Embed Size (px)

Citation preview

Session 2 – Implementation challenges – practical experience and challenges for the preparer

prof. nadzw. dr hab. Radosław Ignatowski Department of Accounting, Faculty of Management, University of Łódź

Presentation prepared for the conference on IFRS: The changes and challenges for preparers and users of financial statements in the European

Union – sharing practical experiences The World Bank Centre for Financial Reporting Reform, Warszawa, December 2013

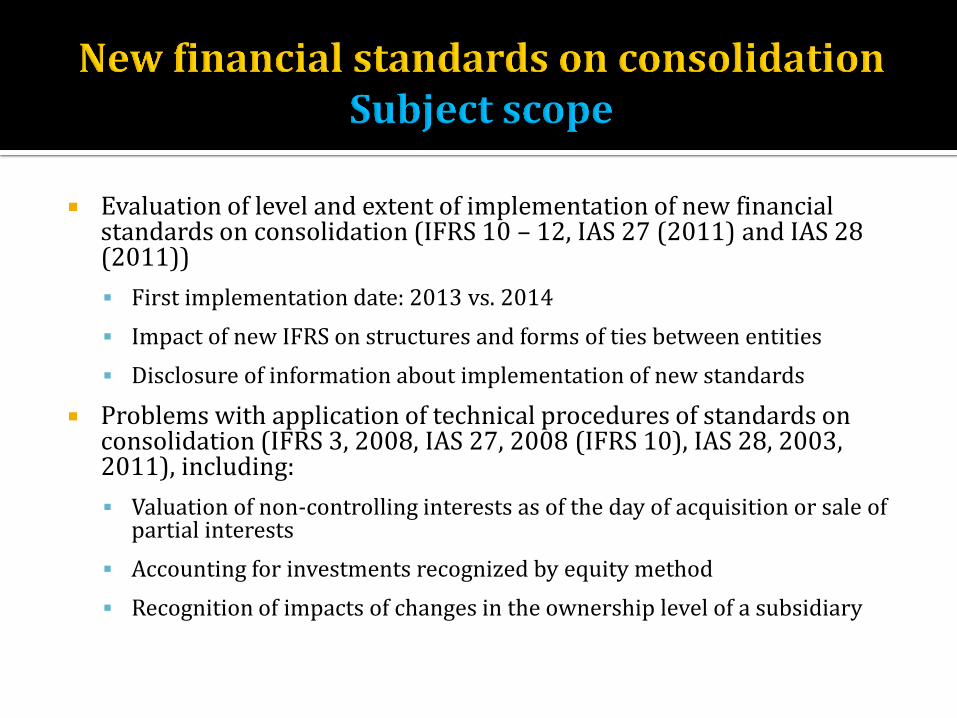

Evaluation of level and extent of implementation of new financial standards on consolidation (IFRS 10 – 12, IAS 27 (2011) and IAS 28 (2011))

First implementation date: 2013 vs. 2014

Impact of new IFRS on structures and forms of ties between entities

Disclosure of information about implementation of new standards

Problems with application of technical procedures of standards on consolidation (IFRS 3, 2008, IAS 27, 2008 (IFRS 10), IAS 28, 2003, 2011), including:

Valuation of non-controlling interests as of the day of acquisition or sale of partial interests

