Embed Size (px)

Citation preview

Indian Journal of Economics & Business, Vol. 12, No. 1, (2013) : 1-12

* College of Business Administration, Central Michigan University, Mt Pleasant, MI 48859

CAPITAL FLOWS, DEGREE OF OPENNESS ANDMACROECONOMIC VOLATILITY

DEBASISH CHAKRABORTY* AND VIGDIS BOASSON*

Abstract

This paper examines the effects of capital inflow on the volatility of output and priceusing panel data. The major contribution of the paper lies in incorporating the effectsof degree of financial openness in analyzing the effects of capital flows onmacroeconomic volatility. Specifically the paper investigates whether the degree offinancial openness influences the impact of capital flows on macroeconomic volatility.Our model uses the KOF globalization index as a proxy for openness. Our resultsshow that as financial openness increases, the capital inflow has less impact onmacroeconomic volatility. This could be due to an increase in the proportion of directforeign investment compared to portfolio investment and with a highly integratedbanking sector the possibilities of a currency and maturity mismatch are lower.

JEL Codes F36 F62 and F65

Keywords: Economic Globalization, Economic Integration, Capital Flows, FinancialLiberalization

1. INTRODUCTIONThere is a great deal of debate among economists about the effects of internationalcapital inflow on economic growth and stability. IMF and the World Bankspearheaded the arguments that developing countries need to open up their capitalaccount in an orderly, deliberate and sustainable fashion in order to accelerateeconomic growth. They also argue that international capital flows also help withmacroeconomic stability. The higher growth results from efficient allocation ofresources and the reduction of macroeconomic volatility came from the ability tosmoothly borrow and lend internationally in response to domestic economicconditions. However, economic data suggests that international capital flows alsoincreases volatility of output, consumption and exchange rates. So often instead ofincreasing macroeconomic stability (as argued by the IMF and the World Bank),capital flows can actually increase macroeconomic instability, at least in the shortrun. This tradeoff between growth and volatility has led to intense debates amongpolicy planners about the efficiency of opening up of the capital account.

2 Debasish Chakraborty and Vigdis Boasson

This paper addresses this debate by investigating the effects of capital inflowon the volatility of output and price using panel data. The major contribution of thepaper lies in incorporating the effects of degree of financial openness in analyzingthe effects of capital flows on macroeconomic volatility.Specifically the paperinvestigates whether the degree of financial openness influences the impact of capitalflows on macroeconomic volatility. Our model uses the KOF globalization index asa proxy for openness. The KOF globalization index is a weighted average economic,political and social openness.

The paper is organized in the following manner. Section 2 provides a survey ofliterature on the effects of capital flows on economic growth and volatility, section3 discusses the data and methodology, section 4 deals with the empirical analysisand section provides the summary and the conclusions of this paper. The paperconcludes that as financial openness increases, the capital inflow has less impacton macroeconomic volatility. This could be due to an increase in the proportion ofdirect foreign investment compared to portfolio investment and with a highlyintegrated banking sector the possibilities of a currency and maturity mismatchare lower.

2. SURVEY OF LITERATUREIt has been argued that financial openness helps augment the level of domesticresources that are crucially needed for economic growth. However, it is also truethat financial openness and the surge in capital inflow contributes to macroeconomicvolatility, especially in developing and emerging economies. The most common effectof a surge in capital inflow is appreciation in the exchange rate. Under a flexibleexchange rate this appreciation comes via the appreciation of the nominal exchangerate. Under fixed exchange rate, a surge in capital flows lead to an expansion ofmoney supply and liquidity, which results in an increase in aggregate demand,increase in the price of non-tradable goods, and inflation. Thus the surge in financialflows has the potential of derailing the economic reform process of the typerecommended by the IMF and the World Bank.

An increase in capital inflow and the consequent surplus in the capital accountareoften matched by a simultaneous deficit in the current account. This deficit incurrent account could be due to increase in private consumption (as in Latin America)or private investment (as in Asia). So a surge in capital inflow, in addition to itsimpact on exchange rate and inflation, thus, has some direct effect on consumption,investment and output. The impact on volatility depends largely on the compositionof the capital flows. It has been argued that the volatility will be less pronounced ifthe proportion of foreign direct investment is higher than portfolio investment.Macroeconomic volatility resulting from surge in capital inflow also increases ifthe possibility of currency mismatch (bank liabilities denominated in foreigncurrencies and bank assets denominated in local currency) and maturity mismatch(bank liability is mainly short term in nature and bank lending is long term innature) higher.

