Embed Size (px)

Citation preview

1.74%

48.3%

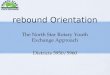

Cautious Rebound in Consumer Auto Loans

C

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

110.0%

cy05 cy06 cy07 cy08 cy09 cy10 cy11 cy12 1st h

Loan to Value Ratio

Prime

Near Prime

Sub Prime

In another sign of

financial institutions

slowly cranking open the

lending spigot, the latest

Loan to Value Ratio data

show a rise, especially

for sub-prime borrowers.

Banks are chasing

after auto loans because

of low repossession

rates and a minimum of

late-payers.

In the heyday of sub-

prime lending, those with

Prime Near Prime Sub Prime

cy05 91.8% 88.3% 98.3%

cy06 92.6% 85.2% 98.6%

cy07 90.4% 85.5% 95.1%

cy08 86.2% 86.7% 84.5%

cy09 85.6% 82.4% 65.3%

cy10 83.7% 80.2% 60.1%

cy11 85.1% 82.5% 66.2%

cy12 1st h 85.5% 82.7% 72.9%

the lowest acceptable FICO score had LV

ratios in the near-100 percent range. As

The recession deepened, banks were requiring larger downpayments

across the board. Even Prime borrowers saw banks expecting upwards

of 20 percent down for an auto loan while Sub-Prime borrowers had to

shell out as much as 40 percent.

In 2011 and the first half of this year, those loan to value ratios have

increased although not nearly to the pre-recession level.

CONTEXT: While the attached data is for (continued next page)

8.81% 15.62%

-3.87% 13.7%

(continued from previous page)

LVs including aftermarket products and leasing, the trend is more important than the actual numbers. The auto industry, to reach any historically reasonable sales levels must have customers from all but the lowest FICO pools. Vehicles continue to improve and consumers have more products to chose from. When combining those two factors, it is no wonder Americans feel they can postpone a new-vehicle purchase. As the Pent Up Demand numbers (Back Page) indicate, the recession-induced delays in would-be buyers is shrinking. In July, for example, the pool of people in the “Pent Up Demand” category was nearly half of the number in the same month a year

August Outlook August is looking fairly good, but not spectacular at

this point. Again, the Vacillation Index (see previous RAS)

is bouncing around like a rubber ball. In the opening half

of August, consumers who were shopping for a new

vehicle changed their minds about buying or not buying

more than 5 times during their search for a vehicle. That’s

up from last year’s 4.9 and cy2000’s 1.6 times.

In the auto industry’s favor, same-store sales are up

nearly 9 percent with floor traffic climbing nearly 14

percent vs. year ago. But closing ratios are down nearly 4

percent as concerns about home-centric

economics (Jitters Index) continues to be a

damper on making large purchases.

Sub-14 Million Delivery Rate

That said, the first-half of the month looked as if it

would produce 1.2 million deliveries or a True Delivery

Rate of slightly under 14 million units. Note that

“deliveries” only count vehicles when the owner takes

possession, unlike “sales” which are based on signed

contracts whether the car or truck is delivered to the

owner during the same month.

C

Page 2… CNW Research: Retail Automotive Summary August 2012

ago. That translates into fewer people who will enter the

shopping funnel. And that translates into more marketing

dollars needing to be spent to put those not actively

looking to buy a vehicle into the shopping “spirit.”

That’s both expensive in terms of ad and incentive

dollars and risky because it relies even more on sub-

prime consumers.

Page 3… CNW Research: Retail Automotive Summary August 2012

A huge jump in sub-prime approvals – 48 percent vs. year ago and 17 percent vs. July -- is underpinnings of the

higher LV Ratio details on the previous pages. The question is if this is sustainable. The unweighted rate of approvals

JITTERS INDEX Fed Gas Child’s Job Day to Day Condition of Food Local Jitters

Taxes Prices Edu Stability Needs Investments Prices Taxes Index

Vs Previous Mo. 0.52% -4.34% 0.42% 0.13% 0.66% -2.17% -0.32% -0.81% -0.81%

Vs Mo. ‘11 11.79% -7.99% 4.37% 0.26% 18.07% 18.39% 4.32% -0.20% 5.33%

for all FICO categories inched upward to 66.36

percent vs. 62.8 percent a year ago.

Used Market Days’ Supply Climbing In August, the Days’ Supply of used vehicles is

up more than 15 percent vs. year ago. That will

translate into softer used prices as dealers

attempt to shed inventory that’s beginning

to back up on their lots.

Trucks are in shorter supply than cars for the

third month running making up less than 90

percent of average days’ supply compared to

120+ percent for cars.

Detroit, Asian and European used cars are all

up in terms of Days’ Supply as well, but Detroit

products are lingering on lots longer than either

their Asian or European counterparts.

CONTEXT; The new and used vehicle industries

aren’t out of the woods just yet. Much will hinge

on the perceptions of consumers after the

Presidential election.

