Embed Size (px)

Citation preview

© 2015 IHS © 2015 IHS

Presentation

ihs.com

IHS

Cambios Fundamentales Que están afectando

el Negocio del Plastico en 2015

Preparado para Acoplasticos

Colombia

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

Junio 1, 2015

CHEMICAL

© 2015 IHS

• Technical + Specialties

• World’s leading business research & forecasting service

• Provider of chemical process economics for the global chemical industry

• Trusted authority on chlor-alkali, vinyl chloride, and bleaching chemicals

• Market and pricing data

• 100-year information supplier

• Authoritative chemical business news

• Information resource for high-level industry executives & professionals

• Commercial + Strategic

• Market, planning & consulting advisory services

• Analytical & technical expertise

Chemical Week

CMAI

SRI Consulting

Harriman Chemsult

2

IHS Chemical

Quien es IHS

© 2015 IHS

Chemicals

Power &

Utilities

Agriculture

Electronics &

Telecom

Government

Metals &

Mining Healthcare

Financial

Military &

Security

Automotive

Energy

Coal

Transportation

Shipping

Aerospace &

Defense

Construction

Energy

Oil & Gas

Consumer

& Retail

….To Deliver Unique, Cross – Disciplinary Content and Knowledge of Your End Markets

© 2015 IHS 4

Presentation Name / Month 2015 Customers of the

Chemical Industry Chemical Industry Value Chain Natural Resources

• Oil

• Gas

• Coal

• Minerals

• Renewables

Mining, Drilling,

Refining & Gas

Processing Olefins (ethylene, propylene, butylene)

Basic Chemicals

Aromatics (benzene, toluene,

xylenes)

Chlor-Alkali (chlorine, caustic

soda)

Others (e.g., ammonia, phosphorous)

Methanol

• Automotive / Transportation

• Consumer products

• Packaging

• Building & construction

• Recreation /Sport

• Industrial

• Medical

• Pharmaceuticals

• Personal care

• Textiles

• Electrical/ Electronics

• Aircraft / Aerospace

• Business equipment

Chemical Intermediat

es

Commodities

Differentiated Commodities

Technical Specialties

• Plastics & Engineering Resins

− Extruded films, pipe, profiles, coatings, sheet, foams, sheet

− Blow-molded parts

− Injection molded parts

− Composites

• Synthetic Fibers

• Rubber Products

• Paints & Coatings

• Adhesives & Sealants

• Lubricants

• Water Treatment products

• Cleaning Products

• Industrial Chemicals

• Flame Retardants

• Many others…

Formulated Products / Performance Materials

© 2015 IHS 5

Presentation Name / Month 2015

AGENDA

• La Economía y La Energía

• Cambios Fundamentales

• Comercio Cambiante

• Conclusiones

© 2015 IHS © 2015 IHS 6

La Economía

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

© 2015 IHS

Economic Growth in Latin America

GDP Growth, %

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Argentina 3.1 0.1 9.5 8.4 0.8 2.9 0.5 -0.8 1.9 3.2 3.9

Brazil 5.0 -0.2 7.6 3.9 1.8 2.7 0.1 -1.4 0.7 1.9 2.5

Chile 3.3 -1.0 5.8 5.8 5.5 4.2 1.9 2.8 3.5 3.8 4.3

Colombia 3.5 1.7 4.0 6.6 4.0 4.7 4.6 3.5 3.7 4.2 4.1

Mexico 1.4 -4.7 5.1 4.0 4.0 1.4 2.1 2.6 3.6 4.0 4.1

Peru 9.2 1.1 8.4 6.5 6.0 5.7 2.4 3.5 4.3 4.9 4.7

-4.0

-1.5

1.0

3.5

6.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Latin America World USA

© 2015 IHS

Resumiendo :

• PIB crecerá mas lento en la región durante el 2015. Principalmente por la recesión en Brasil.

• Devaluación de las monedas en la región tuvo un impacto muy fuerte en Marzo. Ahora esta mas estable.

• Estados Unidos reduce su crecimiento en el primer trimestre a -0.7. Reducción de exportación, problemas con el puerto de California y bajo consumo relacionado con un invierno fuerte.

• Volatilidad en los precios continuara en este 2015.