Capital Flows, Degree of Openness and Macroeconomic Volatility 3

Since capital flows impacts both economic growth and macroeconomic stability,it is critical to weigh in the effects on each one of them before adopting a formalpolicy of opening up the economy. This section provides a brief summary of theeffects of capital flows on economic growth. However, the survey of literature onthe effects of capital flows on volatility is much more extensive, since that is thethrust of this paper.

2a. Effect of Capital Account Liberalization on Economic GrowthThere is mixed evidence on the effects of capital account liberalization on economicgrowth. Licchetta (2006) summarizes the findings of fifteen recent studies on theeffects of capital account liberalization on economic growth as shown in Table 1 asfollows:

Table 1Capital Account Liberalization and Economic Growth

Study # of countries Years Effecton Growth

Alesina, Grilli and Ferretti (1994) 20 1950-89 No effect

Grilli and Ferretti(1995) 61 1966-89 No effectQuinn (1997) 58 1975-89 Positive

Kraay (1998) 117 1985-1997 No effect/mixedRodrik (1998) 95 1975-89 No effect

Klein and Olivei (2000) Up to 92 1986-95 MixedChanda (2001) 116 1976-89 Mixed

Arteta, Eichengreen, Wypolosz (2001) 51-59 1973-92 MixedBekaert, Harvey, Lundblad (2001) 30 1981-97 Positive

Edwards (2001) 62 1980s No effects on poorcountries

O’Donnel 94 1971-94 No effect/mixed

IMF 38 1980-99 Positive/not significantReisen and Soto(2001) 44 1986-1997 Mixed

Edison, Levine, Ricci, Slok (2002a) Up to 89 1973-1995 MixedEdison, Levine, Ricci, Slok (2002b) 57 1980-2000 No effect

Source: Prasad et al. (2003), IMF (2001) and Edison et al. (2002a): reproduced fromLicchetta(2006).

2b. Effects of Capital Account Liberalization on Macroeconomic VolatilityThe effect of capital account liberalization on macroeconomic volatility is similarlymixed. Mendoza (1994) uses a stochastic dynamic business cycle model and findsvery little connections between financial openness and volatility of output andconsumption. He however finds that if the shocks are big and prolonged than outputand consumption volatility increases with degree of financial openness. Baxter andCrucini (1995) find that with increased financial openness output volatility increases

4 Debasish Chakraborty and Vigdis Boasson

but consumption volatility falls (both consumption and relative consumptionvolatility). Possible reason for these differences can be attributed to wealth effecton consumption and the interaction of these assets on the implications of theseeffects on the risks associated with different assets structures.

Sutherland (1996), Senay (1998) and Buch, Dopke and Pierdzioch (2002) usesdynamic stochastic stick-price models and all these studies conclude that the impactof financial openness on macroeconomic volatility depends on some exogenousshocks. In the case of monetary shocks volatility of output increases; In the case offiscal shocks volatility of output decreases. In the case of monetary shocks volatilityof consumption decreases, while in the case of fiscal shocks the volatility ofconsumption increases.

The impact of financial openness on Macroeconomic volatility can be alsoexplained by the structural conditions of the economy. If a country embarking uponfinancial openness has a limited diversification of exports and imports, then financialopenness could contribute to macroeconomic volatility through its impact on theterms of trade and foreign demand shocks. Kose (2002) examines these effects byinspecting the effects on the terms of trade and Senhadji (1998) examines the roleplayed by foreign demand shocks.

Countries where the level of financial openness is not that deep and countrieswhich are highly indebted often can experience capital flow reversal which couldlead to fierce macroeconomic volatility. Also in these countries, changes in the worldinterest rate could trigger serious macroeconomic volatility.Aghion, Banerjee, andPiketty (1999) and Caballero and Krishnamurthy (2001) shows the relationshipbetween financial openness and macroeconomic volatility by focusing on countrieswith not so developed financial markets and countries who are highly indebted.

Financial openness seems to have more impact on small countries than largecountries. Head (1995) and Crucini (1997) made the case that productivity shifts inlarge countries contribute to macroeconomic volatility in small countries.Kose andPrasad (2002) financial openness contributes to macroeconomic volatility much morein small countries (population below 1.5 million) than other developing countries.

Kaminsky and Reinhart (1999) and Glick and Hutchinson (1999) showed thatcountries starting financial liberalization experienced high volatility in output andconsumption due to sudden loss of access to global financial markets.Mendoza (2002)and Arellano and Mendoza (2002) however, shows that sudden stop in access tofinancial markets did not cause any sever macroeconomic volatility.

Razin and Rose (1994) uses cross section data to estimate volatility and foundno significant link between financial openness and macroeconomic volatility. Theyalso argue that financial openness seems to amplify monetary shocks and dampensfiscal shock.

