Embed Size (px)

Citation preview

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Arbitrage-Free XVA

Agostino CapponiColumbia University

joint work with Maxim Bichuch and Stephan Sturm

Financial Engineering Practitioners Seminars

New York, January 25, 2016

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

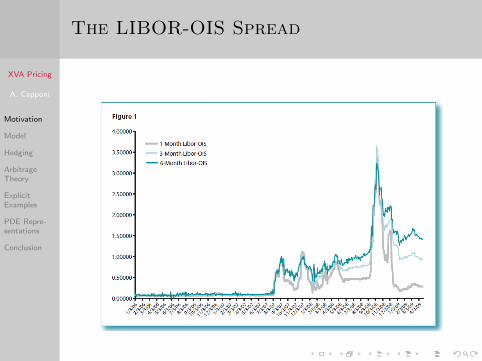

The LIBOR-OIS Spread

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The LIBOR-OIS Spread

Consequences

Widening of spreads is due to counterparty credit riskLIBOR cannot be considered a risk-free rate any longerOne cannot assume the existence of a universal risk-freerate r

Rates at which derivatives traders borrow and lendunsecured cash differHow to price and hedge derivatives in presence of fundingspreads and counterparty risk?

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The LIBOR-OIS Spread

Consequences

Widening of spreads is due to counterparty credit riskLIBOR cannot be considered a risk-free rate any longerOne cannot assume the existence of a universal risk-freerate r

Rates at which derivatives traders borrow and lendunsecured cash differHow to price and hedge derivatives in presence of fundingspreads and counterparty risk?

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

XVA: Motivation and Challenges

Dealers need to account for the total costs of their trades

funding costs: financing the portfolio of liquid securitiesused to replicate the traded positioncollateral costs: funding and retrieving the collateralneeded to secure the deal with the counterpartycloseout costs: losses incurred if a premature liquidationneeds to be executed because the counterparty defaults

Swap quotes offered to clients should reflect the effect ofthese costs, referred to as XVA

Many banks (Barclays, JPM, BoA,...) have introduce XVAdesks

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

XVA: Motivation and Challenges

Dealers need to account for the total costs of their trades

funding costs: financing the portfolio of liquid securitiesused to replicate the traded positioncollateral costs: funding and retrieving the collateralneeded to secure the deal with the counterpartycloseout costs: losses incurred if a premature liquidationneeds to be executed because the counterparty defaults

Swap quotes offered to clients should reflect the effect ofthese costs, referred to as XVA

Many banks (Barclays, JPM, BoA,...) have introduce XVAdesks

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

XVA: Motivation and Challenges

Dealers need to account for the total costs of their trades

funding costs: financing the portfolio of liquid securitiesused to replicate the traded positioncollateral costs: funding and retrieving the collateralneeded to secure the deal with the counterpartycloseout costs: losses incurred if a premature liquidationneeds to be executed because the counterparty defaults

Swap quotes offered to clients should reflect the effect ofthese costs, referred to as XVA

Many banks (Barclays, JPM, BoA,...) have introduce XVAdesks

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

XVA: Motivation and Challenges

Dealers need to account for the total costs of their trades

funding costs: financing the portfolio of liquid securitiesused to replicate the traded positioncollateral costs: funding and retrieving the collateralneeded to secure the deal with the counterpartycloseout costs: losses incurred if a premature liquidationneeds to be executed because the counterparty defaults

Swap quotes offered to clients should reflect the effect ofthese costs, referred to as XVA

Many banks (Barclays, JPM, BoA,...) have introduce XVAdesks

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Related Literature

Practitioner literature: Piterbarg (2010, 2012), Burgard &Kjaer (2010, 2011), Mercurio (2013), Albanese (2015)

(Corporate) Finance literature: Andersen and Duffie(2016), Hull & White (2012, 2013)

