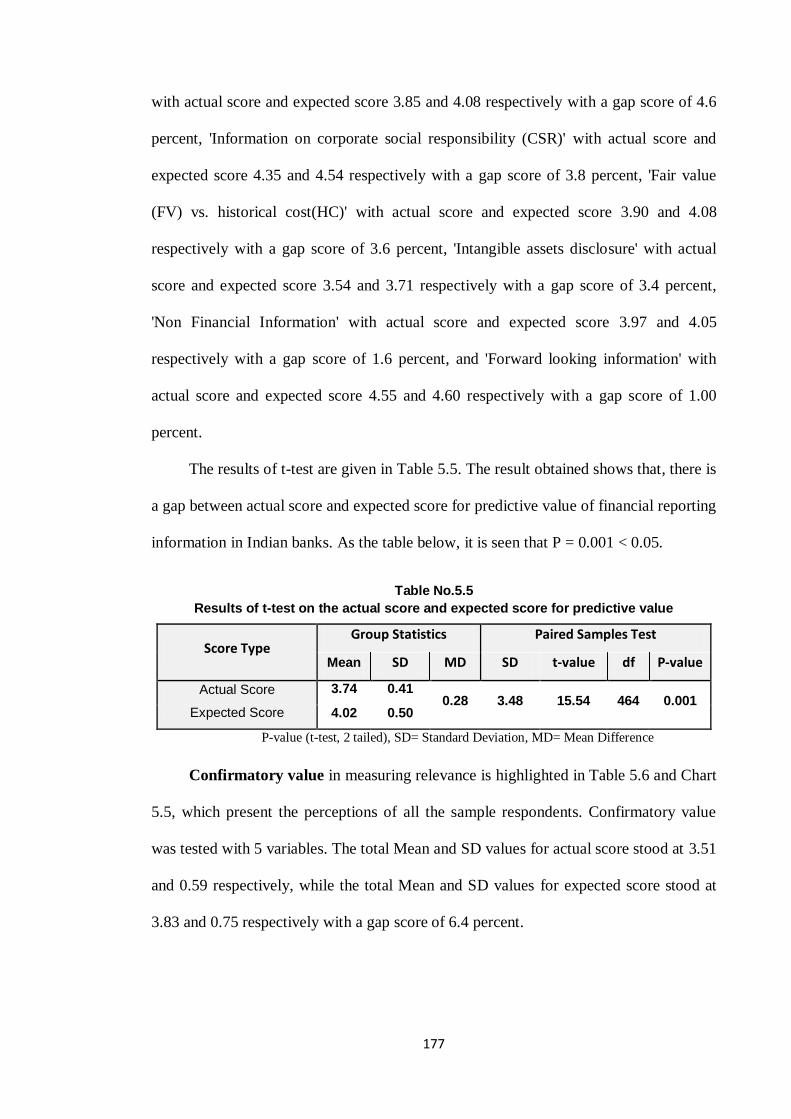

5.4.1. A Comparative Study between the Actual Score and Expected Score

Regarding the Components of Qualitative Characteristics of Financial

Reporting Information in Indian Banks.

Relevance is one of the two fundamental qualitative characteristic of financial

reporting information. Relevance was analyzed with two components: predictive value -

containing 9, and confirmatory value- containing 5 variables.

Predictive value in measuring relevance is highlighted in Table 5.4 and Chart

5.4, which presents the perceptions of all the sample respondents. Predictive value was

tested with 9 variables. The total Mean and SD values for actual score stood at 3.74 and

0.41 respectively, the total Mean and SD values expected Score stood at 4.02 and 0.50

respectively with a gap score of 5.6 percent.

176

Table No.5.4

Actual score and expected score for Predictive value of financial reporting information

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Predictive value 3.74 0.41 74.8 4.02 0.5 80.4 0.28 5.6

Estimate of profits and losses 3.45 0.582 69.0 3.78 0.692 75.6 0.33 6.6

Non Financial Information 3.97 0.556 79.4 4.05 0.617 81.0 0.08 1.6

Forward looking information 4.55 0.604 91.0 4.6 0.576 92.0 0.05 1.0

Information on corporate social responsibility

4.35 0.801 87.0 4.54 0.71 90.8 0.19 3.8

Analysis of cash flow 3.85 0.936 77.0 4.08 0.987 81.6 0.23 4.6

Intangible assets disclosure 3.54 0.727 70.8 3.71 0.877 74.2 0.17 3.4

Off balance activities disclosure 2.85 1.155 57.0 3.69 1.371 73.8 0.84 16.8

Information concerning going concern

3.2 0.801 64.0 3.65 0.66 73.0 0.45 9.0

Fair value (FV) vs. historical cost(HC)

3.9 0.700 78.0 4.08 0.638 81.6 0.18 3.6

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Based on the Mean and Standard Deviation, regarding mean value of actual score

and expected score of predictive value, a mean value of actual score and expected score

of ‘off balance’ activities disclosure' stood at 2.85 and 3.96 respectively with a

maximum gap score of 16.8 percent, and it was followed by the 'Information concerning

going concern' with actual score and expected score 3.20 and 3.65 respectively with a

gap score of 9 percent, 'Estimate of profits and losses' with actual score and expected

score 3.45 and 3.78 respectively with a gap score of 6.6 percent, 'Analysis of cash flow'

74.880.4

5.6

0

20

40

60

80

100

Predictive value

Chart No.5.4 Actual score and expected score for predictive

value of financial reporting information

Actual score Expected score Gap

177

with actual score and expected score 3.85 and 4.08 respectively with a gap score of 4.6

percent, 'Information on corporate social responsibility (CSR)' with actual score and

expected score 4.35 and 4.54 respectively with a gap score of 3.8 percent, 'Fair value

(FV) vs. historical cost(HC)' with actual score and expected score 3.90 and 4.08

respectively with a gap score of 3.6 percent, 'Intangible assets disclosure' with actual

score and expected score 3.54 and 3.71 respectively with a gap score of 3.4 percent,

'Non Financial Information' with actual score and expected score 3.97 and 4.05

respectively with a gap score of 1.6 percent, and 'Forward looking information' with

actual score and expected score 4.55 and 4.60 respectively with a gap score of 1.00

percent.

The results of t-test are given in Table 5.5. The result obtained shows that, there is

a gap between actual score and expected score for predictive value of financial reporting

information in Indian banks. As the table below, it is seen that P = 0.001 < 0.05.

Table No.5.5

Results of t-test on the actual score and expected score for predictive value

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value

Actual Score

Expected Score

3.74 0.41 0.28 3.48 15.54 464 0.001

4.02 0.50

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean Difference

Confirmatory value in measuring relevance is highlighted in Table 5.6 and Chart

5.5, which present the perceptions of all the sample respondents. Confirmatory value

was tested with 5 variables. The total Mean and SD values for actual score stood at 3.51

and 0.59 respectively, while the total Mean and SD values for expected score stood at

3.83 and 0.75 respectively with a gap score of 6.4 percent.

178

Table No.5.6

Actual score and expected score for confirmatory value of financial reporting information

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Confirmatory value 3.51 0.59 70.2 3.83 0.75 76.6 0.32 6.4

Information from supervisory board

3.53 0.666 70.6 3.71 0.667 74.2 0.18 3.6

Information regarding personal policies

3.44 0.752 68.8 3.59 0.758 71.8 0.15 3.0

Information concerning divisions 3.45 1.317 69.0 3.73 1.337 74.6 0.28 5.6

Financial structure disclosed 3.12 0.922 62.4 3.76 0.773 75.2 0.64 12.8

Interim financial reports published

4.03 0.606 80.6 4.38 0.681 87.6 0.35 7.0

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Based on the Mean and Standard Deviation value, regarding mean value of

actual score and expected score of confirmatory value, the mean value of actual score

and expected score of 'financial structure disclosed' stood at 3.12 and 3.76 respectively

with a maximum gap score of 12.8 percent, and it was followed by the 'interim financial

reports published' with actual score and expected score 4.03 and 4.38 respectively with

a gap score of 7.00 percent, 'information concerning divisions' with actual score and

expected score 3.45 and 3.73 respectively with a gap score of 5.6 percent, 'information

from supervisory board' with actual score and expected score 3.53 and 3.71 respectively

70.276.6

6.4

0

20

40

60

80

100

Confirmatory value

Chart No.5.5 Actual score and expected score for confirmatory value of

financial reporting information in banks

Actual score Expected score Gap

179

with a gap score of 3.6 percent, and 'information regarding personal policies' with actual

score and expected score 3.44 and 3.59 respectively with a gap score of 3.00 percent.

The results of t-test are given in Table 5.7.The results show that there is a

statistically significant gap between the actual score and expected score for the

confirmatory value of financial reporting in Indian banks. As the table below, it is seen

that P = 0.001 < 0.05.

Table No.5.7

Results of t-test on the actual score and expected score for confirmatory value

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value Actual Score

Expected Score

3.51 0.59 0.32 0.39 17.79 464 0.001

3.83 0.74

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean Difference

Faithful Representation (Reliability) is one of the two fundamental qualitative

characteristic of financial reporting information. Reliability was analyzed with four

components: completeness - containing 2, neutrality- containing 2, free from material

error- containing 2 and verifiability - containing 2 variables.

Completeness in measuring reliability is highlighted in Table 5.8 and Chart 5.6,

which present the perceptions of all the sample respondents. Completeness was tested

with 2 variables. The total Mean and SD values for actual score stood at 4.13 and 0.49

respectively, while the total Mean and SD values expected score stood at 4.24 and 0.45

respectively with a gap score of 2.2 percent.

