Embed Size (px)

Citation preview

Can Business Regulation Can Business Regulation Stimulate Responsible Stimulate Responsible Corporate Conduct ?Corporate Conduct ?

Gathering Evidence from a Few Gathering Evidence from a Few Indian StatesIndian States

Regional Dialogue (NORTHERN INDIA)Regional Dialogue (NORTHERN INDIA)

Exploring the interplay between Business Exploring the interplay between Business Regulation & Corporate Conduct in India Regulation & Corporate Conduct in India

(BRCC Project)(BRCC Project)

1212thth July 2011, Jaipur July 2011, Jaipur

2

Aspects of Business Regulation Aspects of Business Regulation and Corporate Conductand Corporate Conduct

Sameer ChaturvediSameer ChaturvediCUTS InternationalCUTS International

3

Presentation Theme Presentation Theme

Business Regulation and Business Performance◦ Assessing Business Performance – Global◦ Assessing Business Performance – Inter-State

(India)Business Regulation and Corporate Conduct

◦ Aspects of Business Regulation◦ Corporate Conduct – Global and National

Evolution◦ Aspects of Corporate Conduct

Stakeholder Interaction Framework

4

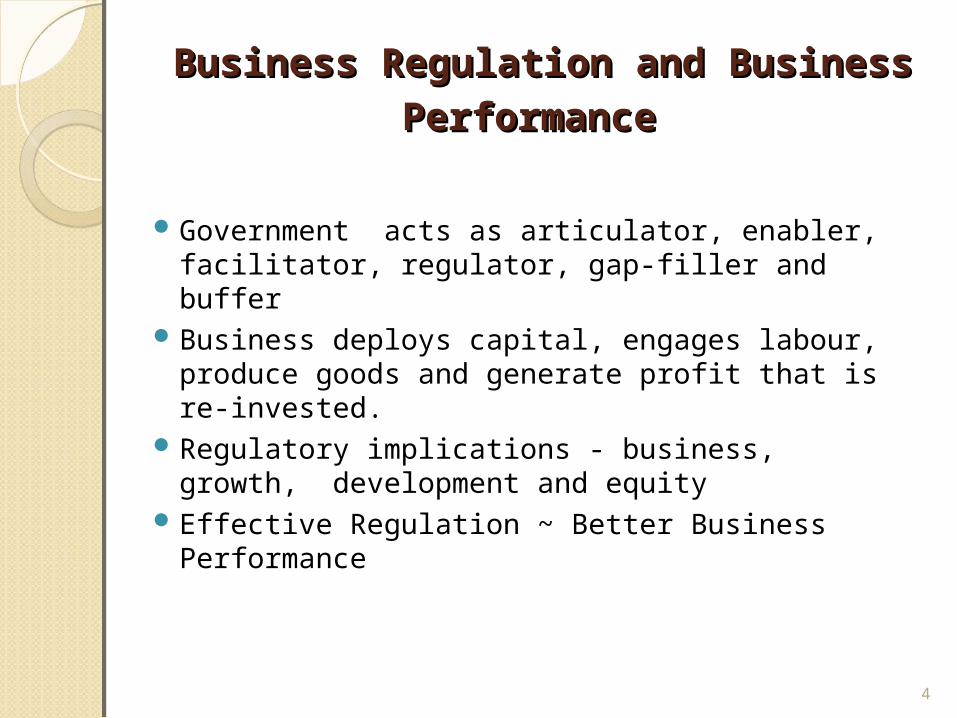

Business Regulation and Business Business Regulation and Business

PerformancePerformance

Government acts as articulator, enabler, facilitator, regulator, gap-filler and buffer

Business deploys capital, engages labour, produce goods and generate profit that is re-invested.

Regulatory implications - business, growth, development and equity

Effective Regulation ~ Better Business Performance

5

Dimensions of Business Dimensions of Business RegulationRegulation

6

Assessing Business Performance Assessing Business Performance

7

Highlights from Doing Business Highlights from Doing Business Report (WB & IFC) 2011Report (WB & IFC) 2011

India’s overall Rank – 134 (out of 183)Getting Credit– 32nd, Protecting Investors - 44th

Enforcing Contracts - 182nd, Construction Permits – 177th, Starting Business – 165th, Taxes – 164th

Registering Property: India - 5 procedures, takes 44 days; Turkey- 6 procedures, takes 6 days.

