Embed Size (px)

Citation preview

Challenges in xVA Pricing and Risk

Andrew McClelland, PhDDirector of Quantitative Research

Numerix

Matlab Computational Finance ConferenceNYC 2017

September 28, 2017

Andrew McClelland, Numerix xVA Pricing and Risk 1/13

Presentation Outline

Quick overview of Numerix and why we prioritize xVA

What is xVA? Some intuition for how things come together

Computational di�culties encountered in xVA

Multi-factor hybrid models and American Monte Carlo1

Matlab for complicated exposures modeling and aggregations

1Used when referring to Least-Squares Monte Carlo, a la Longsta� andSchwartz ('01), in the context of exposures calculations.

Andrew McClelland, Numerix xVA Pricing and Risk 2/13

Numerix Overview 1

Numerix2 founded in '96, headquartered in NYC, 250+ employees

It has origins as a pricing & risk library for derivatives

Oriented towards exotic & multi-factor derivatives, eg . PRDCs

Managing risk for exotics is a very complicated process

Requires sophisticated & delicate models, methods, calibrations etc .

2https://www.numerix.com.Andrew McClelland, Numerix xVA Pricing and Risk 3/13

Numerix Overview 1

Numerix3 founded in '96, headquartered in NYC, 250+ employees

It has origins as a pricing & risk library for derivatives

Oriented towards exotic & multi-factor derivatives, eg . PRDCs

Managing risk for exotics is a very complicated process

Requires sophisticated & delicate models, methods, calibrations etc .

3https://www.numerix.com.Andrew McClelland, Numerix xVA Pricing and Risk 3/13

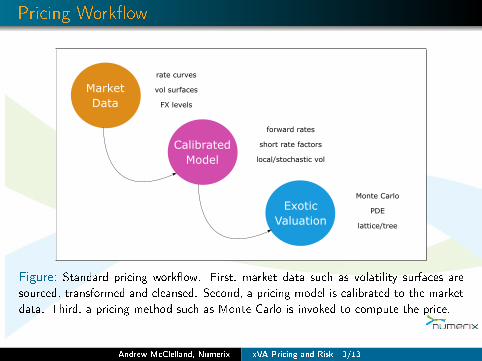

Pricing Work�ow

Market Data

Calibrated Model

ExoticValuation

rate curves

vol surfaces

FX levels

forward rates

short rate factors

local/stochastic vol

Monte Carlo

PDE

lattice/tree

Figure: Standard pricing work�ow. First, market data such as volatility surfaces are

sourced, transformed and cleansed. Second, a pricing model is calibrated to the market

data. Third, a pricing method such as Monte Carlo is invoked to compute the price.

Andrew McClelland, Numerix xVA Pricing and Risk 3/13

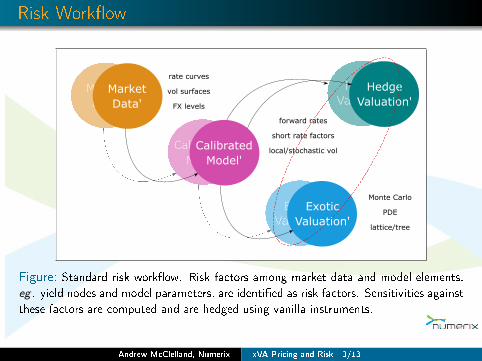

Risk Work�ow

Market Data

Calibrated Model

ExoticValuation

MarketData'

CalibratedModel'

ExoticValuation'

rate curves

vol surfaces

FX levels

forward rates

short rate factors

local/stochastic vol

Monte Carlo

PDE

lattice/tree

Figure: Standard risk work�ow. Risk factors among market data and model elements,

eg . yield nodes and model parameters, are identi�ed as risk factors. Sensitivities against

these factors are computed and are hedged using vanilla instruments.

Andrew McClelland, Numerix xVA Pricing and Risk 3/13

Risk Work�ow

Market Data

Calibrated Model

ExoticValuation

MarketData'

CalibratedModel'

ExoticValuation'

rate curves

vol surfaces

FX levels

forward rates

short rate factors

local/stochastic vol

Monte Carlo

PDE

lattice/tree

HedgeValuation

HedgeValuation'

Figure: Standard risk work�ow. Risk factors among market data and model elements,

eg . yield nodes and model parameters, are identi�ed as risk factors. Sensitivities against

these factors are computed and are hedged using vanilla instruments.