Table No.5.8

Actual score and expected score for completeness of financial reporting information

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Completeness 4.13 0.49 82.6 4.24 0.45 84.8 0.11 2.2

Description corporate governance 4.43 0.69 88.6 4.55 0.60 91.0 0.12 2.4

Contingencies disclosure 3.83 0.93 76.6 3.94 0.91 78.8 0.11 2.2

180

Based on the Mean and Standard Deviation value, regarding mean value of actual

score and expected score for completeness, a mean value of actual score and expected

score of 'description corporate governance’ stood at 4.43 and 4.55 respectively with a

maximum gap score of 2.4 percent, and it was followed by the ‘contingencies

disclosure’ with actual score and expected score 3.83 and 3.94 respectively with a gap

score of 2.2 percent.

The results of t-test are given in Table 5.9. The results show that there is a

statistically significant gap between the actual score and expected score for

completeness of financial reporting in Indian banks. As the table below, it is seen that P

= 0.001 < 0.05.

Table No.5.9

Result of t-test on the actual score and expected score for completeness

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value Actual Score

Expected Score

4.13 0.49 0.11 0.57 4.26 464 0.001

4.24 0.45

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean Difference

Neutrality in measuring reliability is highlighted in Table 5.10 and Chart 5.7,

which present the perceptions of all the sample respondents. Neutrality was tested with

2 variables. The total Mean and SD values for actual score stood at 3.54 and 0.68

82.6 84.8

2.20

20

40

60

80

100

Completeness

Chart No.5.6 Actual score and expected score for completeness of

financial reporting information in banks

Actual score Expected score Gap

181

respectively, while the total Mean and SD values for expected score stood at 3.92 and

0.82 respectively with a gap score of 7.6 per cent.

Table No.5.10

Actual score and expected score for neutrality of financial reporting information

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Based on the Mean and Standard Deviation value, regarding mean value of actual

score and expected score for neutrality, a mean value of the actual score and expected

score of 'information concerning bonuses’ stood at 3.32 and 3.77 respectively with a

maximum gap score of 9.00 percent, and it was followed by the 'Comply or explain

disclosure' with the actual score and expected score 3.76 and 4.07 respectively with a

gap score of 6.2 percent.

The results of t-test are given in Table 5.11. The results show that there is a

statistically significant gap between the actual score and expected score for the

neutrality of financial reporting in banks. As the table below, it is seen that P = 0.001 <

0.05.

70.878.4

7.6

0

10

20

30

40

50

60

70

80

90

Neutrality

Chart No.5.7 Actual score and expected score for

Neutrality of financial reporting information

Actual score Expected score Gap

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Neutrality 3.54 0.68 70.8 3.92 0.82 78.4 0.38 7.6

"Comply or explain" disclosure 3.76 0.98 75.2 4.07 0.96 81.4 0.31 6.2

Information concerning bonuses 3.32 0.68 66.4 3.77 0.78 75.4 0.45 9.0

182

Table No.5.11

Result of t-test on the actual score and expected score for neutrality

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value Actual Score

Expected Score

3.54 0.68 0.38 0.72 11.28 464 0.001

3.92 0.82

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean Difference

Free from material error in measuring reliability is highlighted in Table 5.12

and Chart 5.8, which present the perceptions of all the sample respondents. Free from

material was tested with 2 variables. The total Mean and SD values for actual score

stood at 3.92 and 0.40 respectively, while the total Mean and SD values for expected

score stood at 3.97 and 0.41 respectively with a gap score of 1.00 percent.

Table No.5.12

Actual and expected score for free from material error of financial reporting information

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Based on the Mean and Standard Deviation value, regarding mean value of actual

score and expected score for free from material error, the Mean value of actual score

and expected score of ‘descriptions auditor's report’ stood at 4.21 and 4.31 respectively

78.4 79.4

10

20

40

60

80

100

Free from material error

Chart No.5.8 Actual score and expected score for free from

material error of financial reporting information in Indian banks

Actual score Expected score Gap

Qualitative characteristics of financial reporting

information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Free from material error 3.92 0.4 78.4 3.97 0.41 79.4 0.05 1.0

Descriptions auditor's report 4.21 0.644 84.2 4.31 0.68 86.2 0.1 2.0

Type of auditor’s report 3.63 0.663 72.6 3.64 0.669 72.8 0.01 0.2

183

with a maximum gap score of 2.00 percent, and it was followed by the ‘type of auditor’s

report’ with the same actual and expected score 3.63, 3.64 and without a gap score.

The results of t-test are given in Table 5.13. The results show that there is a

statistically significant gap between the actual score and expected score for free from

material error of financial reporting in Indian banks. As the table below, it is seen that

P= 0.001 < 0.05.

Table No.5.13

Results of t-test actual score and expected score for free from material error

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value Actual Score

Expected Score

3.92 0.40 0.05 0.22 5.14 464 0.001

3.97 0.41

P-value (t-test, two tailed), SD= Standard Deviation, MD= Mean Difference

Verifiability in measuring reliability is highlighted in Table 5.14 and Chart 5.9,

which present the perceptions of all the sample respondents. Verifiability was tested

with 2 variables. The total Mean and SD values for actual score stood at 3.85 and 0.61

respectively, while the total Mean and SD values for expected score stood at 4.19 and

0.67 respectively with a gap score of 6.8 percent.

Table No.5.14

Actual score and expected score for verifiability of financial reporting information

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Verifiability 3.85 0.61 77.0 4.19 0.67 83.8 0.34 6.8

Valid argument estimates in annual report

3.83 0.91 76.6 4.01 0.95 80.2 0.18 3.6

Valid argument for choice accounting principles

3.87 0.48 77.4 4.35 0.51 87.0 0.48 9.6

184

Based on the Mean and Standard Deviation value, regarding mean value of actual

score and expected score of verifiability, a mean value of actual score and expected

score of ‘valid argument for choice accounting principles’ stood at 3.87 and 4.35

respectively with a maximum gap score of 9.6 percent, and it was followed by the

‘Valid argument estimates in annual report’ with actual score and expected score 3.83

and 4.01 respectively with a gap score of 3.6 percent.

The results of t-test are given in Table 5.15. The results show that there is a

statistically significant gap between the actual score and expected score for verifiability

of financial reporting in Indian banks. As the table below, it is seen that P = 0.001 <

0.05.

Table No.5.15

Results of t-test the actual score and expected score for verifiability

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value Actual Score

Expected Score

3.85 0.61 0.34 0.58 12.3 464 0.001

4.19 0.67

P-value (t-test, two tailed), SD= Standard Deviation, MD= Mean Difference

Understandability is highlighted in Table 5.16 and Chart 5.10, which present the

perceptions of all the sample respondents. Understandability was tested with 7

variables. The total Mean and SD values for actual score stood at 3.81 and 0.32

7783.8

6.8

0

20

40

60

80

100

Verifiability

Chart No.5.9 Actual score and expected score for 'Verifiability' of

financial reporting information in Indian banks

Actual score Expected score Gap

185

respectively, while the total Mean and SD values for expected score stood at 4.1 and

0.35 respectively with a gap score of 5.8 percent.

Table No.5.16

Actual score and expected score for understandability of financial reporting information

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Understandability 3.81 0.318 76.2 4.1 0.351 82 0.29 5.8

Manner of organized annual report

4.66 0.684 93.2 4.78 0.574 95.6 0.12 2.4

The extent presented of graphs and tables

2.92 0.756 58.4 3.39 0.764 67.8 0.47 9.4

The extent of jargon in annual report

4.08 0.933 81.6 4.23 0.884 84.6 0.15 3.0

The size of the glossary 2.8 1.402 56.0 3.41 1.512 68.2 0.61 12.2

Information concerning mission and strategy

4.3 0.669 86.0 4.36 0.559 87.2 0.06 1.2

Annual report understandable 4.3 0.724 86.0 4.42 0.625 88.4 0.12 2.4

Classifications financial statement's elements

3.64 0.853 72.8 3.98 0.89 79.6 0.34 6.8

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Based on the Mean and Standard Deviation value, regarding mean value of actual

score and expected score of understandability a mean value of actual score and expected

score of ‘the size of the glossary’ stood at 2.80 and 3.41 respectively with a maximum

gap score of 12.2 percent, and it was followed by the ‘extent presented of graphs and

tables’ with actual score and expected score 2.92 and 3.39 respectively with a gap score

of 9.4 percent, 'classifications financial statement’s elements' with actual score and

76.2 82

5.8

0

20

40

60

80

100

Understandability

Chart No.5.10 Actual score and expected score for Understandability of

financial reporting information in Indian banks

Actual score Expected score Gap

186

expected score 3.64 and 3.98 respectively with a gap score of 6.8 percent, 'extent of

jargon in annual report' with actual score and expected score 4.08 and 4.23 respectively

with a gap score of 3 percent, 'manner of organized annual report' with actual score and

expected score 4.66 and 4.78 respectively with a gap score of 2.4 percent, 'annual report

understandable' with actual score and expected score 4.30 and 4.42 respectively with a

gap score of 2.4 percent, and 'information concerning mission and strategy' with actual

score and expected score 4.30 and 4.36 respectively with a gap score of 1.2 percent.

The results of t-test are given in Table 5.17. The results show that there is a

statistically significant gap between the actual score and expected score for the

understandability of financial reporting in Indian banks. As the table below, it is seen

that P= 0.001 < 0.05.

