Embed Size (px)

Citation preview

Chapter 9 Risk and Return

Why Study Risk and Return?

Is there a way to invest in stocks to take advantage of the high returns while minimizing the risks?

Investing in portfolios enables investors to manage and control risk while receiving high returns.– A portfolio is a collection of financial assets

2

The General Relationship Between Risk and Return

Risk – The meaning in everyday language: The probability of losing some or all of the money invested

Understanding the risk-return relationship involves:– Define risk in a measurable way– Relate that measurement to a return

3

Portfolio Theory—Modern Thinking about Risk and Return

Portfolio theory defines investment risk in a measurable way and relates it to the expected level of return from an investment– Major impact on practical investing activities

4

The Return on an Investment

The rate of return allows an investment's return to be compared with other investments

One-Year Investments– The return on a debt investment is

k = interest paid / loan amount

– The return on a stock investment is k = [D1 + (P1 – P0)] / P0

5

The Expected Return

The expected return on stock is the return investors feel is most likely to occur based on current information– Anticipated return based on the dividends

expected as well as the future expected price

6

The Required Return

The required return on a stock is the minimum rate at which investors will purchase or hold a stock based on their perceptions of its risk

7

Risk—A Preliminary Definition

A preliminary definition of investment risk is the probability that return will be less than expected

Feelings About Risk– Most people have negative feelings about

bearing risk: Risk Aversion– Most people see a trade-off between risk and return– Higher risk investments must offer higher expected

returns to be acceptable

8

Review of the Concept of a Random Variable

In statistics, a random variable is the outcome of a chance process and has a probability distribution– Discrete variables can take only specific

variables– Continuous variables can take any value

within a specified range

9

Review of the Concept of a Random Variable

The Mean or Expected Value– The most likely outcome for the random

variable

For symmetrical probability distributions, the mean is the center of the distribution.

Statistically it is the weighted average of all possible outcomes

10

n

i ii=1

X = XP X

Review of the Concept of a Random Variable

Variance and Standard Deviation– Variability relates to how far a typical

observation of the variable is likely to deviate from the mean

– The standard deviation gives an indication of how far from the mean a typical observation is likely to fall

11

Review of the Concept of a Random Variable

Variance and Standard Deviation– Variance

12

n 22

x i ii=1

Var X X X P X

n 2

X x i ii=1

SD X X P X

Variance is the average squared deviation from the mean

Standard deviation

Concept Connection Example 9-1 Discrete Probability Distributions

13

1.0000

0.06254

0.25003

0.37502

0.25001

0.06250

P(X)X

The mean of this distribution is 2, since it is a

symmetrical distribution.

If you toss a coin four times, what is the chance of getting x heads?