Finance Only (Doc 1409) Prime

Near

Prime Sub Prime

% Change v year ago 2.9% 3.8% 48.3%

% Change v previous month 0.25% 0.54% 17.16%

C

60.0%

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

130.0%

Sept Nov Jan Mar May July Sept Nov Jan. 12 Mar May July

Car V Truck Days' Supply

Car

Truck

C

August

Page 4… CNW Research: Retail Automotive Summary August 2012

Note: This is a Graphs Page. Throughout this issue you will see a C symbol in a table, graph or chart which will take you to an appropriate Graphs Page.

Doc 112m Detroit Asian Euro

May 40.91 44.87 52.36

June 41.57 43.79 52.74

July 41.06 43.92 50.03

August 43.34 41.28 48.62

Sept 44.97 42.05 46.32

Oct 45.62 42.09 46.58

Nov 45.05 44.28 45.32

Dec 45.08 46.39 45.47

Jan. 12 43.22 44.92 45.76

Feb 43.71 45.02 45.66

Mar 44.82 46.87 45.61

Apr 45.36 46.72 45.29

May 44.06 45.22 44.97

June 44.51 46.29 45.71

July 48.06 47.24 46.94

Aug 49.19 48.83 47.26

Shr of Days'

Supply

Car Truck

Sept 104.2% 96.70%

Oct 103.2% 96.35%

Nov 106.1% 95.32%

Dec 106.8% 94.68%

Jan 105.6% 94.95%

Feb 97.8% 105.85%

Mar 92.0% 110.71%

Apr 85.7% 118.41%

May 86.3% 118.66%

June 83.8% 122.14%

July 87.2% 109.67%

Aug 91.3% 108.85%

Sept 93.2% 107.02%

Oct 94.48% 105.31%

Nov 98.03% 104.67%

Dec 101.35% 98.44%

Jan. 12 102.42% 97.67%

Feb 89.93% 109.74%

Mar 88.58% 111.43%

Apr 86.37% 113.57%

May 90.24% 108.21%

June 102.71% 97.53%

July 119.46% 90.32%

Aug 121.64% 88.29%

40

45

50

55

60

65

70

75

80

85

90

Used Vehicle Days' Supply

August

Where the New-Vehicle Money Is: Pickups, Lux, SUV With gasoline prices climbing again, the outlook for Budget and Economy cars as well as electrics, hybrids and diesels

begins to brighten. But in July, it was Pickup Trucks, Luxury Cars and smaller SUVs that took the prizes home.

As a share of total sales, Pickups had their second best month of the year. The Luxury models continued to climb and

July represented their largest share of total sales of 2012. Ditto Entry Level SUVs.

In fact, it appeared as if consumers were looking for high-line products with Near Luxury and Mid-Range SUVs also

registering their largest or close to largest share of total sales of the year.

For the smaller or entry level vehicles, share of market inched up a hair, but didn’t approach the highest monthly level

Page 5… CNW Research: Retail Automotive Summary August 2012

2.09% 2.13% 1.96%

1.93%

1.70% 1.54% 1.68%

Budget Car

12.54%

13.45% 13.81%

12.34% 12.41% 12.13%

12.24%

Economy Car

12.09%

11.40%

11.87%

11.31%

11.78%

12.21%

12.48%

Entry Level SUV

0.14% 0.13%

0.21%

0.16% 0.17% 0.18% 0.20%

Electric Car

of the year.

% Max MSRP Up

But buying small

doesn’t translate into

buying “cheap.”

On an industry-

wide basis,

consumers are

selecting cars that

have a sticker price

that is 69 percent of

the maximum MSRP

for the model chosen,

highest since 2008.

(See document 1336)

That’s up from

66.2 percent a year

ago and down from

81 percent in cy06.