Financial Mathematics literature: Bielecki & Rutkowski(2013), Brigo (2014), Crepey (2011, 2013), Crepey,Bielecki and Brigo (2014)

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Main Contributions

Develop a framework to characterize the total valuationadjustment (XVA) of a European style claim

Derive stochastic differential equations tracking thereplicating portfolios of long and short positions in theclaim

Develop explicit representations of XVA and of thecorresponding hedging strategies

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Main Contributions

Develop a framework to characterize the total valuationadjustment (XVA) of a European style claim

Derive stochastic differential equations tracking thereplicating portfolios of long and short positions in theclaim

Develop explicit representations of XVA and of thecorresponding hedging strategies

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Main Contributions

Develop a framework to characterize the total valuationadjustment (XVA) of a European style claim

Derive stochastic differential equations tracking thereplicating portfolios of long and short positions in theclaim

Develop explicit representations of XVA and of thecorresponding hedging strategies

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

The market model (I)

Treasury desk: borrowing and lending at rates r�f , r�f ,respectively

Stock (St): used to the hedge market risk of thetransaction. Trading happens through repo market at ratesr�r , r�r (Duffie (1996))

Risky bonds (P It , PC

t ): underwritten byinvestor/counterparty and used to hedge default risk.Bonds are not purchased/sold via the repo market

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Stock Short-Selling

TraderTreasury Desk

(1)

(6)

Stock Market

(5) (4)

Repo Market

(2)

(3)

r�r

Figure: Security driven repo activity: Solid lines arepurchases/sales, dashed lines borrowing/lending, dotted lines interestdue; blue lines are cash, red lines are stock.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Stock Purchasing

TraderTreasury Desk

(1)

(6)

Stock Market

(2) (3)

Repo Market

(4)

(5)

r�r

Figure: Cash driven repo activity: Solid lines are purchases/sales,dashed lines borrowing/lending, dotted lines interest due; blue linesare cash, red lines are stock.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

The market model (II)

We consider the dynamics

dSt � µSt dt � σSt dWt

dP It � µIP

It dt � P I

t� d1ltτI¤tu

� pµI � hI qPIt dt � P I

t� d$It

dPCt � µCP

Ct dt � PC

t� d1ltτC¤tu

� pµC � hC qPCt dt � PC

t� d$Ct

for independent default times τI , τC with constant defaultintensities hI , hC and martingales $I , $C

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

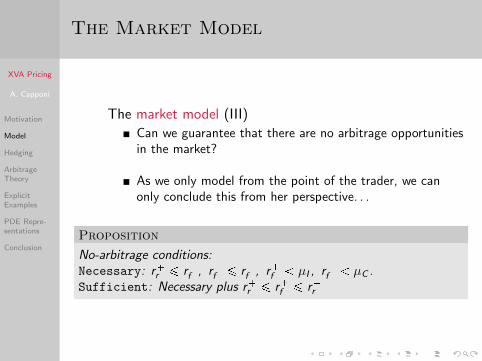

The Market Model

The market model (III)

Can we guarantee that there are no arbitrage opportunitiesin the market?

As we only model from the point of the trader, we canonly conclude this from her perspective. . .

Proposition

No-arbitrage conditions:Necessary: r�r ¤ r�f , r�f ¤ r�f , r�f µI , r�f µC .Sufficient: Necessary plus r�r ¤ r�f ¤ r�r

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

The market model (III)

Can we guarantee that there are no arbitrage opportunitiesin the market?

As we only model from the point of the trader, we canonly conclude this from her perspective. . .

Proposition

No-arbitrage conditions:Necessary: r�r ¤ r�f , r�f ¤ r�f , r�f µI , r�f µC .Sufficient: Necessary plus r�r ¤ r�f ¤ r�r

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

The market model (III)

Can we guarantee that there are no arbitrage opportunitiesin the market?

As we only model from the point of the trader, we canonly conclude this from her perspective. . .

