Embed Size (px)

Citation preview

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 1/83

LOVELY PROFESSIONAL UNIVERSITYDEPARTMENT OF MANAGEMENT

Report on Summer Training

Study of Working Capital Management

of

Gaya Dairy

Submitted to Lovely Professional University

In partial fulfillment of the

Requirements for the award of Degree of

Master of Business Administration

Submitted by: Alok Kumar

Roll No.- RS1901B33

Reg. No.- 10905931

DEPARTMENT OF MANAGEMENT

LOVELY PROFESSIONAL UNIVERSITY

PHAGWARA

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 2/83

CERTIFICATE

This is to certify that the project work entitled “A Study of Working

Capital Management of Gaya Dairy.”Is a piece of bonafide work done

by Alok Kumar, student of Lovely School Of Management, under my

guidance and supervision for the partial fulfillment of the course MBA,

LSM,Jalandhar.

To the best of my knowledge and belief the thesis embodies the work of

the candidate himself and has been duly completed.

Simultaneously, the thesis fulfills the requirements of the rules and

regulations related to the summer internship of the institute and I am

assured that the project is up- to the standard both in respect to the

contents and language for being referred to the examiner.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 3/83

DECLARATION

I hereby declare that the project report entitled “A Study of Working

Capital Management of Gaya Dairy.” Is the produce of my sincere

effort. This Summer Internship Project Report is being submitted by me

alone, at LSM,Jalandhar, for the partial fulfillment of the course MBA,

and the report has not been submitted to any other Educational

institutions or for any other purpose whatsoever.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 4/83

ACKNOWLEDGEMENT

No research can blossom from single person’s mind without proper

guidance, assistance and inspiration from various quarters. My project

was given its present shape by assistance of many people whom I am

greatly indebted to. I express my gratitude and indebtedness toward the

people who helped me during my project work.

This project report is a result of endless effort & immense degree of oil by

many great minds. It was pleasure to work in one of the most valuable

F.M.C.G Company like GAYA DAIRY PROJECT (GAYA).

I express my humble gratitude towards Mr. K.K SHARMA Chief executive

of GAYA DAIRY PROJECT Gaya who treated me as a guide depot for

giving me a chance to pursue my summer training in a prestigious

company.

I express my special thanks to Mr. Shatish Chandra Shukla, General

Manager (Marketing), Magadh diary project Gaya Bihar. Who always gives

me the guidelines time to time during my summer training and they help

me for the completion of my project.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 5/83

I am also thankful to Mr. Anoop Mohanty (Faculty Guide) for providing me

proper inputs and guidance.

I would like to dedicate this work to my college Lovely school of

management,Jalandhar, where I am getting the shape of future Finance

Manager.

Last but not least, I express my gratitude to my parents who financed this

project and have been a moral support to me during this project.

Alok Kumar

Reg. No. 10905931

Lovely School of Mgmt,

Jalandhar,Punjab.

PREFACE

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 6/83

The underlying aim of the summer training in Gaya Dairy is a sincere

attempt to analyze its Working Management by making use of different

financial appraisal techniques. The data for the studies were obtained

from the published annual reports of the company.

Among all the problems of financial management, the problems of

working capital management have probably been recognized as the

most crucial one. It is because of the fact that working capital always

helps a business concern to gain vitality and life strength. The objective

of this study is to critically evaluate working capital management as

practiced in Gaya Dairy.

In this study, a sincere attempt has been made to analyze the

working of Gaya Dairy ltd. by making use of different financial appraisal

techniques like ratio analysis, trend analysis, common-size analysis etc.

The data for the studies were obtained form the published annual reports

of the company.

An effort has been made to appraise the overall financial

performance and efficiency of management, but the scope and depth of

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 7/83

study remained limited due to the limiting factors of time, and resources.

However, it is expected that the study will provide useful information for

better and easier understanding of the financial results of the company.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 8/83

TABLE OF CONTENTS

1. INTRODUCTION

1.1 Overview- Gaya Dairy...................................

1.2 Brief History.....................................................

1.3 Objectives.........................................................

1.4 Organization Structure ....................................

2. OBJECTIVE OF THE PROJECT

2.1 Objective of the study

2.2 Review of literature

3. RESEARCH METHODOLOGY

3.1 Research Methodology..................................

3.2Type of Research............................................

3.3 Sample of design ...........................................

4. SIGNIFICANCE OF THE WORKING CAPITAL

4.1 Introduction of Working Capital................

4.2 Concept of Working Capital.......................

4.3 Importance of Working Capital analysis ..

4.4 Operating and cash conversion cycle.........

4.5 Methods and ratios ....................................

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 9/83

5. ANALYSIS OF WORKING CAPITAL

5.1 Working capital analysis.........................

5.2 Working capital trend analysis...............

5.2 Ratio analysis..........................................

6. CONCLUSION AND RECOMMENDATIONS

6.1 Profitability……………………………

6.2 Working Capital……………………….

REFERENCES

GLOSSARY

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 10/83

ABSTRACT

The summer internship program is under taken after the completion of the

Second semester of the program and faculty supervised.

The summer internship program will equip the students with practical

application skills relevant to various situations.

The summer internship program is an attempt to bridge the gap between

the professional world and the academic institutions. It is a simulation of

the real work environment and enables students to experience the rigors

of a professional organization.

I have completed my 6th week project in Gaya Dairy. I got different type

of knowledge in Gaya Dairy. And met different type of workers in Gaya

Dairy they gave me lot of knowledge day to day about financial system of

Gaya Dairy reported in Gaya Dairy day to day when I did not go to Gaya

Dairy such condition I reported to my faculty guide he has information

about my day to day performance in Gaya Dairy. Now I am mentioning

report which I learned there till now.

I started my project in Gaya Dairy on 18th June Friday and met Mr.

R.N.Mittal who is a Dy. Manager .He gave me a project title “A Study Of

Working Capital Management” and he gave me annual report. Logistic of

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 11/83

procuring milk from various rural areas. And I learned about various types

of milk collection centers. And they collect the milk from different societies

in Gaya distt. in base of (1) Taking Sample (2) Testing Fat and (3) SNF

(Solid Note Fat) and they told me that Society members and Gaya Dairy

follow this system. They take two types of milk, Cow and Buffalo. Also got

an opportunity to learn the Tally system and its advantages in accounting

system.

Friday 18th June 2010, Mr. Kailash Khangarot the corporate guide

briefed about some systems of milk collection in Gaya Dairy :-

(1) Reception dock

(2) Lock Sheet

(3)Online programmed

(4) Variety of milk

(5) Plunger of milk

(6) EMT System

There are one Chilling center under Gaya Dairy. Standard SNF is

8.7% . The Gaya Dairy milk rates will be very important.

Internal Audit is an important part of this system. Mr. R.D.Jat

(Designation Cashier ).briefed about the transaction e.g. telephone,

mobiles, medical claim bills, of the employees and staffs. It is not

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 12/83

more than 20,000 and about deposits, about employee’s salary. How

it is made.