Page 6… CNW Research: Retail Automotive Summary August 2012

10.90%

10.56%

10.37%

10.19%

10.46% 10.58%

10.78%

Full Size Pickup

1.56% 1.71% 1.68%

1.99% 2.05% 2.05% 2.08%

Full Size Van

1.32% 1.35% 1.38% 1.33% 1.46% 1.52%

1.67%

Luxury Car

0.37%

0.28% 0.30% 0.29% 0.31% 0.26%

0.37%

Premium Car

0.19% 0.17% 0.16%

0.15% 0.17%

0.14%

0.17%

Sporty Utility Pickup

1.75% 2.07% 2.19%

2.43% 2.39% 2.64%

2.28%

Touring Car

Page 7… CNW Research: Retail Automotive Summary August 2012

3.70% 3.52% 3.35% 3.35% 3.06%

3.51% 3.80%

Near Luxury Car

0.25% 0.25%

0.31% 0.34%

0.27%

0.34% 0.33%

Premium Sporty Car

12.56% 12.42%

12.87%

12.43%

11.54% 11.21%

11.85%

Standard Mid-Range Car

2.54% 2.23%

2.07% 1.91% 1.91% 1.93% 2.02%

Small Pickup

0.07%

0.05%

0.03% 0.03% 0.02% 0.02% 0.02%

Traditional Car

1.61% 1.54% 1.37%

1.81% 1.90% 1.88% 1.79%

Upper Mid-Range Utility

Page 8… CNW Research: Retail Automotive Summary August 2012

10.78% 11.04%

11.43% 11.87%

12.44% 11.96%

10.76%

Lower Mid-Range Car

8.51%

8.20% 7.99% 8.20%

8.34% 8.28%

8.77%

Lower Mid-Range SUV

1.62%

1.46% 1.33%

1.49% 1.66% 1.74% 1.79%

Large SUV

0.24% 0.20% 0.21%

0.24% 0.29%

0.21% 0.23%

Midi-Van

2.32% 2.27% 1.98%

2.17%

2.66% 2.70% 2.35%

Mid-Range SUV

3.47%

3.86% 3.85%

4.01% 4.14%

3.72% 3.78%

Minivan

Page 9… CNW Research: Retail Automotive Summary August 2012

4.39%

4.64%

4.24%

4.63%

4.05%

4.52%

3.93%

Premium Mid-Range Car

0.02% 0.01%

0.02% 0.02%

0.02% 0.02%

0.02%

Ultra Upscale Car

0.05%

0.04% 0.04% 0.05%

0.04% 0.04% 0.05%

Ultra Luxury Sporty Car

1.61% 1.54% 1.37%

1.81% 1.90% 1.88% 1.79%

Upper Mid-range SUV

0.04% 0.05%

0.02%

0.04%

0.06% 0.05%

0.03%

Ultra-Premium Utility Vehicle

0.17% 0.16% 0.12%

0.18% 0.19% 0.16%

0.19%

Upper Premium Sport Car

Anticipated Aug Actual Aug % Chng YTD YTD % Chng

Document 106m cy12 cy11 12v11 cy2012 cy2011 12v11

Franchised

Dealer Sales 1,521,235 1,431,489 6.3% 10,268,407 9,818,739 4.6%

Independent

Dealer Sales 1,296,127 1,424,219 -9.0% 9,273,921 9,826,771 -5.6%

Casual (Private)

Sales 1,077,250 957,066 12.6% 8,340,759 7,280,942 14.6%

Total Sales 3,894,612 3,812,774 2.1% 27,883,087 26,926,452 3.6%

Page 10… CNW Research: Retail Automotive Summary August 2012

August usually is a relatively slow month for used

sales, but this year’s numbers are distressing, especially

for independent dealers.

Franchised dealers’ used-car operations are on track to

register a six-plus percent gain over year ago with 1.5

million sales, bringing the total year-to-date figure

approaching 10.3 million.

Private Party sales continue to sparkle as more

consumers offer their cars on web sites such as craigslist

and other no-charge outlets.

The Independent dealer body is torn. In some regions

of the country, used sales by Indies are soaring while in

other parts of the country they are in the tank. Regardless

of regional differences, Independents on the whole are on

track to a nine percent decline in August.

What’s at the core of the problem? One might well be

the typical outlets used by Independent dealers to market

their vehicles. Newspaper classified ads, local radio for the

medium-size operations and high visibility on-street

August Used Sales Up 2 Percent on Back of Private Party Sales; Indies Off 9 Percent

signage. All of these are on a downward path when it

comes to attracting buyers. More on that in a later issue of

RAS.

The point, however, is that independent dealers must

change their approach to marketing just as new-car dealers

have done.

Former New-Car Dealers

Turning Profits in Used Market

When GM and Chrysler were shedding dealerships

because of bankruptcy, many turned to the used-car

business. Facilities were already in place. Business

structures likewise were already operating.

So how are those new-converts-to-used doing? In a

CNW survey of nearly 200 such dealerships, the vast

majority struggled through the transition, but better than 80

percent are now operating a profitable used-car business.

Most say the profitability of used cars are on a par with

their final two years as a new-car dealer.