Proposition

No-arbitrage conditions:Necessary: r�r ¤ r�f , r�f ¤ r�f , r�f µI , r�f µC .Sufficient: Necessary plus r�r ¤ r�f ¤ r�r

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

The market model (III)

Can we guarantee that there are no arbitrage opportunitiesin the market?

As we only model from the point of the trader, we canonly conclude this from her perspective. . .

Proposition

No-arbitrage conditions:Necessary: r�r ¤ r�f , r�f ¤ r�f , r�f µI , r�f µC .Sufficient: Necessary plus r�r ¤ r�f ¤ r�r

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

The market model (III)

Can we guarantee that there are no arbitrage opportunitiesin the market?

As we only model from the point of the trader, we canonly conclude this from her perspective. . .

Proposition

No-arbitrage conditions:Necessary: r�r ¤ r�f , r�f ¤ r�f , r�f µI , r�f µC .Sufficient: Necessary plus r�r ¤ r�f ¤ r�r

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

The market model (III)

Can we guarantee that there are no arbitrage opportunitiesin the market?

As we only model from the point of the trader, we canonly conclude this from her perspective. . .

Proposition

No-arbitrage conditions:Necessary: r�r ¤ r�f , r�f ¤ r�f , r�f µI , r�f µC .Sufficient: Necessary plus r�r ¤ r�f ¤ r�r

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Collateralization

Collateral is used to secure the derivatives deal

Collateral is provided in form of cash (80%)

Collateral can be reinvested (rehypothecated) (96%)

The collateral provider receives interests at rate r�c . Thecollateral taker pays interests at rate r�c .

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Collateralization

Collateral is used to secure the derivatives deal

Collateral is provided in form of cash (80%)

Collateral can be reinvested (rehypothecated) (96%)

The collateral provider receives interests at rate r�c . Thecollateral taker pays interests at rate r�c .

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Collateralization

Collateral is used to secure the derivatives deal

Collateral is provided in form of cash (80%)

Collateral can be reinvested (rehypothecated) (96%)

The collateral provider receives interests at rate r�c . Thecollateral taker pays interests at rate r�c .

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Collateralization

Collateral is used to secure the derivatives deal

Collateral is provided in form of cash (80%)

Collateral can be reinvested (rehypothecated) (96%)

The collateral provider receives interests at rate r�c . Thecollateral taker pays interests at rate r�c .

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Collateralization

Collateral is used to secure the derivatives deal

Collateral is provided in form of cash (80%)

Collateral can be reinvested (rehypothecated) (96%)

The collateral provider receives interests at rate r�c . Thecollateral taker pays interests at rate r�c .

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Market Model

TraderTreasury Desk

r�f

r�f

Cash

Stock &Repo Market

Stockr�r r�r

Bond MarketBonds P I , PC

Counterparty

Collateral

r�c r�c

Figure: Solid lines are purchases/sales, dashed linesborrowing/lending, dotted lines interest due; blue lines are cash, redlines stock purchases for cash and black lines bond purchases for cash.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Closeout Payments and Valuation

The closeout value of the claim is decided by a valuationagent (either party or third party) in accordance withmarket practices (ISDA)

The valuation agent determines collateral requirementsand closeout value by calculating the cost-free price of thetransaction

Such a valuation is associated with a publicly knowninterest rate rD

We can then introduce a valuation measure Q underwhich rD-discounted prices are Q martingales.

The XVA will be computed under Q

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Closeout Payments and Valuation

The closeout value of the claim is decided by a valuationagent (either party or third party) in accordance withmarket practices (ISDA)

The valuation agent determines collateral requirementsand closeout value by calculating the cost-free price of thetransaction

Such a valuation is associated with a publicly knowninterest rate rD

We can then introduce a valuation measure Q underwhich rD-discounted prices are Q martingales.

