Embed Size (px)

Citation preview

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Case study: issuing financial

instruments

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Vienna, June 2014

2 2

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

The requirements are set out in International Financial Reporting Standards (IFRS), as issued by the IASB at 1 January 2014, including those with an effective date after 1 January 2014, but not the IFRSs they will replace.

Disclaimer: The IFRS Foundation, the authors, the presenters and the workshop organisers do not accept responsibility for any loss caused by acting or refraining from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise and this presentation is not a form of advice or opinion.

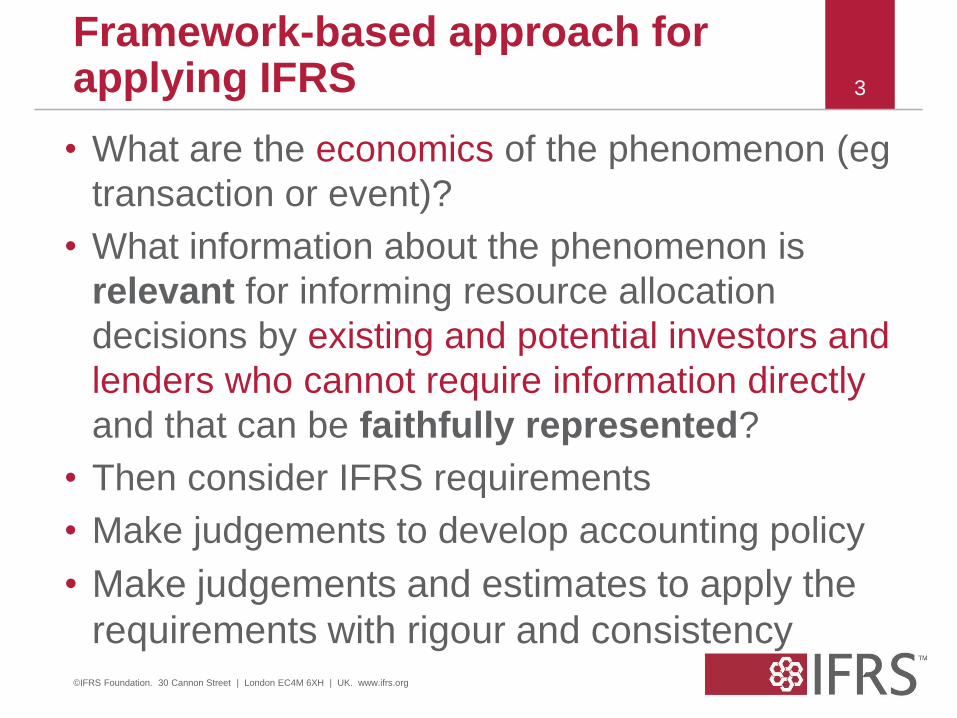

Framework-based approach for applying IFRS

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

3

• What are the economics of the phenomenon (eg

transaction or event)?

• What information about the phenomenon is

relevant for informing resource allocation

decisions by existing and potential investors and

lenders who cannot require information directly

and that can be faithfully represented?