Page 11… CNW Research: Retail Automotive Summary August 2012

Franchised Independent Franchised Franchised Independent Independent

Document 107m Asking Price Asking Price Trans Price % of Asking Trans Price % of Asking

Jan. '12 $11,516 $10,483 $10,855 94.26% $9,715 92.67%

Feb. '12 $11,653 $10,516 $11,090 95.17% $9,784 93.04%

Mar '12 $11,826 $10,592 $11,254 95.16% $9,874 93.22%

Apr ’12 $11,507 $10,216 $10,958 95.23% $9,576 93.74%

May '12 $12,119 $9,987 $11,296 93.21% $9,071 90.83%

June '12 $11,684 $9,937 $10,802 92.45% $9,069 91.27%

July '12 $12,136 $9,842 $11,185 92.16% $8,943 90.87%

Aug '12 $12,103 $9,849 $11,138 92.02% $8,936 90.73%

August '11 $11,458 $10,172 $11,021 96.19% $9,598 94.36%

Sept '11 $11,253 $10,219 $10,807 96.04% $9,572 93.67%

Oct. 11 $11,394 $10,384 $10,952 96.12% $9,744 93.84%

Nov. '11 $11,186 $10,148 $10,654 95.24% $9,452 93.14%

Dec '11 $11,058 $10,039 $10,547 95.38% $9,384 93.48%

Percent Change Yr over Yr 5.63% -3.18% 1.06% -4.34% -6.90% -3.85%

Month Over Month Price -0.27% 0.07% -0.42% -0.15% -0.08% -0.15%

Used Vehicle Prices Continue to Slip Month-Over-Month; Franchised Dealers Flat

The average transaction price for used cars at Franchised new car dealerships kept its head above water compared to

the same month of 2011. Independents weren’t so lucky.

Franchised dealers were asking about 5.6 percent more for their vehicles but had to settle for a 1.1 percent gain in

transaction prices while Indies asked 3.2 percent less than a year ago and suffered a near-7 percent decline in transaction

prices.

Because of on-line resources such as KBB, AutoTrader and the like, consumers are becoming increasingly aware of

what a used vehicle should (in their minds) sell for. They are driving a harder bargain and finding dealers, who are seeing

inventories beginning to grow, willing to make a deal.

CONTEXT: For independent dealers, there are some serious trials on the horizon. Aside from increasing regulations from

BHPH to signage, the marketing landscape is changing rapidly and in a way that will require expensive alterations in how

Indies reach potential customers.

Page 12… CNW Research: Retail Automotive Summary August 2012

cy12 Jan Feb March April May June July

All Sales 912,874 1,148,975 1,404,100 1,184,069 1,334,150 1,285,005 1,153,269

Percent Change v Previous Year 11.4% 15.7% 12.7% 2.4% 25.9% 22.0% 8.9%

Fleet and Commercial Use 39.52% 36.48% 36.92% 38.09% 36.41% 38.25% 38.73%

Total Fleet (Monthly Approximates) 360,768 419,146 518,394 451,012 485,764 491,514 446,661

Percent Change v Previous Year 32.7% 40.5% 31.6% 22.4% 63.5% 77.2% 57.8%

FLEET COMMERCIAL VALUE -- Per Unit $27,219 $27,254 $27,614 $27,943 $27,904 $28,147 $28,221

FLEET COMMERCIAL VALUE -- Total $Bllns $9.82 $11.42 $14.31 $12.60 $13.55 $13.83 $12.61

Percent Change v Previous Year 40.92% 48.55% 39.68% 30.13% 69.34% 84.70% 64.12%

Government Fleet 18,805 23,439 28,222 24,747 25,616 25,315 22,373

Share Gov't of Total Sales 2.06% 2.04% 2.01% 2.09% 1.92% 1.97% 1.94%

Percent Change v Previous Year -27.6% -17.5% -16.7% -18.0% 3.3% 10.8% 2.5%

Small Business Fleet and Commercial Use 35,967 47,338 59,815 51,152 59,770 58,082 53,973

Share Small Business of Total Sales 3.94% 4.12% 4.26% 4.32% 4.48% 4.52% 4.68%

Percent Change v Previous Year 34.3% 29.1% 24.1% 13.1% 72.4% 81.4% 63.8%

Medium Business Fleet and Commercial Use 88,731 116,736 150,520 124,682 142,887 124,388 112,790

Share Medium Business of Total Sales 9.72% 10.16% 10.72% 10.53% 10.71% 9.68% 9.78%

Percent Change v Previous Year -3.6% 57.5% 67.6% 48.5% 104.6% 88.1% 66.6%

Large Business Fleet, Daily Rental, Commer. 217,264 231,633 279,837 250,431 257,491 283,729 257,525

Share Large Business of Total Sales 23.80% 20.16% 19.93% 21.15% 19.30% 22.08% 22.33%

Percent Change v Previous Year 71.0% 45.5% 26.1% 19.8% 53.5% 81.5% 60.4%

40.00%

47.50%

55.00%

62.50%

70.00%Share Retail

August

Commercial-Fleet Has 2nd Best Month of 2012 Commercial and fleet sales are beginning to hum with

all but government units showing 60-plus percent gains

over a year ago. They have seemingly shrugged off the

shackles of the recession.

Excluding upfitting, the average value of a fleet-

commercial vehicle hit its highest point of the year at

$28,221 for a total value of $12.6 billion. That can be doubled when upfitting is included.