• Precios del crudo a niveles inferiores a los esperados afectaran los presupuestos nacionales frenando un poco el crecimiento de la producción industrial. Colombia entre los países mas afectados por la caída del precio del crudo.

• Volatilidad en moneda local también tendrá un efecto limitador de las importaciones pero a su vez beneficia las exportaciones.

© 2015 IHS © 2015 IHS 9

Cambios en el precio del crudo y gas

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

© 2015 IHS

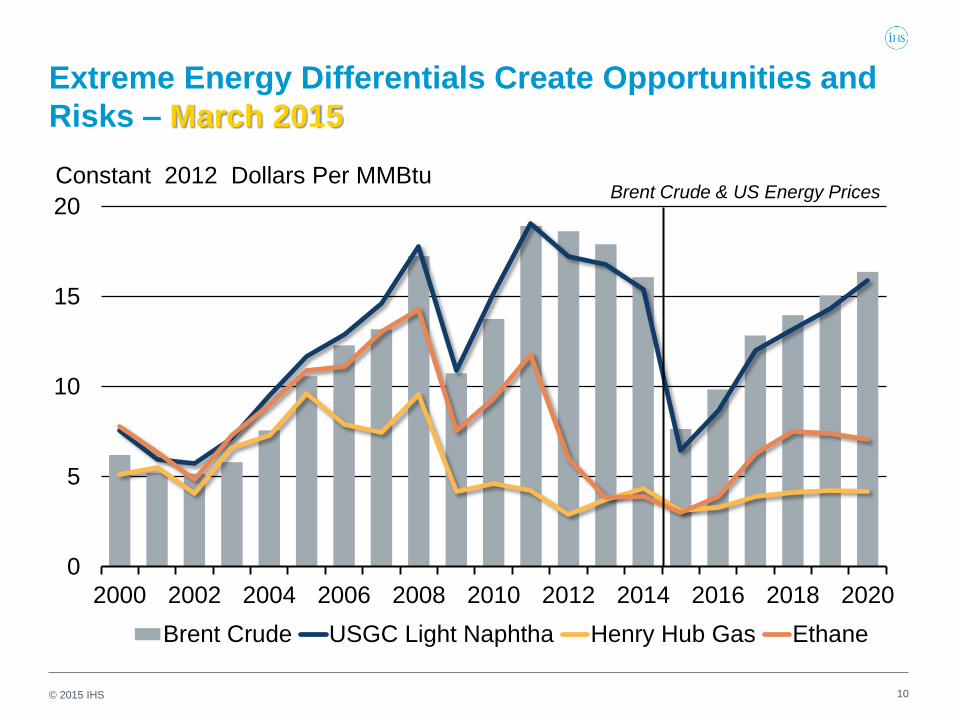

Extreme Energy Differentials Create Opportunities and

Risks – March 2015

10

0

5

10

15

20

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Brent Crude USGC Light Naphtha Henry Hub Gas Ethane

Constant 2012 Dollars Per MMBtu Brent Crude & US Energy Prices

© 2015 IHS

Production of Oil and Natural Gas Selected Countries – USA, Russia and Saudi Arabia

