Embed Size (px)

Citation preview

ACCELERATION OF FINANCIAL MARKET DEEPENING

C H A P T E R V

Bank Indonesia issued the Blueprint for Money Market Development (BPPU) 2025 in an effort to accelerate the creation of a liquid, efficient and deep financial market. The aims were to support monetary and financial system stability and to accelerate national economic development. BPPU 2025 is being implemented by encouraging the digitalization and strengthening of financial market infrastructure, strengthening the effectiveness of monetary policy and developing sources of economic financing and risk management. Implementation of BPPU 2025 is supported by strengthening synergies whether within Bank Indonesia itself or between Bank Indonesia and the relevant authorities and players in the financial industry.

The development and deepening of financial markets have shown positive developments. As part of structural reform efforts to achieve and maintain stability of the Rupiah, Bank Indonesia has made efforts to deepen financial markets together with the other relevant authorities. Good progress has been made on various instruments in the money and foreign exchange markets, even though progress has been somewhat restrained during the Covid-19 pandemic. The average volume of transactions on the Rupiah interbank money market (PUAB) increased from IDR11.7 trillion per day in 2016 to IDR19.0 trillion per day in 2019, before declining to IDR9.6 trillion per day in 2020, as a result of the pandemic. The volume of foreign currency transactions was relatively stable at around USD5.5 billion per day in 2018 and 2019, and slipped to some USD4.7 billion per day in 2020, mainly supported by an increase in domestic non-deliverable forward (DNDF) transactions. This decline in the volume of foreign exchange transactions is commensurate with declines in the components of GDP that are transacted in foreign currency, particularly the exports-imports component of goods and services; these are projected to contract by around 15% in 2020. Deepening of the financial markets was also evidenced by positive developments concerning the number of issuances of short-term securities in 2020, particularly corporate securities (SBK) and certificates of deposit.32

The program for financial market development and deepening should be continued to support economic recovery. A liquid, efficient and deep financial market is the ultimate goal of financial market development. These efforts will help to support stability of the rupiah; to ensure the availability of various instruments for liquidity and risk management; and to facilitate the creation of alternative sources of financing for national development. Despite progress to date in developing Indonesian financial markets, continued efforts face challenges, especially concerning how to reduce the level of credit risk among market participants (counterparty risk). For example, credit risk among the market players is susceptible to changes in global uncertainty; the higher global uncertainty, the higher the level of credit risk, or the greater the pressure

32 In 2020, there were SBK issuances by one corporation that reached IDR566 billion, an

increase from IDR220 billion in 2019. The issuance of certificates of deposit in 2020

amounted to IDR9.3 trillion, down from IDR20.7 trillion in 2019.

on transactions between market participants. A high level of credit risk hinders the development and deepening of a broader financial market, underscoring the need to strengthen financial market infrastructure.