Easterly, Islam and Stiglitz (2004) uses 2 periods panel OLS and IV methodand concludes that neither the level nor the volatility of private capital flows have

Capital Flows, Degree of Openness and Macroeconomic Volatility 5

any significant impact on output growth volatility.Koseand Plummer (2003) use asample of 76 countries over a period of 1960-1999. He uses two indicators of financialopenness: (a) dummy variable for capital account restrictions and (b) private capitalflows. Financial openness is not significant in explaining output and consumptionvolatilities. Financial openness has a significant and non-linear impact on relativeconsumption volatilities (ratio of consumption to output volatilities).

Eozenou Patrick (2008) uses GMM –IV panel estimation method as proposedby Arellano and Bover (1995) and Blundell and Bond (1998) to estimate the followingtwo equations:

�i,j,t = ��i,j,t-1 + �1Q’i,t + �2FDi,t+ �i + �i,t (2)

�i,j,t = ��i,j,t-1 + �1Q’i,t + �2FDi,t + �3FIi,t + �4 (FDi,t*FIi,t) + �i + �i,t (3)

Where j = Y, C and C+G;

Q’i,t are a set of control variable;

FDi,t is a measure of financial development;

FIi,t is a measure of financial openness.

They concluded that lagged dependent variable has significant and positiveeffects on volatility in terms of trade volatility and share of agricultural sector onGDP (all control variables). It also has a positive impact on output growth volatility.However, these terms have no impact on consumption growth volatility. They foundevidence to show that financial openness has a positive impact on output growthvolatility up to a certain level of financial development, but the coefficient is notstatistically significant.The marginal impact of financial development onconsumption is negative for both private and total consumption growth volatility.Themarginal impact of financial openness on consumption is positive for both privateand total consumption growth volatility. Both these coefficients are not significant.So taken independently, each of these two variables has no impact on consumptiongrowth volatility. However inclusion of the interaction term matters. B3 is positiveand significant. B4 is a significant negative coefficient. This suggests that as financialdevelopment increases, the positive impact of financial openness on consumptionvolatility becomes weaker. Financial integration has a positive impact onconsumption volatility when financial development is low, but when financial systemis strong enough, then financial integration lowers consumption volatility. Thispaper concludes that the impact of financial development on consumption dependsupon the level of financial development.

3. METHODOLOGY AND DATASeveralempirical concerns help determine the choice of our econometric model:(i) the potential endogeneity of the domestic savings; (ii) the dynamic relationshipbetween domestic savings and investment as both are impacted by the prior valuesof each other; and (iii) unobserved country- specific effects.1 This leads us to specify

6 Debasish Chakraborty and Vigdis Boasson

the dynamic panel GMM estimator proposed by Arellano and Bond (1991) toovercome these potential issues. According to this technique, the model istransformed in two-step GMM estimator to eliminate the fixed effects to deriveunbiased and consistent estimates. Under this transformation, the lagged valuesof the endogenous variables are used as suitable instruments to overcome thepotential endogeneity problem.

For the measure of volatility, we use the measure employed by Rodrik (1998)and Iverson (2001). Thus volatility is measured by standard deviation of theconcerned economic aggregate. To measure output volatility we use the standarddeviation of real GDP and to measure price volatility we use the GDP deflator. Inorder to maintain sufficient number of data for empirical analysis we use the fiveyear period standard deviation.

We estimate the following two equations in the paper:

Output Volatility

�� � � �� � �� � � � � � � �

10 1 2 3 4 ( )it itGDP GDP it it it it itKF G G KF (4)

Where �GDP is the five-year standard deviation of real GDP;

KF is the capital flow;

G is the globalization index.

Price Volatility

�� � � �� � �� � � �� � � �

10 1 2 3 4 ( )it itPR PR it it it it itKF G G KF (5)

Where �PR is the five-year standard deviation of GDP deflator;

KF is the capital flow;

G is the globalization index.

Panel DataWe collected macroeconomic indicator data on real GDP, GDP deflators, and CPIacross 208 countries for the time-seriesof 1966 – 2009 from the World Bank’sdatabase called “World Databank”. We computed five-year movingstandarddeviations on real GDP growth rates, GDP deflators, and CPI for the period of 1970- 2009. We then matched our volatility variables with the 2012 KOF Index ofGlobalizationacross 208 countries for the time-series of 1970 – 2009. This yielded apanel dataset with 8320 observations. KOF Index of Globalization was introducedin 2002 (Dreher, 2006) and is updated and described in detail in Dreher, Gastonand Martens (2008).