Table No.5.17

Result of t-test on the actual score and expected score for understandability

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value Actual Score

Expected Score

3.81 0.32 0.27 0.25 22.79 464 0.001

4.08 0.35

P-value (t-test, two tailed), SD= Standard Deviation, MD= Mean Difference

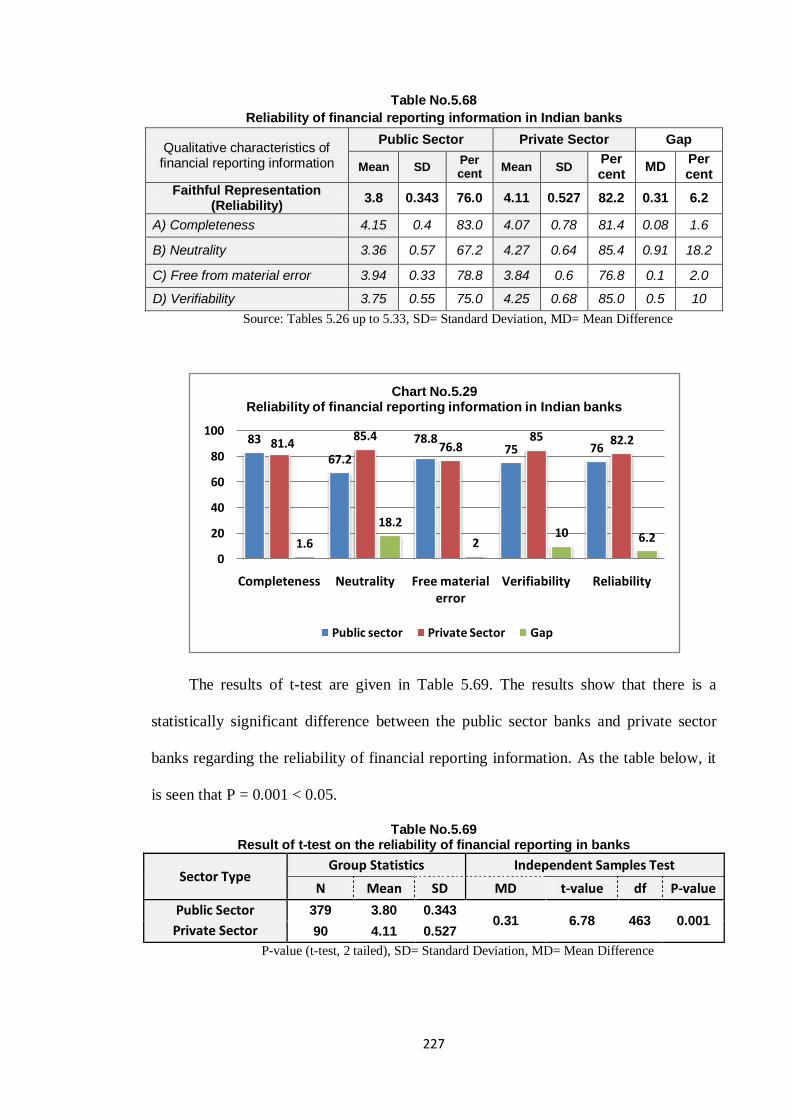

Comparability refers to the quality of information that enables users to identify

similarities in and differences between two set of economic phenomena. Comparability

was analyzed with two components: consistency- containing 5, and comparable -

containing 2 variables.

Consistency in measuring comparability is highlighted in Table 5.18 and Chart

5.11, which present the perceptions of all the sample respondents. Consistency was

tested with 5 variables. The total Mean and SD values for the actual score stood at 3.23

and 0.44 respectively, while the total Mean and SD values for expected score stood at

3.65 and 0.53 respectively with a gap score of 8.4 percent.

187

Table No.5.18

Actual score and expected score for consistency of financial reporting information

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Consistency 3.23 0.44 64.6 3.65 0.53 73.0 0.42 8.4

Changes in accounting policies disclosure

3.31 0.669 66.2 3.73 0.623 74.6 0.42 8.4

Changes in accounting estimates disclosure

3.51 0.673 70.2 3.57 0.745 71.4 0.06 1.2

Effects of accounting policy changes

2.66 0.698 53.2 3.58 0.85 71.6 0.92 18.4

Information concerning companies’ shares

3.05 0.469 61.0 3.31 0.724 66.2 0.26 5.2

Benchmark information 3.6 0.882 72.0 4.08 1.036 81.6 0.48 9.6

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Based on the Mean and Standard Deviation value, regarding mean value of the

actual score and expected score for consistency a mean value of actual score and

expected score of ‘effects of accounting policy changes’ stood at 2.66 and 3.58

respectively with a maximum gap score of 18.4 percent, and it was followed by the

‘benchmark information’ with actual score and expected score 3.60 and 4.08

respectively with a gap score of 9.6 percent, 'changes in accounting policies disclosure'

with actual score and expected score 3.31 and 3.73 respectively with a gap score of 8.4

percent, 'information concerning companies’ shares' with actual score and expected

64.673

8.4

0

10

20

30

40

50

60

70

80

Consistency

Chart No.5.11 Actual score and expected score

for 'Consistency' of financial reporting information in Indian banks

Actual score Expected score Gap

188

score 3.05 and 3.31 respectively with a gap score of 5.2 percent, and 'changes in

accounting estimates disclosure' with actual score and expected score 3.51 and 3.57

respectively with a gap score of 1.2 percent.

The results of t-test are given in Table 5.19. The results show that there is a

statistically significant gap between the actual score and expected score for consistency

of financial reporting in Indian banks. As the table below, it is seen that P = 0.001 <

0.05.

Table No.5.19 Result of t-test on the actual score and expected score for consistency

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value Actual Score

Expected Score

3.23 0.44 0.42 0.47 19.57 464 0.001

3.65 0.53

P-value (t-test, two tailed), SD= Standard Deviation, MD= Mean Difference

Comparable in measuring comparability is highlighted in Table 5.20 and Chart

5.12, which present the perceptions of all the sample respondents. Comparable was

tested with 2 variables. The total Mean and SD values for the actual score stood at 3.77

and 0.39 respectively, while the total Mean and SD values for expected score stood at

4.00 and 0.53 respectively with a gap score of 4.6 percent.

Table No.5.20

Actual score and expected score for comparable of financial reporting information

Qualitative characteristics of financial reporting information

Actual Score Expected Score Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Comparable 3.77 0.39 75.4 4.0 0.53 80.0 0.23 4.6

Financial index numbers and ratios

3.61 0.655 72.2 3.76 0.721 75.2 0.15 3.0

Items of previous year represented

3.94 0.352 78.8 4.25 0.55 85.0 0.31 6.2

Source: primary data, SD= Standard Deviation, MD= Mean Difference

189

Based on the Mean and Standard Deviation value, regarding mean value of actual

score and expected score for comparable the Mean value of the actual score and

expected score of ‘items of previous year represented’ stood at 3.94 and 4.25

respectively with a maximum gap score of 6.2 percent, and it was followed by the

‘financial index numbers and ratios’ with the actual score and expected score 3.61 and

3.76 respectively with a gap score of 3.00 percent.

The results of t-test are given in Table 5.21. The results show that there is a

statistically significant gap between the actual score and expected score for comparable

of financial reporting in Indian banks. As the table below, it is seen that P= 0.001 <

0.05.

Table No.5.21

Result of t-test on the actual score and expected score for comparable

Score Type Group Statistics Paired Samples Test

Mean SD MD SD t-value df P-value

Actual Score

Expected Score

3.77 0.39 0.23 0.44 11.16 464 0.001

4.00 0.53

P-value (t-test, two tailed), SD= Standard Deviation, MD= Mean Difference

75.4 80

4.6

0

20

40

60

80

100

Comparable

Chart No.5.12 Actual score and expected score for comparable of

financial reporting information in Indian banks

Actual score Expected score Gap

190

5.4.2. A Comparative Study between the Public and Private Sector Banks

Regarding the Components of Qualitative Characteristics of Financial

Reporting Information.

Relevance is one of the two fundamental qualitative characteristic of financial

reporting information. Relevance was analyzed with two components: Predictive value -

containing 9 and Confirmatory value- containing 5 variables.

Predictive value in measuring relevance is highlighted in Table 5.22 and Chart

5.13, which present the perceptions of 375 sample respondents of the public sector

banks and 90 sample respondents of the private sector banks. Predictive value was

tested with 9 variables. The total Mean and SD values of banks in the public sector

stood at 3.69 and 0.28 respectively, while the total Mean and SD values for the private

sector stood at 3.96 and 0.71 respectively with a gap score of 5.4 percent.

Table No.5.22

Predictive value of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Predictive value 3.69 0.28 73.8 3.96 0.71 79.2 0.27 5.4

Estimate of profits and losses 3.43 0.56 68.6 3.51 0.67 70.2 0.08 1.6

Non Financial Information 3.96 0.48 79.2 4.02 0.79 80.4 0.06 1.2

Forward looking information 4.59 0.49 91.8 4.34 0.91 86.8 0.25 5.0

Information on corporate social responsibility

4.43 0.73 88.6 4.01 0.99 80.2 0.42 8.4

Analysis of cash flow 3.77 0.92 75.4 4.17 0.93 83.4 0.4 8.0

Intangible assets disclosure 3.46 0.67 69.2 3.89 0.85 77.8 0.43 8.6

Off balance activities disclosure 2.57 1.02 51.4 4.01 0.93 80.2 1.44 28.8

Information concerning going concern

3.1 0.73 62 3.63 0.93 72.6 0.53 10.6

Fair value (FV) vs. historical cost(HC)

3.86 0.66 77.2 4.07 0.85 81.4 0.21 4.2

Source: primary data, SD= Standard Deviation, MD= Mean Difference

191

Based on the Mean and Standard Deviation value, the bank in the private sector

have disclosed more predictive value of financial information (Mean 3.96) than the

banks in the public sector (Mean 3.69). The study found that on seven items of the

financial information in private sector were significantly better than those in the public

sector. These items relate to 'estimate of profits and losses', 'non financial information',

'analysis of cash flow', 'intangible assets disclosure', 'off balance activities disclosure',

'information concerning going concern', and 'fair value vs. historical cost'. On the other

hand, on two items, the predictive value of financial information in the public sector

banks, the score was significantly better than in the private sector, particularly regarding

'forward looking information', and 'information on corporate social responsibility'.

