Embed Size (px)

Citation preview

Capacity Planning

How much long-range capacity is needed

When more capacity is neededWhere facilities should be located

(location)How facilities should be arranged

(layout)

Facility planning answers:

Facility Planning

ForecastDemand

ComputeNeededCapacity

ComputeRated

Capacity

EvaluateCapacity

Plans

ImplementBest Plan

QualitativeFactors

(e.g., Skills)

Select BestCapacity

Plan

DevelopAlternative

Plans

QuantitativeFactors

(e.g., Cost)

Capacity Planning Process

Types of Planning & Time Horizons

Add FacilitiesAdd long lead time equipment

Schedule Jobs Schedule Personnel Allocate Machinery

Sub-ContractAdd EquipmentAdd Shifts

Add PersonnelBuild or Use Inventory

Long Range Planning

Intermediate Range Planning

Short Range Planning Modify

CapacityUse Capacity

*

*

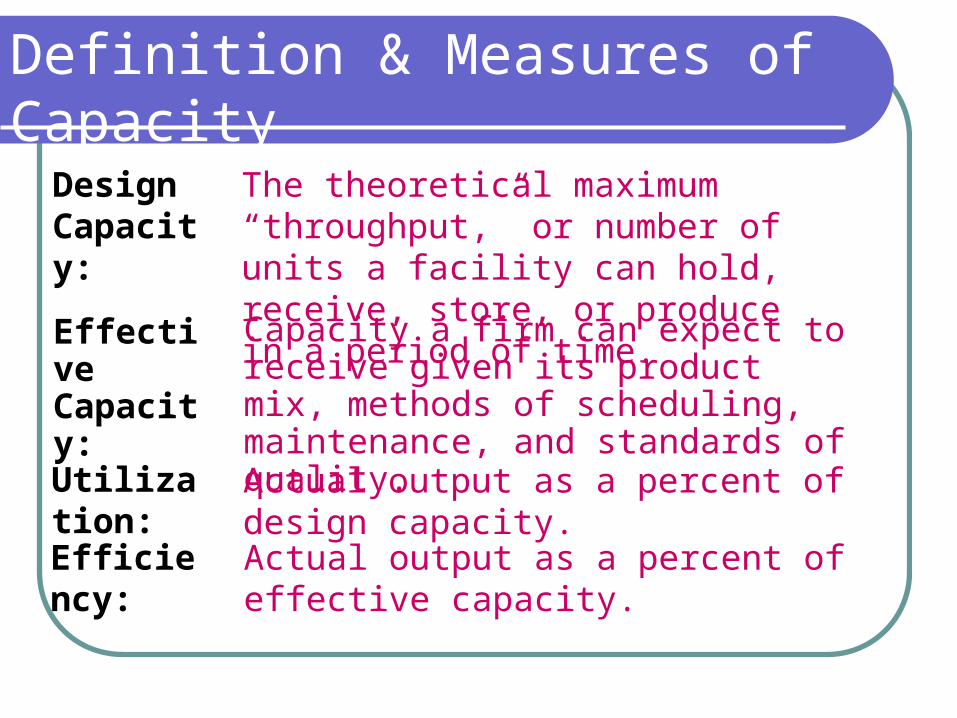

Definition & Measures of Capacity

DesignCapacity:

The theoretical maximum “throughput,” or number of units a facility can hold, receive, store, or produce in a period of time.

Utilization: Actual output as a percent of design capacity.

Effective Capacity:

Capacity a firm can expect to receive given its product mix, methods of scheduling, maintenance, and standards of quality.

Efficiency: Actual output as a percent of effective capacity.