Page 13… CNW Research: Retail Automotive Summary August 2012

Mobile Part 3: Top and Bottom Marketing Areas for Auto Info Usage When it comes to using a mobile device – iPhone,

SmartPhone, etc. – for hunting up information about a

potential new-car acquisition, San Francisco is well ahead

of the curve followed by Washington D.C.

Neither is a surprise, but among the Top 25 are places

like Juneau and Anchorage, Alaska.

By measuring through CNW’s Purchase Path surveys

the use of mobile for collecting new-car information, we’ve

been able to devise a simple Mobile Index that shows the

relative strength of each marketing area in the U.S. with

DMA Name Pop 2009 Mobile Index

San Francisco-Oakland-San Jose, CA 7,084,134 252.00

Washington, DC (Hagerstown, MD) 6,255,641 213.14

Juneau, AK 30,784 190.47

Boston, MA (Manchester, NH) 6,304,369 178.12

Anchorage, AK 428,210 162.15

Monterey-Salinas, CA 744,041 162.06

New York, NY 21,008,149 161.64

Austin, TX 1,833,822 154.63

Atlanta, GA 6,631,136 154.15

Minneapolis-St. Paul, MN 4,553,185 153.51

Denver, CO 4,025,845 153.40

Chicago, IL 9,927,410 152.78

Hartford & New Haven, CT 2,626,159 146.08

Seattle-Tacoma, WA 4,781,250 145.56

Dallas-Ft. Worth, TX 7,090,236 143.39

Fairbanks, AK 93,980 141.00

Baltimore, MD 2,898,828 139.67

Philadelphia, PA 7,913,835 137.28

San Diego, CA 3,092,622 136.36

Honolulu, HI 1,309,261 135.38

Los Angeles, CA 18,065,308 135.04

Detroit, MI 5,057,085 134.00

Santa Barbara-Santa Maria-San Luis Obispo, CA 687,978 129.77

Houston, TX 6,223,472 126.96

DMA Name Pop 2009 Mobile Index

Wheeling, WV-Steubenville, OH 325,043 55.39

Ottumwa, IA-Kirksville, MO 130,207 55.25

Great Falls, MT 167,661 55.14

Montgomery-Selma, AL 635,248 54.97

Sherman, TX-Ada, OK 327,330 54.62

Albany, GA 425,158 54.45

Dothan, AL 249,733 54.08

Paducah, KY-Cape Girardeau, MO-Harrisburg, IL 972,802 53.90

Tri-Cities, TN-VA 801,456 53.22

Shreveport, LA 1,012,378 52.16

Charleston-Huntington, WV 1,164,983 50.29

Laredo, TX 263,573 49.32

Glendive, MT 9,652 48.92

Columbus-Tupelo-West Point, MS 493,530 47.33

Clarksburg-Weston, WV 269,345 46.99

Lafayette, LA 615,605 46.81

Hattiesburg-Laurel, MS 292,840 44.81

Presque Isle, ME 72,941 44.74

Alexandria, LA 245,701 42.92

Monroe, LA-El Dorado, AR 479,032 41.94

Bluefield-Beckley-Oak Hill, WV 343,234 41.07

Meridian, MS 187,476 40.77

Harlingen-Weslaco-Brownsville-McAllen, TX 1,249,997 38.20

Greenwood-Greenville, MS 213,538 33.88

the national score equal to 100. Translated, for example, San

Francisco new-car shoppers are 2.5 times more likely to use a

mobile device to collect auto information before buying.

At the other end of the spectrum, shoppers in Greenwood,

Mississippi are only a third as likely as the national average.

What it Means for Auto Marketing

There is no doubt that mobile is a “screen” that automakers,

dealers and related companies need to include in their

marketing schemes. But being focused on specific DMAs or

Page 14… CNW Research: Retail Automotive Summary August 2012

Industry Jeep O/U Index 300 O/U Indx Ind Mob Eff Jeep Mob Eff 300 Mob Eff Time Delay TV Ad Skip Ad Effect Mob v TV

San Francisco-Oakland-San Jose, CA 13% 6% 79.52 80.52 84.29 2.49 81.83% 83.44 4.93% Washington, DC (Hagerstown, MD) -9% 32% 83.60 84.60 110.35 3.72 73.59% 78.94 -5.58%

Juneau, AK 56% -26% 85.37 86.37 63.17 1.51 51.69% 94.01 10.11% Boston, MA (Manchester, NH) -4% 1% 87.31 88.31 88.18 1.06 69.85% 94.72 8.49%

Anchorage, AK 64% -34% 89.00 90.00 58.74 1.79 61.14% 92.58 4.02%

Monterey-Salinas, CA 14% 26% 89.19 90.19 112.38 2.06 72.09% 90.10 1.01%

New York, NY -41% 74% 89.20 90.20 155.21 0.91 75.53% 95.41 6.96%

Austin, TX 36% -8% 90.20 91.20 82.98 0.83 47.34% 97.51 8.10%

Atlanta, GA 1% 6% 90.10 91.10 95.51 0.97 72.28% 95.50 5.99%

Minneapolis-St. Paul, MN 17% 18% 89.97 90.97 106.17 1.03 67.13% 95.48 6.12%

marketing area can generally keep budgets contained.