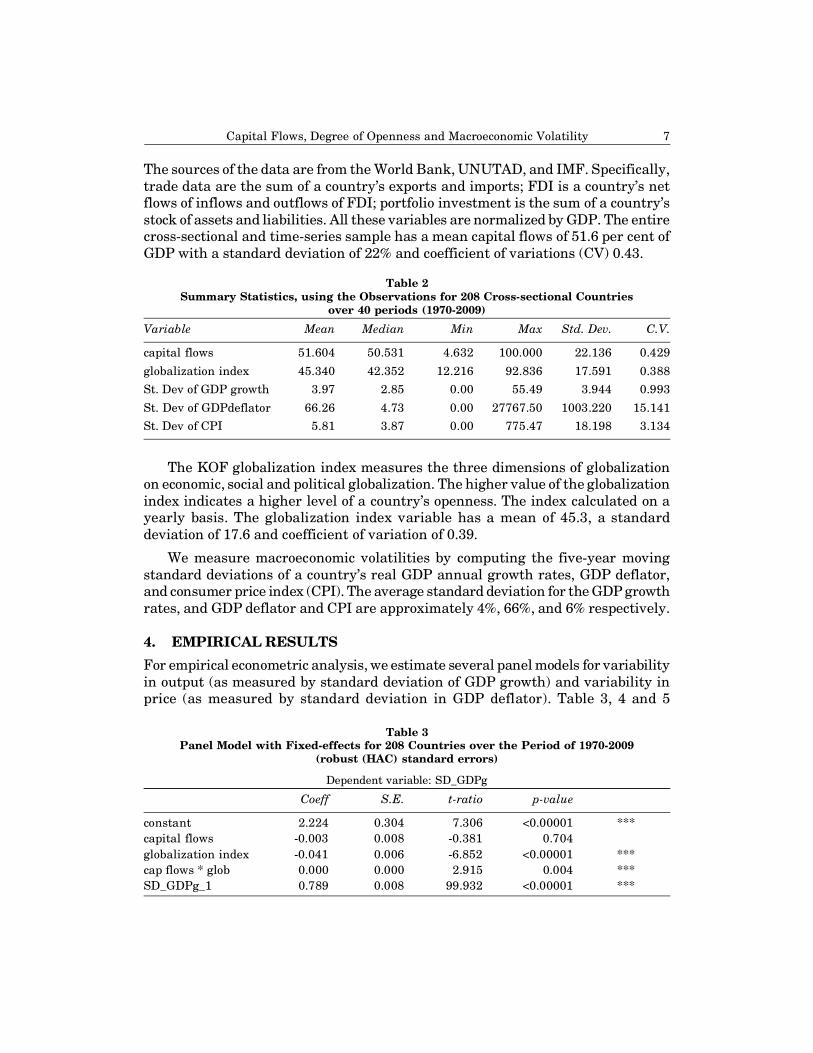

Table 2 presents the summary statistics on the variables of our panel study.The variable on capital flows includes data on trade, FDI and portfolio investment.

Capital Flows, Degree of Openness and Macroeconomic Volatility 7

The sources of the data are from the World Bank, UNUTAD, and IMF. Specifically,trade data are the sum of a country’s exports and imports; FDI is a country’s netflows of inflows and outflows of FDI; portfolio investment is the sum of a country’sstock of assets and liabilities. All these variables are normalized by GDP. The entirecross-sectional and time-series sample has a mean capital flows of 51.6 per cent ofGDP with a standard deviation of 22% and coefficient of variations (CV) 0.43.

Table 2Summary Statistics, using the Observations for 208 Cross-sectional Countries

over 40 periods (1970-2009)

Variable Mean Median Min Max Std. Dev. C.V.

capital flows 51.604 50.531 4.632 100.000 22.136 0.429

globalization index 45.340 42.352 12.216 92.836 17.591 0.388St. Dev of GDP growth 3.97 2.85 0.00 55.49 3.944 0.993

St. Dev of GDPdeflator 66.26 4.73 0.00 27767.50 1003.220 15.141St. Dev of CPI 5.81 3.87 0.00 775.47 18.198 3.134

The KOF globalization index measures the three dimensions of globalizationon economic, social and political globalization. The higher value of the globalizationindex indicates a higher level of a country’s openness. The index calculated on ayearly basis. The globalization index variable has a mean of 45.3, a standarddeviation of 17.6 and coefficient of variation of 0.39.

We measure macroeconomic volatilities by computing the five-year movingstandard deviations of a country’s real GDP annual growth rates, GDP deflator,and consumer price index (CPI). The average standard deviation for the GDP growthrates, and GDP deflator and CPI are approximately 4%, 66%, and 6% respectively.