The results of t-test are given in Table 5.23. The results show that there is a

statistically significant difference between the public and private sector banks regarding

the predictive value of financial reporting. As the table below, it is seen that

P = 0.001 < 0.05.

73.8 79.2

5.4

0

20

40

60

80

100

Predictive value

Chart No.5.13 predictive value of financial reporting information in

Indian banks

Public sector Private Sector Gap

192

Table No.5.23

Result of t-test on predictive value of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 3.69 0.28 0.27 5.88 463 0.001

90 3.96 0.71

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean Difference

Confirmatory value in measuring relevance is highlighted in Table 5.24 and

Chart 5.14, which present the perceptions of 375 sample respondents of the public

sector banks and 90 sample respondents of the private sector banks. Confirmatory value

was tested with 5 variables. The total Mean and SD values for public sector banks stood

at 3.38 and 0.48 respectively, while the total Mean and SD values for private sector

banks stood at 4.06 and 0.67 respectively with a difference score of 13.6 percent.

Table No.5.24

Confirmatory value of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Confirmatory value 3.38 0.48 67.6 4.06 0.67 81.2 0.68 13.6

Information from supervisory board

3.47 0.57 69.4 3.79 0.94 75.8 0.32 6.4

Information regarding personal policies

3.29 0.67 65.8 4.03 0.77 80.6 0.74 14.8

Information concerning divisions 3.37 1.37 67.4 3.81 1.02 76.2 0.44 8.8

Financial structure disclosed 2.87 0.72 57.4 4.17 0.93 83.4 1.3 26

Interim financial reports published 3.91 0.57 78.2 4.52 0.5 90.4 0.61 12.2

Source: primary data, SD= Standard Deviation, MD= Mean Difference

67.681.2

13.6

020406080

100

Confirmatory value

Chart No.5.14 Confirmatory value of financial reporting information

in Indian banks

Public sector Private Sector Gap

193

Based on the Mean and Standard Deviation value and t-test (two-tailed)

analysis, banks in the private sector have disclosed more the confirmatory value of

financial reporting (Mean 4.06) than public sector banks (Mean 3.38). The study found

that on all five items of qualitative characteristics of financial reporting information in

private sector banks significantly better that public sector banks.

The results of t-test are given in Table 5.25. The results show that there is a

statistically significant difference between the public and private sector banks regarding

the confirmatory value of financial reporting. As the table below, it is seen that

P = 0.001 < 0.05.

Table No.5.25

Results of t-test on confirmatory value of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 3.38 0.48 0.68 11.06 463 0.001

90 4.06 0.67

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean Difference

Faithful Representation (Reliability) is one of the two fundamental qualitative

characteristic of financial reporting information. Reliability was analyzed with four

components: completeness- containing 2, neutrality- containing 2, free from material

error- containing 2 and verifiability- containing 2 variables.

Completeness in measuring reliability is highlighted in Table 5.26 and Chart

5.15, which present the perceptions of 375 sample respondents of public sector banks

and 90 sample respondents of private sector banks. Completeness was tested with 2

variables. The total Mean and SD values for public sector stood at 4.15 and 0.40

respectively, while the total Mean and SD values for the private sector stood at 4.07 and

0.78 respectively with a difference score of 1.6 percent.

194

Table No.5.26

Completeness of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Completeness 4.15 0.4 83 4.07 0.78 81.4 0.08 1.6

Description corporate governance (CG)

4.57 0.5 91.4 3.86 1.02 77.2 0.71 14.2

Contingencies disclosure 3.72 0.89 74.4 4.28 0.95 85.6 0.56 11.2

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Based on the Mean and Standard Deviation value and t-test (two-tailed) analysis,

public sector banks have disclosed more completeness of financial reporting (Mean

4.15) than private sector banks (Mean 4.07). The study found that on one item of

completeness of financial reporting in the private sector banks disclosed significantly

better that public sector banks. This item relates to 'Contingencies disclosure'. On the

other hand, on one the item of the completeness of financial reporting, the public sector

banks scored significantly better than the private sector banks, i.e., 'Description

corporate governance' (CG).

The results of t-test are given in Table 5.27. The results show that there isn’t

statistically significant difference between the public and private sector banks regarding

the completeness of financial reporting. As the table below, it is seen that P = 0.17 >

0.05.

83 81.4

1.60

20

40

60

80

100

completeness

Chart No.5.15 Completeness of financial reporting information in

Indian banks

Public sector Private Sector Gap

195

Table No.5.27

Results of T-test on completeness of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 4.15 0.40 0.08 1.38 463 0.17

90 4.07 0.78

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean Difference

Neutrality in measuring reliability is highlighted in Table 5.28 and Chart 5.16,

which present the perceptions of 375 sample respondents of public sector banks and 90

sample respondents of private sector banks. Neutrality was tested with 2 variables. The

total Mean and SD values for public sector banks stood at 3.65 and 0.57 respectively,

while the total Mean and SD values for private sector banks stood at 4.27 and 0.64

respectively with a difference score of 18.2 percent.

Table No.5.28

Neutrality of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Neutrality 3.36 0.57 67.2 4.27 0.64 85.4 0.91 18.2

"Comply or explain" disclosure 3.62 0.93 72.4 4.36 0.94 87.2 0.74 14.8

Information concerning bonuses 3.11 0.51 62.2 4.19 0.63 83.8 1.08 21.6

Source: primary data, SD= Standard Deviation, MD= Mean Difference

67.2

85.4

18.2

0

20

40

60

80

100

Neutrality

Chart No.5.16 Neutralityof financial reporting information in

Indian banks

Public sector Private Sector Gap

196

Table 5.28 shows that the private sector banks have disclosed more neutrality of

financial reporting (Mean 4.27) than public sector banks (Mean 3.36). The study found

that on both items of neutrality of qualitative characteristics of financial reporting

information, the private sector banks disclosed significantly better than public sector

banks.

The results of t-test are given in Table 5.29. The results show that there is a

statistically significant difference between the public and private sector banks regarding

the neutrality of financial reporting information. As the table below, it is seen that

P = 0.001 < 0.05.

Table No.5.29

Results of t-test on neutrality of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 3.36 0.57 0.91 13.23 463 0.001

90 4.27 0.63

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean difference

Free from material error in measuring reliability is highlighted in Table 5.30

and Chart 5.17, which present the perceptions of 375 sample respondents of public

sector banks and 90 sample respondents of private sector banks. Free from material

error as an attribute was tested with 2 variables. The total Mean and SD values for the

public sector banks stood at 3.94 and 0.33 respectively, while those for the private

sector banks stood at 3.84 and 0.60 respectively with a difference score of 2.00 percent.

Table 5.30 shows that the public sector banks have disclosed more free from

material error attribute in measuring of financial reporting (Mean 3.94) than banks in

the private sector (Mean 3.84). The study found that on one item of free from material

error in measuring of qualitative characteristics of financial reporting in the private

sector banks significantly better that public sector banks. This item relates to

197

'descriptions auditor's report'. On the other hand, on one item, of ‘free from material

error’ qualitative characteristics of financial reporting in the public sector banks, the

score being significantly better than in the private sector banks, going by the 'type of

auditor’s report'.

Table No.5.30

Free from material error of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Free from material error 3.94 0.33 78.8 3.84 0.6 76.8 0.1 2.0

Descriptions auditor's report 4.32 0.5 86.4 3.74 0.91 74.8 0.58 11.6

Type of auditor’s report 3.56 0.63 71.2 3.93 0.73 78.6 0.37 7.4

Source: primary data, SD= Standard Deviation, MD= Mean Difference

The results of t-test are given in Table 5.31. The results show that there isn’t

statistically significant difference between the public and private sector banks regarding

the free from material error criterion of financial reporting. As the table below, it is seen

that P = 0.32 > 0.05.