To take the Mobile Index a step further, CNW devised an

Effectiveness component in its analysis.

By using the rate of actual purchases after searching for

auto info on a mobile device and combining that rate with

other data from the Purchase Path surveys, it was possible

to show how Effective mobile is overall.

While SF may have the highest Mobile usage for auto

info, it falls way behind places such as Atlanta, Minneapolis-

St. Paul, Boston and Anchorage in terms of mobile owners

who eventually have a specific brand and model on their

late-term shopping list. The National Average is 81.3.

And by Brand or Model

Even further dissection shows just how effective mobile

is for specific brands and models. In the example below, we

used Jeep and the Chrysler 300 since both are from the

same automaker.

As the table below shows, among those who are

interested in a Jeep, 13 percent are more likely to use a

mobile device to collect information. In Anchorage, the rate is

64 percent higher.

Conversely, in Washington D.C., those interested in a

Chrysler 300 are 32 percent higher than the national average

while in Anchorage, shoppers are 34 percent lower.

Finally, after adjustments for buy rates and other factors,

the simple point is this: It’s more effective to use mobile in

San Francisco for Jeep or the 300 even though it is not the

most effective marketing area when compared to other

DMAs.

Against Time Delay TV

When the data is also accumulated for DVRs and other

time-delayed television ads, mobile still lags. Even though

81.8 percent of San Francisco new-car shoppers skip the ads

when watching a DVR’d show, this traditional media is

somewhat more effective than mobile. At least for now.

Page 15… CNW Research: Retail Automotive Summary August 2012

Why People Select a Hybrid

0%

10%

20%

30%

40%

50%

60%

70%

Q1'04

Q2Q3Q4Q1'05

Q2Q3Q4Q1'06

Q2Q3Q4Q1'07

Q2Q3Q4Q1'08

Q2'08

Q3'08

Q4'08

Q1'09

Q2'09

Q3'09

Q4'09

Q1'10

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Q2'12

Higher Fuel Economy

Document 1109 Q2 ‘04 Q2 ‘05 Q2 ‘06 Q2 ‘07 Q2 '08 Q2 '09 Q2 '10 Q2 '11 Q2 '12

Distinctive Styling 42.87% 40.86% 37.52% 28.82% 20.61% 14.26% 10.24% 9.17% 8.14%

Higher Fuel Economy 26.56% 28.16% 37.93% 30.47% 48.38% 41.86% 49.26% 52.38% 50.26%

Lower Emissions (environment) 32.27% 34.77% 35.16% 35.44% 20.72% 20.11% 20.04% 20.58% 20.33%

New Technology 22.24% 30.94% 15.48% 11.17% 4.06% 2.97% 2.75% 2.73% 1.93%

"Makes a Statement About Me" 35.55% 35.48% 35.48% 46.64% 55.63% 62.58% 63.84% 63.98% 55.72%

Other (incl. incentives, business, etc.) 40.51% 29.79% 38.43% 47.46% 50.60% 58.22% 53.87% 51.16% 63.62%

The world has changed for hybrid

marketers and nothing shows that

more clearly than the reasons buyers

give as the top two reasons for

making the gas-electric choice.

In the second quarter of 2004,

nearly 43 percent of hybrid owners

said they purchased the alternative

powerplant vehicle because it had

distinctive styling (Prius) with another

35 percent saying it made a

statement about the owners/driver. In the second quarter of this year, the largest share of

reasons centered on the hybrid being for business or due to

incentives (state, federal, local, manufacturer). This has been

the case for five of the past nine years the survey has been

conducted.

Distinctive styling was given as one of the top two reasons

by only 8 percent of owners.

While fuel economy remains a key reason for the hybrid

selection at 50 percent in the most recent quarterly survey, it

still trails “makes a statement about me” by nearly 7 points.

As the graphs on the following page also show, the

notion that a hybrid represented new technology has

diminished as a key reason for acquisition. In 2004, it

was 22 percent. Today it is less than 2 percent.

CONTEXT: Fuel economy and “status” continue to be

significant drivers for buying a hybrid and marketing

efforts should zero in on both of those desires. But

consumers are still looking for a deal and aren’t willing

to break the budget without a financial hook.