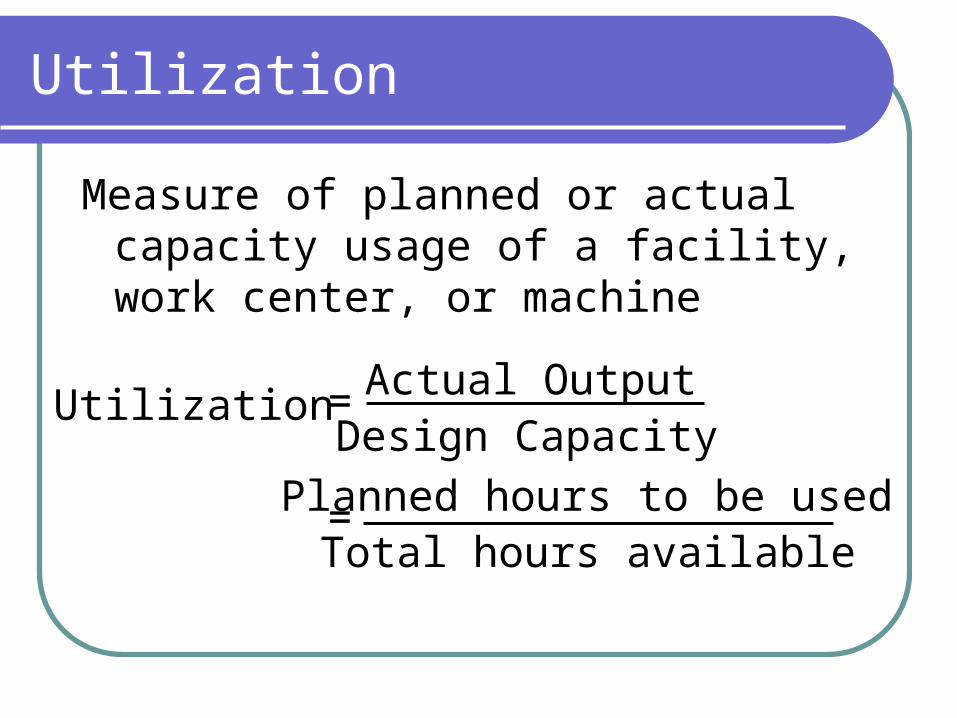

Measure of planned or actual capacity usage of a facility, work center, or machine