CHAPTER – I

INTRODUCTION

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 13/83

INTRODUCTION

Getting Acquainted With The Dairy Industry In India

Indian Dairy Scenario:-

Lot of Indian people start day with tea & milk. Milk is an essential factor of

our daily life. Indian milk business is very old business. Dairy business

adopt modern concept in 1970 with the help of national dairy develop

board through operation flood plan. in first section of this plane, ten state

selected.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 14/83

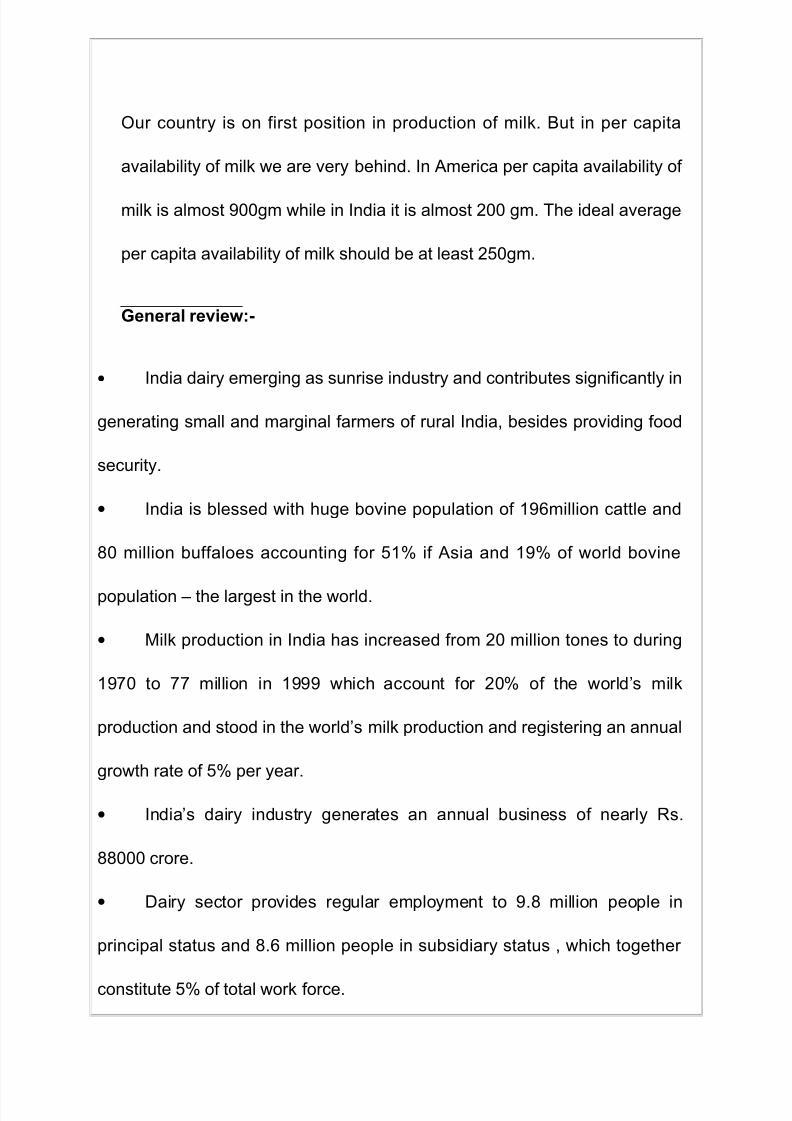

Our country is on first position in production of milk. But in per capita

availability of milk we are very behind. In America per capita availability of

milk is almost 900gm while in India it is almost 200 gm. The ideal average

per capita availability of milk should be at least 250gm.

General review:-

• India dairy emerging as sunrise industry and contributes significantly in

generating small and marginal farmers of rural India, besides providing food

security.

• India is blessed with huge bovine population of 196million cattle and

80 million buffaloes accounting for 51% if Asia and 19% of world bovine

population – the largest in the world.

• Milk production in India has increased from 20 million tones to during

1970 to 77 million in 1999 which account for 20% of the world’s milk

production and stood in the world’s milk production and registering an annual

growth rate of 5% per year.

• India’s dairy industry generates an annual business of nearly Rs.

88000 crore.

• Dairy sector provides regular employment to 9.8 million people in

principal status and 8.6 million people in subsidiary status , which together

constitute 5% of total work force.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 15/83

• Dairy development owes much to the an and pattern of cooperative.

• The dairy infrastructure now comprises 26 states federation, 170

district milk unions and around 100000 village cooperative societies, through

which rural milk production and procurement system have been effectively

linked to urban markets consumption centers.

• Of every 100 litres of milk produced, 44 liters were retained by the

rural fold and 56 liters were the marketable surplus for the urban area. Of

which only 10 liters was handled by the organized sector cooperative and

remaining by traditional sector.

• Operation flood brought milk revolution in the country by transforming

dairying into a core economic activity. The main challenges before the

Indian dairy sector to improving quality, developing international

accepted products and stepping up global marketing strategy.

• The future of Indian dairy industry is promising, since its de-licensing in

1992,the interest of multinationals and Indian corporate in the industry

has been growing, and the industry’s growth potential is high as there is

sufficient domestic demand and good scope for exports of milk and milk

products.

• India is emerging as one of the largest and fastest growing consumers

market in the world with high income elasticity of demand of dairy

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 16/83

product. Indian dairying is energy –efficient, labor intensive and

ecological sound.

• Over 80% of milk sold in urban & semi urban areas is non –pasteurized

from unorganized sector. The overall market for liquid milk is growing

4% per anum.

Similarly in Bihar there is a co-operative federation, known as the Bihar

co-operative dairy federation (BCDF) which provides the milk to whole

Rajasthan with the help of the dairy unions, established in the different

parts of the state.

INTRODUCTION ABOUT COMFED

Dairy development was initiated by the state government in the early

seventies under the auspices of Bihar State Co-Operative Milk Producers

Federation Ltd. (COMFED) registered in 1975. two year later COMFED

assumed responsibility for many of the function of BSDDC. It became the

nodal agency for implementation of operation flood in the state.

Bihar State Co-Operative Milk Producers Federation Ltd. (COMFED) set

up in 1977 as the implementing agency for dairy development programs

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 17/83

in Bihar is registered as a society under the Rajasthan cooperative

societies 1965.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 18/83

HISTORY OF MAGADH DAIRY PROJECT GAYA DAIRY (GAYA)

Sudha: The origin

The mighty Ganges at its origin is but a tiny stream in the Gadgetry ranges

of the Himalayas. Similar is the story of Sudha which inspired 'Operation

Flood' and heralded the 'White Revolution' in India. Father of white

revolution is Dr. vargis kurian (1973) It began with two village co-

operatives and 250 liters of milk per day, nothing but a trickle compared to

the flood it has become today. Today Sudha collects processes and

distributes over a million liters of milk and milk products per day, during the

peak, on behalf of more than a thousand village cooperatives owned by

half a million farmer members. Further, as Ganga-ma carries the

aspirations of generations for Moksha, Sudha became the symbol of the

aspirations of millions of farmers. Creating a pattern of liberation and self-

reliance for every farmer to follow.

The start of a revolution:

The revolution started as awareness among the farmers that grew and

matured into a protest movement and the determination to liberate

themselves. Over four decades ago, the life of a farmer in Kaira District

was very much like that of his counterpart anywhere else in India. Its

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 19/83

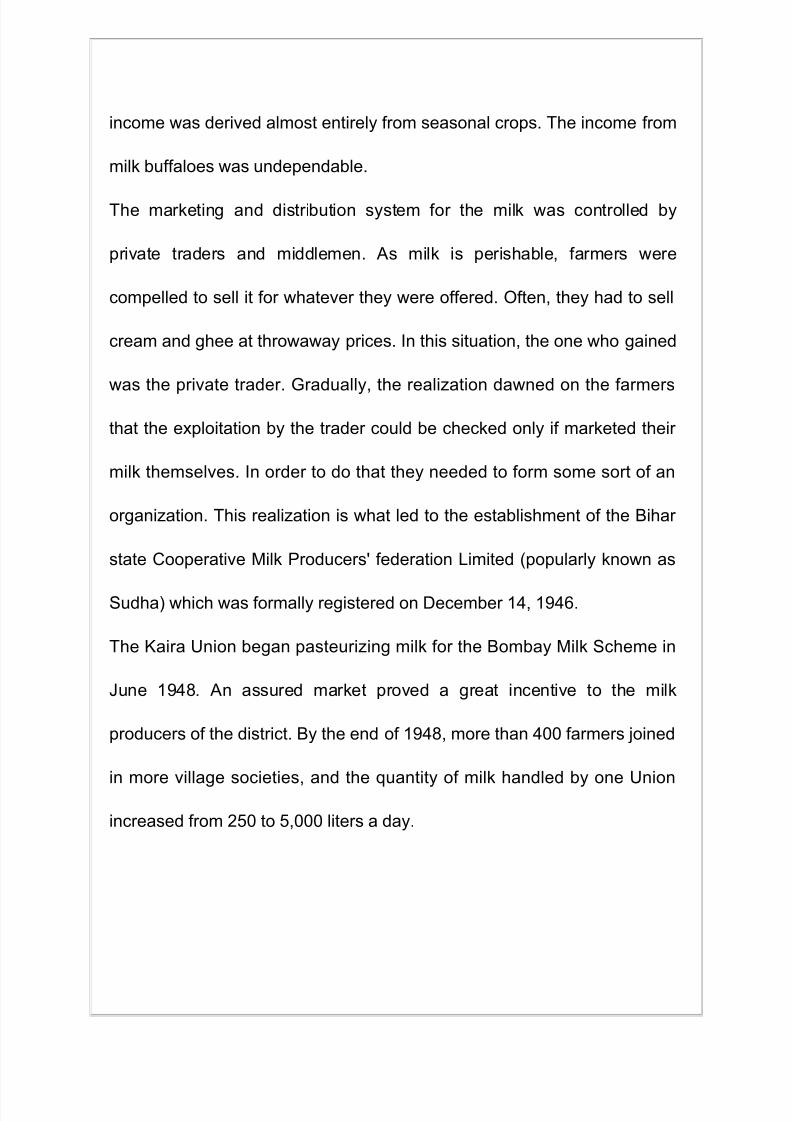

income was derived almost entirely from seasonal crops. The income from

milk buffaloes was undependable.