• Then consider IFRS requirements

• Make judgements to develop accounting policy

• Make judgements and estimates to apply the

requirements with rigour and consistency

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

4

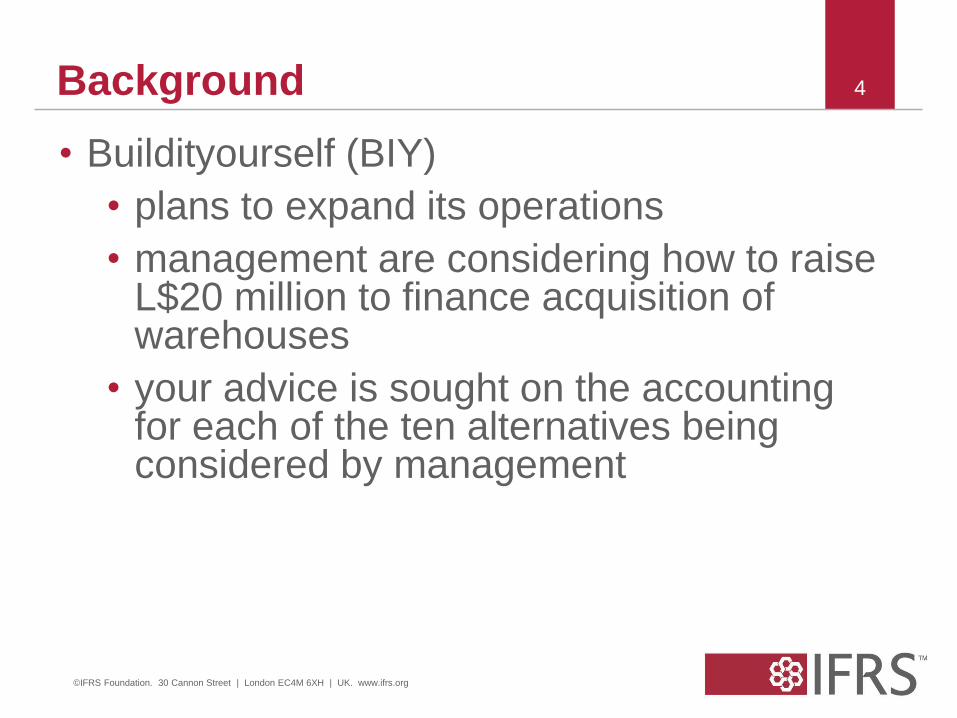

• Buildityourself (BIY)

• plans to expand its operations

• management are considering how to raise L$20 million to finance acquisition of warehouses

• your advice is sought on the accounting for each of the ten alternatives being considered by management

Background

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

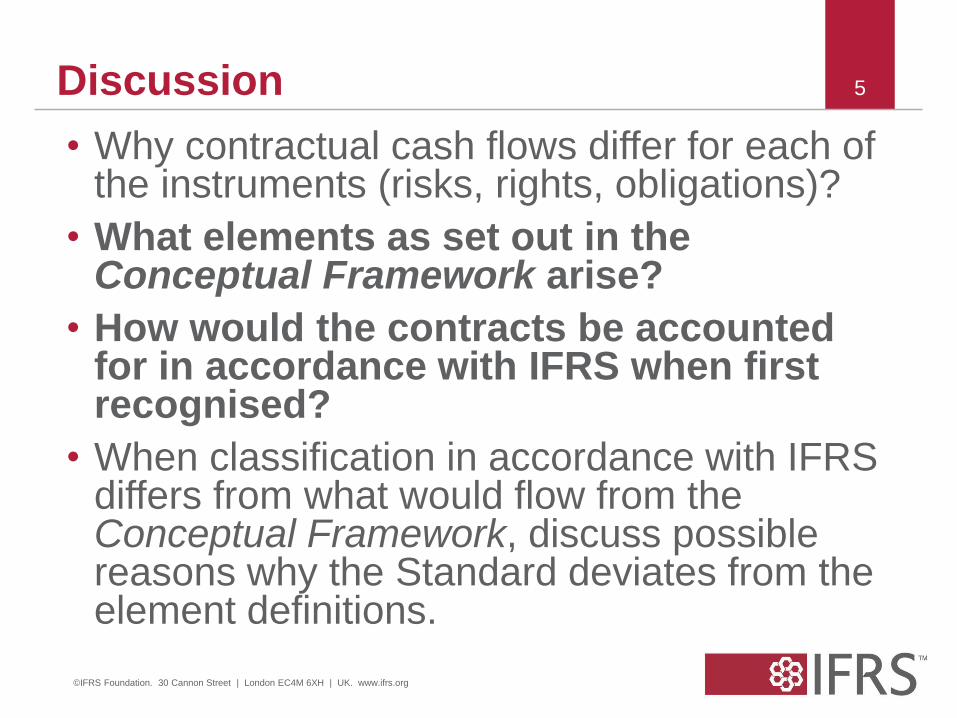

5 Discussion

• Why contractual cash flows differ for each of the instruments (risks, rights, obligations)?

• What elements as set out in the Conceptual Framework arise?

• How would the contracts be accounted for in accordance with IFRS when first recognised?

• When classification in accordance with IFRS differs from what would flow from the Conceptual Framework, discuss possible reasons why the Standard deviates from the element definitions.

6 Identifying elements

Income (¶4.25(a))

• recognised increase in asset/decrease in liability in current reporting period

• that result in increased equity except…

Expense (¶4.25(b))

• recognised decrease in asset/increase in liability in current period

• that result in decreased equity except…

Asset (see Conceptual

Framework ¶4.4(a))

• resource controlled by the

entity…

• expected inflow of

economic benefits

Liability (¶4.4(b))

• present obligation…

• expected outflow of

economic benefits

Equity (¶4.4(c))

• assets – liabilities

6

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

7

IFRSs relevant to the classification of the issue of financial instruments

• IAS 32 Financial Instruments: Presentation

• IAS 39 Financial Instruments: Recognition and Measurement

• IFRS 7: Financial Instruments: Disclosures

• IFRS 9: Financial Instruments (if adopted early)