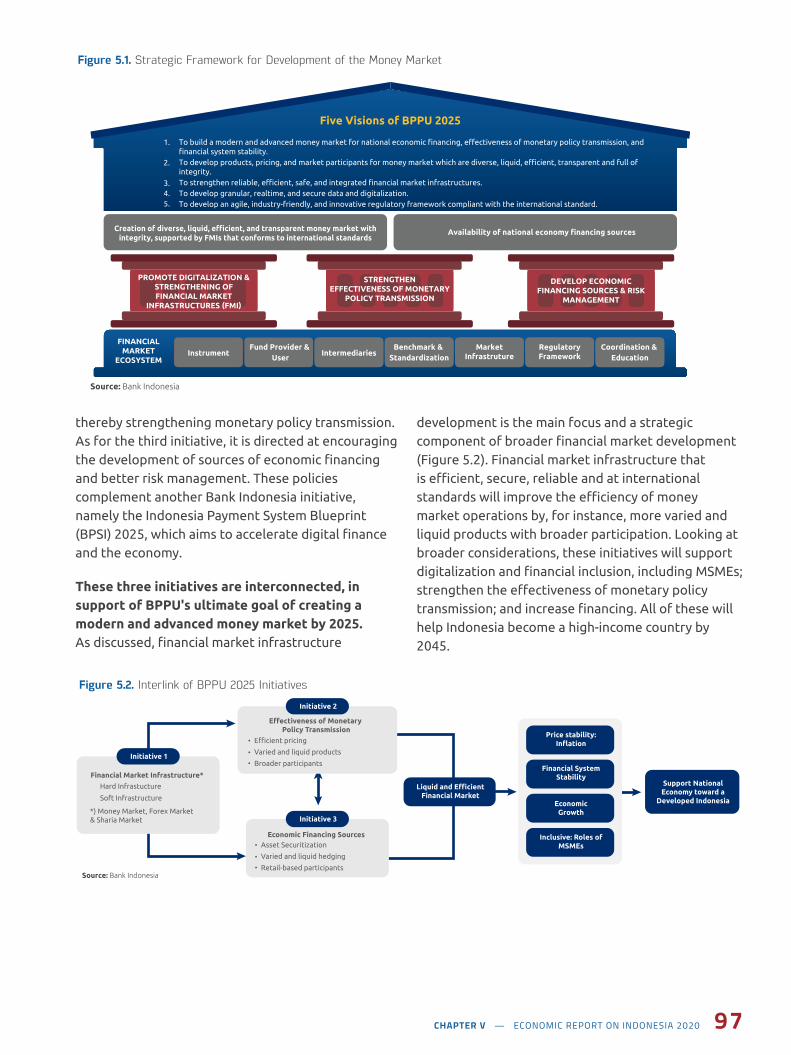

Bank Indonesia formulated the Blueprint for Money Market Development (BPPU) 2025 as a comprehensive policy response to accelerate money market reform through strengthening infrastructure and digitalization. This is being done to create a liquid, efficient and deep financial market in order to support monetary stability, financial system stability and a conducive climate for financing national development. Three main BPPU initiatives (see following paragraph) were adopted to achieve a modern, advanced financial market that complies end-to-end with international standards. Coverage includes the instruments themselves; the basis of the market players; a credible benchmark rate; and various forms of infrastructure (market infrastructure, regulatory framework, coordination and education). The three main BPPU 2025 initiatives encourage the implementation of digitalization and infrastructure in response to the ongoing digital transformation along with the development of new manufacturing technologies (also known as ‘Industry 4.0’). This is in line with Bank Indonesia's efforts to encourage digitalization of the payment system.

There are three main BPPU 2025 initiatives and the goal is to create an integrated development strategy to achieve money market reform in Indonesia. In the first BPPU initiative in 2025, money market reform policies will be focused on developing efficient, safe, reliable and international standard infrastructure, as just mentioned. This will be achieved through the development of various pieces of largely pre-existing, electronic infrastructure, namely: an Electronic Trading Platform (ETP); a so-called ‘matching system’, which improves the current bilateral trading system; a Central Counterparty (CPP) ; a trade repository; the BI Real Time Gross Settlement system (RTGS); and the BI Securities Settlement System (SSS). These constitute the basis for the second and third initiatives in the development of the financial market (Figure 5.1). The second initiative envisages reforms to develop the money market and foreign exchange markets to ensure adequate liquidity, depth and efficiency,

96 CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020

thereby strengthening monetary policy transmission. As for the third initiative, it is directed at encouraging the development of sources of economic financing and better risk management. These policies complement another Bank Indonesia initiative, namely the Indonesia Payment System Blueprint (BPSI) 2025, which aims to accelerate digital finance and the economy.

These three initiatives are interconnected, in support of BPPU's ultimate goal of creating a modern and advanced money market by 2025. As discussed, financial market infrastructure

Figure 5.1. Strategic Framework for Development of the Money Market

Source: Bank Indonesia

Financial Market Infrastructure*

Hard Infrastucture

Soft Infrastructure

*) Money Market, Forex Market & Sharia Market

Initiative 1

Effectiveness of Monetary Policy Transmission

Efficient pricing

Varied and liquid products

Broader participants

Initiative 2

Economic Financing SourcesAsset Securitization

Varied and liquid hedging

Retail-based participants

Initiative 3

Liquid and Efficient Financial Market

Price stability: Inflation

Support National Economy toward a

Developed Indonesia

Financial System Stability

Economic Growth

Inclusive: Roles of MSMEs

Figure 5.2. Interlink of BPPU 2025 Initiatives

development is the main focus and a strategic component of broader financial market development (Figure 5.2). Financial market infrastructure that is efficient, secure, reliable and at international standards will improve the efficiency of money market operations by, for instance, more varied and liquid products with broader participation. Looking at broader considerations, these initiatives will support digitalization and financial inclusion, including MSMEs; strengthen the effectiveness of monetary policy transmission; and increase financing. All of these will help Indonesia become a high-income country by 2045.

Five Visions of BPPU 2025

To build a modern and advanced money market for national economic financing, effectiveness of monetary policy transmission, and financial system stability.To develop products, pricing, and market participants for money market which are diverse, liquid, efficient, transparent and full of integrity.To strengthen reliable, efficient, safe, and integrated financial market infrastructures.To develop granular, realtime, and secure data and digitalization.To develop an agile, industry-friendly, and innovative regulatory framework compliant with the international standard.

Creation of diverse, liquid, efficient, and transparent money market with integrity, supported by FMIs that conforms to international standards

Instrument IntermediariesFund Provider &

UserBenchmark &

StandardizationMarket

InfrastrutureRegulatoryFramework

Coordination & Education

FINANCIAL MARKET

ECOSYSTEM

STRENGTHEN EFFECTIVENESS OF MONETARY

POLICY TRANSMISSION

DEVELOP ECONOMIC FINANCING SOURCES & RISK

MANAGEMENT

Availability of national economy financing sources

1.

2.

3.4.5.