Utilization Actual OutputDesign Capacity

Planned hours to be usedTotal hours available

=

=

Utilization

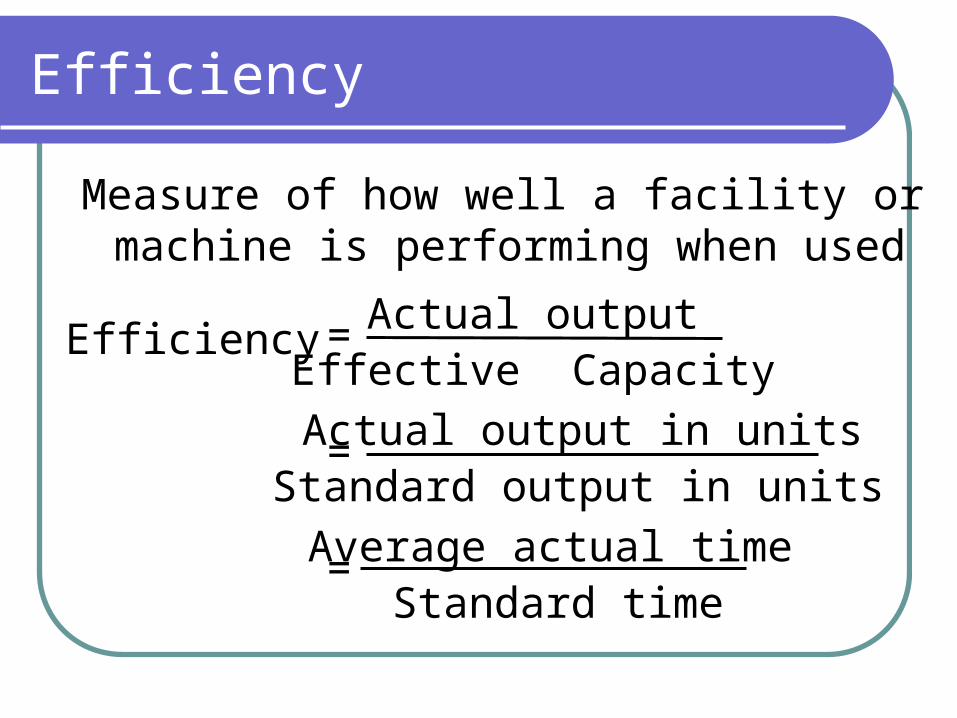

Measure of how well a facility or machine is performing when used

Efficiency Actual outputEffective Capacity

Actual output in unitsStandard output in unitsAverage actual time

Standard time

=

=

=

Efficiency

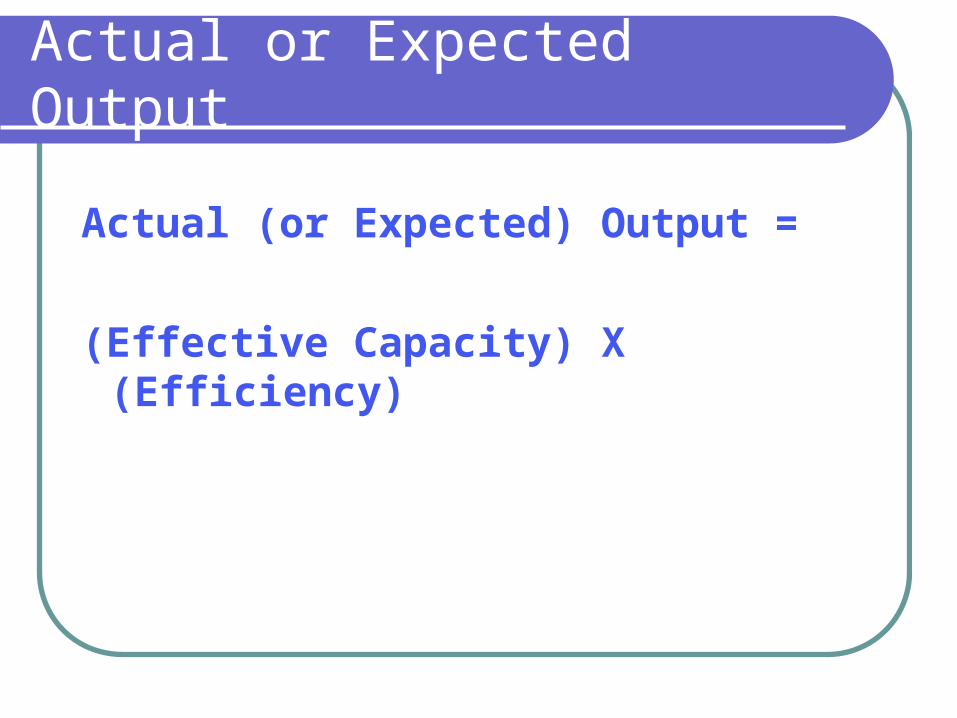

Actual or Expected Output

Actual (or Expected) Output =

(Effective Capacity) X (Efficiency)

Capacity Changes

Changes in capacity will likely have implications for:SalesCash flowQualitySupply chainHuman resourcesMaintenance

Make Good Capacity Decisions:

Forecast demand accuratelyUnderstand the technology and

capacity incrementsFind the optimal operating level

(volume)Build for change

Matching Capacity to Demand

1. Make staffing changes (increasing or decreasing the number of employees)

2. Adjust equipment and processes – which might include purchasing additional machinery or selling or leasing out existing equipment

3. Improve methods to increase throughput; and/or

4. Redesign the product to facilitate more throughput

Matching Capacity to Demand

Demand management Vary prices Change lead times Encourage or discourage business Offer complementary products

Capacity management Adjust staffing Adjust equipment and processes Change methods to facilitate production Redesign the product to facilitate production