Energy in Quadrillion BTU

2008 2009 2010 2011 2012 2013 2014

0

5

10

15

20

25

30

35

40

45

50

USA Gas

USA Oil

Russia Gas

Russia Oil

KSA Gas

KSA Oil

© 2015 IHS

Production of Oil and Natural Gas U.S. Surplus Takes Stocks to Record Levels

© 2015 IHS

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

D-1

4

J-1

5

F-1

5

M-1

5

A-1

5

M-1

5

J-1

5

J-1

5

A-1

5

S-1

5

O-1

5

N-1

5

D-1

5

J-1

6

F-1

6

M-1

6

A-1

6

M-1

6

J-1

6

J-1

6

A-1

6

S-1

6

O-1

6

N-1

6

D-1

6

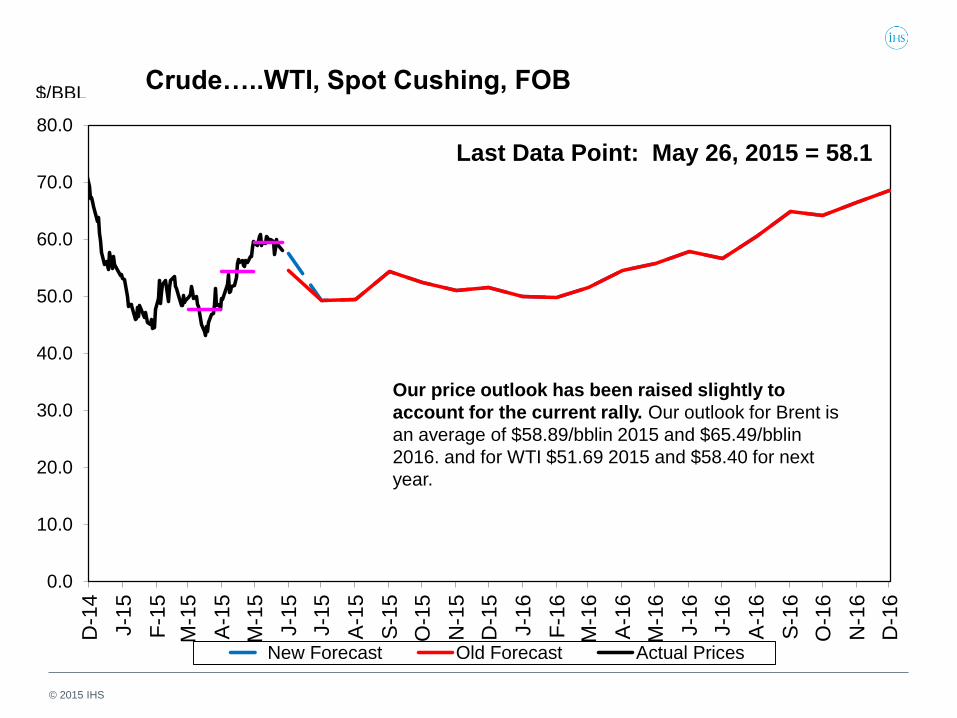

New Forecast Old Forecast Actual Prices

$/BBL Crude…..WTI, Spot Cushing, FOB

Last Data Point: May 26, 2015 = 58.1

Our price outlook has been raised slightly to

account for the current rally. Our outlook for Brent is

an average of $58.89/bblin 2015 and $65.49/bblin

2016. and for WTI $51.69 2015 and $58.40 for next

year.

© 2015 IHS © 2015 IHS 14

THE INDUSTRY

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

© 2015 IHS

HDPE 17%

LLDPE 11%

LDPE 9%

PP 25%

PS 5%

EPS 3%

ABS 3%

PVC 17%

PET 8%

PC 2%

2013 World Polymer Demand = 222 Million Metric Tons

PP World’s Largest Polymer

~ 75 %

Homopolymer

Homopolymer

PP = 19%

© 2015 IHS

Ethylene

Base Chemical Capacity Additions: 2010 – 2020 = 231 Million Metric Tons

16

0

20

40

60

80

Methanol Propylene Ethylene Paraxylene Chlorine Benzene

2010/15 2015/20 2010/20

Million Metric Tons

Methanol Propylene

Benzene Paraxylene

Chlorine

© 2015 IHS 17

Top 5 Countries Adding Base Chemical Capacity 231 Million Tons from 2010 to 2020

0

20

40

60

80

100

120

China UnitedStates

SaudiArabia

S. Korea India

Chlorine Paraxylene Benzene

Methanol Propylene Ethylene

Million Metric Tons

Top five will add nearly 75%

of base chemical capacity.

China will dominate new

capacity, adding 45% of total

© 2015 IHS 18

Regional Trade Is Critical To Success

• Trade is an essential element of

basic chemical supply chains

• Low cost countries such as the

United States and Saudi Arabia

will export increasing volumes

• On-purpose technology will

change propylene trade patterns

• Significant investment in ships,

ports, and infrastructure is

needed to support increasing

trade volumes

5 Countries Adding 75% of Base Chemical

Capacity: 2010 to 2020 (231 MM Metric Tons)