• IFRIC 2 Members’ Shares in Co-operative Entities and Similar Instruments

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

8 8

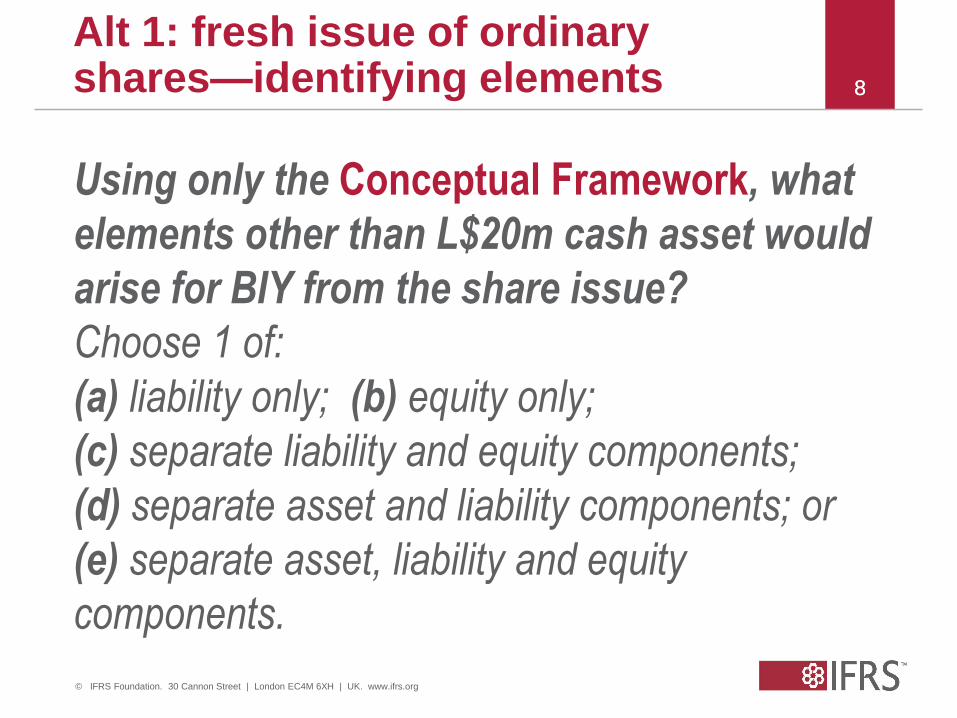

Alt 1: fresh issue of ordinary shares—identifying elements

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the share issue?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

9 Alternative 1—elements

Asset Liability Equity

No. There is no

present

obligation the

settlement of

which is

expected to

result in an

outflow of cash

or other

assets.

Yes. The claim against BIY that

arises from receiving 20m in

exchange for new ordinary shares is

equity (ie on 1/1/20X0 assets (cash)

increased by 20m without a

corresponding increase in liabilities—

because there is no obligation for BIY

to deliver cash or other assets).

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

10 10

Alt 1: fresh issue of ordinary shares—IFRS accounting

On initial recognition how would BIY classify

the shares issued in accordance with IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

11 Alternative 1—IAS 32

Asset Liability Equity

No. There is no

present

obligation for

BIY to deliver

cash or other

resources

(IAS 32.17).

Yes. An equity instrument is any

contract that evidences a residual

interest in the assets of an entity after

deducting all its liabilities (IAS 32.11).

The instrument contains no

contractual obligation to deliver cash

or another financial asset or exchange

under potentially unfavourable

conditions (IAS 32.16).

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

12 12

Alt 2: mandatorily redeemable fixed-term variable-rate debentures

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

13 Alternative 2—elements

Asset Liability Equity

Yes. At 1 January 20X0 BIY has a

present obligation to pay the

contractual cash flows to the

debenture holders. Consequently,

the L$20 million claim against BIY is

all a liability.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14 14

Alt 2: mandatorily redeemable fixed-term variable-rate debentures

On initial recognition how would BIY classify

the instument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

15 Alternative 2—IAS 32

Asset Liability Equity

Yes. At 1 January 20X0 BIY has a

present obligation to pay the

contractual cash flows to the

debenture holders. Consequently,

the L$20 million claim against BIY is

all a financial liability.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

16 16

Alt 3: mandatorily redeemable fixed-term fixed-rate debentures

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

17 Alternative 3—elements

Asset Liability Equity

Yes. At 1 January 20X0 BIY has a

present obligation to pay the

contractual cash flows to the

debenture holders. Consequently, the

L$20 million claim against BIY is all a

liability.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

18 18

Alt 3: mandatorily redeemable fixed-term fixed-rate debentures

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

19 19

Alt 4: mandatorily redeemable debentures, holder can redeem early

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

20 Alternative 4—elements

Asset Liability Equity

Yes. At 1/1/X0 BIY has a present obligation to

pay:

(i) 900k on 31/12/X0, 900k on 31/12/X1 and

20,900k on 31/12/X2. FV at 1/1/X0 =

+19,727,675 (ie PV at say 5%); and

(ii) stand ready to issue another debenture

paying interest at 4.5% for a period of up to 7

years starting 1/1/X3. FV = +272,325

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

21 21

Alt 4: mandatorily redeemable debentures, holder can redeem early

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

22 22

Alt 5: mandatorily redeemable debentures, issuer can redeem early

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

23 Alternative 5—elements

Asset Liability Equity

Yes. The early

redemption feature is an

option (right = resource)

that BIY expects future

economic benefits from.