Page 16… CNW Research: Retail Automotive Summary August 2012

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Q1 '04Q2Q3Q4Q1 '05Q2Q3Q4Q1 '06Q2Q3Q4Q1 '07Q2Q3Q4Q1 '08Q2 '08Q3 '08Q4 '08Q1 '09Q2 '09Q3 '09Q4 '09Q1 '10Q2 '10Q3 '10Q4 '10Q1 '11Q2 '11Q3 '11Q4 '11Q1 '12Q2 '12

Lower Emissions (environment)

0%

5%

10%

15%

20%

25%

30%

35%

Q1 '04Q2Q3Q4Q1 '05Q2Q3Q4Q1 '06Q2Q3Q4Q1 '07Q2Q3Q4Q1 '08Q2 '08Q3 '08Q4 '08Q1 '09Q2 '09Q3 '09Q4 '09Q1 '10Q2 '10Q3 '10Q4 '10Q1 '11Q2 '11Q3 '11Q4 '11Q1 '12Q2 '12

New Technology

0%

10%

20%

30%

40%

50%

60%

70%

Q1 '04Q2Q3Q4Q1 '05Q2Q3Q4Q1 '06Q2Q3Q4Q1 '07Q2Q3Q4Q1 '08Q2 '08Q3 '08Q4 '08Q1 '09Q2 '09Q3 '09Q4 '09Q1 '10Q2 '10Q3 '10Q4 '10Q1 '11Q2 '11Q3 '11Q4 '11Q1 '12Q2 '12

"Makes a Statement About Me"

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Q1 '04Q2Q3Q4Q1 '05Q2Q3Q4Q1 '06Q2Q3Q4Q1 '07Q2Q3Q4Q1 '08Q2 '08Q3 '08Q4 '08Q1 '09Q2 '09Q3 '09Q4 '09Q1 '10Q2 '10Q3 '10Q4 '10Q1 '11Q2 '11Q3 '11Q4 '11Q1 '12Q2 '12

Distinctive Styling

Ewanick Needs Replacing Soon

GM still has a problem Identifying what each brand means

Jean Halliday’s

It certainly has been an interesting several weeks watching General Motors' train wreck in the aftermath of the forced resignation of global Chief Marketing Officer and VP Joel Ewanick. Talk about a corporate nightmare: Reports of Ewanick's financial improprieties on the $500-million-plus Manchester United deal; CEO Dan Akerson's internal embarrassment of Ewanick; whistle blowers and an entrenched corporate culture. Whoever said there's no such thing as negative PR was wrong! The entire incident has focused a ton of unflattering attention on GM and its top brass, leaving auto industry watchers to wonder: who would even want to fill Ewanick's shoes? For now Alan Batey (picture at right) is the interim CMO. Batey was just moved in May to the newly-created post of GM VP for US Sales and Service from the same post at Chevrolet in the US. This Englishman is a GM insider, having started at the automaker in the UK in 1979 as a mechanical engineering apprentice but his career blossomed into senior management jobs overseas. Nothing, however, in his bio offers any hints at his marketing expertise.

Page 17… CNW Research: Retail Automotive Summary August 2012

GM will need to replace Ewanick-

the sooner the better. And his successor really needs to be an experienced auto marketeer with an impressive track record and ad agency experience. Not a sales person, finance expert or engineer. GM needs another change agent, which translates to an outsider. CEO Akerson tried to allay fears that GM's advertising would be in

flux without Ewanick. "I know that a lot of the public views this as a personality-driven industry," he said. "What you saw manifest in the marketplace was a thought-out strategy that was agreed upon with the team.” Time for New Approach If that's the case, it's time for a new approach because GM's “team” strategy to create advertising is churning out some very mediocre work.

(continued next page)

Page 18… CNW Research: Retail Automotive Summary August 2012

When you look at the companies doing break-through advertising you'll see that their CMOs have strong personalities and preferences that drive the work. Look at Chrysler Group. Say what you want about the foibles of CMO Olivier Francois, but he manages to get some of the best auto work in the business from his ad agencies. Francois is also willing to take ad risks- not exactly a GM hallmark. When’s a Team Not a Team Oh, and Akerson's politically-correct “bit” about GM's team working on advertising....which team player blew the whistle that their boss, Ewanick, was spreading the price of Chevy's Manchester deal over different budgets to avoid spending limits? Some team, eh? The truth is Ewanick was an outsider in a still-obviously, insular company that resents newcomers. Ewanick came into the “new” GM in May 2010 after a brief stint at Nissan and a longer one as VP-marketing of Hyundai. GM needed a change agent and Ewanick fit the bill, making some early, quick moves. He orchestrated the move of Chevrolet to Goodby, Silverstein & Partners without a review before Publicis Groupe could even really get started on that newly-won account. Soon after, he shifted Cadillac's ad agency to Fallon, Minneapolis without a review. He directed new ad tags for Chevrolet and Cadillac. He hired several key ad and marketing lieutenants from the outside. He got GM back into the Super Bowl – and then said earlier this year GM would sit out the Big Game in 2013. He consolidated media globally and vowed to save $ 2 billion over 5 years.