© 2015 IHS

Ethylene Equivalent Trade Continues To Expand

19

-40.0

-20.0

0.0

20.0

40.0

00 02 04 06 08 10 12 14 16 18 20

North America South America West Europe Middle East

Indian Sub. Northeast Asia Southeast Asia Others

Ethylene Net Equivalent Trade

Net Exports

Net Imports

Million Metric Tons

© 2015 IHS 20

Chemical Industry Trade Balance in Brazil & Mexico,

Increasing Trade Deficit in Recent Years

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

2007 2008 2009 2010 2011 2012 2013 2014

Brazil Mexico

© 2015 IHS © 2015 IHS 21

El Polietileno

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

© 2015 IHS

Polyethylene: Global Momentum

22

LDPE

LLDPE

HDPE

Total Global Demand = 84.8

Million Metric Tons

2014 Global Demand

LDPE

LLDPE

HDPE

Total Global Demand = 105.4

Million Metric Tons

2019 Global Demand

AAGR 14-19 = 4.9%

18 – 23 = 3.8 %

Growth Forecast

1.3 x GDP 14-19

© 2015 IHS

America’s Polyethylene Trade Balance: South America

part of the solution for surplus product.

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

09 10 11 12 13 14 15 16 17 18 19

South America Net TradeNorth America Net TradeNAM Exports Destined for SAM

Million Metric Tons

© 2015 IHS

-1.9

-2.6

Polyethylene Net Trade Flows North America and Middle East Compete for Global Shares

24

2009 2014 2019

3.5

-0.8

-0.06

-1.5

-4.4

4.8

6.4

-3.0

-2.3

-3.1

13.4

-9.2

(Million Metric Tons)

2.8

-1.8

10.8

-6.2

© 2015 IHS

NAM PE Capacity Addition List

LDPE LLDPE HDPE

2015-2016 2015-2016 2015-2016

2017 2017 2017

2018-2019 2018-2019 2018-2019

Shell

Shell

© 2015 IHS

Actualización del Proyecto Braskem Idesa

• 4.5 Billion dollar project

• Advantaged feedstock with pricing tied to US ethane

• 20 year agreement with Pemex for the supply of ethane

1050 kty ethylene cracker

• 300 kty LDPE – Equistar Lupotech tubular: film line

• 750 kty HDPE: Innovene S: chrome catalyst for blow molding and ziegler

natta for bi-modal pipe and HMW film

• Schedule: Production to begin January 2016 with full ramp up by 2Q 16

• Target markets: Domestic supply, exports to US, S. America, Brazil,

etc….

26

© 2015 IHS © 2015 IHS 27

El Polipropileno

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

© 2015 IHS

Polypropylene: Americas Trade Balance

-1.0

-0.5

0.0

0.5

1.0

1.5

09 10 11 12 13 14 15 16 17 18 19

South America Net Trade North America Net Trade NAM Exports - SAM Imports

Net Trade, Million Metric Tons

© 2015 IHS

North American Propylene North America On Purpose Propylene Capacity Additions Latest

Update

Other Developments:

• Flint Hills purchases the PETROLOGISTICS Propylene PDH facility.

• BASF evaluating “Methane to Propylene” unit for 2019.

Estimated capacity at close to 500 ktons with a world scale 1.5 mmt methanol

plant.

• LYB announces PO/TBA unit for 2019.

This would consume approximately 300 ktons of propylene.

• Oxea to build 2-EH facility with start up in 2016.

Company Location 2014 2015 2016 2017 2018 2019 2020+ Total

BASF US Gulf Coast 250 250 500

Dow Freeport, TX 375 375 750

Enterprise Mont Belvieu, TX 362 363 725

Ascend Alvin, TX 586 587 1173

Formosa Point Comfort, TX 600 600

Williams Redwater, Alberta 250 250 500

RexTac Odessa 400 400

Firm: 0 375 737 363 1436 1487 250 4648

Thousand Metric Tons

© 2015 IHS

North America PP Projects

Polypropylene Capacity Additions

2016 2017 2018 2019 2020 (Thousand Metric Tons per Year)

Company Location

Rextac Odessa, TX 300

Unknown* US gulf Coast 220 220

Unknown* Alberta, Canada 225 225

Formosa* Point Comfort, TX 450

Total: 0 0 445 895 300

* Reported projects not fully verified or approved and not included in IHS capacity database