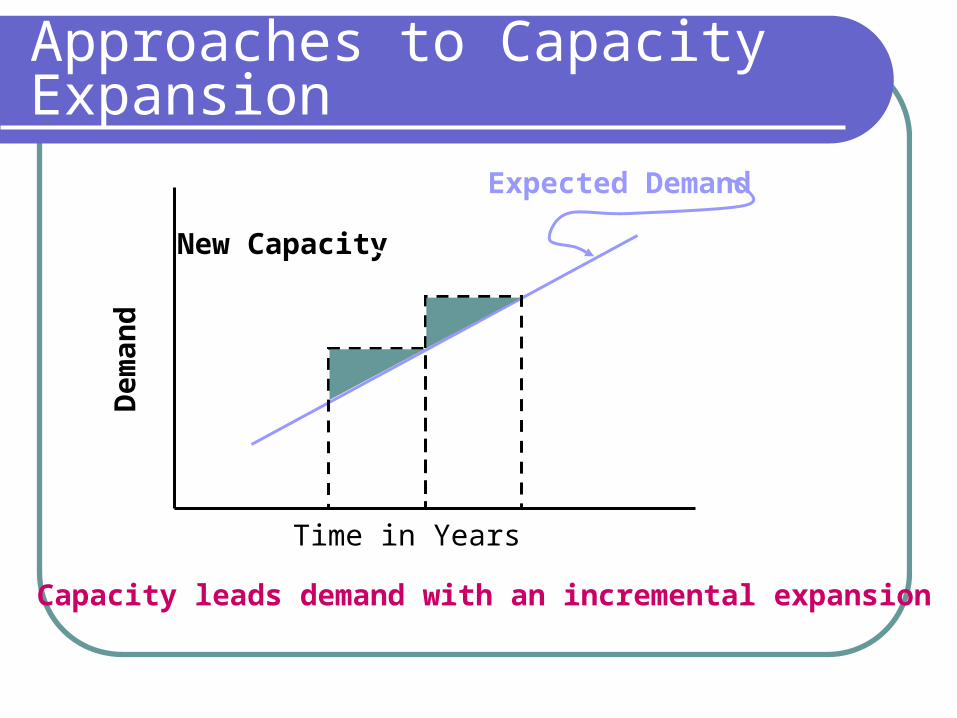

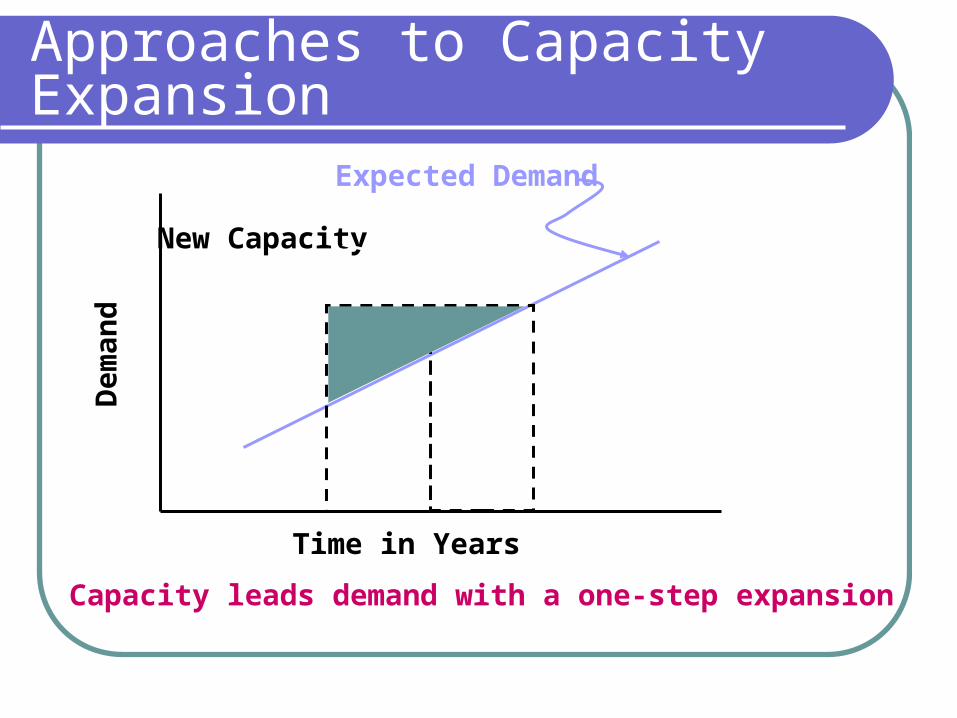

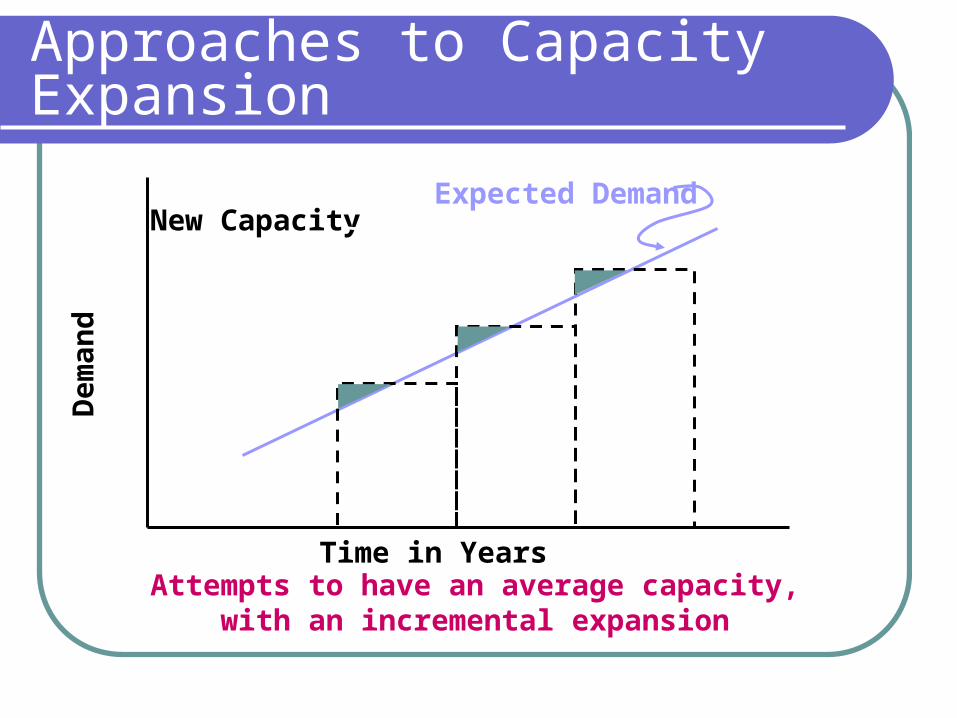

Approaches to Capacity Expansion

Expected Demand Expected Demand

Expected Demand Expected Demand

Time in Years Time in Years

Time in YearsTime in Years

Dem

and

Dem

and

Dem

and

Dem

and

New Capacity

New Capacity New Capacity

New Capacity

Capacity leads demand with an incremental expansion Capacity leads demand with a one-step expansion

Capacity lags demand with an incremental expansionAttempts to have an average capacity, with an