Accounting for investments recognized by equity method

Recognition of impacts of changes in the ownership level of a subsidiary

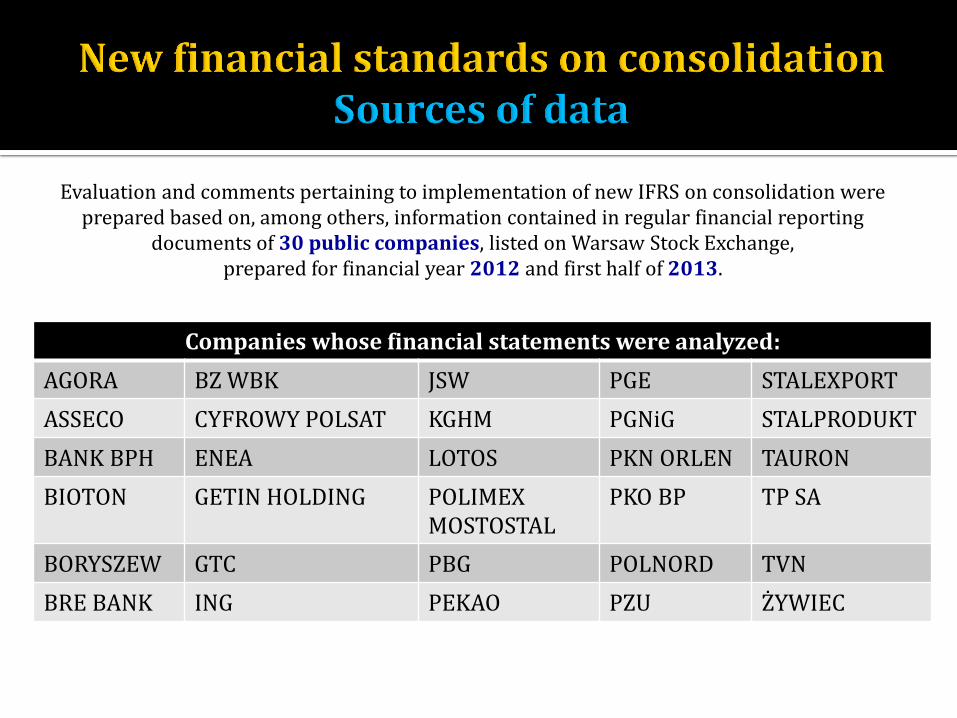

Evaluation and comments pertaining to implementation of new IFRS on consolidation were prepared based on, among others, information contained in regular financial reporting

documents of 30 public companies, listed on Warsaw Stock Exchange, prepared for financial year 2012 and first half of 2013.

Companies whose financial statements were analyzed:

AGORA BZ WBK JSW PGE STALEXPORT

ASSECO CYFROWY POLSAT KGHM PGNiG STALPRODUKT

BANK BPH ENEA LOTOS PKN ORLEN TAURON

BIOTON GETIN HOLDING POLIMEX MOSTOSTAL

PKO BP

TP SA

BORYSZEW GTC PBG POLNORD TVN

BRE BANK ING PEKAO PZU ŻYWIEC

First implementation date: 2013 vs. 2014

Essentially, most companies decided to defer compliance with new IFRS until 2014. In the group of 30 companies, 20 made this decision, including:

Agora, Asseco, BPH, Getin, GTC, ING, JSW, KGHM, PGE, PGNiG

10 companies decided to comply with IFRS in 2013, including:

BRE, BZ WBK, Enea, Stalexport, TP SA, TVN, Żywiec

Decision about complying in 2013 was probably not influenced by type of subordinated entities

Decision about complying in 2013 was probably influenced rather by the effect of application, or essentially lack of one

Impact of new IFRS on structures and forms of ties between economic entities

Almost in all cases, the impact of new solutions (definition of control) and classification of joint agreement provisions had no impact on changing scope of identified subsidiaries

In the group of 30 companies:

Such were the conclusions drawn by 9 out of 10 companies, which implemented new IFRS in 2013: BRE, BZ WBK, Cyfrowy Polsat, Enea, Polimex Mostostal, Stalexport, Stalprodukt, TVN, Żywiec

TP SA has indicated a change in scope of one entity under joint control to a joint operation

GETIN HOLDING has identified the need for more in-depth consideration of new definition of control in order to determine dependence of certain companies which so far were considered subsidiaries

PZU has indicated that the scope of subordinated entities was expanded so as to include certain investment funds

Almost in all cases, the impact of new solutions (definition of control) and classification of joint agreement provisions had no impact on changing scope of identified subsidiaries

From among the 30 companies, only:

(…)

BPH, GTC, Tauron are still analyzing the impact of new concepts and definitions on scope of entities in the group and other forms of subordination

Asseco, Lotos, PBG, Polnord have not provided relevant information

Insignificant or irrelevant impact of new concepts and definitions on ties with subordinated entities results from :