Andrew McClelland, Numerix xVA Pricing and Risk 3/13

Risk Work�ow

Market Data

Calibrated Model

ExoticValuation

MarketData'

CalibratedModel'

ExoticValuation'

rate curves

vol surfaces

FX levels

forward rates

short rate factors

local/stochastic vol

Monte Carlo

PDE

lattice/tree

HedgeValuation

HedgeValuation'

Figure: Standard risk work�ow. Risk factors among market data and model elements,

eg . yield nodes and model parameters, are identi�ed as risk factors. Sensitivities against

these factors are computed and are hedged using vanilla instruments.

Andrew McClelland, Numerix xVA Pricing and Risk 3/13

Numerix Overview 2

After crisis exotics volumes dropped but xVAs, eg . CVA, emerged

Big challenge for banks and managing xVA resembles managing exotics

Nice use case for how our clients use a mix of NX and Matlab

Content should be interesting for this audience also

Sits within larger issue of holistic modeling of trade impact

Andrew McClelland, Numerix xVA Pricing and Risk 4/13

Numerix Overview 2

After crisis exotics volumes dropped but xVAs, eg . CVA, emerged

Big challenge for banks and managing xVA resembles managing exotics

Nice use case for how our clients use a mix of NX and Matlab

Content should be interesting for this audience also

Sits within larger issue of holistic modeling of trade impact

Andrew McClelland, Numerix xVA Pricing and Risk 4/13

Numerix Matlab Interface

Figure: Example of a CVA calculation using the Matlab interface for NX in combination

with native Matlab functionality.

Andrew McClelland, Numerix xVA Pricing and Risk 4/13

Numerix Overview 2

After crisis exotics volumes dropped but xVAs, eg . CVA, emerged

Big challenge for banks and managing xVA resembles managing exotics

Nice use case for how our clients use a mix of NX and Matlab

Content should be interesting for this audience also

Sits within larger issue of holistic modeling of trade impact

Andrew McClelland, Numerix xVA Pricing and Risk 4/13

Numerix Overview 2

After crisis exotics volumes dropped but xVAs, eg . CVA, emerged

Big challenge for banks and managing xVA resembles managing exotics

Nice use case for how our clients use a mix of NX and Matlab

Content should be interesting for this audience also

Sits within larger issue of holistic modeling of trade impact

Andrew McClelland, Numerix xVA Pricing and Risk 4/13

What is xVA?

Traditional valuations involve the risk-neutral valuation formula

Classical Valuation

V (t) = Et

[e−

∫ Tt r(u) duC(T )

]Many ways to derive this formula, equilibrium4, arbitrage5, etc .

Hedging approach6 is a bit restrictive but mimics bank practice

Classical hedging assumptions ignore certain �frictions�

eg . counterparty credit risk, funding spreads & collateral

4eg . Cox, Ingersol and Ross ('85).5eg . Harrison and Kreps ('79).6eg . Black and Scholes ('73) or Burgard and Kjaer ('11).

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

What is xVA?

Traditional valuations involve the risk-neutral valuation formula

Classical Valuation

V (t) = Et

[e−

∫ Tt r(u) duC(T )

]Many ways to derive this formula, equilibrium7, arbitrage8, etc .

Hedging approach9 is a bit restrictive but mimics bank practice

Classical hedging assumptions ignore certain �frictions�

eg . counterparty credit risk, funding spreads & collateral

7eg . Cox, Ingersol and Ross ('85).8eg . Harrison and Kreps ('79).9eg . Black and Scholes ('73) or Burgard and Kjaer ('11).

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

Valuations via Hedging Arguments

Swap HedgeCounterparty

CDS HedgeCounterparty

Bank ClientStructured Swap

Risk-Free Funding Funding Account

Vanilla Swaps

CustodianClearing House

Figure: Basic considerations within hedging derivation of valuation rule.

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

What is xVA?

Traditional valuations involve the risk-neutral valuation formula

Classical Valuation

V (t) = Et

[e−

∫ Tt r(u) duC(T )

]Many ways to derive this formula, equilibrium10, arbitrage11, etc .

Hedging approach12 is a bit restrictive but mimics bank practice

Classical hedging assumptions ignore certain �frictions�

eg . counterparty credit risk, funding spreads & collateral

10eg . Cox, Ingersol and Ross ('85).11eg . Harrison and Kreps ('79).12eg . Black and Scholes ('73) or Burgard and Kjaer ('11).