The marketing and distribution system for the milk was controlled by

private traders and middlemen. As milk is perishable, farmers were

compelled to sell it for whatever they were offered. Often, they had to sell

cream and ghee at throwaway prices. In this situation, the one who gained

was the private trader. Gradually, the realization dawned on the farmers

that the exploitation by the trader could be checked only if marketed their

milk themselves. In order to do that they needed to form some sort of an

organization. This realization is what led to the establishment of the Bihar

state Cooperative Milk Producers' federation Limited (popularly known as

Sudha) which was formally registered on December 14, 1946.

The Kaira Union began pasteurizing milk for the Bombay Milk Scheme in

June 1948. An assured market proved a great incentive to the milk

producers of the district. By the end of 1948, more than 400 farmers joined

in more village societies, and the quantity of milk handled by one Union

increased from 250 to 5,000 liters a day.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 20/83

OBJECTIVES OF ORGANIZATION

The primary concern of Sudha Dairy is to provide best quality and safe

products and services. To achieve this quality objective of Sudha Dairy ltd.are

designed to.

• Meet a well defined needs use and purpose of customer.

• Satisfy customer’s satisfaction for good and safe milk and milk products.

• Comply with applicable national and international slandered.

• Make available milk and milk product at competitive price.

• Ensuring implementation of ISO9002 quality management system.

• Application and adherence of HACCP principles for food safety.

• Motivates employees for professional excellence and participation.

QUALITY POLICY

The dairy believes the delighted customer is the only key for overall

development of the organization and their families.

This is achieved by:

• Education milk producers for clean production.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 21/83

• Manufacturing and supplying milk and milk products and services of

consistent quality at comparative price.

• Adopting innovative and modern technologies and system.

• Developing committed work force.

• Adoption of safety and environment friendly standards with help of

application of HACCP Principles.

ORGANIZATION STRUCTURE

Sudha Dairy is a registered under Bihar cooperative act and is owned by

thousands of its milk producers members. It works on world famous Amul

pattern. As all other cooperative dairies, Sudha Dairy is a part of three tier

structure i.e. dairy cooperative society at village level which form district level

milk producer union which are further federated in state level federation. All

three entities are autonomous and linked to each other by provisions of their

byelaws.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 22/83

The dairy co-operative movement operates on three tier system wherein

farmer members own dairy co-operative societies (DCS) which own district

milk producer's union. The unions collectively own the COMFED.

It is a vertically integrated structure that establishes a direct linkage between

those who produce the milk and

those who consume it.

Federation - Provides service &

support to unions. Marketing

within & outside state, Liaison

with government and NGO

agencies, mobilization of

resources & coordinating & planning programmers / projects.

Union - Develops village milk cooperative network, procures milk from DCS,

processes & markets. Sale of cattle feed and related inputs, promotion of

cross breeding through AI and NS, promotion of fodder development and

general support & supervision to DCS.

DCS - Provides input services (AH, AI) to its members and procurement of

milk.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 23/83

The dairy co-operatives depict the following institutional

FORMULATION OF DCCS AND INTERRELATION WITH SUDHA

DAIRY

FORMULATION OF DCCS AND INTERRELATION WITH SUDHA DAIRY

Milk producers of villages

Management committee of COMFED

(9 members, out of which two from weaker section and one for

woman)

Chairman of COMFED

Board of directors of Sudha Dairy

(total 14 member, including 9 elected members amongst chairmen of

DCSS, out of which 6 from general category, two form weaker section

(bpl, sc/ st etc.) And one from women chairpersons. Rest are

nominated)

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 24/83

CHAPTER – II

OBJECTIVE

OF THE

PROJECT

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 25/83

2.1 OBJECTIVES OF THE STUDY

The main objective of my project is

(A) to study the working capital policy of Gaya dairy, Gaya and to analyze the

trend in working capital for last three years.

(B) to analyze different ratios so to judge the availability and effective usage of

working capital.

2.2 LITERATURE REVIEW

(A) Vishnani S., Shah B. (2007) “Impact of Working Capital Management Policies on

Corporate Performance—An Empirical Study”

It is felt that there is the need to study the role of working capital management policies on

profitability of a company. Conventionally, it has been seen that if a company desires to take

a greater risk for bigger profits and losses, it reduces the size of its working capital in relation

to its sales. If it is interested in improving its liquidity, it increases the level of its working

capital. However, this policy is likely to result in a reduction of the sales volume, therefore of

profitability. Hence, a company should strike a balance between liquidity and profitability.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 26/83

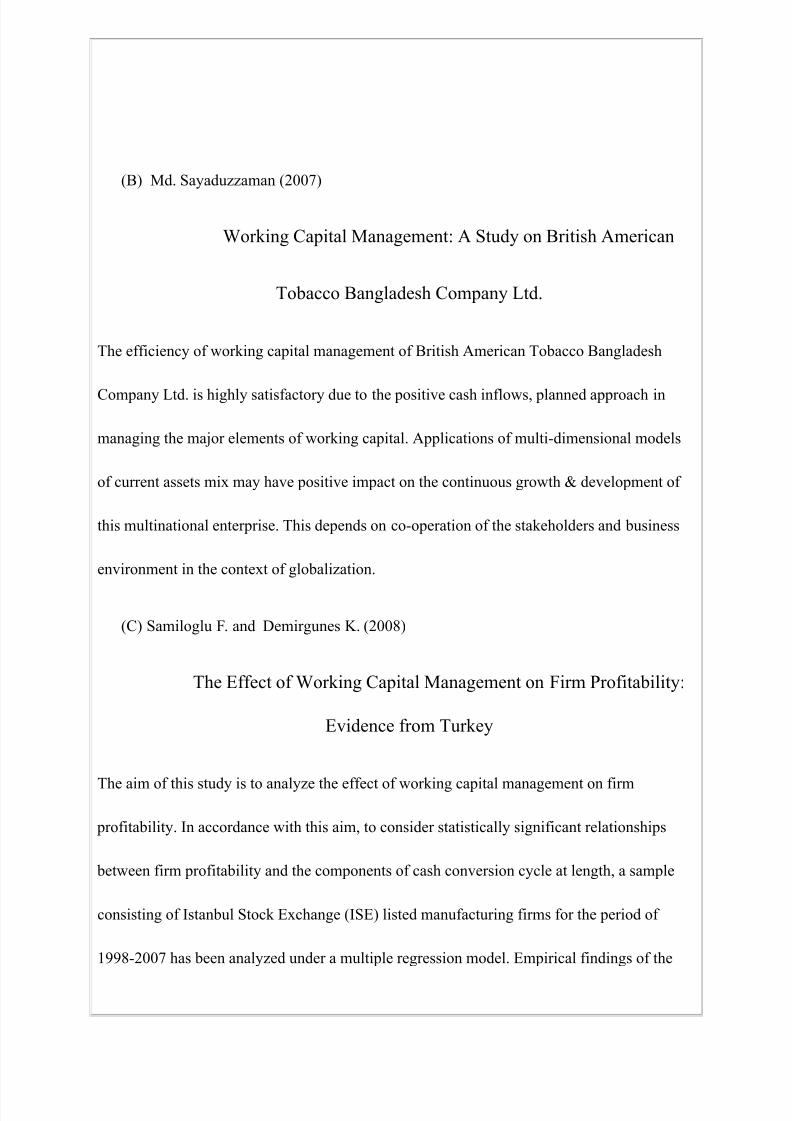

(B) Md. Sayaduzzaman (2007)

Working Capital Management: A Study on British American

Tobacco Bangladesh Company Ltd.

The efficiency of working capital management of British American Tobacco Bangladesh

Company Ltd. is highly satisfactory due to the positive cash inflows, planned approach in

managing the major elements of working capital. Applications of multi-dimensional models

of current assets mix may have positive impact on the continuous growth & development of

this multinational enterprise. This depends on co-operation of the stakeholders and business

environment in the context of globalization.