Table No.5.31

Results of t-test on free from material error of financial reporting in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 3.94 0.33 0.1 2.15 463 0.32

90 3.84 0.60

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean difference

78.8 76.8

20

20

40

60

80

100

Free from material error

Chart No.5.17 Free from material error of financial reporting

information in Indian banks

Public sector Private Sector Gap

198

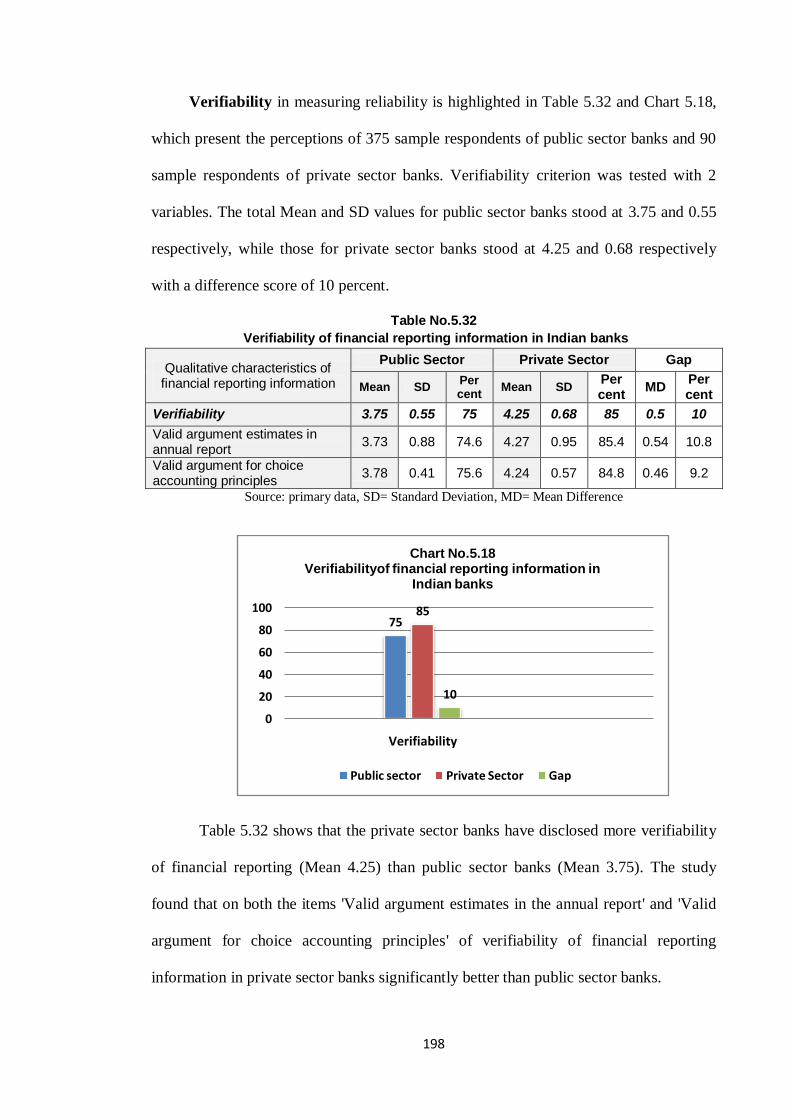

Verifiability in measuring reliability is highlighted in Table 5.32 and Chart 5.18,

which present the perceptions of 375 sample respondents of public sector banks and 90

sample respondents of private sector banks. Verifiability criterion was tested with 2

variables. The total Mean and SD values for public sector banks stood at 3.75 and 0.55

respectively, while those for private sector banks stood at 4.25 and 0.68 respectively

with a difference score of 10 percent.

Table No.5.32

Verifiability of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Verifiability 3.75 0.55 75 4.25 0.68 85 0.5 10

Valid argument estimates in annual report

3.73 0.88 74.6 4.27 0.95 85.4 0.54 10.8

Valid argument for choice accounting principles

3.78 0.41 75.6 4.24 0.57 84.8 0.46 9.2

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Table 5.32 shows that the private sector banks have disclosed more verifiability

of financial reporting (Mean 4.25) than public sector banks (Mean 3.75). The study

found that on both the items 'Valid argument estimates in the annual report' and 'Valid

argument for choice accounting principles' of verifiability of financial reporting

information in private sector banks significantly better than public sector banks.

7585

10

0

20

40

60

80

100

Verifiability

Chart No.5.18 Verifiabilityof financial reporting information in

Indian banks

Public sector Private Sector Gap

199

The results of t-test are given in Table 5.33. The result shows that there is a

statistically significant difference between the public and private sector banks regarding

verifiability of financial reporting. As the table below, it is seen that P = 0.001 < 0.05.

Table No.5.33

Results of t-test on verifiability of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 3.75 0.55 0.5 -7.43 463 0.001

90 4.25 0.68

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean difference

Understandability is highlighted in Table 5.34 and Chart 5.19, which present

the perceptions of 375 sample respondents of public sector banks and 90 sample

respondents of private sector banks. Understandability was tested with 7 variables. The

total Mean and SD values for public sector banks stood at 3.82 and 0.31 respectively,

while the total Mean and SD values for private sector banks stood at 3.79 and 0.35

respectively with a gap score of 0.6 per cent.

Table No.5.34

Understandability of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Understandability 3.82 0.31 76.4 3.79 0.35 75.8 0.03 0.6

Manner of organized annual report 4.65 0.68 93 4.67 0.7 93.4 0.02 0.4

The extent presented of graphs and tables

2.88 0.74 57.6 3.09 0.8 61.8 0.21 4.2

The extent of jargon in annual report

4.11 0.93 82.2 3.98 0.92 79.6 0.13 2.6

The size of the glossary 2.87 1.35 57.4 2.51 1.57 50.2 0.36 7.2

Information concerning mission and strategy

4.29 0.66 85.8 4.34 0.72 86.8 0.05 1.0

Annual report understandable 4.28 0.75 85.6 4.37 0.61 87.4 0.09 1.8

Classifications financial statement's elements

3.65 0.86 73.0 3.59 0.83 71.8 0.06 1.2

Source: primary data, SD= Standard Deviation, MD= Mean Difference,

200

Table 5.34 shows that the banks in the public sector have divulged more easily

understandable of financial reporting information (Mean 3.82) than the banks in the

private sector (Mean 3.79).

The public sector banks indicated higher score in understandability of financial

reporting when compared to private sector banks. The main reason for this difference

score is that there exists high degree of jargon in annual reports 82.2%, size of the

glossary 57.4% and classifications financial statement's elements 73% when compare

with private sector banks 79.6%, 50.2% and 71.8 percent respectively.

The private sector banks have shown more understandability in organized annual

report 93.4%, presented of graphs and tables 61.8% and information concerning mission

and strategy 86.8% when compared with public sector banks 93%, 57.6% and 85.8%

respectively.

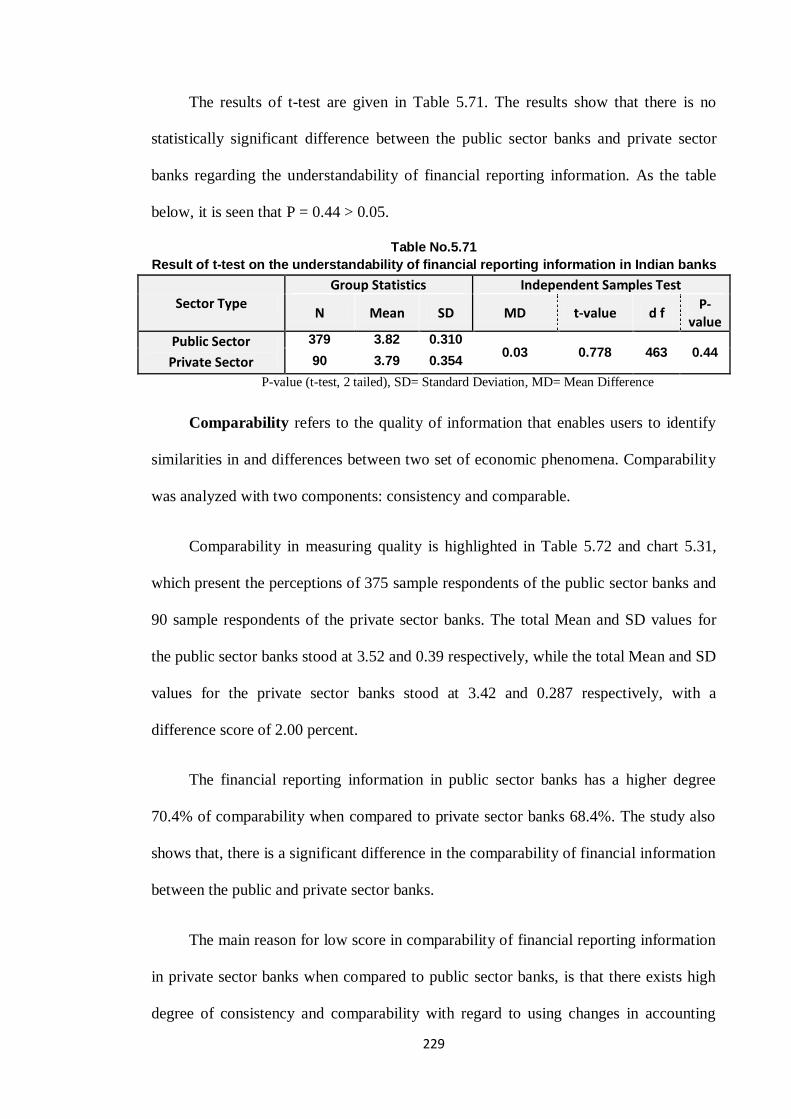

The results of t-test are given in Table 5.35. The results show that there isn’t

statistically significant difference between the public and private sector banks regarding

the understandability of financial reporting information by them. As the table below, it

is seen that P = 0.46 > 0.05.

76.475.8

0.60

20

40

60

80

100

Understandability

Chart No.5.19 Understandabilityof financial ireporting information in

Indian banks

Public sector Private Sector Gap

201

Table No.5.35

Results of t-test on understandability of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 3.82 0.31 0.03 0.78 463 0.46

90 3.79 0.35

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean difference

Comparability refers to the quality of information that enables users to identify

similarities in and differences between two set of economic phenomena. Comparability

was analyzed with two components: Consistency - containing 5, and Comparable-

containing 2 variables.

Consistency in measuring comparability is highlighted in Table 5.36 and Chart

5.20, which present the perceptions of 375 sample respondents of public sector banks

and 90 sample respondents of private sector banks. Consistency was tested with 5

variables. The total Mean and SD values for the public sector banks stood at 3.25 and

0.47 respectively, while the total Mean and SD values for these in the private sector

banks stood at 3.11 and 0.28 respectively with a difference score of 2.8 percent.