incremental expansion

Approaches to Capacity Expansion

Expected Demand

Time in Years

Dem

and

New Capacity

Capacity leads demand with an incremental expansion

Approaches to Capacity Expansion

Expected Demand

Time in Years

Dem

and

New Capacity

Capacity leads demand with a one-step expansion

Approaches to Capacity Expansion

Expected Demand

Time in Years

Dem

and

New Capacity

Capacity lags demand with an incremental expansion

Approaches to Capacity Expansion

Expected Demand

Time in Years

Dem

and

New Capacity

Attempts to have an average capacity, with an incremental expansion

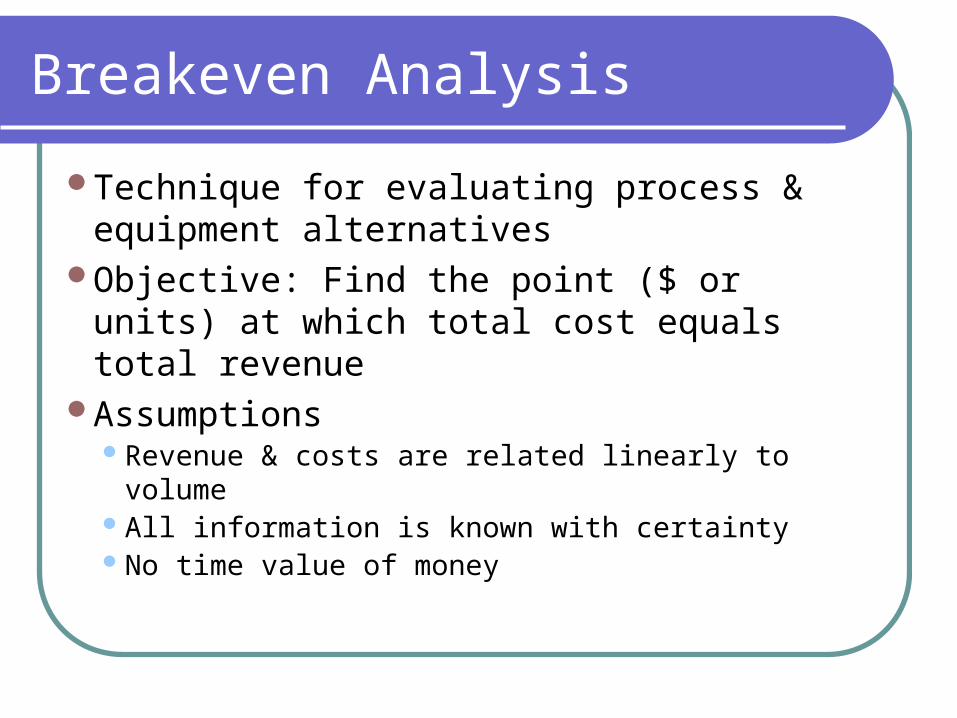

Breakeven Analysis

Technique for evaluating process & equipment alternatives

Objective: Find the point ($ or units) at which total cost equals total revenue

AssumptionsRevenue & costs are related linearly to volumeAll information is known with certaintyNo time value of money

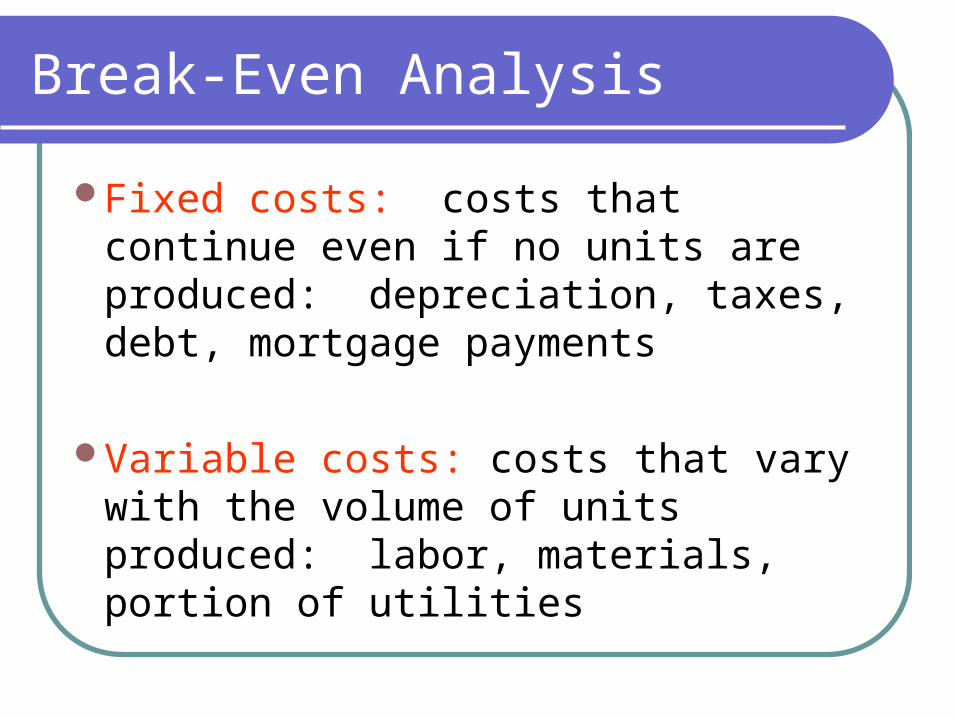

Break-Even Analysis

Fixed costs: costs that continue even if no units are produced: depreciation, taxes, debt, mortgage payments

Variable costs: costs that vary with the volume of units produced: labor, materials, portion of utilities

Breakeven Chart

Fixed cost

Variable cost

Total cost line

Total revenue line

ProfitBreakeven pointTotal cost = Total revenue

Volume (units/period)