Source: Bank Indonesia

PROMOTE DIGITALIZATION & STRENGTHENING OF FINANCIAL MARKET

INFRASTRUCTURES (FMI)

CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020 97

BPPU 2025 Responds to the Challenges of Industry 4.0 and the Digital Economy

5.1.

Deep financial markets play an important role in driving economic growth. Based on the significant role that the financial markets play in stimulating economic growth, the goal of the financial market development and deepening program is to achieve a financial market that is liquid, efficient and deep. This ultimate goal is not only to support the achievement of Bank Indonesia's main objectives in achieving and maintaining the stability of the Rupiah, but also to encourage the creation of instruments to manage liquidity and risk. Furthermore, the final target of the financial market deepening and development program is aimed at supporting brisker economic growth by creating alternative sources of financing for national development. There is considerable room for progress in this regard, because Indonesian financial markets are still relatively underdeveloped and volatile. This is evidenced by the low volume of transactions and composition of Indonesia's derivative instruments in comparison to conditions in peer countries (Charts 5.1 and 5.2).

The development of financial market infrastructure in accordance with international standards (best practices) is the main basis for facilitating transactions, increasing transparency and managing risk. In order to achieve a liquid,

efficient and deep financial market, the development of financial market infrastructure needs to be strengthened, to act as a catalyst in a segmented and fragmented market. In addition, the development of financial market infrastructure can also reduce counterparty risk, which has hindered financial market development to date. This infrastructure development can also be a means of systemic risk mitigation, in support of strong risk management. As performance standards, the financial market infrastructure needs to be based on proven international best practice standards, through the application of the principles for financial market infrastructure (PFMI).33

The development of financial market infrastructure constitutes Bank Indonesia's response to the increasingly rapid development of digital technology, facilitating easier access to financing instruments. Increased digitalization and access to technology will make it easier for companies to work with FinTech firms that offer digital platforms

33 Principles for financial market infrastructure (PFMI) were issued by the Committee

on Payment and Settlement System (CPSS) and the technical committee of the

International Organization of Securities Commissions (IOSCO) in April 2012. These

committees operate under the auspices of the Bank for International Settlements

(BIS). Source: Bank Indonesia, BIS Triennial Survey 2019, calculated

4

7

10

14

19

40

55

0 10 20 30 40 50 60

Philippines

Indonesia

Malaysia

Thailand

Brazil

India

Korea

Billion USD

Chart 5.1. Average Daily Forex Transactions

Source: Bank Indonesia, BIS Triennial Survey 2019, calculated

%

78

6560 58 57

50

40

0

10

20

30

40

50

60

70

80

90

Mal

aysi

a

Brazil

Thai

lan

d

Ko

rea

Ind

ia

Philippines

Ind

on

esia

Chart 5.2. Composition of Derivatives to Total Transactions

98 CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020

to bring together parties, for example, with potential lenders. The financing instruments include long-term instruments such as government securities and corporate bonds, as well as short-term instruments, like commercial securities and certificates of deposit. The general public can easily obtain financial market information through a digital platform that can be readily accessed by all market players, and which is directly connected to the payment infrastructure and transaction settlements. Transactions in the money market through technology applications are becoming easier and more credible, supported by credit scoring data that are increasingly easy to obtain. This can broaden access to financial markets and make it easier for more people to obtain cheap funds, thereby boosting business activities in the real sector.

Financial market development will be carried out by strengthening cooperation between Bank Indonesia, the Government and related authorities. Interlinks between markets increase the need for cross-authority coordination to ensure consistency among market development programs. Accordingly in 2016, Bank Indonesia, the Ministry of Finance and OJK established a Forum for Coordination of Financial Market Development and Deepening (FK-PPPK), as a cross-authority coordination body to align market development programs. FK-PPPK has agreed to formulate a comprehensive and measurable blueprint for the development of the Indonesian financial market, namely the National Strategy for Financial Market Development and Deepening (SN-PPPK). The development of financial market infrastructure is one important element and a main pillar of SN-PPPK, namely the modernization of e-systems and integration of infrastructure across authorities. Furthermore, given the sizeable need for development financing, SN-PPPK is supported by economic financing and risk management consisting of three elements, namely the providers and users of funds, financial instruments and intermediary institutions.

Money market reforms are being accelerated to strengthen policy transmission and support economic financing through the issuance of the Blueprint for Money Market Development (BPPU) 2025. The process of developing and deepening the financial market is continuously being encouraged

to create a more liquid and efficient financial market in support of monetary stability, financial system stability and a conducive climate for financing national development. BPPU 2025 has five main visions aimed at developing the money market: (i) building a modern and advanced money market that supports economic financing and monetary policy transmission and financial system stability; (ii) developing products, actors and pricing in the money market that are varied, liquid, efficient, transparent, inclusive and of integrity; (iii) creating reliable, efficient, secure and integrated money market infrastructure; (iv) developing digital data that have real time, granular and secure characteristics; and (v) reforming the financial market regulatory framework to be agile, industrial friendly, innovative and at international standards. The BPPU 2025 furthers the National Strategy for Financial Market Development and Deepening (SN-PPPK), which fits well with Bank Indonesia's focus on future financial market development.