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

Valuations via Hedging Arguments

Swap HedgeCounterparty

CDS HedgeCounterparty

Bank ClientStructured Swap

Risk-Free Funding Funding Account

Vanilla Swaps

CustodianClearing House

Figure: Modern considerations within hedging derivation of valuation rule, including

counterparty credit risk, funding costs, initial margin requirements.

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

Valuations via Hedging Arguments

Swap HedgeCounterparty

CDS HedgeCounterparty

Bank ClientStructured Swap

Treasury Funding Funding Account

Vanilla Swaps

CustodianClearing House

Figure: Modern considerations within hedging derivation of valuation rule, including

counterparty credit risk, funding costs, initial margin requirements.

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

Valuations via Hedging Arguments

Swap HedgeCounterparty

CDS HedgeCounterparty

Bank ClientStructured Swap

Treasury Funding Funding Account

Vanilla Swaps

CDS Contracts

CustodianClearing House

Figure: Modern considerations within hedging derivation of valuation rule, including

counterparty credit risk, funding costs, initial margin requirements.

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

Valuations via Hedging Arguments

Swap HedgeCounterparty

CDS HedgeCounterparty

Bank ClientStructured Swap

Treasury Funding Funding Account

Vanilla Swaps

CDS Contracts

CustodianClearing House

Initia

l Marg

in

Figure: Modern considerations within hedging derivation of valuation rule, including

counterparty credit risk, funding costs, initial margin requirements.

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

Valuations via Hedging Arguments

Swap HedgeCounterparty

CDS HedgeCounterparty

Bank ClientStructured Swap

Treasury Funding Funding Account

Vanilla Swaps

CDS Contracts

CustodianClearing House

Initia

l Marg

in

Figure: Modern considerations within hedging derivation of valuation rule, including

counterparty credit risk, funding costs, initial margin requirements.

Andrew McClelland, Numerix xVA Pricing and Risk 5/13

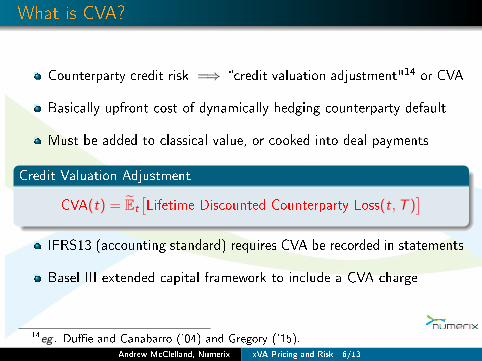

What is CVA?

Counterparty credit risk =⇒ �credit valuation adjustment"13 or CVA

Basically upfront cost of dynamically hedging counterparty default

Must be added to classical value, or cooked into deal payments

Credit Valuation Adjustment

CVA(t) = Et

[Lifetime Discounted Counterparty Loss(t,T )

]IFRS13 (accounting standard) requires CVA be recorded in statements

Basel III extended capital framework to include a CVA charge

13eg . Du�e and Canabarro ('04) and Gregory ('15).Andrew McClelland, Numerix xVA Pricing and Risk 6/13

What is CVA?

Counterparty credit risk =⇒ �credit valuation adjustment"14 or CVA

Basically upfront cost of dynamically hedging counterparty default

Must be added to classical value, or cooked into deal payments

Credit Valuation Adjustment

CVA(t) = Et

[Lifetime Discounted Counterparty Loss(t,T )

]IFRS13 (accounting standard) requires CVA be recorded in statements

Basel III extended capital framework to include a CVA charge

14eg . Du�e and Canabarro ('04) and Gregory ('15).Andrew McClelland, Numerix xVA Pricing and Risk 6/13

What is CVA?

Counterparty credit risk =⇒ �credit valuation adjustment"15 or CVA

Basically upfront cost of dynamically hedging counterparty default

Must be added to classical value, or cooked into deal payments

Credit Valuation Adjustment

CVA(t) = Et

[∫ T

tDiscounted Counterparty Loss(s) ds

]IFRS13 (accounting standard) requires CVA be recorded in statements

Basel III extended capital framework to include a CVA charge

15eg . Du�e and Canabarro ('04) and Gregory ('15).Andrew McClelland, Numerix xVA Pricing and Risk 6/13

What is CVA?