4. EMPIRICAL RESULTSFor empirical econometric analysis, we estimate several panel models for variabilityin output (as measured by standard deviation of GDP growth) and variability inprice (as measured by standard deviation in GDP deflator). Table 3, 4 and 5

Table 3Panel Model with Fixed-effects for 208 Countries over the Period of 1970-2009

(robust (HAC) standard errors)

Dependent variable: SD_GDPg

Coeff S.E. t-ratio p-value

constant 2.224 0.304 7.306 <0.00001 ***capital flows -0.003 0.008 -0.381 0.704globalization index -0.041 0.006 -6.852 <0.00001 ***cap flows * glob 0.000 0.000 2.915 0.004 ***SD_GDPg_1 0.789 0.008 99.932 <0.00001 ***

8 Debasish Chakraborty and Vigdis Boasson

summarize the results of the effects of capital inflow on variability in output andTable 6 summarizes the effects of capital inflow on price variability. Table 3 reportsthe results of the panel model with fixed effects and Arellano robust standard errors.

The laggeddependent variable is positively correlated with the volatility onGDP growth and the result is statistically significant at 1 per cent level. Eventhough capital flows is negatively correlated with the GDP volatility, the result isnot statistically significant. However, the globalization index which is the proxyfor a country’s openness is negatively correlated with the GDP volatility and theresult is statistically significant at 1 per cent level. This result indicates that thehigher the level of openness, the lower level of the volatility on GDP growth. Inother words, if a country increases its level of globalization or openness, it can helpreduce its volatility on GDP growth and stabilize its economy. More interestingly,the interaction between capital flows and globalization is positively correlated withthe volatility on GDP growth and this result is statistically significant at 1 per centlevel. This suggests that as the level of capital flow increases, it increases thevolatility of GDP growth when the country’s level of openness is low. This indicatesthat the level of openness is low, the beneficial effects of globalization is not largeenough to offset the adverse effects of capital flows on volatility of GDP growth.Thus, the impact of capital flows on GDP growth volatility depends on the level ofglobalization or financial openness.

Table 4Dynamic Panel Model with Two-Step GMM Estimator for 208 Countries over the

Period of 1970-2009

Dependent variable: SD_GDPg

Coeff S.E. z p-value

constant 0.87118 0.1706 5.1036 <0.00001 ***SD_GDPg (-1) 0.84319 0.01878 44.9049 <0.00001 ***capital flows 0.00686 0.00329 2.0835 0.03721 **globalization index -0.02125 0.01080 -1.9669 0.04919 **Cap flow*glob 0.00046 0.00028 1.6626 0.09640 *

The lagged dependent variable is positively correlated with the volatility onGDP growth and the result is statistically significant at 1 per cent level. Capitalflows is positively correlated with the GDP volatility; the result is statisticallysignificant at the 5% level. However, the globalization index which is the proxy fora country’s openness is negatively correlated with the GDP volatility and the resultis statistically significant at 5 per cent level. This result also indicates that thehigher the level of openness, the lower level of the volatility on GDP growth. Inother words, if a country increases its level of globalization or openness, it can helpreduce its volatility on GDP growth and stabilize its economy. This estimationmodel also suggests that the impact of capital flows on GDP growth volatilitydepends on the level of globalization or financial openness.