Figure 9-1 Discrete Probability Distribution

14

Concept Connection Example 9-2 Calculating the Mean of a Discrete Distribution

15

Concept Connection Example 9-3 Variance and Standard Deviation

16

17

Review of the Concept of a Random Variable

The Coefficient of Variation– A relative measure of variation — the ratio of the

standard deviation of a distribution to its mean

CV = Standard Deviation Mean

XCV X

Review of the Concept of a Random Variable

Continuous Random Variable– Can take on any numerical value within

some range– The probability of an actual outcome

involves falling within a range of values rather than being an exact amount

18

Figure 9-2 Probability Distribution for a Continuous Random Variable

19

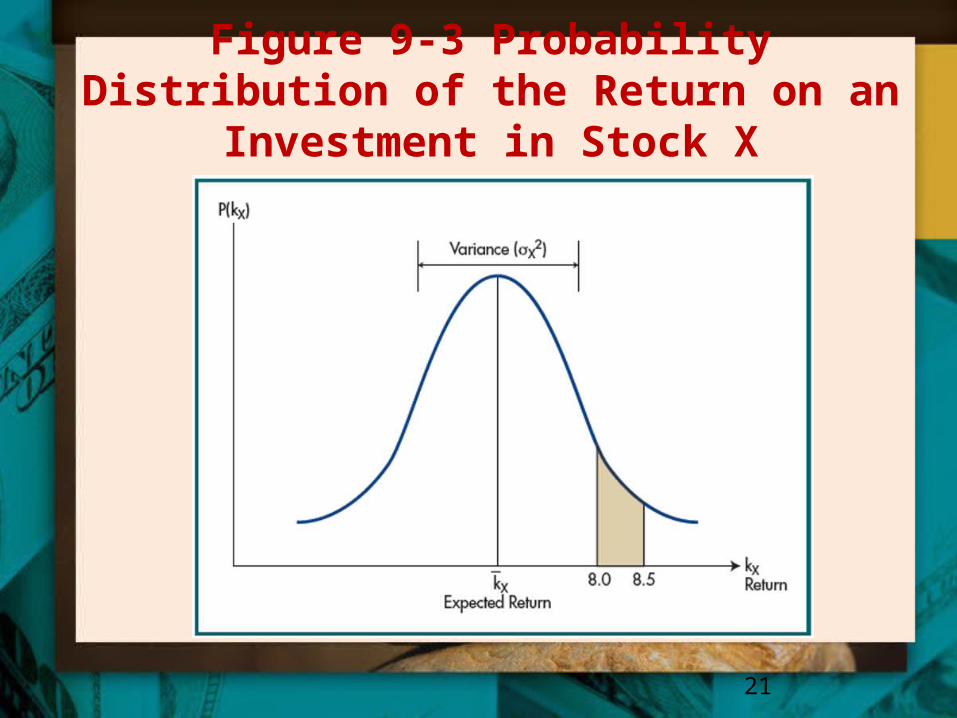

The Return on a Stock Investment as a Random Variable

Return is influenced by stock price and dividends

Return is a continuous random variable

The mean of the distribution of returns is the expected return

The variance and standard deviation show how likely an actual return will be some distance from the expected value

20

Figure 9-3 Probability Distribution of the Return on an Investment in Stock X

21

Figure 9-4 Probability Distributions With Large and Small Variances

22

Risk Redefined as Variability

In portfolio theory, risk is variability as measured by variance or standard deviation

A risky stock has a high probability of earning a return that differs significantly from the mean of the distribution

A low-risk stock is more likely to earn a return similar to the expected return

In practical terms risk is the probability that return will be less than expected

23

Figure 9-5 Investment Risk Viewed as Variability of Return Over Time

24

Both stocks have the same expected return, the high risk stock has a greater variability in return over time.

Risk Aversion

Risk aversion means investors prefer lower risk when expected returns are equal

When expected returns are not equal the choice of investment depends on the investor's tolerance for risk

25

Figure 9-6 Risk Aversion

26

Concept Connection Example 9-4 Evaluating Stand-Alone Risk

27

Harold will invest in one of two companies: Evanston Water Inc. (a public utility) Astro Tech Corp. (a high-tech company).

Public utilities are low-risk - regulated monopolies

High tech firms are high-risk - new ideas can be very successful or fail completely

Harold has made a discrete estimate of the probability distribution of returns for each stock:

Concept Connection Example 9-4 Evaluating Stand-Alone Risk

28

Evaluate Harold's options in terms of the statistical concepts of risk and return.

Concept Connection Example 9-4 Evaluating Stand-Alone Risk

29

First calculate the expected return for each stock.

Next calculate the variance and standard deviation of the return on each stock:

Concept Connection Example 9-4 Evaluating Stand-Alone Risk

30

Concept Connection Example 9-4 Evaluating Stand-Alone Risk

31

Finally, calculate the coefficient of variation for each stock’s return.

Example 9-4 Discussion

Which stock should Harold choose – Astro is better on expected return but

Evanston wins on risk

Consider– Worst cases and Best cases– How variable is each return around its mean– Does a picture (next slide) help?– Which would you choose

Is it likely that Harold’s choice would be influenced by his age and/or wealth?