Counterparty credit risk =⇒ �credit valuation adjustment"16 or CVA

Basically upfront cost of dynamically hedging counterparty default

Must be added to classical value, or cooked into deal payments

Credit Valuation Adjustment

CVA(t) = Et

[∫ T

te−

∫ st r(u) duλ(s)(V (s))+ ds

]IFRS13 (accounting standard) requires CVA be recorded in statements

Basel III extended capital framework to include a CVA charge

16eg . Du�e and Canabarro ('04) and Gregory ('15).Andrew McClelland, Numerix xVA Pricing and Risk 6/13

What is CVA?

Counterparty credit risk =⇒ �credit valuation adjustment"17 or CVA

Basically upfront cost of dynamically hedging counterparty default

Must be added to classical value, or cooked into deal payments

Credit Valuation Adjustment

CVA(t) = Et

[∫ T

te−

∫ st r(u) duλ(s)(V (s))+ ds

]IFRS13 (accounting standard) requires CVA be recorded in statements

Basel III extended capital framework to include a CVA charge

17eg . Du�e and Canabarro ('04) and Gregory ('15).Andrew McClelland, Numerix xVA Pricing and Risk 6/13

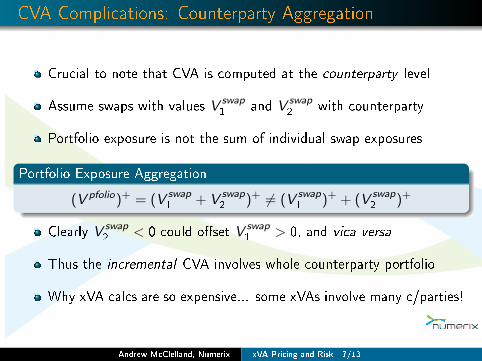

CVA Complications: Counterparty Aggregation

Crucial to note that CVA is computed at the counterparty level

Assume swaps with values V swap1

and V swap2

with counterparty

Portfolio exposure is not the sum of individual swap exposures

Portfolio Exposure Aggregation

(V pfolio)+ = (V swap1

+ V swap2

)+ 6= (V swap1

)+ + (V swap2

)+

Clearly V swap2

< 0 could o�set V swap1

> 0, and vica versa

Thus the incremental CVA involves whole counterparty portfolio

Why xVA calcs are so expensive... some xVAs involve many c/parties!

Andrew McClelland, Numerix xVA Pricing and Risk 7/13

A Practical CVA Computation

Evaluate the CVA formula via discretization and Monte Carlo

Use p = 1, . . . ,P paths and i = 0, · · · ,T timesteps

CVA Calculation

CVA(t0) =1

P

T∑i=1

P∑p=1

λp(si )e−

∫ sit rp(u) du(Vp(si ))+ ∆si

1 Simulate paths state variables Xp,i , eg . rates, hazards, FX

2 Revalue portfolio along all paths V pfoliop,i = V swap

1,p,i + · · ·

3 Evaluate (Vp,i )+, weight by discount factors & hazards and aggregate

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

A Practical CVA Computation

Evaluate the CVA formula via discretization and Monte Carlo

Use p = 1, . . . ,P paths and i = 0, · · · ,T timesteps

CVA Calculation

CVA(t0) =1

P

T∑i=1

P∑p=1

λp(si )e−

∫ sit rp(u) du(Vp(si ))+ ∆si

1 Simulate paths state variables Xp,i , eg . rates, hazards, FX

2 Revalue portfolio along all paths V pfoliop,i = V swap

1,p,i + · · ·

3 Evaluate (Vp,i )+, weight by discount factors & hazards and aggregate

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

CVA Simulation Steps

0 1 2 3 4 5 6 7 8 9 10

Horizon (Yrs)

-0.03

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06Short Rate Trajectories

Figure: Example of simulations involved in a CVA calculation. Portfolio consists of a

5Y swap and a 10Y swap.

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

CVA Simulation Steps

0 1 2 3 4 5 6 7 8 9 10

Horizon (Yrs)

-0.3

-0.2

-0.1

0

0.1

0.2

0.310Y Swap Trajectories

Figure: Example of simulations involved in a CVA calculation. Portfolio consists of a

5Y swap and a 10Y swap.

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

CVA Simulation Steps

0 1 2 3 4 5 6 7 8 9 10

Horizon (Yrs)

-0.15

-0.1

-0.05

0

0.05

0.15Y Swap Trajectories

Figure: Example of simulations involved in a CVA calculation. Portfolio consists of a

5Y swap and a 10Y swap.