(C) Samiloglu F. and Demirgunes K. (2008)

The Effect of Working Capital Management on Firm Profitability:

Evidence from Turkey

The aim of this study is to analyze the effect of working capital management on firm

profitability. In accordance with this aim, to consider statistically significant relationships

between firm profitability and the components of cash conversion cycle at length, a sample

consisting of Istanbul Stock Exchange (ISE) listed manufacturing firms for the period of

1998-2007 has been analyzed under a multiple regression model. Empirical findings of the

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 27/83

study show that accounts receivables period, inventory period and leverage affect firm

profitability negatively; while growth (in sales) affects firm profitability positively.

(D) By Beneda, Nancy, Zhang, Yilei (2008)

Working Capital Management, Growth and Performance of New Public

Companies

The current study contributes to the literature by examining impact of working capital

management on the operating performance and growth of new public companies. The study

also sheds light on the relationship of working capital with debt level, firm risk, and industry.

Using a sample of initial public offerings (IPO's), the study finds a significant positive

association between higher levels of accounts receivable and operating performance. The

study further finds that maintaining control (i.e. lower amounts) over levels of cash and

securities, inventory, fixed assets, and accounts payables appears to be associated with higher

operating performance, as well.

(E) Stuttgart/Munich, June 29, 2009

Study on working capital management

Roland Berger Strategy Consultants study on working capital management: Optimizing

current assets helps tap into cash potential and build buffers against insolvency

• Our study entitled "Working capital – Cash for recovery" looks at 216 European

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 28/83

companies with total sales of EUR 3,700 billion and total EBIT of EUR 422 billion

• Presently, the insolvency risk is increasing as higher cash requirements coincide with

reduced cash supply and high financing costs

• Internal sources of finance are becoming more interesting: one of the main lever is

tapping into the cash potential in working capital

• The companies surveyed had a combined potential of EUR 353 billion in Q1 2009,

roughly one third more than in 2008

• Relative to tied-up working capital, utilities and engineered products companies have the

greatest cash reserves hidden in their working capital

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 29/83

CHAPTER – III

RESEARCH

METHODOLOGY

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 30/83

RESEARCH METHODOLOGY

• Research Methodology is a systematically solve the research problem. It

has many dimensions and research methods constitute a part of the

research methodology.

• Thus when we talk about research methodology, we do not only talk of the

research methods but also consider the logic behind the methods. We use

in context of our research study, so that research results are capable of

being evaluated either by researcher himself or by others.

• To effectively carry out in research, I would use the following research

process, which consists of series of actions or steps.

Research comprises of the following steps:-

1. Formulating the research Problem.

2. Research design & Sample Design.

3. Analysis of data gathered

4. Data analysis comparison

5. Graphics and interpret

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 31/83

1 FORMULATING THE RESEARCH PROBLEM

This is the first step under which the problem is stated in general way

and then ambiguities i.e. understanding and rephrasing the problem

thoroughly and rephrasing the same into a meaningful terms from an

analysis point of view.

The research problem under the present project was to study data of

various funds. For this research process was to be formulated and the

execution of which would result in the desired data.

2. PREPARING THE RESEARCH DESIGN

The function of research design is to provide for the collection of

relevant evidences with minimal expenditure of efforts, time and money.

Research Design

• Type of research

•Sample design

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 32/83

TYPE OF RESEARCH

• The type of research under present is an analytical research. In analytical

research; we use tact's or information already available, and analyze these

to make a critical evaluation of the material. Hence the same would be

done.

• In this project I had collected facts, data, and information.

SAMPLE DESIGN

A sample design is a definite plan determined before any data is actually

collected for obtaining a sample. Researcher must select a sample design,

which should be reliable and appropriate for his report.

3. OBSERVATIONAL DESIGN (COLLECTION OF DATA)

Observational design relates to the condition under which the observations are

to be made. Observational design in respect to research. There are several

ways of collecting the appropriate data, which differ considerably in context of

money, time cost and other resources at the disposal of the researcher.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 33/83

Data can be obtained from two important sources:

• Primary data

• Secondary Data

Primary data

Primary data are the data that are collected afresh and for the first time. Thus

happens to be in character. Primary data are collected by the following ways:-

a) Observation

b) Interview

c) Schedule

d) Questionnaire

Secondary Data

Secondary data are the data that are already collected and are only

analyzed by different sources these sources are as follows:-

• Corporate magazine

• Manuals of various companies

• Books, journals, newspaper

• Employment exchange

The secondary data would be collected from financial statement,

journal of national repute, books of national and international author as well as

the annual report of the company. In addition to this internet access will make

the study more effective and meaningful.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 34/83

CHAPTER – IV

SIGNIFICANCE

OF THE

WORKING CAPITAL

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 35/83

SIGNIFICANCE OF WORKIG CAPITAL

Introduction:-

The management of current assets is similar to that of fixed

assets in the sense that in both case that a firm analyses their effects on its

return and risk. The management of fixed and current assets, however, differs

in three important ways: first, in managing fixed assets, time is a very

important factor; consequently, discounting and compounding techniques play

a significant role in capital budgeting and a minor one in the management of

current assets. Second, the large holding of current assets, especially cash,

strenghthens the firm’s liquidity position (and reduces riskiness), but also

reduces the overall profitability. Thus a risk-return trade off is involved in

holding current assets. Third, levels of fixed as well as current assets depend

upon expected sales, but it is only current assets which can be adjusted with

sales fluctuations in the short run. Thus, the firm has a greater degree of

flexibility in managing currents.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 36/83

CONCEPTS OF WORKING CAPITAL

Gross working capital:-

Gross working capital refers to the firm’s

investment in current assets are the assets which can be converted into

cash within an accounting year and include cash , short-term securities,

debtors,(accounts receivable or book debts) bills receivable and stock

(inventory).

Net Working Capital:-

It’s refers to the difference between current assets and current liabilities.

Current liabilities are those claims of outsiders which are expected to

mature for payments within an accounting year and include creditors

(account payable) , bills payable ,and outstanding expenses . Net Working

Capital can be positive or negative. A positive net working capital will arise

when current assets exceed current liabilities .a negative net working

capital occurs when current liabilities are in excess of current assets.

PERMANENT WORKING CAPITAL:-

We know that the need of current assets arises because of the operating

cycle. The operating cycle is a continuous process and, there for, the need

for current assets is felt constantly. But the magnitude of current assets

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 37/83

needed is not always the same; it increases and decreases over time.

However there is always a minimum level of current

assets which is continuously required by a firm to carry on its business

operations. Permanent or fixed, working capital is the minimum level of

current assets. it is permanent in the same way as the firm’s fixed assets

are. Depending upon the changes in production and sales, the need for

working capital, over and above permanent working capital, will fluctuate.

For example extra inventory of finished goods will have to be minted to

support the peak period of sale, and investment in debtors (receivable) may

also increase during such periods. On the other hand, investment in raw

material, work in process and finished goods will fall if the market is slack.

Amount of

working

capital (Rs)

Temporary or

Fluctuating

Time

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 38/83

VARIABLE OR FLUCTUATING WORKING CAPITAL:-

Variable or fluctuating working capital the extra working capital needed

to support the changing production and sales activities of the firm. Both

kinds of working capital –permanent or fluctuating (temporary)-are

necessary-to facilitate production and sales through the operating cycle.

But the firm to meet liquidity requirements that will last only temporary

working capital. In figure illustrates differences between permanent and

temporary working capital. It is shown that permanent working capital is

stable over time, while temporary working capital is fluctuating – some

times increasing and sometimes decreasing. However, the permanent

working capital need not be horizontal if the firm’s requirement for

permanent capital is increasing (or decreasing) over a period

Amount of working

capital (Rs)

Temporary or

Fluctuating

Permanent

Time

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 39/83

FOCUSING ON MANAGEMENT OF CURRENT ASSETS

The gross working capital concept focuses attention on two aspects of

current assets management:

1. How to optimize investment in current assets?

2. How should current assets be financed?

The consideration of the level of investment in current assets

should avoid two danger points- excessive or inadequate investment in

current assets. Investment in current assets should be just adequate to

the needs of the business firm. Excessive investment in current assets

should be avoided because it impairs the firm’s profitability, as idle

investment earns nothing. On the other hand, inadequate amount of

working capital can threaten solvency of the firms because of its inability

to meet its current obligations. It should be released that the working

capital needs of the firm may be fluctuating with changing business

activity. This may cause excess or shortage of working capital frequently.

The management should be prompt to initiate an action and correct

imbalances.