Eg, if interest rates fall,

BIY could early redeem

the debentures and

issue new debt at a

lower rate. +544,650

Yes. At 1/1/X0 BIY has a

present obligation to pay

1.2m on 31/12/X0, 1.2m on

31/12/X1 and 21,2m on

31/12/X2. FV at 1/1/X0 =

+20,544,650 (ie PV at say

5%). Note: by exercising its

early redemption option BIY

can avoid the contractual

cash outflows in X3–X9)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

24 24

Alt 5: mandatorily redeemable debentures, issuer can redeem early

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

25 25

Alt 6: mandatorily redeemable fixed-term preference shares

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

26 Alternative 6—elements

Asset Liability Equity

Yes. At 1/1/X0 BIY has a present obligation

to pay the contractual cash flows to the

preference shareholders. Consequently,

the 20m claim against BIY is all a liability.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

27 27

Alt 6: mandatorily redeemable fixed-term preference shares

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

28 28

Alt 7: convertible debentures—exercisable only at maturity

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

29 Alternative 7—elements

Asset Liability Equity

Yes. At 1/1/X0 BIY has a

present obligation to

deliver the contractual

cash flows including the

10 year annuity and the

redemption amount—a

liability of +L$17,683,480

(ie PV at 5%)

Yes. At 1/1/X0 the principal

amount must convert into a

fixed amount of ordinary

shares (a residual interest)

on 31/12/X9.

Fair value = +L$2,316,520 .

There is no present

obligation in respect of this

amount because it will be

settled in shares—equity.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

30 30

Alt 7: convertible debentures—exercisable only at maturity

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

31 31

Alt 8: convertible debentures—exercisable before maturity

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

32 Alternative 8—elements

Asset Liability Equity

Yes. At 1/1/X0 BIY has a

present obligation to

deliver the contractual

cash flows—10 year

annuity and redemption

amount—a liability of

+L$16,911,306. Any

variation in the term of

the annuity is controlled

by the debenture

holders, not BIY.

Yes. At 1/1/X0 the debenture

holders hold an option to

convert between 1/1/X4 and

31/12/X9 their debentures

into a fixed number of

ordinary shares (a residual

interest, ie there is no

present obligation because,

if exercised, it will be settled

in a fixed number of ordinary

shares—equity).

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

33 33

Alt 8: convertible debentures—exercisable before maturity

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

34 34

Alt 9: debentures with conditional issuer-held early redemption

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

35 Alternative 9—elements

Asset Liability Equity

Yes. The early

redemption feature is an

option (right = resource)

that BIY expects future

economic benefits from.

If interest rates fall, and

BIY shares share price

exceeds L$26, BIY

could early redeem the

debentures and issue

new debt at a lower rate.

Yes. At 1/1/X0 BIY has a

present obligation to pay

contractual cash flows to the

debenture holders—a

liability.

Market expectations of the

probability of the uncertain

future event regarding the

early redemption feature

occurring affects the FV of

the liability.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

36 36

Alt 9: debentures with conditional issuer-held early redemption

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

37 37

Alt 10: convertible debentures with conditional early redemption

Using only the Conceptual Framework, what

elements other than L$20m cash asset would

arise for BIY from the instrument issued?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

38 Alternative 10—elements

Asset Liability Equity

Yes. See alt. 9. Yes. At 1/1/X0 BIY has a

present obligation to pay

contractual cash flows to the

debenture holders—a

liability.

Yes. See Alt 8.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

39 39

Alt 10: convertible debentures with conditional early redemption

On initial recognition how would BIY classify

the instrument issued in accordance with

IFRS?

Choose 1 of:

(a) liability only; (b) equity only;

(c) separate liability and equity components;

(d) separate asset and liability components; or

(e) separate asset, liability and equity

components.

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

40 40

Compound financial instruments—judgements and estimates

IFRS 9/IAS 39 assessing whether an embedded

derivative is closely related to the host contract?

Fixed for fixed—is BIY using its shares as

currency?

Identifying relevant contractual cash flows.

Determining the appropriate discount rate.

Thank you

©IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

41