Cost

in D

olla

rs

Loss

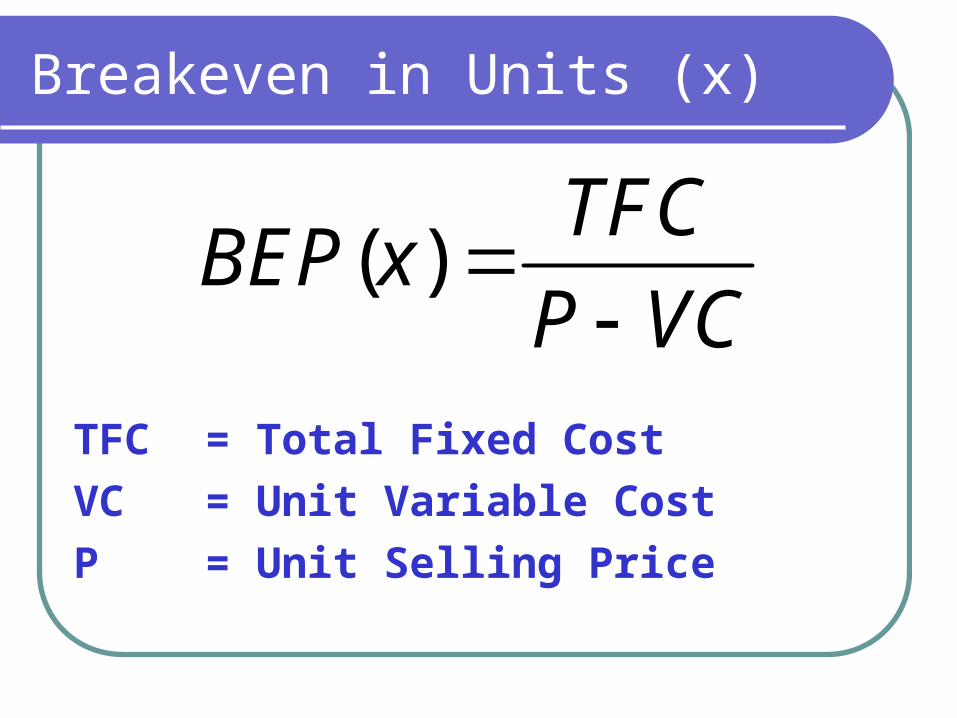

Breakeven in Units (x)

TFC = Total Fixed Cost

VC = Unit Variable Cost

P = Unit Selling Price

( )TFC

BEP xP VC

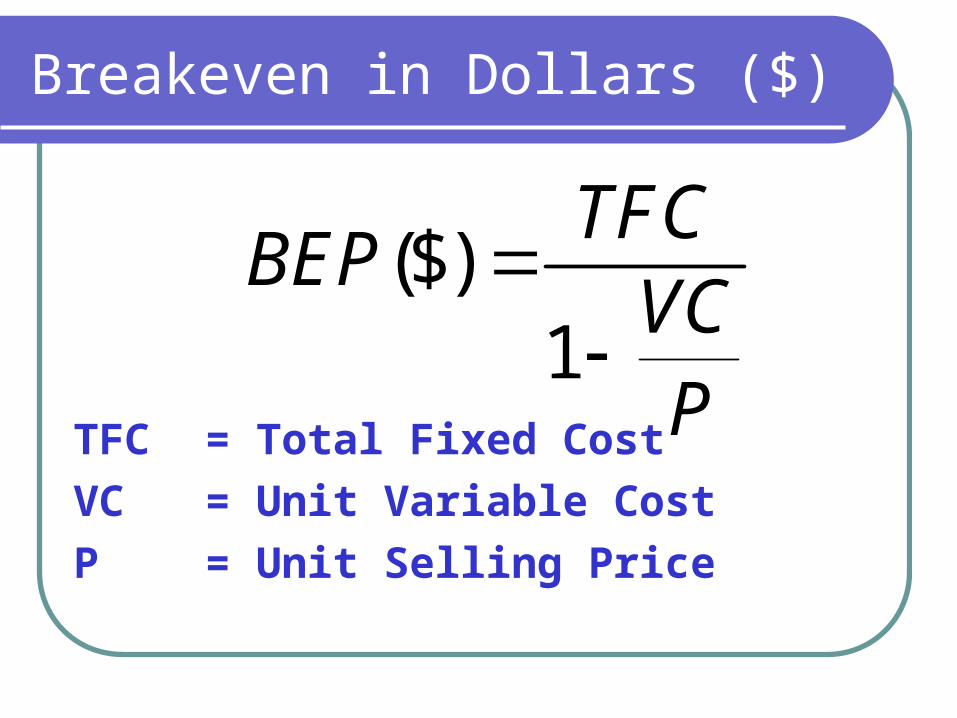

Breakeven in Dollars ($)

($)1

TFCBEP

VCP

TFC = Total Fixed Cost

VC = Unit Variable Cost

P = Unit Selling Price

Breakeven Example

A new process costs $10,000 to set upThe revenue earned is $25,000 per

1,000 units soldThe variable cost is $22.50 per unit

What is the BEP(x)?What is the BEP($)?