Another aspect of the gross working capital point to the

need of arranging funds to finance current assets. Whenever a need for

working capital funds arises due to the increasing level of business

activity or for any other reason. Financing arrangement should be made

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 40/83

quickly. Similarly, if suddenly, some surplus funds arise they should not

be allowed to remain idle, but should be invested in short- term securities.

Thus, the financial manager should have knowledge of the sources of

working capital funds as well as investment avenues where idle funds

may be temporarily invested.

FOCUSING ON LIQUIDITY MANAGEMENT

Net working capital is a qualitative concept. it indicates the liquidity

position of the firm and suggests the extent to which working capital

needs may be financed by permanent sources of funds. Current assets

should be sufficiently in excess of current liabilities to constitute a margin

or buffer for maturing obligations within the ordinary operating cycle of a

business. In order to protect their interests, short term creditors always

like a company to maintain current assets at a higher level than current

liabilities. It is a conventional rule to maintain the level of current assets

twice the level of current liabilities. However, the quality of current assets

should be considered in determining the level of current assets vis – a –

vis current liabilities. A weak liquidity position poses a threat to the

solvency of the company and makes it unsafe and unsound. A negative

working capital means a negative liquidity, and may prove to be harmful

for the company’s reputation excessive liquidity is also bad. it may be due

to mismanagement of current assets. There for, prompt and timely action

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 41/83

should be taken by management to improve and correct the imbalances

in the liquidity position of the firm.

Networking capital concept also covers the equation of judicious mix of long

term and short term funds for financing current assets. For every firm, there is

a minimum amount of net working capital which is permanent. Therefore, a

portion of the working capital should be financed with the permanent sources

of funds such as equity share capital, debentures, long term debt, performance

share capital or retained earnings. Management must, therefore, decide the

extent to which current assets should be financed with equity capital and/or

borrowed capital.

In summary, it may be emphasized that both gross and net concepts of

working capital are equally important for the efficient management of working

capital. There is no precise way to determine the exact amount of gross or net

working capital for any firm. The data and problems of each company should

be analyzed to determine the amount of working capital. There is no specific

rule as to how current assets should be financed. It is not feasible in practice

to finance current assets by short – term sources only. Keeping in view the

constraints of the individual company, a judicious mix of long and short term

finances should be invested in current assets. Since current assets involve

cost of funds, they should be put to productive use.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 42/83

OPERATING AND CASH CONVERSION CYCLE

The need for working capital to run the day-to-day business activities cannot

be overemphasized. We will hardily find a business firm which does not

require any amount of working capital. Indeed, firms differ in their requirement

of the working capital.

We know that a firm should aim at maximizing the wealth of its shareholders.

In its Endeavour to do so, a firm should earn sufficient return from its

operations. Earning a steady amount of profit requires successful sells

activities. The firm has to invest enough funds in current assets for generating

sales. Currents assets are needed because sales do not convert into cash

instantaneously. There is always an operating cycle involved in the conversion

of sales into case.

There is a difference between current and fixed assets in terms of their

liquidity. A firm requires many years to recover the initial investment in fixed

assets such as plant and machinery or land and building. On the contrary,

investment in current assets such as inventories and debtors [account

receivable] is realized during the firm’s operating cycle that is usually less than

a year.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 43/83

What is an operating cycle?

Operating cycle is the time duration required to convert sales, after the

conversion of resources into inventories, into cash. The operating cycle of a

manufacturing company involve three phases:

• Acquisition of resources such as raw material, labor, power and

fuel etc.

•

Manufacture of the product which includes conversion of raw

material into work-in-progress into finished goods.

• Sales of the products either for cash or on credit. Credit sales

create account receivable for collection.

These phases affect cash flows, which most of the time, are neither

synchronized because cash outflows usually occur before cash inflows. Cash

inflows are not certain because sales and collections which give rise to cash

inflows are difficult to forecast accurately. Cash outflows, on the other hand,

are relatively certain. The firm is, therefore, required to invest in current assets

for a smooth, uninterrupted functioning. It needs to maintain liquidity to

purchase raw materials and pay expenses such as wages and salaries, other

manufacturing, administrative and selling expenses and taxes are there is

hardly a matching between cash inflows and outflow. Cash is also held to meet

to any future exigencies. Stocks of raw material and work –in- process are

kept to ensure smooth production and to guard against non-availability of raw

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 44/83

materials of other components. The firms hold stock of finished goods to meet

the demand of customers on continuous basis and sudden demand from some

customers. Debtors (Accounts Receivable) are created because goods are

sold on credit for marketing and competitive reasons.

Purchase Payment Credit Sale

Collection

RMCP+WIPCP+FGCP

Inventory convention period Receivable conversion price

Gross operation cycle

Payable Net operating cycle

Operating Cycle of a manufacturing firm

Thus, a firm makes adequate investment in inventories, and debtors, for

smooth, uninterrupted production and sale.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 45/83

How is the length of operating cycle determined?

The length operating cycle of a manufacturing firm is the sum of (i)

inventory conversion period (ICP) and (ii) debtors (Receivable)

conversion period (DCP). The inventory conversion period is the total

time needed for producing and selling the product. Typically, it includes:

(a) raw material conversion period (rmcp) ,(b)work-in-process conversion

period (WIPCP), and (c) finished goods conversion period (FGCP). The

debtors’ conversion period is the time required to collect the outstanding

amount from the customers. The total of inventory conversion period and

debtors conversion period is referred to as gross operating cycle (GOC).

In practice, a firm may acquire resources ( such as raw material) on

credit and temporarily postpone payment of certain expenses. Payables,

which the firm can defer, are spontaneous sources of capital to finance

investment in current assets,. The creditors (Payables) deferral period

(CDP) is the length of time the firm is able to defer payments on various

resource purchases. The difference between (gross) operating cycle and

payables deferral period is net operating cycle (NOC). if depreciation is

excluded from expenses in the computation of operating cycle, the net

operating cycle also represents the cash conversion cycle(CCC).it is net

time interval between cash collections sale of the product and cash

payments fore resources acquired by the firm. It also represents the time

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 46/83

interval over which additional funds, called working capital, should be

obtained in order to carry out firm’s operations. The firm has to negotiate

working capital from sources such as commercial banks. The negotiated

sources of working capital financing are called non-spontaneous

sources. If net operating cycle of a firm increases, it means further need

for negotiated working capital.

Let us illustrate the computation of the length of operating cycle.

Consider the statement of cost of sales for a firm given in below-

Statement of Cost of Sales ( Rs in lakh)

ITEMACTUAL

20X1

PROJECTE

D 20X2

1 Purchase of raw material X1 X.2 Opening raw material inventory X2 ..3 Closeing raw material inventory X3 ..4 Raw material consumed (1+2-3) X4 X.5 Direct labour X5 X.6 Depriciation X.. X.7 Other mfg. expences X… X.8 Total cost (4+5+6+7) .. X.

9 Opening work-in-processinventory X.. X.

10 Closing work-in-process inventory … X.11 Cost of production (8+9-10) .. X.12 Opening finished goods inventory .. X.13 Closing finished goods inventory .. X.14 Cost of goods sold (11+12-13) .. X.

15Selling administrtive and gen

expences .. X.

16 cost of sales (14+15) .. X.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 47/83

The firm's data for sales and debtors and creditors are given

below

Sales and Debtors (Rs

in lakh)

ITEM

ACTUAL

20X1

PROJECTE

D 20X2

Sales (Credit) X YOpening balance of debtors X. Y.Closing balance of debtors .. ..opening balance of creditors .. ..closing balance of creditors X. ..