Table 5.36 shows that the public sector banks have disclosed better consistency

of financial reporting (Mean 3.25) than banks in the private sector (Mean 3.11). The

study found that on two items of consistency of financial reporting, bank in the private

sector significantly better than those in the public sector banks. These items relate to

‘changes in accounting estimates disclosure’ and ‘information concerning companies'

shares’. On the other hand, on three items of consistency of financial information, banks

in the public sector score significantly better than the private sector banks. These items

included ‘changes in accounting policies disclosure’, ‘effects of accounting policy

changes’, and ‘Benchmark information’.

202

Table No.5.36

Consistency of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Consistency 3.25 0.47 65 3.11 0.28 62.2 0.14 2.8

Changes in accounting policies disclosure

3.36 0.72 67.2 3.1 0.3 62 0.26 5.2

Changes in accounting estimates disclosure

3.5 0.69 70 3.57 0.58 71.4 0.07 1.4

Effects of accounting policy changes

2.69 0.72 53.8 2.53 0.56 50.6 0.16 3.2

Information concerning companies’ shares

3.05 0.49 61.0 3.06 0.35 61.2 0.01 0.2

Benchmark information 3.68 0.88 73.6 3.3 0.84 66 0.38 7.6

Source: primary data, SD= Standard Deviation, MD= Mean Difference,

The results of t-test are given in Table 5.37. The results show that there is a

statistically significant difference between the public and private sector banks regarding

the consistency of financial reporting information reported by them. As the table below,

it is seen that P = 0.01 < 0.05.

Table No.5.37

Results of t-test on consistency of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value df P-value

Public Sector

Private Sector

375 3.25 0.47 0.14 2.78 463 0.01

90 3.11 0.28

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean difference

65 62.2

2.8

0

20

40

60

80

Consistency

Chart No.5.20 Consistency of financial reporting information in

Indian banks

Public sector Private Sector Gap

203

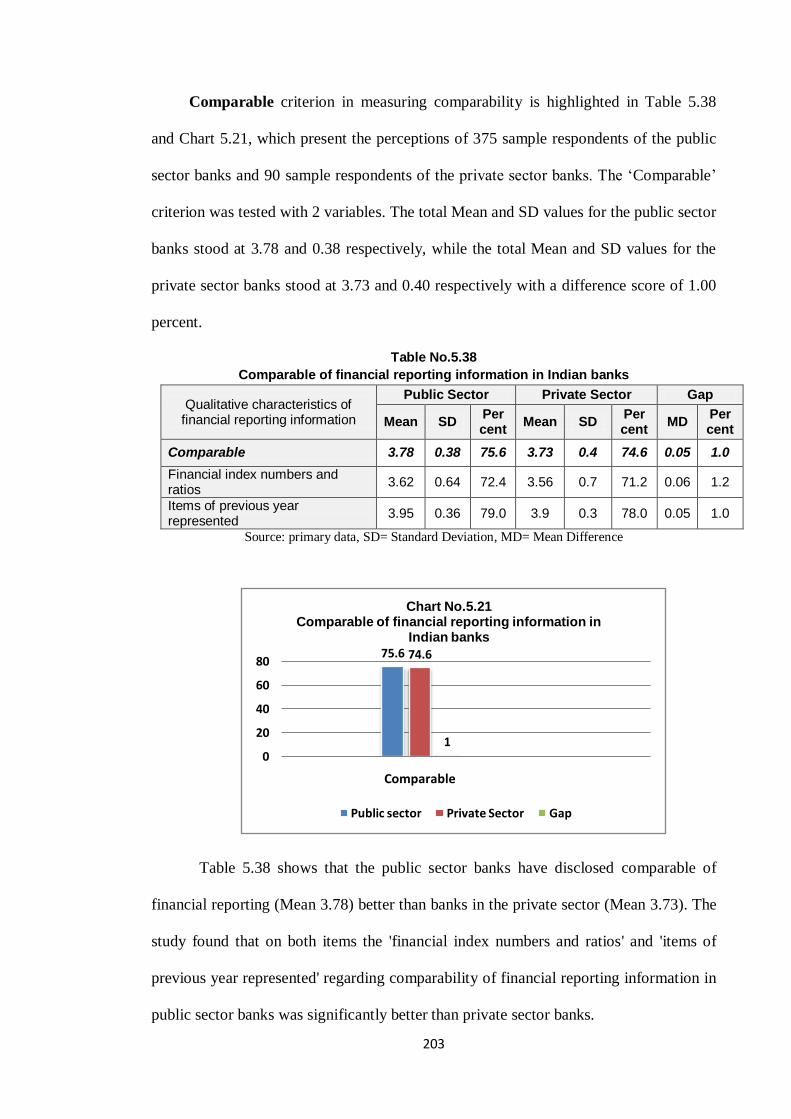

Comparable criterion in measuring comparability is highlighted in Table 5.38

and Chart 5.21, which present the perceptions of 375 sample respondents of the public

sector banks and 90 sample respondents of the private sector banks. The ‘Comparable’

criterion was tested with 2 variables. The total Mean and SD values for the public sector

banks stood at 3.78 and 0.38 respectively, while the total Mean and SD values for the

private sector banks stood at 3.73 and 0.40 respectively with a difference score of 1.00

percent.

Table No.5.38

Comparable of financial reporting information in Indian banks

Qualitative characteristics of financial reporting information

Public Sector Private Sector Gap

Mean SD Per cent

Mean SD Per cent

MD Per cent

Comparable 3.78 0.38 75.6 3.73 0.4 74.6 0.05 1.0

Financial index numbers and ratios

3.62 0.64 72.4 3.56 0.7 71.2 0.06 1.2

Items of previous year represented

3.95 0.36 79.0 3.9 0.3 78.0 0.05 1.0

Source: primary data, SD= Standard Deviation, MD= Mean Difference

Table 5.38 shows that the public sector banks have disclosed comparable of

financial reporting (Mean 3.78) better than banks in the private sector (Mean 3.73). The

study found that on both items the 'financial index numbers and ratios' and 'items of

previous year represented' regarding comparability of financial reporting information in

public sector banks was significantly better than private sector banks.

75.6 74.6

10

20

40

60

80

Comparable

Chart No.5.21 Comparable of financial reporting information in

Indian banks

Public sector Private Sector Gap

204

The results of T-test are given in Table 5.39. The results show that there is no

statistically significant difference between the public and private sector banks regarding

the comparable criterion of financial reporting reported by them. As the table below, it

is seen that P = 0.21 > 0.05.

Table No.5.39

Results of t-test on comparable of financial reporting information in Indian banks

Sector Type Group Statistics Independent Samples Test

N Mean SD MD t-value d f P-value

Public Sector

Private Sector

375 3.78 0.38 0.05 1.27 463 0.21

90 3.73 0.40

P-value (t-test, 2 tailed), SD= Standard Deviation, MD= Mean difference

5.4.3 A Comparative Study between the Public and Private Sector Banks

Regarding the Compliance with RBI Prudential Norms.

The compliance in actual performance in financial reporting with RBI prudential

norms in Indian banking system in respect of asset classification, provisioning norms,

capital adequacy and income recognition are catching up a satisfying level. As table

5.40 and chart 5.22 shows, the score of compliance in actual performance in financial

reporting with RBI prudential norms in Indian banking system average is 90.6 per cent

which is at a very satisfying level. The reason for the above result can be due to the

obligatory nature of the RBI prudential norms especially in the public sector banks

(94%) in which the compliance in actual performance in financial reporting is more

than private sector banks (87.4%).

Table No.5.40

Compliance with RBI prudential norms in Indian banks

RBI prudential norms

Public Sector Private Sector Total

Mean SD Per cent

Mean SD Per cent

Mean SD Per cent

Asset Classification 4.58 0.377 91.6 4.4 0.47 88 4.49 0.403 89.8

Provisioning Norms 4.61 0.382 92.2 4.25 0.682 85.0 4.43 0.477 88.6

Capital Adequacy 4.7 0.352 94.0 4.27 0.641 85.4 4.48 0.456 89.6

Income Recognition 4.9 0.011 98.0 4.54 0.429 90.8 4.72 0.302 94.4

Total 4.7 0.289 94.0 4.37 0.534 87.4 4.53 0.374 90.6

Source: primary data, SD= Standard Deviation, MD= Mean Difference

205

5.4.4. A Comparative Study between the Public and Private Sector Banks

Regarding the Compliance with Accounting Standards.

The compliance in actual performance in financial reporting information with

Accounting Standards in Indian banking system are needed to be improved. As table

5.41 and chart 5.23 shows, the score of compliance in actual performance in financial

reporting with Accounting Standards in Indian banking system average is 81.4 percent.

It is needed to state that the average score of private sector banks is slightly higher than

public sector banks.