BPPU 2025 was also formulated in response to Bank Indonesia's policy on the development of Industry 4.0 and digitalization. BPPU 2025 is supported by three main policy initiatives, namely encouraging digitalization and strengthening financial market infrastructure, strengthening the effectiveness of monetary policy and developing sources of economic financing and risk management. The focus of BPPU 2025 is on the development of a modern, advanced and international standard market ecosystem that is end-to-end, covering 3P+I aspects, namely Products, Players, Pricing and Infrastructure. Strengthening of infrastructure and digitalization as part of the BPPU 2025 initiative, is a response to rising Industry 4.0-driven digital transformation in line with Bank Indonesia's efforts to encourage digitalization through the Indonesia Payment System Blueprint (BSPI) . Technological developments have encouraged the creation of a digital economy, which has become a new driving force of economic growth, utilizing digital platforms that are able to reduce costs, including the time required for economic transactions, and to increase the frequency of transactions. Such rapid technological developments in both the real and financial sectors will demand financial market infrastructure support that is secure, efficient and reliable.

CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020 99

The three main BPPU 2025 initiatives are being carried out together in order to support the development of the money market. The work program of each initiative is carried out by paying attention to interactions among the three initiatives so as to ensure the achievement of BPPU's 2025 goals (Figure 5.3). To encourage interconnections among the three initiatives, policies were adopted that focused on developing money market instruments and foreign exchange markets, namely mandatory clearing through central counterparties. With this policy, clearing and innovation for OTC derivative transactions will be carried out through clearing institutions or central counterparties which also act as counterparty risk managers for market players. The implementation of a central counterparty is a way to reduce market segmentation, increase transparency and mitigate risk among market participants. Modernization of financial market infrastructure will also support the creation of a conducive environment to develop new financing instruments, and thus have a positive impact on meeting the financing needs of the economy in the medium- and long-term.

Figure 5.3. Three Key Initiatives of the 2025 Blueprint for Money Market Development (BPPU 2025)

Key InitiativesBPPU 2025

3

Promote FMI Digitalization & Strengthening FMI

Trading Venue/BI-ETP

Central Counterparty

BI-SSSS

BI-RTGS

Trade Repository

Source: Bank Indonesia

Improving the Effectiveness of Monetary Policy Transmission

Repo

IndONIA dan JIBOR

Overnight Index Swap

DNDF

Local Currency Settlement

Develop Economic Financing Sources and Risk Management

Long-Term Hedging Instrument

Sustainability and Green Financing

Retail-based Investors

Asset Securitization

The interlinkages between the three main initiatives will help achieve the BPPU 2025 final target of creating a modern and advanced money market. Reliable, efficient, secure and integrated financial market infrastructure in the first initiative will be the catalyst to increase the ease of conducting transactions in the financial market, reducing segmentation and increasing market transparency. This ideal infrastructure will provide a way for the money market to function properly through efficient transactions between actors, supported by accountable market conduct, thereby increasing the effectiveness of policy transmission carried out by Bank Indonesia (initiative two). The strengthening of infrastructure and development of the money market will make it easier for market players (including MSMEs) to gain access to financing (initiative three). Strengthening the strategic development plan through improving linkages between these initiatives is expected to support Bank Indonesia's efforts to improve price stability, support financial system stability, help boost economic growth and foster MSME sector inclusiveness. These, in turn, will help Indonesia to become a high-income developed country by 2045.

100 CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020

Digitalization to Strengthen Financial Markets Infrastructure

5.2.

The focus of money market reform policies in the first BPPU 2025 initiative is development of efficient, secure, reliable and international standard money market infrastructure; this constitutes the main foundation for financial markets development. The development of financial market infrastructure will form the foundation to support the creation of a market that functions efficiently. Also, infrastructure development will become the main basis for increasing the ease of conducting transactions in the financial market, thereby supporting a deeper and more liquid financial market. The financial market infrastructure development strategy is focused on developing five (5) elements in an integrated manner, namely: (i) trading venue (market operator); (ii) central counterparty; (iii) trade repository; (iv) payment system; and (v) securities settlement system (Figure 5.4). These are discussed in the following sub-sections. This development of financial market

infrastructure is also integrated and interconnected with the digital infrastructure that will be developed via BI-FAST (an efficient, real-time retail payment system) to accommodate retail digital transactions and digital transformation as stated in BSPI 2025. Infrastructure development is expected to reduce interest rates and transaction costs, thereby making the financial market deeper, more liquid and efficient.