The XVA will be computed under Q

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Closeout Payments and Valuation

The closeout value of the claim is decided by a valuationagent (either party or third party) in accordance withmarket practices (ISDA)

The valuation agent determines collateral requirementsand closeout value by calculating the cost-free price of thetransaction

Such a valuation is associated with a publicly knowninterest rate rD

We can then introduce a valuation measure Q underwhich rD-discounted prices are Q martingales.

The XVA will be computed under Q

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Closeout Payments and Valuation

The closeout value of the claim is decided by a valuationagent (either party or third party) in accordance withmarket practices (ISDA)

The valuation agent determines collateral requirementsand closeout value by calculating the cost-free price of thetransaction

Such a valuation is associated with a publicly knowninterest rate rD

We can then introduce a valuation measure Q underwhich rD-discounted prices are Q martingales.

The XVA will be computed under Q

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Closeout Payments and Valuation

The closeout value of the claim is decided by a valuationagent (either party or third party) in accordance withmarket practices (ISDA)

The valuation agent determines collateral requirementsand closeout value by calculating the cost-free price of thetransaction

Such a valuation is associated with a publicly knowninterest rate rD

We can then introduce a valuation measure Q underwhich rD-discounted prices are Q martingales.

The XVA will be computed under Q

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

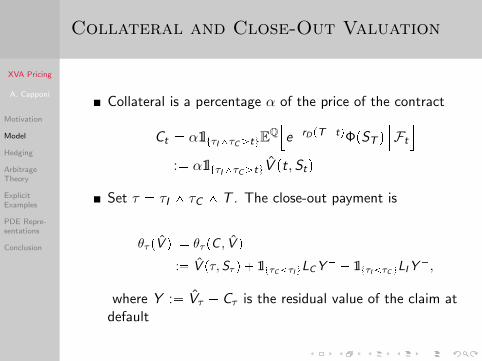

Collateral and Close-Out Valuation

Collateral is a percentage α of the price of the contract

Ct � α1ltτI^τC¡tuEQ�e�rDpT�tqΦpST q

���Ft

�

:� α1ltτI^τC¡tuV pt,Stq

Set τ � τI ^ τC ^ T . The close-out payment is

θτ pV q � θτ pC , V q

:� V pτ,Sτ q � 1ltτC τI uLCY� � 1ltτI τC uLIY

�,

where Y :� Vτ � Cτ is the residual value of the claim atdefault

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Collateral and Close-Out Valuation

Collateral is a percentage α of the price of the contract

Ct � α1ltτI^τC¡tuEQ�e�rDpT�tqΦpST q

���Ft

�

:� α1ltτI^τC¡tuV pt,Stq

Set τ � τI ^ τC ^ T . The close-out payment is

θτ pV q � θτ pC , V q

:� V pτ,Sτ q � 1ltτC τI uLCY� � 1ltτI τC uLIY

�,

where Y :� Vτ � Cτ is the residual value of the claim atdefault

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Wealth Process

It is useful to distinguish between legal and actual wealthprocess

Legal wealth

Vt � ξtSt � ξItPIt � ξCt P

Ct � ψrf

t Brft � ψtB

rrt � Ct ,

Actual wealth

V Ct � ξtSt � ξItP

It � ξCt P

Ct � ψrf

t Brft � ψtB

rrt � Vt � Ct ,

(with B rft funding account B rr

t sec lending account and ξt ,ξIt , ξCt , ψrf

t , ψt number of shares holding)

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Wealth Dynamics

The dynamics of the wealth is given by

dVt ��r�f�ξft B

rft

��� r�f

�ξft B

rft

��� prD � r�r q

�ξtSt

��

� prD � r�r q�ξtSt

��� rDξ

ItP

It � rDξ

Ct P

Ct

dt

� r�c�ψct B

rct

��dt � r�c

�ψct B

rct

��dt

� p� � � qloomoonmartingales

with B rft funding account, B rc

t collateral account, ξt , andψt number of shares in the securities and various accounts