© 2015 IHS © 2015 IHS 31

Comercio de Resinas Cambiando

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

© 2015 IHS

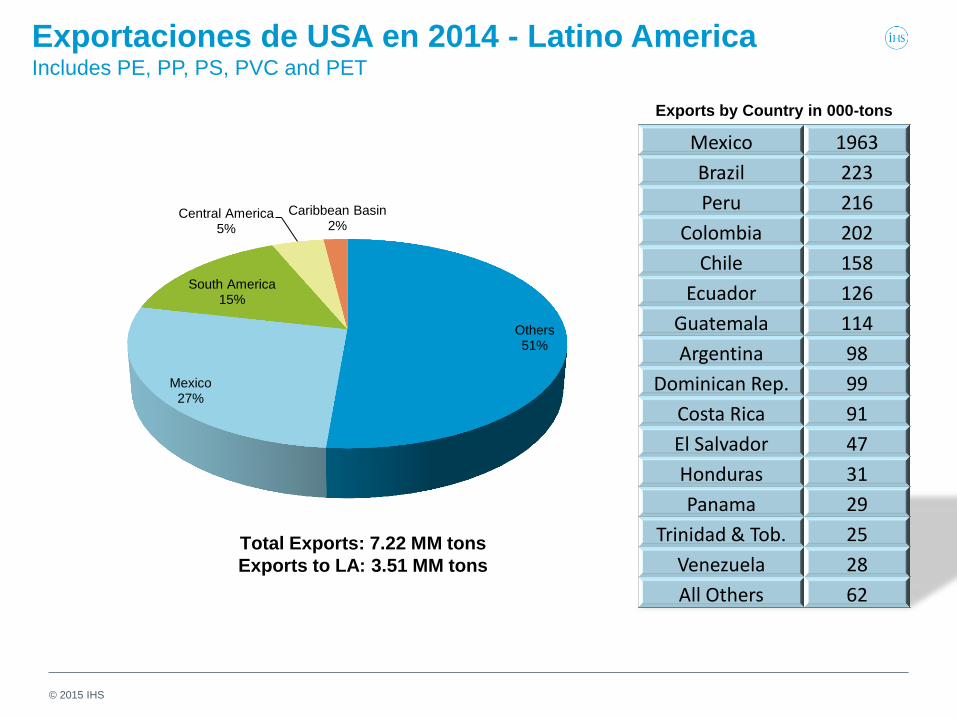

Exportaciones de USA en 2014 - Latino America Includes PE, PP, PS, PVC and PET

Others 51%

Mexico 27%

South America 15%

Central America 5%

Caribbean Basin 2%

Total Exports: 7.22 MM tons

Exports to LA: 3.51 MM tons

Mexico 1963

Brazil 223

Peru 216

Colombia 202

Chile 158

Ecuador 126

Guatemala 114

Argentina 98

Dominican Rep. 99

Costa Rica 91

El Salvador 47

Honduras 31

Panama 29

Trinidad & Tob. 25

Venezuela 28

All Others 62

Exports by Country in 000-tons

© 2015 IHS 33

Cambios en el Comercio del PE en las Americas

(Thousand Metric Tons)

3500

2799

6595

-810

-1895

-3006

2009 2014 2019

© 2015 IHS 34

Cambios en el comercio Neto de PP en Las Americas

(Thousand Metric Tons)

1049

231

1110

31

-382

-907

2009 2014 2019

© 2015 IHS 35

Cambios en el Comercio Neto de PS en Las Americas

(Thousand Metric Tons)

20 50 49

-28

-120 -139

2009 2014 2019

© 2015 IHS 36

Cambios en el Comercio Neto de PVC en Las Americas

(Thousand Metric Tons)