Concept Connection Example 9-4 Evaluating Stand-Alone Risk

33

Continuous approximations of the two distributions are plotted as follows:

Decomposing Risk—Systematic and Unsystematic Risk

Movement in Return as Risk– Total up and down movement in a stock's

return is the total risk inherent in the stock

Separate Movement/Risk into Two Parts– Market (systematic) risk – Business-specific (unsystematic) risk

34

Defining Market and Business-Specific Risk

Risk is Movement in Return

Components of Risk – Market Risk

Movement caused by things that influence all stocks: political news, inflation, interest rates, war, etc.

– Business-Specific Risk Movement caused by things that influence particular firms and/or industries: labor unrest, weather, technology, key executives

Total Risk = Market Risk + Business-Specific Risk

35

PortfoliosA portfolio is the collection of investment assets held by an investor

Portfolios have their own risks and returns

A portfolio’s return is simply the weighted average of the returns of the stocks in it– Easy to calculate

A portfolio’s risk is the standard deviation of the probability distribution of its return– Depends on risks of stocks in portfolio, but...– Very complex and difficult to calculate/measure

36

PortfoliosGoal of the Investor/Portfolio Owner is to capture the high average returns of stocks while avoiding as much of their risk as possible– Done by constructing diversified

portfolios

Investors are concerned only with how stocks impact portfolio performance, – not with stand-alone risk

37

Diversification—How Portfolio Risk Is Affected When Stocks Are Added

Diversification - adding different (diverse) stocks to a portfolio

Business-Specific Risk and Diversification– Business Specific risk: Random events– Good and Bad effects wash out in large portfolio

Business-Specific Risk is said to be “Diversified Away” in a well-diversified portfolio – – Portfolio Theory assumes it is gone

38

Diversifying to Reduce Market (Systematic) Risk

Market risk is caused by events that affect all stocks– Reduced but not eliminated by

diversifying with stocks that do not move together

Not perfectly positively correlated with the market

– Market risk in a portfolio depends on the timing of variations in individual returns (next slide)

39

Figure 9-7 Risk In and Out of a Portfolio

40

Portfolio Theory and the Small Investor

The Importance of Market Risk– Modern portfolio theory assumes

business risk is diversified awayLarge, diversified portfolio

For the small investor with a limited portfolio the theory’s results may not apply

41

Measuring Market RiskThe Concept of Beta

Market risk is crucial – It’s all that’s left because Business-Specific risk

is diversified away– The theory needs a way to measure market risk

for individual stocks

In the financial world, a stock’s “Beta” is a widely accepted measure of its risk– Beta measures the variation in a stock’s return