Capital Flows, Degree of Openness and Macroeconomic Volatility 9

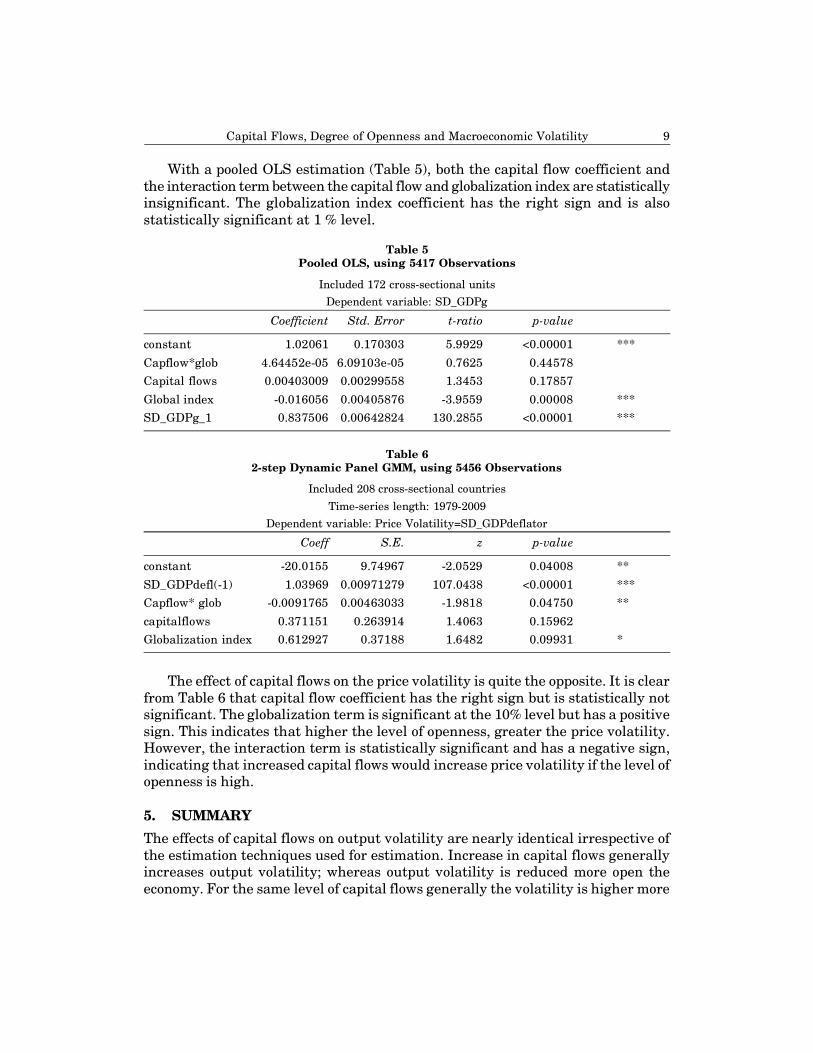

With a pooled OLS estimation (Table 5), both the capital flow coefficient andthe interaction term between the capital flow and globalization index are statisticallyinsignificant. The globalization index coefficient has the right sign and is alsostatistically significant at 1 % level.

Table 5Pooled OLS, using 5417 Observations

Included 172 cross-sectional unitsDependent variable: SD_GDPg

Coefficient Std. Error t-ratio p-value

constant 1.02061 0.170303 5.9929 <0.00001 ***

Capflow*glob 4.64452e-05 6.09103e-05 0.7625 0.44578Capital flows 0.00403009 0.00299558 1.3453 0.17857

Global index -0.016056 0.00405876 -3.9559 0.00008 ***SD_GDPg_1 0.837506 0.00642824 130.2855 <0.00001 ***

Table 62-step Dynamic Panel GMM, using 5456 Observations

Included 208 cross-sectional countries

Time-series length: 1979-2009Dependent variable: Price Volatility=SD_GDPdeflator

Coeff S.E. z p-value

constant -20.0155 9.74967 -2.0529 0.04008 **

SD_GDPdefl(-1) 1.03969 0.00971279 107.0438 <0.00001 ***Capflow* glob -0.0091765 0.00463033 -1.9818 0.04750 **

capitalflows 0.371151 0.263914 1.4063 0.15962Globalization index 0.612927 0.37188 1.6482 0.09931 *

The effect of capital flows on the price volatility is quite the opposite. It is clearfrom Table 6 that capital flow coefficient has the right sign but is statistically notsignificant. The globalization term is significant at the 10% level but has a positivesign. This indicates that higher the level of openness, greater the price volatility.However, the interaction term is statistically significant and has a negative sign,indicating that increased capital flows would increase price volatility if the level ofopenness is high.

5. SUMMARYThe effects of capital flows on output volatility are nearly identical irrespective ofthe estimation techniques used for estimation. Increase in capital flows generallyincreases output volatility; whereas output volatility is reduced more open theeconomy. For the same level of capital flows generally the volatility is higher more

10 Debasish Chakraborty and Vigdis Boasson

open the economy. However volatility in price is increased with globalization andfor the same level of capital inflows, price volatility is reduced as the level of opennessincreases.

ReferencesAghion, P., A. Banerjee, and T. Piketty, (1999), Dualism and Macroeconomic Volatility, Quarterly

Journal of Economics, Vol. 114, pp. 1359-97.Alesina, A., Grilli, V. and Ferretti, G., (1994), The Political Economy of Capital Controls. In

Capital Mobility: The Impact on Consumption, Investment and Growth, ed. L. Leidermanand Razin, Pp. 289-321, Cambridge University Press.

Arellano, C., and E. G. Mendoza, (2002), Credit Frictions and Sudden Stops in Small OpenEconomies: An Equilibrium Business Cycle Framework for Emerging Markets Crises, NBERWorking Paper No. 8880 (Cambridge, Massachusetts: National Bureau of Economic Research).