2240

3100

1745

2009 2014 2019

-332 -787

-1017

© 2015 IHS © 2015 IHS 37

Presentation Name / Month 2015

Comentarios Finales y Precios

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

© 2015 IHS

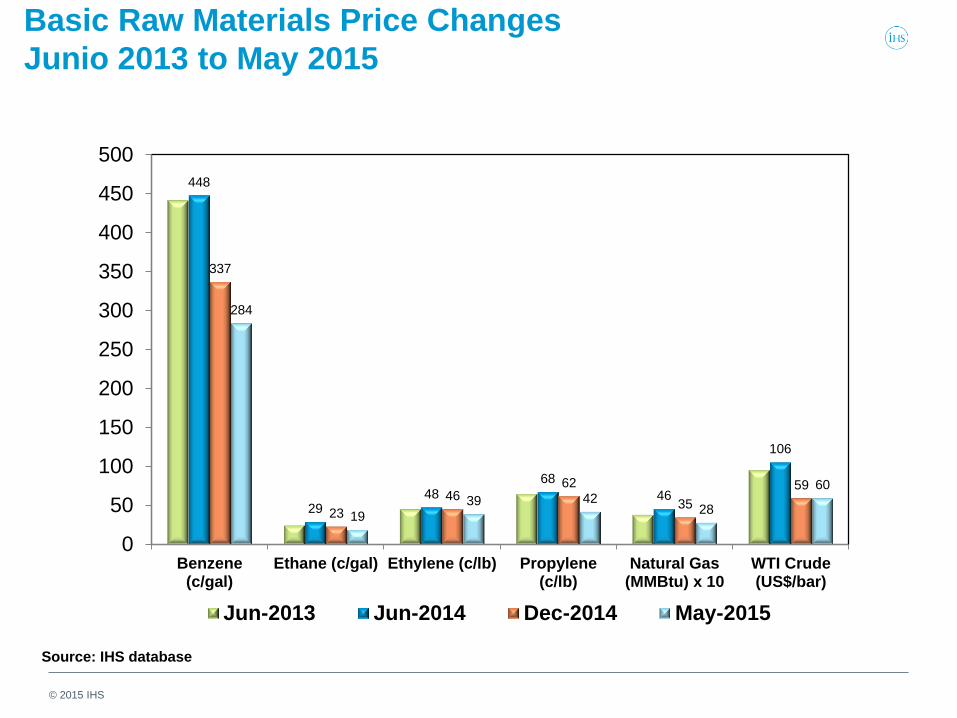

Basic Raw Materials Price Changes

Junio 2013 to May 2015

Source: IHS database

448

29 48

68

46

106

337

23

46 62

35

59

284

19

39 42 28

60

0

50

100

150

200

250

300

350

400

450

500

Benzene(c/gal)

Ethane (c/gal) Ethylene (c/lb) Propylene(c/lb)

Natural Gas(MMBtu) x 10

WTI Crude(US$/bar)

Jun-2013 Jun-2014 Dec-2014 May-2015

© 2015 IHS

US/CAN LDPE: Quarterly Price & Supply/Demand

Plastic Solutions / May 2015

900

1,200

1,500

1,800

2,100

2,400

720

740

760

780

800

820

840

860

880

Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15

Price (FAS Houston) Production Total Demand

Million Metric Tons US$/Ton

© 2015 IHS

US/CAN LLDPE: Quarterly Price & Supply/Demand

Plastic Solutions / May 2015

900

1,200

1,500

1,800

2,100

2,400

1,400

1,450

1,500

1,550

1,600

1,650

1,700

Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15

Price (FAS Houston) Production Total Demand

Million Metric Tons US$/Ton

© 2015 IHS

US/CAN HDPE: Quarterly Price & Supply/Demand

Plastic Solutions / May 2015

900

1,200

1,500

1,800

2,100

2,400

1,750

1,800

1,850

1,900

1,950

2,000

2,050

2,100

2,150

2,200

Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15

Price (FAS Houston) Production Total Demand

Million Metric Tons US$/Ton

© 2015 IHS

NAM PP: Quarterly Price & Supply/Demand

Plastic Solutions / May 2015

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

1,700

1,750

1,800

1,850

1,900

1,950

2,000

2,050

Q1-14 Q2-14 Q3-14 Q4-14 Q1-15 Q2-15 Q3-15 Q4-15

Price (FAS Houston) Production Total DemandFuente: ACC/IHS

Million Metric Tons US$/Ton

© 2015 IHS 43

PEPP/ June 2015

Noreste Asiático PE

Mercados Demanda

• Demanda incrementa en Q1 2015 para reponer

inventarios. Disminuye compra de reciclado.

Producción

• Costos de producción mas competitivos basado en

naftas mas baratas como materia prima.

• Resultando en tasas de operación mas altas a

pesar de paradas por mantenimiento en Q2 lo cual

afecto oferta.

Inventarios

• Demanda alta mantiene inventarios bajos y oferta

limitada.