that accompanies variation in the market's return

42

Measuring Market RiskThe Concept of Beta

Developing Beta– Determine the historical relationship between a

stock's return and the return on the market

Regress stock’s return against return on an index such as the S&P 500

Projecting Returns with Beta– Knowing a stock's Beta enables us to estimate

changes in its return given changes in the market's return

43

Figure 9-8 The Determination of Beta

44

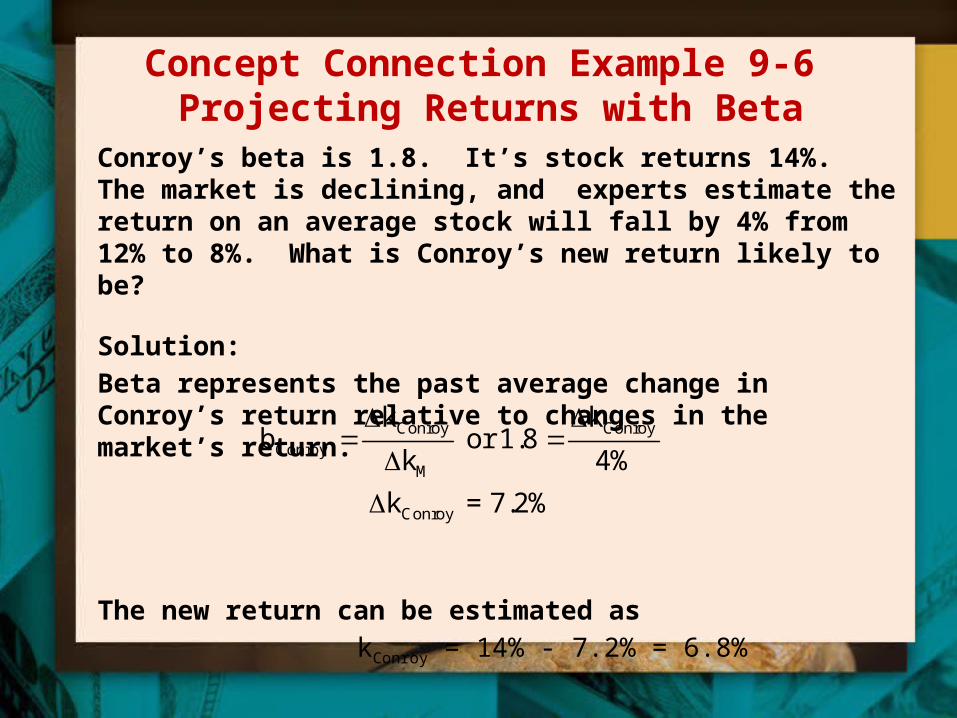

Concept Connection Example 9-6 Projecting Returns with Beta

Conroy’s beta is 1.8. It’s stock returns 14%. The market is declining, and experts estimate the return on an average stock will fall by 4% from 12% to 8%. What is Conroy’s new return likely to be?

Solution:

Beta represents the past average change in Conroy’s return relative to changes in the market’s return.

The new return can be estimated as

kConroy = 14% - 7.2% = 6.8%

Conroy ConroyConroy

M

Conroy

k kb or 1.8

k 4%

k = 7.2%

Measuring Market RiskThe Concept of Beta

Betas are developed from historical data– Not accurate if a fundamental change in the firm or

business environment has occurred– Beta > 1.0 -- the stock moves more than the market– Beta < 1.0 -- the stock moves less than the market– Beta < 0 -- the stock moves against the market

Beta for a Portfolio– The weighted average of the betas of the individual

stocks within the portfolio Weighted by $ invested

46

Using Beta The Capital Asset Pricing Model CAPM)

CAPM attempts to explain how stock prices are set

CAPM's Approach– People won't invest in a stock unless its

expected return is at least equal to their required return for that stock

– CAPM attempts to quantify how required returns are determined

– The stock’s value (price) is estimated based on CAPM’s required return for that stock

47

Using Beta The Capital Asset Pricing Model (CAPM)

Rates of Return, The Risk-Free Rate and Risk Premiums – The current return on the market is kM

– The risk-free rate (kRF) – no chance of receiving less than expected

Investing in any other asset is risky – Investors require a “risk premium” of additional

return over kRF when there is risk

48

The CAPM’s Security Market Line (SML)

The SML proposes that required rates of return are determined by:

49

The Market Risk Premium is (kM – kRF)The Risk Premium for Stock X

The beta for Stock X times the market risk premium In the CAPM a stock’s risk premium is determined only by the stock's market risk as measured by its beta

X RF M RF X

Market Risk Premium

Stock X's Risk Premium

k k k k b

Figure 9-9 The Security Market Line

50

The Security Market Line (SML)

Valuation Using Risk-Return– Use the SML to calculate a required rate

of return for a stock– Use that return in the Gordon model to

calculate a price

51

Concept Connection Example 9-10Valuing (Pricing) a Stock with CAPM

Kelvin paid an annual dividend of $1.50 recently, and is expected to grow at 7% indefinitely.

T- bills yield 6%, an average stock yields 10%. Kelvin is a volatile stock. Its return moves about

twice as much as the average stock in response to political and economic changes. What should Kelvin sell for today?