In the trading venue element of infrastructure development, Bank Indonesia is encouraging the accelerated development and use of market operators to increase liquidity and make transactions in the money market more efficient. In a follow-up to the BI market operator regulations (issued in 2019), Bank Indonesia is encouraging the development of an electronic trading platform (ETP), employing both bilateral and multi-matching systems in 2021. With the ETP matching system, market participants can access instruments in the money

Figure 5.4. End-to-End Development of Financial Market Infrastructure

Source: Bank Indonesia

Support National Economy toward an Advanced Indonesia 2045

Financial Market Development Supporting Monetary Policy

Transmission

Source of Financing Instruments for Economic Development

Real Sector

Financial Sector

Financial Market Infrastructure

ECOSYSTEM Market Participants

MONEY MARKET

FOREIGN EXCHANGE MARKET

SHARIA FINANCIAL MARKET

STRUCTURE PRODUCT MARKET

BOND MARKET

STOCK MARKET

Reliable, efficient, safe, and

integrated FMIs compliant

with international standards

TRADINGVENUE

CSD/SSSTRADE

REPOSITORY

CENTRALCOUNTERPARTY

PAYMENTSYSTEM

Instrument Technology Regulation International Standard

CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020 101

market at the best price available on this platform, using the same information, thereby increasing price transparency and reducing asymmetric information in the money market (Figure 5.5). This development program will be followed by the implementation of standardized instruments which must be transacted through the ETP system, both on bilateral and multilateral matching systems. Bank Indonesia will also modernize the BI-ETP for monetary operations, with this target expected to be attained by 2022 (Figure 5.6).34

Bank Indonesia has prioritized the establishment of central counterparty (CCP) infrastructure for interest rates and exchange rates to reduce segmentation in the financial market. The CCP for interest rates and exchange rates (SBNT CCP) acts as a central clearing institution that does netting of over the counter (OTC) transactions of interest rates and exchange rates, and carries out the risk management function through the netting process.35 The SBNT CCP is expected to carry out industrial testing for instruments that can be cleared through the SBNT CCP in mid-2021 and to start operating in early 2022. The drafting of the regulatory design regarding mandatory clearing is expected to be completed in 2021. This is expected to produce an operational concept for the clearing of OTC Derivative instruments that is in line with OJK regulations

34 Some of the criteria highlighted by IOSCO (2012) are the degree of complexity and

low operational process; depth of liquidity; and availability of fair and reliable prices.

35 Legally, the development of the SBNT CCP is already regulated in the PBI and its

implementing regulations, namely PBI No.21/11/PBI/2019 and PADG No.22/14/

PADG/2020 concerning the Implementation of the SBNT CCP.

regarding the application of margins on OTC Derivative transactions, especially those not cleared through CCP.36 Instruments that may be considered for clearing through the CCP include simple instruments with easy settlement processes and ones that use the Rupiah.37 The development of the SBNT CCP is supported by stronger coordination among the authorities, market players and associations.

The establishment of the CPP will be accompanied by efforts to mitigate additional systemic risk in the financial markets. Formation of the SBNT CPP, which is a clearing house with high concentration risk, could lead to systemic risk in the financial market. The market concentration of the CCP institution, as a systemically important institution, requires a strong regulatory framework; robust corporate governance; good risk management; and the implementation of tight surveillance and monitoring by Bank Indonesia and the related authorities. The CCP will have a complex infrastructure and it must comply with high international standards, given that it has greater inherent risks than other financial market infrastructure. Meanwhile, the development of the SBNT CCP will reduce the risk of OTC derivative transactions conducted by market players, especially if the CCP has received qualified status from an authorized international institution. For this reason, the development of the CCP over the long-term will be undertaken in accordance with international standards, using the 22 principles for financial market infrastructure (PFMI) issued by BIS-IOSCO 2012.

36 Consultative Paper: Margin Requirement for Non-Centrally Cleared Derivatives.

37 Some of the criteria highlighted by IOSCO (2012) are the degree of complexity and

low operational process, depth of liquidity and availability of fair and reliable prices.

Ojan

ETP Multimatching System

Bid Ask

50

14020

14030

14050 14060

14090

14095

60

Best price

Dealer Bank A(Anonymous)

Bid: 1 Mio @14030Ask: 1 Mio @14090

Dealer Bank B(Anonymous)

Bid: 1 Mio @14020Ask: 1 Mio @14060

Dealer Bank C(Anonymous)

Bid: 1 Mio @14050Ask: 1 Mio @14095

Source: Bank Indonesia

Figure 5.5. ETP Multimatching System

2021

Financial Market Infrastructure

2022 2023 - 2025

Implementation of Multimatching ETP Implementation of

CCP SBNTImplementation ofTrade Repository

Implementation ofBI-ETP (GEN III)

Implementation of BI-SSSS (GEN III)

Implementation of BI-RTGS (GEN III)

Payment System Infrastructures Interlink

to Financial Market

Conceptual Design ofBI-SSSS (Gen III)

Conceptual Design ofTrade Repository

Business RequirementDesign BI-RTGS

(Gen III)

Functional and DesignSpecification of

BI-RTGS(Gen III)