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 48/83

CHAPTER – V

ANALYSIS

OF

WORKING CAPITAL

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 49/83

Gross operating cycle (GOC)

The firm’s gross operating cycle (GOC) can be determined as inventory

conversion period (ICP) plus debtors conversion period (DCP).Thus,

GOC is given as follows:

Gross operating =

Inventory

+

Debtors

Conversion period Conversion period

GOC = ICP + DCP …….. (1)

Inventory conversion period

What determines the inventory conversion period? The inventory conversion

(ICP) is the sum of raw material conversion period (RMCP), work-in-process

conversion period (WIPCP) and finished goods conversion period (FGCP):

ICP = RMCP +WIPCP +FGCP

……(2)

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 50/83

Raw material conversion period (RMCP):- The raw material conversion

period (RMCP) is the average time period taken to convert material in to work-

in-process. RMCP depends on: (a) raw material consumption per day, and (b)

raw material inventory. Raw material consumption per day is given by the

number of days in the year (say, 360). The raw material conversion period is

obtained when raw material inventory is divided by raw material consumption

per day. Similar calculations can be made for other inventories, debtors and

creditors. The following formula can be used:

Raw material Raw material Inventory

Conversion =

Period [Rawmaterial

consumption]/360

RMC RMC*360

RMCP = RMI ÷ =

……(3)

360 RMC

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 51/83

• Work-in-process conversion period (WIPCP):- Work-in-process

conversion period (WIPCP) is the average time taken to complete the

semi-finished or work-in-process. It is given by the following formula:

Work-in-process

Work-in-process Inventory

Conversion =

Period [Cost of production]/360

COP WIPI *360

WIPCP = WIPI ÷ =

……..(4)

360 COP

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 52/83

• Finished goods conversion period (FGCP):-

Finished goods conversion period

(FGCP) is the average time taken to sell the finished goods. FGCP can be

calculated as follows:

Finished goods

Finished goods Inventory

Conversion =

Period [Cost of goods sold]/360

CGI FGI*360

FGCP = FGI ÷ ……..(5)

360 CGS

Debtors (receivable) conversion period (DCP)

Debtors conversion period (DCP) is the average

time taken to convert debtors into cash. DCP represent the average collection

period. It is calculated as follows:

Debtors Debtor Debtors*360

Conversion = = …

(6)

Period (DCP) Creditor sales/360 Creditor sales

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 53/83

Creditors (payables) deferral period (CDP)

Creditors (payables) deferral period (CDP) is the

average time taken by the firm in paying its suppliers (creditors). CDP is given

as follows:

Creditors Creditors Credit*360

Deferral = = …(7)

Period Credit purchases/360 Credit purchases

Cash Conversion or Net Operating Cycle

Net operating cycle (NOC) is the difference

between gross operating cycle and payables deferral period.

Gross Creditors

Net operating = Operating = deferral

Cycle Cycle period

NOC = GOC - CDP

…… (8)

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 54/83

Net operating cycle is also referred to as cash conversion cycle. Some people

argue that depreciation and profit should be excluded in the computation of

cash conversion cycle since the firm’s concern is with cash flow associated

with conversion at contrary view is that a firm has to ultimately recover total

costs should include depreciation, and even the profits. Also, in using the

above-mentioned formulae, average figures for the period may be used.

For example, Table shows detained calculations of the components of a

firm’s operating cycle. Table provides the summary of calculations.

During 20X1 the daily raw material consumption was Rs 12.1 lakh and the

company held an ending raw material inventory of Rs827 lakh. If we assume

that this is the average inventory held by the company, the raw material

consumption the projected raw material conversion period is 60 days. This has

happened because both consumption (Rs 16.5 lakh per day) and level of

inventory (Rs 986 lakh) have increased, but the consumption rate has

increased) by 36.4 percent). Thus, the raw material conversion period has

declined by 8 days. Raw materials are the result of daily raw material

consumption and total raw material consumption and total raw material

consumption and total raw material consumption during a period given the

company’s production targets. Thus, raw material inventory is controlled

through control over purchases and production. We can similarly interpret

other calculations in table below

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 55/83

Table:-Operating Cycle Calculation (Hypothetical Example)

( Rs. In lakh)

Item

Actual

19X1

Projected

19X2

1 Raw Materials Conversion Period

(a) Raw material consumption 4,349 5,932(b) Raw material consumption per

day 12.1 16.5

(c) raw material inventory 827 986(d) Raw material inventory holding

days

68d 60d

2 Work-in-process Conversion Period

(a)cost of production* 5,212 7,051

(b)cost of production per day 14.5 19.6

(c)work-in-process inventory 325 498(d) Work-in-process inventory

holding days

22

d 25d

3 Finished Goods Conversion Period

(a) Cost of goods sold* 5,003 6,582

(b) Cost of goods sold per day 13.9 18.3

(c) Finished goods inventory 526 995

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 56/83

(d)Finished goods inventory holding

days

3

8d 54d

4 Collection period

(a) Credit sales (at cost)** 6,087 8,006

(b) sales per day 16.9 22.2

(c) debtor 735 1,040

(d) debtors outstanding days

4

3d 47d

5 Creditors Deferral Period

(a) Credit purchases 4,653 6,091

(b) purchase per day 12.9 16.9

(c) creditors 454 642

(d) Creditors outstanding day

3

5d 38d*Depreciation is including.**All sales are assumed on

credit.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 57/83

Table :-Summery of Operating Cycle Calculations

(Number of Days)

Actual Projected

GROSS OPERATING CYCLE

1 Inventory Conversion Period

(i ) Raw material 68 60

(ii ) Work- in- process 22 25

(iii ) Finished goods 38

12

8 54

13

9

2 Debtors Conversion Period 43 47

3 Gross operating cycle (1 + 2)

17

1

18

6

4 Payment Deferral period 35 38

NET OPERAING CYCLE (3-4)

13

6

14

8

We note a significant change in the company’s policy for 20X2 with regard

to finished goods inventory. It is expected to increase to 54 days holding from

38 days in the previous year. One reason could be a conscious policy decision

to avoid stock out situations and carry more finished goods inventory to

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 58/83

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 59/83

the firm. The process of measurement and analysis of working capital is

performed on the basis of financial statements of the business

enterprise for past few years.

In the present study the analysis of working capital of Gaya Dairy ltd.

Has been made by two techniques vis., trend analysis and ratio

analysis.

WORKING CAPITAL TREND ANALYSIS

The working capital trend analysis represents a picture of variation in

current assets, current liabilities and working capital over a period of time.

Such an analysis enables us to study upward and downward trend in current

liabilities and its effect on the working capital position. The trend analysis is a

tool of financial appraisal where the changes in the factors are compared with

the base year assuming the base year as 100.

In the present study a statement – showing trend of working capital as well

as its structure has been made. It is it scientific and important study

because each component of working capital has got the relationship of

causes and effects.

Following table below shows the structure and trend of working capital of

Gaya Dairy ltd.during the period under review.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 60/83

STRUCTURE AND TREND OF WORKING CAPITAL OF GAYA DAIRY

DURING 2007 TO 2010

PERTICULAR 2007-2008 2008-2009 2009-2010

CURRENT ASSETS

CASH 322389.24 855819.51 836439.2

BANK 18632795.88 35936348.16 27218462.16

LOAN AND ADVANCES 71220809.88 84836477.65 77115112.92

yDEBTORS 300805197.7 311027760.6 356580000.4

STOCK 377580243.7 427327384.8 465048573.5

TOTAL (A) 768561436.4 859983790.7 926798588.2

CURRENT LIABILITIES

CURRENT LIABILITIES AND

PROVISIONS

526439722 512950750.7 442009648.8

TOTAL (B) 526439722 512950750.7 442009648.8

NET WORKING CAPITAL (A-

B)

242121714.4 347033040 484788939.4

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 61/83

Inference

• Current Assets increase to 20.59% in the year of 2009-2010 as

Compare to in the year 2007-2008.

• Current Liabilities in the year 2009-2010 got decreased by

16.04%. As compared to the year 2007-2008.

• In the year 2008-2009 the growth in working capital was

43.33%

As compare to the year 2007-2008 similarly working capital in

the year 2009-2010 has grown to 100.03% as compared to theworking capital in the year 2007-2008

The analysis shows the effective and efficient management of working

capital by the Gaya Dairy.

RATIO ANALYSIS OF WORKING CAPITAL

Trend analysis shows the trend of current assets, current liabilities and

working capital only. It do not interpret the contribution of each item of

working capital in the trend, whereas, it can be done easily by ratio

analysis. The ratio analysis of working capital can be used by

management as a means of checking upon the efficiency in working

capital management of the company. Following ratio haven used to

analysis and interpret working capital of Gaya Dairy ltd.

Current ratio

Quick ratio

Absolute ratio

Stock or inventory ratio

Working capital turnover ratio

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 62/83

CURRENTRATIO

Current ratio is one of the important ratios used in testing liquidity of a

concern. this is a good measure of the ability of company to maintain

solvency over a short run. This is computed by dividing the total current

assets by the total current liabilities and is expressed as:

The current assets of a firm represent those assets, which can be in the

ordinary course of business, converted into cash within one accounting

year. The current liabilities are defines as obligation maturing within a short

period (usually one accounting year). Excess of current assets over current

liabilities is known as working capital and since these two (current assets

and current liabilities) are used in current ratio therefore, this ratio is also

known as working capital ratio.