Concept Connection Example 9-10Valuing (Pricing) a Stock with CAPM

The required rate of return using the SML is:

kKelvin = 6 + (10 – 6)2.0 = 14%

Substituting this along with the 7% growth rate into the Gordon model yields the estimated price:

00

D 1 g $1.5 1.07P $22.93

k g .14 .07

The Security Market Line (SML)

The Impact of Management Decisions on Stock Prices

Management decisions can influence a stock's beta as well as future growth rates An SML approach to valuation may be relevant for policy decisions Recall that management’s goal is generally to maximize stock price

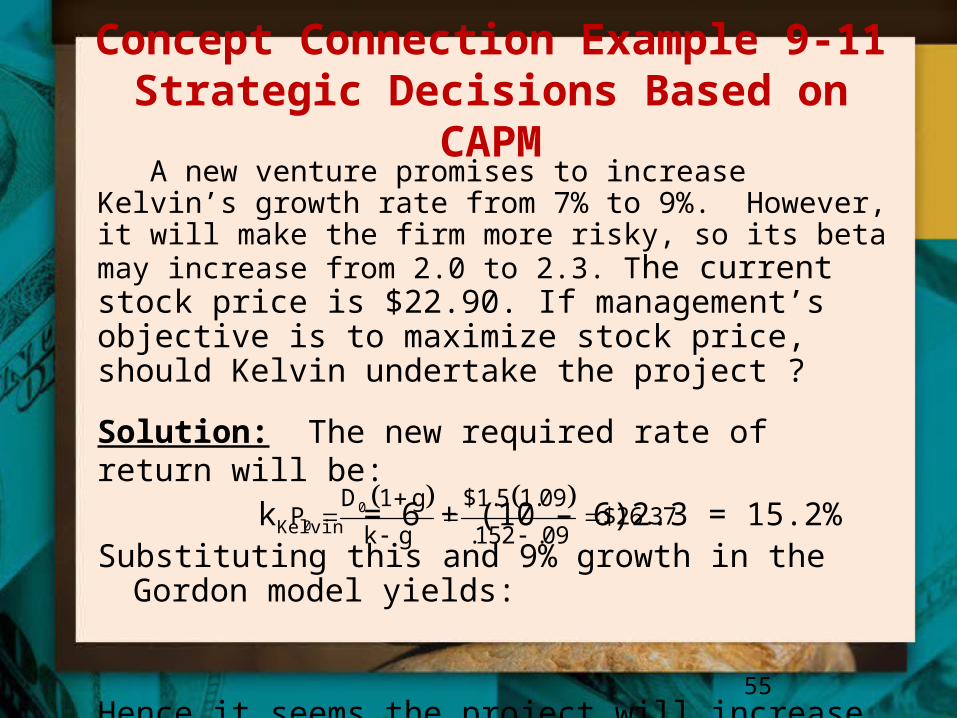

Concept Connection Example 9-11 Strategic Decisions Based on CAPM

55

A new venture promises to increase Kelvin’s growth rate from 7% to 9%. However, it will make the firm more risky, so its beta may increase from 2.0 to 2.3. The current stock price is $22.90. If management’s objective is to maximize stock price, should Kelvin undertake the project ?

Solution: The new required rate of return will be: kKelvin = 6 + (10 – 6)2.3 = 15.2%

Substituting this and 9% growth in the Gordon model yields:

Hence it seems the project will increase the stock’s price helping to achieve management’s goals.

00

D 1 g $1.5 1.09P $26.37

k g .152 .09

The SML – Adjusting to Changes

A change in the risk-free rate– Changes in the risk-free rate cause parallel

shifts in the SML

A change in risk aversion– Attitudes toward risk are reflected in the

slope of the SML (kM – kRF) Changes cause rotations of the SML around its vertical intercept at kRF

56

Figure 9-10 A Shift in the Security Market Line to Accommodate an Increase in the Risk-Free Rate

57

Figure 9-11 A Rotation of the Security Market Line to Accommodate an Increase in Risk Aversion

58

The Validity and Acceptance of the CAPM and its SML

CAPM is an abstraction of reality designed to help make predictions– Its simplicity has probably enhanced its

popularity

CAPM is not universally accepted– Relevance and usefulness is the subject

of an ongoing debate

59