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

CVA Simulation Steps

0 1 2 3 4 5 6 7 8 9 10

Horizon (Yrs)

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3Portfolio Trajectories

Figure: Example of simulations involved in a CVA calculation. Portfolio consists of a

5Y swap and a 10Y swap.

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

CVA Simulation Steps

0 1 2 3 4 5 6 7 8 9 10

Horizon (Yrs)

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3Positive Portfolio Trajectories

Figure: Example of simulations involved in a CVA calculation. Portfolio consists of a

5Y swap and a 10Y swap.

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

CVA Simulation Steps

0 1 2 3 4 5 6 7 8 9 10

Horizon (Yrs)

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3Positive Portfolio Trajectories

Figure: Example of simulations involved in a CVA calculation. Portfolio consists of a

5Y swap and a 10Y swap.

Andrew McClelland, Numerix xVA Pricing and Risk 8/13

Main Challenges in CVA

Portfolios can span multiple risk factors, eg . swaps in many CCYs

Building models is di�cult and building hybrid models is more so

Require correlation structures for (latent) variables & joint calibration

Computing Vp,i can be an O(P2) problem for exotics

In practice this can be extremely expensive and we try to avoid

American MC (AMC) is a powerful regression-based O(P) algorithm

Andrew McClelland, Numerix xVA Pricing and Risk 9/13

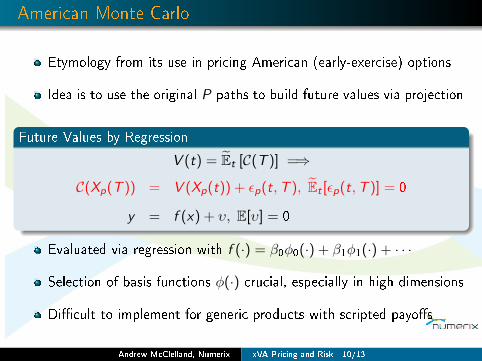

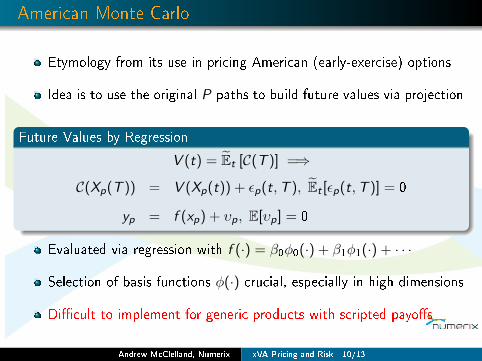

American Monte Carlo

Etymology from its use in pricing American (early-exercise) options

Idea is to use the original P paths to build future values via projection

Future Values by Regression

V (t) = Et [C(T )] =⇒

C(X (T )) = V (X (t)) + ε(t,T ), Et [ε(t,T )] = 0

y = f (x) + υ, E[υ] = 0

Evaluated via regression with f (·) = β0φ0(·) + β1φ1(·) + · · ·

Selection of basis functions φ(·) crucial, especially in high dimensions

Di�cult to implement for generic products with scripted payo�s

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

American Monte Carlo

Etymology from its use in pricing American (early-exercise) options

Idea is to use the original P paths to build future values via projection

Future Values by Regression

V (t) = Et [C(T )] =⇒

C(X (T )) = V (X (t)) + ε(t,T ), Et [ε(t,T )] = 0

y = f (x) + υ, E[υ] = 0

Evaluated via regression with f (·) = β0φ0(·) + β1φ1(·) + · · ·

Selection of basis functions φ(·) crucial, especially in high dimensions

Di�cult to implement for generic products with scripted payo�s

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

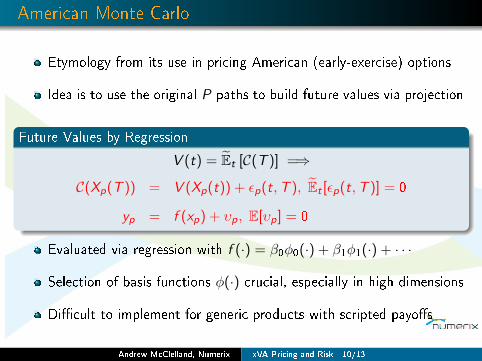

American Monte Carlo

Etymology from its use in pricing American (early-exercise) options

Idea is to use the original P paths to build future values via projection

Future Values by Regression

V (t) = Et [C(T )] =⇒

C(Xp(T )) = V (Xp(t)) + εp(t,T ), Et [εp(t,T )] = 0

y = f (x) + υ, E[υ] = 0

Evaluated via regression with f (·) = β0φ0(·) + β1φ1(·) + · · ·

Selection of basis functions φ(·) crucial, especially in high dimensions

Di�cult to implement for generic products with scripted payo�s

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

American Monte Carlo

Etymology from its use in pricing American (early-exercise) options

Idea is to use the original P paths to build future values via projection

Future Values by Regression

V (t) = Et [C(T )] =⇒