Table No.5.41

Compliance with accounting standards in Indian banks

Accounting Standards

Public Sector Private Sector Total

Mean SD Per cent

Mean SD Per cent

Mean SD Per cent

AS5 Prior Period Items 4.34 0.474 86.8 4.02 0.793 80.4 4.18 0.563 83.6

AS9 Revenue Recognition 3.5 0.58 70.0 4.56 0.543 91.2 4.03 0.707 80.6

AS15 Retirement Benefits 4.13 1.06 82.6 4.44 0.901 88.8 4.28 1.037 85.6

AS18 Related party disclosures

3.59 0.728 71.8 4.03 0.867 80.6 3.81 0.776 76.2

AS22 Taxes on income 4.5 0.542 90.0 4.68 0.47 93.6 4.59 0.533 91.8

AS25 Interim Financial Reporting

3.48 0.58 69.6 3.98 0.821 79.6 3.73 0.662 74.6

AS26 Intangible asset 3.66 0.844 73.2 4.31 0.956 86.2 3.98 0.903 79.6

AS28 Impairment of assets 3.58 0.864 71.6 4.33 0.581 86.6 3.95 0.868 79.0

Total 3.85 0.551 77.0 4.29 0.508 85.8 4.07 0.57 81.4

Source: primary data, SD= Standard Deviation, MD= Mean Difference

91.6 92.294

98

94

0.8885 85.4

90.887.4

89.8 88.6 89.6

94.4

90.6

75

80

85

90

95

100

Asset Classification

Provisioning Norms

Capital Adequacy

Income Recognition

Total

Chart No.5.22 Compliance with RBI prudential norms in Indian banks

Public sector Private Sector Total

206

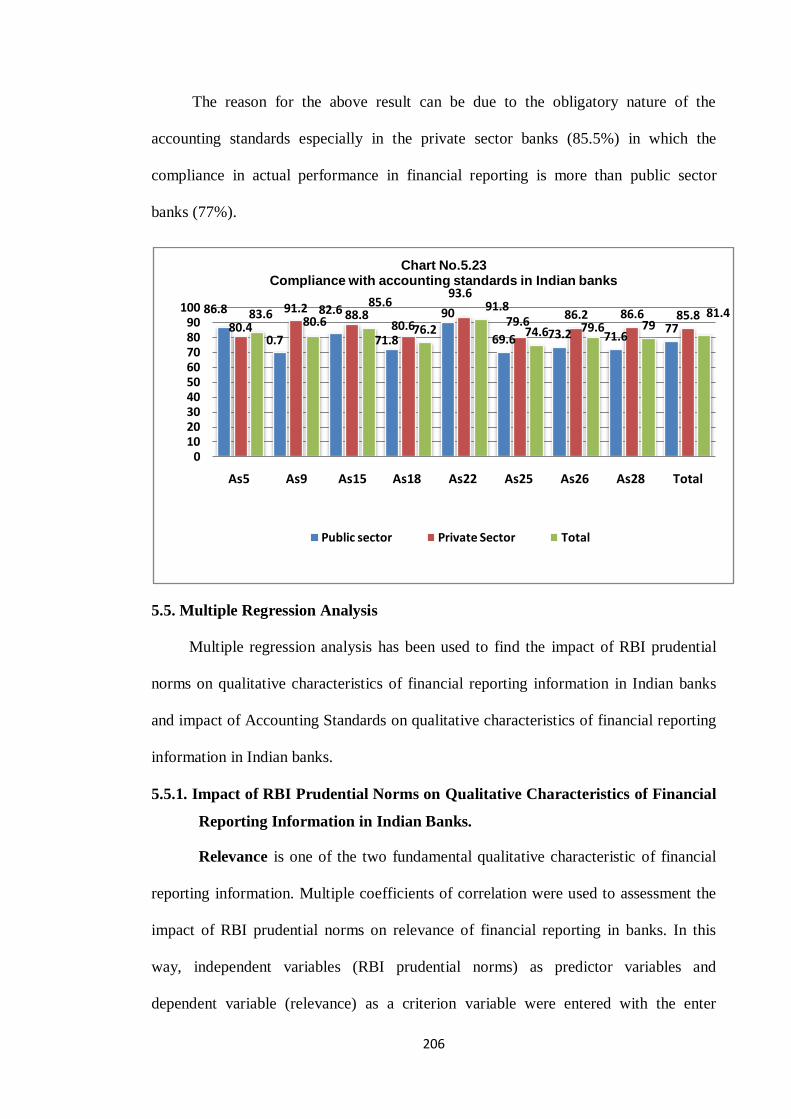

The reason for the above result can be due to the obligatory nature of the

accounting standards especially in the private sector banks (85.5%) in which the

compliance in actual performance in financial reporting is more than public sector

banks (77%).

5.5. Multiple Regression Analysis

Multiple regression analysis has been used to find the impact of RBI prudential

norms on qualitative characteristics of financial reporting information in Indian banks

and impact of Accounting Standards on qualitative characteristics of financial reporting

information in Indian banks.

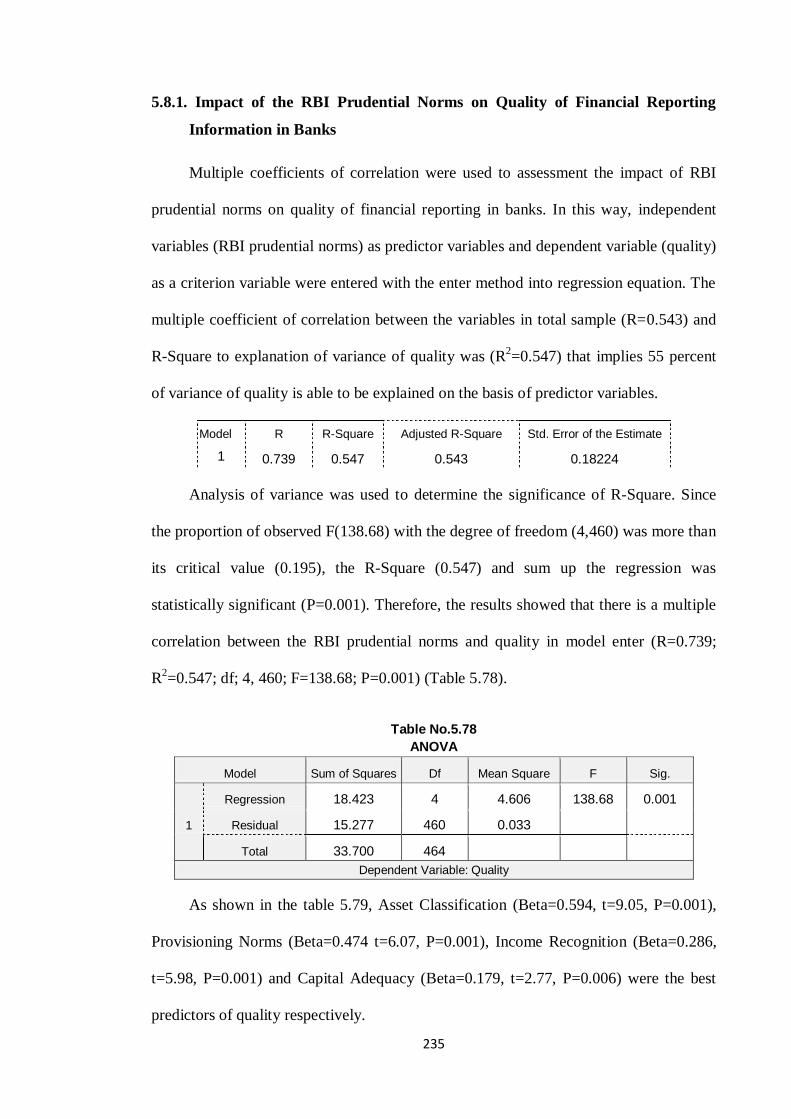

5.5.1. Impact of RBI Prudential Norms on Qualitative Characteristics of Financial

Reporting Information in Indian Banks.

Relevance is one of the two fundamental qualitative characteristic of financial

reporting information. Multiple coefficients of correlation were used to assessment the

impact of RBI prudential norms on relevance of financial reporting in banks. In this

way, independent variables (RBI prudential norms) as predictor variables and

dependent variable (relevance) as a criterion variable were entered with the enter

86.8

0.7

82.6

71.8

90

69.6 73.2 71.67780.4

91.2 88.880.6

93.6

79.686.2 86.6 85.883.6

80.6

85.6

76.2

91.8

74.6 79.6 7981.4

0102030405060708090

100

As5 As9 As15 As18 As22 As25 As26 As28 Total

Chart No.5.23Compliance with accounting standards in Indian banks

Public sector Private Sector Total

207

method into regression equation. The multiple coefficient of correlation between the

variables in total sample (R=0.590) and R-Square to explanation of variance of

relevance was (R2=0.349) that implies 35 percent of variance of relevance is able to be

explained on the basis of predictor variables.

Model R R-Square Adjusted R-Square Std. Error of the Estimate

1 0.590 0.349 0.343 0.38726

Analysis of variance was used to determine the significance of R-Square. Since

the proportion of observed F(61.54) with the degree of freedom (4,460) was more than

its critical value (0.195), the R-Square (0.349) and sum up the regression was

statistically significant (P=.001). Therefore, the results showed that there is a multiple

correlation between the RBI prudential norms and relevance in model enter (R=0.590;

R2=0.349; df; 4, 460; F=61.54; P=0.001) (Table 5.42).

Table No.5.42

ANOVA

Model Sum of Squares df Mean Square F Sig.

1

Regression 36.916 4 9.229 61.538 0.001

Residual 68.987 460 0.150

Total 105.902 464

Dependent variable: Relevance

As shown in the table 5.43, Provisioning Norms (Beta=0.539, t=5.757, P=0.001),

Income Recognition (Beta=.394, t=6.878, P=0.001), and Asset Classification

(Beta=0.313, t=3.982, P= 0.001) were the best predictors of relevance respectively.

Table No.5.43 Coefficients

Model Unstandardized Coefficients

Standardized Coefficients t Sig.