Arellano, M., and S. Bond, (1991), Some Tests of Specification for Panel Data: Monte CarloEvidence and an Application to Employment Equations. Review of Economic Studies 58 (2):277-297.

Arnello, M and O. Bover., (1995), Another Look at the Instrumental Variable Estimation ofError-Components Models, Journal of Econometrics 68 (1): 29-51.

Arteta, C., Eichengreen, B., Wyplosz, C., (2001), When Does Capital Account Liberalization HelpMore Than It Hurts? NBER Working Papers, no. 8414.

BarbaNavaretti, G., G. Calzolari, A. Pozzole and M. Levi, (2010), Multinational banking in Europe:Financial Stability and Regulatory Implications-lessons from the Financial Crisis, mimeo,University of Milan.

Baxter, M., and M. Crucini, (1995), Business Cycles and the Asset Structure of ForeignTrade,International Economic Review, Vol. 36, pp. 821-54.

Bekaert, G., Campbell, R., and Christian, L., (2005), Does Financial Liberalization Spur Growth?Journal of Financial Economics, 77(1): 3–55.

Blanchard, O., M. Das and H. Faruqee, (2010), The Initial Impact of the Crisis on EmergingMarket Countires, Brookings Papers on Economic Activity, Spring, 263-307.

Broda, C., P. Ghezzi and E. Levy-Yeyati, (2009), The New Global Balance, Braclay Capital, 23March.

Buch, C. M., J. Dopke, and C. Pierdzioch, (2002), Financial Openness and Business Cycle Volatility,Working Paper, Kiel: Kiel Institute for World Economics.

Caballero, R. J., and A. Krishnamurthy, (2001), International and Domestic Collateral Constraintsin a Model of Emerging Market Crises, Journal of Monetary Economics, Vol. 48, pp. 513-48.

Chmn, M. and H. Ito, (2008), A New Measure of Financial Openness, Journal of ComparativePolicy Analysis, 10(3), 307-20.

Crucini, M., (1997), Country Size and Economic Fluctuations, Review of International Economics,Vol. 5, No. 2, pp. 204-20.

Dreher, Axel, (2006), Does Globalization Affect Growth? Evidence from a New Index ofGlobalization, Applied Economics 38, 10: 1091-1110.

Dreher, Axel; Noel Gaston and Pim Martens, (2008), Measuring Globalization - GaugingitsConsequence, New York: Springer. Europa World Yearbook, Various Years, Routledge.

Easterly, W., R. Islam, and J. E. Stiglitz, (2001), Shaken and Stirred: Explaining Growth Volatility,Annual World Bank Conference on Development Economics, ed. by B. Pleskovic and N. Stem.

Capital Flows, Degree of Openness and Macroeconomic Volatility 11

Edison, H. J., M. Klein, L. Ricci, and T. Slok, (2002), Capital Account Liberalization and EconomicPerformance: Survey and Synthesis, IMF Working Paper No. 02/120 (Washington:International Monetary Fund).

Edison, Hali J., Ross Levine, Luca Antonio Ricci, and TorstenSløk, (2002), International FinancialIntegration and Economic Growth, Journal ofInternational Money and Finance, 21(6): 749–76.

Edwards, Sebastian. (2001), “Capital Mobility and Economic Performance: Are EmergingEconomies Different?” NBER Working Papers, no. 8076.

Eozenou, Patrick, (2008), Financial Integration and Macroeconomic Volatility: Does FinancialDevelopment Matter? MPRA Paper 12738, University Library of Munich, Germany.

Gavin, M., and R. Hausmann, (1996), Sources of Macroeconomic Volatility in DevelopingEconomies, IADB Working Paper (Washington: Inter-American Development Bank).

Glick, R., and M. Hutchison, (1999), Banking and Currency Crises: How Common are TwinCrises?inFinancial Crises in Emerging Markets, ed. by R. Glick, R. Moreno, and M. Spiegel,(Cambridge: Cambridge University Press).

Grilli, V. and Ferretti, G., (1995), Economic Effects and Structural Determinants of Capital Control,IMF Staff Paper, International Monetary Volume, Vol. 42 No 3 Pp. 517-551.

Head, A. C., (1995), Country Size, Aggregate Fluctuations, and International Risk Sharing,Canadian Journal of Economics, Vol. 28, pp. 1096-19.

Hoggarth, G., L. Mahadevaandj. Martin, (2010), Understanding International Bank Capital Flowsduring the Recent Financial Crisis, Bank of England Financial Stability Paper 8.