C(Xp(T )) = V (Xp(t)) + εp(t,T ), Et [εp(t,T )] = 0

y = f (x) + υ, E[υ] = 0

Evaluated via regression with f (·) = β0φ0(·) + β1φ1(·) + · · ·

Selection of basis functions φ(·) crucial, especially in high dimensions

Di�cult to implement for generic products with scripted payo�s

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

American Monte Carlo

Etymology from its use in pricing American (early-exercise) options

Idea is to use the original P paths to build future values via projection

Future Values by Regression

V (t) = Et [C(T )] =⇒

C(Xp(T )) = V (Xp(t)) + εp(t,T ), Et [εp(t,T )] = 0

yp = f (xp) + υp, E[υp] = 0

Evaluated via regression with f (·) = β0φ0(·) + β1φ1(·) + · · ·

Selection of basis functions φ(·) crucial, especially in high dimensions

Di�cult to implement for generic products with scripted payo�s

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

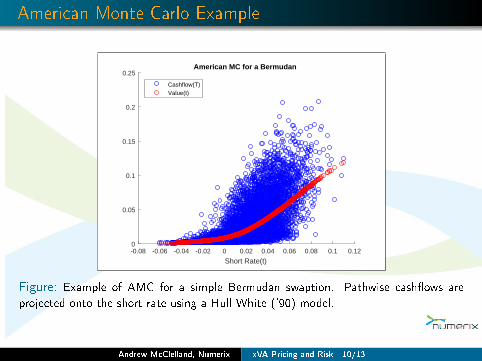

American Monte Carlo Example

-0.08 -0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08 0.1 0.12

Short Rate(t)

0

0.05

0.1

0.15

0.2

0.25American MC for a Bermudan

Cashflow(T)Value(t)

Figure: Example of AMC for a simple Bermudan swaption. Pathwise cash�ows are

projected onto the short rate using a Hull White ('90) model.

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

American Monte Carlo

Etymology from its use in pricing American (early-exercise) options

Idea is to use the original P paths to build future values via projection

Future Values by Regression

V (t) = Et [C(T )] =⇒

C(Xp(T )) = V (Xp(t)) + εp(t,T ), Et [εp(t,T )] = 0

yp = f (xp) + υp, E[υp] = 0

Evaluated via regression with f (·) = β0φ0(·) + β1φ1(·) + · · ·

Selection of basis functions φ(·) crucial, especially in high dimensions

Di�cult to implement for generic products with scripted payo�s

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

General Bermudan Swaption Script

Figure: Example of a Numerix payo� script for a Bermudan swaption. All DISCOUNTING

variables are subjected to a regression as the algorithm works backward in time.

Andrew McClelland, Numerix xVA Pricing and Risk 10/13

Where Does Matlab Come In? 1

Clients using Numerix have their own views on how to aggregate

Instead of writing NX scripts & functions to do the maths use Matlab

Expose intermediate calcs to allow user logic

Many assumptions on counterparty behavior and default correlations

eg . �wrong-way risk" or WWR: exposures correlate with default prob

Subjective and clients want control over default prob trajectories

Andrew McClelland, Numerix xVA Pricing and Risk 11/13

Where Does Matlab Come In? 2

Also complications re. collateral arrangements and margining

Ratings triggers can force lower collateral thresholds and min transfers

Early-terminations as function of market conditions or credit health?

Similarly so for rolling of shorter-term trades

Collateral rehypothecation across counterparties for funding o�sets

Andrew McClelland, Numerix xVA Pricing and Risk 12/13

What Does the Future Hold?

The really di�cult calculations relate to portfolio-level e�ects

Looking for capital impacts (KVA) and initial margin impacts (MVA)

Capital and initial margin requirements are becoming more onerous18

Pricing these and/or optimizing against them is crucial

Also bene�ts to fully tracking cost of collateral transformation

18See eg . Basel FRTB (BCBS365) and Basel-IOSCO (BCBS317).Andrew McClelland, Numerix xVA Pricing and Risk 13/13