B Std. Error Beta

1

(Constant) 2.743 0.310 8.850 0.001

Asset Classification 0.372 0.093 0.313 3.982 0.001

Provisioning Norms 0.540 0.094 0.539 5.757 0.001

Capital Adequacy 0.052 0.081 0.050 0.643 0.521

Income Recognition 0.623 0.091 0.394 6.878 0.001

Dependent variable: Relevance

208

Reliability is one of the two fundamental qualitative characteristic of financial

reporting information. Multiple coefficients of correlation were used to assessment the

impact of RBI prudential norms on reliability of financial reporting in banks. In this

way, independent variables (RBI prudential norms) as predictor variables and

dependent variable (reliability) as a criterion variable were entered with the enter

method into regression equation. The multiple coefficient of correlation between the

variables in total sample (R=0.652) and R-Square to explanation of variance of

reliability was (R2=0.425) that implies 42 percent of variance of reliability is able to be

explained on the basis of predictor variables.

Model R R-Square Adjusted R-Square Std. Error of the Estimate

1 0.652 0.425 0.420 0.30733

Analysis of variance was used to determine the significance of R-Square. Since

the proportion of observed F(85.16) with the degree of freedom (4,460) was more than

its critical value (0.195), the R-Square (0.425) and sum up the regression was

statistically significant (P=0.001). Therefore, the results showed that there is a multiple

correlation between the RBI prudential norms and reliability in model enter (R=0.652;

R2=0.425; df; 4, 460; F=85.16; P=0.001) (Table 5.44).

Table No.5.44 ANOVA

Model Sum of Squares df Mean Square F Sig.

1

Regression 32.173 4 8.043 85.16 0.001

Residual 43.449 460 0.094

Total 75.622 464

Dependent variable: Reliability

As shown in the table 5.45, Asset Classification (Beta=0.762, t=10.324,

P=0.001), and Capital Adequacy (Beta=0.315, t=4.329, P=0.001) were the best

predictors of reliability respectively.

209

Table No.5.45 Coefficients

Model Unstandardized Coefficients

Standardized Coefficients

t Sig. B Std. Error Beta

1

(Constant) 1.376 0.246 5.593 0.001

Asset Classification 0.765 0.074 0.762 10.324 0.001

Provisioning Norms 0.133 0.074 0.157 1.790 0.074

Capital Adequacy -0.279 0.064 0.315 4.329 0.001

Income Recognition -0.063 0.072 0.047 0.878 0.381

Dependent variable: Reliability

Understandability is the quality of information that enables users to comprehend

its meaning. Understandability is enhanced when information is classified,

characterized and presented clearly and concisely. Multiple coefficients of correlation

were used to assessment the impact of RBI prudential norms on understandability of

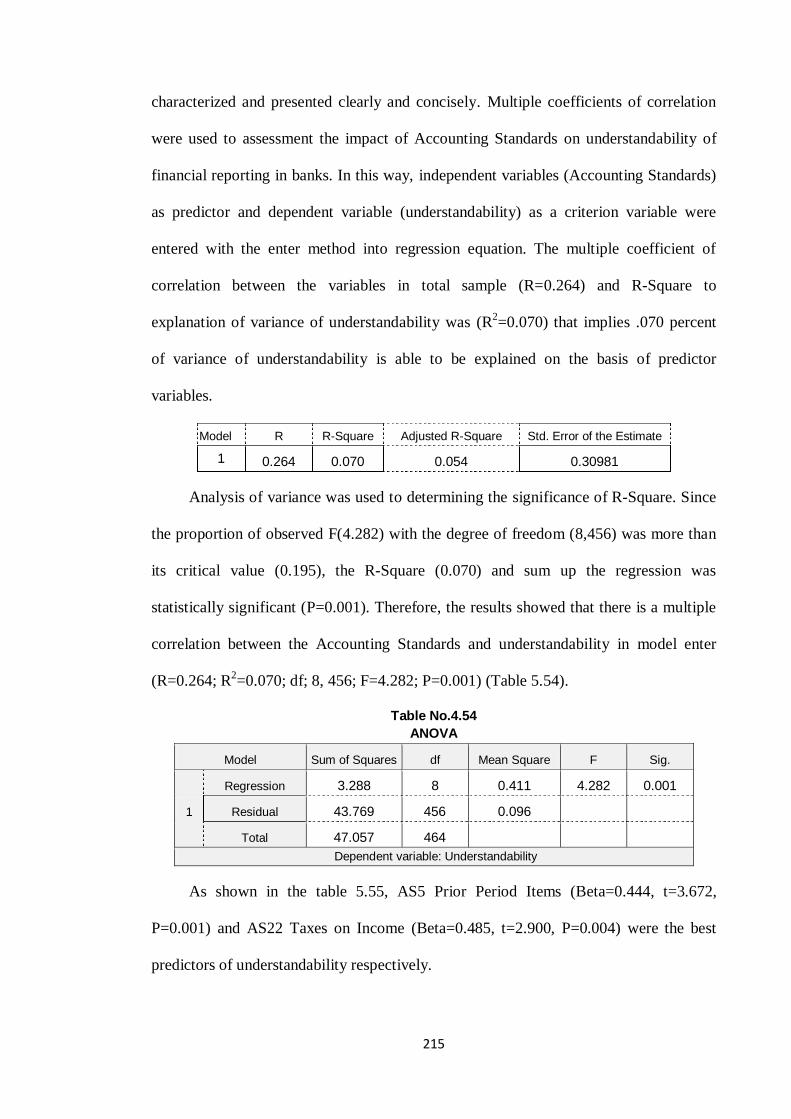

financial reporting in banks. In this way, independent variables (RBI prudential norms)

as predictor variables and dependent variable (understandability) as a criterion variable

were entered with the enter method into regression equation. The multiple coefficient of

correlation between the variables in total sample (R=0.188) and R-Square to

explanation of variance of understandability was (R2=0.035) that implies .035 percent

of variance of understandability is able to be explained on the basis of predictor

variables.

Model R R-Square Adjusted R-Square Std. Error of the Estimate

1 0.188 0.035 0.027 0.31414

Analysis of variance was used to determine the significance of R-Square. Since

the proportion of observed F(4.212) with the degree of freedom (4,460) was more than

its critical value (0.195), the R-Square (0.035) and sum up the regression was

statistically significant (P=0.002). Therefore, the results showed that there is a multiple

correlation between the RBI prudential norms and understandability in model enter

(R=0.188; R2=0.035; df; 4, 460; F=4.212; P=0.002) (Table 5.46).

210

Table No.5.46

ANOVA

Model Sum of Squares df Mean Square F Sig.

1

Regression 1.663 4 0.416 4.212 0.002

Residual 45.394 460 0.099

Total 47.057 464

Dependent variable: Understandability

As shown in the table 5.47, Provisioning Norms (Beta=0.363, t=3.188, P= 0.002),

and Asset Classification (Beta=0.206, t=2.152, P= 0.032) were the best predictors of

relevance respectively.

Table No.5.47 Coefficients

Model Unstandardized Coefficients

Standardized Coefficients

t Sig. B Std. Error Beta

1

(Constant) 3.804 0.251 15.127 0.001

Asset Classification 0.163 0.076 0.206 2.152 0.032

Provisioning Norms 0.243 0.076 0.363 3.188 0.002

Capital Adequacy 0.021 0.066 0.031 0.326 0.744

Income Recognition 0.093 0.074 0.088 1.269 0.205

Dependent variable: Understandability

Comparability refers to the quality of information that enables users to identify

similarities in and differences between two set of economic phenomena. Multiple

coefficients of correlation were used to assessment the impact of RBI prudential norms

on comparability of financial reporting in banks. In this way, independent variables

(RBI prudential norms) as predictor variables and dependent variable (comparability) as

a criterion variable were entered with the enter method into regression equation. The

multiple coefficient of correlation between the variables in total sample (R=0.635) and

R-Square to explanation of variance of comparability was (R2=0.402) that implies 40

percent of variance of comparability is able to be explained on the basis of predictor

variables.

211

Model R R-Square Adjusted R-Square Std. Error of the Estimate

1 0.634 0.402 0.397 0.29041

Analysis of variance was used to determine the significance of R-Square. Since

the proportion of observed F(77.30) with the degree of freedom (4,460) was more than

its critical value (0.195), the R-Square (0.402) and sum up the regression was

statistically significant (P=0.001). Therefore, the results showed that there is a multiple

correlation between the RBI prudential norms and comparability in model enter

(R=0.634; R2=0.402; df; 4, 460; F=77.30; P=0.001) (Table 5.48).

Table No.5.48 ANOVA

Model Sum of Squares df Mean Square F Sig.

1

Regression 26.079 4 6.520 77.30 0.001

Residual 38.796 460 0.084

Total 64.875 464

Dependent variable: Comparability

As shown in the table 5.49, Asset Classification (Beta=0.656, t=8.70, P= 0.001),

Income Recognition (Beta=.195, t=3.56, P=0.001), and Provisioning Norms

(Beta=0.21, t=2.34, P= 0.019) were the best predictors of comparability respectively.

Table No.5.49 Coefficients

Model Unstandardized Coefficients

Standardized Coefficients t Sig.

B Std. Error Beta

1

(Constant) 1.683 0.232 7.240 0.001

Asset Classification 0.609 0.070 0.656 8.703 0.001

Provisioning Norms 0.165 0.070 0.210 2.344 0.019

Capital Adequacy 0.115 0.061 0.140 1.882 0.060

Income Recognition 0.242 0.068 0.195 3.560 0.001

Dependent variable: Comparability

212

5.5.2. Impact of Accounting Standards on Qualitative Characteristics of Financial

Reporting Information in Indian Banks.

Relevance is one of the two fundamental qualitative characteristic of financial

reporting information. Multiple coefficients of correlation were used to assessment the

impact of Accounting Standards on relevance of financial reporting information in

Indian banks. In this way, independent variables (Accounting Standards) as predictor

variables and dependent variable (relevance) as a criterion variable were entered with