Enforcing Contracts, - 1420 days in India; 406 days in China; 281 days in Russia; 230 days in Korea

Taxation Payments (No.) – In India 56 in a year, in China & France only 7 payments in a year

Closing Business - 7 yrs in India & 1.7 yrs in China Recovery rate (closing a business) - India is 16.3%,

36.4% in China, 81.7% in Korea & 92.7% in Japan

8

Inter-state Variations in India – Inter-state Variations in India – Highlights from Doing Business Highlights from Doing Business India Report (WB & IFC) 2009 India Report (WB & IFC) 2009

Not much variation in starting business – Maximum is 41 days (Kochi) & Minimum is 30 days (Noida)

Construction Permits - takes 37 procedures in Mumbai, as against 15 in Ahmedabad, Bengaluru and Chennai

258 days for construction permits in Kolkata, as against Bengaluru, where the same work gets done in 97 days

Registering Property - 126 days in Bhubaneshwar whereas it takes 24 days in Jaipur

In Bengaluru, a firm has to bear 32.5% cost of claim in enforcing contracts, whereas in Patna it is 17%

It requires 10.8 years to close a business in Kolkata, whereas in Ahmadabad, the time spent for such formalities is 6.8 years.

9

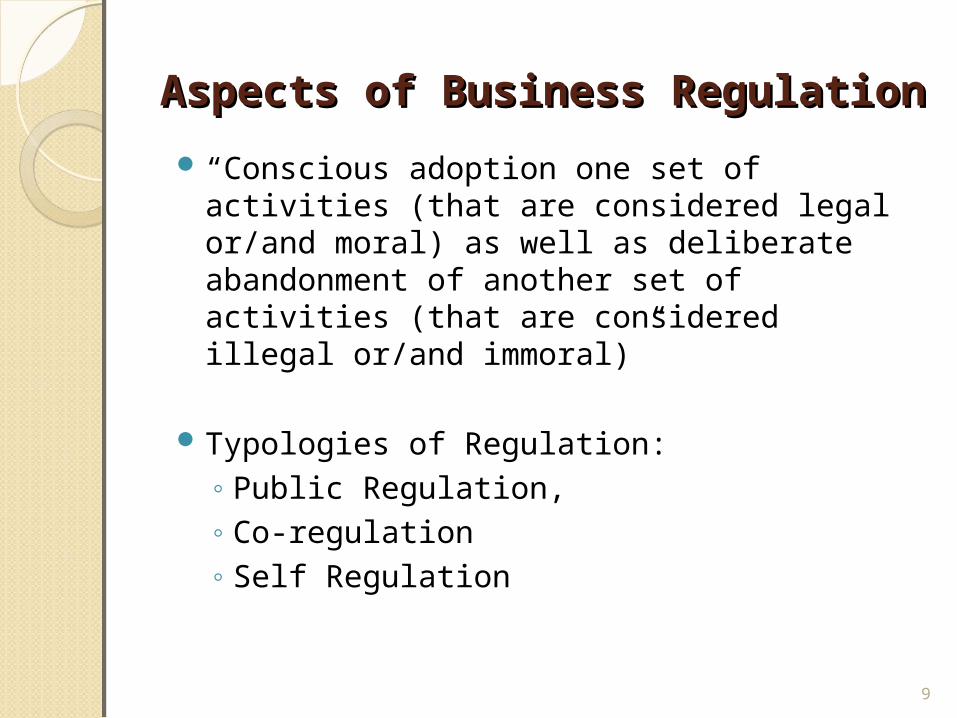

Aspects of Business RegulationAspects of Business Regulation

“Conscious adoption one set of activities (that are considered legal or/and moral) as well as deliberate abandonment of another set of activities (that are considered illegal or/and immoral)”

Typologies of Regulation:◦ Public Regulation,◦ Co-regulation◦ Self Regulation

10

Evolution of Concept GloballyEvolution of Concept Globally

1948 – Universal Declaration on Human Rights1997 – SA 8000 (Social Accountability

International)1998-2006 – Global Reporting Initiative (G3)2000 – Millennium Declaration2000 – United Nations Global Compact2001 – OECD Guidelines for MNEs2003 – UN Norms on Responsibilities of TNCs

and other Businesses on Human Rights2010 – Guidance on Social Responsibility ISO

260002011 - Guiding Principles on Business and

Human Rights

11

Evolution of Concept NationallyEvolution of Concept Nationally

Mahatma Gandhi’s notion of large Businesses as ‘Trusts’

1950-60: Nehruvian mixed economy model, private sector with responsibility in development

Individual Code of Conducts & Responsibility1991 Liberalization reforms, raised expectations2007 – Guidelines on Corporate Governance for

Central Public Sector Enterprises, GoI2009 – Voluntary Guidelines on Corporate

Governance and Corporate Social Responsibility 2010 - Guidelines on Corporate Social

Responsibility for Central PSE, GoI2011 – Guidelines on Social, Environmental and

Economic Responsibilities of Business

12

Aspects of Corporate ConductAspects of Corporate Conduct

Facets - corporate governance, corporate social responsibility, fair trade, labour norms, credibility charters, integrity codes, embodiment of green business practices, accountability initiatives, proactive disclosures, stakeholder engagements…

Determinants of Corporate Conduct ◦ Internal◦ Operational◦ External

13

Stakeholder Interaction FrameworkStakeholder Interaction Framework

14

Thank You!Thank You!