With the help of this ratio the analyst can review the extent to which

the company can covert such liabilities with current assets. The current

ratio gives the analyst a general picture of the adequacy of the working

capital of a company and ability of the company to meet its day-to-day

payment obligation. “it likewise measures the margin of safety provided for

paying current debts in the event of a reduction in the values of current

assets.”

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 63/83

The current ratio is very useful as a measure of short terms debt

prying ability but it is tricky to interpret this ratio. Experts are of the view

that the value of current assets should be at least double the amount if

current liabilities.

Walker and Bough have the same view when they ay “a good current

ratio may mean a good umbrella for creditors against the rainy days.”But to

the management it reflects bad financial planning or presence of idle

assets or over capitalization”

IDLE CURRENT RATIO: 2:1

If this ratio is higher than standards than it is assumed

Very good short –term liquidity/solvency.

Excess stocks, bad debts and idle cash.

Under trading

If this ratio is lower than standards than it is assumed

Unsatisfactory short-term liquidity.

Shortage of stocks, less credit sales, shortage of cash.

Over trading

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 64/83

CURRENT RATIO OF GAYA DAIRY LTD.DURING 2007 TO 2010

YEAR

CURRENT

ASSETS

CURRENT

LIABILITIES

CURRENT RATIO

(A) (B) (C) (B)/(C)

2007-2008 768561436.4 526439722 1.46

2008-2009 859983790.7 512950750.7 1.68

2009-2010 926798588.2 442009648.8 2.01

INFERENCE:-

This table reveals that current ratio has increased that is

making improvements in its short term solvency. It is because of increase in

current assets as compared to current liabilities. Still this is lower than

standard current assets ratio that shows a little bit unsatisfactory liquidity

position of the company.

The Current Ratio for the year 2009-2010 has taken the Value of 2.01:1, which

is very satisfactory and as per the standard required (2:1).The current ratio of

2.01:1 indicates, that for every Rs 1 of current liability the company Rs 2 of

current assets, which indicates more liquidity and hence more amount of

working capital.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 65/83

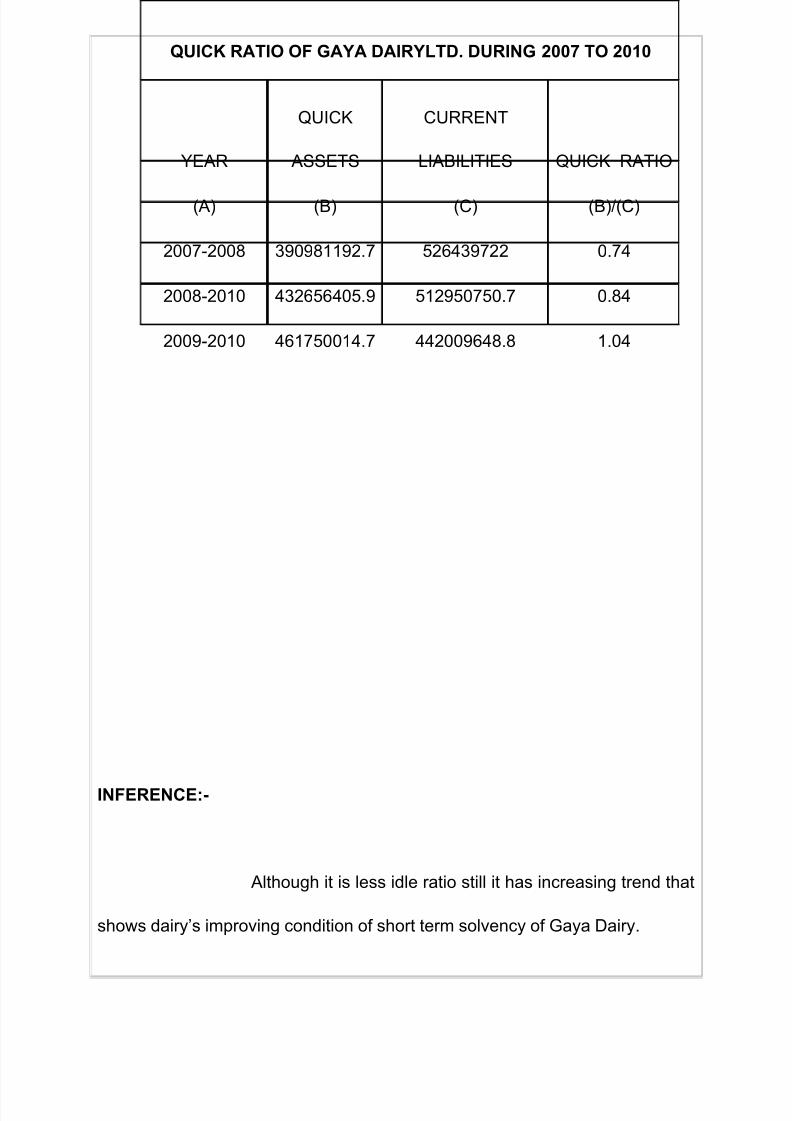

QUICK RATIO

The solvency of a company is batter indicated by quick

Rato.the fundamental this Ratio is to enable the financial management of a

company to ascertain that would happen

If current creditors press for immediate payment and either not

Possible to push up the sales of closing or it id sold, a heavy loss is likely to be

suffered. This problem arises because closing stock is two steps away from

the cash and their price more or less uncertain according to market demand.

The term quick assets include all current assets except inventories and

prepaid expenses. It shows the relationship of quick assets and current

liabilities. The Ratio is calculated as following:

An indicator of a company's short-term liquidity. The quick ratio measures a

company's ability to meet its short-term obligations with its most liquid assets.

The higher the quick ratio, the better the position of the company.

Also known as the "acid-test ratio" or the "quick assets ratio".

IDLE QUICK RATIO 1:1

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 66/83

INFERENCE:-

Although it is less idle ratio still it has increasing trend that

shows dairy’s improving condition of short term solvency of Gaya Dairy.

QUICK RATIO OF GAYA DAIRYLTD. DURING 2007 TO 2010

YEAR

QUICK

ASSETS

CURRENT

LIABILITIES QUICK RATIO

(A) (B) (C) (B)/(C)

2007-2008 390981192.7 526439722 0.74

2008-2010 432656405.9 512950750.7 0.84

2009-2010 461750014.7 442009648.8 1.04

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 67/83

Quick ratio for the year 2009-10 is above the ideal standard. It is 1.04:1, which

indicates that for every Re1 of current liability the company has Rs 1.04 of

current assets, hence the company is in sound position in terms of working

capital position.

ABSOLUTE LIQUDITY RATIO

The absolute liquid ratio between absolute liquid

assets and current liabilities is calculated by dividing the liquid assets and

current liabilities. Expressed in formula, the ratio is:

Cash + Marketable Securities

= Absolute Liquidity Ratio

Current Liabilities

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 68/83

The term liquid assets include cash bank balance and marketable securities, if

current liabilities are to pay at once, only balance of Cash and marketable

securities will be utilized. Therefore, to measure the absolute liquidity of a

business, this ratio is calculated.

IDLE RATIO: 0.5: 1

The idea behind the norm id that if all creditors for demand for payment, at

least 50% of their claim should be satisfied at once.

The table shown on the next page reflects the absolute liquidity ratio Gaya

Dairy Ltd.

ABSOLUTE LIQUIDITY RATIO OF GAYA DAIRYLTD. DURING 2007 TO

2010

YEAR

ABSOLUTE

LIQUID ASSETS

CURRENT

LIABILITIES

ABSOLUTE

RATIO

(A) (B) (C) (B)/(C)

2007-2008 18955185.12 526439722 0.04

2008-2009 36792167.67 512950750.7 0.07

2009-2010 28054901.36 442009648.8 0.06

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 69/83

INFERENCE

This ratio is very below from idle ratio. It is making insecure

creditors claim but it is getting increasing trend. It is needed to maintain this

trend.

Ratios for all the above mentioned years right from 2007 up to 2010 are close

to the standard. For year 2009-10, the ratio is well above the standard, which

indicates the healthy picture of the company in terms of availability of working

capital (quick assets) in order to meet current liabilities.

INVENTORY TURNOVER RATIO

Every firm has to maintain a certain level of inventory of finished good so as to

be able to meet the requirements of the business. But the level of inventory

should neither to be high not to be low. It to high inventory means higher

carrying cost and higher risk of stocks becoming obsolete whereas to low

inventory may mean the loss of business opportunities. it is very essential to

keep sufficient stock in business .

it is express in number of time . Stock turnover ratio or inventory turn over

ratio indicates the no. of times the stock has been turned over during the

period and evaluates the efficiency with which a firm a able to manage its

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 70/83

inventory. This ratio indicates whether investment in stock is with in proper

limit or not.