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Arbitrage Pricing

Definition

A price P P R, of a derivative security with terminal payoffξ P σpSt ; t ¤ T q is called trader’s arbitrage-free, if for all γ P Rbuying γ securities for the price γP and hedging in the marketwith an admissible strategy does not create trader’s arbitrage.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Replicating Wealth

V�t pγq: wealth process when replicating the claim

γΦpST q, γ ¡ 0. This means hedging the position afterselling γ securities with terminal payoff ΦpST q.��V�

t pγq�: wealth process when replicating the claim

�γΦpST q, γ ¡ 0. This means hedging the position afterbuying γ securities with terminal payoff ΦpST q.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Replicating Wealth Equation

The BSDEs

$'&'%

�dV�t pγq � f �

�t,V�

t ,Z�t ,Z

I ,�t ,ZC ,�

t ; V�dt

� Z�t dWQt � Z I ,�

t d$I ,Qt � ZC ,�

t d$C ,Qt

V�τ pγq � γ

�θτ pV q1ltτ Tu � ΦpST q1ltτ�Tu

$'&'%

�dV�t pγq � f �

�t,V�

t ,Z�t ,Z

I ,�t ,ZC ,�

t ; V�dt

� Z�t dWQt � Z I ,�

t d$I ,Qt � ZC ,�

t d$C ,Qt

V�τ pγq � γ

�θτ pV q1ltτ Tu � ΦpST q1ltτ�Tu

describe the wealth dynamics for buying/selling γ options

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

No arbitrage

Theorem

Let Φ be a function of polynomial growth. If V�0 ¤ V�

0 , thenall prices in the closed interval rπinf � V�

0 ,V�0 � πsups are free

of trader’s arbitrage.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Definition of XVA

Definition

The seller’s XVA is given as

XVAsellt � V�

t � V pt,Stq

and the buyer’s XVA as

XVAbuyt � V�

t � V pt,Stq.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Extended Piterbarg Model

Extension of Piterbarg’s model

Allow for default of investor and counterpartyDefault risk is hedged by risky bondsMaintain Piterbarg’s assumption of symmetric rates:rf � r�f � r�f , rr � r�r � r�r , rc � r�c � r�cThe total costs of replicating long and short positionscoincide, and XVAsell

t � XVAbuyt

Note: If rf � rr � rc � rD we have no funding costs andrecover the classical CVA/DVA setting

XVAt � DVAt � CVAt

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Extended Piterbarg Model

Extension of Piterbarg’s model

Allow for default of investor and counterpartyDefault risk is hedged by risky bondsMaintain Piterbarg’s assumption of symmetric rates:rf � r�f � r�f , rr � r�r � r�r , rc � r�c � r�cThe total costs of replicating long and short positionscoincide, and XVAsell

t � XVAbuyt

Note: If rf � rr � rc � rD we have no funding costs andrecover the classical CVA/DVA setting

XVAt � DVAt � CVAt

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Extended Piterbarg Model

Proposition (XVA decomposition)

Define η � hQI � hQC � 2rr � rf . On tτ ¡ tu, the total valuationadjustment is given by:

XVAt

Vt

��prr � rf q � αprf � rcq

1 � e�pη�rr qpT�tq

η � rrloooooooooooooooooooooooooomoooooooooooooooooooooooooonreplicating strategy and collateral costs

��rr � rf � hQC

LC

1 � e�pη�rr qpT�tq

η � rr

�p1 � αq1Vt 0

�looooooooooooooooooooooooooooooooomooooooooooooooooooooooooooooooooon

CVA

��rr � rf � hQI

LI

1 � e�pη�rr qpT�tq

η � rr

�p1 � αq1Vt¡0

�loooooooooooooooooooooooooooooooomoooooooooooooooooooooooooooooooon

DVA

:� Adj t

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Hedging Strategies

ξt � Adj t∆t ,

ξIt �XVAt � LI p1 � αqpVtq

�

e�prD�hQI qpT�tq,

ξCt �XVAt � LC p1 � αqpVtq

�

e�prD�hQC qpT�tq.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Extended Piterbarg Model