Source: Bank Indonesia

Figure 5.6. Money Market Infrastructure Development Road Map

102 CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020

Regarding the trade repository element, Bank Indonesia is accelerating its development program in an effort to increase the transparency of financial market data, especially OTC derivative transactions in the money market and foreign exchange market. The transparency of financial market data through the use of accurate granular data and information will help the authorities to formulate appropriate policies, including for regulatory and supervisory technology in the framework of digitizing regulations in the financial market. In Indonesia, there is currently no trade repository (TR) which records all OTC derivative transactions. Consequently, development is aimed at establishing a TR institution that meets international technical standards and qualifications to obtain qualified TR status. TR development will also provide data feeds and granular information on OTC derivative transactions to the omni data repository of Bank Indonesia, which is currently being developed to capture digital transactions data in the Indonesian economy. This development is also aimed at taking advantage of a unique investor ID to facilitate the monitoring of transactions data related to underlying transactions on the financial market.

The development of payment system infrastructure and a securities settlement system will continue to be strengthened in line with the acceleration of digital transformation. The development of a payment system and a securities settlement system that supports digital payments, both retail and wholesale, will be vital in the development of future payment systems. Development of the payment system is aimed at increasing efficiency and facilitating cross border payments that will assist the standardization process for the settlement of transactions conducted in the financial market. Strengthening of BI-RTGS, as the main payment system infrastructure, will include: (i) core system aspects covering multicurrency and liquidity saving mechanisms, as well as interconnections with other financial market infrastructure through the use of ISO20022 standard message formats and (ii) non-core system aspects which include the broadening of membership and usage. Meanwhile, strengthening of the BI-SSSS securities settlement system infrastructure will include the development of an administrative system for monetary instruments and government instruments such as Government Securities that can accommodate development needs of instruments in the future.

CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020 103

The Development of Money and Forex Markets to Strengthen the Effectiveness of Policy Transmission

5.3.

With the support of modern infrastructure, policy in this second BPPU 2025 initiative would encourage the development of more liquid, deeper and more efficient money and foreign exchange markets, thereby strengthening the effectiveness of Bank Indonesia's monetary policy transmission. The focus of the second initiative is to emphasize the development of money and foreign exchange market instruments, in line with the increasing needs of market players for a variety of liquidity management instruments, investment instruments and risk management instruments. This initiative is to be carried out in an integrated manner, being interconnected with the first BPPU 2025 initiative (the establishment of efficient, secure, reliable and international standard financial market infrastructure). This measure supports Bank Indonesia's efforts to strengthen the effectiveness of monetary policy transmission in safeguarding monetary stability and financial system stability, ultimately helping to place Indonesia on a trajectory to become an advanced country.

In the money market, Bank Indonesia continues to develop the repo market and instruments to manage interest rate risk. Bank Indonesia continues to develop a collateralized market through the repo secondary market, which will make it easier for market players to manage their liquidity. It focuses on various agendas, especially: the expansion of underlying repo transactions (by developing securities lending, triparty repos and increased linkages with FinTech) and widening the adoption of standard contracts, such as the General Master Repo Agreement (GMRA) in Indonesia. An increase in repo transactions is consistent with Bank Indonesia's monetary policy which uses the repo rate as the policy interest rate. An increase in transactions liquidity in the repo market would, in turn, improve the effectiveness of Bank Indonesia's monetary policy transmission.

Bank Indonesia is also continuing to develop risk management instruments in the money market. This policy is focused on developing interest rate derivatives, such as the overnight index swap (OIS) and interest rate swap (IRS). In 2020, the piloting of OIS transactions by several banks showed progress, although the liquidity of the OIS market still needs to be improved. In the future, optimizing the role of banks and money market brokers in quoting prices for the IRS and OIS will be an important element in developing risk management instruments. Efforts to encourage the development of OIS and IRS will also be strengthened by steps to encourage standardization in pricing for IRS and OIS transactions, and the use of a so-called ‘systematic internaliser’ and ETP as a more transparent and efficient means to quote prices.38 OIS and IRS instruments are also candidates for the standardization of transactions conducted on ETP and cleared through the CCP, recognizing that improving governance from the implementation of IRS and OIS transactions is a key concern of Bank Indonesia.

Development of the money market is also aimed at developing short-term securities instruments. This initially involves strengthening the regulatory framework by issuing provisions on money markets, financing instruments such as: certificates of deposit (NCD); commercial securities (SBK); and retail money market instruments.39, 40 These efforts are to be continuously encouraged to provide alternative sources of short-term financing in the money

38 The term ‘systematic internaliser’ refers to banks that provide certain facilities used

in conducting transactions on the Money Market and Foreign Exchange Market in

their accounts with Service Users (as regulated by PBI No.21/5/PBI/2019 and PADG

No. 21/20/PADG/2019). Technically, a systematic internaliser is an electronic system

owned by a bank to facilitate instrument transactions in the money market and

foreign exchange market between banks and their customers.