4,000

$100,000

Strategy Driven Investment

Select investments as part of a coordinated strategic plan

Choose investments yielding competitive advantage

Consider product life cycles Include a variety of operating factors in the

financial return analysisTest investments in light of several revenue

projections

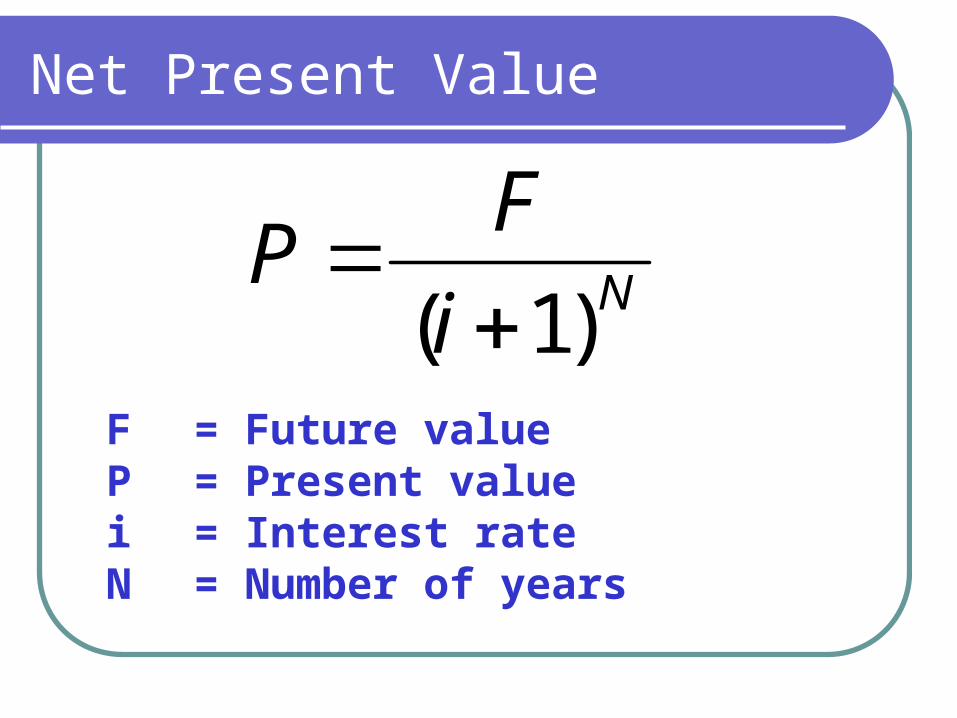

Net Present Value

Ni

FP

)1(

F = Future valueP = Present valuei = Interest rateN = Number of years

Net Present Value Example #1

A new machine costs $5,000 Over the 3 years of useful life of the machine it

produces revenues of $2,000 per year, paid at the end of each year

At the end of the 3rd year the machine is sold to a competitor for $1,000

What is the NPV of the investment if the company has a cost of capital of 10%?

NPV Solution #1

0 1 2 3 3

5,000 2,000 2,000 2,000 1,000

(1.1) (1.1) (1.1) (1.1) (1.1)NPV

NPV = $725.02

Net Present Value Example #2

Machine A Price = $15,000 Maintenance costs =

$5,000 at the end of each of 3 years

Salvage value = $2,000 at the end of year 3

Discount rate = 10%

Machine B Price = $20,000 Maintenance costs =

$4,000 at the end of each of 3 years

Salvage value = $7,000 at the end of year 3

Discount rate = 10%

NPV Solution #2

Which machine should the production manager buy?

0 1 2 3 3

15,000 5,000 5,000 5,000 2,000

(1.1) (1.1) (1.1) (1.1) (1.1)ANPV

0 1 2 3 3

20,000 4,000 4,000 4,000 7,000

(1.1) (1.1) (1.1) (1.1) (1.1)BNPV

NPVA = -25,931.63

NPVB = -24,688.20

Machine B

Limitations of Net Present Value

Investments with the same present value may have significantly different project lives and different salvage values

Investments with the same net present values may have different cash flows

We assume that we know future interest rates - which we do not

We assume that payments are always made at the end of the period - which is not always the case