0.08 0.1 0.12 0.14 0.16 0.18 0.20

10

20

30

40

50

60

70

80

90

100

rf

Pric

e C

ompo

nent

s (%

)

FundingDVA

0.08 0.1 0.12 0.14 0.16 0.18 0.220

30

40

50

60

70

80

rf

Pric

e C

ompo

nent

s (%

)

FundingDVA

Figure: Left graph: hQI � 0.15, hQC � 0.2. Right graph: hQI � 0.5,

hQC � 0.5.

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

The Impact of Differential Rates

What if borrowing and lending rates differ?: r�f � r�f ,r�r � r�r , r�c � r�c

BSDE becomes nonlinear: V�t � V�

t . We have ano-arbitrage interval for prices

But, we can use the semilinear PDE representation v tothe BSDE V for numerical analysis

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

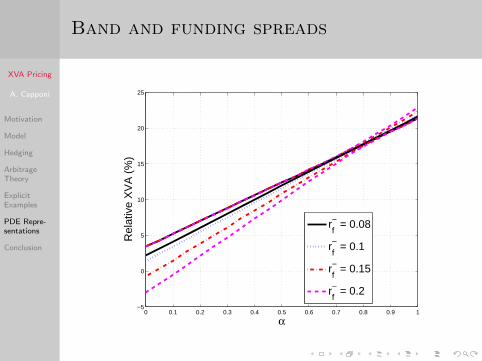

Band and funding spreads

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1−5

0

5

10

15

20

25

α

Rel

ativ

e X

VA

(%

)

rf− = 0.08

rf− = 0.1

rf− = 0.15

rf− = 0.2

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Replicating strategies

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 10.075

0.08

0.085

0.09

0.095

0.1

0.105

0.11

0.115

α

Sto

ck s

hare

s

rf− = 0.08

rf− = 0.1

rf− = 0.15

rf− = 0.2

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 10.025

0.03

0.035

0.04

0.045

0.05

0.055

0.06

0.065

αS

hare

s of

Tra

der

bond

rf− = 0.08

rf− = 0.1

rf− = 0.15

rf− = 0.2

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

Conclusion

Developed an arbitrage-free valuation framework for XVA

Seller’s and buyer’s XVA characterized as the solution of anonlinear BSDEs with random terminal condition

Funding component of XVA is predominant, withDVA/CVA terms becoming material if trader/counterpartyare very risky

The no-arbitrage band widens as funding spreads andcollateral levels increase

XVA Pricing

A. Capponi

Motivation

Model

Hedging

ArbitrageTheory

ExplicitExamples

PDE Repre-sentations

Conclusion

References

M. Bichuch, A. Capponi, and S. Sturm. Arbitrage-free XVA – Conditionallyaccepted in Mathematical Finance.

D. Brigo, A. Capponi, and A. Pallavicini. Arbitrage-free bilateralcounterparty risk valuation under collateralization and application to creditdefault swaps. Mathematical Finance 24, 125–146, 2014. Short version inRisk.

L. Bo, and A. Capponi. Bilateral credit valuation adjustment for largecredit derivatives portfolios. Finance and Stochastics, 18, 431-482, 2014.

A. Capponi. Measuring portfolio counterparty risk. Creditflux, 2014.

A. Capponi. Pricing and Mitigation of Counterparty Credit Exposure. J.P.Fouque, J. Langsam, eds. Handbook of Systemic Risk. CambridgeUniversity Press, Cambridge, 2013.

![Novak Mark [2016] - Az xVA hatasai egy teremtett vilagban](https://img.dokumen.tips/doc/110x75/58740c4f1a28ab6f1d8b79a7/novak-mark-2016-az-xva-hatasai-egy-teremtett-vilagban.jpg)