39 PBI No.19/2/PBI/2017 concerning Certificate of Deposit Transactions in the Money

Market.

40 PBI No.19/9/PBI/2017 concerning the Issuance and Transactions of Commercial

Securities (SBK) in the Money Market.

104 CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020

market and to manage Rupiah liquidity for market players. Periodic and measured evaluations will be continuously carried out to take into account various concerns over the market ecosystem that hinders the development of short-term securities. The main focus of the development of NCD and SBK instruments is achieved through interlinking with financial market infrastructure, so that the electronification of transactions is followed by direct processing of transaction settlements and recording at the central custodian. The harmonization of regulations with the relevant authorities is undertaken to support tax clarity and the development of an investor base, such as mutual funds. Besides that, the licensing and registration processes are also made easier through e-licensing and e-registration to create a fast, efficient and transparent process while paying attention to aspects of governance and the principle of prudence.

In the foreign exchange market, development is focused on exchange rate derivative instruments to support Bank Indonesia’s efforts to stabilize the Rupiah exchange rate. Development of the foreign exchange market is focused on Domestic Non-Deliverable Forward (DNDF) and Local Currency Settlement (LCS) instruments as well as other derivative transactions. This development is focused on instruments and standardization, strengthening benchmark rates and secondary market prices, broadening the base of market players and strengthening coordination and collaboration with stakeholders. Efforts to develop these instruments are also intended to support stabilization of the Rupiah exchange rate. The development of the DNDF has made a positive contribution to the foreign exchange market and it may be further strengthened through higher transaction liquidity. DNDF development efforts will be carried out by increasing DNDF supply and demand in the onshore market, and via the standardization of instruments that can be transacted through market operators and cleared through CCP. In addition, the use of standard contracts, through the use of annex credit support, for example, will be pursued.

Bank Indonesia continues to develop the LCS by strengthening and expanding cooperation with new partner countries. The strengthening of LCS cooperation modalities continues to be encouraged,

mainly through the expansion of underlying transactions that not only include trade but also investment; the expansion of instruments that can be used for LCS transactions such as DNDF; and the inclusion of digital cross border payments as part of the underlying LCS transactions. Furthermore, efforts to develop the LCS will be carried out by expanding and strengthening LCS cooperation with new partner countries, especially the Philippines, Korea, India and Saudi Arabia, which are all interested in implementing the LCS with Indonesia. In terms of financial market infrastructure, ETP development for LCS transactions will be accompanied by transaction settlement through multicurrency RTGS and omni channel repositories for granular data and information storage. This development is expected to encourage the use of LCS in the future. The development of LCS is also part of the government's program to support national economic recovery.41 In this regard, Ministries and institutions provide access, facilities, incentives and the acceleration of export-import services for companies that carry out LCS transactions in accordance with the provisions of the applicable laws.

Bank Indonesia is also encouraging the development of other derivative instruments to support risk management to boost the effectiveness of monetary policy transmission. Efforts to increase the liquidity of derivative instruments, whether simple or complex in nature, continue to be carried out to provide alternative hedging for market players, especially companies with exposure to interest rates and exchange rates. In general, it is necessary to strengthen the regulatory framework for derivative transactions so as to minimize the risk of default by implementing the close-out netting mechanism. Strengthening the regulatory framework will also be carried out through coordination with the relevant Ministries/Agencies through the amendment of laws and regulations governing bankruptcy. Strengthening of this regulatory framework is important for the Indonesian financial market to attain netting jurisdiction status. This would support development of risk management in financial market infrastructure, particularly SBNT CCP, as well as increase counterparty limits, thus making it easier to conduct derivative transactions on the domestic money market.

41 Government Regulation (PP) No.23 of 2020 concerning the implementation of the

national economic recovery program.

CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020 105

Money Market Transformation for Development Financing and Risk Management

5.4.

The third initiative of BPPU 2025 is aimed at encouraging new sources of economic financing and risk management. Infrastructure development costs in the 2020-2024 period will be high, up to IDR6,455 trillion, indicating the need for significant support from the private sector to provide development financing.42 To make progress in this regard, money market development policies are aimed at encouraging the development of sources of economic financing and at better risk management. Backed by strong financial market infrastructure, these efforts focus on four main areas, namely: (i) innovation in financing instruments supported by the use of digital technology; (ii) long-term hedging instruments for risk management; (iii) financial literacy education and development of the retail investor base; and iv) strengthening financial market development coordination between Bank Indonesia, OJK and the Ministry of Finance through FK-PPPK, including efforts to harmonize regulations on macroprudential, microprudential and tax policies.