Significant concentration of capital in subordinated entities:

equity share of mother company is very high,

equity instruments are a fundamental premise for controlling other entities

Low importance of affiliated entities and joint ventures in business strategies of economic entities

number (size) of affiliated entities and joint ventures is disproportionately low compared to subsidiaries and financial data of investors in entities

Most numerous group Asseco (200 companies) has interests in 5 affiliated entities and 2 joint ventures

Second from among the largest groups: GTC (118 companies) has interests in 6 affiliated entities and 5 joint ventures

Disclosure of information about implementation of new standards

General critical area of implementation of new solutions:

▪ Rather frivolous and complacent approach to disclosure requirements set forth in par. 30 and 31 of IAS 8

General critical area of implementation of new solutions:

Rather frivolous and complacent approach to disclosure requirements set forth in par. 30 and 31 of IAS 8

Among the 30 companies:

BPH, GTC, Tauron are still analyzing the impact of new concepts and definitions on the scope of entities in the group and other forms of subordination, as well as their impact on financial statements

Asseco, Lotos, PBG, Polnord have not provided relevant information

(…)

(…)

(…)

(…)

(…)

(…)

General critical area of implementation of new solutions:

There are, nonetheless, numerous cases of high level of accuracy in disclosed information: e.g. : PKN Orlen, Agora, ING, …

(…)

(…)

(…)

(…)

Concept of control, capital group and disclosure of relevant information

Valuation of non-controlling interests as of the day of acquisition or sale of partial interest

Accounting for investments recognized by equity method

Recognizing the impacts of changes in level of equity ownership in the subordinated entity

Concepts and definitions vs. disclosures

Noticeable application of „Ctl C – Ctl V” (copy&paste) method in preparing explanatory notes for financial statements

Certain irregularities determining the composition of a capital group

Certain irregularities in defining fundamental notions

Certain discrepancies in understanding disclosures pertaining to composition of the group

Valuation of non-controlling interests as of the day of acquisition

Noticeable avoidance of fair value measurement and thus recognizing only the „acquired” value of the company:

Does the price paid for 80% shares determine the value of the remaining 20% of shares?

Can market price of shares of public companies be a determinant for the value of non-controlling interests?

Wybrane dane giełdowych spółek

41

Company # of Shares Price/ share (PLN)

Market Value

(mln PLN)

Trades (in ‘000

PLN)

# of Shares traded

% of Shares traded

Asseco 77.565.530 50,00 3.878,3 2.533,6 50.673 0,07

BPH 76.667.911 60,20 4.615,4 4.025,3 66.865 0,09

Cersanit 216.384.043 9,95 2.153,0 228,4 22.955 0,01

Polsat 348.352.836 15,70 5.469,1 67.879,7 4.323.547 1,24

Enea 441.442.578 18,90 8.343,2 2.533,63 134.054 0,03

GTC 219.372.990 19,96 4.159,3 4.950,6 261.107 0,12

KGHM 200.000.000 186,00 37.200,0 156.398,6 840.853 0,42

PKN Orlen 427.709.061 51,15 21.877,3 72.895,0 1.425.124 0,33

TP SA 1.335.649.021 16,90 22,572,5 80.607,9 4.769.696 0,36

TVN 343.673.164 15,76 5,416,3 13.870,1 880.083 0,26

Valuation of non-controlling interests as of the day of change in ownership level

In IAS 27 (2008) and IFRS 10 there is no regulation with respect to the basis for valuation of non-controlling interests as of the day of sale of part of 100% shares owned so far

Does the price received for shares sold determine the initial value of non-controlling interests?

Will fair value of re-identified net assets of the subsidiary constitute the basis for initial value of non-controlling interests?

Valuating profit of bargain purchase under the equity method

Current regulations of IAS 28 in scope of determining value of gains from a bargain purchase are not consistent with regulations pertaining to determining gains from bargain purchase in case of acquisitions

Recognizing impacts of changes in ownership levels of a subsidiary

Regulations of par. 30 and 31 of IAS 27 (2008), as well as par. B96 of IFRS 10 in scope of recognizing results of sale of partial interest in subsidiaries do not provide a complete answer as to how such changes should be recognized?

If the indicated principle is accounting for impacts directly in equity, does it mean recognition on the level of retained profits, or in other items as well?