Yet, under Ewanick, GM's advertising was never anything special. There were some one-off gems here and there during his 2-year reign as CMO. But for the most part, the work was lack luster. Last fall, even Ewanick criticized the work Goodby, Silverstein & Partners was doing for Chevrolet, calling it inconsistent and giving it grades of “C”, “B,” and some “As.”

The agencies never really seemed to capture the essence of each brand: Cadillac, Chevrolet, Buick and GMC. Agencies get their marching orders from their clients. It's my understanding GM's marketing team isn't writing clear “briefs” for the agencies to follow in order to develop relevant creative.

There has been one very recent exception. The launch

work for or the new Cadillac ATS compact sedan, themed “Cadillac ATS vs. the World,” that just arrived in July from Fallon. (continued next page)

Page 19… CNW Research: Retail Automotive Summary August 2012

(continued from previous page) About time! Troubles Foretold There was evidence this year that all was not well in the marketing ranks at GM. Two of Ewanick's high-profile hires, Liz Boone and Kevin Mayer, decided to leave. One doesn't voluntarily leave one's job after a couple of years or so because the company is a great place to work. Since Ewanick's split, CEO Akerson gave the world a pretty good idea of what it's like to work there. During a conference call he told employees "we're a global company that operates as small, little fiefdoms. That's got to stop." He added “we've got to get this company and its culture into the 21st century.” GM Still Mired in the Past Oh brother. He admitted GM's corporate culture is mired in its past. Nothing like top-down directives to improve morale and culture. GM has tried to get its arms around its culture over the

years. In the mid-90s, GM hired at least one Organizational Physiologist to study and improve the way staffers worked together. Changing the culture is not an easy thing to do, especially after decades of fiefdoms. But Akerson's real topper was his internal humiliation of Ewanick for his public appearance earlier this summer in Cannes where he cursed a blue streak on stage bantering with Joel Goodby, founder of the ad agency bearing his name. The Farley Award Akerson decided to make an example of Ewanick on how NOT to behave in public as a GM exec, so he created the "Farley Award," according to Bloomberg. At work, Ewanick had to sport the “award,” named after Ford Motor exec Jim Farley, who was quoted in an industry 2011 book, “Once Upon a Car,” as saying “f... GM.” Is that any way to treat a global executive? Sounds like discipline from a private school in the 1950s. Maybe it's something Akerson, 63, learned in the Navy. That sort of reprisal has NO place inside a major corporation in 2012. And this from a guy who is demanding changes to GM's culture! So, how long do you think the line will be for wanna-be CMOs for GM's open post- to come and work for this CEO? Not very.

Page 20… CNW Research: Retail Automotive Summary August 2012

Back Page *Deliveries not sales Aug 1-15 Aug 1-15 % Chng Actual Sales Aug '12 Full Mo

cy2012 cy2011 12 v 11 Aug '11 Sales Change

New Cars Extension

Detroit 3 125,182 113,135 10.6% 171,251 189,486 10.6%

Asian 123,748 103,296 19.8% 279,837 335,243 19.8%

European 25,416 21,373 18.9% 68,321 81,245 18.9%

Ttl Pass. Cars 274,346 237,804 15.4% 519,409 605,974 16.7%

New Trucks

Detroit 3 159,681 148,627 7.4% 349,041 375,001 7.4%

Asian 32,178 31,242 3.0% 177,063 182,368 3.0%

European 3,545 3,226 9.9% 26,403 29,014 9.9%

Ttl Lt. Trucks 195,404 183,095 6.7% 552,507 586,382 6.1%

Ttl Industry 469,750 420,899 11.6% 1,071,916 1,192,357 11.2%

Aug 1-15 Full Aug % Chng Prev Mo Prev Mo % Chng

cy2012 cy2011 12 v 11 cy2012 cy2011 12 v 11

Lease Share 27.2% 25.3% 7.4% 26.9% 25.2% 6.7%

Floor Traffic - New 75.06 66.04 13.7% 91.98 66.04 39.3%

Floor Traffic - Used 86.24 76.97 12.0% 85.04 76.97 10.5%

Aug 1-15 Prev Yr % Chng % Chng Pent Up Demand Units

cy2012 Full Aug Same Mo '11 Prev Mo July '12 90,400

Avg. New MSRP $37,156 $34,629 7.30% 0.09% July '11 175,000

Total Discounts $4,975 $4,786 3.95% 0.69% % Change -48.3%

Manufacturer Incentives $3,634 $3,239 12.20% 0.83%

Dealer Incentives $1,341 $1,547 -13.32% 0.32% Purchase Delay Months

Core Transaction Price**** $32,181 $29,843 7.83% -0.01% July '12 3.24

% Mfg Incentive of MSRP 9.78% 9.35% 4.6% July '11 5.5

% Ttl Discounts of MSRP 13.39% 13.82% -3.1% % Change -41.1%