The role of the private sector continues to be encouraged to support development financing. Bank Indonesia supports the steps of the Government and related authorities to increase the role of the private sector in infrastructure financing. One of the steps taken by the Government is to develop blended finance by establishing the Indonesia Sustainable Development Goals One (SDG One) platform through PT. Sarana Multi Infrastruktur (SMI). Besides that, the Government has also provided various tax incentives ranging from tax holidays and tax allowances to lowering tax rates for both economic activities and certain financial instruments. In this regard, Bank Indonesia continues to strengthen coordination

42 Physical infrastructure development in Indonesia in the period 2020-2024 to increase

infrastructure stock from 43% of GDP in 2017 to 50% of GDP in 2024, requires

financing of IDR6,445 trillion (RPJMN, Bappenas 2019). This financing can be met from

the Government (37% of the need), State Owned Enterprises (BUMN) and Regional

Owned Enterprises (BUMD) (21%) and the private sector (42%).

with the Government and the relevant authorities to optimize the role of the financial markets as a source of development financing.

Bank Indonesia encourages innovation in the development of alternative financial instruments for issuers and investors. This is intended to make it easier for investors to be able to choose a financing instrument that is suitable for their needs. One such instrument is asset securitization marketed through Asset Backed Securities Collective Investment Contracts (KIK-EBA) or Participation Letter Asset Backed Securities (EBA-SP). These are suitable for companies wishing to obtain financing from the financial market but who do not want dilution of ownership and an increase in their debt ratio. Greater availability of innovative instruments will offer investment alternatives that are in line with the risk-return tastes of institutional and retail investors. Investors who wish to invest in infrastructure projects with relatively affordable amounts can invest in the Infrastructure Fund Collective Investment Contract (KIK-Dinfra) or Asset Backed Securities KIK (KIK-EBA).

Bank Indonesia encourages the development of financing instruments aimed at promoting sustainable and green finance. Bank Indonesia will continue to be actively involved in developing sustainable and green finance (SGF) instruments, especially pertaining to financial market development that is carried out within the framework of inter-authority cooperation. Bank Indonesia is currently preparing a roadmap and strategic development plan for the development of SGF as a part of innovative financing. Bank Indonesia also supports the steps taken by the Government and OJK, to issue various programs and policies to encourage the development of the SGF instrument. Since 2018, the Government has issued green sukuk three times, currently a relatively attractive instrument for investors. In the private sector, domestic banks have also issued green

106 CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020

financing instruments. To accelerate the development of the SGF, the formation of a national task force will encourage coordination and synergy in the development of the SGF instrument so as to further enhance the development of sustainable financing instruments.

The development of hedging instruments continues to be strengthened to assist risk management. The development of long-term hedging instruments, in the form of cross currency swaps, interest rate swaps and call spread options, is being continued in order to assist market players with hedging and long-term risk management. The development of benchmark rates in the form of JIBOR replacement and LIBOR replacement continues to be carried out in line with credible benchmark reforms. This will have a positive impact on the development of cross currency swap instruments that utilize floating interest rates as part of hedging activities. Meanwhile, the development of the call spread option instrument is focused on efforts to increase flexibility in implementing dynamic hedging, as well as to raise market participants' awareness of this instrument. The development of financial market infrastructure to support increased liquidity of long-term hedging transactions is also carried out through the application of a ‘systematic internalizer’ and electronic trading platform to facilitate price transparency and the ease of conducting transactions.

Bank Indonesia also supports increasing the knowledge and financial literacy of market players through the education and information dissemination process, which is one of the main initiatives of BPPU 2025. Education and dissemination in the context of increasing investor financial literacy is focused on institutions, regulations and various products in financial markets. These entail capacity building at relevant authorities, such as OJK, market player associations and the

banking sector. Other efforts include increasing the number of market players, by outreach activities to state-owned companies, the private sector and other business actors.43 The material covers topics like: instruments and products; infrastructure; treasury certification; and a code of ethics to increase the credibility of market players. In addition, educational activities can be undertaken utilizing internet technology, so that financial literacy programs can reach all levels of society, thereby increasing the retail investor base.

Implementation of the BPPU 2025 money market development strategy is supported by strengthening coordination among authorities. BPPU 2025 is part of the national financial market development program. It is a follow-up and integral part of the national strategy that was prepared in 2018 in the National Strategy for Financial Market Development and Deepening (SN-PPPK). It is a comprehensive policy framework that is the main focus of the Development Financing Coordination Forum through the Financial Markets (FKPPPK). The implementation of BPPU 2025 is supported by strengthened coordination between policy stakeholders, including discussions of several main issues in the financial market, such as: close-out netting; tax issues; fiscal incentives; the harmonization of regulations; and other major priorities for FKPPPK. It is hoped that the strengthening of coordination will provide ideas for a more comprehensive market development policy that will deepen Indonesia's financial market to a level comparable to other financial markets in the region. Coordination is also needed to strengthen financial market infrastructure and to develop development financing instruments in order to support the long-term goal of making Indonesia a high-income developed country by 2045.

43 Outreach to BUMN Companies is carried out in collaboration with the Ministry of

BUMN to implement the BUMN Hedging SOP guidelines.

CHAPTER V — ECONOMIC REPORT ON INDONESIA 2020 107