HIGHER RATIO INDICATES:-

Stock is sold out fast.

Same volume of sales from less stock or more sales from

Same stock

Too high ratio shows stock outs or over trading.

Less working capital requirement.

LOWER RATIO REVEALS:-

Stock a sold out at a slow speed.

Same volume of sale for more stock or less sale from same stock.

More working capital requirement.

Too low ratio show obsolete stock or under trading.

Formula of stock turn over ratio:-

The ration is calculated by dividing the cost of goods sold by the amount of

average stock at cost.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 71/83

Inventory turnover Ratio =

Inventory turn over ratio measures the velocity of

conversion of stock in to sales. Usually a high inventory turnover / stock

velocity indicates efficient management of inventory because more frequently

the stock are sold, the lesser amount of money is required to finance the

inventory. Low inventory turn over ration indicate inefficient management of

inventory. in low inventory turn over implies over investment in inventories, the

business, poor quality of goods, stock accumulation, accumulation of absolute

and slow moving good and low profit as compared to total investment the

inventory turn over ratio is also an index profitability where a high ratio signifies

more profit ‘a low ratio signifies low profit some time a high inventories.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 72/83

INVENTORY TURNOVER RATIO OF GAYA DAIRY LTD.

DURING 2007 TO 2010

YEAR

COST OF

GOOD

SOLD

AVERAGE

INVENTO

RY

INVENTORY

TURNOVER(TIM

ES)

INVENTORY

TURNOVER(DA

YS)

(A) (B) (C)

(D) = (B)/

(C) (E)= 365/D

2007-

2008

295507603

1

377580243

.7 7.83 46.64

2008-

2009

350101435

0

427327384

.8 8.19 44.55

2009-

2010

399510464

1

465048573

.5 8.59 42.49

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 73/83

INFERENCE:-

As compared to year 2007-2008, in the year 2008-

09, the inventory turnover increased to 8.19 times. Similarly, in the year 2009-

10 it increased to 8.59 times, which indicates that the times taken in converting

raw material into finished product and finally selling it got reduced considerably

and hence indicates quick release of working capital

WORKING CAPITAL TURNOVER

A measurement comparing the depletion of working capital to the generation

of sales over a given period. This provides some useful information as to how

effectively a company is using its working capital to generate sales.

A company uses working capital (current assets - current liabilities) to fund

operations and purchase inventory. These operations and inventory are then

converted into sales revenue for the company. The working capital turnover

ratio is used to analyze the relationship between the money used to fund

operations and the sales generated from these operations. In a general sense,

the higher the working capital turnover, the better because it means that the

company is generating a lot of sales compared to the money it uses to fund

the sales.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 74/83

WORKING CAPITAL RATIO OF GAYA DAIRYLTD. DURING 2007

TO 2010

YEAR NET SALES

WORKING

CAPITAL

CURRENT

RATIO

(A) (B) (C) (B)/(C)

2007-2008

320751031

4 242121714.4 13.24

2008-2009

374780503

1 347033040 10.8

2009-2010

426614396

5 484788939.4 8.8

INFERENCE:

In spite of an increase in Net Working Capital, the Working

capital turnover ratio of Gaya Dairy got reduced to 10.8 times in the year 2008-

2009, as compared to the year 2007-08. Similarly, in the year 2009-10, the

working capital turnover ratio further reduced to 8.8 times as compared to

13.24 times in the year 2009-10. The reduction in working capital turnover ratio

is on account of massive growth in net working capital as compared to a slight

growth in the sales of the company.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 75/83

CHAPTER – VI

CONCLUSION

AND

RECOMMENDATIONS

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 76/83

CONCLUSION AND RECOMMENDATION

Financial analysis is analysis of financial statements of and

enterprise. Financial statement reorganized collection of data according to

logical and constituent accounting procedures. How ever financial statements

in their traditional from giving historical data and information are of little us to

these who use them to draw certain conclusion.

Financial appraisal is scientific evaluation of profitability

and financial strength of any business concern. Financial appraisal techniques

include ratio analysis, common size analysis, trend analysis, fund flow analysis

etc. these techniques may be applied in the financial appraisal of any entity

and Gaya Dairy ltd. Is no exception to it.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 77/83

PROFITABILITY

The measurement of profitability is a tool of overall measurement of efficiency

an overall study profitability of Gaya Dairy has been Dade in relation to sales

operating assets capital employed and its net worth.

By analysis the working result i.e. Profit and loss account of Gaya Dairy ltd. It

was found that the net profit before interest and tax of the Gaya Dairy is

showing increasing trends. This is very good for Gaya Dairy ltd. The increase

in the profits is nearly 24% more then previous year the reason is good sales

growth between years. For this following suggestion should be considered.

• Proper cost control is required and cost control technique should be

adopted for it.

• Operating expenses, admn. Expenses should be specially considered to

be reduced.

• Inventory is the biggest items of balance sheet that must have

demanded a large amount of maintaining cost. So efficient inventory

management should be done. Inventory should be reduced extent that

would help to recover blocking money in inventory.

• The service staff should be given proper training and better environment

for work.

• Proper advertisement and sales promotion is required.

• Dairy has to pay large fix interest charged. Hence long term borrowing

should be reduced so that the earning are satisfactorily earmarked with

them.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 78/83

Working capital

• In the year 2008-2009 the growth in working capital was 43.33% as

compare to the year 2007-2008 similarly working capital in the year

2009-2010 has grown to 100.03% as compared to the working capital in

the year 2007-2008. The management should follow the same trend

in near future too so to have considerable appreciation in working

capital every year.

• The Current Ratio for the year 2009-2010 has taken the Value of 2.01:1,

which is very satisfactory and as per the standard required (2:1).The

current ratio of 2.01:1 indicates, that for every Rs 1 of current liability the

company Rs 2 of current assets, which indicates more liquidity and

hence more amount of working capital. The company need to further

enhance the value of ratio.

• Quick ratio for the year 2009-10 is above the ideal standard (1:1). It is

1.04:1, which indicates that for every Re1 of current liability the

company has Rs 1.04 of current assets, hence the company is in sound

position in terms of working capital position. It would be better for the

company if in near future it could further enhance the value of the

ratio

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 79/83

• Absolute quick ratio for the years right from 2007 up to 2010 are close

to the standard. For year 2009-10, the ratio is well above the standard

(0.5:1), which indicates the healthy picture of the company in terms of

availability of working capital (quick assets) in order to meet current

liabilities. The same position should be sustained in near future too.

• As compared to year 2007-2008, in the year 2008-09, the inventory

turnover increased to 8.19 times. Similarly, in the year 2009-10 it

increased to 8.59 times, which indicates that the times taken in

converting raw material into finished product and finally selling it got

reduced considerably and hence indicates quick release of working

capital. In near future it would be more profitable for the company, if

the value of ratio gets increased to 11- 14%.

• In spite of an increase in Net Working Capital, the Working capital

turnover ratio of Gaya Dairy got reduced to 10.8 times in the year 2008-

2009, as compared to the year 2007-08. Similarly, in the year 2009-10,

the working capital turnover ratio further reduced to 8.8 times as

compared to 13.24 times in the year 2007-08. The reduction in working

capital turnover ratio is on account of massive growth in net working

capital as compared to a slight growth in the sales of the company. The

value of ratio could be better in near future , if the growth in sales

matches with the growth in net working capital.

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 80/83

BIBLIOGRAPHY

I.M.Pandey, (1978), financial management, Ninth addition, UBS

Publication New Delhi.

Van Horn,(2002),Financial Management and Policy,12 th edition,

Publisher Dorling Kindersley India ltd.

Horne Wwachonicz, J.R.Bhaduri (2005), Fundamentals and Financial

management, 12 th edition, Pearson publisher.

MY Khan, P.K.Jain (1981), Financial Management,5 th edition, Publisher

Mc graw hill companies.

Financial statement for the year ended 2007-08 as obtained from Gaya

Dairy

Annual-Report 2006-07 of Gaya Dairy.

Financial dailies.

Economic Times

Business Standard

Business Magazines

Business India

8/8/2019 Capital Manageemnt - Alok

http://slidepdf.com/reader/full/capital-manageemnt-alok 81/83

GLOSSARY

1) HACCP: HACCP stands for Hazard Analysis and Critical Control Points.

HACCP is an industry-wide effort approved by the scientific community as