Precios

• Precios de PE firmes en Mayo. Debido a oferta

limitada. Sin embargo, esperamos que los precios

se debiliten ligeramente en Junio , como resultado

de mayor oferta.

© 2015 IHS

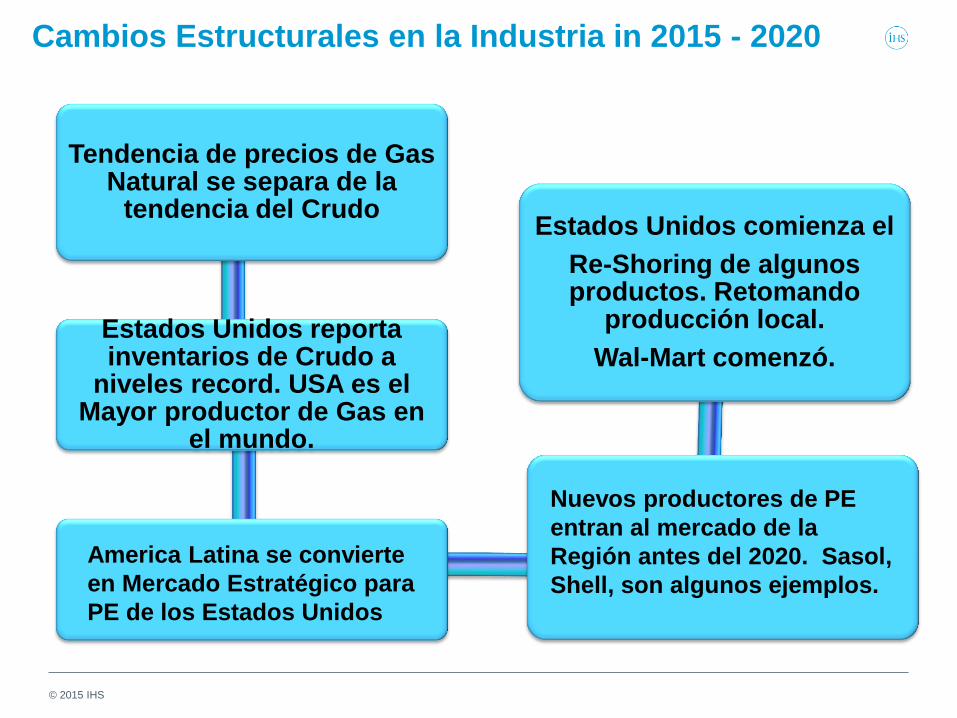

Cambios Estructurales en la Industria in 2015 - 2020

Tendencia de precios de Gas Natural se separa de la

tendencia del Crudo

Estados Unidos reporta inventarios de Crudo a

niveles record. USA es el Mayor productor de Gas en

el mundo.

Estados Unidos comienza el

Re-Shoring de algunos productos. Retomando

producción local.

Wal-Mart comenzó.

America Latina se convierte

en Mercado Estratégico para

PE de los Estados Unidos

Nuevos productores de PE

entran al mercado de la

Región antes del 2020. Sasol,

Shell, son algunos ejemplos.

© 2015 IHS

Conclusiones

• Precio de Crudo se mantendrá a niveles inferiores a los 60 dólares el

barril para el 2015.

• Excedentes en Asia se orientan a mercados en las Americas ahora que

son mas competitivos.

• Proyecto Braskem/Idesa en Mexico arranca a principios del 2016. PE

de esta planta entrara en mercados de las Americas en sus primeros

años. Casi un 40 por ciento de su producción inicialmente será

exportada.

• Capacidad Nueva en USA incrementara la oferta de PE

significativamente en el 2017.

• Como prepararnos para capitalizar las oportunidades de

crecimiento en el periodo 2017 al 2020.

• Ante los cambios en energía y otras variables, el poder mantener

claro lo fundamental de los mercados será de gran utilidad.

© 2015 IHS

Warren Buffett’s

3 Principios Básicos Para

Triunfar

•Cash

•Conocimiento

•Información

© 2015 IHS © 2015 IHS

Presentation

ihs.com

IHS

Rina Quijada

IHS Chemical Sr Director Latin America

+ 1 832 619 8586

27 May 2015

CHEMICAL

GRACIAS