International Monetary Fund, (2012), International Financial Statistics Indicators.Kaminsky G. L., Reinhart C. M., (1999), The Twin Crises: the Cause of Banking and Balance-of-

payments Problems, The American Economics Review, 89(3), 473-500.Karras, G., and E. Song, (1996), Sources of Business-Cycle Volatility: An Exploratory Study on a

Sample of OECD Countries, Journal of Macroeconomics, Vol. 18, No. 4, pp. 621-37.

Kim, S. H., M. A. Kose, and M. Plummer, (2003), Dynamics of Business Cycles in Asia, Review ofDevelopment Economics, Vol. 7, No. 3.

Klein, M., and Olivei, G., (1999), Capital Account Liberalization, Financial Depth and EconomicGrowth. NBER WorkingPaper. 7384, Cambridge, Massachusetts.

Kose, M. A., (2002), Explaining Business Cycles in Small Open Economies, Journal of InternationalEconomics, Vol. 56, pp. 299-327.

Kose, M. A., and K. Yi, (2003), The Trade-Comovement Problem in International Macroeconomics,IMF Working Paper, Washington: International Monetary Fund.

Kraay, Aart. (1998), In Search of the Macroeconomic Effects of Capital Account Liberalization,Unpublished, World Bank Group.

Licchetta M., (2006), Macroeconomic Effects of Capital Account Liberalization in EmergingMarkets, Ph.D. in Economics Working Papers, University of Rome [Online], Available athttp://dep.eco.uniroma1.it/phd/wp/01200604_licchetta_macroeconomicseffects.pdf (January12, 2007).

Mendoza, E. G., (2002), Credit, Prices, and Crashes: Business Cycles with a Sudden Stop, inPreventing Currency Crises in Emerging Markets, ed. by Frankel, J., and S. Edwards,(Chicago: University of Chicago Press).

Mendoza, E . G., (1994), The Robustnessof Macroeconomic Indicators of Capital Mobility, inCapital Mobility: The Impact on Consumption, Investment, and Growth, ed. by LeonardoLeiderman and Assaf Razin (Cambridge: Cambridge University Press), pp. 83-111.

12 Debasish Chakraborty and Vigdis Boasson

Obstfeld, M., and K. Rogoff, (1995), Exchange Rate Dynamics Redux, Journal of Political Economy,Vol. 103, pp. 624-60.

Obstfeld, M., J. Shambaugh and A. Taylor, (2009), Financial Instability, Reserves, and CentralBank, Swap Lines in the Panic of 2008, NBER Working Paper 14826, March.

Prasad, E., K. Rogoff, S. Wei, and M. A. Kose (2003), The Effects of Financial Globalization onDeveloping Countries: Some Empirical Evidence, IMF Working Paper (Washington:International Monetary Fund).

Quinn, D., (1997), The Correlates of Change in International Financial Regulation, AmericanPolitical Science Reviews, Vol. 91, No, Pp. 535-571.

Razin, Assaf and Andrew K. Rose, (1994), Business-Cycle Volatility and Openness: an ExploratoryCross-Sectional Analysis, in Capital Mobility: The Impact on Consumption, Investment,and Growth, ed. by Leonardo Leiderman and Assaf Razin (Cambridge: Cambridge UniversityPress), pp. 48-76.

Reinhart, Carmen, and Kenneth Rogoff, (2002), The Modern History of Exchange RateArrangements: A Reinterpretation, NBER Working Paper (Cambridge, Massachusetts:National Bureau of Economic Research).

Reisen, H. and Soto, M., (2001), Which Type of Capital Inflows Foster Developing Country Growth?International Finance, Vol. 4, Issue 1, Pp. 1-14.

Rodrik, Dani. (1998), Who Needs Capital-Account Convertibility? In Should the IMF PursueCapital-Account Convertibility. Essays in International Finance, no. 207, Princeton:International Finance Section, Department of Economics, Princeton University, 55–65.

Schindler, M. (2009), Measuring Financial Integration: A New Data Set, IMF Staff Papers, 56(1),222-38.

Senay, O., (1998), The Effects of Goods and Financial Market Integration on MacroeconomicVolatility, The Manchester School Supplement, Vol. 66, pp. 39-61.

Senhadji, A., (1998), Dynamicsof the Trade Balance and the Terms-of-Trade in LDCs: The S-Curve, Journal of International Economics, Vol. 46, pp. 105-31.

Sutherland, A., (1996), Financial Market Integration and Macroeconomic Volatility, ScandinavianJournal of Economics, Vol. 98, pp. 521-39.

UNCTAD 2012, UNCTADStat, http://unctadstat.unctad.org.

World Bank 2012, World Development Indicators, Washington, DC.

�����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������